29

1 INNOVATIONS IN INDEXING – APPLICATION TO ASIA Asia Roadshow November/December 2011

| Date post: | 29-Mar-2018 |

| Category: |

Documents |

| Upload: | duongduong |

| View: | 215 times |

| Download: | 1 times |

1

INNOVATIONS IN INDEXING – APPLICATION TO ASIA

Asia Roadshow November/December 2011

2

Agenda

1. STOXX Ltd. – Introduction Page 03

2. Evolution of indexing - Asia Page 08

3. The next level – enhanced indexing Page 21

3

1. STOXX LTD - INTRODUCTION

4

STOXX at a glance

Shareholder

structure

History of STOXX » STOXX was founded in 1998 and the first to launch the European family of

indices - STOXX® indices, including the EURO STOXX 50® Index, which marked the beginning of a unique success story

» Deutsche Börse and SIX Group are the shareholders of STOXX

STOXX is marketing agent for DAX, SMI indices and iNAV ® » Unified sales platform not only for STOXX indices but also for leading

national indices » Provides real time indicative net asset value (iNAV® ) calculation service

Global

presence

Unified sales

platform

Focus on

innovation

and clients

STOXX aims Global » STOXX has over 60 employees worldwide » STOXX is headquartered in Zurich, Switzerland and has satellite offices in

Frankfurt, Hong Kong, London, Madrid, New York, Paris, Singapore, Stockholm, and Tokyo

STOXX is dedicated to deliver innovation in indices » The indices are licensed to more than 400 companies among the world’s

largest financial products issuers, capital owners, and asset managers » Proven track record for innovation to be continued

5

STOXX – the proven innovator in the last decade and the future

» First index provider using free-float market cap weighting throughout its

index family

» First index provider offering an optimized investability

(by considering borrowing availability) for both sector & country indices

» Offering access to direct dividend investments

("dividend point indices")

» Leading provider of European volatility concepts

Innovation in indexing

» First pan-European equity, size, and sector ETFs, and futures and options

» First buy-write ETFs globally, first dividend point, and volatility strategy

ETFs

Innovative financial products

Innovations

1368

657

191

225

169

96

80

688

357

65

114

82

48

42

2049

727

335

53

270

83

66

36

36131716Kospi

S&P

STOXX

DAX

RTS

Nikkei

Taiex

Nasdaq

STOXX is a leading global index provider

ETF market

A

Derivatives market

B

Struct. prod. market

C

Index pro-vider

31 Dec 2010 30 Jun 2011

AuM1)

# ETFs AuM1)

# ETFs Delta2)

AUM/#

MSCI 337.8 389 366.9 453 9/16

S&P 301.1 315 325.6 355 8/13

BarCap 111.2 84 126.4 100 14/19

STOXX (incl. DAX and SIX)

89.7 283 105.3 290 17/2

Russell 80.5 70 84.5 91 5/30

FTSE 54.9 161 60.6 175 10/9

Dow Jones

46.7 138 54.5 159 17/15

Markit 45.1 112 48.3 125 7/12

Nasdaq 31.7 61 33.6 62 6/2

NYSE 16.6 41 17.3 46 4/12

Traded futures & options3) Index

# issues in 2010

# issues in Q1-Q3/2011

Delta Q1-Q3/2011 vs. 2010

DAX 139`526 234'871 168%

STOXX 44`363 52'719 119%

S&P 8`669 8'272 95%

Dow Jones

5`950 5'766 97%

Hang Seng

1`942 5'772 297%

Euronext 4`561 4'154 91%

FTSE 1`586 1'045 66%

MSCI 1`672 2'044 122%

Number 4 globally in the ETF market

Number 3 out of the top 7 derivatives globally

Largest provider of SP underlyings globally

Market position

1) bn USD; Source: BlackRock 2) figures in % 3) In million contracts

Source: BlackRock, Homepagestatistics, FIA, Structured Retail Products

6

2010 H1/2010 H1/2011

7

STOXX operates a unique global index family with innovative

focus

Total Market Index

(“TMI”)

Standard

indices

(“STOXX“)

Advanced

indices

(“STOXX+“)

Broad

indices

Blue-

chip

indices

Sector

indices

Style

indices

Size

indices

Leverage

and Short

indices

Risk

Control indices

Optimal

Leverage

indices

(Sub-) Regions

» Global » Americas » Asia » Pacific

» All Europe » Latin America » BRIC

Global index universe

Comprehensive set of indices … available worldwide

Total 53 countries covered

Countries » Argentina » Australia » Austria » …

» … » Ukraine » United Kingdom » USA

8

2. EVOLUTION OF INDEXING - ASIA

9

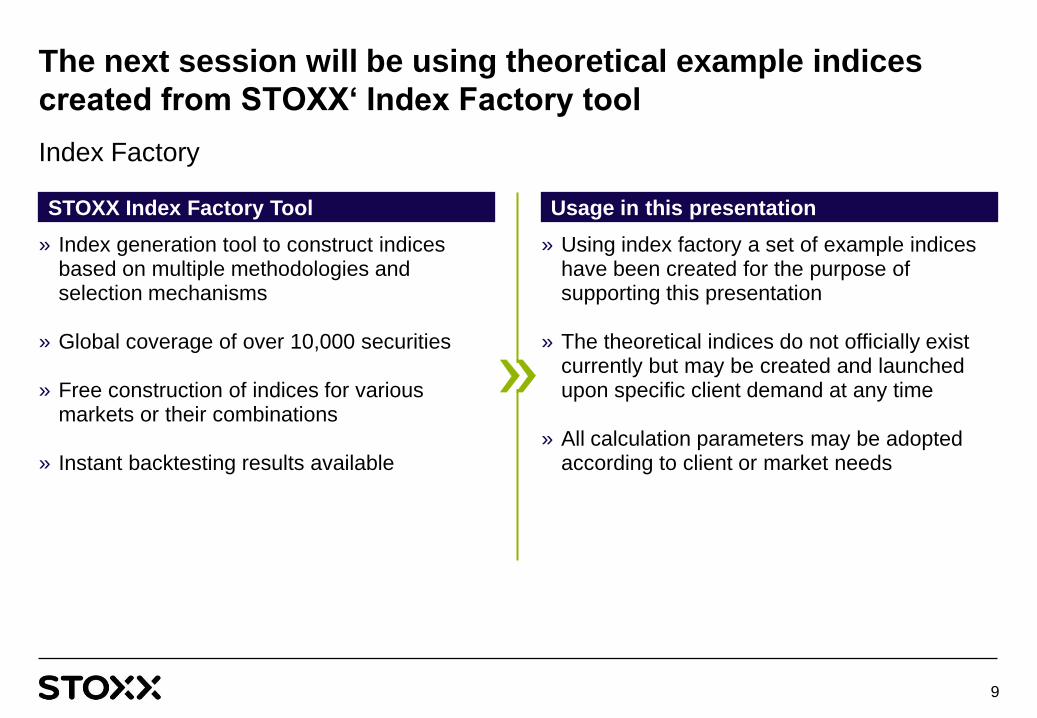

The next session will be using theoretical example indices

created from STOXX„ Index Factory tool

» Index generation tool to construct indices based on multiple methodologies and selection mechanisms

» Global coverage of over 10,000 securities

» Free construction of indices for various markets or their combinations

» Instant backtesting results available

STOXX Index Factory Tool

» Using index factory a set of example indices have been created for the purpose of supporting this presentation

» The theoretical indices do not officially exist currently but may be created and launched upon specific client demand at any time

» All calculation parameters may be adopted according to client or market needs

Usage in this presentation

Index Factory

10

Evolution of indexing for a region will be looked at in three

major steps

» Compilation of broad market benchmarks (TMI indices)

» Construction of represen-tative, liquid and tradeable blue chip indices

Individual countries

» Developed market core index

» Stepwise addition of emerging markets according to investors preferences

Regional indices

» Application of enhanced index strategies to previously built indices

Enhanced indices 3 2 1

Overview

In the next step examples for constructing these steps for the Asian region will be discussed

11

First step is creation of a broad market index for the individual

country as market measurement

STOXX Japan TMI STOXX Singapore TMI STOXX Hong Kong TMI

Step 1a - country TMI indices

1) Annualized 27/12/01 – 14/11/11

2) in mn USD for current composition

Return1) 0.39%

Volatility1) 25.28%

Ø ADTV2) 6.68

Ø MCap2) 1,484.11

Return1) 7.71%

Volatility1) 24.43%

Ø ADTV2) 1.18

Ø MCap2) 249.30

Return1) 9.46%

Volatility1) 20.77%

Ø ADTV2) 0.22

Ø MCap2) 66.52

0

500

1,000

1,500

2,000

2,500

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10

0

500

1,000

1,500

2,000

2,500

3,000

3,500

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10

0

500

1,000

1,500

2,000

2,500

3,000

3,500

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10

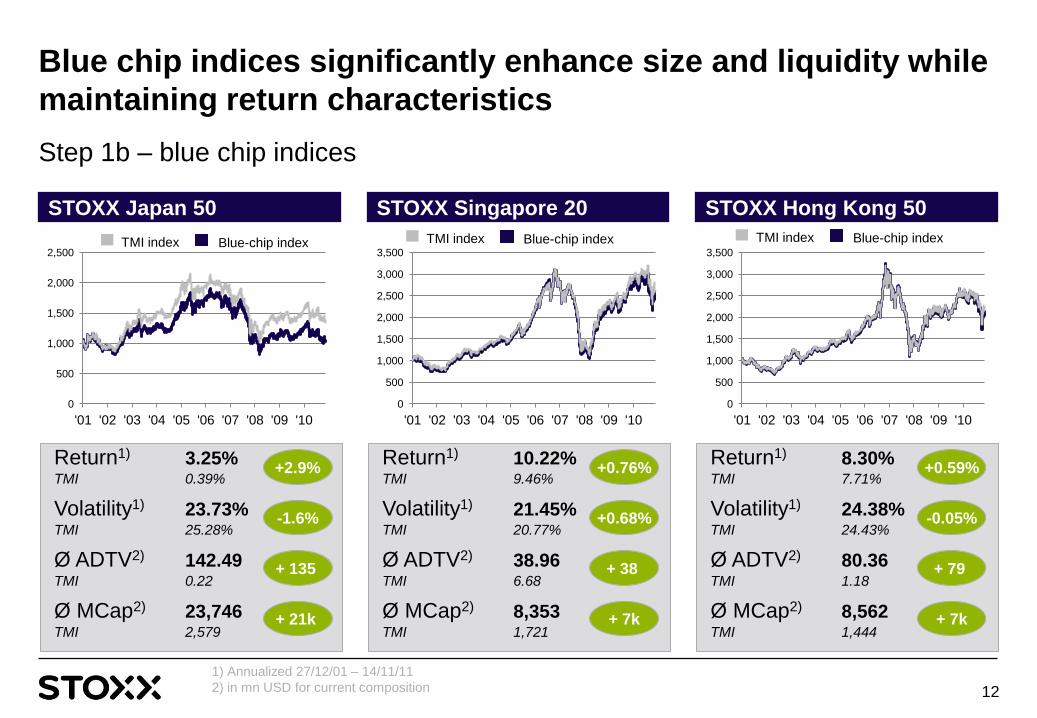

12

Blue chip indices significantly enhance size and liquidity while

maintaining return characteristics

Return1) 3.25% TMI 0.39%

Volatility1) 23.73% TMI 25.28%

Ø ADTV2) 142.49 TMI 0.22

Ø MCap2) 23,746 TMI 2,579

STOXX Japan 50 STOXX Singapore 20 STOXX Hong Kong 50

Step 1b – blue chip indices

1) Annualized 27/12/01 – 14/11/11

2) in mn USD for current composition

Return1) 8.30% TMI 7.71%

Volatility1) 24.38% TMI 24.43%

Ø ADTV2) 80.36 TMI 1.18

Ø MCap2) 8,562

TMI 1,444

Return1) 10.22% TMI 9.46%

Volatility1) 21.45% TMI 20.77%

Ø ADTV2) 38.96 TMI 6.68

Ø MCap2) 8,353 TMI 1,721

0

500

1,000

1,500

2,000

2,500

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10

0

500

1,000

1,500

2,000

2,500

3,000

3,500

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10

0

500

1,000

1,500

2,000

2,500

3,000

3,500

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10

+2.9%

-1.6%

+ 135

+ 21k

+0.76%

+0.68%

+ 38

+ 7k

+0.59%

-0.05%

+ 79

+ 7k

Blue-chip index TMI index Blue-chip index TMI index Blue-chip index TMI index

13

Regional index covers entire region with high liquidity and

market cap – significant underrun vs. global equity

Step 2a – regional indices

Developed market Asia index (DMAI)

DMAI STOXX Global 1800

» Developed Asia Index with significantly different performance to global index

» Underperformance over last 10 years overall though compared to global developed markets

Source: STOXX calculations

0

500

1000

1500

2000

2500

2002 2003 2004 2005 2006 2007 2008 2009 2010

Return1) 4.9% STOXX Gl. 1800 7.1%

Volatility1) 23.5% STOXX Gl. 1800 17.8%

-2.2%

+5.7%

14

Results of index calculations in the presentation will be

compared on risk / return matrix

Overview risk / return profile

Risk / Return matrix Indices

» STOXX Japan 50 » STOXX Singapore 20 » STOXX Hong Kong 50 » DMAI

1) Footnote, 10 pt

0%

2%

4%

6%

8%

10%

12%

18% 19% 20% 21% 22% 23% 24% 25% 26%

DMAI

STOXX

Singapore 20

STOXX

Japan 50

STOXX Hong

Kong 50

No huge diversification effect on portfolio – strong dominance of Japan

15

Small portion of South Korean stocks to the developed market

basket leads to improved risk return profile

Step 2b – regional indices with further markets (1/4)

DMAI + South Korea (DMAI+SK)

DMAI+SK DMAI

» South Korean Index with extreme outperformance

» Addition of only 20 stocks adds over 3% performance p.a. and reduces risk

Source: STOXX calculations

Return1) 8.1% DMAI 4.9%

Volatility1) 22.4% DMAI 23.5%

+3.2%

-1.1%

South Korea Index

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2002 2003 2004 2005 2006 2007 2008 2009 2010

16

Addition of further markets lead to smaller change in risk

return profile – lower risk observed

Step 2b – regional indices with further markets (2/4)

DMAI+SK + Malaysia (DMAI+SK+MA)

DMAI+SK+MA DMAI

» Addition of Malaysia (20 stocks) adds further performance and risk reduction

» Smaller additional effect though

Source: STOXX calculations

Return1) 8.4% DMAI 4.9%

Volatility1) 22.1% DMAI 23.5%

+3.5%

-1.4%

Malaysia Index

0

500

1000

1500

2000

2500

3000

2002 2003 2004 2005 2006 2007 2008 2009 2010

17

Adding markets with smaller companies such as Phillipines

with limited impact on portfolio

Step 2b – regional indices with further markets (3/4)

DMAI+SK+MA + Phillipines (DMAI+SK+MA+PH)

DMAI+SK+MA+PH DMAI

» Addition adds only 1/10 % to performance

» This is due to relatively small market cap of Philippine stocks added

Source: STOXX calculations

Return1) 8.5% DMAI 4.9%

Volatility1) 22.1% DMAI 23.5%

+3.6%

-1.4%

Philippine Index

0

1000

2000

3000

4000

5000

6000

2002 2003 2004 2005 2006 2007 2008 2009 2010

18

Addition of major market such as China leads to further risk

reduction – negative impact on performance though

Step 2b – regional indices with further markets (4/4)

DMAI+SK+MA+PH + China (DMAI+SK+MA+PH+CN)

DMAI+SK+MA+PH+CN DMAI

» 30 Chinese stocks offer additional diversification potential and reduce risk by further 0.5%

» Performance impact is negative due to relative underperformance of China

Source: STOXX calculations

Return1) 8.3% DMAI 4.9%

Volatility1) 21.6% DMAI 23.5%

+3.4%

-1.9%

China Index

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2002 2003 2004 2005 2006 2007 2008 2009 2010

19

Results of index calculations in the presentation will be

compared on risk / return matrix

Overview risk / return profile

Risk / Return matrix Indices

» STOXX Japan 50 » STOXX Singapore 20 » STOXX Hong Kong 50 » DMAI » DMAI+SK » DMAI+SK+MA » DMAI+SK+MA+CN » DMAI+SK+MA+CN+PH

Source: STOXX calculations

0%

2%

4%

6%

8%

10%

12%

18% 19% 20% 21% 22% 23% 24% 25% 26%

DMAI

DMAI + EM

STOXX

Singapore 20

STOXX

Japan 50

STOXX Hong

Kong 50

Addition of EM with significant improvement of risk/return profile

20

Index calculation framework allows fast analysis and

implementation of asset allocation strategies for Asia

» Index performance for developed Asia has not been overly exciting over 10 year time span compared to global developed markets

» Addition of small portions of more emerging markets can significantly shift risk return profile into the right direction

» Not all markets are equally tradeable for all market participants

» Countries with larger companies add more value to this approach than smaller ones

Observations

» Overall asset allocation to different markets drives portfolio performance

» Standardized frameworks for constructing indiviudal indices to fit investor needs forms as a basis to startegically steer investments

» The road does not end here – enhanced indexing as next step of development on top of the standard market indices! More in the next chapter!

Conclusions

Intermediary summary

21

3. THE NEXT LEVEL – ENHANCED INDEXING

22

Enhanced indexing adds further dimension to the investment

objective

» Enables investors to indivually choose their desired risk level, while maintaining exposure to the desired underlying market

» ALREADY LAUNCHED

STOXX Asia

100 Risk

Control

Enhanced indexing applications to Asia

» Strategy aimed at optimizing the level of exposure to the target market depending on current market conditions

» ALREADY LAUNCHED

STOXX Asia

100 Optimal

Leverage

» Using already developed index and applying equal weighting strategy to the portfolio to conquer the shortcomings of market cap weighted portfolios

» CONCEPT ONLY

Asia Equal

Weight

» Application of STOXX‘ groundbreaking ESG rating model to the developed Asia markets

» Enables investors to comply with sustainability restrictions » CONCEPT ONLY

STOXX Asia

ESG Leaders

Index

0

500

1000

1500

2000

2500

3000

3500

2002 2004 2006 2008 2010

23

Risk control indices allow investors to choose their risk level

while investing in specific markets

» The risk control strategy is available at multiple risk

levels ranging from 5% to 20% but could also

accommodate custom levels

» The strategy leverages or de-leverages an investment

in an underlying index according to the current market

volatility

» If market volatility is below the desired risk level,

the investment is leveraged up to achieve the

higher risk level

» If market volatility is higher than the desired risk

level the investment is de-leveraged by means

of cash investment to achieve the lower risk

level

Name Performance1) Volatility1)

STOXX Asia 100 Risk Control 20%

9.27% 18.96%

STOXX Asia 100 5.10% 25.63%

Concept Overview

STOXX Asia 100 Risk Control Performance Chart

1) Annualized June 2002-2011

STOXX Asia 100

STOXX Asia 100 Risk Control 20%

0

500

1000

1500

2000

2500

3000

2002 2004 2006 2008 2010

24

Optimal leverage uses a leverage factor between 0.5 and 4 to

optimized returns from an underlying index

» The optimal leverage strategy ensures high leverage

in bull markets, by increasing the leverage factor due

to increasing index returns

» Reduces leverage in turbulent market by reducing the

leverage factor due to increasing volatility

» Uses volatility as risk measure to ensure a timely

response to market turbulences

» The index portfolio consists of

» Leveraged STOXX blue-chip index

» A loan in the overnight money-market to

finance the leverage

» The optimal leverage factor is determined monthly

based on the risk / return profile of the underlying

blue-chip index

Name Performance1) Volatility1)

STOXX Asia 100 Optimal Leverage

2.03% 20.03%

STOXX Asia 100 5.10% 25.63%

Concept Overview

STOXX Asia 100 Optimal Leverage Performance Chart

1) Annualized June 2002-2011

STOXX Asia 100

STOXX Asia 100 Optimal Leverage

300

500

700

900

1100

1300

2006 2007 2008 2009 2010 2011

25

Equal weighting of each constituent brings small or large cap

effects to the fore

» Equal weighting uses an existing index and modifies

the weighting to level all components weights on a

quarterly basis

» This enhances the weight of small and mid caps in

the indices – the performance does thus change

accordingly

» Mismatch of majority of allocated capital to highly

valued companies is broken up leading to positive

performance effect historically

» Phases of strong outperformance but also

underperformance observed historically

Name Performance1) Volatility1)

DMAI Equal Weight -3.26% 25.3%

DMAI -4.54% 25.7%

Concept Overview

Asia Index Equal Weight Performance Chart

1) Annualized 2006-2011

DMAI

DMAI Equal Weight

CONCEPT

0%

2%

4%

6%

8%

10%

12%

18% 19% 20% 21% 22% 23% 24% 25% 26%

DMAI

DMAI + EM

STOXX Asia 100

26

Results of index calculations in the presentation will be

compared on risk / return matrix

Overview risk / return profile

Risk / Return matrix Indices

» STOXX Japan 50 » STOXX Signapore 20 » STOXX Hong Kong 50 » DMAI » DMAI+SK » DMAI+SK+MA » DMAI+SK+MA+CN » DMAI+SK+MA+CN+PH » STOXX Asia 100 » STOXX Asia 100 Risk Control » STOXX Asia 100 Optimal Lev.

Source: STOXX Calculations

STOXX Asia 100

Optimal Leverage

STOXX

Singapore 20

STOXX

Japan 50

STOXX Hong

Kong 50

Overlay of strategies can shift risk levels massively: varying effects on returns

STOXX Asia 100

Risk Control 20%

27

STOXX ESG Indices are based on a transparent rating model –

coverage includes STOXX Asia 600 Index

Overview index concept

» STOXX Global ESG Leaders Index » Index made up of the sum of the three specialized indices » Contains global leaders in Environmental, Social and Governance

fields based on STOXX Global 1800 Index universe

» STOXX Global ESG Environmental Leaders, Social Leaders and Governance Leaders Indices » Selection of top 25% companies in each area Relative company

E, S and G ratings ranging from 0 to 100 indicating relative position to remaining basket as basis for selection

» Total of 128 Key Performance Indicators (KPI) relevant to sustainability criteria are used as basis for the rating model

» KPIs are approved by DVFA / EFFAS and are based on the KPI for ESG 3.0 Standard

» Data is provided by index partner Sustainalytics

Broad Index

E, S and G Specialized

Indices

Base Indicators mapped to

DVFA/EFFAS

KPI 3.0 Standard

CONCEPT

28

Customization and enhancing of index concepts allows

individual steering of risk return profile

» If you look at an index product for the Asian region, make sure to consider the country composition

and its fit to your investment objectives

» Indices for all requirements of country allocation and strategy overlay can be constructed easily at your demand based on a fully standardized set of index and strategy rules

» Your index provider should be able to help you implement the ideal underlying for your investment product – from simple to highly complex – just give us a call!

Contact Details: Konrad Sippel Global Head of Product Development STOXX Ltd. [email protected] +49 69 211 17369

Three things to take home today

Summary

29

Disclaimer

About STOXX STOXX Ltd. is an established and leading index specialist of European origins. The launch of the first STOXX® indices in 1998, including the EURO STOXX 50® Index, marked the beginning of a unique success story, based on the company’s neutrality and independence. Since then, STOXX has been at the forefront of market developments, continuously expanding its portfolio of innovative indices – and now operating on a global level, across all asset classes. The indices are licensed to more than 400 companies among the world’s largest financial products issuers, capital owners, and asset managers. They are used not only as underlyings for financial products such as ETFs, futures and options, and structured products, but also for risk and performance measurement. In addition, STOXX Ltd. is the marketing agent for the indices of Deutsche Börse AG and SIX Swiss Exchange Indices, among them the DAX® and the SMI® indices.

The indices in the presentation and the trademarks used in the index names are the intellectual property of

STOXX Ltd, or SIX Swiss Exchange AG, or Deutsche Börse AG.

The use of the STOXX®, DAX®, and SMI indices® and of the respective index data for financial products or

for other purposes requires a license from STOXX, Deutsche Börse AG, or SIX Swiss Exchange AG. STOXX

and its owners do not make any warranties or representations, express or implied, with respect to the

timeliness, sequence, accuracy, completeness, currentness, merchant- ability, quality, or fitness for any

particular purpose of its index data. STOXX and its owners are not providing investment advice through the

publication of indices or in connection therewith. In particular, the inclusion of a company in an index, its

weighting, or the exclusion of a company from an index, does not in any way reflect an opinion of STOXX or

its owners on the merits of that company. Financial instruments based on the STOXX®, DAX®, or SMI

indices® are in no way sponsored, endorsed, sold, or promoted by STOXX or its owners.