23

University of Dhaka Department of Accounting & Information Systems Assignment On Institutional Shareholders in Bangladesh

| Date post: | 15-Jul-2015 |

| Category: |

Education |

| Upload: | abdullahais16 |

| View: | 889 times |

| Download: | 1 times |

University of Dhaka

Department of Accounting & Information Systems

Assignment

On

Institutional Shareholders in

Bangladesh

Course Name: Corporate Governance Course Code: 7104

Date of Submission: 11/08/2014

Submitted to:

Dr. Dhiman Kumar Chowdhury

Professor

Department of Accounting & Information Systems

Faculty of Business Studies

University of Dhaka

Submitted by:

Name ID Serial No.

Mir Imrul Hasnat 16004 01

A. B. M. Abdullah 16010 03

Md. Ababil Chowdhury 16013 04

Md. Billal Hossain Shourav 16025 06

Syeda Seemia Mahbub 16026 07

Naima Islam 16063 15

Sahera Khatun 16083 18

Md. Mehedi Hasan 16088 20

MBA 16th

Batch, Section – C

Department of Accounting & Information Systems,

Letter of Transmittal

Department of Accounting & Information Systems

University of Dhaka

August 11, 2014

Dr. Dhiman Kumar Chowdhury

Professor

Dept. of Accounting & Information Systems

University of Dhaka

Subject: Submission of final assignment

Dear Sir,

We are delighted to submit our assignment on ‘Institutional Shareholders in Bangladesh’.

This paper has been prepared according to your authorization. To prepare this paper, we have

gone through many articles, reports, journals, research papers and websites for collecting

necessary information.

We are thankful to you for assigning us for preparing such a paper that will increase our

knowledge in different areas of capital market.

Sincerely Yours,

Syeda Seemia Mahbub

On behalf of the group

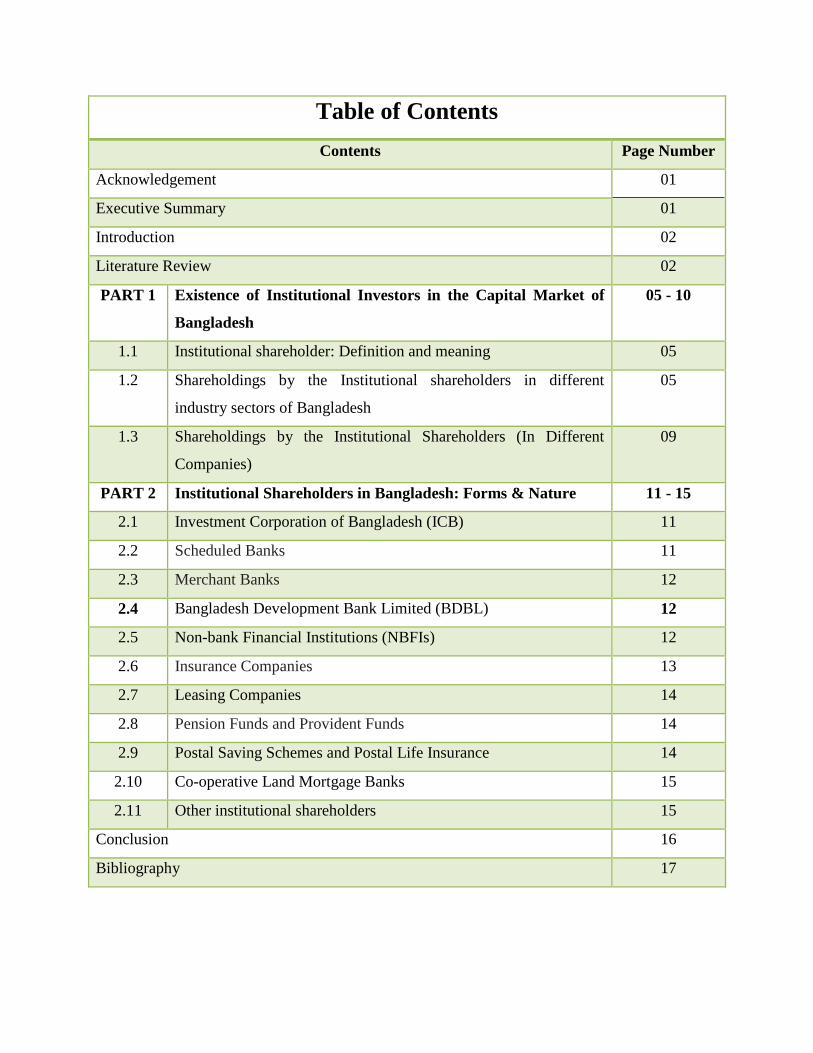

Table of Contents

Contents Page Number

Acknowledgement 01

Executive Summary 01

Introduction 02

Literature Review 02

PART 1 Existence of Institutional Investors in the Capital Market of

Bangladesh

05 - 10

1.1 Institutional shareholder: Definition and meaning 05

1.2 Shareholdings by the Institutional shareholders in different

industry sectors of Bangladesh

05

1.3 Shareholdings by the Institutional Shareholders (In Different

Companies)

09

PART 2 Institutional Shareholders in Bangladesh: Forms & Nature 11 - 15

2.1 Investment Corporation of Bangladesh (ICB) 11

2.2 Scheduled Banks 11

2.3 Merchant Banks 12

2.4 Bangladesh Development Bank Limited (BDBL) 12

2.5 Non-bank Financial Institutions (NBFIs) 12

2.6 Insurance Companies 13

2.7 Leasing Companies 14

2.8 Pension Funds and Provident Funds 14

2.9 Postal Saving Schemes and Postal Life Insurance 14

2.10 Co-operative Land Mortgage Banks 15

2.11 Other institutional shareholders 15

Conclusion 16

Bibliography 17

1

Acknowledgement

We are heartily grateful to our instructor Dr. Dhiman Kumar Chowdhury whose encouragement,

guidance and support from the initial to the final level enabled us to complete this paper. We

would also like to extend our thanks to all those writers, researchers, journalists and bloggers

whose works provided us with all the necessary information.

Executive Summary

Shareholders in the capital market are either individual shareholders or institutional shareholders.

Institutional shareholders are mainly different types of business or non-business organizations.

These investors play very important roles in developing and stabilizing the capital market. But

the capital market of Bangladesh is facing a serious shortage of institutional investors.

The institutional shareholders in the capital market are of different categories, for example-

Investment Corporation of Bangladesh, Bangladesh Development Bank Limited, scheduled

banks, merchant banks, insurance companies, leasing companies, non-bank financial institutions,

pension funds, postal saving schemes & postal life insurance, co-operative land mortgage banks,

employee insurance funds and so on.

The companies listed in Dhaka Stock Exchange (DSE) have on an average 16.81% institutional

shareholding in their share capital. Companies with large proportion of institutional shareholding

in the share capital are very few. Moreover, 58 companies have no institutional shareholding in

their share capital.

It has been found that in the capital market of Bangladesh, institutional shareholdings are high in

companies in some industry sectors, for example- mutual funds, ternary, service & real estate,

pharmaceuticals etc. On the other hand, institutional shareholding is very low in companies of

telecommunication, textile, jute, food & allied sectors. Most of the companies of other industry

sectors do not have significant portion of institutional shareholdings in their share capital.

The shortage of institutional shareholders is hampering the overall development of the capital

market of Bangladesh. But there are opportunities of increasing the base of institutional

2

shareholders in the capital market. But the government should take proper steps to attract these

investors to participate in the capital market.

Introduction

Background: In the capital emerging capital markets around the world, the position and

participation of institutional shareholders is very significant. But the situations of the capital

market of Bangladesh are very much lagging behind in this regard. Here, institutional

shareholders are negligible and unwell to expand their investment in the capital market.

Increasing the base of institutional shareholders in the capital market of Bangladesh has become

a burning question. Before we attempt to this increase base, we need to find out the present

position of this shareholders in the capital market. Moreover, we need to clearly identify the

institutional shareholders existing in the capital market.

Objective: The objectives of this paper are to:-

Describe the concept and meaning of institutional shareholder

Find out the presence of institutional shareholders in the capital market of Bangladesh

Identify the institutional shareholdings in the capital structure of the listed companies of

Bangladesh

Describe the existing institutional shareholders in the capital market of Bangladesh etc.

Methodology & limitations: This paper has been prepared based on content analysis.

Information has been collected from different articles, journals, websites, research papers and

annual reports. In some cases, we have performed mathematical calculations through Microsoft

Excel. The main limitation of this study is that information has been collected form secondary

data sources like annual reports, websites, articles, research papers. Moreover, we have

performed this study with our limited knowledge and within a limited time.

Literature Reviews

Afroz, T. (2004) presented some suggestions for increasing the institutional base in the capital

market of Bangladesh. Some of these suggestions are:- (a) Removing regulatory barriers to

enable contractual savings funds (such as, insurance company funds, pension and provident

3

funds etc.) to invest substantial amount of their collections into capital market instruments with

better earning capacity, (b) Enforcing a level playing regulatory measure for public and private

mutual funds, (c) Proper restructuring of ICB and making it more answerable and transparent;

and (d) Reforming current regulatory regime into one where more coordination is guaranteed

among various regulators (for example- SEC, the Bangladesh Bank, the Department of

Insurance, Ministry of Finance, Ministry of Commerce, other concerned ministries etc.) who

directly or indirectly influence capital market mechanism for institutional investment.

Akhter, R. and Ahmed, S. (2013) mentioned, “It is said that stock market is a gambling market.

There is scope of manipulation to earn more profit. In manipulation major contribution is made

by institutional buyers.”

CMDMPM, BSEC (2012) “Institutional investor participation in Bangladesh‟s capital markets

has been limited. We recognize the need to improve the enabling environment through the

adoption of policies that stimulate the expansion of the institutional investor base specifically

with respect to three types of institutional investors: mutual funds, insurance companies, and

pension and provident funds.”

Institutional Investment is negligible in Bangladesh. Institutional investment as percentage of

total market capitalization ranges between 4.53 per cent and 4.88 per cent during 2005-2008.

Institutional investment brings long-term commitment and greater focus on the fundamentals

and, hence, stability in the market. Furthermore, the presence of institutional investor is also

expected to ensure better valuation levels due to their special analytical skills. Bangladesh capital

market missed this source of efficiency gains as institutional investment is very small in both

absolute and percentage terms. (Banerjee et al., 2010)

Malik, M. and Imam, O. M. (2007) have found that in Bangladesh foreign holdings are

increasing in those firms that have good governance. They observe a positive relationship

between institutional ownership and firm performance suggesting that institutional shareholders

have the incentive as well as the power to monitor and control the behavior of firms, and have

played a significant role in corporate governance. The role of large institutions in corporate

governance is particularly important in countries where legal protection of shareholders‟ interest

4

is weak for historical and institutional reasons. This is a situation that exists in many transition

economies.

Moazzem, K. G. (2013) has pointed out that some institutional shareholders, for example,

financial institutions were found to behave like retail investors. They were non-compliant with

laws and performed unauthorized transactions in the secondary market. They have the tendency

to invest for short periods in the market for achieving high capital gains. But institutional

investors like the financial institutions are likely to supply long-term money in the capital

market.

Sayeed, Y. (2004) identified a serious dearth of institutional investors in the capital market of

Bangladesh. In this country, the institutional investor community like investment & merchant

banks, mutual funds, pension & provident funds, life insurers etc. has unfortunately not

developed due to multifarious impediments. The market is essentially retail based and prone to

high risk. The newly licensed merchant banks are yet to make any tangible mark, the government

pension funds are essentially non-funded and non-accounted-for liabilities, provident and

insurance funds restrained under age old qualitative and quantitative restrictions and growth of

private mutual fund retarded under stringent regulatory frame-work and an uneven playing field.

None of these ground realities has been conducive to growth of a healthy and vibrant capital

market.

5

PART 1

Existence of Institutional Investors in the Capital Market of Bangladesh

1.1 Institutional shareholder: Definition and meaning

In the capital market there are two types of shareholders- individual and institutional. General

people who buy/sell their shares in the market are individual shareholders. On the other hand,

many institutions, firms, associations and organizations who buy/sell shares of listed companies

in the capital market for investment purposes are institutional shareholders. Examples of

institutional shareholders are banks, insurance companies, mutual funds and many other financial

institutions. In this paper, we will focus mostly on this type of shareholders.

Generally, these shareholders are large organizations with considerable assets to invest in the

securities of the listed companies. In some capital markets, these institutional shareholders

undertake large volume of transactions. For example, in the New York Stock Exchange, 70% of

the trading is performed on behalf of the institutional shareholders. (Business Dictionary, 2014)

Institutional shareholders are more knowledgeable compared the individual shareholders. So,

they are stronger than the individual shareholders in protecting their own interest. Moreover,

institutional shareholders in many cases have to comply with fewer regulations in share trading

compared to the individual shareholders.

1.2 Shareholdings by the Institutional shareholders in different industry sectors of

Bangladesh

To find out the position of institutional shareholders in the capital market and in different

industry sectors of Bangladesh, we have analyzed the information of 303 listed companies from

19 industry sectors of Dhaka Stock Exchange (DSE). In our analysis we have excluded 3

industry sectors, for example- Treasury Bonds, Corporate Debentures and debentures. The

findings of this analysis are shown in (Table 1.1).

From (Table 1.1), we see that the institutional shareholders constitute a small portion of

shareholding in the capital market. Present shareholding by institutional shareholders in DSE

listed companies is on an average 16.81%. This has been calculated by taking the institutional

6

shareholdings in 303 companies listed in DSE. Again, we can also see that institutional

shareholding exists in 245 companies and in 58 companies this type of shareholding is 0%.

Table 1.1 Institutional Shareholding in DSE

No. Industry Sectors Total

Companies

Total Companies

with Institutional

Shareholdings in

Share Capital

Total Companies

with no Institutional

Shareholdings in

Share Capital

Average Percentage

of Institutional

Shareholdings in the

Overall Industry

01 Banks 30 26 04 14.89%

02 Cement 07 05 02 14.10%

03 Ceramics 05 05 0 17.43%

04 Engineering 25 21 04 16.47%

05 Financial Institutions 23 21 02 15.26%

06 Food & Allied 18 14 04 10.90%

07 Fuel & Power 16 12 04 14.24%

08 Insurance 46 31 15 12.30%

09 IT Sector 06 05 01 15.04%

10 Jute 03 01 02 9.79%

11 Mutual funds 41 29 12 30.53%

12 Pharmaceuticals 26 24 02 18.26%

13 Service & Real Estate 03 03 0 18.62%

14 Ternary 05 04 01 19.44%

15 Paper & Printing 01 01 0 8.51%

16 Telecommunication 02 02 0 9.25%

17 Travel & Leisure 03 02 01 15.44%

18 Textiles 34 30 04 11.67%

19 Miscellaneous 09 09 0 11.68%

Total 303 245 58 16.81% *

Average institutional shareholding in 303 listed companies in DSE *

Source: Website of Dhaka Stock Exchange (DSE)

From the above table, we see that the highest institutional shareholding exists in the Mutual Fund

sector. In this sector, mutual funds have on an average 30.53% institutional shareholding in their

7

share capital. Among the mutual funds, 70.73% funds (29 out of 41) have institutional

shareholding in their share capital. The mutual funds which have high institutional shareholding

in share capital are – NCCBL Mutual Fund-1 (83.81%), LR Global Bangladesh Mutual Fund

One (81.16%), AIBL 1st Islamic Mutual Fund (76.31%), MBL 1st Mutual Fund (69.03%),

Grameen Mutual Fund One (61%), EBL First Mutual Fund (60%) and Trust Bank 1st Mutual

Fund (60%). It is important to note that among the 41 mutual funds Investment Corporation of

Bangladesh (ICB) occupies 8 funds and ICB Asset Management Company Limited which is a

subsidiary of ICB, occupies 11 funds. (DSE, 2013)

From (Table 1.1), we see that the second highest institutional shareholding exists in Tannery

sector. In this sector, companies have on an average 19.44% institutional shareholding in their

share capital. In this industry segment, 80% of the companies (4 out of 5) have institutional

shareholding in their share capital. Among these tannery companies which have high

institutional shareholding are - Apex Footwear Limited (39.81%) and Apex Tannery (33%).

From (Table 1.1), we see that the third highest institutional shareholding exists in Service & Real

Estate sector. In this sector, companies have on an average 18.62% institutional shareholding in

their share capital. The company which has the highest institutional shareholding in this sector is

Samorita Hospital (32.01%).

In the Pharmaceutical sector, companies have on an average 18.26% institutional shareholding

(Table 1.1). In this sector, 92.31% companies (24 out of 26) have institutional holding in their

share capital. Companies with high institutional shareholding in this sector are - Orion Pharma

Ltd. (49.56%), AFC Agro Biotech Ltd. (48.11%), ACI Limited. (37.73%), Wata Chemicals

Limited (36.10%) and Central Pharmaceuticals Limited (29.51%).

According to (Table 1.1), considerable shareholding by the institutional shareholders also exists

in Ceramics sector. Ceramic companies have on an average 17.43% institutional shareholding in

their share capital. All the listed companies in this sector have institutional shareholding and the

highest institutional shareholding is in Fu-Wang Ceramic (29%).

Companies in the Engineering sector have on an average 16.47% institutional holding in their

share capital as per (Table 1.1). Here, 84% companies (21 out of 25) have institutional

shareholding. The top companies according to institutional shareholding are - Aftab Automobiles

8

(47.49%), Anwar Galvanizing (41.38%), National Polymer (40.15%), BSRM Steels Limited

(38.07%) and Appollo Ispat Complex Limited (33.53%).

(Table 1.1) shows that in Travel & Leisure sector, companies have average 15.44% institutional

holding in their share capital. Here, 2 companies out of 3, have institutional shareholding. The

higher institutional shareholding is in Unique Hotel & Resorts Limited (29.14%).

The listed financial institutions have average 15.26% shareholding by the institutional

shareholders (Table 1.1). In this sector, 91.30% companies (21 out of 23) have institutional

shareholding. Here, the companies with high institutional shareholding are- ICB (70.82%),

Uttara Finance (31.95%), Islamic Finance & Investment Ltd. (24.30%) and First Lease Finance

and Investment Ltd. (23.92%).

According to (Table 1.1), institutional shareholders own on an average 15.04% shares in the

companies of IT sector. In this sector, 83.33% companies (5 out of 6) have institutional holding

in their share capital. Among the IT companies, the highest institutional shareholding exists in

Aamra Technologies limited (28%).

From (Table 1.1), we see that institutional shareholders on an average own 14.89% shares in

banks. In banking sector, 86.67% companies (26 out of 30) have institutional shareholding. The

banks with highest institutional shareholding are - AB Bank Limited (54.86%), IFIC Bank

(33.91%), Bank Asia Ltd (29.21%), Pubali Bank (26.90%) and Southeast Bank (23.61%).

In the fuel & power companies average institutional shareholding is 14.24% (Table 1.1). Among

these companies 75% companies (12 out of 16) have institutional holding in share capital. In this

sector, top companies as per institutional shareholding are - Bd. Welding Electrodes (31.68%),

Summit Power Limited (29.01%) and Padma Oil Co. (25.39%).

Institutional shareholders also hold shares in the cement companies. Average shareholding by

these investors in cement companies is 14.10% (Table 1.1). Among these companies, 71.43% (5

out of 7) have institutional shareholdings. In this sector, the company which has the highest

institutional shareholding is Confidence Cement (26.50%).

In the insurance sector, 67.39% companies (31 out 46) have institutional shareholding. Average

institutional shareholding among these companies is 12.30% (Table 1.1). In this sector, top

9

companies according to institutional shareholding are - United Insurance 56.34%, National Life

Insurance (48.54%), Pragati Life Insurance Ltd. (29.75%), Northern General Insurance Company

Ltd. (27.16%), Pragati Insurance (26.83%) and Karnaphuli Insurance (26.55%).

Companies in Textile sector have an average 11.67% institutional shareholding (Table 1.1). In

this sector, 88.24% companies (30 out of 34) have institutional shareholdings. According to

institutional shareholding, top companies in this sector are - Apex Spinning & Knitting Mills

Limited (30.79%), The Dacca Dyeing & Manufacturing Co. Ltd. (23.75%), Generation Next

Fashions Limited (21.59%), Sonargaon Textiles (21.49%) and Mozaffar Hossain Spinning Mills

Ltd. (20.78%).

Among the miscellaneous companies (which are not included in any industry sector), average

shareholding by the institutions is 11.68%. Total 9 companies fall in this category. The highest

institutional shareholding among the miscellaneous companies is in Aramit (36.95%).

Average institutional shareholding is low in the companies of Food & Allied sector. The average

is only 10.90% (Table 1.1). In this sector, 77.78% companies (14 out of 18) have institutional

shareholding in their capital. According to institutional shareholding, top companies in this

sector are - National Tea (46.06%), Olympic Industries (30.31%) and Fu Wang Food (25%).

From (Table 1.1), we see that there are three sectors where companies get very low institutional

shareholding, for example, Paper & Printing, Telecommunication and Jute sectors. In Paper &

Printing sector, there is only one company and institutional shareholding in the share capital of

that company is 8.51%. In the Telecommunication sector, there are only two companies and they

have 9.25% institutional shareholding in their share capital. In the Jute sector there are there

companies but only one has institutional shareholding in its share capital. The only jute company

which has institutional shareholding in its share capital is Jute Spinners (29.36%).

1.3 Shareholdings by the Institutional Shareholders (In Different Companies)

In this section, we will discuss the portion of institutional shareholding in the companies of DSE.

In the previous section, we showed that 245 DSE listed companies out of 303 companies have

institutional shareholdings in their share capital. We have found that most of the companies (145

out of 245) have small portion of institutional shareholding which is less than or equal to 20%.

10

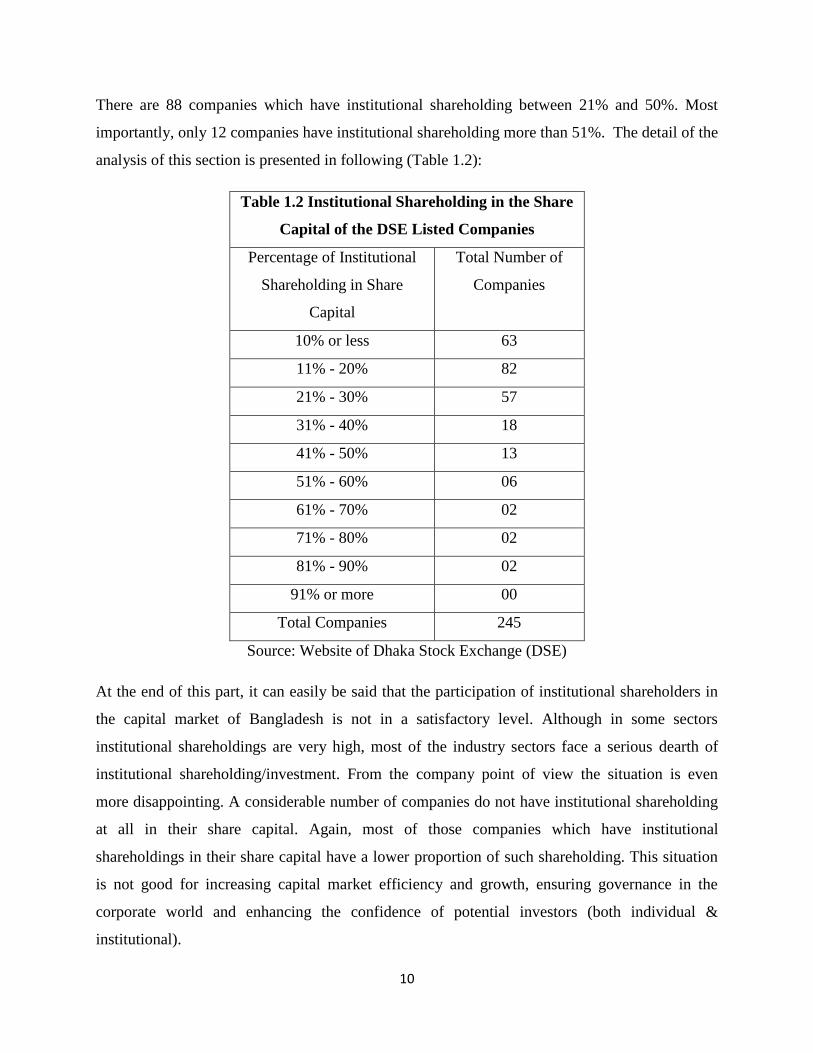

There are 88 companies which have institutional shareholding between 21% and 50%. Most

importantly, only 12 companies have institutional shareholding more than 51%. The detail of the

analysis of this section is presented in following (Table 1.2):

Table 1.2 Institutional Shareholding in the Share

Capital of the DSE Listed Companies

Percentage of Institutional

Shareholding in Share

Capital

Total Number of

Companies

10% or less 63

11% - 20% 82

21% - 30% 57

31% - 40% 18

41% - 50% 13

51% - 60% 06

61% - 70% 02

71% - 80% 02

81% - 90% 02

91% or more 00

Total Companies 245

Source: Website of Dhaka Stock Exchange (DSE)

At the end of this part, it can easily be said that the participation of institutional shareholders in

the capital market of Bangladesh is not in a satisfactory level. Although in some sectors

institutional shareholdings are very high, most of the industry sectors face a serious dearth of

institutional shareholding/investment. From the company point of view the situation is even

more disappointing. A considerable number of companies do not have institutional shareholding

at all in their share capital. Again, most of those companies which have institutional

shareholdings in their share capital have a lower proportion of such shareholding. This situation

is not good for increasing capital market efficiency and growth, ensuring governance in the

corporate world and enhancing the confidence of potential investors (both individual &

institutional).

11

PART 2

Institutional Shareholders in Bangladesh: Forms & Nature

In the capital market of Bangladesh also, shareholders can be divided into two segments –

individual shareholders and institutional shareholders. In this part of the paper, we will discuss

different types of institutional shareholders in details. The institutional shareholders in the capital

market of Bangladesh are: Investment Corporation of Bangladesh (ICB), Scheduled banks,

Merchant banks, Bangladesh Development Bank Limited (BDBL), Non-bank financial

institutions (NBFIs), Insurance companies, Leasing companies, Pension funds and provident

funds, Postal savings schemes, Postal life insurance, Co-operative land mortgage banks, Pension

and provident funds, Employees insurance funds and Security deposits. (Sayeed, 2004; Islam et

al., 2008; Mohajan et al., 2012; Azad, 2012)

2.1 Investment Corporation of Bangladesh (ICB)

Being a government-owned corporation, ICB works for building up an organized and vibrant

capital market in Bangladesh. It provides institutional assistance to the companies. As the largest

institutional investor, the corporation tries to meet up the equity gap in the enterprises. ICB

performs all its activities through the formation of three subsidiaries- the ICB Capital

Management Ltd (ICML), the ICB Asset Management Company Ltd. (IAMCL) and the ICB

Securities Trading Company Ltd. (ISTCL). Up to the end of June 2013, ICML invested Taka

4.70 billion in the investor account. Up to the end of June 2013, IAMCL has floated fifteen

mutual funds (12 closed-end and 3 open-end) and the total investment in these fifteen funds has

been stood at 30.30 billion. ISTCL has become the largest shareholder in the country with a

turnover of Taka 103.10 billion which is 10.70% of the total market turnover of both Dhaka

Stock Exchange (DSE) and Chittagong Stock Exchange (CSE) in the financial year 2012-2013.

(Bangladesh Bank 2013, p. 63-64)

2.2 Scheduled Banks

In Bangladesh, there are 56 scheduled banks which play important roles as the institutional

shareholders. The scheduled banks have significant investing activities in the capital market of

Bangladesh. Up to the end of June 2013, all the scheduled banks jointly have Taka 259.20 billion

12

investment in securities and this investment was 5.82% of total market capitalization of both

DSE and CSE. (Bangladesh Bank 2013, p. 64)

2.3 Merchant Banks

There are 51 merchant banks operating in Bangladesh. The main three functions of these banks

are- underwriting IPOs, managing new issues and providing portfolio investment management

services. These banks play very important roles as the institutional shareholders in the capital

market of Bangladesh. Total outstanding loan in the merchant banks was amounted to Taka 130

billion up to September, 2013. (Bangladesh Merchant Bankers Association, 2013; Mufazzal,

2014)

2.4 Bangladesh Development Bank Limited (BDBL)

Bangladesh Development Bank Limited also works as the institutional investor. It performs

share and security trading, operates mutual funds, underwrites public issues and provides

brokerage house services. BDBL has a subsidiary called BDBL Securities Limited (BSL) which

provides all sorts stock brokerage and dealing services. Up to the end of December 2013, the

total investment in securities by the BDBL had a market value of Taka 24.28 billion. (Islam et

al., 2008; Bangladesh Development Bank Limited 2013, p. 26)

2.5 Non-bank Financial Institutions (NBFIs)

Non-bank financial institutions are an important group of institutional shareholders in

Bangladesh. At present, there are 31 non-bank financial institutions in Bangladesh (Bangladesh

Bank 2013, p. 51). Among these 31 institutes, we have analyzed the investment portfolio of 14

financial institutions whose financial information is available. We have found that most of these

non-bank financial institutions keep major portions of their total investment in the capital market

securities. Among the 14 non-bank financial institutions, 9 kept more than 60% of their total

investment in the capital securities. Even some of them have kept 100% of their total investment

in the capital market securities. Now, (Table 2.1) in the next page shows the details of

investment in capital market securities by these 14 NBFIs:

13

Table 2.1 Investment in Shares by NBFIs

SL

No

Company Name Total

Investment

(Taka)

Total Investment

in Shares

(Taka)

% of

Investment

Made in

Shares

01 Bangladesh Industrial Finance Co.

Ltd

37,89,77,858 23,29,05,923 61.46%

02 BD Finance 582,401,228 418,007,379 71.77%

03 Delta Brac Housing Finance

Corporation Ltd.

358,102,856 266,103,356 74.31%

04 Fareast Finance & Investment

Limited

182,991,316 182,991,316 100%

05 FAS Finance & Investment Ltd 161,186,659 79,984,979 49.62%

06 CSP Finance 227,037,547 227,037,547 100%

07 IDLC Finance Ltd. 523,510,863 485,088,328 92.66%

08 IPDC Ltd 920,970,869 7 ,000,000 0.76%

09 Lanka Bangla Finance 3,515,894,297 2,023,416,003 57.55%

10 National Housing Finance &

Investment Ltd

20,582,396 20,582,396 100%

11 Phoenix Finance & Investment Ltd. 789,138,062 642,553,973 81.42%

12 Prime Finance & Investment Ltd 967,560,066 428,376,886 44.27%

13 Union Capital Ltd. 1,627,749,003 344,721,150 21.18%

14 Uttara Finance & Investment Ltd. 1,730,971,743 455,382,832 26.31%

Average investment in shares 62.95%

Source: 2012 Annual Reports of NBFIs.

2.6 Insurance Companies

Insurance companies are also an important segment of institutional shareholders in Bangladesh.

At present, there are 77 insurance companies in Bangladesh, 46 of them are non-life insurance

and 31 of them are life insurance companies. Among these 77 insurance companies 2 are state

14

owned - Sadharan Bima Corporation & Jiban Bima Corpration. (Insurance Development &

Regulatory Authority Bangladesh, 2013)

These insurance companies have huge investment in the capital market securities. In fact, capital

market securities are the main source of investment for insurance companies in Bangladesh. It

has been found in research that most of the insurance companies have kept more than 70% of

their total investment in capital securities. (Samina, 2012)

2.7 Leasing Companies

At present, leasing companies are growing in Bangladesh. There are 15 leasing operating in this

country and the money value of leasing business in Bangladesh is more than 3.16 billion

(Mohajan, 2012). These leasing companies also invest in the capital market. These companies

are also regarded as the non-institutional segment of institutional investors in the capital market

of Bangladesh. (Azad, 2012)

2.8 Pension Funds and Provident Funds

The pension and provident funds of the government employees in Bangladesh are in unfunded

condition. On the other hand, the private sector pension funds and provident funds are invested

in different sources. At present, the total monetary value of the private sector provident funds is

31,500 crore of which 15% is invested in government securities, 50% is invested in the fixed

deposits and the rest 35% is invested in the capital market securities. So, these private sector

pension funds and provident funds constitute a large group of institutional shareholders in this

country. (Uddin, 2013)

2.9 Postal Saving Schemes and Postal Life Insurance

In Bangladesh, postal department of the government plays a very important role in deposit

mobilization. At present, this department runs 6 deposit schemes. Again, this department also

runs 3 life insurance policies. A significant amount of the fund collected through these saving

schemes and insurance policies is also invested in the shares in different companies. So, postal

department in this country is also an important institutional shareholder. (Moulick et al., 2011;

Mohajan et al., 2012)

15

2.10 Co-operative Land Mortgage Banks

In Bangladesh, there are 119 co-operative banks. Among them 48 are co-operative land

mortgage banks (Board of Investment Bangladesh, 2012). These banks also play their roles as

the institutional shareholders in capital market of Bangladesh. (Mohajan et al., 2012; Azad,

2012)

2.11 Other institutional shareholders

There are some other forms of institutional shareholders in Bangladesh also. But no specific

information is available regarding these institutional shareholders. Perhaps, they have a very

negligible impact in the capital market or they do not get much attention. Some of these

institutional shareholders are:- Employee Insurance Funds, Pension Deposit Schemes, Security

Deposits and Gift Certificate Deposits, Surcharge and Development Charges. (Mohajan et al.,

2012; Azad, 2012)

In this part, we have discussed the major types of institutional shareholders in the capital market

of Bangladesh. But there are some institutional shareholders which cannot be brought under a

specific category. In many cases, the private limited companies and the listed public limited

companies (other than banks, insurance companies, financial institutions and leasing companies

etc.) buy the shares of other listed public limited companies. Here, the companies purchasing

listed shares become the institutional shareholders.

At the end of this part, it can be said that institutional shareholders in the capital market have

very different and diverse forms. But these investors have a low base in the market. Although

some of them have active participation in the capital market, others have very limited

participations. In some cases, institutional investors are reluctant to increase their investment and

participation in the capital market because of the volatility of the market. Sometimes their

participation is barred by regulations and legal proceedings. Moreover, some institutional

shareholders keep largest portion of their investment in the T-bills and in Fixed Deposits of

banks with a view to reducing investment risks.

16

Conclusion

Institutional shareholders are very important elements for the development and expansion of

capital market in a country. These shareholders supply long-term investment in market, increase

governance in the corporate sector and increase the confidence of local retail shareholders &

foreign shareholders. As a result, institutional shareholders have significant presence and

activities in most of the emerging capital market of the world. But the condition of the capital

market of Bangladesh is quite different. Here, the presence of institutional shareholders is very

limited and their activities in the capital market are also not in a satisfactory level.

In Bangladesh, there may be many reasons which discourage institutional shareholders to expand

their presence and activities in the capital market. Again, there are also some factors that obstruct

institutional shareholders to come to the capital market. The policy makers of this country should

address and resolve all these unfavorable factors and impediments. They should try to increase

the institutional shareholders‟ base in the capital market.

In our study, we have found that there are many categories of institutional shareholders in the

capital market although their participations are limited. Again, there are many potential

institutional shareholders which can be brought in the capital. These two things suggest that if

the government and regulatory bodies make the capital market attractive for the institutional

shareholders, the participation and activities of these shareholders in the capital market will

increase dramatically in the future. This chance of increasing institutional shareholders‟ base in

the capital market of Bangladesh makes us hopeful.

17

Bibliography

1) Afroz, T. (2004). Regulating Institutional Investments for Capital Market Development.

[Online]. Available at: http://saarclaw.org/expert_talk_detail.php?eid=1010. [Accessed

05 June 2014].

2) Akhter, R. and Ahmed, S. (2013). Behavioral Aspects of Individual Investors for

Investment in Bangladesh Stock Market. ISSN (P): 2308-5096, International Journal of

Ethics in Social Sciences, Vol. 1.

3) Alam, M. S. (2012). Evolution of the Bangladeshi Provident Fund and Its Investment:

Towards and Independent Trustee. University of Canberra.

4) Azad, A. K. (2012). BANGLAPEDIA: Capital Market. [Online]. Available at:

http://www.banglapedia.org/HT/C_0037.htm [Accessed 20 June 2014].

5) Banerjee, P. K., Siddique, M., Musa, M. and Chowdhury, F. (2010). Investment Climate

in Bangladesh: Enhanced Role of the Capital Market. Working paper No: 3/2010,

Investment Climate Series.

6) Bangladesh Bank. 2012-13 Annual Report.

http://www.bangladesh-bank.org/pub/annual/anreport/ar1213/index1213.php . Accessed

June 2014.

7) Bangladesh Capital Market Development Master Plan 2012-2022. [Online]. Bangladesh

Security & Exchange Commission. Available at: http://www.secbd.org/whatsnew.html.

[Accessed 05 June 2014].

8) Bangladesh Development Bank Limited. 2012 Annual Report.

http://www.bdbl.com.bd/image/pdf/BDBL%20Financial%20Report%202013.pdf .

Accessed June 2014.

9) Board of Investment Bangladesh (2013). An Overview of Financial Sector in

Bangladesh. [Online]. Available at: http://www.boi.gov.bd/index.php/investment-

climate-info/finance-and-banking#coorporative-banks . [Accessed 02 June 2014].

10) Bangladesh Merchant Bankers Association (2014). Member‟s Name [Online]. Available

at: http://www.support.solvercircle.com/list-of-merchant-banks/ . [Accessed 22 June

2014].

18

11) Banerjee, P. K. and Siddique, M. (2010). Investment Climate in Bangladesh: Enhanced

Role of the Capital Market. Working paper No: 3/2010. Investment Climate Series.

Economic Research Group.

12) Choudhury, A. H. (2013). Stock Market Crash in 2010: An Empirical Study on Retail

Investor‟s Perception in Bangladesh. ASA University Review, Vol. 7.

13) Hawladar, M. H. (2013). Lease Financing. [Online]. Available at:

http://www.ebanglapedia.com/en/article.php?id=3203#.U97fzPldWSo. [Accessed 19

June 2014].

14) ICB Securities Trading Company Limited. 2012-13 Annual Report.

http://www.istcl.com.bd/index.php?option=com_content&view=article&id=36&Itemid=

21. Accessed June 2014.

15) IDRA (2013). List of Insurance Companies in Bangladesh. [Online]. Available at:

http://www.idra.org.bd/idra-org/Ins-Com.htm . [Accessed 05 June 2014].

16) Islam, I., Khan, S. and Shahid, A. I. (2008). Bangladesh: Growth, Investment,

Opportunity. AT Capital Research. Asian Tiger Capital Partners.

17) Khaled, K. I., Chowdhury, T. M., Bari, M. A. and Kabir, N. (2011). Probe Committee

Report on Stock Market Scan, Ministry Finance, Bangladesh.

18) Malik, M. and Imam, O. M. (2007). Firm Performance and Corporate Governance

Through Ownership Structure: Evidence from Bangladesh Stock Market. International

Review of Business Research Papers Vol. 3 No.4, Pp. 88-110.

19) Moazzem, K. G. (2013). Structural and Institutional Weaknesses in the Capital Market:

The Case of Institutional Investment. Centre for Policy Director (CPD).

20) Mohajan, H.K. (2012). The Lease Financing in Bangladesh: A Satisfied Progress in

Business and Industrialization, International Journal of Finance and Policy Analysis,

4(1): 9–24.

21) Mohajan, H. K., Datta, R. and Das, A. K. (2012). EMERGING EQUITY MARKET

AND ECONOMIC DEVELOPMENT: BANGLADESH PERSPECTIVE. Int. J. Eco.

Res. v3i3, 126 - 143 ISSN: 2229-6158.

22) Moulic, M., Mukherjee, P., Rahman, S. M. and Grahan, A. N. (2011). Deposit

Assessment in Bangladesh. Internal Finance Corporation, World Bank Group.

19

23) Mufzzal, M. (2014). Merchant banks, stock brokers in dire straits. [Online]. Available at:

http://www.thefinancialexpress-bd.com/2014/05/30/36812/print. [Accessed 11 June

2014].

24) Samina, Q. S. (2012). Investment Portfolio of Insurance Companies in Bangladesh: A

Study on Selected Insurance Companies of Bangladesh. World Journal of Social

Sciences. Vol. 2. No. 7. Issue. Pp. 37 – 47.

25) Sayeed, Y. (2004). HISTORICAL IMPEDIMENTS IN DEVELOPMENT OF A DEBT

SECURITIES „MARKET‟ IN BANGLADESH. AIMS of Bangladesh Limited.

26) Uddin, A. Z. (2013). BB moves to get more pension fund in govt securities. [Online].

Available at: http://newagebd.com/detail.php?date=2013-01-18&nid=37146. [Accessed

02 June 2014].

27) Websites: Dhaka Stock Exchange. Available at: http://www.dsebd.org/.