Page 1

www.icm

rr.or

g

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

SR. NO. PARTICULARS PAGE NO.

1.

A STUDY ON MEASURING THE EXTENT OF FACTORS

INFLUENCING THE URBAN CO-OPERATIVE BANKS

PROFITABILITY

DR.R.UMAMAHESWARI

1-10

2.

PORTFOLIO CONSTRUCTION ON DIFFERENT INVESTMENT

PROPOSALS AND THEIR RETURNS

S. ALAGUSAMY Dr.R.SUBRAMANIAN

10-27

3.

A STUDY ON A COMPARATIVE STUDY OF SECTOR FUNDS

WITH SPECIAL REFERENCE TO SHAREKHAN LIMITED,

CHENNAI

P. ARUNSHANKAR B. PRABHU

28-46

4.

A COMPARATIVE STUDY ON WORKING CAPITAL

MANAGEMENT OF PAINT COMPANIES WITH SPECIAL

REFERENCE TO BERGER PAINTS INDIA LIMITED AND KANSAI

NEROLAC PAINTS LIMITED – HOSUR

S. GOKULAKRISHNAN

47-69

5. A STUDY ON ROLE OF FUNDAMENTAL AND TECHNICAL

ANALYSIS IN EQUITY RESEARCH.

V.MANGAYARKARASI

70-87

6.

A STUDY ON COMPARATIVE ANALYSIS ON GOLD VERSUS

CRUDE OIL AT HARVEST FUTURES CONSULTANT INDIA (P)

LIMITED CHENNAI

A.MOHANA

88-109

7.

A STUDY ON FLUCTUATIONS IN INDIAN STOCK MARKET

JEGADEESAN.M

110- 125

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

A Peer Reviewed International Journal

IJFRR

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

ISSN 2321-0354

Page 2

www.icm

rr.or

g

1

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

A STUDY ON MEASURING THE EXTENT OF FACTORS INFLUENCING THE

URBAN CO-OPERATIVE BANKS PROFITABILITY

WITH SPECIAL REFERENCE TO COIMBATORE DIST, TAMILNADU, INDIA

Dr.R.UMAMAHESWARI

Assistant Professor

PG Department of Management Science

Sree Saraswathi Thyagaraja College, Pollachi

Coimbatore (Dist), Tamilnadu, India

ABSTRACT

Banking system occupies an important place in a nation‘s economy. A banking institution is indispensable

in a modern society. The Co-operatives play an important role in the Indian financial system, especially at the rural

level. The origins of the Urban Cooperative Banking (UCBs) movement in India can be traced to the close of

nineteenth century when, inspired by the success of the experiments related to the co-operative movement in Britain

and cooperative credit movement in Germany such societies were set up in India. Cooperative societies are based on

the principles of cooperation, - mutual help, democratic decision making and open membership. This paper looked

into the various factors influencing the profitability of the UCBs and also the correlation between the factors to

determine the profitability.

Keywords: UCBs, correlation analysis, profitability

1.1. INTRODUCTION

Banking system occupies an important place in a nation‘s economy. A banking institution is indispensable

in a modern society. It plays a pivotal role in the economic development of a country and forms the core of the

money market in an advanced country. Agriculture forms the backbone of the Indian economy. Despite converted

industrialization in over last two decades, agriculture occupies a place of pride. Being the largest industry in the

country, agriculture is the source of livelihood for over seventy percent of population in the country. The financial

requirements of Indian farmers are met through loans borrowed from money lenders and co-operative credit

societies.The Co-operatives play an important role in the Indian financial system, especially at the rural level. Co-

operatives as a great instrument to help poor and the weakest in improving their economic conditions through self-

reliance and mutual aid. In Indian economy, co-operative banks or credit societies have developed over the period

with the specific objective of financing agricultural and other economic units in the unorganized sectors.

A Peer Reviewed International Journal

IJFRR

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

ISSN 2321-0354

Page 3

www.icm

rr.or

g

2

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

The origins of the urban cooperative banking movement in India can be traced to the close of nineteenth

century when, inspired by the success of the experiments related to the co-operative movement in Britain and

cooperative credit movement in Germany such societies were set up in India. Cooperative societies are based on the

principles of cooperation, - mutual help, democratic decision making and open membership. Cooperatives

represented a new and alternative approach to organization as against proprietary firms, partnership firms and joint

stock companies which represent the dominant form of commercial organization.

1.2. REVIEW OF LITERATURE

1. Amit Basak (2009)1 Urban Cooperative Banks (UCBs) figure among the vital segments of the banking

industry of the country. They essentially cater to the credit needs of persons of small means. Though some

UCBs have performed creditably in the recent years, a large number of them have shown discernible signs

of weakness. The operational efficiency is unsatisfactory and characterized by low profitability, ever-

growing Non-Performing Assets (NPAs) and relatively low capital base. The large-scale sickness in the

UCBs has shaken the public confidence in cooperative banks. In this context, this paper makes an attempt

to examine the working and financial performance of the UCBs. To make the analysis simpler and

presentable, the author takes up the Contai Co-operative Bank Ltd., one of the leading UCBs in West

Bengal for a case study. The objective of the study is to identify and analyze the trend, progress and

problems of this bank, to throw light on the problems of swelling NPAs and to offer some meaningful

suggestions for improving the efficiency and effectiveness of this bank. The study is based on secondary

data and other information provided by the bank in its published annual reports. The relevant data have

been collected for the period from 1995-96 to 2006-07. This data have been analyzed with the help of

statistical tools like ratios, percentages, averages and trend analysis, chi-square test, and multiple regression

analysis.

2. Sampath P. Sing and Varsha S. Vrade (1974)2 of National Institute of Bank Management (NIBM) have

made a number of studies on the profitability of nationalized banks covering different aspects of

measurement of cost of funds to a bank; monitoring branch profitability; profit management; profit

management in banks; ranking of banks according to their performance in terms of deposits; branch

network and credit deposit ratio.

3. Bhatia (1978)3 in his thesis on ―Banking structure and performance‖ attempts to describe and analyse the

economic performance of the Indian Banking System as it is reflected in output, price and profitability

performance during the period 1950-68. The study suggest that the Banking Regulations in India should

not emphasize direct regulation of the rate of return as much as the regulation if the asset portfolio of banks

in order to improve the output performance of the Indian Banking System

4. Bhairav H. Desai and Mayar Raj J. Farmar (2000)4 in their article on ―concept of break even analysis and

banks profitability – a case study‖, attempted to determine the factors affecting the profitability as well as

the margin of safety of commercial banks are interest expenses and non-interest expenses.

5. Dash (2000)5, attempted to evaluate the financial performance of Nawanagar Co-operative bank by using

operational ratios, profitability ratios, productivity ratios and solvency ratios. He concluded that despite

satisfactory financial performance, there are certain grey areas which need immediate attention. Effective

steps are required to improve profitability and capital base activities.

1.3 NEED / IMPORTANCE OF THE STUDY

UCBs have always been the major vehicle for nation‘s economic development. Co-operative banks which

have been in existence for a century in India are found in both rural and urban areas. There are plenty of surpluses

1 Amit Basak , “Performance Appraisal of Urban Cooperative Banks: A Case Study”, The Icfai University Journal of Accounting

Research, Vol. 8, No. 1, pp. 31-44, January 2009. 2 Sing S.P. “Profitability of nationalized Banks”, Economic and political weekly, Vol. IX. No. 35. 3 Bhatia R.C “Banking structure and performance, A case study of Indian Banking system”, 1965-68 Ph.D. Thesis, West Viginia

University.

4 Bhairav.H.D. Desai (2000)” concept of break even analysis and Banks profitability – A case study, “The Indian Journal of Commerce,

Vol. 53, No. 182. pp. 53-59.

5 Dash .D.K (2000), “Financial Performance Evaluation through Ratio analysis – A case study of Nawanagar Co-operative Bank

Jamnagar (Gujarat, Indian Co-operative Review, Vol: XXXVII, No. 3, pp.162- 170.

ISSN 2321-0354

Page 4

www.icm

rr.or

g

3

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

resource with the urban and semi urban people, and their channelization towards economic growth is the main task

of the banks. No wonder that management of funds has emerged as an area of vital importance for banks. Notable

development has also taken place in the diversification of bank lending work, certain sectors like agriculture, small

and tiny industrial units, small transport operators; retail traders etc. which were neglected by the commercial banks

are now receiving credit from UCBS. But several factors have contributed to the poor performance of the UCBs in

India. The UCBs are facing increasing competition and therefore reduced market power; they have not modernized

their operation which leads to poor financial management and risk assessment techniques. Owing to certain structure

weakness, failure to mobilize sufficient deposits, the amounting overdue and lack of trained staff, the co-operatives

had failed to come up to expectations. In recent years, the profitability performance of UCBs in India has become a

novel topic for discussion.

1.4. STATEMENT OF THE PROBLEM

There is ample evidence to show the declining profitability of the banking industry. With the change in the

social and economic objectives of co-operative banks, particularly of the UCBs in India, it becomes extremely

essential to assess their profitability performance. However, in most of the studies covering the recent period,

‗profit‘ has been used as one of the many indicators of their performance appraisal. This dilutes the importance of

profits to a large extent. Despite the change in thrust, banks remain commercial organizations and profit factor

cannot be ignored without endangering viability of banks and continuity of their operations. In fact, the approach of

policy-makers towards profitability too has changed, with the result that low profits have become a fact of life.

Therefore, it is high time to concentrate efforts on analyzing the profits and profitability position of Urban Co-

operative Banks, so that the confidence of the public in the soundness of the banking system remains unimpaired

and the social objectives of banks do not necessarily dilute. The Urban Co-operative Bank suffers from political as

well as governmental interference and official bureaucracy in respect of resource mobilization and recovery of

loans. This has adversely affected their profitability and viability. The optimum utilization of financial resource

refers to maximization of financial return and minimization of cost and this shall be the major essence of financial

management and better utilization of funds in UCBs. The financial analysis of UCBs needs to be studied with their

impact and their effect on solvency and profitability. In this context it is felt that an in–depth analysis of ―FINANCIAL

MANAGEMENT OF URBAN CO-OPERATIVE BANKS‖ will highlight the need for the study. Hence, an attempt is

made to study the ―FINANCIAL MANAGEMENT OF URBAN CO-OPERATIVE BANKS IN

COIMBATORE DISTRICT”.

1.5. OBJECTIVES OF THE STUDY

1. To assess the factors responsible for profitability.

2. To analyze the correlation between factors of profitability.

3. To assess the performance of selected UCBs by analyzing the possible impact of various sources and uses of

funds on profitability and solvency of the banks

4. To offer suitable suggestions for the efficient and effective utilization of funds.

1.6. HYPOTHESES OF THE STUDY

1. The increase in credit has an indirect and positive effect on the profitability of banks.

2. The incremental flow of Deposits has positive relation to the bank‘s profitability.

1.7. RESEARCH METHODOLOGY

For the study, Coimbatore District in Tamil Nadu was selected purposely. All the five banks in Coimbatore

district namely Coimbatore UCB, Udumalpet UCB, Pollachi UCB, Tirupur UCB, and Mettupalayam UCB have

been included for the study. The study is based on both primary as well as secondary data. The main sources of

secondary data with regard to various aspects of UCBs are annual report and office records. Data have also been

compiled from various journals and magazines relating to the study. The primary data were also collected from

officials of the banks with the help of an interview schedule. To elicit the opinion of customers about bank services,

a separate interview schedule was administered.

ISSN 2321-0354

Page 5

www.icm

rr.or

g

4

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

All the selected banks were in the Coimbatore district when the study was commenced. In October 2008,

Tirupur and some of the nearby areas of Tirupur were separated from Coimbatore district and were included in the

newly constituted Tirupur district. So Udumalpet UCB and Tirupur UCB previously included in the Coimbatore district

are now in the newly constituted Tirupur District. As the study period (1997-98 to 2008-09) end in 2008-09, the researcher

decided to show all the selected banks to be a part of the Coimbatore district. This will in no way affect any of the

technical aspects of the research.

PERIOD OF THE STUDY

The study covered a period of twelve financial years from 1997-98 to 2008-09. The financial year starts

from 1st day of April of a year and ends on 31

st day of March of next year.

DATA COLLECTION

SECONDARY DATA

The information collected for the study is purely based on secondary in nature. The data for the study have

been collected from the Urban Co-operative Banks in Coimbatore District for the financial period from 1997-98 to

2008-2009. The required information are collected from the volumes of published reports by the Statistical

Department of RBI at Mumbai, RBI Bulletins, Reports on Trend and Progress of Banking in India, Report on

Currency and Finance, books relating to urban co-operative banks, journals, magazines, and unpublished reports.

1.8. FRAMEWORK OF ANALYSIS

The following is the framework of analysis applied by the researcher to identify solutions to the objectives

of the study.

MEASURING THE EXTENT OF FACTORS INFLUENCING THE BANK PROFITABILITY

To identify the prominent factors responsible for the profitability of UCB and to measure the extent of

influence of the independent variables on the dependent variable the following tools was applied by the researcher.

a) Correlation Analysis

1.9. LIMITATIONS OF THE STUDY

The study covers only the period between 1997-98 to 2008-09. It does not consider the changes, if any, before

or after the period.

The calculations have been made on the basis of the figures provided in the published financial statements.

Hence the study is subjected to inherent limitations of accounting and accounting practices.

The financial position of a bank is affected by several factors like economical, social, political, etc., but only

financial factors is considered here.

The financial performance are not compared with a similar firm in the same industry

MEASURING THE EXTENT OF FACTORS INFLUENCING THE BANK PROFITABILITY

CORRELATION ANALYSIS

Correlation co-efficient among the different variables has been worked out so as to arrive at a correlation

matrix, which incorporates correlation co-efficient of all the selected variables with the dependent variable, as well

as correlation coefficients among different independent variables. The calculated correlation co-efficient values

were compared with a critical value of simple correlation co-efficient available in the statistical tables (Fisher

and Yates) for its significance.

The correlation coefficient matrices of the selected variables with the dependent variable, i.e., return on total assets

of selected co-operative banks for the periods from 1997-98 to 2008-2009 presented below.

ISSN 2321-0354

Page 6

www.icm

rr.or

g

5

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

TABLE 1

CORRELATION ANALYSIS BETWEEN SELECTED VARIABLES WITH RETURN ON TOTAL

ASSETS

Varia

bles

No.

Ratios

COIMBATORE

UCB UDUMALPET UCB

R p-value r p-value

X1 Advances to Assets .244 .222 0.517 .043**

X2 Debt - Equity Ratio -.091 .389 -0.258 0.209

X3 Investments to Total Assets -.511 .045** -0.231 0.235

X4 Other Assets to Total Assets -.129 .345 0.319 0.156

X5 Credit Deposit Ratio -.024 .471 0.484 0.055

X6 Investments Deposit Ratio -.481 .056 -0.186 0.281

X7 Credit + Investments Deposit Ratio -.349 .133 0.074 0.41

X8 Fixed Assets to Total Assets .301 .171 -0.287 0.183

X9 Fixed Assets to Net worth .450 .071 -0.21 0.256

X10 Return on Advances .973 .000* 0.974 .000**

X11 Interest Income to Total Assets .604 .019** 0.404 0.096

X12 Other Liabilities to Total Assets -.129 .345 0.319 0.156

X13 Net worth to Capital employed -.349 .133 0.082 0.399

X14 Return on Net worth .832 .000* 0.518 .042**

X15 Wage Bill to Total Income -.227 .239 -0.21 0.257

X16 Operating Expenses to Total Income -.137 .336 -0.042 0.448

X17 Interest Expended to Total Expenses .205 .261 -0.034 0.458

X18 Interest expended to interest earned .306 .167 -0.519 .042**

X19 Equity paid up to Capital Employed -.468 .063 0.072 0.412

X20 Spread to Working Fund .230 .236 0.518 .042**

X21 Burden to Working Fund -.378 .113 0.119 0.356

X22 Operating profit to Total Assets .046 .444 0.104 0.374

X23 Interest Income to Total Income .093 .387 0.555 .031**

X24 Non-Interest Income to Working Fund .026 .468 -0.223 0.243

X25 Non Operating Expenses to Total Assets .378 .113 -0.024 0.47

X26 Equity paid up to Net worth .316 .158 0.031 0.462

X27 Return on capital employed .062 .424 0.133 0.34

X28 Deposits to Total Assets .246 .221 -0.166 0.303

X29 Liquid Assets to Total Assets .429 .082 -0.024 0.47

X30 Provision & Contingencies to Total Assets -.331 .147 -0.252 0.215

X31 Cash Deposit Ratio .516 .043** -0.267 0.2

X32 Investments to Advances -.529 .038** -0.286 0.183

X33 Interest cover .340 .140 0.781 .001*

*Correlation is significant at the 0.01 level (p<0.01) **Correlation is significant at the 0.05 level (p<0.05)

ISSN 2321-0354

Page 7

www.icm

rr.or

g

6

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

TABLE 2

CORRELATION ANALYSIS BETWEEN SELECTED VARIABLES WITH RETURN ON TOTAL

ASSETS

Variables

No. Ratios

POLLACHI UCB TIRUPUR UCB

R p-value r p-value

X1 Advances to Assets 0.821 .001* 0.374 0.116

X2 Debt - Equity Ratio - - - -

X3 Investments to Total Assets -0.888 .000* 0.632 .014**

X4 Other Assets to Total Assets 0.615 .017** 0.556 .030**

X5 Credit Deposit Ratio 0.733 .003* 0.91 .000*

X6 Investments Deposit Ratio -0.872 .000* 0.76 .002*

X7 Credit + Investments Deposit Ratio -0.886 .000* 0.866 .000*

X8 Fixed Assets to Total Assets 0.092 0.388 -0.78 .001*

X9 Fixed Assets to Net worth 0.734 .003* -0.864 .000*

X10 Return on Advances 0.9 .000* 0.999 .000*

X11 Interest Income to Total Assets 0.399 0.1 -0.76 .002*

X12 Other Liabilities to Total Assets 0.615 .017** 0.556 .030**

X13 Net worth to Capital employed -0.361 0.124 0.943 .000*

X14 Return on Net worth 0.952 .000* 0.385 0.108

X15 Wage Bill to Total Income -0.605 .019** 0.621 .016*

X16 Operating Expenses to Total Income -0.651 .011** 0.152 0.318

X17 Interest Expended to Total Expenses 0.742 .003* -0.569 .027**

X18 Interest expended to interest earned 0.811 .001* -0.878 .000*

X19 Equity paid up to Capital Employed 0.862 .000* 0.657 .010*

X20 Spread to Working Fund -0.794 .001* 0.779 .001*

X21 Burden to Working Fund -0.863 .000* -0.199 0.267

X22 Operating profit to Total Assets -0.086 0.395 0.857 .000*

X23 Interest Income to Total Income -0.635 .013** -0.552 .031**

X24 Non-Interest Income to Working Fund 0.694 .006* 0.505 .047**

X25 Non Operating Expenses to Total Assets 0.667 .009* -0.855 .000*

X26 Equity paid up to Net worth 0.675 .008* -0.93 .000*

X27 Return on capital employed -0.346 0.135 0.829 .000*

X28 Deposits to Total Assets 0.863 .000* -0.852 .000*

X29 Liquid Assets to Total Assets 0.367 0.12 -0.635 .013**

X30 Provision &Contingencies to Total Assets -0.423 0.085 0.377 0.114

X31 Cash Deposit Ratio 0.355 0.129 -0.126 0.348

X32 Investments to Advances -0.843 .000* 0.627 .015**

X33 Interest cover 0.609 .018** 0.974 .000*

*Correlation is significant at the 0.01 level (p<0.01) **Correlation is significant at the 0.05 level (p<0.05)

ISSN 2321-0354

Page 8

www.icm

rr.or

g

7

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

TABLE 3

CORRELATION ANALYSIS BETWEEN SELECTED VARIABLES WITH RETURN ON TOTAL

ASSETS

Variables

No. Ratios

METTUPALAYAM UCB

r p-value

X1 Advances to Assets -0.143 0.328

X2 Debt - Equity Ratio 0.056 0.432

X3 Investments to Total Assets -0.242 0.225

X4 Other Assets to Total Assets -0.094 0.386

X5 Credit Deposit Ratio -0.38 0.111

X6 Investments Deposit Ratio -0.259 0.208

X7 Credit + Investments Deposit Ratio -0.33 0.147

X8 Fixed Assets to Total Assets 0.232 0.234

X9 Fixed Assets to Net worth 0.279 0.19

X10 Return on Advances 0.994 .000*

X11 Interest Income to Total Assets 0.518 0.042

X12 Other Liabilities to Total Assets -0.094 0.386

X13 Net worth to Capital employed -0.355 0.129

X14 Return on Net worth 0.898 .000*

X15 Wage Bill to Total Income -0.367 0.12

X16 Operating Expenses to Total Income 0.034 0.459

X17 Interest Expended to Total Expenses -0.341 0.139

X18 Interest expended to interest earned 0.031 0.462

X19 Equity paid up to Capital Employed -0.354 0.13

X20 Spread to Working Fund 0.256 0.211

X21 Burden to Working Fund 0.169 0.3

X22 Operating profit to Total Assets -0.269 0.199

X23 Interest Income to Total Income 0.239 0.228

X24 Non-Interest Income to Working Fund -0.159 0.31

X25 Non Operating Expenses to Total Assets 0.285 0.185

X26 Equity paid up to Net worth 0.259 0.209

X27 Return on capital employed -0.302 0.17

X28 Deposits to Total Assets 0.373 0.116

X29 Liquid Assets to Total Assets 0.387 0.107

X30 Provision & Contingencies to Total Assets -0.156 0.314

X31 Cash Deposit Ratio 0.329 0.148

X32 Investments to Advances -0.244 0.222

X33 Interest cover 0.903 .000*

*Correlation is significant at the 0.01 level (p<0.01) **Correlation is significant at the 0.05 level (p<0.05)

ISSN 2321-0354

Page 9

www.icm

rr.or

g

8

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

1.10.FINDINGS

In Coimbatore UCB, it can be seen by table 1 that the variables namely X10(Return on Advances), X11 (Interest Income to

Total Assets), X14 (Return on Net worth), and X31 (Cash Deposit Ratio) have significant positive correlation with bank

profitability and the coefficient are 0.973, 0.604, 0.832 and 0.516 respectively.

In Udumalpet UCB, the variables namely X1 (Advances to Assets), X10 (Return on Advances), X14 (Return on Net worth),

X20 (Spread to Working Fund), X23 (Interest Income to Total Income), and X33 (Interest cover) have significant positive

correlation with bank profitability and the coefficient are 0.517, 0.974, 0.518, 0.518, 0.555, and 0.781 respectively.

An observation of the table 2 reveals that in Pollachi UCB, the variables namely X1 (Advances to Assets), X4

(Other Assets to Total Assets), X5 (Credit Deposit Ratio), X9 (Fixed Assets to Net worth), X10 (Return on Advances), X12

(Other Liabilities to Total Assets), X14(Return on Net worth), X17 (Interest Expended to Total Expenses), X18 (Interest

expended to interest earned), X19 (Equity paid up to Capital Employed), X24 (Non-Interest Income to Working Fund), X25

(Non-Operating Expenses to Total Assets), X26 (Equity paid up to Net worth), X28 (Deposits to Total Assets), and X33

(Interest cover) have significant positive correlation with bank profitability and the coefficient are 0.821, 0.615, 0.733,

0.734, 0.900, 0.615, 0.952, 0.742, 0.811, 0.862, 0.694, 0.667, 0.675, 0.863 and 0.609 respectively.

In Tirupur UCB, the variables namely X3 (Investments to Total Assets), X4 (Other Assets to Total Assets),

X5 (Credit Deposit Ratio), X6 (Investments Deposit Ratio), X7 (Credit + Investments Deposit Ratio), X10 (Return on

Advances), X12 (Other Liabilities to Total Assets), X13 (Net worth to Capital employed), X15 (Wage Bill to Total

Income), X19 (Equity paid up to Capital Employed), X20 (Spread to Working Fund), X22 (Operating profit to Total

Assets), X24 (Non-Interest Income to Working Fund), X27 (Return on capital employed), X32 (Investments to

Advances), X33 (Interest cover), have significant positive correlation with bank profitability and the coefficient are

0.632, 0.556, 0.910, 0.760, 0.866, 0.999, 0.556, 0.943, 0.621, 0.657, 0.779, 0.857, 0.505, 0.829, 0.627, and 0.974

respectively.

It is seen from table 3 that in Mettupalayam UCB, the variables namely X10 (Return on Advances), X14(Return on

Net worth), and X33 (Interest cover) have significant positive correlation with bank profitability and the coefficient are 0.994, 0.898

and 0.903 respectively.

1.11. Testing of Hypothesis

The correlation analysis proves the Hypothesis 1 and 2. The increase in the credit position of the bank has

positive effect on the profitability of banks. From the correlation coefficient matrics of the selected variables with

the dependent variable, i.e., return on total assets of UCBs for the period1997-98 to 2008-09, it can be seen that X5 -

Credit deposit ratio (r 0.733, p-value 0.003), in Pollachi UCB, the same variable(r 0.91, p-value 0.000) and X7

Credit + investment Deposit ratio (r 0.866, p-value 0.000) in Tirupur UCB, has significant correlation with positive

effect on profitability of Banks.

The second hypothesis holds good for Urban Co-operative Bank. The proportion of X28 - Deposits to total

assets (r- 863, p-value 0.000) has showed a positive correlation for Pollachi UCB. This reveals that the incremental

flow of deposits has positive impact on the profitability of selected Urban Co-operative Banks.

1.12. SUGGESTIONS

There is imperative need for launching direct development and transformation process of the co-operative

banking system towards self – sufficient and self- reliance mode.

All UCBs must adopt efficient and effective entrepreneurship skills and knowledge.

Freedom must be given to the co-operative banking system to choose their auditors, fixing accountability and

responsibility.

The UCBs need to prepare a comprehensive perspective plan for product diversification for enhancing their fee-

based income.

ISSN 2321-0354

Page 10

www.icm

rr.or

g

9

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

The UCBs should take the initiative for opening ― No Frills Account‖ to the vast sections of disadvantage and

low – income group so as to ensure greater financial inclusion.

Undertake proper assessment and regular bank audits

Establishment of apex bank for urban banks

End political intervention in co-operative banks

End dual control and redefine the functions of the authorities.

To have better functioning of Co-operative banks, the Government of India should take necessary steps to

establish‖ the Co-operative Bank of India.‖

1.13. CONCLUSION

The survival and success of urban co-operative banks depend upon the performance mainly based on the

mobilization and utilization of resources. This study is especially useful for policy makers, bankers, and researchers

as it provides adequate information about the determinants of the bank earning and profit.

1.14. SCOPE FOR THE FURTHER RESEARCH

In future efforts should be made by the researchers to identify factors responsible for poor performance of banks.

This can be possible through profitability analysis of branch banks. Moreover, factors basically responsible for low

performance of such banks should also be determined. Apart from the profitability, the concept of productivity also plays a

significant role in determining the efficiency and performance of service industry like banks. In future, it would be better

to apply the concept of productivity for analyzing the profitability of banks. More emphasis should be given to the factors,

viz., the level of non-performing assets, management of assets-liability, customer satisfaction, improvement of information

and communication technology, formulation of appropriate policies for the human resource development and corporate

governance to make the study more reliable and fruitful. The future researchers can consider the primary data for their

research to assess the customer satisfaction, employee satisfaction, turnover assessment, etc.

REFERENCES

1. Wessel and Robert, H., “Principles of Financial Analysis”, Macmillan Publishing Company, New York, 1961.

2. Desai, D.D., “Banking Finance for Agricultural Production and Marketing”, University of Bombay, Ph.D. Thesis, 1977, p. 200.

3. Reserve Bank of India, “Report of the Committee on Urban Co-operative Banks”, Bombay, 1979.

4. Purushotham, P., “Operational Growth of PACS in Andhra Pradesh”, IndianCo-operative Review, Vol XV. No.4, July 1978, pp. 479-491.

5. National Federation of State Co-operative Banks Limited, Accounting Manual, Vol.II, Bombay, 1979.

6. Masthan Jugga Rao., “Working of Scheduled Urban Co-operative Banks: Problems and Prospects”, Urban Credit, Vol.XX10, No3, Sept.,

2002, p.31.

7. Sarkar, A.N and Hanamashetty, J.S. “Co-operation in India” Sahitya Bhawan Publishers & Distributors (P) Ltd., Agra, 2002.

8. Philip Molyneux, Jonathan Williams, “Managerial Finance”; Volume: 31, Publisher: Emerald Group Publishing Limited, 2005, p. 26–35.

9. Geeta Sharma Ganesh Kawadia, “Efficiency of Urban Co-operative Banks of Maharashtra: A DEA Analysis”, The ICFAI Journal of Bank

Management, Vol. 5, Nov 2006, p. 25-38.

10. Asher, Mukul, G., “Paradigm shift in the way urban co-operative banks are managed, governed, and regulated in India”, Journal of Financial Regulation & Compliance”, Vol. 15, LKY School of Public Policy, National University.

ISSN 2321-0354

Page 11

www.icm

rr.or

g

10

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

PORTFOLIO CONSTRUCTION ON DIFFERENT INVESTMENT PROPOSALS AND

THEIR RETURNS

S. ALAGUSAMY Dr.R.SUBRAMANIAN *

* Assistant Professor

Sengunthar Institute of Management Studies

Sengunthar Arts and Science College

Tiruchengode (Tk), Namakkal (Dt) 637205.

ABSTRACT

―Portfolio Construction on different Investment proposals and their Returns‖ is an analytical project to

study the construction of investment portfolio over various phases of trade cycle for a period of Six years through

the data collected from published sources. . It aims to find out the best portfolio construction which will maximize

the return for the investor at any given period of trade cycle in terms of pricing efficiency, liquidity and stability

through the informational role. The selected investments for the portfolio construction taken for the study are

Shares, Mutual Fund, Currencies, Commodities – Metals (Gold, Silver).

Keywords: Portfolio Construction, Shares, Mutual Fund, Currencies, Commodities

1. Introduction to Portfolio Construction

In Finance industry portfolio construction deals with how to divide the investor's wealth across

some asset classes selected from a given asset classes' menu in order to maximize the investor's gain. An asset class

is a specific category of investments such as stocks, bonds, cash, and commodities. In quantitative finance portfolio

construction is achieved by an optimization process.

Portfolio construction deals with how to divide the investor wealth across some asset classes' in order to

maximize the investor gain. An asset class is a specific category of investments such as bonds, stocks, and

commodities. Assets within the same class generally exhibit similar risk characteristics, behave similarly in the

market place, and are subject to the same laws and regulations.

A Peer Reviewed International Journal

IJFRR

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

ISSN 2321-0354

Page 12

www.icm

rr.or

g

11

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

1.2 Introduction of the Study

In Finance industry portfolio construction deals with how to divide the investor's wealth across some asset

classes selected from a given asset classes' menu in order to maximize the investor's gain. An asset class is a specific

category of investments such as stocks, bonds, cash, and commodities. In quantitative finance portfolio construction

is achieved by an optimization process. A pioneering work in this regard is the well known Markowitz model. Given

a target performance, Markowitz method provides the optimal strategy which minimizes the investment risk. This

method and variations of it, are extensively used at the present by many asset managers. However, recent evolutions

of the world market showed limitations of this method and motivated many researchers and practitioners to study

alternative methodologies to portfolio construction. Main drawbacks of the Markowitz method are summarized in:

The asset classes performance is assumed to be multivariate Gaussian distributed, Investors make a one

shot allocation; the model does not face the portfolio rebalancing during the investment life time.

The first drawback is shown by basic econometric analysis of the world market to be inappropriate to

capture relevant statistical properties of asset classes' performances, while the second one does not allow the

investor to have a tight control of portfolio evolution during the investment life{time. Recently, Optimal Dynamic

Asset Allocation (ODAA) proposes a methodology to overcome such limitations. ODAA deals with how to

optimally allocate a multi-period investment. First studies in ODAA faced the problem on how to divide the

investment among stock and money markets. More recently, some work appeared in the literature concerning

optimal strategies for long{lived investors under stochastic investment opportunities. In particular, the work in

studies portfolio rebalancing in the presence of stochastic variation in the interest rate, the work in considers the

effects of inflation in a portfolio of stock or nominal bonds, the work in and takes into account the uncertainty in the

asset returns prediction.

Portfolio construction deals with how to divide the investor wealth across some asset classes' in order to

maximize the investor gain. An asset class is a specific category of investments such as bonds, stocks, and

commodities. Assets within the same class generally exhibit similar risk characteristics, behave similarly in the

market place, and are subject to the same laws and regulations. Due to unpredictability of their behavior, asset

classes‘ dynamics is usually modeled by means of stochastic processes.

1.3 Background of the Study

India is growing in a faster growth rate than any other developed country in the world. The Indian

company‘s contribution in the world economic growth is enormous. The investors like Institutional investors and

small Investors like common people are searching for a good opportunity to invest in various investment

perspectives like Shares, Mutual Funds, Gold, Bonds, Bank, Post office etc...

ISSN 2321-0354

Page 13

www.icm

rr.or

g

12

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

The Indian capital market has witnessed a major transformation and structural change the past one decade

as a result of ongoing financial sector reforms initiated by the Government of India. One of the major objectives of

these reforms was to bring the Indian capital market up to a certain international standard. Due to such reforming

process, one of the significant step taken in the secondary market is the introduction of derivative products in two

major Indian stock exchanges viz. National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) , with a

view to provide tools for risk management to investors and to improve informational efficiency of the cash market.

The instruments are used for risk management by hedging i.e. taking opposite position in the futures.

In the last decade, many emerging and transition economies have started introducing diversified portfolio

construction. Policy makers and regulators in the markets are concerned about the impact of futures on the

underlying cash market. It had long been argued that a very undesirable feature of the Indian stock market was the

mixing of cash and futures trading. Such mixing was caused by the existence of the ‗badla system‘, combined with

long settlement cycles. All this has been ended by the package of reforms implemented after the stock market crisis

of March 2001. There is need for assessing the resulting new situation which is still in transition but some useful

experience has been gathered over the last few months. Such assessment has to be based on an examination of the

nature of inter-relationships, both direct and indirect, between the operation of the futures market and the cash

markets.

Institutional investors have lot of data can easily take their investment decision. But the small investor can‘t

do like that. This is because the small investor unclear on how to analyze the investment perspective and also they

don‘t know how to take decision during the market failures. This study provides the suggestion for small investor

about where to invest the money for higher returns as well as with minimal amount of risks in all the cases, whether

market is big boom or on recession. An important aspect to study is the migration of most of the speculative activity

from one investment to another investment provides easier and high returns.

1.4 Statement of the Problem

The market in which investment happens is unstable and unpredictable one. The investors may have the

chances of losing their investment or loosing higher return. This happens only when the investors are not aware of

market situations and high yielding investment choices. The main sufferer in all the investment alternatives during

the unstable state is the Small investors. The problems faced by them are higher losing of the capital.

1.5 Period of Study

The period of the study has been taken-Up from the year 2007 to 2012(6 Years), a sufficient time for any

portfolio to correct themselves according to their ups and downs.

ISSN 2321-0354

Page 14

www.icm

rr.or

g

13

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

2. REVIEW OF LITERATURE

Mark Rubinstein (1973). According to their results, investors are risk averse and show preference for

positive asymmetry, being even disposed to pay a significant price for the "safety" that the latter provides

Ross (1976), Arditti & John (1980) and Breeden & Litzenberger (1978), among others, evidencing the

important contribute of these instruments for the expansion contingencies covered by the market. On the other hand,

some empirical studies demonstrate that options‘ introduction has positive effects both on volatility and on

underlying asset price, contributing to market stability [e.g. Nabar and Park (1988), Conrad (1989), Gemmill (1989),

Detemple & Selden (1991), Haddad & Voorheis (1991), Figlewski & Webb (1993)].

Leland (1999) suggests a new evaluation methodology, considered more appropriated to the asymmetrical

return distributions exposed in the third section. Leland (1999) modifies the traditional risk measure, beta, so that it

captures all the elements of risk, here. In the sequence of this adjustment, the performance of any investment

strategy can be more precisely evaluated.

Fernandes (2003) evaluated index fund implementation in India. In this paper, tracking error of index funds

in India is measured. The consistency and level of tracking errors obtained by some well-run index fund suggests

that it is possible to attain low levels of tracking error under Indian conditions. At the same time, there seems to be

periods where certain index funds appear to depart from the discipline of indexation.

Pendaraki, Zopounidis and Doumpous (2005) studied construction of portfolios, developed a multi-criteria

methodology and applied it to the Greek market of equity funds. The methodology is based on the combination of

discrete and continuous multi-criteria decision aid methods for mutual fund selection and composition.

Zakri (2005) matched a sample of socially responsible funds to randomly selected conventional funds of

similar net assets to investigate differences in characteristics of assets held, degree of portfolio diversification and

variable effects of diversification on investment performance. The study found that socially responsible funds do not

differ significantly from conventional funds in terms of any of these attributes.

Agarwal (2007) provides an overview of mutual fund activity in emerging markets. It describes their size

and asset allocation. This paper analyzes the Indian Mutual Fund Industry pricing mechanism with empirical studies

on its valuation. It also analyzes data at both the fund-manager and fund-investor levels.

Guha (2008) focused on return-based style analysis of equity mutual funds in India using quadratic

optimization of an asset class factor model proposed by William Sharpe. The study found the ―Style Benchmarks‖

of each of its sample of equity funds as optimum exposure to 11 passive asset class indexes. The study also analyzed

the relative performance of the funds with respect to their style benchmarks. The results of the study showed that the

funds have not been able to beat their style benchmarks on the average.

Anand and Murugaiah (2008) examined the components and sources of investment performance in order to

attribute it to specific activities of Indian fund managers. They also attempted to identify a part of observed return

which is due to the ability to pick up the best securities at given level of risk. For this purpose, Fama's methodology

ISSN 2321-0354

Page 15

www.icm

rr.or

g

14

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

is adopted here. The study covers the period between April 1999 and March 2003 and evaluates the performance of

mutual funds based on 113 selected schemes having exposure more than 90percent of corpus to equity stocks of 25

fund houses. The empirical results reported reveal the fact that the mutual funds were not able to compensate the

investors for the additional risk that they have taken by investing in the mutual funds. The study concludes that the

influence of market factor was more severe during negative performance of the funds while the impact selectivity

skills of fund managers was more than the other factors on the fund performance in times of generating positive

return by the funds. It can also be observed from the study that selectivity, expected market risk and market return

factors have shown closer correlation with the fund return.

3. Objectives of the study

The ultimate objective of this study is to create a deeper understanding of this new phenomenon especially

in Indian scenario the specific Indian setting. It aims to find out whether the diversified portfolio has contributed

towards the improvement of the reducing risk in capital and increasing returns with functions in terms of pricing

efficiency, liquidity and stability. Moreover this project will also be helpful in making the people more informative

and knowledgeable about the investment options in the unstable market.

1. To analyze the performance of the selected investment alternatives in India through the returns given

by them.

2. To find out which investment alternatives gives the maximum return.

3. To find the optimum selection of investment.

4. To offer suitable suggestions for the common man about where to invest money for higher returns.

3.1 Limitations of the Study

Taking into consideration the objectives of the study and its coverage both in terms of time span and the

number of banks, the study is prone to many limitations. Some of the major unavoidable limitations of the present

work are as follows:

The study has been undertaken only through the analysis of only selected investment alternatives.

While computing the data for the purpose of analysis, the approximation of decimal places leads to minor

variations in ratios and percentage analysis, which are bound to exist in the present study.

Various accounting and statistical tools extensively used for the present study have their own limitations.

Financial information collected for the present study is entirely secondary in nature. In such a case, the

study carries all the limitations inherent with the secondary data and financial information.

There may be chance of giving a higher return on selection of some other alternative investment.

Thus, the findings of the present study should be used judiciously and carefully taking into account the

various limitations.

ISSN 2321-0354

Page 16

www.icm

rr.or

g

15

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

4 RESEARCH METHODOLOGY

4.1Type of Project

Portfolio Construction on Different Investment Proposals and their Returns is an analytical project

to study the construction of investment portfolio over various phases of trade cycle for a period of three years

through the data collected from published sources.

4.2 Data Source

Secondary data Viz., Interest rates, Share prices, Mutual fund unit prices, Net Asset value , Currency

prices on various dates, Bid price of Initial Public offers, Interest rates of Bonds and Debentures, Prices of

Commodities like Gold, Silver, Copper were to collected for the period 2007 to 2012 (6 Years).

They are collected from various websites such as NSE India, Amfi India, Forex, Kitco, Mcx, Published

journals and News papers.The selected investments for the portfolio construction taken for the study are,

Shares – Selected shares from Nifty.

Mutual Fund – Selected Funds.

Currencies – Selected Currencies.

Commodities – Metals (Gold, Silver).

4.3 Sample Design

Simple Random Sampling is the foundation of Probability Sampling. It is a special case of probability

sampling in which every unit in the population has the same chance of being selected. Thus the investments are

selected at randomly.

4.4 Tools for Analysis

To suit the objectives of the study, the following tools and techniques were applied for the study.

Comparative Analysis.

Percentage Analysis.

5. INVESTMENT ALTERNATIVES

5.1 Shares

In finance a share is a unit of account for various financial instruments including stocks, mutual funds, limited

partnerships, and REIT's. In British English, the usage of the word share alone to refer solely to stocks is so common

that it almost replaces the word stock itself.

ISSN 2321-0354

Page 17

www.icm

rr.or

g

16

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

In simple Words, a share or stock is a document issued by a company, which entitles its holder to be one of the

owners of the company. A share is issued by a company or can be purchased from the stock market.By owning a

share you can earn a portion and selling shares you get capital gain. So, your return is the dividend plus the capital

gain. However, you also run a risk of making a capital loss if you have sold the share at a price below your buying

price.

Quick Facts on Stocks and Shares

Owning a stock or a share means you are a partial owner of the company, and you get voting rights in

certain company issues.

Over the long run, stocks have historically averaged about 10% annual returns However, stocks offer no

guarantee of any returns and can lose value, even in the long run.

Investments in stocks can generate returns through dividends, even if the price.

5.2 Mutual Funds

Mutual funds are investment companies that pool money from investors at large and offer to sell and buy

back its shares on a continuous basis and use the capital thus raised to invest in securities of different companies.

At the beginning of this millennium, mutual funds out numbered all the listed securities in New York Stock

Exchange. Mutual funds have an upper hand in terms of diversity and liquidity at lower cost in comparison to bonds

and stocks.

Mutual funds are investment companies that pool money from investors at large and offer to sell and buy

back its shares on a continuous basis and use the capital thus raised to invest in securities of different companies.

The stocks these mutual funds have are very fluid and are used for buying or redeeming and/or selling shares at a net

asset value. Mutual funds posses shares of several companies and receive dividends in lieu of them and the earnings

are distributed among the share holders.

Mutual funds can be either or both of open ended and closed ended investment companies depending on

their fund management pattern. An open-end fund offers to sell its shares (units) continuously to investors either in

retail or in bulk without a limit on the number as opposed to a closed-end fund. Closed end funds have limited

number of shares.

Mutual funds have diversified investments spread in calculated proportions amongst securities of various

economic sectors. Mutual funds get their earnings in two ways. First is the most organic way, which is the dividend

they get on the securities they hold. Second is by the redemption of their shares by investors will be at a discount to

the current NAVs (net asset values).

ISSN 2321-0354

Page 18

www.icm

rr.or

g

17

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

5.3 Currency

Originally, only very large enterprises had access to the foreign exchange trading (forex / fx / currency)

trading in the inter-bank business, the largest and most liquid financial market in the world. In this market,

currencies up to a value of around 1,500 billion USD are bought and sold by its approximately 200,000 world-wide

participants every day and 24 hours per day.

In the past few years this highly attractive market has become more and more accessible to individual

clients. The market participants, who are linked world-wide by modern communication systems, control the prices

(rates), as this market too, follows the laws of supply and demand.

As a result continuous changes in rates are seen. Foreign exchange trading (buying and selling of different

currencies) consists of making profitable use of these market fluctuations on the basis of well-tried currency trading

models. The special advantage of this investment as opposed to traditional investments such as fixed interest shares

etc. is that profits can also be made in case of the USD falling instead of rising compared to other currencies.

A deal is concluded between two different currencies, with one currency theoretically representing the loan

currency (debit) and the other one the investment currency (credit). Results are limited to the amount of the

difference between the entrance and exit prices. It is possible to trade using 100 times or more of our own capital.

This is called leverage or gearing. A relatively small market movement will have a proportionately larger impact on

the funds we have deposited or will have to deposit

Trading successfully is no simple matter. It takes time, market knowledge and market understanding and a

large amount of self restraint.

The Foreign exchange market is volatile by nature. The practice of trading it by way of margin increases

that volatility exponentially. We are talking about a very 'fast market' which is naturally inconsistent. In order to

make a successful trade, a trader has to take into account technical and fundamental data and make an informed

decision based on his perception of market sentiment and market expectation. Timing a trade correctly is probably

the most important variable in trading successfully. Invariably there will be times when a traders' timing will be off.

So don't expect to generate returns on every trade.

5.4 Commodity

A commodity is something that is supplied in several different places without any qualitative difference.

For example: gold, crude oil, copper, wheat and so on. Therefore, barring man-made taxes and transportation costs,

their prices would be broadly similar in all locations. So there is a thriving market for commodities worldwide—

unlike equities, which are usually country specific. And in the recent past, commodities have become an accepted

asset class with significant chunks of smart money being invested in commodities markets worldwide.

ISSN 2321-0354

Page 19

www.icm

rr.or

g

18

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

Given the global growth in GDP, we remain in the early stages of a multiyear bull market in commodities. It is

clearly a consumption-driven story, with the leading players being China and India and followed by a host of other

fast developing nations.

Besides, there is the argument frequently made that ―commodity prices cannot go to zero‖ and thus are, in a

sense, bounded on the upside as well as on the downside. In other words, rising input costs of raw materials, labour

or even capital will force supply and demand responses so that price increase is controlled. It may be pertinent and

topical to note at this point that crude oil has gone to $100 per barrel levels but the experience of just a decade ago

shows that high prices fed by high demand eventually led to a downward spiral with low prices and low demand

brought about by lower consumption due to high prices.

So if there is no guarantee that prices will continue going up, then where is the guarantee of returns? Well,

just as in equity trading, markets can and do move both ways. The trick is to use not only the futures markets but

also the spot markets for getting returns commensurate with the perceived risk. However, futures markets, unlike

spot markets, are a virtual zero-sum game and work using leverage (only a margin of 5-25% of the contract value

typically has to be deposited to take the ‗position‘). Sure, there is a lot of money waiting to be made in the

commodity markets over the next decade, but all trading needs care, identification of sources of return and learning

more and more about the markets as an ongoing process.

Like all markets, commodity markets are meeting places of buyers and sellers and the commodity

exchanges in India mainly trade bullion, base metals, energy and agricultural produce. Unlike developed countries,

foreign currency and stock indices are not part of our commodity markets and are unlikely to be integrated in the

near future.

One clear and useful economic function that commodity markets perform is that they provide a platform for

price risk management for both producers and consumers. Commodity prices typically move in tandem with

inflation and as demand for goods and services increases, the price of goods and services usually rises too, as does

the price of the commodities used to produce those goods and services.

ISSN 2321-0354

Page 20

www.icm

rr.or

g

19

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

6. DATA ANALYSIS AND INTERPRETATION

INVESTMENTS & RETURNS CHARTS

CONSOLIDATED STATEMENT OF INVESTMENT AND RETURNS - 2007

Table No.1

S.No Alternatives Principal Sale Proceeds Capital Gain Contributing

%

1 Shares 149861 223579 73718 49.19

2 Mutual Fund 149452.5 424060.85 274608.35 183.74

3 Currency 149701.5 195097.5 45396 30.32

4 Commodities – gold 149875.2 170035.2 20160 13.45

5 Commodities –silver 149528.11 139201.77 -10326.34 -6.91

Total 748418 1151974 403556 269.80

Chart No.1

While observing the data it is interfered that in the year 2007, return from Mutual Fund ranks 1st with

183.74 % followed by shares in secondary market which fetches 49.19%

But on the other hand the currency trading investment lead to a negative mark and result in loss of capital

invested up to -6.91%. The overall investment fetches a return of 269.80%.

ISSN 2321-0354

Page 21

www.icm

rr.or

g

20

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

CONSOLIDATED STATEMENT OF INVESTMENT AND RETURNS - 2008

Table No.2

S.No Alternatives Principal Sale Proceeds Capital Gain Contributing %

1 Shares 149904.2 77774.6 -72129.6 -48.11

2 Mutual Fund 149274.2 68873.79 -80400.41 -53.86

3 Commodities – gold 149874.75 153945.75 4071 2.71

4 Commodities -silver 149897.2 108331.6 -41565.6 -27.72

5 currency 149863.9 184917.57 35053.67 23.39

Total Investment 748814.25 593843.31 -154970.94 -20.69

Chart No.2

The above statement shows the investment in various alternatives and their returns. It also shows the percentage of

returns in positive and negative values for the year 2008.

The total investment for the year, the return on the total investment, capital gain or loss and the percentage of return

on investment is also shown.

ISSN 2321-0354

Page 22

www.icm

rr.or

g

21

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

CONSOLIDATED STATEMENT OF INVESTMENT AND RETURNS – 2009

Table No.3

S.No Alternatives Principal Sale Proceeds Capital Gain Contributing %

1 Shares 149440.4 289324.25 139883.85 93.6

2 Mutual Fund 149841.5 262779.84 112938.34 75.37

3 Commodities – gold 149539.5 185962.5 36423 24.35

4 Commodities -silver 149912.4 229874.7 79962.3 53.33

5 currency 149762.21 145945.1 -3817.11 -2.54

Total Investment 748496.01 1113886.39 365,390.38 48.81

Chart No.3

The above statement shows the investment in various alternatives and their returns. It also shows the percentage of

returns in positive and negative values for the year 2009.

The total investment for the year, the return on the total investment, capital gain or loss and the percentage of return

on investment is also shown.

ISSN 2321-0354

Page 23

www.icm

rr.or

g

22

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

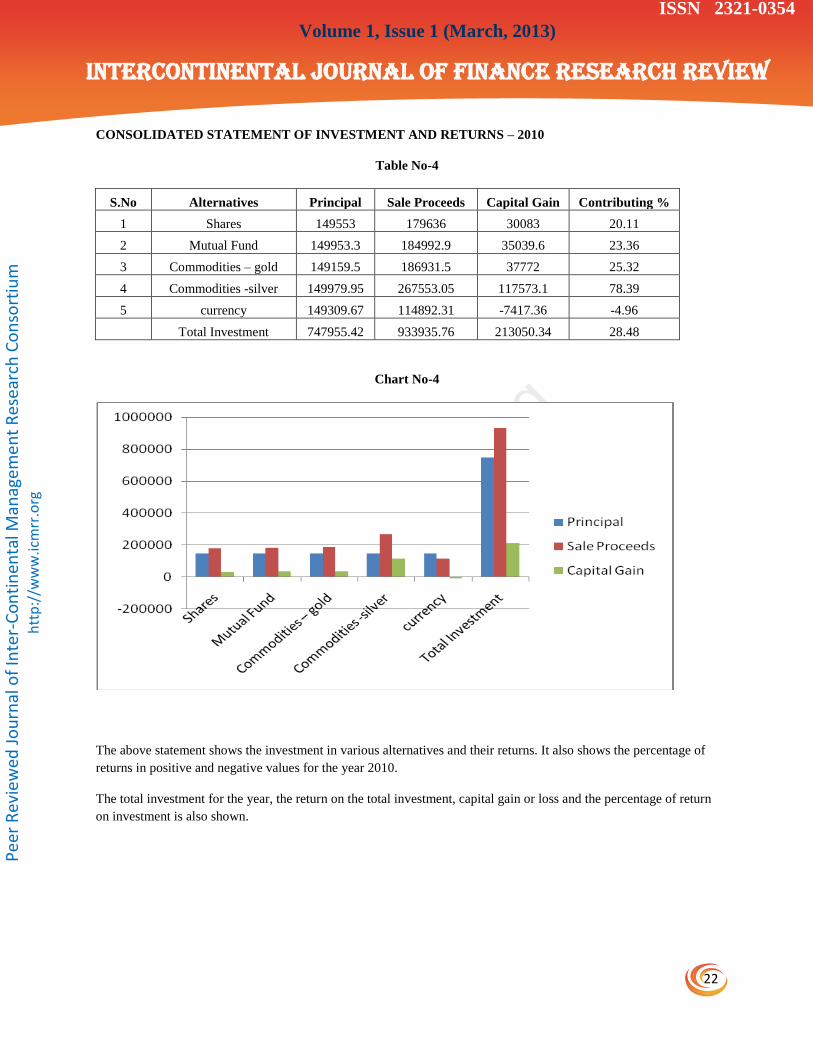

CONSOLIDATED STATEMENT OF INVESTMENT AND RETURNS – 2010

Table No-4

S.No Alternatives Principal Sale Proceeds Capital Gain Contributing %

1 Shares 149553 179636 30083 20.11

2 Mutual Fund 149953.3 184992.9 35039.6 23.36

3 Commodities – gold 149159.5 186931.5 37772 25.32

4 Commodities -silver 149979.95 267553.05 117573.1 78.39

5 currency 149309.67 114892.31 -7417.36 -4.96

Total Investment 747955.42 933935.76 213050.34 28.48

Chart No-4

The above statement shows the investment in various alternatives and their returns. It also shows the percentage of

returns in positive and negative values for the year 2010.

The total investment for the year, the return on the total investment, capital gain or loss and the percentage of return

on investment is also shown.

ISSN 2321-0354

Page 24

www.icm

rr.or

g

23

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

CONSOLIDATED STATEMENT OF INVESTMENT AND RETURNS – 2011

Table No-5

S.No Alternatives Principal Sale Proceeds Capital Gain Contributing %

1 Shares 149603.9 120542.7 -29061.2 -19.42

2 Mutual Fund 149316.92 112194.26 -37122.66 -24.86

3 Commodities – gold 149958 165348 15390 10.26

4 Commodities -silver 149976.3 137800.2 -12176.1 -8.11

5 currency 149179.59 175482.83 26303.24 17.63

Total Investment 748034.71 711367.99 -36666.72 -4.9

Chart No-5

The above statement shows the investment in various alternatives and their returns. It also shows the percentage of

returns in positive and negative values for the year 2011.

The total investment for the year, the return on the total investment, capital gain or loss and the percentage of return

on investment is also shown.

ISSN 2321-0354

Page 25

www.icm

rr.or

g

24

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

CONSOLIDATED STATEMENT OF INVESTMENT AND RETURNS - 2012

Table No-6

S.No Alternatives Principal Sale Proceeds Capital Gain Contributing %

1 Shares 149404.5 183193.8 33789.3 22.61

2 Mutual Fund 149706.88 194582.61 44875.73 29.97

3 Commodities – gold 149614 154147.5 5533.5 3.69

4 Commodities -silver 149656 155740 6084 4.06

5 currency 149622 155338.02 5716.02 3.82

Total Investment 748003.38 687261.93 95999.05 12.83

Chart No-6

The above statement shows the investment in various alternatives and their returns. It also shows the percentage of

returns in positive and negative values for the year 2012.

The total investment for the year, the return on the total investment, capital gain or loss and the percentage of return

on investment is also shown.

ISSN 2321-0354

Page 26

www.icm

rr.or

g

25

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

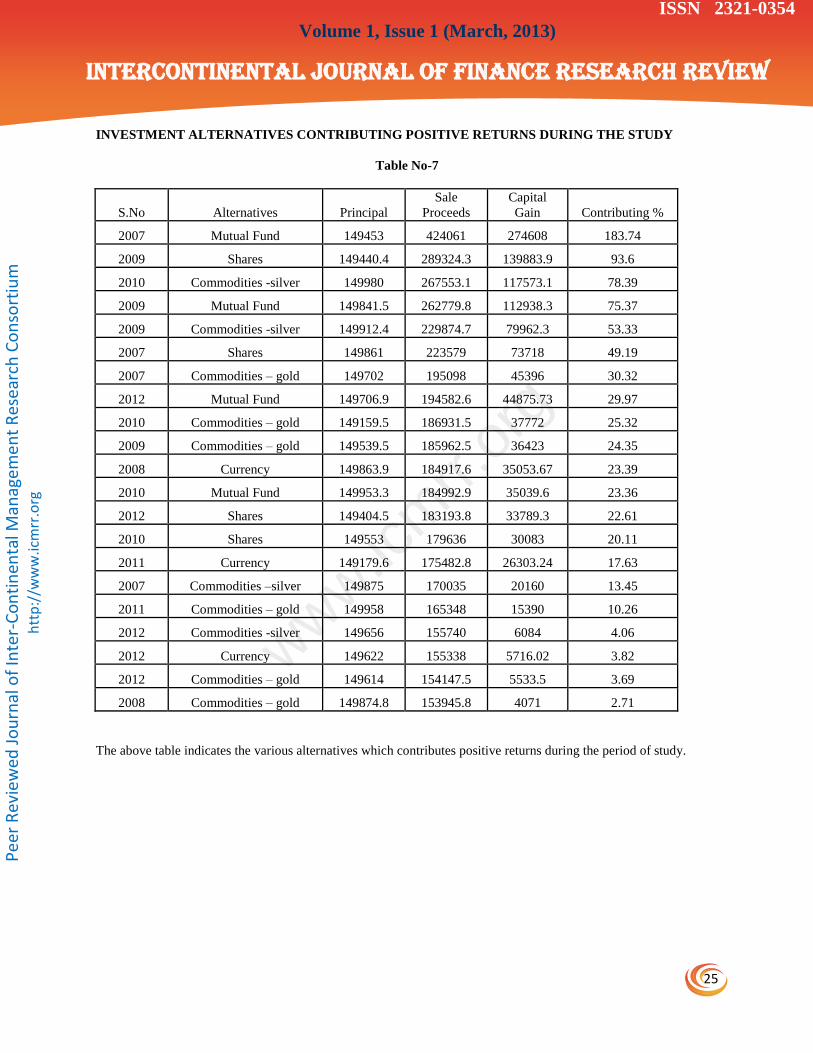

INVESTMENT ALTERNATIVES CONTRIBUTING POSITIVE RETURNS DURING THE STUDY

Table No-7

S.No Alternatives Principal

Sale

Proceeds

Capital

Gain Contributing %

2007 Mutual Fund 149453 424061 274608 183.74

2009 Shares 149440.4 289324.3 139883.9 93.6

2010 Commodities -silver 149980 267553.1 117573.1 78.39

2009 Mutual Fund 149841.5 262779.8 112938.3 75.37

2009 Commodities -silver 149912.4 229874.7 79962.3 53.33

2007 Shares 149861 223579 73718 49.19

2007 Commodities – gold 149702 195098 45396 30.32

2012 Mutual Fund 149706.9 194582.6 44875.73 29.97

2010 Commodities – gold 149159.5 186931.5 37772 25.32

2009 Commodities – gold 149539.5 185962.5 36423 24.35

2008 Currency 149863.9 184917.6 35053.67 23.39

2010 Mutual Fund 149953.3 184992.9 35039.6 23.36

2012 Shares 149404.5 183193.8 33789.3 22.61

2010 Shares 149553 179636 30083 20.11

2011 Currency 149179.6 175482.8 26303.24 17.63

2007 Commodities –silver 149875 170035 20160 13.45

2011 Commodities – gold 149958 165348 15390 10.26

2012 Commodities -silver 149656 155740 6084 4.06

2012 Currency 149622 155338 5716.02 3.82

2012 Commodities – gold 149614 154147.5 5533.5 3.69

2008 Commodities – gold 149874.8 153945.8 4071 2.71

The above table indicates the various alternatives which contributes positive returns during the period of study.

ISSN 2321-0354

Page 27

www.icm

rr.or

g

26

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

INVESTMENT ALTERNATIVES CONTRIBUTING NEGATIVE RETURNS DURING THE STUDY

Table No-8

S.No Alternatives Principal Sale Proceeds Capital Gain Contributing %

2008 Mutual Fund 149274.2 68873.79 -80400.41 -53.86

2008 Shares 149904.2 77774.6 -72129.6 -48.11

2008 Commodities -silver 149897.2 108331.6 -41565.6 -27.72

2011 Mutual Fund 149316.92 112194.26 -37122.66 -24.86

2011 Shares 149603.9 120542.7 -29061.2 -19.42

2011 Commodities -silver 149976.3 137800.2 -12176.1 -8.11

2007 currency 149528.11 139201.77 -10326.34 -6.91

2010 currency 149309.67 114892.31 -7417.36 -4.96

2009 currency 149762.21 145945.1 -3817.11 -2.54

The above table indicates the various alternatives which contributes negative returns during the period of study.

7. FINDINGS

1. The analysis shows the investment in shares fetch a positive return on investment during the years 2007,

2009, 2010 and 2012.

2. During the period of study, the investment in shares incur a capital loss in the years of 2008 and 2011.

3. The analysis shows the investment in mutual funds fetch a positive return on investment during the years

2007, 2009, 2010 and 2012.

4. During the period of study, the investment in mutual funds incurs a capital loss in the years of 2008 and

2011.

5. Investment in gold found to be continuously showing a positive return on investment throughout the period

of study.

6. Except in the years 2008 and 2011, investment in silver has also contributed a positive return on

investment.

7. Alternatively currency fetches a positive return on investment in those years whenever shares and mutual

funds give a negative return.

8. The total return on investment found to be positive in the years of 2007,2009,2010,2012.

ISSN 2321-0354

Page 28

www.icm

rr.or

g

27

Volume 1, Issue 1 (March, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

8. SUGGESTIONS

From the above study the suggestions for the investor are,

1. As India is a developing country the investors always should give more preference to shares, mutual funds

and gold as a part of investment.

2. During the period of the study there may be a changes in import and export, the investor should keep an eye

on the forex trading.

3. In order to reduce the risk on the capital investment, the investor should invest up to 25% in bank deposit,

bonds and debenture which gives fixed return.

4. As the commodity market gaining important in current market condition, the investor can invest 10 to 15%

of his investment in commodity market especially in metals.

5. Any investor should construct his portfolio according to the phase of trade cycle prevails in the country to

get maximum returns.

9. CONCLUSION