45

Intensive Course Intensive Course on Indirect on Indirect Taxes Taxes ISSUES ON INPUT TAX CREDIT BY BY VIKRAM D. MEHTA VIKRAM D. MEHTA (Chartered Accountant) (Chartered Accountant)

Intensive Course Intensive Course on Indirect on Indirect TaxesTaxes

ISSUES ON INPUT TAX CREDIT

BYBY

VIKRAM D. MEHTAVIKRAM D. MEHTA(Chartered Accountant)(Chartered Accountant)

SetSet--off provision under VAToff provision under VAT

►►BASICBASIC PROVISIONPROVISION::--

SectionSection 4848 ofof MVATMVAT Act,Act, 20022002 providesprovides thatthat thetheStateState governmentgovernment may,may, byby Rule,Rule, makemake provisionsprovisionsforfor SetSet--offoff andand refundrefund andand SectionSection 4949 empowersempowers

Vikram Mehta 2

forfor SetSet--offoff andand refundrefund andand SectionSection 4949 empowersempowersthethe StateState governmentgovernment forfor thethe reimbursementreimbursement ofofthethe taxtax paidpaid onon declareddeclared goodsgoods underunder locallocal SalesSalesTaxTax ActAct ,, whichwhich areare resoldresold inin thethe coursecourse ofof interinter--StateState tradetrade oror commercecommerce.. InIn pursuancepursuance ofof powerspowersgrantedgranted underunder SectionSection 4848 andand 4949 ofof thethe MVATMVAT Act,Act,20022002,, MaharashtraMaharashtra GovernmentGovernment hashas incorporatedincorporatedRulesRules 5151 toto 5656 forfor grantgrant ofof setset--offoff..

IssueIssue

►►Whether set off is a vested and substantial Whether set off is a vested and substantial right of the dealer?right of the dealer?

►►Vested and substantial right of the dealer is Vested and substantial right of the dealer is only to the extent the rules provide for the only to the extent the rules provide for the only to the extent the rules provide for the only to the extent the rules provide for the same. same. TThe government has the power to he government has the power to notify the rules in respect of the set off notify the rules in respect of the set off which can be claimed by the dealerwhich can be claimed by the dealer(Central (Central Pulp Mills, SA Pulp Mills, SA No.No.161 161 of 1972 of 1972 dtdt. 11. 11--1212--19731973.).)

Vikram Mehta 3

IssueIssue

In In Tata Motors Ltd. Tata Motors Ltd. vsvs State of Maharashtra State of Maharashtra (2004) (2004) 136 STC (1) 136 STC (1) it it was held that once was held that once the set off rules are the set off rules are made, then made, then such a such a vested statutory right cannot be later on vested statutory right cannot be later on vested statutory right cannot be later on vested statutory right cannot be later on withdrawn or withdrawn or modified with retrospective modified with retrospective effect. The Government effect. The Government has however has however acquired power to make rules acquired power to make rules retrospectively retrospectively vide vide section section 83(383(3).).

Vikram Mehta 4

SetSet--off provision under VAToff provision under VAT

�� RuleRule 5151::-- SetSet--offoff onon stockstock asas onon 3131..33..20052005..

�� RuleRule 5252::-- ItemItem onon whichwhich setset--offoff isis availableavailable..

�� RuleRule 5353::-- ItemItem onon whichwhich retentionretention isis applicableapplicable..

�� RuleRule 5454::-- ItemItem onon whichwhich nono setset--offoff eligibleeligible..

Vikram Mehta 5

�� RuleRule 5454::-- ItemItem onon whichwhich nono setset--offoff eligibleeligible..

�� RuleRule 5555::-- TermsTerms andand ConditionsConditions forfor grantgrant ofof setset--offoff

�� RuleRule 5656::-- ReRe imbursementimbursement ofof taxtax onon declareddeclaredgoodsgoods..

IssueIssue

►►When the set off under rule 48(5) can be When the set off under rule 48(5) can be disallowed? disallowed?

►►The set off cannot be disallowed merely on The set off cannot be disallowed merely on allegation that the bills are allegation that the bills are hawalahawala bills or bills or allegation that the bills are allegation that the bills are hawalahawala bills or bills or vendors have not paid taxes.vendors have not paid taxes.

►►The dept have to categorically prove that on The dept have to categorically prove that on every goods purchased by the appellant the every goods purchased by the appellant the concerned vendor has not paid tax.concerned vendor has not paid tax. M/s M/s SS P P & Co. vat Appeal No. 3 of & Co. vat Appeal No. 3 of 2009 2009 dtdt 66--44--20092009

Vikram Mehta 6

IssueIssue►►Whether set off can be claimed on Whether set off can be claimed on purchases debited in CWIP or on when purchases debited in CWIP or on when CWIP is capitalized?CWIP is capitalized?

►►Sec 52 Sec 52 --Set off would be available on Set off would be available on purchase treated as Capital Asset, (as purchase treated as Capital Asset, (as purchase treated as Capital Asset, (as purchase treated as Capital Asset, (as defined under the I T Act ).therefore set off defined under the I T Act ).therefore set off is allowable on purchases debited in CWIPis allowable on purchases debited in CWIP

►►However, in the event the set off is claimed However, in the event the set off is claimed at the time of capitalization the dealer shall at the time of capitalization the dealer shall have to prove that no set off has been have to prove that no set off has been claimed in the year of purchase.claimed in the year of purchase.Vikram Mehta 7

Rule 52.Rule 52. SetSet--off in respect of off in respect of purchase of goods on or after 1purchase of goods on or after 1stst

April 2005April 2005

►►This rule specifies the eligible purchase on which This rule specifies the eligible purchase on which the dealer is entitled to claim setthe dealer is entitled to claim set--off subject to off subject to following conditions:following conditions:

Vikram Mehta 8

following conditions:following conditions:►►Available to Registered Dealers (subject to Available to Registered Dealers (subject to Exception in Rule 55)Exception in Rule 55)

►► Purchase of goods or entry of goods made on or Purchase of goods or entry of goods made on or after 1after 1stst April 2005.April 2005.

►►Taxes should be charged/collected separately.Taxes should be charged/collected separately.

Rule 52.Rule 52. SetSet--off in respect of off in respect of purchase of goods on or after 1purchase of goods on or after 1stst

April 2005April 2005

►►Goods debited to Trading , P&L A/c would Goods debited to Trading , P&L A/c would be eligible for setbe eligible for set--offoff

►►Set off would be also available on purchase Set off would be also available on purchase

Vikram Mehta 9

►►Set off would be also available on purchase Set off would be also available on purchase treated as Capital Asset, (as defined under treated as Capital Asset, (as defined under the I T Act ).the I T Act ).

►►Set off also available of Entry tax paid under Set off also available of Entry tax paid under Motor Vehicles Entry into local Areas Act Motor Vehicles Entry into local Areas Act 1987.1987.

►►Set off also available of Entry tax paid under Set off also available of Entry tax paid under Entry of goods into local Areas Act 2003.Entry of goods into local Areas Act 2003.

Set-off under this rule would not be available if it is already claimed under any earlier laws.Set-off is available in the month of purchase of goods, itselfSet-off under this rule is available subject to reduction of set-off as specified in rule 53 and non admissibility of set-off as provided in Rule 54

Vikram Mehta 10

non admissibility of set-off as provided in Rule 54 of MVAT Rules,2005.Other conditions specified in Rule 55

Issue Pertaining to Rule 52Issue Pertaining to Rule 52Contd…Contd…

►►A company was not covered under VAT Audit for A company was not covered under VAT Audit for the period the period 0808--09 09 In this year commercial vehicles In this year commercial vehicles was purchased and capitalized. No setwas purchased and capitalized. No set--off of off of capital item was claimed in the return. In the capital item was claimed in the return. In the period period 0909--10 10 there is VAT Audit and that there is VAT Audit and that

Vikram Mehta 11

period period 0909--10 10 there is VAT Audit and that there is VAT Audit and that commercial vehicles is sold.commercial vehicles is sold.

Whether setWhether set--off the commercial vehicles can be off the commercial vehicles can be claimed in claimed in 0909--1010

Rule: 54 Rule: 54 NonNon--admissibility of setadmissibility of set--off. off.

►►No setNo set--off under any ruleoff under any rule shall be admissible in shall be admissible in respect of, respect of, --

►► (a)(a) purchases of motor vehicles (being passenger purchases of motor vehicles (being passenger vehicles) which are treated by the claimant dealer vehicles) which are treated by the claimant dealer as capital assets and parts, components and as capital assets and parts, components and

Vikram Mehta 12

as capital assets and parts, components and as capital assets and parts, components and accessories (irrespective of whether it is treated as accessories (irrespective of whether it is treated as capital asset or not).capital asset or not).

►►The above rule does not apply to the dealer The above rule does not apply to the dealer engaged in the business of transferring the right engaged in the business of transferring the right to use (whether or not for a specified period).to use (whether or not for a specified period).

Rule: 54 Rule: 54 NonNon--admissibility of admissibility of setset--off.off.

►► (g) No Set off on purchases made from a works contractor (g) No Set off on purchases made from a works contractor if the contract if the contract results in immovable propertyresults in immovable property

►► The above does not apply if the WCT purchase pertains to The above does not apply if the WCT purchase pertains to plant and machinery;plant and machinery;

►► How can one define the term “results in immovable How can one define the term “results in immovable

Vikram Mehta 13

►► How can one define the term “results in immovable How can one define the term “results in immovable property”?property”?

►► Outcome of some process or action, or effect is the result. Outcome of some process or action, or effect is the result. In this clause , if outcome of the process of works contract In this clause , if outcome of the process of works contract is immovable property then the tax charged by the works is immovable property then the tax charged by the works contractor is not eligible for setcontractor is not eligible for set--off.off.

►►It would be a matter of fact as to whether a It would be a matter of fact as to whether a works contract has resulted in immovable works contract has resulted in immovable property. Immovable property as referred in property. Immovable property as referred in the cases of general clauses Act would the cases of general clauses Act would the cases of general clauses Act would the cases of general clauses Act would mean Land & building or similar things mean Land & building or similar things attached or fastened to earth are attached or fastened to earth are immovable property.immovable property.

Vikram Mehta 14

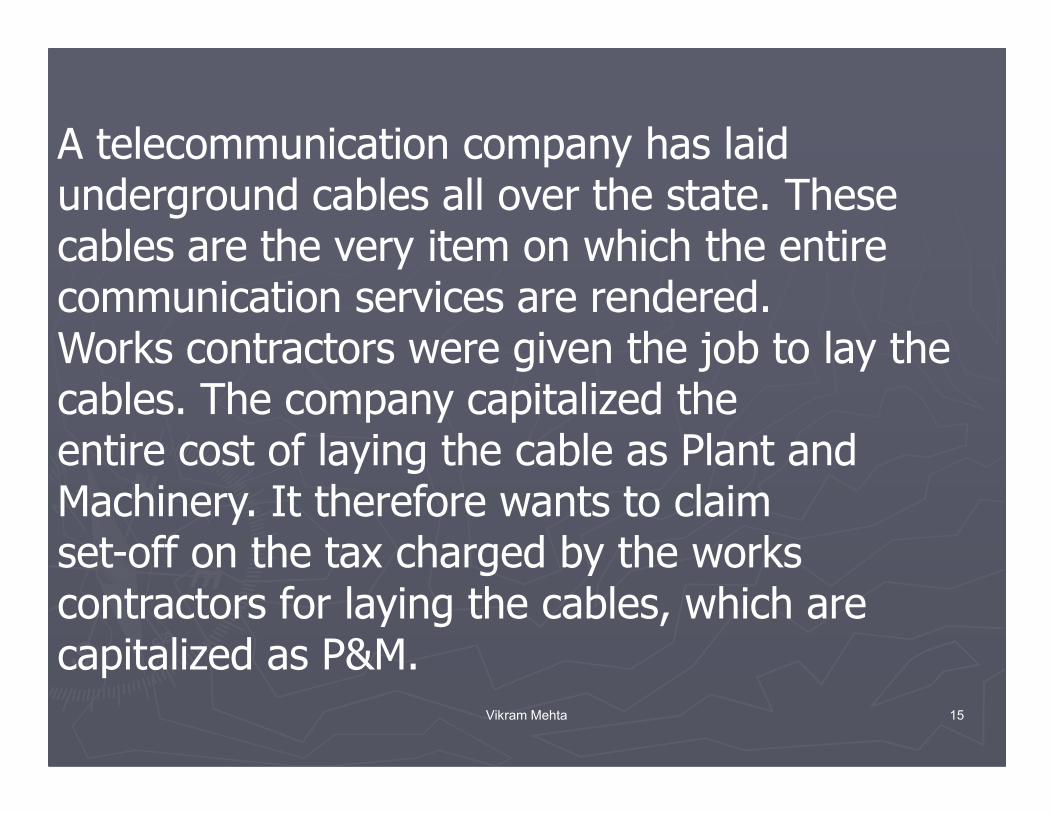

A telecommunication company has laid underground cables all over the state. These cables are the very item on which the entire communication services are rendered.Works contractors were given the job to lay the cables. The company capitalized the

Vikram Mehta 15

cables. The company capitalized theentire cost of laying the cable as Plant and Machinery. It therefore wants to claimset-off on the tax charged by the works contractors for laying the cables, which arecapitalized as P&M.

IssueIssue

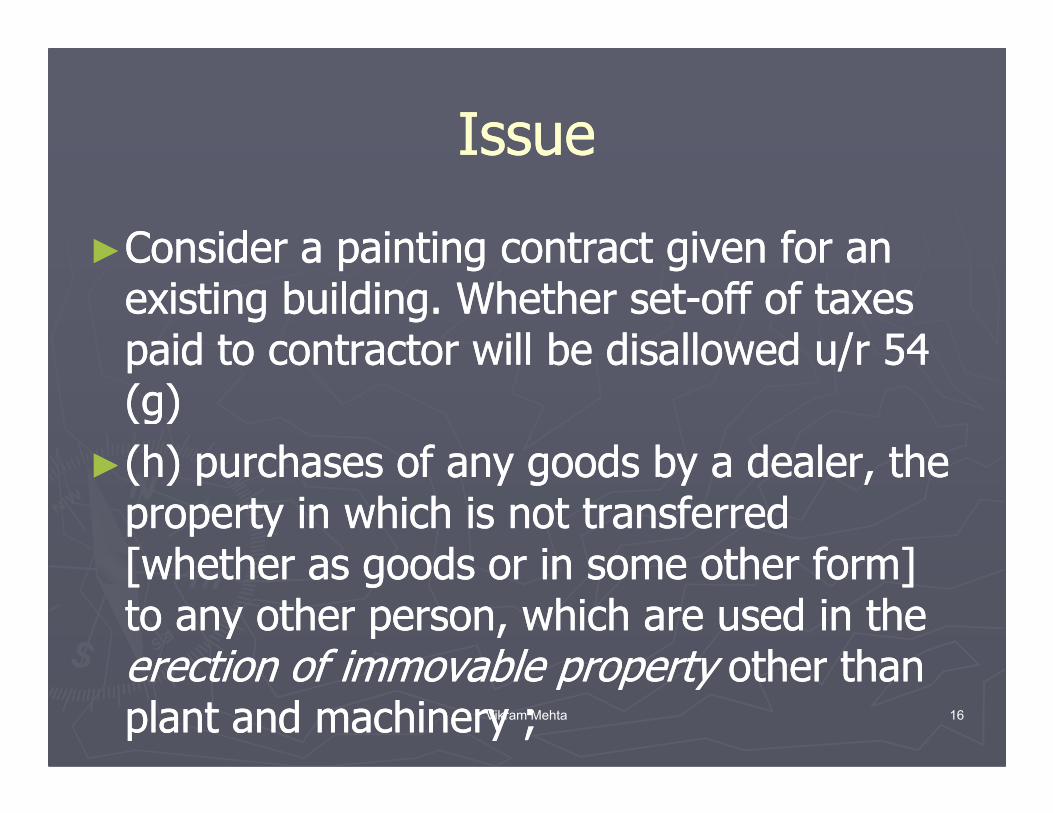

►►Consider a painting contract given for an Consider a painting contract given for an existing building. Whether setexisting building. Whether set--off of taxes off of taxes paid to contractor will be disallowed u/r 54 paid to contractor will be disallowed u/r 54 (g)(g)(g)(g)

►►(h) purchases of any goods by a dealer, the (h) purchases of any goods by a dealer, the property in which is not transferred property in which is not transferred [whether as goods or in some other form] [whether as goods or in some other form] to any other person, which are used in the to any other person, which are used in the erection of immovable propertyerection of immovable property other than other than plant and machinery ;plant and machinery ;Vikram Mehta 16

IssueIssue

►►If paints are purchased and used to If paints are purchased and used to whitewash an existing bldg whether set off whitewash an existing bldg whether set off would be allowable under 54 (h)?would be allowable under 54 (h)?

Vikram Mehta 17

►► j) Purchases made on or after thej) Purchases made on or after the 20th June 2006 of mandap, tarpaulin, 20th June 2006 of mandap, tarpaulin, pandal, shamiana, decoration of such mandap, pandal or shamiana, and pandal, shamiana, decoration of such mandap, pandal or shamiana, and furniture, fixtures, lights and light fittings, floor coverings, utensils and other furniture, fixtures, lights and light fittings, floor coverings, utensils and other articles ordinarily used alongwith a mandap, pandal or shamiana if the articles ordinarily used alongwith a mandap, pandal or shamiana if the purchasing dealer has opted for composition of tax under subpurchasing dealer has opted for composition of tax under sub--section (4) of section (4) of section 42. section 42.

►► (k) No set(k) No set--off is available on the purchases made on or after 1st April 2005 off is available on the purchases made on or after 1st April 2005

Rule: 54 Rule: 54 NonNon--admissibility of admissibility of setset--off.off.

Vikram Mehta 18

►► (k) No set(k) No set--off is available on the purchases made on or after 1st April 2005 off is available on the purchases made on or after 1st April 2005 by a hotelier on:by a hotelier on:

►► Purchase treated as capital assets and Purchase treated as capital assets and ►► Which do not pertain to the supply by way of or as part of service or in any Which do not pertain to the supply by way of or as part of service or in any

other manner, being food or any other article for human consumption or other manner, being food or any other article for human consumption or any drink [whether or not intoxicating ] where such supply or service is any drink [whether or not intoxicating ] where such supply or service is made or given for cash, deferred payment or other valuable consideration.made or given for cash, deferred payment or other valuable consideration.

►► (l) purchases of office equipment, furniture, fixture and (l) purchases of office equipment, furniture, fixture and electrical installation by a claimant dealer during the period electrical installation by a claimant dealer during the period commencing from the 1st April 2005 and ending on the 7th commencing from the 1st April 2005 and ending on the 7th September 2006 if such goods purchased are treated by the September 2006 if such goods purchased are treated by the claimant dealer as capital assets .claimant dealer as capital assets .

►► Exception:Exception: The claimant dealer not engaged in the business The claimant dealer not engaged in the business

Rule: 54 Rule: 54 NonNon--admissibility of admissibility of setset--off.off.

Vikram Mehta 19

►► Exception:Exception: The claimant dealer not engaged in the business The claimant dealer not engaged in the business of transferring the right toof transferring the right to use the said goods (whether or not use the said goods (whether or not for a specified period) for anyfor a specified period) for any purpose.purpose.

►Consider a case where dealer buys software, modifies the said software and then sells the said software under his own brand name. The software sold is considerably different in all respect then the one which is purchased can the dealer claim set-

Rule: 54 Rule: 54

Vikram Mehta 20

one which is purchased can the dealer claim set-off on software purchase as a Trader. It is pertinent to note that under the excise law his activity is treated as manufacture and excise duty is charge. He is recognized as an STPI unit from where he exports and sells locally the manufactured of software.

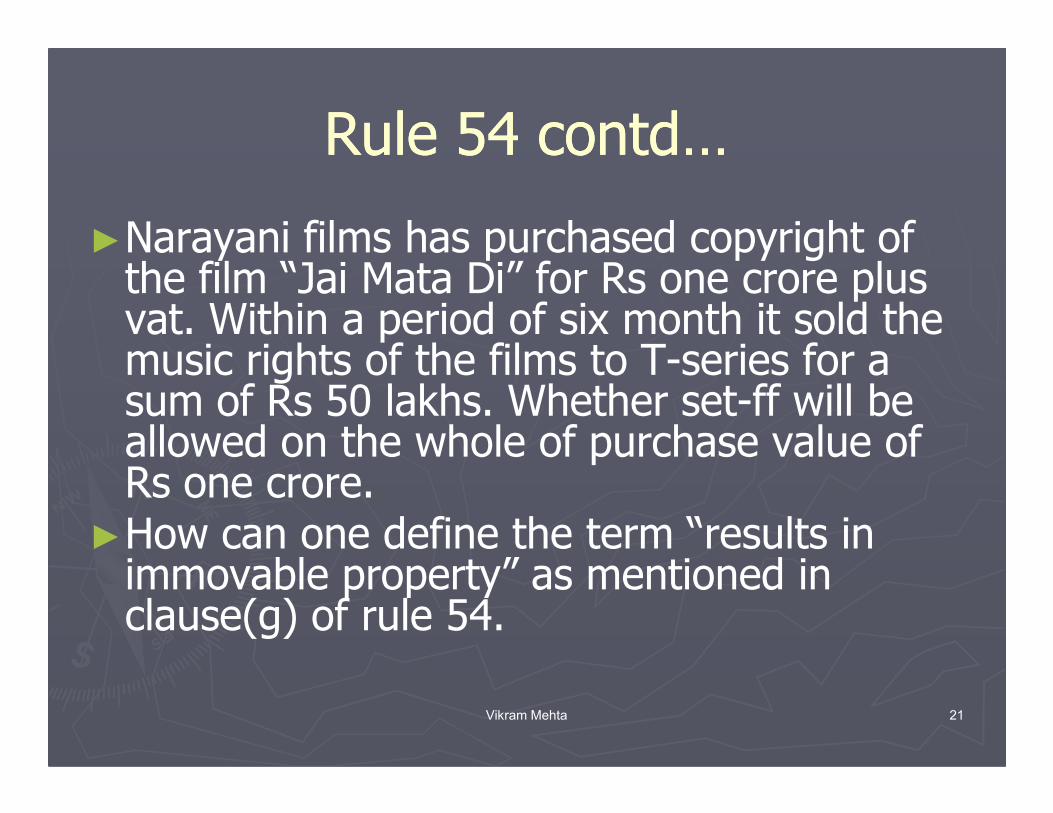

Rule 54 contd…Rule 54 contd…

►Narayani films has purchased copyright of the film “Jai Mata Di” for Rs one crore plus vat. Within a period of six month it sold the music rights of the films to T-series for a sum of Rs 50 lakhs. Whether set-ff will be

Vikram Mehta 21

sum of Rs 50 lakhs. Whether set-ff will be allowed on the whole of purchase value of Rs one crore.

►How can one define the term “results in immovable property” as mentioned in clause(g) of rule 54.

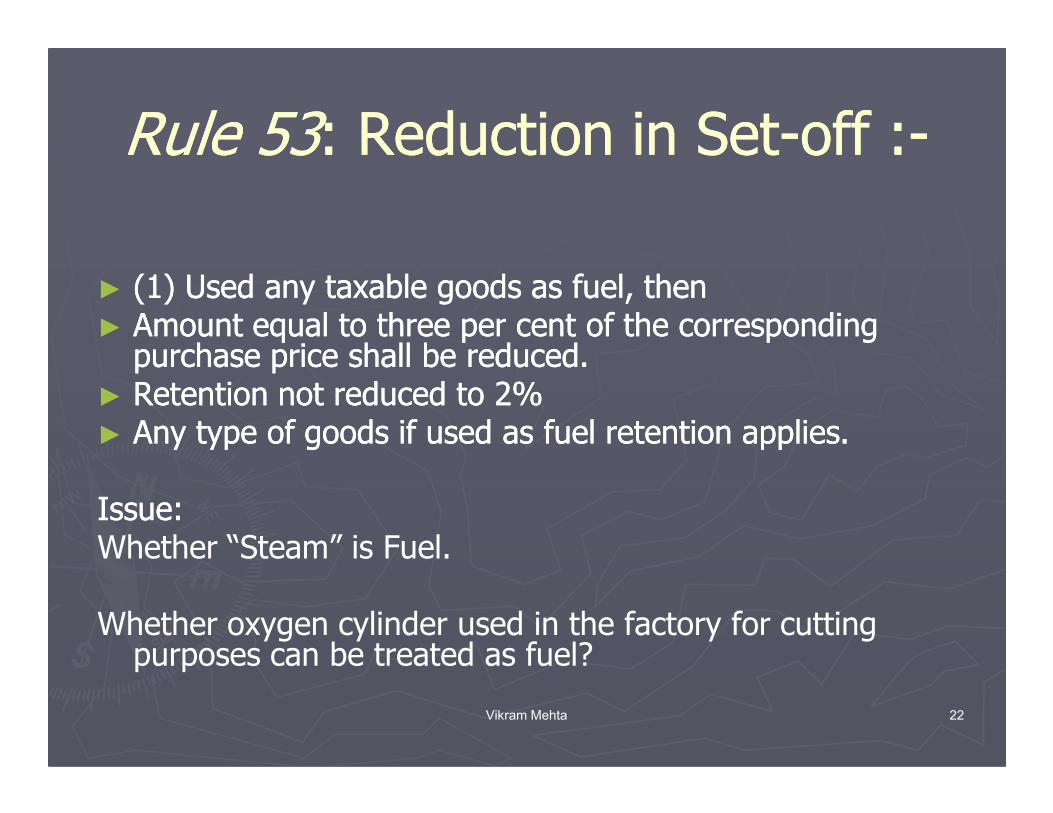

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

►► (1) Used any taxable goods as fuel, then (1) Used any taxable goods as fuel, then ►► Amount equal to three per cent of the corresponding Amount equal to three per cent of the corresponding

purchase price shall be reduced.purchase price shall be reduced.►► Retention not reduced to 2% Retention not reduced to 2%

Vikram Mehta 22

►► Retention not reduced to 2% Retention not reduced to 2% ►► Any type of goods if used as fuel retention applies.Any type of goods if used as fuel retention applies.

Issue:Issue:Whether “Steam” is Fuel.

Whether oxygen cylinder used in the factory for cutting purposes can be treated as fuel?

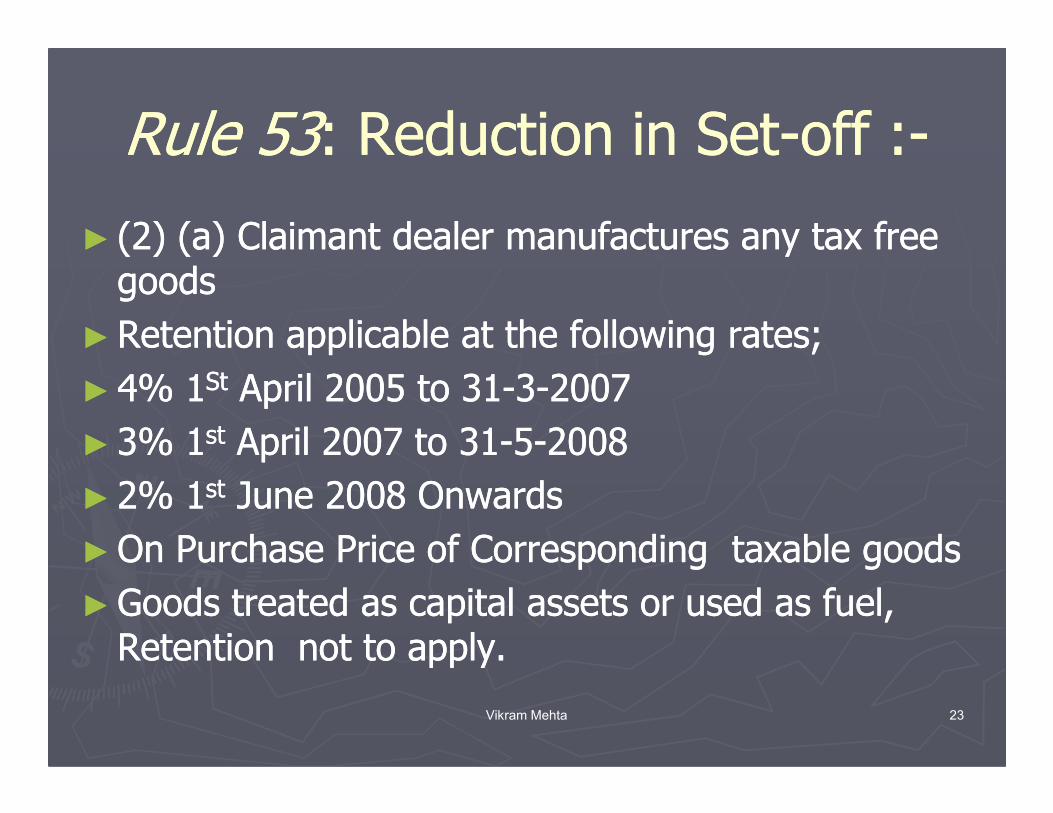

►► (2) (a) Claimant dealer manufactures any tax free (2) (a) Claimant dealer manufactures any tax free goods goods

►►Retention applicable at the following rates; Retention applicable at the following rates;

►► 4% 14% 1StSt April 2005 to 31April 2005 to 31--33--20072007

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 23

►► 4% 14% 1 April 2005 to 31April 2005 to 31--33--20072007

►► 3% 13% 1stst April 2007 to 31April 2007 to 31--55--20082008

►► 2% 12% 1stst June 2008 OnwardsJune 2008 Onwards

►►On Purchase Price of Corresponding taxable goods On Purchase Price of Corresponding taxable goods

►►Goods treated as capital assets or used as fuel, Goods treated as capital assets or used as fuel, Retention not to apply. Retention not to apply.

►► (b)Claimant dealer resells any tax free goods and (b)Claimant dealer resells any tax free goods and the taxthe tax--free goods are packed in any material, free goods are packed in any material,

►►Retention applicable at the following rates; Retention applicable at the following rates; ►► 4% 14% 1StSt April 2005 to 31April 2005 to 31--33--20072007►► 3% 13% 1stst April 2007 to 31April 2007 to 31--55--20082008►► 2% 12% 1stst June 2008 OnwardsJune 2008 Onwards

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 24

►► 2% 12% 1stst June 2008 OnwardsJune 2008 Onwards►►On the purchase price of the corresponding On the purchase price of the corresponding purchases of packing materials,purchases of packing materials,

►►Retention not to apply when goods, being Schedule Retention not to apply when goods, being Schedule A tax free goods, are exported.A tax free goods, are exported.

►►Covers direct exports u/s5(1) and exports u/s 5(3)Covers direct exports u/s5(1) and exports u/s 5(3)

►► (3) Claimant dealer dispatches any taxable goods outside (3) Claimant dealer dispatches any taxable goods outside the State, to any place within India, not by reason of sale, the State, to any place within India, not by reason of sale, to his own place of business or of his agent or where the to his own place of business or of his agent or where the claimant dealer is a commission agent, to the place of claimant dealer is a commission agent, to the place of business of his principal, business of his principal,

►► Retention applicable at the following rates; Retention applicable at the following rates;

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 25

►► Retention applicable at the following rates; Retention applicable at the following rates;

►► 4% 14% 1StSt April 2005 to 31April 2005 to 31--33--20072007

►► 3% 13% 1stst April 2007 to 31April 2007 to 31--55--20082008

►► 2% 12% 1stst June 2008 OnwardsJune 2008 Onwards

►► On Purchase Price of Corresponding taxable goods On Purchase Price of Corresponding taxable goods

►► Goods used as Capital assets or used as fuel shall not be Goods used as Capital assets or used as fuel shall not be liable for retentionliable for retention

►► ExplanationExplanation..-- For dispatch of Goods covered under For dispatch of Goods covered under Schedule B retention of only 1% to apply.Schedule B retention of only 1% to apply.

►► Provisio: No Retention is to be made applicable if Provisio: No Retention is to be made applicable if the goods dispatched comes back in the state the goods dispatched comes back in the state within a period of Six months, whether after within a period of Six months, whether after processing or otherwise i.e. in the same form or processing or otherwise i.e. in the same form or

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 26

processing or otherwise i.e. in the same form or processing or otherwise i.e. in the same form or not.not.

►►Recent Circular of Commissioner on the issue of Recent Circular of Commissioner on the issue of whether principal to principal is Branch trf, to whether principal to principal is Branch trf, to clarifying the stand of the dept.(Cir. No 5T of 2009)clarifying the stand of the dept.(Cir. No 5T of 2009)

►► Finally circular no 2T of 2010 dated 11Finally circular no 2T of 2010 dated 11thth January January 2010 making F form Mandatory From Jan 2010. 2010 making F form Mandatory From Jan 2010.

►► (9)(a) Definition of Corresponding goods referred in 53(1) (2a) (9)(a) Definition of Corresponding goods referred in 53(1) (2a) and (3)and (3)

►► Corresponding goods (not being consumable, stores, or goods Corresponding goods (not being consumable, stores, or goods treated as capital assets, parts, components and accessories of treated as capital assets, parts, components and accessories of capital assets and goods used as fuel) which are resold or are capital assets and goods used as fuel) which are resold or are so dispatched outside the State or are used in or relation to the so dispatched outside the State or are used in or relation to the

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 27

so dispatched outside the State or are used in or relation to the so dispatched outside the State or are used in or relation to the manufacture of goods so sold or dispatched and are contained manufacture of goods so sold or dispatched and are contained in the goods so sold, resold or dispatched and the packing in the goods so sold, resold or dispatched and the packing material used along with the goods so sold, resold or material used along with the goods so sold, resold or dispatched. Any reference to the corresponding purchase price, dispatched. Any reference to the corresponding purchase price, corresponding taxable goods or corresponding purchases of corresponding taxable goods or corresponding purchases of packing material shall be construed accordingly. packing material shall be construed accordingly.

Rule 53Rule 53: Reduction in Set: Reduction in Set--offoff

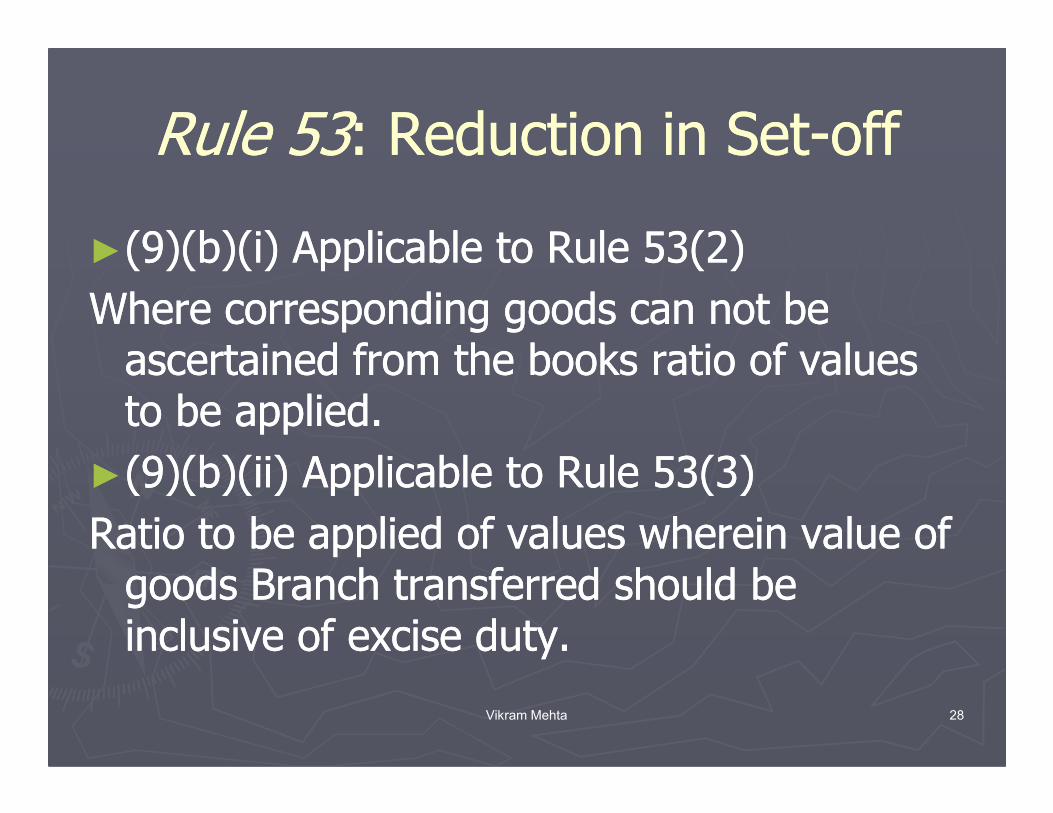

►►(9)(b)((9)(b)(ii) Applicable to Rule 53(2)) Applicable to Rule 53(2)

Where corresponding goods can not be Where corresponding goods can not be ascertained from the books ratio of values ascertained from the books ratio of values to be applied.to be applied.

Vikram Mehta 28

to be applied.to be applied.

►►(9)(b)(ii) Applicable to Rule 53(3)(9)(b)(ii) Applicable to Rule 53(3)

Ratio to be applied of values wherein value of Ratio to be applied of values wherein value of goods Branch transferred should be goods Branch transferred should be inclusive of excise duty.inclusive of excise duty.

An exporter of fresh fruits buys cartons for packing of fresh fruits, which are to be exported. The question raised is whether retention is applicable on cartons purchased.

Branch transfer inward consequence

A dealer is selling taxable as well as tax free goods. For the

Issue

Vikram Mehta 29

A dealer is selling taxable as well as tax free goods. For the convenience of the customers, he buys carry bags, The carry bags are given to the customers when ever they buys goods (i.e. both taxable and tax free goods) it is put in the carry bag and given to the customers. Whether retention needs to be applied on the purchase of carry bags to the extent to which they are used for tax free goods.

►► (4) Claimant dealer has made a sale by way of transfer of (4) Claimant dealer has made a sale by way of transfer of property in goods (whether as goods or in some other form) property in goods (whether as goods or in some other form) involved in the execution of works contract involved in the execution of works contract

►► The claimant dealer has opted for composition of tax under The claimant dealer has opted for composition of tax under subsub--section (3) of section 42, section (3) of section 42,

►► Retention of Set off on the corresponding amount pertaining Retention of Set off on the corresponding amount pertaining

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 30

►► Retention of Set off on the corresponding amount pertaining Retention of Set off on the corresponding amount pertaining to purchases other than capital assets and goods in which to purchases other than capital assets and goods in which property is not transferred shall shall be calculated, as under property is not transferred shall shall be calculated, as under ----

�� by multiplying the said amount of setby multiplying the said amount of set--off by the fraction off by the fraction 16/25 where the dealer has opted to pay tax @ 8% on the 16/25 where the dealer has opted to pay tax @ 8% on the total contract value, and total contract value, and

A dealer is a works contractor and uses welding electrodes in a Fabrication work inwhich tax is paid by composition. Whether retention would be applicable on theelectrodes.

Issue

Vikram Mehta 31

electrodes.

Another issue pertains to the rate of tax which is be levied in respect of concrete mixture

►► (6) If out of the gross receipts of a dealer in any (6) If out of the gross receipts of a dealer in any year, receipts on account of sale are less than fifty year, receipts on account of sale are less than fifty per cent. of the total receipts, per cent. of the total receipts, --

►► (a) then to the extent that dealer is a hotel or club, (a) then to the extent that dealer is a hotel or club, not being covered under composition scheme, the not being covered under composition scheme, the dealer shall be entitled to claim setdealer shall be entitled to claim set--off only,off only,--

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 32

not being covered under composition scheme, the not being covered under composition scheme, the dealer shall be entitled to claim setdealer shall be entitled to claim set--off only,off only,--

►► (i) on the purchases effected in that year (i) on the purchases effected in that year corresponding to the food and drinks (whether corresponding to the food and drinks (whether alcoholic or not) which are served, supplied or, as alcoholic or not) which are served, supplied or, as the case may be, resold or sold, and the case may be, resold or sold, and

►► (ii) on the purchases of capital assets and (ii) on the purchases of capital assets and consumables pertaining to the kitchens and sale, consumables pertaining to the kitchens and sale, service or supply of the said food or drinks, andservice or supply of the said food or drinks, and

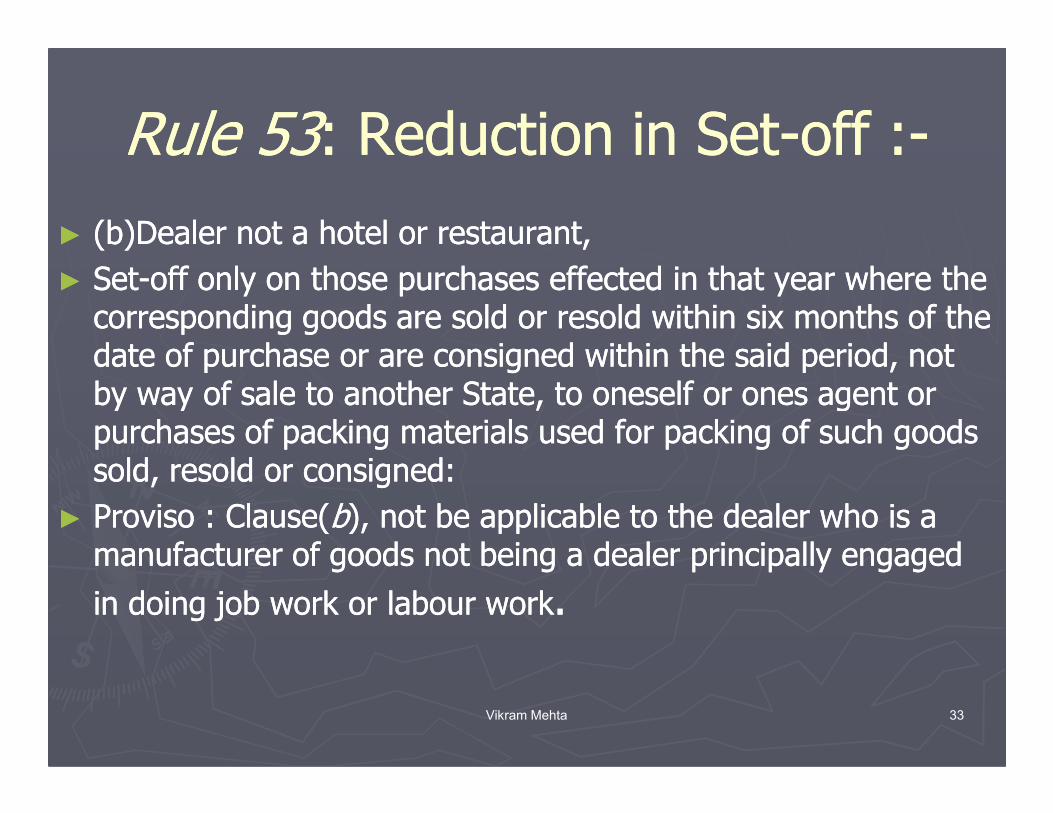

►► (b)Dealer not a hotel or restaurant,(b)Dealer not a hotel or restaurant,

►► SetSet--off only on those purchases effected in that year where the off only on those purchases effected in that year where the corresponding goods are sold or resold within six months of the corresponding goods are sold or resold within six months of the date of purchase or are consigned within the said period, not date of purchase or are consigned within the said period, not by way of sale to another State, to oneself or ones agent or by way of sale to another State, to oneself or ones agent or

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 33

by way of sale to another State, to oneself or ones agent or by way of sale to another State, to oneself or ones agent or purchases of packing materials used for packing of such goods purchases of packing materials used for packing of such goods sold, resold or consigned:sold, resold or consigned:

►► Proviso : Clause(Proviso : Clause(bb), not be applicable to the dealer who is a ), not be applicable to the dealer who is a manufacturer of goods not being a dealer principally engaged manufacturer of goods not being a dealer principally engaged

in doing job work or labour workin doing job work or labour work..

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

►► Manufacturer shall be entitled to claim setManufacturer shall be entitled to claim set--off on his off on his purchases of plant and machinery which are treated as purchases of plant and machinery which are treated as capital assets and purchases of parts, components and capital assets and purchases of parts, components and accessories of the said capital assets, and on purchases of accessories of the said capital assets, and on purchases of consumables, stores and packing materials in respect of a consumables, stores and packing materials in respect of a period of three years starting from the end of the year period of three years starting from the end of the year containing the date of effect of the certificate of containing the date of effect of the certificate of

Vikram Mehta 34

containing the date of effect of the certificate of containing the date of effect of the certificate of registration.registration.

►► Explanation.Explanation.-- For the purposes of this subFor the purposes of this sub--rule, "receipts" rule, "receipts" means the receipts pertaining to all activities including means the receipts pertaining to all activities including business activities carried out in the State but does not business activities carried out in the State but does not include Branch transfers and Consignment transfers.include Branch transfers and Consignment transfers.

►► The entire rule is reThe entire rule is re--casted on 23casted on 23--1010--08 with retrospective 08 with retrospective effect from 8effect from 8--99--06. 06.

►► ((7A) Claimant dealer has purchased office equipment, 7A) Claimant dealer has purchased office equipment, furniture or fixtures and has treated them as capital furniture or fixtures and has treated them as capital assets , then Retention of 3% on the corresponding assets , then Retention of 3% on the corresponding amount of setamount of set--off is calculated and the balance shall off is calculated and the balance shall be allowed.be allowed.

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 35

be allowed.be allowed.

►►The above proviso is not applicable to dealer The above proviso is not applicable to dealer engaged in the business of transferring the right to engaged in the business of transferring the right to use these goods.use these goods.

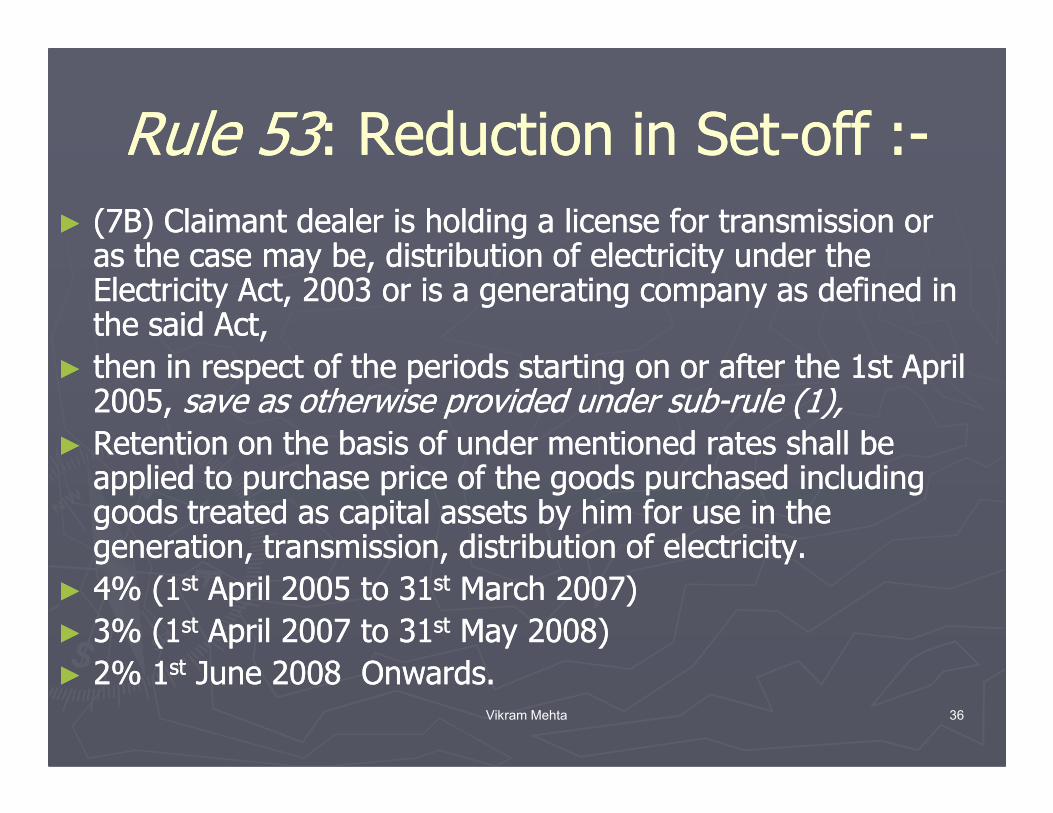

►► (7B) Claimant dealer is holding a license for transmission or (7B) Claimant dealer is holding a license for transmission or as the case may be, distribution of electricity under the as the case may be, distribution of electricity under the Electricity Act, 2003 or is a generating company as defined in Electricity Act, 2003 or is a generating company as defined in the said Act, the said Act,

►► then in respect of the periods starting on or after the 1st April then in respect of the periods starting on or after the 1st April 2005, 2005, save as otherwise provided under subsave as otherwise provided under sub--rule (1),rule (1),

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 36

2005, 2005, save as otherwise provided under subsave as otherwise provided under sub--rule (1),rule (1),

►► Retention on the basis of under mentioned rates shall be Retention on the basis of under mentioned rates shall be applied to purchase price of the goods purchased including applied to purchase price of the goods purchased including goods treated as capital assets by him for use in the goods treated as capital assets by him for use in the generation, transmission, distribution of electricity.generation, transmission, distribution of electricity.

►► 4% (14% (1stst April 2005 to 31April 2005 to 31stst March 2007)March 2007)

►► 3% (13% (1stst April 2007 to 31April 2007 to 31stst May 2008)May 2008)

►► 2% 12% 1stst June 2008 Onwards.June 2008 Onwards.

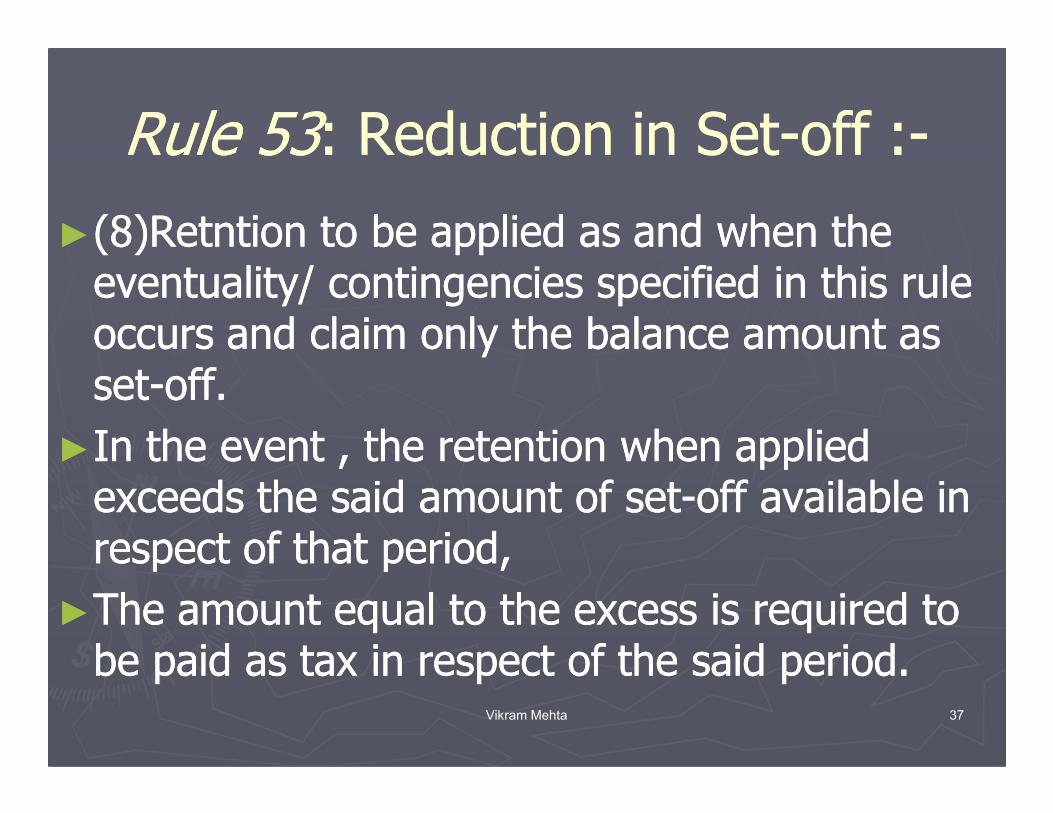

►►(8)Retntion to be applied as and when the (8)Retntion to be applied as and when the eventuality/ contingencies specified in this rule eventuality/ contingencies specified in this rule occurs and claim only the balance amount as occurs and claim only the balance amount as setset--off.off.

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 37

setset--off.off.

►►In the event , the retention when applied In the event , the retention when applied exceeds the said amount of setexceeds the said amount of set--off available in off available in respect of that period,respect of that period,

►►The amount equal to the excess is required to The amount equal to the excess is required to be paid as tax in respect of the said period.be paid as tax in respect of the said period.

►► 53(53(1010)Dealer being executing contract of processing of textiles, )Dealer being executing contract of processing of textiles,

►► then setthen set--off on the goods purchased on or after 1off on the goods purchased on or after 1stst April 2005, shall be April 2005, shall be allowed to the extent of tax paid on purchases in excess of the amount allowed to the extent of tax paid on purchases in excess of the amount calculated as under; calculated as under;

►► 4% 14% 1StSt April 2005 to 31April 2005 to 31--33--20072007

►► 3% 13% 1stst April 2007 to 31April 2007 to 31--55--20082008

2% 12% 1 June 2008 OnwardsJune 2008 Onwards

Rule 53Rule 53: Reduction in Set: Reduction in Set--off :off :--

Vikram Mehta 38

►► 2% 12% 1stst June 2008 OnwardsJune 2008 Onwards

►► For the goods in respect of which property is transferred during the said For the goods in respect of which property is transferred during the said processing, and processing, and

►► For packing materials used for packing of the said textiles,For packing materials used for packing of the said textiles,

►► For other purchases including purchases of capital assets as permissible For other purchases including purchases of capital assets as permissible under other rulesunder other rules

►► Above rule introduced on 23Above rule introduced on 23rdrd October 2008 with retrospective effect from October 2008 with retrospective effect from 11stst April 2005.April 2005.

Issues In Rule 53Issues In Rule 53

A works contractor “A” has granted a subA works contractor “A” has granted a sub--contract to ‘B’. Mr. A undertake to pay the contract to ‘B’. Mr. A undertake to pay the taxes.taxes.

(i)(i) When full setWhen full set--off is eligible on the material off is eligible on the material used by Mr. B in the course of execution used by Mr. B in the course of execution

Vikram Mehta 39

(i)(i) When full setWhen full set--off is eligible on the material off is eligible on the material used by Mr. B in the course of execution used by Mr. B in the course of execution contract.contract.

(ii)(ii) Whether retention would made applicable Whether retention would made applicable to Mr. B if Mr. A pays works contract under to Mr. B if Mr. A pays works contract under composition composition

Issues In Rule 53Issues In Rule 53Contd…..Contd…..

► Whether works contractor who transfer a property in goods worth less then 50% of the contract value shall be hit by rule 53(6).

Vikram Mehta 40

Issues In Rule 53Issues In Rule 53Contd…..Contd…..

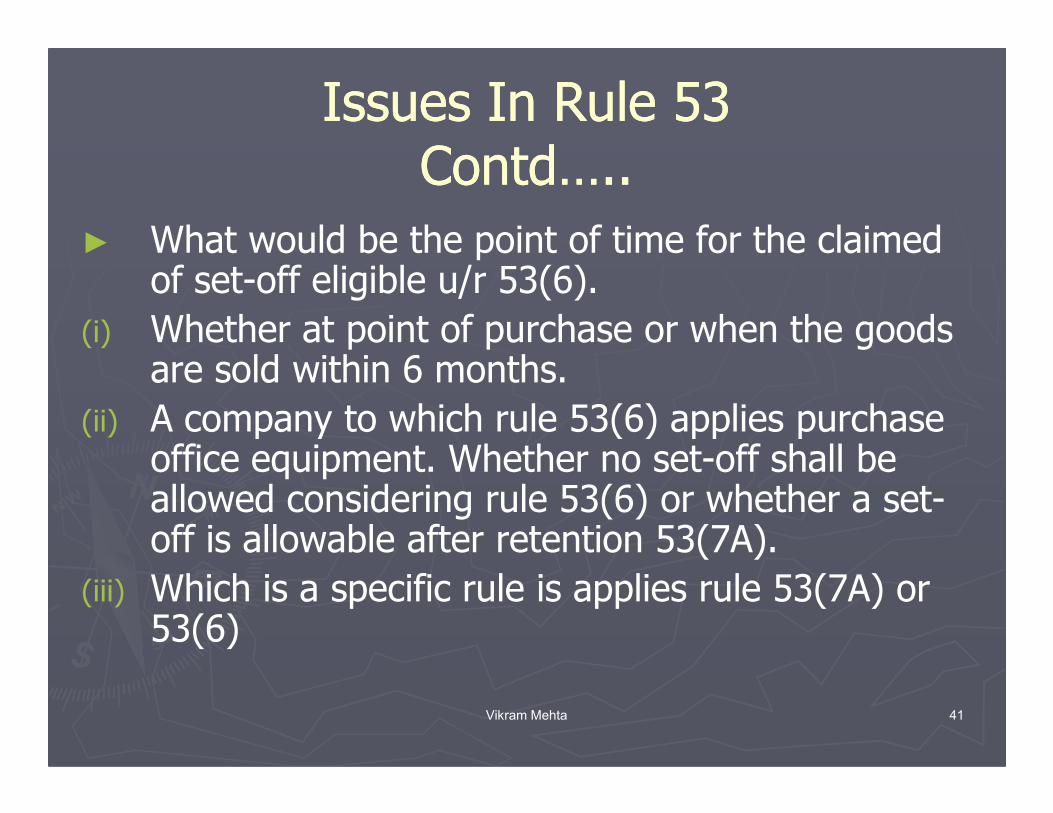

► What would be the point of time for the claimed of set-off eligible u/r 53(6).

(i) Whether at point of purchase or when the goods are sold within 6 months.

(ii) A company to which rule 53(6) applies purchase

Vikram Mehta 41

(ii) A company to which rule 53(6) applies purchase office equipment. Whether no set-off shall be allowed considering rule 53(6) or whether a set-off is allowable after retention 53(7A).

(iii) Which is a specific rule is applies rule 53(7A) or 53(6)

Issues In Rule 53Issues In Rule 53Contd….. Contd…..

►►53(9B)53(9B)--Specifies the methodology for Specifies the methodology for calculating the ratio u/r 53(2) and 53(3) calculating the ratio u/r 53(2) and 53(3) whether the dealer can calculate ratio on whether the dealer can calculate ratio on quantities and not values as specific in the quantities and not values as specific in the

Vikram Mehta 42

quantities and not values as specific in the quantities and not values as specific in the rule.rule.

►►Whether setWhether set--off will be allowable on items off will be allowable on items debited to profit & loss account in respect a debited to profit & loss account in respect a dealer who is processor of textiles dealer who is processor of textiles

IssueIssue

►►Whether the vat paid for Whether the vat paid for repairs of motor car eligible for repairs of motor car eligible for set off?set off?set off?set off?

►►NONO

Vikram Mehta 43

Rule 55Rule 55Some issues on setSome issues on set--off:off:--

► Rule 55 was amended from 8th September 2006 to allow set-off of tax paid on purchase of goods prior to registration if those goods are (1) treated as capital asset and not sold before the date of registration or (2) not sold or disposed off before the date of effect of registration or (3) used and consumed in the manufacture of goods and the manufactured goods are not sold before the date of

Vikram Mehta 44

the manufactured goods are not sold before the date of effect of registration.

► A second hand car dealer who goes for composition scheme is entitled to claim set-off on tax paid on purchase of goods used for refurbishing the second hand motor car, as the notification prohibits only the set-of on tax paid on purchase of motor vehicle or entry tax paid on motor vehicle. Thus the dealer is entitled to set off on capital assets, consumables and profit and loss accounts items.

Vikram Mehta 45