42

1 Insurance Association of Turkey & Turkish Insurance Market 18 April 2016

| Date post: | 08-Sep-2018 |

| Category: |

Documents |

| Upload: | truongtuyen |

| View: | 231 times |

| Download: | 0 times |

1

Insurance Association of

Turkey &

Turkish Insurance Market

18 April 2016

2

Turkish Insurance Market: An

Overview

3

As of today;

37Non Life

1 Reinsurance

4 Life

19 Life and

Pension

A total of 61 companies are

actively operating

Number of Insurance Companies

4

Company employees 19.353

75.000employedMore than

Brokers 119Loss adjusters 1 305

Agents 15 587

Number of employees

5

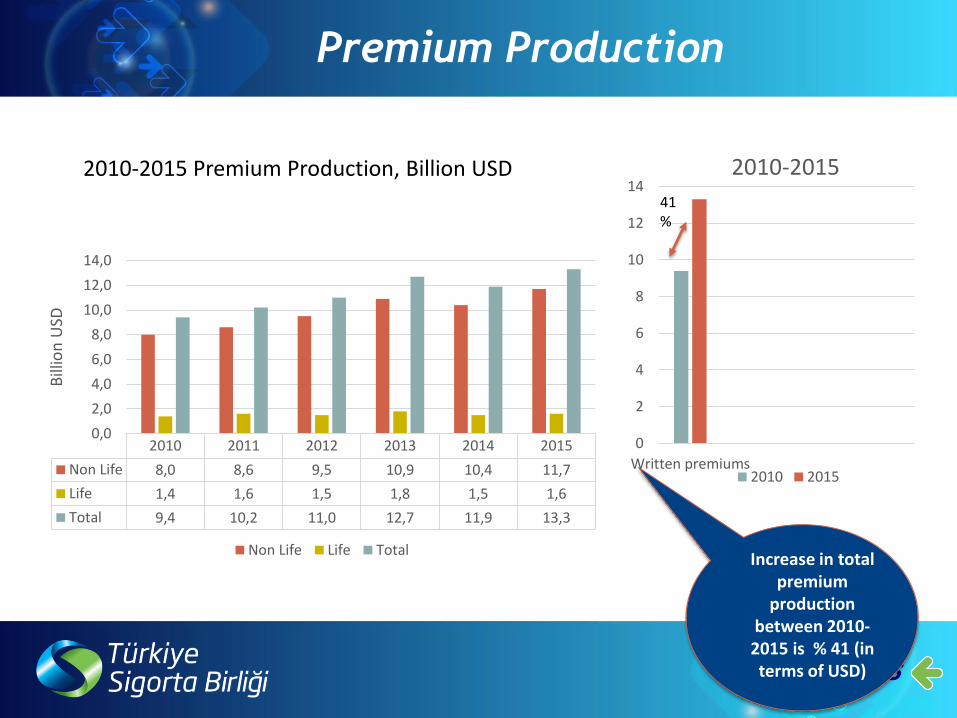

Prim Üretimi 2010 – 2015

Increase in total premium

productionbetween 2010-2015 is % 41 (in terms of USD)

Premium Production

2010 2011 2012 2013 2014 2015

Non Life 8,0 8,6 9,5 10,9 10,4 11,7

Life 1,4 1,6 1,5 1,8 1,5 1,6

Total 9,4 10,2 11,0 12,7 11,9 13,3

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

Bill

ion

USD

Non Life Life Total

0

2

4

6

8

10

12

14

Written premiums

2010-2015

2010 2015

2010-2015 Premium Production, Billion USD

41%

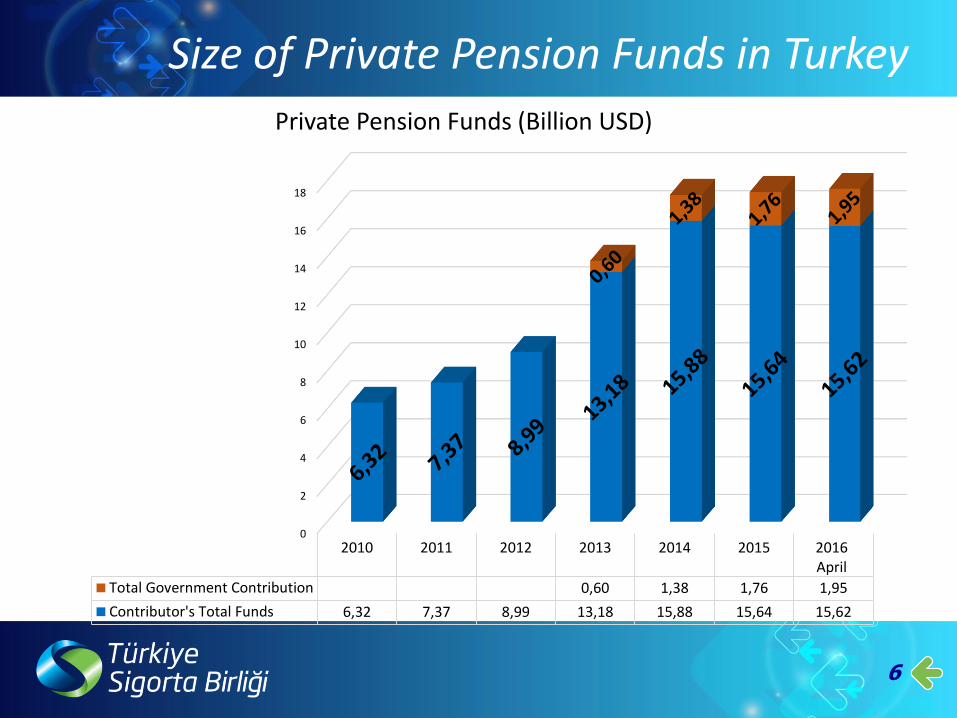

Size of Private Pension Funds in Turkey

6

0

2

4

6

8

10

12

14

16

18

2010 2011 2012 2013 2014 2015 2016April

Total Government Contribution 0,60 1,38 1,76 1,95

Contributor's Total Funds 6,32 7,37 8,99 13,18 15,88 15,64 15,62

Private Pension Funds (Billion USD)

7

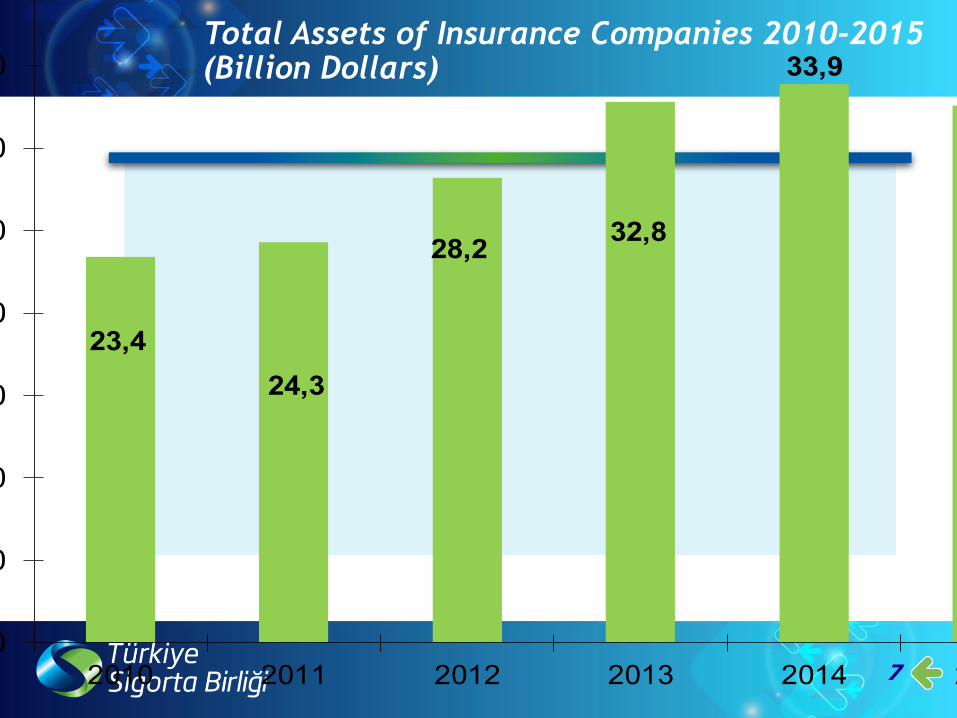

Total Assets of Insurance Companies 2010-2015 (Billion Dollars)

23,4

24,3

28,232,8

33,9

32,6

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

2010 2011 2012 2013 2014 2015

Ass

ets

(bill

ion d

olla

rs)

Assets

Assets

8

0

10

20

30

40

50

60

70

80

20102011

20122013

2014

30,739,2

49,7

62,8

76,5

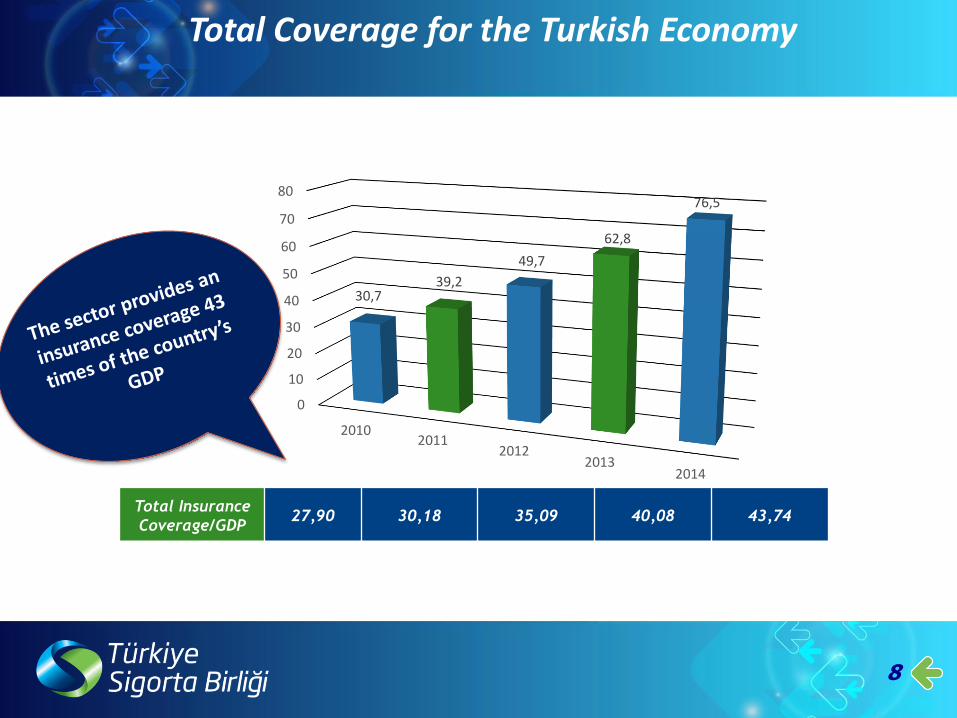

Total Insurance

Coverage/GDP27,90 30,18 35,09 40,08 43,74

Verilen Toplam Teminat Tutarı (Trilyon TL)

Total Coverage for the Turkish Economy

9

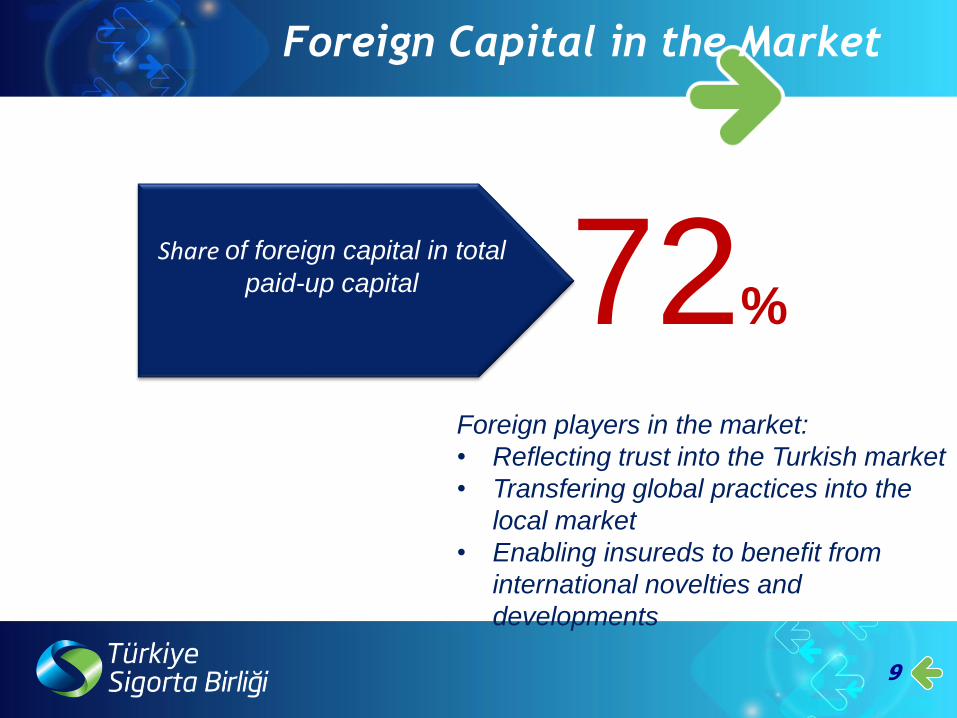

72%

Foreign players in the market:

• Reflecting trust into the Turkish market

• Transfering global practices into the

local market

• Enabling insureds to benefit from

international novelties and

developments

Foreign Capital in the Market

Share of foreign capital in total

paid-up capital

10

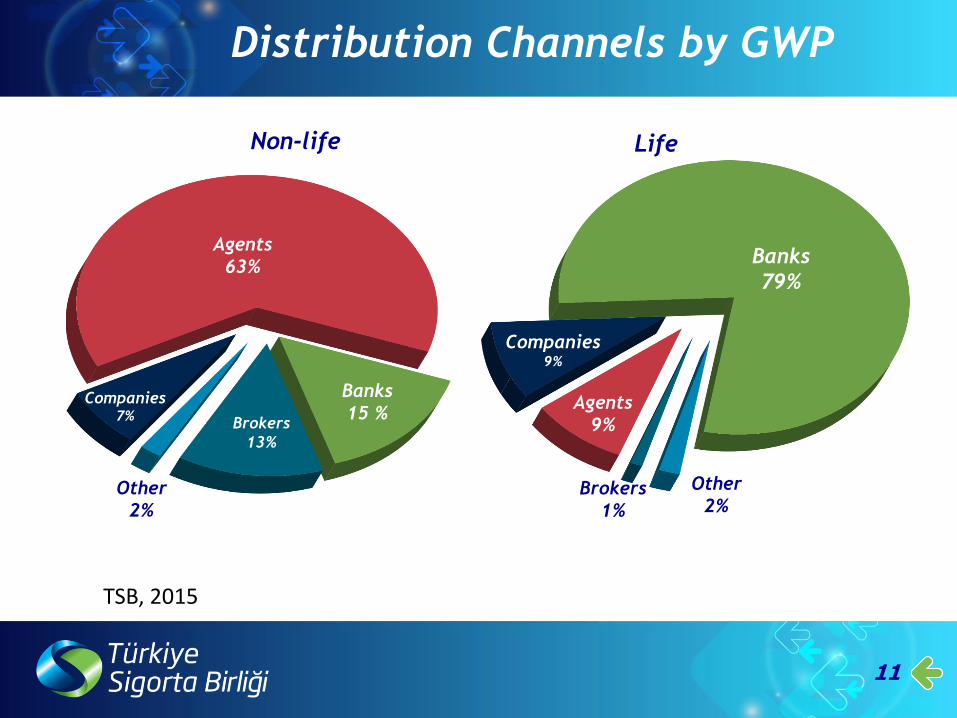

Prim Üretimi Dağılımı (2015)

ACCIDENT4% HEALTH/SICKNESS

11%

OWN DAMAGE18%

MARINE2%

FIRE/NATURAL FORCES

14%GENERAL LOSES

MTPL24%

GENERAL LIABILITY2%

OTHER3%

LlFE12%

GWP broken down by branches

TSB, 2015

11

Dağıtım Kanalları (2015)

Agents

63%

Banks

15 %Brokers

13%

Other

2%

Companies7%

Banks

79%

Brokers

1%

Other

2%

Agents

9%

Companies9%

Non-life Life

Distribution Channels by GWP

TSB, 2015

12

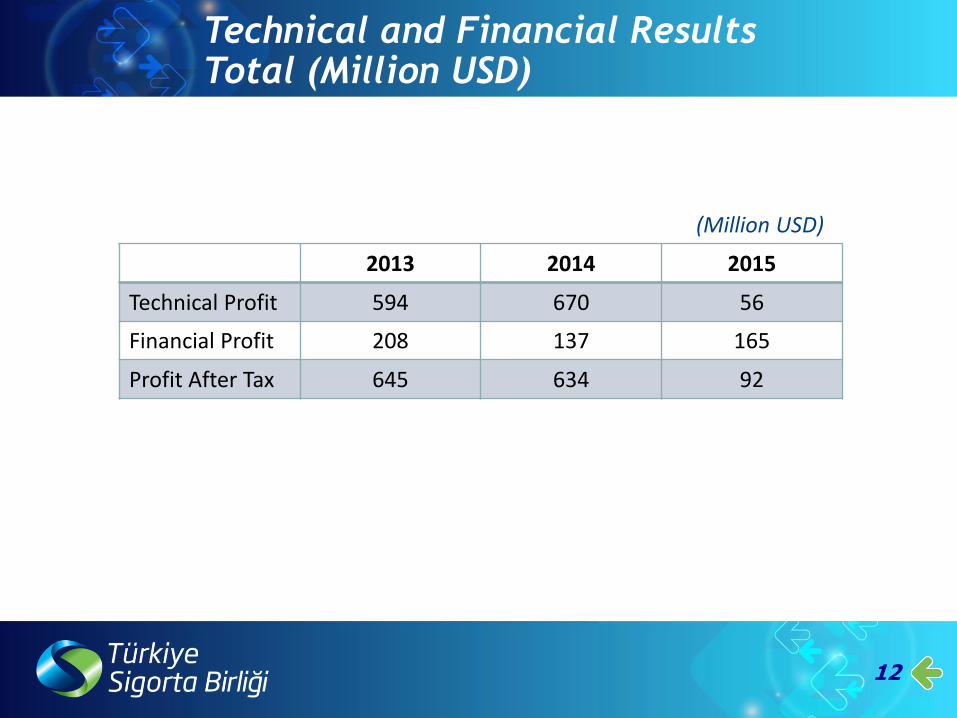

Technical and Financial ResultsTotal (Million USD)

2013 2014 2015

Technical Profit 594 670 56

Financial Profit 208 137 165

Profit After Tax 645 634 92

(Million USD)

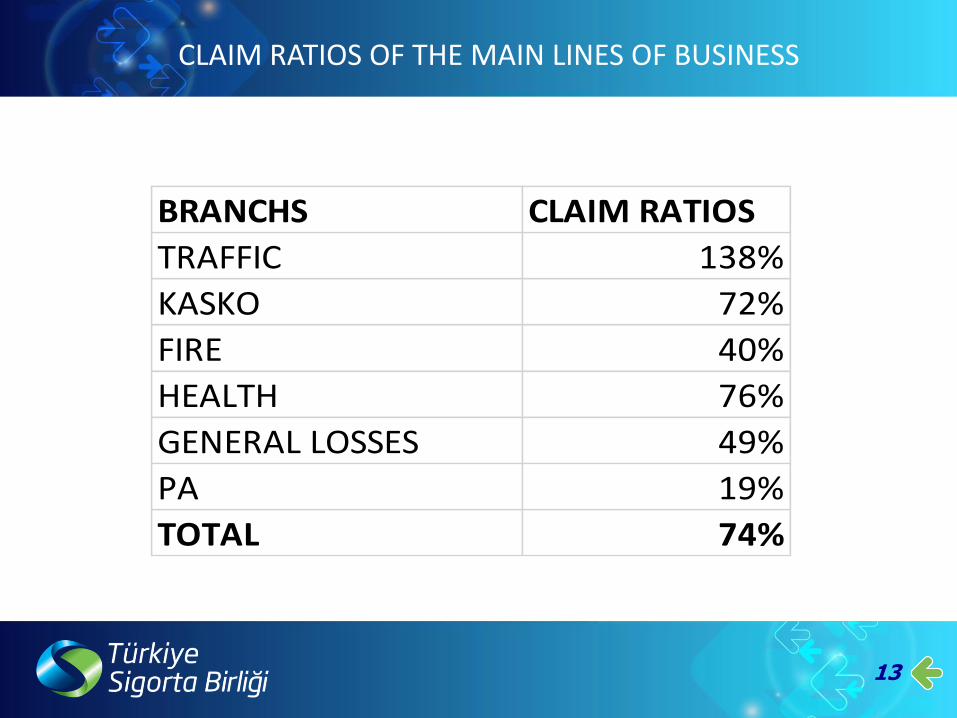

CLAIM RATIOS OF THE MAIN LINES OF BUSINESS

13

BRANCHS CLAIM RATIOS

TRAFFIC 138%

KASKO 72%

FIRE 40%

HEALTH 76%

GENERAL LOSSES 49%

PA 19%

TOTAL 74%

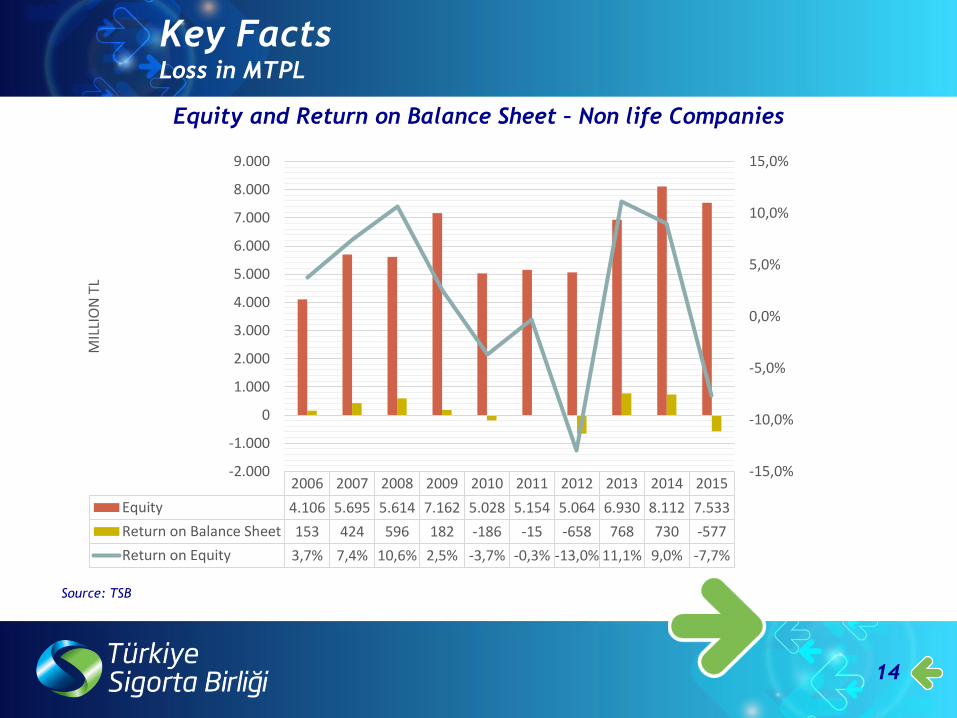

14

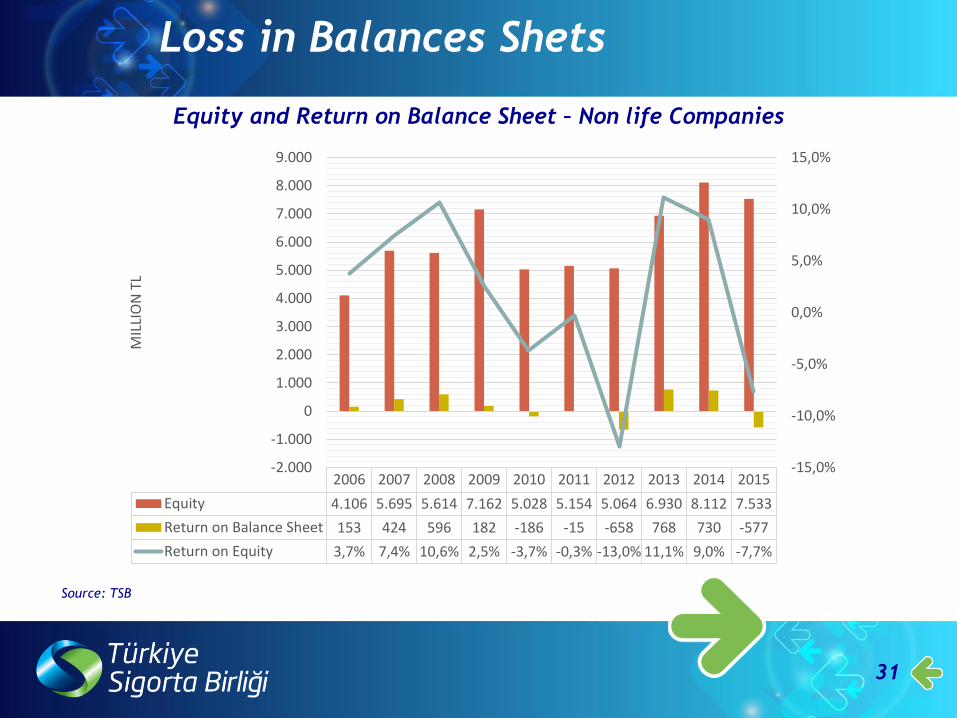

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Equity 4.106 5.695 5.614 7.162 5.028 5.154 5.064 6.930 8.112 7.533

Return on Balance Sheet 153 424 596 182 -186 -15 -658 768 730 -577

Return on Equity 3,7% 7,4% 10,6% 2,5% -3,7% -0,3% -13,0% 11,1% 9,0% -7,7%

-15,0%

-10,0%

-5,0%

0,0%

5,0%

10,0%

15,0%

-2.000

-1.000

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

MIL

LIO

NTL

Equity and Return on Balance Sheet – Non life Companies

Key FactsLoss in MTPL

Source: TSB

15

Prospects for the

Turkish Insurance

Sector:

Turkish Insurance Sector Vision

16

Vision 1

To become one of the largest insurance and privatepensions market in the region

Vision 2

To contribute to the growth of the Turkish economy andto deveoplement of the Istanbul Finance Center Project

Vision 3

To help the government to create a safety net for Turkishsociety in case of unforeseen events

SEKTÖR PRIM ÜRETIMI (MILYAR TL)

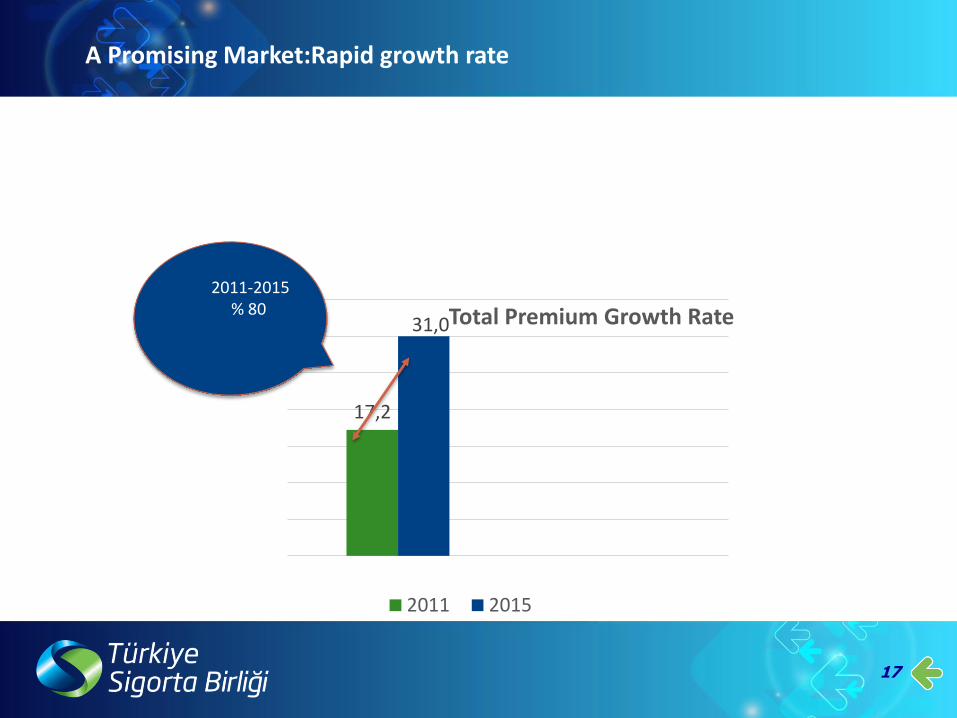

A Promising Market:Rapid growth rate

17

17,2

31,0Total Premium Growth Rate

2011 2015

2011-2015 % 80

18

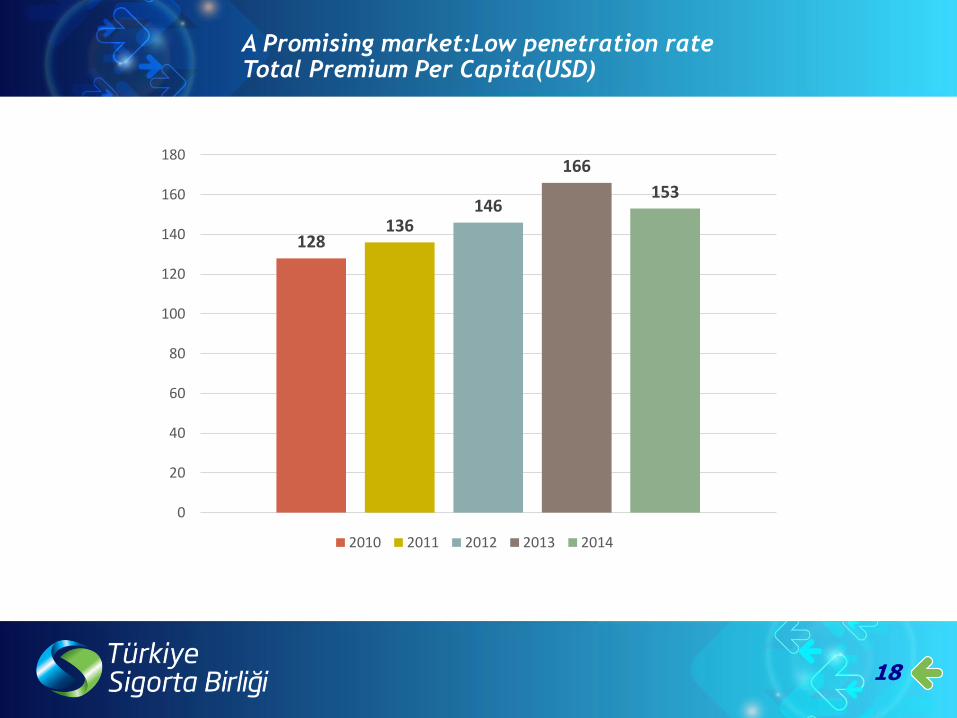

A Promising market:Low penetration rateTotal Premium Per Capita(USD)

128136

146

166

153

0

20

40

60

80

100

120

140

160

180

2010 2011 2012 2013 2014

19

Life/Non-life PER PREMIUM PRM /GDP

Developed Countries 3.666 $ 8,15%

Emerging Countries 135 $ 2,71%

World 662 $ 6,17%

Turkey 153 $ 1,4 %

Oranı – Sektörün Büyüme Potansiyeli

WORLD TURKEY

Source : SIGMA 2014

LIFE 55%

NON LIFE45%

LIFE 12%

NON-LIFE…

A Promising market:Low penetration rate

20

A Promising market:Low penetration RateOECD COUNTRIES :PRIVATE PENSIONS /GDP

Source: OECD Global Pension Statistics

4.9

36,6

Bireysel Emeklilik Sistemi Katılım Oranı – Sektörün Büyüme Potansiyeli

21

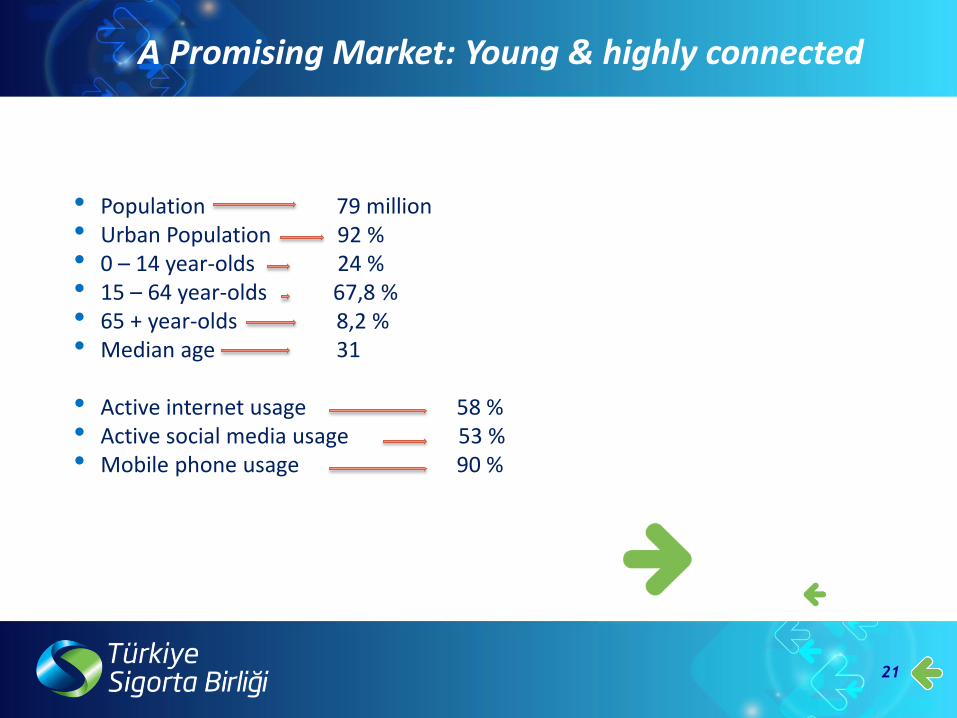

Fırsat Sunan Demografik Yapı / İletişime Açık Genç Nüfus

• Population 79 million• Urban Population 92 %• 0 – 14 year-olds 24 %• 15 – 64 year-olds 67,8 %• 65 + year-olds 8,2 %• Median age 31

• Active internet usage 58 %• Active social media usage 53 %• Mobile phone usage 90 %

A Promising Market: Young & highly connected

22

Büyük Yatırım Projeleri• In Turkey, investments realized in the past5 years totalled around 69 billion dollars

• Turkish banks and insurance companieshave undertaken financing and insuringof very large scale projects such as theThird Bridge, the Third Airport, Avrasya Tunnel, Izmir-Istanbul Highway, privatization of the facilities forgeneration and delivery of electricity

• Large scale investment projects notablyChannel Istanbul, Urban Hospitals, YHT are expected to continue

Source: The Banks Association of Turkey /Projects Finance

Statistics /June

2015

A Promising Market:

Large Scale Investment Projects

23

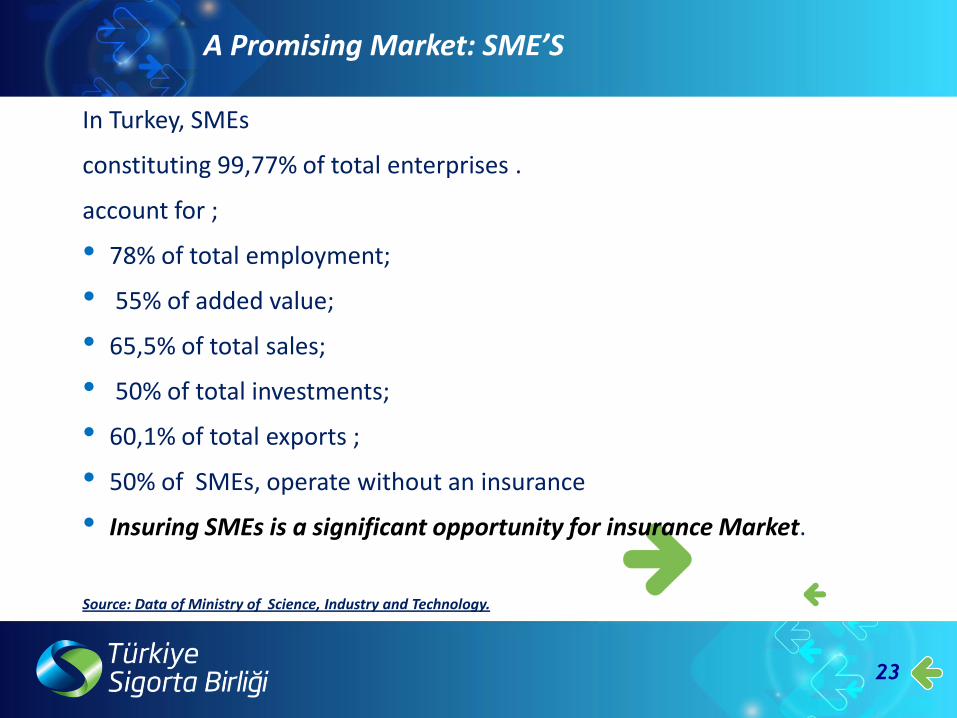

KOBİ’lerin SigortalanmasıIn Turkey, SMEs

constituting 99,77% of total enterprises .

account for ;

• 78% of total employment;

• 55% of added value;

• 65,5% of total sales;

• 50% of total investments;

• 60,1% of total exports ;

• 50% of SMEs, operate without an insurance

• Insuring SMEs is a significant opportunity for insurance Market.

Source: Data of Ministry of Science, Industry and Technology.

A Promising Market: SME’S

24

• The rules and regulations are in compliance with the EU norms and thesector is highly regulated and supervised sector.

• The authority and the association have been working together to achievecompliance with the Solvency 2 regulations

Sonuç

A Promising Market:Sound and ClearFinancials

25

Pazarlamaya Yönelik FırsatlarTurkey present a promising market with opportunities to all local and foreign investors considering these parameters.

. Insurance companies can reach out to consumers who lack insurance awarenessand to young people by using:

• Digital marketing tools

• Designing and offering tailor-made products &

• Putting customer satisfaction in the center

Market Opportunities

26

Yeni Ürünlere Yönelik FırsatlarTurkish Insurance Market continues its development with new products:

• Regulations have been enacted related to annuity products

• A model on complementary health insurance is on its way

• Legal protection insurance for employees is in the governmentprogramme in 2016

• Despite its potential, surety insurance is still a neglected branch

• Demand for products such as long term care insurance is expected torise as a result of socio-cultural changes in the society particularşyurbanisation, cultural and demographic changes

Market Opportunities

27

Motor Third Party

Liability Insurance

(MTPL)

28

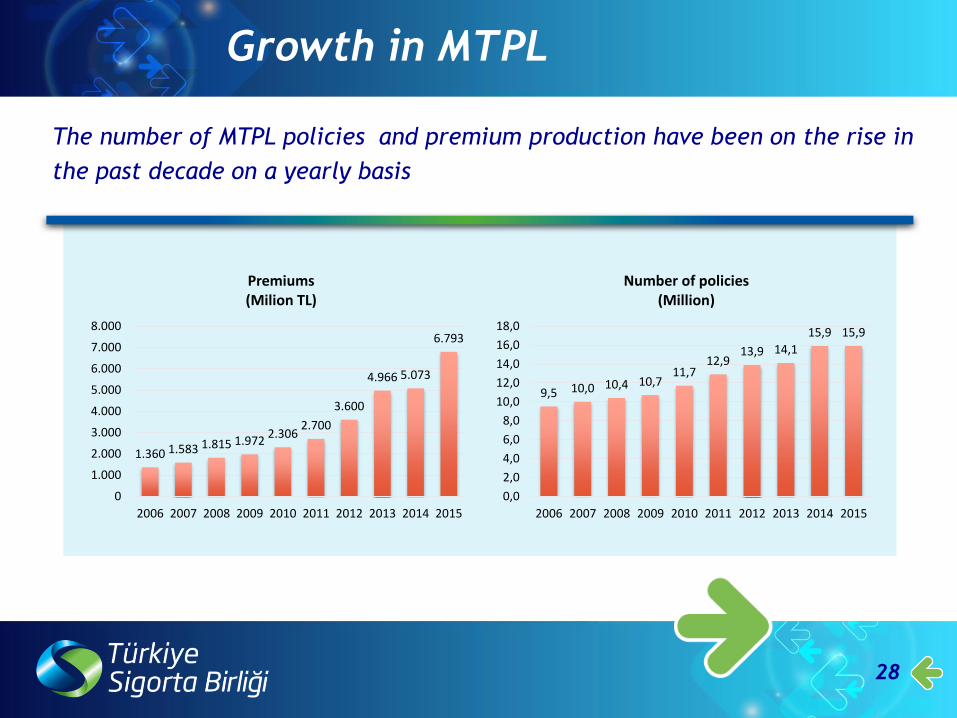

Growth in MTPL

The number of MTPL policies and premium production have been on the rise in

the past decade on a yearly basis

1.360 1.583 1.815 1.9722.306

2.700

3.600

4.966 5.073

6.793

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Premiums(Milion TL)

9,5 10,0 10,4 10,711,7

12,913,9 14,1

15,9 15,9

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Number of policies(Million)

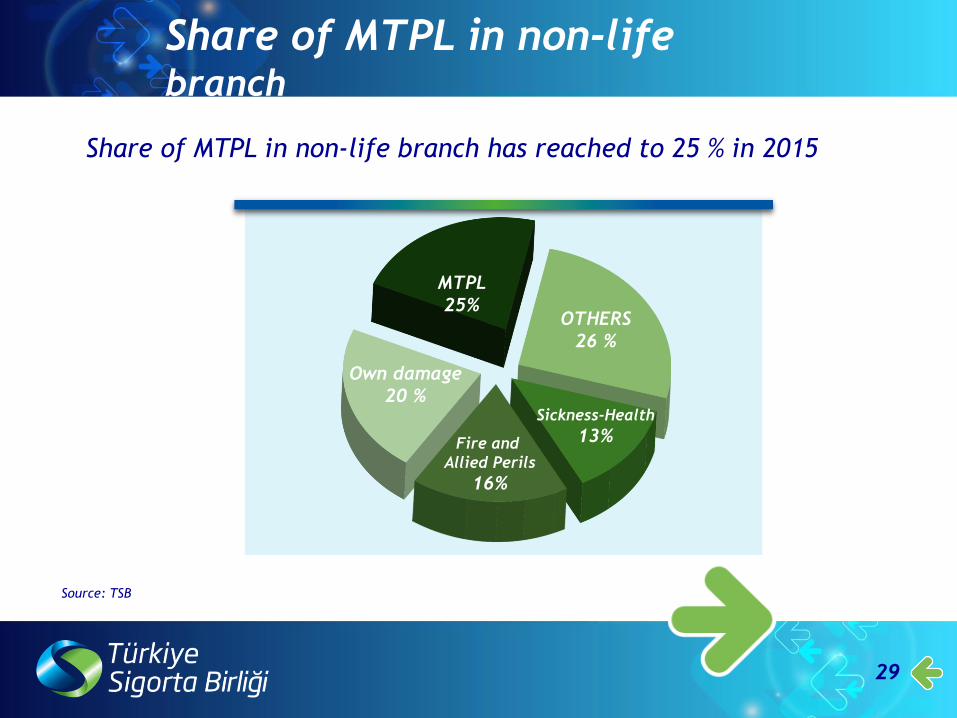

Share of MTPL in non-life branch

Share of MTPL in non-life branch has reached to 25 % in 2015

29

MTPL

25%

Own damage

20 %

OTHERS

26 %

Sickness-Health

13%Fire and

Allied Perils

16%

Source: TSB

30

Loss in MTPL

In the last decade, companies reported loss in MTPL for each and every

single period

Total amount of loss : 7 billion TL

-119 -245 -467

-296 -587 -462

-1.285

-654 -885

-2.345 -2.500

-2.000

-1.500

-1.000

-500

0

Teknik Zarar

Source: TSB

31

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Equity 4.106 5.695 5.614 7.162 5.028 5.154 5.064 6.930 8.112 7.533

Return on Balance Sheet 153 424 596 182 -186 -15 -658 768 730 -577

Return on Equity 3,7% 7,4% 10,6% 2,5% -3,7% -0,3% -13,0% 11,1% 9,0% -7,7%

-15,0%

-10,0%

-5,0%

0,0%

5,0%

10,0%

15,0%

-2.000

-1.000

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

MIL

LIO

NTL

Equity and Return on Balance Sheet – Non life Companies

Loss in Balances Shets

Source: TSB

32

Reasons for Making Loss in

MTPL

33

Reasons for Making Loss in MTPL

Coverages within the scope of MTPL are:

• Material Damage Coverage

• Health Expenses Coverage

• Permanent Disability and

• Loss of Support (Death) Coverage

Varying interpretations due to lack of clarity in the

definitions and coverages of the indemnities provided under

MTPL

Lack of a standard calculation method

Retroactive court decisions

34

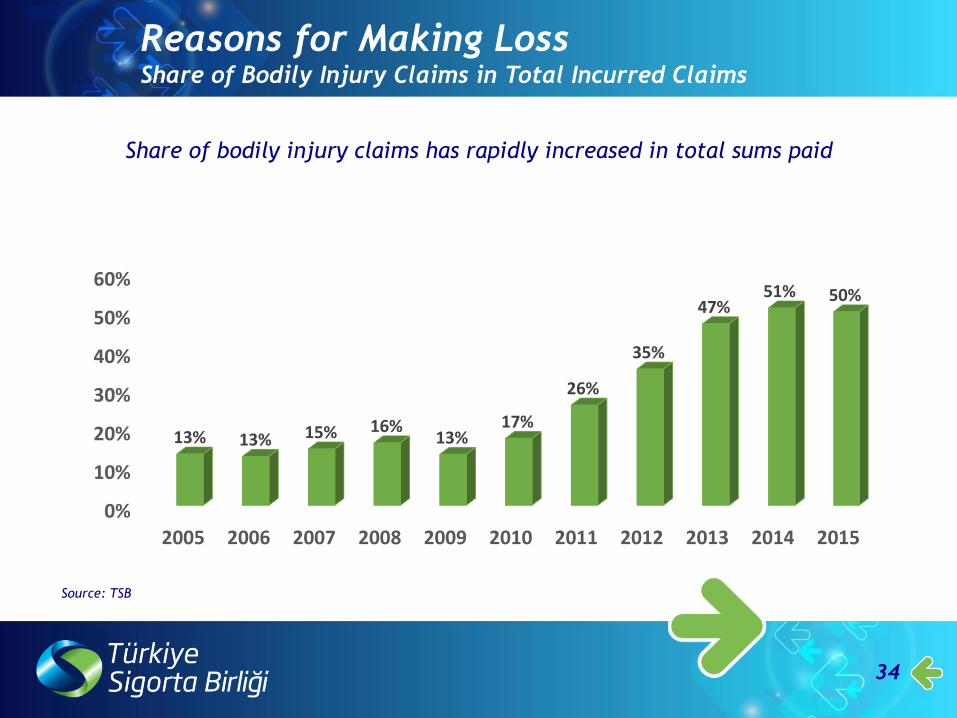

Reasons for Making LossShare of Bodily Injury Claims in Total Incurred Claims

Share of bodily injury claims has rapidly increased in total sums paid

0%

10%

20%

30%

40%

50%

60%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

13% 13% 15% 16%13%

17%

26%

35%

47%51% 50%

Source: TSB

35

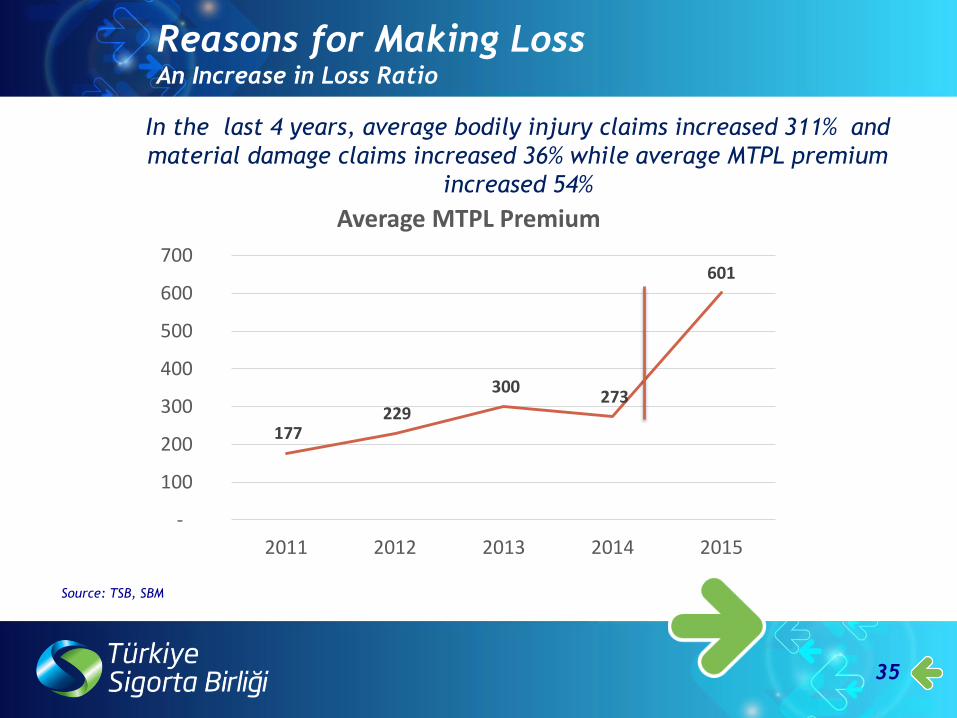

In the last 4 years, average bodily injury claims increased 311% and

material damage claims increased 36% while average MTPL premium

increased 54%

177 229

300 273

601

-

100

200

300

400

500

600

700

2011 2012 2013 2014 2015

Average MTPL Premium

Reasons for Making LossAn Increase in Loss Ratio

Source: TSB, SBM

36

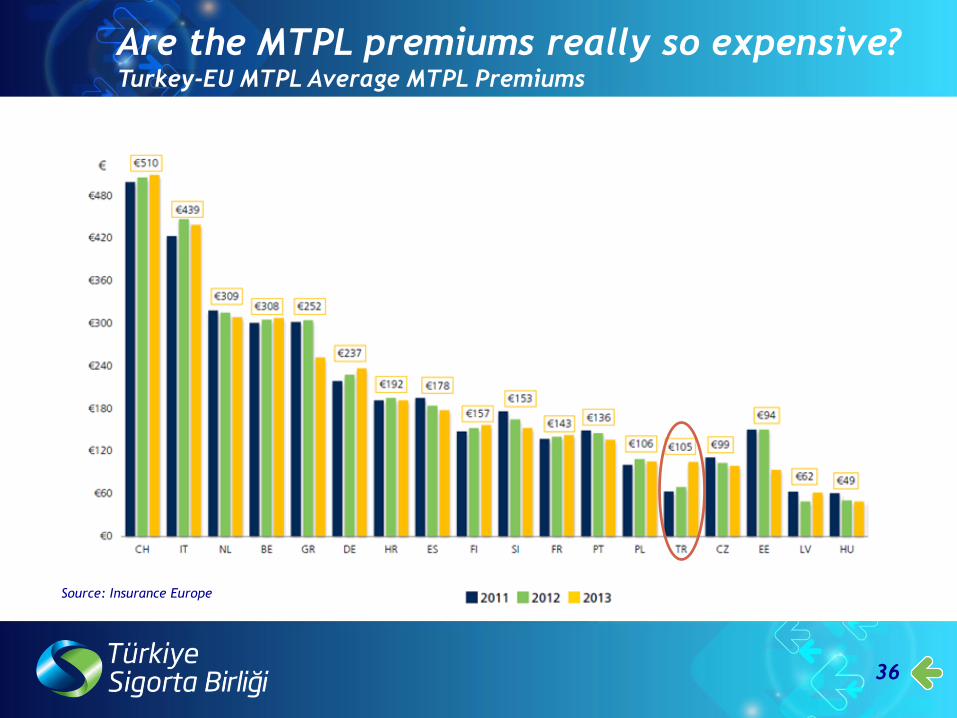

Source: Insurance Europe

Are the MTPL premiums really so expensive?Turkey-EU MTPL Average MTPL Premiums

37

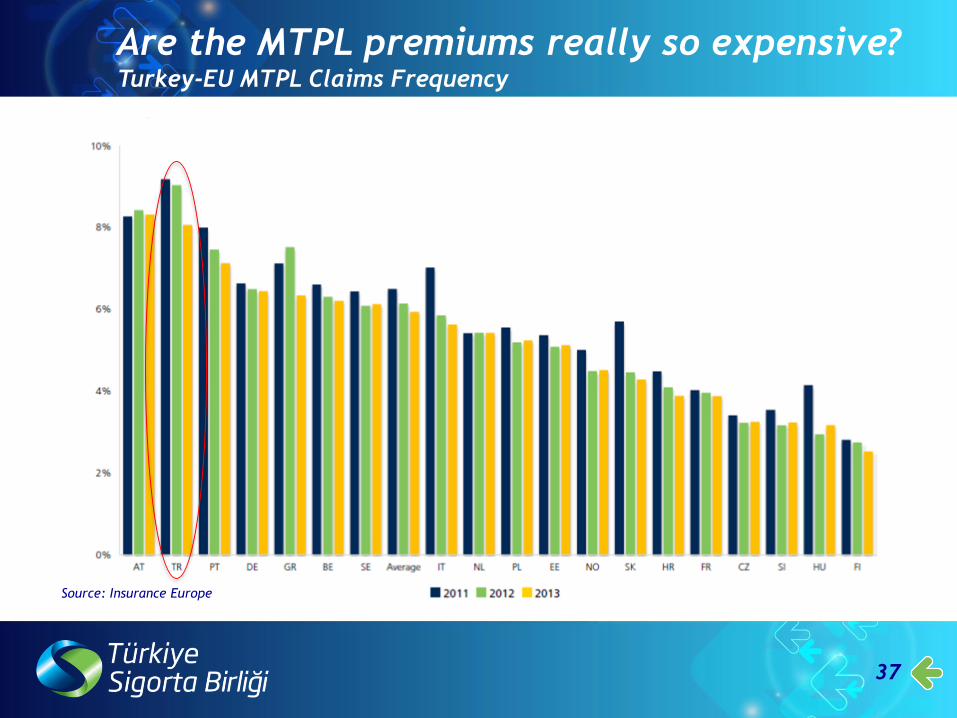

Are the MTPL premiums really so expensive?Turkey-EU MTPL Claims Frequency

Source: Insurance Europe

38

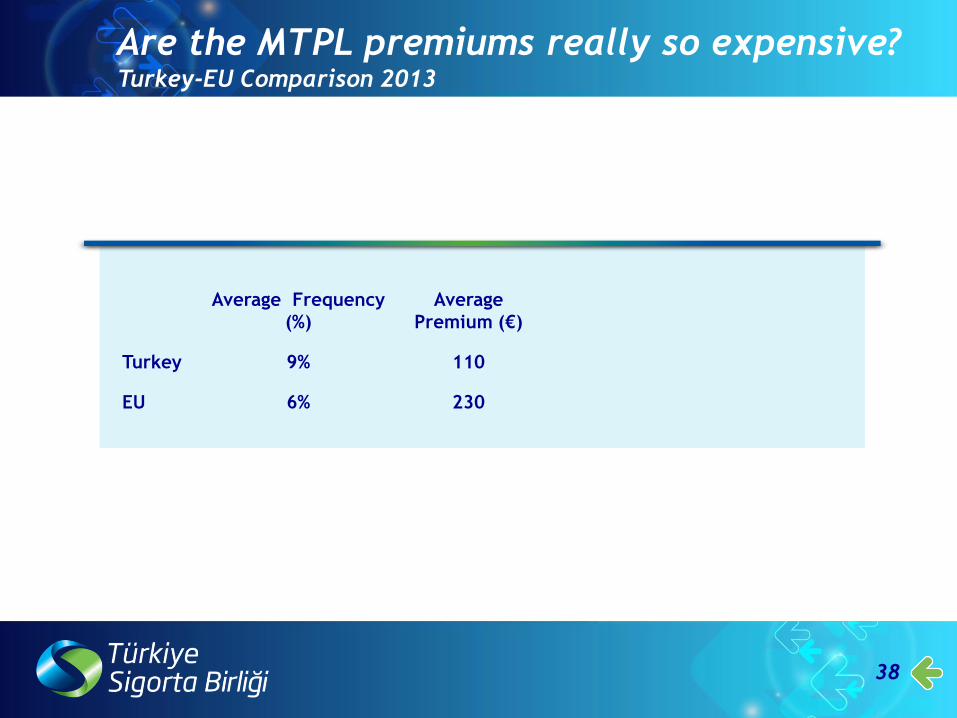

Are the MTPL premiums really so expensive?Turkey-EU Comparison 2013

Average Frequency

(%)

Average

Premium (€)

Turkey 9% 110

EU 6% 230

39

Turkey was amongst the countries with the lowest average MTPL

premiums and the highest claims frequency

Are the MTPL premiums really so expensive?Turkey-EU Comparison

• SO WHAT IS THE SOLUTION??

40

41

THE GOOD NEWS IS…

Regulatory changes needed in the Highway Traffic

Law realized Last Week in the Parliamentum,

Finally…

42

Thank you...