40

Integrating Prepaid into Your Overall Payments Strategy Overall Payments Strategy Dan Horne, Chief Knowledge Officer, Global Prepaid Exchange Ralph Calvano, SVP/GM, FIS Prepaid Solutions

| Date post: | 16-Mar-2018 |

| Category: |

Documents |

| Upload: | nguyenthuy |

| View: | 221 times |

| Download: | 3 times |

Integrating Prepaid into Your Overall Payments StrategyOverall Payments StrategyDan Horne, Chief Knowledge Officer, Global Prepaid Exchange

Ralph Calvano, SVP/GM, FIS Prepaid Solutions

Agenda

• Dan Horne

Chief Knowledge Officer, Global Prepaid ExchangeThe prepaid opportunity– The prepaid opportunity

– Prepaid market update

– Global prepaid adoption

Challenges and opportunities– Challenges and opportunities

• Ralph Calvano

SVP/General Manager, FIS Prepaid Solutions– Market trends

– The prepaid value chain

– Prepaid strategy integration

– Critical success factors

2

Integrating Prepaid with Your Integrating Prepaid with Your Overall Payments Strategyy gy

Dan HorneChief Knowledge Officer, Global Prepaid Exchange

dan horne@globalprepaidexchange [email protected]

Our PlanOur Plan

» I will provide some background on prepay » I will provide some background on prepay and how it is working here and in different

kmarkets.

» Ralph will discuss the powerful benefits that stem from integrating prepaid products into stem from integrating prepaid products into your current offering.

» We will finish by addressing any questions.y g y q

Lots of Hype!Lots of Hype!

5% of all consumer spending – Growing to 20%!!

The ProblemsThe Problems

f l» Definitional» What exactly is “Prepaid?”y p

» Lack of Validation

» Purpose of the Researchp

Still there is huge opportunityStill, there is huge opportunity

» Instead of getting caught up in the hype» Successful business cases have been based on recognition of gaps in the market» Demonstrable cost savingsg» Noticeable end‐user benefit

» Patience is a virtue» Profits come with scale» Profits come with scale» Scale is often slow to materialize

» Awareness, TRUST, Trial, Repurchase/Reuse» Awareness, TRUST, Trial, Repurchase/Reuse

Organising the AppsOrganising the Apps

» Consumer‐ loaded» Gift» MobileGPR» GPR

» Travel/FX» Remittance» Specialty marketsp y

» Teen

Business Case Built on Relative Advantage

» Differing benefit structures» Security – especially vis‐à‐vis cash » Security – especially vis‐à‐vis cash » Convenience – e.g., travel FX» Accounting – tracking and budgeting» Access – purchases in the virtual worldp» Risk avoidance and choice» Personal information security» Personal information security

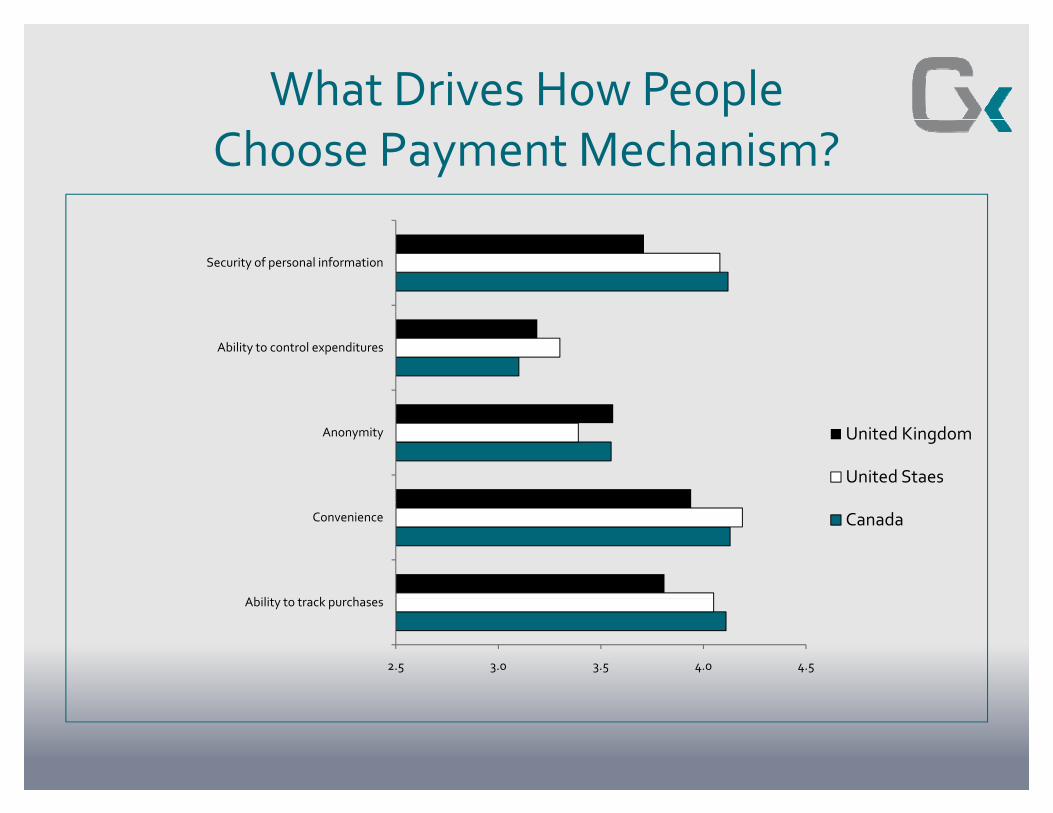

What Drives How PeopleChoose Payment Mechanism?

Security of personal information

Ability to control expenditures

Anonymity United Kingdom

United Staes

Abilit t t k h

Convenience Canada

2.5 3.0 3.5 4.0 4.5

Ability to track purchases

Organising the AppsOrganising the Apps

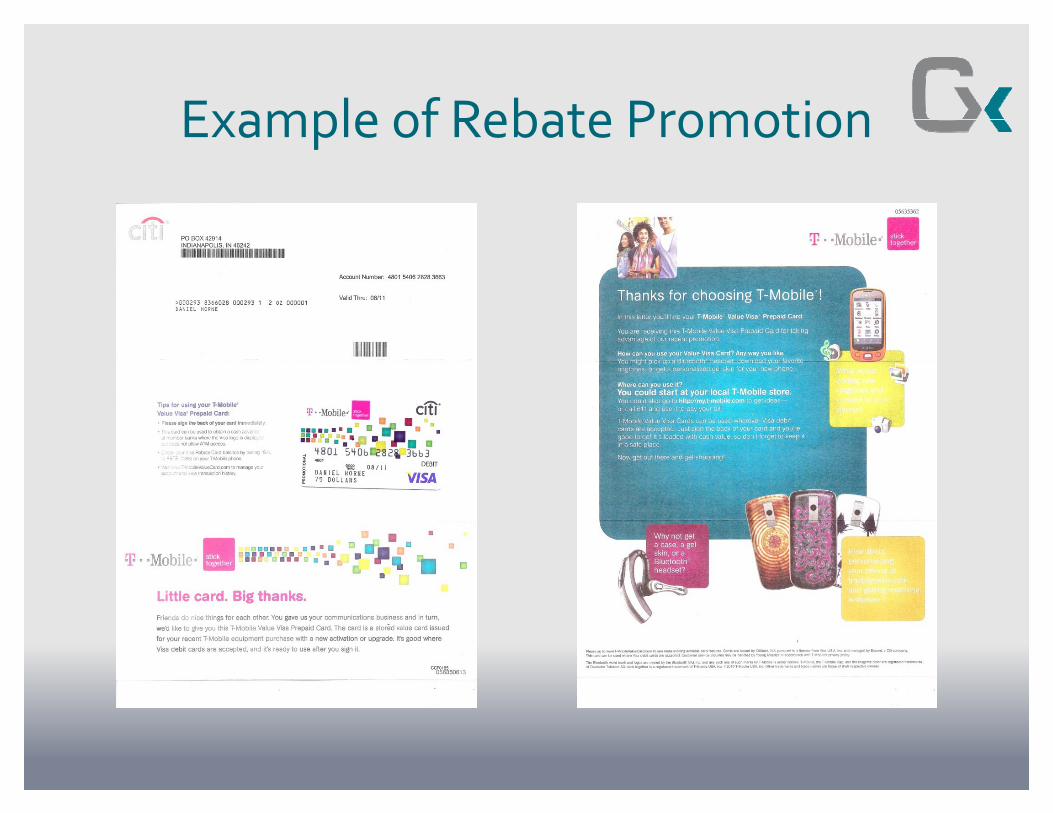

» Corporate loaded» Payrolly» Promotions

» Rebate» Rebate

» Purchasing» Insurance

Example of Rebate PromotionExample of Rebate Promotion

Organising the AppsOrganising the Apps

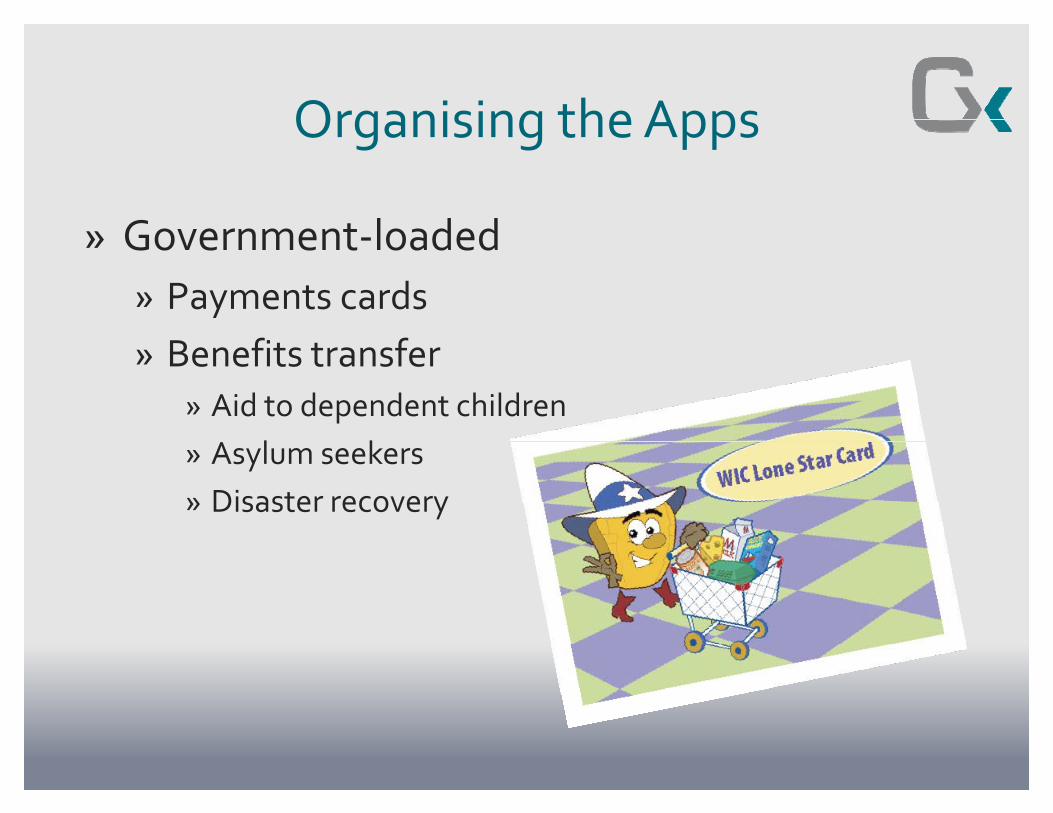

» Government‐loaded» Payments cardsy» Benefits transfer

» Aid to dependent children» Aid to dependent children» Asylum seekers» Disaster recovery» Disaster recovery

B i C B il C R d iBusiness Case Built on Cost Reductions

» Prepaid is an extension of electronic paymentsp y» Reduction in the physical

» Speed and distribution advantages» Speed and distribution advantages» Recurring payments

» Reduction in risk» Reduction in risk

Where in the world?Where in the world?

» Again, markets are app dependent

» Different countries may see different d d di i products depending on circumstances

EuropeEurope

» UK – gift, insurance, gov’t benefits, g ,travel

» France meal » France – meal vouchers

» Italy –GPR» Emerging markets –» Emerging markets –remittance,

di GPRspending, GPR

OthersOthers

» South America» South America» Promotions» Remittance

» Africa» Mobile » Mobile payments

» India» Travel/FX

Changing DeliveryChanging Delivery

» EGCs – (codes)» E‐mailed» Amazon and iTunes

» Mobile» Many applications» Few have made a mark

» Safaricom, SMART money and G Cash

ChallengesChallenges

» Regulatory» US» EuropeElsewhere» Elsewhere

» Distribution

» Consumer Acceptance

Questions and Comments:Questions and Comments:

Dan Hornedan horne@globalprepaidexchange [email protected]

www.globalprepaidexchange.com+1 401 499 1250

Integrating Prepaid with Your

Ralph Calvano

Integrating Prepaid with Your Overall Payments StrategyRalph Calvano

SVP/GM, FIS Prepaid Solutions

954 556 2200954.556.2200

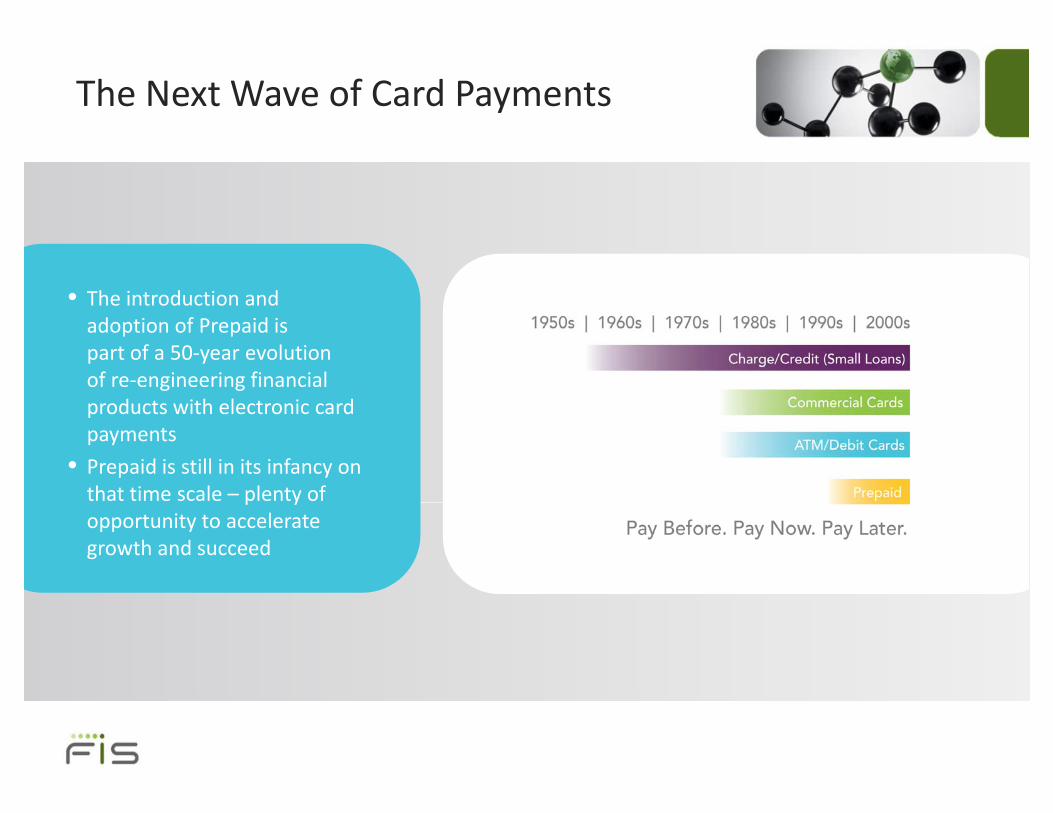

The Next Wave of Card Payments

• The introduction and adoption of Prepaid is part of a 50‐year evolution of re‐engineering financial products with electronic cardproducts with electronic card payments

• Prepaid is still in its infancy on that time scale – plenty of p yopportunity to accelerate growth and succeed

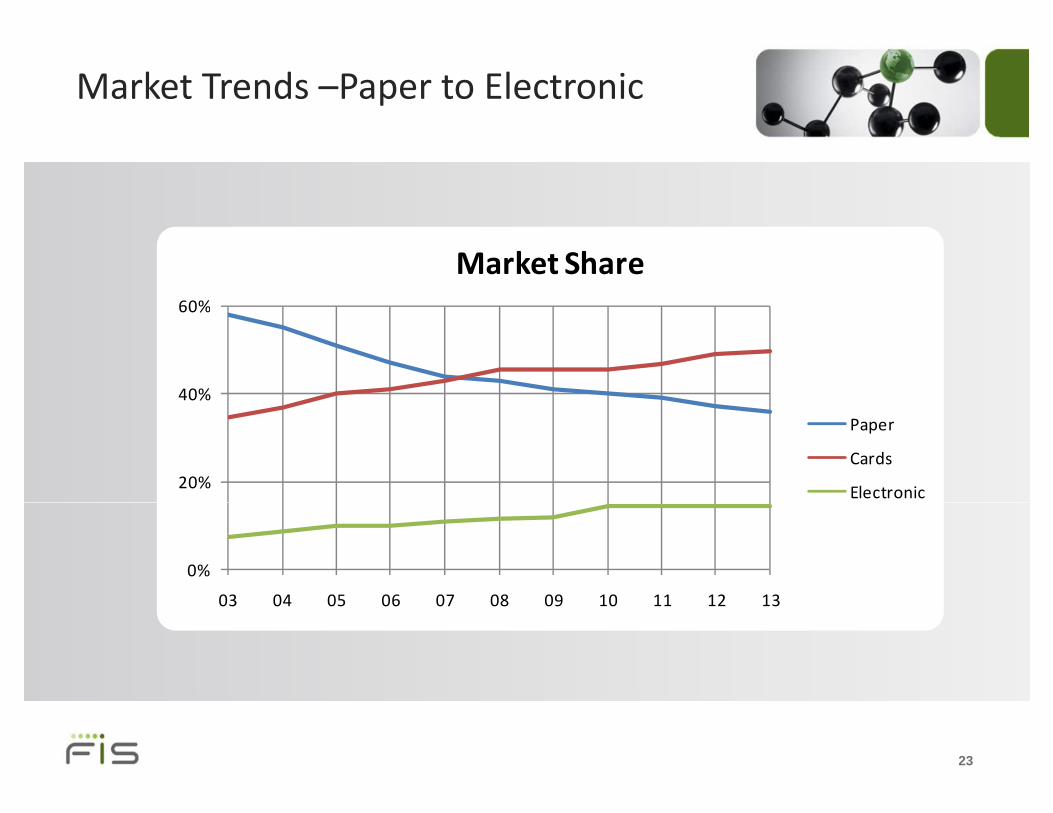

Market Trends –Paper to Electronic

60%

Market Share

40%

60%

20%

Paper

Cards

Electronic

0%

03 04 05 06 07 08 09 10 11 12 1303 04 05 06 07 08 09 10 11 12 13

23

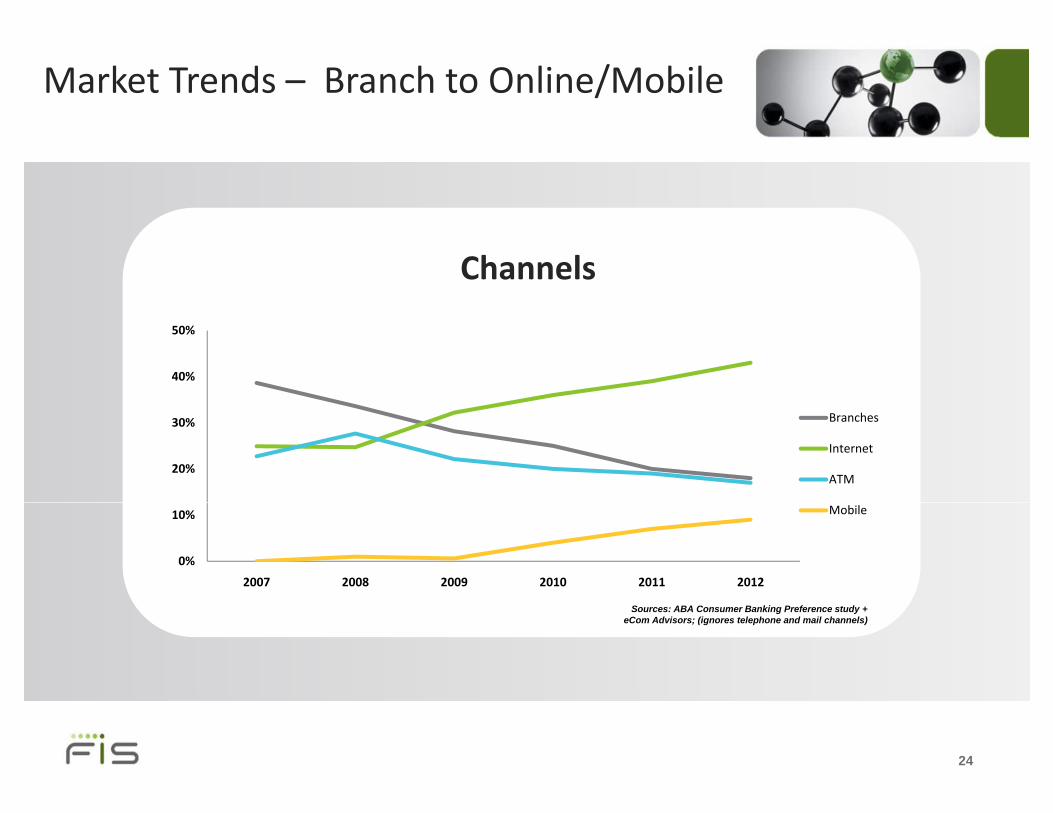

Market Trends – Branch to Online/Mobile

Channels

40%

50%

20%

30% Branches

Internet

ATM

0%

10%

2007 2008 2009 2010 2011 2012

Mobile

Sources: ABA Consumer Banking Preference study + eCom Advisors; (ignores telephone and mail channels)

24

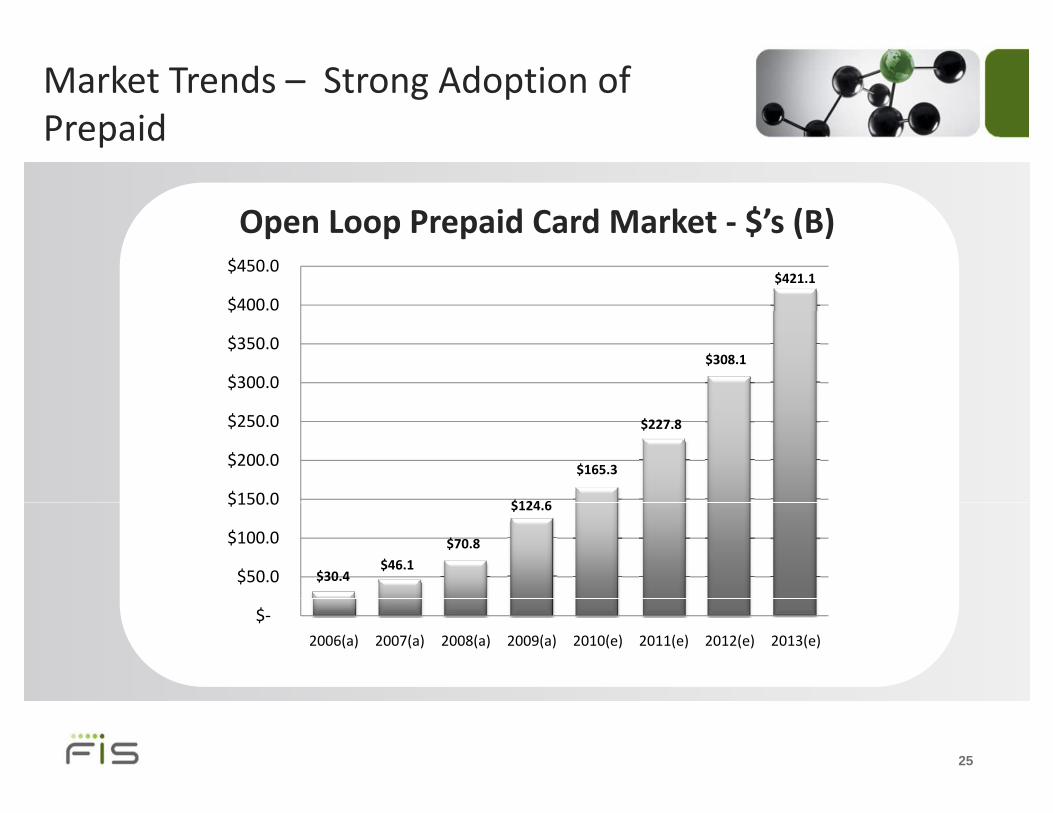

Market Trends – Strong Adoption of P idPrepaid

O L P id C d M k t $’ (B)Open Loop Prepaid Card Market ‐ $’s (B)

$400.0

$450.0 $421.1

$300.0

$350.0

$

$308.1

$150.0

$200.0

$250.0

$124 6

$165.3

$227.8

$50.0

$100.0

$150.0

$30.4$46.1

$70.8

$124.6

$‐2006(a) 2007(a) 2008(a) 2009(a) 2010(e) 2011(e) 2012(e) 2013(e)

25

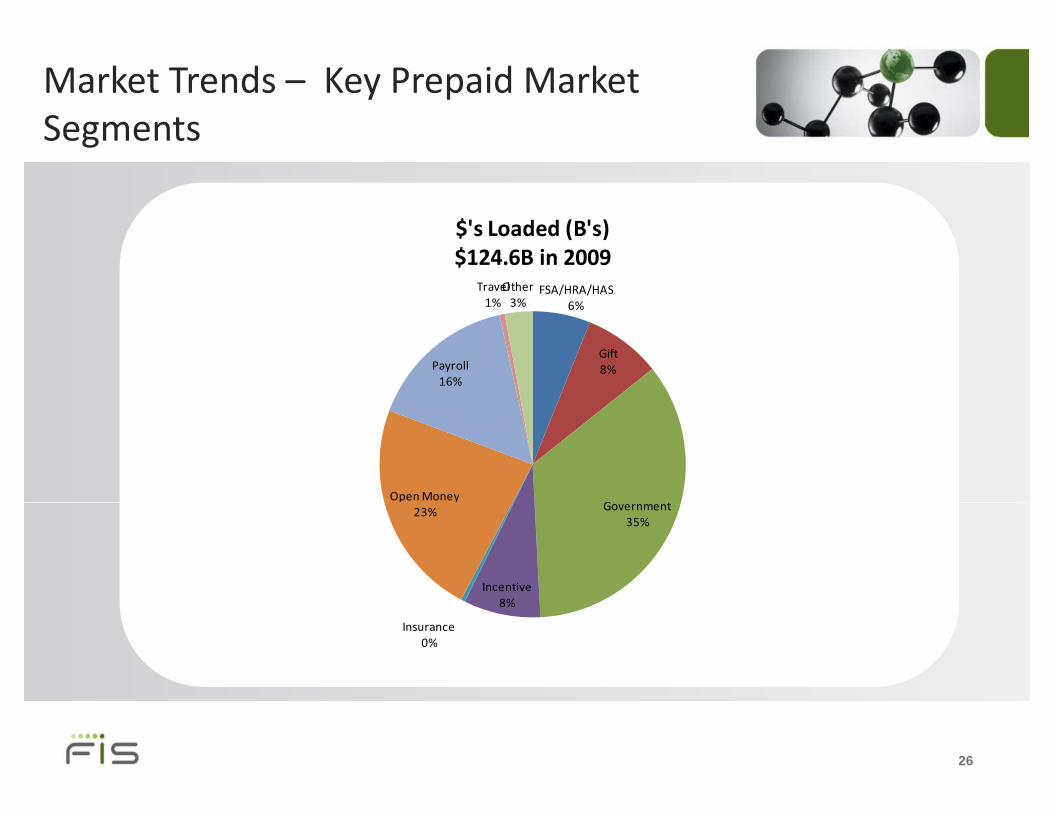

Market Trends – Key Prepaid Market S tSegments

FSA/HRA/HAS6%

Travel1%

Other3%

$'s Loaded (B's)$124.6B in 2009

Gift8%Payroll

16%

G tOpen Money

Government35%

Incentive

23%

8%

Insurance0%

26

Prepaid Strategic Insight

id d l fPrepaid cards as a tool for payment innovation

27

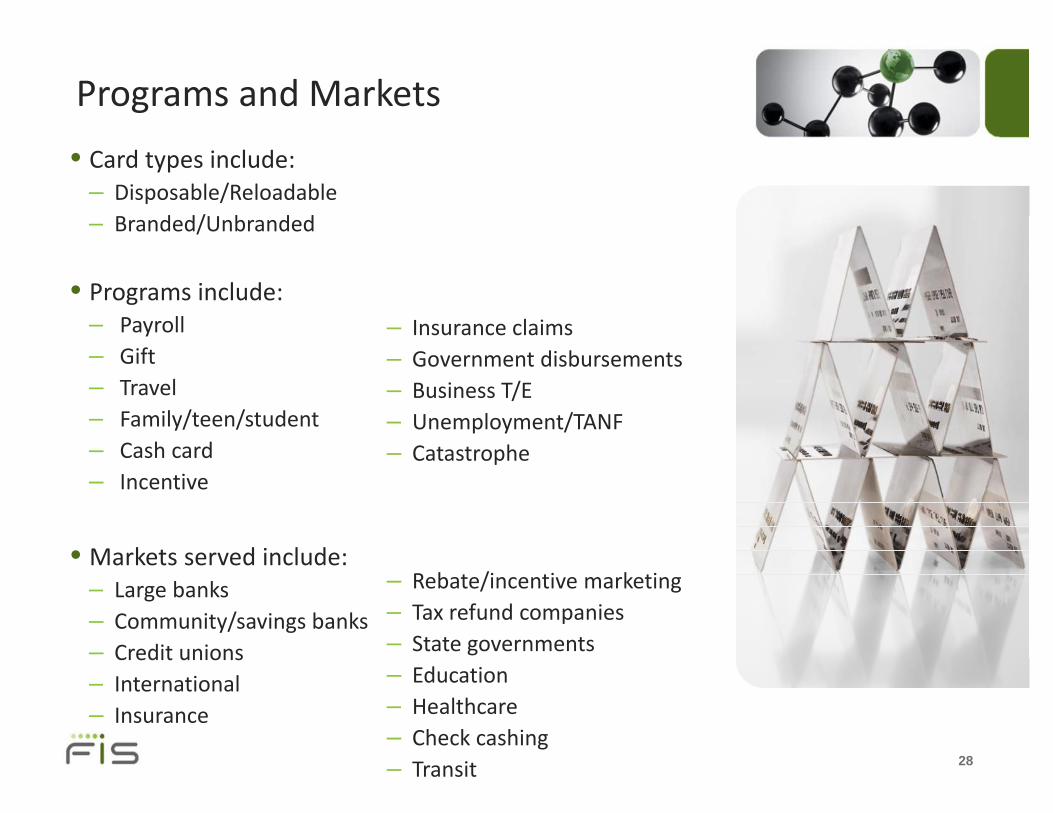

Programs and Markets

• Card types include:– Disposable/Reloadable

d d/ b d d– Branded/Unbranded

• Programs include:– Payroll– Gift– Travel

– Insurance claims– Government disbursements– Business T/E

– Family/teen/student– Cash card– Incentive

– Unemployment/TANF– Catastrophe

• Markets served include:– Large banks – Rebate/incentive marketingg– Community/savings banks– Credit unions– International

– Tax refund companies– State governments– Education

28

– Insurance – Healthcare– Check cashing– Transit

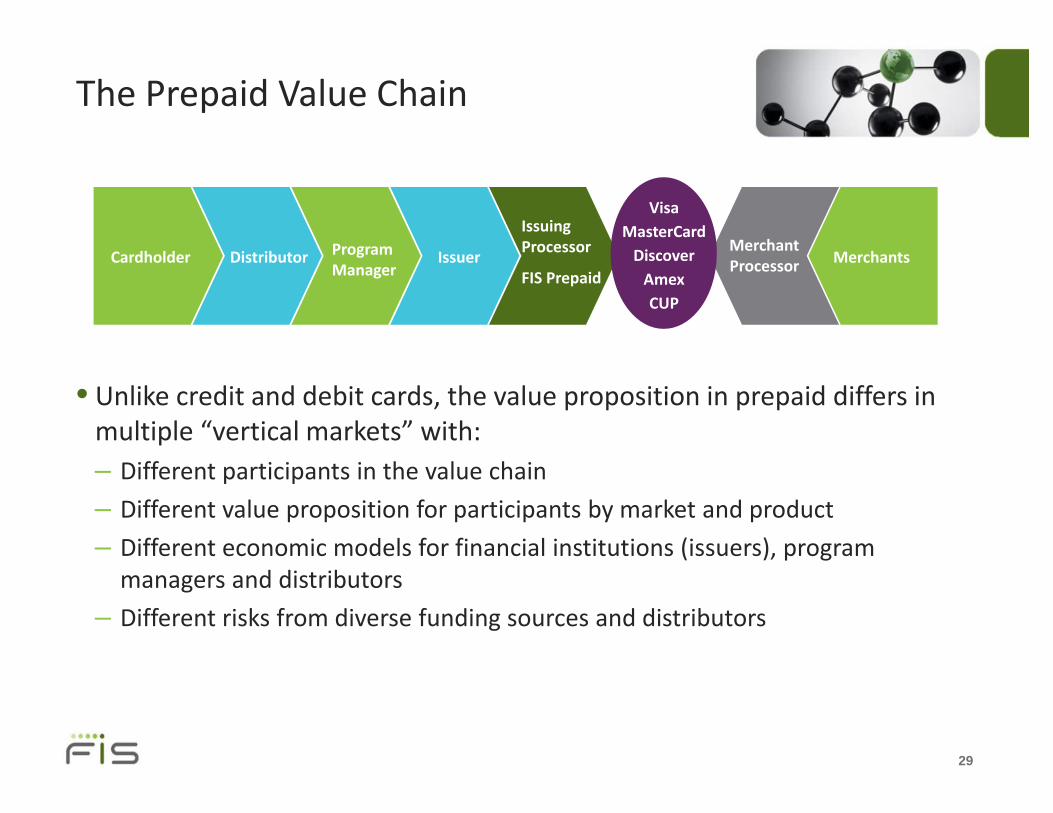

The Prepaid Value Chain

Visa

Cardholder Distributor Program Manager

Issuer

Issuing Processor

FIS Prepaid

MasterCardDiscoverAmexCUP

Merchant Processor Merchants

• Unlike credit and debit cards, the value proposition in prepaid differs in , p p p pmultiple “vertical markets” with:– Different participants in the value chain

Diff t l iti f ti i t b k t d d t– Different value proposition for participants by market and product

– Different economic models for financial institutions (issuers), program managers and distributors

– Different risks from diverse funding sources and distributors

29

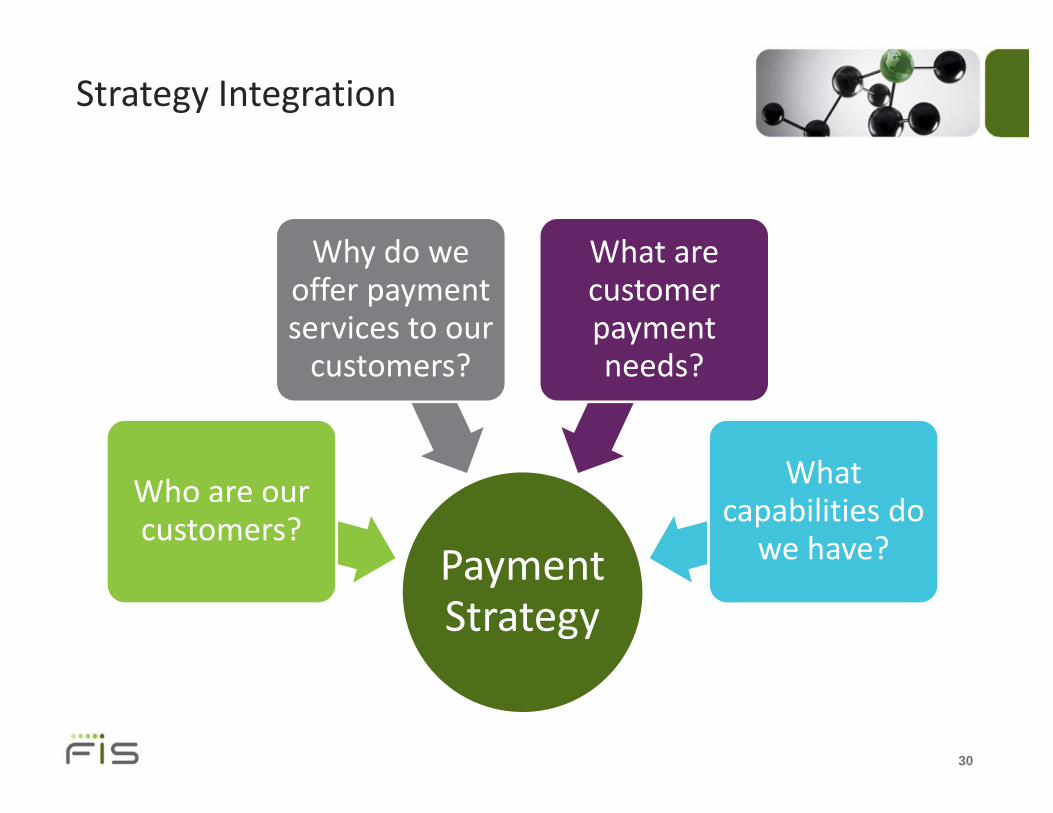

Strategy Integration

Why do we offer payment

What are customer

services to our customers?

payment needs?

Who are our What biliti d

Payment customers? capabilities do

we have?

Strategy

30

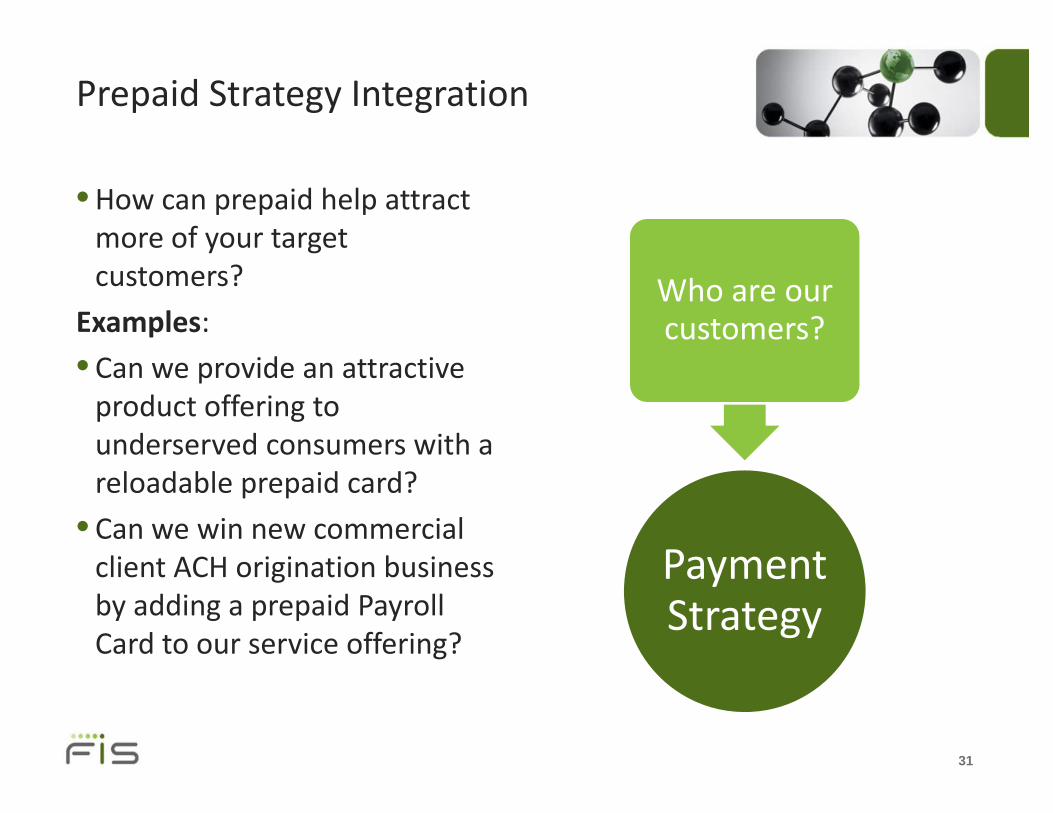

Prepaid Strategy Integration

•How can prepaid help attract more of your target customers?

lWho are our

Examples:

• Can we provide an attractive product offering to

customers?

product offering to underserved consumers with a reloadable prepaid card?

• Can we win new commercial client ACH origination business b ddi id P ll

Payment by adding a prepaid Payroll Card to our service offering?

Strategy

31

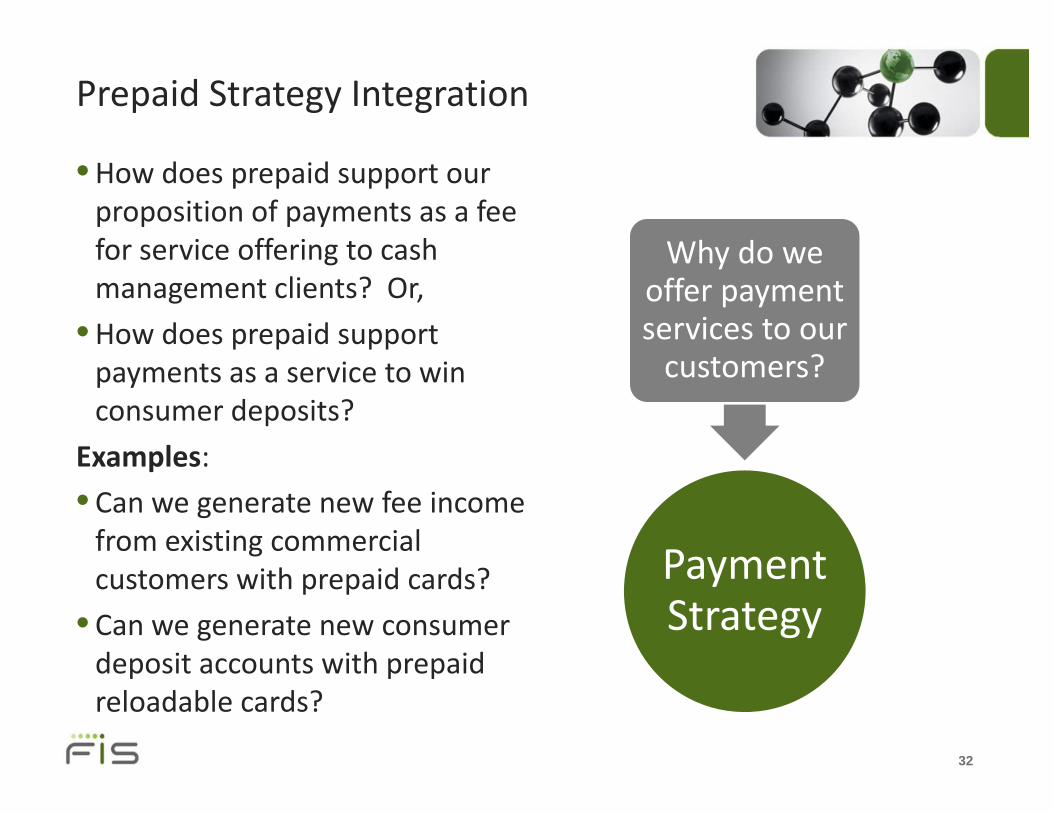

Prepaid Strategy Integration

•How does prepaid support our proposition of payments as a feeproposition of payments as a fee for service offering to cash management clients? Or,

Why do we offer payment

•How does prepaid support payments as a service to win consumer deposits?

services to our customers?

consumer deposits?

Examples:

• Can we generate new fee income• Can we generate new fee income from existing commercial customers with prepaid cards? Payment

• Can we generate new consumer deposit accounts with prepaid l d bl d ?

Strategy

reloadable cards?

32

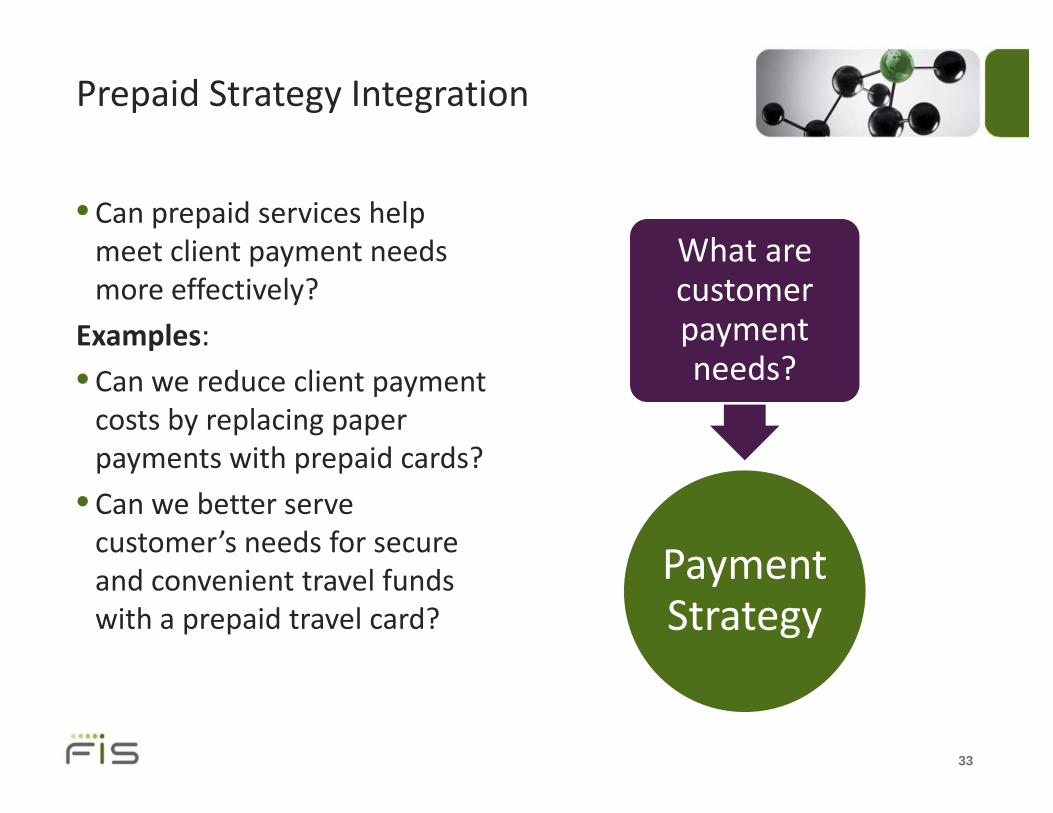

Prepaid Strategy Integration

• Can prepaid services helpCan prepaid services help meet client payment needs more effectively?

What are customer

Examples:

• Can we reduce client payment

payment needs?

costs by replacing paper payments with prepaid cards?

• Can we better serve• Can we better serve customer’s needs for secure and convenient travel funds Payment with a prepaid travel card? Strategy

33

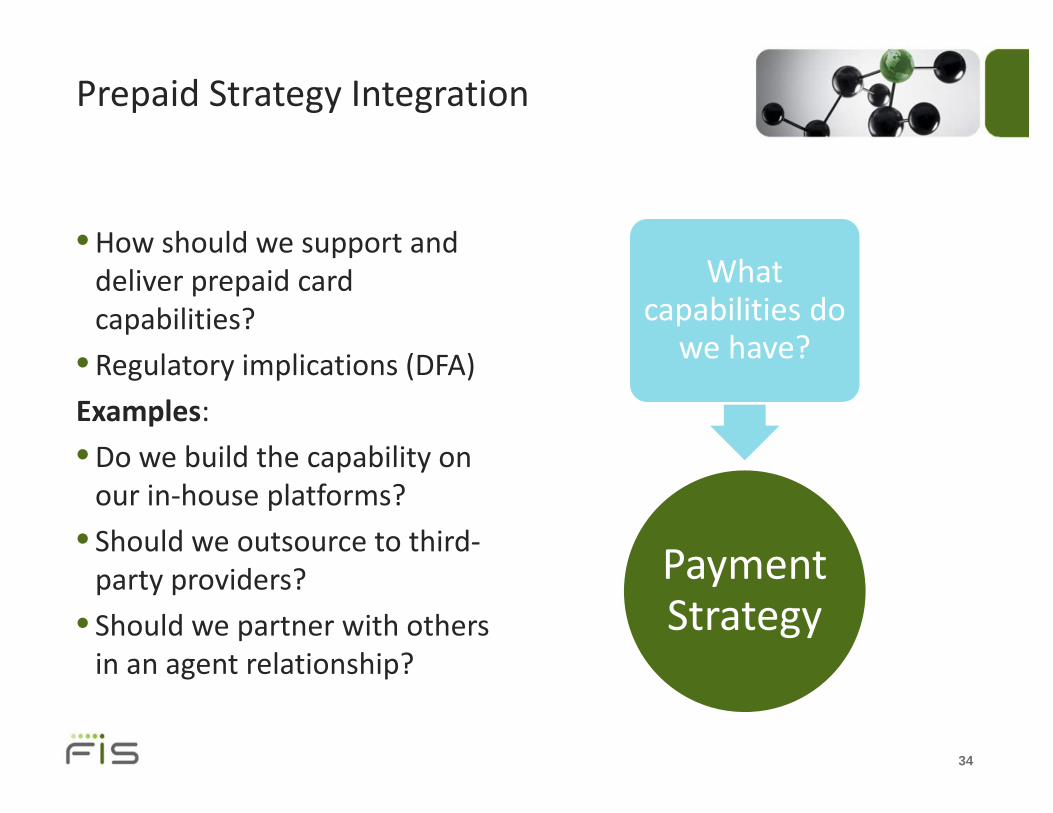

Prepaid Strategy Integration

•How should we support and deliver prepaid card

biliti ?

What capabilities docapabilities?

• Regulatory implications (DFA)

Examples:

capabilities do we have?

Examples:

•Do we build the capability on our in‐house platforms?our in house platforms?

• Should we outsource to third‐party providers? Payment

• Should we partner with others in an agent relationship?

Strategy

34

Strawman Strategies ‐ Consumer

Extend Consumer Transaction Account OfferingExtend Consumer Transaction Account Offering

• Business Challenge– How to grow revenue in consumer deposit productsg p p

– New regulatory environment reduces revenues (CardAct, DFA, Overdraft, etc.)

– Low volume accounts less/un‐profitable

• Strategic Opportunity– Offer reloadable prepaid card product to low volume/deposit consumers

– Differentiated product offering with different economicsDifferentiated product offering with different economics

– Lower risk, check‐less product

– Lower cost electronic service delivery

– Leverage retail services such as cash‐to‐card loading

– Extend reach into new segment, bringing new customers and revenues into the franchisethe franchise

35

Strawman Strategies ‐ Consumer

Create New Fee Income from Value‐Added Payment Services

• Business Challenge– How to replace revenues lost to new regulations

– How to increase the relationship value of existing accounts

• Strategic Opportunity• Strategic Opportunity– Offer consumer prepaid accounts to address tactical consumer needs

– Gift givingg g

– On‐the‐road travel payments

– Family accounts (students, teens, dependents)

G t f i hil ti t t d t il– Generate new fee income while meeting customer payment needs not easily met with existing debit accounts

36

Strawman Strategies ‐ Commercial

Generate New Business by Improving Client’s Payment Processes

• Business Challenge– How to win more business in a crowded cash management marketplace

– Constant client pressure to reduce their costs affects margins

• Strategic Opportunity• Strategic Opportunity– Use prepaid platform capabilities to replace paper‐based payments with card‐based electronic payments

– Incentive, insurance, payroll and rebate are examples

– Add value and differentiation through innovation

Reduce commercial client costs and generate new fee revenues– Reduce commercial client costs and generate new fee revenues

37

Critical Success Factors When launching a new Prepaid ProgramWhen launching a new Prepaid Program

• Solid business case • Vetting and qualifying partners• Fine tuning program requirements

•Determining the right distribution channels to market

• Educating internal staff– Sales

O i– Operations

– Call center

38

Q ti & AQuestions & Answers

Th k YThank You