32

International Financial Services Centre India’s 1 st IFSC in GIFT City Gujarat

International Financial Services CentreIndia’s 1st IFSC in GIFT City Gujarat

GIFT City: Highlights

• Strategic Location12 kms from Ahmedabad International Airport (8th

busiest in India)

• Global Financial and IT Hub with a domestic tariff area and a multi services SEZ

• Globally benchmarked(International Financial Services Centre)

• Greenfield Smart City with state-of-the-art infrastructure

• Vertical City1st of its kind in the country in scale, scope, and quality

With a total area of 673 acres, GIFT city is home to 225+ companies and employs 10,000+ people

International Financial Services Centre Authority (IFSCA)

*RBI- Reserve Bank of India, *SEBI- Securities and Exchange Board of India, *IRDAI- Insurance Regulatory and Development Authority & *PFRDA- Pension Fund Regulatory and Development Authority

IFSCA has been established as a unified financial regulator by the Government of India under the

IFSCA Act, 2019

The Authority is mandated to develop and regulate Financial Institutions, Financial Services and Financial Products in the

International Financial Services Centre (IFSC) in India

To develop and regulate IFSC’s in India, IFSCA has been vested

with powers of four Indian regulators namely- RBI, SEBI,

IRDAI & PFRDA

IFSC: Potential & Opportunities

Huge Domestic Demand for

Financial Services

Connecting ~30 Mn strong Indian

diasporaAccess to large

hinterland economy

Inbound & Outbound Gateway for Financial Services

IFSC is emerging as a leading Fund

Destination

IFSC Units are considered person resident outside India under the Foreign Exchange Management Act

Potential of IFSC in India Opportunities at IFSC GIFT City

BANKS

● Indian banks

● Foreign banks

CAPITAL MARKET

● Stock/Commodity

Exchanges

● Clearing Corporation

● Depository

● Depository Participant

● Broker

INSURANCE

● Indian & Foreign

Insurer

● Indian & Foreign

Reinsurer

● Indian & Foreign

Intermediaries

Emerging Business

Segments

● Global inhouse centres

● International Bullion

Exchange

● Aircraft Leasing & Financing

● Global Fintech Hub

● Finance Company

● Ancillary Services

ASSET MANAGEMENT

● Alternate Investment Fund

● Investment Advisers

● Wealth Management

● Portfolio Manager

● Custodial Services

● Mutual Funds

IFSC GIFT City: Tax RegimeThe latest Global Financial Centers Index, London (Sep 2020) puts IFSC at GIFT City at the top amongst 15 centers globally, which are likely to gain greater significance in next 24 months

100% Tax Exemption (for

10 out of 15 years)

Minimum Alternate Tax1

@0%

No CTT/STT/GST/S

tamp Duty

No Capital Gain Tax

Withholding tax @4% on interest paid

on Debt Instruments

Competitive AIF Tax Regime

1Concessional Rate of MAT applicable for IFSC units at 9%, however MAT provisions not applicable for companies opting for concessional tax rate under Sec. 115 BAA of Income Tax Act, 1961.

Tax Regime Presence in IFSC GIFT City

IFSC: Business Opportunities

BankingInternational

Bullion Exchange Alternate

Investment Funds (AIF)

Aircraft leasing & Financing

Capital Markets FinTech HubGlobal Inhouse Centers (GIC)

Insurance & Reinsurance

Alternative Investment Funds (AIFs)

AIFS in IFSC- Benefits (1/4)

01

03

0405

IFSC AIFs

Opportunity to set up an offshore presence at reasonable cost

Potential to benefit from newer opportunities as regulatory framework for asset management evolves

AIFs in IFSC offer viable alternatives to offshore feeder funds/ FPIs

Income Tax holiday for fund manager for 10 years

Leverage, co-investment permissible; diversification norms not applicable to IFSC AIFs

Savings in GST on management fees leading to competitive advantage

For Category III AIFs - No capital gain tax on specified securities and concessional tax regime on regular income

07

06 02

Lower operating costs coupled with regulatory relaxations makes IFSC a preferred destination for funds

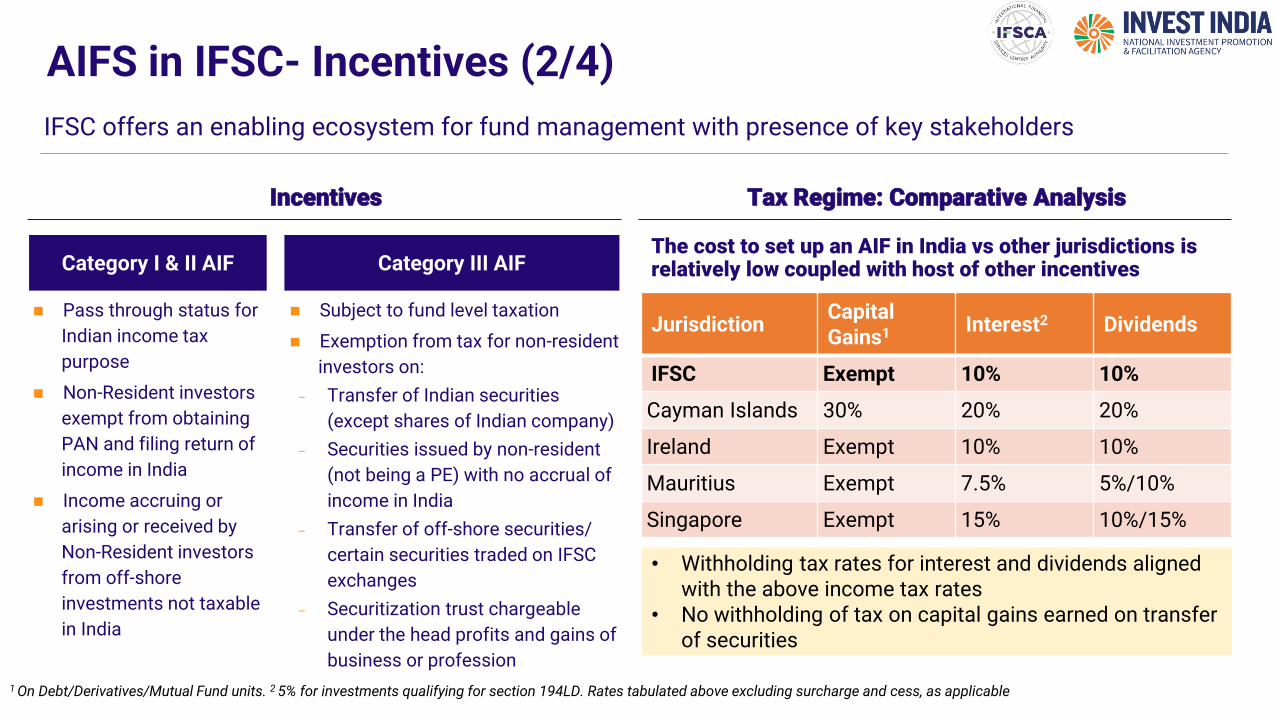

AIFS in IFSC- Incentives (2/4)

Tax Regime: Comparative Analysis

JurisdictionCapital Gains1 Interest2 Dividends

IFSC Exempt 10% 10%

Cayman Islands 30% 20% 20%

Ireland Exempt 10% 10%

Mauritius Exempt 7.5% 5%/10%

Singapore Exempt 15% 10%/15%

The cost to set up an AIF in India vs other jurisdictions is relatively low coupled with host of other incentives

• Withholding tax rates for interest and dividends aligned with the above income tax rates

• No withholding of tax on capital gains earned on transfer of securities

1 On Debt/Derivatives/Mutual Fund units. 2 5% for investments qualifying for section 194LD. Rates tabulated above excluding surcharge and cess, as applicable

Incentives

Category I & II AIF Category III AIF

◼ Pass through status for

Indian income tax

purpose

◼ Non-Resident investors

exempt from obtaining

PAN and filing return of

income in India

◼ Income accruing or

arising or received by

Non-Resident investors

from off-shore

investments not taxable

in India

◼ Subject to fund level taxation

◼ Exemption from tax for non-resident

investors on:

- Transfer of Indian securities

(except shares of Indian company)

- Securities issued by non-resident

(not being a PE) with no accrual of

income in India

- Transfer of off-shore securities/

certain securities traded on IFSC

exchanges

- Securitization trust chargeable

under the head profits and gains of

business or profession

IFSC offers an enabling ecosystem for fund management with presence of key stakeholders

Inbound Investments - AIFs in IFSC (3/4)

Outbound Investments - AIFs in IFSC (4/4)

Banking

Banking in IFSC (1/3)

The IFSCA Banking regulations supersede the RBI IBU guidelines

Key BenefitsOverview

Indian and Foreign Bans can set-up an IBU as a

branch-

● Foreign Banks not having presence in India may

also be permitted to set up an IBU

● Foreign Banks can also set up representative

offices in IFSC

Parent bank to satisfy the following conditions for

IBU branch license:

● Provide a minimum capital of US$20 million to

IBU, which shall be always maintained on an

unimpaired basis

● Submit ‘No objection’ letter from its home

regulator for setting up IBU in IFSC

● Submit an undertaking to provide liquidity to IBU,

whenever needed.

Exemption from CRR / SLR / PSL requirements

Capital to be maintained at HO level

Borrower limits to apply as per Parent’s Capital

Tax exemption in respect of interest paid to non-residents

Income earned on transfer of Non-deliverable derivative contracts by non-resident is exempt from tax

Interest on deposits exempt in respect of Non-Residents and Persons Not Ordinarily Resident as well

Banking in IFSC (2/3)

Permissible ActivitiesBusiness Opportunities in IBU

◼ Investment in Global Securities

◼ Money market operations such as Repo and

enhance yield/ lower borrowing

◼ Ease of Raising Capital & Liquidity such as

Perpetual Debt Issuances, Deposits and other

liabilities

◼ Trading Member on IFSC exchanges for interest

rate and currency derivatives segments

◼ Arbitrage between NDFs and currency derivatives

◼ Merchant Banking

◼ Bullion Depository Receipt Financing

◼ Credit insurance

◼ Portfolio Management Services, Investment

Advisory, Client FPI accounts

◼ Lending to AIFs

Deposits

◼ Retail

◼ Corporate

Lending/Investment Products

◼ Loans, trade finances and acceptances,

commitments and guarantees

◼ Credit enhancement, credit insurance

Derivative Products

◼ Over the counter (OTC) derivative contracts

◼ Non-deliverable forwards (NDFs)

Transaction Banking

◼ Trade assets and contingencies

◼ Escrow accounts services

16+ Banks have presence in IFSC GIFT City carrying a wide spectrum of activities

Banking in IFSC (3/3)

IBUs have prudent regulatory requirements for funding ratios and reserve requirements

Maintenance of Ratios

◼ IBUs to maintain LCR and NSFR (as and

when made applicable by IFSCA) at IBU

level

◼ LCR and NSFR may be maintained at

parent level with IFSCA’s permission

◼ Leverage ratio may be maintained at

parent level as per home regulator

Reserve Requirement Exposure Ceiling

◼ The liabilities of IBU exempt from SLR

and CRR requirements

◼ Retail Deposit Reserve Ration (RDRR) at

3% of deposits raised from QIs and QRIs

◼ May be maintained in investment grade

and above sovereign securities

◼ Single Borrower Limit – 5% of Parent’s

Tier I Capital;

◼ Group Borrower Limit – 10% of Parent’s

Tier I Capital

Key considerations

Lender of last resort is not available to IBUs

IFSC unit treated as a non-resident under FEMA

Retail banking opened for both resident and non-resident

Deposit insurance not available to IBUs

Adherence to KYC, AML and other norms as prescribed by

IFSCA

Exchange margins for OTC derivative contracts to reflect

Net MTM

Insurance

IFSC Insurance Business: Who can set up?

● Indian and Foreign Insurers

● Indian and Foreign Reinsurers

● Indian and Foreign Intermediaries

● Foreign institution can setup IFSC Insurance Office under

branch route

● No FDI Cap for Foreign Entities setting up branch

● No requirement of having a local JV partner

● Entity based in IFSC would be treated as Non-resident

Insurance in IFSC (1/3)

Permissible Activities

Insurance in IFSC (2/3)

Reinsurance Life Insurance Insurance Intermediary

● Reinsurance for IFSC Insurance

Offices (direct insurers) in IFSC

● Retrocession for IFSC Insurance

Offices (reinsures) in IFSC

● Provide retrocession services to

- Reinsurers and Foreign

Reinsurers Branch based in

India

- Cedants/reinsurers based

outside India

● Reinsurance/retrocession

treaties/contracts in foreign

currency

● Insure NRIs , PIOs , Indian

employees based abroad

● Cater various Life Insurance /

Investment products to foreign

clients

● Within GIFT IFSC: Transact

business within IFSC

● SEZ Business: Transact

intermediary business with other

SEZs in India

● Offshore to Offshore Business:

Transact insurance intermediation

business outside India

● Inward Business: Can place

business from other countries to

IFSC Insurance Offices in GIFT

IFSC

General Insurance● Insurance business for risks of

Units in IFSC

● Insurance business for risks

situated in SEZs across India

● Direct insurance business outside

India (subject to local laws)

● Provide insurance in relation to

offshore risks of exporters &

importers

Plethora of benefits offered to Insurance activities in IFSC

Insurance in IFSC (3/3)

Tax

• Tax holiday: 100% for 10 years out of

any 15 years

• No GST on services rendered in IFSC

or to an IFSC unit

Regulatory

• Relaxed Eligibility Norms to attract

global player for Net Owned Funds

and Capital requirement

• IFSC Insurance offices allowed to

retrocede 90% of its reinsurance

business

Others

Keyenablers

• Operating guidelines for Foreign

Intermediaries

• Allowing subsidiaries of foreign

entities in IFSC

• Enabling framework for facilitating

Protection & Indemnity Club

• Setting up of regional head quarters

for Asian market

• Minimum application of exchange

control laws

Capital Markets

Capital Markets (1/5)Eligible Participants

Registrars, Share transferagent

Alternative InvestmentFunds, Mutual Funds,PMS

List of Products traded and eligible investors on IFSC exchanges

◼ Foreign investors in IFSC exchanges classified as a) FPIs registered with SEBI and, b) Eligible Foreign Investors (foreign investors other than FPIs)

◼ Investments by FPIs and EFIs in IFSC exchanges treated as ‘capital asset’ and resultant gains not chargeable to capital gains tax inIndia

Index F&O Single Stock F&O Commodities Futures Currencies Debt

NIFTY 50 India INX – 200 + F&O Stock Gold (10 troy ounce) Euro – USD Medium Term Notes

NIFTY Bank NSE IFSC – 200 + F&O Stock Silver (500 troy ounce) GBP – USD Green Bonds

NIFTY IT Global Stocks – 5 + F&O Stock Trading Offered

Copper JNY – USD Green Masala Bonds

S&P BSE Sensex Brent Crude Oil AUD – USD

S&P BSE India 50 INR linked derivatives pairing including USD

Depositoryparticipant, Custodian,Credit rating agency,Trustee

International Exchanges

India INX and NSE IFSC

Trading member,Stockbroker,Underwriter

Investmentadvisor, Portfoliomanager, ClearingMember

◼ NRIs permitted by SEBI but subject to RBI concurrence

◼ Financial institution resident in India eligible to invest funds offshore, to the extentpermitted

◼ Person resident in India eligible to investfunds offshore, permitted under LRS Scheme

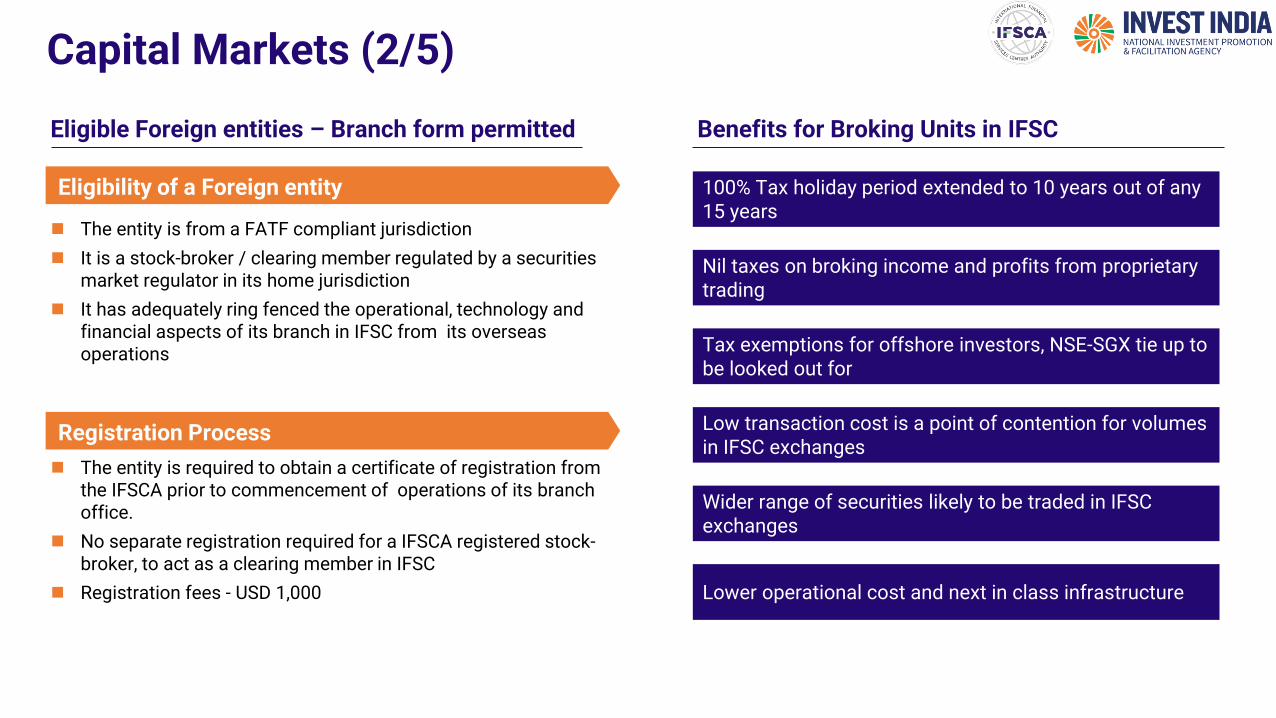

Capital Markets (2/5)

Eligibility of a Foreign entity

Eligible Foreign entities – Branch form permitted

◼ The entity is from a FATF compliant jurisdiction

◼ It is a stock-broker / clearing member regulated by a securities market regulator in its home jurisdiction

◼ It has adequately ring fenced the operational, technology and financial aspects of its branch in IFSC from its overseas operations

Registration Process

◼ The entity is required to obtain a certificate of registration from the IFSCA prior to commencement of operations of its branch office.

◼ No separate registration required for a IFSCA registered stock-broker, to act as a clearing member in IFSC

◼ Registration fees - USD 1,000

Benefits for Broking Units in IFSC

Tax exemptions for offshore investors, NSE-SGX tie up to be looked out for

Low transaction cost is a point of contention for volumes in IFSC exchanges

Lower operational cost and next in class infrastructure

Wider range of securities likely to be traded in IFSC exchanges

100% Tax holiday period extended to 10 years out of any 15 years

Nil taxes on broking income and profits from proprietary trading

Capital Markets (3/5)

Person resident outsideIndia

(Foreign investors)

Non-Resident Indian

(Permitted by SEBI butsubject to RBIconcurrence)

Financial institution resident in India eligible to invest funds offshore,

to the extent permitted

Person resident in India eligible to invest funds offshore, to the extent permitted under LRS

Scheme

Foreign Investor

SEBI Registered FPI & Eligible Foreign Investors

Banking unit in IFSC

Permitted to invest in ◼ Equity shares

◼ Equity derivatives

◼ Currency derivatives

◼ Commodity derivatives

◼ Fixed Income securities

◼ Commodities

◼ Primary market issuance

◼ Currency derivatives

◼ Exchange traded currency derivatives on Rupee

◼ Interest Rate derivatives

◼ Primary market issuance with prior approval from RBI

Registrationrequirement

No set up required in IFSC to operate as a client and cannot provide any services

Foreign Bank having SEBI intermediary registration in India can act as intermediary in IFSC to provide following services after obtaining approval from SEBI:

◼ Act as a trading member

◼ Act as a clearing member

◼ Act as a client

Eligible Participants

Capital Markets (4/5)Guidelines for Investment Advisor in IFSC

Investment Advisory Fees

Foreign clients

Subject to outbound investment norms specified under FEMAprovisions

◼ Financial institution resident in India

◼ Person resident in India subject to LRS with net worth USD 1 Mn

◼ Person resident outside India

◼Non-resident Indian

Invest in foreign currency Indian clients

IFSC IATax benefits

available

Registration Process

◼ Investment Adviser (‘IA’) can be set up as a Company or a Limited Liability

Partnership in IFSC.

◼ Partners and representatives of applicants offering investment advice

shall have following qualifications and experience requirements :

a) Professional qualification or post-graduate degree or post graduate

diploma (minimum two years tenure) in specified fields, and

b) Experience of at least five years in activities relating to advice in

financial products or securities, or fund/ asset/ portfolio management,

or investment advisory services.

◼ Minimum net worth for IA in IFSC – USD 700,000. In case IA in IFSC is

unable to satisfy this requirement, net worth of its parent can be

considered.

◼ Maintain net worth separately and independently for each activity

undertaken, as required under other relevant regulations.

Investment Advisory Services◼ An IA in IFSC can provide services only to :

a) Non-resident Indian

b) Person resident outside India.c) Resident financial institution resident eligible under FEMA to invest funds

offshore,d) Person resident in India who is eligible under FEMA, to invest funds

offshore.

◼ Provisions of the IA Regulations, the guidelines and circulars issued thereunder, shall apply to IAs setting up/ operating in IFSC.

Net Worth SEBI (Investment Advisers) Regulations, 2013

Non Binding Advice

Capital Markets (5/5)Guidelines for Investment Advisor in IFSC

Investment Advisory Fees

Foreign clients

Subject to outbound investment norms specified under FEMAprovisions

◼ Financial institution resident in India

◼ Person resident in India subject to LRS with net worth USD 1 Mn

Invest in foreign currency Indian clients

IFSC PMSTax benefits

available

Registration Process

◼ Portfolio Manager (‘PM’) can be set up as a

a) Branch of a SEBI registered intermediary (except trading or clearing

member) or in collaboration of its international associates subject to

SEBI approval.

b) Company or a Limited Liability Partnership in IFSC by other entities

based in India or foreign jurisdiction. However, formation of separate

Company or LLP not required for existing Company or LLP in IFSC.

◼ Minimum net worth for PM in IFSC – USD 750,000. In case of branch,

parent to fulfil net worth requirement.

◼ Maintain net worth separately and independently for each activity

undertaken, as required under other relevant regulations.

Certification Requirement

◼ Non-resident principal officer and employee having decision making authority

to have certification from organization recognized by Financial Market

Regulator in foreign jurisdiction

◼ Certification from NISM mandatory deal in Indian securities market

◼ A Portfolio Manager in IFSC can provide services only to :

a) Non-resident Indian

b) Person resident outside India.

c) Resident financial institution resident eligible under FEMA to invest

funds offshore,

d) Person resident in India who is eligible under FEMA, to invest funds

offshore.

Net Worth

Portfolio Management Services

◼ Person resident outside India

◼Non-resident Indian

Global In-House Centres

Global In-House Centres (1/2)

GICs can provide support services, directly or indirectly, to entities within its financial services group

Banks, Non-banking financial companies

Financial intermediaries and Investment Banks

Actuaries, Insurance and Re-insurance

Brokerage firms, Clearing Houses and Depositories & Custodians

Stock Exchanges

Other financial services notified by IFSCA

Permissible Entities to be Supported

CONDUCTING BUSINESS

❑ GIC Business can be set up as a company, LLP, Branch or other legal entity

ELIGIBILITY CRITERIA

❑ Entity under a financial services group can set up a GIC in IFSC

❑ The support services should be to carry out a financial service in respect of a financial product

PERMITTED CURRENCY

❑ Deal in freely convertible foreign currency

❑ May defray administrative expenses in INR by maintaining an INR account as may be specified by the authority.

PERMISSIBLE ACTIVITIES

❑ GIC to exclusively cater to its financial services group

Salient Features of GIC in IFSC

Setting up GIC unit in GIFT IFSC

GIC may conduct business as company/branch/anyother mode permitted by authority

Submission of application for SEZ Approval

Submission of registration application to IFSCA

Grant registration by IFSCA

Grant of SEZ Approval

Commencement of business by GIC unit

Toronto

New York

LondonParis

Frankfurt

Dubai

Singapore

GIFT City Gujarat, India

Tokyo South Korea

Shanghai Hong Kong

Global In-House Centres (2/2)

Aircraft Leasing

Aircraft Leasing in IFSC (1/2)

IFSC offers a robust regulatory environment to cater to domestic and international aviation industry

Overview

• The entity shall set up operations in IFSC in India

by way of a company or a LLP or a trust or any

other form as may be specified by the IFSCA.

• The person controlling the entity shall be located

in a FATF compliant jurisdiction or jurisdiction

permitted by the Government of India.

• The entity shall deploy resources commensurate

with the business operations in IFSC.

• A minimum capital of USD 200,000 or its

equivalent in freely convertible foreign currency, is

to be maintained at all times by the entity.

• The capital is to be brought in before entering into

any permissible activity or 12 months from the

date of grant of registration.

Permissible Activities

❑ Operating lease arrangement including sale and lease back, purchase, novation, transfer, assignment,

PERMITTED CURRENCY

❑ To deal in freely convertible foreign currency only

❑ The entity is permitted to defray its administrative expenses in INR by maintaining an INR account.

FEES

❑ Application Fee: USD 1,000 (one time)

❑ Registration Fee: USD 5,000 (one time)

❑ Annual Fee: 3,000 (second year onwards)

Salient Features

Aircraft Leasing in IFSC (2/2)

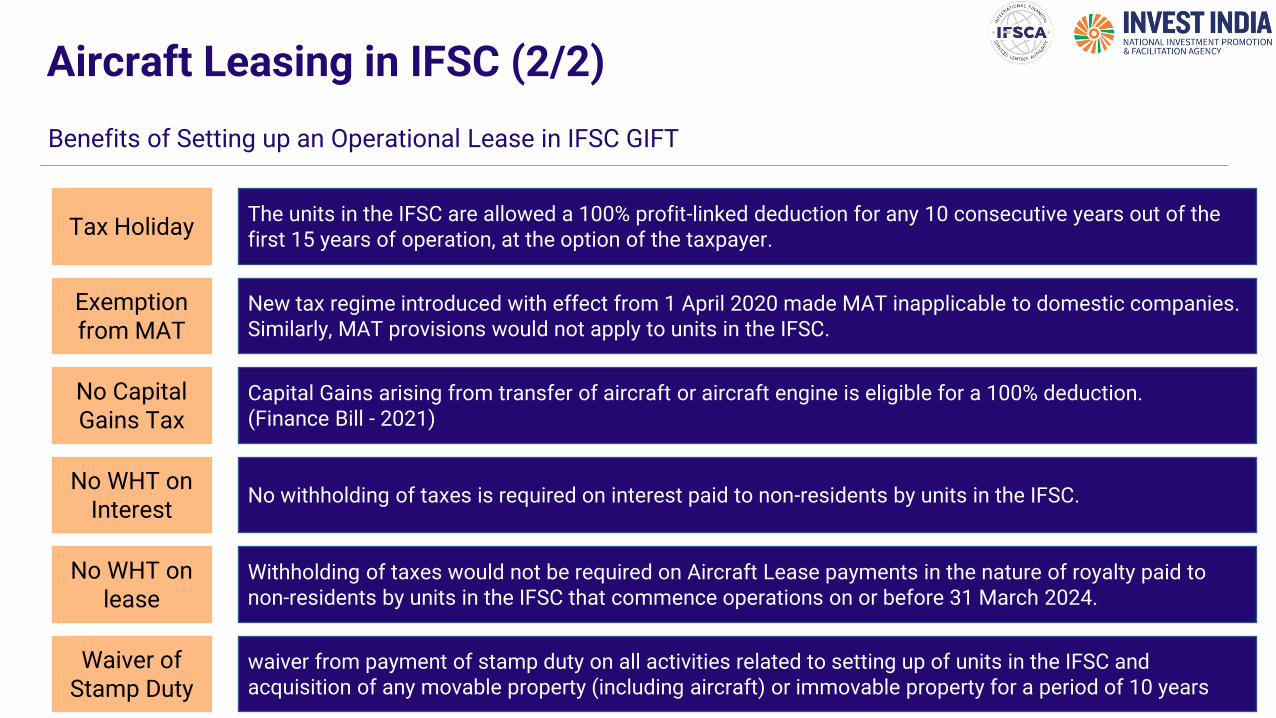

Benefits of Setting up an Operational Lease in IFSC GIFT

The units in the IFSC are allowed a 100% profit-linked deduction for any 10 consecutive years out of the first 15 years of operation, at the option of the taxpayer.

Tax Holiday

New tax regime introduced with effect from 1 April 2020 made MAT inapplicable to domestic companies. Similarly, MAT provisions would not apply to units in the IFSC.

Exemption from MAT

Capital Gains arising from transfer of aircraft or aircraft engine is eligible for a 100% deduction.(Finance Bill - 2021)

No Capital Gains Tax

No withholding of taxes is required on interest paid to non-residents by units in the IFSC.No WHT on

Interest

Withholding of taxes would not be required on Aircraft Lease payments in the nature of royalty paid to non-residents by units in the IFSC that commence operations on or before 31 March 2024.

No WHT on lease

waiver from payment of stamp duty on all activities related to setting up of units in the IFSC and acquisition of any movable property (including aircraft) or immovable property for a period of 10 years

Waiver of Stamp Duty

32

World’s Most Awarded Investment Promotion Agency

NATIONAL INVESTMENT PROMOTION & FACILITATION AGENCY