International Securities Operational Market Practice Book New issues • New issuance draft and final documentation • Distribution processing Corporate actions • Corporate action event notifications • Corporate action processing Income • Income event notifications • Payment processing January 2012

Transcript

International SecuritiesOperational Market Practice Book

New issues • New issuance draf t and f ina l documentat ion

• D is t r ibut ion process ing

Corporate act ions • Corporate ac t ion event not i f i ca t ions

• Corporate ac t ion process ing

Income • Income event not i f i ca t ions

• Payment process ingJa

nuar

y 20

12

M A R K E T P R A C T I C E B O O K

2

M A R K E T P R A C T I C E B O O K

3

Updates

The MPB may be subject to a yearly review further to consultation with the International Securities Market Advisory Group.

The main updates of this January 2012 version compared to February 2011 are:

• Chapter 1 / section 1.2.: ISMAG Best Practices Summary #3. on Naming Convention - Updated

• Chapter 3 / section 3.3.6.1.: Corporate Actions / Reg S - 144A transfers, flow “c” in table - Corrected

• Annex 1: Letters of Representation June 2011 versions - Updated

1.2. ISMAG BEST PRACTICES SUMMARY ...................................................................................................................19

1.3. INFORMATION TAXONOMY .....................................................................................................................................22

1.3.2. Specific recommendations ...............................................................................................................................23

CHAPTER 2: NEW ISSUES .............................................................................................................................................272.1. SCOPE ......................................................................................................................................................27

2.2. INFORMATION FLOW ...............................................................................................................................................27

2.2.1. New issues documentation description ............................................................................................................27

2.2.1.2. Final documentation ..................................................................................................................................28

2.2.1.3. Updated documentation after closing date................................................................................................29

2.2.2. New issues draft documentation flows .............................................................................................................30

2.2.2.2.1. Documentation flow for Programmes at establishment ....................................................................32

2.2.2.2.2. Documentation flow for issuance under Programme at acceptance ................................................34

2.2.3. New issues final documentation flows ..............................................................................................................36

2.2.3.1. Documentation flow for Stand-Alone securities at issuance .....................................................................36

2.2.3.2. Documentation flow for Stand-Alone securities when updates/changes occur

after closing date .......................................................................................................................................37

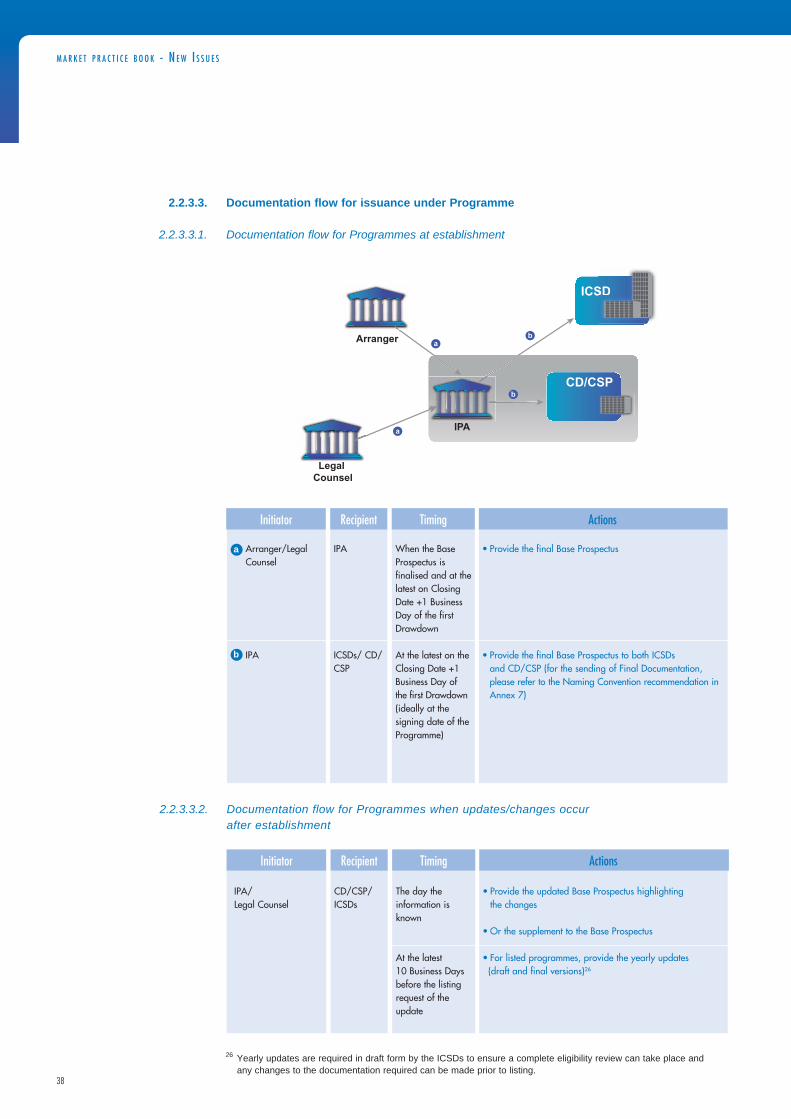

2.2.3.3. Documentation flow for issuance under Programme ................................................................................38

2.2.3.3.1. Documentation flow for Programmes at establishment ....................................................................38

2.2.3.3.2. Documentation flow for Programmes when updates/ changes occur

after establishment ...........................................................................................................................38

2.2.3.3.3. Documentation flow for issuance under Programme at issuance ....................................................39

2.2.3.3.4. Documentation flow for issuance under Programme when

updates/changes occur after closing date ........................................................................................40

2.3.1. New issues same day syndicated distribution ..................................................................................................40

2.3.2. Same day syndicated distribution flow .............................................................................................................41

3.2. INFORMATION PROVISION FLOW ..........................................................................................................................44

3.2.1. Corporate action information ............................................................................................................................44

3.2.1.1. Information description ..............................................................................................................................44

3.2.1.2. Preliminary information ..............................................................................................................................44

3.2.1.3. Complete information ................................................................................................................................45

3.2.2. Information provision and timing per event types .............................................................................................47

3.2.2.1. Information flow for Predictable events other than those occurring upon a

triggering event or at the option of the Issuer ...........................................................................................47

Table of contents

M A R K E T P R A C T I C E B O O K

6

3.2.2.2. Information flow for Predictable events occurring upon a triggering event or at

the option of the Issuer .............................................................................................................................48

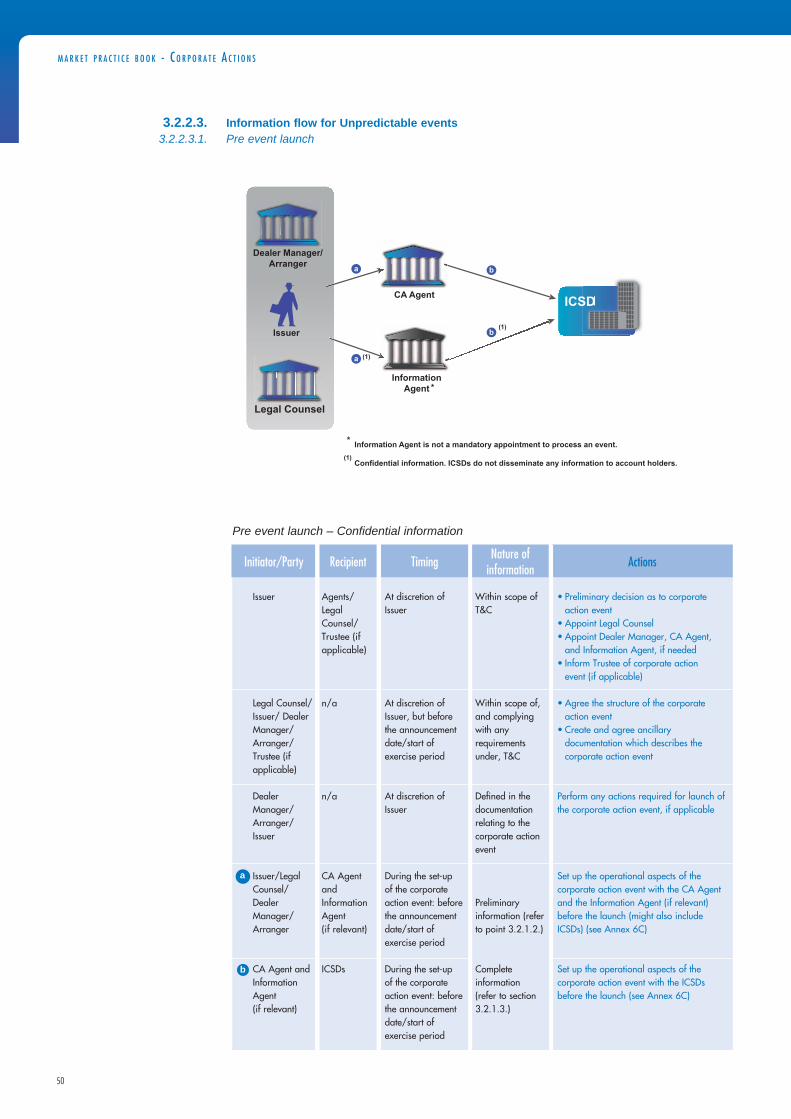

3.2.2.3. Information flow for Unpredictable events .................................................................................................49

3.2.2.3.1. Pre event launch ...............................................................................................................................49

3.2.2.3.2. Event launch or post launch .............................................................................................................51

3.3.2. Instructions from holders .................................................................................................................................52

3.3.3. Announcements during the lifecycle of an event .............................................................................................57

3.3.4. Outcome of Events & Instructions ...................................................................................................................59

3.3.4.1. Outcome at event level ............................................................................................................................60

3.3.4.2. Outcome at instruction level .....................................................................................................................60

3.3.5. Proceeds information .......................................................................................................................................60

3.3.5.1. Main Proceeds information ......................................................................................................................60

3.3.6.1. Regulation S. – 144A Transfers (and vice-versa): triggered by investors instructions ............................68

3.3.6.2. Conversion Event – Bonds into Shares: triggered by investors instructions ...........................................70

3.3.6.3. Redemption in Cash or Shares: triggered by an external event ..............................................................72

CHAPTER 4: INCOME .....................................................................................................................................................754.1. SCOPE ......................................................................................................................................................75

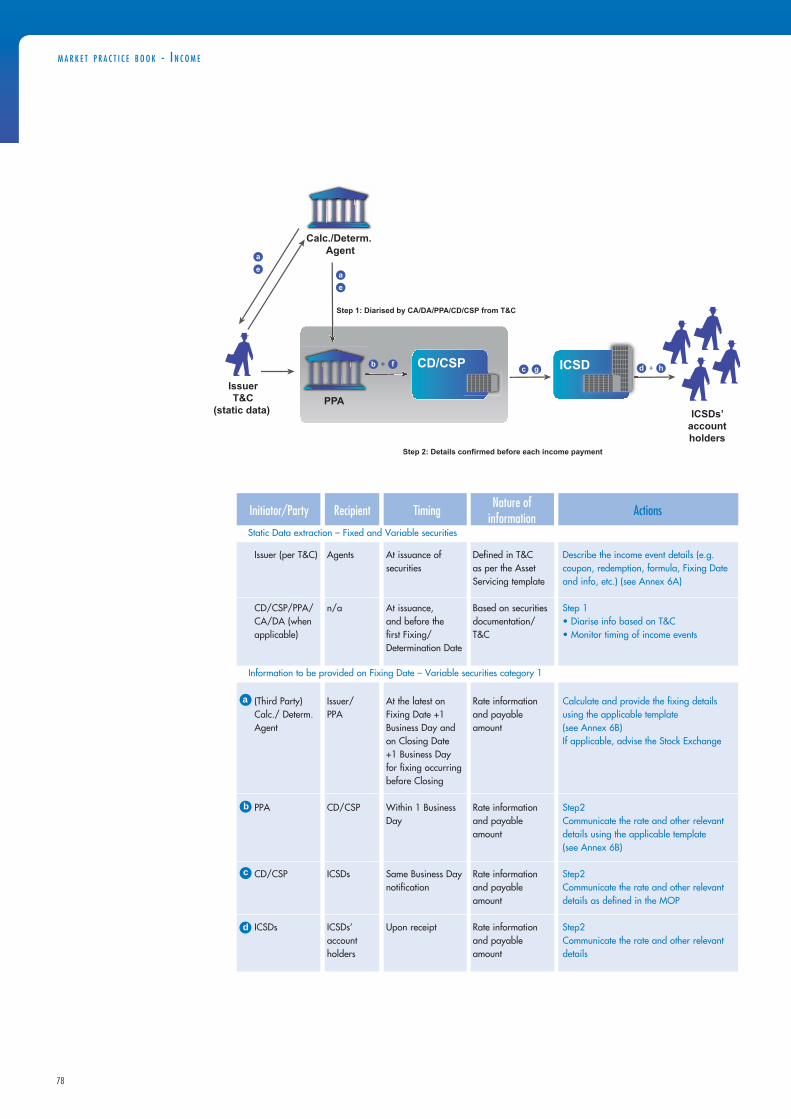

4.2. INFORMATION PROVISION FLOW ..........................................................................................................................75

4.2.1. Income information ...........................................................................................................................................75

4.2.1.1. Information description ..............................................................................................................................75

4.2.1.2. Information transmission ...........................................................................................................................76

4.2.2. Information provision and timing - Fixed and variable rate instruments ...........................................................77

4.3.3. Processing of amendments .............................................................................................................................81

4.3.3.2. Amendments root cause – Who? Why? What? .......................................................................................82

4.4. INVESTIGATIONS AND INQUIRIES .........................................................................................................................83

4.4.1. Pre-payment queries: priority linked to payment date ......................................................................................83

4.4.2. Post-payment queries: priority linked to payment amount difference ..............................................................84

M A R K E T P R A C T I C E B O O K

7

ANNEXES ......................................................................................................................................................85ANNEX 1 A: ISMAG - Issuer Blanket Letter of Representation ........................................................................................87

ANNEX 1 B: ISMAG - Issuer Agent Letter of Representation ..........................................................................................89

ANNEX 1 D: Notice of Revocation of ISMAG Adherence.................................................................................................92

ANNEX 2: ICMA Guidance Note to the market ................................................................................................................93

ANNEX 3: EU Prospectus Directive ..................................................................................................................................96

6A: Final Documentation Fields ................................................................................................................................110

6B: Notification Fields for Predictable Events ...........................................................................................................124

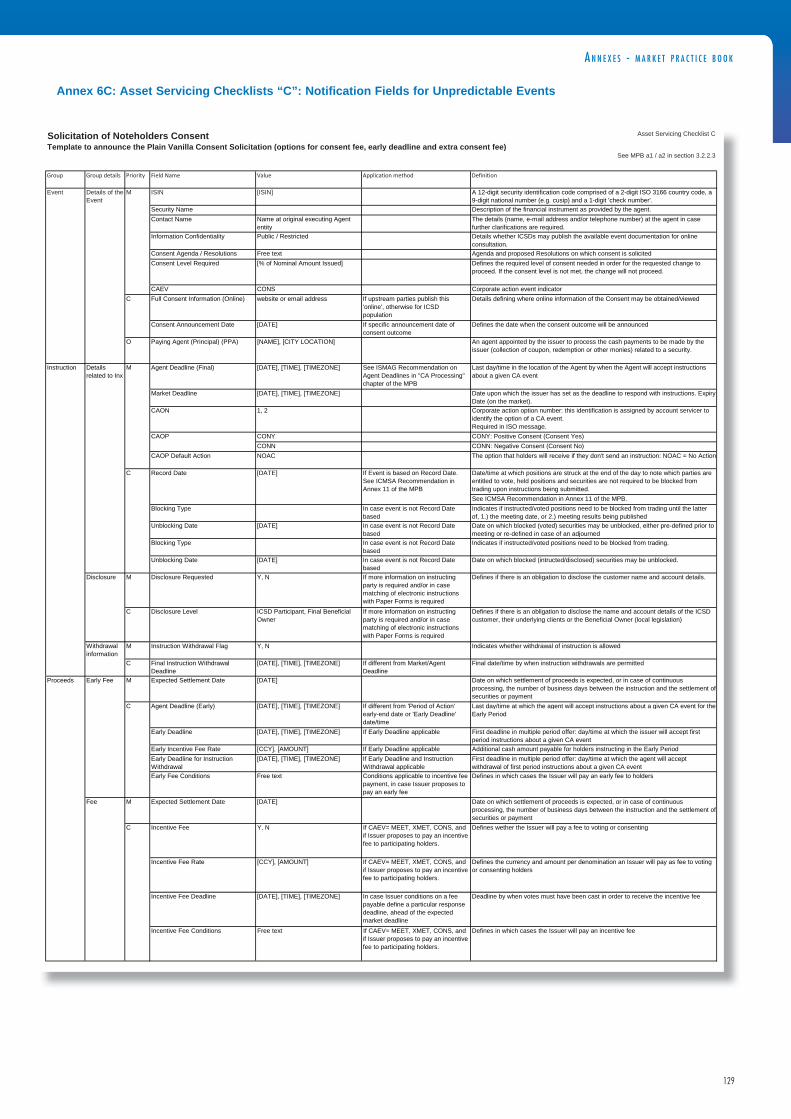

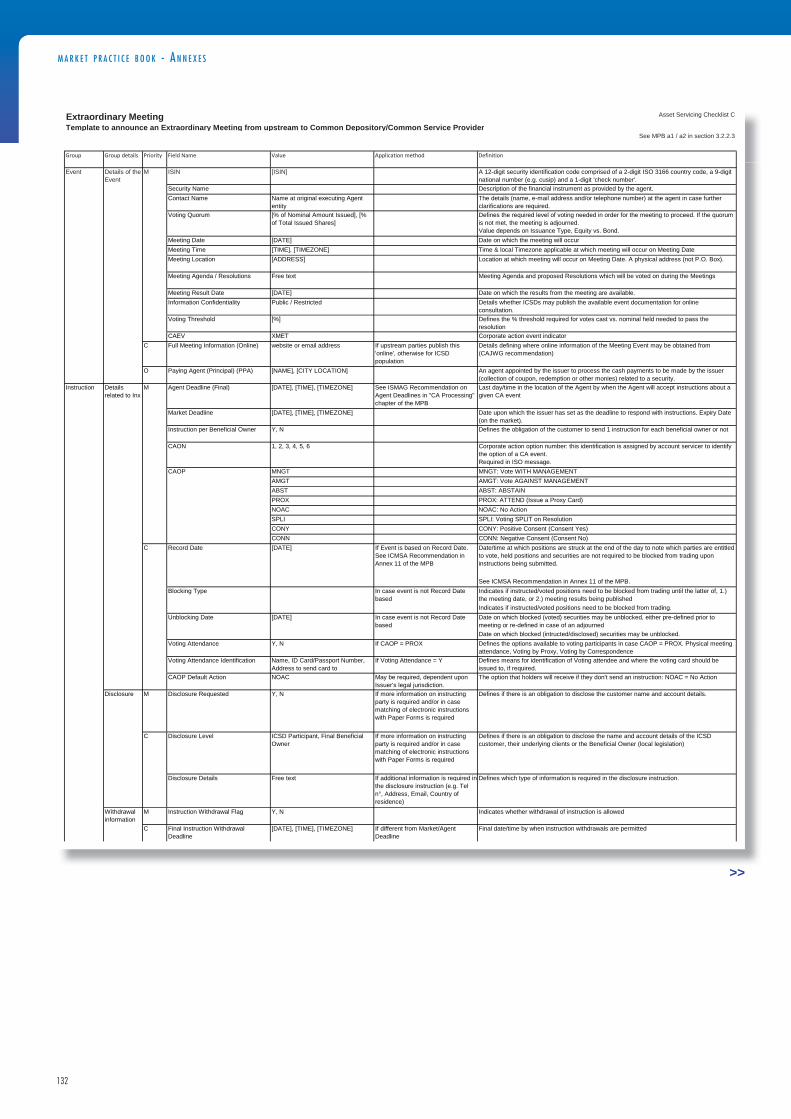

6C: Notification Fields for Unpredictable Events ......................................................................................................129

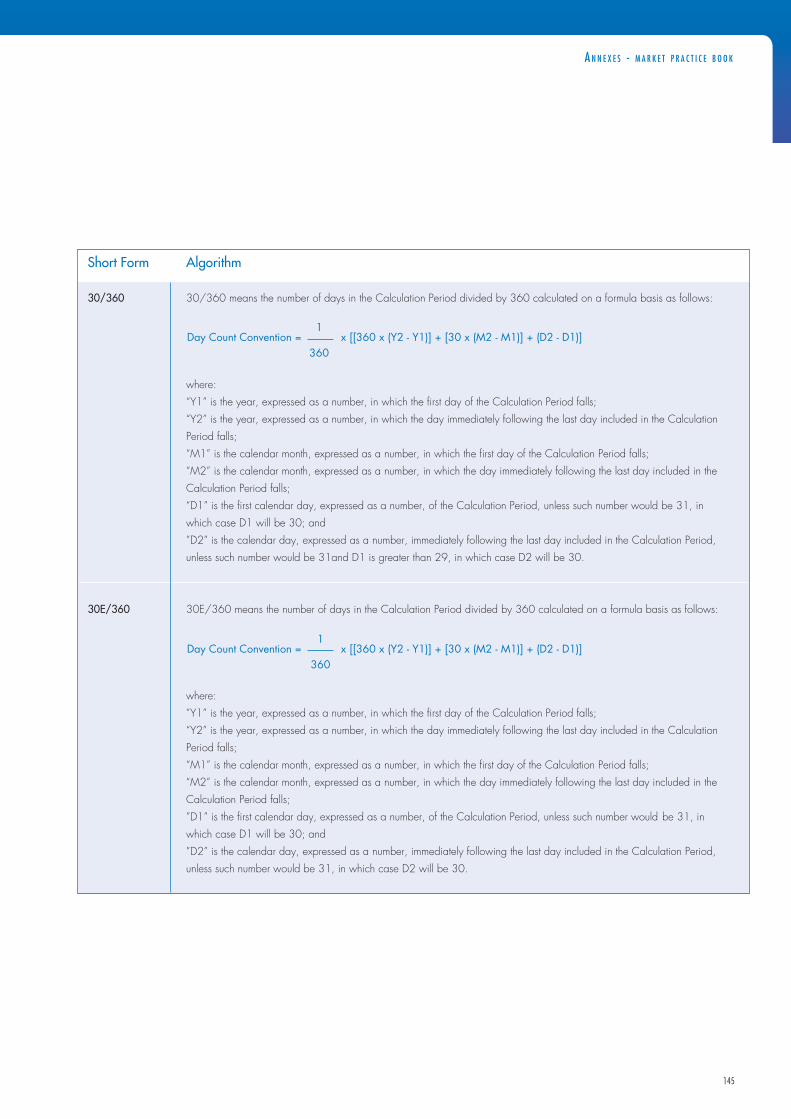

ANNEX 8: Day Count Conventions recommendation .....................................................................................................144

ANNEX 9: Units and Nominal recommendation .............................................................................................................146

ANNEX 10: ICMSA Recommendation with respect to requirements for Payment Business Days ................................147

ANNEX 11: ICMSA Recommendation for Record Dates ................................................................................................148

ANNEX 12: ICMSA Recommendation for the Treatment of Partial Redemptions ..........................................................150

ANNEX 13: ICMSA Guidelines for the Issuance of Confidential Securities within the ICSDs........................................151

ANNEX 14: ISMAG Terms of Reference ........................................................................................................................152

14 A : ISMAG – Change Programme Definition Phase, Terms of Reference ..........................................................152

14 B : ISMAG – Implementation Phase, Terms of Reference ..................................................................................155

ANNEX 16: Glossary of Template Fields ........................................................................................................................171

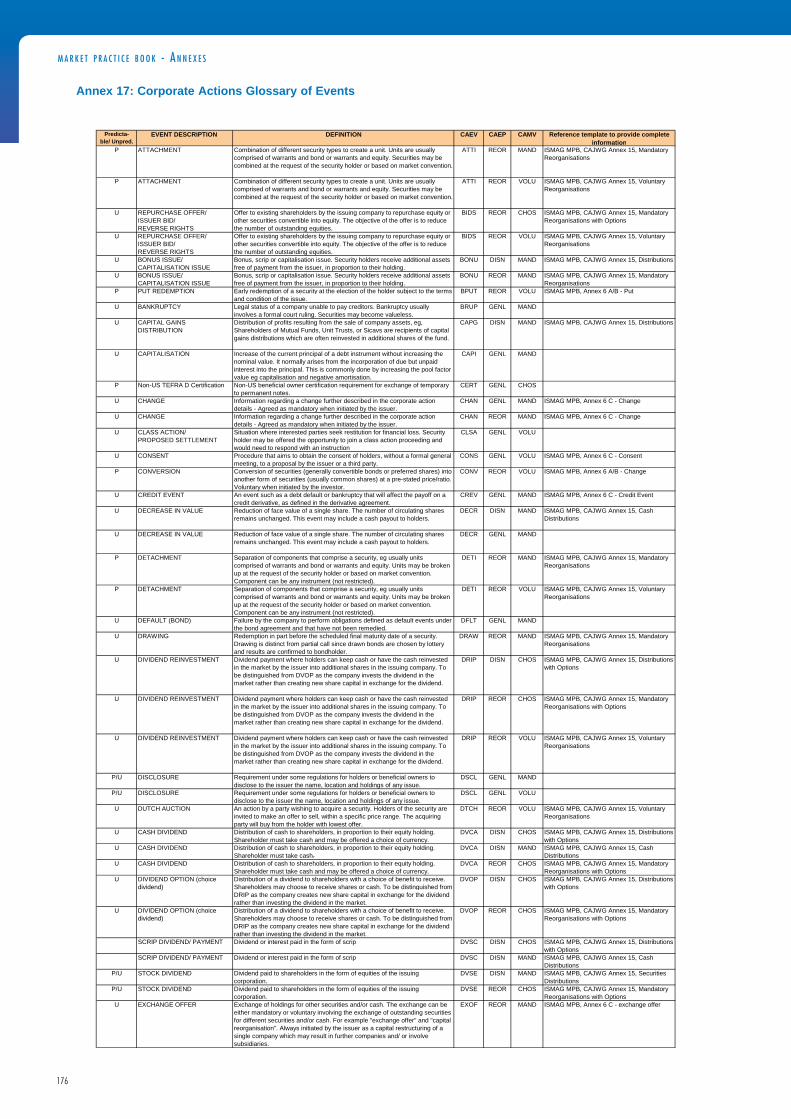

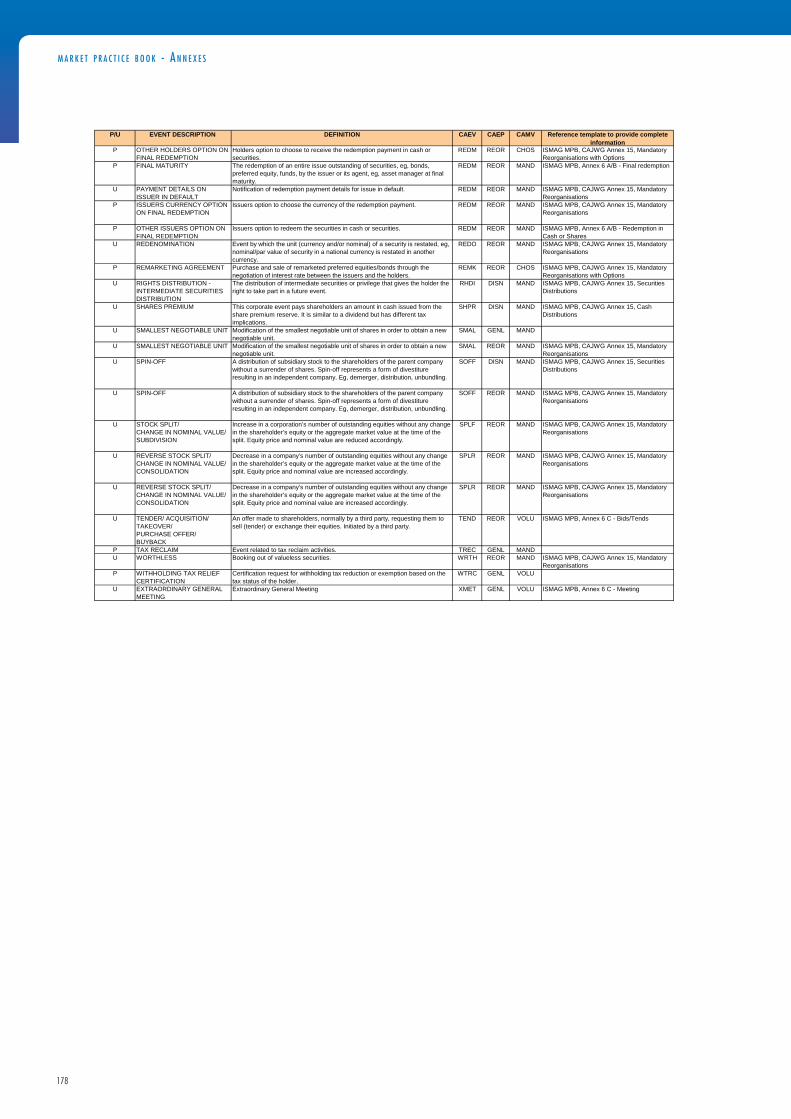

ANNEX 17: Corporate Actions Glossary of Events.........................................................................................................176

ANNEX 18: Income Amendments Root Cause – Methodology quick card ....................................................................179

M A R K E T P R A C T I C E B O O K

8

M A R K E T P R A C T I C E B O O K

9

Introduction

This operational Market Practice Book (MPB), issued by the two International Central Securities Depositories (ICSDs), Euroclear Bank and Clearstream Banking, describes the best practices for operational processes in new issues, corporate actions and income for international securities primarily issued through and deposited with the ICSDs.

The MPB was created in conjunction with valuable input from a wide variety of market practitioners in the international securities industry, and under the auspices of a market body, the International Securities Market Advisory Group (ISMAG). Working Groups for each of the operational streams were set up for this purpose. The role of the ISMAG is to guide and promote the design and implementation of a change programme. The programme is aimed to achieve a high degree of standardisation and operational efficiency in the issuance and asset servicing of international securities issued through the ICSDs. Different end-to-end intermediaries such as Issuers, Agents, Common Depositories, ICSDs, Custodians, Lead Managers and Trade Associations are represented in ISMAG.

The MPB has been drafted to describe improvements to existing operational market practices, focusing on timeliness, coverage and quality of information provision and processing for new issues, corporate actions and income.

The independent chairman of ISMAG has agreed that the MPB reflects the main issues raised by its membership and has confirmed his support for its publication.

In parallel, the Trade Associations participating in the ISMAG may issue their own recommendations to their members. The International Capital Market Association (ICMA) has issued a Guidance Note which sets out its view about how its members should comply with this MPB. A copy of the Guidance Note can be found in Annex 2. By implementing the recommendations contained within this Market Practice Book, Issuers and their Agents will, to a large extent, ensure an efficient and effective end-to-end service to investors.

From 2011, Issuers and Agents have the opportunity to market their adherence by officially joining the market framework, developed by the ICSDs after ISMAG consultation. The market framework and a summary of best practices are defined in the following chapter.

M A R K E T P R A C T I C E B O O K

10

This publication will be regularly reviewed and updated to reflect changes and developments in the market.

The operational practices, as described in this Market Practice Book are not intended to impose any legal obligations on market participants but aim to provide a set of recommendations for an efficient operational framework to asset service international securities.

Views on the content of this document are welcome, and should be addressed in writing to the ISMAG Project Management Office, by emailing either [email protected] or [email protected]

Unless otherwise stated, all deadlines of this document refer to the ICSDs’ deadlines and are expressed in a hh:mm 24-hour format, in Central European Time (CET), on any Business Day.

For variations to those ICSDs’ deadlines, please refer to the individual contractual service descriptions of each party.

Legal disclaimer

Timing convention

M A R K E T P R A C T I C E B O O K

11

Glossary

Agent A generic term describing an entity that acts on behalf, and upon request, of the Issuer. The term “Agent” includes any Paying Agent, Issuing and Paying Agent, Fiscal Agent, Registrar, Determination Agent, Calculation Agent, Withholding Agent (if appointed by the Issuer), Corporate Action Agent, Conversion Agent, Exchange Agent or any other agent appointed by the Issuer.

ANNA ANNA - the Association of National Numbering Agencies, incorporated as a Belgian srcl, has been designated by ISO as the responsible entity for overseeing the maintenance and assignment of ISIN and CFI code standards.

Arranger An entity responsible for arranging and structuring a Programme.

Base Prospectus The document published by the Issuer in relation to a Programme and made available to prospective investors. May also be called by another name, such as offering circular or information memorandum.

Business Day (as used in this document) Any day except Saturdays, Sundays and public holidays in jurisdictions in which respective parties are operating.

Calculation Agent An agent appointed by the Issuer to process and disseminate coupon rate fixing or redemption information and to determine any amount payable under the securities.

Classical Global Note (CGN) A form of Global Certificate which requires physical annotation on the attached schedule to reflect changes in the IOA.

Closing Date For syndicated issuance, the date on which the issue proceeds are paid to the Issuer and the securities are created and distributed to investors through the ICSDs.

Common Code A 9-digit number used to uniquely identify individual securities between the ICSDs and their participants, and allocated by one of the ICSDs.

Common Depository (CD) An entity appointed by the ICSDs to provide safekeeping and asset servicing for securities in CGN form.

Common Safekeeper (CSK) An entity appointed by the ICSDs to provide safekeeping for NGN and NSS.

Common Service Provider (CSP)

An entity appointed by the ICSDs to provide asset servicing for NGN and NSS.

Conversion Agent or Exchange Agent

An agent appointed by the Issuer to instruct the execution of conversion or exchanges of securities.

Corporate Action Agent (CA Agent)

An agent appointed by the Issuer to act on its behalf in relation to a specific unpredictable corporate action.

CSK Election Form A form which is sent by the relevant Principal/Issuing and Paying Agent indicating which ICSD will act as “Common Safekeeper (CSK)” for NGN/NSS intended to constitute ECB Eligible Collateral.

M A R K E T P R A C T I C E B O O K

12

Dealer An entity appointed by the Issuer to structure and place a non-syndicated issue.

Dealer Manager An entity appointed by the Issuer to structure the management of a specific unpredictable corporate action.

Determination Agent An agent appointed by the Issuer to make certain determinations in accordance with the T&C and responsible for the monitoring of external factors (e.g. basket of securities, index, underlying assets) used to determine all or part of the Rate Fix Formula.

Determination Date The date on which the payable amount will be determined by combining the elements mathematically calculated on Fixing Date and the last elements of the formula (it may or may not coincide with the Fixing Date). It is often quite close to Payment Date.

Drawdown The issuance of a security under a Programme.

Effectuation Authorisation An Effectuation Authorisation must be sent to the appointed CSK by the Issuer. It instructs the CSK to act as agent with respect to the effectuation of each Global Note and, as such, to sign each Global Note as the final act making such note a valid security in accordance with the terms of such Global Note.

EMTN Euro Medium Term Note.

European Pre-Issuance Messaging (EPIM)

Central messaging link allowing IPAs and dealers to electronically request ISIN’s and common codes for ECP, ECD and MTN issuances from the ICSDs using standardised message formats. EPIM improves the communication process by offering a single communication channel using a standard protocol and reliable systems architecture.

Final Terms A document containing the specific terms and conditions of a security issued under Programme. It may also be referred to as a Pricing Supplement.

Fiscal Agent An agent appointed by the Issuer where no Trustee is appointed, to act as a Paying Agent and to perform certain administrative functions.

Fixed rate instruments Zero coupon securities and securities paying a fixed interest amount, usually with a final redemption payment pre-defined as a fixed percentage. The coupon and redemption details and features are fully determined in the T&C.

Fixing Date The date determined in the T&C of a security on which some or all of the elements of the rate/income calculation formula are known and the rate can be calculated. The calculation of the final payable amount may or may not be possible at this time.

Global Certificate Certificate representing an entire issue of securities. These may be temporary global certificates or permanent global certificates and in CGN or NGN form.

ICSD Account Holders Any entity holding an account with an ICSD.

Information Agent An agent appointed by the Issuer to disseminate information to holders and, in certain cases, to solicit responses.

M A R K E T P R A C T I C E B O O K

13

International Central Securities Depository (ICSD)

Securities settlement system for international securities. In this context, Clearstream Banking and Euroclear Bank.

International Securities (as used in this document) those securities primarily issued through and deposited with Clearstream Banking and Euroclear Bank.

IOA Issue Outstanding Amount.

ISIN A 12-digit alpha-numeric identifier assigned in accordance with ISO 6166 standards and used globally to uniquely identify a security.

Issue Date For non-syndicated issuance, the date on which the issue proceeds are paid to the Issuer and the securities are created and distributed to investors through the ICSDs.

Issuer An entity issuing securities.

Issuer/ICSD Agreement An Issuer-ICSD agreement must be signed by the issuer or its agent. The issuer must send a signed copy to Euroclear Bank and Clearstream Banking (Luxembourg) prior to the acceptance of any NGN/NSS intended to constitute ECB Eligible Collateral.

Issuing Agent (IA) An agent appointed by the Issuer to issue securities to the market and receive corresponding payments, if applicable, from the Dealer on the Issue Date.

Issuing and Paying Agent (IPA) An agent appointed by the Issuer to act as both the Issuing Agent and the Paying Agent under a Programme.

Lead Manager (LM) An entity appointed by the Issuer to structure and lead the placement of a Syndicated Issue.

Legal Counsel A law firm or lawyer appointed by an entity involved in the new issues or corporate actions process as its legal adviser.

Manual of Procedures (MOP) Appendix to the common depository agreement. Together with the contract, the documents governing the relationship between the ICSDs and their service providers (CD/CSP).

New Global Note (NGN) A form of Global Certificate which refers to the records of the ICSDs to determine the IOA.

New Safekeeping Structure (NSS)

A holding structure for international registered debt securities issued in CGN form jointly through Euroclear Bank and Clearstream Banking, to be recognised as potentially eligible collateral for Eurosystem monetary policy and intra-day credit operations.

M A R K E T P R A C T I C E B O O K

M A R K E T P R A C T I C E B O O K

14

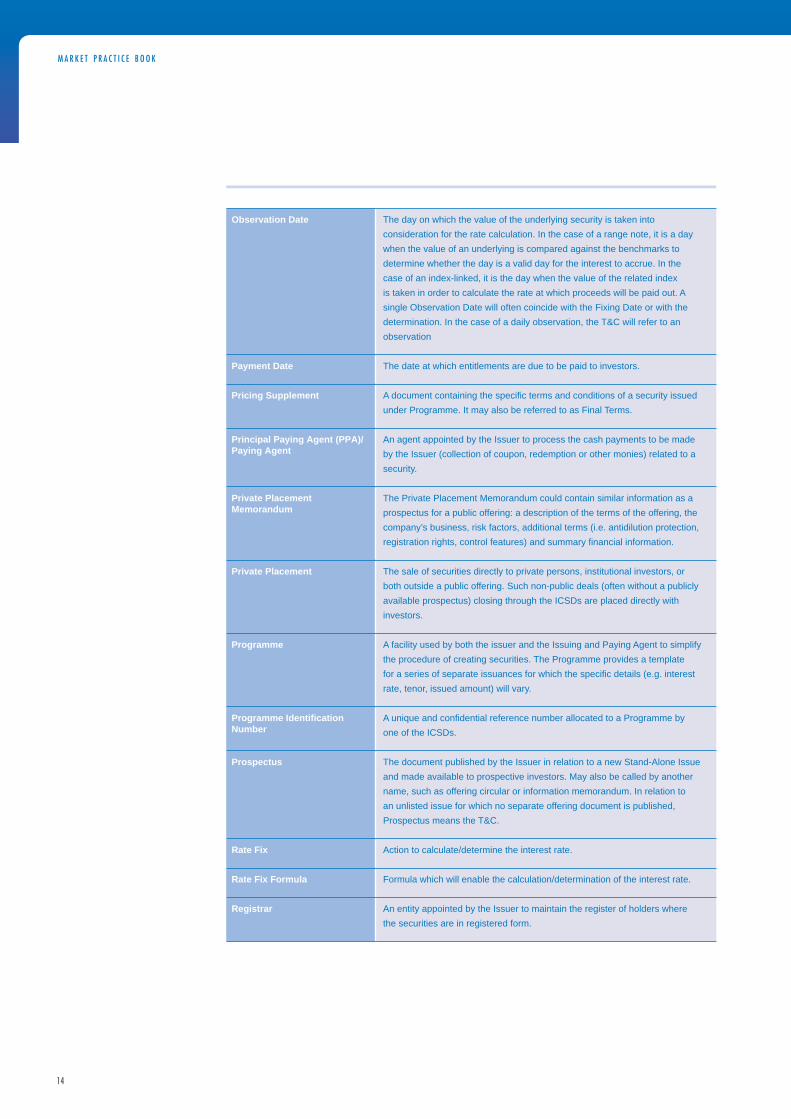

Observation Date The day on which the value of the underlying security is taken into consideration for the rate calculation. In the case of a range note, it is a day when the value of an underlying is compared against the benchmarks to determine whether the day is a valid day for the interest to accrue. In the case of an index-linked, it is the day when the value of the related index is taken in order to calculate the rate at which proceeds will be paid out. A single Observation Date will often coincide with the Fixing Date or with the determination. In the case of a daily observation, the T&C will refer to an observation

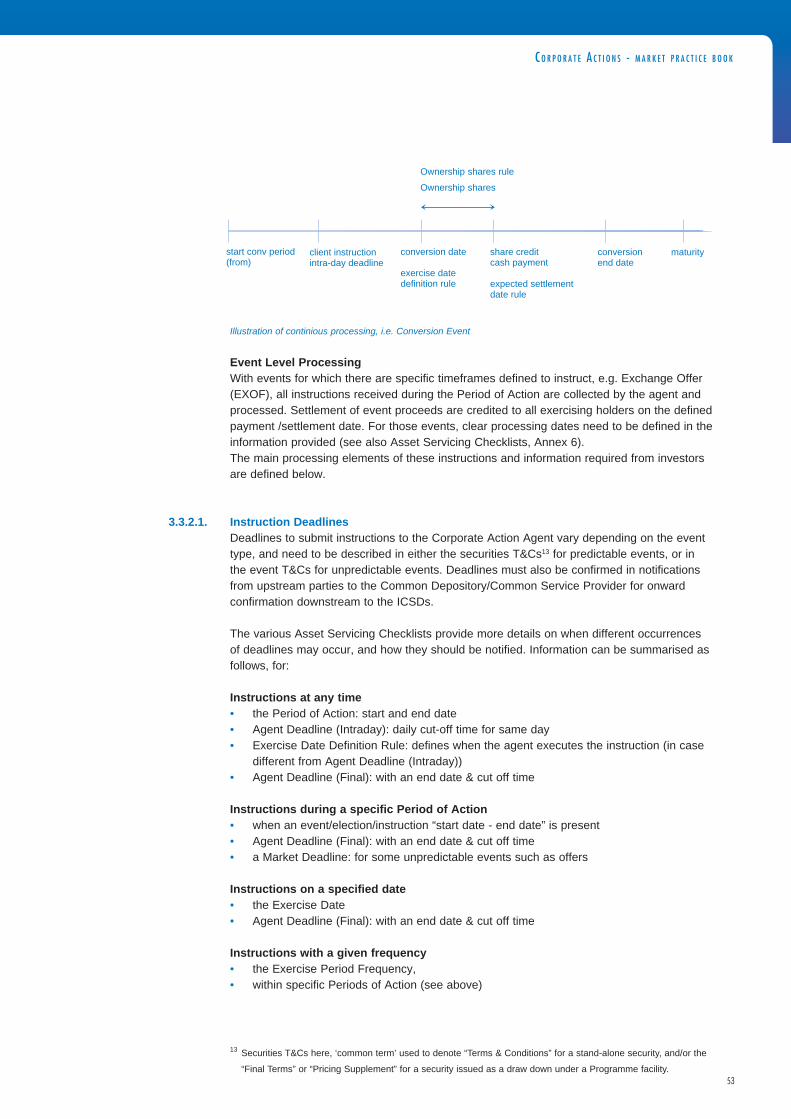

Payment Date The date at which entitlements are due to be paid to investors.

Pricing Supplement A document containing the specific terms and conditions of a security issued under Programme. It may also be referred to as Final Terms.

Principal Paying Agent (PPA)/Paying Agent

An agent appointed by the Issuer to process the cash payments to be made by the Issuer (collection of coupon, redemption or other monies) related to a security.

Private Placement Memorandum

The Private Placement Memorandum could contain similar information as a prospectus for a public offering: a description of the terms of the offering, the company’s business, risk factors, additional terms (i.e. antidilution protection, registration rights, control features) and summary financial information.

Private Placement The sale of securities directly to private persons, institutional investors, or both outside a public offering. Such non-public deals (often without a publicly available prospectus) closing through the ICSDs are placed directly with investors.

Programme A facility used by both the issuer and the Issuing and Paying Agent to simplify the procedure of creating securities. The Programme provides a template for a series of separate issuances for which the specific details (e.g. interest rate, tenor, issued amount) will vary.

Programme Identification Number

A unique and confidential reference number allocated to a Programme by one of the ICSDs.

Prospectus The document published by the Issuer in relation to a new Stand-Alone Issue and made available to prospective investors. May also be called by another name, such as offering circular or information memorandum. In relation to an unlisted issue for which no separate offering document is published, Prospectus means the T&C.

Rate Fix Action to calculate/determine the interest rate.

Rate Fix Formula Formula which will enable the calculation/determination of the interest rate.

Registrar An entity appointed by the Issuer to maintain the register of holders where the securities are in registered form.

M A R K E T P R A C T I C E B O O K

15

Regulation S (RegS) The Regulation S exemption under the Securities Act of 1933 exempts securities from SEC registration if the offering is made outside of the United States to non-US persons.

Reversal A reversal is a payment correction processed by ICSDs after a client account has been credited. This correction is due to wrong or late information from upstream intermediaries.

Rule 144A The Rule 144A exemption under the Securities Act of 1933 exempts securities from SEC registration if the offering is through a private placement in the United States to sophisticated institutional investors meeting the requirementsto be considered Qualified Institutional Buyers (QIBs).

Signing & Closing Agenda The guide to the conditions that must be satisfied, i.e. the documents that need to be produced and exchanged between the parties and the checklist or all other items that need to be addressed for the transaction to close.

Stand-Alone Securities Securities that are not issued under a Programme.

STP Straight-Through Processing.

Syndicated Issue A new issue distributed through a number of underwriters.

Terms and Conditions (T&C) The contractual provisions governing the securities set out in (or incorporated into) the global certificate and publicised in a Prospectus (for Stand-Alone issues) or a Base Prospectus supplemented by Final Terms (for issuance under Programme).

Trustee An entity appointed by the Issuer to act on behalf of investors in relation to the securities.

Value Date The date on which cash becomes available to the account owner.

Variable rate instruments Instruments for which the coupon and/or redemption payments are linked to one or several unknown components. These variable components are to be provided on a Fixing/ Determination Date. These can include, but are not limited to, variable coupons (range notes, forex-linked securities), early or partial redemptions, or payments related to structured finance securities or equity linked notes. The components are defined in the T&C but the payments resulting from the performance of these components have to be determined prior to the calculation of the actual coupon and/or redemption payment, which could also be an amount equal to zero.

Withholding Agent An agent appointed by local tax authorities and/or Issuers to retain withholding taxes on their behalf.

M A R K E T P R A C T I C E B O O K

16

B E S T P R A C T I C E S - M A R K E T P R A C T I C E B O O K

17

ISMAG best practices described in detail within the Market Practice Book are summarised in this section.

The best practices are defined mainly for upstream parties, i.e. Issuers, their Legal Counsel and their Agents, to address inefficiencies and risks linked to information provision processes, being:

• information coverage: quality & completeness• information timeliness• information processing

The adherence to and usage of the best practices, e.g. how to best draft documentation at issuance of an international security and/or how to best communicate the subsequent income and corporate actions notification information during the life cycle of this security, will to a large extent ensure an efficient and effective service to investors.

The ICSDs have developed a market framework to foster this adherence by the market.

Market FrameworkThe market framework has been developed to:• achieve improved market performance by optimizing end-to-end operational efficiencies,• increase market transparency towards both investors and issuers, and,• maintain market attractiveness and competitiveness.

ISMAG Adherence

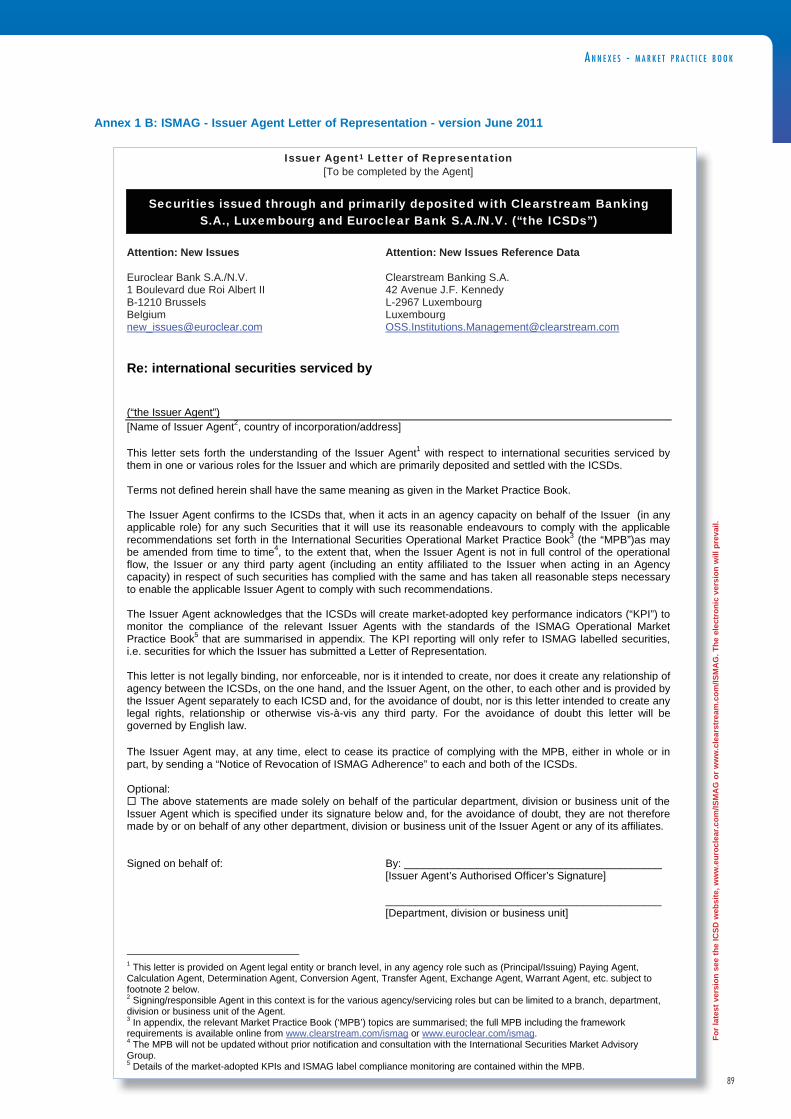

Issuers have the opportunity to market their engagement, acknowledge their adherence to the best practices, by providing the Issuer Letter of Representation (LoR) to both ICSDs, either on a blanket level, for all their future new issuances, or on a programme level, for all their future drawdowns. An “ISMAG Adherent” label will be assigned to their securities issued as from the defined effective date (closing date) and the ICSDs will publish the names of Adherent Issuers on their websites. The Issuer LoR is in Annex 11.

An “Exception Processing Notification” is available to exclude, at security (ISIN) or Programme level, securities structured in a manner that may prevent calculation Agents to provide information as per the defined benchmarks. These securities will be labelled as “ISMAG Exempt”. This “Exception Processing Notification” is in Annex 11.

The purpose of the “ISMAG Adherent” and “ISMAG Exempt” labels are two-fold;

1. to bring transparency to investors on their securities portfolio and related expected service levels, i.e. in line with ISMAG recommendations, and,

2. to increase servicing transparency for Issuers on their securities’ compliance vs. the best practices.

Issuers are encouraged to liaise with their appointed Agents by providing instructions and information to enable them to comply with the MPB best practices.

1. Market Framework and ISMAG Best Pract i ces Summary

1.1.

1.1.1.

1 Annex1: Revised June 2011 versions of the LORs. The latest versions, if any, are available from www.euroclear.

com/ISMAG or www.clearstream.com/ISMAG. These electronic versions will prevail.

M A R K E T P R A C T I C E B O O K - B E S T P R A C T I C E S

18

The Issuers’ Agents, in any agency role (such as Principal/Issuing Paying Agent, Calculation Agent, Determination Agent, Corporate Action Agent) also have the possibility to market their adherence to the best practices by providing an Issuer Agent Letter of Representation (Annex 11). Once such letter is received by both ICSDs, the Issuer’s Agent name will appear on their respective websites as “ISMAG Adherent”.

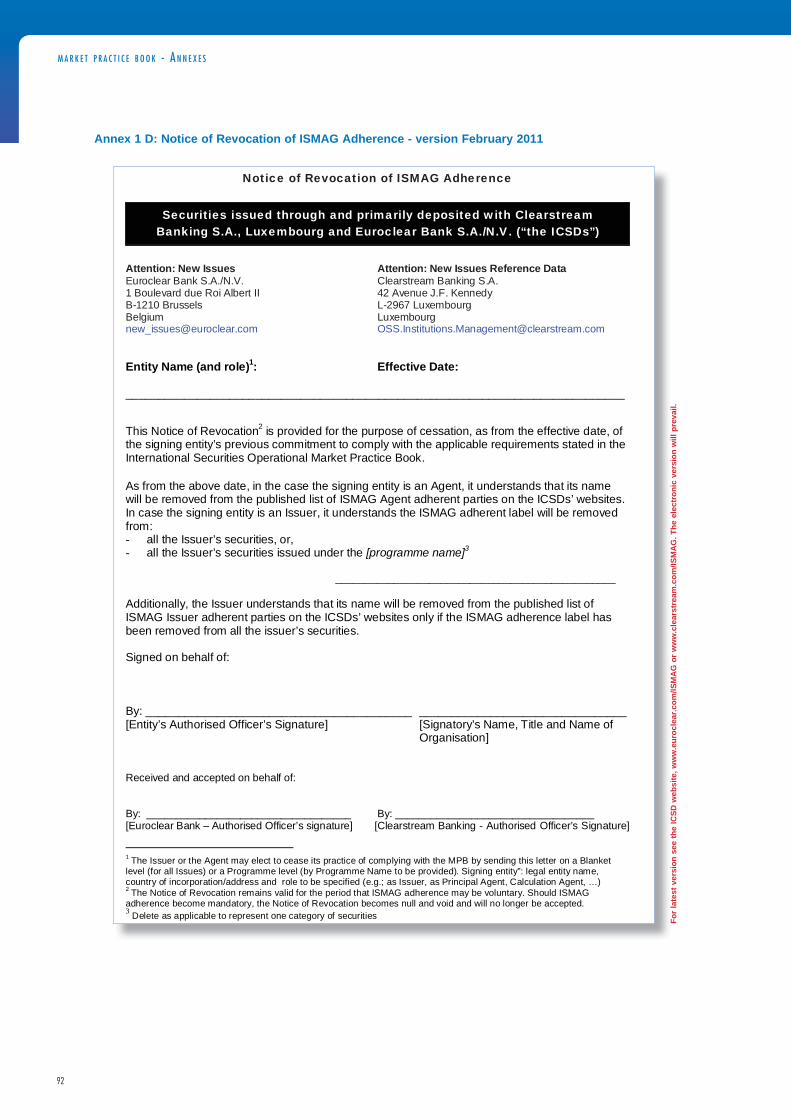

Both Issuers and Issuers’ Agents have the possibility to cease its practice of complying with the MPB, either in whole or in part, by sending a Notice of Revocation of ISMAG Adherence (Annex 11) to both ICSDs.

Market framework adherence starts on a voluntary basis but will become mandatory for all newly issued securities during 2012.

ISMAG Adherent securities compliance monitoring

To ensure adequate implementation of the best practices, the ICSDs will monitor those adherent Issuers and the Issuers’ agents that have signed LoRs, based on market-adopted key performance indicators (“KPI”) on the items listed in the appendices attached to the Issuer and Agent LoRs.

Targeted benchmarks have been defined for below KPIs, some others need to be further defined (TBD):

**These benchmarks will be re-assessed according to the measured performance levels with the ISMAG in the implementation phase. (The ISMAG implementation phase Terms of Reference is in Annex 14b.)

Compliance level results will not be published but will be shared with Issuers and their Agents in multilateral discussions, for the basis of improving the global performance of their issues.

Monitoring illustration: Timeliness of Rate Fixing on ISMAG Adherent securities - Monitoring Issuers’ Calculation Agents’ performance:

1.1.2.

KPIs that will be monitored as from 2011 2011** 2012** 2013**

Receipt of final issue documentation by Closing Date + 1 Business Day• from IPA (under programme)• from LM (stand alones)

90% 95% 98%

85% 90% 95%

Income rate fixing by Fixing/Determination + 1 BusinessDay (except for “ISMAG exempt” securities)• from Calculation Agent 89% 93% 96%

Income reversals • Volumes• Timeliness: from 15 CD to 10 CD after payment date

0.6% 0.45% 0.3%

New KPIs to be defined (mainly for Corporate Actioninformation coverage and timeliness vs MPB benchmarks)e.g. Final redemption in cash or shares fixing timeliness

TBD TBD TBD

B E S T P R A C T I C E S - M A R K E T P R A C T I C E B O O K

19

1.2.

In 2011: minimum benchmark is 89%

• Issuers compliance result for this KPI Issuers A & C, having global performance > 89% = compliant for this KPIIssuer B, having global performance of 86% < 89% = not compliant for this KPI

• Calculation Agents compliance result for this specific KPI: Calculation Agent 2 & 3, having global performance > 89% = compliant for this KPICalculation Agent 1 has a global performance of 82% < 89% = not compliant for this KPI

In case the results are systematically below the yearly pre-defined benchmark per KPI, i.e. for more than 3 quarters (9 months), and no clear action plan is shared by the Issuer and/or their Agents to improve performance, the following measures might be taken by the ICSDs:

1) Issuers/Agents names removed from the published list of ISMAG adherent parties2) Either,

a) removal of ISMAG Adherent label on each security, or,b) replacement of ISMAG Adherent label with non-compliant label.

ISMAG Best Practices SummaryAll ISMAG best practices are summarised below with further reference to the relevant section of the MPB for more detailed information. This summary complements the LoR appendices.

1. Relevant parties, i.e. external and/or internal legal counsels, to apply to the extent possible and whenever applicable, the ISMAG taxonomy/checklists and specific recommendations2 while drafting issuance documentation (draft and final), e.g. Programme base prospectus, final terms, etc., and corporate action event documentation.

• to ensure completeness and common understanding• see section 1.3. ISMAG taxonomy

2 ISMAG specific recommendation “do’s and dont’s” on Day Count Conventions, Interest Period Adjustments,

Record Dates, etc.

M A R K E T P R A C T I C E B O O K - B E S T P R A C T I C E S

20

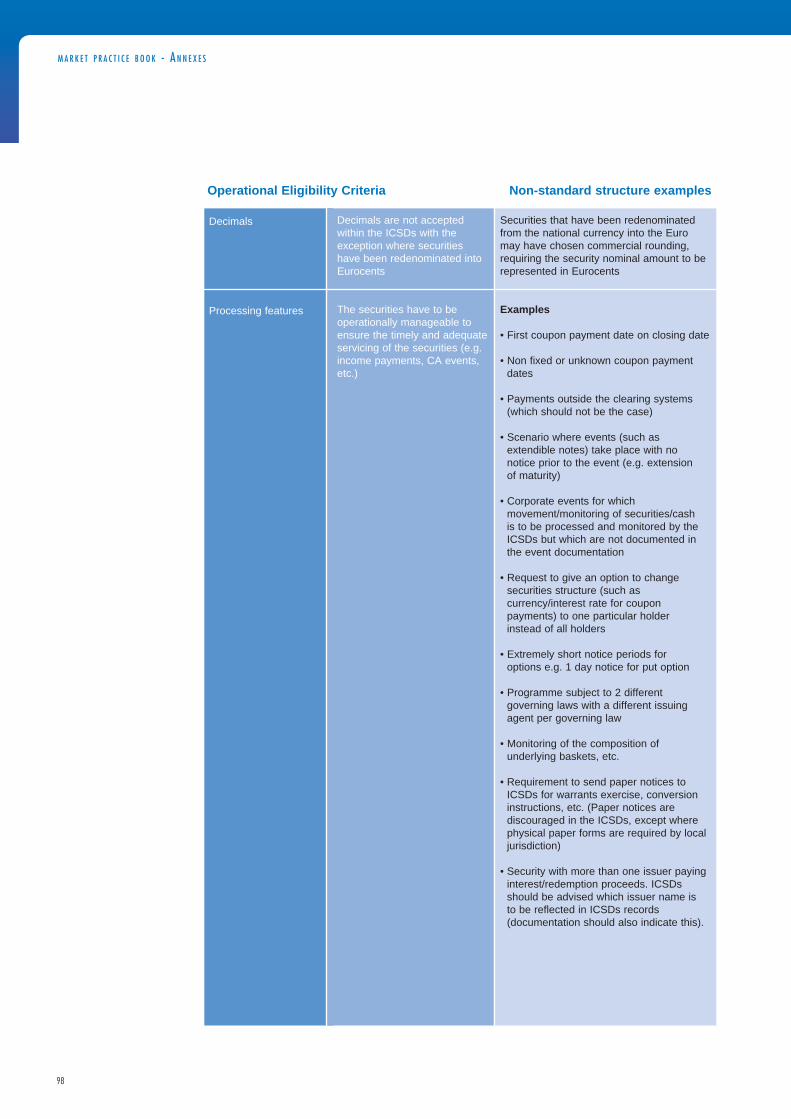

2. Relevant parties, i.e. external and/or internal legal counsels, Lead Manager, Arranger, Dealer, etc., to highlight, in the very early stage of issuance, to Issuing Agents and/or ICSDs any non-standard structure of the security for initial eligibility assessment e.g. such as additional paperwork requirements, Tefra certification on Registered issues, etc. (Annex 4 in MPB)

• to ensure efficient asset servicing to investors• see section 1.3. ISMAG taxonomy, section 2.2.2. New Issues draft documentation flows,

and Annex 4

3. Relevant parties, i.e. external and/or internal legal counsels, Lead Manager, Arranger, Dealer, etc., to provide the Issue Final Documentation on Closing/Issue Date to the Issuer Agent/ to the CD/CSP and no later than Closing/Issue Date + 1 Business Day to both ICSDs, using the naming convention for issuances under Programme and Stand-Alone securities.

• Benchmarks to ensure Information timeliness: see New Issues section 2.2.3.• Naming convention to ensure efficient document flows: see Annex 7• Lead Managers and Issuing Agents performance will be monitored by the ICSDs with

specific benchmarks to achieve (see 1.1)

4. Lead Managers to settle, to the extent possible and whenever applicable, syndicated closings during the same day distribution process, by organising an earlier closing, permitting the credit of securities in the ICSDs by 12:30 CET on the closing date

• to ensure earlier finality of settlement• see New Issues section 2.3.

5. Relevant parties i.e. Issuer, Lead Manager, Legal Counsel to provide any amended/updated documentation after issuance as soon as determined (e.g. in case of manifest errors and/or securities T&Cs changes), as per the listed information in the relevant checklist, to the Issuer Agent/Fiscal Agent/Trustee for onward delivery to the ICSDs/CD/CSP within same business day of receipt

• to ensure completeness: see Annex 6C “Security Change Value Notification” template, and

• timely receipt of information by investors: see New Issues section 2.2.3.

6. Calculation/Determination Agent, and any other relevant Agent, to provide the applicable accurate rate fixing notifications3 to their Paying Agent no later than fixing/determination date +1 Business Day providing all required information listed in the relevant checklist for onward delivery to the CD/CSP no later than one business day following receipt.

• to ensure completeness: see Annex 6B “Interest” template, and• timely receipt of information by investors: see Income section 4.2.2.• Calculation Agents performance will be monitored by Paying Agents with specific

benchmarks to achieve (see above)

3 Rate Fixing Notifications: applicable only to variable rate instruments, whether for (ir)regular income payments

or partial or final redemption payments.

B E S T P R A C T I C E S - M A R K E T P R A C T I C E B O O K

21

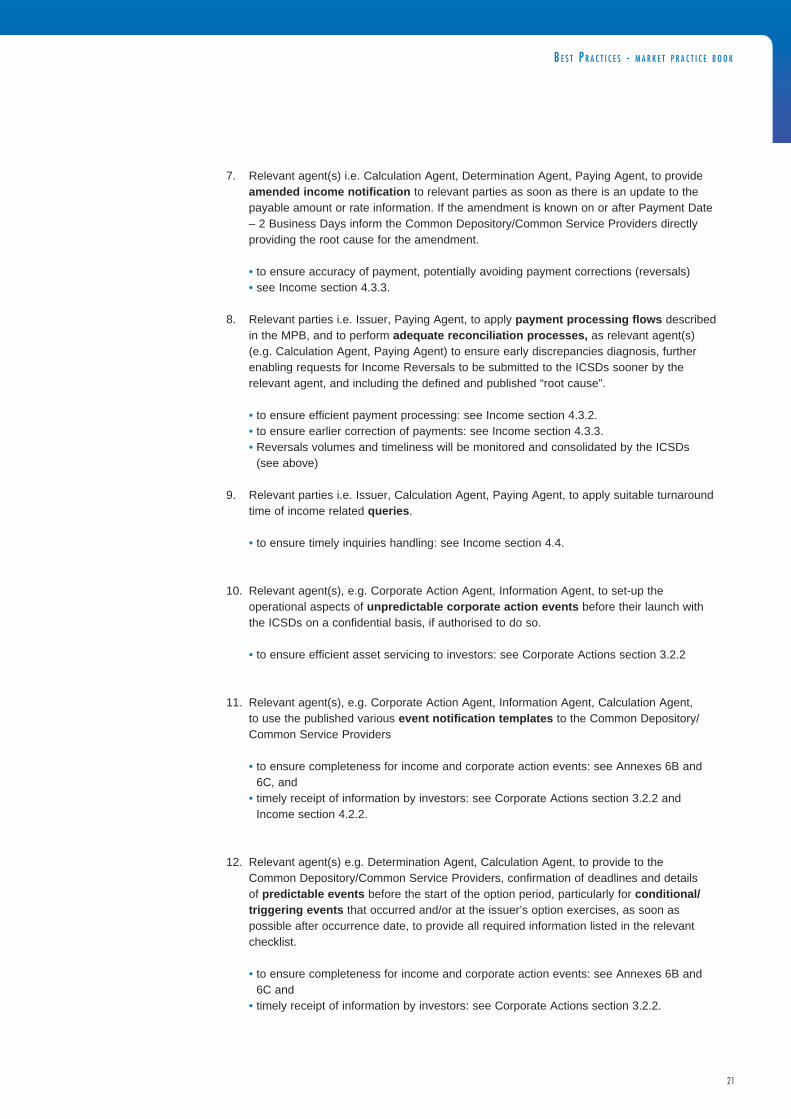

7. Relevant agent(s) i.e. Calculation Agent, Determination Agent, Paying Agent, to provide amended income notification to relevant parties as soon as there is an update to the payable amount or rate information. If the amendment is known on or after Payment Date – 2 Business Days inform the Common Depository/Common Service Providers directly providing the root cause for the amendment.

• to ensure accuracy of payment, potentially avoiding payment corrections (reversals)• see Income section 4.3.3.

8. Relevant parties i.e. Issuer, Paying Agent, to apply payment processing flows described in the MPB, and to perform adequate reconciliation processes, as relevant agent(s) (e.g. Calculation Agent, Paying Agent) to ensure early discrepancies diagnosis, further enabling requests for Income Reversals to be submitted to the ICSDs sooner by the relevant agent, and including the defined and published “root cause”.

• to ensure efficient payment processing: see Income section 4.3.2.• to ensure earlier correction of payments: see Income section 4.3.3.• Reversals volumes and timeliness will be monitored and consolidated by the ICSDs

(see above)

9. Relevant parties i.e. Issuer, Calculation Agent, Paying Agent, to apply suitable turnaround time of income related queries.

• to ensure timely inquiries handling: see Income section 4.4.

10. Relevant agent(s), e.g. Corporate Action Agent, Information Agent, to set-up the operational aspects of unpredictable corporate action events before their launch with the ICSDs on a confidential basis, if authorised to do so.

• to ensure efficient asset servicing to investors: see Corporate Actions section 3.2.2

11. Relevant agent(s), e.g. Corporate Action Agent, Information Agent, Calculation Agent, to use the published various event notification templates to the Common Depository/Common Service Providers

• to ensure completeness for income and corporate action events: see Annexes 6B and 6C, and

• timely receipt of information by investors: see Corporate Actions section 3.2.2 and Income section 4.2.2.

12. Relevant agent(s) e.g. Determination Agent, Calculation Agent, to provide to the Common Depository/Common Service Providers, confirmation of deadlines and details of predictable events before the start of the option period, particularly for conditional/triggering events that occurred and/or at the issuer’s option exercises, as soon as possible after occurrence date, to provide all required information listed in the relevant checklist.

• to ensure completeness for income and corporate action events: see Annexes 6B and 6C and

• timely receipt of information by investors: see Corporate Actions section 3.2.2.

M A R K E T P R A C T I C E B O O K - B E S T P R A C T I C E S

22

13. Relevant agent(s) e.g. Determination Agent, Conversion Agent, Calculation Agent, to provide announcements to the Common Depository/Common Service Providers during the lifecycle of an event (e.g. all updates or changes to the terms of an event such as suspension periods, changes to event deadlines, etc.) as soon as they are determined, providing all required information listed in the relevant checklists

• to ensure completeness: see Annexes 6B and 6C and• timely receipt of information by investors: see Corporate Actions section 3.3.

14. Relevant agent(s) e.g. Corporate Action Agent to provide to the Common Depository/ Common Service Providers event outcome notifications the same day, and at the latest 1 Business Day after the outcome determination date (e.g. result of a meeting/consent), providing all required information listed in the relevant checklist.

• to ensure completeness: see Annexes 6B and 6C and• timely receipt of information by investors: see Corporate Actions section 3.3.

15. Relevant agent(s), e.g. Corporate Action Agent, Conversion Agent, to provide to the Common Depository/Common Service Providers ICSD’s instruction reference in mark-up/mark-down instructions and provide confirmation when the exercise date is linked to an instruction for continuous processing events such as conversions, exercise of warrants, etc

• to ensure adequate follow-up of investors instructions, and• timely receipt of information by investors: see Corporate Actions section 3.3.

ISMAG taxonomyImplementation of ISMAG taxonomy and checklists by all upstream parties in the processing chain will ensure completeness and common understanding of information related to the servicing of international securities.

Generic recommendations

At Issuance of a security (or an event)

Improve communication between front, middle & back offices (including ICSDs) before issuance of specific structure securities and/or launch of unpredictable events; this maintains flexibility and innovation in the market, while avoiding asset servicing issues directly impacting end investors. Structures created by front office sales teams may be tailor-made for investors’ needs but are not necessarily manageable in a straightforward manner. These structures may, from a back office view, create unforeseen operational risks which impact end investors, e.g. some date fixing principles described in the T&C are not feasible in reality to enable timely income distribution or even use of funds on the due income payment date.

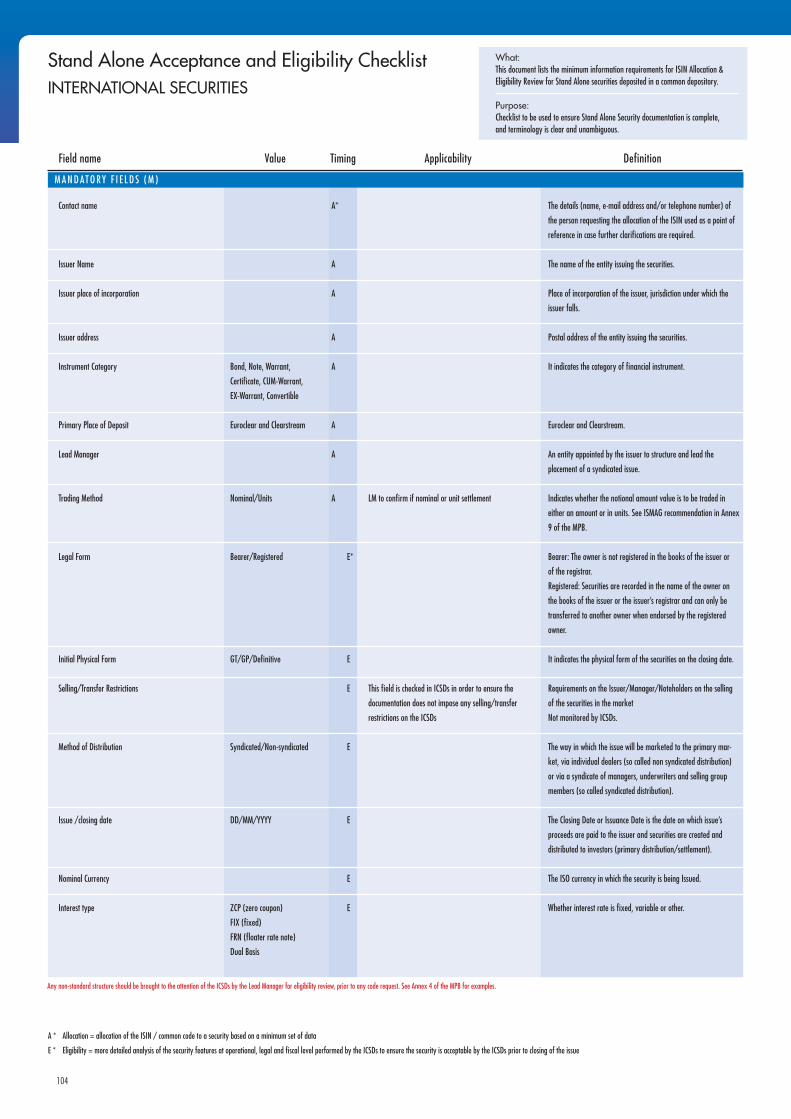

Ensure that draft information listed in securities or programme T&C is complete as per ISMAG Stand Alone Acceptance and Eligibility Checklist or Programme Acceptance Checklist (Annex 5).

1.3.

1.3.1.

B E S T P R A C T I C E S - M A R K E T P R A C T I C E B O O K

23

Ensure that final information listed in securities T&C is complete as per ISMAG Asset Servicing Checklists (Annex 6A), according to each event to be described; and as per ISMAG Specific recommendations “Do’s/Don’ts” on Paperwork, Day Count Conventions, Interest Period Adjustment, Record Dates, Payment Business Days, Units/Nominal terminology, etc.

For issuance under programme,

• avoid current reconciliation issues between the Final Terms and the Programme T&C; • ensure that Final Terms list information required as per the Asset Servicing Checklists

(Annex 6A), according to events to be described.

During the life cycle of the security

For ‘predictable’ corporate action and income events, ensure that information to be notified by upstream parties is complete as per ISMAG Asset Servicing Checklists (Annex 6B), according to each event to be described.

For ‘unpredictable’ corporate action events, ensure that information listed in draft and final events T&C is complete as per ISMAG Asset Servicing Checklists (Annex 6C), according to each ‘unpredictable’ event to be described (i.e. before launch date).

For ‘unpredictable’ corporate action events, ensure that information to be notified by upstream parties is complete as per ISMAG Asset Servicing Checklists (Annex 6C), according to each ‘unpredictable’ event to be described.

Specific recommendations

To clarify issuance and event documentation, a series of specific recommendations are set out below. For each of the topics listed, the recommendation aims at avoiding confusion, and reducing interpretation issues, e.g. by making explicit some features that are currently often implicit.

Naming Convention (Annex 7)

Naming Convention for Final Documents describes how to structure your e-mail subject and attachment name(s), some general e-mail guidelines, and includes the relevant contact details at the ICSDs. This convention is to be used when sending final New Issues documentation to the ICSDs by e-mail for more efficient transmission.

Day Count Convention (Annex 8)

Ensure that the issuance documentation • refers to the Day Count Convention using the ISMAG recommended short definition,

if using a ‘Top 6’ DCC;• uses long definitions which are in line with the ISMAG recommended long definitions,

if using a ‘Top 6’ DCC.

Adjustment of Coupon Period

DO always specify whether coupon period is adjusted or not adjusted, both for Fixed and Variable rate securities in the final documentation (Asset Servicing Checklists Annex 6A, field name: adjustment of interest period: Y = adjusted, N = unadjusted).

1.3.2.

M A R K E T P R A C T I C E B O O K - B E S T P R A C T I C E S

24

Fixed Coupon Amount

If the issuer intends to pay a fixed coupon amount, DO ensure that the issue documentation always specifies the coupon period as unadjusted. If the intention is to pay a fixed rate, but not a fixed coupon amount, then DO NOT include a fixed coupon amount, and always specify whether the coupon period is adjusted or not.

Paperless instructions

• DO NOT include requirements for (or examples of) paper form instructions in issue or event documentation, wherever possible (so avoid non-electronic communication means for all information required from investors);

• DO highlight at issuance whether paper is required by local jurisdiction as a non standard structure;

• DO use recommended standard wording in the T&C: ‘Securities may be only exercised/ exchanged/converted/… in accordance with the rules and operating procedures of Euroclear and Clearstream.’

Units / Nominal (Annex 9)

• DO NOT mix Unitary and Nominal terminology within the same security documentation

• DO ensure that the issuance documentation; - Clearly indicates whether Units or Nominal is being used, by providing the binary field ‘Trading Method’; - Provides the relevant fields as described in the example in annex 9.

Non-English documentation

ISMAG recommends that all international new issues documentation submitted to the ICSDs for the purpose of determining issuance eligibility and/or ISIN assignment; are clearly documented in English. Deviation from the above recommendation is subject to the discretion of the ICSDs new issues teams and may result in the issue being assessed as ineligible due to the inability of the ICSDs to adequately assess and understand the content of the documentation and inherent terms and conditions.

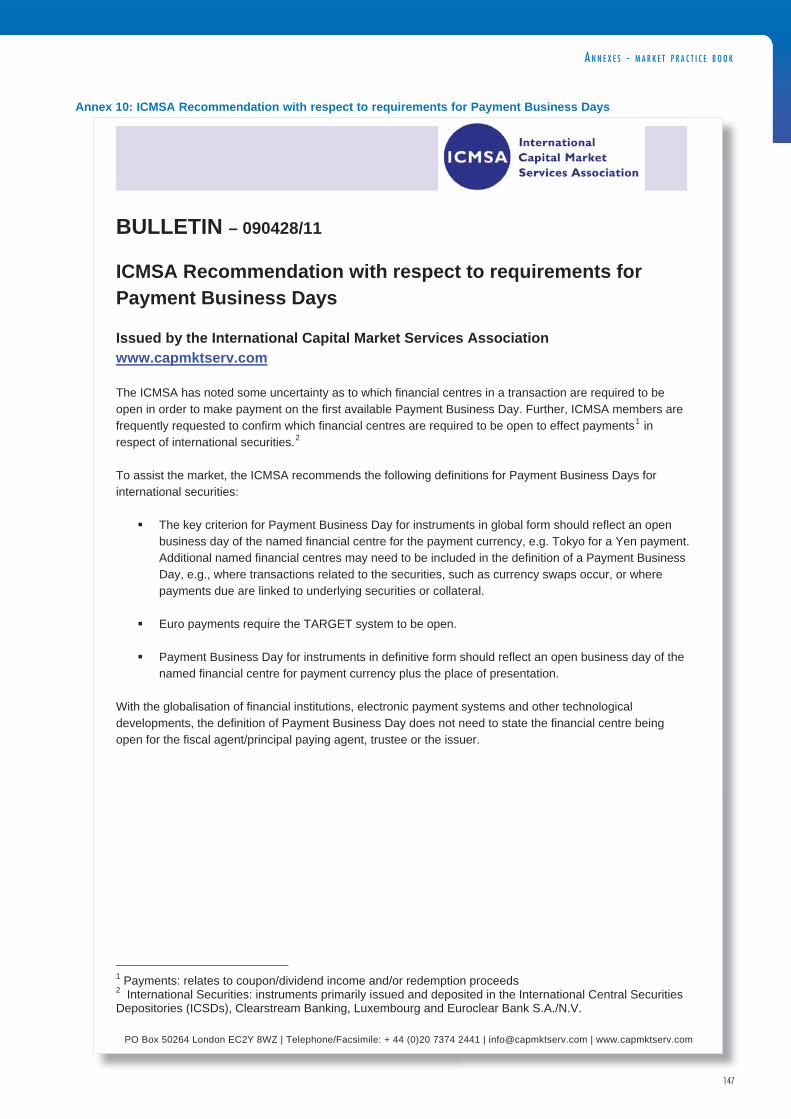

ICMSA Recommendation on Payment Business Days (Annex 10)

For instruments in global form: DO reflect an open business day of the named financial centre for the payment currency, e.g. Tokyo for a Yen payment;

• Additional named financial centres may need to be included in the definition of a Payment Business Day, e.g. where transactions related to the securities, such as currency swaps occur, or where payments due are linked to underlying securities or collateral;

• For Euro payments: the TARGET system needs to be open.

B E S T P R A C T I C E S - M A R K E T P R A C T I C E B O O K

25

For instruments in definitive form:

• reflect an open business day of the named financial centre for payment currency and the place of presentation;

DO NOT state the financial centre being open for the fiscal agent/principal paying agent, trustee or the issuer.

ICMSA Recommendation on Record Dates (Annex 11)

• DO NOT, as issuer of bearer securities, - include definitions referring to a record date, or - create provisions within the governing documentation referring to a snapshot date different from Payment Date -1 Business Day;

• DO, for all instruments in global registered form with Closing Dates after 1st January 2010 word legal documentation with a record date as at the ‘close of the Business Day (in the ICSDs) prior to the Entitlement Date’.

ICMSA recommendation on Partial Redemption (Annex 12)• In new Stand–alone Issues Documentation for which the Issuances are intended to

be maintained in Permanent Global Form, the application of the “Pool Factor” should be utilised as the standard procedure for all cases where a Partial Redemption of the securities can occur.

• In updating Programme Documentation, Issuers are encouraged through their Programme Arrangers and Legal Advisers, to effect the appropriate amendments to the constituting documentation, in order to provide for the “Pool Factor” to be utilised for all future issuances, where appropriate. If not updated, consideration should be given to an express provision in relation to any appropriate new issue.”

Confidential Securities (Annex 13)

To assist the primary market with determining the proper use of the confidentiality flag, the ICSDs feel it is important to underline the associated consequences of identifying a secu-rity as confidential vis-à-vis the market. Such securities, when created within the ICSDs:

• are not displayed to the ICSD’s clients via their respective websites or to external third party entities that access these websites

• are suppressed from any ICSD data feeds to third party data vendors, thus ensuring the security is not available or visible to any external parties.

The ICSDs wish to avoid data discrepancies where:

• securities marked as confidential are listed on a Stock Exchange, this results in the security being made available to third parties, either directly by the Stock Exchange themselves or via third party data vendors that receive a data feed from the Stock Exchange.

M A R K E T P R A C T I C E B O O K

26

• securities are identified as confidential to the Paying Agent and ICSDs, but details of the issuance have been provided to third party data vendors (e.g. Bloomberg, Reuters and Telekurs)

• one ICSD is requested to make an issue confidential, but the other ICSD is not, this impacts the consistency of the reference data between the two ICSDs and the availability of the security details to external parties.

The ICSD’s therefore recommend that:1. publicly listed securities are not created as confidential. 2. the request of confidentiality be made consistently to all intermediaries involved in the

issuance chain. 3. appropriate internal procedures are in place to advise the Issuing and Paying Agent

for the issue and/or the ICSDs when the confidential marker must be removed.

N E W I S S U E S - M A R K E T P R A C T I C E B O O K

27

2. New Issues

ScopeThe scope of this chapter is related to the timely dissemination of full and complete new issues draft and final documentation and the primary distribution of securities.

Information flowNew issues documentation description

Clear1 issuance documentation is critical for:

• the Issuer to ensure that its rights and obligations are clearly defined;• all intermediaries (Issuer’s Agents/CD/CSP/ICSDs) to enable timely settlement and

effective asset servicing (e.g. corporate actions and income events), throughout the lifetime of a security; and

• the investors to make appropriate investment decisions.

New issuance documentation encompasses both the contractual and operational documents. The contractual documentation governs the responsibilities of the Issuer and its Agents to service the securities (e.g. the T&C, the Agency agreement,…). In case of conflicts, the legal documents always prevail. The operational documentation, describing all asset servicing critical information are also needed for efficient processing (e.g. taxation information,…).

Typically, from an operational perspective, the documents of reference are:

for Stand-Alone securities:• the Prospectus or Offering Circular, Placement Memorandum or other relevant

documentation; • for private placement issues, the Private Placement Memorandum or the legal T&C;

for issuance under Programme, documentation is required at two levels:• Programme: the Base Prospectus or Offering Circular which provides the common set

of T&C for any issuance under such a Programme;• Issuance under Programme: the Pricing Supplement or Final Terms which contain the individual characteristics of each particular security defined previously.

Draft documentation

Prior to the Closing Date2, for Stand-Alone securities and for issuance under Programme, Dealers, Lead Managers and Agents are requesting ISIN and/or Common Code allocation from the ICSDs, based on preliminary and provisional (‘draft’) securities information.

For issuance under Programme, the ICSDs also provide the IPA with (a) Programme identification number(s) that is (are) allocated at the level of the Programme and that is (are) conditional upon receipt of the provisional (‘draft’) Programme documentation.

2.1.

2.2.2.2.1.

2.2.1.1.

1 Please refer to Chapter 1 section 1.3. on information quality & completeness and also refer to the EU Prospectus

Directive art. 5 (see Annex 3).

2 Closing Date (for Syndicated Issuance) or Issue Date (for non-Syndicated Issuance).

M A R K E T P R A C T I C E B O O K - N E W I S S U E S

28

2.2.1.2.

The ‘draft’ information serves two purposes:

• it enables the ICSDs to allocate:- the ISIN and/or Common Code for Stand-Alone securities; and - Programme Identification number(s) and subsequently ISIN and/or Common Codes for

issuance under Programme; • it enables the ICSDs to assess the eligibility in their respective settlement systems.

Features and Terms of a security could be subject to change until the documentation is final, in which case the relevant parties need to be informed.

Draft information flows are:

for Stand-Alone securities: • the LM providing the draft prospectus to the ICSDs as soon as it is available if unusual

features in the structure require an eligibility review, or in any case at the latest on ISIN and/or Common Code allocation request;

for issuance under Programme: • for the allocation of a Programme Identification number, the IPA must provide the ICSDs

with the draft Base Prospectus of the Programme (including the draft form of Pro Forma Final Terms); and

• for the allocation of the ISIN and/or Common Code of an issuance under Programme, the IPA should provide the ICSDs with draft Final Terms if the issuance under Programme has a non-standard structure and/or for complex tax regimes detailed.

For end-to-end flows please refer to section 2.2.2. New issues draft documentation flows.

Final documentation

Documents are considered ‘final’ if:• for legal documents: the version is conformed or certified;• for operational documents: the version sent by the party responsible for its creation,

as per the ICMA Guidance Note is noted as “Final”.

The ‘final’ operational information serves to enable timely settlement and effective asset servicing of the securities.

From an ICSD perspective, final information flows are:

for Stand-Alone securities: • the LM providing the legal documentation and the final prospectus to the ICSDs at the

latest on closing date +1 Business Day, as per the ICMA Guidance Note;

for issuance under Programme: • the IPA providing the ICSDs with the final Base Prospectus of the Programme on

closing date +1 Business Day of the first issuance under Programme, as per the ICMA Guidance Note; and

• the IPA providing the ICSDs with the Final Terms of the issuance under Programme on closing date +1 Business Day, as per the ICMA Guidance Note.

N E W I S S U E S - M A R K E T P R A C T I C E B O O K

29

For end-to-end flow please refer to section 2.2.3. New issues final documentation flows.

For the sending of Final Documentation, please refer to the Naming Convention recommendation (see Annex 7).

Updated documentation after Closing Date

Updates to documentation after Closing Date should be provided in an easily analysable and comprehensible form, as per art.20 of the EU Prospectus Directive (see Annex 3).

It must be communicated by the Issuer or its appointed party (LM/Legal Counsel/PPA) to all intermediaries (Issuer’s Agents/CD/CSP/ICSDs) to allow for timely and effective asset servicing throughout the lifetime of a security, so that investors can make the appropriate investment decisions.

Updates to final T&C after Closing Date are usually processed via the following methods:

• Manifest errors3

• Consent of investor 4

• Noteholders’ meetings

Updates and changes linked to information outside the scope of the T&C should be communicated in advance by the Issuer to the intermediaries (Issuers’ Agents/CD/CSP/ICSDs) for an impact assessment in terms of asset servicing.

3 In this Market Practice Book the term ‘manifest errors’ shall include, besides errors obvious on the face of the

document, any other modifications made pursuant to the Trustee/Agent power under T&C (without holder consent).

4 In closely held issues it is possible to get all investors to consent without the need for a meeting.

2.2.1.3.

M A R K E T P R A C T I C E B O O K - N E W I S S U E S

30

New issues draft documentation flows

The end-to-end operational flows for draft documentation provision are illustrated below, both for Stand-Alone securities and for issuance under Programme.For ICMA constituency: please also refer to the ICMA Guidance Note (see Annex 2).

Documentation flow for Stand-Alone securities codes allocation & eligibility

ICSDSD

CD/CSP

Issuer

Agent(s)

Lead Manager

Legal Counsel

a’

d e c

L l

a

a’

b

a

a

Issuer

Issuer

Legal Counsel

a

a

a’

Initiator Recipient Timing

LM/Legal

Counsel

Agent(s)

LM/Agent(s)

At the Issuer’s

discretion

At the Issuer’s

discretion

In the very early

stage of issuance

or before the fixing

of pricing details

(generally on the

Closing Date -5

Business Days) 5

and prior to the

listing request 6

if any

Actions

• Appoint LM, Legal Counsel to structure and sell

the security

• Agree key terms of the issue (including choice of

form, i.e. CGN or NSS, or NGN

• Drafting of the terms in an easily analysable and

comprehensible manner and wherever possible, using

standard terms and formats to allow easy identification

and understanding of all relevant securities features

(see Chapter 1 section 1.3.)

• Appoint Agent(s)

• Draft and review all relevant legal documentation:

the T&C including the minimum requirements

(cf. Stand-Alone Acceptance and Eligibility Checklist in

Annex 5) for ISIN and/or Common Code allocation7 &

• Drafting of the terms in an easily analysable and

comprehensible manner and wherever possible, using

standard terms and formats to allow easy identification

and understanding of all relevant securities features

(see Chapter 1 section 1.3.)

5 Exceptions to this timing may occur, ex: for short pricing issues.

6 Please refer to the respective Stock Exchange listing rules for the relevant timing requirements.

7 For debt type instruments, the ISIN request will be sent to the clearing system where the security is deposited

whereas for equity type instruments, the ISIN needs to be requested to the numbering agency of the country of

incorporation of the underlying security/issuer.

2.2.2.

2.2.2.1.

N E W I S S U E S - M A R K E T P R A C T I C E B O O K

31

LM

LM

LM

PPA

ICSDs

ICSDs

LM

LM

b

b

Initiator Recipient Timing

ICSDs

ICSDs

ICSDs

ICSDs

LM

CD/CSP

Agent(s)

ICSDs

In the very early

stage of issuance

and prior to the

listing request if any

At the code

allocation request

or immediately after

the fixing of pricing

details (generally on

the Closing Date -5

Business Days)

On the Closing Date

-1 Business Day

On the Closing Date

-1 Business Day

On acceptance

Within 1 working

day (24 hours) of

receipt10

On acceptance

On acceptance

On occurrence and

before closing

Actions

• Inform the ICSDs of any non-standard structure of the

security for initial eligibility assessment

(cf. Non-standard/Unusual Structures in Annex 4)

• Provide the draft Prospectus/Offering Circular/

Placement Memorandum8 of the security including the

minimum requirements (cf. Stand-Alone Acceptance and

Eligibility Checklist in Annex 5) for ISIN and/or Common

Code allocation & eligibility review

• If incomplete (e.g. closing date, maturity date, nominal

amount and currency, issue price, denomination are

missing) also provide the complete term sheet

Additional requirements for NGNs:

• Provide an executed Issuer-ICSD Agreement (also for NSSs)

• Provide a copy of the usual legal opinion on validity

and enforceability of securities, if required9

• Provide an Effectuation Authorisation (also for NSSs)

• For NGNs & NSSs, provide the CSK election form

• Perform the 2 steps of the acceptance process, i.e.

ISIN and/or Common Code allocation & eligibility

review11

• Appoint the Common Depository as per Mandate

Allocation Rules (or CSP & CSK) and advise LM

• Advise Common Depository (or CSP & CSK)

• Relay ISIN, Common Code, Common Depository

(or CSP & CSK) information

• Highlight pre-closing security features updates, if any,

together with the last version of the draft document12

8 Some instruments, such as Warrants, Equity Linked Notes, unlisted/ undocumented notes, do not have a draft

Prospectus. Those instruments, although issued as Stand-Alone securities, are very similar to issuance under

Programme flows described hereafter. In case a draft Prospectus does not exist, codes allocation & eligibility are

performed on a complete draft term sheet.

9 The LM has the possibility to consult the list of jurisdictions already covered by a legal opinion on both Euroclear

and Clearstream websites.

10 Dependent on any eligibility issues that may arise that requires further clarification from the LM.

11 Upon specific request by the LM, the first step, i.e. code allocation, could be performed independently of the

eligibility review. However, the eligibility review would still need to take place to complete the acceptance of the

security. The ICSDs expect the LM to handle the primary distribution of such securities.

12 For efficiency purposes, the number of draft versions sent should be limited (unless a structure change is taking

place) and focus on the last version of the draft Prospectus to be received in time to ensure eligibility.

b

b

e

c

b

d

M A R K E T P R A C T I C E B O O K - N E W I S S U E S

32

Documentation flow for new Programme set up and subsequent issuance under Programme codes allocation & eligibility

Documentation flow for Programmes at establishment

2.2.2.2.

2.2.2.2.1.

ICSDSD

Issuer IPA

Arranger

Legal Counsel

b

b

L l

a

c

a

a

Issuer

Arranger/

Legal Counsel

Arranger

a

b

Initiator Recipient Timing

Arranger/

Legal

Counsel/ IPA

IPA

IPA

At the Issuer’s

discretion

In the very early

stage of issuance

or at the latest

10 Business

Days before the

signing date of the

Programme and

prior to the listing

request13 if any

In the very early

stage of issuance

and prior to the

listing request if any

Actions

• Appoint Arranger, Legal Counsel, IPA, Dealer(s)

• Agree key terms of the Programme

• Drafting of the terms in an easily analysable and

comprehensible manner and wherever possible, using

standard terms and formats to allow easy identification

and understanding of all relevant securities features

(see Chapter 1 section 1.3.)

• Draft and review all relevant legal documentation:

the terms of the Programme including minimum

requirements (cf. Programme facility acceptance

checklist) for Programme number(s) allocation &

eligibility review, the Agency Agreement, the Issuer-

ICSDs Agreement per Issuer under the Programme

(for NGNs/NSS), Dealer Agreement, …

• Drafting of the terms in an easily analysable and

comprehensible manner and wherever possible, using

standard terms and formats to allow easy identification

and understanding of all relevant securities features

(see Chapter 1 section 1.3.)

• Inform the IPA of any non-standard structure of the

Programme (cf. Non-standard/Unusual Structures in

Annex 4)

d

13 Please refer to the respective Stock Exchange listing rules for the relevant timing requirements.

N E W I S S U E S - M A R K E T P R A C T I C E B O O K

33

IPA

IPA

ICSDs

IPA

IPA

c

Initiator Recipient Timing

ICSDs

ICSDs

IPA

ICSDs

ICSDs

As soon as advised

by the Arranger

At the Programme

acceptance

request, or at the

latest 10 Business

Days before the

signing date of the

Programme and

prior to the listing

request if any

On Programme

acceptance

Within 3 working

days of receipt16

On Programme

acceptance

On occurrence

and before the

signing date of the

Programme

Actions

• Inform the ICSDs of any non-standard structure of the

Programme (cf. Non-standard/Unusual Structures in

Annex 4)

• Provide the draft Programme Base Prospectus14,

and the draft pro forma Final Terms15, including the

minimum requirements (cf. Programme Acceptance

Checklist in Annex 5) for Programme number(s)

allocation & eligibility review

• Review eligibility of the Programme and provide

Programme number(s)

• Appoint Common Depository as per Mandate

Allocation Rules (or CSP & CSK)

Additional requirements for NGNs:

• Provide an executed Issuer-ICSDs Agreement per issuer

for the Programme if allowing for NGN issuance (also for

NSSs)

• Provide a copy of the legal opinion on validity and

enforceability of securities issued under the Programme,

if required17

• Provide CSK election form (also for NSSs)

• Highlight pre-signing updates, if any, together with

the last version of the draft document18

c

c

c

c

14 In case a draft Base Prospectus is incomplete or does not exist, the Programme facility acceptance is performed

on alternative documents such as the Agency Agreement, Trust Deed,… with additional information related to

specific fields (e.g. taxation details, selling restrictions, final terms template, issuer details, etc.). However, the

eligibility review should be limited to a minimum number of documents.

15 Draft pro forma Final Terms are needed at this stage to ensure that all required information will be made available at

drawdown level, is presented in a structured way, and is consistent with the information provided at programme

level.

16 Dependent on any eligibility issues that may arise that requires further clarification from the IPA.

17 The IPA has the possibility to consult the list of jurisdictions already covered by a legal opinion on both Euroclear

and Clearstream websites.

18 For efficiency purposes, the number of draft versions sent should be limited (unless a structure change is taking

place) and focus on the last version of the draft Base Prospectus to be received in time to ensure eligibility.

M A R K E T P R A C T I C E B O O K - N E W I S S U E S

34

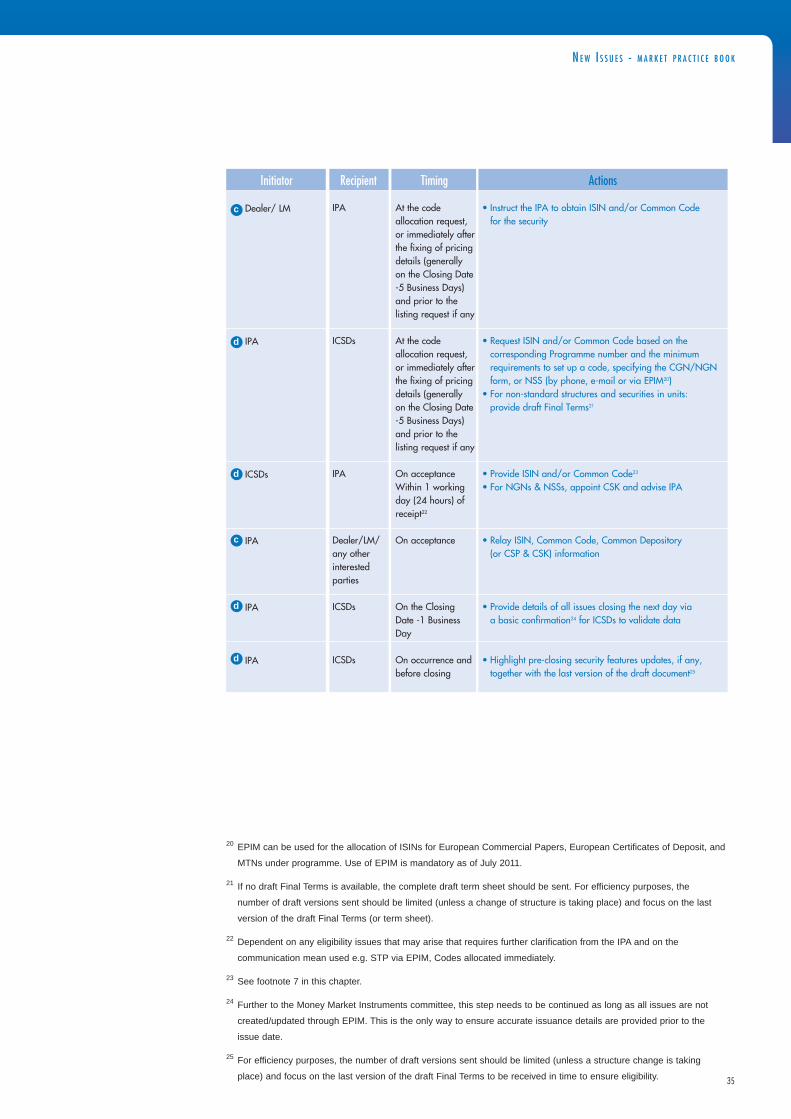

Documentation flow for issuance under Programme at acceptance 2.2.2.2.2.

ICSDSD

Issuer IPA

Dealer/LM*

Legal Counsel

c

b

L l

a

d

a

a

b

* LM for syndicated MTNs

Initiator Recipient Timing Actions

Issuer

Legal Counsel

Dealer/ LM

IPA

a

b

At the Issuer’s

discretion

In the very early

stage of issuance

or before the fixing

of pricing details

(generally on the

Closing Date -5

Business Days), and

prior to the listing

request if any

In the very early

stage of issuance

or before the fixing

of pricing details

(generally on the

Closing Date -5

Business Days), and

prior to the listing

request19 if any

As soon as advised

by the Dealer/LM

• Appoint LM (for Syndicated Issues)

• Agree key terms of the issue

• Drafting of the terms in an easily analysable and

comprehensible manner and wherever possible, using

standard terms and formats to allow easy identification

and understanding of all relevant securities features

(see Chapter 1 section 1.3.)

• Draft and review all relevant legal documentation,

including the minimum requirements (cf. CP/CD/MTNs

acceptance checklist) for ISIN and/or Common Code

allocation

• Drafting of the terms in an easily analysable and

comprehensible manner and wherever possible, using

standard terms and formats to allow easy

identification and understanding of all relevant

securities features (see Chapter 1 section 1.3.)

• Highlight any special features of the security

(e.g. complex tax regimes, securities in units, paper form

requirements, etc.)

(cf. Non-standard/Unusual Structures in Annex 4)

• Highlight any special features of the security

(e.g. complex tax regimes, securities in units, paper form

requirements, etc.)

(cf. Non-standard/Unusual Structures in Annex 4)

c

Dealer/LM

Legal

Counsel/ IPA

Dealer/ LM/

IPA

IPA

ICSDsd

19 Please refer to the respective Stock Exchange listing rules for the relevant timing requirements.

N E W I S S U E S - M A R K E T P R A C T I C E B O O K

35

20 EPIM can be used for the allocation of ISINs for European Commercial Papers, European Certificates of Deposit, and

MTNs under programme. Use of EPIM is mandatory as of July 2011.

21 If no draft Final Terms is available, the complete draft term sheet should be sent. For efficiency purposes, the

number of draft versions sent should be limited (unless a change of structure is taking place) and focus on the last

version of the draft Final Terms (or term sheet).

22 Dependent on any eligibility issues that may arise that requires further clarification from the IPA and on the

communication mean used e.g. STP via EPIM, Codes allocated immediately.

23 See footnote 7 in this chapter.

24 Further to the Money Market Instruments committee, this step needs to be continued as long as all issues are not

created/updated through EPIM. This is the only way to ensure accurate issuance details are provided prior to the

issue date.

25 For efficiency purposes, the number of draft versions sent should be limited (unless a structure change is taking

place) and focus on the last version of the draft Final Terms to be received in time to ensure eligibility.

c

d

Initiator Recipient Timing Actions

Dealer/ LM

IPA

ICSDs

IPA

IPA

IPA

At the code

allocation request,

or immediately after

the fixing of pricing

details (generally

on the Closing Date

-5 Business Days)

and prior to the

listing request if any

At the code

allocation request,

or immediately after

the fixing of pricing

details (generally

on the Closing Date

-5 Business Days)

and prior to the

listing request if any

On acceptance

Within 1 working

day (24 hours) of

receipt22

On acceptance

On the Closing

Date -1 Business

Day

On occurrence and

before closing

• Instruct the IPA to obtain ISIN and/or Common Code

for the security

• Request ISIN and/or Common Code based on the

corresponding Programme number and the minimum

requirements to set up a code, specifying the CGN/NGN

form, or NSS (by phone, e-mail or via EPIM20)

• For non-standard structures and securities in units:

provide draft Final Terms21

• Provide ISIN and/or Common Code23

• For NGNs & NSSs, appoint CSK and advise IPA

• Relay ISIN, Common Code, Common Depository

(or CSP & CSK) information

• Provide details of all issues closing the next day via

a basic confirmation24 for ICSDs to validate data

• Highlight pre-closing security features updates, if any,

together with the last version of the draft document25

IPA

ICSDs

IPA

Dealer/LM/

any other

interested

parties

ICSDs

ICSDs

c

d

d

d

M A R K E T P R A C T I C E B O O K - N E W I S S U E S

36

New issues final documentation flows

The end-to-end operational flows for final documentation provision are illustrated below, both for Stand-Alone securities and for issuance under Programme.For ICMA constituency: please also refer to the ICMA Guidance Note (see Annex 2).

Documentation flow for Stand-Alone securities at issuance

ICSDSD

CD/CSP

Fiscal AgentPPA

Lead Manager

Legal Counsel

a

b

c

L l

a

c

Legal Counsel

Fiscal Agent/PPA

LM

a

b

c

Initiator Recipient Timing

LM/Fiscal

Agent/PPA

CD/CSP

CD/CSP

/PPA

/ICSDs

At the latest on the

Closing Date

On the Closing

Date

On the Closing

Date and at the

latest on the Closing

Date +1 Business

Day

Actions

• Provide the Global Certificate and the final T&C to

Fiscal Agent/PPA/LM

• Provide the authenticated Global Certificate and the

final T&C

• Provide the legal documents and the final Prospectus

of the security (for the sending of Final Documentation,

please refer to the Naming Convention recommendation in

Annex 7)

2.2.3.

2.2.3.1.

N E W I S S U E S - M A R K E T P R A C T I C E B O O K

37

Documentation flow for Stand-Alone securities when updates/changes occur after Closing Date