31

Intellectual Property & Tax: How to maximise the opportunities 18 April 2012 Paul Garland, Michael Cashman & Suzy Schmitz

Intellectual Property & Tax:

How to maximise the opportunities

18 April 2012

Paul Garland, Michael Cashman & Suzy Schmitz

Taxation impacts on the creation,

commercialisation and ownership of IP

Government schemes to reward innovation and

tax-efficient structures are available

These are relevant when creating, acquiring and

exploiting IP

Today’s session will cover:

1. Taxation in the life-cycle of IP within a

business, from research and development

to disposal

2. Tax issues relating to IP ownership,

including intra-group licences and IP

holding companies

Introduction

1

Taxation is

relevant at

every stage in

the IP life

cycle

Co

nte

nts

Section Page

1 Introduction 2

2 Generating and Acquiring IP 4

3 Commercialising IP 14

4 Group arrangements 22

5 Questions?

2

Generating and acquiring

intellectual property

1 3

Summary of relevant IP rights

Taxation

regimes are

relevant to a

range of

intellectual

property

rights

Patents

Trade Marks

Copyright &

Database Right

Confidential

information and

know how

• protect inventions

• can encompass products and processes

• duration of 20 years from their filing date

Important for: software companies, products

• designate source or origin of goods or services

• registered for 10 years and can be renewed

• can comprise words, logos, slogans, colours

Important for: suppliers of goods/services

• copyright can protect literary works and databases

• Database Right also protects databases

• attach on creation

Important for: information/data companies

• techniques, processes, information, used by a

company, including trade secrets & know how

• protected by common law duty of confidence

Important for: all businesses 4

IP rights are “intangible assets”

Part 8 of the

Corporation

Tax Act 2009

(CTA) is

relevant to IP:

5

Section Key term/Summary of section

712 “Intangible asset”

• has the meaning it has for accounting purposes

• covers intellectual property, including:

– registered and unregistered rights

– similar rights under the law of other countries

– know how and confidential information

713 “Intangible fixed asset”

• defined as “intangible asset acquired or created by the

company for use on a continuing basis in the course of the

company's activities”

• Includes an option or other right to acquire or dispose of an

intangible asset

715 “Goodwill”

• Part 8 CTA applies to goodwill

• Goodwill has the meaning it has for accounting purposes

Company IP

IP acquired

IP produced by/for the company

IP licensed in

Generating and acquiring IP

IP can

accumulate

within a

company in a

variety of

ways

6

A key issue is obtaining a deduction for the costs incurred in

creating IP. Under general principles, a deduction is available for direct

costs incurred in developing IP when the expenditure is recognised as a

deduction in the P&L account. This is generally when the expenditure is

incurred

Enhanced deductions may also be available – see discussion below

Some expenditure will be treated as capital expenditure and written

off over time. For example certain expenditure incurred on the creation

of a website

If IP development is done on an intra-group basis, consider alternative

remuneration structures to minimise up-front tax bills

Cost sharing agreements can be extremely useful in spreading

development costs between group companies and ensuring that the IP is

owned by the correct group company – but any cost sharing arrangement

must be correctly structured to avoid unexpected tax charges

7

General Taxation issues for company-produced IP

When

activities are

carried on

which create

IP a number

of tax issues

should be

considered:

In addition to the general tax rules, many jurisdictions offer incentives

for R&D activities in their jurisdiction

The specific incentives which are available for certain R&D

expenditure can be quite valuable and are likely to be an important

consideration in designing and structuring an IP development

programme – this is especially true where a multi-national group has

a choice of jurisdictions in which to undertake R&D activities

Generally, the incentive is provided in the form of enhanced tax

deductions in relation to specific forms of R&D expenditure

As an added benefit, in some jurisdictions there will be an opportunity

for excess R&D deductions to be “sold back” to the government for a

cash payment – this can be helpful for the cash flow of early stage

companies

8

Tax Incentives for R&D Activities

Incentives

exist to

encourage

companies to

invest in and

undertake

R&D activities

Small and medium sized companies can claim a tax deduction equal to

225% of the expenditure incurred on qualifying R&D activities which benefit

a UK trade

The expenditure can include in-house R&D and also sub-contracted

R&D. In addition, there is no geographical restriction on the expenditure

As an additional benefit, an SME can surrender some or all of the loss

relating to the R&D deduction back to HMRC in exchange for a cash

payment

Cash payment equal to approximately 25% of the R&D expenditure –

therefore the amount of the cash payment is less than the amount of tax that

may be saved if the relief was set against future profits – but the ability to

obtain an improved cash flow position is attractive to early stage companies

Large companies can claim broadly similar relief, with a deduction equal

to 130% of qualifying expenditure – but it cannot surrender a loss for a cash

payment

9

UK Tax Incentives for R&D Activities

The UK has

some

generous tax

reliefs

available for

qualifying

R&D activities

In the recent budget the Chancellor announced the introduction

of an “above the line” R&D tax credit

The new R&D tax credit rate will be a minimum of 9.1% of

expenditure

Loss making companies will be able to claim this as a payable

credit

The main driver behind this new credit is to allow the R&D

credit to be included in the budget calculations to support R&D

investment

10

Proposed New UK Tax Incentives

The recent

UK budget

introduced a

new relief for

R&D

expenditure

The patent box regime will be phased in over a five year period commencing

in 2013. Effectively 60% of the benefit would apply in 2013/14, then 70% in

2014/15 and so on, until 100% is available in 2017/18

Under the patent box regime a 10% rate of corporation tax will apply to net

income arising from patents, and also “embedded income” included in the

price of patented products

The patent box regime applies to companies only

It applies to income from qualifying patents granted by the UK and European

Patent offices, or equivalent offices in the EU

Complicated calculation to determine the amount of “embedded income” that

may benefit

The jury remains undecided on whether the complexity of the regime will induce

non-UK companies engaged in these activities to consider alternative regimes

offered by other jurisdictions

UK Patent Box Rules

11

Another

incentive to

be introduced

are the UK

patent box

rules

The main issue when acquiring IP is to obtain a tax deduction for

the costs of acquisition

If the IP is acquired by way of a licence, a deduction for the royalty

payments will be available when the payments are recognised in

the accounts.

By contrast, if a lump sum payment is made the question is

whether it is a payment to use the IP (and thus effectively a

royalty) or to acquire the IP.

The cost of an outright acquisition of IP will generally be

amortised on the basis used in the accounts.

It is possible to elect for the IP to be written down at a specified

fixed rate. This election would be used where the accounts do not

amortise the IP.

Acquisition of IP - Tax Issues

12

Commercialising IP

2 13

Licensing

- data

- brand

- technology

- technology

Commercialising IP - options

IP can be

exploited in

many

different ways

14

Sale

- patent portfolio

- manufacturing

arm (HDDs)

- brand

Licensing of IP Sale of IP

Commercialising IP – the stakeholders

15

Developing

an IP strategy

involves

various

stakeholders

• Identify the value of the technology

• Make sure the strategy fits the business

• IP is often about peoples’ knowledge

• Protect / enforce the rights

• Tax advice

Legal People

Technical Business

When developing a licensing model, consider:

–payment through a lump sum one-off fee, a fee based on

usage (royalty) or a combination?

–when/how will fees be reassessed/increased?

–should minimum fees be set?

–will sales/exploitation targets apply?

–what happens if the IP is invalidated?

Royalties may differ depending on the IP right involved

Licensing IP – payment

Payment for

the benefit of

a licence can

be structured

in a number

of ways

16

The payment may either be the receipt of royalties or one or more

lump sum payments

Royalty payments and payments with the characteristics of royalties

which are received by companies will be taxed when the payment is

recognised in the P&L

Lump sum payments may be recognised over time

If royalties are paid cross border, withholding tax issues may arise.

Tax treaty relief may be required to minimise double tax

Specific tax incentives, such as the UK patent box regime, may be

available

Exploitation of IP – General Tax Issues

17

IP can be

exploited

either by the

sale of the IP

or by the

grant of a

licence to use

the IP

Licence payments may give rise to VAT consequences:

VAT applies to supplies of services, which includes the grant,

assignment or surrender of any right

The grant of a licence to use IP is therefore a supply for

purposes, and as a consequence VAT is payable on the

royalties

Where the IP is supplied to a business in another EU state, no

VAT is chargeable as the supply is a zero rate export

Similarly, the supply of IP to a non-EU business is also VAT

free, as such a supply is outside the scope of VAT

VAT Issues

18

When IP is no longer recognised in the balance sheet, there will be a

disposal for tax purposes

Credit or debit to be brought into account for tax purposes on that

realisation, calculated by comparing proceeds with costs and

amortisation

Consider any potential tax charges if transferring IP to an IP holding

company

Various reliefs may be available to shelter any credit or debit:

– intra –group transfers can be made on a tax free basis, but beware

of future de-grouping charges if the transferee leaves the group

– roll-over relief if proceeds reinvested

Disposal of IP

19

Tax issues on

the disposal

of IP

A few other issues to consider:

Where transactions are between related parties, transfers will be

treated as occurring at market value

A number of countries (such as Japan, China, USA and UK) are quite

strict on transfer pricing, as they consider substantial tax may be

obtained. The US, for example, got $3.4 billion from GlaxoSmithKline

in respect of marketing intangibles

To avoid transfer pricing adjustments, royalty rates between

connected companies should be on an arms length basis

Important to ensure arrangements are adequately documented

Group R&D facilities should also be provided on an arms length basis

Other Tax Issues

20

Group Arrangements

3 21

Typical scenario of:

Parent company

Multi-jurisdiction operating companies

Multi-jurisdiction services and marketing companies

R&D centres

Outsourced development work

May well be beneficial to set up an IP holding company

Single group company which is the owner of the world-wide IP

of a multi-national group of companies

Costs / benefit analysis required

Intra-group arrangements

22

Group structure

23

IP Holding

Company

Operating

Entities

= IP assignments &

licence fees = IP intra-group licences KEY:

R&D Company Operating

Entities Operating

Entities

Third

party

R&D Co

PARENT COMPANY

Tax savings (more to come on this)

Revenue shifting

Streamlines management and control

Manpower and resource efficiency savings

Maximises value

Flexibility on disposals

IP holding company - benefits

24

In which jurisdiction will the IP be exploited?

What general tax planning opportunities exist to reduce the overall

group tax cost and the compliance costs?

Any potential withholding tax costs must be reduced or eliminated

The company must be structured/operated to be tax resident only in

its jurisdiction of incorporation

The application of potential anti-abuse rules must be considered

The company must have adequate substance and/or an acceptable

assumption of risk to justify the profits it is allocated

Any tax cost arising on the transfer of the IP to the IP holding

company

Tax Issues to consider

25

A number of

tax issues

need to be

considered

when

establishing

an IP holding

company

Additional legal risks/considerations:

What IPR?

Assignability of IPR

Recordal

Licensing IPR

Intra-group licences

Future IPR and R&D

Damages and injunction risk

IP holding company

26

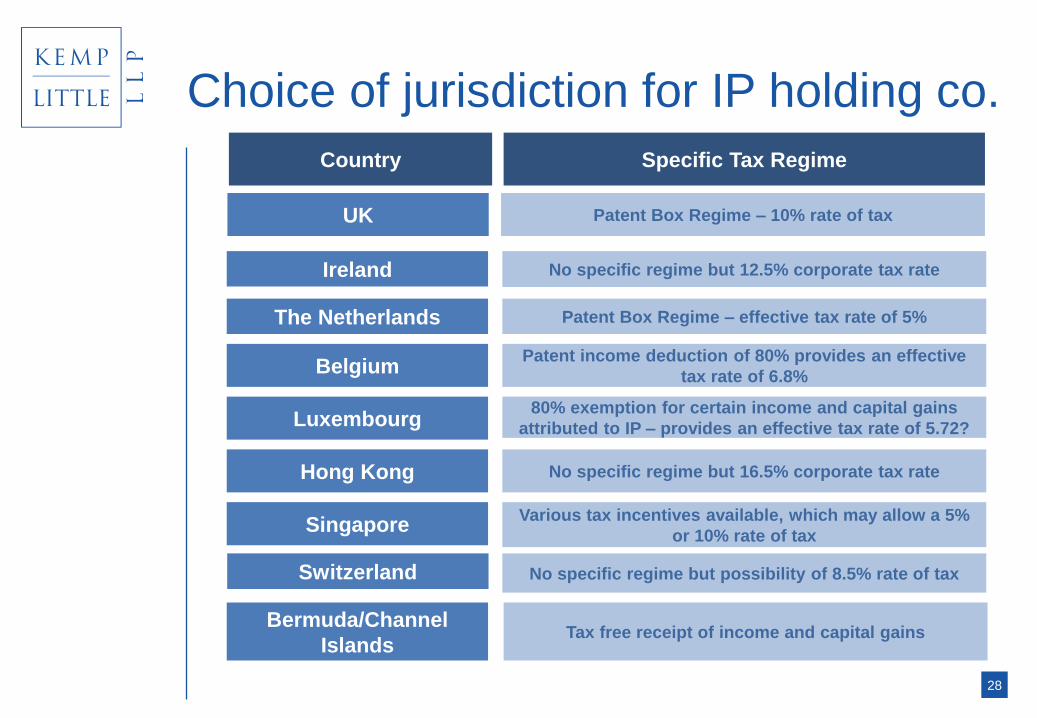

Choice of jurisdiction for IP holding co.

27

Choice of jurisdiction for IP holding co.

28

Country

UK

Specific Tax Regime

Patent Box Regime – 10% rate of tax

Ireland No specific regime but 12.5% corporate tax rate

The Netherlands Patent Box Regime – effective tax rate of 5%

Belgium Patent income deduction of 80% provides an effective

tax rate of 6.8%

Luxembourg 80% exemption for certain income and capital gains

attributed to IP – provides an effective tax rate of 5.72?

Hong Kong No specific regime but 16.5% corporate tax rate

Singapore Various tax incentives available, which may allow a 5%

or 10% rate of tax

Bermuda/Channel

Islands Tax free receipt of income and capital gains

Switzerland No specific regime but possibility of 8.5% rate of tax

Ou

r te

am

Paul Garland

Head of IP/Litigation

ddi 020 7710 1617

Michael Cashman

Tax partner

ddi 020 7710 1619

29

Suzy Schmitz

IP/Litigation Associate

ddi 020 7710 1632

Treatment costing 50p per child per year will allow them to

attend school, learn more effectively & live more prosperous

lives.

Kemp Little is

supporting SCI to

treat 40,000 children

suffering from

neglected tropical

diseases.