22

Insurance Strategies for Multinational Operations Go Global or Buy Local

Speakers:

Dave Arick, Global Risk Management, International Paper Company

Petra Riga, Head International Sales & Distribution, Zurich Insurance

Learning Objectives

At the end of this session, you will: • Distinguish coverage, administrative burdens and corporate

support for local versus global programs • Create a framework for deciding which approach is best for

your company in different circumstances

• Be prepared to earn corporate support from management and local operations for your chosen approach

Agenda

Introduction Risk manager view and thoughts • Brief description of International Paper • Risk philosophy regarding global programs vs. local programs • Experience with property, liability, D&O - similarities, issues • Broker and insurer resources/support Zurich view and thoughts • Understanding Customer risk strategy and exposure • Country regulatory and tax considerations • Coverage and claims needs • Supporting tools • Proposal of best options Conclusion & Wrap up

International Paper Overview • World’s largest paper and packaging company

• Industrial packaging - containerboard, corrugated boxes • Printing papers - copy paper, envelopes, business forms, file folders • Pulp - used in tissue, towels, diapers, cosmetics, hygiene products • Consumer packaging - packaging for food, cosmetics, pharma; cups, lids, food containers, plates

• Manufacturing operations in over 20 countries • $23.6 Billion in global sales for 2014 • 58,000 employees (24,000 outside the U.S.)

Global, Local, or “Glocal”? Company risk philosophy dependent upon firm’s structure and practices

• Centralized oversight/control vs. regional or local autonomy • Focus on cost reduction vs. ensuring compliance • Senior management support • Importance of global consistency throughout firm’s practices • Company history and evolution • Insurance/risk expertise, awareness, resources throughout the world

All of these factors influence the decision process…

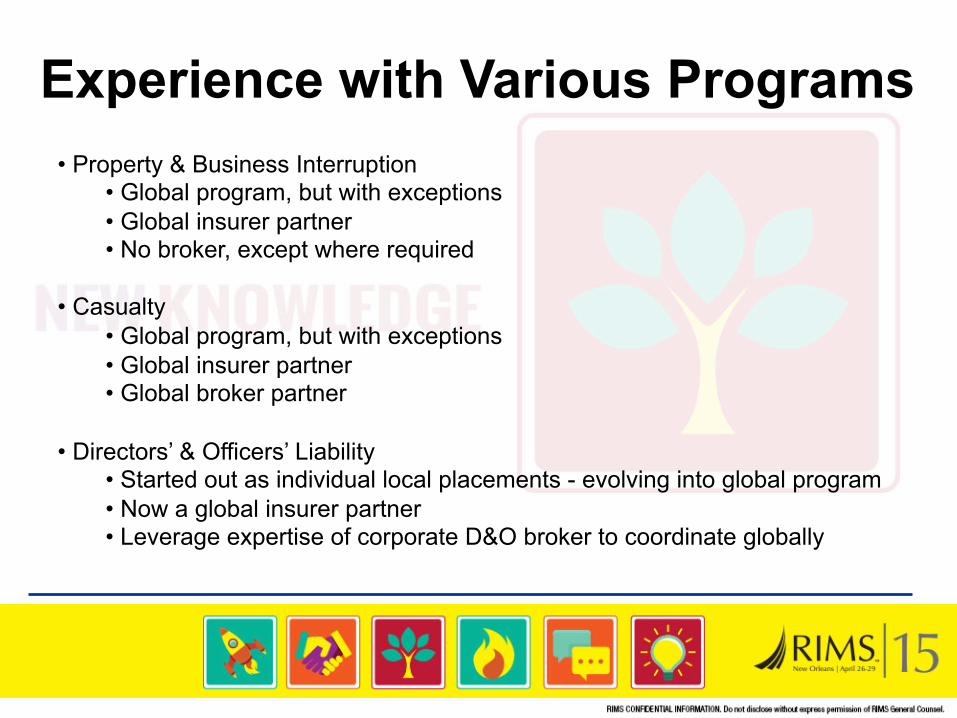

Experience with Various Programs • Property & Business Interruption

• Global program, but with exceptions • Global insurer partner • No broker, except where required

• Casualty • Global program, but with exceptions • Global insurer partner • Global broker partner

• Directors’ & Officers’ Liability • Started out as individual local placements - evolving into global program • Now a global insurer partner • Leverage expertise of corporate D&O broker to coordinate globally

Broker/Insurer Support Items to consider before engaging partners to build a global program: • Local/global expertise and track record in coverage contemplated • Geographic footprint matches your firm • Strong coordination team to support you (prefer in home country) • Willingness to research and answer tough questions about local issues like compliance & regulations, tax considerations, transfer pricing • Expertise in managing (and for insurers, paying) local claims • Technology to administer program (policies, premium movement, claims data)

Who can best provide what you need? Insurer, broker, or combination of the two?

Building the Picture

Understand customer’s risk strategy

and exposure

Understand country regulatory and

tax requirements Implement Solution

Consider & propose the best solution for the customer

Coverage & Claims Requirements

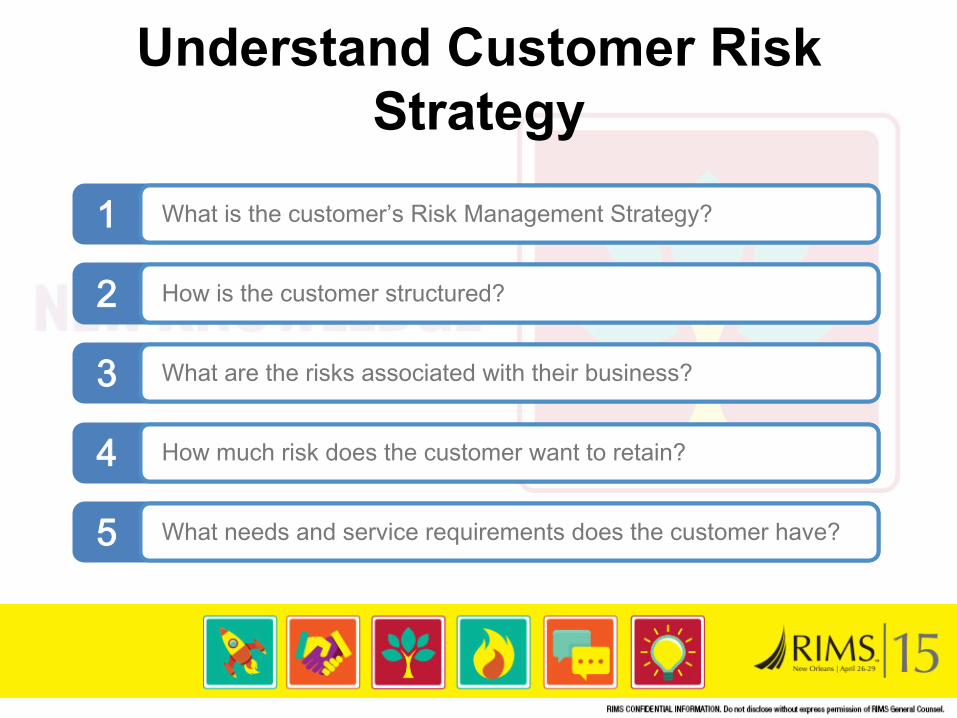

Understand Customer Risk Strategy

1 What is the customer’s Risk Management Strategy?

2 How is the customer structured?

3 What are the risks associated with their business?

4 How much risk does the customer want to retain?

5 What needs and service requirements does the customer have?

Customers Footprint

Regulation & Tax

240+ jurisdictions Sometimes multiple provinces per country Licensing requirements Premium tax requirements Varying definitions for

Non-admitted business Lines of Business

Conflicts of laws Insurer, Broker and other Regulations Varying business practices

Increased attention to corporate governance issues around the world

Increased shareholder demands to demonstrate good corporate governance standards

Increased awareness of prohibited nature of non-admitted business in many territories

Increased scrutiny and tax audits on foreign corporations and insurers

Reputation of Insurer, Broker and Customer

Regulation & Tax

Customers expect their international programs to satisfy multiple requirements. For local regulation we need to understand what is conduct of insurance.

So what does Conduct of Insurance

mean?

The answer varies country

by country

Zurich has the information not only for ‘risk coverage’ but for a variety of other insurance activities in our

Zurich MIA tool

Marketing?

Negotiation?

Loss adjustment?

Claim payment?

Risk coverage?

Risk engineering?

Premium payments?

Our Customers Footprint

Austria Hong Kong Greece Peru Sweden

Turkey

Luxembourg

Trinidad & Tobago

Liechtenstein France

Cyprus

South Africa Australia

Japan Mex. N'Lands, Ger., Switz. Panama, Portugal

Australia Colombia

Republic of Korea

Canada (Various Provinces) Costa Rica

Croatia

Canada (Yukon)

Czech Republic

New Zealand Norway Chile Israel

Finland

Iceland

Bulgaria Paraguay Hungary Estonia Spain Italy

France

Belgium

Lithuania

Denmark

Malta

Bulgaria

Mexico Japan Netherlands Panama

Canada (Ontario)

New Zealand Norway

Pakistan

China

Series1

Canada (Quebec) Canada (New Brunswick) Canada (BC, Alberta)

Series1

Austria

Romania

Slovakia

Slovenia

Poland Series1 Latvia

Ireland

United Kingdom

0

10

20

30

40

50

60

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100

Varia

tions

Per

mitt

ed (%

)

Business Scenarios Permitted (%)

Mapping Country Regulations

• Data for 180+ jurisdictions • Per 42 Lines of Business • Per 5 Business Scenarios

• Variations on Risk Engineering, Premium Payment, Loss Adjusting, Claims Payments

• Dedicated Legal Department managing 140+ law firms around the globe

• Details on out of territory and applicable FoS taxes • Zurich Underwriters, by using MIA can ensure that out of

territory taxes are accounted for and disbursed

• Zurich has tax representatives globally to ensure out of territory taxes are properly handled

Coverage & Claims

Understanding the legal and tax situation in a country tells one part of the story.

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

• Locations with large exposures may require different levels of protection

• Manufacturing/Sales/R&D sites drive different service requirements/coverage

Overlaying the customer’s specific situation & expectations allows us to propose appropriate solutions.

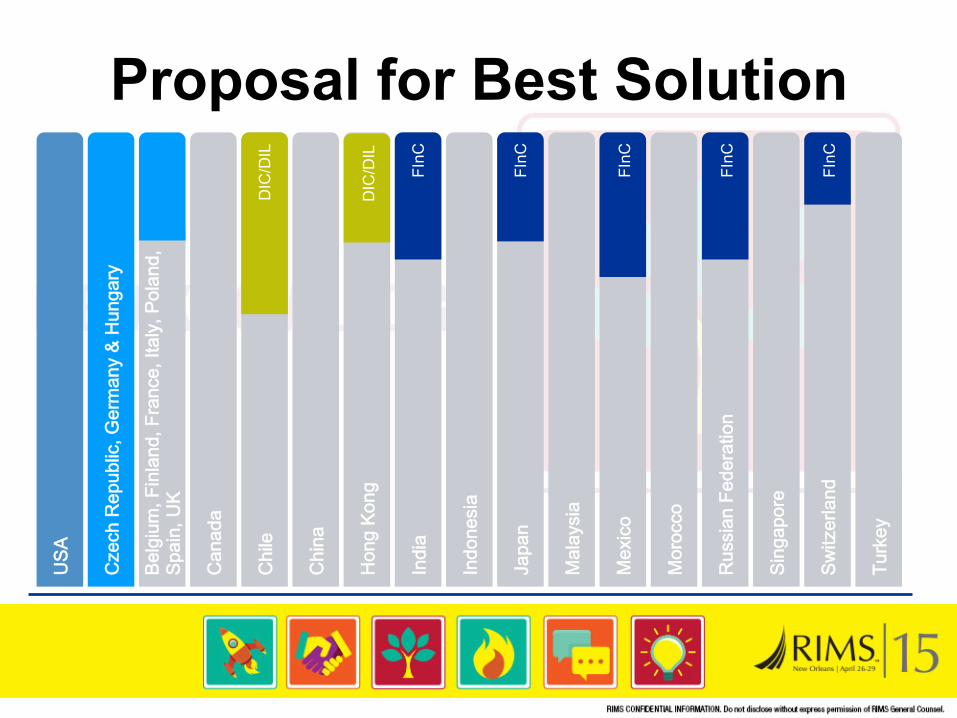

Proposal for Best Solution

Belg

ium

, Fin

land

, Fra

nce,

Ital

y, P

olan

d,

Spai

n, U

K

Cze

ch R

epub

lic, G

erm

any

& H

unga

ry

Can

ada

Chi

le

DIC

/DIL

Chi

na

USA

Mor

occo

Indi

a FI

nC

Indo

nesi

a

Japa

n FI

nC

Mal

aysi

a

Hon

g Ko

ng

DIC

/DIL

Mex

ico

FInC

Rus

sian

Fed

erat

ion

FInC

Sing

apor

e

Switz

erla

nd

FInC

Turk

ey

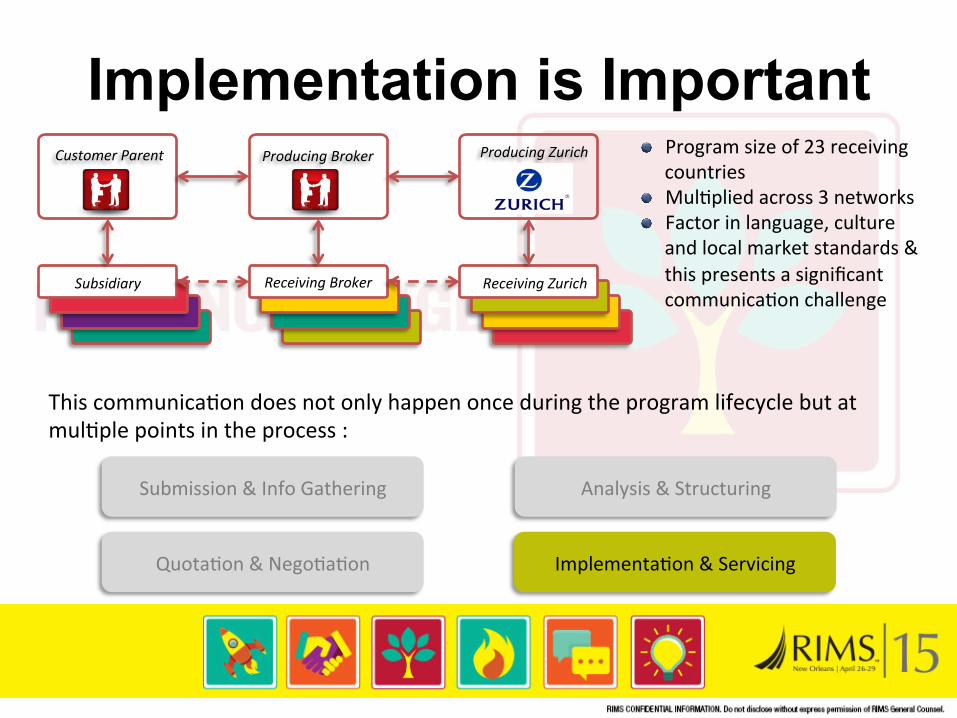

Implementation is Important

Subsidiary Receiving Broker Receiving Zurich

Producing Zurich Customer Parent Producing Broker Program size of 23 receiving countries

Mul=plied across 3 networks Factor in language, culture and local market standards & this presents a significant communica=on challenge

This communica=on does not only happen once during the program lifecycle but at mul=ple points in the process :

Submission & Info Gathering Analysis & Structuring

Quota=on & Nego=a=on Implementa=on & Servicing

Transparency of Information

CLAIMS Review the complete claims history of your organization, from a global overview right down to specific claims detail.

RISK ENGINEERING Helping you manage various risk improvement actions relating to your business.

INSURANCE PROGRAMS All your global Insurance Programs at your fingertips - drill down to review specific policy details with real-time portfolio overviews.

ZURICH MIA Access our unique database on local regulations and taxes.

Your Global Risk Management center providing essential real time information related to your insurance solutions with Zurich

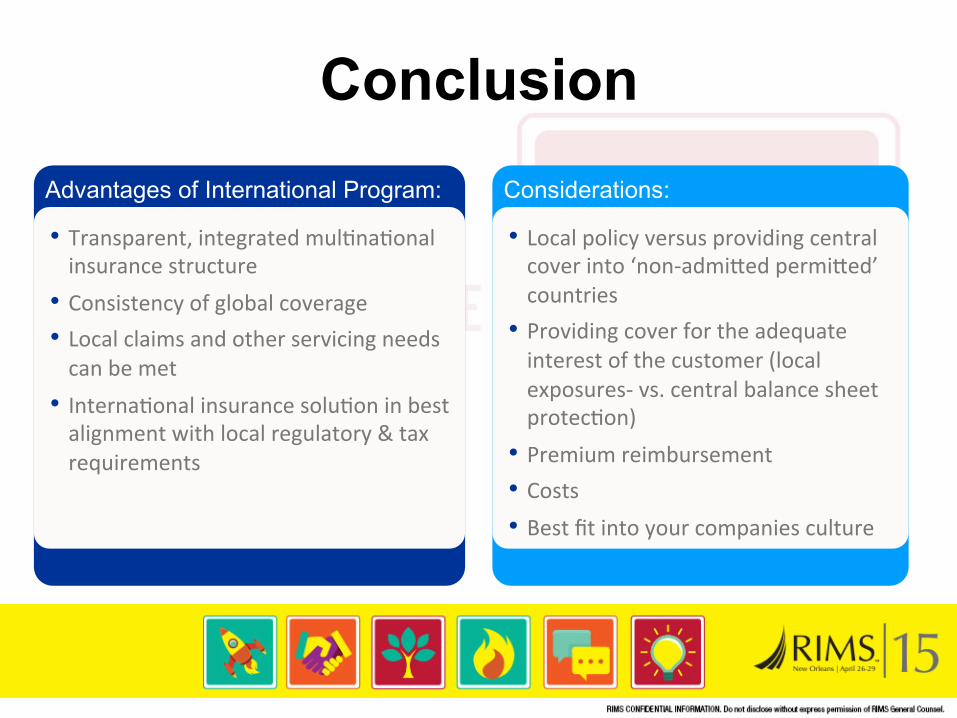

Conclusion

Advantages of International Program:

• Transparent, integrated mul=na=onal insurance structure

• Consistency of global coverage • Local claims and other servicing needs can be met

• Interna=onal insurance solu=on in best alignment with local regulatory & tax requirements

Considerations:

• Local policy versus providing central cover into ‘non-‐admiWed permiWed’ countries

• Providing cover for the adequate interest of the customer (local exposures-‐ vs. central balance sheet protec=on)

• Premium reimbursement • Costs • Best fit into your companies culture

Questions ?

Thank you !

This is intended as a general descrip=on of certain types of insurance and services available to qualified customers through the companies of Zurich in North America, provided solely for informa=onal purposes. Nothing herein should be construed as a solicita=on, offer, advice, recommenda=on, or any other service with regard to any type of insurance product underwriWen by individual member companies of Zurich in North America, including Zurich American Insurance Company. Your policy is the contract that specifically and fully describes your coverage, terms and condi=ons. The descrip=on of the policy provisions gives a broad overview of coverages and does not revise or amend the policy. Coverages and rates are subject to individual insured mee=ng our underwri=ng qualifica=ons and product availability in applicable states. Some coverages may be wriWen on a nonadmiWed basis through

licensed surplus lines brokers.