30

INTERNATIONAL EXPERIENCE IN INNOVATIONS IN METRO RAIL Gerald Ollivier Transport Cluster Leader Singapore, World Bank

INTERNATIONAL EXPERIENCE ININNOVATIONS IN METRO RAIL

Gerald OllivierTransport Cluster Leader

Singapore, World Bank

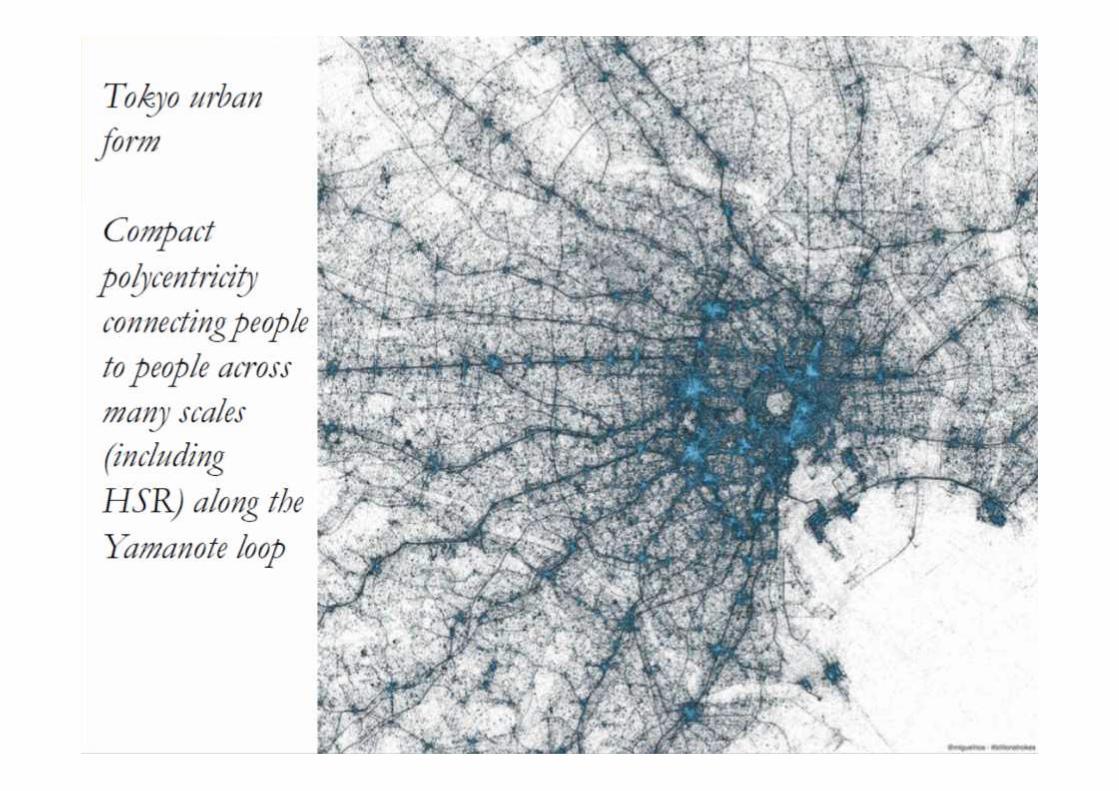

Innovation 1: Density Aligned withTransit

From Serge Salat

London’s Jobs densities are clearlyclustered around subway stations

Source: Urban Morphology Institute (2015)

Population Density (London)

Source: Urban Morphology Institute (2015)

Innovation 2: TOD-Land ValueCapture Typology of Stations

• Node Value based on itslocation in the network

• Place Value based on itsurban qualities

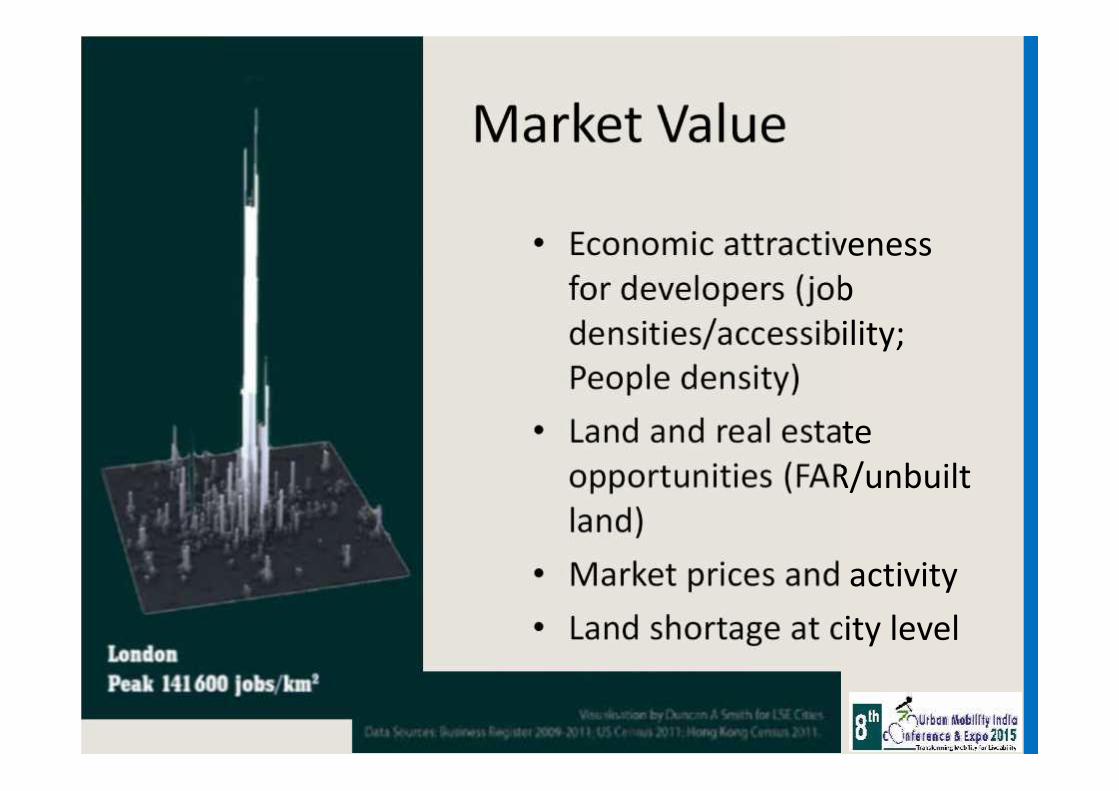

• Market Value, based onits economic potential

The “3V Framework”

The 3V Framework (Serge Salat, Gerald Ollivier)

• Hub, Interchange, Single station• Diversity of connectivity• Node Accessibility/Centrality• Intensity of node activity

Node Value (London Tube)

0

10

20

30

40

50

60

70

80

90

Mill

ion

peop

le /

yea

r

Rank

Source: Urban Morphology Institute

0

50

100

150

200

250

1 2 3 4 5 6

Num

ber o

f sta

tions

Number of lines per station

• Mix of land uses• Density of social

infrastructure• Compactness• Physical form

and streetpatterns

• Walkability andbikability

Place Value

Source: Urban Morphology Institute

• Economic attractivenessfor developers (jobdensities/accessibility;People density)

• Land and real estateopportunities (FAR/unbuiltland)

• Market prices and activity• Land shortage at city level

Market Value

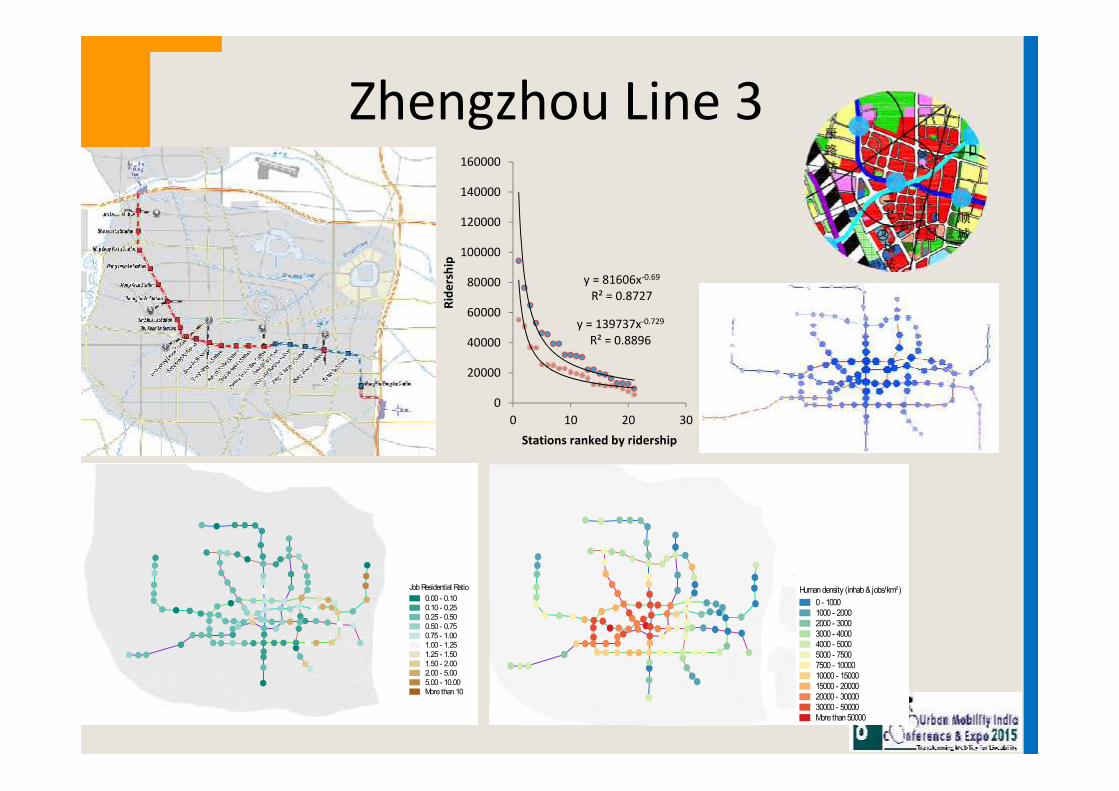

y = 81606x-0.69

R² = 0.8727

y = 139737x-0.729

R² = 0.8896

0

20000

40000

60000

80000

100000

120000

140000

160000

0 10 20 30

Ride

rshi

pStations ranked by ridership

Humandensity (inhab& jobs/km²)0 - 10001000 - 20002000 - 30003000 - 40004000 - 50005000 - 75007500 - 1000010000 - 1500015000 - 2000020000 - 3000030000 - 50000More than50000

JobResidential Ratio0.00 - 0.100.10 - 0.250.25 - 0.500.50 - 0.750.75 - 1.001.00 - 1.251.25 - 1.501.50 - 2.002.00 - 5.005.00 - 10.00More than10

Zhengzhou Line 3

Results in Zhengzhou Line 3

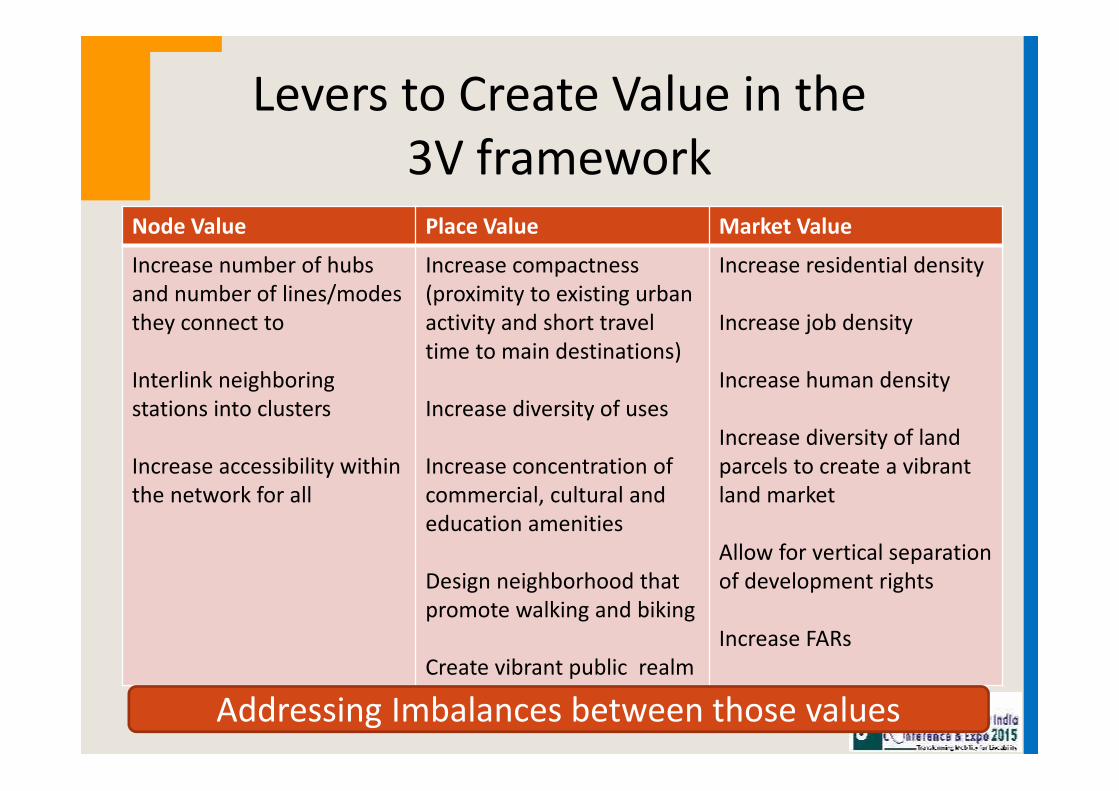

Node Value Place Value Market Value

Increase number of hubsand number of lines/modesthey connect to

Interlink neighboringstations into clusters

Increase accessibility withinthe network for all

Increase compactness(proximity to existing urbanactivity and short traveltime to main destinations)

Increase diversity of uses

Increase concentration ofcommercial, cultural andeducation amenities

Design neighborhood thatpromote walking and biking

Create vibrant public realm

Increase residential density

Increase job density

Increase human density

Increase diversity of landparcels to create a vibrantland market

Allow for vertical separationof development rights

Increase FARs

Levers to Create Value in the3V framework

Addressing Imbalances between those values

Innovation 3: Look at accessibilitywith open data (GTFS) and open tools

(Open Transit Indicators)

Zhengzhou Urban Transport

Transit Level of Service IndicatorsBasic Transit System Indicators

• Average headway/frequency• Number of service hours• On-time performance• 平均发车频率• 服务时长• 准点性能评价

Service Schedule服务时间• Number of stops• Average distance between

stops• 公交站点总数• 平均站点间距

Stops站点• Number of modes• Total length of transit routes• 公交模式数量• 公交线路总长

Routes线路

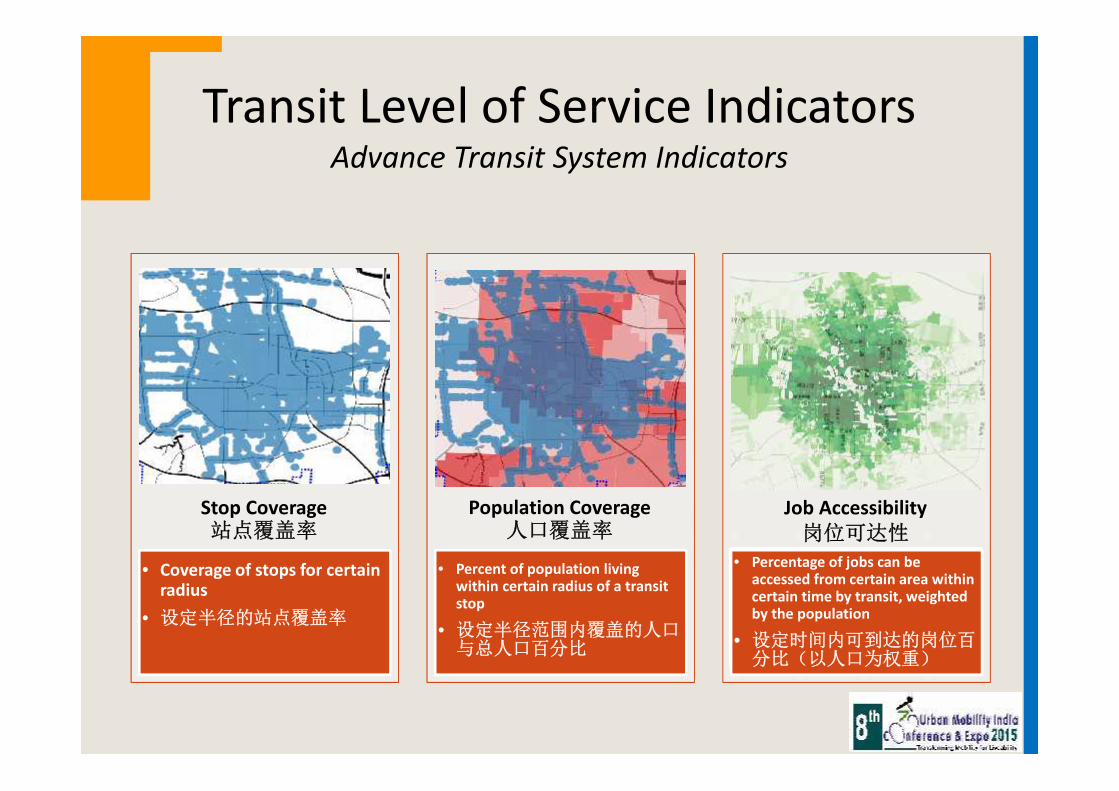

Transit Level of Service IndicatorsAdvance Transit System Indicators

• Coverage of stops for certainradius

• 设定半径的站点覆盖率

Stop Coverage站点覆盖率

• Percent of population livingwithin certain radius of a transitstop

• 设定半径范围内覆盖的人口与总人口百分比

Population Coverage人口覆盖率

• Percentage of jobs can beaccessed from certain area withincertain time by transit, weightedby the population

• Percentage of jobs can beaccessed from certain area withincertain time by transit, weightedby the population

• 设定时间内可到达的岗位百分比(以人口为权重)

Job Accessibility岗位可达性

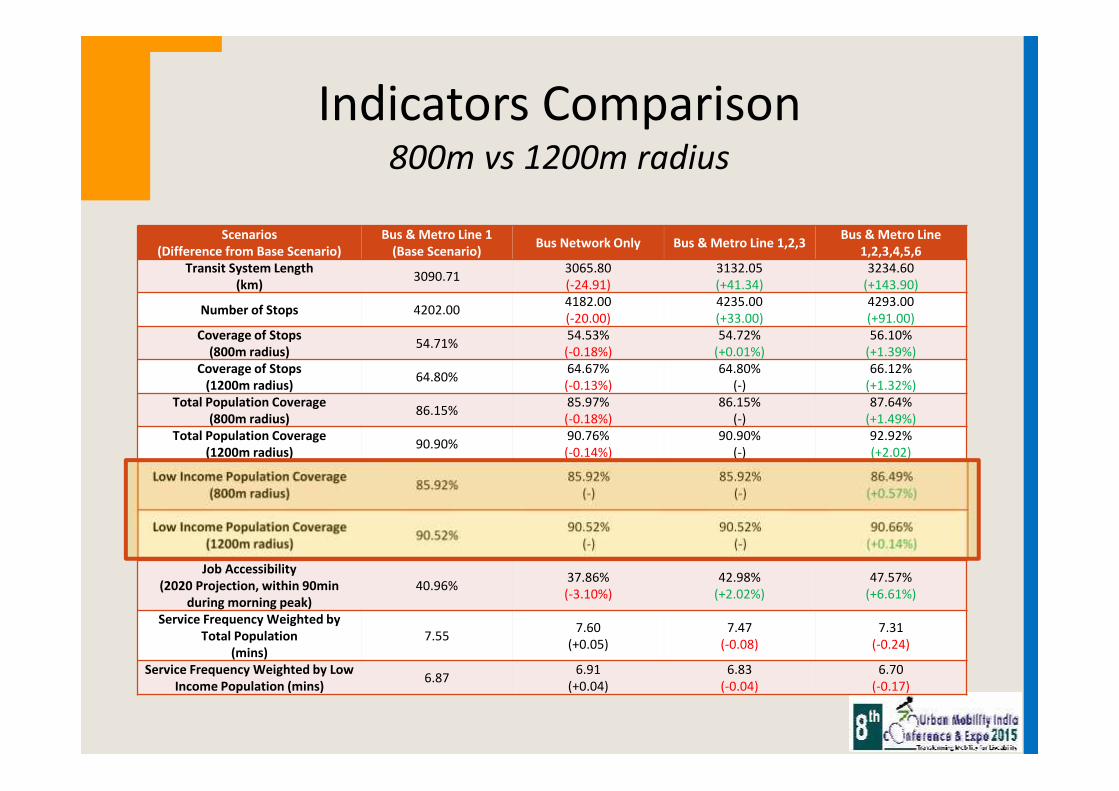

Scenarios(Difference from Base Scenario)

Bus & Metro Line 1(Base Scenario) Bus Network Only Bus & Metro Line 1,2,3 Bus & Metro Line

1,2,3,4,5,6Transit System Length

(km) 3090.71 3065.80(-24.91)

3132.05(+41.34)

3234.60(+143.90)

Number of Stops 4202.00 4182.00(-20.00)

4235.00(+33.00)

4293.00(+91.00)

Coverage of Stops(800m radius) 54.71% 54.53%

(-0.18%)54.72%

(+0.01%)56.10%

(+1.39%)Coverage of Stops

(1200m radius) 64.80% 64.67%(-0.13%)

64.80%(-)

66.12%(+1.32%)

Total Population Coverage(800m radius) 86.15% 85.97%

(-0.18%)86.15%

(-)87.64%

(+1.49%)Total Population Coverage

(1200m radius) 90.90% 90.76%(-0.14%)

90.90%(-)

92.92%(+2.02)

Low Income Population Coverage(800m radius) 85.92% 85.92%

(-)85.92%

(-)86.49%

(+0.57%)

Low Income Population Coverage(1200m radius) 90.52% 90.52%

(-)90.52%

(-)90.66%

(+0.14%)

Job Accessibility(2020 Projection, within 90min

during morning peak)40.96% 37.86%

(-3.10%)42.98%

(+2.02%)47.57%

(+6.61%)

Service Frequency Weighted byTotal Population

(mins)7.55 7.60

(+0.05)7.47

(-0.08)7.31

(-0.24)

Service Frequency Weighted by LowIncome Population (mins) 6.87 6.91

(+0.04)6.83

(-0.04)6.70

(-0.17)

Indicators Comparison800m vs 1200m radius

Accessibility for the Poor

Innovation 4: PPP Financing

From George Darido

PPP Example: Lima Metro 2:Project Financing Sources

• Government of Peru will finance its contribution towards the PPP frombudgetary resources and loans provided by International FinancialInstitutions (IFIs).

• World Bank (IBRD) loan for US$ 300 million approved on September 15, 2015(P145610)

US$ million % of FinancingTotal Public Financing by GoP 4,185 71.7%Total Foreign Debt 1,900 32.6%IBRD (2015) 300 5.2%IADB 300 5.2%CAF 150 2.5%Other/future IFI loans 1150 19.7%Public Treasury 2,285 39.1%Concessionaire (Private Financing) 1,651 28.3%Total Estimated Cost 5,836 100%

Risk MatrixRisk Type Public, Private or Shared RiskDemand Public assumes all fare revenue risk and must develop and implement a public

transport reorganization plan.Land Acquisition andResettlement

100% Public, must provide required land to the concessionaire “free and clear”

Design 100% Private, must meet all requirements and obtain required approvalsInterferences and utilities • Private is responsible for all known utility relocation, geological conditions

and other related interferences.• Public is responsible for all unknown utility relocation, geological conditions

and chance archeological finds.Construction and Financing Private responsible for all costs and time overruns under its responsibility (input

costs, availability of material and equipment, design or implementationproblems, environmental requirements, etc).

Operational Performance • Private must meet level of service requirements or is penalized.• Private receives a minimum annual operations payment but Gov’t may

regulate level of service above this.Ancillary revenues Shared: gross revenues to be split between Public and Private on all advertising,

commercial leasing and other services within concession areas (stations andimmediate surroundings) with approval by Granting Authority.

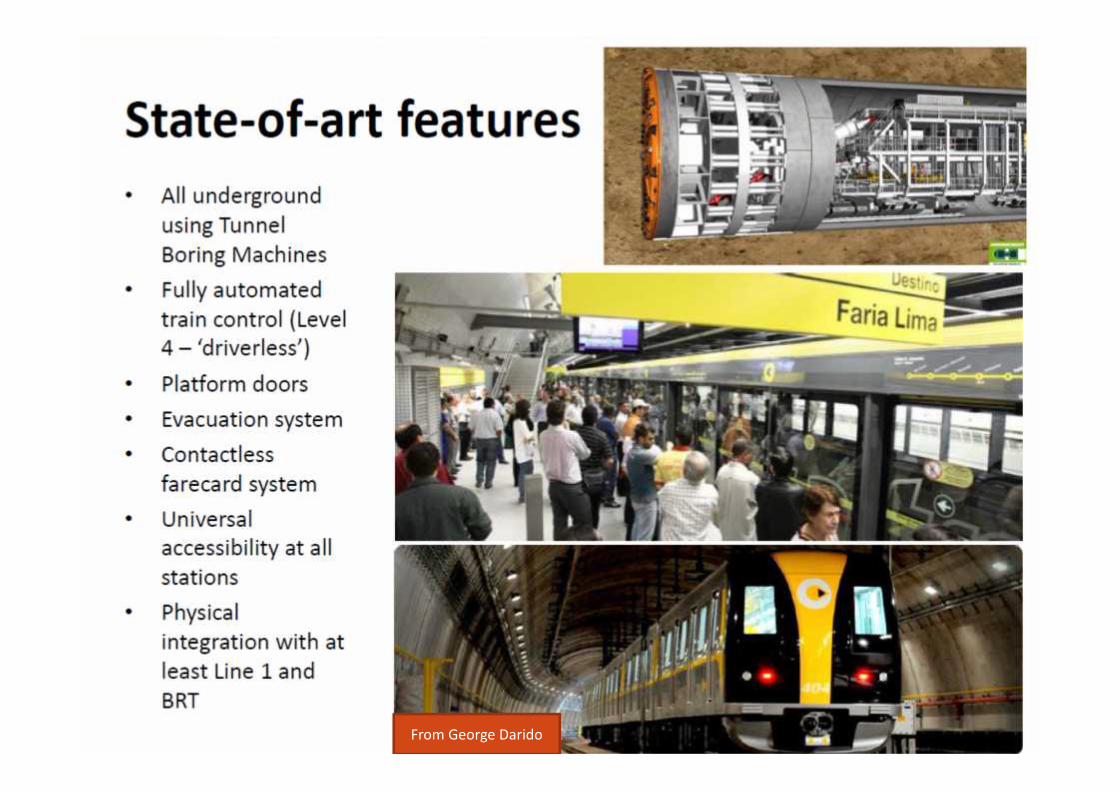

Innovation 5: Technology

From George Darido