1 l INTERIM REPORT Q1 2020 The interim report has been prepared in accordance with the IAS 34 Interim Financial Reporting and requirements set by the Bank of Estonia for quarterly reporting by credit institutions. LUMINOR BANK AS, Estonia

Transcript

1

l

INTERIM REPORT

Q1 2020 The interim report has been prepared in

accordance with the IAS 34 Interim

Financial Reporting and requirements set

by the Bank of Estonia for quarterly

reporting by credit institutions.

LUMINOR BANK AS, Estonia

Luminor Bank AS Interim report for the period ended 31 March 2020

2

CONTENTS

CEO COMMENT ................................................................................................................................................................................. 3

Luminor Bank AS Interim report for the period ended 31 March 2020

3

CEO COMMENT

The first quarter of 2020 witnessed global events that no one could have predicted before the start of the year. The COVID-19 pandemic made us swiftly readjust the priorities that we had set for the year, with ensuring the safety of our employees and customers becoming our main focus.

Luminor is an important part of the Baltic economy. We continue to offer banking services and financial infrastructure in our home markets even under the emergency situations declared by the Baltic governments, while taking comprehensive measures to assure the safety of our employees and customers. We are helping to mitigate the economic harm caused by the pandemic by offering simplified grace period solutions for both private individuals and corporate customers.

Collaboration is one of Luminor’s core values and we view it as vitally important both in dealing efficiently with the current situation and in preparing to come out of it. Luminor has taken an active role in developing the measures that the Baltic governments have prepared for stimulating the economies and mitigating the impact of COVID-19. We will use state guarantees to provide investment and working capital loans to companies in all three countries and we are also investigating how we can participate in the guarantee programmes offered by the European Investment Fund.

Luminor started the year with a significantly improved funding position and we fully intend to use our strong financial standing for the benefit of our customers. We have introduced a new operating model and made our operations more efficient, so we were stronger and nimbler when the crisis hit, which allowed us to adapt quickly to the changing circumstances. We continued to improve our funding structure in the first quarter of 2020 and we have brought the loan-to-deposit ratio down to 99.7% from 108.4% a year ago. The underlying business performance without extraordinary expenses has improved as well. There was a net loss in the first quarter of 21.2 million EUR that was due mainly to provisions for credit impairments caused by the spread of COVID-19.

On 4 March, Luminor issued the first covered bonds from the Baltic region, for 500 million EUR, with an interest rate spread over mid-swap of 0.25% and a final yield of -0.18%. This set the record for the lowest-ever rate paid by a non-government issuer from the Baltics. The funds received were used to broaden our funding base and to increase our liquidity buffers further.

Remote services have become additionally important for health and safety reasons during the current crisis. We have put more people in our call centres to advise our customers, and we launched remote customer onboarding in Latvia in the first quarter of this year, which made us the first bank in the country to provide this service fully remotely. The service will be extended to Lithuania and Estonia during 2020. Another step in promoting our online business was the launch of the e-Commerce Gateway, an acquiring solution for online merchants in all three Baltic countries.

Luminor is also making good progress in becoming independent from the networks and payment systems of our former parent banks. In the first quarter of this year, we finished setting up independent payment infrastructure on all the core banking systems in the three countries. We are also making strong headway with the carveout on international payment flows processed through the Nordea Group, and we plan to become fully independent on those payments during the first half of 2020. Although current circumstances forced us to revisit our migration schedule at the end of March, the process of moving our customer accounts to the targeted unified systems is progressing, and it should be finalised in Latvia, Lithuania and Estonia in 2020. Luminor Retail Banking increased its presence in the housing loan market by 5% and continued to focus on balanced active sales of lending products and on attracting customer deposits in the first quarter of 2020, but market fluctuations caused by the first impacts of the current pandemic were already being witnessed at the end of March. Corporate Banking focused on measures to help our customers cope with the heavy blow dealt to their business developments by the outbreak of the virus. More than 24 million EUR of provisions for credit losses were set up in Corporate Banking in the first quarter, with 90% of those provisions in response to the expected impact of COVID-19 on the financial standing of our customers and to sharply lower oil prices.

The distress caused in financial markets by the pandemic has also impacted pension assets under management, which fell to 1.3 billion EUR. This is down 11% from the end of 2019 and is at the same level as a year before.

Luminor remains committed to our proactive and vigilant stance in detecting and preventing money laundering and terrorism financing, and in the first quarter of 2020 we continued to enhance our financial crime risk management framework.

Like the rest of the euro area, the Baltics are preparing to take a hit from the economic impact of the health crisis and the ensuing lockdown of economies. It is of the utmost importance that we start focusing on how those economies will recover, with the aid of substantial support from both the EU and national governments. The Baltic banks are well capitalised with stronger balance sheets and can be part of the solution by extending liquidity and keeping the credit flowing to the real economy. Intensive work is being done at Luminor to prepare for how the economic lockdown will impact the economy. We are strengthening the organisational capabilities that will let us support our customers, we are working with different scenarios for how the crisis will evolve and for the economic impact it will have, we are reviewing our costs and financial plans, and we are doing much more besides. More importantly, we are preparing for how we can contribute to restarting the economy.

Luminor Bank AS Interim report for the period ended 31 March 2020

4

I am very grateful to the entire Luminor team, who have responded wonderfully well in dealing with these extraordinary circumstances and ensuring the vital banking services and support that our customers need, while also preparing for how we will exit this crisis. Building tomorrow starts today.

Erkki Raasuke

CEO

Luminor Bank AS Interim report for the period ended 31 March 2020

5

MANAGEMENT REPORT

General information

Luminor Bank AS (Luminor) was established on 1 October 2017 through the merger of the Baltic operations of DNB Bank ASA (Commercial Register no. 984 851 006, DNB) and Nordea Bank Abp (Commercial Register no. 2858394-9, Nordea) to create a new-generation financial service provider for local businesses and financially active people.

On 30 September 2019 it was announced that the transaction signed on 13 September 2018 between DNB, Nordea and US-based private equity firm Blackstone had been concluded and as a result a consortium led by private equity funds managed by Blackstone acquired a 60.1% majority stake in the bank. The bank’s initial owners Nordea and DNB each retained a 19.95% equity stake in Luminor, but an arrangement has been made by the consortium and Nordea for the purchase of Nordea’s remaining stake over the coming years.

Luminor is the third-largest provider of financial services in the Baltics, with some 900 000 clients, 2 501 employees, and market share of 16.0% in deposits and 18.0% in lending as at the end of March 2020. Luminor has total shareholders’ equity of 1.6 billion EUR and it is capitalised with a CET1 ratio of 20.5%. Luminor’s core business is serving entrepreneurial people in the Baltics with a primary focus on local companies and the financially active people.

Luminor offers its customers a wide range of products and services through all possible channels, digital and physical, with 34 customer service centres in total in Latvia, Lithuania and Estonia, of which nine are meet-up points. Luminor owns 357 ATMs throughout the Baltic states, and additionally provides services through 100 ATMs in partnership with other financial services providers.

31 March 2020

Estonia Latvia Lithuania GroupGr Total

Number of customers ~132 000 ~226 000 ~566 000 ~924 000

Market shares

Lending 12.9% 22.9% 19.7% 18.0%

Deposits 8.7% 17.2% 20.9% 16.0%

Number of client service centres, including meet- up points

8 10 16 34

Number of employees 600 875 1 026 2 501

Macroeconomic overview

It is clear by now that the COVID-19 outbreak will have significant economic implications, although it is hard to predict the length and severity of its impact. The consensus outlook for global growth for 2020 is clearly negative, with a recovery coming only in 2021. The impact on the Baltic economies is likely to be concentrated in the second and third quarters of the year, and that impact will be severe, but temporary.

There is, however, a significant degree of uncertainty in how the gradual re-opening of the economies will impact the spreading of the virus. The Baltic states were quick at closing borders and imposing social distancing, and hence currently have fatalities per million inhabitants which are less than 5% of the levels seen in large parts of Europe (e.g. the UK, France, Benelux). Whether this is indicative of a more successful strategy of protecting public health, or whether we are looking at a more prolonged impact from the virus in the Baltics, is too early to say.

The experience of other countries hit by COVID-19 suggests that growth will drop substantially in the Baltic economies in the near term, as both production and consumption is negatively impacted by the measures needed to contain the virus, and from the disruption of global supply chains. Sharp recessions in the Baltic economies, concentrated to the second quarter, are very likely, but should be followed by a gradual recovery from Q3 onwards. Some of the key trading partners for the Baltic states, including Germany and Denmark, have already taken the first steps towards a gradual reopening of their economies. GDP growth in the euro area, the

Luminor Bank AS Interim report for the period ended 31 March 2020

6

key destination for Baltic exports, however decelerated noticeably already in the end of 2019, to only 1% in the fourth quarter compared to a year earlier, being dragged down by lower activity levels in manufacturing and trade.

The economic expansion in the Baltic states has been robust in recent years, with GDP growth outpacing the euro area average by a significant margin. In addition, in stark contrast to the situation going into the Global Financial Crisis, Baltic private as well as public sector debt in relation to GDP is among the lowest in Europe, which may cusion the economic shock from the pandemic. Domestic demand and business activity held up well in the region until the pandemic started, with very tight labour markets supporting high-single digit wage growth and strong retail sales. However, this strong starting points does not entirely insulate the region’s economies from feeling the impact from the pandemic.

The European Central Bank (ECB) has delivered substantial support for the euro area as a whole, and the Baltic countries will benefit on top of this from targeted extraordinary fiscal support measures at both the national and EU levels to mitigate the consequences of the crisis. The impact of these measures is yet uncertain however, as the crisis hits subsegments of the economy very differently and the availability of the fiscal support for those sectors mostly hit. There is no doubt that the loss of activity in the coming quarters will be significant, but it is crucial that the economies can recover swiftly after the spread of the virus has been contained and as the gradual reopening from lockdown proceeds.

COVID-19

After the outbreak of COVID-19, all three Baltic countries declared a state of emergency, and as a result the regular way of living was changed immediately. Different measures were put in place to decrease the speed of infection, and thereby protect public health, and ensure the stability of the health care system. Many of these measures have had severe effects on regular activities in the societies, impacting directly or indirectly businesses and jobs.

Following the footsteps of other countries in the world, Estonian, Latvian, and Lithuanian governments have launched programs to stimulate the economies to mitigate the negative effects from the pandemic.

At large, the state measures put in place can be divided into five major categories, represented in all Baltic countries:

• Employment measures – granting limited sums per person to support the individuals, who have lost all or majority of their

income, and companies, to allow them to keep people employed, in order to survive state of emergency;

• Tax measures – allowing exemptions or suspension or deductions of tax contributions of private individuals and companies

in affected sectors;

• Liquidity measures – deferring tax deadlines, granting loan guarantees and loans to companies;

• Stimulating the economy – accelerating investment programs and public expenditure, reducing capital adequacy

requirements for financial institutions;

• Sector- or company-specific measures – targeted financial support or loans to sectors and companies most heavily impacted

(retail, tourism, large employers), important from national interest or recovery perspective (transportation, aviation, etc).

In Estonia, the state-owned financial institution KredEx is providing capital loans and investment loans, and offers extraordinary loan guarantees in co-operation with banks since the end of March. KredEx targets specific sectors and companies hit by pandemic, as well as projects of national importance, covering amounts up to 5 million EUR per company.

In Latvia, the loan guarantees and liquidity loans are provided by state-owned financial institution ALTUM, directly and in cooperation with commercial banks. Latvia has also introduced number of measures to support retail companies to survive the crisis. There are different tax related measures implemented in Latvia, including repayment of overpaid VAT.

Lithuania has introduced a 5 billion EUR “Economic and Financial Action Plan” to support the economy, maintain business liquidity, jobs, and healthcare. As an example, small fixed payouts are distributed to self-employed people affected by the state of emergency. Lithuania is also injecting 1 billion EUR into the economy by accelerating investment programs, and has introduced a number of tax and consumption-oriented measures.

In addition, there are number of measures targeted at banks - banks can operate temporarily below the level of capital defined by the Pillar 2 Guidance, the capital conservation buffer and the liquidity coverage ratio requirements, or use capital instruments that do not qualify as Common Equity Tier 1 instruments. In addition, the countercyclical capital buffer and/or systemic risk buffer requirements have been reduced. The ECB has eased conditions for targeted longer-term refinancing operations (TLTRO III) and added some funding possibilities for banks (including the Pandemic Emergency Funding Facility).

Luminor Bank AS Interim report for the period ended 31 March 2020

7

Being an important part of the Baltic economies, in order to support our customers in this difficult time and offer best financial advice, Luminor has kept its customer service centers open, though strict measures have been adopted to protect our employees and customers – we are more frequently cleaning the facilities and ATM’s, we have put in place mandatory facemasks and safety screens for employees, and we also are limiting the number of simultaneous customer visits to service centers. To prevent the spread of virus, over 70% of our employees are working remotely.

To help our customers withstand the crisis, Luminor offers simplified grace period solutions both to private individuals and corporate customers in all three Baltic countries. This means that bank is not asking any additional documents from the customer, not changing the loan agreement conditions and not taking any fee.

We also aim to help distribute the state guaranteed loans, and utilize other potential programs to ensure the availability of investment and working capital loans for companies in all three countries.

Business development

Luminor completed its cross-border merger on 2 January 2019 and continues its operations in all the three Baltic countries through the bank headquartered in Estonia and its branches in Latvia and Lithuania. After the completion of the merger, all assets, rights and liabilities of Luminor Bank AS (Latvia) and Luminor Bank AB (Lithuania) were transferred to Luminor Bank AS in Estonia. The bank continues its activities in Latvia and Lithuania through its locally established branches. A new organisational set up and a new governance structure were also introduced, and new members of management bodies were appointed.

The deposits and financial instruments of the depositors and customers using the investment services of Luminor Bank AS and its Latvian branch and Lithuanian branch are guaranteed by the deposit guarantee and investor protection scheme established and operated by the Estonian Guarantee Fund.

The process of setting up independent payment infrastructure for all the core banking systems in the three countries was completed in February 2020. Luminor established its own correspondent banks network in 2019 and gained independence in international payments from the correspondent banking accounts of DNB. It is now making good headway with the international payment flows processed through the Nordea Group, planning to become independent on payments during the first half of 2020.

The gradual migration of the legacy Nordea customers in Latvia to the Luminor information systems continued in the beginning of 2020. The process of finalising the systems and migrating the customers to the targeted unified systems is progressing, with the aim to finalize the migration in all countries during 2020. Even with the ongoing pandemic, this remains one of Luminor’s top priorities for the year.

PRODUCT AND DIGITAL DEVELOPMENT

In the first quarter of 2020 Luminor continued strengthening its Daily Banking offering with the launch of several new services. Remote customer onboarding was launched in Latvia, making Luminor the first bank in the country to provide the service fully remotely. Luminor aims to extent this service to Lithuania and Estonia during the year.

Luminor also launched the e-Commerce Gateway, an acquiring solution for online merchants, in all three Baltic states. The e-Commerce Gateway provides card acquiring services for accepting VISA and Mastercard cards, and uses the Open Banking application programming interfaces (APIs) of major banks to enable account-to-account payments to be acquired.

Luminor also launched its Black Card in Latvia. This credit card is an excellent value proposition for domestic and overseas use and the aim is for it to become the target credit card for Luminor customers in all three countries.

The Luminor Investor platform was launched in Estonia in February 2020, following its launch in Latvia and Lithuania in October 2019. The investment platform is tailored for investors of all levels of experience and offers a wide range of non-complex financial instruments, with more than 14 500 instruments in total. The platform was built jointly with Scandinavian partners and gives a simplified customer experience that lets customers build their savings at their own pace.

THE RETAIL BANKING SEGMENT

The focus of the Retail Banking team remained on achieving balanced sales of our lending products and attracting customer deposits, and it increased the bank’s presence in the housing loan market by 5%, mainly through the Latvian and Lithuanian markets. The market share for newly issued consumer loans has increased by some 3% in Latvia and Lithuania, while it declined by 0.4% in the Estonian market. Lending volumes for the mass business customers have remained stable and at the same level as in the first quarter of 2019. The portfolio of deposits of private clients has grown by 4.5% from the same quarter of 2019. By the end of March the Retail

Luminor Bank AS Interim report for the period ended 31 March 2020

8

Banking team was already seeing the first impact of the COVID-19 outbreak as market fluctuations squeezed the assets under management of retail customers by 153 million EUR.

The e-Commerce Gateway was launched for mass business customers at the end of the first quarter and within the first two weeks of launch it had received 52 applications and converted 13 of them into agreements.

The Retail Banking team continued to focus on its migration work during the quarter and the first mass business clients were successfully migrated from the legacy Nordea systems to the targeted Luminor unified information systems. The team continued to consolidate the distribution channels and improve efficiency in related areas. Two service centres were relaunched with a new concept in the first quarter of 2020 and Luminor was serving its customers in a total of 34 locations across the Baltics.

THE CORPORATE BANKING SEGMENT

The top priority for the Corporate Banking team in the first quarter of 2020 was to take measures to help corporate customers cope with the impact of COVID-19 on their business. More than 24 million EUR of provisions for credit losses were set up in corporate banking in the first quarter of 2020, and 90% of those provisions were in response to the expected impact of COVID-19 on the financial standing of clients and to sharply lower oil prices.

The lending portfolio decreased by 19% compared to the last year as a result of the repricing and optimisation of the portfolio and slower new sales, partly due to COVID-19. The deposits of corporate customers remained at the same level as in the first quarter of 2019, as the Corporate Banking team has been putting more emphasis on improving the quality of deposits by replacing large concentrated accounts with more diversified SMEs.

Trading income showed solid results as higher market volatility brought along increased customer activity in the risk hedging transactions.

THE WEALTH MANAGEMENT SEGMENT

Wealth Management introduced several new solutions for our customers in the first quarter.

The Luminor Investor platform was rolled out in full in all three Baltic states and was promoted to customers interested in financial investments, also the new VISA Infinite card for the Private Banking segment was introduced for Latvian and Lithuanian customers.

Business growth and customer satisfaction remained firmly in the focus of the Private Banking and Pensions teams.

The distress caused in financial markets by COVID-19 reduced the pension assets managed to 1.3 billion EUR, which was roughly the same as a year earlier and 11% down from the end of 2019.

By the end of the first quarter Luminor had 291 000 second pillar pension customers and 63 000 third pillar customers.

The Private Banking team focused on growing the assets under management and reached 1.37 billion EUR in the first quarter of 2020, which was 7% more than in the same quarter of 2019 and 3.6% less than at the end of 2019.

The focus remains on achieving a high level of customer satisfaction by being available for our customers, and on ensuring operational communication in the face of the elevated volatility in financial markets.

CORPORATE SOCIAL RESPONSIBILITY

The safety and well-being of Luminor employees and customers has been and remains our top priority in all our activities. We at Luminor are keeping our customer service centers open and continuing to offer banking services to our customers even under the current difficult circumstances, but we have taken comprehensive measures to assure the safety of our employees and our customers. These measures include the maximum possible use of remote work, extra attention to cleaning and the availability of disinfectants in all our facilities and ATM’s, the provision of protective equipment for all our employees, and limits on the number of customer visits to the customer service centers at any one time.

Remote services have become especially crucial in the current pandemic, and Luminor has encouraged customers to use digital services to the greatest extent possible. Working together with our partners, Luminor initiated a community investment project in the first quarter of 2020 that aims to help local companies take their business online or advance their current e-business capabilities. We are also currently offering our payment solution e- Commerce Gateway for free so that we can help promote safer e-business.

Luminor Bank AS Interim report for the period ended 31 March 2020

9

The rapidly changing environment, the large number of unknowns, and the new ways of working can all cause considerable stress. For that reason, we are paying special attention to communication and consultation with our employees so that we can aid them in adapting to the new circumstances and let them focus on their work and life balance. Separate webinars to share the knowledge we have gained have been delivered for Luminor customers, covering topics like remote working and cyber security during the current crisis.

In our concern for environmental sustainability, Luminor developed risk-adjusted environmental and social risk evaluation procedures in the first quarter of 2020 to be applied to all legal entities. The procedure requires E&S evaluation for every new customers and during every annual review of existing customers with a limit extending EUR 0.5 million. To support this, we ran training courses for the employees most connected to the topic.

Efficient governance is of great importance to us and so we reviewed and updated Luminor’s governance policies and procedures. An audit was carried out in this that recommended further improvements to the Management Board.

EFFORTS TO PREVENT FINANCIAL CRIME

Luminor remains vigilant and committed to detecting and preventing financial crime, and we regularly review our anti-financial crime (AFC) practices and invest in the human and technological resources that are needed. We work constantly to get a better understanding of our customers and their transactions, and to manage and report any potential financial crime risk. Luminor predominantly serves residents of Estonia, Latvia and Lithuania, and customers who have a strong personal or business connection to the Baltic states.

During the first quarter of 2020, Luminor has further enhanced its financial crime risk management framework to prevent, detect, manage and report potential financial crime risk, and this has supported its conservative approach towards money laundering and financial crime. The framework covers technology, policies and procedures for detecting financial crime, risk assessments, training and awareness-raising, and ongoing monitoring of new and developing financial crime risks. As we are subject to a wide range of legal requirements, Luminor is transparent in all its activities and works closely with all the supervisory and regulatory authorities. Luminor also follows the international guidelines, recommendations and standards issued by the regulatory and supervisory authorities, international bodies and local banking associations, and the financial intelligence units in each Baltic state.

Luminor continued to invest in its systems and processes so it can adapt in a constantly changing environment. The bank is further developing its common monitoring and screening solution in all three Baltic states and has envisaged several further developments that are to be delivered during 2020.

Luminor considers that awareness-raising activities are an important component of the financial crime risk management framework. During the first quarter, 31 training events related to AFC and corporate compliance areas were held on 10 different topics.

OTHER EVENTS

On January 27 Auri Loog joined Luminor as the Head of Internal Audit Division. She is a Certified Internal Auditor with a solid experience in banking and auditing sectors. The former Head of Internal Audit Jelena Gute went on to lead Luminor’s Group Finance Department.

EVENTS AFTER 31 MARCH 2020

In order to be prepared for dealing efficiently and expertly with the additional workload potentially caused by the economic impact of COVID-19 and support our customers also in the most difficult cases, a Credit Advisory and Restructuring division has been established as of 1 May 2020. It is a temporary dedicated unit with a planned duration of 18 months with a possible 6-month extension period, supporting the current teams working in this field. The Head of the new division is Solvita Deglava. She has strong experience in the restructuring area, having worked in that capacity in different banks.

Luminor Bank AS Interim report for the period ended 31 March 2020

10

Financial results

Net loss in the first quarter amounted to 21.2 million EUR and was mainly driven by loan loss provisions as a result of the COVID-19 pandemic. Loan loss provisions amounted to 26.4 million EUR compared to 7.3 million EUR net reversals in same period last year, resulting in a 1.05% loan loss ratio.

Net interest income in the first quarter was 54.1 million EUR compared to 63.8 million EUR a year ago and was impacted by continued repricing and rightsizing of the balance sheet. Interest income declined by 3% while the loan portfolio decreased by 12% as a result of planned effort to ensure fair pricing of risk and improve profitability. Interest expense increased by 54% or 5.8 million EUR as a result of the process to become an independently funded bank and continuous work with funding diversification. Consequently, net interest income-to-loans ratio in the first quarter was 2.2% compared to 2.3% in the same period last year. Net commission income decreased by 5% compared to same quarter last year, with one of the key drivers being early signs of lower customer activity due to COVID-19 pandemic.

Total operating expenses in the first quarter were 71.4 million EUR and have decreased by 1% compared to the same period last year. Exceptional costs have increased from 17.2 million EUR in the first quarter last year to 25.3 million EUR this year. In the first quarter this year the largest part were IT expenses, which constituted 89% and other costs were 11% of total exceptional expenses. Total operating expenses excluding exceptional costs have decreased by 16% compared to the same period last year. The underlying business performance has improved, which is also reflected in cost-to-income ratio without exceptional costs of 57.5% compared to 59.7% in the first quarter last year.

The funding structure continued to improve as a loan-to-deposit ratio reached 99.7% compared to 108.4% a year ago. It was supported by 567 million EUR increase in deposits and 1.4 billion EUR decline in lending portfolio.

* Quarterly ratios (ROE, ROA, NIM, C/I, Credit impairment ratio) are expressed on an annualised basis

** If loan recoveries prevail, the ratio is negative

Luminor Bank AS Interim report for the period ended 31 March 2020

11

Explanations

Average equity (belonging to the owners of the company) = (equity at the end of the reporting period + equity at the end of the previous period) / 2

Return on equity (ROE) = Net profit / Average equity * 100

Average assets = (assets at the end of the reporting period + assets at the end of the previous period) / 2

Return on assets (ROA) = Net profit / Average assets * 100

Average interest earning assets = (interest-earning assets at the end of the reporting period + interest-earning assets at the end of the previous period) / 2

Net interest margin (NIM) = Net interest income / Average interest earning assets * 100

Cost / Income ratio = Total operating expenses / Net total operating income * 100

Credit impairment ratio = Net losses or reversal on loans to customers / Net loans, average * 100

Loans / Deposits ratio = Loans to customers / Deposits from customers * 100

CET 1 ratio = Common Equity Tier 1 Capital / Risk-weighted Assets

Loans to customers at the end of the first quarter totalled 9.9 billion EUR, having been 10.2 billion EUR in December 2019. The composition has slightly changed during last 12 months as the share of loans to business customers has decreased from 46% to 43% while loans to individual customers have increased from 52% to 56% at the Baltic level. Luminor’s share of the lending market in the Baltics has decreased from 20.9% to 18.0% over the past 12 months.

Deposits from customers at the end of the first quarter totalled 10.0 billion EUR, having been 10.2 billion EUR in December 2019. The composition has been stable, with deposits from individual customers comprising 40% of the deposit portfolio of Luminor at the Baltic level, followed by 39% from business customers and 17% from public sector. Luminor’s share of the deposit market in the Baltics has decreased from 16.9% to 16.0% over the past 12 months.

Luminor Bank AS Interim report for the period ended 31 March 2020

12

ASSET QUALITY FOR Q1 2020

The adverse impact of COVID-19 is reflected in asset quality of Luminor.

The most severe consequences will most probably be seen in industries like accommodation, tourism, and aviation. Even though Luminor’s portfolio towards these economic sectors is relatively small, negative trends in the portfolio are still observed since many other industries are quite severely affected as well. As a result, requests for modifications (including grace period) reached 0.9 billion EUR at the end of March 2020 and exceeded 1.1 billion EUR (11% of the total credit portfolio) by the middle of April 2020.

Considering the situation, and the generous terms for modifications, the number of modifications has been limited so far.

Approximately 70% of modification requests came from business customers. Earlier applications for modification from business customers compared to individual customers can be explained by the following reasons:

• business customers have been affected first; moreover, professional financial management leads business customers to

immediately approach the bank, if foreseeing the need for modifications;

• individual customers often have unemployment benefits.

The largest part of modification requests from business customers are for industries like real estate activities, transportation and storage, wholesale and retail trade, manufacturing.

The most common modification type is grace period on principal payments. Luminor is restrictive (applying only exceptionally) towards granting full grace period (including grace on interest payments).

The volume of overdue loans is fluctuating and not yet showing negative trends, however, depending on the development of the pandemic and measures taken by governments, this might accelerate in the second quarter of 2020.

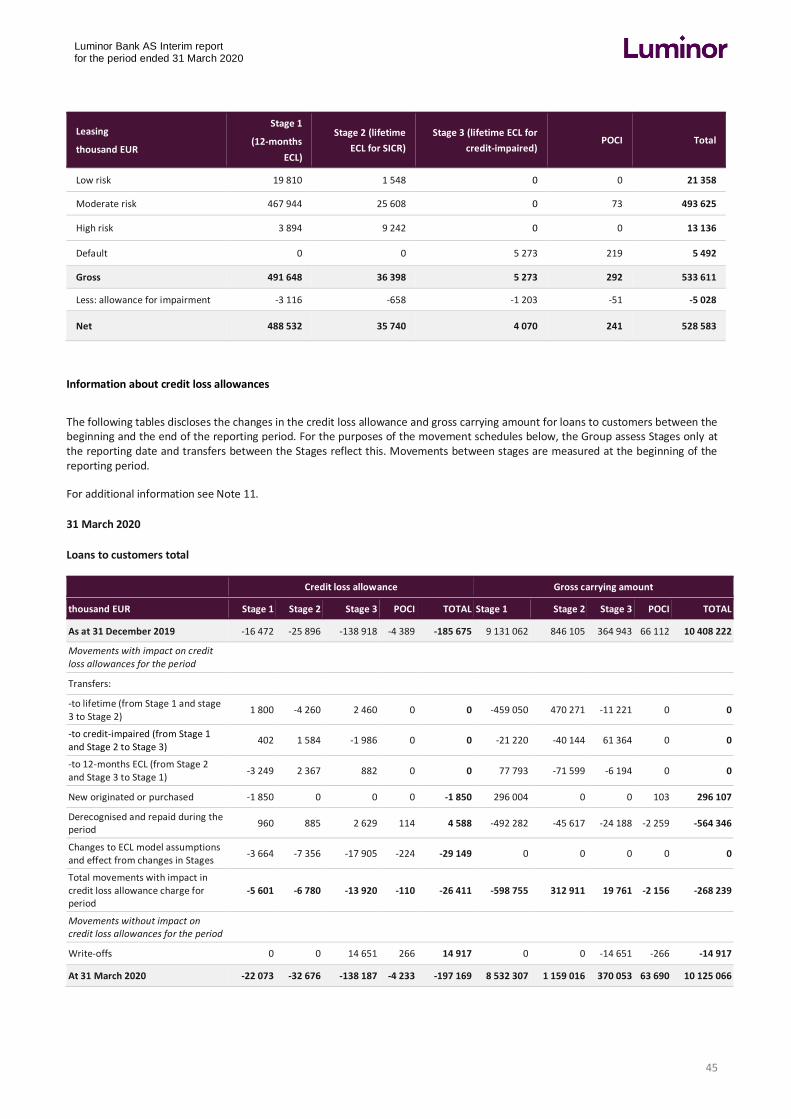

During the first quarter, Luminor loan loss provisions reached 26.4 million EUR. Approximately 50% of the provisions was for Stage 3 while the rest was for Stage 1 and 2 exposures. Stage 1 and 2 provisions increased mainly due to changes in the macroeconomic outlook in the models, and an increase of watch list customers. 60% of Stage 3 provisions in the period related to new non-performing loans (NPLs). In addition, 30% represented additional provisions on existing NPLs relating to the energy sector.

The share of non-performing loans (NPL ratio) was 3.9% at the end of the quarter, which is an increase of 0.1 percentage points from the previous quarter. The NPL ratio for the mortgage loans portfolio was unchanged at 2.9%.

Total impairment allowances on the balance sheet were 197.2 million EUR at the end of the quarter, of which 142.2 million EUR related to Stage 3 exposures. This can be compared with total non-performing loans of 393.5 million EUR.

Luminor Bank AS Interim report for the period ended 31 March 2020

13

Asset quality of Luminor as at 31 March 2020

31 March 2020

thousand EUR* Total Estonia Latvia Lithuania

Financial institutions

Stage 1

Gross carrying amount 8 720 6 688 1 148 884

Impairment allowances -38 -29 -4 -5

Carrying amount 8 682 6 659 1 144 879

Stage 2

Gross carrying amount 5 210 2 860 2 306 44

Impairment allowances -100 -72 -27 -1

Carrying amount 5 110 2 788 2 279 43

Stage 3

Gross carrying amount 104 98 6 0

Impairment allowances -2 -1 -1 0

Carrying amount 102 97 5 0

Total carrying amount for financial institutions 13 894 9 544 3 428 922

Public sector

Stage 1

Gross carrying amount 155 914 67 233 8 702 79 979

Impairment allowances -28 -18 0 -10

Carrying amount 155 886 67 215 8 702 79 969

Stage 2

Gross carrying amount 43 2 0 41

Impairment allowances 0 0 0 0

Carrying amount 43 2 0 41

Stage 3

Gross carrying amount 378 0 0 378

Impairment allowances 0 0 0 0

Carrying amount 378 0 0 378

Total carrying amount for the public sector 156 307 67 217 8 702 80 388

Impairment ratio % = Total Allowances / Total Gross Loans

The credit quality of loans as at 31 March 2020 is disclosed in the table below using the risk scale set in the Luminor Credit Manual: the probability of default for low-risk rating grades (1 to 4) is in the range of 0.00% to 0.75%, for moderate-risk rating grades (5 to 7) it ranges from 0.75% to 3.00%, and for high-risk rating grades (from 8 to 10) it is from 3.00% to 40.00%.

Luminor Bank AS Interim report for the period ended 31 March 2020

16

Economic sectors

The following table breaks down the loans and advances to customers at their carrying amounts, as categorised by the economic sectors of our counterparties.

*Private individuals do not include non-profit organisations and self-employed individuals.

Information about credit-impaired loans and collaterals

The amount of credit-impaired loans is reported together with the value of related collateral held as security in the tables below. Credit-impaired loans are most often secured by real estate and movable assets. The value for such collateral is equal to its market value and not its liquidation value, and this is updated shortly after the default has been identified.

31 March 2020

thousand EUR Gross

Allowance for

impairment Net Fair value of collateral

Business customers 227 752 -96 735 131 017 160 272

One of the main objectives for Luminor is to create a self-sustaining combined banking group. A key requirement for achieving this is that the former parent funding provided in equal parts by DNB and Nordea should gradually be replaced by other forms of funding such as deposits and wholesale funding from third parties.

Luminor has achieved tangible results in getting closer to being a self-funded banking group. Deposits from customers stood at 9 959 million EUR at the end of the first quarter of 2020, and at 10 235 million EUR on 31 December 2019. In March 2020 Luminor issued its inaugural five-year covered bond for 500 million EUR, which received a long-term rating of Aa1 from Moody’s. The covered bond issuance raised the value of bonds outstanding under the EMTN programme to 1 156 million EUR at the end of the first quarter of 2020 from 652 million EUR at 31 December 2019. The senior unsecured bonds issued under the EMTN programme have been assigned a rating of Baa2 by Moody’s.

In addition to its deposits from customers and wholesale funding, Luminor has outstanding debt facility lines with its former parent companies DNB and Nordea. This funding amounted to 150 million EUR at the end of the first quarter of 2020 and was provided in the form of a syndicate, with each syndicate partner providing 50%. The covered bond issuance meant the total amount committed to the facility under the agreement, used and unused combined, was reduced to 2 337 million EUR as at 31 March 2020 from 2 837 million EUR as at 31 December 2019. The amount of the facility is committed for five years from 1 October 2019, initially three years

Luminor Bank AS Interim report for the period ended 31 March 2020

17

with the option for Luminor to extend it by up to two years, and it can be drawn with maturities of one, two or three years. The facility is partly secured, as Luminor has assigned mortgage loans to it with a carrying value of 1 762 million EUR as at 31 March 2020 and 1 929 million EUR as at 31 December 2019. The total committed but unused credit line was 2 187 million EUR as at the end of the first quarter of 2020 and 1 932 million EUR as at 31 December 2019.

On 2 April 2020 Luminor received its minimum own funds and eligible liabilities (MREL) requirement as a decision of the Single Resolution Board (SRB) dated 20 December 2019 that was executed for Luminor by the decision of Finantsinspektsioon, the Estonian FSA, dated 1 April 2020. The MREL decision sets the following MREL requirements for Luminor:

• Luminor Holding AS (parent company of Luminor Bank AS) shall comply with the MREL at the consolidated level of Luminor Bank AS, on a consolidated level of 17.28% of total liabilities and own funds at all times, and 11.97% of total liabilities and own funds shall be met with subordinated instruments;

• Luminor Holding AS shall have a transitional period until 30 June 2022 to comply with these requirements.

As at 31 March 2020 the total MREL ratio stands at 17.0% on the consolidated level of Luminor Bank AS (16.3% as at 31 December 2019) and 12.1% of total liabilities and own funds were subordinated instruments (11.5% as at 31 December 2019) . It should be noted that the MREL requirements have been set using data from 31 March 2019. This means the decision does not consider any subsequent events.

Rating

On 13 September 2018 Moody’s assigned Luminor long and short-term, foreign and local currency deposit ratings of Baa1/Prime-2, with a stable outlook. There have been no changes to Luminor’s ratings since then. On 25 March 2020 Moody’s issued an updated credit opinion for Luminor.

On 11 March 2020 Moody’s assigned a definitive Aa1 rating to the mortgage covered bonds issued by Luminor Bank AS under the Estonian Covered Bonds Act.

LIQUIDITY

Luminor’s structural liquidity risk is conservative and well-balanced, and based on metrics to measure liquidity risk, is appropriately adopted to the current economic and regulatory environment. Luminor uses a range of metrics to measure liquidity risk. One metric used is the Liquidity Coverage Ratio (LCR). The LCR for Luminor was 144% as at the end of the first quarter and 150% as at 31 December 2019 by the definition of the LCR in the Capital Requirements Regulation (CRR). The liquidity buffer is composed of highly liquid central bank eligible securities and cash. Long-term liquidity risk is measured as the Net Stable Funding Ratio (NSFR). As at the end of the first quarter of 2020, Luminor’s NSFR was 126%, while as at 31 December 2019 it was 123%.

372

4 2713 950

1738

150

11561610

All other Liabilities Corporate

deposits

Retail deposits Public sector

deposits

Parent Funding Debt securit ies

issued

Equity

Luminor Bank AS Interim report for the period ended 31 March 2020

18

Q1 2020 Q4 2019 Q3 2019 Q2 2019 Q1 2019

LCR 143.7% 149.8% 144.3% 132.5% 131.2%

NSFR 126.0% 123.0% 118.0% 127.4% 122.0%

Deposit structure

Deposits from customers are predominantly from residents of the Baltics. In total, 99.2% of all deposits in terms of volume are from EU residents.

Deposits by residency per country:

Total Estonia Latvia Lithuania

CAPITAL

The capitalisation of Luminor is sufficient to ensure financial stability and provide the capital needed to deliver the business strategy. As at 31 March 2020 the total consolidated Capital Ratio of Luminor Bank AS was 20.5% and as at 31 December 2019 it was 19.7%, making it comfortably above the internal target of 17%. As at 31 March 2020 the own funds of Luminor were 1 598 million EUR and as at 31 December 2019 they were 1 572 million EUR, and they were fully composed of Common Equity Tier 1 (CET1) capital.

In its Capital Adequacy calculations Luminor uses the standardised method to calculate risk weighted exposure amounts for credit risk and market risk. Risk weighted exposure amounts for operational risk are calculated using the Basic Indicator Approach method.

As at 31 March 2020, the Leverage Ratio, calculated in accordance with the CRR, was 11.5%, and as at 31 December 2019 it was 10.9%. The leverage ratio is calculated as total Tier 1 own funds divided by the total risk exposure measure, including the risk position on assets and off-balance-sheet liabilities.

Capital ratios

Position Q1 2020 Q4 2019 Q3 2019 Q2 2019 Q1 2019

Leverage Ratio 11.46% 10.88% 10.89% 10.59% 12.00%

CET 1 Ratio 20.54% 19.66% 18.73% 17.99% 20.02%

T1 Capital Ratio 20.54% 19.66% 18.73% 17.99% 20.02%

Total Capital Ratio 20.54% 19.66% 18.73% 17.99% 20.02%

1.1%

97.0%

1.9% 1.2%

97.5%

1.3% 0.4%

97.5%

2.1%0.8%

97.8%

1.4%

Baltic, Estonia, Latvia, Lithuania

Other EU Non-EU

Luminor Bank AS Interim report for the period ended 31 March 2020

19

According to the prudential requirements, the Pillar 2 requirement set by the ECB in the 2019 Joint Decision on Capital and the Systemic risk and Countercyclical risk buffer requirements set by the Latvian, Estonian and Lithuanian regulators, Luminor Group is required to hold capital exceeding 10.8% CET1 and 15.2% Total capital. Estonian regulator has set a 1.0 % Systemic risk buffer requirement that applies to Luminor’s exposures in Estonia and translates to 0.2% from Luminor’s total risk weighted exposure amount. As response to the COVID-19 situation, the systemic risk buffer will be 0% starting from 1 of May 2020. Lithuanian regulator has set a 1.0% Countercyclical buffer requirement that applies to Luminor’s exposures in Lithuania and forms 0.5% of Luminor’s total risk weighted exposure amounts. As reponse to the COVID-19 situation, the countercyclical buffer was set to 0% starting from 1 April 2020.

Own funds requirements

thousand EUR 31 March 2020 31 December 2019

TOTAL RISK EXPOSURE AMOUNT 7 781 232 7 969 099

1. RISK-WEIGHTED EXPOSURE AMOUNTS FOR CREDIT, COUNTERPARTY CREDIT AND DILUTION RISKS AND FREE DELIVERIES

Regional governments or local authorities 12 815 13 445

Public sector entities 567 674

Institutions 52 457 54 281

Corporations 3 582 956 3 742 611

Retail 1 341 714 13 742 611

Secured by mortgages on immovable property 1 508 980 1 532 931

Exposures in default 275 703 292 472

Items associated with particularly high risk 154 512 134 498

Equity 6 089 5 778

Other items 118 775 128 517

TOTAL RISK EXPOSURE AMOUNT FOR POSITION, FOREIGN EXCHANGE AND COMMODITIES RISKS

21 921 19 232

TOTAL RISK EXPOSURE AMOUNT FOR OPERATIONAL RISK (OpR ) 684 108 679 644

TOTAL RISK EXPOSURE AMOUNT FOR CREDIT VALUATION ADJUSTMENT 20 635 17 784

Luminor Bank AS Interim report for the period ended 31 March 2020

20

Statement of the Management Board

The interim report of Luminor Bank AS for the first quarter of 2020 consists of the following parts and reports:

• The Management Report;

• The Condensed Consolidated Interim Financial Statements.

The data and additional information presented in the interim report of Luminor Bank AS for the first quarter of 2020 are true and complete. The Condensed Consolidated Interim Financial Statements have been prepared according to the principles of the International Accounting Standard IAS 34 Interim Financial Reporting and the requirements established by the Credit Institutions Act for the disclosure of information.

Luminor Bank AS and the Bank’s subsidiaries are going concerns.

Erkki Raasuke

CEO and Chairman of the

Management Board

Tallinn, 26 May 2020

Luminor Bank AS Interim report for the period ended 31 March 2020

Total equity at 31 December 2019 34 912 1 412 243 1 198 183 916 1 632 269

Total equity at 31 December 2019 34 912 1 412 243 1 198 183 916 1 632 269

Profit (loss) for the period 0 0 0 -21 192 -21 192

Other comprehensive income 0 0 4 0 4

Total comprehensive income for the period 0 0 4 -21 192 -21 188

Transfer to mandatory reserve 0 0 0 0 0

Other 0 0 0 -1 031 -1 031

Total equity at 31 March 2020 34 912 1 412 243 1 202 161 693 1 610 050

* On 28 May 2019 Luminor’s shareholders decided to carry out a bonus share issue, followed by a reduction of share capital. The bonus share issue is based on the bank’s interim balance sheet as of January 2, 2019 and involves a partial conversion of share premium in the amount of 216 030 920 EUR into share capital. Following the bonus issue, the share capital of the bank has been reduced by the same amount and was paid out to the shareholders in September 2019.

Luminor Bank AS Interim report for the period ended 31 March 2020

25

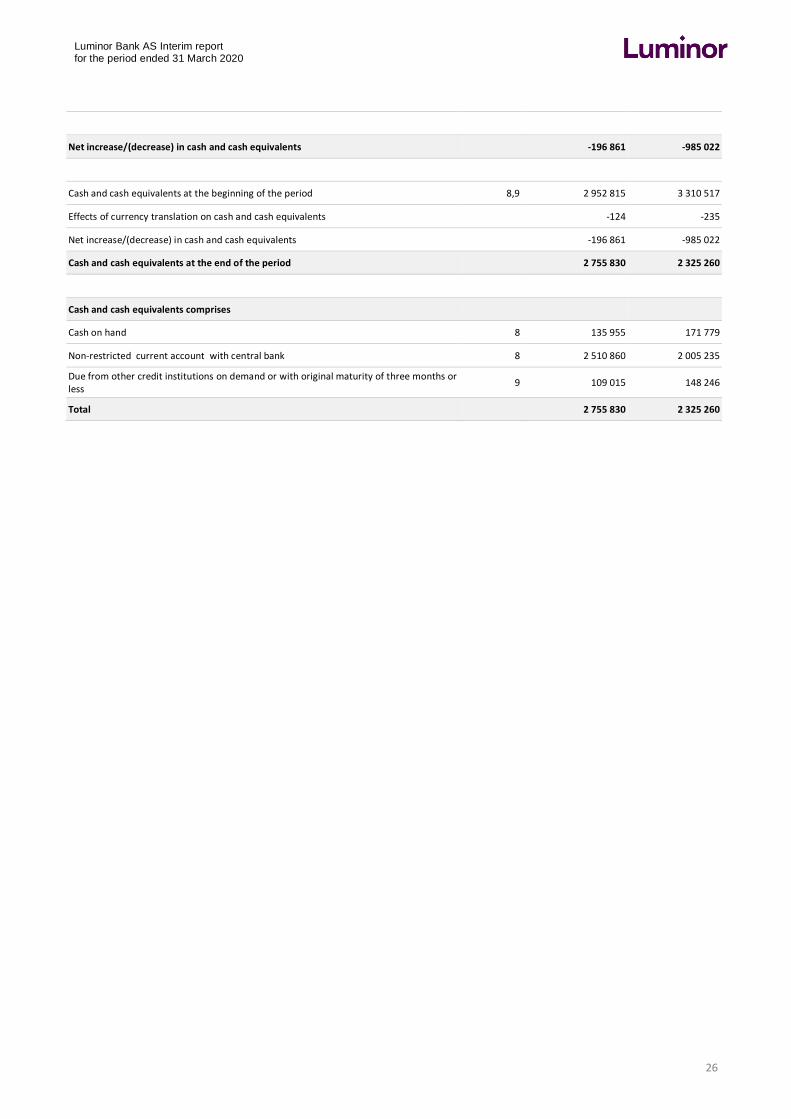

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

thousand EUR Notes Q1 2020 Q1 2019

Cash flows from operating activities

Profit before tax -18 965 28 010

Adjustment for:

-Net impairment (losses)/ reversal on loans to customers 11 26 411 -7 276

-Dividend income -18 -29

-Share of profit from an associate -311 -214

-Loss/(profit) from foreign currency revaluation 124 235

-Depreciation, amortisation and impairment 2 990 3 571

-Other adjustments 1 674 -301

-Interest income 4 -70 624 -74 550

-Interest expenses 4 16 544 10 736

Cash flow from operations before changes in operating assets/liabilities -42 175 -39 818

Change in operating assets/liabilities

Increase (-) / decrease (+) of lending to customers 269 868 211 118

Increase (-) / decrease (+) of other assets -4 740 5 736

Cash flow from operating activites -656 993 -950 991

Investing activities

Acquisition of property and equipment and intangible assets -979 -2 632

Acquisition of investment property 0 800

Proceeds from disposal of property and equipment and intangible assets 625 8 401

Dividend received 18 29

Cash flow from investing activities -336 6 598

Financing activities

Debt securities issued 503 313 0

Payments of principal on leases -670 -811

Cash flows from financing activities 502 643 -811

Luminor Bank AS Interim report for the period ended 31 March 2020

26

Net increase/(decrease) in cash and cash equivalents -196 861 -985 022

Cash and cash equivalents at the beginning of the period 8,9 2 952 815 3 310 517

Effects of currency translation on cash and cash equivalents -124 -235

Net increase/(decrease) in cash and cash equivalents -196 861 -985 022

Cash and cash equivalents at the end of the period 2 755 830 2 325 260

Cash and cash equivalents comprises

Cash on hand 8 135 955 171 779

Non-restricted current account with central bank 8 2 510 860 2 005 235

Due from other credit institutions on demand or with original maturity of three months or less

9 109 015 148 246

Total 2 755 830 2 325 260

Luminor Bank AS Interim report for the period ended 31 March 2020

27

NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

1. SIGNIFICANT ACCOUNTING POLICIES

CORPORATE INFORMATION

Luminor Bank AS (Luminor, the Bank or the Group) is a local credit institution whose parent company is Luminor Holding AS that is ultimately controlled by BCP VII, an investment fund managed by an affiliate of Blackstone Group Inc. Other shareholders of Luminor Holding AS - Nordea Bank Abp and DNB BANK ASA - are considered to be the entities with significant influence over the Group. The Luminor Bank’s registered legal address is Liivalaia 45, 10145, Tallinn, Republic of Estonia.

New company Luminor Holding AS, established on the 14th of May 2019, is the new parent company of Luminor Bank AS since 23 September 2019. Until 23 September 2019 the parent company was Luminor Group AB.

On 2 January 2019 Luminor Bank AS has completed its cross-border merger and continues its operations in all Baltic countries through the Estonian registered bank, Luminor Bank AS, and its branches in Latvia and Lithuania.

On 30 September 2019 a consortium led by private equity funds managed by Blackstone acquired a 60.1% majority stake in the Luminor Holding AS, the owner of Luminor Bank AS. Luminor Bank AS previous owners, Nordea Bank Abp ("Nordea") and DNB BANK ASA ("DNB"), each retained a 19.95% equity stake in the Bank.

In the current interim report, “Bank” (or Luminor Bank AS) refers to Luminor Bank AS. “Group” refers to the consolidated financial statements of Luminor Bank AS and its subsidiaries.

As at 31 March 2020 Luminor Bank AS directly or indirectly owned majority in the following subsidiaries (100%):

Registered country Republic of Estonia:

Registered country Republic of Latvia:

Registered country Republic of Lithuania:

• Luminor Liising AS

• Luminor Pensions Estonia AS

• Promano Estonia OÜ

• Luminor Asset Management IPAS

• Luminor Finance SIA

• Luminor Latvijas atklātais pensiju fonds AS

• Luminor Līzings SIA

• Luminor Līzings Latvija SIA

• Promano Lat SIA

• Realm SIA

• Salvus SIA

• Salvus 2 SIA

• Salvus 3 SIA

• Salvus 4 SIA

• Salvus 6 SIA

• Trioleta SIA

• Baltic ipasums SIA

• Industrius UAB

• Intractus UAB

• Promano Lit UAB

• Recurso UAB

• Luminor Investiciju Valdymas UAB

• Luminor Lizingas UAB

• Gėlužės projektai UAB (under liquidation)

As at 31 March 2020 Luminor Bank AS had ownership in the following associated companies (25%):

• ALD Automotive AS

• ALD Automotive SIA

• ALD Automotive UAB

• SIA Kredītinformācijas Birojs

Luminor Bank AS Interim report for the period ended 31 March 2020

28

BASIS OF PREPARATION

The condensed consolidated interim financial information of Luminor Bank AS (Luminor, the Bank or the Group) was prepared in accordance with IAS 34 Interim Financial Reporting as adopted by the European Union. The condensed consolidated interim financial information does not contain all the information and disclosures required in the annual financial statements and should be read in conjunction with the annual financial statements of Luminor Bank AS for the year ended 31 December 2019.

The accounting policies adopted in the preparation of the condensed consolidated interim financial information are consistent with those followed in the preparation of the Luminor Bank AS annual financial statements for the year ended 31 December 2019, except for the adoption of new standards effective as of 1 January 2020. The Group has not early adopted any standard, interpretation or amendment that has been issued but is not yet effective. Several amendments and interpretations apply for the first time in 2020, but do not have a material impact on the interim condensed consolidated financial statements of the Group.

Group decided to present financial information in interim report at the same format as it was presented in the annual financial statements of Luminor Bank AS for the year ended 31 December 2019, therefore comparative data for the period Q1 2019 has been updated accordingly.

2. SIGNIFICANT ACCOUNTING ESTIMATES AND JUDGMENTS

The Group makes estimates and applies assumptions that affect the amounts recognised in the consolidated financial statements and the carrying amounts of assets and liabilities. Estimates and judgements are continuously evaluated and are based on management’s experience and expectations of future events. In the first quarter of the 2020 global COVID-19 pandemic affected many economies, individuals and companies and thus also required Luminor to react and make certain judgements which inter alia had the effect on the impairment amounts.

IMPAIRMENT OF FINANCIAL INSTRUMENTS

The Group recognizes credit losses in accordance with IFRS 9. The Standard applies a forward-looking expected credit loss (ECL) approach. The Group is required to recognize an allowance for expected losses for all loans and other debt financial assets not held at fair value through profit or loss (FVPL), together with loan commitments and financial guarantee contracts. The assets to test for impairment are divided into three groups depending on the stage of credit deterioration. Stage 1 includes assets where there has been no significant increase in credit risk since initial recognition or which are classified as low credit risk (credit rating indicating investment grade). The allowances for stage 1 assets are based on the expected credit losses associated with the probability of default in the next twelve months (12-month expected credit loss). Stage 2 includes assets where there has been a significant increase in credit risk. The allowances for stage 2 assets are based on the expected credit losses associated with the probability of default over the life of the asset (lifetime expected credit losses). Stage 3 includes credit-impaired (defaulted) assets, and the allowances reflect the lifetime expected credit losses. Material assets in stage 3 are tested for impairment on an individual basis, while for immaterial stage 3 assets a collective assessment is performed. Loss allowances based on lifetime expected credit losses are calculated also for additional category - purchased or originated credit-impaired assets (POCI) - regardless of the changes in credit risk during the lifetime of an instrument.

The Group’s ECL calculations are outputs of complex models with a number of underlying assumptions regarding the choice of variable inputs and their interdependencies. Elements of the ECL models that are considered accounting judgements and estimates include:

• evaluating the criteria for assessment of significant increase in credit risk and allocation of loans to stage 1 or 2; identification of unlikely to pay criteria and assignment of loans to stage 3;

• classification of forbearance and Watch list;

• assessing accounting interpretations and modelling assumptions used to build the models that calculate ECL, including the various formulas and the choice of inputs;

• the modelling and calculation of key parameters of ECL model, including probability of default (PD), loss given default (LGD) and exposure at default (EAD);

• determining the macro-economic indicators and incorporating forward-looking information into the ECL model;

• estimating the above-mentioned indicators for reliable future period and for three different scenarios (baseline, optimistic and pessimistic) and assigning probabilities to those scenarios;

Luminor Bank AS Interim report for the period ended 31 March 2020

29

• estimating ECL under base case and risk case scenarios for stage 3 material assets individual assessments and assigning probabilities to those scenarios;

• setting principles for stage 3 immaterial assets collective assessment.

The model applied (including triggers for significant increase in credit risk) was not changed in the first quarter of 2020. The macroeconomic parameters were reviewed to reflect the outlook due to COVID-19.

More qualitative and quantitative information on an impairment of financial assets in light of COVID-19 is provided in Note 3 General Risk Management Policies.

FAIR VALUE OF FINANCIAL INSTRUMENTS

Where the fair values of financial assets and financial liabilities recorded on the statement of financial position cannot be derived from active markets, they are determined using a variety of valuation techniques that include the use of mathematical models. The input to these models is taken from observable markets where possible, but where this is not feasible, a degree of judgement is required in establishing fair values. For the fair value of financial assets and liabilities refer to Note 17.

3. GENERAL RISK MANAGEMENT POLICIES

MAIN GOALS

The aim of risk management at Luminor is to achieve an optimal balance between the risk of losses and the earnings potential in a medium- and long-term perspective.

The Luminor Risk Management function is organised in order to ensure efficient and effective risk management and full implementation of the principles and requirements outlined in Luminor’s Risk Policy and Strategy.

The risk management principles are the following:

• Risk Accountability: every area in the Group is accountable for the risks arising from their activities;

• Risk Identification, Assessment, Measurement, Monitoring, Mitigation and Reporting: all material exposures must be identified, assessed, managed and reported in a timely and accurate manner;

• The Group shall have a conservative overall risk profile and only assume risk which Luminor is able to identify, assess, manage and monitor;

• The Group is committed not to offer products or services or perform other acts which entail a risk of contributing to unethical conduct, infringement of human or labour rights, corruption or serious environmental harm.

The Group maintains a Recovery Plan following the Bank Recovery and Resolution Directive adopted by the European Parliament. The plan serves as one of Luminor’s key risk management tools and ensures procedures for restoration of the Group’s solvency following situations of severe stress without any involvement by or support from the authorities or taxpayers.

Luminor’s risk appetite in general is low. The Group assesses its capital and liquidity adequacy on an ongoing basis.

The Group analyses, evaluates, accepts and manages the risks or combinations of risks to which it is exposed to. The most important types of risk the Group is exposed to are solvency risk, credit risk, model risk, market risk, liquidity risk, operational risk, reputational risk, and business model risk. Concentration risk is assessed as part of the credit risk, other types of concentration risk are assessed to be less material for the Group. Market risk includes foreign exchange risk and interest rate risk. Operational risk includes also compliance, fraud and financial crime, business continuity and IT stability risks, as well as risks related to cyber- and information security.

In the light of COVID-19 epidemic developments in Europe, the ECB-led Comprehensive Assessment (i.e. both the Asset Quality Review and Stress Test exercises) has been put on hold until further notice. The ECB will inform Luminor when the new information on revised dates and timelines is available. Luminor has reprioritized its strategic activities for year 2020 accordingly and is focusing on a COVID-19 impact assessment and performs institution-wide stress tests under COVID-19 affected macroeconomic scenarios and financial shocks.

Luminor Bank AS Interim report for the period ended 31 March 2020

30

The risk management in the Group is organised in such a way that any possible conflicts of interest are avoided or escalated.

Organisational Structure of the Risk Management function:

The Enterprise Risk Department is a centralized center of expertise and manages risk management tools and processes which run across different risk types. The control function for operational risk lies under the responsibility of the Operational Risk Department. The Market & Liquidity Risk Department is responsible for market risk and liquidity risk control. The control function for credit risk is split under the responsibility of the Credit Risk Department and Credit Risk Quantification Department. The Model Risk & Validation Department owns the model risk framework and respective validation activities. The Risk Programmes: CA & IRB Department and Risk Transformation Department drive Luminor’s development and further improvement of risk management. The Risk division is part of the second line of defence and the organisational departments within the Risk division report directly to the Group Chief Risk Officer (CRO).

Risk management processes and the effectiveness of internal control are assessed by the Internal Audit function (third line of defence).

The internal control framework – as a system of organisational measures, actions covering the whole Luminor Group, including the Management’s responsibilities and tasks, and the activities of all business lines and internal units, including internal control functions, outsourced activities and distribution channels and internal procedures – ensures the effective and efficient operations and prudent conduct of business, compliance with laws, regulations, supervisory requirements and Luminor’s internal policies, the adequate and continuous identification, assessment, measurement, monitoring, mitigation and reporting of risks, the sound administrative and accounting procedures as well as the reliability of financial and non-financial information and submission thereof in a timely manner. The Management Board is responsible for establishing and monitoring the adequacy and effectiveness of internal control system and for overseeing all business lines and internal units in the Group.

The Management Board and/or Supervisory Council approve the most important policies and strategies comprising the Group’s risk management framework.

The Supervisory Council Risk Committee advises the Supervisory Council regarding the setting and monitoring of risk appetite, strategy and further matters related to risk management. The Supervisory Council Risk Committee raises concerns and warns, where appropriate, when specific developments materially affect or may affect Luminor’s risk profile.

The Credit Committee is a decision-making body regarding individual credit cases and contributes to the development of a sound and uniform credit culture in the Group. The Credit Committee provides recommendations regarding important credit regulations.

COVID-19

The COVID-19 pandemic and the preventive measures imposed by most of the European countries had an adverse impact on economies in the first quarter of 2020. Luminor has been monitoring the spread of COVID-19 since early 2020 and was preparing to adjust its risk management to the new reality. The impact on different types of risks is disclosed further below.

CREDIT RISK

Credit risk is defined as the risk for the Group to incur losses due to customers’ failure to fulfil their financial obligations towards the Group. Credit exposures arise primarily in lending activities, including from off-balance sheet financial instruments, such as loan commitments, guarantees and letters of credit.

The key principles of Luminor’s credit risk management are outlined in the Group Credit Policy, Credit Strategy for Legal Entities and Credit Strategy for Private Individuals. Practical aspects of the application of the principles set out in these documents, and decision-making processes are regulated by the Credit Manual for Legal Entities and Credit Manual for Private Individuals.

Group Chief Risk Officer

Enterprise RiskOperational

RiskMarket &

Liquidity RiskCredit Risk

Credit Risk Quantification

Model Risk & Internal

Validation

Risk Programmes:

CA & IRB

Risk Transformation

Luminor Bank AS Interim report for the period ended 31 March 2020

31

The spread of the COVID-19 is a global tragedy that requires governments, private businesses, and all citizens to work together and fight this disease and its consequences. In a first instance, this has required governments across Europe and also in the Baltic states to impose significant constraints on social- and economic life to slow the spread of the disease, avoid overburdening of the health care system, and by doing so saving lives. These social- and economic constraints carry high costs, because they imply a significant reduction of economic activity, including businesses being almost entirely shut down in certain sectors, and strongly increasing unemployment as a consequence.

Since Luminor is one of the largest banks in the Baltic region, many of Luminor’s customers are directly or indirectly affected by this situation, some of our customers are severely affected. We in Luminor feel therefore strongly that we need to play as constructive role as possible to support our customers during this time of need and to serve the Baltic states and communities by securing a robust and stable financial system and robust and stable financial services.

This also requires from Luminor to extend additional support and additional solutions to our customers in order to make sure that our customers get through this difficult period as well as possible. On the other hand, Luminor is also charged with the responsibility to protect Luminor’s depositors, and to make sure that Luminor’s balance sheet and the Baltic financial system do not become overburdened by businesses for which there is no outlook of recovering from this crisis into a sound and viable business. These customers need to be significantly restructured, and in cases where even that is no longer feasible, some businesses might have to be wound down in an orderly manner.

In order to be able to appropriately work with customers and manage COVID-19 related credit risks, the Group prepared a dedicated “COVID-19 Manual” for Legal Entities. Luminor’s general focus on our customers’ ability and willingness to perform their financial obligations is maintained. When considering modifications, particular emphasis is put on whether deteriorations are triggered by the external COVID-19 shock and a robust recovery is expected afterwards. Luminor’s standard approach and procedures are applied if deteriorations started already before COVID-19 or deteriorations are not related to COVID-19. The industry in which the customer operates, the fact whether Luminor is the main lender, and the type of credit product also play a role. In case of new lending, the financial ability to serve the credit remains a key aspect. For individual customers payment holidays on principal payments for a limited period of time might be granted either automatically if certain predefined conditions are met or through performing individual assessments. By the end of first quarter 2020 no industry-wide private moratoria which would comply with the European Banking Authority’s (the EBA) Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis were in place.

Credit decisions are made by Credit Committees and authorised individuals according to defined powers to act, which are risk adjusted. The decision of the Credit Committee must be unanimous. Powers to act for individuals (Credit Officers and persons from Sales, Restructuring & Recovery) are personal and based on competence level. Some extent of flexibility for decision taking on “automatic” changes was introduced to be able to handle more customer requests for modifications.

Modifications and forbearances

Luminor has defined standard modification solutions for COVID-19 affected customers. For individual customers standard/automatic grace period for principal payments is granted if the customer had acceptable payment history (no more than 21 days overdue during last 12 months): up to 6 months for mortgage loans, up to 3 months for consumer loans and leasing agreements. For business customers solutions are also product specific. For commercial loans, a grace period up to 6 months is granted for low and medium risk level customers. For leasing agreements, a grace period up to 3 months is possible, if the leasing object is a passenger car and historical overdues during the last 12 months did not exceed 15 days; and for low and medium risk transportation sector entities where exposure does not exceed 2 million EUR and historical overdues and trends in historical financial results evidence that difficulties are purely COVID-19 related.

Individual evaluation of modification requests is performed for all other cases. For COVID-19 affected customers the state support programmes or state guarantees are used whenever feasible.

Forbearance treatment in essence is kept unchanged, the integral condition is financial difficulties. Currently the modification is not classified as forbearance if

• individual customers have good payment history and acceptable loan-to-value (LTV) ratio, meaning overdues below 21 days during last 12 months and LTV below 85 per cent;

• business customers are considered low and medium risk, taking into account the combination of financial risk and industry risk.

Besides regular reports prepared and presented to the Group’s management bodies to follow the level and developments of the assumed credit risk, specific COVID-19 related reports are being prepared which are also shared with the ECB.

Luminor Bank AS Interim report for the period ended 31 March 2020

32

Impairment policies

The Group recognises credit losses in accordance with the requirements of IFRS 9. IFRS applies a forward-looking expected credit loss (ECL) approach. For more detailed information on the impairment policies, please refer to Note 5 General Risk Management Policies of the Luminor Bank AS Annual Report 2019. In the first quarter of 2020 the impairment methodology remained unchanged.

Different authorities – the ECB, EBA, European Securities and Markets Authority (ESMA), IFRS Foundation, Basel Committee on Banking Supervision (BCBS) – have announced various measures to deal with the crisis and minimise the effect on the economies. The Group acts in line with above mentioned institutions’ guidance in regards of ECL. The modifications granted for COVID-19 affected customers do not automatically indicate Significant Increase in Credit Risk (SICR), nor classification to forbearance or default status. However, the obligation to assess for unlikeliness to pay (which consequently triggers default status) remains in place.

The set of SICR triggers was not changed:

• Significant increase of lifetime PD – significant increase of lifetime PD since initial recognition until the reporting date (2.5 times and 0.6 p.p. jointly);

• Risk grade 9 or 10 – risk grade 9 or 10 as at the reporting date;

• >30 days past due – more than 30 days past due as at the reporting date;

• Forborne performing – forborne performing status as at the reporting date (forbearance not triggering non-performing status) in accordance with FINREP instruction reporting requirements;

• Watch list – watch list status as at the reporting date.

If at least one of the above SICR indicators is identified after initial recognition of the financial instrument and was not present as of its origination the financial asset is treated as facing a significant increase in credit risk.

Three macroeconomic variables - annual change in real GDP, unemployment rate and annual change of residential real estate price - are included in the PD and LGD estimation modelling for the individual customers segment and two of them – annual change in real GDP together with unemployment rate – are used for PD and LGD estimation modelling in case of the business customers segment. The following tables show the parameters that were used for macroeconomic modelling as at 31 March 2020 and 31 December 2019. For the first quarter of 2020 the forecasts of macroeconomic variables were updated by Luminor macroeconomists at the end of March 2020 with projections and assumptions over three years. Following the ECB guidance, excessively procyclical forecasts were avoided assuming not only the nearest short-term downturn (the first year) but also the recovery period in the market after that (the second and the third year). Starting from the fourth year it is assumed that risk parameters (PD and LGD) converge to their long-term average levels (estimated over the cycle).

Luminor Bank AS Interim report for the period ended 31 March 2020

The adverse impact of COVID-19 is reflected in asset quality of Luminor.

The most severe consequences will most probably be seen in industries like accommodation, tourism, and aviation. Even though Luminor’s portfolio towards these economic sectors is relatively small, negative trends in the portfolio are still observed since many other industries are quite severely affected as well. As a result, requests for modifications (including grace period) reached 0.9 billion EUR at the end of March 2020 and exceeded 1.1 billion EUR (11% of the total credit portfolio) by the middle of April 2020.

Considering the situation, and the generous terms for modifications, the number of modifications has been limited so far.

Approximately 70% of modification requests came from business customers. Earlier applications for modification from business customers compared to individual customers can be explained by the following reasons:

Luminor Bank AS Interim report for the period ended 31 March 2020

35