26

Wind industry today - recent growth - Global

Installed Wind Power in the World- Annual and Cumulative -

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1983 1990 1995 2000 2005 2009

Year

MW

per

year

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Cu

mu

lati

ve M

W

Source: BTM Consult ApS - March 2010

The Global Wind Power Market in US$

0

30,000

60,000

90,000

120,000

150,000

2009 2010 2011 2012 2013 2014

mill. U

S$

0

120,000

240,000

360,000

480,000

600,000

Cu

mu

lati

ve m

ill. U

S$

Forecast offshore Offshore 2009 Onshore 2009

Forecast onshore Cumulative marketSource: BTM Consult ApS - March 2010

Expected development 2010-2014

Expectation is for more growth

Wind industry today - recent growth in US installations

AWEA US Wind Industry Annual Market Report - Year ending 2009

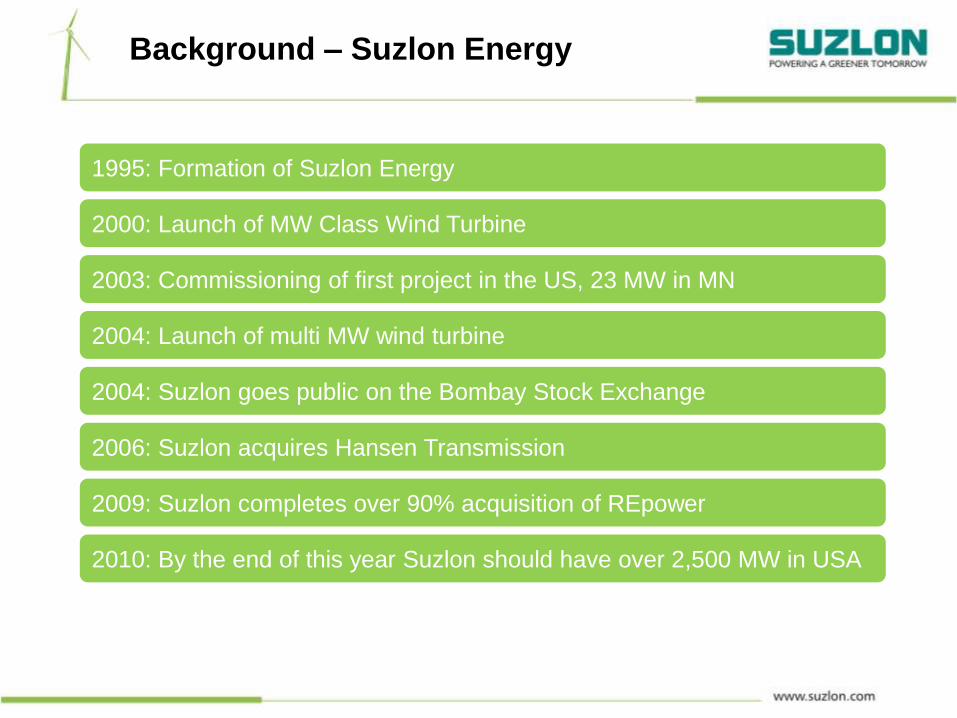

Background – Suzlon Energy

1995: Formation of Suzlon Energy

2000: Launch of MW Class Wind Turbine

2003: Commissioning of first project in the US, 23 MW in MN

2004: Launch of multi MW wind turbine

2004: Suzlon goes public on the Bombay Stock Exchange

2006: Suzlon acquires Hansen Transmission

2009: Suzlon completes over 90% acquisition of REpower

2010: By the end of this year Suzlon should have over 2,500 MW in USA

Vision & Mission

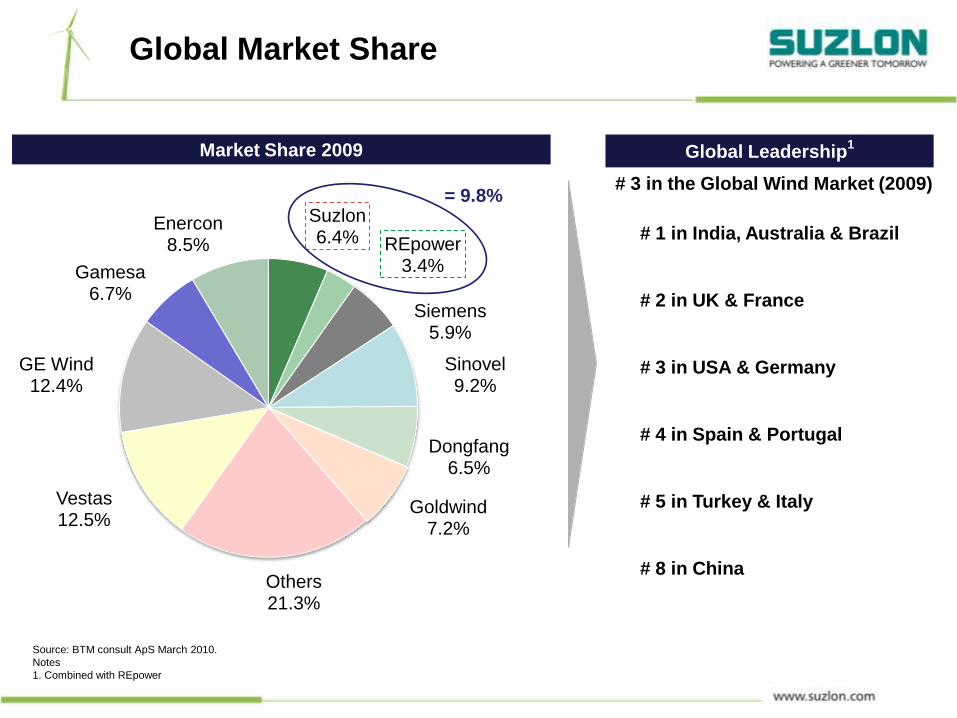

Global Market Share

Source: BTM consult ApS March 2010.

Notes

1. Combined with REpower

# 3 in the Global Wind Market (2009)

# 1 in India, Australia & Brazil

# 2 in UK & France

# 3 in USA & Germany

# 4 in Spain & Portugal

# 5 in Turkey & Italy

# 8 in China

Market Share 2009 Global Leadership1

Suzlon6.4% REpower

3.4%

Siemens5.9%

Sinovel9.2%

Dongfang6.5%

Goldwind7.2%

Others21.3%

Vestas12.5%

GE Wind12.4%

Gamesa6.7%

Enercon8.5%

= 9.8%

Total installations of 11,889 MW including REpower, accounting for ~9% of global installations

Germany

Italy

France

UK

Belgium

Canada

China (installed fleet:

375 MW)

• Shandong Luneng

• Guohua

• Datang

• Honiton

• Jingneng

Australia (installed fleet: 384 MW)

• AGL Energy

• TrustPower

• Renewable Power Ventures Pty

Ltd.

• Pacific Hydro

• Infigen Energy

Turkey (installed fleet: 32

MW)

• Ayen Enerji

India (installed fleet: 4,833 MW)

• Tata Power

• Bajaj Auto

• ONGC

• British Petroleum

Portugal (installed fleet: 103 MW)

• Techneira S.A

• Energi Kontoret

• Martifer Energy Systems

Spain (installed fleet: 233 MW)

• Iniciativas Energetitas

• Eólia Renovables group

• Spanish Savings Bank Unicaja

USA (installed fleet: 1,752 MW)

• John Deere

• Edison Mission Group

• Iberdrola Renewables

• Horizon Wind/ EDP

• Duke Energy

Brazil (installed fleet: 242 MW)

• SIIF Energies do Brasil Ltda

(SIIF)

• Servtec Instalacoses

Nicaragua (installed fleet: 40 MW)

• Amayo

Japan

SuzlonREpowerBoth

Suzlon Group - extensive global footprint

1 As on December 2009; Includes all SCADA connected systems

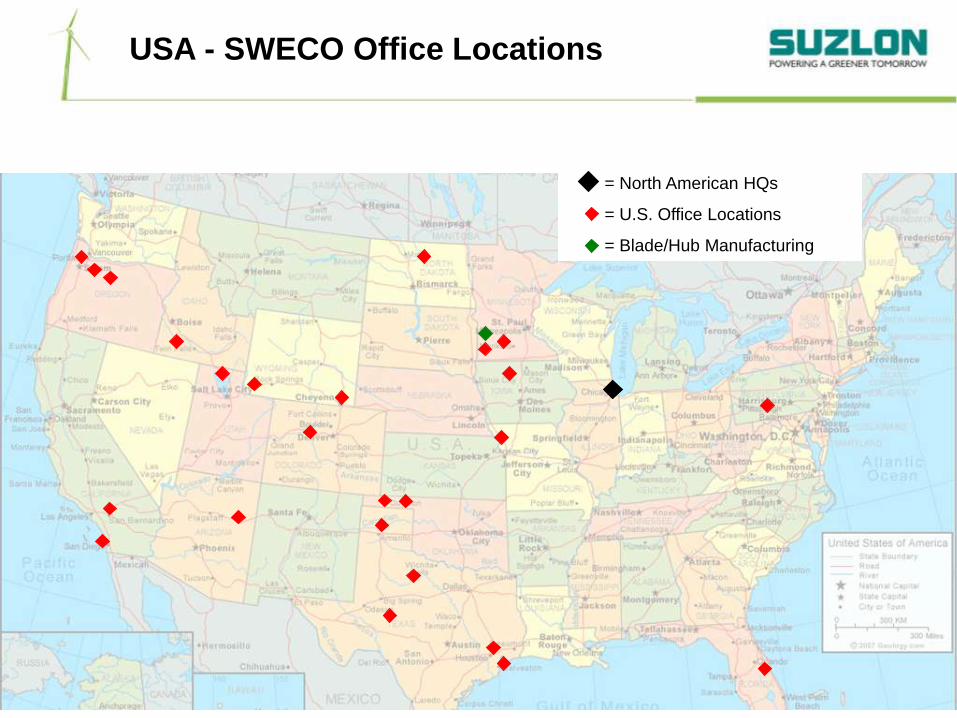

USA - SWECO Office Locations

= North American HQs

= U.S. Office Locations

= Blade/Hub Manufacturing

161 S64 WTG’s

813 S88 WTG’s

2255 Total MW

114 @ 2.1 MW = 240 MW

Under construction

Washington:

Kittitas Valley 48 S88

Oregon:

Hay Canyon 48 S88

Pebble Springs 47 S88

Rattlesnake 49 S88

Wheatfield 46 S88

Star Point 47 S88

Leaning Juniper 43 S88

Arizona:

Dry Lake 30 S88

Dry Lake II 31 S88

Idaho:

Cassia 14 S88

Mtn Home 20 S88

Tuana Springs 8 S88

Wyoming:

Mtn Wind 1 29 S88

Mtn Wind II 38 S88

Happy Jack 14 S88

Silver Sage 20 S88

Texas:

JD1, 2, 3, 5 & 6 40 S64

JD4 38 S88

JD7-11 40 S64

Ocotillo 28 S88

High Plains 8 S64

North Dakota:

Rugby 71 S88

Iowa:

Hardin 7 S88

Crosswinds 10 S88

Oklahoma:

Sleeping Bear 45 S88

Buffalo Bear 9 S88

Minnesota:

Buffalo Ridge 24 S88

Cisco 4 S88

Corn Plus 2 S88

Ewington 10 S88

Federated/Nobles 2 S88

Marshall 9 S88

Odin 10 S88

Shane Cowell 1 S88

Wind Share 3 S88

Grant County 10 S88

S64 Turbines 58 S64

Illinois:

Agriwind 4 S88

Big Sky 114 S88

Indiana:

Meadow Lake 47 S88

Pennsylvania:

Forward 14 S88

Lookout 18 S88

Missouri:

Bluegrass 27 S88

Conception 24 S88

Cow Branch 24 S88

Loess Hills 4 S64

Kansas:

Greensburg 10 S64

Utah:

Spanish Fork 9 S88

South Dakota:

Buffalo Ridge 24 S88

Site Summary

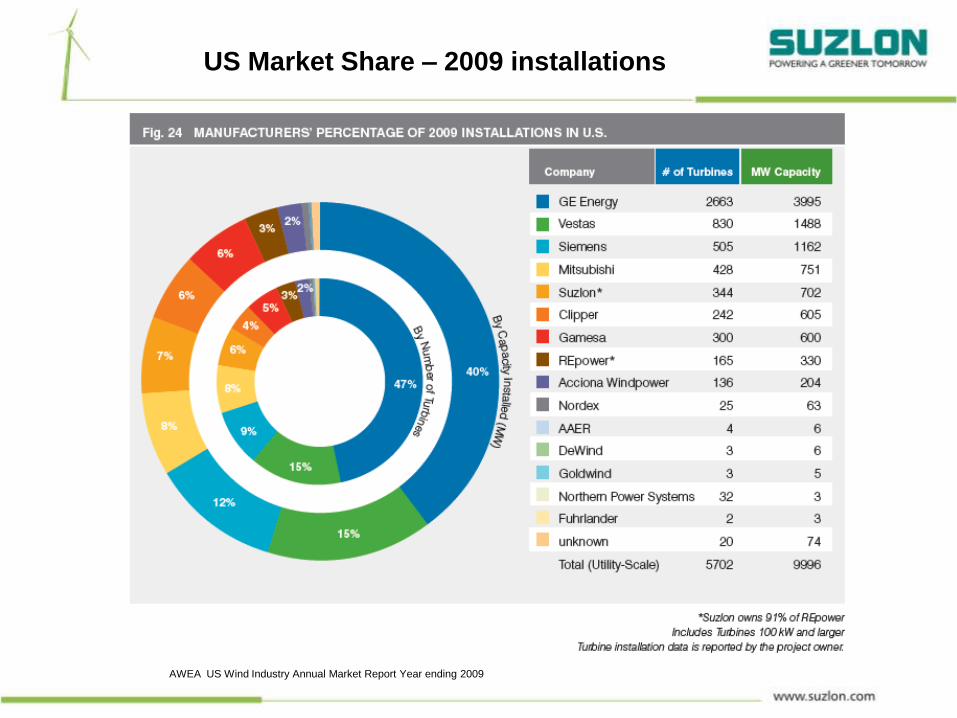

US Market Share – 2009 installations

AWEA US Wind Industry Annual Market Report Year ending 2009

USA - What’s needed for more growth

• A national RES, Energy Bill, or Climate Bill with teeth will provide long term consistent growth.

• Policy makers must realize the implications of their legislation.

Policy

• Improved technology and industry advancements will drive costs down and production up making wind more competitive

Technology and Advancements

• Financial markets must open up and remain available to wind so that projects can be financed.

• Natural gas prices need to steady (or increase) so wind energy will be more competitive.

Macroeconomic Cooperation

Considering the CUSTOMER

Wind industry today – how the Customers stack up

AWEA US Wind Industry Annual Market Report Year ending 2009

Customer needs – new turbines

• Wind class - IEC IIA

• Nominal Power – 2100 kW, 60 hertz

• Temperature Ranges

– Low Temperature Version:

• operation range -30ºC to

+40ºC

• structural range -40ºC to

+50ºC

• Operational Parameters

– Cut-in Wind Speed: 3 m/s

– Rated Wind Speed: 14 m/s

– Cut-out Wind Speed: 25 m/s

– Survival Wind Speed: 59.5 m/s

• Certifications

– Germanischer Lloyd, Germany

– ISO 9001

Customer needs – logistics support

Customer needs – construction support

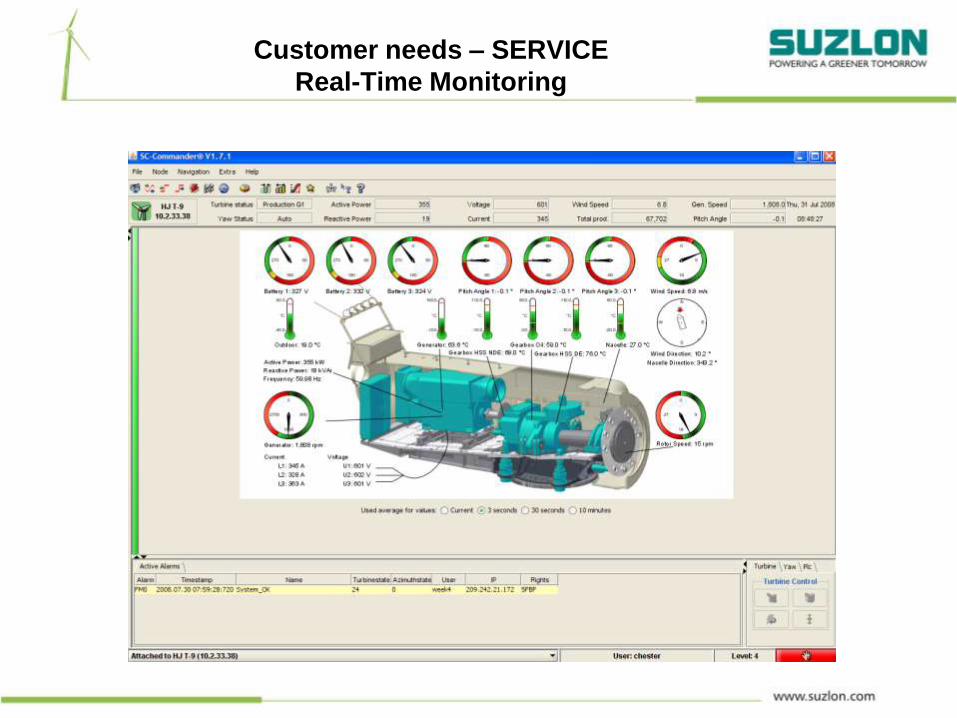

Customer needs – SERVICE

Real-Time Monitoring

Customer needs – SERVICE

technical support

• Main Frame – Girder– Cast box frame with

corrosion proof paint

• Yaw System– Slide bearing with gear ring– Automatic greasing system– 3 – 600 volt electric motors

with brake, gearbox, and pinion

• Vibration Sensing– Vibration switch on main

frame from emergency stop– Analyzer with x/y axis

accelerometer on main frame, z axis accelerometer on gear box mounting

• On-board Hoist– Electrical chain hoist

mounted on side rail in back of nacelle

Generator

Cooler

CouplingElectrical

CabinetRotor

Brake

Gearbox

Oil Cooler

Rotor Bearing

Rotor LockYaw drive

Main frame

Girder BeamsGenerator

Rotor Shaft

Customer needs – SERVICE

replacement parts

Customer service objective

•Provide high quality parts and service at fair price, minimal lead

time + best delivery scenario

•Innovation – we’ll provide maximum equipment availability and

work with client to achieve high production and profitability

•Trust and open exchange – work to benefit of all parties

•Localization – provide product and support when & where

needed

•Provide Customer Service at such a high level during warranty

period that extension of that service is the best value proposal

for the customer

Expectation of Suppliers

•High quality, fair cost, minimal lead time + best delivery scenario

•Innovation – work with us maintain a game changing product portfolio

•Trust and open exchange – work to benefit of all parties

•Localization – provide product and support when & where needed

•Work with us to meet our Customer Service Objectives (end to end)

Professional Connections

Supply Chain Networking

Stay on top of legislation that affects US