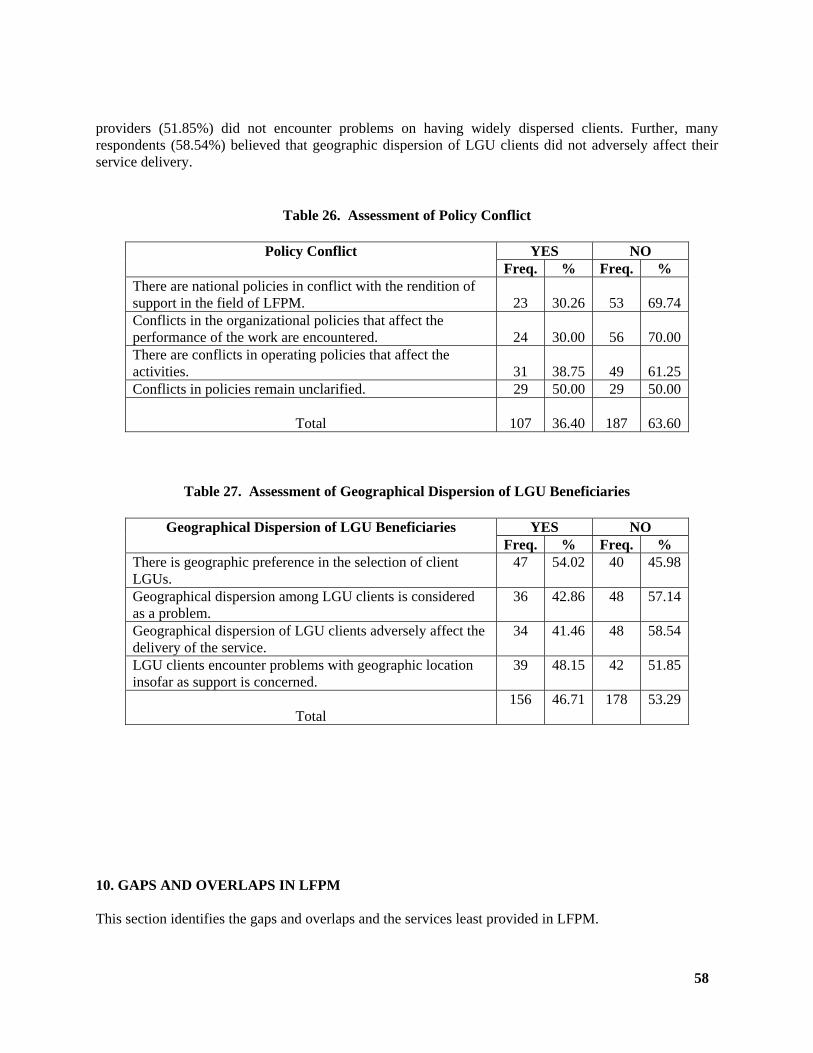

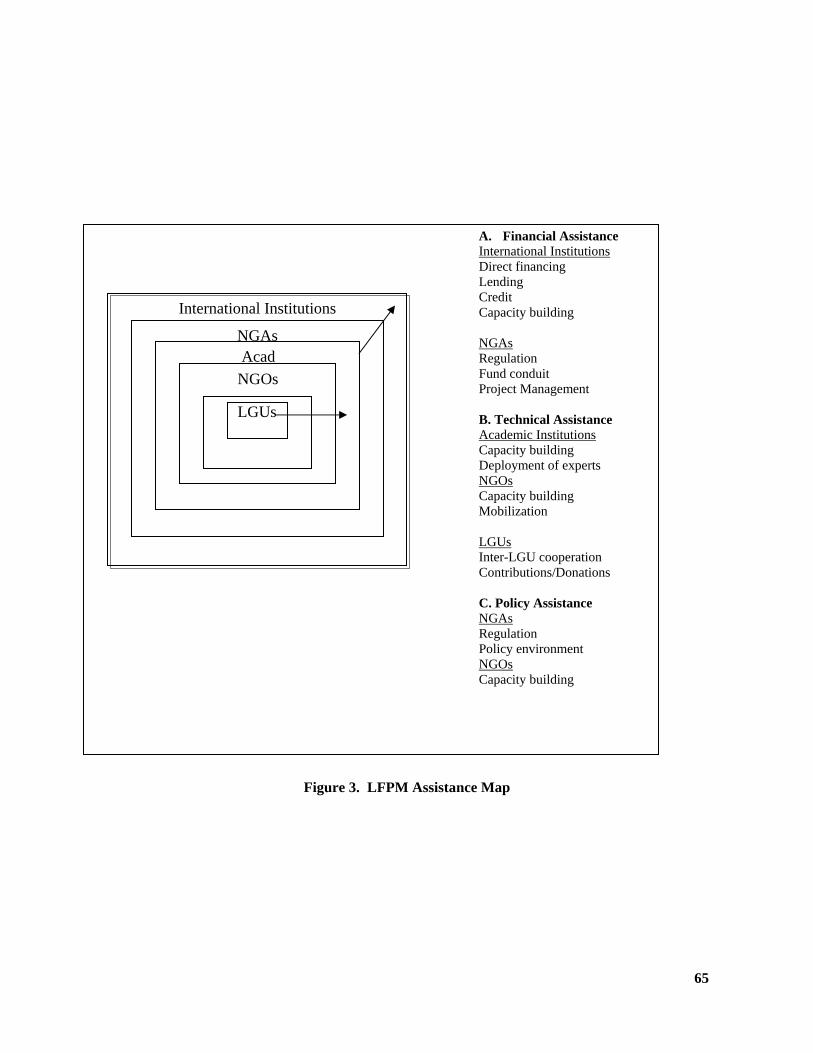

104

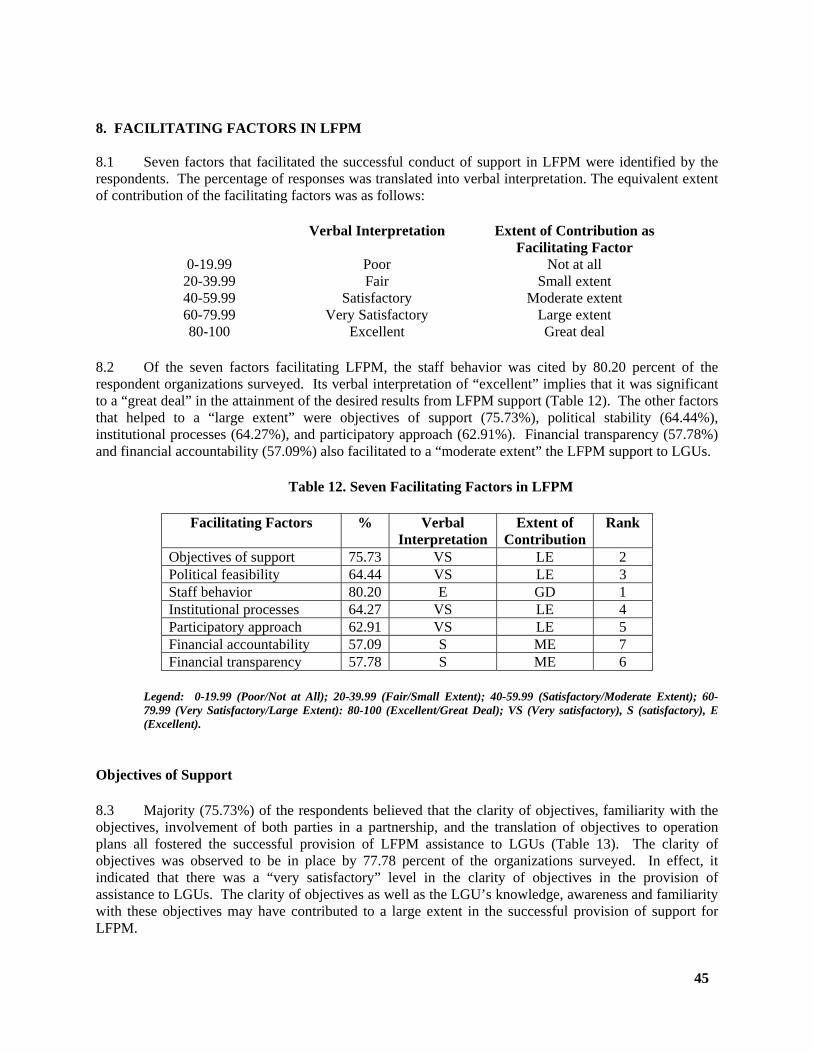

Rufo Mendoza, Ph.D. June 2007 INSTITUTIONAL MAPPING AND ANALYSIS OF ORGANIZATIONS EFFORTS, INITIATIVES AND ASSISTANCE TO LOCAL FINANCIAL PLANNING AND MANAGEMENT

Rufo Mendoza, Ph.D.

June 2007

INSTITUTIONAL MAPPING AND ANALYSIS OF ORGANIZATIONS

EFFORTS, INITIATIVES AND ASSISTANCE TO LOCAL FINANCIAL

PLANNING AND MANAGEMENT

DISCLAIMER

“The views expressed in this report are strictly those of the authors and do not necessarily reflect those of the United States Agency for International Development (USAID) and the Ateneo de Manila University”.

Abstract This project report discusses various forms of support provided to local government units (LGUs) in local financial planning and management (LFPM). It aims to provide an inventory and a consolidated report of organizations or institutions that support the progress of financial planning and management in LGUs. The principal findings of this study are firstly, LFPM institutional assistance at the local level is limited. Secondly, national government agencies and international finance institutions provide financial, technical and policy assistance while academic institutions, nongovernment organizations and to a certain extent the LGUs themselves focused on technical assistance. Finally, LFPM assistance impresses upon local chief executives the relationship between local government fiscal performance and managerial enhancement.

TABLE OF CONTENTS

Page List of Tables

iv

List of Figures v List of Appendix Tables v List of Appendices v Acronyms and Abbreviations vi Preface and Acknowledgments ix 1. Introduction

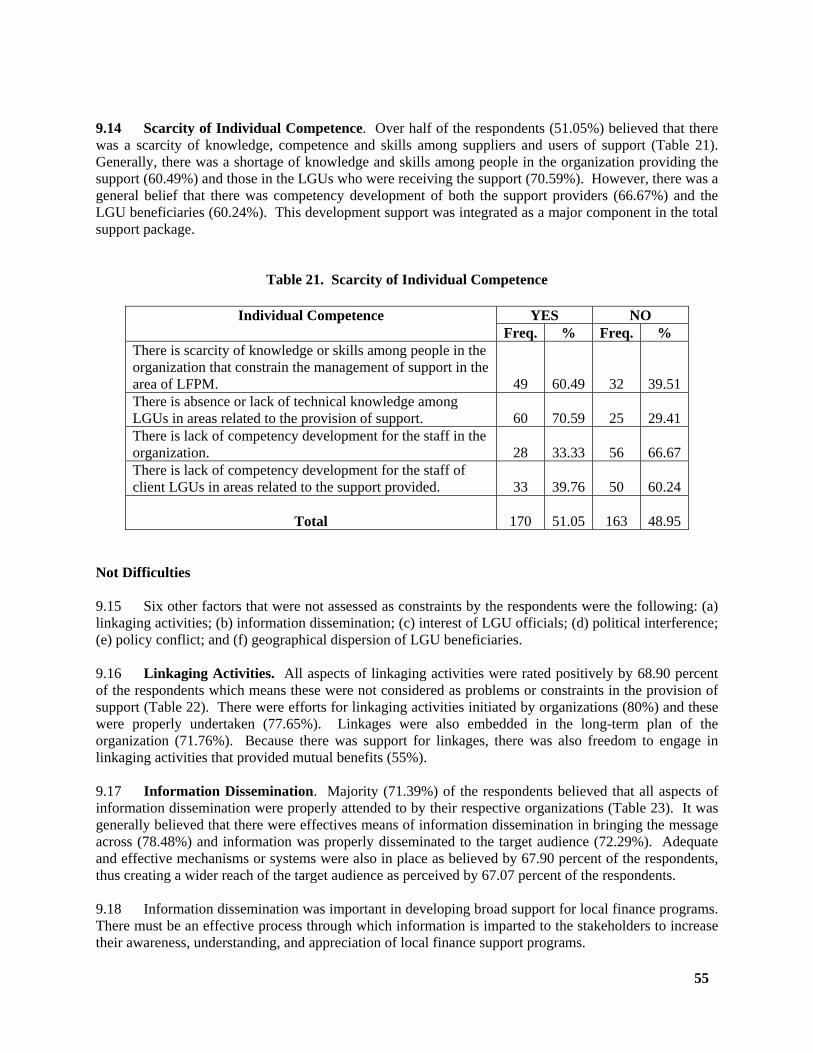

1

2. Rationale for The Study

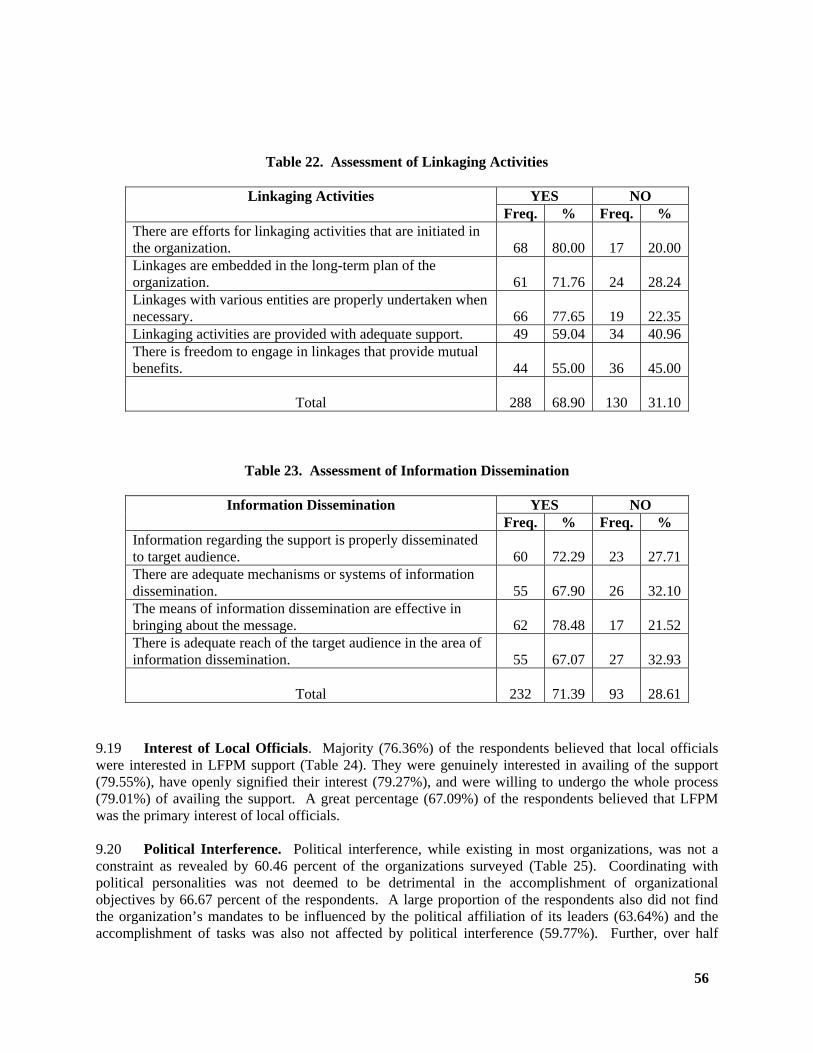

1

3. Research Framework and Methodology

3

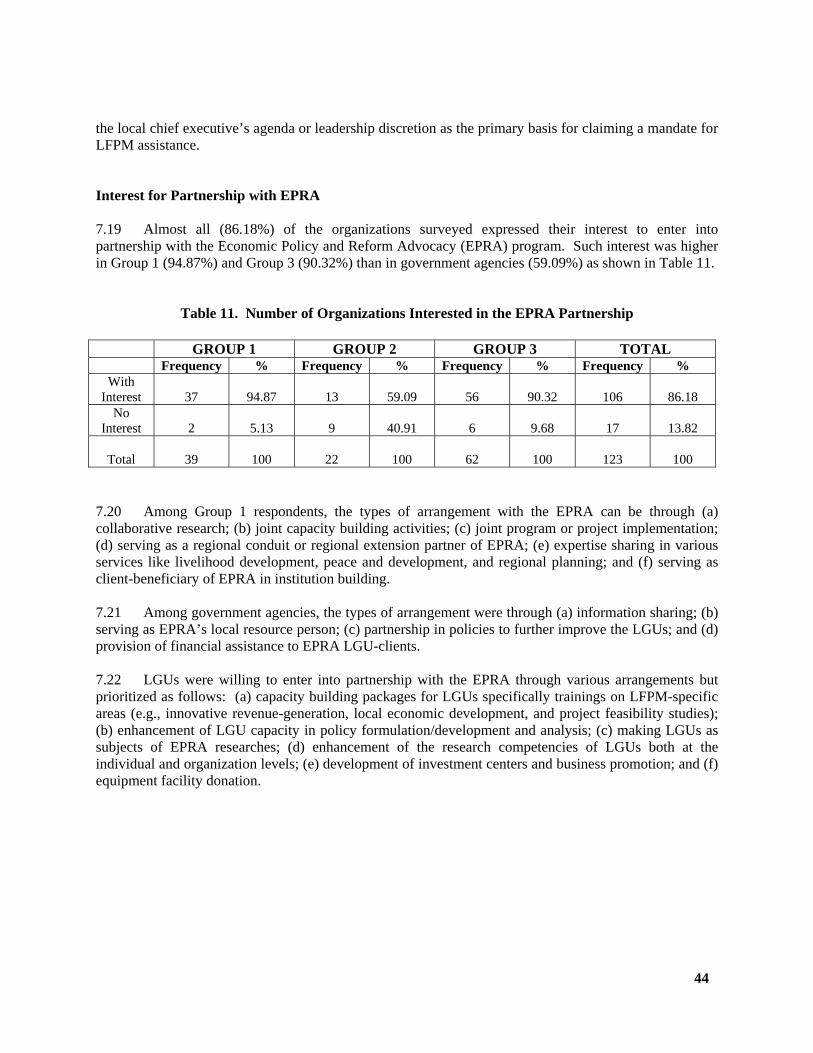

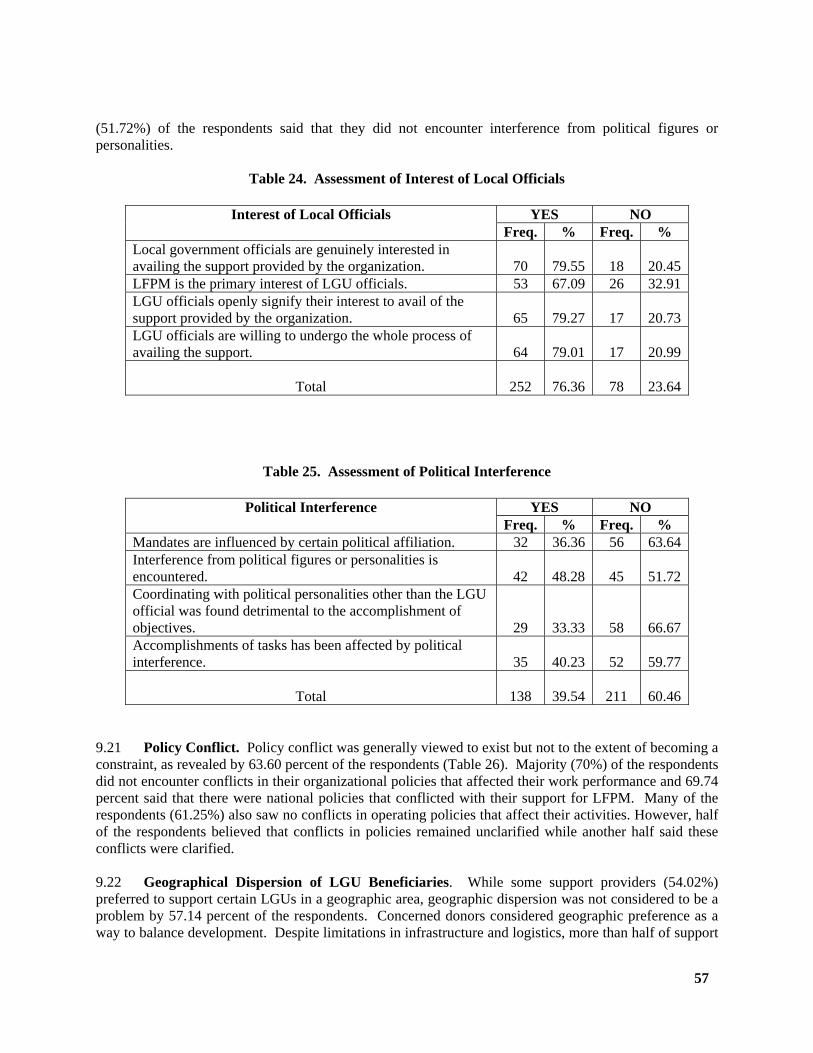

4. Types and Nature of LFPM Assistance

6

5. Areas of LFPM Assistance

16

Revenue Generation 16 Government Accounting 21 Internal Auditing 21 Local Government Budgeting 22 Local Economic Development 22 Local Development Planning 24 Procurement Process 25 6. Specific Assistance by Donors in LFPM

27

Donor Activity in the Philippines 27 A. Asian Development Bank 27 B. Asia Foundation and Transparent Accountable Governance 28 C. Australian Agency for International Development 29 D. Canadian International Development Agency 31 E. Japan 32 F. New Zealand Aid for International Development 33 G. United States Agency for International Development 33 H. The World Bank 33

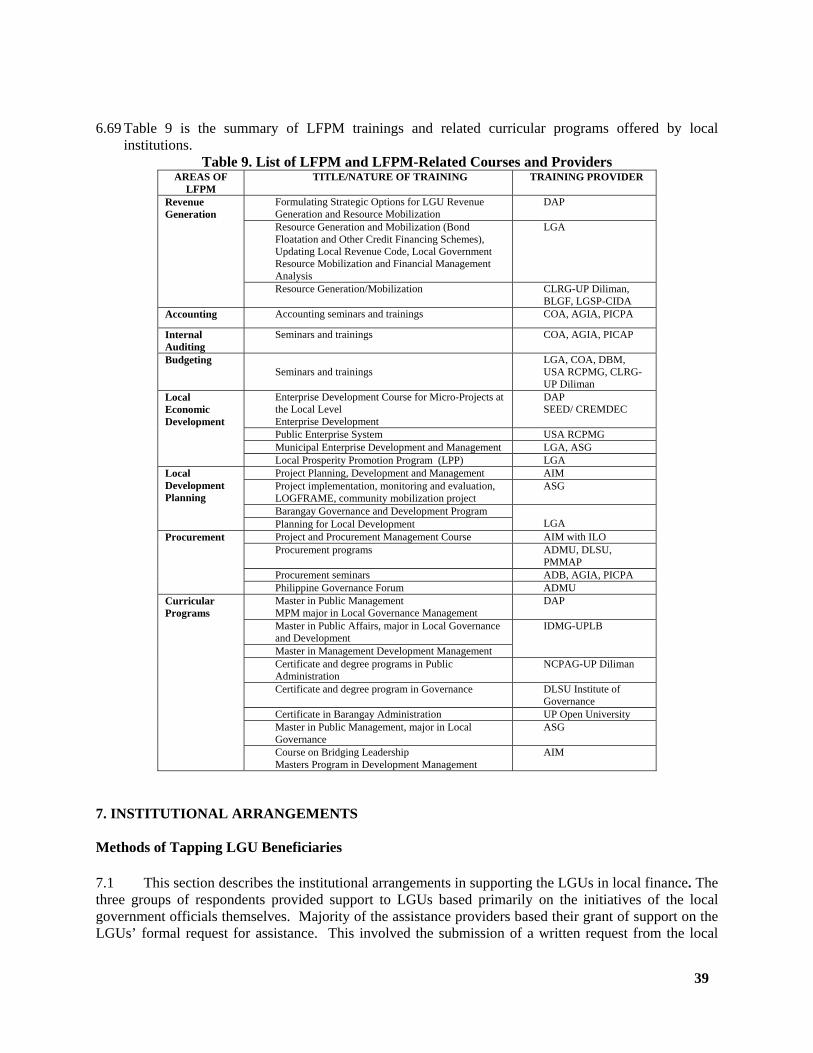

Training Programs and Courses in LFPM Offered by Local Institutions

42

A. Ateneo School of Government 35 B. Asian Institute of Management 36 C. Development Academy of the Philippines 36 D. Local Government Academy 37 E. Institute of Development Management and Governance, UP Los Baños 38 F. Local Governance Training and Resource Institutes Philippine Network 38

ii

7. Institutional Arrangements

40

Methods of Tapping LGU Beneficiaries 40 Forms of Working Arrangements 40 Provision of LFPM Support as Mandate 43 Interest for Partnership with EPRA 44

8. Facilitating Factors in LFPM

45

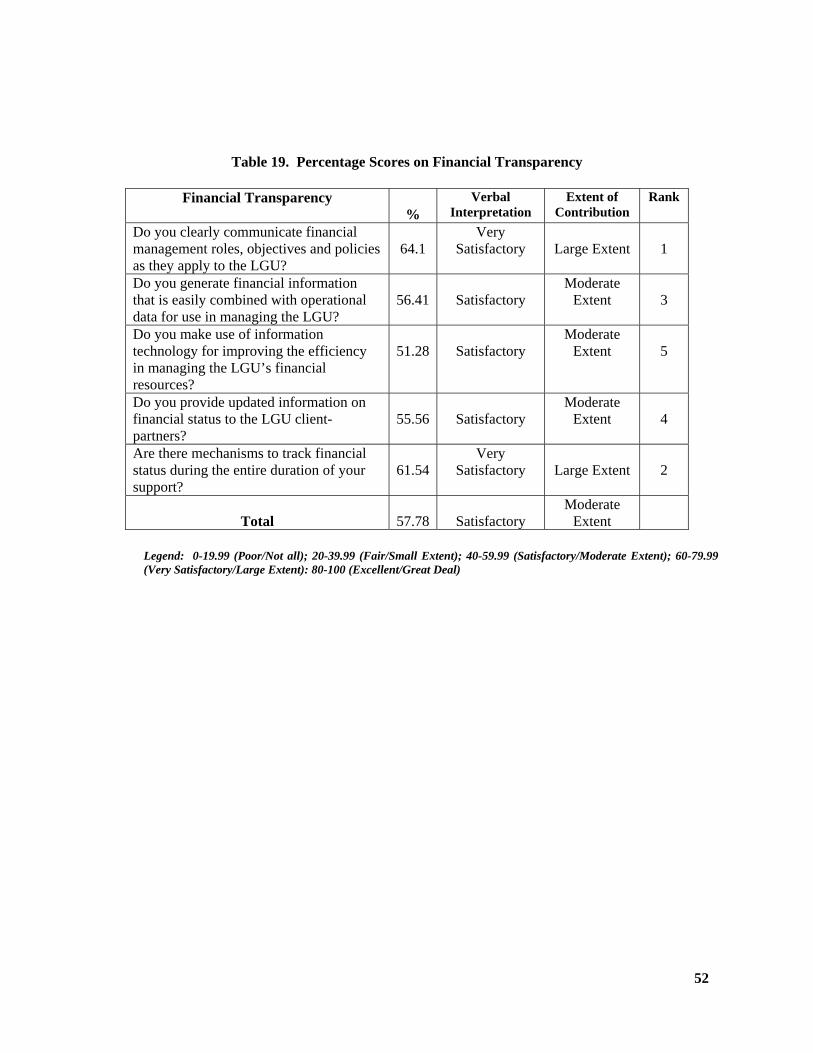

Objectives of Support 45 Political Feasibility 46 Staff Behavior 47 Institutional Processes 48 Participatory Approach 49 Financial Accountability 50 Financial Transparency 50

9. Description of Constraints in LFPM Assistance

53

Common Areas of Confusion 53 Difficulties 54 Not Difficulties 55

10. Gaps and Overlaps in LFPM

59

Mismatch of LFPM Assistance with Current Demands in Local Governments 59 Competing or Conflicting Roles of Government Institutions 60 Weak Coordination Among NGOs to Consolidate and Direct their Assistance to LGUs

60

Loose Internal LGU Financial Management 61 IRA-Related Issues 62 Grey Areas in Local Development Planning 63 11. Summary of Findings

64

Limited LFPM Institutional Assistance at the Local Level 64 Role Differentiation Not Meeting Current Needs 64 Fiscal Performance and Managerial Enhancement 64 Matching of Assistance with Current Demands 66 Harmonization of Functions among Government Institutions 67 Enhancing the Functioning of Networks 68 Strengthening the Internal Financial Management of LGUs 68 References

72

Appendix Table

73

Appendices

75

iii

LIST OF TABLES

TABLE TITLE PAGE

1 Process Flow of Discussion of LFPM Assistance 6 2 Types, Description, Areas of LFPM, and Nature of Assistance 7 3 Gawad Galing Pook Applicants and Awardees by Categories 9 4 Sources of LGU Revenues 14 5 Types and Nature of Assistance by Groups of Providers 15 6 LGUs with Bond Issuance 18 7 LGUs with BOT Projects 20 8 Areas of LFPM and Assistance Provided in Each Area 26 9 List of LFPM and LFPM-Related Courses and Providers 39 10 Number of Organizations with Mandate to Provide Support in LFPM 43 11 Number of Organizations with Interest for EPRA Partnership 44 12 Seven Facilitating Factors in LFPM 45 13 Percentage Scores of the Objectives of Support 46 14 Percentage Scores on Political Feasibility 47 15 Percentage Scores on Staff Behavior 48 16 Percentage Scores on Institutional Processes 49 17 Percentage Scores on Participatory Approach 50 18 Percentage Scores on Financial Accountability 51 19 Percentage Scores on Financial Transparency 52 20 Assessment of Funding Limitations 54 21 Scarcity of Individual Competence 55 22 Assessment of Linkaging Activities 56 23 Assessment of Information Dissemination 56 24 Assessment of Interest of Local Officials 57 25 Assessment of Political Interference 57 26 Assessment of Policy Conflict 58 27 Assessment of Geographical Dispersion of LGU Beneficiaries 58 28 Least Provided LFPM Assistance 59 29 Gaps and Overlaps in LFPM Assistance 61 30 Some Potential Policy Action Arenas for EPRA 70

iv

LIST OF FIGURES

FIGURE TITLE PAGE

1 Operational Framework for the Institutional Mapping of Support Systems to LFPM and Institutional Analysis

3

2 Outputs from Support to LFPMS 42 3 LFPM Assistance Map 65 4 Competency-Based Education Framework for Oversight Function in

Academic Institutions

67

LIST OF APENDIX TABLES

APPENDIX TABLE

TITLE PAGE

1 Inventory Count of Support in LFPM 73 2 Inventory of Support (In Percentage) 74

LIST OF APPENDICES

APPENDIX TITLE PAGE

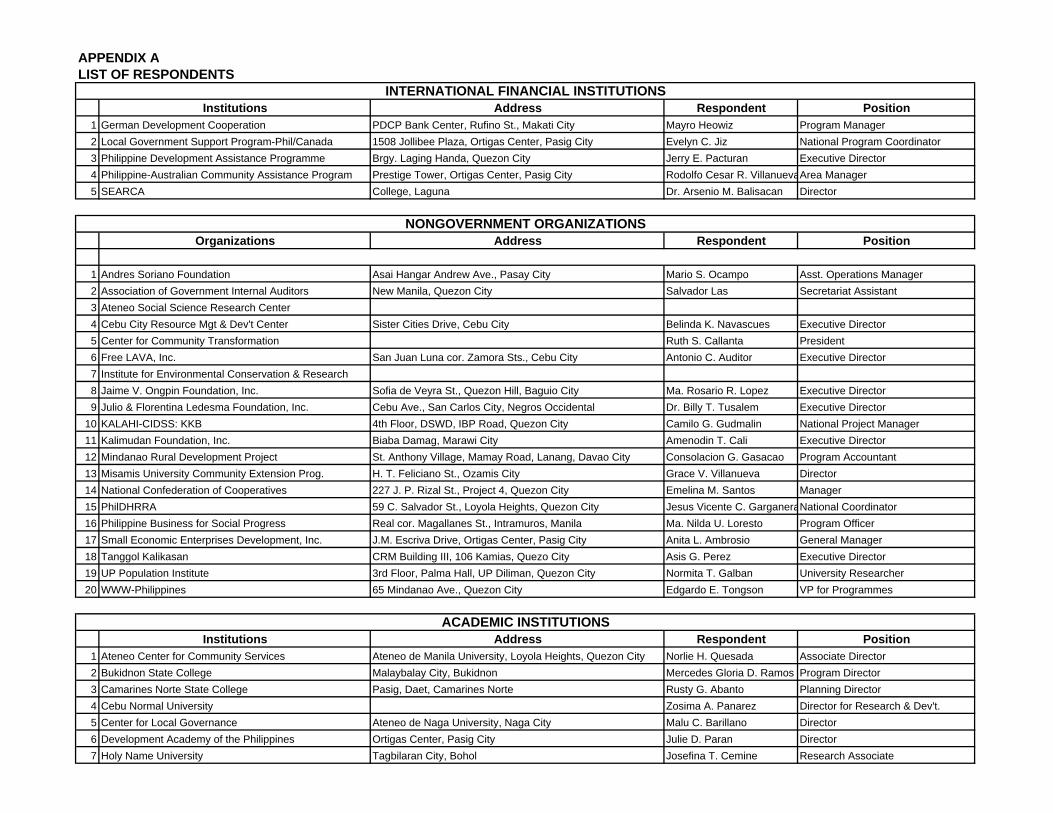

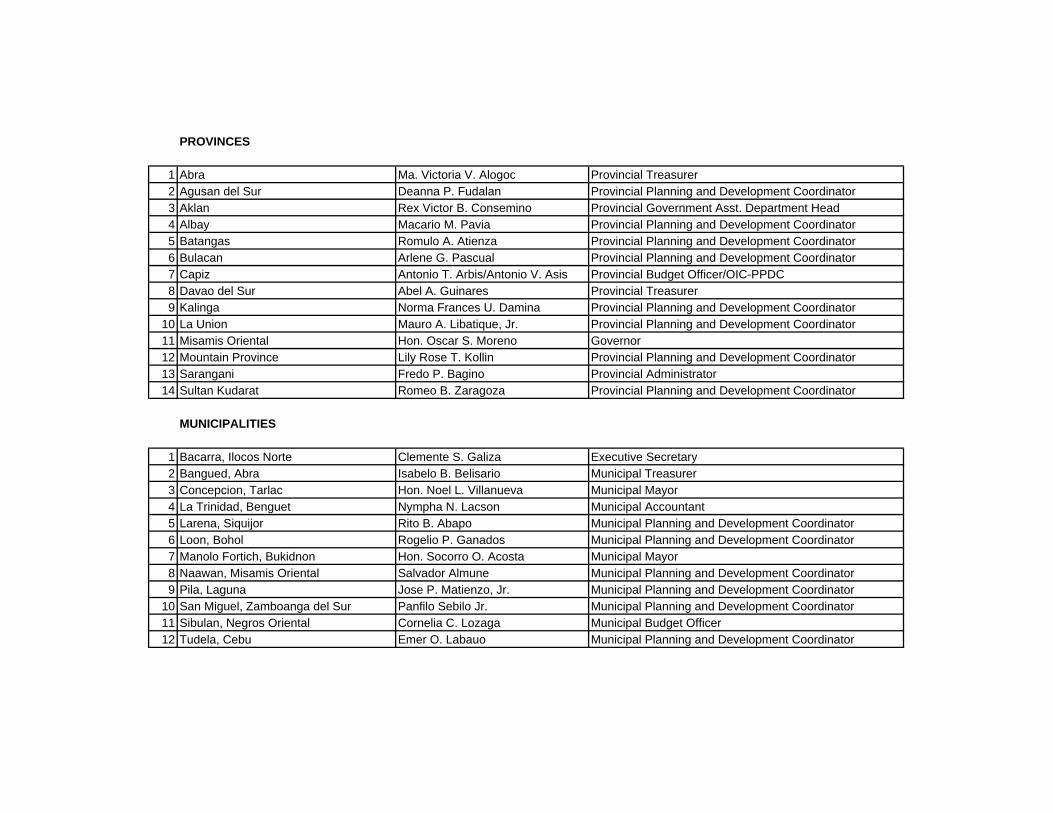

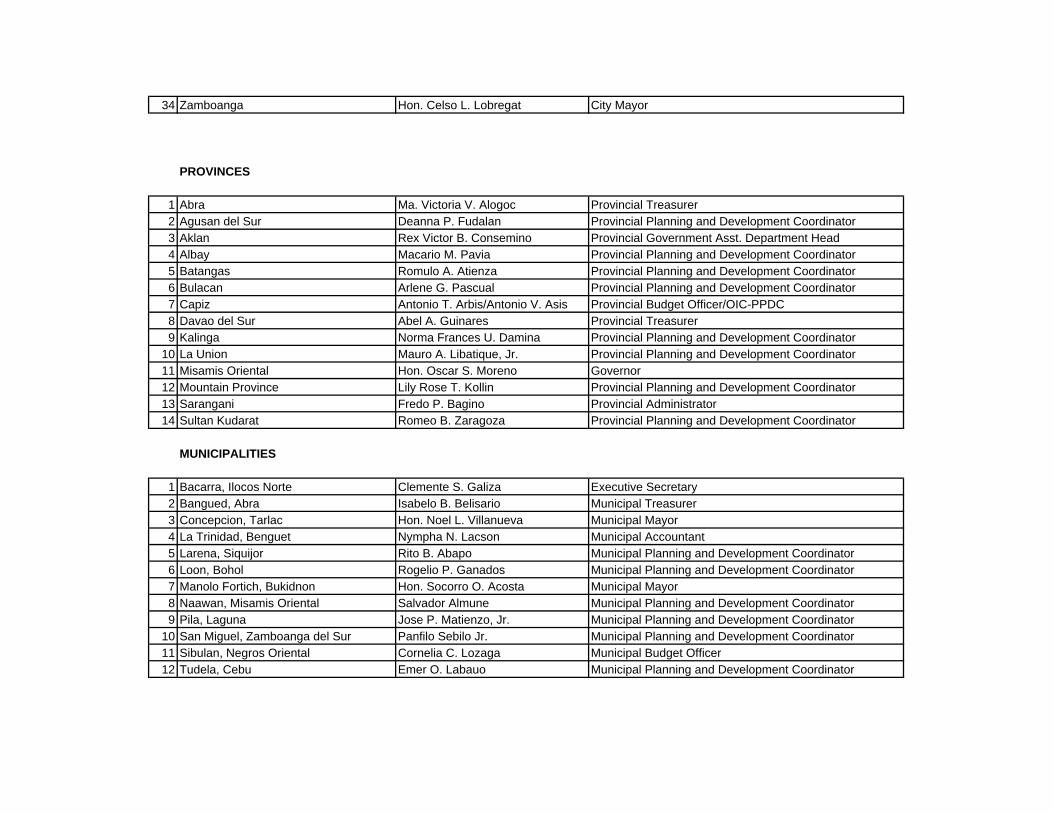

A List of Respondents 75 B Selected List of Books, Researches, and Studies on Local Financial

Planning and Management 79

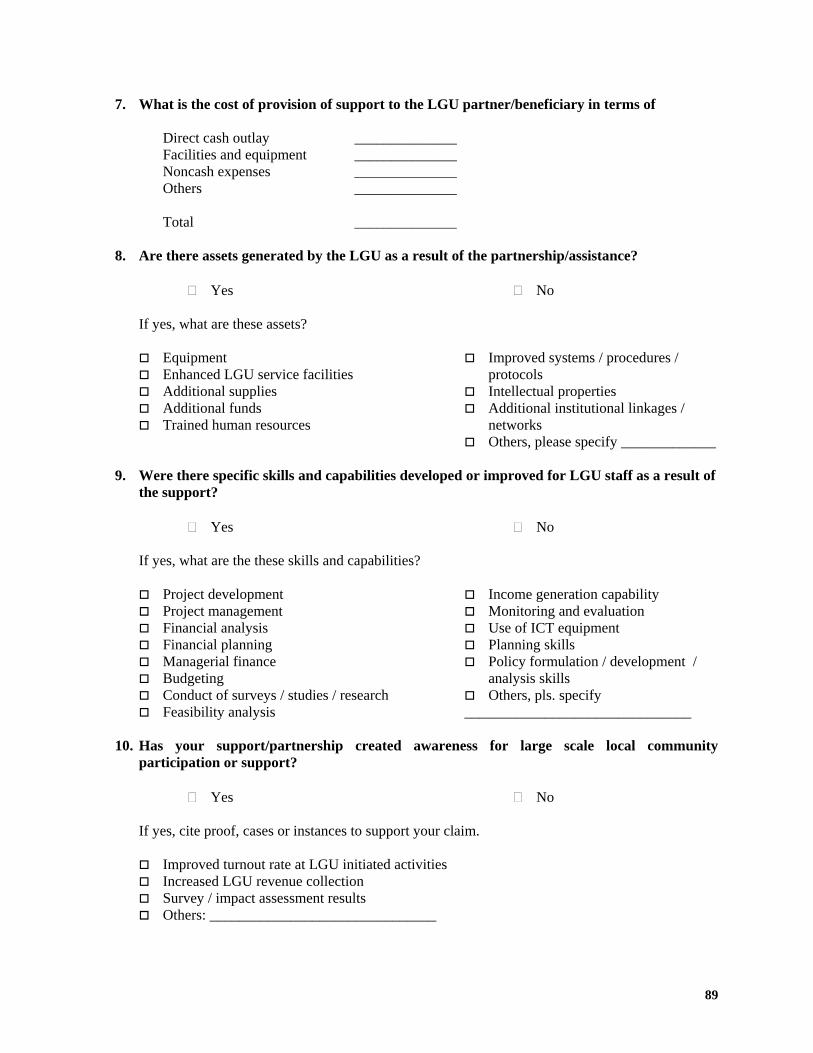

C Survey Questionnaire 85

v

ACRONYMS AND ABBREVIATIONS ADB Asian Development Bank ADMU Ateneo de Manila University AGIA Association of Government Internal Auditors AIM Asian Institute of Management ALRF Assessment Loan Revolving Fund APP Annual Procurement Plan ARMM Autonomous Region of Muslim Mindanao ASF Andres Soriano Foundation ASG Ateneo School of Government AusAID Australian Agency for International Development BLGD Bureau of Local Government Development BLGF Bureau of Local Government Finance BLGS Bureau of Local Government Supervision BOT Build-Operate-Transfer BTEP Business Tax Enhancement Program CBETA Competency-Based Education, Training, Assessment, and Accreditation CBO Community-based Organizations CBRM Community-Based Resource Management CCPSP Coordinating Council for Private Sector Participation CD Community Development CDD community-driven development CDS City Development Strategies CHED Commission on Higher Education CIDA Canadian International Development Agency CLRG Center for Local and Regional Governance CLUP Comprehensive Land Use Plan COA Commission on Audit CREMDEC Cebu City Resource Management and Development Center CSO Civil Society Organization CSC Civil Service Commission DA Department of Agriculture DAP Development Academy of the Philippines DAR Department of Agrarian Reform DBM Department of Budget and Management DBP Development Bank of the Philippines DILG Department of Interior and Local Government DLSU De La Salle University DOF Department of Finance DSWD Department of Social Welfare and Development DTI Department of Trade and Industry EPRA Economic Policy and Reform Advocacy Program GFIs Government Financial Institutions GIS Geographic Information System GOCCs Government Owned and Controlled Corporations GOP Government of the Philippines GPRA Government Procurement Reform Act HRD human resources development IDMG-UPLB Institute of Development Management and Governance, University of the Philippines

Los Banos IEC Information, Education and Communication IFIs International Financial Institutions ILO International Labor Organization IPD Institute of Politics and Development

vi

IRA Internal Revenue Allotment IT information technology JBIC Japan Bank for International Cooperation JFLFI Julio and Florentina Ledesma Foundation, Inc. JICA Japan International Cooperation Agency JSDF Japan Social Development Fund KALAHI Kapit-Bisig Laban sa Kahirapan LBP Land Bank of the Philippines LCE Local Chief Executive LCP League of Cities of the Philippines LDC Local Development Council LFPM Local Financial Planning and Management LGA Local Government Academy LGC Local Government Code LGSP Local Government Support Program LGSPA Local Government Support Program in ARMM LGU Local Government Units LGUGC LGU Guarantee Corporation LLDA Laguna Lake Development Authority LOGOFIND Local Government Finance and Development Project LoGoTRI-PhilNet Local Governance Training and Resource Institutes Philippine Network MDF Municipal Development Fund MDFO Municipal Development Fund Office MNLF Moro National Liberation Front MOA Memorandum of Agreement MST Multi-stakeholder Team NATCCO National Confederation of Cooperatives NCPAG-UPD National College of Public Administration and Governance, University of the Philippines

Diliman NDCC National Disaster Coordinating Council NEDA National Economic and Development Authority NGA National Government Agency NGAS National Government Accounting System NGOs Non-Government Organizations NZAID New Zealand’s International Aid and Development Agency OCOV One Cluster, One Vision for Local Government ODA Official Development Assistance PACAP Philippines-Australia Community Assistance Program PAGBA Philippine Association of Government Budget Administrators PAHRDF Philippines-Australia Human Resource Development Facility PALS Philippines-Australia Local Sustainability PASTT Philippines-Australia Short-Term Training Facility PATSARRD Philippines-Australia Technical Support for Agrarian Reform and Rural Development PBSP Philippine Business for Social Progress PDF project development facility PICPA Philippine Institute of Certified Public Accountants PNB Philippine National Bank PO Peoples Organisations PSEEAP Public Service Excellence, Ethics and Accountability Program PSLP Asia Public Sector Linkages Program PTTAF Policy, Training and Technical Assistance Facility PVB Philippine Veterans Bank RA Republic Act RPT Real Property Tax SEC Securities and Exchange Commission TA Technical Assistance

vii

TAG Transparent Accountable Governance UNDP United Nations Development Programme UP University of the Philippines UPOU University of the Philippines Open University UPSURP UP School of Urban and Regional Planning USAID United States Agency for International Development WB World Bank WDDp Water District Development Project WWF Worldwide Wildlife Foundation

viii

PREFACE AND ACKNOWLEDGMENTS This final report on the project “Institutional Mapping and Analysis of Organizations’ Efforts, Initiatives, and Assistance to Local Financial Planning and Management (LFPM)” identifies and describes the various support provided to the LGUs in the form of efforts, initiatives, and assistance in LFPM. The project aims to provide an inventory and a consolidated report on organizations or institutions that support the progress of financial planning and management in LGUs.

This is the first time that the theme of local financial planning and management has been mapped and reported. The results will provide the Economic Policy and Reform Advocacy (EPRA) program a significant opportunity to gain a general understanding of and explore possible solutions to LFPM directly from institutional providers and beneficiaries. Thus, the study also determines the most important needs as well as constraints and challenges in LFPM that can, in the long run, help LGUs manage their LFPM effectively and efficiently. The project commenced in late January 2006. The preparatory work and data gathering for a national inventory of institutions started on the second week of February and ended in March 2006. This study is the collective efforts of individuals who have shared their ideas and time. The project gratefully acknowledges EPRA and its Executive Director, Dr. Cielito Habito, for believing in the research study and for extending the necessary expert guidance to the project. Ms. Deanna Lijauco, Ms. Gmelina Guiang, and the rest of the EPRA staff provided practical inputs and overall management support for the project. Mr. Austere Panadero, Assistant Secretary of the DILG provided constructive suggestions. The Leagues of Cities of the Philippines and its president, Mayor Jerry Trenas endorsed the survey and Executive Director Atty. Gil Cruz and Ms. Hazel Biniza facilitated the survey through his assistance. Mr. Norberto Malvar and Ms. Pamela Quizon of the BLGF shared their invaluable insights on the current situation of local finance. Dean Corazon Abansi of De La Salle Lipa shared insightful comments on the survey checklists. Mr. Gorgonio R. Virrey, Ms. Carla Gonzales-Jimena and Ricardo G. Buraga provided administrative assistance and Dr. Serlie Barroga-Jamias helped in editing the report.

Finally, the respondents—staff and officials of national government agencies, local government units (LGUs), NGOs, international donors, and academic institutions—who provided vital contributions as active participants and inspirations. This Institutional Mapping Report would hopefully assist LGUs and institutions to take actions where LFPM assistance is needed most.

ix

1. INTRODUCTION

1.1 The Local Government Code (LGC) of 1991 (Republic Act No. 7160) has changed many features of Philippine local governance. The Code enables the local government units (LGUs) to exercise their power to create and broaden their own sources of revenue and claim their right to a just share in national taxes. It also gives the LGUs the power to levy taxes, fees or charges that would accrue exclusively for their use and disposition. Thus, LGUs no longer confine themselves with the traditional sources of revenues; they are also engaged in credit financing, bond floatation, and other non-traditional schemes to enable them to finance local development programs and projects. More importantly, they can avail of credit facilities from both public and private financial institutions to finance infrastructure and other socio-economic development projects. This fiscal decentralization afforded to LGUs has made sound local financial planning and management (LFPM) very important in Philippine local governments. 1.2 Following the grant of autonomy to LGUs, some organizations have opened opportunities for LGUs to improve their capacity to raise revenues and to spend money for effective governance and delivery of important basic services to their constituents. The national government, in particular, has provided facilities to enhance the capacity of local governments in planning and managing their financial resources. International organizations and funding agencies have provided funding sources not only to strengthen the management capacity but also to realize the development goals of the LGUs. Both public and private financial institutions have offered options to finance local development initiatives. The non-government organizations (NGOs) have also re-focused their strategies to enhance participatory local governance among many LGUs. Furthermore, academic institutions have continued to support the LGUs in discovering new technologies and in disseminating knowledge. 2. RATIONALE FOR THE STUDY 2.1 Years after the enactment of the Code in 1991, the idea of complete autonomy for LGUs has yet to be fully realized. The LGUs have not fully exercised their inherent fiscal powers as autonomous governments. Indeed, it is generally believed that the local governments have not explored the available financial packages within their reach. Currently, less than 10 percent of all the 1,696 LGUs exercise their new financing mandate (Amatong, 2005). Only 21 or 1.24 percent of all LGUs have issued bonds (BLGF, 2005) and only 15 or 0.88 percent have build-operate-transfer (BOT) projects (BOT Center, 2005). The Galing Pook Foundation (2006) has documented only 8 (4.8%) of 171 awardees that are finance-related. Given the multitude of support mechanisms and policies of the organizations involved in the development of financial planning and management, it is necessary to conduct an institutional study that will determine the status of support provided by the various organizations. 2.2 The general powers and attributes of LGUs in the Philippines are found in Chapter 2 of the LGC of 1991 which explicitly described the political and corporate nature of LGUs. Section 14 states that “when a new local government unit is created, its corporate existence shall commence upon the election and qualification of its chief executive and a majority of the members of the sanggunian.” This is further reinforced by Section 15 which states “every local government unit is a body politic and corporate endowed with powers to be exercised by it in conformity with law. As such, it shall exercise powers as a political subdivision of the national government and as a corporate entity representing the inhabitants of its territory.” LFPM is broadly classified under the corporate functions and powers of the LGUs. Since

2

the enactment of the Code in 1991, however, the corporate functioning seems to be the weakest link in the financial management chain of the LGU. 2.3 This study consists of an institutional mapping of on-going support to LFPM and an institutional analysis of selected LGUs through a case documentation of innovative LFPM practices that harness inter-local cooperation. The institutional mapping identifies and describes the various forms of support—efforts, initiatives, and assistance—provided to LGUs; these terms are used interchangeably in this study. Institutions cover all forms of organizations: government and non-government organizations, international finance institutions, and academic institutions. The mapping is divided into two phases: (1) inventory and consolidation of organizations or institutions, and (2) interpretation of data to determine the following: organizational relevance, importance and impact on the Economic Policy and Reform Advocacy (EPRA) Project; difficulties and constraints; facilitating factors; and gaps and overlaps. 2.4 The institutional analysis also has two phases: (1) selection of LGUs, and (2) analysis of selected LGUs. The latter assesses the extent of involvement and participation of the LGUs’ Local Finance Committees and Local Development Councils in the planning and budget management processes, in the authorization procedures, and in the leadership patterns in the planning process. The second phase evaluates processes that underlie the LGUs’ LFPM practices and their openness to partner with the EPRA Project. 2.5 The baseline information generated will assist the EPRA Project and its multi-stakeholders team (MST) in identifying priority action arenas and in exploring partnerships with other players engaged in LFPM. The study can also provide various institutions some bases for strategic thinking and policy directions which may redound to the best interest of the LGUs and the communities. The study is the first comprehensive initiative on LFPM mapping in the Philippines, thus the information will constitute the principal database in LFPM assistance to the country. 2.6 Basically, the study was constrained by the lack of comprehensive and available baseline information to establish LFPM assistance. Updated directories of institutions in local governance and development were also hard to find, hence forcing the researchers to exert extra effort in identifying the respondent institutions. Further, there were really no specific persons in the LGUs who can claim direct LFPM responsibilities. 2.7 Because only a few institutions were fully engaged in LFPM, the study made an inventory of institutions covering sector-specific programs and projects with thrust in local governance. This way, the study was approached in both contexts: (a) with LFPM as the main field of service of the institutions, and (b) with LFPM as a component of programs and projects. 2.8 Theoretically, the study reflects a commitment to serious institutional and managerial improvements (Frederickson, 1999) with particular focus on implementation and achievement of results not only on policy and planning but on the involvement of some stakeholders in both planning and implementation (Clark, 1996)). The study is current and fits into the needs of those engaged in research in contemporary governance practices.

3

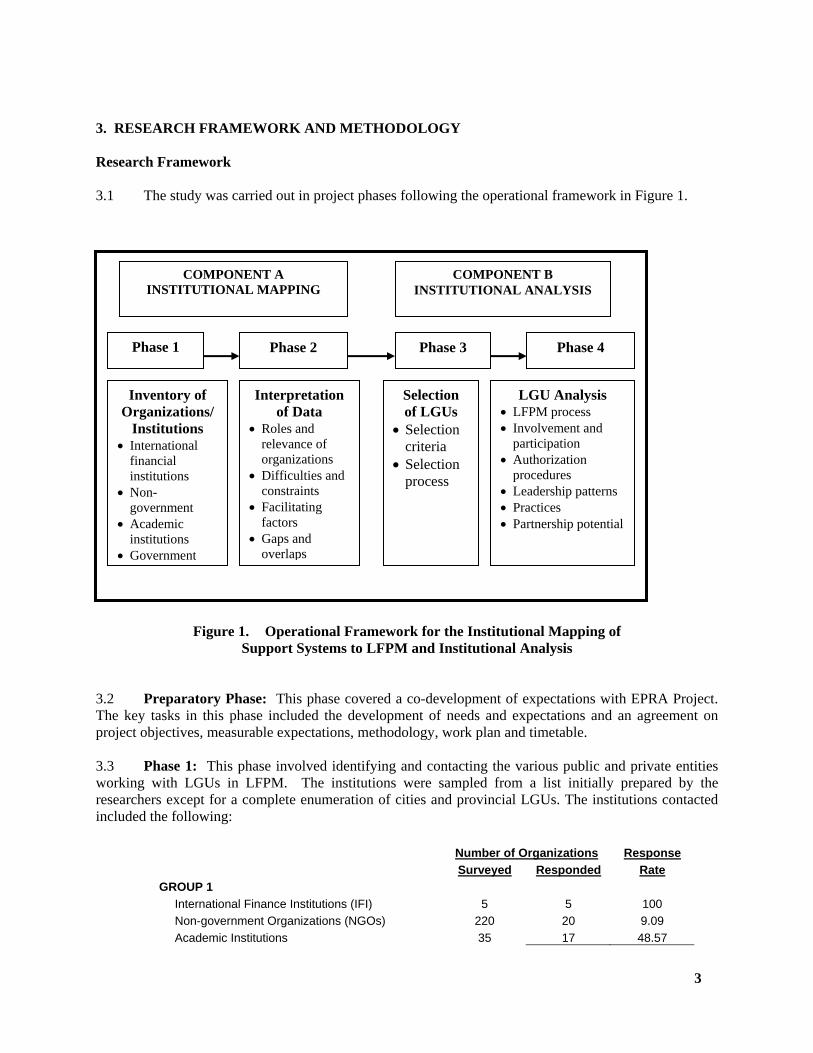

3. RESEARCH FRAMEWORK AND METHODOLOGY

Research Framework 3.1 The study was carried out in project phases following the operational framework in Figure 1.

Figure 1. Operational Framework for the Institutional Mapping of Support Systems to LFPM and Institutional Analysis

3.2 Preparatory Phase: This phase covered a co-development of expectations with EPRA Project. The key tasks in this phase included the development of needs and expectations and an agreement on project objectives, measurable expectations, methodology, work plan and timetable. 3.3 Phase 1: This phase involved identifying and contacting the various public and private entities working with LGUs in LFPM. The institutions were sampled from a list initially prepared by the researchers except for a complete enumeration of cities and provincial LGUs. The institutions contacted included the following:

Number of Organizations Response Surveyed Responded Rate GROUP 1 International Finance Institutions (IFI) 5 5 100 Non-government Organizations (NGOs) 220 20 9.09 Academic Institutions 35 17 48.57

COMPONENT A INSTITUTIONAL MAPPING

COMPONENT B INSTITUTIONAL ANALYSIS

Phase 1 Phase 2 Phase 3 Phase 4

Selection of LGUs

• Selection criteria

• Selection process

LGU Analysis • LFPM process • Involvement and

participation • Authorization

procedures • Leadership patterns • Practices • Partnership potential

Inventory of Organizations/

Institutions • International

financial institutions

• Non-government

• Academic institutions

• Government

Interpretation of Data

• Roles and relevance of organizations

• Difficulties and constraints

• Facilitating factors

• Gaps and overlaps

4

Sub-total 260 42 16.15 GROUP 2 National Government Agencies (NGAs) 19 18 94.74

Government Owned and Controlled Corp. (GOCCs) 3 3 100.00

Sub-total 22 21 95.45 GROUP 3 Provinces 79 14 17.72 Cities 112 34 30.36 Municipalities 142 12 8.45 Sub-total 333 62 18.02 GRAND TOTAL 615 123 20.00

3.4 An inventory of organizations and institutions that provided assistance in LFPM was then produced. Majority of data on the international finance institutions’ (IFIs) assistance were gathered through secondary information as these assistance fell under country assistance programs. 3.5 The 11-page checklist type of survey focused on two areas: (1) purely financial planning and management, and (2) financial planning and management-related initiatives. The survey questionnaires were sent to key informants via postage and electronic mail. The response rate was 20 percent. 3.6 The major reason given by the LGUs for not returning the survey questionnaires was that they did not have any assistance programs for other LGUs except for those in their respective barangays. The NGOs, on the other hand, whose programs/projects were sector-specific, did not have direct LFPM assistance, but the assistance naturally followed in project implementation. Majority of the sent emails bounced back, indicating that NGO directories were not updated. Thus, the survey was followed-up through telephone calls or by physically going to each of the concerned offices. 3.7 The key informants for Group 1 were mostly directors (32.43%) and executive directors (13.52%). Group 2 composed mostly of auditors (45%) and directors (22.7%). Group 3 composed of local financial and administration teams, mostly planning and development officers (45.0%). 3.8 Phase 2. In this phase, results of the study were interpreted and analyzed to extract meanings that would be helpful to EPRA in developing its policy reform agenda and strategic approaches. The role(s) of the different organizations and institutions in the development of financial planning and management in LGUs were identified. The strength of support extended by organizations and institutions to LGUs in terms of relevance, importance, and impact were assessed. Problems faced by the organizations and institutions in terms of difficulties and constraints were appraised. Facilitating factors of the organizations and institutions in the provision of support were identified. Gaps and overlaps in the initiatives, efforts, and assistance to LFPM were also determined. LFPM lessons for the future of local governments were likewise drawn. 3.9 Phase 3 and Phase 4. These phases involved the (a) development of a set of criteria to select LGUs for case studies, and (b) analysis of LGUs with innovative and locally-harnessed practices. The

5

theme of all the case studies was “Inter-LGU Collaboration in Local Financial Planning and Management.”

3.10 There were three variations of the theme:

Case 1: A city and three municipalities (in Luzon) Case 2: A province and three municipalities (in the Visayas-Mindanao areas); and Case 3: A metropolitan city and barangays

3.11 The cases focused on the practices of the LGUs in collaborating with other LGUs in LFPM. In addition, the case studies involved an in-depth institutional analysis of the selected LGUs based on the following:

a. Extent of involvement and participation of the Local Finance Committee and Local

Development Council in the planning and budget management processes; b. Authorization procedures and leadership patterns (factors that determined the ascent to

and maintenance of the position of power and the leaders’ relationship with their followers, network of influence, and access to political power above the barangay level) in the planning process;

c. Evaluation of factors which underlie practices in LFPM and in budget formulation and

execution, such as the information rules, information routines, incentive structures, and level of transparency and accountability; and

d. Openness or willingness of selected LGUs to partner with the Ateneo-EPRA Project.

Process Flow of Discussion 3.12 This report has four major parts – types and nature of assistance; institutional arrangements; facilitating factors and constraints; and policy directions for the EPRA Project (Table 1). The study proceeded with the general problem question: “What is the status of assistance provided by institutions to the development of LFPM in the Philippines?” In so doing, the types of assistance provided to LGUs and their concomitant nature were inventoried or mapped. The report revolved around the seven identified areas of LFPM, categorized as (a) purely financial planning and management areas, and (b) financial planning and management-related areas. These form Part I of the report. 3.13 Part II discusses the institutional arrangements including the identification of methods of tapping the LGU beneficiaries, working arrangements of institutions with LGUs including the terms and conditions of support provided, provision of LFPM support as a mandate, and interest for partnership with the EPRA Project. The benefits derived from the assistance as well as the satisfaction of work relationships are also documented. 3.14 Part III presents the facilitating factors like objectives of support, political feasibility, staff behavior, financial accountability and transparency, and the approaches used in the assistance. The constraints in LFPM assistance are described in terms of common areas of confusion and difficulties. Also discussed are the major gaps and overlaps in LFPM assistance.

6

3.15 Part IV discusses the policy options for EPRA and the identification of proposed interventions in addressing the gaps identified in Part III. A set of action arenas was developed for EPRA and its MST together with the summary of findings.

Table 1. Process Flow of Discussion of LFPM Assistance

Part I. Types and Nature of Assistance Part II. Institutional Arrangements List all types of assistance provided to

the LGUs. Describe the nature of assistance. Identify the areas of LFPM where

assistance is provided.

Identify the methods of tapping LGU beneficiaries

Identify the institutional arrangements in LFPM assistance.

Determine whether provision of support is an organizational mandate.

Assess the interest for partnership with EPRA.

Identify the benefits derived from LFPM assistance.

Part III. Facilitating Factors and Constraints

Part IV. Policy Directions for EPRA

Determine the facilitating factors in LFPM assistance.

Identify the difficulties in LFPM assistance.

Identify major gaps and overlaps in LFPM.

Suggest policy options for the EPRA’s MST.

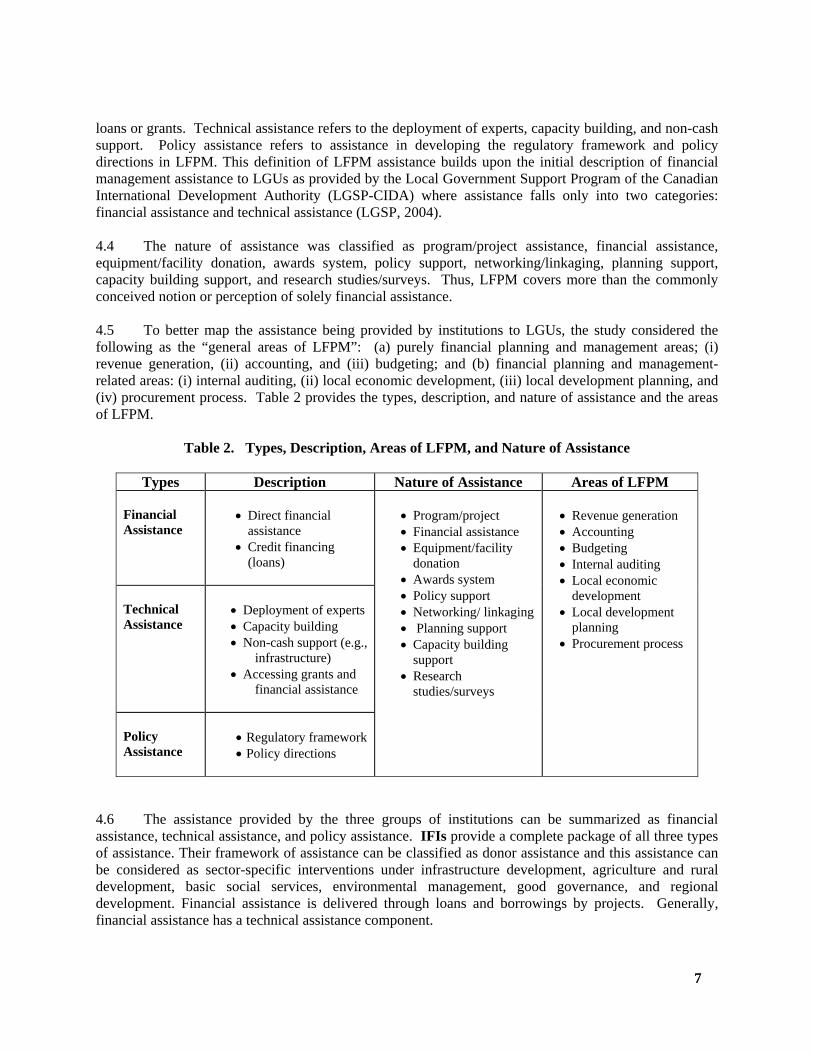

4. TYPES AND NATURE OF LFPM ASSISTANCE 4.1 This section reports the assistance of various institutions to the LGUs. The institutions were classified into groups as follows:

• Group 1: IFIs, NGOs, and academic institutions • Group 2: National government agencies (NGAs) and government owned and controlled

corporations (GOCCs)

• Group 3: LGUs (provinces, cities, and municipalities)

4.2 Altogether, the study covered around 123 institutions broken down into Group 1 (42), Group 2 (21), and Group 3 (62). Making an inventory of institutions directly engaged with LGUs on LFPM proved to be difficult because majority of these institutions were involved with LGUs on sector-specific interventions. These interventions were project or program-based in traditional development areas of health, education, agriculture and rural development, environment, and others. LFPM was a consequential management function of these projects/programs. 4.3 The type of LFPM assistance was three-fold: financial assistance, technical assistance, and policy assistance. Financial assistance refers to direct financial assistance and credit financing either through

7

loans or grants. Technical assistance refers to the deployment of experts, capacity building, and non-cash support. Policy assistance refers to assistance in developing the regulatory framework and policy directions in LFPM. This definition of LFPM assistance builds upon the initial description of financial management assistance to LGUs as provided by the Local Government Support Program of the Canadian International Development Authority (LGSP-CIDA) where assistance falls only into two categories: financial assistance and technical assistance (LGSP, 2004). 4.4 The nature of assistance was classified as program/project assistance, financial assistance, equipment/facility donation, awards system, policy support, networking/linkaging, planning support, capacity building support, and research studies/surveys. Thus, LFPM covers more than the commonly conceived notion or perception of solely financial assistance. 4.5 To better map the assistance being provided by institutions to LGUs, the study considered the following as the “general areas of LFPM”: (a) purely financial planning and management areas; (i) revenue generation, (ii) accounting, and (iii) budgeting; and (b) financial planning and management-related areas: (i) internal auditing, (ii) local economic development, (iii) local development planning, and (iv) procurement process. Table 2 provides the types, description, and nature of assistance and the areas of LFPM.

Table 2. Types, Description, Areas of LFPM, and Nature of Assistance

Types Description Nature of Assistance Areas of LFPM Financial Assistance

• Direct financial

assistance • Credit financing

(loans)

Technical Assistance

• Deployment of experts • Capacity building • Non-cash support (e.g.,

infrastructure) • Accessing grants and

financial assistance

Policy Assistance

• Regulatory framework • Policy directions

• Program/project • Financial assistance • Equipment/facility

donation • Awards system • Policy support • Networking/ linkaging • Planning support • Capacity building

support • Research

studies/surveys

• Revenue generation • Accounting • Budgeting • Internal auditing • Local economic

development • Local development

planning • Procurement process

4.6 The assistance provided by the three groups of institutions can be summarized as financial assistance, technical assistance, and policy assistance. IFIs provide a complete package of all three types of assistance. Their framework of assistance can be classified as donor assistance and this assistance can be considered as sector-specific interventions under infrastructure development, agriculture and rural development, basic social services, environmental management, good governance, and regional development. Financial assistance is delivered through loans and borrowings by projects. Generally, financial assistance has a technical assistance component.

8

4.7 There are very specific assistance initiatives of IFIs under LFPM like (a) the World Bank’s Islands of Good Governance, Local Government Finance and Development Project (LOGOFIND), and Re-Engineering Program under the Department of Budget and Management (DBM); (b) the Asian Development Bank’s (ADB) technical assistance (TA) on strengthening local government finance and budgeting; and (c) the Siquijor Integrated Rural Development Program (SIRMAP) of the German Development Cooperation. SIRMAP emphasizes local economic development and administrative simplification of procedures/ operations as routes for both community development and management capability building. SIRMAP focuses on harnessing interlocal cooperation of doing things together to maximize local capacities and resources. 4.8 The United States Agency for International Development (USAID) assists Philippine institutions in undertaking programs to improve efficiency, transparency and accountability. USAID’s programs seek to achieve improved performance of selected government institutions. Through its Livelihood Enhancement and Peace (LEAP) Program (and LEAP's predecessor programs), USAID has assisted, or is assisting, some 21,000 former Moro National Liberation Front (MNLF) combatants to become commercial producers of corn, rice or seaweed. It has also provided consultants for the BOT to enhance LGUs alternative sourcing of funds. ADB, however, has significantly targeted local financial management as its intervention focus in many of its technical assistance. 4.9 There seems to be a consensus among donors to promote equitable sharing of the benefits of economic growth, reduce poverty at a faster pace, and enhance the self-reliance and service delivery capacity of local governments. Direct LFPM assistance falls under the good governance framework and becomes secondary to other frameworks. 4.10 In the NGOs’ group, results showed that barely half of the NGO respondents actively extended their operations to assist LGUs in LFPM for two reasons. First, specific programs and projects of NGOs were found to have only circumstantial level of assistance to LGUs as one of the former’s beneficiaries. Second, the most frequent NGO/CBO tasks have been community mobilization and capacity building outside LFPM. In other words, LGUs are just one of the target beneficiaries of NGOs. Further, the services of NGOs are mostly outside of LFPM. 4.11 It is generally believed, however, that the increased involvement of NGOs in capacity building has increased the LGU’s demands upon them for their capacity and expertise development. Most respondents cited capacity building, more than any other kind of assistance, as the form of support given by the NGOs to LGUs. 4.12 NGOs’ support to the LGUs was seen as an indirect result of their day-to-day operations. Only two of the NGOs inventoried – the Julio and Florentina Ledesma Foundation, Inc. (JFLFI) and the Cebu City Resource Management and Development Center (CREMDEC) – had specific programs to increase the LGUs’ revenue generation through real property taxation and business permits and licenses. Most of the respondents that supported revenue generation, such as the Center for Community Transformation, the Andres Soriano Foundation, and the National Confederation of Cooperatives (NATCCO), were involved in providing policy support, strategic planning, and capacity building - common assistance provided by NGOs to the LGUs. Institutions such as the Worldwide Wildlife Foundation (WWF) Philippines have supported LGUs in revenue generation through the User Fee System program that it has been implementing in dive sites across the country. 4.13 Since these NGOs’ projects aimed to promote sustainable economic and rural growth through poverty reduction and equity programs, the NGOs would consequently be directly involved with the local

9

governments. CREMDEC was involved in both financial accounting and reporting, in assisting with the establishment of the new government accounting system through awards systems, and in providing technical assistance and capacity building programs. Its operation was highly tied with Cebu City’s local development initiatives, which included accounting and transparency programs. 4.14 Since the inception of the Gawad Galing Pook Innovations and Excellence in Local Governance Awards, a total of 1,592 applications have accepted from the LGUs (Table 3). Of these, 171 (10.7%) have been awarded as models of exemplary and innovative local governance practices in the Philippines. It is noteworthy that of the 128 entries in local administration and management, only 15 got awards, eight of which (or 4.6% of the total awardees) were finance-related. Also, local administration and management (where LFPM belongs as a category) was ranked only 7th in exemplary practices. 4.15 Among the LGUs awarded in finance-related initiatives were (a) Cebu City’s tax computerization project (1994); (b) Binangonan, Rizal’s increased tax collection (1995); (c) Tagaytay City’s financial engineering (1998); (d) San Fernando City, Pampanga’s tax mapping to break financial barriers (2000); (e) Muntinlupa City’s real property tax computerization and administration project (2000); (f) Nueva Vizcaya’s reformed the real property tax system (2002); (g) Cabuyao City’s streamlined business permit process through the one-stop-shop (2002); and (h) Quezon City’s improved revenue collection and spending (2003). 4.16 LFPM is also classified under the enterprise and livelihood development award. Seventeen (6.4%) of 266 LGU applicants have been given this award. Despite the recognition given to the two LFPM areas – financial management and enterprise/livelihood development – however, these have not created as much impact as initiatives in environmental protection and welfare services. This reflects that priorities given by LGUs to LFPM initiatives have not merited recognition by award giving bodies or worse, may not have created enough impact to merit recognition. Nonetheless, this shows that LFPM is a rich area for engaging the assistance of LGUs.

Table 3. Gawad Galing Pook Applicants and Awardees by Categories Program Categories Number of

Applicants Number of Awardees

Rank

Environmental Protection 322 42 1 Enterprise and Livelihood Development 266 17 4 Health and Nutrition 240 16 5 Welfare Services 174 21 2 Agriculture 155 18 3 Local Administration and Management 128 15 7 Service Delivery 89 Education 78 8 9 Protective Services 75 16 6 Housing program 65 Integrated Area Development 10 8 Infrastructure Services 8 10 Total 1592 171

Source: Galing Pook Foundation, 2006 4.17 The LGUs’ need for LFPM assistance is an area which NGOs are indirectly supporting as part of their local development efforts. Due to the importance given to NGOs, their efforts in all activities that

10

they are spearheading must be coordinated. The ADB, for instance, has recognized the capabilities of NGOs in their development programs. In a 1999 study1, ADB stated that since 1990, 25 percent of all ADB projects have had some form of NGO/community based organizations’ (CBO) involvement, and in 1998, more than US$2 billion (49% of all ADB projects) incorporated NGO/CBO activities. 4.18 The academe’s main contribution in LFPM is technical assistance, especially in capacity building and deployment of experts. Notable is the emergence of curricular programs in governance for LGUs in various schools. Among these are the Ateneo de Manila University through the Ateneo School of Government; the University of the Philippines (UP) Diliman though the National College of Public Administration and Governance (NCPAG); the UP Los Baños through the Institute of Development Management and Governance (IDMG); the UP Open University (UPOU); the De La Salle University through the Institute of Governance; and the Development Academy of the Philippines (DAP). 4.19 The Ateneo School of Government offers the Master in Public Management, major in Local Governance, now a customized off-campus program to specific LGUs. The pilot program of this type started in 2005 in the City of Calapan where local officials and employees enjoyed a scholarship grant of the city government. The NCPAG of UP Diliman has a long-standing executive education program for Local Chief Executives. The NCPAG and UPOU have a collaborative offering - the Master in Public Management via distance education. The IDMG of the College of Public Affairs of UP Los Baños offers a Masters degree in Public Affairs, major in Local Governance and Development. The degree’s enrollees alone comprise 10 percent of the total graduate students in UP Los Baños. This program offers fiscal management in LGUs as a major course. Meanwhile, assistance to LGUs comes in the form of on-call individual deployment of faculty experts and occasional institutional researches with academic partners here and abroad. The Certificate in Barangay Administration Program of the UP Open University also emanated from IDMG. The DAP has a Master in Public Management (MPM), major in Local Governance Management, with Local Fiscal Management and Resource Mobilization as a major course. 4.20 Local governance programs have likewise emerged in other universities in the provinces. The University of San Agustin in Iloilo City has a Resource Center for Public Management and Governance providing support to LGUs. The Resource Center was established specifically to support the university’s extension work, thus, in effect, institutionalizing the latter’s efforts to build the LGUs’ capability. The Mindanao Center for Local Governance of the Mindanao State University assists LGUs, mostly barangays of Lanao Sur and LGSP partner LGUs, on capacity building. Specifically, the center conducts local development planning seminars and researches on business permits and licenses. However, majority of LFPM assistance outside Metro Manila can be classified as seminars and trainings only. 4.21 The NGAs exercise their regulatory mandates and extend their activities to LGUs. The Bureau of Local Government Finance (BLGF) of the Department of Finance (DOF), the Department of Interior and Local Government (DILG), the Commission on Audit (COA), and the National Economic and Development Authority (NEDA) lead the government agencies in providing support to LFPM. The most common forms of BLGF assistance are in real property taxation (RPT) especially in tax mapping, revisions of the Real Property Tax Administration (RPTA), databasing of RPTs, and information support. 4.22 The DILG has the Local Government Academy (LGA) as its primary training arm. The LGA was created as a national training institution that would coordinate, synchronize, rationalize, and deliver training programs for local governments. One category in LGA’s training program is Fiscal Management, which includes two major courses: (a) Professionalizing Local Fiscal Managers: A Key to Greater Local Fiscal Autonomy, and (b) Seminar/Workshop on Resource Mobilization and Updating the Local Revenue Code. In practice, there are other departments in the DILG that cater to the training of LGUs. However,

11

the LGA has one of the most expansive training programs in LFPM. The COA likewise has its own training unit that caters to both its own pool of state auditors and to officials and employees of LGUs. It also provides customized training programs, particularly on updates in the New Government Accounting System (NGAS) to certain LGUs or clusters of LGUs. 4.23 Also worth noting is the monitoring and evaluation nature of assistance provided by the NGAs. This study, however, reflected a ‘diminished role’ of NGAs as monitors of the decentralized modes of LGU operations. 4.24 Key assistance can be understood by examining the mandates of each government institution. The Land Bank of the Philippines (LBP), for example, provides a wide range of institutional credit as part of its LGU institutional strengthening program. Its lending program to LGUs includes financing for local infrastructure and other socio-economic development projects in accordance with approved local development plans and investments programs. The bank requires the LGU a counterpart of 25 percent of total project cost. The loans are payable in five years. Similarly, the LBP’s Water District Development Project provides participant LGUs investments on sewerage and sanitation based on the local residents’ wishes and willingness to pay. The bank cost-shares 90 percent while the LGUs provide the remaining 10 percent.

4.25 There are institutional arrangements in co-managing the loans. For example, the LGU appoints a point person to coordinate with the LBP Project Management Office. The LBP also has a Support Credit Program for low-cost housing, health, water systems, flood control and sanitation, and forestry and waste disposal projects with a maximum loanable amount of Php3.0 million. The program is supported by the Japan Bank for International Cooperation (JBIC). Another assistance program is the LBP-LGU Cooperative Strengthening Partnership program, which aims to strengthen capabilities in operations management and sustainability of cooperatives in the LGUs’ locale. This program is a technical assistance program of the LBP funded by LGUs with the LBP providing the necessary information, education and communication (IEC) materials. It is generally recognized that credit financing from government financial institutions (GFIs) is the most popular form of external financing among LGUs.

4.26 To date, the most active GFI in LGU lending is the LBP, with reportedly around Php18 billion in LGU loan portfolio as of yearend of 2001. Privatized former GFI Philippine National Bank (PNB) has released an aggregate of Php6.828 billion to LGUs from 1996 to 2001, while the Development Bank of the Philippines (DBP) had an outstanding LGU portfolio of Php4.659 billion as of the end of February 2002. The Philippine Veterans Bank (PVB), a new player in the LGU market, has so far lent Php677 million to LGUs from 1999 to 2001. 4.27 GFIs were limited to providing direct financial assistance. It was the BLGF that provided the policy and regulatory directions for financial management in local governments. The BLGF played a catalytic role in the effective and sustainable management of fiscal and financial resources of LGUs, transforming them into self-reliant communities. The major services of the BLGF were the following:

• Evaluating and processing of appointment and designation of local treasurers; acting on administrative cases filed against the treasurers;

• Providing technical assistance in the review and updating of local revenue codes; • Rendering opinions and rulings, and issuing circulars and guidelines on local assessment and

treasury operations;

12

• Providing financial assistance in the form of soft loan to LGUs for the conduct of (a) general

revision, (b) RPTA project, and (c) business tax enhancement program; • Conducting seminar-workshop on resource mobilization; and • Issuing certificates on the borrowing and debt service capacity of LGUs.

4.28 The increasing demands on the LGUs coupled with bureaucratic challenges have been forcing the BLGF to effectively function based on its mandates. It was also noted that LGUs were not knowledgeable on how to avail of the various service facilities of the BLGF. In fact, a major technical assistance of ADB is the strengthening of the local financial planning and budgeting among LGUs. Such assistance also addresses the functioning of BLGF and helps in developing its capacities beyond being just a processor of appointments for local treasurers as perceived by the LGUs.

4.29 Another model currently being used is the fund conduit and project management model through the Municipal Development Fund Office (MDFO). Here, the MDFO serves as a fund conduit for multilateral loans such as the Community-based Resource Management Program (CBRMP) and the LOGOFIND project of the World Bank. The facility, called LOGOFIND, has funding support from the World Bank and targets mainly the lower income class LGUs (3rd to 6th income classes). Between 1995 and 2001, the MDFO released Php1.959 billion in loans to LGUs. As to government support, national government allotments to LGUs by type of funds were the following: Municipal Development Fund, Countrywide Industrialization Fund, Local Government Empowerment Fund, Local Officials Insurance Premium Fund, UF-Municipal Development Fund, UF-Support for Foreign-Assisted Projects, Special Financial Assistance to LGUs, Foreign-Assisted Projects Support Fund, and Poverty Alleviation Fund. The total amount allocated to these funds varies from year to year depending on the General Appropriations Act. The MDFO is being considered as a GOCC in the future. 4.30 The decentralization of fiscal responsibilities also gave rise to intergovernmental fiscal transfers. The LGUs receive financial assistance from the national government in the form of revenue sharing through the Internal Revenue Allotment (IRA). Tobacco-producing LGUs share from the tobacco excise taxes as provided for in Republic Act 7171 and Memorandum Order No. 61. National governments also provide grant mechanisms like the Local Empowerment Fund, the DepEd School Building program, the President’s Bridge program, the President’s Social Assistance Fund and the Philippine Development Assistance Fund, commonly referred to as pork barrel. These grants are usually provided to assist LGUs in their special expenditures during calamities and emergencies and to mobilize LGUs towards national government priorities. An example is the assistance provided by the National Disaster Coordinating Council (NDCC) under the Department of National Defense (DND) during calamities and emergencies. These grants are administered by various national government agencies. 4.31 National budget transfers to LGUs consumed 22.5 percent of the national government’s annual revenue collections. At the same time, only 32.6 percent of LGU expenditures were financed by local revenues (Capuno, 2002). For a large percentage of LGUs, the share of own revenues was considerably lower. This growing gap between LGU expenditures and generated revenues is being filled by expanding transfers from the national budget through the IRA. Support in revenue generation was dominant in real property taxation and business permits and licenses and obscure in build-operate-transfer (BOT) schemes and municipal bond floatation. This clearly indicates that organizations and institutions provide support in the traditional areas of revenue sourcing. Non-traditional areas are yet to be explored by those providing assistance to LGUs.

13

4.32 Alternative revenue generation sourcing like municipal bonds and BOT schemes are relegated only to project development and policy support. A noticeable absence of assistance in this area from the academe is noted. The long history of centralization is still seen in the traditional modes of revenue sourcing. The results confirm previous studies that local development projects are largely financed through four mechanisms: (a) directly by government/commercial financing institutions; (b) through the line departments using the LGUs’ own budget/shares (IRA); (c) borrowings from international financing institutions by the national government; and (d) co-financing by LGUs and NGOs. 4.33 The LGUs’ LFPM assistance to other LGUs was in both policy and technical assistance. Policy assistance refers to building up a regulatory framework (e.g., tax collection policies and revenue codes). Direct technical assistance through grants and donations is provided by higher levels of LGUs to their own barangays. Most LFPM assistance to barangays was in information support on revenue enhancement, which the barangays were currently engaged in. Activities for LFPM assistance provided by LGUs to other LGUs included: (a) enactment of municipal/city/barangay ordinances pertaining to local taxation and revenue code; (b) assessment of real property and analysis of revenue collection; (c) scholarship grants; (d) financial grants and other donations to LGUs; (e) seminar and information support on revenue enhancement; (f) active participation in leagues; and (g) establishment of one-stop shop processing centers and their replicates in different areas. 4.34 Inter-LGU LFPM assistance was noted to be high among the LGUs as part of the performance of their mandate for municipality/city to barangay operation. Other forms of assistance were capacity-building through networking and linkaging using study tours and exchanges. Twenty five percent (25%) of the LGUs provided financial assistance to other LGUs for study tours. Further, trainings were conducted to facilitate local policy directions. Majority of the assistance was in the form of “big brother” type where richer LGUs assisted other LGUs especially in times of emergency. For example, the Cebu provincial government donated Php2 million to the Oriental Mindoro provincial government to assist flood victims in late 2005 (The Governor Newsletter, 2006). Another was a city-province model where Quezon City donated Php5.3 million to the province of Southern Leyte for victims of a landslide (Philippine Star, 2006).

4.35 Table 4 provides a summary of the sources of LGU revenues. Most of the LGUs relied on national government grants/shares with alternative revenue sources (commercial credit, bonds, BOT, etc.) being maximized only by higher income LGUs. Alternative sourcing of revenue is a growth area in LFPM.

4.36 Results of this survey showed a higher response rate from respondents of cities at 30.36 percent (34 of 112 cities) than from municipalities at 8.45 percent (12 of 142). This can be attributed to the revenue capacity or stronger position of cities – income-wise - to assist in LFPM compared to municipalities. Inter-local cooperation and assistance were also emphasized in cities. These results confirm the recent documentation and study of best practices by the DOF which concluded that:

“Fourteen years hence, the situation is both inspiring and disturbing. It is inspiring because a number of LGUs have exercised the initiatives in revenue generation using their new taxing power which funded vital development projects that have brought progress to their provinces and municipalities. What is disturbing is that only a small minority of local governments has taken advantage of the new financing options made available to them. Specifically, of 1,696 LGUs (79 provinces, 114 cities and 1,503 municipalities), less than 10% exercised their new financing mandate. The provincial and the city governments appear

14

to be more active in pursuing joint venture agreements and bond issuance compared to municipalities.” (Amatong, 2005)

Table 4. Sources of LGU Revenues LGUs NG

and GFI

Credit

NG Grants/ Shares

BOT Bond Flota- Tion

Donor Assist-

ance (TA)

Commer- cial Credit

Co-financed by LGU

and NGO Majority of LGUs

• •

High Income LGUs

• • • •

Middle Income LGUs

• •

Lower Income LGUs

• • •

Source: Modification of Tan, Roberto, 2004. Global Trends in Financing Sub-National Government and Para-Statal Entities: The Philippine Experience

4.37 In summary, the technical and policy assistance were the two most dominant types of LFPM assistance by institutions. Appendix Table 2 shows that 30.73 percent of the respondent organizations were engaged in capacity building while 18.21 percent provided policy support. The other nature of support included (a) planning support (17.24%); (b) networking and linkaging (15.50%); (c) program/project type (13.88%); (d) research, studies, and surveys (12.03%); (e) financial assistance (10.08%); (g) equipment or facility donation (4.93%); and (h) award system (3.69%).

4.38 Capability building was performed primarily by international funding agencies, NGOs, and academic institutions with varying roles in the provision of support. International funding agencies usually provided funds for capacity building while some NGOs and academic institutions packaged and conducted training programs and study missions. On the other hand, the NGAs provided resource persons on various subject matters as part also of their advocacy to encourage adherence to certain national rules and regulations. Among LGUs, capability building support mostly followed a vertical flow, that is, a higher level of local government assisted a lower level local government. This was best exemplified by provinces helping the municipalities, and the cities and municipalities assisting the barangays. Capability building included training and seminars, study missions, and exchange or twinning arrangements.

4.39 Policy support involved (a) provision of policy agenda and direction, (b) preparation of guidelines, (c) clarification of issues, and (d) initiatives to entice implementation of policies. This was done primarily through the issuance of orders, memoranda, and circulars. Provision of policy agenda and direction was distinct among international funding agencies. Meanwhile, the provision of guidelines, clarification of issues, and monitoring of policy implementation were done by the national government agencies, particularly the DOF through the BLGF, Department of Budget and Management (DBM), DILG, and the COA.

4.40 For the areas of LFPM, Appendix Table 2 shows that the organizations provided assistance primarily in local development planning (23.49%), budgeting (15.81%), local economic development

15

(15.54%), and accounting (13.85%). They assisted least in (a) revenue generation (10.93%); and (b) internal auditing (9.94%). The details of assistance in each area of LFPM are discussed in the succeeding parts of this report. 4.41 Table 5 shows the types and nature of assistance by groups of providers. The three groups

generally provided three types of assistance (financial, technical, and policy), except for the NGOs and academic institutions (which belonged to Group 1) which provided only technical assistance. Further, each group of organizations provided a distinctive nature of assistance.

Table 5. Types and Nature of Assistance by Groups of Providers

Groups Types of Assistance Nature of Assistance Program/Project Loans Policy-based Loans Technical Assistance Grants/Loans Infrastructure Support Technical Cooperation Program Commodity Assistance Emergencies’ Assistance Advisory Services Development Studies Trainings/scholarships

Group 1 International Financial Institutions (Multilateral/Bilateral)

Financial Assistance Technical Assistance Policy Assistance

Support to civil society organizations (CSOs) Training/Capacity Building Dispatch of Experts Community Organization and Mobilization

NGOs Technical Assistance

Sector-specific Development Interventions Curricular Programs in Local Governance Short-term Courses Policy Support Deployment of Experts

Academic Institutions Technical Assistance

Project Feasibility Studies

Lending Program to LGUs LGU Credit Support Technology Promotions

Group 2 GOCC (LBP, DBP, PVB)

LGU-Cooperative Strengthening Partnership Internal Revenue Allotment Shares in National Wealth

National Government (Revenue Shares)

Tobacco Excise Tax Calamity Fund President’s Bridge Program DepEd School Building Program

National Government (Grants)

Financial Assistance Technical Assistance Policy Assistance

Local Government Empowerment Fund Interlocal Cooperation Group 3

LGUs Financial Assistance Technical Assistance Policy Assistance

Calamity Assistance

5. AREAS OF LFPM

16

Revenue Generation 5.1 This part details the assistance given to LGUs by the different groups of organizations in four sub-areas of revenue generation: real property taxation, business permits and licenses, bond floatation, and BOT scheme. 5.2 Real Property Taxation. For the three groups of respondents, assistance to LGUs in RPT was primarily in the form of capacity building and policy support. International funding agencies and some NGOs provided both financial and technical assistance necessary to train officials, employees, and constituents of local governments. These were usually in the aspects of RPT assessment and valuation and in the computerization of the RPT system. Educational institutions served as the training arms of international funding agencies and NGOs; at the same time, they offered their own developed training programs. Some NGOs also provided training programs. 5.3 Among the national government agencies that provided training programs in RPT, the most prominent were the DOF’s BLGF and the DILG. Their support ranged from the offering and conduct of their own developed training programs to the provision of resource persons, and the contracting out of trainings to other private institutions like universities and NGOs with track records in training. In the policy aspect of RPT, the BLGF provided primary support. It issued Local Finance Circulars, RPT opinions and rulings, and assessment regulations. The DBM issued local budget circulars covering a wide range of subjects in LFPM, including RPT.

5.4 The BLGF has the RPTA Project, a countrywide project with funding assistance from the World Bank. The RPTA Project has the following objectives: (a) to support efforts on LGU resource mobilization through the improvement of RPT collection; (b) to enhance administration of foreign-assisted projects; and (c) to develop a model in tax administration for replication in other LGUs. The five components of the RPTA Project are as follows: (a) tax mapping—identifying real property units, establishing property boundaries, determining actual use of properties, and discovering undeclared properties; (b) records conversion and management—conversion of tax mapping information to individual property records with the necessary classification, and appraisal and assessment of real properties. Also included are the preparation of collective assessment rolls as well as the installation and maintenance of a basic system in records management in the local assessment office; (c) tax collection enforcement—review and revision of existing procedures in collection recording, accounting, and disposition of RPTs, both for collectible and delinquent accounts; (d) data computerization—establishment and operationalization of a computer-assisted database for RPTA, including the familiarization/training of key personnel, encoding and validation of data, acquisition and installation of standard RPTA system, generation of reports, and preparation of complementary manual of procedures; and (e) geographic information system (GIS)—digitization of all tax maps with the inclusion of necessary information on every piece of land at the Treasurer’s and Assessor’s Offices and the possibility of linkages with other offices. This system is being used as an aid for ocular inspection, verification of the location of properties by owners, generation of vicinity maps, identification of overlapping in properties, and identification of duplicate assessment of real properties.

5.5 Business Permits and Licenses. The support to LGUs in business permits and licenses (BPL) was also in capacity building and policy. The training on BPL was on the revision or updating of the local revenue tax code that was focused primarily on taxing business establishments. Capacity building on BPL also involved system design or improvement in procedures, processing time, and documentary requirements in applying for local business licenses. Establishment of a one-stop shop had also been a

17

primary subject of discussions in local study missions where a group of local officials observe the practices of LGUs which have established one-stop shops.

5.6 One entity that focused on the BPL system was The Asia Foundation. The foundation has helped enhance the BPL system of several cities in Mindanao. It also worked on “Making Cities Work” to enhance the investment climate and business-enabling environment of LGUs. The BLGF implements the Business Tax Enhancement Program (BETP) aimed to provide medium-term financing and technical support to LGUs for the implementation of programs and activities that will accelerate the growth of local revenue from business taxes. The primordial objective of the BETP is to promote local autonomy and self-reliance by (a) increasing locally sourced revenues and reducing dependency on IRA; (b) accelerating growth of local business tax collections; (c) training of LGUs’ qualified personnel in examining books of accounts of businesses to determine gross receipts; (d) introduction of innovative practices to enlist the cooperation of businesses taxpayers; (e) training of LGUs on the “presumptive income level” in estimating business gross receipts and on the referral to income tax returns for the same purpose; and (f) improving overall LGU management systems in business tax collections. 5.7 The BETP has four components: (a) business tax mapping—identifying the business, establishing business location, determining business nature or type, and discovering undeclared business; (b) records conversion and management—conversion of business mapping information to individual business records, classification, estimation of capitalization or value, preparation of business records, and installation and maintenance of basic management system in business records in the Local Business Tax Office; (c) tax collection and enforcement—review and revision of existing procedures on the collection, recording, accounting, and disposition of business taxes; and (d) data computerization—establishment and operationalization of a computer-assisted database, including the familiarization or training of key personnel, encoding and validation of data, acquisition and installation of standard system, generation of reports, and preparation of complementary manual of procedures. 5.8 Bond Floatation. The LGC of 1991 empowered the LGUs to engage in new modes of financing other than the traditional real property and business taxation. These new modes, which used to be employed by NGAs and GOCCs, included issuance of bonds, establishment and operation of local enterprises, and joint venture arrangements like the BOT scheme. The bond floatation and the BOT were the two popular and common alternatives for sourcing funds to finance projects that the LGUs were engaged in. Caloocan City had the highest recorded bond floated at Php 620 million. 5.9 The DOF (2005) reported that less than 10 percent of the 1,696 LGUs in the Philippines have exercised their new financing mandate (Table 6). Only 21 have issued bonds; 17 have BOT projects that are either completed, under concession, awarded, or in the process of bidding; and 164 have availed of loan packages. These are clear indications that support in bond floatation was primarily in capacity building and research. In addition, the bond floatation of LGUs included guarantee as provided by three entities: the Housing Guarantee Corporation, LGU Guarantee Corporation (LGUCC), and Philippine Veterans Bank (PVB).

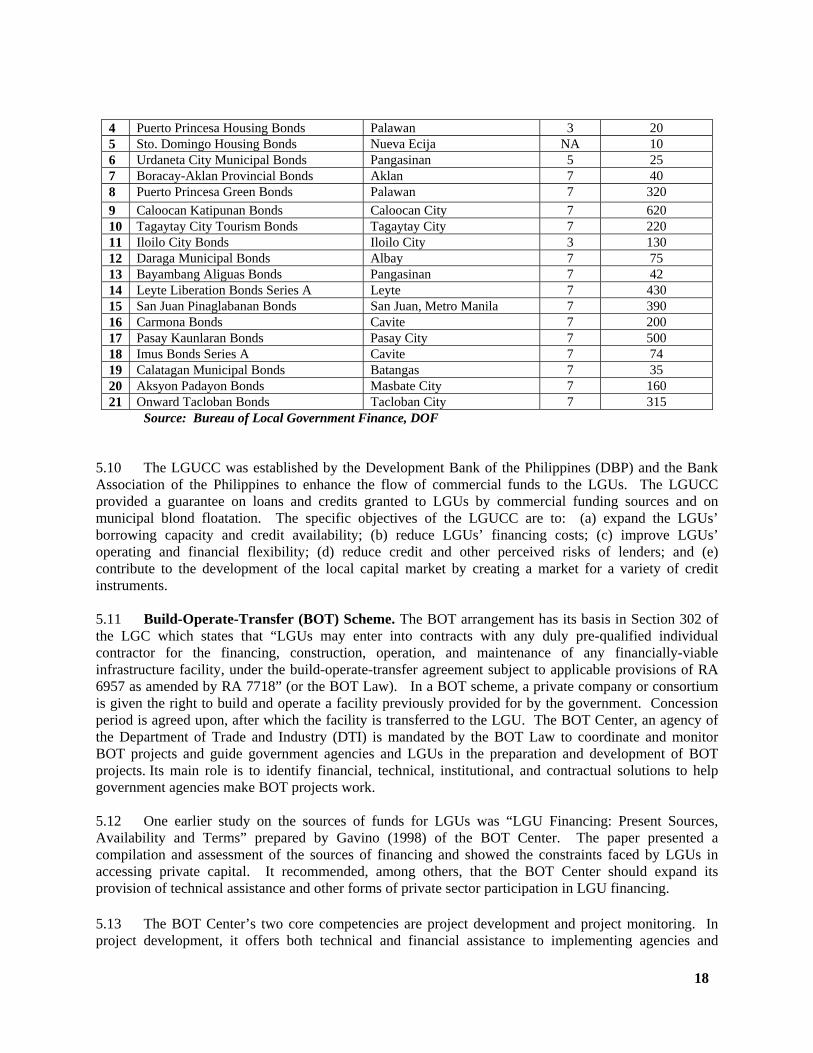

Table 6 LGUs with Bond Issuance Bond Name Area Term

(Years) Project Amount (Million Pesos)

1 Victorias Mabuhay Bonds Negros Occidental 2 8 2 Legazpi Suerte Bonds Albay 3 26 3 Claveria Housing Bonds Misamis Oriental 3 20

18

4 Puerto Princesa Housing Bonds Palawan 3 20 5 Sto. Domingo Housing Bonds Nueva Ecija NA 10 6 Urdaneta City Municipal Bonds Pangasinan 5 25 7 Boracay-Aklan Provincial Bonds Aklan 7 40 8 Puerto Princesa Green Bonds Palawan 7 320 9 Caloocan Katipunan Bonds Caloocan City 7 620 10 Tagaytay City Tourism Bonds Tagaytay City 7 220 11 Iloilo City Bonds Iloilo City 3 130 12 Daraga Municipal Bonds Albay 7 75 13 Bayambang Aliguas Bonds Pangasinan 7 42 14 Leyte Liberation Bonds Series A Leyte 7 430 15 San Juan Pinaglabanan Bonds San Juan, Metro Manila 7 390 16 Carmona Bonds Cavite 7 200 17 Pasay Kaunlaran Bonds Pasay City 7 500 18 Imus Bonds Series A Cavite 7 74 19 Calatagan Municipal Bonds Batangas 7 35 20 Aksyon Padayon Bonds Masbate City 7 160 21 Onward Tacloban Bonds Tacloban City 7 315

Source: Bureau of Local Government Finance, DOF 5.10 The LGUCC was established by the Development Bank of the Philippines (DBP) and the Bank Association of the Philippines to enhance the flow of commercial funds to the LGUs. The LGUCC provided a guarantee on loans and credits granted to LGUs by commercial funding sources and on municipal blond floatation. The specific objectives of the LGUCC are to: (a) expand the LGUs’ borrowing capacity and credit availability; (b) reduce LGUs’ financing costs; (c) improve LGUs’ operating and financial flexibility; (d) reduce credit and other perceived risks of lenders; and (e) contribute to the development of the local capital market by creating a market for a variety of credit instruments. 5.11 Build-Operate-Transfer (BOT) Scheme. The BOT arrangement has its basis in Section 302 of the LGC which states that “LGUs may enter into contracts with any duly pre-qualified individual contractor for the financing, construction, operation, and maintenance of any financially-viable infrastructure facility, under the build-operate-transfer agreement subject to applicable provisions of RA 6957 as amended by RA 7718” (or the BOT Law). In a BOT scheme, a private company or consortium is given the right to build and operate a facility previously provided for by the government. Concession period is agreed upon, after which the facility is transferred to the LGU. The BOT Center, an agency of the Department of Trade and Industry (DTI) is mandated by the BOT Law to coordinate and monitor BOT projects and guide government agencies and LGUs in the preparation and development of BOT projects. Its main role is to identify financial, technical, institutional, and contractual solutions to help government agencies make BOT projects work. 5.12 One earlier study on the sources of funds for LGUs was “LGU Financing: Present Sources, Availability and Terms” prepared by Gavino (1998) of the BOT Center. The paper presented a compilation and assessment of the sources of financing and showed the constraints faced by LGUs in accessing private capital. It recommended, among others, that the BOT Center should expand its provision of technical assistance and other forms of private sector participation in LGU financing.

5.13 The BOT Center’s two core competencies are project development and project monitoring. In project development, it offers both technical and financial assistance to implementing agencies and

19

LGUs. In project monitoring, it is involved even after the project’s successful tender and award. Specifically, the BOT Center is concerned with the following:

• Technical assistance—pre-screening of projects for possible financing, review of technical assumptions, market assessment, and provision of legal advice.

• Financial assistance- in the form of the Project Development Facility which is a loan facility

that can be availed of to finance pre-investment studies and to tender document preparation including the provision of assistance during the bidding process up to contract award.

• Marketing activities—promotion of the Private Sector Participation Program and projects to

potential investors and project stakeholders through on-line promotions and publications. • Policy review and formulation - conducted in coordination with implementing agencies and

oversight agencies to create a policy environment that responds to private sector concerns and ensures the protection of consumers and the public in general.

• Capacity-building - enhancing the skills of LGUs in determining emerging opportunities and

in shepherding projects through the preparation and approval process. 5.14 From Table 7, the construction of public markets and of commercial centers was the popular BOT projects entered into by the LGUs. Seven of the 17 projects were public markets. The schemes usually entered into by the LGUs were characterized by the participation of the private sector as the major sponsor of the project. LGUs preferred this scheme because the private sector assumed certain risks which had been traditionally borne by the public while the project had not yet been transferred to the LGUs. These risks included financing, design, construction and operating risks. This is the reason why only two of the 17 BOT projects were joint ventures between the LGU and the private sector. 5.15 The World Bank places the transfer of knowledge for development and the building of human and institutional capacity at par with the transfer of financial resources and the building of physical capacity. It has assisted the Government of the Philippines (GOP) in (a) establishing a revolving fund - the Municipal Development Fund (MDF) - to provide LGUs with direct access to long-term financing; (b) created an institutional capacity to assist local governments in project preparation and implementation; (c) strengthened local technical and financial capacity for project implementation and service management by creating a Municipal Training Program (MTP); and (d) improved the fiscal performance of local government by enhancing the RPTA system. The Bank also helped develop a policy framework for local government financing that encourages stronger LGUs to access market-based credit; provided public funding and capacity building through the MDF; and targeted funding for poorer LGUs and social and environmental projects. This policy framework is currently being implemented through the LOGOFIND which was approved by the Bank in March 1999. 5.16 The LOGOFIND Project expands and upgrades the basic infrastructure, services, and facilities of participating LGUs and strengthens their capabilities in municipal governance, investment planning, revenue generation, and project development and implementation. It has four components. The LGU sub-projects component strengthens, repairs, and improves basic infrastructure, social services, and environmental facilities. The second component provides training and capacity-building to LGUs in sub-project development and implementation; municipal planning, finance, and management; improvement of training modules and delivery mechanisms; and piloting of new programs, including distance learning, LGU twinning, and collaboration with LGUs, NGOs, and the private sector. The third component

20

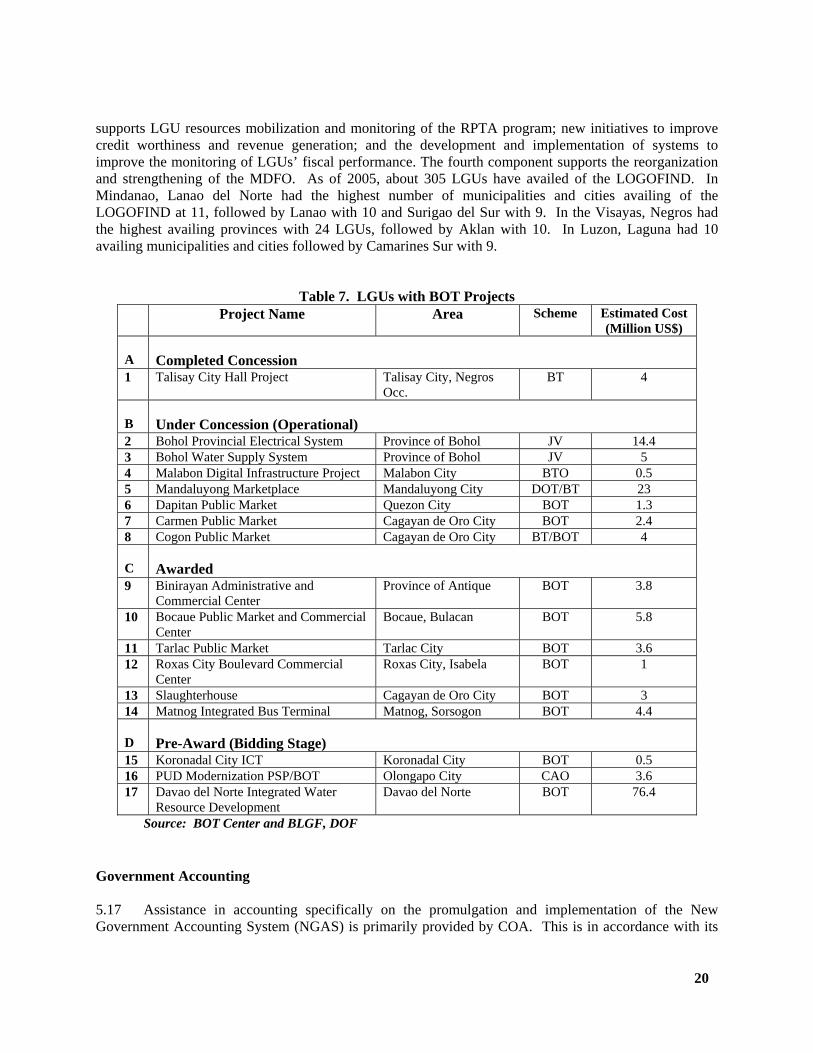

supports LGU resources mobilization and monitoring of the RPTA program; new initiatives to improve credit worthiness and revenue generation; and the development and implementation of systems to improve the monitoring of LGUs’ fiscal performance. The fourth component supports the reorganization and strengthening of the MDFO. As of 2005, about 305 LGUs have availed of the LOGOFIND. In Mindanao, Lanao del Norte had the highest number of municipalities and cities availing of the LOGOFIND at 11, followed by Lanao with 10 and Surigao del Sur with 9. In the Visayas, Negros had the highest availing provinces with 24 LGUs, followed by Aklan with 10. In Luzon, Laguna had 10 availing municipalities and cities followed by Camarines Sur with 9.

Table 7. LGUs with BOT Projects Project Name Area Scheme Estimated Cost

(Million US$) A

Completed Concession

1 Talisay City Hall Project Talisay City, Negros Occ.

BT 4

B

Under Concession (Operational)

2 Bohol Provincial Electrical System Province of Bohol JV 14.4 3 Bohol Water Supply System Province of Bohol JV 5 4 Malabon Digital Infrastructure Project Malabon City BTO 0.5 5 Mandaluyong Marketplace Mandaluyong City DOT/BT 23 6 Dapitan Public Market Quezon City BOT 1.3 7 Carmen Public Market Cagayan de Oro City BOT 2.4 8 Cogon Public Market Cagayan de Oro City BT/BOT 4 C

Awarded

9 Binirayan Administrative and Commercial Center

Province of Antique BOT 3.8

10 Bocaue Public Market and Commercial Center

Bocaue, Bulacan BOT 5.8

11 Tarlac Public Market Tarlac City BOT 3.6 12 Roxas City Boulevard Commercial

Center Roxas City, Isabela BOT 1

13 Slaughterhouse Cagayan de Oro City BOT 3 14 Matnog Integrated Bus Terminal Matnog, Sorsogon BOT 4.4 D

Pre-Award (Bidding Stage)

15 Koronadal City ICT Koronadal City BOT 0.5 16 PUD Modernization PSP/BOT Olongapo City CAO 3.6 17 Davao del Norte Integrated Water

Resource Development Davao del Norte BOT 76.4

Source: BOT Center and BLGF, DOF Government Accounting 5.17 Assistance in accounting specifically on the promulgation and implementation of the New Government Accounting System (NGAS) is primarily provided by COA. This is in accordance with its

21