26

1 Innovative Technologies for a Better Competitiveness Jean Sentenac

| Date post: | 28-Mar-2018 |

| Category: |

Documents |

| Upload: | nguyencong |

| View: | 231 times |

| Download: | 2 times |

1

Innovative Technologiesfor a Better Competitiveness

Jean Sentenac

2

Axens

Process Licensing Catalysts & Adsorbents

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

3

Agenda

Better competitiveness …• By tackling demand issue

• Gasoline/Diesel imbalances• By converting the bottom of the barrel

• Cheaper crudes processing• In the EU context

• Quality• Renewables• CO2 Emissions

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

4

-0.6-0.5-0.4-0.3-0.2-0.10.00.10.20.30.40.50.60.7

Source: Axens & other sources

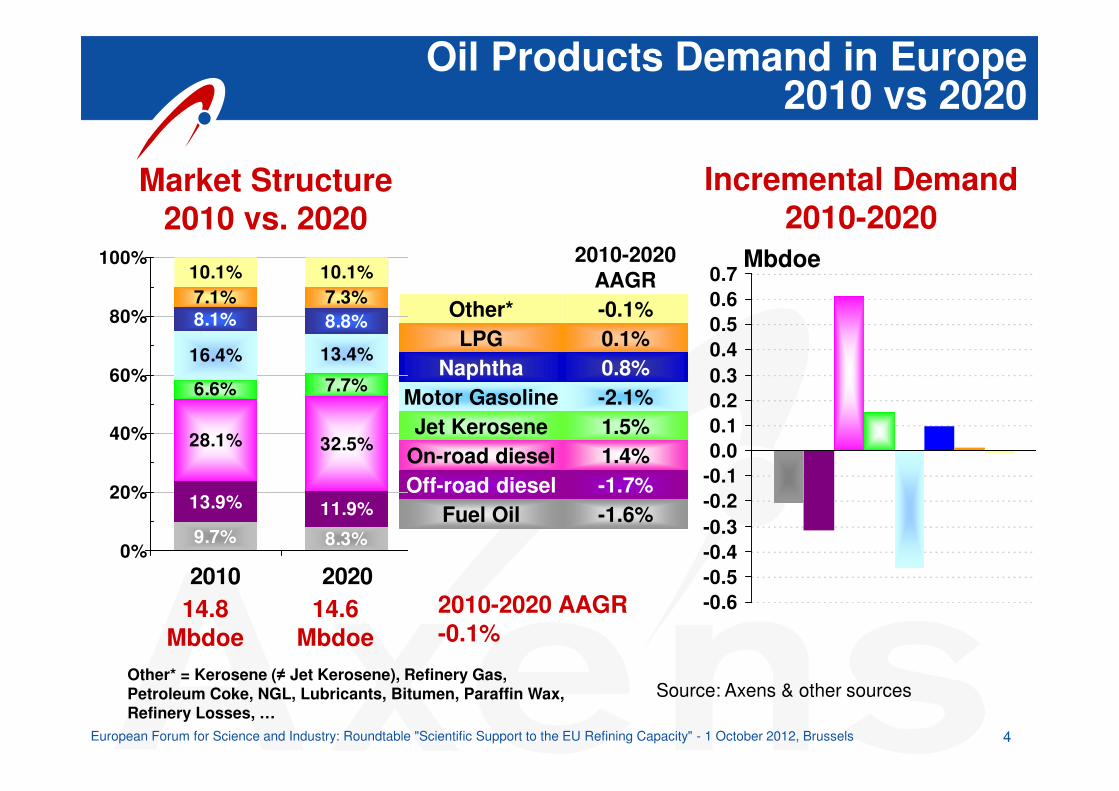

Market Structure2010 vs. 2020

Oil Products Demand in Europe2010 vs 2020

Other* = Kerosene (� Jet Kerosene), Refinery Gas, Petroleum Coke, NGL, Lubricants, Bitumen, Paraffin Wax, Refinery Losses, …

2010-2020 AAGR

Other* -0.1%LPG 0.1%

Naphtha 0.8%Motor Gasoline -2.1%Jet Kerosene 1.5%

On-road diesel 1.4%Off-road diesel -1.7%

Fuel Oil -1.6%

Mbdoe

Incremental Demand 2010-2020

9.7%

13.9%

28.1%

6.6%

16.4%

8.1%7.1%10.1%

8.3%

11.9%

32.5%

7.7%

13.4%

8.8%7.3%10.1%

0%

20%

40%

60%

80%

100%

2010 202014.8

Mbdoe14.6

Mbdoe2010-2020 AAGR-0.1%

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

5

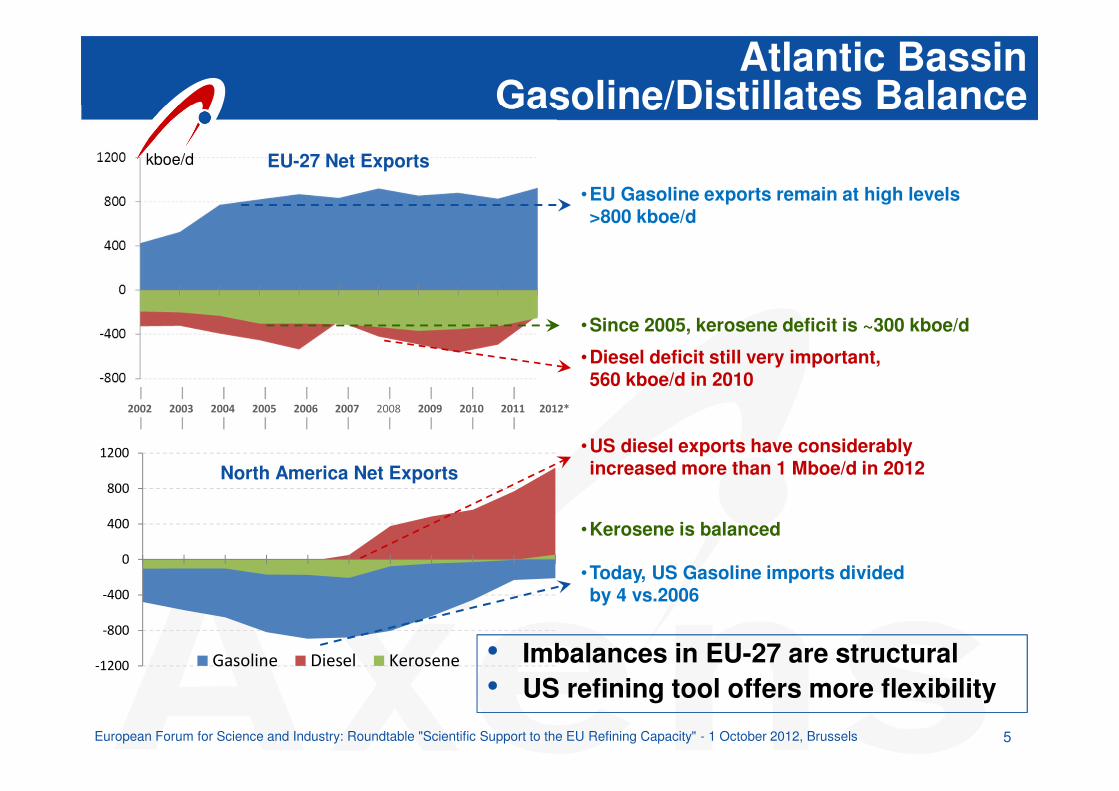

Atlantic BassinGasoline/Distillates Balance

kboe/d

�����

����

����

�

���

���

����

���� � ����� ���� �

EU-27 Net Exports

���� ���� ���� ���� ���� ���� ���� ���� ��� �� ���

North America Net Exports

•EU Gasoline exports remain at high levels >800 kboe/d

•Diesel deficit still very important, 560 kboe/d in 2010

•Since 2005, kerosene deficit is ~300 kboe/d

•US diesel exports have considerably increased more than 1 Mboe/d in 2012

•Today, US Gasoline imports divided by 4 vs.2006

•Kerosene is balanced

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

• Imbalances in EU-27 are structural• US refining tool offers more flexibility

6

European Gasoline / Distillates Imbalances

• In case of change in consumer behavior(buy more gasoline cars and less diesel cars), fuel demand not significantly impacted before 2025

• Offer : Capacity change scenarios do not solve Gasoline and Distillate issues together

• Biofuels (EtOH) worsen gasoline imbalances

Technological innovation will play a role

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

7

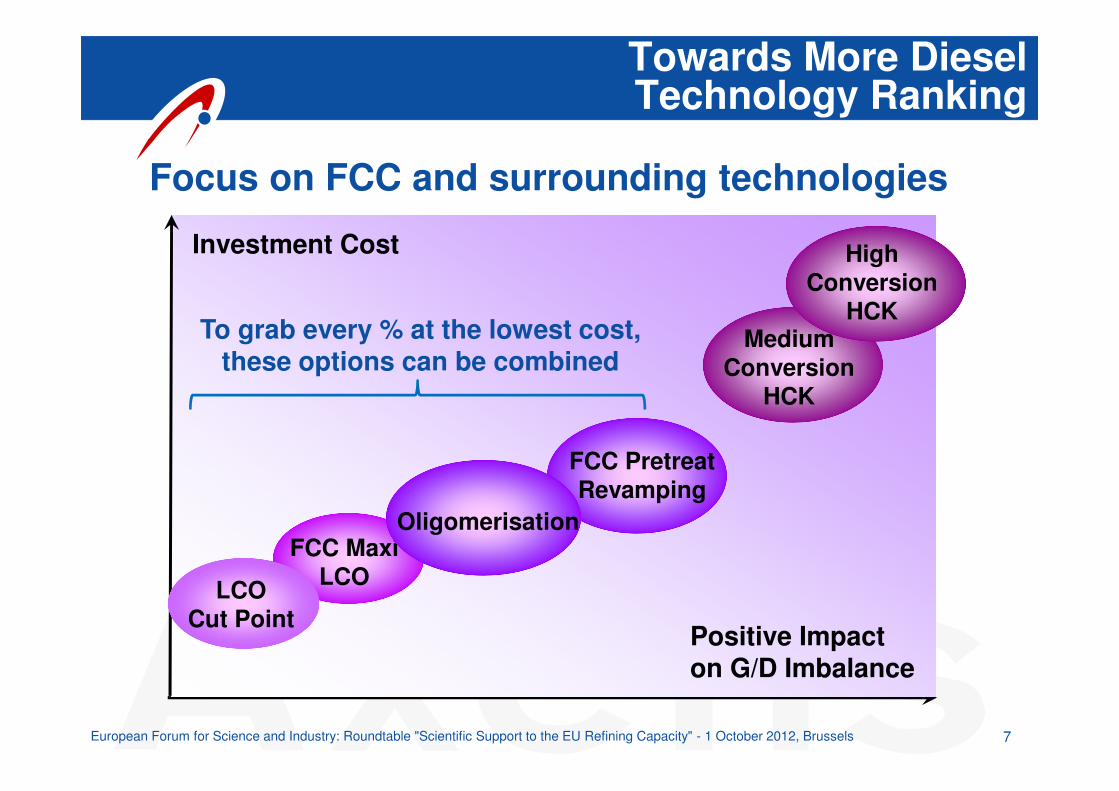

Towards More DieselTechnology Ranking

Positive Impacton G/D Imbalance

Investment Cost

FCC MaxiLCO

FCC Pretreat Revamping

Medium Conversion

HCK

Oligomerisation

LCO Cut Point

High Conversion

HCK

Focus on FCC and surrounding technologies

To grab every % at the lowest cost, these options can be combined

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

8

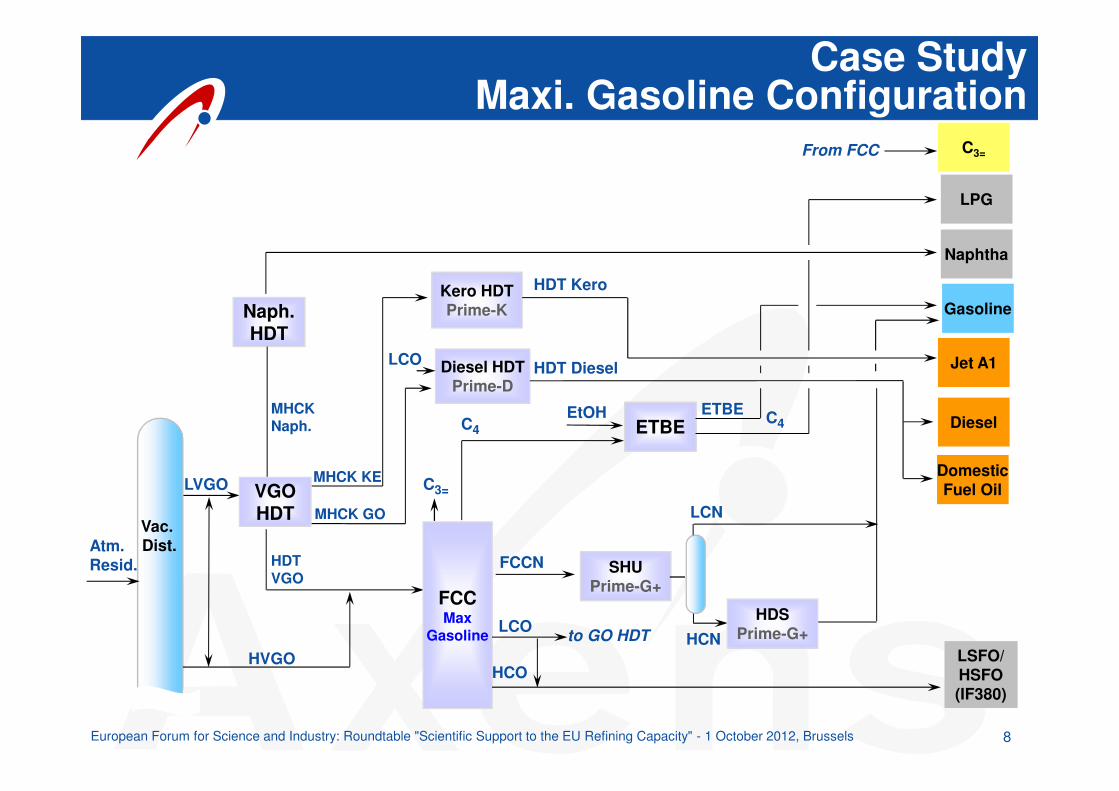

Case Study Maxi. Gasoline Configuration

Naph. HDT

Kero HDTPrime-K

SHUPrime-G+

Diesel HDTPrime-D

FCCMax

Gasoline

HVGO

HDT Kero

FCCN

LCO

HCO

HCN

EtOHMHCK Naph.

MHCK GO

HDT VGO

ETBEETBE

MHCK KE

HDSPrime-G+

LCN

LSFO/HSFO(IF380)

LPG

to GO HDT

Naphtha

Gasoline

VGOHDT

Atm. Resid.

Vac.Dist.

LVGO

LCO

C3=

C4C4

From FCC C3=

Domestic Fuel Oil

Diesel

Jet A1HDT Diesel

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

9

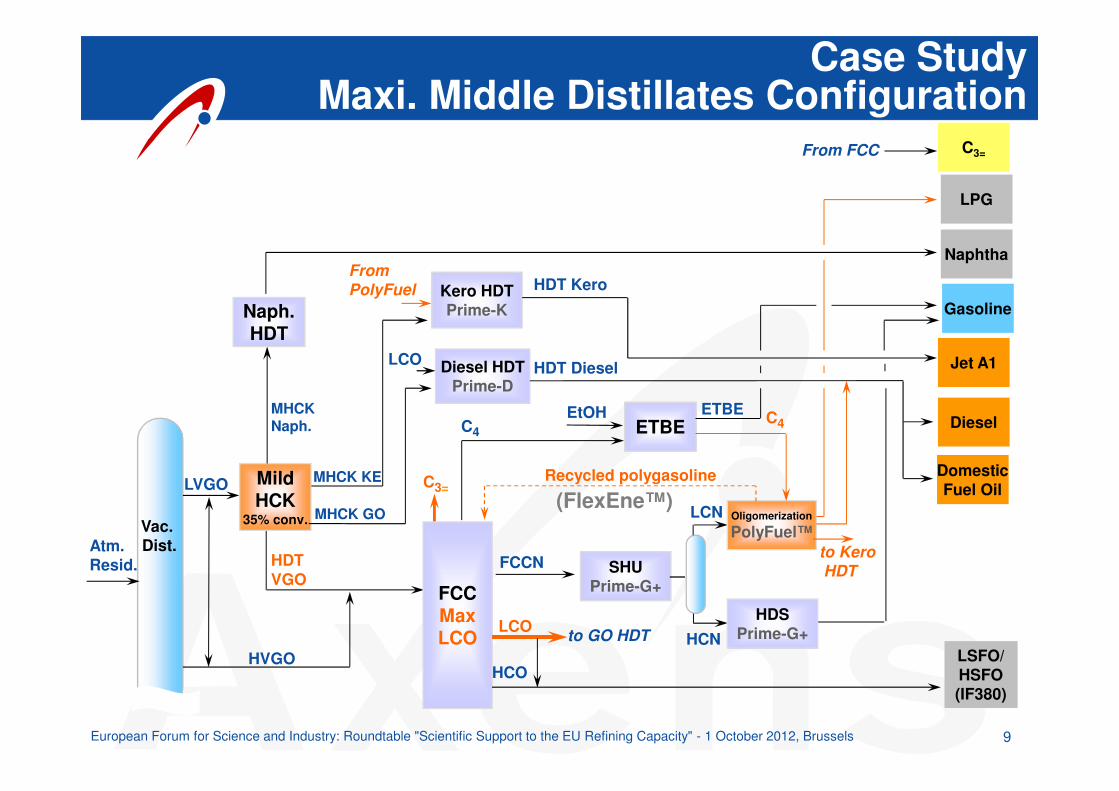

Case Study Maxi. Middle Distillates Configuration

SHUPrime-G+

Mild HCK

35% conv.

FCCMax LCO

Atm. Resid.

LVGO

HVGO

FCCN

LCO

HCO

HCN

EtOHMHCK Naph.

MHCK GOVac.Dist.

HDT VGO

ETBEETBE

HDSPrime-G+

LCN Oligomerization

PolyFuel™

Recycled polygasoline

From FCC

to GO HDT

MHCK KE

LCO

Domestic Fuel Oil

Diesel

Jet A1

LSFO/HSFO(IF380)

C3=

LPG

Naphtha

GasolineNaph. HDT

to KeroHDT

FromPolyFuel

C3=

C4C4

Kero HDTPrime-K

HDT Kero

Diesel HDTPrime-D

HDT Diesel

(FlexEne™)

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

10

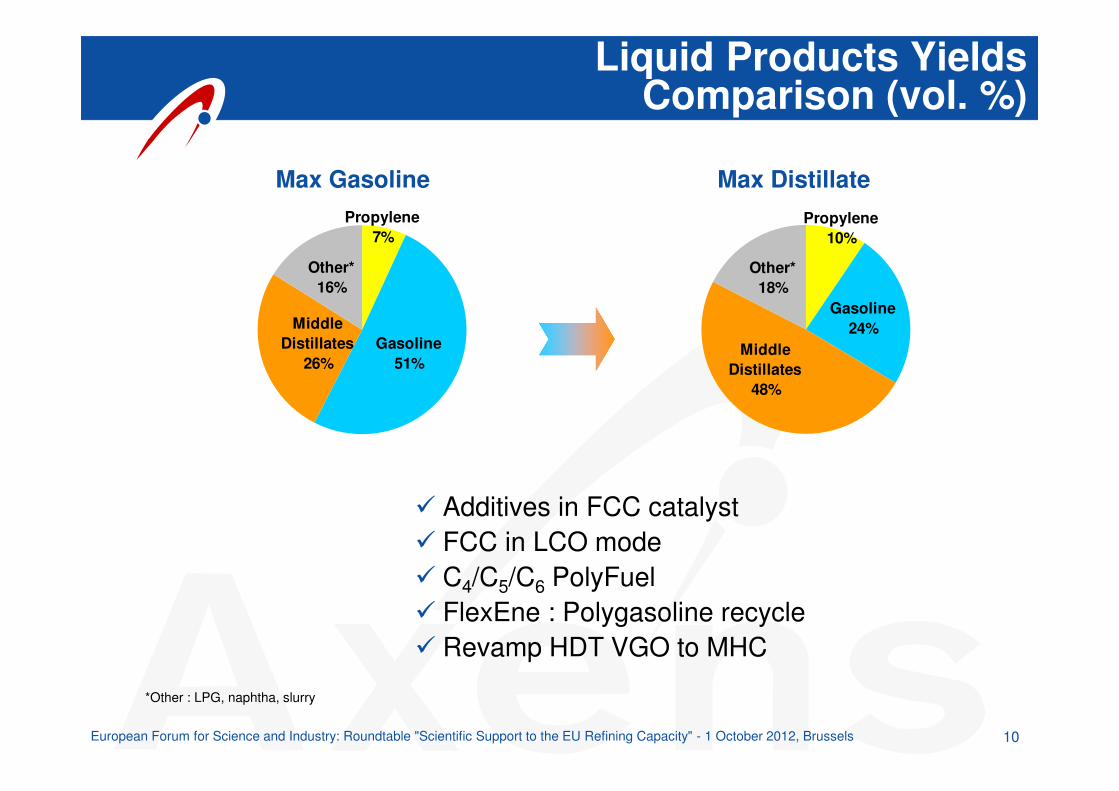

Liquid Products Yields Comparison (vol. %)

Propylene10%

Other*18%

Middle Distillates

48%

Gasoline24%

*Other : LPG, naphtha, slurry

Propylene7%

Other*16%

Middle Distillates

26%Gasoline

51%

� Additives in FCC catalyst� FCC in LCO mode � C4/C5/C6 PolyFuel� FlexEne : Polygasoline recycle � Revamp HDT VGO to MHC

Max Gasoline Max Distillate

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

11

Agenda

Better competitiveness …• By tackling demand issue

• Gasoline/Diesel imbalances• By converting the bottom of the barrel

• Cheaper crudes processing• In the EU context

• Quality• Renewables• CO2 Emissions

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

12

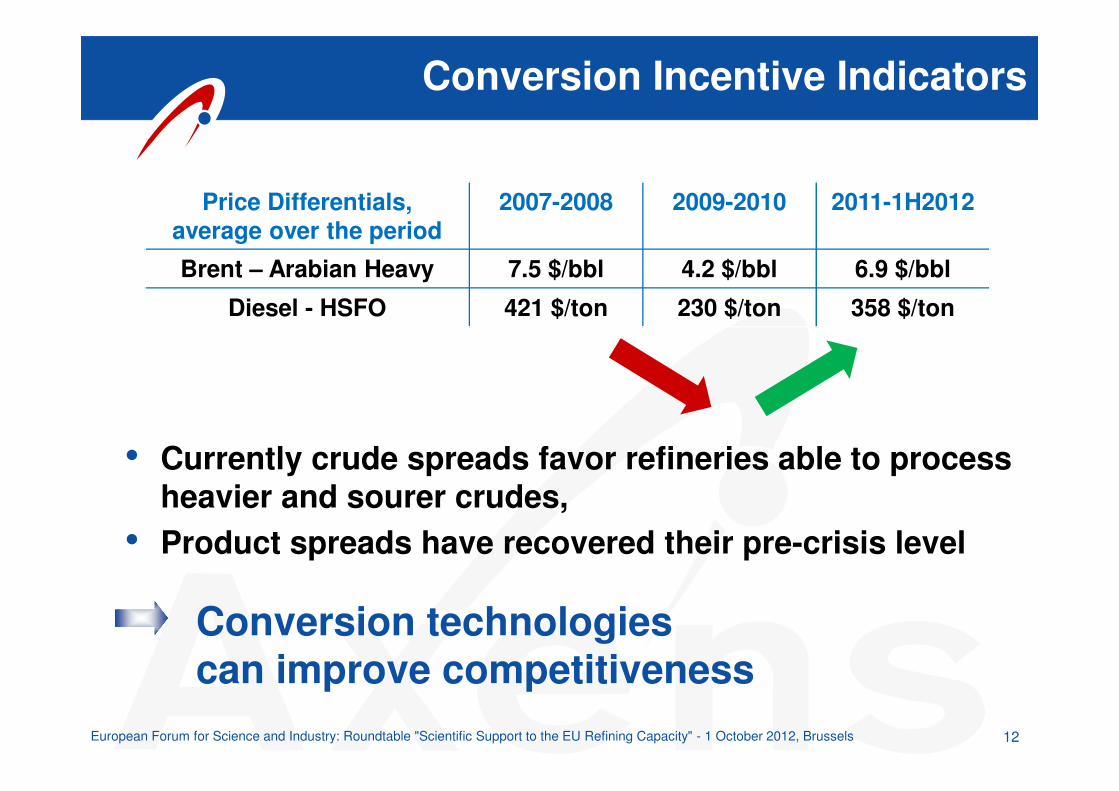

Conversion Incentive Indicators

• Currently crude spreads favor refineries able to process heavier and sourer crudes,

• Product spreads have recovered their pre-crisis level

Price Differentials,average over the period

2007-2008 2009-2010 2011-1H2012

Brent – Arabian Heavy 7.5 $/bbl 4.2 $/bbl 6.9 $/bbl

Diesel - HSFO 421 $/ton 230 $/ton 358 $/ton

Conversion technologies can improve competitiveness

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

13

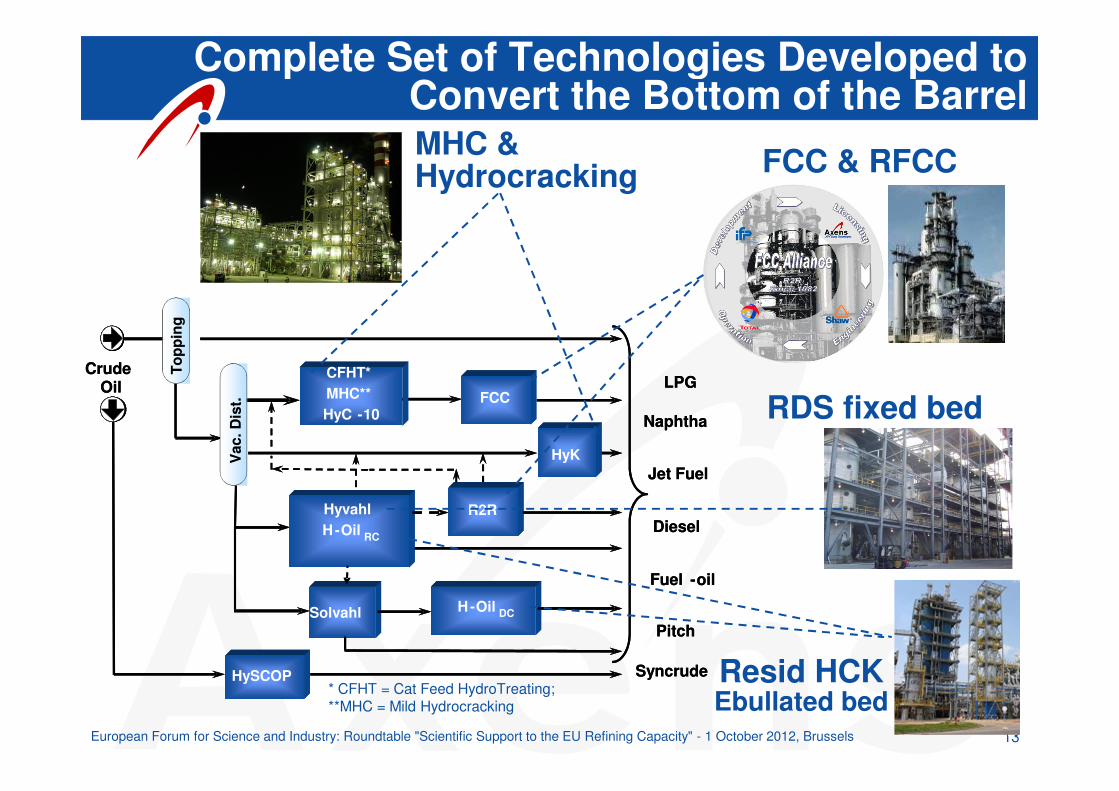

CrudeOil

Naphtha

Jet Fuel

Diesel

Fuel -oil

FCC

CFHT*MHC**HyC -10

HyK

Solvahl H-Oil DC

HyvahlH-Oil RC

HDHPLUS ®

R2R

HySCOP

LPG

Pitch

Topp

ing

Vac

. Dis

t.

Syncrude

CrudeOil

Naphtha

Jet Fuel

Diesel

Fuel -oil

FCC

CFHT*MHC**HyC -10

HyK

Solvahl H-Oil DC

HyvahlH-Oil RC

R2R

HySCOP

LPG

Pitch

Topp

ing

Vac

. Dis

t.

Syncrude

Complete Set of Technologies Developed toConvert the Bottom of the Barrel

* CFHT = Cat Feed HydroTreating;**MHC = Mild Hydrocracking

MHC & Hydrocracking FCC & RFCC

RDS fixed bed

Resid HCKEbullated bed

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

14

Agenda

Better competitiveness …• By tackling demand issue

• Gasoline/Diesel imbalances• By converting the bottom of the barrel

• Cheaper crudes processing• In the EU context

• Quality• Renewables• CO2 Emissions

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

15

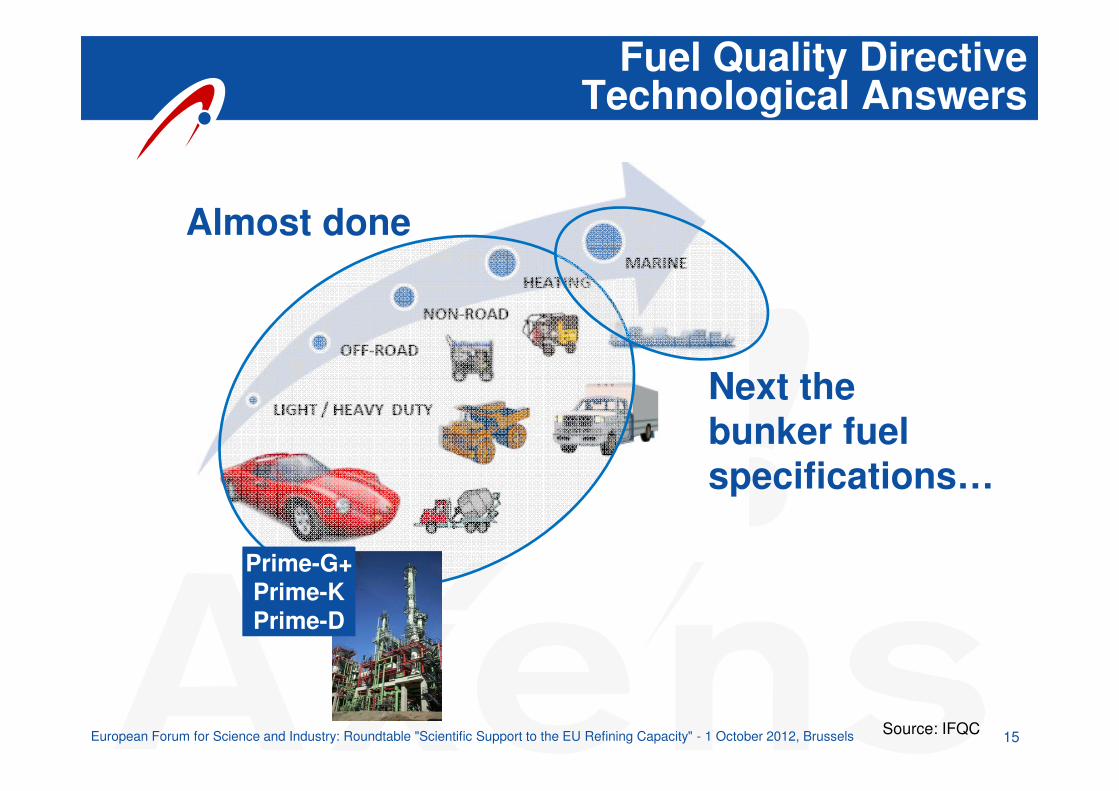

Fuel Quality DirectiveTechnological Answers

Next thebunker fuel specifications…

Almost done

Source: IFQCEuropean Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

Prime-G+Prime-KPrime-D

16

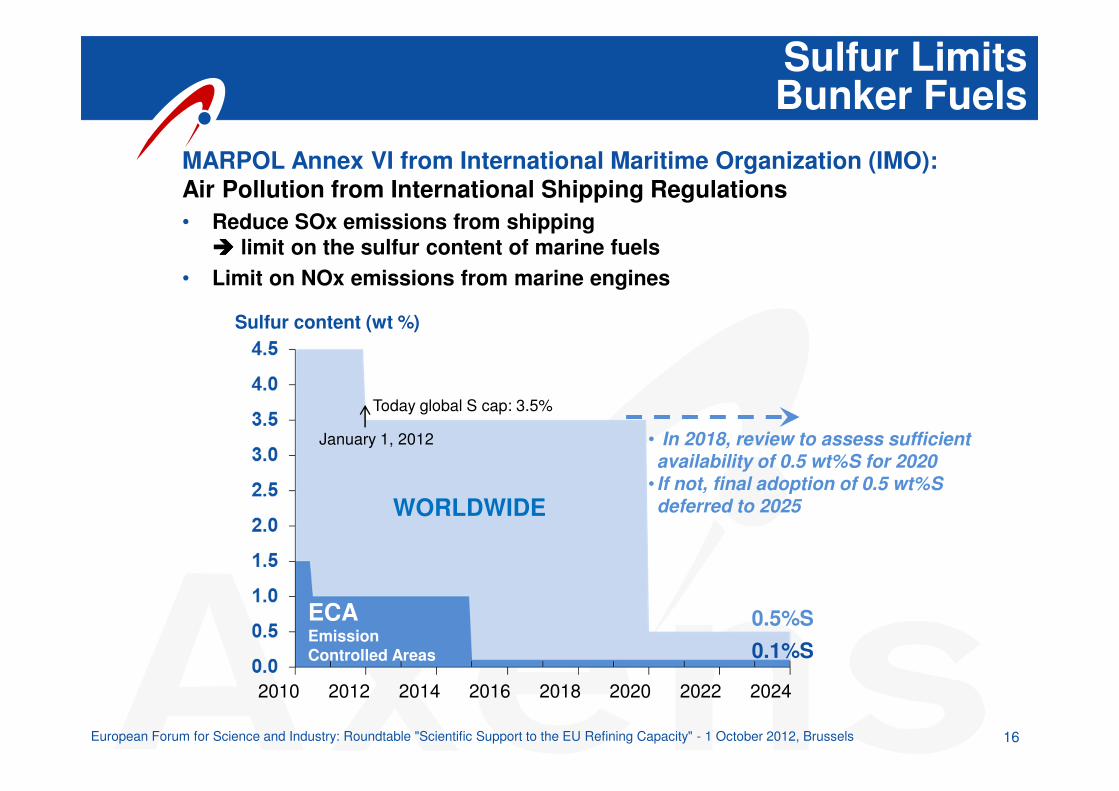

Sulfur LimitsBunker Fuels

Sulfur content (wt %)

2010 2012 2014 2016 2018 2020 2022 2024

• In 2018, review to assess sufficient availability of 0.5 wt%S for 2020

• If not, final adoption of 0.5 wt%S deferred to 2025

0.5%S0.1%S

WORLDWIDE

ECAEmission Controlled Areas

MARPOL Annex VI from International Maritime Organization (IMO):Air Pollution from International Shipping Regulations• Reduce SOx emissions from shipping

���� limit on the sulfur content of marine fuels• Limit on NOx emissions from marine engines

Today global S cap: 3.5%

January 1, 2012

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

17

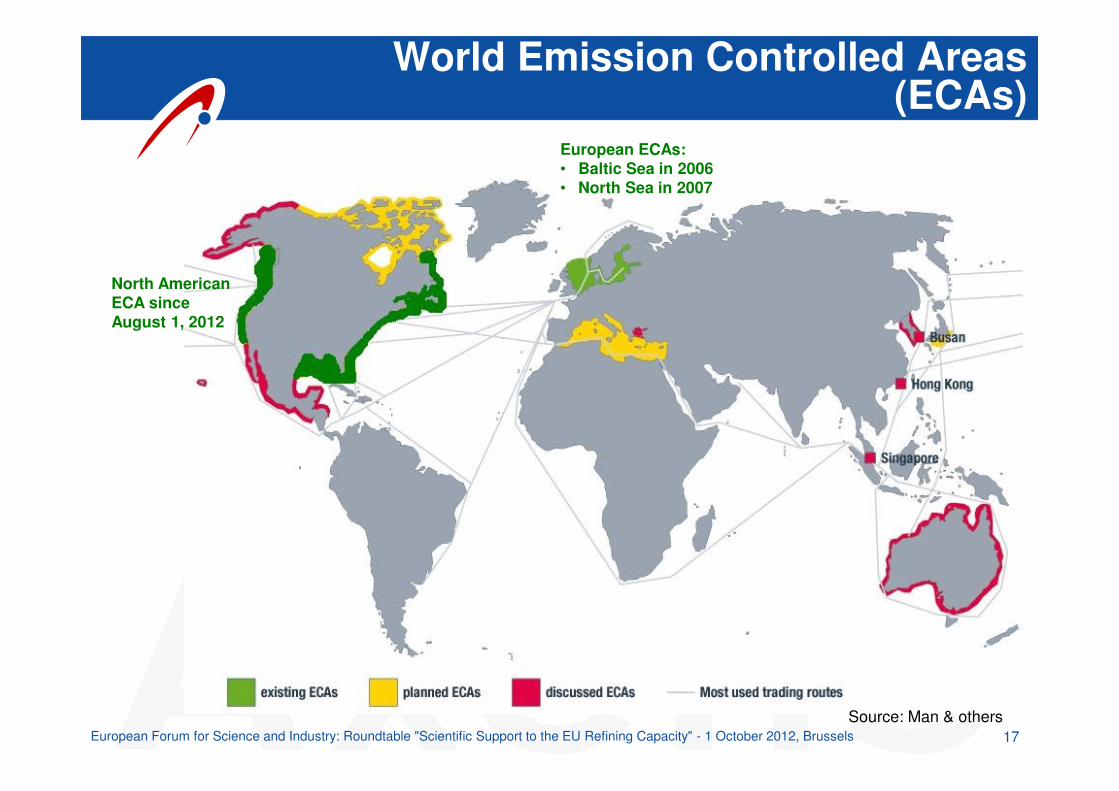

World Emission Controlled Areas(ECAs)

Source: Man & others

North AmericanECA since August 1, 2012

European ECAs:• Baltic Sea in 2006• North Sea in 2007

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

18

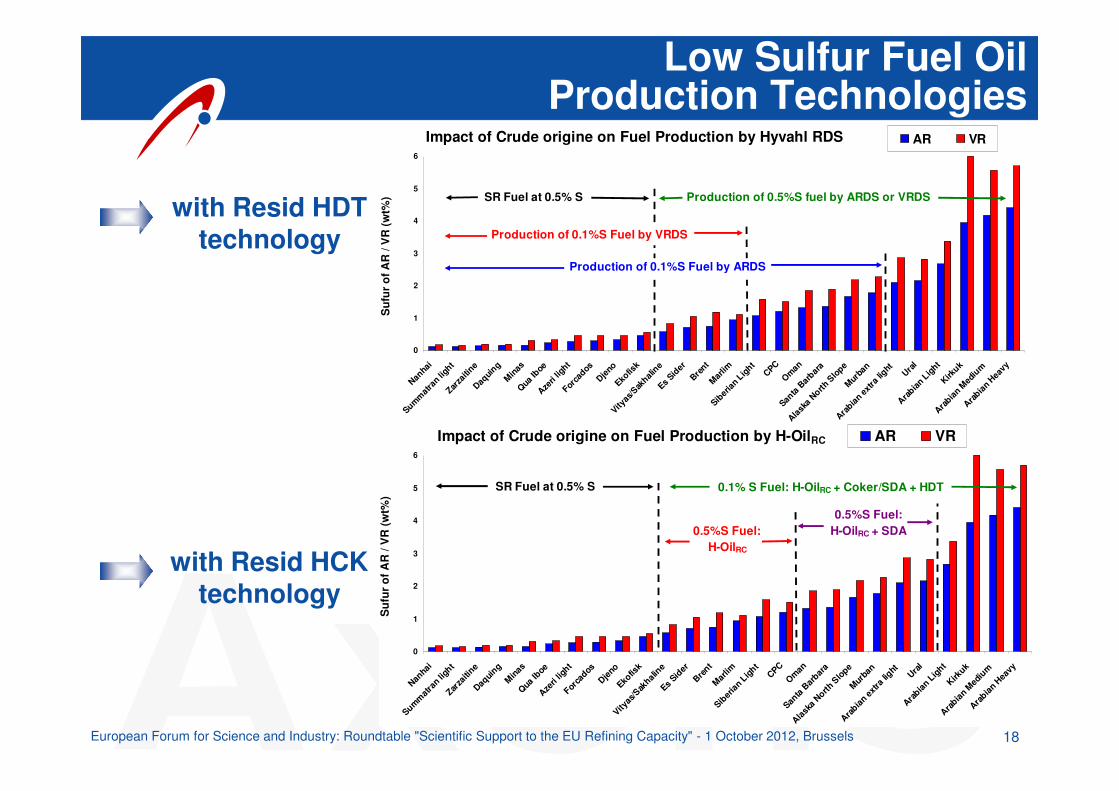

Low Sulfur Fuel Oil Production Technologies

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

with Resid HDT technology

Impact of Crude origine on Fuel Production by Hyvahl RDS

0

1

2

3

4

5

6

Nanha

i

Summatr

an lig

htZar

zaitin

eDaq

uing

Minas

Qua Ib

oeAze

ri lig

htFor

cados

Djeno

Ekofis

k

Vityas

/Sak

haline

Es Sid

erBre

ntMar

limSib

erian

Ligh

t

CPCOman

Santa

Barbar

a

Alaska

North

Slop

eMur

ban

Arabian

extra

light Ura

l

Arabian

Ligh

tKirk

uk

Arabian

Med

ium

Arabian

Hea

vy

Suf

ur o

f AR

/ V

R (w

t%)

AR VR

SR Fuel at 0.5% S Production of 0.5%S fuel by ARDS or VRDS

Production of 0.1%S Fuel by VRDS

Production of 0.1%S Fuel by ARDS

Impact of Crude origine on Fuel Production by H-OilRC

0

1

2

3

4

5

6

Nanha

i

Summatr

an lig

htZar

zaitin

eDaq

uing

Minas

Qua Ib

oeAze

ri lig

htFor

cados

Djeno

Ekofis

k

Vityas

/Sak

haline

Es Sid

erBre

ntMar

limSib

erian L

ight

CPCOman

Santa

Barbar

a

Alaska

North

Slope

Murban

Arabian

extra

light Ura

l

Arabian

Ligh

tKirk

uk

Arabian M

ediu

mAra

bian H

eavy

Suf

ur o

f AR

/ V

R (w

t%)

AR VR

SR Fuel at 0.5% S

0.5%S Fuel:H-OilRC + SDA

0.1% S Fuel: H-OilRC + Coker/SDA + HDT

0.5%S Fuel:H-OilRC

with Resid HCK technology

19

Agenda

Better competitiveness …• By tackling demand issue

• Gasoline/Diesel imbalances• By converting the bottom of the barrel

• Cheaper crudes processing• In the EU context

• Quality• Renewables• CO2 Emissions

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

20

Syngas

FTSynthesis

+ UpgradingGasification

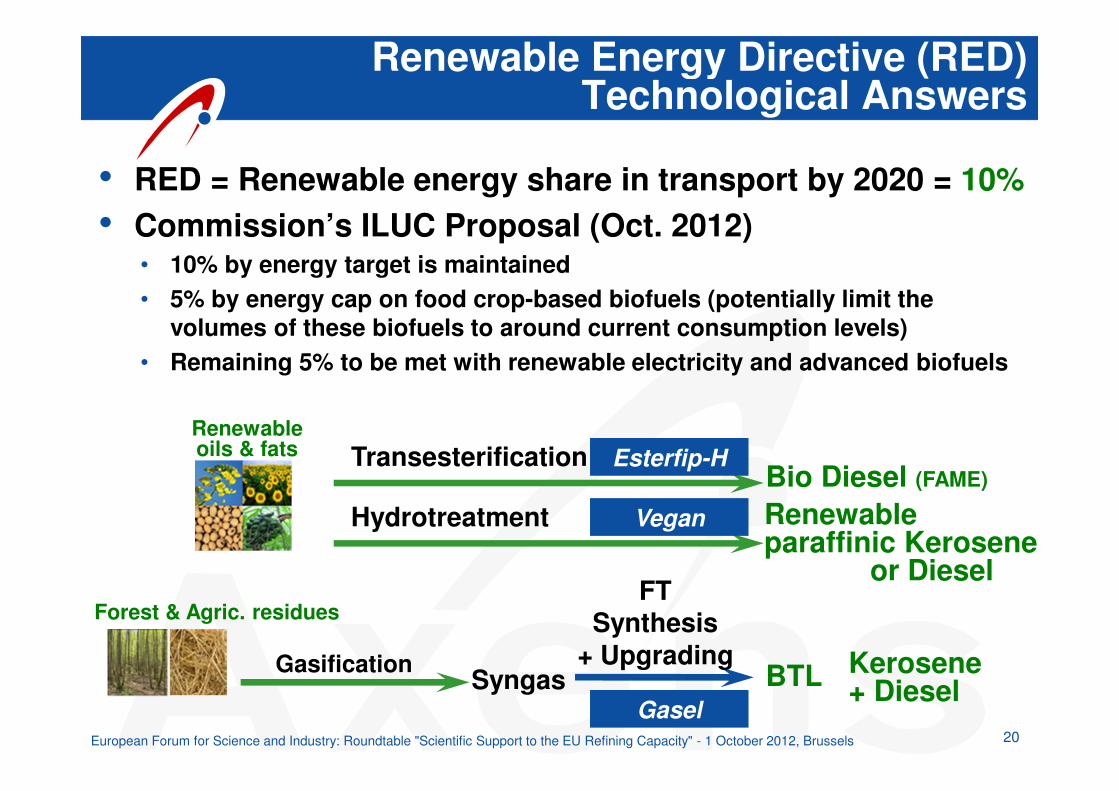

Renewable Energy Directive (RED)Technological Answers

Gasel

Renewable oils & fats

Forest & Agric. residues

Transesterification Esterfip-H

Hydrotreatment Vegan

BTL

Bio Diesel (FAME)

Renewable paraffinic Kerosene

or Diesel

Kerosene + Diesel

• RED = Renewable energy share in transport by 2020 = 10%• Commission’s ILUC Proposal (Oct. 2012)

• 10% by energy target is maintained• 5% by energy cap on food crop-based biofuels (potentially limit the

volumes of these biofuels to around current consumption levels)• Remaining 5% to be met with renewable electricity and advanced biofuels

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

21

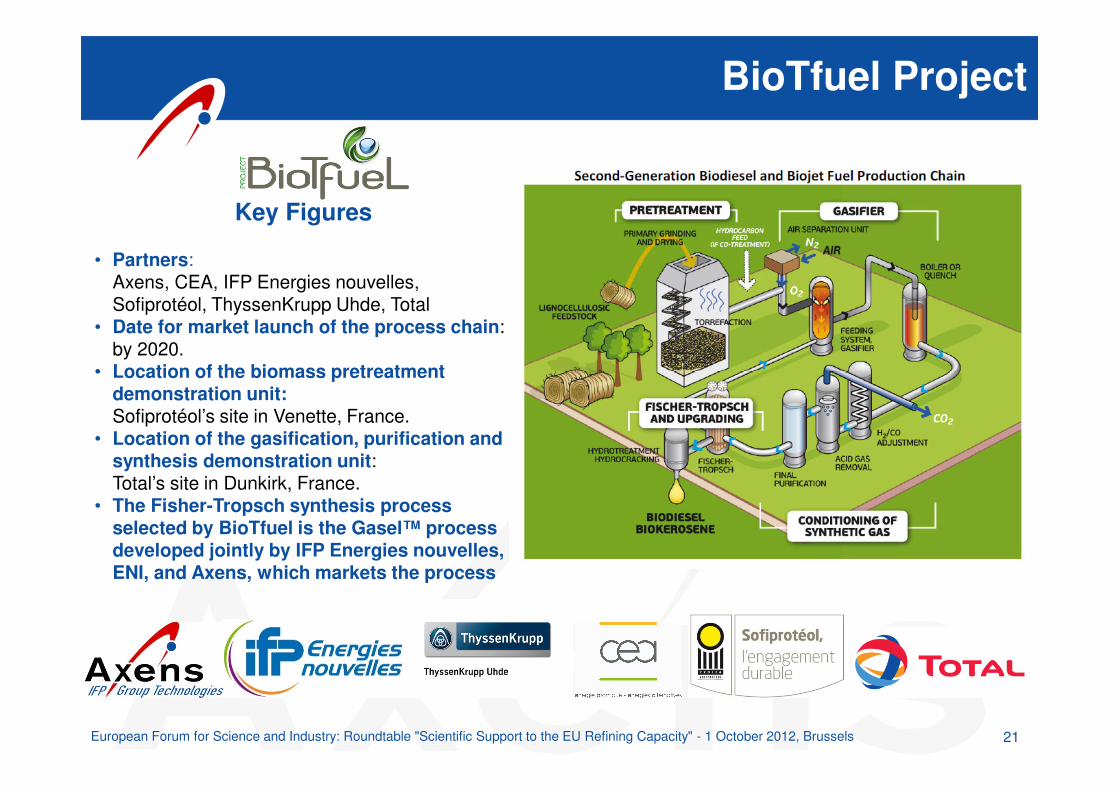

BioTfuel Project

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

Key Figures

• Partners: Axens, CEA, IFP Energies nouvelles, Sofiprotéol, ThyssenKrupp Uhde, Total

• Date for market launch of the process chain: by 2020.

• Location of the biomass pretreatment demonstration unit: Sofiprotéol’s site in Venette, France.

• Location of the gasification, purification and synthesis demonstration unit: Total’s site in Dunkirk, France.

• The Fisher-Tropsch synthesis process selected by BioTfuel is the Gasel™ process developed jointly by IFP Energies nouvelles, ENI, and Axens, which markets the process

22

Agenda

Better competitiveness …• By tackling demand issue

• Gasoline/Diesel imbalances• By converting the bottom of the barrel

• Cheaper crudes processing• In the EU context

• Quality• Renewables• CO2 Emissions

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

23

EU ETS + Action Plan Energy EfficiencyTechnological Answers

Emissions CO2 per CWT(kg/ton)

Top 10% average:29.5 kg/ton

Refinery XAllowances to be purchased

• Benchmarking analysis• Sites will have to purchase

emissions above the average level of emissions of the top 10% line

• In average, european refining industry will purchase ��������25% of its CO2 emissions

Free allowances

EU ETS Phase III (2013-2020)

Source: M. Lane, Concawe, 5th Platts Annual Refining Conference, Brussels, Sept. 2011CWT: Complexity weighted metric ton

24

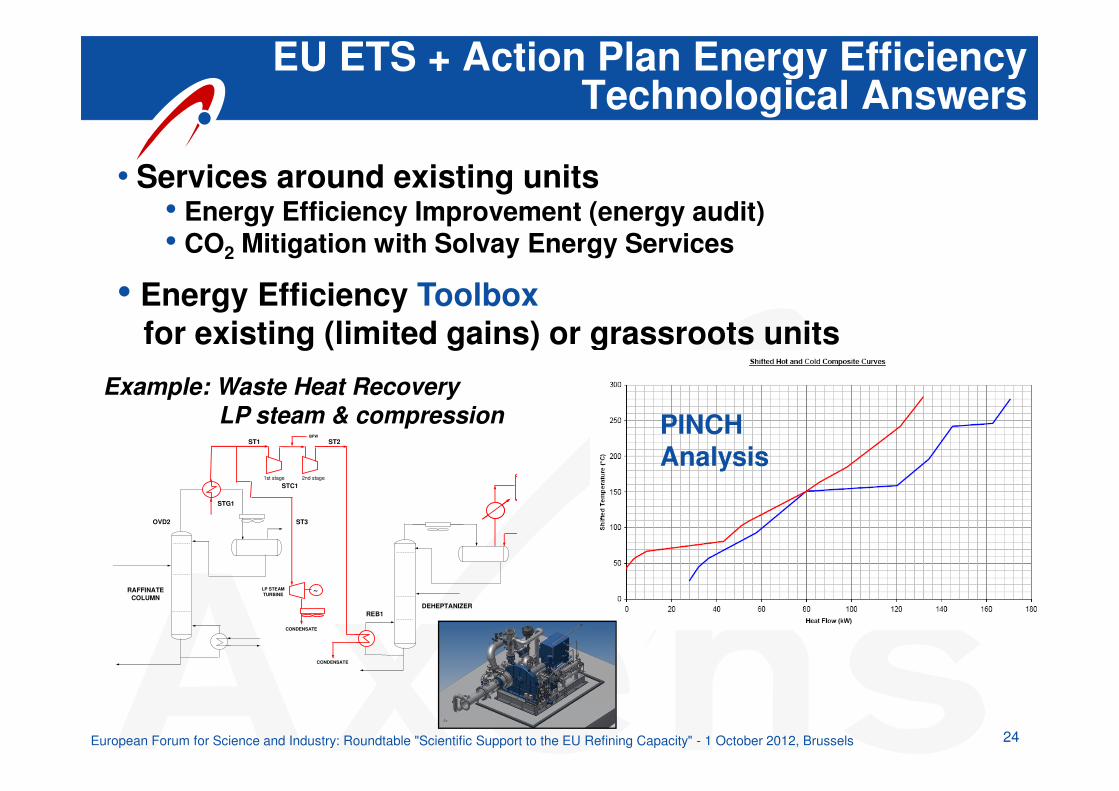

EU ETS + Action Plan Energy EfficiencyTechnological Answers

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

• Services around existing units• Energy Efficiency Improvement (energy audit)• CO2 Mitigation with Solvay Energy Services

• Energy Efficiency Toolboxfor existing (limited gains) or grassroots units

PINCH Analysis

Example: Waste Heat Recovery LP steam & compression

RAFFINATECOLUMN

REB1

OVD2

STG1

ST1 ST2

STC1

DEHEPTANIZER

1st stage 2nd stage

BFW

LP STEAMTURBINE

CONDENSATE

CONDENSATE

ST3

~

25

• To improve European refining competitiveness• some solutions already exist• some have reached

an advanced stage of development• To go further …

• Continue to invest in catalyst research• Finance demonstrators• Set up incentive mechanisms

for conversion projects

Conclusion

European Forum for Science and Industry: Roundtable "Scientific Support to the EU Refining Capacity" - 1 October 2012, Brussels

IFP Energies nouvelles R&D Center(Lyon, France)

Industrial Development (Axens Salindres Manufacturing plant)

26

Innovative Technologiesfor a Better Competitiveness