22

Interdependence of Preferential Economic Policies across Subjects Peter Egger* & Georg Wamser * ETH Zürich, CEPR Workshop on PTAs and the WTO: A New Era WTO, November 04, 2010

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | abner-stone |

| View: | 219 times |

| Download: | 0 times |

Interdependence of Preferential Economic Policies across

Subjects

Peter Egger* & Georg Wamser

* ETH Zürich, CEPR

Workshop on PTAs and the WTO: A New Era

WTO, November 04, 2010

MotivationMany Economic Integration Agreements

affect services; directly or indirectly:• Some Goods Trade Agreements (customs

unions; free trade areas; single market programme)

• Specific Service Trade Agreements under auspices of WTO (economic integration agreements; GATS commitments)

• Bilateral Investment Treaties• Bilateral Tax Treaties• Currency Unions including Pegs

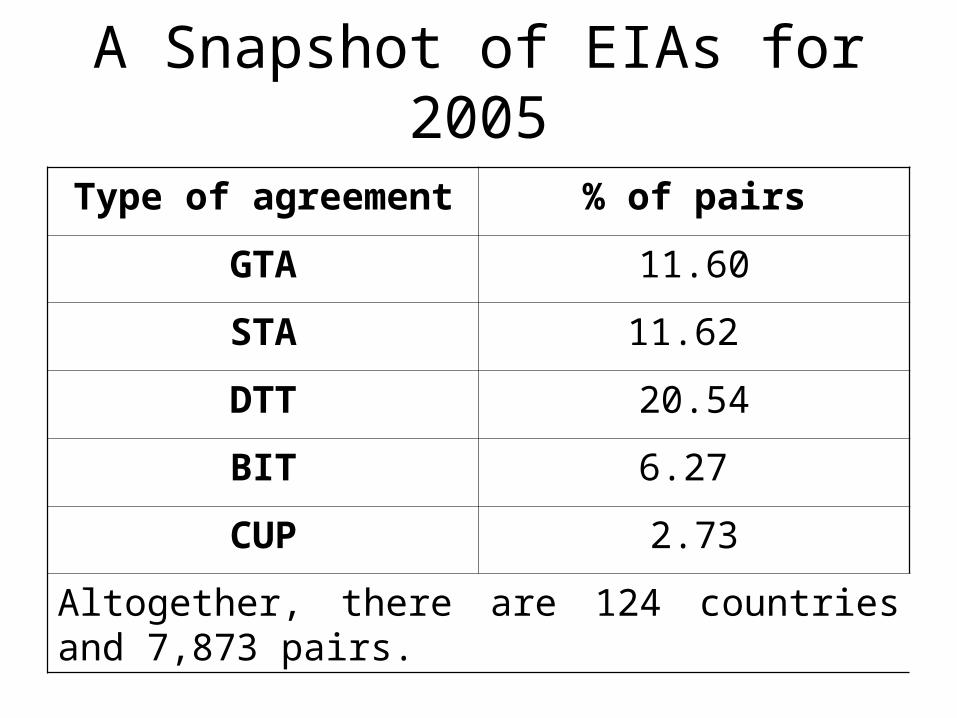

A Snapshot of EIAs for 2005

Type of agreement % of pairs

GTA 11.60

STA 11.62

DTT 20.54

BIT 6.27

CUP 2.73

Altogether, there are 124 countries and 7,873 pairs.

A Snapshot of EIAs for 2005Countries with/and

GTA STA BIT DTT CUP None

GTA

STA 5.5

BIT 1.9 1.6

DTT 6.0 4.4 5.3

CUP 0.9 0.9 0.4 1.4

None 3.8 5.5 0.5 10.1 1.2 66.5

What’s Behind That Simple TableReality is a jungle of EIAs

(Spaghetti Bowl in 5-dimensional space):25=32 combinations possible

The following ones are most frequent:

Agreements Frequency (All Years?2005)GTA

STA

B I T

DTT

CUP

# of pairs % of all EIAs

0 0 0 0 0 5,238 66.53

0 0 1 0 0 800 10.16

0 1 0 0 0 429 5.45

1 0 0 0 0 300 3.81

0 0 1 1 0 257 3.26

Questions

• Determinants of each type of EIA (economic fundamentals)?

• How is membership correlated given fundamentals?

• What are consequences of EIAs and their combination?

• Which outcomes are affected?

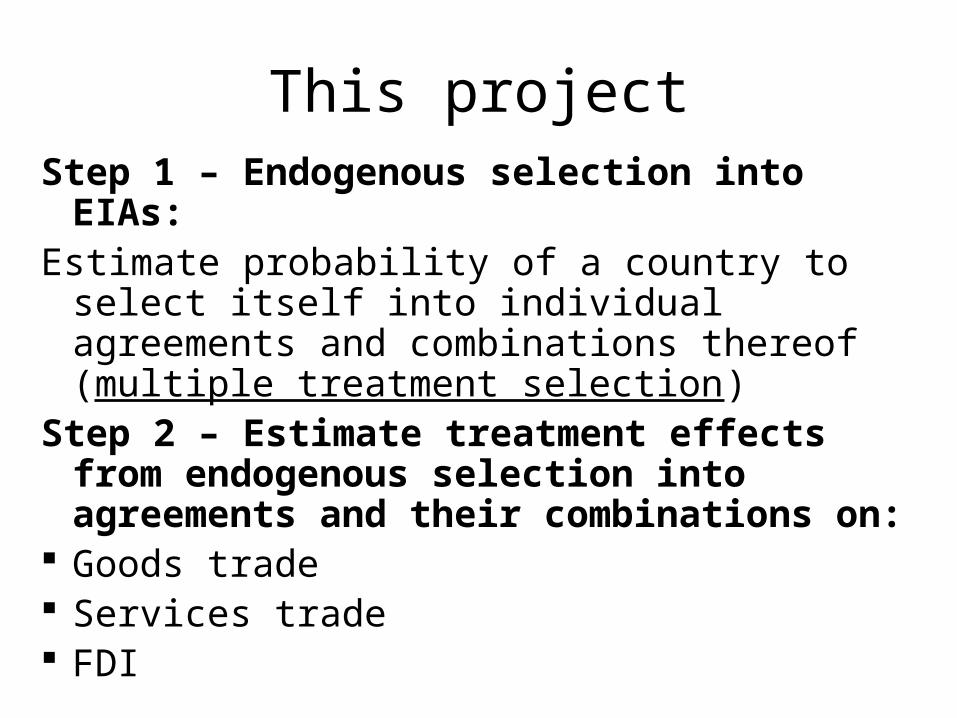

This projectStep 1 – Endogenous selection into EIAs:Estimate probability of a country to select itself

into individual agreements and combinations thereof (multiple treatment selection)

Step 2 – Estimate treatment effects from endogenous selection into agreements and their combinations on:

Goods trade Services trade FDI

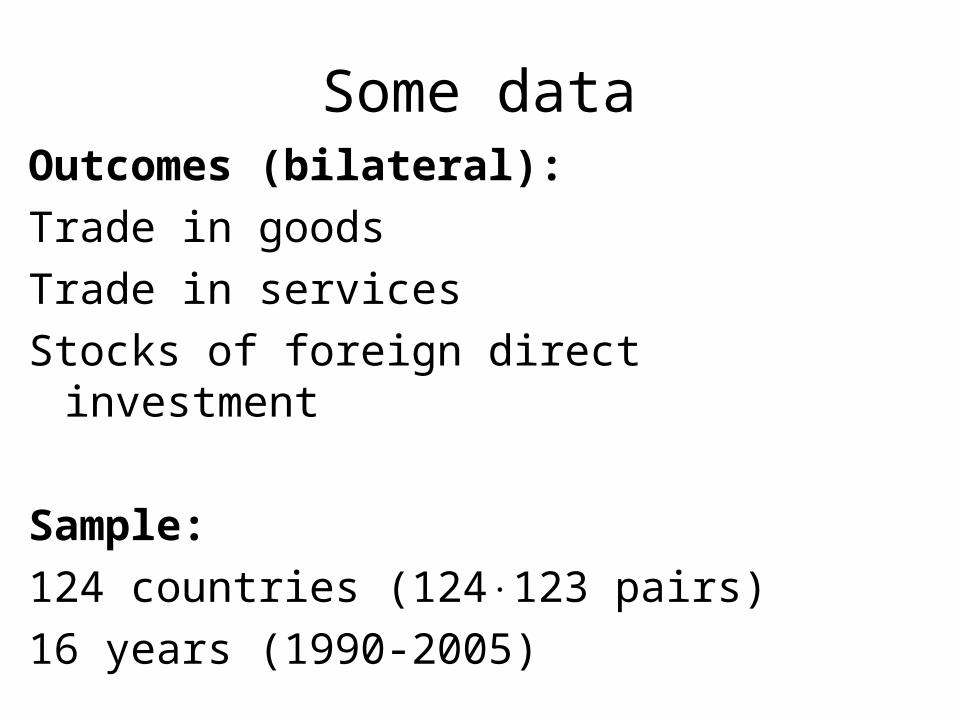

Some dataOutcomes (bilateral):

Trade in goods

Trade in services

Stocks of foreign direct investment

Sample:

124 countries (124123 pairs)

16 years (1990-2005)

Goods Trade Inside and OutsideCountries with/and

GTA STA BIT DTT CUP None else

GTA

STA 4.7598.2

BIT 5.94100

6.22100

DTT 5.6799.4

6.1799.3

5.5798.8

CUP 5.8098.8

7.2098.3

5.72100

6.4299.6

None else

1.2889.0

-.08789.5

4.8196.4

4.1298.2

1.2597.2

-.37771.6

Means: log exports (top) and % of exports>0 (bottom).

Service Trade Inside and OutsideCountries with/and

GTA STA BIT DTT CUP None else

GTA

STA 5.9317.3

BIT 4.3332.0

4.7226.7

DTT 5.7320.9

5.9024.3

4.0923.9

CUP 6.1036.5

6.1049.0

3.4129.4

5.4833.2

None else

3.110.52

00

4.1410.6

4.429.5

2.344.4

2.260.97

Means: log exports (top) and % of exports>0 (bottom).

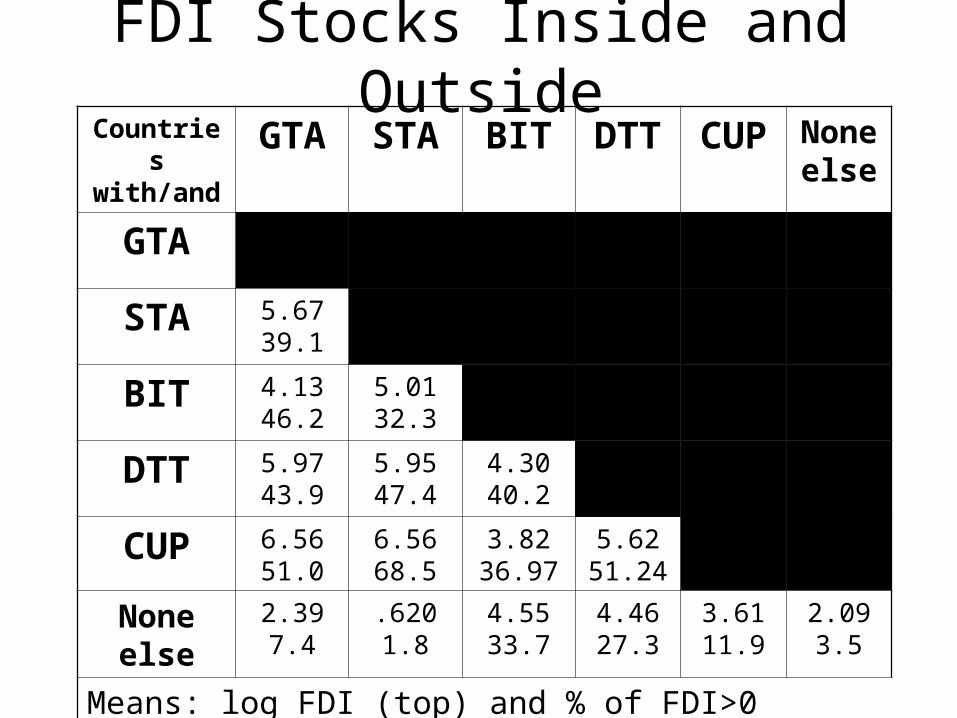

FDI Stocks Inside and OutsideCountries with/and

GTA STA BIT DTT CUP None else

GTA

STA 5.6739.1

BIT 4.1346.2

5.0132.3

DTT 5.9743.9

5.9547.4

4.3040.2

CUP 6.5651.0

6.5668.5

3.8236.97

5.6251.24

None else

2.397.4

.6201.8

4.5533.7

4.4627.3

3.6111.9

2.093.5

Means: log FDI (top) and % of FDI>0 (bottom).

Summary Statistics for OutcomeOutcome Mean Std.Dev. Pairs

Goods trade (US$) .751 4.12 98,899

P(goods trade>0) .779 .415 127,019

Service trade (US$) 4.00 2.34 3,548

P(service trade>0) .083 .169 120,964

FDI stocks (US$) 3.76 3.53 10,538

P(FDI stocks>0) .083 .276 126,859

Values are expressed in logs.

Correlation Coefficients for Outcome

Outcome (binary) (G) (S) (F)

Goods trade (G) 1.00 - -

Service trade (S) 0.14 1.00 -

FDI stocks (F) 0.10 0.16 1.00

Outcome (logs) (G) (S) (F)

Goods trade (G) 1.00 - -

Service trade (S) 0.84 1.00 -

FDI stocks (F) 0.81 0.78 1.00

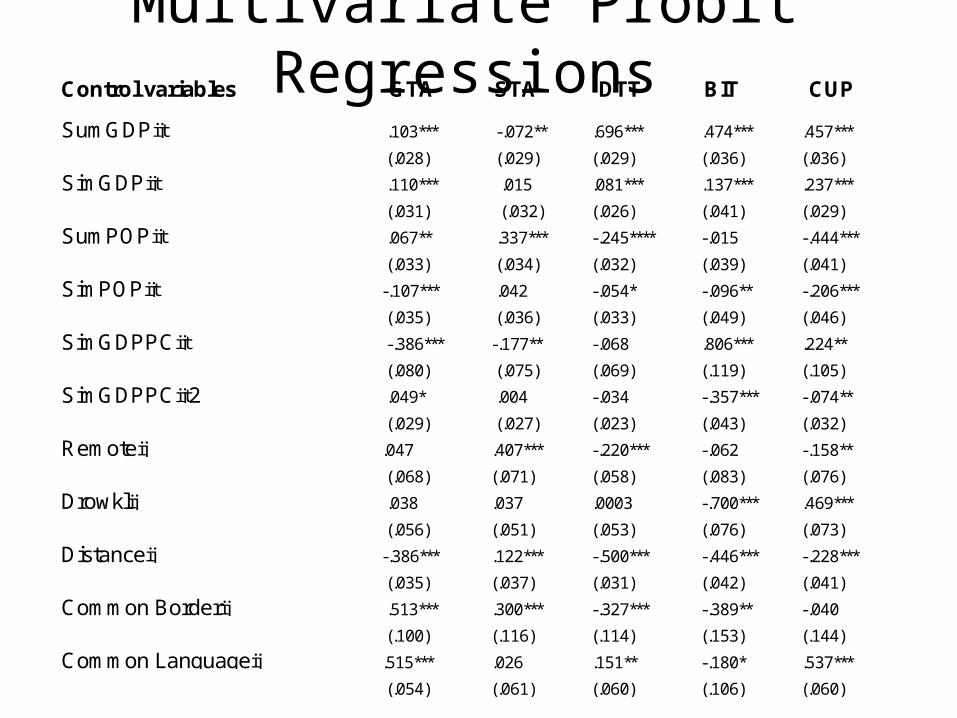

Multivariate Probit RegressionsControl variables GTA STA DTT BIT CUP

SumGDPijt .103*** -.072** .696*** .474*** .457***

(.028) (.029) (.029) (.036) (.036)

SimGDPijt .110*** .015 .081*** .137*** .237***

(.031) (.032) (.026) (.041) (.029)

SumPOPijt .067** .337*** -.245**** -.015 -.444***

(.033) (.034) (.032) (.039) (.041)

SimPOPijt -.107*** .042 -.054* -.096** -.206***

(.035) (.036) (.033) (.049) (.046)

SimGDPPCijt -.386*** -.177** -.068 .806*** .224**

(.080) (.075) (.069) (.119) (.105)

SimGDPPCijt2 .049* .004 -.034 -.357*** -.074**

(.029) (.027) (.023) (.043) (.032)

Remoteij .047 .407*** -.220*** -.062 -.158**

(.068) (.071) (.058) (.083) (.076)

Drowklij .038 .037 .0003 -.700*** .469***

(.056) (.051) (.053) (.076) (.073)

Distanceij -.386*** .122*** -.500*** -.446*** -.228***

(.035) (.037) (.031) (.042) (.041)

Common Borderij .513*** .300*** -.327*** -.389** -.040

(.100) (.116) (.114) (.153) (.144)

Common Languageij .515*** .026 .151** -.180* .537***

(.054) (.061) (.060) (.106) (.060)

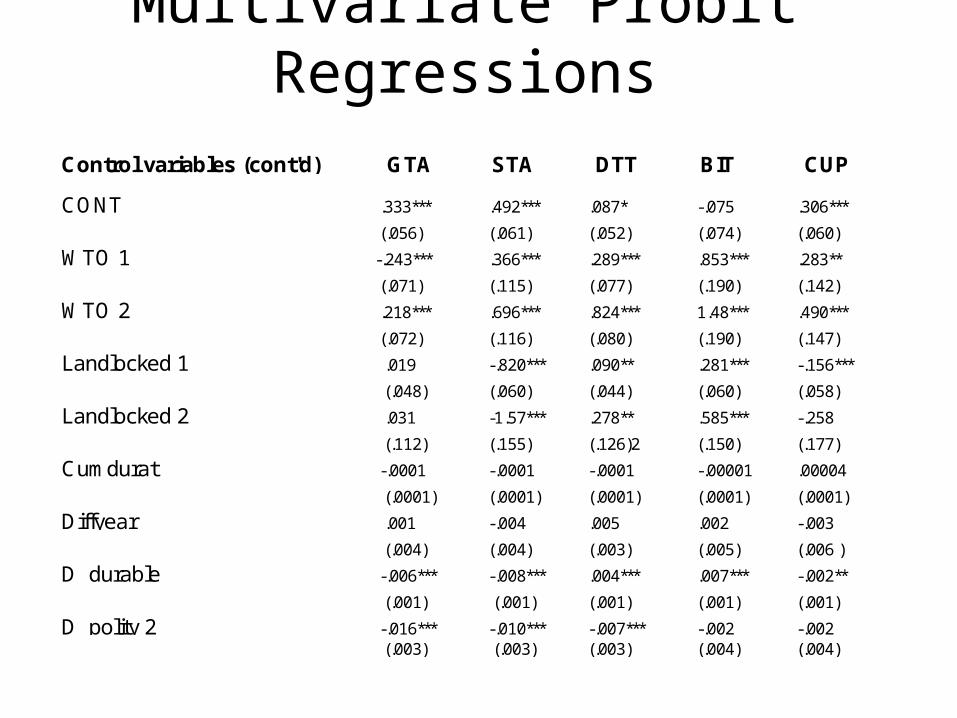

Multivariate Probit Regressions

Control variables (cont'd) GTA STA DTT BIT CUP

CONT .333*** .492*** .087* -.075 .306***

(.056) (.061) (.052) (.074) (.060)

WTO 1 -.243*** .366*** .289*** .853*** .283**

(.071) (.115) (.077) (.190) (.142)

WTO 2 .218*** .696*** .824*** 1.48*** .490***

(.072) (.116) (.080) (.190) (.147)

Landlocked 1 .019 -.820*** .090** .281*** -.156***

(.048) (.060) (.044) (.060) (.058)

Landlocked 2 .031 -1.57*** .278** .585*** -.258

(.112) (.155) (.126)2 (.150) (.177)

Cumdurat -.0001 -.0001 -.0001 -.00001 .00004

(.0001) (.0001) (.0001) (.0001) (.0001)

Diffyear .001 -.004 .005 .002 -.003

(.004) (.004) (.003) (.005) (.006 )

D_durable -.006*** -.008*** .004*** .007*** -.002**

(.001) (.001) (.001) (.001) (.001)

D_polity 2 -.016*** -.010*** -.007*** -.002 -.002 (.003) (.003) (.003) (.004) (.004)

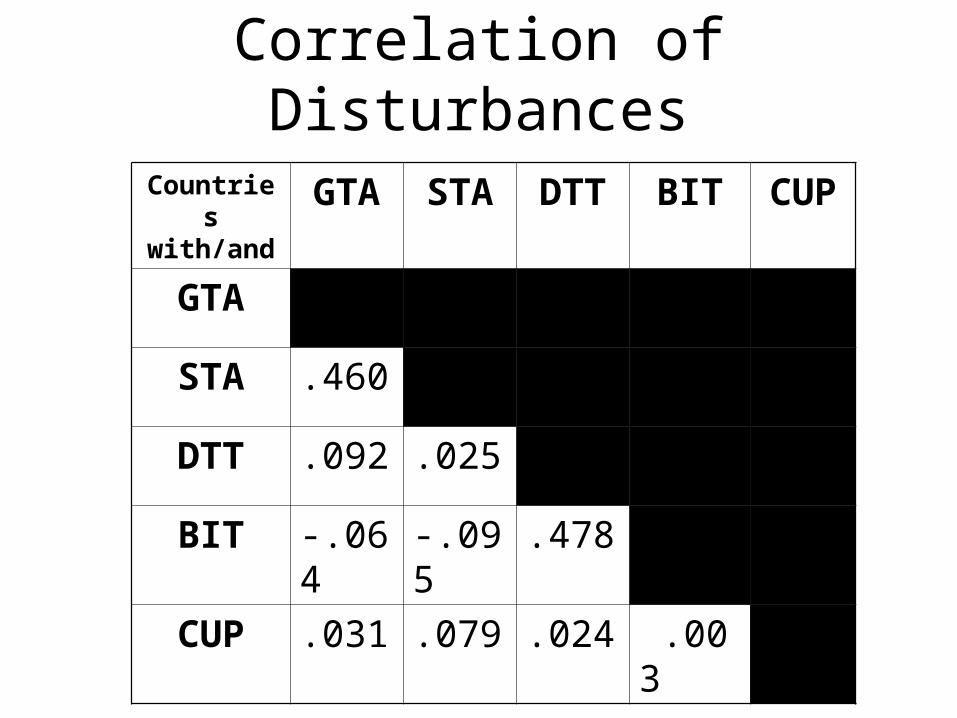

Correlation of Disturbances

Countries with/and

GTA STA DTT BIT CUP

GTA

STA .460

DTT .092 .025

BIT -.064 -.095 .478

CUP .031 .079 .024 .003

Outline of work for the summerEstimation of treatment effects on outcome

by propensity score matching:

For goods trade, services trade, FDI stocks each:

• Propensity of positive outcome (ext. margin)

• Log level (int. margin)

Using propensity score matching for multiple treatments (and estimated propensities from multivariate probit)

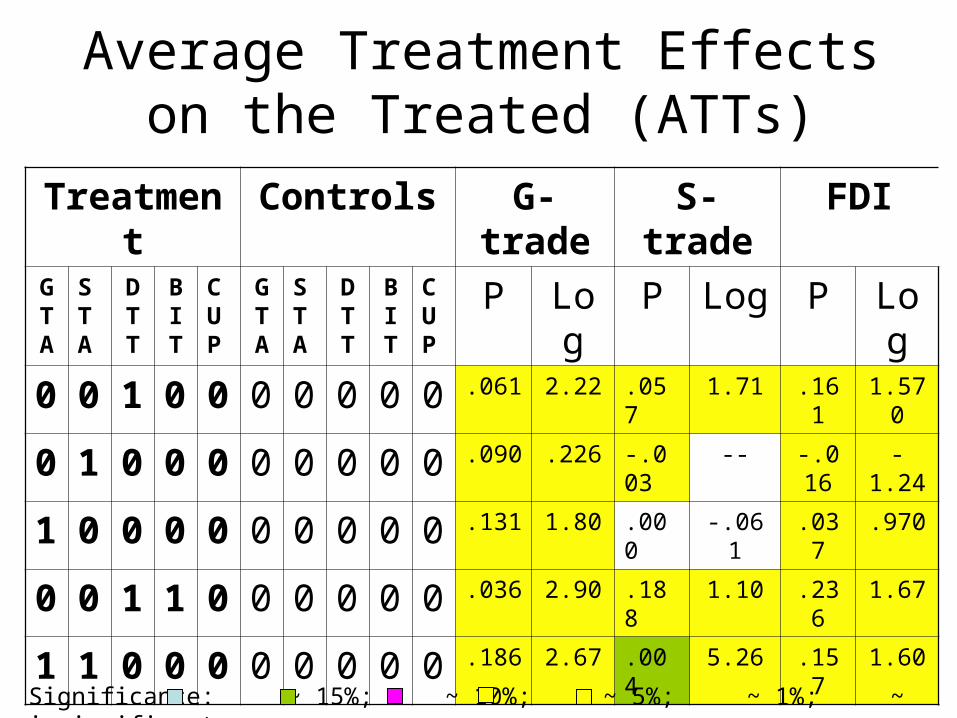

Estimating ATTs

32 EIA combinations (treatments) possible

More than an economist can digest and more than the econometrician can estimate:

Of the 32 ATTs, 10 are based on more than 1,000 units both in the treatment and control group

Next table focuses on the ATTs of the most frequent combinations of “pills taken”

Average Treatment Effects on the Treated (ATTs)

Treatment Controls G-trade S-trade FDI

GTA

STA

DT T

B I T

CUP

GTA

STA

DT T

B I T

CUP

P Log P Log P Log

0 0 1 0 0 0 0 0 0 0 .061 2.22 .057 1.71 .161 1.570

0 1 0 0 0 0 0 0 0 0 .090 .226 -.003 -- -.016 -1.24

1 0 0 0 0 0 0 0 0 0 .131 1.80 .000 -.061 .037 .970

0 0 1 1 0 0 0 0 0 0 .036 2.90 .188 1.10 .236 1.67

1 1 0 0 0 0 0 0 0 0 .186 2.67 .004 5.26 .157 1.60

Significance: ~ 15%; ~ 10%; ~ 5%; ~ 1%; ~ insignificant.

Foregone Trade and FDISuppose every pair would use all modes

corresponds to Average Treatment Effect (ATE) of “11110” relative to “00000”

World effects (for average/randomly drawn pair) of

Margin G-trade S-trade FDI

Extensive .120 .474 .269

Intensive 4.44 1.46 2.53

Conclusions

• Estimated effects pertain to long run

• Short run (conditional on initial state) is also accessible

• In general: standard errors larger for intensive margin than for extensive margin (less observations).

• Int.marg. effects relatively large but– Estimates pertain mainly to DC-with-LDC.– Have large standard errors.

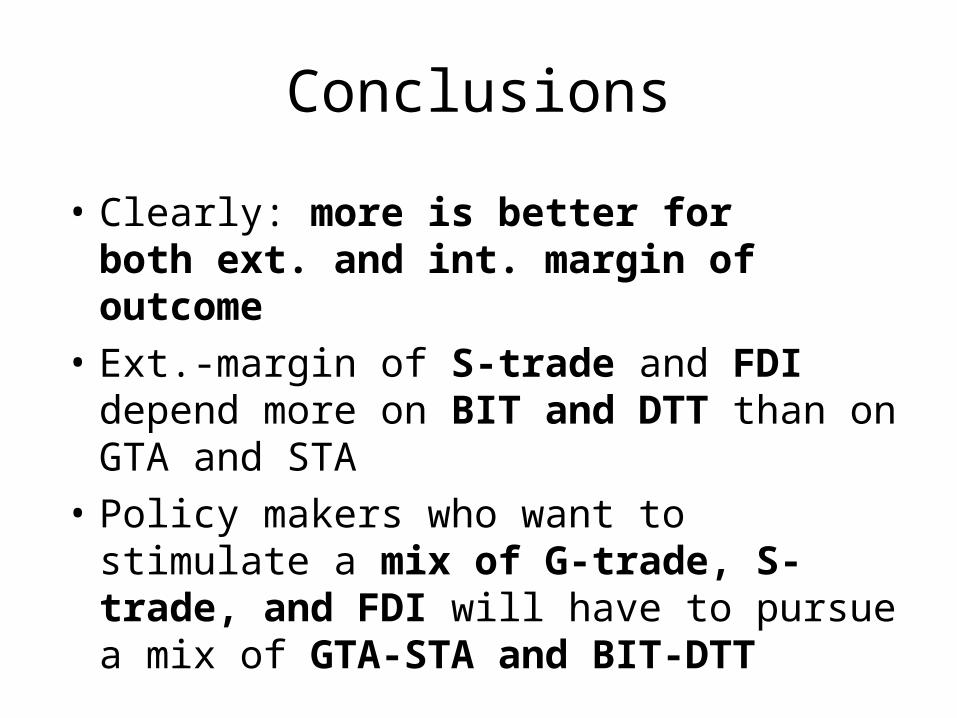

Conclusions

• Clearly: more is better forboth ext. and int. margin of outcome

• Ext.-margin of S-trade and FDI depend more on BIT and DTT than on GTA and STA

• Policy makers who want to stimulate a mix of G-trade, S-trade, and FDI will have to pursue a mix of GTA-STA and BIT-DTT