103 Chapter 10 Innovation in Sukuk structures Moinuddin Malim, Badr Al-Islami The word Sukuk first appeared in the early days of the Islamic empires and could originally be described as a credit note issued to soldiers and government officials. They could exchange it for commodities, materials or goods via the treasury or the finance ministry. Today, the word Sukuk is used to describe Shari’ah-compliant debt capital market instruments and has raised growing interest in the finance industry worldwide. From the issuance of the first ever sovereign international Sukuk by Malaysia in 2002, the Sukuk market has been growing exponentially until the recent global financial crisis. Although, almost all Islamic banking products are made to deliver the same economic results as conventional ones, they are designed within a Shari’ah-compliant legal structure. Today, however, Sukuk has been the focus of much debate amongst Shari’ah scholars. Many discus- sion points have been raised: they challenge Sukuk’s raison d’être as Islamic bonds have the same economic outcome as conventional ones and follow the same life cycle post issuance. Some scholars have argued that Sukuk do not seem to be in line with the original purpose of the Shari’ah. This chapter will try to present a concise and to-the-point discussion on various arguments around the different Sukuk structures and analyse whether they require innovation and development. Also, it will describe the various platforms used for the issuance of Sukuk and try to answer the question of the necessity to change the local laws to better suit the Shari’ah requirements as well as analyse whether the conventional elements can be removed from the Sukuk structures. Prior to expanding on the discussion which has become the most debated issue in the Islamic banking and financing circles, it is necessary to understand the evolution of the Sukuk industry compared to the global bond markets. Historical overview Today the total amount of Sukuk issued in any currency stands at slightly more than $133 billion. 1 Exhibit 10.1 below shows Sukuk issuance since 2001, with a peak reaching $46.52 billion in 2007. 10-Islamic IB-chapter 10-ppp.indd 103 15/02/2010 11:20

Transcript

103

Chapter 10

Innovation in Sukuk structures

Moinuddin Malim, Badr Al-Islami

The word Sukuk first appeared in the early days of the Islamic empires and could originally be described as a credit note issued to soldiers and government officials. They could exchange it for commodities, materials or goods via the treasury or the finance ministry. Today, the word Sukuk is used to describe Shari’ah-compliant debt capital market instruments and has raised growing interest in the finance industry worldwide.

From the issuance of the first ever sovereign international Sukuk by Malaysia in 2002, the Sukuk market has been growing exponentially until the recent global financial crisis. Although, almost all Islamic banking products are made to deliver the same economic results as conventional ones, they are designed within a Shari’ah-compliant legal structure. Today, however, Sukuk has been the focus of much debate amongst Shari’ah scholars. Many discus-sion points have been raised: they challenge Sukuk’s raison d’être as Islamic bonds have the same economic outcome as conventional ones and follow the same life cycle post issuance. Some scholars have argued that Sukuk do not seem to be in line with the original purpose of the Shari’ah. This chapter will try to present a concise and to-the-point discussion on various arguments around the different Sukuk structures and analyse whether they require innovation and development. Also, it will describe the various platforms used for the issuance of Sukuk and try to answer the question of the necessity to change the local laws to better suit the Shari’ah requirements as well as analyse whether the conventional elements can be removed from the Sukuk structures.

Prior to expanding on the discussion which has become the most debated issue in the Islamic banking and financing circles, it is necessary to understand the evolution of the Sukuk industry compared to the global bond markets.

Historical overview

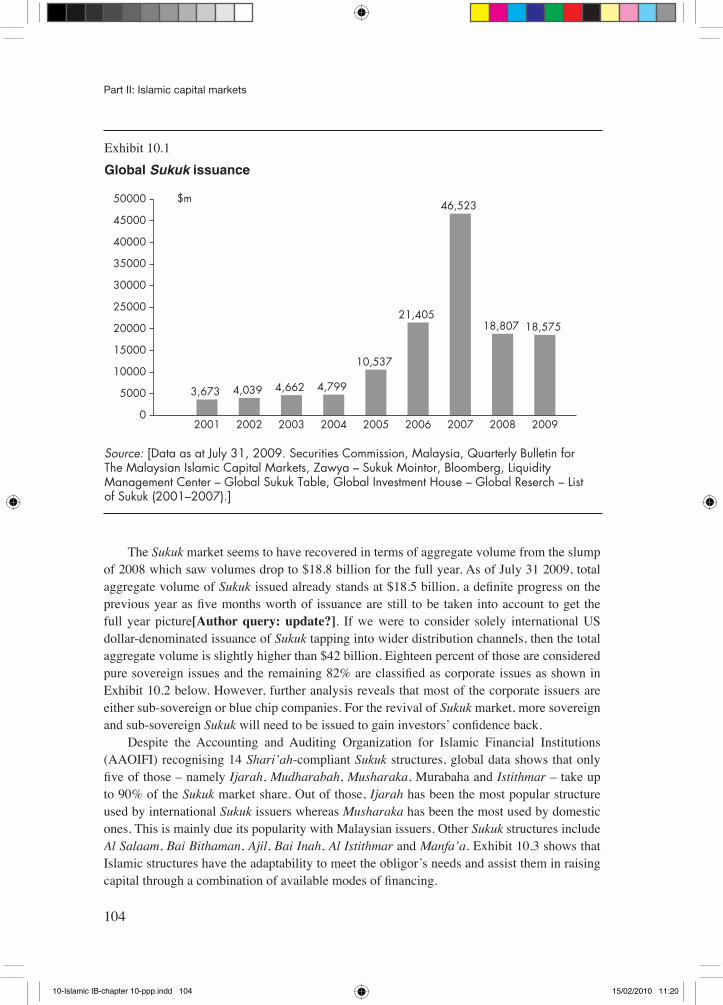

Today the total amount of Sukuk issued in any currency stands at slightly more than $133 billion.1 Exhibit 10.1 below shows Sukuk issuance since 2001, with a peak reaching $46.52 billion in 2007.

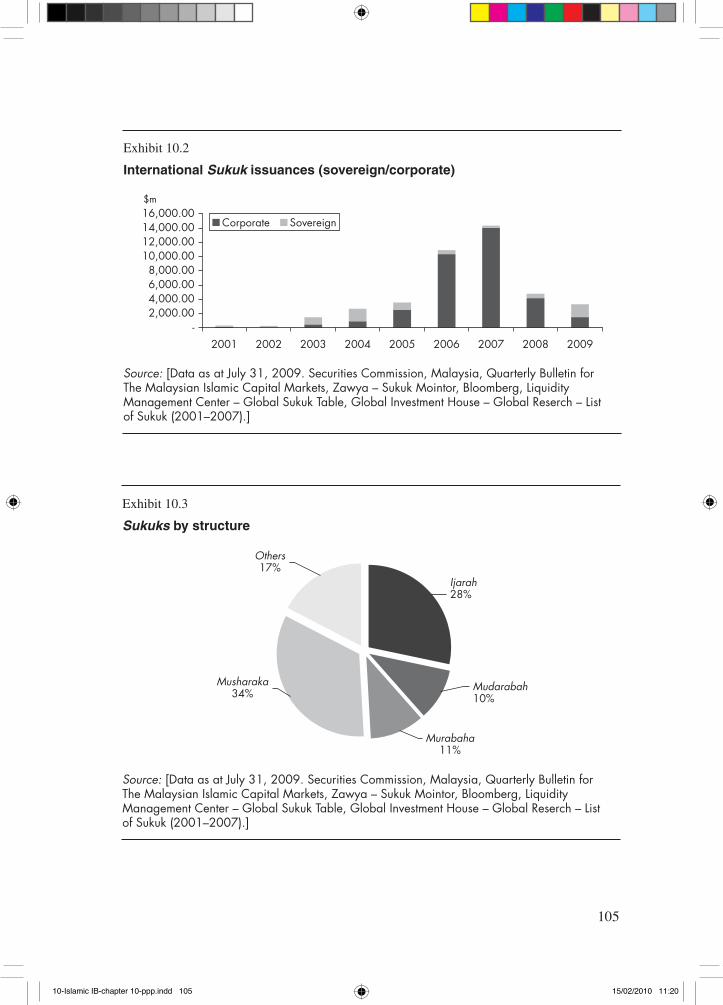

The Sukuk market seems to have recovered in terms of aggregate volume from the slump of 2008 which saw volumes drop to $18.8 billion for the full year. As of July 31 2009, total aggregate volume of Sukuk issued already stands at $18.5 billion, a definite progress on the previous year as five months worth of issuance are still to be taken into account to get the full year picture[Author query: update?]. If we were to consider solely international US dollar-denominated issuance of Sukuk tapping into wider distribution channels, then the total aggregate volume is slightly higher than $42 billion. Eighteen percent of those are considered pure sovereign issues and the remaining 82% are classified as corporate issues as shown in Exhibit 10.2 below. However, further analysis reveals that most of the corporate issuers are either sub-sovereign or blue chip companies. For the revival of Sukuk market, more sovereign and sub-sovereign Sukuk will need to be issued to gain investors’ confidence back.

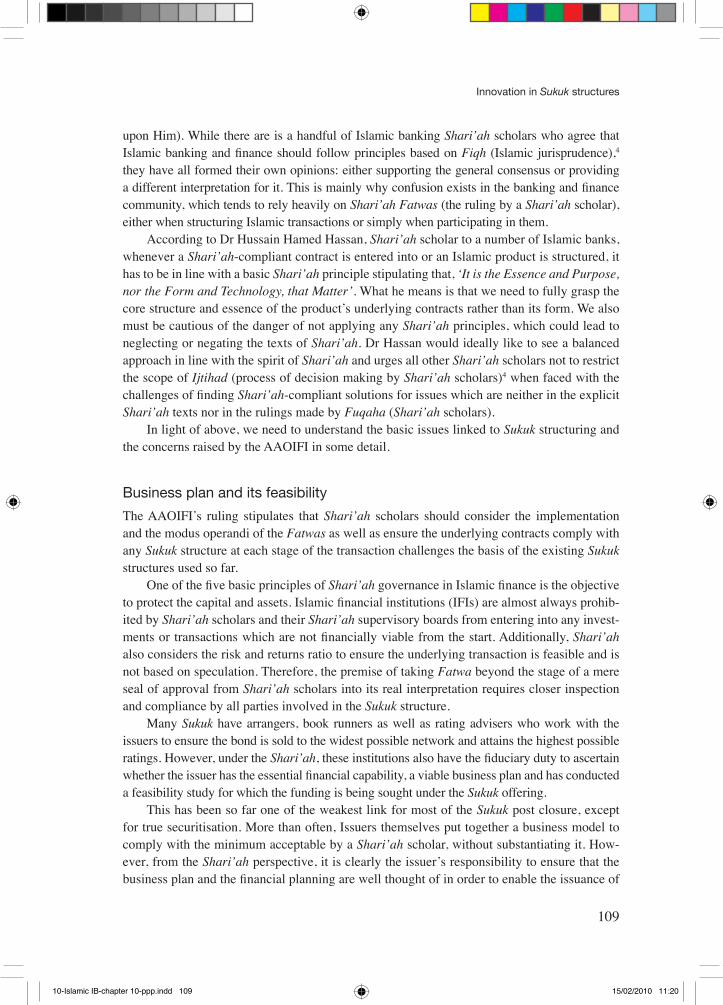

Despite the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) recognising 14 Shari’ah-compliant Sukuk structures, global data shows that only five of those – namely Ijarah, Mudharabah, Musharaka, Murabaha and Istithmar – take up to 90% of the Sukuk market share. Out of those, Ijarah has been the most popular structure used by international Sukuk issuers whereas Musharaka has been the most used by domestic ones. This is mainly due its popularity with Malaysian issuers. Other Sukuk structures include Al Salaam, Bai Bithaman, Ajil, Bai Inah, Al Istithmar and Manfa’a. Exhibit 10.3 shows that Islamic structures have the adaptability to meet the obligor’s needs and assist them in raising capital through a combination of available modes of financing.

3,673 4,039 4,662 4,799

10,537

21,405

46,523

18,807 18,575

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

2001 2002 2003 2004 2005 2006 2007 2008 2009

$m

Exhibit 10.1

Global Sukuk issuance

Source: [Data as at July 31, 2009. Securities Commission, Malaysia, Quarterly Bulletin forThe Malaysian Islamic Capital Markets, Zawya – Sukuk Mointor, Bloomberg, LiquidityManagement Center – Global Sukuk Table, Global Investment House – Global Reserch – Listof Sukuk (2001–2007).]

International Sukuk issuances (sovereign/corporate)

Source: [Data as at July 31, 2009. Securities Commission, Malaysia, Quarterly Bulletin forThe Malaysian Islamic Capital Markets, Zawya – Sukuk Mointor, Bloomberg, LiquidityManagement Center – Global Sukuk Table, Global Investment House – Global Reserch – Listof Sukuk (2001–2007).]

Exhibit 10.3

Sukuks by structure

Source: [Data as at July 31, 2009. Securities Commission, Malaysia, Quarterly Bulletin forThe Malaysian Islamic Capital Markets, Zawya – Sukuk Mointor, Bloomberg, LiquidityManagement Center – Global Sukuk Table, Global Investment House – Global Reserch – Listof Sukuk (2001–2007).]

Source: [Data as at July 31, 2009. Securities Commission, Malaysia, Quarterly Bulletin forThe Malaysian Islamic Capital Markets, Zawya – Sukuk Mointor, Bloomberg, LiquidityManagement Center – Global Sukuk Table, Global Investment House – Global Reserch – Listof Sukuk (2001–2007).]

Bahrain5% Indonesia

2%Kuwait

1%

Malaysia57%

Pakistan2%

Qatar2%

Saudi Arabia9%

UAE20%

Others2%

Exhibit 10.5

Sukuk issuances by currency

Source: Data as at July 31, 2009. Securities Commission, Malaysia, Quarterly Bulletin forThe Malaysian Islamic Capital Markets, Zawya – Sukuk Mointor, Bloomberg, LiquidityManagement Center – Global Sukuk Table, Global Investment House – Global Reserch – Listof Sukuk (2001–2007).

In terms of Islamic debt capital markets, it is undoubtedly Malaysia which, as early as the 1990s, introduced a series of measures to develop Sukuk in the country. Exhibit 10.4 shows how other countries now have caught on the trend and how the global Sukuk market is geo-graphically split at a global level. Exhibit 10.5 shows the currency denomination: besides the Malaysian ringgit, the US dollar is the preferred currency of denomination. This is even more the case for international Sukuk. While there have been attempts to issue in British pound, euro or Japanese yen, they have not had the success issuers had hoped for.

Today, following the example of Malaysia, countries such as Saudi Arabia, Indonesia, Pakistan and, to a lesser extent, the UAE, have successfully launched local currency Sukuk. We also need to understand that capital markets activity in these countries (except Malaysia) has been non-existent or fairly limited. They will be able to develop thanks to a basic infra-structure, clear policy guidelines and as well a defined Shari’ah framework – all of which will encourage corporate as well as sovereign issuers to use capital markets as an instrument to raise liquidity.

One interesting aspect of Sukuk is that most of the issues to date have been subscribed by institutional investors including corporate houses, insurance companies, pension funds mutual funds, hedge funds and banks – both Islamic and conventional. This can be explained by the fact that Sukuk yield superior returns which otherwise would not be available, especially to banks which buy Sukuk on a ‘held to maturity’ (HTM) or ‘available for sale’ (AFS) basis. The main reason for the banks’ active role in the Sukuk market – and especially up to the global crisis – has been the surplus liquidity due to high oil prices and booming economies.

Basic structures and issues

While there are a variety of Sukuk structures available, the most common of them used to date are based on Al Ijarah (sale and lease back), Musharaka (partnership and joint venture), Mud-harabah (trusteeship and fund management), Murabaha (deferred sale) and Wakalah (invest-ment agency). Appendix A provides simplified flowcharts on how these structures work. The attraction of Sukuk is that a combination of those structures can be used to put a Sukuk together so that it can meet clients’ requirements and fit with their existing investment models. In addi-tion to the basic few Islamic structures highlighted above, the salient features of the different types of investment Sukuk are summarised in the table in Appendix B.

The suitability of a Sukuk structure over another is a choice made solely by the obligor or issuer and based on the availability of underlying assets or the project under consideration. In an ideal world, it would be very simple for all obligors to issue Sukuk Al Ijarah which has minimal Shari’ah compliance issues. However, it is up to the market to gauge its risk appetite as well as determine acceptable return criteria. Today, any individual or corporate contemplat-ing using Islamic financial products should consider the following factors prior to switching from existing conventional to Islamic practice.

• Generally, consumers are driven by the price and will not pay more for a Shari’ah-compli-ant solution.

• In all Islamic countries, conventional banking remains the dominant player and controls the pricing of the underlying instrument.

• Islamic financial institutions and Islamic instruments face the dilemma that both by way of practice and existence, they have been structured to conform to the characteristics of conventional finance and hence do not follow a form as prescribed in traditional Shari’ah jurisprudence.

During the last decade or so, Islamic finance has received a tremendous boost mainly due to the popularity of Sukuk and the way these instruments have co-existed alongside the conven-tional debt capital markets. However, as basic Shari’ah law is not implemented in any of the Muslim countries’ economic models, it is not difficult to gauge why Sukuk’s structures are closely replicating conventional bonds.

The rationale behind the latitude from Shari’ah scholars and their supervisory boards with Islamic institutions regarding the structure of Islamic instruments – including Sukuk – has been to encourage the migration of investors from conventional practices to Islamic hereby gaining critical mass. We have not yet reached the critical point where at least the majority if at least two thirds of the banking industry has migrated to an Islamic model. There are how-ever jurisdictions such as Saudi Arabia, Brunei, Iran and Sudan where the finance industry is mostly Islamic. Malaysia, who has introduced a dual banking system, has positively supported and developed Islamic banking and finance.

To implement a fully Islamic financial system, we would need to narrow down and switch the products from asset-backed (products that conform to the Islamic jurisprudence in spirit) to asset-based (products that fully comply with Islamic jurisprudence). However, Shari’ah scholars are split in their opinion whether Islamic finance has reached the necessary critical mass to oper-ate this switch or whether it still needs to replicate the conventional modality in essence, while retaining Shari’ah principles. One school of thought maintains that no latitude should have been given in the first place and strict compliance to Shari’ah must be adhered to. However, this view will not help the Islamic industry to develop and prosper. It would be virtually impossible to migrate to a total Islamic banking and finance system without first acquiring significant market share. If Shari’ah authorities have so far tolerated the irregularities or Mafasid when Sukuk begun to be issued and at a time when there were only a handful of Islamic financial institutions, now is a bad time to revisit the matter. This does not mean that key rules should not be respected when structuring any type of Sukuk but we must not drive the change towards the most purist form until Islamic finance as a whole has a major market share and/or has reached critical mass.

Structuring Sukuk

The structuring of Sukuk has come under scrutiny post the AAOIFI ruling issued in February 2008, coupled with the economic downturn which has affected the global markets.2

The structuring of Sukuk, especially those based on Mudarabah, Musharaka or Wakalah, has been the focal point of discussion of various Shari’ah forums including the AAOIFI recently. The argument was first raised by a prominent contemporary Islamic jurist, Sheikh Muhammed Taqi Usmani in his article in 2007.3 Much debate and discussion have since followed. How-ever, we need to fully understand the finer points of discussion between the various schools of thoughts under the Islamic jurisprudence, which is why some confusion has arisen for those who are not familiar with the spirit of Islam and its evolution since Prophet Muhammed (Peace be

upon Him). While there are is a handful of Islamic banking Shari’ah scholars who agree that Islamic banking and finance should follow principles based on Fiqh (Islamic jurisprudence),4 they have all formed their own opinions: either supporting the general consensus or providing a different interpretation for it. This is mainly why confusion exists in the banking and finance community, which tends to rely heavily on Shari’ah Fatwas (the ruling by a Shari’ah scholar), either when structuring Islamic transactions or simply when participating in them.

According to Dr Hussain Hamed Hassan, Shari’ah scholar to a number of Islamic banks, whenever a Shari’ah-compliant contract is entered into or an Islamic product is structured, it has to be in line with a basic Shari’ah principle stipulating that, ‘It is the Essence and Purpose, nor the Form and Technology, that Matter’. What he means is that we need to fully grasp the core structure and essence of the product’s underlying contracts rather than its form. We also must be cautious of the danger of not applying any Shari’ah principles, which could lead to neglecting or negating the texts of Shari’ah. Dr Hassan would ideally like to see a balanced approach in line with the spirit of Shari’ah and urges all other Shari’ah scholars not to restrict the scope of Ijtihad (process of decision making by Shari’ah scholars)4 when faced with the challenges of finding Shari’ah-compliant solutions for issues which are neither in the explicit Shari’ah texts nor in the rulings made by Fuqaha (Shari’ah scholars).

In light of above, we need to understand the basic issues linked to Sukuk structuring and the concerns raised by the AAOIFI in some detail.

Business plan and its feasibility

The AAOIFI’s ruling stipulates that Shari’ah scholars should consider the implementation and the modus operandi of the Fatwas as well as ensure the underlying contracts comply with any Sukuk structure at each stage of the transaction challenges the basis of the existing Sukuk structures used so far.

One of the five basic principles of Shari’ah governance in Islamic finance is the objective to protect the capital and assets. Islamic financial institutions (IFIs) are almost always prohib-ited by Shari’ah scholars and their Shari’ah supervisory boards from entering into any invest-ments or transactions which are not financially viable from the start. Additionally, Shari’ah also considers the risk and returns ratio to ensure the underlying transaction is feasible and is not based on speculation. Therefore, the premise of taking Fatwa beyond the stage of a mere seal of approval from Shari’ah scholars into its real interpretation requires closer inspection and compliance by all parties involved in the Sukuk structure.

Many Sukuk have arrangers, book runners as well as rating advisers who work with the issuers to ensure the bond is sold to the widest possible network and attains the highest possible ratings. However, under the Shari’ah, these institutions also have the fiduciary duty to ascertain whether the issuer has the essential financial capability, a viable business plan and has conducted a feasibility study for which the funding is being sought under the Sukuk offering.

This has been so far one of the weakest link for most of the Sukuk post closure, except for true securitisation. More than often, Issuers themselves put together a business model to comply with the minimum acceptable by a Shari’ah scholar, without substantiating it. How-ever, from the Shari’ah perspective, it is clearly the issuer’s responsibility to ensure that the business plan and the financial planning are well thought of in order to enable the issuance of

the Sukuk. Similarly, investors should consider the credit worthiness of the issuer as well as the feasibility study in order to fully assess the risk they are willing to take. Therefore, Shari’ah holds the issuer responsible for the integrity and accuracy of the business model. Additionally, under Islamic jurisprudence, if the issuer fails to deliver the desired returns due to an inher-ent flaw in the feasibility study and on which premises investors bought the product, then the Sukuk manager is liable for the full compensation of the investment.

From a liability view point, there are three schools of thoughts: some Islamic jurists state that it is the person (Sukuk manager or managing partner) presenting the feasibility study who is fully responsible for the Sukuk’s failure to produce the expected results – apart from a case of force majeure. Some others deem the Sukuk manager responsible for capital protection only, with the exclusion of returns. And a third thinks that a pure risk and reward sharing model is the way forward. This has caused more concerns within the Sukuk industry. It will be interest-ing to see how this debate will evolve and if Shari’ah scholars will reach common ground to enable this industry to truly grow. However, one thing is very clear and all Shari’ah scholars seem to agree: the Sukuk manager is responsible for providing evidence that the failure of the Sukuk and the consequent loss of capital for the investors were not due to his own negligence.

Having an accurate and viable financial plan takes care of most of the issues faced by the issuers when it comes to Sukuk issuance, especially under the Mudharabah, Musharaka and Wakalah structures. Basically, a Sukuk should be issued only when solidly backed by the financial and business planning, that is, the underlying assets for which the Sukuk is issued.

Ownership and transferability of assets

The question of ownership and transferability of the Sukuk’s underlying assets emerged as a contentious issue, which has sparked much discussion within the Shari’ah fraternity. This is due to the various Madhabs (different schools of thought within Islamic jurisprudence )4 and the various regulators drafting the law of the land based on conventional banking as well as conventional finance platforms of different regions.

The AAOIFI and other Islamic bodies – including the Islamic Financial Services Board (IFSB) – have addressed the Shari’ah concerns. The IFSB has issued the Capital Adequacy Requirements for Sukuk, Securitization and Real Estate Investment under – IFSB-7 – Pub-lished Standards.5 While the AAOIFI is keen to see ownership and transferability of assets under Sukuk structures, the IFSB’s Standard addresses the capital adequacy requirements for Sukuk and securitisation. The purpose of the IFSB is to provide clear guidelines on the asset re-recognition criteria, especially for Islamic asset-backed securities (ABS).

One of the achievements of the IFSB has been to distinguish between three types of Sukuk structures: (1) asset-backed (ABS); (2) pay through; and (3) pass through. It became necessary to make this distinction as not all Sukuk issued today are true ABS, though they may appear to have real assets supporting them. Prior to delving into the debate of ownership and transfer-ability, it is essential that we understand the basic difference between asset-backed structures and asset-based structures.

• Asset-backed structures. Islamic ABS are similar to conventional ones: they expose the Sukuk holder to losses due to impairment of the asset (or cash flows) and the credit risk is

essentially based on the underlying value of the asset (or cash flows) and not that of the obligor.

• Asset-based structures – pay through. Any Sukuk structure whereby the income generated from the underlying asset is paid to the Sukuk holder through the issuer and where the obligor has issued a purchase undertaking will constitute a pay through structure. Usually such struc-tures are based on transactions where the obligor undertakes to purchase the asset on maturity or a termination event at the exercise price. The exercise price is designed to compensate the Sukuk holder for principal and profit. In such cases, the credit risk is based on the obligor’s corporate credit rating and can also carry any other form of credit enhancement.

• Asset-based structure – pass through. In a pass through structure, a separate entity issues the purchase undertaking for the asset to the Sukuk holders exercisable at maturity or during the tenure of the Sukuk in case of an event of default or breaches. Hence the obligor is not obliged to repurchase the assets or issue any undertaking to this effect. Credit enhancement can come from the separate entity which may have recourse on the obligor but it guarantees the repayment of the Sukuk to Sukuk holders.

For the AAOIFI’s Shari’ah condition to be met, a Sukuk must transfer all ownership rights in the assets from the obligor to the investor via Sukuk structure. However, from a pure Shari’ah perspective, the requirement of asset transfer stems from the legal title transfers under the law of the land which depends on the jurisdiction and the applicable legal system. While some jurisdictions recognise the beneficial and/or equitable title, ownership rights do not necessarily require transfer of registered and/or legal title of the asset. Also under Islamic jurisprudence, there is no requirement for a registered and/or legal title of the asset to be transferred as long as there is a legally-binding contract between the parties. However, in some jurisdictions, registration of title is considered a conclusive proof of ownership of asset. Furthermore, if the essence of the AAOIFI’s ruling is to enable and/or allow the investors to step into the obligor’s shoes and perform related duties pertaining to the ownership then it essentially entails the appointment of an administrator from inception.

The IFSB recognises that from a Shari’ah perspective, subject to independent interpreta-tion of the jurist in their own jurisdiction, there are four key criteria that need to be considered in order for a sale under Sukuk structure to be classified as a ‘true sale’.

1 Transfer of assets should not be construed as a secured loan structured to avoid bankruptcy

or insolvency proceedings by the court or other competent authorities.2 The bankruptcy or insolvency of the obligor must not affect the assets that have been trans-

ferred to the Sukuk holder via the issuer.3 In case the Sukuk holder or issuer elects to do so, the assets must then be transferred. 4 The sale must be free and clear of all prior overriding liens.

Most importantly, we need to understand that the local banking and financial laws under which the Sukuk are issued are in their infancy in most of the jurisdictions. The desire of Shari’ah scholars and various Shari’ah regulatory bodies to bring substance over form will not be realised in the short term. There are often conflicts between local jurisdictions and the Shari’ah laws and often, there are no ways of finding a compromise between the two. The ownership and trans-

ferability of assets need a lot more concerted efforts by the legal and Shari’ah fraternity. It is imperative to develop alternatives similar to the Malaysian model, that is, to develop a parallel Islamic banking system which recognises the needs of Shari’ah compliance vis-à-vis local laws (to be improved upon further) when it comes to Sukuk structures and let it evolve over time.

The purchase undertaking

Sukuks have created valuable opportunities for the investors in general, and for the ethical investors more specifically, while contributing positively towards the development of the national economies and business activities. The success of Sukuk can be attributed to the use of existing conventional platforms as well as the structures through which the obligator’s credit risk has been captured to create instruments on par with conventional bonds, even if this is the cause of most contention today.

The main area of disagreement is not whether Sukuk are Shari’ah-compliant but rather the underlying structure itself. At times, Shari’ah scholars have given a broader interpretation and issued Fatwas on those guidelines. One of the main points of contention is the purchase under-taking, especially in non Ijarah-based structures where the Sukuk manager (managing partner, managing agent and investment agent acting as the Mudharib, Musharik or Wakeel) provides a purchase undertaking. While there is no debate when purchase undertaking is performed by a third party, disagreement essentially revolves around the obligor (in his capacity as Sukuk manager) extending an undertaking to buy the Sukuk back at exercise price which is designed to compensate the Sukuk holder for principal and profit upon maturity or on the termination event. Additionally, in debt-based Sukuk where the goods have been sold or assets delivered, there is no question of having any purchase undertaking at face value at all. Similarly in a Salam Sukuk prior to delivery of goods, the issuer’s obligation is a tangible liability on the debt in monetary terms to the seller and this does not constitute a purchase undertaking either. However, jurists from different Madhabs have conflicting opinions on purchase undertaking prior to delivery of goods.

Today, confusion comes from the use of purchase undertaking mostly in Mudharabah, Musharaka, Wakalah and – to a lesser extent – Ijarah structures (only for the value consider-ation which means that scholars do not have any objection to a purchase undertaking for the applicable market value at the time of re-purchase of the assets).

The main cause of this debate, triggered by the AAOIFI ruling of 2008, is that purchase undertaking is considered equivalent to a guarantee of principal and profit. However, there is a conflict between Shari’ah scholars regarding the purchase undertaking as a guarantee of prin-cipal or profit. Some maintain the popular view that purchase undertaking is only a ‘promise’ and as such, a purchase understanding should not be considered as a guarantee, which negates the essence and purpose of the contract based on trust in the case of Mudharabah, Musharaka and Wakalah structures.

The issues pertaining to purchase undertaking are more complex than they seem. Some Shari’ah scholars maintain that when a purchase undertaking is issued by the Sukuk manager, it does not mean that in case of a natural loss, damage or destruction of the underlying assets, the Sukuk manager is liable to pay back the principal. Unless stipulated in the Sukuk condi-tions, there is also no need for the Sukuk manager to sell or liquidate the asset at maturity.

Shari’ah does not prohibit Sukuk managers or any of the related parties from buying the assets back at maturity for a value which is determined by a prescribed and pre-agreed mechanism or formula between the issuer acting on behalf of the Sukuk holder and the obligor. In most cases, the market price may be difficult to ascertain at the time of the issuance of the Sukuk and more critically, the nature of the asset may be of a strategic importance to the obligor who may not want to sell the assets in the secondary market. Additionally, the lack of availability of active secondary market may also cause the asset value to be inaccurately calculated in relation to the actual value perceived by the obligor. Hence, conditions such as selling the asset at fair market value may not be a satisfactory solution for purchase undertaking to be associated with Sukuk.

Most Shari’ah scholars agree that in a purchase undertaking and under the Mudharabah, Musharaka or Wakalah contract conditions, the Sukuk manager cannot be made to guarantee the principal and/or a fixed amount of profit. However, some scholars allow purchase under-taking on the basis that the issuance of purchase undertaking at the original value is not the same as providing a guarantee. While this is yet another issue to be resolved by the Shari’ah scholars, it is clear that a purchase undertaking cannot be considered as a guarantee unless it is possible to pay the principal back to the Sukuk holders in all circumstances. Some Shari’ah scholars supporting purchase undertaking consider it a unilateral agreement only binding the originator of the ‘promise’ but not allowing the beneficiary to enforce the promise in case of an actual purchase at maturity or of a termination event caused by a total or partial loss. On the other hand, Shari’ah scholars cannot seem to agree on whether the originator can be made to purchase the assets at a higher value in case the fair market value of the assets is higher.

In cases where purchase undertaking value is inferior to the fair market value, then most Shari’ah scholars maintain that Sukuk holders cannot be made to pay for the difference unless the Sukuk manager can prove without doubt that the value deterioration was not caused by his action or lack of. In cases of total loss or destruction of assets due to causes independent of the Sukuk manager, only then the loss can be passed on to the Sukuk holders. These are the two conditions stipulated by the majority of Shari’ah scholars, which pose a problem for traditional arrangers and the legal fraternity as the risk is passed on to the Sukuk holders, which is not the case for con-ventional bonds. Usually a conventional bond (unless it is an asset-back security) is settled in full on maturity. If those two conditions are to be implemented, then it will be a difficult proposition to introduce this instrument on a debt platform and mostly, it will be difficult to find any investors with such a risk appetite unless the rewards are proportional to the risk.

While the purchase undertaking issue remains unresolved, we need to understand the basis under which purchase undertaking as a ‘promise’ has been allowed by Shari’ah which states that: (a) whoever takes something has to return it; and (b) the claimant has to produce evidence of his claim and the party who denies the claim must swear that his stand is correct. Hence the onus of proof is on the Sukuk manager. This is the core of the purchase undertaking and its use in Sukuk. Having said that Shari’ah scholars still need to devise a more flexible mechanism and let it evolve with time and practice.

Profit distribution

Over the last few years, Sukuk have seen their structures change to render them more viable and also similar to conventional instrument. These changes were introduced to ensure inves-

tors used to conventional bond fundamentals do not shy away from underlying Islamic struc-ture which sees them take a quasi equity or asset risk.

Added variants such as Shari’ah compliant liquidity facilities were applied to structures such as Mudharabah, Musharaka and Wakalah where the income generation ability of the underlying assets may not suffice to pay out the periodic coupon payment under the Sukuk. This is due to time mismatch of cash inflow and outflow or shortfall in cash inflows or any other reason.

It is very clear that Shari’ah does not allow the Sukuk manager to provide the investors any guarantee of payment in the form of a fixed return, profit or a coupon based on any under-lying benchmark. However, when we probe deeper into the underlying structure, we need to understand how Shari’ah looks at it. Is there a need for a detailed feasibility study to ascertain the viability of the underlying project and the expected returns? What is the ratio of distri-bution of the net profit between the Sukuk manager and the Sukuk holders? While Shari’ah allows the Sukuk manager to get an incentive and a share in the profit distribution, the calcula-tion and methodology of such an incentive fee should be fixed under the Shari’ah guidelines. There is no specific Shari’ah provision in investment and Ijarah Sukuk structures preventing the Sukuk manager from taking the balance of excess profit. However, some contemporary Shari’ah scholars object to this as those structures seem to have combined different aspects of the Sukuk such as liquidity facility, interest free loan from the Sukuk manager, purchase undertaking at face value, and so on.

The matter of ascertaining profit prior to the proposed periodic distribution date is the core responsibility of the Sukuk manager for any type of Sukuk. Here, the major emphasis is on the fact that most of the Sukuk’s underlying assets in general do not have a clearly ascer-tainable market value. In either case, attaining an estimate of fair market value is left on the judgment call of the Sukuk manager. Most Muslim jurists agree that the Sukuk manager acting as a trustee may value the asset according to the market and/or to the best of his abilities. Such valuation is acceptable for determining profit or loss incurred on the asset vis-à-vis the actual book value of the asset. In case the value being assessed is greater than the book value, then the Sukuk manager can either liquidate such portion to realise a profit or sell it to a third party, or even buy the portion himself. Shari’ah scholars are split on the issue of ‘on account’ profit distribution in case the profit is less than expected or in case there was no profit or a loss in the market value of the assets during the investment activity. The solution adopted by most Shari’ah scholars is to allow the Sukuk manager to arrange for cash either through an interest-free facility to be deducted from future profits or through the actual liquidation of the asset or from the proceeds at the time of purchase undertaking being exercised. However, this has to be a voluntary act by the Sukuk manager and not a binding contract enforced by the Sukuk holders. In order to protect the Sukuk holders, not servicing profit is considered a cause for termination and the purchase undertaking is invoked whereby the obligor is bound to purchase the Sukuk’s underlying assets at the exercise price.

Rating and listing of Sukuk

Given the high oil prices and increased customer interests in Islamic banking, the Middle Eastern banks have been faced with huge liquidity pools which they have invested in Sukuk.

Those have provided higher yield in comparison to other money market products. With Sukuk as a new investment vehicle, arrangers found it easier to sell a rated Sukuk to a bank treasury than to the corporate banking unit as it had to go through a detailed credit and cash flow sen-sitivity analysis. Most treasury departments were allowed to invest in rated securities through their propriety book. Additionally, in many jurisdictions, banks are not allowed to invest in cross border securities – including Sukuk – unless they are rated. This issue together with demand from the Issuer to tap into a larger distribution network and bigger Sukuk denomina-tion encouraged issuers to seek a rating for the Sukuk and/or the obligor. The listing of Sukuk gave investor confidence from a compliance, transparency and disclosures perspective, which is what a renowned regulator requires from the Issuer. The choice of listing is based on inves-tor’s acceptability of the listing exchange and level of confidence on its governance, compli-ance, transparency. Today, London, Dubai, Luxembourg, Bahrain and Labuan (Malaysia) are the favourite listing options by the Issuers for US dollar-denominated Sukuk whereas local currency Sukuk are typically listed on their local stock exchanges.

International rating agencies including S&P, Moody’s, Fitch, Capital Intelligence and other local rating agencies realised the potential of this new product and developed their understanding of Islamic finance. Today, rating agencies consistently aim to share objective and accurate insights of Sukuk as well as other Islamic products for the benefit of all market constituents.

Notable support has come from S&P and Moody’s in helping investors understand the risk associated with Sukuk. There is no material difference in the risk analysis between a Sukuk and a conventional bond. While assigning a rating, the agencies do recognise that collateral foreclosures can be much more difficult in some markets than others. They also understand that Sukuk based on Musharaka, Mudharabah and Wakalah can bear above-average credit risk. However, the rating agencies have been able to provide market participants with indepen-dent and objective opinions about the creditworthiness of issuers and Sukuk while restraining from commenting on the Shari’ah compliance of a particular issue or issuer. Additionally, rating agencies do not provide any recommendation on sell, buy or hold a particular security. Rating agencies do provide opinion on the ability and willingness of an issuer to meet financial obligations in a timely manner while taking into consideration the relevant legal and jurisdic-tional aspects of the Sukuk transaction. When legal counsels are engaged by the arrangers and the issuers, rating agencies also resort to their opinions to analyse issues such as enforceability, recognition of choice of law, insolvency and security-related matters. The sole purpose of the rating agencies is to help investors make informed decisions and issuers access debt markets. In addition, they also help issuers benchmark their creditworthiness against their peers’ to enable investors to effectively price each Sukuk based on its merits and risk consideration.

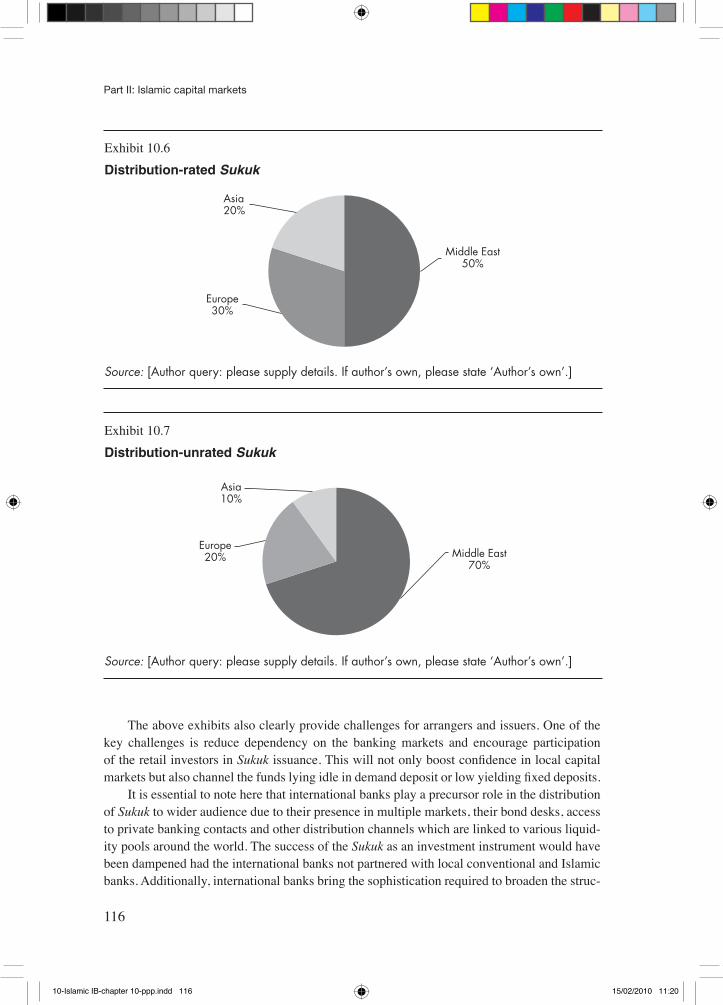

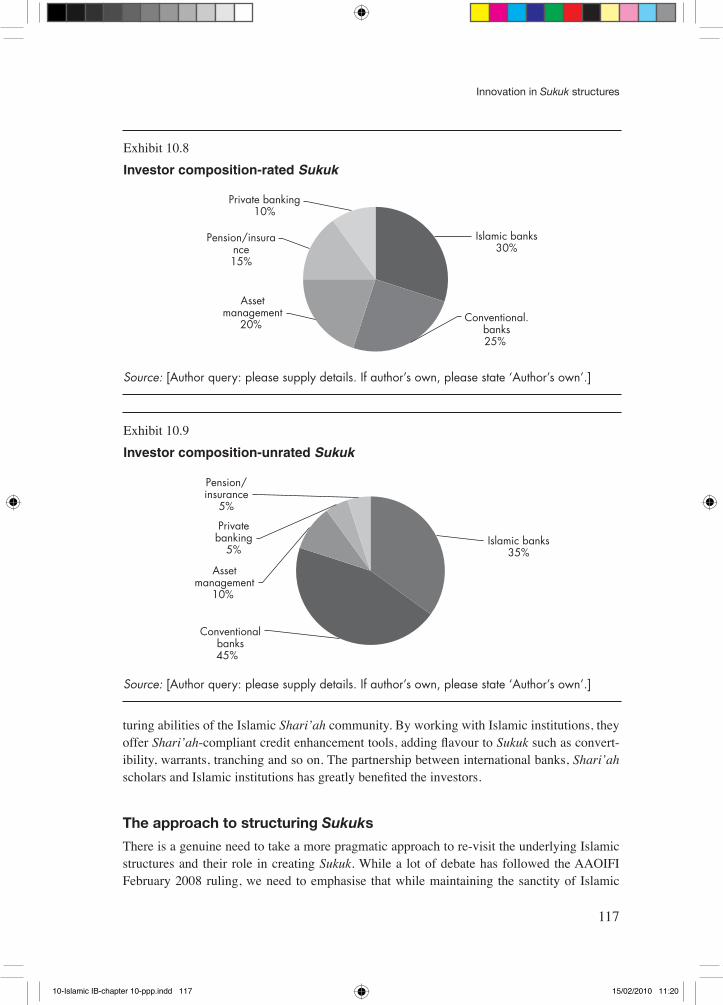

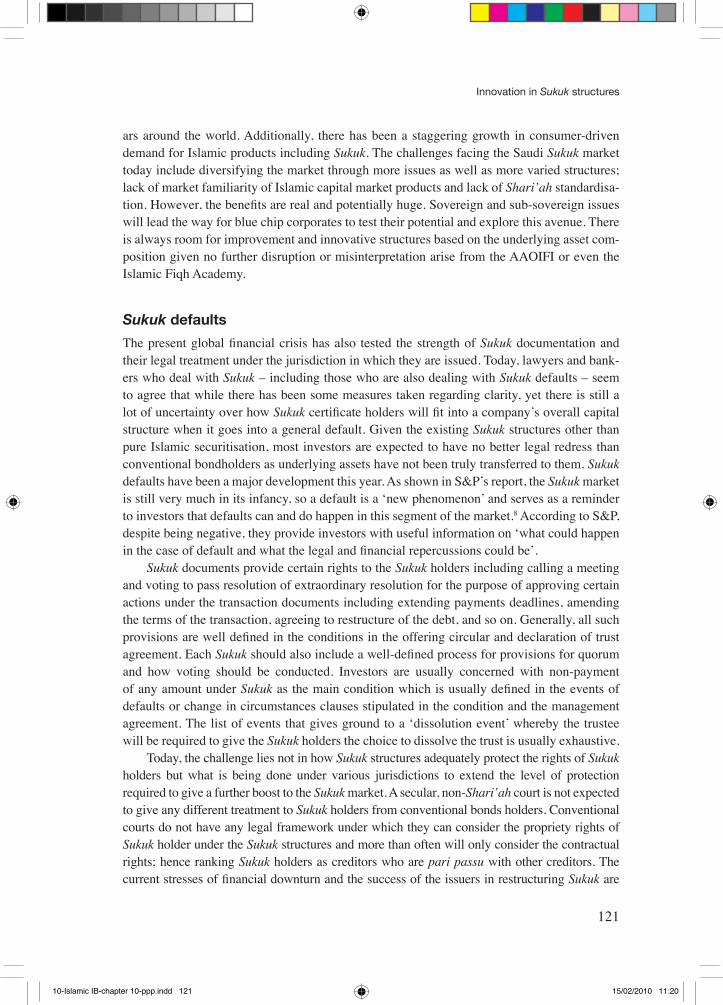

The Middle Eastern experience shows that a typical five-year US dollar-denominated and unrated sovereign or sub-sovereign Sukuk is better subscribed in the regional market as the Issuers are better known to the investors whereas the rated sovereign or sub-sovereign Sukuk attracts wider distribution as shown in the exhibits below.

In the past five years[Author query: state specific years], it has been noticed that unrated Sukuk are not easily sold outside the Middle East unless the issuers are sovereign. Addition-ally, arrangers are able to seek a bigger share of non-banking investor type for similar type of issuers when Sukuk are rated as seen in the exhibits below.

The above exhibits also clearly provide challenges for arrangers and issuers. One of the key challenges is reduce dependency on the banking markets and encourage participation of the retail investors in Sukuk issuance. This will not only boost confidence in local capital markets but also channel the funds lying idle in demand deposit or low yielding fixed deposits.

It is essential to note here that international banks play a precursor role in the distribution of Sukuk to wider audience due to their presence in multiple markets, their bond desks, access to private banking contacts and other distribution channels which are linked to various liquid-ity pools around the world. The success of the Sukuk as an investment instrument would have been dampened had the international banks not partnered with local conventional and Islamic banks. Additionally, international banks bring the sophistication required to broaden the struc-

Exhibit 10.6

Distribution-rated Sukuk

Middle East50%

Europe30%

Asia20%

Source: [Author query: please supply details. If author’s own, please state ‘Author’s own’.]

Exhibit 10.7

Distribution-unrated Sukuk

Source: [Author query: please supply details. If author’s own, please state ‘Author’s own’.]

turing abilities of the Islamic Shari’ah community. By working with Islamic institutions, they offer Shari’ah-compliant credit enhancement tools, adding flavour to Sukuk such as convert-ibility, warrants, tranching and so on. The partnership between international banks, Shari’ah scholars and Islamic institutions has greatly benefited the investors.

The approach to structuring Sukuks

There is a genuine need to take a more pragmatic approach to re-visit the underlying Islamic structures and their role in creating Sukuk. While a lot of debate has followed the AAOIFI February 2008 ruling, we need to emphasise that while maintaining the sanctity of Islamic

Exhibit 10.8

Investor composition-rated Sukuk

Source: [Author query: please supply details. If author’s own, please state ‘Author’s own’.]

Islamic banks30%

Conventional.banks25%

Assetmanagement

20%

Pension/insurance15%

Private banking10%

Exhibit 10.9

Investor composition-unrated Sukuk

Source: [Author query: please supply details. If author’s own, please state ‘Author’s own’.]

jurisprudence, Islamic law allows Ijtihad, Ijma and Qiyas.4 However, the onus of providing a liberal structure and the underlying Fatwas by the Shari’ah scholars still obliges the Shari’ah scholars, obligor, issuer, the structuring agent, the lawyers and even the rating agencies to implement a process which follows the Shari’ah approved business plan or feasibility study. Essentially, we need to maintain the spirit of Shari’ah and avoid clouding different aspects of Shari’ah into one unified opinion which either approves or discredits the Sukuk and its under-lying structure.

Will innovation in Sukuk and its evolution lead this industry in a different direction? We need to have an open-minded approach and be ready to adapt to new solutions.

We need to be ready to consider changing delivery platforms so that Sukuk and its underly-ing structures can evolve towards their ultimate goal of creating a pure Islamic economy, based on ethical principles, which can benefit all regardless of their beliefs or differences in religion. However, if purists persuade the general masses to get rid of all of the irregulari-ties currently existing in Sukuk structures, Sukuk are in danger of becoming not only less popular but also of disappearing completely. Also, is now the right time to change Sukuk structures? Do we need to issue specific types of Sukuk on different platforms: Ijarah Sukuk on the bond platform as it currently exists, and Mudharabah, Musharaka and Wakalah on quasi equity or fund-based platforms? It is too early to start confusing investors, as it was not long also when the Islamic financial terminology was aligned as closely as possible to the global financial audience. On the other hand, standardisation of Sukuk regulations based on the guidelines provided by AAOIFI and IFSB will most definitely improve the brand image, reduce cost and time to market. While Islamic finance thrives to achieve harmony amongst its players, one needs to remember that Sukuk do not dominate any given market as the major source of capital raising. The total aggregate Sukuk raised to date [Author query: state specific time here?] in any currency stands at best as slightly higher than $133 billion and does not even represent 0.16% of the $83 trillion of outstanding bonds in the global bond market as at 2008.6

As Khalid Howladar, senior credit officer for asset-backed and Sukuk finance at Moody’s says: ‘As Sukuk issuers begin to face distress, it is important that investors focus on the sub-stance and not the form of their risk, which is a concern in Islamic Finance’.7 Moody’s further confirms that while most Islamic participants acknowledge that Sukuk should grant the investor a share in either the asset or the business venture along with related cash flows and the underly-ing risks; most Sukuk structures are designed to replicate conventional bonds. It acknowledges that assets in such structures are there for Shari’ah compliance purposes only and ultimately have no reflection on the underlying risk of the asset especially in a distress situation. While the AAOIFI and IFSB have been trying to standardise and harmonise the underlying structures as well as the documentation used for the creation of a Sukuk, the actual decline in the Sukuk market was more due to the global credit market conditions rather than a direct reaction to the statement made by the AAOIFI. In Moody’s opinion, the AAOIFI’s statement will have a posi-tive effect on improving transparency and will effectively result in bringing the ‘substance’ in Sukuk. This should also help investors share risks of the assets. Moody’s would like to see the AAOIFI’s guidelines push Islamic transaction towards broad standardisation and hence force the investors to understand risk and return profile of each structure separately, irrespective of the type of Sukuk structures used.

There is no argument that Sukuk do need to move towards creating security in favour of Sukuk holders, even if actual asset ownership transfers are not possible for any reason. Shari’ah scholars encourage the Sukuk manager to establish reserve accounts to protect the Sukuk’s capital investment and be able to pay profit and return on the pre-agreed periodic pay-ment dates rather than having liquidity facility. The Sukuk holders take the risk of real assets which have a potential to depreciate over time. If reliance is shifted to purchase undertaking from obligor at market value, Sukuk will become an un-marketable instrument. Should we move towards changing the periodic distribution on the basis of the asset’s ability to pay back the principal and profit repayment during the term of the Sukuk? Additionally, the key to suc-cess in Islamic finance – and more particularly in Sukuk is reliance, not only upon Shari’ah scholars Fatwas and guidance on documentation, but also on the regulators who need to actively promote meaningful changes to the legal, regulatory system and other infrastructures. It is not an easy task as the regulators in almost all jurisdictions are more accustomed to a debt-based financing system. This is also not taking away any credit from regulators who are now forced to consider such changes due to popular demand and/or market forces. Only when these changes are implemented, will we see truly indigenous Islamic financial markets.

These are a few of the considerations which will form the basis of how Sukuk will be structured in the future. There is an investor base and issuer demand both in the Islamic and in the secular world. The Sukuk system is in its evolutionary stage and currently provides a great tool for portfolio diversification. Sukuk have been effectively used by Issuers to tap into the liquidity pools available in different regions. Even though Sukuk in some selective Muslim countries have become the favourite way to raise capital, it has not reached the point of being the main source of capital raising. There may also be the case where a formal domestic capi-tal market may simply not even exist in those countries. Additionally, some countries such as Malaysia, closely followed by Pakistan, Saudi Arabia and Indonesia, are tapping in the retail and mass consumer segments for capital raising activities through Sukuk. In this regard, whether it is Sukuk or a conventional bond, the choice needs to be available to all investor segments including the mass retail market. Until Sukuk becomes a popular investment vehicle available to all segments thorough various platforms, it is not expected to reach the level of sophistication as desired today by a few eminent Shari’ah scholars.

Emerging market leader

The Kingdom of Saudi Arabia – being by far the largest economy in the Middle East thanks to its massive oil wealth – has been working slowly and gradually to create and maintain buoyant Islamic finance deals globally as well as at home. While all of the Saudi Banks offer Islamic banking products as demonstrated by the establishment of Al Inma Bank along with Al Rajhi Bank, National Commercial Bank, Saudi British Bank or Riyad Bank and are undertaking an increasingly high number of Shari’ah-compliant transactions. The World Bank and Interna-tional Finance Corporation have issued a report, ‘Doing Business 2010: reforming through difficult times’ and have ranked Saudi Arabia the 13th easiest place to do business globally amongst 183 countries. A much improved performance if we compare it to its rank of 67th place back in 2004. This is a position which gives Islamic finance more weight as well as posi-tions the Kingdom to provide an excellent channel to encourage Sukuk issuance at all levels.

As Saudi Arabia is perceived to have the strictest interpretation of the Shari’ah, it is very important to note the development of the Saudi markets vis-à-vis Islamic financing structures. It is widely acknowledged that if a structure is deemed acceptable by Saudi Shari’ah scholars, it should then be acceptable globally especially, in the Muslim world. The recent develop-ments in the Sukuk industry in Saudi Arabia started with the inaugural Sukuk issued by Saudi Basic Industries Company (SABIC) in 2006. In this Sukuk, investors’ returns were derived from certain rights under marketing contracts, a share of which for a specified period of time – 20 years – was bought from SABIC by the Sukuk holders. The SABIC Sukuk was considered as one of the most innovative structures back then and was followed by further tranches in 2007 and 2008. SABIC Sukuk was the first ever Sukuk to be approved by the Shari’ah board of a Saudi bank and under the listing rules of Capital Market Authority (CAM). It also was the first Saudi Sukuk to use non-tangible underlying assets. Similarly, in 2007, the Saudi Electric-ity Company’s Sukuk Al-Istithmar used the right to charge fees for the reading and mainte-nance of electricity meters, deriving the returns for the Sukuk holders. Yet another innovative structure was developed, combining Ijarah and Mudharabah structures in relation to usufruct rights over a number of floors that formed a part of the Holy Mosque Endowment Complex in Makkah.

The Saudi initiatives have now received support from CAM who on June 13, 2008 launched the bond and securities market – Tadawul. The first two deals on this platform were SABIC Sukuk. This has given huge boost to the issuers who can now attract more funding in the primary market as investors are able to actively trade on the secondary market. Tadawul offers an automated order-driven secondary exchange for trading conventional bonds and Sukuk on its platform which is considered as a significant symbolic move. The move should further stimulate the Sukuk market through supply from issuers and demand from investors. Not only institutional and semi-sovereign investors who are liquidity rich such as General Organization for Social Insurance (GOSI), the Saudi Public Investment Fund and the Saudi Pension Fund, but also [Author query: missing text? Who will provide?]will provide a positive stimulus for the retail sector to participate and actively trade in bonds and Sukuk. This has been seen as one of the more positive development which will provide an alternative channel to raise fund-ing for the issuers who were originally limited to either IPOs or the banking market. While the base of the Saudi Sukuk market pay is low in comparison to Malaysia, it is moving towards the right direction thanks to the maturity of the institutional and semi-sovereign investors. Another interesting development in Saudi Sukuk market could come from Saudi Arabian Monetary Authority (SAMA) and whether it may decide to start offering short term Sukuk similar to the Kingdom of Bahrain, Brunei and Gambia. That way, short term liquidity would be managed – instead of using the existing Treasury bills – for maturity lengths ranging from 1 to 52 weeks. This would build a full maturity spectrum of Sukuk for duration management, allowing fixed and floating coupons to diversify price risk and building a repurchase facility for day to day liquidity management. If SAMA decides to take this route, it will need to tackle issues such as introduction of primary dealers and incentives for banks to underwrite and distribute their commitment.

The Kingdom [Author query: is this Saudi Arabia?] has been able to create demand interlinked with the ability of the practitioners to harness new products permissible not only under the Saudi Islamic jurisprudence but also widely acceptable to most Shari’ah schol-

ars around the world. Additionally, there has been a staggering growth in consumer-driven demand for Islamic products including Sukuk. The challenges facing the Saudi Sukuk market today include diversifying the market through more issues as well as more varied structures; lack of market familiarity of Islamic capital market products and lack of Shari’ah standardisa-tion. However, the benefits are real and potentially huge. Sovereign and sub-sovereign issues will lead the way for blue chip corporates to test their potential and explore this avenue. There is always room for improvement and innovative structures based on the underlying asset com-position given no further disruption or misinterpretation arise from the AAOIFI or even the Islamic Fiqh Academy.

Sukuk defaults

The present global financial crisis has also tested the strength of Sukuk documentation and their legal treatment under the jurisdiction in which they are issued. Today, lawyers and bank-ers who deal with Sukuk – including those who are also dealing with Sukuk defaults – seem to agree that while there has been some measures taken regarding clarity, yet there is still a lot of uncertainty over how Sukuk certificate holders will fit into a company’s overall capital structure when it goes into a general default. Given the existing Sukuk structures other than pure Islamic securitisation, most investors are expected to have no better legal redress than conventional bondholders as underlying assets have not been truly transferred to them. Sukuk defaults have been a major development this year. As shown in S&P’s report, the Sukuk market is still very much in its infancy, so a default is a ‘new phenomenon’ and serves as a reminder to investors that defaults can and do happen in this segment of the market.8 According to S&P, despite being negative, they provide investors with useful information on ‘what could happen in the case of default and what the legal and financial repercussions could be’.

Sukuk documents provide certain rights to the Sukuk holders including calling a meeting and voting to pass resolution of extraordinary resolution for the purpose of approving certain actions under the transaction documents including extending payments deadlines, amending the terms of the transaction, agreeing to restructure of the debt, and so on. Generally, all such provisions are well defined in the conditions in the offering circular and declaration of trust agreement. Each Sukuk should also include a well-defined process for provisions for quorum and how voting should be conducted. Investors are usually concerned with non-payment of any amount under Sukuk as the main condition which is usually defined in the events of defaults or change in circumstances clauses stipulated in the condition and the management agreement. The list of events that gives ground to a ‘dissolution event’ whereby the trustee will be required to give the Sukuk holders the choice to dissolve the trust is usually exhaustive.

Today, the challenge lies not in how Sukuk structures adequately protect the rights of Sukuk holders but what is being done under various jurisdictions to extend the level of protection required to give a further boost to the Sukuk market. A secular, non-Shari’ah court is not expected to give any different treatment to Sukuk holders from conventional bonds holders. Conventional courts do not have any legal framework under which they can consider the propriety rights of Sukuk holder under the Sukuk structures and more than often will only consider the contractual rights; hence ranking Sukuk holders as creditors who are pari passu with other creditors. The current stresses of financial downturn and the success of the issuers in restructuring Sukuk are

at a crossroad and it is too early to form any view on this subject. While a series of Sukuk offer-ings closed successfully, defaults were uncommon, excepting for a few Sukuk only. One thing is certain: new precedents will be set and new challenges will continue to develop and surface. However, the Islamic banking industry has established itself as a key mode of financing for all types of investors and Sukuk has become a choice instrument for them.

Conclusion

Sukuk are dynamically designed to deliver the promised financial results regardless of the state of the asset, which has caused Sukuk to be compared to conventional bonds. Like any other financial product, Sukuk will be only successful if it clearly meets the needs of both the issuers and the investors. If an entity requires equity, it will raise equity but not a Sukuk or a bond. Sukuk serve a particular need of the issuer who is looking to tap into a wider distribution channel through both Islamic and non-Islamic investors. Sukuk has yet to become an accept-able quasi-equity instrument where investors are willing to take such risk. Perhaps with time, evolution and market demand, Sukuk will be pushed to a level of sophistication where Sukuk structures will be split into both quasi-equity raising as well as Islamic debt raising activities. When and if this happens, clearly it will be the issuers’ and the investors’ choice, driven by market forces. Today, investors are looking at investing in Sukuk as they are perceived to bear low risk and provide predictable income. Both the need of issuers and investors are met by current structures of Sukuk and as such no new or innovative structures are needed to further enhance the prospects of the Sukuk market. Any substantial changes made today would mean total migration to a Shari’ah based system without first acquiring significant market share, and therefore, could be harmful to nurturing the Sukuk market.

We also need to recognise that Sukuk and Islamic finance have been able to attract atten-tion of various regulators who would like to facilitate the use of such instruments to tap into the liquidity pools available in various regions. Today, concerted efforts are being made by countries such as Turkey, Singapore, UK, Hong Kong, Germany, France, Thailand, Italy and Japan, to put together their legislations to facilitate Islamic finance based on the popularity of Sukuk.9 The current global financial situation has seen increasing attention being paid to Islamic financial solutions and some countries are fast-tracking their interest to acquiring and promoting Islamic finance. The most recent steps by a non-Muslim country to encourage Islamic finance were taken by France. An amendment to article 2011 of the French Civil Code was passed on September 17 2009 by the French National Assembly (Assemblée Nationale) to help promote the development of Islamic finance in France. This amendment is intended to assist in the structuring of Shari’ah-compliant products in France using French trusts (fiducies). The adoption of this amendment first by the French Senate (Sénat) in June and now by the National Assembly shows the determination not only of the French government but also of the French parliament to adjust French legisla-tion to the requirements of Islamic finance. Whether this move in the right direction is enough to boost the Sukuk market in France remains to be seen but no doubt gives new perspectives to Islamic investors.10 France has followed up the G20’s ambitious agenda to reform financial regu-lation, covering four main areas: the strengthening of prudential standards, the redefinition of the scope of regulation, the revision of accounting standards and the strengthening of risk manage-ment. France sees a benefit to the investors as well as its economy in moving towards a positive

legislation to encourage Islamic finance. However, the regulator is not convinced with issues such as transparency, legal standardised documentations and liquidity which are still linked with the Islamic finance industry. The obvious interest of countries like France and others is to attract the huge liquidity pool available with the oil generating countries from the Middle East and more specifically the sovereign wealth funds which have a considerably bigger appetite and do not pull out funds as quickly as other investors. France, UK, Germany, Italy and other European countries can take advantage of the Sukuk market by introducing positive legislations facilitating their local issuers structuring Sukuk without heavily taxing the foreign investors. This will give another impetus to the Sukuk markets globally and also help the European issuers create a euro denominated Sukuk market.

The existing debate on issues listed above, if not resolved quickly, may possibly attract a negative perception on these regulators in such jurisdictions who have taken a long time to fully comprehend the fundamentals of Islamic finance and its implementation under the con-ventional regulatory framework.

It is also possible that the current uproar on Sukuk structures will push the questionable Sukuk towards a hybrid structure, which could very well be somewhere between the current Sukuk structures and true asset-backed transactions. In order to satisfy Shari’ah requirements and yet also retain investors’ interest, in addition to secured Sukuk (that is, Islamic securitisa-tion structures), new innovation may come into these non-secured structures and may provide recourse to investors to both the corporate credit of the obligor as well as to the assets in case the obligor fails to fulfil his obligations.

While Sukuk have been very successful in the past, the demand for Sukuk needs to be rekindled for corporate as well as sovereign and sub-sovereign issuers. The Sukuk market gen-erally remains a relatively young asset class which is facing the teething issues that are typical of any early stage product developmental challenges. During its short life span, clear short-comings have emerged which require constructive efforts from various regulators, Shari’ah scholars, lawyers, arrangers and the rating agencies to effectively address them. Sukuk as an instrument has huge potential for all types of issuers. Amongst these challenges are:

• a consensus on Sukuk structures amongst Islamic scholars around the world;• greater clarity in transaction structures with increased standardisation and lower overall

complexity;• a more predictable legal framework;• harmonisation and standardisation of Sukuk regulations;• a better education of issuer and investors about Sukuk and Shari’ah compliance;• a central information body in which all data can be publicly accessed;• developing active local debt capital markets to increase domestic participation; • a focus on substance over form;• a more liquid secondary market;• multicurrency Sukuk to be offered to have a greater distribution network;• large ticket Sukuk to be issued in international currency;• small to mid-sized Sukuk to be issued in local or domestic currency;• ease of accessibility of local investors in both primary and secondary markets;• assumption of the ‘true risk’ of the assets by the investors; and

• product invocation [Author query: innovation or invocation] with focus on developing alternatives for controversial products.

The sooner, the Islamic finance fraternity, its participants and players can work out these issues; the better it will be for the Sukuk as an asset category to become an active part of debt raising options available to Issuers around the world.

The debate on Sukuk is not over yet and the final verdict is not out. Will further innovation give way to Sukuk’s growth or will there be further enhancements in the underlying structures, or perhaps investors will agree to share the risk with the right sort of rewards? The Islamic finance industry is still in its infancy. If we start distinguishing between the products which are compliant from a pure Islamic jurisprudence perspective, but contrary to the higher objec-tives of Shari’ah while maintaining the spirit of Shari’ah, then the Islamic financing industry whether it is Sukuk or any other product may not survive in any form or shape.

Whichever Sukuk structure survives the scrutiny of Islamic jurisprudence, one thing is sure: Sukuk will thrive primarily in the Muslim world and in those jurisdictions who would like to tap into the liquidity pool available within the regions where investors prefer Halal returns.

Exhibit 10.10

[Author query: please supply exhibit title.]

Source: [Author query: please supply details. If author’s own, please state ‘Author’s own’.]

Ijarah Sukuk is essentially sale and lease back structures under which certificates are issued on stand-alone assets identified on the balance sheet. The assets can be parcels of land to be leased, buildings, leased plants and machineries, equipment such as aircrafts and ships. The rental rates of returns on these Sukuks can be both fixed and floating depending on the particular originator. The income generated under a Sukuk al Ijarah comes from the underlying rent receivables.

The obligor seeking to raise funding through the issuance of Sukuk al Ijarah sells certain assets to the issuer. The issuer, then, pays for the assets using the proceeds of the Sukuk issu-ance and holds title to the assets on trust for the Sukuk holders. The issuer acting in its capacity as lessor leases the assets back to the originator or obligor as the lessee for a fixed period of time and for a rent. At maturity, the originator or obligor may have the right to purchase the assets back from the issuer at a price which would generally represent the redemption value for the Sukuk holders at maturity.

Exhibit 10.11

[Author query: please supply exhibit title.]

Source: [Author query: please supply details. If author’s own, please state ‘Author’s own’.]

Under the Sukuk Al Musharaka, the Sukuk holders contribute a capital amount to the issuer. The issuer then enters into a joint venture with the party seeking finance (the originator) where the issuer provides the capital received from the Sukuk holders, and the originator supplies either the assets and/or their own capital required for the business to function. The profits from the Musharaka business are distributed to the issuer and the originator at a predetermined basis. Any losses are shared in proportion to the capital contribution, and the Issuer pays a periodic distribution amount to the Sukuk holders from the Musharaka profit distribution.

This type of Sukuk has a few advantages; first, employing Musharaka returns is preferred from the viewpoint of jurists as such an arrangement would strengthen the paradigm of Islamic banking that considers partnership contracts as the embodiment of core ideals. Secondly, the floating rate of returns on these certificates would not depend on benchmarking with market references such as Libor, but would instead be contingent on the firm’s balance sheet actualities.

Sukuk Al Mudharabah

Essentially, Mudharabah is a contract between the Mudharib (the trustee or fund manager who is the skilled entrepreneur) and the fund provider (issuer acting on behalf of the Sukuk holders) whereby the issuer provided the capital to an enterprise to be managed by the Mudharib under a specified business plan. The profit generated by the Mudharib or the underlying activity are shared in accordance with the terms of the Mudharabah agreement while losses are borne

Exhibit 10.12

[Author query: please supply exhibit title.]

Source: [Author query: please supply details. If author’s own, please state ‘Author’s own’.]

solely by the capital provider, unless the losses are due to the Mudharib’s misconduct, negli-gence or breach of contractual terms.

The special purpose vehicle (SPV) issues Sukuk Al Mudharabah and will pay proceeds to the company or Mudharib which will be invested in accordance with an agreed investment plan prepared by the investment manager. The Mudharib shall distribute any profit generated in accordance with the terms of the investment management agreement.

On the scheduled redemption date, the SPV will have the right to require the obligor to purchase all of the assets, and the exercise price payable by obligor is intended to fund the redemption amount.

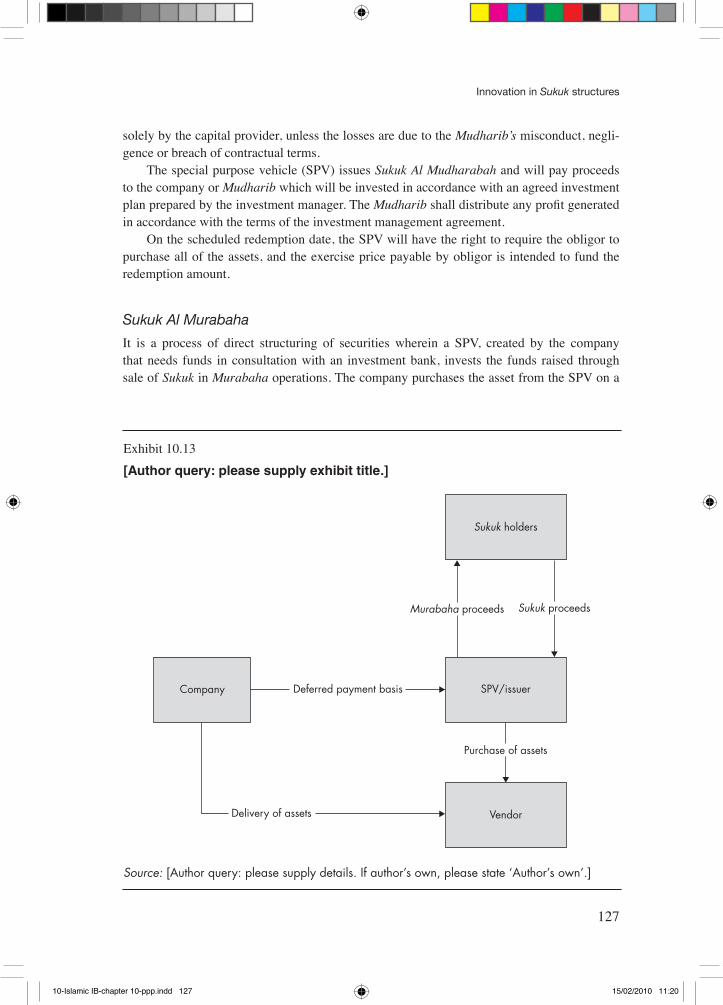

Sukuk Al Murabaha

It is a process of direct structuring of securities wherein a SPV, created by the company that needs funds in consultation with an investment bank, invests the funds raised through sale of Sukuk in Murabaha operations. The company purchases the asset from the SPV on a

Exhibit 10.13

[Author query: please supply exhibit title.]

Source: [Author query: please supply details. If author’s own, please state ‘Author’s own’.]

Murabaha basis. The periodic instalments paid by the company in future to the SPV account for the repayment of the cost and the profit component.

Sukuk al Murabaha cannot be traded in the secondary market at a negotiated price, and hence, they are not liquid. It has been found, in parts of the Islamic world, that the sale of debt at a pre-negotiated price or at a discount opens the floodgates of Riba.

Only if investors hold on to the instruments till maturity, the yield on the instrument would constitute legitimate profit. The non-permissibility of secondary market trading, how-ever, severely limits the liquidity, and therefore, attractiveness of the instrument from inves-tor’s viewpoint.

Sukuk Al Wakalah

It is a process whereby the Sukuk holders appoint the obligor an agent through the issuer to carry out certain pre-determined activities.

The SPV (issuer) will issue the Wakala Sukuk, the proceeds of which will be used to acquire a pool of underlying assets. The payments resulting from this pool of assets will serve as the basis for the periodic distribution amounts payable to certificate holders.

The obligor will undertake irrevocably to purchase the assets held by the issuer at the maturity (redemption) date of the Sukuk at a predefined price. Sukuk redemption (or dissolu-tion) can also occur earlier if defined events of default occur.

The obligation of obligor ranks pari passu with all other senior unsecured obligations of the obligor.

Exhibit 10.14

[Author query: please supply exhibit title.]

Source: [Author query: please supply details. If author’s own, please state ‘Author’s own’.]

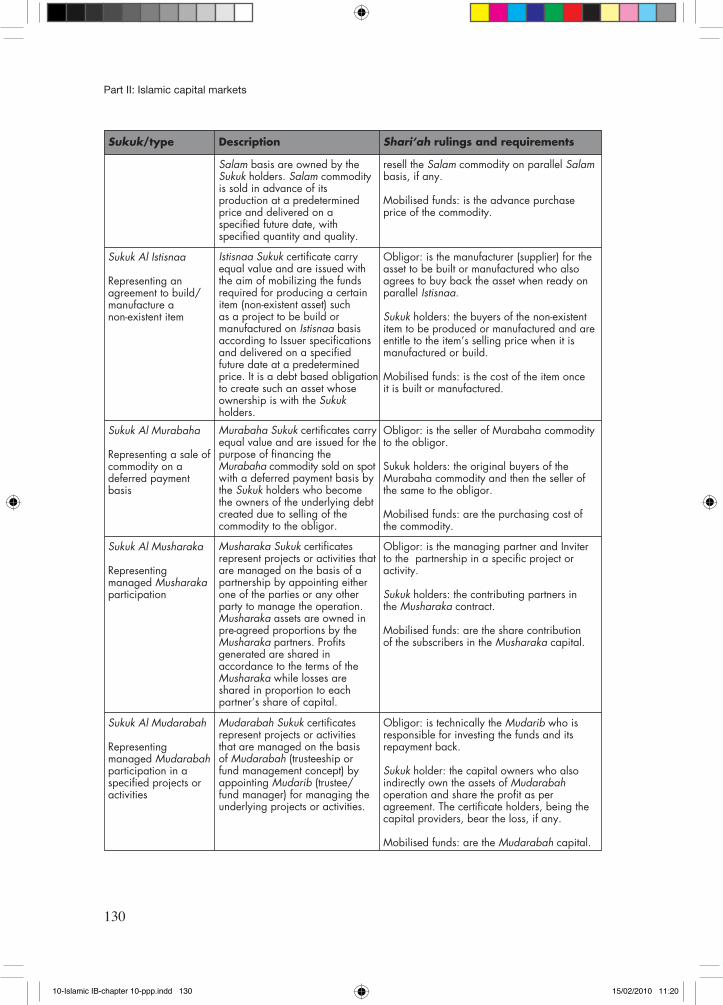

Sukuk/type Description Shari’ah rulings and requirements

Sukuk Al Ijarah

Representingownership of leasedassets

Obligor: sells services, that is providingeducation degree.

Sukuk holders: buyers of the services (a formof Usufruct) who can also re-sell such usufruct.

Mobilised funds: is the purchase price of theservices.

Ijarah Sukuk certificates carryequal value and are issued eitherby the owner of a leased asset oran asset to be leased by promise,or by its financial intermediary.The purpose of this Sukuk is to sellthe asset and recover its valuefrom the Sukuk holders, who thenbecome the beneficial or realowners of the assets and lease itback to the obligor.

Obligor: seller of a leased asset or an assetto be leased in a Sukuk on promise to buyback.

Sukuk holder : buyers of the beneficial orreal interest in the asset and should carryits risks and benefits who in turn lease theasset back to the obligor.

Mobilised funds: is the purchase price ofthe asset given to the obligor.

Sukuk Al Ijarah

Representingusufructs of existingassets

Ijarah Sukuk certificates carryequal value and are issued eitherby the owner of usufruct of anexisting asset or by its financialintermediary. The purpose ofleasing or subleasing the asset isto receive gross rental value fromthe revenue of subscription from theSukuk holders, who then becomethe beneficial or real owners ofthe usufruct of the asset and leaseback the asset to the obligor.

Obligor: seller of the usufruct of anexisting asset which is leasedbacked under Sukuk.

Sukuk holders: buyers of theusufruct and should carry its risksand benefits who in turn lease theasset back to the obligor.

Mobilised funds: is the purchaseprice of the usufructs

Sukuk Al Ijarah

Representingusufructs to be madeavailable in the futureas per description

Sukuk Al Ijarah

Representing servicesof a specified supplier

Sukuk Al Salam

Representing anadvance purchaseof a Salam commodity

Ijarah Sukuk certificates carryequal value issued for the sakeof leasing assets that the Lessor isliable to provide in the futurewhere by its gross rental isrecovered from the subscriptionincome from the Sukuk holders,who then become the beneficialor real owners of the usufruct ofthese future assets and agree tolease back the asset whencompleted.

Ijarah Sukuk certificate carryequal value issued for the sake ofproviding or selling servicesthrough a specified supplier (suchas educational degree in auniversity) and obtaining thevalue in the form of subscriptionincome from the Sukuk holderswho become the owners ofservices provided.

Obligor: seller of the usufruct of an assetto be made available in the future as perspecification with an agreement to leaseback the asset once ready.

Sukuk holders: buyers of the usufruct andshould carry its risks and benefits who inturn lease the asset back to the obligorwhen it is ready.

Mobilised funds: is the purchase priceof the usufructs of the future asset.

Exhibit 10.15

Global Sukuk issuance

Salam Sukuk certificates carryequal value issued for the sakeof mobilizing Salam capital forproducing a Salam commodityand the items to be delivered on

Obligor: seller of the Salam commodity forpayment in advance

Sukuk holders: buyers of that commodity whoare entitled to the Salam commodity. They can

Sukuk/type Description Shari’ah rulings and requirements

Salam basis are owned by theSukuk holders. Salam commodityis sold in advance of itsproduction at a predeterminedprice and delivered on aspecified future date, withspecified quantity and quality.

Istisnaa Sukuk certificate carryequal value and are issued withthe aim of mobilizing the fundsrequired for producing a certainitem (non-existent asset) suchas a project to be build ormanufactured on Istisnaa basisaccording to Issuer specificationsand delivered on a specifiedfuture date at a predeterminedprice. It is a debt based obligationto create such an asset whoseownership is with the Sukukholders.

Murabaha Sukuk certificates carryequal value and are issued for thepurpose of financing theMurabaha commodity sold on spotwith a deferred payment basis bythe Sukuk holders who become the owners of the underlying debtcreated due to selling of thecommodity to the obligor.

Musharaka Sukuk certificatesrepresent projects or activities thatare managed on the basis of apartnership by appointing eitherone of the parties or any otherparty to manage the operation.Musharaka assets are owned inpre-agreed proportions by theMusharaka partners. Profitsgenerated are shared inaccordance to the terms of theMusharaka while losses areshared in proportion to eachpartner’s share of capital.

Mudarabah Sukuk certificatesrepresent projects or activitiesthat are managed on the basisof Mudarabah (trusteeship orfund management concept) byappointing Mudarib (trustee/fund manager) for managing theunderlying projects or activities.

Obligor: is the manufacturer (supplier) for theasset to be built or manufactured who alsoagrees to buy back the asset when ready onparallel Istisnaa.

Sukuk holders: the buyers of the non-existentitem to be produced or manufactured and areentitle to the item’s selling price when it ismanufactured or build.

Mobilised funds: is the cost of the item onceit is built or manufactured.

Obligor: is the seller of Murabaha commodityto the obligor.

Sukuk holders: the original buyers of theMurabaha commodity and then the seller ofthe same to the obligor.

Mobilised funds: are the purchasing cost ofthe commodity.

Obligor: is the managing partner and Inviterto the partnership in a specific project oractivity.

Sukuk holders: the contributing partners inthe Musharaka contract.

Mobilised funds: are the share contributionof the subscribers in the Musharaka capital.