Integrating IP portfolio and company valuation A thesis submitted to the Bucerius/WHU Master of Law and Business Program in partial fulfillment of the requirements for the award of the Master of Law and Business (“MLB”) Degree Anna Konchenkova Date: 4 August 2010 12 385 words (excluding footnotes) Supervisor 1: Prof. Dr. Holger Ernst Supervisor 2: Prof. Dr. Peter Witt

Transcript

Integrating IP portfolio and

company valuation

A thesis submitted to the Bucerius/WHU Master of Law and Business Program in partial fulfillment of the requirements for the award of the Master of Law and Business (“MLB”) Degree

Anna Konchenkova

Date: 4 August 2010

12 385 words (excluding footnotes)

Supervisor 1: Prof. Dr. Holger Ernst

Supervisor 2: Prof. Dr. Peter Witt

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 2 -

Table of Contents

Table of Contents...............................................................................................................2

Table of Figures..................................................................................................................3

Table of Tables...................................................................................................................4

List of Abbreviations .........................................................................................................5

Chapter 1: Introduction

I. Background of the study …………………………………………...……6

II. Research problems and objectives……………………………...….……..8

III. Research design and methodology………………………………...…….10

IV. Conceptualization………………………………………...…………..….10

V. Overview of chapters……………………………………………….....…11

Chapter 2: IP importance in the overall value of the company

I. Importance of IP for the company…………………………………..…...13

II. Need to value IP…………………………………....................................16

III. Importance of IP for investors in their company valuation….……..……18

IV. Existing approaches for patent valuation………………………….……..23

1. Qualitative………………………………………………….………….25

2. Quantitative………………………………………………….………...30

2.1 Cost based method……………………………………….…....…30

2.2. Market based method………………………………………….…31

2.3. Income based method………………………………………....…32

2.4. Other methods………………………………………………........33

Chapter 3: Practical insight into IP and company valuation

I. Determinants influencing investor’s decision in valuing IP portfolio…...37

II. Tendencies in valuing IP portfolio from the investor point of view……..41

III. Conclusions from the interviews…………………………………………44

Chapter 4: Overall conclusion and recommendations……………………..45

Bibliography……………………………………………………………………...…..48

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 3 -

Table of Figures:

Figure 1: Components of S&P 500 Market Value…………………………………….…6

Figure 2: Intangible Value as Percent of Market Value for Non-US Markets………..….7

Figure 3: Advantages of reporting IP …………………………………………………...18

Figure 4: How important is a company’s IP portfolio compared to other assets?............19

Figure 5: An importance of IP in assessment of an investment………………………….20

Figure 6: Rating and Valuations of Patents – Overview…………………………...……25

Value-Study (last visited 01.07.2010)9 The securities Exchange Act of 1934, also called ’34 Act10 Ibid11 Scott, Financial Times Report 03.06.2010, http://www.ft.com/cms/s/0/641dffcc-6ddb-11df-b5c9-

00144feabdc0.html (last visited 01.06.2010)12 Smart Recession Investing: Use Intellectual Property Metrics to Identify Sources of Return That Others Can't See,

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 9 -

Eckardt, Intellectual Property strategists and former Boston Consulting Group partners, argue

that all investors - from venture capitalists to institutional and even individual stock investors -

need to assess the IP position of their investment targets in order to find sources of return.

Investors who understand and can apply the IP framework for analyzing investments will have a

significant wealth creation opportunity13. But the question is how to value IP and integrate it into

the overall value of the company. Academics and economists began struggling to come up with

some standardized measurement years before the technology boom brought the issue to the

forefront, Best Practices LLC CEO Christopher Bogan said.14 Those who are unable to identify

and assess the future potential of a new technology are doomed to failure. But few have

systematic processes in place to identify and track potentially disruptive technologies15.

A few years ago patents were regarded as only an expense to the company which

provided protection from the rivals but now it is commonly used as a business tool. The question

in front of investors is how to valuate and capture the overall value of the company which will

give the full picture and ease the investment decision. Due to lack of literature on how practically

investors valuate IP portfolio in order to identify the technological strength of the company and

its potential revenue creation this paper investigates this topic and answers the following

questions:

- What is the significance of patents to the company valuation;

- What are the reasons for valuation patents and patent portfolios by

management and investors;

- What are the existing techniques and methods of valuating patents; and

- How do investors currently valuate patent portfolio in order to capture the

full value of the company, if they do it at all, and how do they integrate it

into the overall company valuation.

13 Ibid14 Stock, Intangibles remain a hidden asset: non-financial metrics are key to IR's story in a recession, in: Investor

Relations Business 2003, Vol. 8, Issue 5, p. 215 Bower, Christensen, Clayton, in: Harvard Business Review 1995, Vol. 73, Issue 1, p. 49

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 10 -

III Research design and methodology

A number of interviews were conducted in order to collect primary information on how

investors currently valuate companies comprising IP.

To foster cooperation and openness of discussion, it was agreed that none of the

companies, the persons interviewed, or the specific companies would be identified or generally

described in this study. Therefore, no specific company or its practices are identified in this

paper.

Due to a weak interviewees’ response, the study also uses some information taken from

researches conducted by some companies, institutions and practitioners.

Some data was derived also from documentary information. Documentary sources which

included text books and research papers, magazine articles, information available on the internet,

survey reports, business plans, and annual reports were collected, compared and integrated.

Another source of information will be comments solicited from the professionals in the field.

IV Conceptualisation

The notion of defining terms is to avoid misconceptions and ambiguity in the use of the

words. Even though in the paper a lot of terms are presented but the following are the most

abundant.

Intangible Asset: Is an asset that is not physical in nature16 (IAS 38)

Intellectual Property (IP): A broad categorical description for the set of intangibles

owned and legally protected by a company from outside use or implementation without consent.

Intellectual property can consist of patents, trade secrets, copyrights and trademarks17.

16 “IAS38 intangible assets”, StartRunGrow, 200717 Economic dictionary, available at http://www.investopedia.com/terms/i/intellectualproperty.asp (last visited

01.07.2010)

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 11 -

Patent: Gives the right to its holder (patentee) to exclude others from making, using,

selling, offering to sell, or importing that which is claimed in the patent, for a fixed period of

time18.

Patent portfolio: Collection of related patents19.

In the frame of the Master Thesis Patents and Intellectual Property used interchangeably

and consequently Patent Portfolio and IP Portfolio identified equally here, but as already was

stated patents are only one type of intellectual property where others include trade secrets,

copyrights and trademarks.

V Overview of Chapters

The study comprises of four chapters. Chapter one consists of the following:

An Introduction

Research Problem and Objectives

Research Design and Methodology

Conceptualisation

Overview of chapters

Chapter two will discuss IP importance in the overall value of the company. And in particular,

why IP need to be valuated, what are the advantages of IP valuation. The importance of IP from the

investor as long as from the management point of view in the overall value of the company will be

regarded. This chapter will give an overview of the existing approaches in quantitative and qualitative

valuation of patents and patent portfolios of the company. It will include the review of the relevant and

related literature on patent portfolio valuation. Advantages and disadvantages of current approaches for

patent valuation will be assessed which will give bases for further discussion in next chapters.

Chapter three deals with received information from the investors and analysts during conducted

interviews in the field. The main questions which were asked are the following:

- Do investors value IP during their overall company valuation?

18Patel, A patent portfolio development strategy for start-up companies, in: Fenwick & West LLP White Paper19 Parchomovsky, Wagner, Patent Portfolios, in: University of Pennsylvania Law Review, Vol. 154, Issue 1, pp. 1-77

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 12 -

- If yes, then how they do it? What methods do they use?

- Do they do valuation by themselves or they ask for a professional advice?

- What are the obstacles in valuing IP?

During the interviews some tendencies in the investor’s behaviour concerning IP portfolio valuation as

a part of the overall company valuation were uncovered and presented. The gap between what is in

theory exists and how it currently applicable by the investors and analyst will be discussed.

Chapter four concludes and provides a summary of the research as well as further

recommendations.

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 13 -

Chapter 2

I Importance of IP for the company

“As firms shift to open models of innovation based on collaboration and external

sourcing of knowledge, they are exploiting their intellectual property, notably patents, not only

by incorporating protected inventions into new products, processes and services, but also by

licensing them to other firms or public research organizations, using them as bargaining chips in

negotiations with other firms, and as means of attracting external financing from banks, venture

capitalists and other sources”20. By means of exploiting patents there is an enormous possibility

to create extra revenue for the company and that is exactly what investors are looking for while

investing in a new project or company. Extra revenue creation is just one of the advantages that

patents can bring into the company. Cohen et al. conducted a survey where they found out the

reasons for patenting product innovation and what companies are expecting from patents (Table

1)21.

Table 1: Reason for patenting product innovation (% of respondents and ordinal rank)

US Japan

Prevent copying 98.9 (1) 95.5 (1)

Patent blocking 80.3 (2) 92.6 (2)

Prevent Lawsuits 72.3 (3) 90.0 (3)

Use for negotiations 55.2 (4) 85.8 (4)

Enhance reputation 38.8 (5) 57.9 (7)

Licensing revenue 29.5 (6) 66.7 (5)

Measure performance 7.8 (7) 60.1 (6)

20 Kamiyama, Sheehan, Martinez, Valuation and exploitation of intellectual property, in: STI Working Paper

2006/5, p.3 21 Cohen, Goto, Nagata, Nelson, Walsh, R&D Spillovers, Patents and the Incentives to Innovate in Japan and the

United States, in: Research Policy 2002, Vol. 31, Issue 8/9, p. 1359

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 14 -

One of the most important features of patent information is that it can be used for a

strategic technology management22. Richard Thoman, CEO of the $20 billion sales Xerox

Corporation said: “I’m convinced the management of intellectual property is how value added is

going to be created at Xerox. And not just here, either. Increasingly, companies that are good at

managing IP will win. The ones that aren’t will lose”23. While talking about IP it is relevant to

focus on patents as they have the “greatest effect on the commercial success and market value of

companies today” and also “patent databases are a virtual Alexandrian library of information”24.

All the necessary data could be extracted from the publicly available sources. Especially

when combined with new automated data-mining and visualization software, these databases can

be powerful sources of rich competitive intelligence25. But before figuring out how to obtain

competitive intelligence and thereby advantage compared to others, one should understand first

the value of patents and what they can bring into the company: how they can be used not only as

a legal tool but also as a valuable business tool for revenue creation. Recent case can

demonstrate the hidden value of patent portfolio and how the right exploitation of it could

maintain the livelihood of the company.

Telecommunication Corporation Nortel which has Nortel’s Long Term Evolution or LTE

a high-speed wireless technology known as “4G” could have earlier exploited their patent

portfolio, identifying licensing opportunities as a source of revenue generation. Only after filing

for insolvency Nortel found out that their technology including patents might be worth as much

as $1.1 Billion. Peter Conley a managing director of MDB Capital Group LLC, who estimated

their value, stated that they would be a “natural fit” for BlackBerry maker RIM26. This kind of

natural fit could have saved Nortel’s company.

In order to avoid such mistakes patent portfolio should be properly managed in order to

discover the prospects for exploitation.

22 Ernst, Patent information for strategic technology management, in: World Patent Information 2003, Vol. 25,

Issue 3, pp. 233-24223 Rivette, Kline, Discovering New value in Intellectual Property, in: Harvard Business Review 2000, Vol. 78, Issue

1, pp. 54-6624 Ibid25 Ibid26 Miller, Nortel may raise as much as $1.1 Billion from patents, http://www.businessweek.com/news/2010-05-

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 15 -

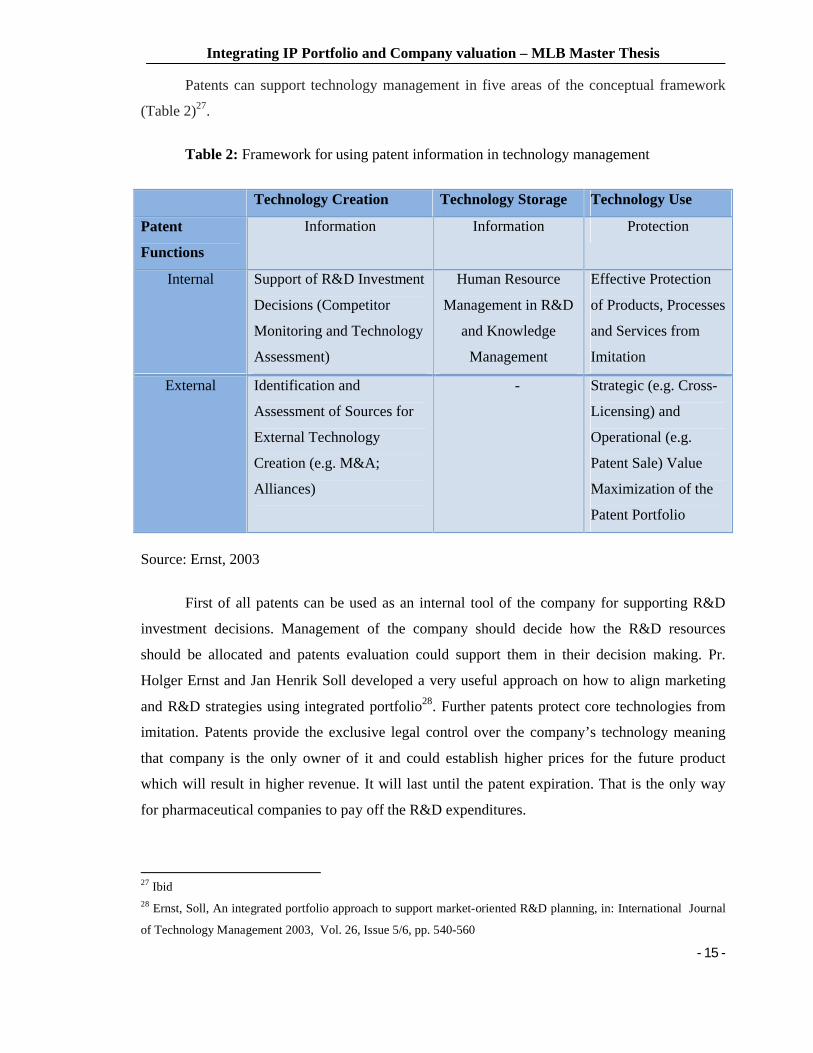

Patents can support technology management in five areas of the conceptual framework

(Table 2)27.

Table 2: Framework for using patent information in technology management

Technology Creation Technology Storage Technology Use

Patent

Functions

Information Information Protection

Internal Support of R&D Investment

Decisions (Competitor

Monitoring and Technology

Assessment)

Human Resource

Management in R&D

and Knowledge

Management

Effective Protection

of Products, Processes

and Services from

Imitation

External Identification and

Assessment of Sources for

External Technology

Creation (e.g. M&A;

Alliances)

- Strategic (e.g. Cross-

Licensing) and

Operational (e.g.

Patent Sale) Value

Maximization of the

Patent Portfolio

Source: Ernst, 2003

First of all patents can be used as an internal tool of the company for supporting R&D

investment decisions. Management of the company should decide how the R&D resources

should be allocated and patents evaluation could support them in their decision making. Pr.

Holger Ernst and Jan Henrik Soll developed a very useful approach on how to align marketing

and R&D strategies using integrated portfolio28. Further patents protect core technologies from

imitation. Patents provide the exclusive legal control over the company’s technology meaning

that company is the only owner of it and could establish higher prices for the future product

which will result in higher revenue. It will last until the patent expiration. That is the only way

for pharmaceutical companies to pay off the R&D expenditures.

27 Ibid28 Ernst, Soll, An integrated portfolio approach to support market-oriented R&D planning, in: International Journal

of Technology Management 2003, Vol. 26, Issue 5/6, pp. 540-560

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 16 -

Moreover patents are very helpful in exploiting external company strategy. Companies

may assess competitor’s position and think of R&D alliances or M&A in order to gain external

technological knowledge. These kinds of activities are extremely beneficial for the companies

from the efficiency gains point of view through reduced development time and costs, access to

superior knowledge and the reduction of technological risks29. They also can use patents as a

strategic tool for cross-licensing, as a bargaining chip in the litigation procedure, as long as in

operational strategy like patent sale.

All this information confirms that intellectual property and patents in particular are

important as value drivers for companies operating in highly competitive environments30. Patents

are an extremely valuable source of information which management of the company should

know how to extract by using the valuation techniques. Patents provide an important signal to

competitors, suppliers, customers and investors about the validity of the company’s business31.

II Need to value IP.

The primary reason for valuing IP is to maximize its value and therefore the value of the

owner organization through optimum management decisions32. Otsuyama developed a scheme

when there is a demand for valuation of IP at each stage of IP exploitation33. Need for IP

valuation is low when IP is exploited for defense purposes, that is, preventing other firms from

intervening and helping to fend off attacks from them. The value of IP gradually becomes

important as soon as IP is exploited to secure superiority when there is an expansion of

alternative product designs and need for enforcement against infringers. As soon as IP

considered is a business tool, its value is recognized independently. In this case IP is used as a

source of profits for the company. The next stage is when IP is exploited as management strategy

and its valuation becomes necessary for management decision making. The last stage where IP

valuation becomes essential is when IP is exploited as a financial asset. In this case IP becomes

a proxy of the financing method for IP holding firms and is regarded as an investment asset for 29 Ibid30 Levitas, Mcfadyen, Managing liquidity in research-intensive firms: Signaling and cash flow effects of patents and

alliance activities, in: Strategic Management Journal 2009, Vol. 30, Issue 6, pp. 659-67831 Kamiski, Metrics and Measurement for Patent Departments, in: Foley & Lardner LLP White Paper 200532 Valuation of intellectual property, in: IP for Innovation Handbook (ip4inno), p. 533 Otsuyama, “Patent valuation and intellectual assets management”, Chapter 5, Patent Strategy Handbook, Tokyo,

2003

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 17 -

financial institutions34. Valuing IP is essential for investors so that they can see the future

potential of the company and make correct investment decisions.

There is an obvious necessity to value IP – inevitable part of the overall value of the

technology based company. But lack of a universal approach on how to value IP makes it

difficult to extract a potential value from IP hidden in it.

Traditional financial and accounting indicators are of very limited help to correctly assess

the presence and quality of internally generated assets.35 Internally generated IP is treated as an

immediate expense. “The same applies to Research and Development related to the creation of

IP. The costs incurred for the creation of IP are reported at one single point in time, while the IP

is accounted for only in the context of a commercial transaction”36.

It is crucially important to integrate IP into the overall value of the company in order to

support management and to ease the decision making for investors. As companies have more

information on the value of IP which could be integrated into the true value of the company, they

could report it to outside interested parties like investors and enjoy better market value of the

company afterwards. Figure 3 illustrates how IP accounting can ease the task for managers and

investors37. Particularly, reporting IP despite informing the investors about the true value of the

company, explains how the IP relates to business segments. On the other side, investors receive

valuable information about the drivers of company performance. By receiving this kind of

information investors can better estimate risks and revenues of an investment. It reduces

information asymmetries between the management and investors which will increase

predictability and lowers volatility.

34 Ibid35 Hand, Lev, Intangible assets: Values, measures, and risks, 2. edition, Oxford University Press, New York 2003 36Ghafele, Getting a grip on accounting and intellectual property, World Intellectual Property Organization Articles,

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 18 -

Figure 3:

As there are visible advantages from reporting IP, some changes in legislation were

introduced in the United States. In 2002 Senator Paul Sarbanes and Representative Michael

Oxley drafted the Sarbanes-Oxley Act, which created new standards for corporate accountability

and enhanced intellectual property reporting system38. Still the reporting system is not in

common use among companies: there is a big informational asymmetry between the

management of the company and investors concerning IP value.

From all said above one could make a conclusion that there is a need to value IP from

management point of view not only as a compulsory duty for the compliance with current

legislation, which is also one of the reasons for the valuation but also in order to capture the full

value of the company and as pointed out by Otsuyama in each stage of development IP. Investors

have their own reasons to value IP which will be discussed in the next chapter.

III Importance of IP for investors in their company valuation

In order to identify high value patents and determine a strategy to their exploitation, a

rating and a valuation of patents are necessary in the frame of all company valuation.

38 Valoir, Sarbanes-Oxley Compliance and Intellectual Property Portfolios, in: Intellectual Property and Technology

Law Journal 2010, Vol. 22, Issue 4, pp. 1-5

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 19 -

Institutional investors such as venture capitalists need to appraise patents for their decision

making. In the research work the focus will be made mostly on institutional investors, though a

venture capitalist approach for patent evaluation also will be considered.

Research made by a Mergermarket in association with CRA International and K&L Gates

about the importance of IP assets in M&A transactions reveals that 84% of corporate

respondents and 72% of private equity respondents view IP portfolio as equally important or

even more important than other assets39. This suggests that investors are aware of IP asset

importance.

Interesting observation can be made from Figure 4. Corporate respondents place a

noticeably stronger emphasis on the IP portfolio which constitutes 40% compared to private

equity practitioners who submit only 12% of their votes toward IP portfolio.

Figure 4:

These findings shed more light on the institutional and VC investor’s attitude while

valuing the IP portfolio of the targeted company. VC’s do not pay as much attention to the IP

39 Brodowski, M&A Insights: Spotlight on Intellectual Property Rights, in: Mergermarket study in association with

CRA International and K&L Gates, December 2008, p. 4

0%10%20%30%40%50%60%70%80%90%

100%

Corporates Private equity practitioners

40%

12%

24%

36%

20%

24%

8% 28%6%

0%

Perc

enta

ge o

f re

spon

dent

s

How important is a company’s IP portfolio compared to other assets?

Not Important

Less Important

As Important

More Important

Crucial

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 20 -

portfolio compared to corporate investors. “The decrease in importance to private equity maybe

the result that private equity tends to have startup and early stage companies whose IP maybe

primarily applications. Because those applications may never issue as a patent, the value to the

equity investors may be lower.”40

On this basis one could conclude that investors and in particular corporate investors give

a lot of weight to IP when making their investment decisions.

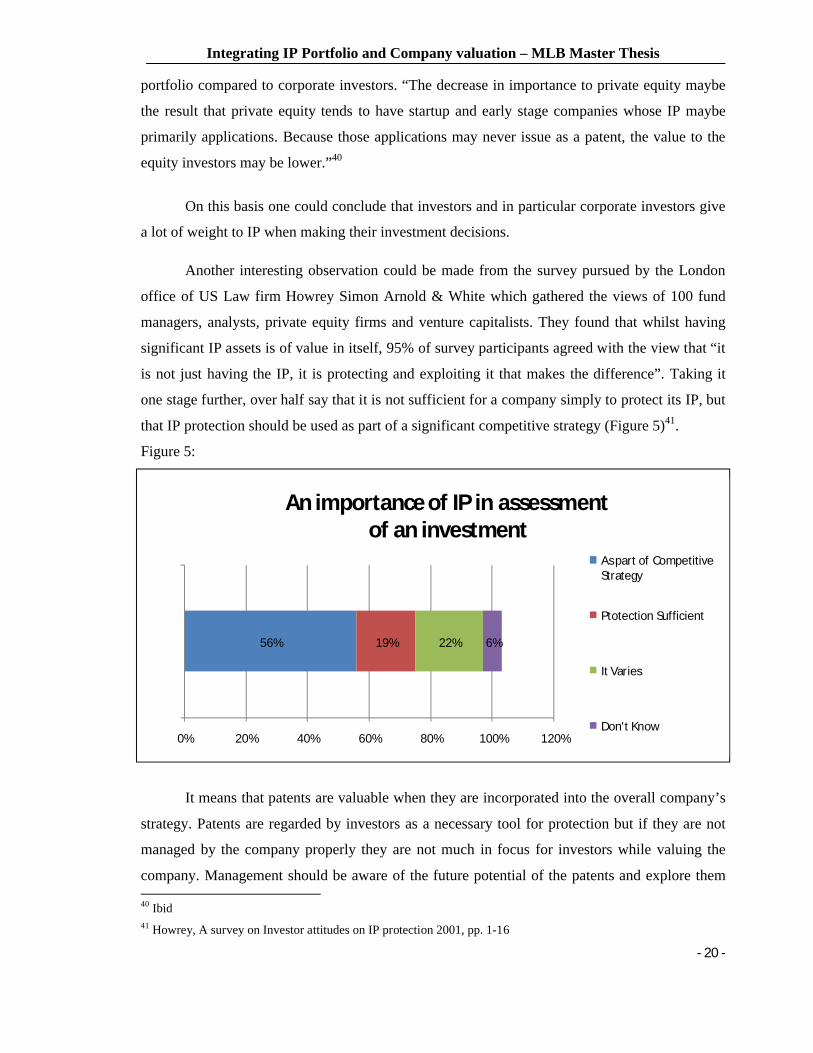

Another interesting observation could be made from the survey pursued by the London

office of US Law firm Howrey Simon Arnold & White which gathered the views of 100 fund

managers, analysts, private equity firms and venture capitalists. They found that whilst having

significant IP assets is of value in itself, 95% of survey participants agreed with the view that “it

is not just having the IP, it is protecting and exploiting it that makes the difference”. Taking it

one stage further, over half say that it is not sufficient for a company simply to protect its IP, but

that IP protection should be used as part of a significant competitive strategy (Figure 5)41.

Figure 5:

It means that patents are valuable when they are incorporated into the overall company’s

strategy. Patents are regarded by investors as a necessary tool for protection but if they are not

managed by the company properly they are not much in focus for investors while valuing the

company. Management should be aware of the future potential of the patents and explore them 40 Ibid41 Howrey, A survey on Investor attitudes on IP protection 2001, pp. 1-16

56% 19% 22% 6%

0% 20% 40% 60% 80% 100% 120%

An importance of IP in assessmentof an investment

As part of Competitive Strategy

Ptotection Sufficient

It Varies

Don't Know

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 21 -

Only then could investors integrate such information into their business value model as they

know that management aware of company’s value driver.

“Despite the high value placed on IP strategy by survey participants, only one in three say

that they “always” or “usually” formally analyze and assess the value of a company’s IP when

they are looking to invest. This is more likely to be the case for those following Pharmaceuticals

or IT companies and infrequently those specializing in Consumer brands, Telecoms or Media,

where formal measurement may depend on the company involved”42.

It is very much dependent on which industry the company is operating in so that IP and

especially patents play a significant role for the value of the company itself and can be viewed as

a value added. But as already been said patents themselves do not have any value. Interviews

conducted by Munari and Oriani reveal the following significant information about how venture

capitalists approach patents and what they are looking for in the start-up companies in order to

make an investment decision43.

All the investors said that presence or absence of IP is the starting point and essential for

the value of start-ups. “Patents analyzed to determine its technical and legal validity, the value

added to the product in the end market by its utilization and its country coverage. Indeed, the IP

portfolio is fundamental to the competitive positioning and life cycle of a product in the

marketplace and, thus, the breadth and strength of the patent protection of the product itself and

the fence around it need to be analyzed” said one of the interviewees, a Partner in Sofinnova44.

Managing Director of Novartis Venture Fund attached big weight to patents as freedom

to operate. Recent Mergermarket survey confirms this statement: when valuing a target’s IP

assets, freedom to operate is the most important factor contributing to the value of IP (4,27

points out of 5)45.

Chief Technology Officer of TTVenture named IP as a “condition sine qua non” to invest

in a company “as it is the means to access the market and it offers barriers to entry, protection

and a tangible way of technological transfer”. But he mentions that patents per se have no value.

“We look at patents in conjunction with the company’s business model to verify the extent to

42 Ibid43 Munari, Oriani, The Economic Valuation of Patents. Methods and Applications, 1 edition, Edward Elgar

Publishing Limite, GBR, 2010, p. 28044 Interview with Partner in Safinnova conducted by Munari, Oriani.45 Brodowski, M&A Insights: Spotlight on Intellectual Property Rights, in: Mergermarket study in association with

CRA International and K&L Gates, December 2008, p. 9

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 22 -

which patents protect the core technology of the company and not only a marginal component”

he said46.

Venture capitalists do not adopt monetary techniques to determine patent value, though

patents can indirectly enter in the valuation of the entire company as demonstrated by the

interviews with Saffinova and TTVenture: “We do not evaluate each patent through quantitative

techniques, but we assess the value of the company as a whole. The presence of patent is only

condition to invest, but it is not an asset per se. Patents come with business models and patents

without entrepreneurs have no value because they do not generate cash flows. We perform an

economic valuation of the company through qualitative techniques (i.e. benchmarking with

industrial competitors or past performance) and quantitative tools like the net present value. We

assess the expected revenues, costs, investments, time of development, risk of both technical

failure and market competition and cost of capital. However, the value of a company depends

also on the value of its patents, calculated in terms of the net present value of the commercial

applications which takes into account the technical development risk, rate of market penetration,

price of product, market size/peak sales and length of product life”47.

From the conducted interviews it is obvious that patents are extremely important in the

screening and due diligence phases for VC firms. They are a prerequisite for the company’s high

valuation but do not constitute a separate part of it.

A survey conducted by the Institute of Intellectual Property tried to find what matters

institutional investors consider most important in terms of information on technology-based

intangible assets and whether they introduce such matters in their corporate valuation models.

All institutional investors in Japan were asked to answer some questions regarding this topic. As

a result of the survey, it was found out that special importance was attached to qualitative

information that indicates relationships with strategy and organization among information on

technology-based intangible assets48.

There are the following matters to which investors attach importance and thereby regard

company as a more valuable entity:

- “Manager’s proper analysis of own company’s advantage and duration on

terms of technological development

46 Interview with Chief Technology Officer TTVenture, conducted by Munari, Oriani47 Ibid48 Ban, Group on disclosure of technology-based intangible assets, in: IIP Bulletin 2003

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 23 -

- Understanding potential customers and properly analyzing market size in

terms of development of new technology and products

- Ratio of the sale of a new product in the total sales

- Being able to understand the use of new technology and products and

analyzing the scale and growth potential of the customer market

- Establishing guidelines for preventing the outflow of technology and trade

secrets and those for obtaining and managing intellectual property, as internal rules

- Link between corporate strategy and research and development/

technological development

- Organization that manages and strengthens intellectual property in the core

business

- Consistently analyzing research and development, strategy and domain

- Outline of intellectual property portfolio

- Distinctiveness of the core technology

- Period of accumulation of unique technology in the field in which the

company has competitive advantage

- Strategic obtainment of patents, including peripheral patents

- Reflecting advanced know-how and technology on product price

- Appropriately managing technology for globalization

- Clearly demonstrating vision and strategy concerning research and

development as well as technology

- Income from patent rights and its change

- Degree of dependence of income on the development of new products”49.

All this information plays a crucial role in valuing the company. It is interesting to see

whether this kind of information is captured by existing approaches to valuation which will

be discussed in the next chapter.

IV Existing approaches for patent valuation

“One would be hard-pressed to find a major investment bank that employs even one

individual with experience in evaluating patent portfolio, as matters stand now, due diligence

49 Ban, Group on disclosure of technology-based intangible assets, in: IIP Bulletin 2003

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 24 -

regarding patent assets is usually more myth than reality”50. It is mostly due to inadequacies in

patent valuation methodology51. Lognormal distribution of patent value, which is spreading the

valuation of patents across a large range of values, add a certain degree of difficultness in patent

valuation and choosing the right method for the valuation52.

Scientific literature represents several approaches on how to execute valuation of patents

and patent portfolio, but all of them have pluses and drawbacks, some of them are quite difficult

to implement. There is no universal approach to value patents although a lot of attempts have

been made to come up with a useful and manageable method. Already in October 2008 Italian

Ministry of Economic Development, the Italian Banking Association, the Italian Confederation

of Industry and the Conference of Rectors of the Italian Universities signed a cooperation

protocol on the financial and economic valuation of patents. Italy is therefore the first country in

Europe to provide an instrument for valuating patents shared by both public and private sectors53.

Not only in Italy had these initiatives taken place. Germany’s standards body, the Deutsche

Institut fur Normung (DNI), adopted a valuation standard PAS 1070 “General Principles of

Proper Patent Valuation"54. The PAS defines general principles and requirements for a reliable

and appropriate valuation of patents. Its main intention is to serve as a guideline for users of

patent value information, to enable a quality assessment of valuation reports and expert

appraisals. In June 2010 DIN published General Principles for monetary patent valuation55.

Although they are tools for patent valuation, they are not commonly in use.

50 Rivette, Kline, Discovering new value in intellectual property, in: Harvard Business Review 2000, Vol. 78, Issue

1, p. 66 51 Carte, The maximum achievable profit method of patent valuation, in: International Journal of Innovation and

Technology Management 2005, Vol. 2, Issue 2, p. 13552 Ibid53 Modiano, New protocol on patent evaluation, in: Managing Intellectual Property 2008, Issue 185, p. 7954 Wurzer, General principles of proper patent valuation: the forthcoming European Standard, in: Presentation in

Hungarian Patent Office, November 2008, available at

http://www.mszh.hu/English/ipv/IP_Valuation_Budapest_2008_Wurzer.pdf (last visited 20.07.2010)55 Available at http://www.nadl.din.de/cmd?artid=129173643&bcrumblevel=2&level=tpl-art-

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 25 -

1. Qualitative methods to value patents

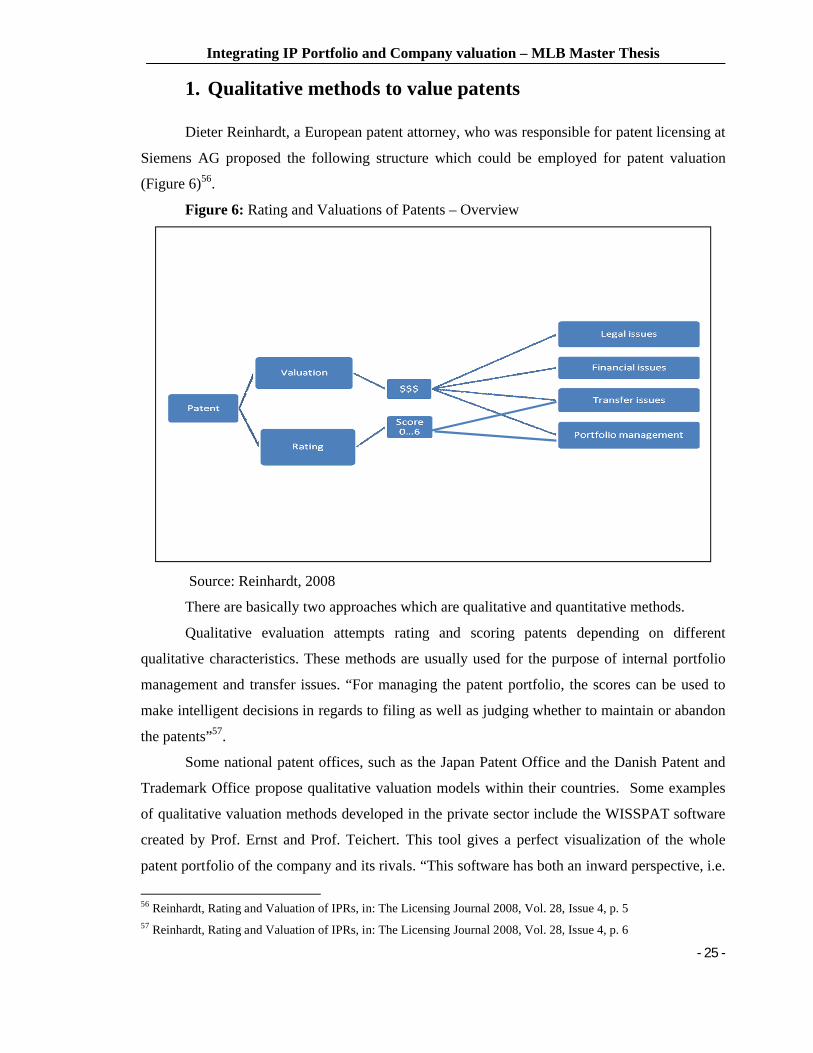

Dieter Reinhardt, a European patent attorney, who was responsible for patent licensing at

Siemens AG proposed the following structure which could be employed for patent valuation

(Figure 6)56.

Figure 6: Rating and Valuations of Patents – Overview

Source: Reinhardt, 2008

There are basically two approaches which are qualitative and quantitative methods.

Qualitative evaluation attempts rating and scoring patents depending on different

qualitative characteristics. These methods are usually used for the purpose of internal portfolio

management and transfer issues. “For managing the patent portfolio, the scores can be used to

make intelligent decisions in regards to filing as well as judging whether to maintain or abandon

the patents”57.

Some national patent offices, such as the Japan Patent Office and the Danish Patent and

Trademark Office propose qualitative valuation models within their countries. Some examples

of qualitative valuation methods developed in the private sector include the WISSPAT software

created by Prof. Ernst and Prof. Teichert. This tool gives a perfect visualization of the whole

patent portfolio of the company and its rivals. “This software has both an inward perspective, i.e.

56 Reinhardt, Rating and Valuation of IPRs, in: The Licensing Journal 2008, Vol. 28, Issue 4, p. 557 Reinhardt, Rating and Valuation of IPRs, in: The Licensing Journal 2008, Vol. 28, Issue 4, p. 6

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 26 -

the reassessment of the effectiveness and efficiency of companies’ current R&D policy, as well

as an outward perspective which focused mainly on the assessment of a potential target of

mergers & acquisition”58.

Another example of qualitative valuation includes the valuation tool called “PRISM”

developed by QED Intellectual Property. This tool classifies patents into four basic management

models, namely:

1. “Monopoly (patents for internal exploitation with high value)

For all these valuation models the patent value indicators need to be used.

Until today different patent value indicators were determined. Such as forward citations60

which show in which and how many younger patents, the patent in question was cited as peace

of prior art, backward citations61 which show the number and types of prior art documents cited

against the patent, family size62, which is the number of patents filed on the same invention in

other countries or regions. Reitzig identified these indicators as ”first generation” indicators of

patent value as they do not particularly involve in-depth knowledge of institutional details of the

patent system63. As a “second generation” he pointed out on patent-specific economic

considerations, such as referring to the filing strategy or the legal contents of backward citations.

Last and also a very valuable source of information are full-text documents themselves, which

58 Teichert, Text Mining for Technology Monitoring, in: IEEE IEMC 2002 White Paper, Institute for Innovation

Management59 Information-Technology Promotion Agency, Japan (IPA), Report of IPA Intellectual Property Study Group 2004,

IPA, Tokyo60 Trajtenberg, A penny for your quotes: patent citations and the value of innovations, in: Journal of Economics

1990, Vol. 21, Issue 1, pp. 172-187; Albert, Avery, Narin, McAllister, Direct validation of citation counts as

indicators of industrially important patents, in: Research Policy 1991, Vol. 20, Issue 3, pp. 251-259; Harhoff,

Scherer, Vopel, Citations, family size, opposition and the value of patent rights, in: Research Policy 2003, Vol. 32,

Issue 8, pp. 1343-136361 Narin, Hamilton, Olivastro, The increasing linkage between US technology and public science, in: Research

Policy 1997, Vol. 26, Issue 3, pp. 317-33062 Lanjouw, Schankerman, Characteristics of patent litigation: a window on competition, in: Journal of Economics

2001, Vol. 32, Issue 1, pp. 129-15163 Reitzig, Improving patent valuations for management purposes – validating new indicators by analyzing

application rationales, in: Research Policy 2004, Vol. 33, Issue 6/7, p. 942

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 27 -

are a “third generation” indicator for patent value64. Reitzig gives a good overview of the

established indicators of patent value and pointed out on the validity from the theoretical and

empirical point of view (Table 3)65.

Table 3: Established indicators of patent value

Variable Validity Availability in time(month after filing date)

Key inventors + + 18+(preliminary)b,ca.42+(finally)c ELegal disputes (opposition in particular)

++ +/- ca.42+(preliminary)b,ca.49+(finally)c

M,partially E

M: manual computation necessary; E: electronic computation possible.a(-) Weak; (+/-) Medium; (+) Strong; (++) Very strong.bInformation available after publication of application. Information can still change during the granting procedure.cLower bound.dDifferently computed indicators in different studies.Source: Reitzig 2004

While valuing patents there are different combinations of indicators which could be

employed. Different companies use different sets of indicators in order to find the value of

patents. For example, Zeebroeck use the following metrics for patent valuation: forward

citations, grant decisions, families, renewals and oppositions66. The reasons why those kinds of

value indicators were chosen are:

- “Have been found positively correlated with the value of patents in the

64 Ibid65 Ibid66 Zeebroeck, The puzzle of patent value indicators, in: CEB Working Paper No. 07/023, April 2009

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 28 -

literature

- Can be extracted from patent databases

- Could inform on the existence of a potential market for the invention”67.

Reinhardt in order to come up with a patent score group a number of indicators into the

bibliographic, procedural, content related, technological, and enterprise related factors68.

Bibliographic indicators could be identified from the data bases or the front page of the

patent. Into the bibliographical indicators he includes:

- patent age, which pointed out on the remaining lifetime of the patent

- forward citations

- backward citations

- key inventors.

Further, procedural indicators need to be identified such as:

- family size;

- legal status, which is status of the patents in the various patent countries;

- legal actions, patents that survived nullity actions or were successfully involve in

infringements suits

- patent procedure, patents were filed via European Patent Office (EPO), in accordance

with Patent Cooperation Treaty (PCT) or as national applications

The content related indicators include:

- number of patent claims

- number of categories in patent claims

- text elements

- number of words describing the object of the invention

- number of words describing the advantage of the invention

Then technological indicators add up to the overall value of the patent:

- technology

- number of patens in same IPC classes

- trend of patent filings in same IPC classes

- status of technology

And the last but not least group of indicators is enterprise related, which used to appraise

the enterprise that owns the patent:

67 Ibid68 Reinhardt, Rating and Valuation of IPRs, in: The Licensing Journal 2008, Vol. 28, Issue 4, p. 7

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 29 -

- ownership

- size and/or reputation of the company owning the paent

- market value of the enterprise

- Tobin’s Q, which is ratio of the market value of assets to the replacement costs of the

assets

- co-operations - number of R&D cooperations69.

After all the indicators were identified they were integrated into the key factors which

are legal position, difficulty of designing around, proof of infringement and technological

position of the patent. All key factors get weighted and receive a score from one to six where

six stands for the highest value. All these scores need to be compiled into the final score of

the patent and show the patent quality. As stated by Reinhardt, only a few patents have low

and high score, while the lion’s share of patents have a medium score around three70.

Prof. Ernst takes one step further and suggests to analyze the dynamic development of the

indicators over time integrating them into the patent portfolio71.

Even though this kind of information appears more valuable to the management of the

company in their decisions on investment of R&D resources, it could also be useful to the

investors who are interested in the companies with a potential where patent portfolio could

perfectly visualize company’s competitive position and possible future revenue generation.

Finn Valentin and Rasmus Lund Jensen, for example, emphasize the need to assess not

only patents alone but a patent portfolio as a whole in terms of the complementarities between

multiple patents. They examine effects of the configuration of patents, which are thickets

(consist of a large number of heterogeneous patents, brought together by the complementarity

roles for the same focal technology), fence (functionally similar patents) and scope related

configurations on firm value72.

Even though theoretically there are a lot of approaches that were developed in order to

value patents and patent portfolios from the qualitative side, there is an obvious gap between

theory and practice meaning that they are hardly implemented not only by management of the

companies but also by investors during their valuation of the companies.

69 Ibid70 Ibid71 Ernst, Patent information for strategic technology management, in: World Patent Information 2003, Vol. 25,

Issue 3, p. 23572 Finn, Rasmus Lund, Patenting strategies and valuation of science-based start-ups, in: Annual Conference of the

EPIP Association, Sept. 2009

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 30 -

2. Quantitative approaches for patent valuation

The monetary or quantitative perspective of patent valuation represents three “classic”

approaches: income, cost and market-based approaches. They are most commonly used for

patent appraisal even though they have a lot of shortcomings when applied to patent valuation.

There are also more sophisticated methods: the relief from royalty, the technology factor, the real

options, and the Monte Carlo simulation methods. The following is a brief overview of these

approaches:

2.1 Cost based method

The cost-based method aims at determining a patent's value by defining the

necessary development costs for the product covered by the patent73. The costs include the cost

of developing the invention, as well as the cost of patenting the invention. This method can be

used to set a lower limit of patent value74. Within the cost approach one can look at the

reproduction costs, the replacement costs, the historic costs, and the avoided costs. “The

reproduction costs are the costs of an exact replica of the subject matter of the patent, whereas

the replacement costs are the costs of a subject matter having the functionalities claimed in the

patent. The historic costs of the patent include the development costs of the relevant portions of

the product or process covered by the patent and the related patent costs. Finally, the avoided

costs are the costs that a patent owner can save by owning the patent. This can be in the form of

future royalties that the owner otherwise would have to pay to a licensor”75.

One of the advantages of this method is that IP becomes visible in the company’s books

and IP awareness is increased. “The method is also a useful indicator of IP value in the case of IP

assets whose future benefit is not yet evident”76. Further cost based measures are objective and

consistency can be achieved and if a recent acquisition cost of a patent exists it is a reliable

indicator of value. There are several disadvantages which should be taken into account. There is

73 Sherry, Teece, Royalties, evolving patent rights, and the value of innovation, in: Research Policy 2004, Vol. 33,

Issue 2, pp. 179–191.74 Carte, The maximum achievable profit method of patent valuation, in: International Journal of Innovation and

Technology Management 2005, Vol. 2, Issue 2, p. 13675 Reinhardt, Rating and Valuation of IPRs, in: The Licensing Journal 2008, Vol. 28, Issue 4, p. 1576 Valuation of intellectual property, in: IP for Innovation Handbook (ip4inno), p. 6

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 31 -

no direct correlation between cost of development and the future revenue potential of assets77. In

addition, it can be problematic to properly assign accumulated costs to a single intangible asset78.

As a result the cost based approach is used only in limited circumstances. The cost

approach is most suitable for valuation for financial accounting and corporate tax purposes79.

Cost is, however, a relevant benchmark where a patent has recently been acquired80.

2.2 Market based method

The market-based approach tries to value a patent by referring to similar transactions that

have occurred recently, for example, the patent value is determined by comparing the patent to

similar patents that were sold in the past81. This approach comprises a plurality of methods,

namely, a transaction oriented, a price oriented, a profit oriented and a license based method.

These methods are very similar and only distinguishable with respect to the criteria used for the

comparison. “In the transaction oriented method one tries to identify the financial terms for

transactions of comparable patents and in the profit and price oriented methods one tries to find

the financial terms of transactions generating the same price, respectively. In applying the license

agreements based method one is looking for concluded license agreements in which either a

comparable patent was licensed, or in which royalties were paid that correspond to expected

royalties. In both cases the focus is on finding a royalty rate that is accepted in the market”82.

The advantage of this method is that it makes use of prices actually paid for comparable

assets and the variety of market based approaches gives flexibility in comparison. This approach

is easy to use if the market exists. But the main disadvantage is that the unique features of a

77 Pitkethly, The valuation of patents: A review of patent valuation methods with consideration of option based

methods and the potential for further research, in: Judge Institute Working Paper WP 21/97, Cambridge, The Said

Business School, University of Oxford78 Achleitner, Nathusius, Schraml, Quantitative valuation of Platform Technology Based Intangibles Companies, in:

Working Paper No. 2007-02, Center for Entrepreneurial and Financial Studies 79 Kamiyama, Sheehan, Martinez, Valuation and exploitation of intellectual property, in: STI working paper 2006/5,

p.27 (1-48)80 Zieger, Scheffer, Methods for Patent Valuation, Presentation at EPO-OECD-BMWA International Conference on

Intellectual Property as an Economic Asset: Key Issues in Valuation and Exploitation, 2005, available at

http://www.oecd.org/dataoecd/34/63/35428822.pdf (last visited 28.07.2010)81 Arora, Fosfuri, Gambardella, Markets for technology: the economics of innovation and corporate strategy, in:

MIT Press, Cambridge, 2001.82 Reinhardt, Rating and Valuation of IPRs, in: The Licensing Journal 2008, Vol. 28, Issue 4, p. 16

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 32 -

specific patent cannot be compared in the same way and consequently could be priced wrongly.

This could lead to an undervalue or contrary overvalue of the patent.

2.3 Income based method

The income-based approach considers a patent's possibility to provide an economic

benefit in the form of cash flows. With this approach, future cash flows are estimated and then

discounted83. Discounted Cash Flow (DCF) method is one variety of income-based approach.

With the DCF method, the patent value is calculated as the present value of future cash flows.

The present value of cash flows is calculated by applying a discount rate which adequately

reflects the cost of capital. Consequently, the DCF method requires three major components: the

forecast cash flow, the projected economic life of specific projects and IP, and the appropriate

cost of capital84.

Although DCF method does attempt to determine an economic value of a patent, it does it

in a very limited way because many of the factors that determine the ability of a patent to

generate profit are not explicitly considered85. But inspite of having these drawbacks it is one of

the most commonly used to value patents as it is widely understood.

After making an overview of most commonly used approaches it would be relevant to

point out on their shortcomings which arise when valuation of patents is needed. It seems that

these approaches are able to capture only half of the value of a patent. The cost approach, for

example, does not consider future cash flows generated from the patented technology. Even

though the income based approach covers this gap, it does not take into account the cost of

developing technology in the valuation technique. These methods do not account for all of the

known factors which affect the value of a patent such as patent breadth, novelty and the like,

which accounted in qualitative approaches for patent valuation but should also be considered in

the quantitative approaches too. It is worth mentioning that these methods do not value the patent

per se but patented technology, which sometimes could be misleading. The value of a patent is

83 Amram, The challenge of valuing patents and early-stage technologies, in: Journal of Applied Corporate Finance

2005, Vol. 17, Issue 2, pp. 68–81.84 Brealey, Myers, Principles of Corporate Finance, 5 edition, McGraw-Hill Companies, 199685 Carte, The maximum achievable profit method of patent valuation, in: International Journal of Innovation and

Technology Management 2005, Vol. 2, Issue 2, pp. 135–151

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 33 -

not always equal to the value of patented technology; usually value of patents is higher86. Only in

some industries, like in pharmaceuticals, where patents are a prerequisite for successful R&D,

the value of the patent could be equal to the value of the project87. That is why to employ these

approaches to evaluate patents could be not as sufficient as the ones examined further.

2.4 Other methods

More sophisticated and thus not commonly used approaches are the following.

The relief from royalty approach is similar to the income approach with the only

difference that the present value of cash flows is multiplied by an appropriate percentage royalty

rate. Thus, this method measures the royalty fees that a company does not have to pay to a third

company because it actually owns the patent88.

The technology factor approach is also based on the income approach, but it defines an

upper limit of maximum achievable income with the patented technology, which is then

shortened by competitive attributes in order to derive the expected income89.

“The income approach with its discounted cash flow method and the approaches based

around it have to be seen as “now or never” propositions, i.e., the firm has to decide in the

beginning whether it wants to perform the investment and if it does, it can no longer change its

strategy. If a firm does not invest, the investment opportunity is lost for future periods”90. There

are no other options and these neglects the value of flexibility in investments decisions91.

Comparably, the option based approach gives this “flexibility”. Patent evaluation based

on real options is similar to the income approach, but it is less static and firms can change their

86 Ernst, Legler, Lichtenthaler, Determinantsof patent value: Insights from a simulation analysis, in: Technological

Forecasting and Social Change 2010, Vol. 77, Issue 1, pp. 1-1987 Ibid88 Sherry, Teece, Royalties, evolving patent rights, and the value of innovation, in: Research Policy 2004, Vol. 33,

Issue 2, pp. 179–19189 Carte, The maximum achievable profit method of patent valuation, in: International Journal of Innovation and

Technology Management 2005, Vol. 2, Issue 2, pp. 135–15190 Ernst, Legler, Lichtenthaler, Determinantsof patent value: Insights from a simulation analysis, in: Technological

Forecasting and Social Change 2010, Vol. 77, Issue 1, pp. 1-1991 Bloom, Reenen, Patents, real options and firm performance, in: The Economic Journal 2002, Vol. 112, Issue 448,

pp. 97–116

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 34 -

behavior and strategy92. But still the option based approach remains static, even though it

employs more realistic assumptions93. In the contrary, the Monte Carlo approach allows for

explicitly considering the risk and uncertainty about predictions of the future94.

All of the valuation methods that have been presented above tend to have one of two limitations.

They are either overly simplistic by making unrealistic assumptions or too complex to be applied

in many managerial settings in reality95. By contrast, the real options and Monte Carlo

simulation models are more realistic because they capture costs and revenues as well as risk and

uncertainty96. However, these models often become very complex when applied to real world

settings97.

The Mergermarket survey confirmed that in practice the DCF approach is the most

frequently used approach. Second approach after the DCF is comparable transactions, which is

market based approach, where comparable transactions used in order to identify the value of IP.

On the third position is cost based approach, which is misleading as this approach one of the less

likely to capture the real value of IP, but has a good rating. The fourth place reserved by

probability or decision tree approach, which is more suitable for the IP valuation as it take into

account various possibilities or probabilities which could be employed through the patent life.

But as one can see this approach not frequently used and it ranked as a less important from the

point of view of valuators. Most difficult in terms of implementation, but most appropriate for

the IP valuation is option based approach and Monte Carlo simulations which received the last

two positions in the Figure 7. Thus the valuation experts and the IP experts must work together

92 Adner, Levinthal, What is not a real option: considering boundaries for the application of real options to business

strategy, in: Academy of Management Review 2004, Vol. 29, Issue 1, pp. 74–8593 Kogut, Kulatilaka, Real options pricing and organizations: the contingent risks of extended theoretical domains,

in: Academy Management Review 2004, Vol. 29, Issue 1, pp. 102–11094 Ernst, Legler, Lichtenthaler, Determinantsof patent value: Insights from a simulation analysis, in: Technological

Forecasting and Social Change 2010, Vol. 77, Issue 1, pp. 1-1995 Carte, The maximum achievable profit method of patent valuation, in: International Journal of Innovation and

Technology Management 2005, Vol. 2, Issue 2, pp. 135–15196 Vassolo, Anand, Folta, Non-additivity in portfolios of exploration activities: a real options-based analysis of

equity alliances in biotechnology, in: Strategic Management Journal 2004, Vol. 25, Issue 11, pp. 1045–106197 Carte, The maximum achievable profit method of patent valuation, in: International Journal of Innovation and

Technology Management 2005, Vol. 2, Issue 2, pp. 135–151

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 35 -

to ensure that both groups note all the risks facing the company and the effect that those risks

will have on the valuation98.

Figure 7: When you explicitly value IP assets, how often do you use the following

valuation techniques?

Source: A Mergermarket study in association with CRA International and K&L Gates, 2008

In order to capture the advantages of two approaches, the real options approach and

Monter Carlo simulations were combined to give a new approach for patent valuation99. The

real option approach in this case takes into account uncertainty about future value and Monte

Carlo simulations help to estimate the value. This new approach attempts to bridge the gap

between the closeness to reality and managerial applicability in patent valuation. Patent value is

identified as a surplus in profit that derives from comparing a specific R&D project with patent

98 Brodowski, M&A Insights: Spotlight on Intellectual Property Rights, in: Mergermarket study in association with

CRA International and K&L Gates, December 2008, p. 1099 Ernst, Legler, Lichtenthaler, Determinantsof patent value: Insights from a simulation analysis, in: Technological

Forecasting and Social Change 2010, Vol. 77, Issue 1, pp. 1-19

3,92 3,512,67 2,28 2,00

1,49

00,5

11,5

22,5

33,5

44,5

Nev

er

A

lway

s

Frequency of valuation technique

Frequency of valuation technique

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 36 -

protection and the same project without patent protection100. Consequently this approach

evaluates a patent per se.

After over viewing all the approaches for patent and patent portfolio valuation the attempt

to find out how practically investors proceed with patent portfolio valuation while conducting

assessment and valuation of the company was undertaken. The next chapter strives to answer the

following questions:

- What are the determinants that influence on the decision of investors whether to include

information about patent’s value into the overall value of the company?

- Whether the type of investor makes difference while valuing company which comprises

IP?

- What are the main trends in valuing patents? Do they get valuated by the investors at all?

- What are the approaches used by investors while valuing patents?

100 Ibid

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 37 -

Chapter 3

I Determinants influencing investor’s decision in valuing IP portfolio

A number of interviews were conducted with analysts and investors on the question how

investors integrate IP portfolio into the company valuation. The following findings were

revealed:

1. It is very much dependant on the industry in which the company operates

whether IP will be integrated by the investors into the overall valuation of the company.

It was documented by scholars that patent strength varies between industries in such that

in most industries patents are less featured that other means of protecting innovation101. Meaning

that they do not have a lot of weight in the company valuation and investors do not integrate this

information in their value model. Results of the 2008 Berkeley Patent Survey confirm that the

importance of patents to investors depends on the industry. Among biotechnology firms, for

instance, respondents were much more likely to reveal that commercial banks considered

patenting by the target firm important (43%) than software firm respondents (13%), investment

banks consider patenting in biotechnology more important (62%) compare to software (36%)102.

It is obvious that when a patent is essential for protecting patented technology it gets

accounted by the investor. In order to confirm this statement an interview with a pharma analyst

was conducted.

Interview with pharma analyst:

Pharma analyst from the investment bank pointed out that patents play a crucial role in

the pharmaceutical industry as they are the proxy for the future generation of cash flow and they

protect a new drug from the intervention of generics before the patent expiration. The analyst

stated that they do not value patents separately but they give them a rating as strong or a weak

patent which will be reflected in the overall value of the company. They divided patents in to

composition of matter patents and formulation patents. The United States Supreme Court has

defined "composition of matter" to mean "all compositions of two or more substances and all 101 Levin, Klevorik, Nelson, Winter, Appropriating the returns from industrial research and development, in:

Brookings Papers on Economic Activity 1987, Issue 3, p. 793 102 Graham, Merges, Samuelson, Sichelman, High technology entrepreneurs and the patent system: results of the

2008 Berkeley patent survey, available at http://ssrn.com/abstract=1429049 (last visited 01.06.2010)

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 38 -

composite articles, whether they be the results of chemical union, or of mechanical mixture, or

whether they be gases, fluids, powders or solids”103. From the words of the analyst formulation

patents are the patents which are granted after the expiration of the composition of matter patents

and aim to prolong patent protection in the markets for their pharmaceutical products.

Composition of matter patents is regarded as a strong protection from the generic drugs and they

receive a high ranking compare to the formulation patents, which will appear in the higher value

of the company. If a company has a composition of matter patent it will have a strong bargaining

power in terms of higher pricing of the company.

That is the only qualitative approach to value patents which was employed by the analyst.

To measure the value of the company analysts need to estimate future revenues and margins of

all the products in order to calculate future cash flows. For this, they have to model the impact of

patent protection on the overall value of the company. What is taken into account is that

composition of matter patents are stronger and hence difficult to challenge what lead to higher

protection from the rivals, higher future cash flows, which consequently makes the value of the

company higher. On the other side, reformulation patents can be more easily challenged which is

taken into account accordingly.

Early stage companies, for example biotechnology companies, which do not generate

revenues are very often evaluated in accordance with a real option approach. Pharma analyst said

that by using this approach it is possible to capture some uncertainties concerning patents, this

approach more flexible compare to others. But as was pointed out by the analyst there is no one

right approach to value the company and approaches vary from analyst to analyst. Some analysts

use net present value (NPV) of future cash flows with using probability adjustments for the

particular stage of development. As was explained, there are several stages in drug development

with a different level of probability whether the product will be launched on the market. For

example, if a drug is in phase one of development the probability that this particular product will

get to the market is only 10-20%, versus 70-90% if the drug is in phase three. These probabilities

vary according to indications and results available. The NPV in each stage is determined and the

expected net present value (ENPV) is calculated by taking the sum of the product of different

NPVs and the likelihood of their occurrence. But as plain NPV method is too static for the patent

valuation the probability adjustments need to be implemented.

103 Diamond v. Chakrabarty, 447 U.S. at 308 (1980)

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 39 -

From the point of view of the interviewed analyst modeling scenarios using both NPV

without probability adjustments and real option valuations are more useful as it is a yes or no

game.

From the interview it can be seen that not only one approach could be implemented in

order to value IP, but a combination of approaches depending on the stage of the project valued.

As was observed, when the project is not generating cash yet, the real option approach is

applicable. As soon as the constant revenue stream established, modeling scenarios using NPV

come into play. One should point out that the patent per se is not valued, the whole accent is on

the future cash flow of the patented technology, which is understandable as it is something

certain but one should also admit that patents are the essential value added and in the case with

pharma analyst not taken fully into account.

Interview with a venture capitalist:

As was discussed with the venture capitalist, the industry in which the company is

operating has a definite influence whether IP portfolio will be integrated into the overall value of

the company. In some industries it is very important to have a protection, patents for example, in

order to keep competitors on an arm length distance and have exclusive rights for the generation

of the future cash flow. The example of pharmaceutical companies was made. For these types of

companies patents are an inevitable part of the business and their existence gives a higher value

to the company. They most probably will be valued separately as they started to be regarded as

an asset of the company if they generate revenue through the products which have patented

technology or if they simply licensed to other companies.

This shows that investors already start to see patents not only as a legal tool for protecting

technology, but a business asset which could be employed in different company strategies like

licensing, cross-licensing, can be used as a bargaining chip and the like.

On the question how venture capitalists would include the value of patents into the

overall value of the company, the answer was that they usually do not integrate the value of the

patents per se but they look on their presence in the firm and their quality whether they can keep

rivals on the distance, whether the company having them has freedom to operate. Venture

capitalists said that they do not put a price tag on patents but they keep them in mind while

valuing the company. If the company has a sophisticated and well developed patent portfolio

which is managed on a constant basis, meaning that it would be hard for the investor to assess all

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 40 -

of it, he would probably ask for professional advice in order to value it. But it is very rare that

start-ups have a sophisticated patent portfolio in the early stage of development.

From this interview it is obvious that patents are the soft factor in company valuation,

meaning that they just one of the factor which add value to the company during its due diligence

and viewed by the investor as necessary part of the company, but they do not valued separately.

And as was discussed in this section industry in which company is operating add certain degree

of importance whether patents will be valued or not.

2. It is very much dependant on the type of investor whether information about IP

will be integrated into the company valuation.

Another observation which became uncovered during the conducted interviews is that is

not only industry which has influence whether patents will be valued or not and in which extent,

but also the type of investor plays a cruscial role in this process.

The study of Munari and Toschi revealed that Venture Capitalists (VCs), professional

intermediaries, and Corporate Venture Capitalists (CVCs), non-financial entity, differ in their

valuation ability. As CVCs possess more internal expertise and knowledge that can be leveraged

in the course of the due diligence process, they therefore develop more expertise in the valuation

of specific technological capabilities of the company and consequently while making their

investment decisions they measure technological content and quality of patents104. It shows the

general tendency that it is dependent on the ability of the investor and his qualification to value

patents and patent portfolios of the company and therefore include this information into their

valuation model of the whole company. A high degree of investor specialization plays an

important role in this process. It helps to reduce information asymmetry and uncertainty in the

valuation process. This held true not only among VCs and CVCs but institutional investors also.

The observation from the own held interviews obviously shows that venture capitalists do

not evaluate IP portfolios separately from the overall value of the company. His observation

mostly cover VCs. They rarely employ qualitative approaches as they leave it to the management

of the company. Quantitative approaches could take place if the patents are exploited and

generate revenue for the company. Investors look at the technology which a company owns and

104 Munari, Toschi, The relationship between patent portfolios and VC investments: the case of nanotechnology, in:

4th Annual Conference of the EPIP Association “Measuring the value of IPRs: theory, business practice and public

policy”, September 2009

Integrating IP Portfolio and Company valuation – MLB Master Thesis

- 41 -

whether patents can be helpful to maintain this technology and create free environment to

operate.

From the institutional investor point of view as they do investments in more mature

companies with a large patent portfolio they try to implement sophisticated approaches to value

it in order to reduce all the risks associated with it. As was found from the interview with the

pharma analyst the companies comprised patents get valuated with an option based approach,

which is considered to be comparably difficult to implement in contrast to the income based

approach for example. This shows that IP receives a growing importance in the company and

already more appropriate approaches are employed for their valuation. As was previously

discussed the option based approach dominates over other approaches as it allows to consider

different sources of uncertainty that characterize both patents and investment opportunities

linked to them.

As a result one could make a conclusion that it depends on the type of investor whether

IP valuation will be integrated into the overall value of the company and how it will take place.

Some investors have a specific expertise and can implement it into their valuation model, but as

long as they are not fluent in the valuation of technology-based company it could be a risky