24

Insurance solutions for pension schemes Insurance Provider Survey July 2014

Insurance solutions forpension schemesInsurance Provider Survey

July 2014

Summary

Introduction 5

Why insure? 6

1. Insurance solutions available 7

1.1 Traditional bulk annuities 8

1.2 Longevity only 11

1.3 Medical underwriting 13

1.4 The Irish market 15

2. Structuring a deal 17

3. Characteristics of insurers 19

4. Insurers’ market outlook 21

Contact us 23

Contents

3Insurance solutions for pension schemes

Wind-up

Pricing

Reinsurance

Sovereign annuities

ReinsuranceDe-riskingLongevity

Solv

ency

IID

Bpe

nsio

nsc

hem

es

Medical underwritingWind-up

Market outlook

Medical underwritingDeferred premium

Free asset ratio

Deal structureAffordability

Dat

aBuy-in

PredictabilityCollateral

Buy

-out

Ris

k

Insu

ranc

e

Pri

cing

Market outlook

Buy-in DB pension schemes

Wind-up

Colla

tera

l

Solvency IIData

Pricing

Win

d-up

Sovereign annuities

Free

asse

tra

tio

Pre

dict

abili

ty

Free asset ratioAffordabilityIn

sura

nce

Market outlook

Deal structure

Market outlookDeferred premium

Insurance Data Sovereign annuitiesDeferred premiumWind-up Mar

ket

outl

ook

ReinsuranceAffordabilityDeal structure

CollateralPricing

Although Defined Benefit (“DB”) pension schemes are becoming rarer as a vehicle for companies to provide pensions tocurrent employees, the size of accrued benefits mean that they remain a challenge for sponsors and trustees looking tomanage the risk that they pose.The market for insured solutions has changed a huge amount over the last ten years, from the early 2000s when there werejust two providers in the UK focussing on insuring schemes in wind-up to the mid 2000s when a large number of newcompanies joined the market. Although many of these new entrants have since left the market or been consolidated, today wesee a well established market with a number of players committed to offering insured solutions as a way of de-riskingschemes.In order to assist companies and trustees who are considering insured solutions for their scheme, we conducted a survey inearly 2014 of the main insurance companies who participate in this area in the UK and the Republic of Ireland. The focus ofthis survey was on the insurers who have written business directly with pension schemes. For this reason, we have notincluded the longevity reinsurers who operate in this market.This report sets out the results of that survey and offers some insights into the market from the perspective of insurers.We would like to thank the following insurance companies for participating in the survey:► Abbey Life (and Deutsche Bank London in its capacity as a derivative solution provider)► Aviva► Just Retirement► Legal & General► Partnership► Pension Insurance Corporation► Prudential► Rothesay Life► Swiss ReIn addition to the above UK providers, two insurers who operate solely in the Republic of Ireland also participated in thesurvey.Please note that the survey results are shown on a ‘no-names’ basis. Where relevant, the insurers have been allocated areference number but this changes in the different tables.We hope that you find the report interesting and informative.

Iain BrownPartner and Head of Pensions AdvisoryJuly 2014

Insurance solutions for pension schemes 5

Introduction

For both companies and trustees, the impact of volatile pension deficits can be significant and detrimental. An increasing numberof companies and trustees are looking at options to remove or reduce pension risk. An effective way of removing risk is throughthe purchase of insurance products; there are a wide range of options offered by insurers to help companies and trustees to de-risk their pension schemes.

There are a variety of benefits in using insurance solutions for both trustees and employers:

Insurance solutions for pension schemes 6

Why insure?

Employers:► Risk reduction - Insurance solutions can be used to

remove the risks associated with DB pension liabilities,e.g. investment, longevity, inflation and interest raterisk

► Strengthened balance sheet - Depending on thestructure of the deal, the employer can transfer theresponsibility for the pension liabilities to the insurerand remove the liabilities from the company balancesheet

► Tailored risks - Specific types of risk, such as longevityrisk, can also be removed or reduced separately

► Cash cost stability - The future funding costs of aninsured pension scheme are typically much morepredictable and less volatile at future valuations.

Trustees:► Insurer covenant - Insurance generally increases

member security as an insurer covenant is typicallystronger than an employer covenant. Insurers aresubject to strict regulatory requirements and arerequired to hold a large amount of capital to covertheir liabilities

► Employer covenant - Trustees can use insurancesolutions to reduce their reliance on the sponsor andtherefore reduce the pension scheme’s exposure to adeterioration of the sponsor’s financial position

► Predictability - The steady cashflows promised byinsurers will be desirable for many trustees

► Administration costs – When schemes reach a certainmaturity, it will often be more cost effective to securethe benefits with an insurer rather than continuing torun the scheme.

The market for insurance solutions for UK pension schemes is sophisticated and constantly evolving. New products and optionsare being developed all the time and in recent years, insurers have developed a range of solutions to help pension schemes meettheir specific needs.

Figure 1.1 below shows the amount of business written during 2013 by the insurers in our survey, split between bulk annuitiesand longevity-only transactions:

Figure 1.1: Business written in 2013

Insurance solutions for pension schemes 7

Section 1 – Insurance solutionsavailable

2.8

3.7

1.4

0.4 0.3 0.2 0.1

5.0

0.3

5.0

0.1 0.010.0

1.0

2.0

3.0

4.0

5.0

6.0

Comp A Comp B Comp C Comp D Comp E Comp F Comp G Comp H Comp I Comp J

£bn

Bulk annuity Longevity-only Medical underwritten bulk annuity

EY insightIn terms of business written, the market in 2013 was relatively concentrated, with three major writers of bulk annuity businessand two of longevity only business who write directly with pension schemes. However, this hides other trends, such as thedevelopment of the medical underwriting market.

Bulk annuity insurance policies are an effective way ofremoving pension risk and can be broadly split into twocategories:

► Buy-in (or partial buy-in) – the purchase of a bulk annuitycontract that covers all or some of the pension payments.The contract is held as an asset of the scheme

► Buy-out – the purchase of a bulk annuity contract thatcovers pension payments. Members are provided withindividual annuity contracts removing the scheme’sliability to pay pensions completely

► As shown in Figure 1.2, different insurers target differentsizes of liabilities.

The providers can be thought of as falling into two broadcategories:

► Whole of market players – companies who target all sizesof liabilities

► Providers who focus on a certain segment of the market(for example larger sized deals)

The market for mid-sized deals is the most competitive withmost insurers being willing to quote for deals between £50mand £500m in liabilities.

Generally, there appears to be a competitive market for mostsizes of deal – however, it can be challenging to obtaincompetitive quotes for very small liabilities, depending on thecapacity of the insurers who quote at those levels. Someinsurers set minimum levels for liabilities and would onlyconsider any deals above the minimum level.

The size of liabilities that an insurer will be willing to takeoften varies and depends on a variety of commercial andeconomic factors.

Insurance solutions for pension schemes 8

1.1 Traditional bulk annuities

Figure 1.2: What size of scheme liabilities are you prepared to write a (traditional) bulk annuity contract for?

4

5

7

8

6

0

1

2

3

4

5

6

7

8

9

Less than £20m £20m - £50m £50m - £100m £100m - £500m Greater than £500m

Num

ber

ofre

spon

ses

Size of liabilities

EY InsightWhen considering a bulk annuity transaction, it is vital tounderstand the insurers who operate in the market, the sizeof liabilities they target and the solutions they offer.

The majority of providers adopt a flexible approach to meet the specific needs of the client in order to help them achieve anoptimal solution for their pension scheme. The table below shows some of the wide range of options offered by insurers for bulkannuity contracts, along with some issues to consider:

Insurance solutions for pension schemes 9

1.1 Traditional bulk annuities (cont’d)

Option What is it? Benefits/issues to consider

Deferred premiums Option to fully insure members’ benefits but part of thepremium will be payable over a specified future period tomeet the employer/scheme’s requirements.

This allows the employer/scheme to remove risk/volatilityand lock into pricing at attractive market conditions. Further,companies can defer payments until they become moreaffordable and have more certainty over futurecontributions. This can also be structured to tie in with anexisting Recovery Plan.

Delayed pensionpayments

The trustees continue to make pension payments untilthe insurer takes over, i.e., delayed pension paymentsfrom insurer. The trustees decide on when the insurerstarts making payments. Employer support will berequired in the period where the scheme continues tomake pension payments.

This is a useful option for underfunded schemes; the laterthe insurer starts making payments, the lower the cost of theinsurance. Insurers are likely to offer this option to schemeswhere the employer is unlikely to become insolvent duringthe period where the scheme makes payments.

Exclude cover fordeflation risk

Schemes insuring pension benefits typically protectagainst deflation risk, which arises when schemes areunable to reduce inflation-linked pensions when inflationis negative.

Insuring for deflation risk can be expensive due to a lack ofliquidity in the swap markets and insurers in our survey havenoted that excluding deflation pricing could reduce pricing bya reasonable amount (depending on the period that cover isexcluded).

Full risk transfer Insurer takes on full responsibility for all pension schemerisks including data issues, GMP reconciliation, GMPequalisation, etc.

Schemes should consider the state of their data anddetermine whether the additional premium payable for thisoption is worthwhile.

Future accrual foractive members

Transaction where the ongoing accrual of liabilities foractive members is insured.

The insurer is unlikely to accept the risk of the employerpaying higher than expected salary increases.

Salary linkage fordeferred members

Transaction where salary linkage for deferred membersis insured.

The insurers in our survey generally did not offer this option.

Profit sharing Insurer makes payments to the trustees/sponsor if theexperience under the contract is better than assumed inthe insurer’s pricing.

This is a relatively unusual feature of transactions, thoughcertain insurers may consider it on a case by case basis.

Progressive/stagedrisk transfer

A transaction completed in pre-determined stages,where liabilities are transferred across from scheme toinsurer (possibly according price or funding relatedtrigger points).

This allows the employer/scheme to manage the workinvolved in such exercises in stages and also to transactwhen conditions are favourable.

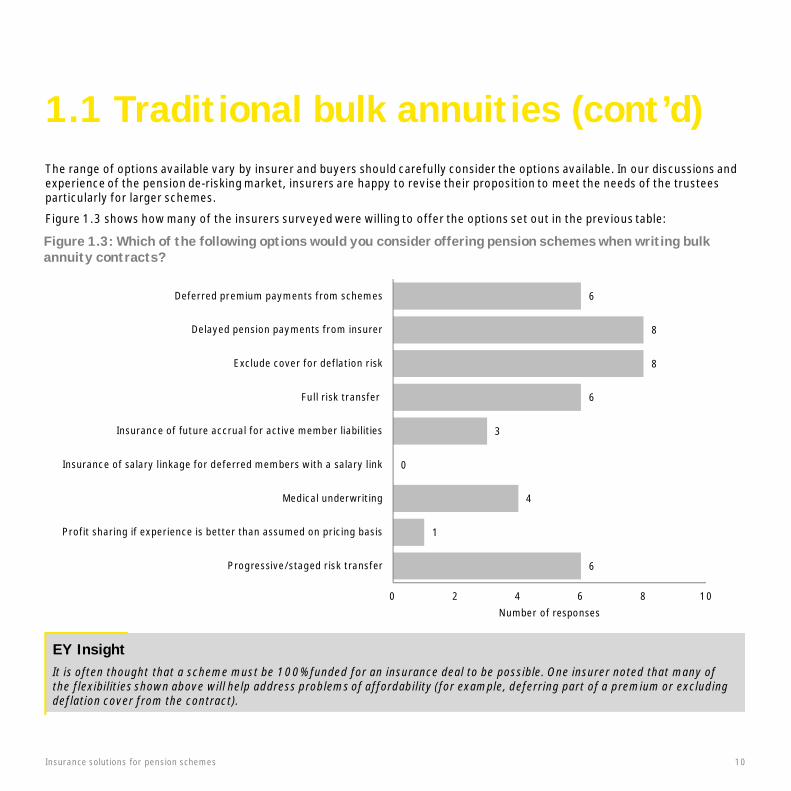

The range of options available vary by insurer and buyers should carefully consider the options available. In our discussions andexperience of the pension de-risking market, insurers are happy to revise their proposition to meet the needs of the trusteesparticularly for larger schemes.

Figure 1.3 shows how many of the insurers surveyed were willing to offer the options set out in the previous table:

Insurance solutions for pension schemes 10

1.1 Traditional bulk annuities (cont’d)

Figure 1.3: Which of the following options would you consider offering pension schemes when writing bulkannuity contracts?

6

1

4

0

3

6

8

8

6

Progressive/staged risk transfer

Profit sharing if experience is better than assumed on pricing basis

Medical underwriting

Insurance of salary linkage for deferred members with a salary link

Insurance of future accrual for active member liabilities

Full risk transfer

Exclude cover for deflation risk

Delayed pension payments from insurer

Deferred premium payments from schemes

0 2 4 6 8 10Number of responses

EY InsightIt is often thought that a scheme must be 100% funded for an insurance deal to be possible. One insurer noted that many ofthe flexibilities shown above will help address problems of affordability (for example, deferring part of a premium or excludingdeflation cover from the contract).

What is it?Longevity only transactions (often referred to as ‘longevityswaps’) can be used to transfer the risk of scheme membersliving longer than expected to a counter-party (generally aninsurer or bank). Typically, under a longevity swap:► The pension scheme agrees to pay a fixed series of

payments based on the expected benefits, including amargin to the counter-party for covering this risk

► The counter-party agrees to make payments based on theactual mortality experience

The first longevity swap in the UK was carried out in 2009.Since then, several dozen deals have been completed and thereare several providers who have shown an interest in writingbusiness in this area.Figure 1.4 shows that there are potentially up to five providerswho will write longevity only transactions. It should be noted atthis point that we have only considered providers who havewritten longevity only business directly with pension schemes.We are aware that there are several more reinsurers who arewilling to ultimately accept this longevity risk from schemes,but via a traditional insurer. We’re also aware of at least onereinsurer that is establishing a direct insurer for this purpose.In a recent longevity transaction, one insurer reinsured itspension scheme using its own life company as the directinsurer. Although more complicated, this route would be opento other companies if they are prepared to set up a captiveinsurer to act as the direct writer.

Deal sizeThe chart below shows the minimum size of liabilities thatinsurers would be willing to cover as part of a longevity onlytransaction.

As can be seen from Figure 1.5, providers still target largerliabilities (typically over £500m). Generally, deals for largerliabilities have been completed on a ‘named life’ basis (i.e., theprovider is insuring the longevity risk of the actual schemepopulation).

However there is a push from some insurers to offer longevityswaps to smaller schemes. For example, one provider hasdeveloped an index-based solution specifically to targetsmaller schemes.

Insurance solutions for pension schemes 11

1.2 Longevity onlyEY InsightAlthough longevity only transactions have generally beenrestricted to larger schemes so far, one insurer noted that akey business objective was to take longevity insurance to amuch wider range of schemes.

4

6

1

Yes

No

In certaincircumstances

0 2 4 6 8Number of responses

1

1

3

0 1 2 3 4

£50m

£300m

£500m+

Number of responses

Figure 1.4: Do you offer longevity only deals?

Figure 1.5: For named-life longevity only deals, whatis the minimum size of liabilities you would beprepared to transact on?

The willingness to cover deferred liabilities ultimately dependson the terms offered by reinsurers. Generally, deferredliabilities will be more expensive to cover than pensionerliabilities, although this will depend on age – for example it’spossible that older deferred pensioners (near or at retirementage) may be available at a similar price to current pensioners.

One of the perceived drawbacks to longevity swaps is that itcan be difficult to buyout the scheme once longevityinsurance is in place. However, most of the insurers surveyedsaid that they would consider insuring a scheme (through abuy-in or buy-out) that already had longevity insurance inplace - see Figure 1.8.

Exactly how this would be done would depend on the specificcircumstances of the scheme but is most likely to involvenovation of the existing longevity swap to the new insurer.

Deal structureLongevity only transactions can be structured in the followingways:

► Insurance contract – insurance regulations and capitalrequirements apply for these contracts. Most of thelongevity risk is passed onto the reinsurance market

► Derivative contract – banking regulations and ISDArequirements apply for these contracts. In addition tobeing reinsured, longevity risk can also be passed on tocapital market investors

Figure 1.6 shows that most providers will only structure alongevity swap as an insurance contract, although oneprovider is currently willing to offer this as a derivativecontract.

Almost all of the longevity swaps that have been completed sofar have covered current pensioner liabilities only. However,some providers are willing to cover deferred pensionerliabilities too (at least under certain conditions) –see Figure 1.7.

Insurance solutions for pension schemes 12

1.2 Longevity only (cont’d)

5

1

0 1 2 3 4 5 6

Insurance contract

Derivative contract

Number of responses

Figure 1.6: How would you structure the contractfor a longevity only deal?

Figure 1.7: Would you cover deferred pensionerliabilities as part of a longevity-only deal?

Figure 1.8: Would you consider writing a buy-in orbuyout contract for a scheme that already hadlongevity insurance in place?

1

1

3

0 1 2 3 4

Yes

No

In certaincircumstances

Number of responses

4

1

4

0 1 2 3 4 5

Yes

No

In certaincircumstances

Number of responses

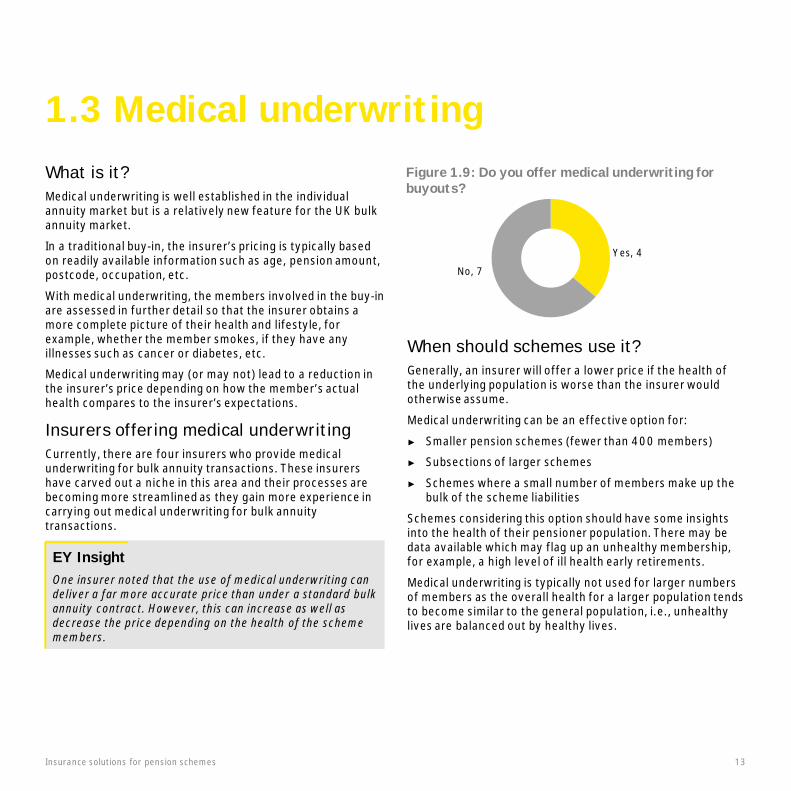

What is it?Medical underwriting is well established in the individualannuity market but is a relatively new feature for the UK bulkannuity market.

In a traditional buy-in, the insurer’s pricing is typically basedon readily available information such as age, pension amount,postcode, occupation, etc.

With medical underwriting, the members involved in the buy-inare assessed in further detail so that the insurer obtains amore complete picture of their health and lifestyle, forexample, whether the member smokes, if they have anyillnesses such as cancer or diabetes, etc.

Medical underwriting may (or may not) lead to a reduction inthe insurer’s price depending on how the member’s actualhealth compares to the insurer’s expectations.

Insurers offering medical underwritingCurrently, there are four insurers who provide medicalunderwriting for bulk annuity transactions. These insurershave carved out a niche in this area and their processes arebecoming more streamlined as they gain more experience incarrying out medical underwriting for bulk annuitytransactions.

When should schemes use it?Generally, an insurer will offer a lower price if the health ofthe underlying population is worse than the insurer wouldotherwise assume.

Medical underwriting can be an effective option for:

► Smaller pension schemes (fewer than 400 members)

► Subsections of larger schemes

► Schemes where a small number of members make up thebulk of the scheme liabilities

Schemes considering this option should have some insightsinto the health of their pensioner population. There may bedata available which may flag up an unhealthy membership,for example, a high level of ill health early retirements.

Medical underwriting is typically not used for larger numbersof members as the overall health for a larger population tendsto become similar to the general population, i.e., unhealthylives are balanced out by healthy lives.

Insurance solutions for pension schemes 13

1.3 Medical underwriting

EY InsightOne insurer noted that the use of medical underwriting candeliver a far more accurate price than under a standard bulkannuity contract. However, this can increase as well asdecrease the price depending on the health of the schememembers.

Figure 1.9: Do you offer medical underwriting forbuyouts?

Yes, 4

No, 7

Data collectionThere are different approaches to collecting the data formedical underwriting:► Telephone interview with scheme members► Questionnaire sent to members► GP’s report on health of membersSome combination of the above may also be used (forexample, a questionnaire followed by a GP’s report wherefurther information is deemed necessary). Whilst differentinsurers in this sector have different approaches, it is alsopossible to agree a consistent method where more than onequotation is being sought.

Further considerationsInsurers have noted that the average cost can decrease whenmedical underwriting is used. However, it could increase theprice if the membership is healthier than expected. Further,once a scheme has received a medically underwrittenquotation (even if it does not transact), this will need to bedisclosed to any future insurer approached for a quotation.Most insurers in our survey noted that they would insure orconsider insuring schemes that have previously insured someof their membership via a medically underwritten buy-in, asshown in Figure 1.10. However, use of such insurance, oreven obtaining such quotes, can constrain the ability to insurethe remaining liabilities.The impact on price is likely to depend on the specificcharacteristics of the liabilities that had previously beenmedically underwritten.

In addition, most insurers would also insure or considerinsuring schemes that received a medically underwrittenquote but had not transacted. See Figure 1.11.

In the cases where insurers are willing to insure a scheme thathas previously received a quotation on a medicallyunderwritten basis, this is likely to be reflected in a higherpremium or at the very least greater due diligence by theinsurer.

Insurance solutions for pension schemes 14

1.3 Medical underwriting (cont’d)

EY InsightBased on the survey responses, having a previous medicallyunderwritten quote will not necessarily make it impossibleto later seek a standard annuity quotation. However, wewould suggest that trustees/companies considering medicalunderwriting should initially have a reason to believe thatthis approach will be beneficial.

Figure 1.10: Would you insure a scheme that hadpreviously transacted on a medically underwrittenbuy-in?

Figure 1.11: Would you insure a scheme that hadpreviously received a medically underwritten buy-inquote, but had not transacted?

Yes, 3

No, 3

In certaincircumstances,

4

Yes, 4

No, 2

In certaincircumstances,

4

Two of the insurers surveyed operate solely in the Republic ofIreland.

Much like the UK, the Irish bulk annuity market has evolvedfrom being almost entirely focussed on securing benefits forschemes in wind-up to also being used by trustees/sponsorsto de-risk their schemes.

Whilst the market for insurance solutions in Ireland is smallerrelative to the UK, it has experienced significant growth overthe last couple of years and business levels are expected toremain high into 2015 as shown below in Figure 1.12.

Our survey showed that the two insurers were both open toinsuring liabilities of most sizes within the Irish market asshown in Figure 1.13.

Insurance solutions for pension schemes 15

1.4 The Irish market

A different market compared to the UK?There are some differences between the UK and Irishmarkets.

Some of these differences arise from the fact that the twocountries have different legislative frameworks. For example,there is no equivalent to the UK debt on employer regulationsin Ireland. For this reason, companies in Ireland who chooseto insure benefits arguably have more scope to restructurethe benefits than their counterparts in the UK do. This has ledto the innovation of products such as sovereign annuities(explained below) that do not exist in the UK.

In addition, a scheme that is winding up can require deferredpensioners to take cash transfer values, rather than having tosecure these benefits with an insurer as would generally bethe case in the UK.

Despite these differences, insurers may find opportunities toapply UK developed solutions to the Irish market.

EY InsightAlthough smaller than the UK, the Irish market has grownsignificantly and is expected to continue to do so.

2 2 2

1

0

1

2

3

Less than€25m

€20m - €100m €100m -€500m

Greater than€500m

Num

ber

ofre

spon

ses

Size of liabilities

Figure 1.12: Expected size of bulk annuity market inRepublic of Ireland

Figure 1.13: What size of scheme liabilities are youprepared to write a bulk annuity contract for?(Irish responses only)

0.4 0.4

0.0

0.1

0.2

0.3

0.4

2014 2015

£bn

Bulk annuity

Sovereign annuitiesOne key difference between the UK and Irish markets is thatlegislation recently introduced in Ireland permits the use of‘sovereign annuities’ by occupational pension schemes.

Sovereign annuities are a form of bulk annuity where thepayments are linked to the performance of specifiedgovernment bonds. For example, in the case of a default bythe government on its bond, this would be reflected in thepayments made by the sovereign annuity too.

Both insurers surveyed in Ireland offer sovereign annuities.For this purpose, the sovereign annuities are linked to ‘IrishAmortising Bonds’ issued specifically for this purpose by theNational Treasury Management Agency (NTMA)

Due to the nature of sovereign annuities, a discount againststandard pricing is typically available. This could be up toaround 5-7% based on current conditions. It is worth notingthat at points during 2013, a larger discount against standardpricing was available. This was one reason why the majority ofthe business written in 2013 was done via sovereignannuities.

Due to this discount, often a higher proportion of a scheme’sbenefits can be insured than would otherwise be the case.Sovereign annuities can also be used to restructure thebenefits of a scheme.

Longevity only in IrelandAlthough longevity swaps are possible in principle, theinsurers surveyed indicated that pension schemes in Irelandwere generally too small to support a longevity-only marketsimilar to that which exists in the UK.

One insurer noted that they would consider writing a longevityswap but only if the liabilities were at least €1bn. There arevery few schemes of this size in Ireland.

Further, an insurer noted that there was a lack of publishedmortality data for Irish annuitants, and that additional datawould be helpful in developing this market.

Scheme funding considerationsIn March 2014, the Pensions Authority issued revisedguidance on scheme funding for Irish schemes. The new rules,which will require underfunded schemes to take definiteactions to address ongoing deficits, may force more sponsorsand trustees to look at the full wind-up option.

We expect this change will increase the demand for buy-outsof pensioner liabilities.

Insurance solutions for pension schemes 16

1.4 The Irish market (cont’d)

EY InsightA large proportion of the bulk annuity business written inIreland is done via sovereign annuities. These offer schemesand companies additional flexibility when consideringinsured solutions.

This section sets out some issues to consider whenstructuring a deal.

CPI-linked benefitsAs a result of UK government announcements in 2010,many pension schemes switched from Retail Price Index(RPI) inflation to Consumer Price Index (CPI) inflation for thepurposes of statutory minimum pension increases in paymentand deferment. Given the lack of CPI-linked financialinstruments in the market, there is the perception that CPI-linked benefits are difficult to insure.In practice, the majority of insurers are willing to coverbenefits linked to CPI inflation. However, whilst a margin ofRPI-1% might typically be used by schemes/sponsors forfunding/accounting purposes, insurance is very unlikely to beavailable at this level.Insurers indicated that a margin of 0.2%-0.5% against RPImight typically be reflected in pricing. The margin will varybased on insurer and the price at which they are able to hedgethe risk themselves.It is common for schemes taking out buy-in contracts toconvert CPI linked benefits to RPI or fixed benefits wherepossible or simply to take out an RPI-linked contract with theoption to convert at some point in the future.

Pricing movementsOnce a deal has been agreed in principle, different insurersuse different methods for updating the price to allow forchanges in market conditions before deal completion. SeeFigure 2.1 opposite. The different approaches include linkingthe price to:► A specific agreed index or formula► A portfolio of gilts or swaps (which the scheme can also

hold to immunise itself against adverse pricingmovements)

► The price of the assets the insurer will use to back theliabilities

Asset transfersAll the insurers said that they would accept an in-specietransfer of assets, subject to being offered appropriateassets.

Figure 2.2 shows the types of asset accepted. In some cases,the insurer would look to sell the assets, in which case a keycriteria is liquidity. Generally, bond-like assets of anappropriate duration are most popular with insurers, i.e.,similar to what insurers use to back the liabilities.

Insurance solutions for pension schemes 17

Section 2 – Structuring a dealFigure 2.1: How does pricing move once a deal hasbeen agreed in principle?

Figure 2.2: Which assets would you accept for an in-specie transfer?

3

2

6

0 1 2 3 4 5 6 7

Backing assets

Portfolio of gilts/swaps

Marketconditions/agreed index

Number of responses

9

8

1

1

0 5 10

Government bonds

Corporate bonds

Swaps

Property

Number of responses

CollateralCollateral is a common issue arising in buy-in insurancetransactions. Typical collateral might involve the insurer ringfencing the premium paid on its balance sheet (so that it isavailable to the trustees in the event of the insurer becominginsolvent).

Collateral is often viewed as attractive by trustees as it addssecurity. However, insurers will charge for this additionalsecurity and collateral arrangements can add complexity tothe transaction process (e.g., legal costs).

Figure 2.3 illustrates insurers’ view of collateral; almost two-thirds of insurers are willing to offer collateral to a scheme. Itshould be noted that collateral is generally only available forlarger deals (as a result of the added complexities). From theresponses in our survey, generally insurers required theliabilities to be at least £500m for collateral to be offered asan option.

As mentioned previously, most insurers will increase thepremium charged if collateral is offered but the actual costcan vary significantly depending on collateral structure. Basedon the responses in our survey, the cost can vary from 0.5%up to 4%.

Insurance solutions for pension schemes 18

EY InsightTrustees who take out collateral as part of a buy-in contractmay find that this raises an issue when it comes toultimately converting the buy-in to a buy-out. This isbecause the collateral will need to be relinquished as part ofthe buy-out meaning that in certain circumstances it couldbe viewed that moving to buy-out has actually reducedsecurity for individual members rather than increasing it.Trustees should therefore consider this issue at the outset.

Figure 2.3: Would you offer collateral to a scheme aspart of a buy-in?

Yes, 2

No, 4

In certaincircumstances,

4

This section concentrates on internal factors for insurancecompanies to the extent that they will impact on bulk annuitytransactions.

Insurer covenantWe would always suggest that trustees/sponsors seek tounderstand the strength of an insurer when considering a bulkannuity or longevity only transaction.

Insurers are subject to minimum capital requirements in orderto ensure the security of any insurance contracts. The freeasset ratio is the ratio of the insurer’s assets to its liabilitieswhere the liabilities are calculated using prudent assumptions.A high free asset ratio suggests a strong financial positionwhere the insurer holds enough sufficiently high-qualityassets to cover their obligations, and vice versa.

In practice, most insurers hold more than the minimumrequirement and the assets held are actually determined bythe insurer’s risk appetite The average free asset ratio wasaround 200% from our survey responses (with the highestresponses received being over 300%).

It should be noted that this is a relatively crude test offinancial strength given the deficiencies of the Solvency Iregime and we would recommend that due diligence on theinsurer is carried out.

ReinsuranceInsurers in most lines of business use reinsurance to reducetheir risks. The level of reinsurance will be determined by theinsurer’s risk appetite and the terms offered by reinsurers.Insurers are likely to include an allowance for reinsurancecosts in the pricing of their products.

From our survey, there is wide variation in the amount oflongevity risk that insurers reinsure - see Figure 3.2. Theaverage amount of longevity risk reinsured was 43% (with acorresponding median of 65%).

From a trustee perspective, the key consideration is whetherthe availability of reinsurance is key to the deal. In ourexperience, the initial quotation is generally not subject toreinsurance. It is only the larger deals that are the possibleexception to this (e.g., greater than £1billion).

Insurance solutions for pension schemes 19

Section 3 – Characteristics of insurers

2

4

0

1

0 1 2 3 4 5

150% to 200%

200% to 250%

250% to 300%

Over 300%

Figure 3.2: How much longevity risk do you typicallyreinsure?

Figure 3.1: What is your free asset ratio (based onlatest FSA returns)?

4

2

2

3

0 1 2 3 4 5

Not disclosed

Over 75%

50% to 75%

Less than 50%

Number of responses

Team sizeThe pension insurance market has existed for many years andthe main insurance providers are well-established companies.The survey respondents imply that pricing team sizes tend tofall into two broad categories: larger teams of at least 30people and smaller teams of less than 10.

It is interesting to note that some insurers are also willing tooutsource pricing to support deals if required.

Solvency II for insurers……Solvency II is scheduled to come into effect on 1 January2016. One of the main impacts will be the amount of capitalinsurers must hold to reduce the risk of insolvency.

The majority of survey respondents confirmed that they donot anticipate significant changes to their pricing following theintroduction of Solvency II. In other words, the currentunderstanding of Solvency II is factored into pricing.

……and for pension schemes?There has been much discussion over recent years aboutwhether Solvency II will be extended to cover pensionschemes in the UK. The latest draft of the Institutions forOccupational Retirement (IORP) directive released by EIOPAsets out certain requirements for pension schemes taken fromthe Solvency II regime for insurers (for example coveringdisclosure and risk management requirements).

The most controversial proposals around introducingSolvency II style funding requirements for pension schemeswere not included. However, there is a reasonable chance thatsuch requirements will be introduced by EIOPA in the future. Ifthis does materialise, we would expect to see a large increasein interest for full buyouts by pension schemes and sponsorsas this will be seen as preferable to running schemes subjectto such prudent funding requirements.

Insurance solutions for pension schemes 20

Section 3 – Characteristics of insurers(cont’d)

EY InsightNo significant step change in pricing is expected with regardto the introduction of Solvency II for insurers.

However, Solvency II capital requirements for pensionschemes could fundamentally change the market through alarge increase in demand.

UKThe insurers surveyed currently hold £55bn of bulk annuitieson their books. However, we estimate that this onlyrepresents 3% of total DB liabilities in the UK. This suggeststhat there is a significant opportunity for growth in this area.

There is a general consensus from the insurers that the size ofthe UK bulk annuity and longevity market will each be around£10bn over the next 2 years, with some modest growth from2014 to 2015.

It is worth noting that since the survey was completed,several large bulk annuity and longevity deals have beenannounced which could mean that the market in 2014 will beeven larger than shown.

These views suggest a positive outlook for the UK buyoutmarket in the short to medium term, and reflects the strongdemand for buyout solutions from private sector DB pensionschemes. Most companies participating in our survey did notdisclose their sales targets for 2014, but did note a largeappetite for deals.

Some insurers suggested that ultimately the size of the UKmarket is constrained by the availability of longevityreinsurance.

2014 BudgetIn his March 2014 Budget speech, the Chancellor announcedthat individuals retiring from DC schemes would be able totake all their funds as cash at their marginal rate of taxation.

This is likely to have a significant impact on individual annuitybusiness written by insurers. Several of the insurers whoparticipated in this survey also write individual annuities. Ifdemand for individual annuities reduces significantly, theseinsurers may choose to place more emphasis on their bulkannuity business which could lead to a more competitive bulkannuity market.

Insurance solutions for pension schemes

Section 4 – Insurers’ market outlook

21

9.5

11.0

10.3

11.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

2014 2015

£bn

Bulk annuity Longevity-only

EY InsightOne insurer expressed that they would like to write as muchbusiness as they can, as long as the price is right and it fitstheir risk profile.

Figure 4.1: Expected size of UK market(average from insurers in survey)

► Transaction process - Given the complexity, time pressureand costs involved in these transactions, it is essential thatadvisors ( for example actuarial consultants and lawyers) andinsurers work together co-operatively to ensure an efficientand pragmatic process. Some insurers will notify advisorswhen there is an opportunity to transact within their client’sbudget. Further, some firms are selective with who theychoose to quote with and might only quote on deals with ahigh likelihood of completing a transaction.

► Data - Having good data (including an accurate benefitspecification) was a key emphasis for most of the insurers inour survey, as poor quality data can delay transactions.However, it was noted that the data did not need to beperfect in order for a transaction to be successful.

► Asset transfers - Some firms also noted that asset transfersfrom existing fund managers can be challenging, particularlywith the increase in new business premiums. Firms with an in-house investment management function are generally betterequipped to deal with asset transfers.

► Expansion overseas - There were firms who are seeking toapply the expertise gained from the UK de-risking market intoother countries. Specific territories mentioned includeJersey, Channel Islands, Netherlands, USA, Canada andEurope.

► Other - Irish insurers also noted that there was a lack ofpublished mortality data on Irish annuitants. Additional datacould help reduce margins and make pricing more affordable.

Insurance solutions for pension schemes 22

4.1 - Top business issues for insurers

EY InsightIt is sometimes thought that data must be perfect for atransaction to go ahead. In our experience and fromconversations with insurers this isn’t the case and there areoptions available where concerns exist over the data.

6

62

1

6

2

Transaction process Client solutions

Asset transfers Expansion into other countriesData Other

Figure 4.2: What are your key business issues?

We also asked insurers to comment on the top business issuesthat affect them. The responses can be broadly put in thefollowing categories:

► Solutions -There was a strong focus from insurers to developclient-specific solutions to help both trustees and employersachieve de-risking objectives. In particular, firms emphasiseda willingness to transact with underfunded schemes andcould provide a range of options to make a transaction moreaffordable, e.g., underwriting, deferral of premiums, usingilliquid assets or implementing trigger monitoring. Firms alsoexpressed a desire to provide longevity insurance to a widerrange of market participants (currently, this is mainly offeredto larger pension schemes).

For further information or an informal discussion about the insurance market for pension schemes, please contact one of ourteam listed below.

Alternatively, please visit http://www.ey.com/pension-insurance

Insurance solutions for pension schemes 23

Contact us

Iain BrownPartner

Tel: +44 20 7951 7546Mobile: +44 7977 023 389Email: [email protected]

Sean BottomleyDirector

Tel: +44 11 3298 2327Mobile: +44 7740 923 265Email: [email protected]

Matthew MignaultSenior Manager

Tel: +44 20 7951 7630Mobile: +44 7827 257 370Email: [email protected]

Christopher BownDirector

Tel: +44 20 7951 3231Mobile: +44 7730 733 861Email: [email protected]

Vicky ParamourSenior Manager

Tel: +44 20 7951 1458Mobile: +44 7789 030 921Email: [email protected]

Adam PoulsonSenior Manager

Tel: +44 11 3298 2424Mobile: +44 7876 397 927Email: [email protected]

Andrew StokerPartner

Tel: +44 20 7951 4473Mobile: +44 7788 355 834Email: [email protected]

Kenny ChengExecutive

Tel: +44 20 7951 2429Mobile: +44 7725 252 578Email: [email protected]

Christian MaleedyManager

Tel: +44 20 7951 0226Mobile: +44 7810 182 425Email: [email protected]

Melanie XuExecutive

Tel: +44 20 7951 2889Email: [email protected]

Philip WheelerSenior Manager

Tel: +44 14 1226 9557Mobile: +44 7786 313 701Email: [email protected]

Robert HeatonSenior Manager

Tel: +44 11 3298 2519Mobile: +44 7767 494 887Email: [email protected]

EY client contacts EY insurance specialists

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisoryservices. The insights and quality services we deliver help build trustand confidence in the capital markets and in economies the worldover. We develop outstanding leaders who team to deliver on ourpromises to all of our stakeholders. In so doing, we play a critical rolein building a better working world for our people, for our clients andfor our communities.

EY refers to the global organization, and may refer to one or more, ofthe member firms of Ernst & Young Global Limited, each of which is aseparate legal entity. Ernst & Young Global Limited, a UK companylimited by guarantee, does not provide services to clients. For moreinformation about our organization, please visit ey.com.

Ernst & Young LLPThe UK firm Ernst & Young LLP is a limited liability partnership registered in England andWales with registered number OC300001 and is a member firm of Ernst & Young GlobalLimited.

Ernst & Young LLP, 1 More London Place, London, SE1 2AF.

© 2014 Ernst & Young LLP. Published in the UK.All Rights Reserved.

ED NONE

1486839(UK) 06/14. Creative Services Group.

In line with EY’s commitment to minimise its impact on the environment, thisdocument has been printed on paper with a high recycled content.

Information in this publication is intended to provide only a general outline of the subjectscovered. It should neither be regarded as comprehensive nor sufficient for making decisions,nor should it be used in place of professional advice. Ernst & Young LLP accepts noresponsibility for any loss arising from any action taken or not taken by anyone using thismaterial.

ey.com/uk

![PENSION SCHEMES BILL [HL]...The Pension Schemes Bill aims to build on recent pension reforms such as automatic enrolment in workplace pensions. Once automatic enrolment is fully rolled](https://static.documents.pub/doc/80x56/5f2b1cd54a936062d305db0d/pension-schemes-bill-hl-the-pension-schemes-bill-aims-to-build-on-recent-pension.jpg)