20

©2009, The McGraw-Hill Companies, All Rights Reserved 3-1 McGraw-Hill/Irwin Chapter Three Interest Rates and Security Valuation

©2009, The McGraw-Hill Companies, All Rights Reserved3-1McGraw-Hill/Irwin

Chapter ThreeInterest Rates

and Security

Valuation

©2009, The McGraw-Hill Companies, All Rights Reserved3-2McGraw-Hill/Irwin

Various Interest Rate Measures

• Coupon rate– periodic cash flow a bond issuer contractually

promises to pay a bond holder• Required rate of return (rrr)

– rates used by individual market participants to calculate fair present values (PV)

• Expected rate of return (Err)– rates participants would earn by buying securities at

current market prices (P)• Realized rate of return (rr)

– rates actually earned on investments

©2009, The McGraw-Hill Companies, All Rights Reserved3-3McGraw-Hill/Irwin

Required Rate of Return

• The fair present value (PV) of a security is determined using the required rate of return (rrr) as the discount rate

CF1 = cash flow in period t (t = 1, …, n)~ = indicates the projected cash flow is uncertainn = number of periods in the investment horizon

nn

rrrFC

rrrFC

rrrFC

rrrFCPV

)1(

~...

)1(

~

)1(

~

)1(

~3

32

21

1

©2009, The McGraw-Hill Companies, All Rights Reserved3-4McGraw-Hill/Irwin

Expected Rate of Return

• The current market price (P) of a security is determined using the expected rate of return (Err) as the discount rate

CF1 = cash flow in period t (t = 1, …, n)~ = indicates the projected cash flow is uncertainn = number of periods in the investment horizon

nn

ErrFC

ErrFC

ErrFC

ErrFCP

)1(

~...

)1(

~

)1(

~

)1(

~3

32

21

1

©2009, The McGraw-Hill Companies, All Rights Reserved3-5McGraw-Hill/Irwin

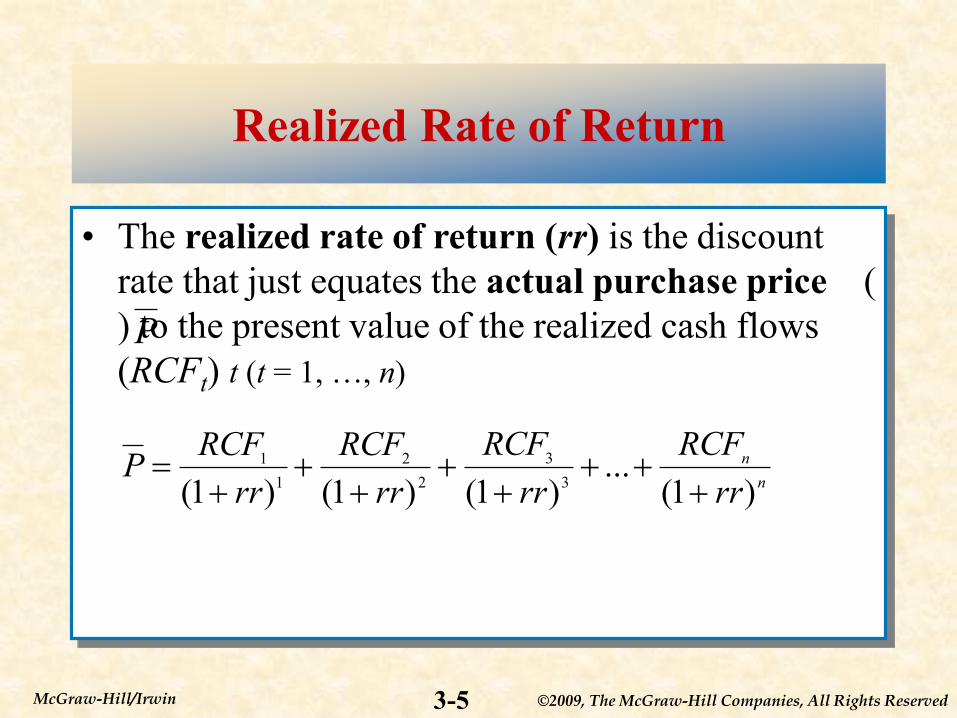

Realized Rate of Return

• The realized rate of return (rr) is the discount rate that just equates the actual purchase price ( ) to the present value of the realized cash flows (RCFt) t (t = 1, …, n)P

nn

rrRCF

rrRCF

rrRCF

rrRCFP

)1(...

)1()1()1( 33

22

11

©2009, The McGraw-Hill Companies, All Rights Reserved3-6McGraw-Hill/Irwin

Bond Valuation

• The present value of a bond (Vb) can be written as:

M = the par value of the bondINT = the annual interest (or coupon) paymentT = the number of years until the bond maturesi = the annual interest rate (often called yield to maturity (ytm))

)()(2

)2/1()2/1(1

2

2,2/2,2/

2

12

TiTi

T

tT

d

t

db

ddPFIVMPVIFAINT

iM

iINTV

©2009, The McGraw-Hill Companies, All Rights Reserved3-7McGraw-Hill/Irwin

Bond Valuation

• A premium bond has a coupon rate (INT)greater then the required rate of return (rrr) and the fair present value of the bond (Vb) is greater than the face value (M)

• Discount bond: if INT < rrr, then Vb < M• Par bond: if INT = rrr, then Vb = M

©2009, The McGraw-Hill Companies, All Rights Reserved3-8McGraw-Hill/Irwin

Equity Valuation

• The present value of a stock (Pt) assuming zero growth in dividends can be written as:

D = dividend paid at end of every yearPt = the stock’s price at the end of year tis = the interest rate used to discount future cash flows

st iDP /

©2009, The McGraw-Hill Companies, All Rights Reserved3-9McGraw-Hill/Irwin

Equity Valuation

• The present value of a stock (Pt) assuming constant growth in dividends can be written as:

D0 = current value of dividendsDt = value of dividends at time t = 1, 2, …, ∞

g = the constant dividend growth rate

giD

gigDP

s

t

s

t

t

10 )1(

©2009, The McGraw-Hill Companies, All Rights Reserved3-10McGraw-Hill/Irwin

Equity Valuation

• The return on a stock with zero dividend growth, if purchased at price P0, can be written as:

• The return on a stock with constant dividend growth, if purchased at price P0, can be written as:

gPDg

PgDis

0

1

0

0 )1(

0/ PDis

©2009, The McGraw-Hill Companies, All Rights Reserved3-11McGraw-Hill/Irwin

Relation between InterestRates and Bond Values

Interest Rate

Bond Value

12%

10%

8%

874.50 1,000 1,152.47

©2009, The McGraw-Hill Companies, All Rights Reserved3-12McGraw-Hill/Irwin

Impact of Maturity onInterest Rate Sensitivity

Absolute Value of Percent Change in aBond’s Price for a

Given Change inInterest Rates

Time to Maturity

©2009, The McGraw-Hill Companies, All Rights Reserved3-13McGraw-Hill/Irwin

Impact of Coupon Rates onInterest Rate Sensitivity

Bond Value

Interest Rate

Low-Coupon Bond

High-Coupon Bond

©2009, The McGraw-Hill Companies, All Rights Reserved3-14McGraw-Hill/Irwin

Duration

• Duration is the weighted-average time to maturity (measured in years) on a financial security

• Duration measures the sensitivity (or elasticity) of a fixed-income security’s price

to small interest rate changes

©2009, The McGraw-Hill Companies, All Rights Reserved3-15McGraw-Hill/Irwin

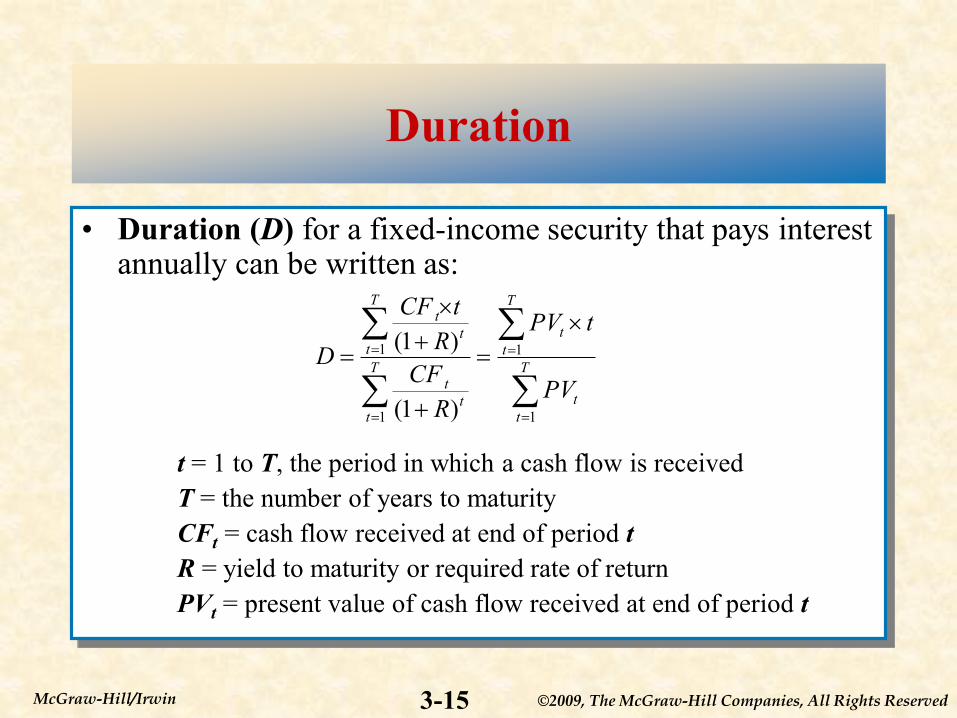

Duration

• Duration (D) for a fixed-income security that pays interest annually can be written as:

t = 1 to T, the period in which a cash flow is receivedT = the number of years to maturityCFt = cash flow received at end of period tR = yield to maturity or required rate of returnPVt = present value of cash flow received at end of period t

T

tt

T

tt

T

tt

t

T

tt

t

PV

tPV

RCF

RtCF

D

1

1

1

1

)1(

)1(

©2009, The McGraw-Hill Companies, All Rights Reserved3-16McGraw-Hill/Irwin

Duration

• Duration (D) (measured in years) for a fixed-income security in general can be written as:

m = the number of times per year interest is paid

T

mtmt

t

T

mtmt

t

mRCF

mRtCF

D

/1

/1

)/1(

)/1(

©2009, The McGraw-Hill Companies, All Rights Reserved3-17McGraw-Hill/Irwin

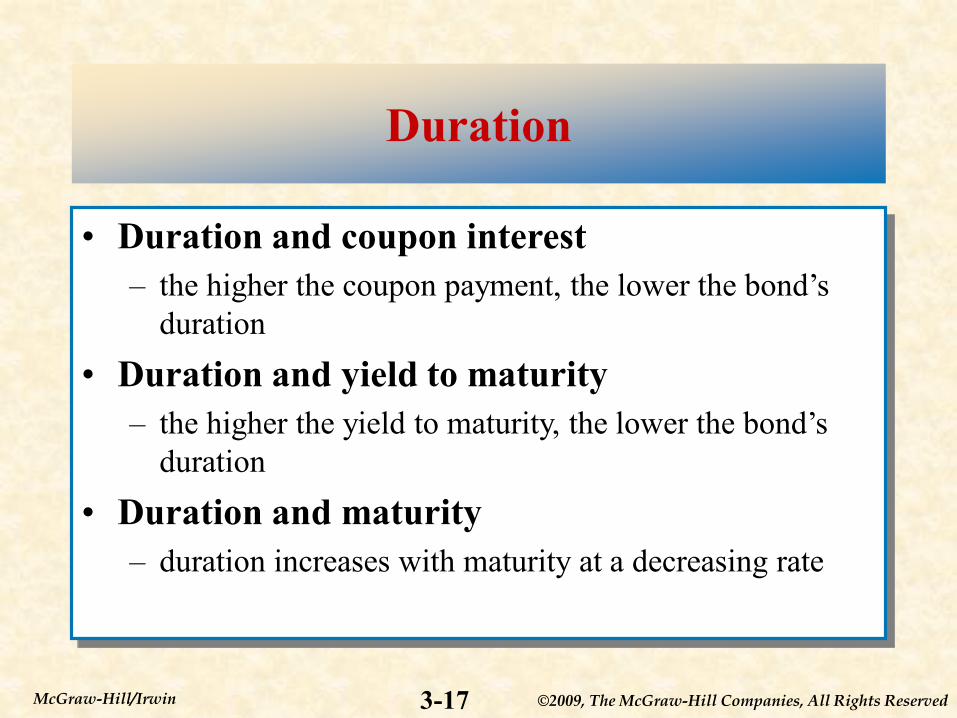

Duration

• Duration and coupon interest– the higher the coupon payment, the lower the bond’s

duration• Duration and yield to maturity

– the higher the yield to maturity, the lower the bond’s

duration• Duration and maturity

– duration increases with maturity at a decreasing rate

©2009, The McGraw-Hill Companies, All Rights Reserved3-18McGraw-Hill/Irwin

Duration and Modified Duration

• Given an interest rate change, the estimated percentage change in a (annual coupon paying) bond’s price is found by rearranging the durationformula:

MD = modified duration = D/(1 + R)

RMDR

RDPP

1

©2009, The McGraw-Hill Companies, All Rights Reserved3-19McGraw-Hill/Irwin

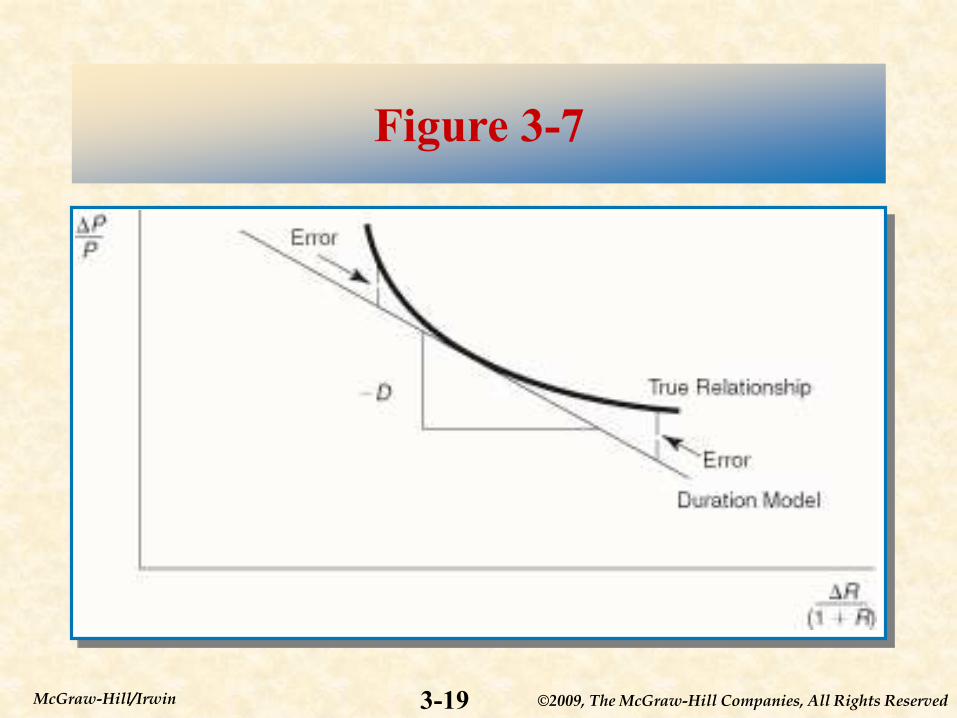

Figure 3-7

©2009, The McGraw-Hill Companies, All Rights Reserved3-20McGraw-Hill/Irwin

Convexity

• Convexity (CX) measures the change in slope of the price-yield curve around interest rate level R

• Convexity incorporates the curvature of the price-yield curve into the estimated percentage price change of a bond given an interest rate change:

22 )(21)(

21

1RCXRMDRCX

RRD

PP

![[PPT]Interest Rates and Bond Valuation - Community …faculty.ccbcmd.edu/~jwhitelo/mngt257/ppt/Chap007.ppt · Web viewTitle Interest Rates and Bond Valuation Author Kent P. Ragan](https://static.documents.pub/doc/80x56/5ae021f97f8b9afd1a8d9432/pptinterest-rates-and-bond-valuation-community-jwhitelomngt257pptchap007pptweb.jpg)