Page 1

i

AN

INTERNSHIP REPORT

ON

NEPAL RASTRA BANK

PAWAN KAWAN

ROLL NUMBER:

P.U. REGISTRATION NUMBER:

INTERNSHIP REPORT SUBMITTED TO

UNIGLOBE COLLEGE

(POKHARA UNIVERSITY AFFILIATED)

SUBMITTED FOR THE DEGREE OF

MASTER OF BUSINESS ADMINISTRATION (MBA-FINANCE)

KATHMANDU

15th April 2014

Page 2

ii

INFORMATION SHEET

Name of the Company : Nepal Rastra Bank

Address of the Company : Baluwatar, Kathmandu

Phone Number of the Company : 01 4410158

Data of Internship Commencement : September 23, 2013

Date of Internship Completion : December 20, 2013

Name of the Industry Guide : Mr. Bilash Chandra Rai

Designation of the Industry Guide : Assistant Director

Student’s Name : Pawan Kawan

Student’s e-mail ID : [email protected]

Page 3

iii

BONAFIDE CERTIFICATE

Certified that this project report An Internship Report On Nepal Rastra Bank

is the bona-fide work of Pawan Kawan Who carried out the internship work under

my supervision. This report is forwarded for examination.

Prof. Dr. Radhe Shyam Pradhan Mr. Dipkar Thapa

Academic Director MBA Program Director

Date:

Page 4

iv

DECLARATION

This Internship Report entitled "Internship Report on Nepal Rastra Bank,

Baluwatar” which is submitted by me in partial fulfillment of the requirement for the

award of MBA degree of Pokhara University Comprises only my original work and

due acknowledgement have been made to materials used in the report.

____________________

Pawan Kawan

Date: 15th April, 2014

Page 5

v

ACKNOWLEDGEMENT

This report is the result of continuous effort made and extended support of many

people. The preparation of this report needed a lot of effort and suggestions of many

people in order to get to its complete form. Firstly I would like to thank Pokhara

University for designing a platform where we can gain not only theoretical knowledge

but also practical knowledge.

I would like to express my intense gratitude to our Academic DirectorProf. Dr. Radhe

Shyam Pradhan for providing me his valuable guidance and suggestions throughout

the internship period. This study would not have seen light of the day without their

constructive and consistence guidance.

I would like to thank Mr. Kishor Kumar Dhakal, Deputy Director, Mr. Bilash

Chandra Rai, Assistant Director for their valuable support, inspiration and

cooperation. In the same way I would also like to thank Mr Bijaya Kumar Shrestha,

Deputy Director, Mr. Aasta Bahadur Shrestha, Assistant for their keen cooperation.

Finally, I would like to pay heartwarming thanks to my family and my dear friends for

their valuable support and assistance, without their support this report would not be

possible. I have tried my best to design a complete application that fulfill all the

requirements. Though I am not a professional or experienced in this field but I had

tried my level best to make this project according to the internship guidelines.

Sincerely,

Pawan Kawan

Page 6

vi

ABBREVIATIONS

ACU : Asian Clearing Union

BFIs : Bank and Financial Intuitions

BOD : Board of Directors

FMD : Financial Management Department

LOLR : Lender of Last Resort

NRB : Nepal Rastra Bank

SLF : Standing Liquid Facility

SOA : Service Oriented Architecture

STP : Straight Through Preocessing

T-Bills : Treasury Bills

& : And

KBO : Kathmandu Banking Office

CMD : Currency Management Department

BRT : Biratnagar

JNP : Janakpur

BRG : Birgunj

PKR : Pokhara

SID : Siddharthanagar

NEP : Nepalgunj

DHN : Dhangadi

Page 7

vii

Table of Contents

INFORMATION SHEET ........................................................................................................i

BONAFIDE CERTIFICATE....................................................................................................iii

DECLARATION ................................................................................................................. iv

ACKNOWLEDGEMENT ....................................................................................................... v

ABBREVIATIONS .............................................................................................................. vi

LIST OF TABLE.................................................................................................................. ix

LIST OF FIGURE ................................................................................................................. x

CHAPTER I ORGANIZATIONAL PROFILE ............................................................................... 1

1.1 Description of Organization...................................................................................... 1

1.1.1 Organization’s Vision, Missions, Objectives and Functions ...................................... 3

1.1.2 Major Markets and Customers .............................................................................. 4

1.1.3 Products and Services ........................................................................................... 6

1.1.4 Organization Design and Structure ........................................................................ 9

1.1.5 Financial Structure.............................................................................................. 13

1.1.5.1 Statement of Balance Sheet.................................................................... 13

1.1.5.2 Income Statement................................................................................. 16

1.1.5.3 Statement of changes in Equity .............................................................. 18

1.1.6 Organizational Performance ................................................................................ 18

CHAPTER II JOB PROFILE AND ACTIVITIES PERFORMED ..................................................... 20

2.1 Activities Performed in the Organization................................................................. 20

2.2 Steps of Reconciliation........................................................................................... 28

2.3 Problem Solved ..................................................................................................... 32

2.4 Intern’s Key Observation........................................................................................ 33

2.5 Strength, Weakness, Opportunity and Threat (SWOT) Analysis ................................ 33

CHAPTER III LESSON LEARNT AND FEEDBACK.................................................................... 36

3.1 Key Skills and Attitudes Learnt ............................................................................... 36

3.2 Feedback to Organization ...................................................................................... 38

3.3 Feedback to College/University .............................................................................. 39

REFERENCES ................................................................................................................... 41

ANNEX I: List of Banks and Financial Institutions ............................................................... 43

ANNEX II: BALANCE SHEET AS 2066/67 ............................................................................ 53

ANNEX III: BALANCE SHEET AS 2066/67............................................................................ 54

ANNEX IV: STATEMENT OF CHANGES IN EQUITY AS 2066/67 ............................................. 55

Page 8

viii

ANNEX V: PAY ORDER ..................................................................................................... 56

ANNEX VI: OLD GENERAL LEDGER .................................................................................... 57

ANNEX VII: NEW GENERAL LEDGER .................................................................................. 58

ANNEX VIII: MERGER OF BANK AND FINANCIAL INSTITUTIONS (BFIs) ................................. 59

ANNEX IX: OWNERSHIP STRUCTURE OF GOVERNMENT SECURITIES ................................... 60

ANNEX X: SOME MEMORIES AT NEPAL RASTRA BANK....................................................... 61

Page 9

ix

LIST OF TABLE

Details Page No.

Table 1 List of Governors............................................................................................ 2

Table 2 List of Banks and Financial Institutions ...................................................... 5

Table 3 Board of Directors .......................................................................................... 9

Table 4 Management Committee ............................................................................. 10

Table 5 Audit Committee .......................................................................................... 11

Table 6 Statement of Financial Position .................................................................. 14

Table 7 Statement of Income and Expenditure ....................................................... 16

Table 8 Statement of changes in Equity ................................................................... 18

Table 9 Duration of Internship ................................................................................. 20

Table 10 Old General Account Code ....................................................................... 26

Table 11 New Code for General Ledger Posting ..................................................... 26

Page 10

x

LIST OF FIGURE

Details Page No.

Figure 1 Growth of BFIs ............................................................................................. 6

Figure 2 Organizational structure of Nepal Rastra Bank ...................................... 13

Figure 3 Sections in Financial Management Department (FMD) ......................... 21

Figure 4 Debit Items .................................................................................................. 28

Figure 5 Credit Items................................................................................................. 29

Figure 6 Account Movement ..................................................................................... 30

Page 11

1

CHAPTER I ORGANIZATIONAL PROFILE

1.1 Description of Organization

A central bank is a public institution that manages a state's currency, money supply,

and interest rates. Central banks also usually oversee the commercial banking

system of their respective countries. The primary function of a central bank is to

manage the nation's money supply, through active duties such as managing interest

rates, setting the reserve requirement, and acting as a lender of last resort to

the banking sector during times of bank insolvency or financial crisis.

NRB, the central bank of Nepal, established in 1956 under the Nepal Rastra Bank Act

1955. The preamble of Nepal Rastra Bank Act 1955 is:

“Preamble: Whereas, it is expedient to establish a Nepal Rastra Bank to function as

the Central Bank to formulate necessary monetary and foreign exchange policies, to

maintain the stability of price, to consolidate balance of payment for sustainable

development of the economy of Nepal, and to develop a secure, healthy and efficient

system of payment; to appropriately regulate, inspect and supervise in order to

maintain the stability and healthy development of banking and financial system; and

for the enhancement of public credibility towards the entire banking and financial

system of the country.”

Nepal Rastra Bank (NRB), the Central Bank of Nepal, was established to discharge

the central responsibilities including guiding the development of the embryonic

domestic financial sector. Since inception, there has a significant growth in both the

number and the activities of the domestic financial institution.

It has seven branch offices located at Biratnagar, Janakpur, Birgunj, Pokhara,

Siddharthanagar, Nepalgunj and Dhangadi. It supervises the commercial banks in

Nepal and guides monetary policy. Nepal Rastra Bank also oversees foreign exchange

rates and the country’s foreign exchange reserve. NRB has power to control and

regulate these institutions, which has been authorized by the Nepal Rastra Bank Act,

2058. Nepal Rastra Bank (NRB) is non-profit organization fully subscribed by the

Nepal Government. Nepal Government has empowered the Nepal Rastra Bank (NRB)

by law to regulate, supervise and monitor the banking sector for better economic

environment. It plays a key role in Nepalese economic system, in which no other

Page 12

2

organization is likely to substitute it. The Nepal Rastra Bank (NRB) gives direction

and regulation to the commercial banks, whenever needed for proper management of

banking sectors.NRB has been a member of Asian Clearing Union (ACU), Tehran

Iran and Alliance for Financial Inclusion.

History of Banking Sector in Nepal

The banking in Nepal was started only after the establishment of Nepal Bank Limited

in 1937. Nepal Bank Ltd. is the first modern bank of Nepal. It is taken as the

milestone ofmodern banking of the country. This was established on 30th Kartik, 1994

B.S (1937 A.D) until mid-1940’s only metallic coins were used as medium of

exchange. So the Government felt need of separate institution or body to issue

national currencies and promote financial organization in the country. Hence, the

Nepal Rastra Bank act 2012 was formulated, which was approved by Government.

Accordingly, the Nepal Rastra Bank was established in 2013 B.S as the central bank

of Nepal. Similarly, Nepal Industrial Development Bank was established to accelerate

industrial development in 1st Ashad 2016 B.S, which eventually turned into

Agriculture Development Bank in 7th Magh, 2024 B.S. In 10th Magh, 2022B.S a fully

government owned second commercial Rastria Banijya Bank was established.

For more than two decades, no more banks have been established in the country. After

declaring free economy and privatization policy, Government encourage the foreign

bank for joint venture in Nepal. As a result, Nepal Arab Bank Ltd. (NABIL) was

established in 2041 B.S. This is the first modern bank with latest banking technology.

Now 31 commercial banks have been opened in the country.

Since its establishment, NRB has been lead by fifteen proficient governors, Mr.

Himalayan Shumsher J. B. Rana being the first governor of NRB. Currently, Dr. Yuba

Raj Khatiwada is the governor of the bank. Following are the lists of governors of

NRB since its inception.

Table 1 List of Governors

S.N. Name of Governor Term of office

1. Mr. Himalaya Shumsher J.B. Rana April 26, 1956 – February 7, 1961

2. Mr. Laxmi Nath Gautam February 8, l961 – June 17, l965

Page 13

3

3. Mr. Pradyuma Lal Rajbhandari June l8, l965 – August 13, l966

4. Dr. Bhekh Bahadur Thapa August 14, l966 – July 26, l967

5. Dr. Yadav Prasad Pant April 24, l968 – April 28, l973

6. Mr. Kul Shekhar Sharma April 29, l973 – December 12, l978

7. Mr. Kalyana Bikram Adhikary June 13, l979 – December 8, l984

8. Mr. Ganesh Bahadur Thapa March 25, l985 – May 22, l990

9. Mr. Hari Shankar Tripathi August 10, l990 – January 17, l995

10. Mr. Satyendra Pyara Shrestha January l8, l995 – January l7, 2000

11. Dr. Tilak Bahadur Rawal January l8, 2000 - January l7, 2005

12. Mr. Deependra Purush Dhakal August 29, 2000 – April 27, 2001

13. Mr. Bijaya Nath Bhattarai January 31, 2005 –January 30, 2010

14. Mr. Deependra Bahadur Kshetry January 15, 2009 – July 26, 2009

15. Dr. Yuba Raj Khatiwada March 22, 2010 – Present

1.1.1 Organization’s Vision, Missions, Objectives and Functions

Vision

To become “A modern, dynamic, credible and effective Central Bank”

Mission

To maintain macro-economic stability through sound and effective monetary, foreign

exchange and financial sector policies.

Objectives of the Bank

According to Nepal Rastra Bank Act 1955, the objectives of the NRB are as follows:-

a) To formulate necessary monetary and foreign exchange policies in order to

maintain the stability of price and balance of payment for sustainable

development of economy, and manage it.

b) To promote stability and liquidity required in banking and financial sector.

Page 14

4

c) To develop a secure, healthy and efficient system of payment.

d) To regulate, inspect, supervise and monitor the banking and financial system

e) To promote entire banking and financial system of the Nepal and to enhance

its public credibility.

Functions, Duties and Powers of the Bank

In order to achieve the objectives, the functions, duties and powers of the NRB as per

Nepal Rastra Bank Act 1955 are as follows:

a) To issue bank notes and coins.

b) To formulate necessary monetary policies in order to maintain price stability

and to implement or cause to implement them.

c) To formulate foreign exchange policies and to implement or cause to

implement them.

d) To determine the system of foreign exchange rate.

e) To manage and operate foreign exchange reserve.

f) To issue license to commercial banks and financial institutions to carry on

banking and financial business and to regulate, inspect, supervise and monitor

such transactions.

g) To act as a banker, advisor and financial agent of

h) Government of Nepal.

i) To act as the banker of commercial banks and financial institutions and to

function as the lender of the last resort.

j) To establish and promote the system of payment, clearing and settlement and

to regulate these activities.

k) To implement or cause to implement any other necessary functions which the

Bank has to carry out in order to achieve the objectives of the Bank under this

Act.

1.1.2 Major Markets and Customers

The Nepal Rastra Bank (NRB) is the central bank of Nepal. It supervises the banks

and financial institutions (licensed by the Bank) in Nepal and guides monetary policy.

Nepal Rastra Bank also oversees foreign exchange rates and the country's foreign

Page 15

5

exchange reserves and regulates the foreign exchange policy. The bank is engaged in

the promotion of financial inclusion policy within the nation, and is also a member of

the Alliance for Financial Inclusion. It made a Maya Declaration Commitment in

2013 to promote financial literacy, prepare a financial sector development strategy by

the end of 2014, and improve mobile money services. It is also a member of the Asian

Clearing Union. Nepal Rastra Bank serves as regulatory body of all BFIs in Nepal. It

also serves as government's bank. It also performs the economic activities of import

and export along with the maintenance of balance of payment is its major concern.

Following are the major market and customers of Nepal Rastra Bank:

1. Government of Nepal

2. Banks and Financial Institutions

3. Corporations or the firms

4. Investors

NRB is the supreme bank of the country, thus it provide services to Government of

Nepal, Banks and Financial Institutions, Corporations or the firms and Investors.

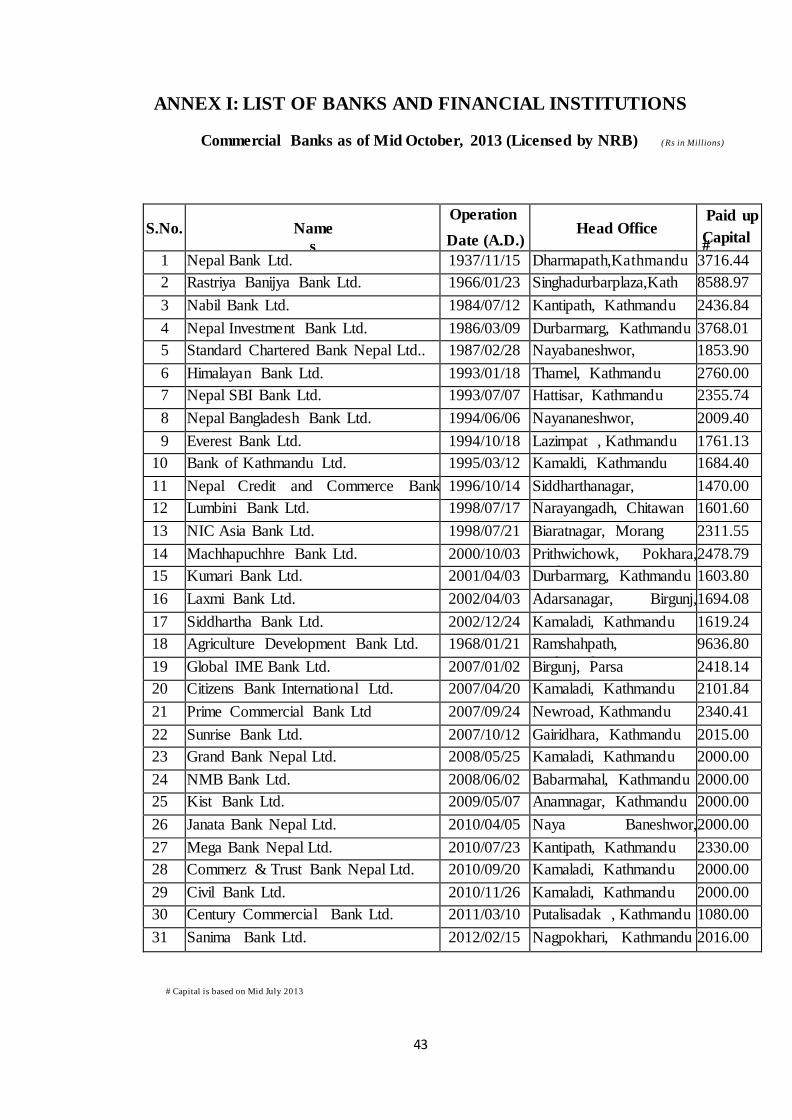

List of Banks and Financial Institutions

Table 2 List of Banks and Financial Institutions

As of Mid October, 2013 (NRB)

S.N. Financial Institutions Numbers

1 Commercial Banks 31

2 Development Banks 87

3 Finance Companies 59

4 Micro-finance Development Banks 35

5 Saving & Credit Cooperatives Limited

Banking Activities)

15

6 NGOs (Financial Intermediaries) 31

Page 16

6

All the Bank or Financial institution are governed by Banks and Financial Institutions

Act, 2063 (2006). Hence Bank means a corporate body established to conduct

financial transactions mentioned in section 47(1). And Financial Institution means a

corporate body incorporated to carry on the transactions as referred to in Sub-section

(2), (3) or (4) of Section 47, and this term also includes a development bank, finance

company or micro-finance development bank.

Growth of Bank and Financial Institutions (BFIs)

Banking Industry, normally, occupies a bigger chunk in the financial system. Same is

the case in Nepal. With the liberalized policies taken since 1980s, banking industry

has been growing in a rapid pace. Chart 1.1 below shows how the number of Bank

and Financial Institutions (BFIs), of class 'A', 'B', 'C', and 'D', increased in Nepalese

banking industry in the last two and half decades. Nepalese Banking Industry saw the

highest growth in the decade of 2000-2010. On the one hand, it increased people

awareness and banking habit as well as made them more demanding and choosy.

Figure 1 Growth of BFIs

(Source: Bank and Financial Institutions Regulation Department, NRB)

1.1.3 Products and Services

Being the Central Bank of Nepal, Nepal Rastra Bank provides various services to the

government, banks and financial institutions, and to its various customers. NRB

doesn’t perform the functions like other banks but it performs regulating and

supervising functions. Hence its products and services are related to these functions.

Central banks usually have supervisory powers, intended to prevent bank runs and to

Page 17

7

reduce the risk that commercial banks and other financial institutions engage in

reckless or fraudulent behavior. Some of the basic products of Public Debt

Management Department are listed as:

1. Treasury Bills (T-Bills)

2. Repo and Reverse Repo

3. Outright Purchase/Sell

4. Bank Rate

5. Standing Liquid Facility (SLF)

6. Treasury Bonds like Development Bonds, Special Bonds, National Saving

Bonds, and Citizen Saving Bonds.

7. Loans against Treasury Securities

The functions/services provided by NRB are as follows:

1. Bank of Note Issue:

The central bank has the sole monopoly of note issue in almost every country.

The currency notes printed and issued by the central bank become unlimited legal

tender throughout the country.

2. Banker, Agent and Adviser to the Government:

The central bank functions as a banker, agent and financial adviser to the

government,

(a) As a banker to government, the central bank performs the same functions for the

government as a commercial bank performs for its customers. It maintains the

accounts of the central as well as state government; it receives deposits from

government; it makes short-term advances to the government; it collects cheques and

drafts deposited in the government account; it provides foreign exchange resources to

the government for repaying external debt or purchasing foreign goods or making

other payments,

(b) As an Agent to the government, the central bank collects taxes and other payments

on behalf of the government. It raises loans from the public and thus manages public

Page 18

8

debt. It also represents the government in the international financial institutions and

conferences,

(c) As a financial adviser to the lent, the central bank gives advise to the government

on economic, monetary, financial and fiscal matters such as deficit financing,

devaluation, trade policy, foreign exchange policy, etc.

3. Bankers' Bank:

The central bank is the apex body to control the BFIs. . It maintains the account of

different government organizations along with the accounts of different financial

institutions, and market makers. The NRB gives direction and regulation to the

commercial banks, whenever needed for proper management of banking sectors. The

central bank acts as a friend, philosopher and guide to the commercial banks

4. Lender of Last Resort:

As the supreme bank of the country and the bankers' bank, the central bank acts as the

lender of the last resort. In other words, in case the commercial banks are not able to

meet their financial requirements from other sources, they can, as a last resort,

approach the central bank for financial accommodation. The central bank provides

financial accommodation to the commercial banks by rediscounting their eligible

securities and exchange bills.

5. Clearing Agent:

As the custodian of the cash reserves of the commercial banks, the central bank acts

as the clearing house for these banks. Since all banks have their accounts with the

central bank, the central bank can easily settle the claims of various banks against

each other with least use of cash.

6. Credit Control:

These days, the most important function of a central bank is to control the volume of

credit for bringing about stability in the general price level and accomplishing various

other socio-economic objectives. The significance of the function has increased so

Page 19

9

much that for property understanding. The central bank has acquired the rights and

powers of controlling the entire banking.

7. Collection of Data:

Central banks in almost all the countries collects statistical data regularly relating to

economic aspects of money, credit, foreign exchange, banking, economic growth etc.

from time to time, committees and commission are appointing for studying various

aspects relating to the aforesaid problems.

1.1.4 Organization Design and Structure

As per section 14 of Nepal Rastra Bank Act, 2002, the Board of Nepal Rastra Bank

(NRB) comprises of seven members: four ex officio members - the Governor (who is

the Chairman), the Secretary, Ministry of Finance, two Deputy Governors, and three

other Directors, who are appointed from amongst the persons renowned in the field of

Economics, Monetary, Banking, Finance and Commercial Laws.

The Governor, Deputy Governors and other Directors are appointed by Government

of Nepal, Council of Ministers for term of five years. Government may, reappoint the

retiring Governor for another one term and the retiring other Directors for any term, if

it is deemed necessary.

The Board of Directors, chaired by the Governor, is the apex body of policy making

and the Governor also discharges his duty as the chief executive of the Bank. The

BOD of Nepal Rastra Bank is as follows:

Table 3 Board of Directors

S.N Members Name Position

1. Governor Dr. Yuba Raj Khatiwada Chairperson

2. Secretary, Ministry of Finance Mr. Shanta Raj Subedi Member

3. Two Deputy Governors 1. Mr. Gopal Prasad

Kaphle

2. Mr. Maha Prasad

Adhikari

Member

4. Three Directors appointed by 1. Dr. Sri Ram Poudyal Member

Page 20

10

theGovernment of Nepal from

amongst the persons renowned

in the fields of Economic,

Monitory, Banking, Finance

and Commercial Law

2. Dr. Ramhari Aryal

3. Mr. Bal Krishna Man

Singh

Source: www.nrb.org.np/aboutus/bod.php, 2013

The organization structure of the bank is based on formal hierarchies and the works

are procedure-oriented like any other government institutions. The Audit committee is

directly under the BOD while the two deputy governors are assigned with two groups

each:

a) The monetary and foreign exchange policy group and banking management

group

b) Regulation and supervision group and support service group respectively.

The other departments as internal audit and the legal departments are directly under

the governor.

Board Committees

Board committees are comprises of:

Table 4 Management Committee

Governor Chairman

Deputy Governor Member

Deputy Governor Member

Senior Officer (Designated by the Governor) Member Secretary

Source: www.nrb.org.np/aboutus/bod.php, 2013

There shall be a Management Committee, to remain under the Board to be chaired by

the Governor in order to conduct the business of the Bank in a smooth manner. The

two Deputy Governors shall be other members of the Management Committee, and

one senior officer of the Bank designated by the Governor shall act as the member

Page 21

11

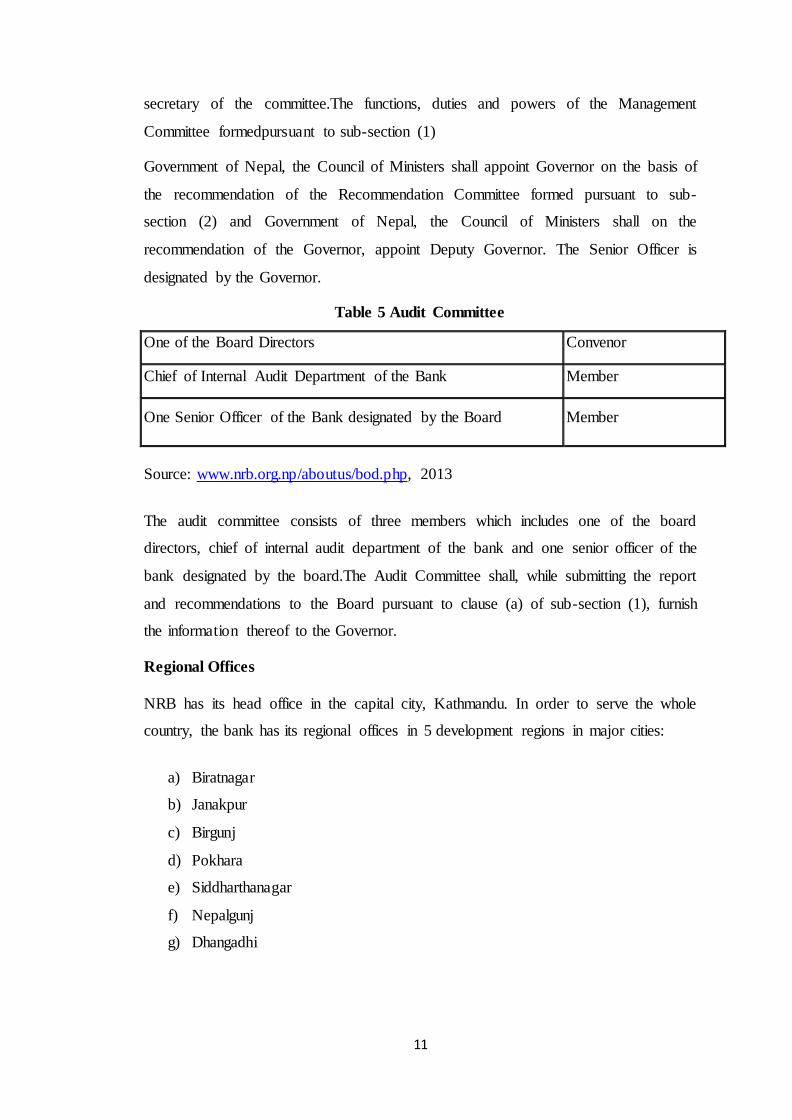

secretary of the committee.The functions, duties and powers of the Management

Committee formedpursuant to sub-section (1)

Government of Nepal, the Council of Ministers shall appoint Governor on the basis of

the recommendation of the Recommendation Committee formed pursuant to sub-

section (2) and Government of Nepal, the Council of Ministers shall on the

recommendation of the Governor, appoint Deputy Governor. The Senior Officer is

designated by the Governor.

Table 5 Audit Committee

One of the Board Directors Convenor

Chief of Internal Audit Department of the Bank Member

One Senior Officer of the Bank designated by the Board Member

Source: www.nrb.org.np/aboutus/bod.php, 2013

The audit committee consists of three members which includes one of the board

directors, chief of internal audit department of the bank and one senior officer of the

bank designated by the board.The Audit Committee shall, while submitting the report

and recommendations to the Board pursuant to clause (a) of sub-section (1), furnish

the information thereof to the Governor.

Regional Offices

NRB has its head office in the capital city, Kathmandu. In order to serve the whole

country, the bank has its regional offices in 5 development regions in major cities:

a) Biratnagar

b) Janakpur

c) Birgunj

d) Pokhara

e) Siddharthanagar

f) Nepalgunj

g) Dhangadhi

Page 22

12

Departments of Nepal Rastra Bank

The present internal organization of the Bank consists of its Central Office in

Kathmandu with 19 departments, in addition to the offices of the Governor and the

two Deputy Governors. The departments of Nepal Rastra Bank are:

a) Office of the Governor

b) Human Resources Management Department

c) General Services Department

d) Financial Management Department

e) Research Department

f) Foreign Exchange Management Department

g) Internal Audit Department

h) Banks and Financial Institutions Regulation Department

i) Bank Supervision Department

j) Development Bank Supervision Department

k) Finance Company Supervision Department

l) Micro-Finance Promotion and Supervision Department

m) Information Technology Department

n) Bankers Training Center

o) Legal Division

p) Public Debt Management Department

q) Corporate Planning Department

r) Banking Office, Thapathali

s) Currency Management Department

Organization Structure of NRB

An organizational structure assists in defining authority and accountability,

relationships, activities and communicating channels. It assists in deciding

organizational relationship. It helps the employee to get clear job of their job

responsibilities and avoid overlapping of works by different department. The

organization structure of NRB are as follows:

Page 23

13

Figure 2 Organizational structure of Nepal Rastra Bank

Source: www.nrb.org.np, 2013

1.1.5 Financial Structure

NRB is the apex body which supervises and controls all financial institutions. NRB is

regulatory body for other banks and financial institutions and act as central bank. It

maintains the account of different government organizations along with the accounts

of different is financial institutions, and market makers. It is fully owned by the

government of Nepal.

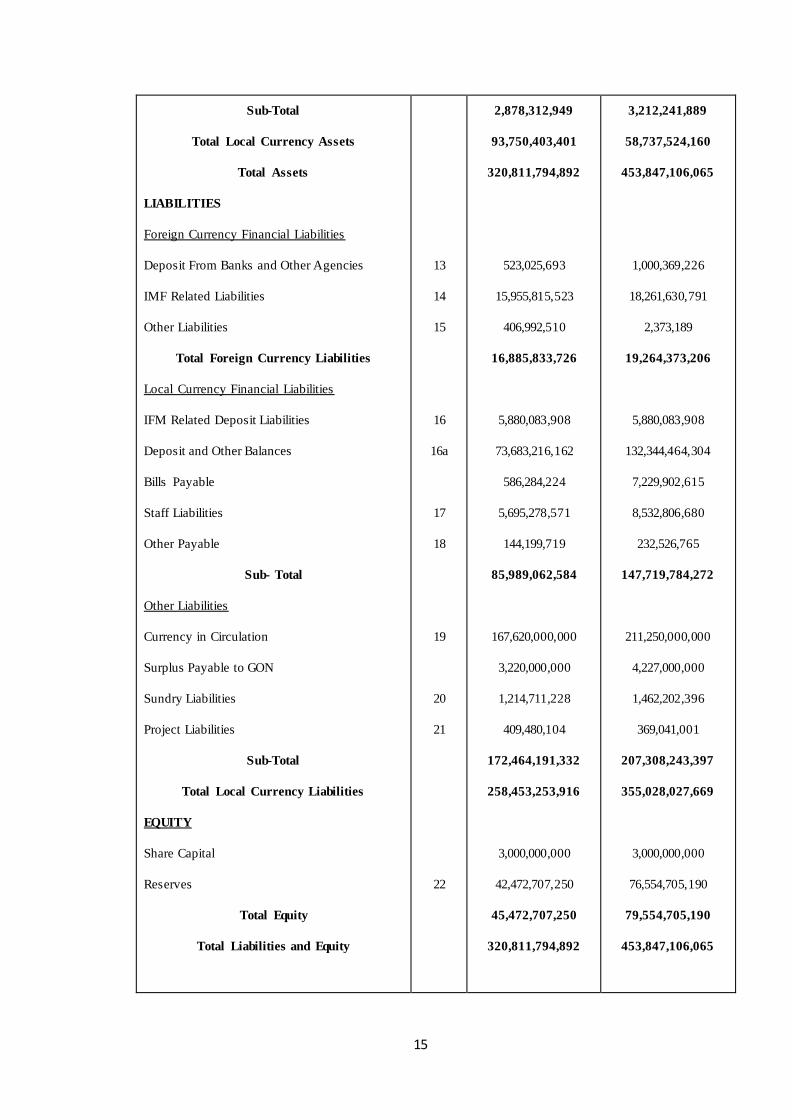

1.1.5.1 Statement of Balance Sheet

This report analyzed the position of various form of financial assets and liabilities of

foreign currency, financial assets and liabilities of local currency, other assets and

Page 24

14

liabilities and equity of Nepal Rastra Bank. Total assets, liabilities and equity of

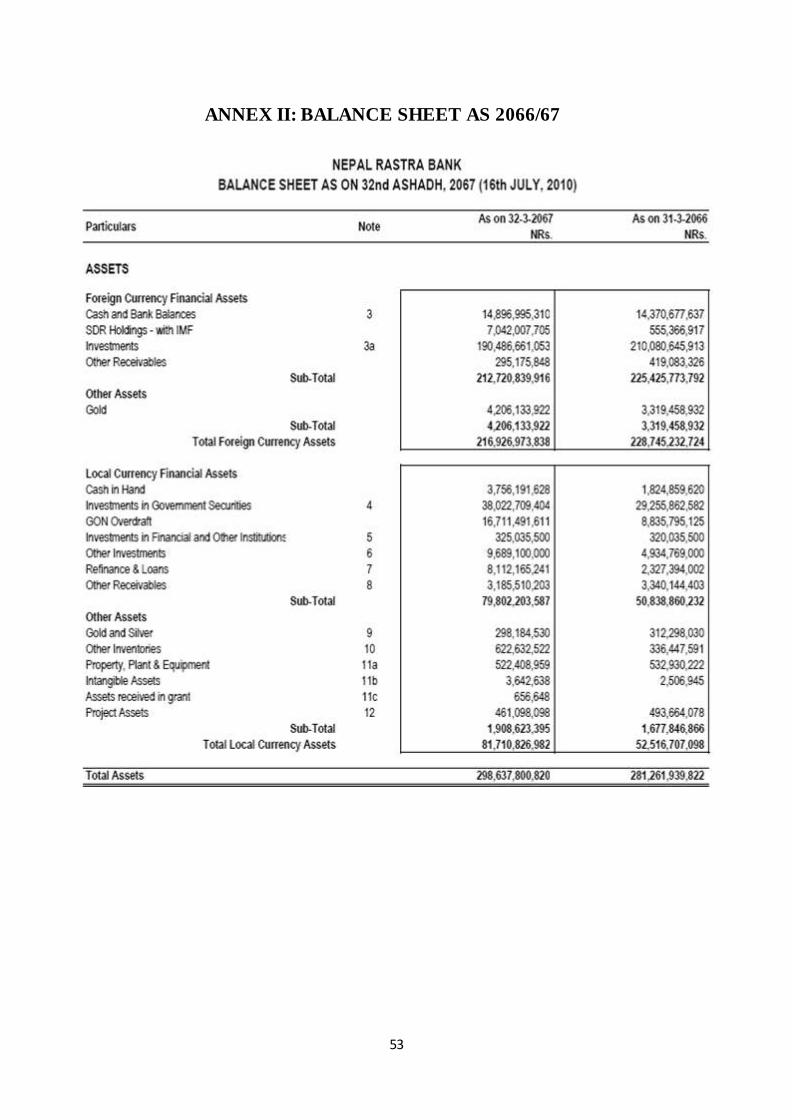

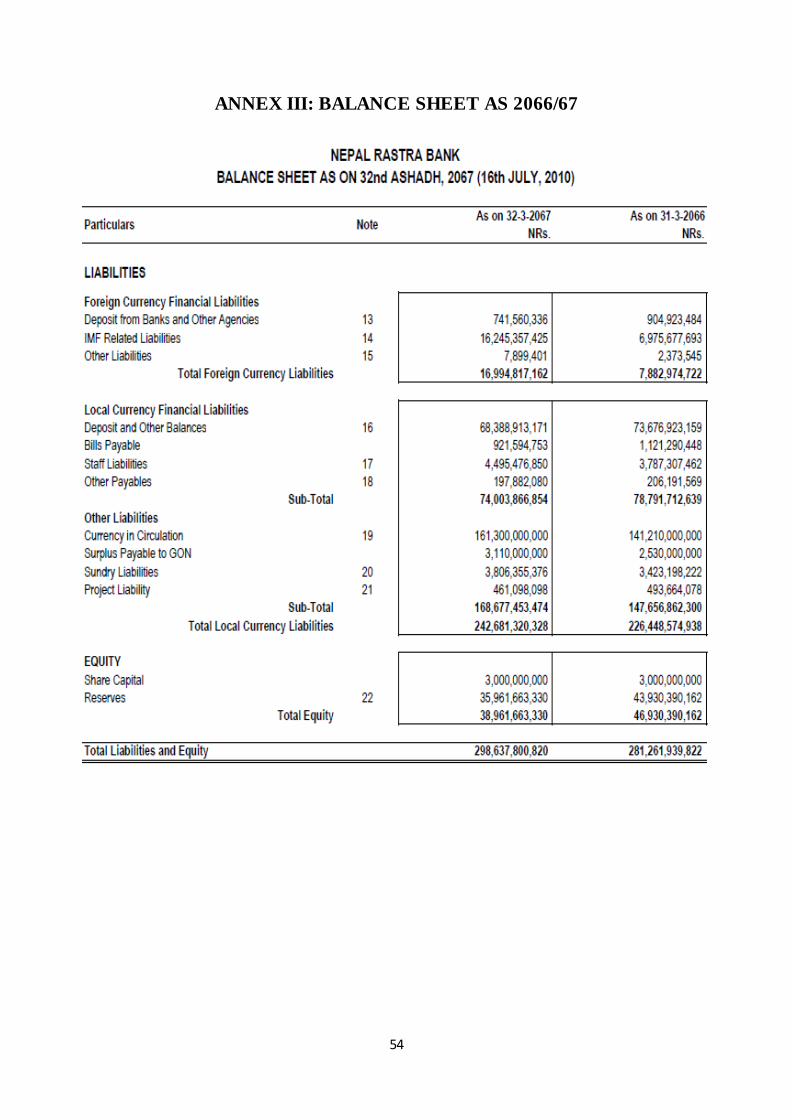

Nepal Rastra Bank for the year ended 2066/67 are presented in ANNEX II and III.

And statement of financial position as 2068/69 are as follows:

Table 6 Statement of Financial Position

Particular Note As on 31-3-2068 As on 31-3-2069

ASSETS

Foreign Currency Financial Assets

Cash and Bank Balance

IME Related Assets: Special Drawing

Right Holding

Investment

Other Receivables

Total Foreign Currency Assets

Local Currency Financial Assets

Cash in Hand

Investment in Government Securities

GON Overdraft

Investments in Financial and Other Institutions

Other Investments

Loans&Receivable and Refinance

Other Receivables

Sub-Total

Other Assets

Gold and Silver

Other Inventories

Property, Plant & Equipment

Intangible Assets

Assets Received in Grant

Project Assets

3

3a

4

5

6

7a,b

8

9

10

11a

11b

11c

12

16,337,109,975

6,730,704,535

0

203,545,377,189

448,199,792

227,061,391,491

373,0978,127

36,509,216,412

20,764,094,278

337,892,500

10,782,610,000

14,951,607,667

3,795,691,468

90,872,090,452

309,091,119

1,636,700,152

519,867,158

2,206,358

968,058

409,480,104

21,779,942,504

7,368,831,080

0

364,600,510,228

1,360,298,093

395,109,581,905

2,088,188,303

33,656,571,458

0

337,892,500

10,390,905,000

4,586,972,914

4464752096

55,525,282,271

292,612,967

1,859,346,980

540,424,208

150,094,134

722,599

369,041,001

Page 25

15

Sub-Total

Total Local Currency Assets

Total Assets

LIABILITIES

Foreign Currency Financial Liabilities

Deposit From Banks and Other Agencies

IMF Related Liabilities

Other Liabilities

Total Foreign Currency Liabilities

Local Currency Financial Liabilities

IFM Related Deposit Liabilities

Deposit and Other Balances

Bills Payable

Staff Liabilities

Other Payable

Sub- Total

Other Liabilities

Currency in Circulation

Surplus Payable to GON

Sundry Liabilities

Project Liabilities

Sub-Total

Total Local Currency Liabilities

EQUITY

Share Capital

Reserves

Total Equity

Total Liabilities and Equity

13

14

15

16

16a

17

18

19

20

21

22

2,878,312,949

93,750,403,401

320,811,794,892

523,025,693

15,955,815,523

406,992,510

16,885,833,726

5,880,083,908

73,683,216,162

586,284,224

5,695,278,571

144,199,719

85,989,062,584

167,620,000,000

3,220,000,000

1,214,711,228

409,480,104

172,464,191,332

258,453,253,916

3,000,000,000

42,472,707,250

45,472,707,250

320,811,794,892

3,212,241,889

58,737,524,160

453,847,106,065

1,000,369,226

18,261,630,791

2,373,189

19,264,373,206

5,880,083,908

132,344,464,304

7,229,902,615

8,532,806,680

232,526,765

147,719,784,272

211,250,000,000

4,227,000,000

1,462,202,396

369,041,001

207,308,243,397

355,028,027,669

3,000,000,000

76,554,705,190

79,554,705,190

453,847,106,065

Page 26

16

It is clearly seen that financial assets of foreign currency is in increasing trend in the

fiscal year 2068/69 and financial assets of local currency is in decreasing trend in the

fiscal year 2068/69 and financial liabilities of foreign currency and local currency is

in the increasing trend in the fiscal year 2068/69. The equity which includes share

capital and reserve is also in increasing trend in the fiscal year 2068/69.The total

assets in the fiscal year 2068 and 2069 is 320,811,794,892 and 453,847,106,065 and

total liabilities and equity in the fiscal year 2068 and 2069 is 320,811,794,892 and

453,847,106,065.

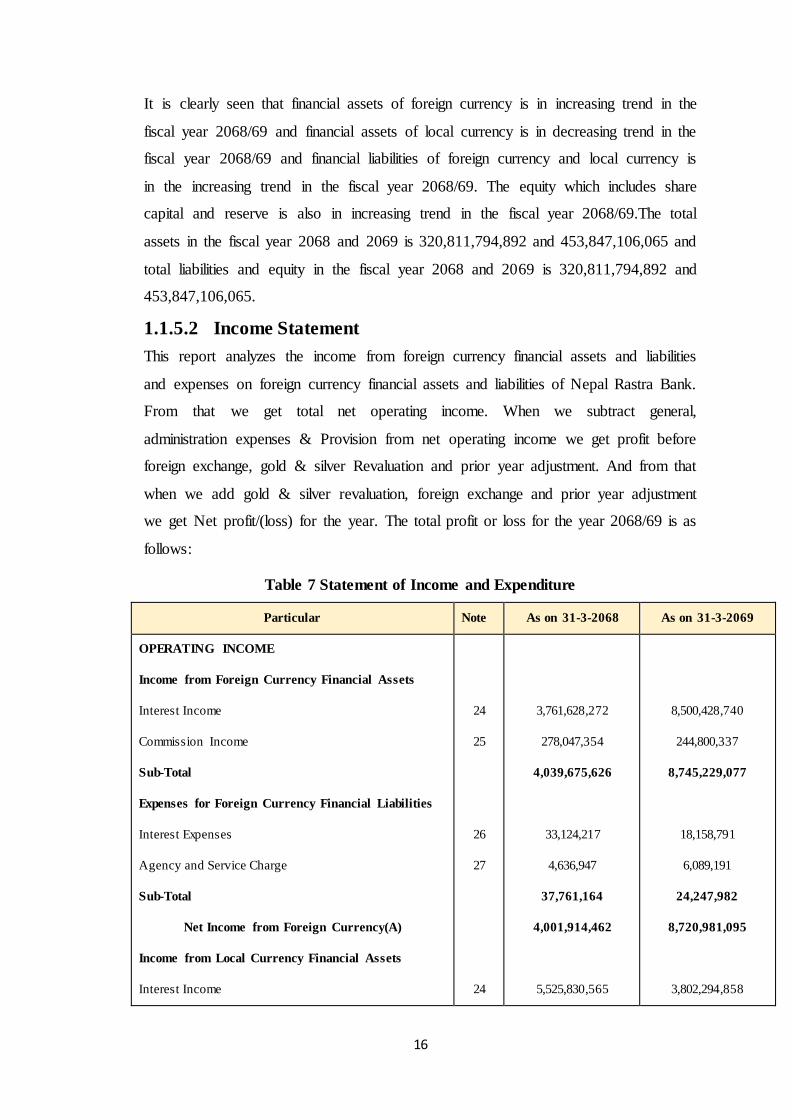

1.1.5.2 Income Statement

This report analyzes the income from foreign currency financial assets and liabilities

and expenses on foreign currency financial assets and liabilities of Nepal Rastra Bank.

From that we get total net operating income. When we subtract general,

administration expenses & Provision from net operating income we get profit before

foreign exchange, gold & silver Revaluation and prior year adjustment. And from that

when we add gold & silver revaluation, foreign exchange and prior year adjustment

we get Net profit/(loss) for the year. The total profit or loss for the year 2068/69 is as

follows:

Table 7 Statement of Income and Expenditure

Particular Note As on 31-3-2068 As on 31-3-2069

OPERATING INCOME

Income from Foreign Currency Financial Assets

Interest Income

Commission Income

Sub-Total

Expenses for Foreign Currency Financial Liabilities

Interest Expenses

Agency and Service Charge

Sub-Total

Net Income from Foreign Currency(A)

Income from Local Currency Financial Assets

Interest Income

24

25

26

27

24

3,761,628,272

278,047,354

4,039,675,626

33,124,217

4,636,947

37,761,164

4,001,914,462

5,525,830,565

8,500,428,740

244,800,337

8,745,229,077

18,158,791

6,089,191

24,247,982

8,720,981,095

3,802,294,858

Page 27

17

Commission Income

Sub-Total

Expenses on Local Currency Financial Liabilities

Interest Expenses

Agency and Service Charge

Sub-Total

Net income from Local Currency(B)

Total Net Operating Income(A+B)

General, Administration Expenses& Provision

Profit before Foreign Exchange, Gold&Silver

Revaluation Gain/(Loss) and prior year adjustment

Foreign Exchange Gain/(Loss) (Net)

Gold and Silver Revaluation Gain/(Loss) (Net)

Amount Transferred from Gold and Silver

Securities Revaluation

Other

Prior Year Adjustment

Net Profit/(Loss) for the year

25

26

27

29

31(i)

5,671,983

5,531,502,548

69,787,799

363,431,242

433,219,041

5,098,283,507

9,100,197,969

4,977,550,254

4,122,647,715

1,858,159,100

1,184,717,792

0

0

(18,579,822)

7,146,944,785

4,268,845

3,806,563,703

176,437,818

340,824,841

517,262,659

3,289,301,044

12,010,282,139

6,742,362,163

5,267,919,976

30,764,828,683

1,706,448,801

0

2,449,259

6,426,511

37,748,073,230

We can see that the net operating income is increasing trend in the fiscal year

2068/69. The profit before foreign exchange, gold & silver revaluation and prior year

adjustment is also in increasing trend in 2069. When we add foreign exchange, gold &

silver revaluation and prior year adjustment we get net profit/ (loss) for the year which

is also in increasing trend in the year 2069. The total profit for the year 2068 is

7,146,944,785 and in 2069 are 37,748,073,230.

Page 28

18

1.1.5.3 Statement of changes in Equity

Table 8 Statement of changes in Equity

Particular

Balance as at 31-

3-2068

Amount transferred

from/to profit

Interfund

transfer

Balance as at 31-

3-2069

Capital

General Reserve

Monetary Laibility Reserve

Exchange Equilisation Fund

Gold and Silver Equilisation

Grants Assets Reserve

Gramin Swabalam Kosh

Investment Revaluation Fund

Other Reserve Fund

Security Revaluation Fund

3,000,000,000

14,307,172,070

1,798,600,000

11,761,771,035

5,368,797,475

968,058

253,400,000

0

8,981,998,612

0

0

593,866,400

282,378,400

30,764,828,683

1,706,448,801

0

0

2,449,259

732,771,856

0

0

1591,165,306

0

0

(232,727,266)

(245,459)

0

0

(1358438040)

0

3,000,000,000

16,492,203,776

2,080,978,400

42,526,599,718

6,842,519,010

722,599

253,400,000

2,449,259

8,355,832,428

0

Total 45,472,707,250 34,082,243,399 (215,459) 79,554,705,190

The above table clearly shows that the total balance at 2068 is 45,472,707,250 and in

2069 are 79,554,705,190 which is in increasing trend because the year between 2068

and 2069 the interfund transfer amount of gold& silver equalization reserve, grant

assets reserve and other reserve fund is in negative which may get effect in balance at

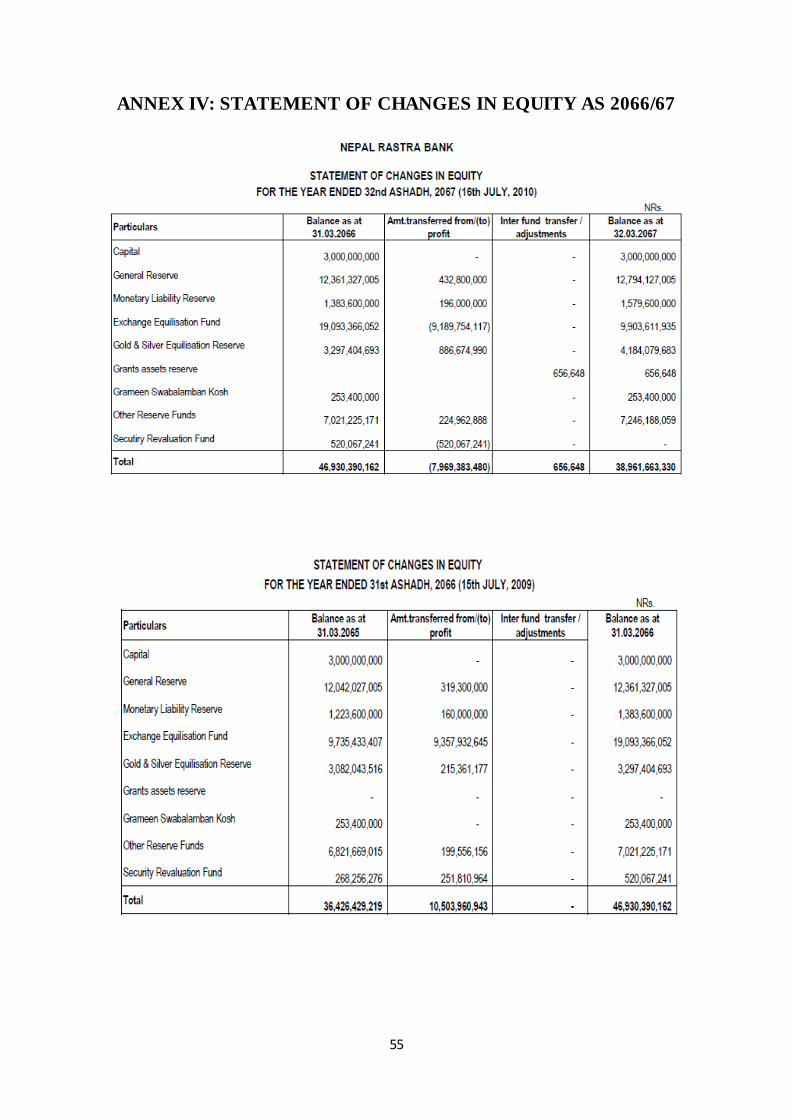

2069. The statement of change in equity for 2066/67 is on ANNEX IV.

1.1.6 Organizational Performance

Nepal Rastra Bank is the central bank and the regulatory body for other banks and

financial institutions. It doesn’t have its core products and services to measure its

performance. Hence, performance of the organization can be reflected on the basis of

the other functions of this organization.

The other functions of Nepal Rastra Bank are:

a) Issuance of monitory policies

b) Issuance of notes

Page 29

19

c) Controlling other financial institutions

d) Debt manager of the government

e) Economic advisory role to the government

f) Lender of the Last Resort (LOLR)

g) Foreign currency exchange

h) Enhance payment and clearing system

As envisaged by the Nepal Rastra Bank (NRB) Act, 2002, monetary policy has been

adopting the objectives of maintaining price and external sector stability, financial

stability and facilitating high and sustainable economic growth. This monetary policy

has been formulated on the basis of the analysis of currentmacroeconomic situation,

review of previous year's monetary policy, internal andexternal economic and

financial outlook and priorities of government budget for2013/14. In addition,

suggestions received from Nepal Bankers' Association,Development Bankers'

Association, Nepal Finance Company Association, MicroFinance Bankers'

Association, and industrial and commercial associations and other stakeholders are

also incorporated while formulating this monetary policy.

Nepal Rastra Bank Act, 2002 has placed NRB as an autonomous institution

empowered to regulate and supervise banks and financial institutions. As a regulator,

it has been continuously issuing various policies, guidelines and directives, to the

licensed institutions, in line with international best practices and norms. As a

supervisor, NRB supervises the activities of the BFIs based on the existing legal

framework and guiding policies. In order to strengthen the inspection and supervision

functions of the NRB, off-sitesupervision has been made more effective by timely

updating the informationreceived from BFIs. Likewise, in the process of on-site

inspection, priority has beengiven to examine the asset quality through conducting on-

site inspection of big borrowers' collateral and projects.To discharge the

responsibilities of supervisor, NRB has set four separate departments to look after the

supervision of each class of BFIs i.e. 'A', 'B', 'C' and 'D' class institutions - Bank

Supervision Department, Development Bank Supervision Department, Finance

Company Supervision Department and Micro Finance Promotion and Supervision

Department. These supervision departments basically monitor BFIs‟ compliance with

rules, regulations and directives.

Page 30

20

CHAPTER II JOB PROFILE AND ACTIVITIES

PERFORMED

2.1 Activities Performed in the Organization

During the internship period, the internee was placed in the Financial Management

Department (FMD) of Nepal Rastra Bank (NRB) Central Office, Baluwatar,

Kathmandu. Internee has completed the twelve weeks of internship period and has

visited various departments and performs various activities in different Sections. In

these three months of Internship period, Internee was assigned the task of

Reconciliation Section and Pension Section of Financial Management Department

(FMD). Internee has perform the task like General Ledger, Pay order and Pension

Posting. Internee got opportunity to work in these sections for various weeks. It is

presented as follows:

Table 9 Duration of Internship

Internee got opportunity to work 9 weeks at Reconciliation Section and 3 weeks at

Pension Section. In this time durations Internee perform the General Ledger task for 3

weeks and Pay Order for 6 weeks at Reconciliation Section. The total durations of

Internship is 12 weeks at Nepal Rastra Bank.

There are various departments in NRB. One of them is FMD. There are different

sections at FMD which are presented as follows:

S.N Job Title Section weeks

1 General Ledger Reconciliation 3

2 Pay Order Reconciliation 6

3 Pension Pension 3

Total Durations 12

Page 31

21

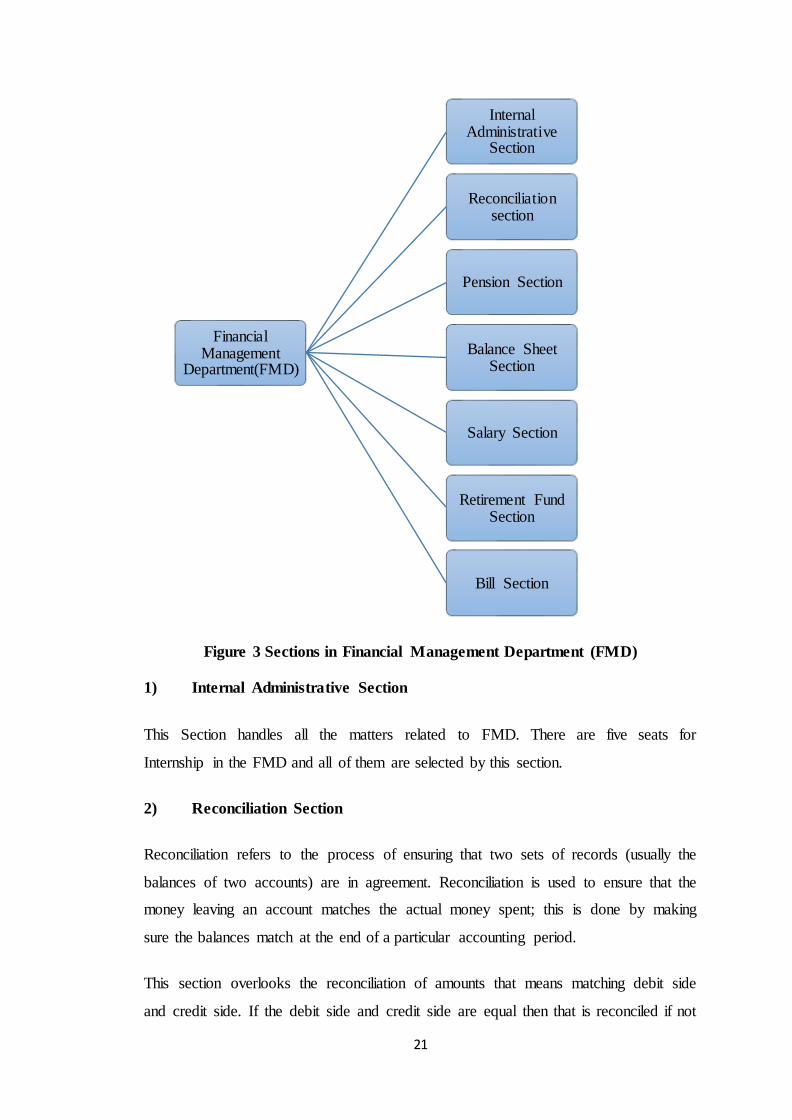

Figure 3 Sections in Financial Management Department (FMD)

1) Internal Administrative Section

This Section handles all the matters related to FMD. There are five seats for

Internship in the FMD and all of them are selected by this section.

2) Reconciliation Section

Reconciliation refers to the process of ensuring that two sets of records (usually the

balances of two accounts) are in agreement. Reconciliation is used to ensure that the

money leaving an account matches the actual money spent; this is done by making

sure the balances match at the end of a particular accounting period.

This section overlooks the reconciliation of amounts that means matching debit side

and credit side. If the debit side and credit side are equal then that is reconciled if not

Financial Management

Department(FMD)

Internal Administrative

Section

Reconciliation section

Pension Section

Balance Sheet Section

Salary Section

Retirement Fund Section

Bill Section

Page 32

22

then that is not reconciled. To ensure the reliability of the financial records,

reconciliations must, therefore, be performed for all Balance Sheet accounts on a

regular and ongoing basis. A robust reconciliation process improves the accuracy of

the financial reporting function and allows the Finance Department to publish

financial reports with confidence.

3) Pension Section

A pension is a contract for a fixed sum to be paid regularly to a person, typically

following retirement from service. This Section is created to handle all pension

related job. At present there are 2214 persons who take pension at Nepal Rastra Bank.

This section helps to provide pension to the deserved employees. At present, the retire

employees age above 70 are given 10% more pension and 20% more to aged above

80.

4) Balance Sheet Section

A balance sheet or statement of financial position is a summary of the financial

balances of organization. This section of FMD is one of the most crucial section

which has the responsibility to prepare balance sheet of NRB. This section is most

important section and Interns are not allowed to enter in this section because it covers

very serious information which should not leaked.

5) Salary Section

A salary is a form of periodic payment from an employer to an employee, which may

be specified in an employment contract. Salary is a fixed amount of money or

compensation paid to an employee by an employer in return for work performed. All

the staff in NRB takes salary and this section is responsible to record all the salary

paid and due. This section is created to handle the salary matters in NRB.

6) Retirement Fund Section

This section is specially created to manage the retirement funds at NRB. This Section

takes certain portion of salary for retirement funds.

Page 33

23

7) Bill Section

There are two branches in bill section. They are Travel and Purchase. This section

keeps records of payments of travels of employees for office work. And this section

also keeps record of purchase of furniture, computers, spare parts, petrol etc.

Olympic Banking System

The Finance Department of Nepal Rastra Bank uses OLYPIC Banking Software to

carry out day to day financial activities from Baisakh 2070.The OLYMPIC Banking

System is one of the most comprehensive and modern solutions to support all aspects

of modern and sophisticated private banking. Internee also has opportunity to use the

software for reconciliation.

It is based on fully integrated, online and front to back system. It meets the

requirements of Private Banking and Wealth Management institutions across all

geographies. OLYMPIC Banking has wide application; it can be used for Retail

Banking, Corporate Banking and Central Bank.

Retail Banking

The OLYMPIC Banking System for Retail Banking is a fully integrated and modular

solution which addresses the day-to-day operational needs of retail and universal

banks, providing efficient and comprehensive support to their business requirements.

To help banks overcome challenges - such as intense competition, increasing client

expectations and lower margins – the OLYMPIC Banking System offers a unique

competitive advantage by improving profitability and extending client reach. Banks

provide their clients with the relevant information via a 360-degree single source view

into their positions, products and services: support from OLYMPIC Banking System

enables them to propose the right offerings at the right time and through the right

channel.

The OLYMPIC Banking System is a highly parameterisable solution which provides

a flexible response to an ever-changing environment. New products and processes can

be configured in a matter of minutes and implemented through multiple distribution

channels. With its service-oriented architecture (SOA) and Web services-based

Page 34

24

model, it enables the easy integration of any third-party application: as a result the

bank can deliver a fully integrated business solution. Enabling Straight Through

Processing (STP) to reduce manual processes across the entire institution is one of the

critical objectives achieved by the OLYMPIC Banking System. Profitability and

client satisfaction increase while costs are reduced.

The OLYMPIC Banking System is a multi-branch, multi-entity, multi-currency,

multi-language and multi-channel system. Online e-Banking and mobile Banking are

available in various configurations in order to deliver the best possible client

experience.

Corporate Banking

The OLYMPIC Banking System for Corporate Banking is an integrated, modular

banking solution that addresses the needs of banks principally serving corporate and

commercial customers.

From commercial loans to trade finance, from cash management and payments to

syndicated lending, commercial banks need a truly global banking software platform

to respond to ever more demanding customers, in real-time and through multiple, yet

integrated and consistent distribution channels.

The OLYMPIC Banking System is a highly parameterisable solution providing a

flexible response to an ever changing business environment. New products and

processes can be configured in a matter of minutes and deployed through multiple

distribution channels. Its service-oriented architecture (SOA), and Web services-based

model enable the easy integration of third-party applications to deliver a fully

integrated response across all the relevant business processes.

OLYMPIC Banking System is able to manage the entire business work-flow - be it

for commercial loans or complex trade finance operations - from origination to

settlement. The integrated OLYMPIC modules provide increased visibility across all

business activities together with the ability to monitor and control the various risks

across multiple activities. Eliminating manual processing and enabling Straight

Through Processing (STP) across the entire organisation is one of the critical

Page 35

25

objectives achieved by the OLYMPIC Banking System, to increase profitability and

customer satisfaction while reducing costs.

Central Bank

The recent financial crisis has had a major impact on practices of central banks and

other government agencies. Central banks need to be able to react quickly to

changing market conditions and regulatory frameworks. They have to face new

challenges such as handling more complex instruments and enforcing strict

compliance processes.

The OLYMPIC Banking System is a browser-based, fully integrated, online, real-

time, front-to-back and parameter-driven solution. With OLYMPIC for Central

Banks, central banks are equipped with the right information to make decisions in

real-time. The system supports the needs of a wide range of users from the front,

middle and back office with a broad range of instruments and functionality.

The OLYMPIC Banking System's high levels of flexibility and powerful

management facilities have enabled ERI to develop a specialized version for the

central bank and statutory authority market. It includes all relevant standard

OLYMPIC functionality, together with functions developed specifically to meet the

unique requirements of central banks.

ERI has made a long term commitment to central banks. The OLYMPIC Banking

System is a unique, proven industry solution that supports all asset classes, manages

risk and performance, and helps optimise returns. For central banks, it provides

business process support for reserve management, monetary policy execution, asset

management and banking services.

The OLYMPIC Banking System for Central Banks configuration has been installed

successfully in a growing number of central banks around the world.

Gateway for Olympic Banking System

The address of the system is http://192.168.160.21:9081/PROD/Olympic.do. And the

old code for the Departments is listed below:

Page 36

26

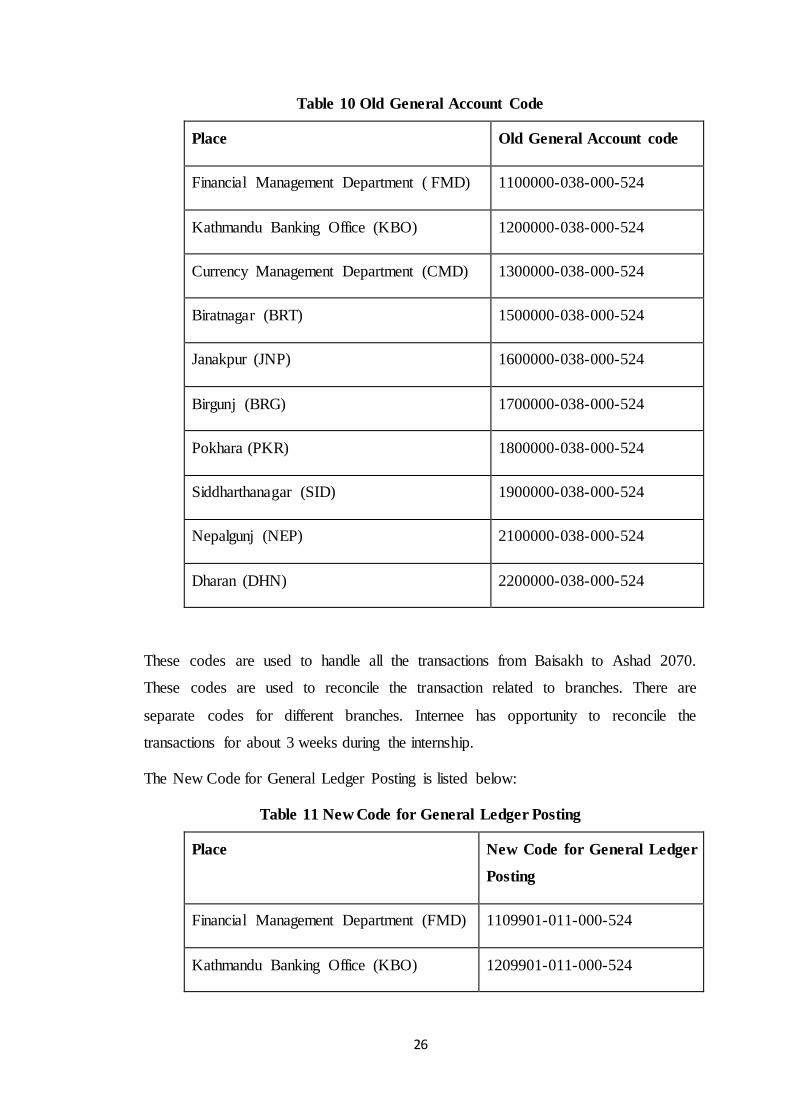

Table 10 Old General Account Code

Place Old General Account code

Financial Management Department ( FMD) 1100000-038-000-524

Kathmandu Banking Office (KBO) 1200000-038-000-524

Currency Management Department (CMD) 1300000-038-000-524

Biratnagar (BRT) 1500000-038-000-524

Janakpur (JNP) 1600000-038-000-524

Birgunj (BRG) 1700000-038-000-524

Pokhara (PKR) 1800000-038-000-524

Siddharthanagar (SID) 1900000-038-000-524

Nepalgunj (NEP) 2100000-038-000-524

Dharan (DHN) 2200000-038-000-524

These codes are used to handle all the transactions from Baisakh to Ashad 2070.

These codes are used to reconcile the transaction related to branches. There are

separate codes for different branches. Internee has opportunity to reconcile the

transactions for about 3 weeks during the internship.

The New Code for General Ledger Posting is listed below:

Table 11 New Code for General Ledger Posting

Place New Code for General Ledger

Posting

Financial Management Department (FMD) 1109901-011-000-524

Kathmandu Banking Office (KBO) 1209901-011-000-524

Page 37

27

Currency Management Department (CMD) 1309901-011-000-524

Biratnagar (BRT) 1509901-011-000-524

Janakpur (JNP) 1609901-011-000-524

Birgunj (BRT) 1709901-011-000-524

Pokhara (PKR) 1809901-011-000-524

Siddharthanagar (SID) 1909901-011-000-524

Nepalgunj (NEP) 2109901-011-000-524

Dharan (DHN) 2209901-011-000-524

These are the New code for General Ledger posting. From the 1st shrawan 2070 these

codes has been used. For some days Internee reconcile the transactions by using these

codes but later all transactions has been reconcile by the staff themselves who has

issue the cheque.

Pay Order

A bank pay order is a document that gives instructions to a bank to give out or pay

some specified amount of cash to a third party. Such orders are generally recognized

by the bank which guarantees that the payment will be made.

The basic task of Reconciliation Sections is reconcile the pay order. Internee has done

the task related to pay order for about 6 weeks. The code used for the reconciliation of

pay order is as follows:

The Code for Pay order is 1100000-014-000-524

Internee has learned the steps to reconcile the pay order which is listed out as follows:

1. Go to http://192.168.160.21:9081/PROD/Olympic.do

2. Click Equity

3. Click Client

4. Type pay order code: 1100000-014-000-524

Page 38

28

5. Click Ok

6. Account Movements found

7. Right click on Account

8. Bank reconciliation (Status option)

9. Click unreconciled movements

10. Match debit and credit items.

Internee has used this software in Reconciliation Section to reconcile general accounts

and pay order. Internee got opportunity to use the Olympic banking system software

which is not used by any commercial banks in Nepal till now. Only NRB uses this

software in Nepal.

2.2 Steps of Reconciliation

The steps of reconciliation of pay order by taking one example are as follows:

Figure 4 Debit Items

The above picture shows the debit items but Internee try to reconcile the amount of Rs

19490 which is not reconciled yet. So Internee took its transaction date and reference

number i.e. 469507.

Page 39

29

Figure 5 Credit Items

The above picture shows the credit item which is not reconciled. After taking the

transaction date and reference number of debit then same item must be searched in

credit side. Internee must match the item of debit side with item of credit side by

matching reference number. Internee matched the debit and credit item by matching

the reference number i.e. 469507. Then Internee must take the transaction date as

well.

Page 40

30

Figure 6 Account Movement

The above picture shows the account movements which includes all debit and credit

items. The items can be reconciled or not reconciled. This is needed to know the

account set of certain transaction.

After finding debit and credit items with same reference number Internee must go to

account movement to take account set of respective items. In this process, Internee

takes an example of Rs19490 which need to reconcile. The account set for debit item

is 746651 and credit item has account set 744958.

After taking the account set from account movement Internee must go to debit side

and credit side to reconcile the item. Then pay order reconciliation process completed

for pay order of Rs 19490.

Activities performed by Internee in Reconciliation Section are as follows:

Using of Olympic Banking System use by NRB for reconciliation.

Matching debit and credit items.

Page 41

31

Whenever the debit item is not matched with existing credit item then it is

informed to Supervisor.

Internee has visited the Bill Section and Salary Section for finding the pay

order which is not matched with debit items.

Internee has opportunity to interact with different employees in different

sections.

Internee got opportunity to work seating near Deputy Director Mr. Bijaya

Kumar Shrestha and interact on different matters.

Understand the government system of attendance i.e. Internee must sign the

attendance sheet at beginning and ending of the day.

Teach the new Intern about the reconciliation process and other problem

solving technique.

Making the letter to different section whenever the credit item was not found

in the system.

Internee at Pension Section

A pension is a contract for a fixed sum to be paid regularly to a person who get

retirement from service. The common use of the term pension is to describe the

payments a person receives upon retirement, usually under pre-determined legal or

contractual terms. A recipient of a retirement pension is known as a pensioner or

retiree.

The pension section is one of the sections under FMD. This Section is created to

provide pension to the deserved employees. At present there are 2214 persons who

take pension at Nepal Rastra Bank. Presently, the retire employees age above 70 are

given 10% more pension and 20% more to age above 80. All the transactions related

to pension are recorded in the books manually at NRB. Transaction related to pension

is not recorded in computer till now. The head of the pension section is Mr. Kishor

Kumar Dhakal, Deputy Director. The process to calculate the pension is as follows:

Pension = 𝑑𝐿𝑎𝑠𝑡 𝑆𝑎𝑙𝑎𝑟𝑦∗𝑆𝑒𝑟𝑣𝑖𝑐𝑒 𝑝𝑒𝑟𝑖𝑜𝑑

50

Page 42

32

Activities performed by Internee at Pension Section are as follows:

Recording the increased pension of 2068 and 2070 in the pension book

manually.

Corrected the record whenever Internee found that the past records are

incorrect.

Sometime the total pension in the book was not matched with the present

pension sheet, then that must be corrected.

Employees age above 70 are given 10% more pension and 20% more to age

above 80 but these amount must be separately given and should not recorded

with present pension. Thus Internee found out and corrected different such

cases where 10% and 20% pension are added to pension.

Understand the process of providing pension at NRB.

Incorrect transaction are recorded in separate sheet and provided to supervisor.

2.3 Problem Solved

During 12 weeks of internship period different problems has been arises related to

reconciliation and Pension and Internee was successful in solving these problems. The

problems that were solved during internship are as follows:

During reconciliation, sometime debit item does not matched with credit item

then such transaction must be inform to supervisor.

When debit item did not match with credit item during reconciliation then

Internee visited Bill Section and Salary Section for finding the credit item.

If there are many items that are not matched then letter must be typed and sent

to concern section to solve the problem.

New Intern are unaware about reconciliation and pension recording, so

Internee teaches them about the reconciliation process and pension recording.

Record regarding increase pension are not recorded in pension book since

2068, thus Internee recorded all those records.

Internee found out and corrected different cases regarding 10% and 20% more

pension added to net pension which should not be added.

Incorrect and hard problem are recorded in separate sheet and provided to

concern supervisor.

Page 43

33

2.4 Intern’s Key Observation

Although there are different sections, Internee got opportunity to work at

Reconciliation Section and Pension Section. Having theoretical knowledge and

practical knowledge in the field is two different parts of education system. As a whole

intern believe that the observation of real banking scenario that made during the

internship period will be helpful to understand the banking system. The key

observations during the internship period are as follows:

The electronic equipments like computer and its peripherals were mostly out

of proper working conditions.

There is proper coordination between the staffs.

No proper managed infrastructure.

Infrastructure of the bank is not sufficient and there is not CCTV as well.

Staffs have problems with computers and its applications.

The working system of the department is systematic and rigid.

The concept of transfer, rotation and promotion of employees cause several

problems.

All employees must do attendance through electronically which avoids staffs

delay in bank.

There are four employees Unions at NRB to protect the right of employees.

All staffs are polite and kind to the interns.

2.5 Strength, Weakness, Opportunity and Threat (SWOT) Analysis

The SWOT analysis of the organization is as follows:

a) Strengths

NRB is the apex body to regulate all BFIs.

The bank is a self-dependent institution with strong legal structure.

The bank has sufficient physical resources for operation of the various

activities.

The bank has the skilled and qualified human resources.

The bank has global exposures as it is the central bank of Nepal.

Page 44

34

NRB has been a member of Asian Clearing Union (ACU), Tehran Iran

and Alliance for Financial Inclusion.

A strong organizational culture has been build up to make the bank more

effective and efficient.

The Staffs can communicate with the managers and other higher

authorities as and when required.

b) Weaknesses

The bank has poor human resources plans and policies for career

development, reward and punishment and performance evaluation.

The bank follows the traditional management practices.

The old staffs feel uneasy in using computers and other equipments.

The bank makes delay in preparation and presentation of financial

statement due to use of traditional accounting practice.

Recording of pension are still done manually.

Due the improper division of departmental work some departments are

overloaded while others are under loaded and office layout.

The bank has inefficient IT infrastructure.

There is a poor coordination between departments and corporate

governance.

c) Opportunities

As the bank has the global exposure, there is an access to international

institutions for learning and knowledge sharing.

The bank is using modern technology to enhance the efficiency in sectors

like accounting, human resources management, anti-money laundering.

The bank is using Olympic banking system which is not used by any

other banks in Nepal.

The extended financial market helps in increasing the scope and use of

monetary policy instruments.

Being the Central bank, it is working for the financial stability in Nepal.

Page 45

35

d) Threats

Due to the fluctuation of interest and exchange rate in international

market there can be effect on foreign investment.

There is a wrong reporting from public and private media which leads to

flow of incorrect information.

Monetary policy implementation can be ineffective due to political

instability.

Excess liquidity in the market at present is the headache for NRB.

The bad performance of India also affects the economy of Nepal as

Nepali currency is pegged with Indian currency.

The development of informal financial market and co-operatives are

affecting the task of macroeconomic management

It is difficult to match with the international practices due rapid

development of technology in the international market.

Decrease customer trust from Banking and Financial Institutions.

Current unfavorable political condition.

Page 46

36

CHAPTER III LESSON LEARNT AND FEEDBACK

3.1 Key Skills and Attitudes Learnt

During the 12 weeks of internship Internee has perform different jobs assigned to him

in the bank. Internee has also visited different departments and sections as well. This

Internship period is quite fruitful to Internee as he got opportunity to complete

internship at central bank.

Generally an internship is a great way to get an inside glimpse of a company, an

industry, and a particular occupation. It helps to discover the career whichever is right

or wrong. With more and more people doing internships, employers are coming to

expect to such interns listed on the resumes of potential employees. Thus, internships

often turn into job offers. All the more reason to do an internship is the first

impression you make on who may be a future employer by showing the key skills and

attitudes learnt during the internship program.

i. Communication Skills: Daily interaction with staffs of bank has increased the

communication skills. It had helped to be good listener and good speaker as well. It

has also proven that one cannot be a good speaker unless s/he is a good listener.

ii. Teamwork Skills: This internship helps the Internee to work in team. Banking

requires a great deal of teamwork and integrity within the departments. During

internship period almost all activities performed were based on teamwork which has

developed an efficient team work skills that has helped to solve assigned task properly

and in productive way working as a team member.

iii. Computer & Technical Skills: During internship, various computer software and

other devices were handled thus enhancing practical skills. This internship provide

opportunity to use Olympic Banking System.

iv. Initiative: Initiation is always important in jobs or entrepreneurship. During

internship initiatives were taken to solve the mismatched transactions during the

reconciliation and even in recording pension amounts.

Page 47

37

v. Interpersonal Skills: Regular interaction with people out there in the bank Inter

has enabled to maintain good relationship with others and friendly and wholesome

ties that has further served to develop interpersonal skills.

vi Problem-Solving Skills: Many challenges and problems were faced during

internship at reconciliation section and pension section which were solved under the

guidance of the supervisor. It has helped to identify the problems, understand its

reason and its accurate mitigation or solution in right time.

vii. Analytical Skills: While different problems and issues were confronted, great

deal of time and concentration was given to analyzing those issues and problems to

pick out the roots. It has helped to develop an analytical mind that might be very

helpful in doing jobs in future.

viii. Flexibility / Adaptability: Since the professional setting teaches to adopt a

situational approach towards work, it was frequent event for me where a great deal of

adaptability was required. Getting with the environment and working accordingly

remaining within organizational culture and team has enriched the adaptability.

ix. Organizational Skills: Working in an organization bounded to work remaining

within organizational culture and behavior which helped to understand the

organization and activities to be performed. The government rules and regulation

regarding different issues were learned. So, the organizational skills were gained

during internship.

x. Leadership Skills: Observing the managers and head of department, there quality

and skills were closely watched. It has developed leadership skills and qualities

during internship. The working style of the directors and deputy directors has been

closely watched at NRB which is fruitful to the Internee.

xi. Self-Confidence: A self confident person is someone who inspires others. A self

confident person is not afraid to ask questions on topics where they feel they need

more knowledge. Self confidence is one of the most important attitudes which help us

Page 48

38

develop our career. This skill of asking question with any hesitation and good

communication with different stakeholders has developed self confidence.

xii. Creativity: During internship analytical skills were developed that in turn has

fostered creativity and innovation.

xiii. Self – Motivation: Internship has helped to understands responsibility on the job

and complete it without any prodding from others. Working in a supportive work

environment and taking the initiative has provided to be self-directive and increased

self-esteem.

3.2 Feedback to Organization

It was an interesting experience to do internship in Central bank of Nepal, i.e. NRB.

The staffs were highly cooperative and due to their keen help learned big deal about

activities in NRB. This type of internship is good for the entire development of the

Internee personality. It would be a great help to intern students in selection of job or

future field of work.

Working as an intern in NRB was a great experience which led to learn different skills

and attitudes in professional working environment. It was right place where the

theories studied in college were really implemented in practical grounds. It further

helped to find out the gap between what to learn and what market needs. So, RBB was

a good choice as an intern organization due to the fact that it was very gainful and

rewarding. Some of the study and observations made during internship has led some

feedback and recommendations. Some of the suggestions for efficiency and

effectiveness in performance are:

a) Bank should optimally use the resources available and any required resources

should be assessed. Use of modern technology is impulse of today’s banking.

Thus, new and effective means of technology should be used for providing

service to the customer.

b) Re-structure and re-organize the job and responsibilities so that there is

efficiency in job completion.

c) Proper maintenance of computers and other devices should be ensured timely

in regular fashion.

Page 49

39

d) Reduce the over-employed staff so as to reduce cost and bring efficiency in the

job.

e) The organization should improve its departmental overload which is now for

few staff only.

f) The operations should be systematized and in proper flow of the work.

g) The bank has inefficient IT infrastructure i.e. Server Room, Back up etc. so it

should be improved.

h) The concept of transfer, rotation and promotion of job problematic which cause

several problems. It should be improved. Also proper planning of leave of

staffs should be done.

i) Staffs should be familiar with IT and technologies.

j) Staffs should be provided adequate training on use of computers and other

devices.

k) Good corporate governance should be ensured that maintains sustainable

profitability in the system.

3.3 Feedback to College/University

Internship is defined as learning, proper supervision of the intern is essential. Ongoing

supervision of the intern student is key to the success of the internship program.

The college and university both institutions have provided us an opportunity to gain

some practical knowledge on what we are learning in our class rooms. Theory unless

made behavior have no use. Thus, this internship program offered by college and

university in fact has been proven to be the first milestone in professional career.

The internship program is to be conducted by the students as per the requirement of

the university. It is also a responsibility of the college to provide good and practical

opportunities to the students to impart the real world situations. There are some

recommendations to the college and university, which are:

a) The college/university should prepare a fixed framework of internship

activities to be carried out by students during internship.

b) Such framework should be initially conveyed to the students so that any

misunderstandings and confusions may be avoided.

Page 50

40

c) Proper inspection of intern student should be made by college in proper time

and in regular manner during the tenure of internship.

d) Since it was first time much confusion were hovering around in matter of

report preparation and during selection of organization. Faculty should take

possible steps to mitigate such perplexity.