6/22/16

1

1111

©20

12Cli+

onLarson

AllenLLP

INTERMEDIATEGOVERNMENTALACCOUNTING

KarinSlater,CPFOCFOMontroseCountySchoolDistrict

June23,2016

2

TheGovernmentalEnvironment

• Keyenvironmentalcharacteris=cs– Twocharacteris=csofthegovernmentalenvironmenthavehadanimportantimpactonthedevelopmentofpublic-sectoraccoun=ngandfinancialrepor=ngprac=ce:1)Notalloftheac=vi=esofstateandlocalgovernmentshavethesamefinancialobjec=ves(opera=onalaccountability).

2)Governmentshaveaspecialresponsibilitytodemonstratethattheyhavecompliedwithrestric=onsontheuseofresources(fiscalaccountability).

3

TheGovernmentalEnvironment

• Differentfinancialobjec=vesfordifferentac=vi=es– Privatesectorenterprisessetouttomakeaprofitbyprovidinggoodsorservicestocustomers

◊ Some=messervicesofferedbygovernmentsfunc=oninmuchthesamewayasprivate-sectorbusinessessotheyaredescribedasbusiness-typeac=vi=es(i.e.governmentoperatedgolfcourses).

◊ Some=messervicesofferedbygovernmentsdonotfunc=onlikeprivate-sectorbusinessessotheyaredescribedasgovernment-typeac=vi=es(i.e.publicsafety.)

6/22/16

2

4

TheGovernmentalEnvironment

• Fiscalaccountability– Budgetsinthepublicsectorfunc=onasmorethanjustafinancialplan.Theyaretheconcretemanifesta=onofalegisla=vebody’sabilitytosetpublicpolicy.

– Theappropriatedbudgetofastateorlocalgovernmentenjoystheforceoflawandviola=onsaresubjecttolegalsanc=ons

5

TheGovernmentalEnvironment

• FundAccoun=ng– Intheprivatesectorgenerallyeventhemostcomplexbusinessesarepresentedasasingle,unitaryen=tyforthepurposesoffinancialrepor=ng.

– Governments,however,arerequiredtousefundrepor=ngtoaccompanytheirgovernmentwidefinancialstatements.

6

TheGovernmentalEnvironment

• Specialmeasurementfocusandbasisofaccoun=ngforgovernmenten==es– Government’susetwodifferentmeasurementfocus.

◊ Business-typeac=vi=esuseaneconomicresourcesmeasurementfocus.

◊ Government-typeac=vi=esuseafinancialresourcesmeasurementfocus.

6/22/16

3

7

FinancialReporKngModel

• Fundaccoun=ng-wasspecificallydevelopedtoprovideinforma=ononfiscalaccountabilitytousersofthefinancialstatements.

• Government-widefinancials–TheGASBdeterminedthatgovernment-widefinancialstatementsarenecessarytoprovideinforma=ononopera=onalaccountability.

8

GovernmentalFunds(Government-typeacKviKes)

• Governmentalfundsinclude:– Generalfund– Specialrevenuefunds– Capitalprojectfunds– Debtservicefunds– Permanentfunds

9

GovernmentalFunds

• Generalfund–isthechiefopera=ngfundofastateorlocalgovernment.GAAPprescribesthatthegeneralfundbeused“toaccountforandreportallfinancialresourcesnotaccountedforandreportedinanotherfund.”

6/22/16

4

10

GovernmentalFunds

• Specialrevenuefunds–usedtoaccountforandreportproceedsofspecificrevenuesourcesthatarerestrictedorcommicedtoexpenditureforspecifiedpurposeotherthandebtserviceorcapitalprojects.Notesshoulddisclosethepurposeforeachmajorspecialrevenuefund.

11

GovernmentalFunds

• Debtservicefunds–usedtoaccountforandreportfinancialresourcesthatarerestricted,commiced,orassignedtoexpenditureforprincipalandinterest.– Careshouldbetakeninapplyingthenumberoffundsprincipalwithregardstodebtservicefunds.Soundfinancialmanagementdictatesthatgovernmentsshouldaccountforeachdebtissueseparatelyintheiraccoun=ngsystems,butasingledebtservicefundiso+ensufficientforexternalfinancialrepor=ngpurposes.

12

GovernmentalFunds

• Capitalprojectsfunds–usedtoaccountforandreportfinancialresourcesthatarerestricted,commiced,orassignedtoexpenditureforcapitaloutlays,includingtheacquisi=onorconstruc=onofcapitalfacili=esandothercapitalassets.Excludescapitalprojectsfinancedbyproprietaryfunds,trustfunds,privateorganiza=ons,orothergovernments.

6/22/16

5

13

GovernmentalFunds

• Permanent–usedtoaccountforandreportresourcesthatarerestrictedtotheextentthatonlyearnings,andnotprincipal,maybeusedforpurposesthatsupporttherepor=nggovernment’sprograms,thatis,forthebenefitofthegovernmentoritsci=zenry.

14

ProprietyFunds(business-typeacKviKes)

• ProprietaryFunds– 1)Enterprisefunds– 2)Internalservicefunds

15

ProprietaryFunds

• Enterprisefunds–maybeusedtoreportanyac=vityforwhichafeeischargedtoexternalusersforgoodsorservices(definedasan“exchange”or“exchangelike”transac=onasdiscussedinGASB33).GAAPalsorequirestheuseofanenterprisefundwhere:– Debtbackedsolelybyfeesandcharges– Legalrequirementtorecovercostswithfeesandcharges– Pricingpoliciesoftheac=vityestablishfeesandchargesdesignedtorecovercosts

6/22/16

6

16

ProprietaryFunds

• Internalservice–usedtoallocatethecostofcertainsharedac=vi=estootherfunds.– Theuseofaninternalservicefundisneverrequiredandmustalwaysbeeliminatedingovernment-widestatements.

– Thegoalofaninternalservicefundshouldbetomeasurethefullcostofprovidinggoodsorservicesforthepurposeoffullyrecoveringthatcostthroughfeesorcharges.Fullcost,forthispurposeincludesthecostofcapitalassetsusedinprovidinggoodsorservicestocustomers.

17

FiduciaryFunds

• GAAPdefinesfiduciaryfundsasfundsthatareused“toreportassetsheldinatrusteeoragencycapacityforothersandthereforecannotbeusedtosupportthegovernment’sownprograms.”

18

FiduciaryFunds

• Fiduciaryfunds– Pensionandotheremployeebenefittrustfunds– Investmenttrustfunds– Privatepurposetrustfunds– Agencyfunds

6/22/16

7

19

BasisofAccounKng

• Basisofaccoun=ngdetermineswhenthegovernmentwillrecognizetransac=onsintheaccoun=ngrecordsandwhentheywillbereportedinthefinancialstatements.– Governmentalfundsusethemodifiedaccrualbasisofaccoun=ng.

– Proprietaryfundsusetheaccrualbasisofaccoun=ng.

20

BasisofAccounKng

• Accrualbasisofaccoun=ngrecognizestransac=onswhentheyoccur,despitethe=mingoftherelatedcashflows.– Usingthisbasisofaccoun=ng,revenuesarerecognizedintheaccoun=ngperiodwhichtheybecomeobjec=velymeasurableandthegovernmentearnsthem.

– Expensesarerecognizedintheperiodincurredassumingthattheyaremeasurable.

21

BasisofAccounKng

• Modifiedaccrualbasisofaccoun=ngmodifiestheaccrualbasisofaccoun=ngtoreflectthespendingoffinancialresources.– Revenuesarerecognizedwhentheyaremeasurableandavailable.

◊ Measurablemeansyouhavesomeobjec=vewaytoquan=fytherevenue.

◊ Availablemeanscollec=blewithinthecurrentperiodorsoonenoughtherea+ertobeusedtopayliabili=esofthecurrentperiod.

6/22/16

8

22

MeasurementFocus

• Measurementfocusdetermineswhatagovernmentmeasuresandreportsinitsfinancialstatements.– Governmentsusetheflowofcurrentfinancialresourcesmeasurementfocus.

– Proprietaryfundsusetheeconomicresourcesmeasurementfocus.

23

Governmentalvs.ProprietaryFunds

24

RevenueRecogniKonforGrants

• The“available”criterionappliestoreimbursementgrants.Forexpendituredrivengrantsingovernmentalfunds,revenuesarerecognizedatthe=meoftheexpenditureonlyifthereimbursementwillbereceivedwithinthegovernment’speriodofavailability.

6/22/16

9

25

Government-WideStatements

• Thegovernment-widestatementsinclude:– StatementofNetPosi=on.– StatementofAc=vi=es(costofservicesapproach).– Economicresourcesmeasurementfocus.– Accrualbasisofaccoun=ng.– Governmentalac=vi=es.– Business-typeac=vi=es.– Discretelypresentedcomponentunits.

26

StatementofNetPosiKon(PreviouslyStatementofNetAssets)

• Allassets(includingcapitalassets)• DeferredInflows• Allliabili=es(includinglong-termliabili=es)• DeferredOullows• Netposi=on(ratherthanfundbalances,retained

earnings;GASB34wascalledtotalnetassets).– Investedincapitalassets,netofrelateddebt– Restricted– Unrestricted

• Choicebetweenclassifiedformatororderofliquidity.

27

DeferredOuVlows(1of3)

• DeferredouVlowofresources:aconsumpKonofnetposiKonbythegovernmentthatisapplicabletoafuturereporKngperiod

• HasaposiKveeffectonnetposiKon,similartoassets

• OuVlowofresources:aconsumpKonofnetposiKonbythegovernmentthatisapplicabletothereporKngperiod

StatementofNetPosiKon

6/22/16

10

28

StatementofNetPosiKonDeferredOuVlows(2of3)

SometransacKonsinwhichtheresulKngitemshouldbereportedasadeferredouVlowofresources(currentlyclassifiedasassets)–GrantpaidinadvanceofmeeKngKmingrequirement–Deferredamountsfromtherefundingofdebt(debits)–Coststoacquirerightstofuturerevenues(intra-enKty)–Deferredlossfromsale-leaseback

29

StatementofNetPosiKonDeferredOuVlows(3of3)

SometransacKonsinwhichtheresulKngitemshouldbereportedasadeferredouVlowofresources(currentlyclassifiedasassets)-Debtissuancecosts(otherthaninsurance)

• IniKaldirectcostsincurredbythelessorforoperaKngleases

• AcquisiKoncostsforriskpools• LoanoriginaKoncosts

30

StatementofNetPosiKonDeferredInflows(1of3)

• Deferredinflowofresources:anacquisiKonofnetposiKonbythegovernmentthatisapplicabletoafuturereporKngperiod

• HasanegaKveeffectonnetposiKon,similartoliabiliKes

• Inflowofresources:anacquisiKonofnetposiKonbythegovernmentthatisapplicabletothereporKngperiod

6/22/16

11

31

StatementofNetPosiKonDeferredInflows(2of3)

SometransacKonsinwhichtheresulKngitemshouldbereportedasadeferredinflowofresources(currentlyclassifiedasliabiliKes)–GrantsreceivedinadvanceofmeeKngKmingrequirement–Taxesreceivedinadvance–Deferredamountsfromrefundingofdebt(credits)–Proceedsfromsalesoffuturerevenues–Deferredgainfromsale-leaseback

32

StatementofNetPosiKonDeferredInflows(3of3)

SometransacKonsinwhichtheresulKngitemshouldbereportedasadeferredinflowofresources(currentlyclassifiedasliabiliKes)–“Regulatory”credits(gainsorotherreducKons)–“Unavailable”revenueingovernmentalfunds–LoanoriginaKonfees(excludingpoints)–lessoraccounKng–Commitmentfees(acerexerciseofexpiraKon)

33

DifferencefromFundStatements(1of2)

• Long-termassets– Receivables– CapitalAssets

• Liabili=es– Debt– CompensatedAbsences– ClaimsandJudgments– PensionBenefitObliga=on– OtherPostEmploymentBenefits(OPEB)

6/22/16

12

34

DifferencefromFundStatements(2of2)

• Inventory(expensewhenusedratherthanwhenpurchased).Previouslyhadtheop=onofusingtheconsump=onmethodorthepurchasemethod,butnowwecanonlyusetheconsump=onmethod.

• Interestpayableonlong-termdebt.

35

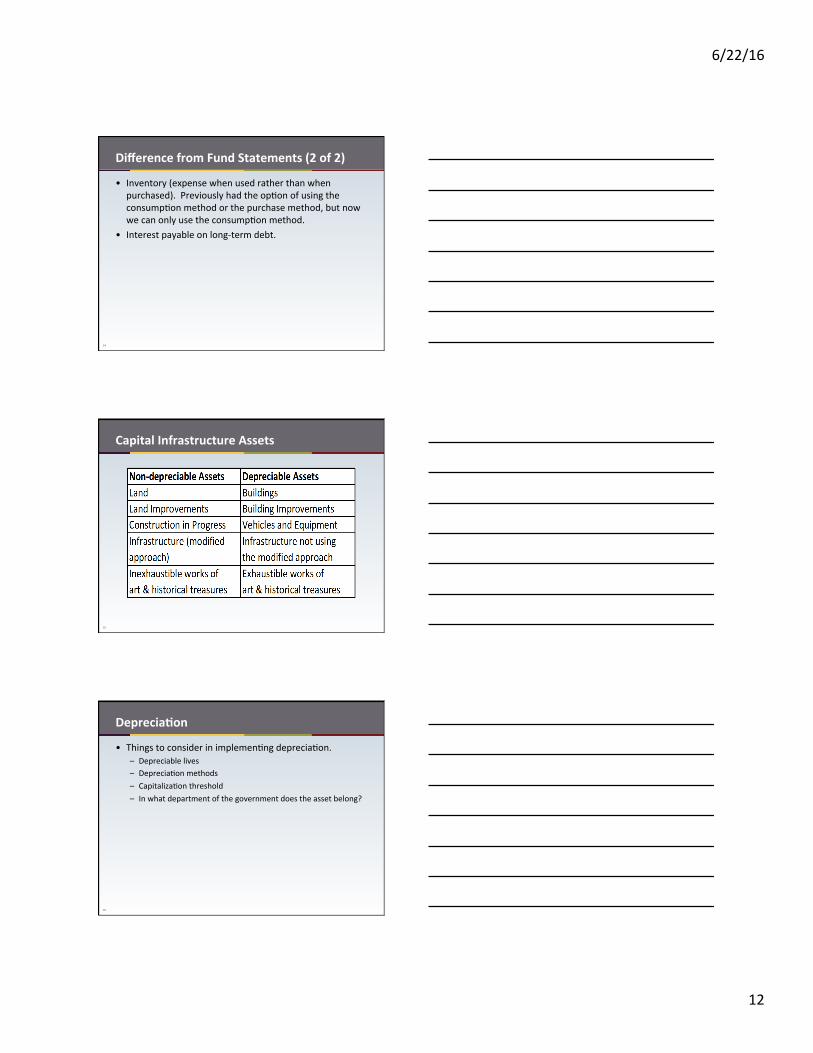

CapitalInfrastructureAssets

36

DepreciaKon

• Thingstoconsiderinimplemen=ngdeprecia=on.– Depreciablelives– Deprecia=onmethods– Capitaliza=onthreshold– Inwhatdepartmentofthegovernmentdoestheassetbelong?

6/22/16

13

37

DefiniKonofInfrastructure

• Infrastructure,definedas:– Long-livedcapitalassetsthatcanbepreservedforasignificantlygreaterperiodthanmostcapitalassets

– Normallysta=onaryitems– Examples:

◊ Roadsandbridges,dams◊ Waterandsewersystems

38

InfrastructureAssets

• Repor=ngalterna=ves– Historicalcostbaseddeprecia=on– Modifiedapproach

39

“Modified”Approach

• Nodeprecia=onisrequiredifthegovernmentdemonstratesthatitismaintainingqualifyinginfrastructureassetsapproximatelyatorabovethecondi=onlevelestablished.

• Condi=onassessmentsmustbeperformedatleasteverythreeyears.

6/22/16

14

40

StatementofAcKviKes

• Netcostformat(expensesminusprogramrevenue–netcost)

• Expensesbyfunc=ons/programs• Revenuesby:

– Program(chargesforservicesandprogramspecificopera=ngandcapitalgrants)or

– General(i.e.taxesandothernonprogramrevenue)

• Special,extraordinaryitemsandtransfers

41

Expenses

• Expensesarereportedbyfunc=on– Directexpenses–required– Indirectexpensesalloca=onpermiced

◊ Separatecolumnforindirectexpensesifallocated– Deprecia=on– Interest

42

ProgramandGeneralRevenues

• Programrevenuesreducethenetcostofaprogram.– Chargesforservices– Programspecificgrantsandcontribu=ons

• Netcostisfinancedbygeneralrevenues.Allrevenuesaregeneralrevenuesunlesstheyarerequiredtobereportedasprogramrevenues.

6/22/16

15

43

DifferencesfromFundStatements

• Recogni=onofrevenuesonaccrualbasis.– Propertytaxes–noavailabilitycriterion,recordedonfullaccrualbasisofaccoun=ng.

– Recogni=onofexpensesforlong-termliabili=es.◊ Compensatedabsences◊ Claimsandjudgments◊ Pensionbenefitobliga=on◊ OPEB

44

GASB34RequirementsFundLevelStatements

• FundPresenta=ons– Majorfunds– Non-majorfundspresentedinasinglecolumnbycategory– Majorfundconceptdoesnotapplytofiduciaryfundsorinternalservicefunds

45

MajorFundCriteria

• GeneralFundisalwaysamajorfund• Individualfundis:

– Atleast10percentofassetsincludingdeferredoullows,liabili=esincludingdeferredinflows,revenue,expenditures/expenses,(excludingextraordinaryitems)oftherelevantcategoryorfundtype

• Atleast5percentoftotalgovernmentalandenterprisefundscombined

• Otherfundsthataredeemedtobeimportantforseparatedisclosure

6/22/16

16

46

GovernmentalFundStatements

• RequiredStatements:– BalanceSheet– StatementofRevenue,Expenditures,andChangesinFundBalances

– Characteris=csofgovernmentalfundstatements:◊ Currentfinancialresourcesmeasurementsfocus◊ Modifiedaccrual◊ Reconcilia=onrequiredtogovernment-widestatementsforbothstatements

47

TreatmentofInternalServiceFunds

• Removethe‘doublingup”effectofinternalservicefundac=vity.

• Generally,assetsandliabili=esarereportedwithgovernmentalac=vi=es–unlessinternalservicefundsprimarilysupportbusiness-typeac=vi=es.

48

ProprietaryFunds

• Economicresourcesmeasurementfocus• Accrualbasisofaccoun=ng• Enterpriseredefined

– Debtsecuredsolelybypledgeofnetrevenuesfromfeesorcharges

– Lawsorregula=onsrequirerecoveryofcost– Pricingpolicydesignedtorecovercost

6/22/16

17

49

ProprietaryFundStatements

• ClassifiedStatementofNetPosi=on• StatementofRevenue,Expenses,andChangesinNet

Posi=on• StatementofCashFlows• Reconcilia=onrequiredforfinancialposi=onand

opera=ngstatements(ifnecessary)

50

ProprietaryFundStatements

• StatementofNetPosi=on(previouslyNetAssets)– Classified–currentvs.longterm– Restrictedassetsmustbereportedassuch– Netposi=on

◊ Investedincapitalassets,netofrelateddebt◊ Restricted◊ Unrestricted

51

ProprietaryFundStatements

• Opera=ngStatement– Dis=nguishbetweenopera=ngandnon-opera=ng– Capitalcontribu=onsandtransfersreportedseparately

6/22/16

18

52

ProprietaryFundStatements

• CashFlow– Fourcategoriesofcashflows

◊ Opera=ng◊ Non-capitalfinancing◊ Capitalandrelatedfinancing◊ Inves=ng

Directmethodisrequiredforcashflows

53

ComponentUnitPresentaKons

• Discretepresenta=oningovernment-widestatements• Majorcomponentunitrepor=ngchoices:

– Separatecolumnsinthegovernment-widestatements– Separatestatementsa+erfundpresenta=ons– Condensedinforma=oninthenotes

54

RequiredSupplementaryInformaKon

• Budgetarycomparisonsforgeneralfundandmajorspecialrevenuefunds– Originalandfinalbudget– ActualonbudgetarybasisorGAAPbasis– Reconcilia=ontoGAAPbasisstatements– Whenapplicable–infrastructure-modifiedapproach

◊ Threemostrecentcondi=onassessments◊ Es=matedamounttomaintainandpreserveversusactualamountforthelastfiveyears

6/22/16

19

55

MD&AManagementDiscussionandAnalysis

• TheMD&Aisasec=onofagovernment'sannualreportinwhichmanagementdiscussesnumerousaspectsofthecompany,bothpastandpresent.Amongotherthings,theMD&Aprovidesanoverviewofthepreviousyearofopera=onsandhowthegovernmentfaredinthat=meperiod.Managementwillusuallyalsotouchontheupcomingyear,outliningfuturegoalsandapproachestonewprojects.

56

MD&A

• TheMD&Aisaveryimportantsec=onofanannualreport,especiallyforthoseanalyzingthefundamentals,whichincludemanagementandmanagementstyle.Althoughthissec=oncontainsusefulinforma=on,investorsshouldkeepinmindthatthesec=onisunaudited.

57

MD&A

• MD&A’sshould:• enablereaderstoviewthegovernmentthroughthe

eyesofmanagement;• complementaswellassupplementfinancial

statements;• bereliable,thatis,complete,fairandbalanced,and

providingmaterialinforma=on—namely,informa=onthatcouldinfluenceareasonableinvestorinmakingadecisiontoinvestorcon=nuetoinvestinthegovernment;

6/22/16

20

58

MD&A

• Haveaforward-lookingorienta=on;• focusonmanagement’sstrategyforgenera=ngvalue

forinvestorsover=me;• bewriceninplainlanguage,withcandorandwithout

exaggera=on,andembodythequali=esofunderstandability,relevance,comparabilityandconsistencyoverrepor=ngperiods.

59

FinancialStatementDataAnalysis

• MD&Aistheonlyrequiredcomponentofthefinancialstatementsthathascompara=veinforma=on.Thesecompara=vesummariesorschedulesinclude:– NetPosi=ons– ChangesinNetPosi=ons– CapitalAssets– Long-termdebt

60

FiscalHealthAnalysisforColoradoCounKesandMunicipaliKesRaKo1:CashtoLiabiliKesRaKo(CLR)

En=ty-WideUnrestrictedCashandInvestmentsEn=ty-WideCurrentLiabili=es

RaKo2:UnrestrictedFundBalanceRaKo(UFB)

GeneralFundUnrestrictedFundBalanceGeneralFundtotalExpenditures(NetofTransfers

RaKo3:DebtBurdenRaKo(DBR)

TotalGovernmentalRevenueofFund(s)PayingDebtTotalGovernmentalDebtPayments

6/22/16

21

61

FiscalHealthAnalysisforColoradoCounKesandMunicipaliKesRaKo4:TaxRevenueperCapita(TRC)

TotalGovernmentalFundsTaxRevenuePopulaKon

RaKo5:ExpendituresperCapita(EPC)

GeneralFundTotalExpenditures(NetofTransfersPopulaKon

62

FiscalHealthAnalysisforColoradoCounKesandMunicipaliKesRaKo6:OperaKngMarginRaKo(OMR)GeneralFundTotalRevenue–(GeneralfundTotalExpenditures,NetofTransfersGeneralFundTotalRevenue

• RaKo7:EnterpriseFundsNetPosiKon(EFNP)CurrentYearNetPosi=onoftheEnterpriseFundPriorYearNetPosi=onoftheEnterpriseFundhcp://www.leg.state.co.us/OSA/coauditor1.nsf/LocalGovPublic?openform

63

CAFRPreparaKon

• DiscussionTopics– CAFRPrepara=on-overviewandcommonpilalls– CapitalAssets–presenta=onanddisclosureissuesandstrategies

– Long-TermDebt–presenta=onanddisclosureissuesandstrategies

– RevenueRecogni=onandDeferredRevenue–governmentalvs.government-wide

6/22/16

22

64

CAFRPreparaKonCommonPiVallsinCAFRPresentaKon• Conver=ngfrommodifiedaccrualtofullaccrual

statements• Footnotesdonotagreewithwhatispresentedinthe

basicfinancialstatements• Implementa=onofnewpronouncementsandrelated

disclosures

65

CAFRPreparaKonKeystoPreparingCAFR• Repor=nginforma=oninthefundstatementsunderthe

correctfunc=onalorac=vity– (i.e.interestexpenditures,debtprincipalpaymentsandcapitaloutlay)

• Preparingfootnotedisclosuresthat=eintothebasicfinancialstatementsandprovideenoughinforma=ontoagreetoreconcilingitems– (debtdisclosure,capitalassetsdisclosureandaccountsreceivabledisclosure)

• Reducethenumberofsubsidiaryschedules.Themoreschedulesandprepara=onworksheetsthatarecreated,thegreaterthelikelihoodofanerror

66

CAFRPreparaKonKeystoPreparingCAFR

• Investedincapitalassets,netofrelateddebt– Itemstoexcludefromthecalcula=on

◊ Unexpendedbondproceeds.Bondsonlybecomecapital-relateddebt,andbondproceedsonlybecomecapitalassets,astheproceedsareexpendedforacapitalpurpose.

◊ *Bondissuancecosts.Unlikepremiumsanddiscounts,unamor=zedbondissuancecostsdonot"followthedebt"andareignoredforpurposesofthiscalcula=on.

◊ *Internalborrowings.Borrowingswithintheprimarygovernmentdonotqualifyforpurposesofthiscalcula=on.

6/22/16

23

67

CAFRPreparaKonKeystoPreparingCAFR• Investedincapitalassets,netofrelateddebt(con=nued)

– Itemstoincludeinthecalcula=on◊ Intangiblecapitalassets.Thefactthatacapitalassetisintangibledoesnotmakeitanythelesscapital.

◊ Refundingbonds.Refundingbondsassumethecharacterofthedebttheyreplace.Accordingly,bondsusedtorefundcapital-relateddebtarethemselvesconsideredtobecapital-related.

68

CAFRPreparaKonCapitalAssets

• Keyiscapitalassetfootnote• Typicalgovernmenthasnumerousassetsinconstruc=on

inprogressaccountanditisrecommendedthatgovernmentsconsideratransfercolumntoaccountforcompletedprojectsthatgetmovedfromnondepreciableassetstodepreciable

69

CAFRPreparaKonCapitalAssets

• Capitaladdi=ons-Purchasedassetsversuscontributedassets– Purchasedassetsarefundexpendituresandtoreconciletofullaccrualbasis

needto“credit”expenditures– Ifcapitaloutlayreportedinthefundstatementsdoesnotagreetothe

purchasedcapitaladdi=onsneedtodeterminethoseitemsreportedundercapitaloutlayandwhatfunc=ontheybelongforrepor=ngonthestatementofac=vi=es

– Ifcapitaloutlayalreadyreportedwithinfunc=onalexpendituresinthefundstatementsneedtoremovetheappropriatecapitaladdi=onsfromthefunc=onalexpenditurestoreporttheaccrualbasedfunc=onalexpenses

– Contributedassetsarenotconsideredfundexpendituresorrevenuesandneedto“credit”appropriatecapitalcontribu=onrevenueac=vity

– Helpfultodis=nguishbetweenaddi=onsthatarecontributedversuspurchasedtoaidthereaderwhencomparingfundac=vi=es

6/22/16

24

70

CAFRPreparaKonCapitalAssets

• Disposalofcapitalassets-Repor=ngandcalcula=nggain/loss– Governmentsrou=nelyreportdisposalsofcapitalassets.Thisac=vity

isreportedinthedele=oncolumnofthefootnoteanditisimportanttoproperlyexplaininthereconcilia=onwhattypeofac=vitythisrepresentedduringtheyear

– Disposalsthemselvesarenotreportedinthegovernmentfundstatements

– Cashproceedsreceivedarereportedinthefundstatementsasotherfinancingsource

– Government-widepresenta=onreportdifferenceofbookvalueofdisposalandproceedsreceivedfromsaleofcapitalassetsasagain/lossonsaleofassets.Thelossisreportedasafunc=onalexpensewithintheproperfunc=onalrela=vetotheassetdisposedofandthegainistypicallyreportedasageneralrevenue

71

CAFRPreparaKonCapitalAssets

• Deprecia=on– Reconcilingamounttoagreetothefootnoteaddi=onfigure– Detailinfootnotetodisclosetheexpensebyfunc=on

72

CAFRPreparaKonLong-TermLiabiliKes

• Agenda– Reviewdisclosurerequirements– Presenta=onsugges=ons– Inter-rela=onshipsandaccuracychecks

6/22/16

25

73

CAFRPreparaKonLong-TermLiabiliKes

• CommonDisclosureRequirements(GASBCod.2300)– Shouldincludealllong-termliabili=es,includingcompensatedabsencesandclaimsandjudgments

– Tableofchanges– Amountduewithinoneyearofstatementdate– Whichgovernmentalfundstypicallyusedtoliquidateotherlong-termliabili=essuchascompensatedabsencesinprioryears

74

CAFRPreparaKonLong-TermLiabiliKes

• CommonDisclosureRequirements(GASBCod.2300)– Debtservicerequirementstomaturity–principalandinterest(variableratedebtshoulduserateinplaceatyearendanddisclosevariableratestructure)

– Debtrefunding– Interestrates,maturitydates,subordinatefeatures(generallyaccepted)

– Pledgedassetsandrestric=vecovenants(SFASNo.5)

75

CAFRPreparaKonLong-TermLiabiliKes

• ComponentUnitDisclosure(Cod.2300.115)– Uptoprofessionaljudgment– Basedoncomponentunit’ssignificancetototaldiscretelypresentedcomponentunitsandrela=onshiptoprimarygovernment

6/22/16

26

76

CAFRPreparaKonLong-TermLiabiliKes

• OtherSpecialDisclosure/Repor=ng– Bond,taxorrevenuean=cipa=onnotes– Specialassessmentdebt– Demandbonds– Conduitdebt

77

CAFRPreparaKonLong-TermLiabiliKes

• Presenta=onSugges=ons– Includetableofchangesatthebeginningofyourlong-termliabili=esfootnote

– Includealllongtermliabili=esinthesametable– Totaltheen=retableandreflectthatamountinyourreconcilia=on

78

CAFRPreparaKonLong-TermLiabiliKes

• Inter-rela=onshipsandaccuracychecks– UsesubtotalsinthetablethatwillagreedirectlytotheSONPandGovernmentalFundsStatementofRevenue,ExpendituresandChangesinFundBalance:

◊ Endingamounts–currentandlongterm=SONP◊ Newdebtissued=StatementofRevenue◊ PremiumsordiscountsshouldbeseparateOtherFinancingSource/Use=StatementofRevenue

◊ Principalpayments=StatementofRevenue◊ Lossonrefunding–disclosureshouldstateamountofprincipalrefunded

6/22/16

27

79

CAFRPreparaKonLong-TermLiabiliKes

• Inter-rela=onshipsandaccuracychecks– InternalServicefunddebt–eithershowseparatelyinfootnoteorinreconcilia=on,toagreetobalancesheet

80

CAFRPreparaKonRevenueRecogniKonandDeferredRevenue

• Agenda– Reviewstandards–modifiedaccrualversusaccrual– Rela=onship–government-widevs.governmentalfunds– Rela=onshiptoreconcilia=ons–governmentalfundsandgovernment-widestatements

81

CAFRPreparaKonRevenueRecogniKonandDeferredRevenue

• Standards–Modifiedaccrualbasis-GASBCodifica=on1600.106– Revenuesaretoberecognizedintheaccoun=ngperiodtheybecomebothmeasurableandavailabletofinanceexpendituresofthefiscalperiod

– Availablemeanscollec=blewithinthecurrentperiodorsoonenoughtherea+ertobeusedtopayliabili=esofthecurrentperiod

– Lengthof=meusedtodefineavailableshouldbedisclosedinthesummaryofsignificantaccoun=ngpolicies

6/22/16

28

82

CAFRPreparaKonRevenueRecogniKonandDeferredRevenue

• Standards–AICPAAccoun=ngandAuditGuide–StateandLocalGovernments6.12– Notesthatmanygovernmentsusethepropertytaxstandardandaccruebasedoncashreceivedduringadefinednumberofdaysa+eryearend

– Manygovernmentsapplythis=meperiodapproachforalltypesofrevenuesandinallgovernmentalfunds

– Paragraph6.13–Differencesbetweenamountreportedasreceivablesandtheamountsrecognizedasrevenuesarereportedasdeferredinflows(aliability)(PriortoGASB63&GASB65wascalleddeferredrevenues)

83

CAFRPreparaKonRevenueRecogniKonandDeferredRevenue• StandardsGenerally

– Measurabilityisusuallynottheproblem– Defining“available”istheproblem– Realkeytodefiningavailabilityiswhethersuchresourceswillbeusedtopayliabili=esofthecurrentperiod

84

CAFRPreparaKonRevenueRecogniKonandDeferredRevenue

• Rela=onship–government-widevs.governmentalfunds– Asauditorshaveseentwocommonproblems:

◊ Measurabletransac=onisrecordedasrevenueinbothpresenta=ons,regardlessofwhencashwasreceived

◊ Measurabletransac=onisdeferredinbothpresenta=ons,eventhoughaccrualbasisaccoun=ngclearlyrequiresrevenuerecogni=on

6/22/16

29

85

CAFRPreparaKonRevenueRecogniKonandDeferredRevenue

• Examples– Developmentfeestobepaidoveraperiodofseveralyears– Long-termnotesreceivable

• DisclosureExamples– Considerinclusionoffootnoteifextensivedifferencesexist

86

GASB–“ALottoGetOurArmsAround”

87

ExposureDracs/PreliminaryViews

• PreliminaryViews– Recogni=onofElementsofFinancialStatementsandMeasurementApproaches

– EconomicCondi=onRepor=ng:FinancialProjec=ons

6/22/16

30

88

GASB65–ItemsPreviouslyReportedasAssetsandLiabiliKes• Objec=veofthisStatementistodeterminewhethercertainbalancescurrentlyreportedasassetsandliabili=esshouldcon=nuetobereportedassuchorinsteadshouldbereportedas:– Adeferredoullowsofresources,or– Anoullowofresources(expense/expenditure);

• Or– Adeferredinflowsofresources,or– Aninflowsofresources(revenue).– Effec=veforperiodsbeginninga+erDecember15,2012.– EarlyApplica=onisencouraged.

89

ItemstobeReportedasDeferredOuVlows

• Transac=onsinwhichtheresul=ngitemshouldbeclassifiedasadeferredoullowofresources:– Resourcesadvancedtoanothergovernmentinrela=ontoagovernmentmandatednonexchangetransac=onoravoluntarynonexchangetransac=onwhen=merequirementsaretheonlyeligibilityrequirementsthathavenotbeenmetbytheothergovernment(paragraph19ofStatementNo.33,Accoun)ngandFinancialRepor)ngforNonexchangeTransac)ons).

90

ItemstobeReportedasDeferredOuVlows

• Transac=onsinwhichtheresul=ngitemshouldbeclassifiedasadeferredoullowofresources:– Deferredlossresul=ngfromsale-leasebacktransac=ons(paragraph242ofStatement62).

– Netbalance(debit)ofdirectloanorigina=oncosts,includinganypor=onrelatedtopoints,formortgageloansheldforresalepriortothepointofsale(paragraph467ofStatement62).

– Feespaidtopermanentinvestorstoensuretheul=matesaleofloanspriortothepointofsale(paragraph469ofStatement62).

6/22/16

31

91

ItemstobeReportedasanOuVlowofResources• Transac=onsinwhichtheresul=ngitemshouldberecognizedasanoullowofresources:– Acquisi=oncostsforinsuranceen==esandpublicen=tyriskpools(paragraphs28–30ofStatementNo.10,Accoun)ngandFinancialRepor)ngforRiskFinancingandRelatedInsuranceIssues,andparagraphs412–414ofStatement62).

– Ini=aldirectcostsincurredbythelessorforopera=ngleases(paragraph227ofStatement62).

– Debtissuancecosts(paragraph12ofStatementNo.7,AdvanceRefundingsResul)nginDefeasanceofDebt,andparagraph187ofStatement62).

92

ItemstobeReportedasanOuVlowofResources• Transac=onsinwhichtheresul=ngitemshouldberecognizedasanoullowofresources:– Netbalance(debit)ofdirectloanorigina=oncosts,includinganypor=onrelatedtopoints,relatedtolendingac=vi=es(paragraph45ofStatement10andparagraph434ofStatement62).

– Feespaidrelatedtoapurchasedloanoragroupofloans(paragraph442ofStatement62).

– Netbalance(debit)ofdirectloanorigina=oncosts,includinganypor=onrelatedtopoints,formortgageloansheldforinvestment(paragraph467ofStatement62).

93

ItemstobeReportedasanOuVlowofResources• Transac=onsinwhichtheresul=ngitemshouldberecognizedasanoullowofresources:– Netbalance(debit)ofdirectloanorigina=oncosts,includinganypor=onrelatedtopoints,relatedtolendingac=vi=es(paragraph45ofStatement10andparagraph434ofStatement62).

– Feespaidrelatedtoapurchasedloanoragroupofloans(paragraph442ofStatement62).

– Netbalance(debit)ofdirectloanorigina=oncosts,includinganypor=onrelatedtopoints,formortgageloansheldforinvestment(paragraph467ofStatement62).

– Feespaidtopermanentinvestorstoensuretheul=matesaleofloansa+ertheul=matesaleoccurs(paragraph469ofStatement62).

6/22/16

32

94

ItemstobeReportedasDeferredInflows

• Transac=onsinwhichtheresul=ngitemshouldbeclassifiedasadeferredinflowofresources:– Resourcesreceivedinadvanceinrela=ontoanimposednonexchangetransac=on(paragraph18ofStatement33).

– Resourcesreceivedinadvanceinrela=ontoagovernment-mandatednonexchangetransac=onoravoluntarynonexchangetransac=onwhen=merequirementsaretheonlyeligibilityrequirementsthathavenotbeenmetbythereceivinggovernment(paragraph19ofStatement33).

– Deferredcreditamountsresul=ngfromtherefundingofdebt(paragraph5ofStatement23,andparagraph221ofStatement62).

95

ItemstobeReportedasDeferredInflows

• Transac=onsinwhichtheresul=ngitemshouldbeclassifiedasadeferredinflowofresources:– Proceedsfromthesaleoffuturerevenues(paragraphs13–16ofStatement48).

– Unavailablerevenuerelatedtotheapplica=onofmodifiedaccrualaccoun=ng(StatementNo.6,Accoun)ngandFinancialRepor)ngforSpecialAssessments,andStatement33).

– Deferredgainresul=ngfromsale-leasebacktransac=ons(paragraph242ofStatement62).

– Netbalance(credit)ofloanorigina=onfees,excludinganypor=onrelatedtopoints,formortgageloansheldforresalepriortothepointofsale(paragraph467ofStatement62).

96

ItemstobeReportedasDeferredInflows

• Transac=onsinwhichtheresul=ngitemshouldbereportedasadeferredinflowofresources:– Netbalance(credit)ofloanorigina=onfeesrelatedtopointsforlendingac=vi=esandmortgageloansheldforinvestment(paragraph45ofStatement10andparagraphs434and467ofStatement62).

– Resourcesgeneratedbycurrentratesintendedtorecovercoststhatareexpectedtobeincurredinthefuture(paragraph482ofStatement62).

– Gainsorotherreduc=onsofnetallowablecostsintendedtoreduceratesoverfutureperiods(paragraph482ofStatement62).

6/22/16

33

97

ItemsreportedasInflowofResources

• Transac=onsinwhichtheresul=ngitemshouldberecognizedasaninflowofresources:– Netbalance(credit)ofloanorigina=onfees,excludinganypor=onrelatedtopoints,relatedtolendingac=vi=es(paragraph45ofStatement10andparagraph434ofStatement62).

– Commitmentfeesrealizeduponexerciseorexpira=onofthecommitment(paragraphs437and438ofStatement62).

– Commitmentfeeschargedforenteringintoanagreementthatobligatesthegovernmenttomakeoracquirealoanortosa=sfyanobliga=onoftheotherpartyunderaspecifiedcondi=onwhenexerciseisconsideredremote(paragraphs437and438ofStatement62).

98

ItemsreportedasInflowofResources

• Transac=onsinwhichtheresul=ngitemshouldberecognizedasaninflowofresources:– Feesreceivedrelatedtoapurchasedloanoragroupofloans(paragraph442ofStatement62).

– Netbalance(credit)ofloanorigina=onfees,excludinganypor=onrelatedtopoints,formortgageloansheldforinvestment(paragraph467ofStatement62)

– Netbalance(credit)ofloanorigina=onfees,includinganypor=onrelatedtopoints,formortgageloansheldforresalea+erthesaleoccurs(paragraph467ofStatement62)

99

ItemsreportedasInflowofResources

• Transac=onsinwhichtheresul=ngitemshouldberecognizedasaninflowofresources:– Feesthatarerealizeda+erthefundingofmortgageloanshasoccurredora+erthecommitmenttoguaranteethefundingofmortgageloansexpires(paragraph469ofStatement62)

– Feesrealizedwhenacommitmentisarrangeddirectlybetweenapermanentinvestorandaborrower(paragraph470ofStatement62)

6/22/16

34

100

RevenueRecogniKoninGovernmentalFunds

• Revenuesandothergovernmentalfundfinancialresourcesshouldberecognizedintheaccoun=ngperiodinwhichtheybecomebothmeasurableandavailable(NCGAStatement1,paragraph62).

• Whenanassetisrecordedingovernmentalfundfinancialstatementsbuttherevenueisnotavailable,thegovernmentshouldreportadeferredinflowofresourcesunKlsuchKmeastherevenuebecomesavailable.

101

OtherAreasAddressedbyGASB65

• Useofthetermdeferredshouldbelimitedtodeferredinflowsanddeferredoullowsofresources

• Majorfundcalcula=onguidancewillbeamended:– Useaggregateassets/deferredoullowsandaggregateliabili=es/deferredinflowsinthecalcula=on

102

GASB67and68

• Accoun=ngandFinancialRepor=ngforPensions–anamendmenttoGASB27– Changestotheseagentemployerswouldbeasfollows:

◊ Recognizeanetpensionliability(accrualbasis)◊ Netpensionliability=employer’stotalpensionliabilitylesstheamountofplannetposi=onrestrictedforpensions(plannetposi=on),asoftheendoftheemployer’srepor=ngperiod.

6/22/16

35

103

GASB67and68

• Accoun=ngandFinancialRepor=ngforPensions–anamendmenttoGASB27(con=nued)– Disclosurerequirements:

◊ Forthecurrentyear,changesinthenetpensionliability◊ Significantassump=onsusedtocalculatethetotalpensionliability,includingassump=onsusedincalcula=onthediscountamount

◊ Thedateoftheunderlyingactuarialvalua=on,informa=onaboutchangesofassump=onsandbenefitterms

◊ Thebasisfordeterminingtheemployercontribu=onstotheplan◊ Theindividualcomponentsofthecurrent-periodpensionexpense

104

GASB67and68

• Accoun=ngandFinancialRepor=ngforPensions–anamendmenttoGASB27(con=nued)– Disclosurerequirements(con=nued):

◊ Explana=onsofchangesinthedeferredoullowsofresourcesanddeferredinflowsofresourcesrelatedtopensionsduringthecurrentperiod

◊ Descrip=onoftheplan◊ Numberofgovernmentspar=cipa=ngintheplan◊ Classesofemployeescovered◊ Numberofre=redemployeesreceivingbenefits◊ Numberofinac=veemployeesen=tledbutnotyetreceivingbenefits

◊ Numberofac=veemployees

105

GASB67and68

• Accoun=ngandFinancialRepor=ngforPensions–anamendmenttoGASB27(con=nued)– RequiredSupplementaryInforma=on:

◊ Changesinthenetpensionliability◊ Informa=onaboutthecomponentsofthenetpensionliabilityandrelatedra=osasoftheemployer’syear-end• Totalpensionliability• Amountofplannetposi=on• Netpensionliability• Plannetposi=onas%ofthetotalpensionliability• Amountofcovered-employeepayroll• Netpensionliabilityasa%ofcovered-employeepayroll

6/22/16

36

106

StatementNo.69

• GovernmentCombina.onsandDisposalsofGovernmentOpera.onsEffec=veDate:TheprovisionsofStatement69areeffec=veforgovernmentcombina=onsanddisposalsofgovernmentopera=onsoccurringinfinancialrepor=ngperiodsbeginninga+erDecember15,2013,andshouldbeappliedonaprospec=vebasis.

107

Statement70

Accoun.ngandFinancialRepor.ngforNonexchangeFinancialGuaranteesEffec=veDate:TheprovisionsofStatement70areeffec=veforfinancialstatementsforrepor=ngbeginninga+erJune15,2013.

108

StatementNo.71• PensionTransi.onforContribu.onsMadeSubsequenttotheMeasurementDate—anamendmentofGASBStatementNo.68Effec=veDate:TheprovisionsofthisStatementshouldbeappliedsimultaneouslywiththeprovisionsofStatement68.

6/22/16

37

109

StatementNo.72

FairValueMeasurementandApplica.onEffec=veDate:TherequirementsofthisStatementareeffec=veforfinancialstatementsforrepor=ngperiodsbeginninga+erJune15,2015.

110

StatementNo.73• Accoun.ngandFinancialRepor.ngforPensionsandRelatedAssetsThatAreNotwithintheScopeofGASBStatement68,andAmendmentstoCertainProvisionsofGASBStatements67and68Effec=veDate:TheprovisionsinStatement73areeffec=veforfiscalyearsbeginninga+erJune15,2015—exceptthoseprovisionsthataddressemployersandgovernmentalnonemployercontribu=ngen==esforpensionsthatarenotwithinthescopeofStatement68,whichareeffec=veforfiscalyearsbeginninga+erJune15,2016.Earlierapplica=onisencouraged.

111

Statements74and75

• StatementNo.74FinancialRepor.ngforPostemploymentBenefitPlansOtherThanPensionPlansEffec=veDate:TheprovisionsinStatement74areeffec=veforfiscalyearsbeginninga+erJune15,2016.Earlierapplica=onisencouraged.

• StatementNo.75Accoun.ngandFinancialRepor.ngforPostemploymentBenefitsOtherThanPensionsEffec=veDate:TheprovisionsinStatement75areeffec=veforfiscalyearsbeginninga+erJune15,2017.Earlierapplica=onisencouraged.

6/22/16

38

112

Statements76and77

• GASBStatementNo.76,TheHierarchyofGenerallyAcceptedAccoun.ngPrinciplesforStateandLocalGovernmentsEffec=veDate:TheprovisionsinStatement76areeffec=veforrepor=ngperiodsbeginninga+erJune15,2015.Earlierapplica=onisencouraged.

• GASBStatementNo.77,TaxAbatementDisclosuresEffec=veDate:TherequirementsofthisStatementareeffec=veforrepor=ngperiodsbeginninga+erDecember15,2015.Earlierapplica=onisencouraged.

113

Statements78and79

• GASBStatementNo.78,PensionsProvidedthroughCertainMul.ple-EmployerDefinedBenefitPensionPlansEffec=veDate:TherequirementsofthisStatementareeffec=veforrepor=ngperiodsbeginninga+erDecember15,2015.

• GASBStatementNo.79,CertainExternalInvestmentPoolsandPoolPar.cipantsEffec=veDate:TherequirementsofthisStatementareeffec=veforrepor=ngperiodsbeginninga+erJune15,2015,exceptfortheprovisionsinparagraphs18,19,23–26,and40,whichareeffec=veforrepor=ngperiodsbeginninga+erDecember15,2015..

114

Statements80and81

• GASBStatementNo.80,BlendingRequirementsforCertainComponentUnits—anamendmentofGASBStatementNo.14Effec=veDate:TherequirementsofthisStatementareeffec=veforrepor=ngperiodsbeginninga+erJune15,2016.Earlierapplica=onisencouraged.

• GASBStatementNo.81,IrrevocableSplit-InterestAgreementsEffec=veDate:TherequirementsofthisStatementareeffec=veforperiodsbeginninga+erDecember15,2016.Earlierapplica=onisencouraged.

6/22/16

39

115

GASBStatementNo.82,

PensionIssues—anamendmentofGASBStatementsNo.67,No.68,andNo.73Effec=veDate:TherequirementsofthisStatementareeffec=veforrepor=ngperiodsbeginninga+erJune15,2016,exceptfortherequirementsofparagraph7inacircumstanceinwhichanemployer’spensionliabilityismeasuredasofadateotherthantheemployer’smostrecentfiscalyear-end.Inthatcircumstance,therequirementsofparagraph7areeffec=veforthatemployerinthefirstrepor=ngperiodinwhichthemeasurementdateofthepensionliabilityisonora+erJune15,2017.Earlierapplica=onisencouraged.

116

IssuesUniquetoColoradoGovernments

• BudgetRepor=ngRequirements• TABOR

117

BudgetReporKngRequirements

• CRS92-1-103requireseachlocalgovernmenttoadoptanannualbudget.Totheextentthatthefinancialac=vi=esofanylocalgovernmentarefullyreportedinthebudgetorbudgetsofaparentlocalgovernmentorgovernments,aseparatebudgetisnotrequired.Suchbudgetshallpresentacompletefinancialplanbyfundandbyspendingagencywithineachfundforthebudgetyear.

6/22/16

40

118

TABOR

• TheTABORamendmentwasapprovedbyColoradovotersin1992.TABORplaceslimitsonrevenue,spending,anddebtwhichmaybeweakenedonlybytheapprovalofthevoters.

119

TABOR

• TABORrequirestheestablishmentof“emergencyreserves…tousefordeclaredemergenciesonly”,amoun=ngto“3%ormoreofitsfiscalyearspendingexcludingbondeddebtservice”.[TABOR(5)]

120

TABOR

• “Fiscalyearspendingmeansalldistrictexpendituresandreserveincreasesexcept,astoboth,refundsmadeinthecurrentornextfiscalyearorthosefromgi+s,federalfunds,collec=onsforanothergovernment,pensioncontribu=onsbyemployeesandpensionfundearnings,reservetransfersorexpenditures,damageawards,orpropertysales”.[TABOR(2)(e)]

6/22/16

41

121

TABOR

• Theterm“reserve”inthedefini=onoffiscalyearspendingreferstofundbalances,and“reservetransfersorexpenditures”meansmoneyswhicharepassedfromonefundofcashorassetsheldasareservetoanothersuchfundormoneyswhicharedisbursedfromsuchfund.[C.R.S.24-77-102(12-14)]

122

ManagementProcess

• To-Do’sforManagers– Plan– Perform– Evaluate– Communicate

123

ManagementProcessOverviewofthePlanningFramework

• Goal/Vision:Toincreasethevalueofstakeholders’interestintheorganiza=on

• Mission:Fundamentalwayinwhichtheen=tywillachievethegoalofincreasingstakeholders’value

• StrategicObjecKves:Broad,long-termgoalsthatdeterminethefundamentalnatureanddirec=onofthebusinessandthatserveasaguidefordecisionmaking

6/22/16

42

124

ManagementProcessOverviewofthePlanningFramework

• TacKcalObjecKves:Mid-termgoalsforposi=oningtheorganiza=ontoachieveitslong-termstrategies.

• OperaKngObjecKves:Short-termgoalsthatoutlineexpecta=onsforperformanceofday-to-dayopera=ons

• BusinessPlan:Acomprehensivestatementofhowtheorganiza=onwillachieveitsobjec=ves

• Budgets:Expressionsofthebusinessplaninfinancialterms.

125

ManagementCycle

Plan

Perform

Evaluate

Communicate

126

ManagerialReporKng

• ManagementorManagerialAccoun=ngcanuseinnova=veanalysesandpresenta=ontechniquestoenhancetheusefulnessofinforma=ontopeoplewithinthegovernmenten=ty.

6/22/16

43

127

ManagementVs.FinancialAccounKng

ManagementAccounKng FinancialAccounKng

PrimaryUsers Managers,employees Lenders,governmental agencies,public

ReportFormat Flexible,drivenbyuser's BasedonGAAP

needs

PurposeofReports Provideinforma=onfor Reportonpast planning,control, performance

performancemeasurement &decisionmaking

128

ManagementVs.FinancialAccounKngManagementAccounting FinancialAccounting

Natureof Objectiveandverifiablefor ObjectiveandInformation decisionmaking;more verifiable

subjectiveforplanning(reliesonestimates)

UnitsofMeasure Monetaryathistoricalor Monetaryathistoricalcurrentmarketor andcurrentmarketprojectedvalues;physical valuesmeasuresoftimeornumberofobjects

Frequencyof Preparedasneeded;mayor PreparedonaperiodicReports maynotbeonaperiodic basis

basis

129

AnalysisforDecisionMaking

• Short-runDecisionAnalysisisthesystema=cexamina=onofanymanagementdecisionwhoseeffectswillbefeltoverthecourseofthenextyear.– Planning:

◊ Discovertheproblemorneed◊ Iden=fyallreasonablecoursesofac=onthatcansolvetheproblemormeettheneed

6/22/16

44

130

ConKnue:Short-RunDecisionAnalysis

– Planning◊ Prepareathoroughanalysisofeachpossiblesolu=onandiden=fyitstotalcosts,savings,otherfinancialeffects,andanyqualita=vefactors.

◊ Selectthebestcourseofac=on

◊ Con=nuethroughthemanagementcycle.

131

IncrementalAnalysisforShort-RunDecisions

• IrrelevantCostsandRevenuesarethosethatwillnotdifferbetweenthealterna=ves.

• DifferenKalCostsandRevenues(incrementalcosts)arethosethatchangebetweenalterna=ves.

• Firststepinincrementalanalysisistoeliminateanyirrelevantrevenuesorcosts.

132

IncrementalAnalysisforShort-RunDecisions

• OpportunityCostsarethebenefitsthatareforfeitedorlostwhenonealterna=veischosenoveranother.

• Outsourcingistheuseofsuppliersoutsidetheorganiza=ontoperformservicesorproducegoodsthatcouldbeperformedorproducedinternally.

6/22/16

45

133

• KeeporDropunprofitable(unproduc=ve,under-achieving)segments,divisions,orservices.

• SellorProcess-Furtherisadecisionaboutwhethertosellajointproductatthesplit-offpointorsellita+erfurtherprocessing.Ingovernment,thisisnotsomuchasselling,butprovidingtheservice.

IncrementalAnalysisforShort-RunDecisions

134

CapitalInvestmentAnalysis

• Processofmakingdecisionsaboutcapitalinvestments.Consistsofiden=fyingtheneed,analyzingcoursesofac=ontomeetthatneed,preparingreportsformanagers,choosingthebestalterna=ve,andalloca=ngfundsamongcompe=ngneeds.

135

MeasuresUsedinCapitalInvestmentAnalysis

• NetIncomeandNetCashInflowsareameanstomeasurethebenefitifinvolvescashreceipts.

• CostSavingsmeasurethebenefits,suchasreducedcosts,fromproposedcapitalinvestments.

• TimeValueofMoneyshouldbeusedindecisionmaking(PresentValueandFutureValue)

6/22/16

46

136

MeasuresUsedinCapitalInvestmentAnalysis

• PaybackPeriodMethoddeterminestheminimum=meitwilltaketorecovertheini=alinvestment.

– Paybackperiod=CostofInvestment

– AnnualNetCashInflows

137

HelpfulWebsites

• GovernmentalAccoun=ngStandardsBoardhcp://gasb.org/

• GovernmentFinanceOfficersAssocia=on hcp://www.gfoa.org/

• ColoradoGovernmentFinanceOfficerAssocia=onhcp://www.cgfoa.org/

[email protected]