15

International Perspectives on the Future of Audit— International Auditing Standard Setting Prof. Arnold Schilder, IAASB Chairman Nexia International Annual Conference Paris, 2 November 2011

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | claud-walsh |

| View: | 215 times |

| Download: | 0 times |

International Perspectives on the Future of Audit—International Auditing Standard

Setting

Prof. Arnold Schilder, IAASB Chairman

Nexia International Annual Conference

Paris, 2 November 2011

• A Changing Environment

• Responding to Change and Strategic IAASB Initiatives

• Recent IAASB Approvals

• The Road Ahead: 2012-2014

• Global Uptake and Uses of the Clarified ISAs

Agenda

2

• Impact of global financial crisis on audit policy

– Questions raised in face of changing environment:o Role of the auditor and audit o Quality of auditing: audit effectiveness; professional

judgment; professional skepticismo Market structures and participantso Governance and structures (firms, standard-setters,

regulators)

• Developments in corporate financial reporting

– Financial reporting infrastructure (standards & frameworks); spotlight on new areas, incl. disclosures; narrative reporting

Changing Environment: Areas of Challenge

Changing Environment

3

The Audit Quality Framework

Responding to Change: Audit Quality

4

• Auditor Reporting – Consultation Paper (May 2011)– In process of analyzing responses (78 letters so far- not Nexia…)– Wide range of views in relation to information needs of users and

who is best placed to provide such information– Strong acknowledgement of need to coordinate with others in this

area (PCAOB, EC and others)• Disclosures – Discussion Paper

– Broad support for IAASB initiative, but also recognized that improving disclosures will require collaboration and co-operation of many; strong support for need for a disclosure framework

– Disparity of views groups as to some issues raised, such as expected audit effort for such disclosures as stress tests

Consultation in Key Areas

Responding to Change: Strategic Initiatives

5

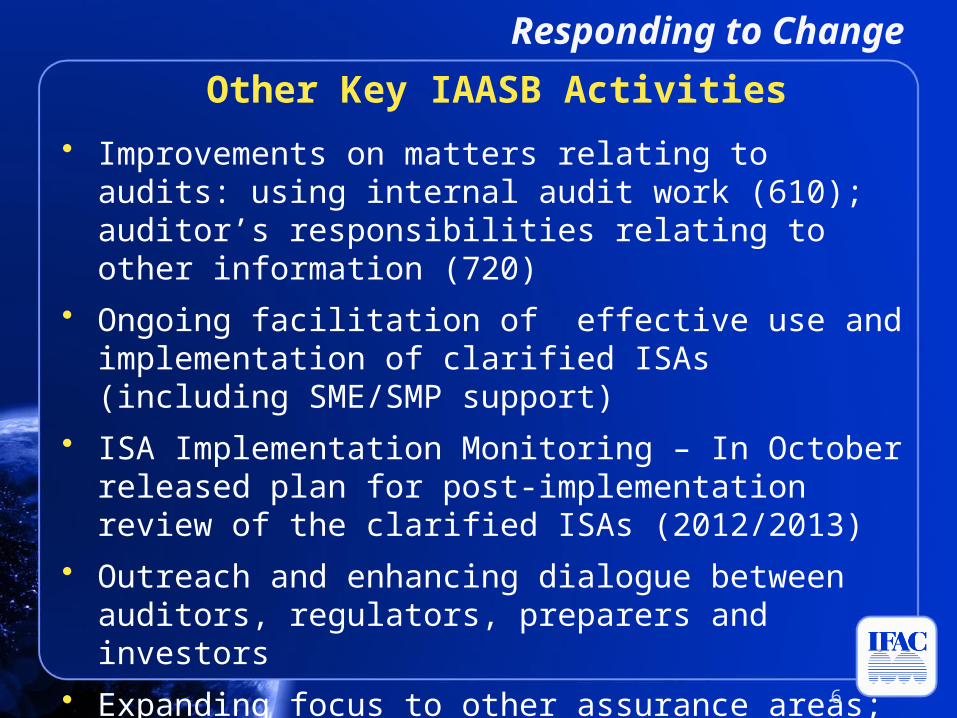

• Improvements on matters relating to audits: using internal audit work (610); auditor’s responsibilities relating to other information (720)

• Ongoing facilitation of effective use and implementation of clarified ISAs (including SME/SMP support)

• ISA Implementation Monitoring – In October released plan for post-implementation review of the clarified ISAs (2012/2013)

• Outreach and enhancing dialogue between auditors, regulators, preparers and investors

• Expanding focus to other assurance areas; standards and guidance for non-assurance areas

Other Key IAASB Activities

6

Responding to Change

Responding to Change

• Strengthening the suite of other assurance standards

– Revisions of existing assurance standards

– Proposed ISAE 3000–“umbrella” standard, for information other than historical financial information

– Proposed ISRE 2400–review engagements

– New assurance standards

– ISAE 3402–controls of a service organization

– Proposed ISAE 3410–greenhouse gas statements

– ISAE 3420–compilation of pro-forma financial information

• Revision of standard for compilation engagements

Expanding Focus: Other Current projects

7

• IAPN 1000 – Special Considerations in Auditing Financial Instruments (formerly proposed IAPS 1000)

– First release of new non-authoritative ‘IAPN’ vehicle

• Provides practical assistance to auditors without imposing obligations; for use by NSS in disseminating useful material, and firms for training/internal guidance purposes

– Purpose/risks of using FIs; controls; valuation methods; presentation/disclosure; etc.

– Audit planning considerations; risk assessment & responses; valuation (e.g. testing of models; use of third party pricing sources; use of experts); etc.

•Expected release: Dec 2011 (approved text available now)

International Auditing Practice Note 1000

Recent IAASB approvals

8

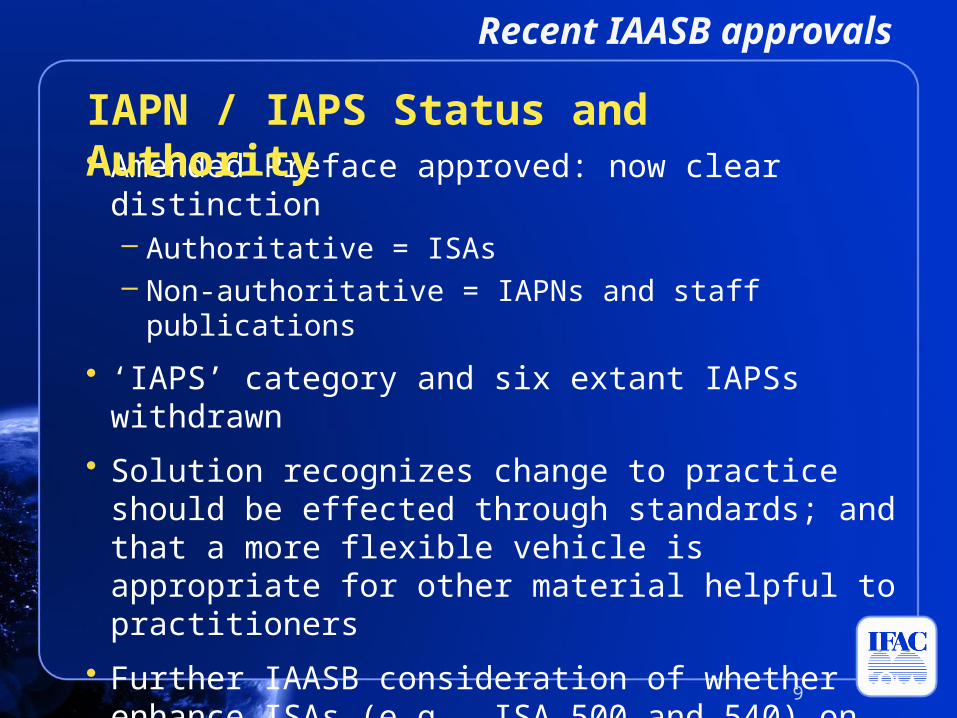

• Amended Preface approved: now clear distinction– Authoritative = ISAs– Non-authoritative = IAPNs and staff publications

• ‘IAPS’ category and six extant IAPSs withdrawn

• Solution recognizes change to practice should be effected through standards; and that a more flexible vehicle is appropriate for other material helpful to practitioners

• Further IAASB consideration of whether to enhance ISAs (e.g., ISA 500 and 540) on specific areas– Consideration of PCAOB developments– Other areas where addition guidance on auditing financial

instruments may be needed

IAPN / IAPS Status and Authority

Recent IAASB approvals

9

• New ISAE 3420, Assurance Engagements to Report on Compilation of PFI included in a Prospectus (approved Sept 2011)

– Developed in response to European developments, primarily, but also broader calls to help harmonize practice

• Reasonable assurance engagement

− Presumed columnar format presentation: (a) unadjusted financial info; (b) pro forma adjustments; (c) resulting pro forma column

• Minimum requirements for suitable criteria

• Dual approach to opinion: PFI has been […properly compiled on the basis stated] / […compiled, in all material respects, on the basis of the applicable criteria]

• Effective for assurance reports dated ≥ March 31, 2013

Pro Forma Financial Information

Recent IAASB approvals

10

The Road Ahead :2012-14

• Premised on three key themes

– Supporting global financial stability

– Enhancing the role, relevance and quality of assurance and related services in an evolving world

– Facilitating adoption and implementation of the standards

• Common messages

– Continue focus on current projects: AQ, Auditor Reporting, Disclosures, and assurance /related services standards (including those pertaining to SMP needs)

– Retain flexibility/ capacity to respond to developments

– Consider longer-term horizon

IAASB Strategy and Work Program 2012-2014

11

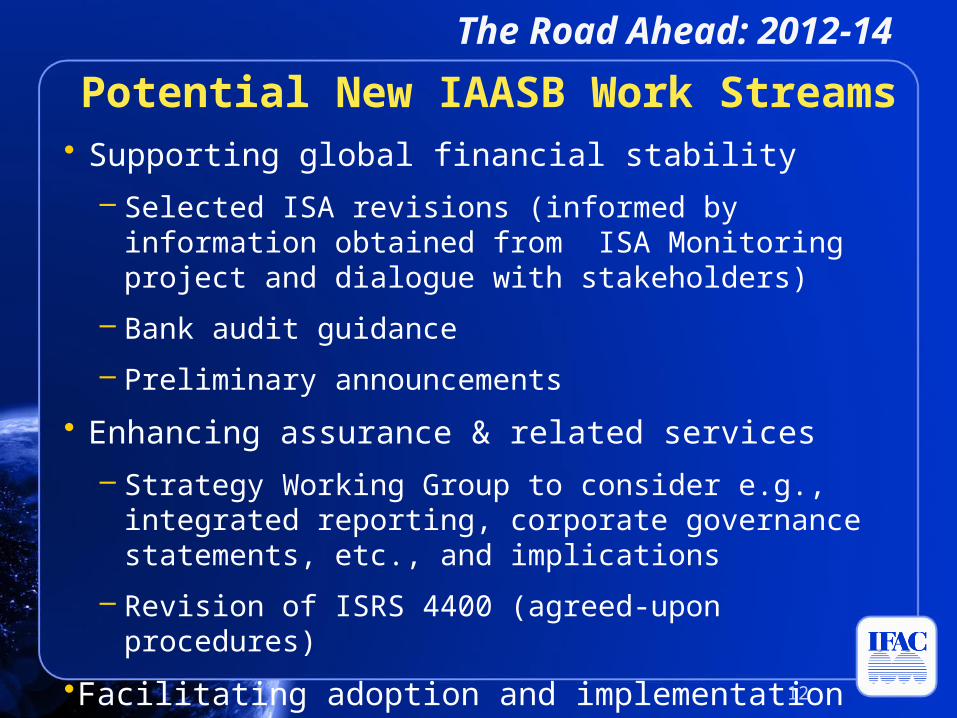

• Supporting global financial stability

– Selected ISA revisions (informed by information obtained from ISA Monitoring project and dialogue with stakeholders)

– Bank audit guidance

– Preliminary announcements

• Enhancing assurance & related services

– Strategy Working Group to consider e.g., integrated reporting, corporate governance statements, etc., and implications

– Revision of ISRS 4400 (agreed-upon procedures)

•Facilitating adoption and implementation

– Proportional application of ISQC 1 staff guidance

The Road Ahead: 2012-14

12

Potential New IAASB Work Streams

Global Auditing Standards: Where Are We Now?

• International Organization of Securities Commissions (IOSCO)• Basel Committee on Banking Supervision• Financial Stability Board• International Organization of Supreme Audit Institutions (INTOSAI)• United Nations Conference on Trade and Development (UNCTAD)• World Bank• World Federation of Exchanges

Expressed support for Clarified ISAs:

Clarified ISAs

Other uses of Clarified ISAs globally:

• INTOSAI Congress (INCOSAI) through International Standards of Supreme Audit Institutions (ISSAIs)

• Forum of Firms: Top 24 global auditing networks’ methodologies align (welcome to Nexia!)

13

Americas: Bahamas, Barbados, Brazil, Canada, Cayman Islands, Costa Rica, Guyana, Jamaica, Mexico, Nicaragua, Panama, Puerto Rico (private companies), Trinidad and Tobago, Uruguay, USA (private companies), Europe: Albania, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, Georgia, Greece, Hungary, Iceland, Ireland, Kosovo, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Norway, Romania, Serbia, Slovakia, Slovenia, Sweden, Switzerland, Turkey, United KingdomAsia Pacific: Australia, Bangladesh, China, Hong Kong, India, Japan, Kazakhstan, Malaysia, Mongolia, Nepal, New Zealand, Pakistan, Philippines, Singapore, South Korea, Sri Lanka Africa/ Middle East: Botswana, Kenya, Lebanon, Lesotho, Malawi, Mauritius, Namibia, Sierra Leone, South Africa, Swaziland, Tanzania, Tunisia, Uganda, United Arab Emirates (Abu Dhabi and Dubai), Zambia, Zimbabwe

Jurisdictions Currently Using Clarified ISAs, or Committed to Using Them in the Near Future:

Clarified ISAs: Global Adoption

14

http://www.iaasb.org