21

INSTITUTE OF COMPANIES SECRETARIES OF INDIA TAXATION ASPECTS OF DIRECT TAX DUE DILIGENCE September 26, 2009 Rajiv Anand Executive Director PricewaterhouseCoopers

| Date post: | 02-Jan-2016 |

| Category: |

Documents |

| Upload: | cornelius-gregory |

| View: | 213 times |

| Download: | 0 times |

INSTITUTE OF COMPANIES SECRETARIES OF INDIA

TAXATION ASPECTS OF DIRECT TAX DUE DILIGENCE

September 26, 2009

Rajiv AnandExecutive Director PricewaterhouseCoopers

Slide 2 PricewaterhouseCoopers

September 26, 2009

Why Tax Due Diligence

Methodology of Doing a Tax Due Diligence

Impact of Tax Due Diligence on Deal

CONTENTS

Slide 3 PricewaterhouseCoopers

September 26, 2009

To avoid any uncertain tax claims from the tax authorities in future

Review whether enterprise value needs adjustment from tax perspective

Review whether there is any un-provided tax liability in the financials

Review of brought forward losses / unabsorbed allowances

Review of tax holiday claims

WHY TAX DUE DILIGENCE ?

Slide 4 PricewaterhouseCoopers

September 26, 2009

Corporate Income Tax review

Withholding Tax review (TDS)

METHODOLOGY OF TAX DUE DILIGENCE

Slide 5 PricewaterhouseCoopers

September 26, 2009

Understanding the nature of business

Conduct detailed review of financials for the review period

Conduct detailed review of tax documents like the income tax returns, assessment / appeal orders, pending litigations / appeals, demands, etc.

CORPORATE INCOME TAX REVIEW – HOW UNDERTAKEN

Slide 6 PricewaterhouseCoopers

September 26, 2009

CORPORATE TAX REVIEW INTER-ALIA FOCUSES ON….

ISSUES REMARKS

Carry forward of losses

Analyze continuity of brought forward losses –

- To analyze implications under Section 79 of the Act

- To analyze the conditions pertaining to transfer of Unit if the Unit is enjoying tax holiday

Transaction between Group Companies

Deemed Dividend Implications

– Inter group-company transactions need to be reviewed

– Loans / advances given to group companies could qualify as deemed dividend under certain circumstances

Benefit Test

– To analyze whether or not the Target obtained any benefit in respect of payments made to group companies

Slide 7 PricewaterhouseCoopers

September 26, 2009

ISSUES REMARKS

Tax Holiday Claims If a new unit has commenced manufacturing during the due diligence review period and which is otherwise eligible for tax holiday, the following to be analyzed –

– Whether the unit has been formed as a result of splitting up / reconstruction of an already existing business

– Other conditions are fulfilled

Capital / Revenue expenditure

– To analyze whether any item of capital nature has been claimed as revenue

CORPORATE TAX REVIEW INTER-ALIA FOCUSES ON…. ..Contd.

Slide 8 PricewaterhouseCoopers

September 26, 2009

ISSUES REMARKS

Deductions / Exemptions

– Analyze the conditions required for claiming deductions and exemptions

– Applicability of Section 14A of the Income-tax Act

– Inter-se setting off of profits and losses between eligible and non-eligible units

Provisions – To review the movement of various provisions in the books of account to examine whether they are contingent in nature

Litigations – To review the stand taken by the company in ongoing litigations

CORPORATE TAX REVIEW INTER-ALIA FOCUSES ON…. ..Contd.

Slide 9 PricewaterhouseCoopers

September 26, 2009

Understanding nature of expenses / payments

Review of standard agreements pertaining to expenditures which get covered under various tax withholding provisions like sections 195, 192, 194H, 194I, 194J

Reconciliation of taxes withheld as per Profit & Loss Account and as per TDS returns

WITHHOLDING TAX (TDS) – HOW UNDERTAKEN

Slide 10 PricewaterhouseCoopers

September 26, 2009

Applies when following conditions are fulfilled:

• Payment is in nature of income in the hands of non-resident;

• Such income is taxable in India; and

• At the time of credit or payment

Payment must be in the nature of “Income”

• Ericsson Communications Ltd. (Delhi ITAT)

Payment must be “Taxable in India”

• Option to choose between DTA and ITA, 1961

• Case Study

WITHHOLDING TAX (TDS) – SECTION 195

Slide 11 PricewaterhouseCoopers

September 26, 2009

Assessee deemed to be in default - Penal Provisions:

- 201(1) – Recovery of tax from defaulting payer

- 201(1A) – Interest levy is mandatory

– Reasonable cause not relevant

- 271C – Penalty for failure to deduct, unless reasonable cause proved

WITHHOLDING TAX (TDS) – SECTION 195 …Contd.

Slide 12 PricewaterhouseCoopers

September 26, 2009

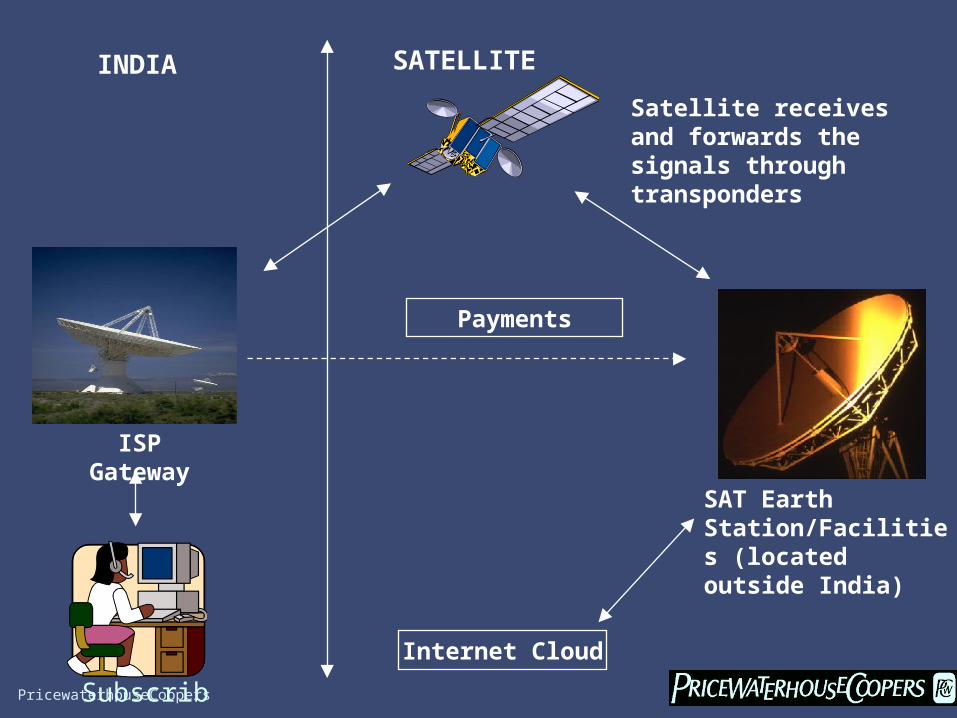

• ISP contracts with SAT for availing connectivity/ access to the Internet cloud

• ISP has its own gateway in India for availing connectivity/access

• Satellite/ other network facilities of SAT operated by SAT

• ISP has no possession/ control over the satellite/ other SAT facilities

• Transaction merely affords connectivity

ISP in India SAT Overseas

Satellite Connectivity Payments

CASE STUDY – TDS UNDER SECTION 195

Slide 13 PricewaterhouseCoopers

September 26, 2009

Internet Cloud

Satellite receives and forwards the signals through transponders

SATELLITE

SAT Earth Station/Facilities (located outside India)

ISP Gateway

Subscriber

Payments

INDIA

Slide 14 PricewaterhouseCoopers

September 26, 2009

Connectivity Payments

WHETHERROYALTY?

WHETHER TECHNICAL SERVICE FEE?

Issue CASE STUDY – TDS UNDER SECTION 195

Slide 15 PricewaterhouseCoopers

September 26, 2009

Definition of Royalty

• Payments for ‘Right to use’

- equipment

- secret formula or process

What is ‘Right to use’

• Royalty in respect of licenses ‘to use’ ….are income to the recipient from letting [OECD Commentary]

• Phrase interpreted to mean a “leasing transaction” [Memorandum explaining Finance Act 2001]

• Letting/leasing would envisage separation of ownership of an asset and its possession

CASE STUDY – TDS UNDER SECTION 195

Slide 16 PricewaterhouseCoopers

September 26, 2009

…..what is ‘Right to use’

• Klaus Vogel:

- Clean distinction between letting the asset to the payer and the use of it by the payee himself

- Payee using the asset himself to provide services to payer while not letting the same to him does not qualify as ‘right to use’

Right to use Equipment - Criteria for determination

• Customer has physical possession/ control over the equipment

• Has significant economic or possessory interest in the equipment

• Provider does not bear any risk of substantially diminished receipts or substantially increased expenditures

• Provider does not use the property concurrently to provide services to others [OECD Report]

CASE STUDY – TDS UNDER SECTION 195

Slide 17 PricewaterhouseCoopers

September 26, 2009

Whether Right to use secret formula/process – Criteria

• Imparting information about ideas and principles underlying the program viz. logic, algorithms or programming language or techniques may be characterized as right to ‘use secret formula’ [OECD Commentary]

None of the conditions fulfilled in present case – No leasing of any

asset whether tangible or otherwise

CASE STUDY – TDS UNDER SECTION 195

Slide 18 PricewaterhouseCoopers

September 26, 2009

What is a “technical service”

• One party undertakes to use customary skills of his calling to execute work himself for another person

• When special skills or knowledge related to a technical field are required for provision of a service

• Point of time when the special skill or knowledge is used – a relevant criteria

• Technology/medium used in providing a service - not a relevant criteria

• Provision of online advice through communication with technicians – a technical service

• Mere provision of access to a trouble-shooting database - not a technical service

SAT not providing any technical service to ISP

CASE STUDY – TDS UNDER SECTION 195

Slide 19 PricewaterhouseCoopers

September 26, 2009

• Since SAT not having taxable presence in India, no TDS required under law

• Issues to be managed

- Many judgments take contrary view

- Recent Karnataka High Court decision

CASE STUDY – TDS UNDER SECTION 195

Slide 20 PricewaterhouseCoopers

September 26, 2009

Estimating the tax, interest and penalty exposure that the Target may have on account of defaults and/or aggressive and/or unacceptable stands taken by it

Depending on the risk profile of the issues unearthed in the review exercise, appropriate representations and warranties to be secured from Vendor. In cases where high risk exposure is involved, appropriate adjustments in enterprise valuation to be considered

IMPACT OF DUE DILIGENCE ON THE DEAL

© 2009 PricewaterhouseCoopers. All rights reserved. “PricewaterhouseCoopers” refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity. *connectedthinking is a trademark of PricewaterhouseCoopers LLP (US).

Thank You

Rajiv Anand Executive Director / Partner Tel : +91 11 4115 0201

Mobile : +91-9810223812

Email : [email protected]