Winter 2017-2018 Management · Digitalization · Strategy · Systems · Global Hau Thai-Tang Top Ford executive sees changing automaker-supplier relationship in new-tech era Start-up scene Ontario Young high-tech companies strengthen region's role in global automotive industry Blockchain Auto industry expects digital ledger to offer great potential for cost savings, data security Interview: Ola Kaellenius Daimler R&D boss values global network of competence centers INSIDE: DAIMLER SPECIAL IT and the changing face of automotive R&D (p. 19-26)

Transcript

Winter 2017-2018

Management · Digitalization · Strategy · Systems · Global

Hau Thai-TangTop Ford executive seeschanging automaker-supplier relationship in new-tech era

Start-up scene Ontario Young high-tech companiesstrengthen region's role in global automotive industry

BlockchainAuto industry expects digital ledger to offer great potential for cost savings, data security

Interview: Ola Kaellenius Daimler R&D boss values global network of competence centers

INSIDE:DAIMLER SPECIALIT and the changing face of automotive

R&D (p. 19-26)

Winter 2017-20182

The future is digital, whether for your car or for your business. You need

experts who understand mobility as well as digitalization – people who

pave the way with Big Data & Analytics, Industry 4.0, the Connected

Car, Artificial Intelligence and new Customer Experiences. At MHP, we

introduce the future to the world’s premier automotive companies.

Allow us to introduce you. www.mhp.com

Excellence in Management- and IT-Consulting for Mobility and Manufacturing.

Accelerate into a successful future.

With your trusted mobility and digitization experts.

beau

fort

8.de

WE WISH ALL MOBILITY EXPERTS JOYFUL HOLIDAYS AND A SUCCESSFUL 2018!

In 2018, information technology will even more strongly deter-mine the direction of the global automotive industry. Wheth-er it's new business areas for traditional car brands, making powertrains more environmentally friendly, or getting cars to drive without drivers at the wheel, the key enablers will have to be hardware and software.

There has been major progress on all these fronts in 2017 and this will continue in the new year. Advanced robotics will make car production smarter. Artificial intelligence and ma-chine learning will increase the likelihood that autonomous vehicles will one day help realize near-accident-free personal mobility. As ever-greater computing power becomes available, connected functionality in the car will become more usable and useful. And the new business models for transportation now under development will, with the help of seamless con-nectivity, make it easier for people to get from A to B in a prac-tical, comfortable and sustainable manner.

Are we actually going to see any tangible results from these developments in 2018 already? Probably not. But there will be continued progress. There will surely be more electric cars on the road and driver assistance will continue to improve on the

way to fully autonomous vehicles. Moreover, more powerful computers and software will increase manufacturing and sup-ply chain efficiency. And cooperation between automakers, IT service providers, regulators and city and regional authorities will undoubtedly move to the next level, as they jointly look for new mobility solutions.

In our outlook for the year 2018, which starts on page 55, we talk about artificial intelligence, blockchain, augmented reality, micro-services platforms and quantum computing as some of the key trends now embraced by automakers. All these tech-nologies come from the IT sector and all are finding strong use cases in the auto industry. It's further proof that these two worlds are now settling into a very productive phase of coop-eration.

The automotiveIT International team wishes you a happy and relaxing holiday season and a very good start to the new year!

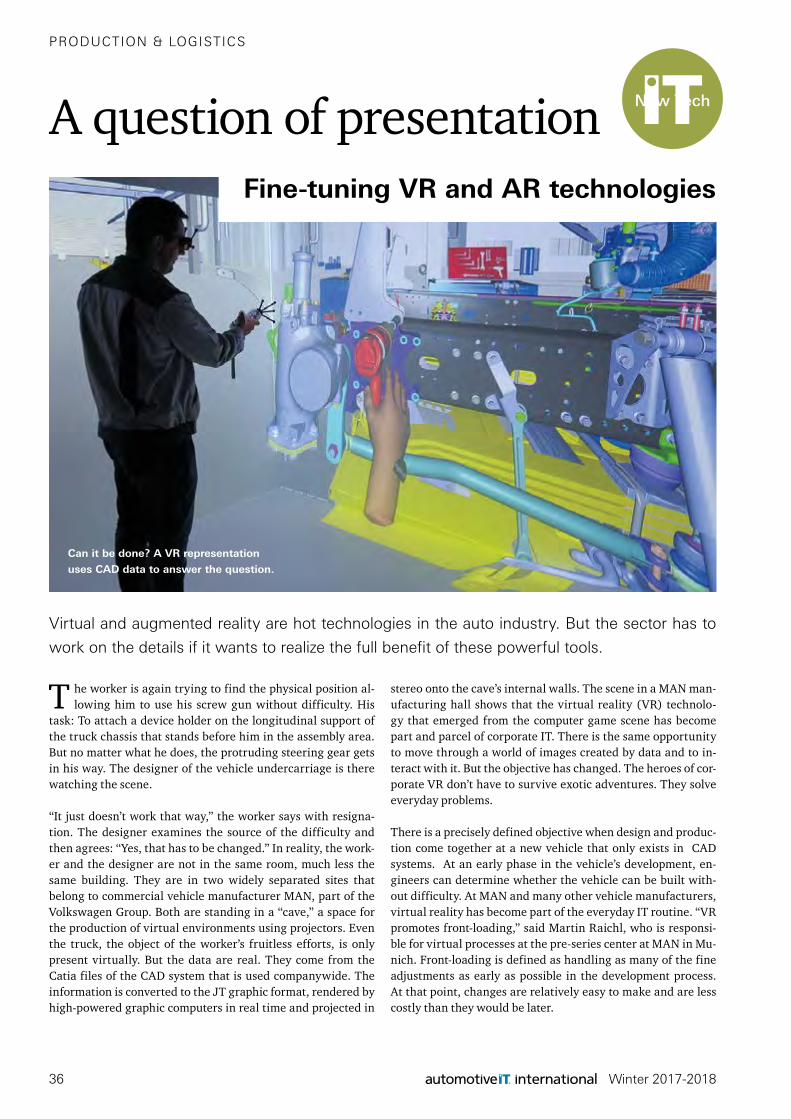

Virtual reality. Automotive companies are beginning to deploy virtual and augmented reality in their factories and IT and production executives see major benefits. But the technology needs further refinement as users complain about heavy headsets, modest image quality and workers' unfamiliarity with the systems. Automakers BMW and Audi and VW's truck brand MAN are hard at work to make the systems fit to be used in a wide range of processes.

Ford's supply base. Top executive Hau Thai-Tang says the carmaker is adopting a new way to deal with its suppliers as focus increasingly shifts to software.

Artificial intelligence. Automakers agree that ma-chine learning will be essential in getting autonomous cars to behave properly in complex traffic situations.

36

32 6

Winter 2017-2018 5

TABLE OF CONTENTS

New technology. Survey finds growing focus on next-generation connected-car technologies.

Global R&D. A worldwide network of competence centers helps Daimler meet local requirements.

Agile workplace. automotiveIT visits two carmakers that have already built new work environments.

CES & Detroit Auto Show. Preview: Two big trade shows will set the automotive agenda for 2018.

IT Trends 2018. AI, blockchain and quantum computing are set for growth in coming year.

Blockchain. Auto industry expects digital ledger to lower transaction costs and boost security.

Shifting boundaries. Daimler's IT department is providing support for digitalization programs.

Porsche. Digitalization chief moves sports car brand into a world beyond just the car.

LA Auto Show. Lines blur between automotive and IT as both industries pursue new mobility.

Germany’s top 25. IT service providers to the auto industry post strong business growth.

Ola Kaellenius. R&D boss looks for software talent across global network of development centers.

Ontario. The Canadian province strives to be a center for high-tech automotive development.

Ian Robertson. Retiring BMW sales boss sees role for car show-rooms in "multi-channel world."

Hyperloop. An exciting new mode of transportation faces a wide range of obstacles.

VW electrifies. German carmaker embarks on major electric-vehicle push as industry trend accelerates.

24 Management · Top 25 der IT-Dienstleister

automotiveIT 08/09 · 2017

_Unter Vorbehalt. Die 25 größten IT-Dienstleister in der Autoindustrie überraschen mit guten Zahlen und noch besseren Prognosen. Doch die Zukunft der Branche ist ungewiss und die Stimmung könnte jederzeit umschlagen.

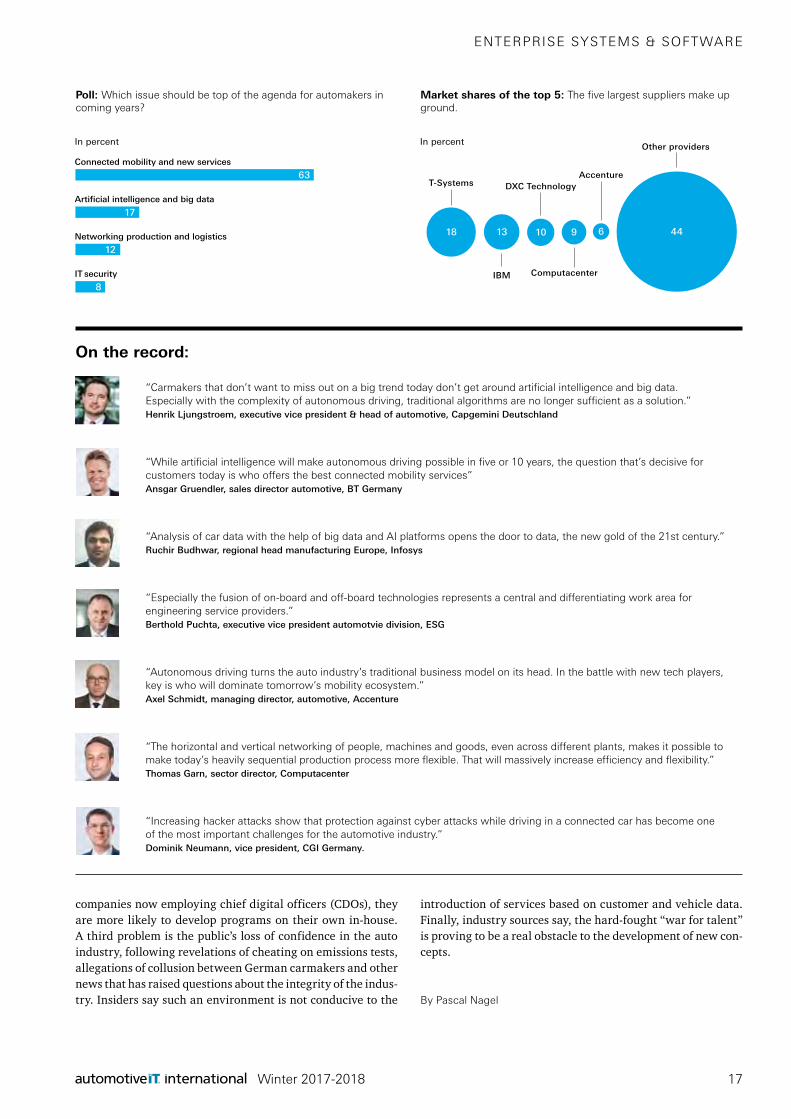

T-Systems

18

IBM

13

DXC Technology

10

Computacenter

9

Accenture

6

Sonstige

44

In Prozent

Marktanteile der Top Five: Die fünf größten Anbieter können Boden gutmachen.

Qu

elle

: au

tom

oti

veIT

In Prozent

Umfrage: Welches Thema sollte bei den OEMs in den kommenden Jahren ganz oben auf der Agenda stehen?

Künstliche Intelligenz und Big Data

17

Vernetzte Mobilität und neue Services

63

Vernetzung von Produktion und Logistik

12

IT-Security

8

T-SystemsIBM

DXC TechnologyComputacenter

AccentureMHP

NTT DataInfosys

Atos Information TechnologyCapgemini

All for One Steeb

ESG Elektroniksystem und LogistikSulzer

AltranH&D International Group

CGIAbat

BT Germany

MVI Solve-IT

BearingPoint

Cenit

operational services

Allgeier

ckc

msg systems

8

28

44

55

12

30

4946

15

38

50 52

Daimler Special (p. 19-26)

20 22 24

Winter 2017-20186

DECISION MAKERS

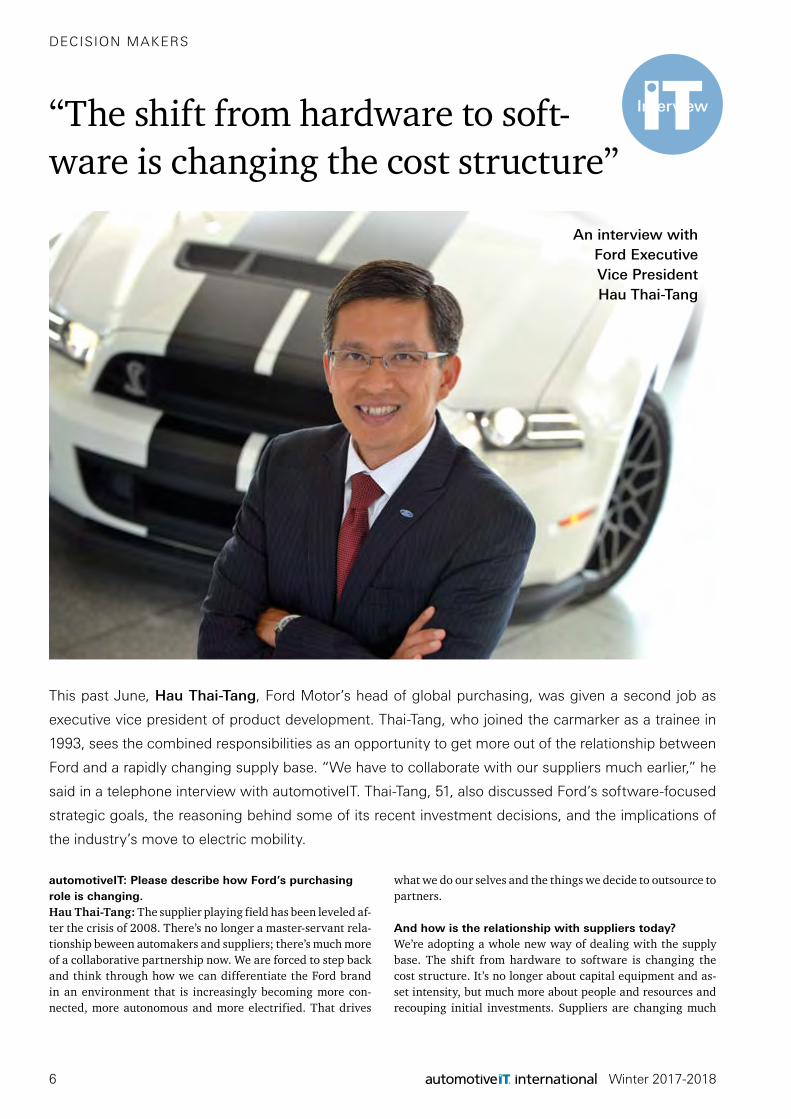

automotiveIT: Please describe how Ford’s purchasing role is changing.Hau Thai-Tang: The supplier playing field has been leveled af-ter the crisis of 2008. There’s no longer a master-servant rela-tionship beween automakers and suppliers; there’s much more of a collaborative partnership now. We are forced to step back and think through how we can differentiate the Ford brand in an environment that is increasingly becoming more con-nected, more autonomous and more electrified. That drives

what we do our selves and the things we decide to outsource to partners.

And how is the relationship with suppliers today?We’re adopting a whole new way of dealing with the supply base. The shift from hardware to software is changing the cost structure. It’s no longer about capital equipment and as-set intensity, but much more about people and resources and recouping initial investments. Suppliers are changing much

This past June, Hau Thai-Tang, Ford Motor’s head of global purchasing, was given a second job as

executive vice president of product development. Thai-Tang, who joined the carmarker as a trainee in

1993, sees the combined responsibilities as an opportunity to get more out of the relationship between

Ford and a rapidly changing supply base. “We have to collaborate with our suppliers much earlier,” he

said in a telephone interview with automotiveIT. Thai-Tang, 51, also discussed Ford’s software-focused

strategic goals, the reasoning behind some of its recent investment decisions, and the implications of

the industry’s move to electric mobility.

“The shift from hardware to soft-ware is changing the cost structure”

An interview with Ford Executive Vice President Hau Thai-Tang

Interview

Winter 2017-2018 7

DECISION MAKERS

faster. With traditional hardware, we assume 10 year amor-tization and depreciation of physical assets. In the software space, assets may be out of date after a mere 10 months.

How do you decide which components and systems you buy, where you want to take equity stakes in specialist companies and whether you need to own a particular technology?We look at whether a technology is key to differentiating the brand, whether we expect there to be an imbalance between supply and demand and whether our product portfolio will have sufficient scale to justify the capital investment. And we ask the question: what value does it bring to the company?

With Ford's investment in Velodyne, you've clearly iden-tified lidar as a technology you want to own.We see lidar as a critical enabling technology for level 4 (auton-omous) driving and above. Lidar is an integral part of how we are developing our virtual driving system, so we felt we need-ed a very strong and close partnership with lidar companies. That’s why we took an ownership stake in lidar specialist Velo-dyne. And why our Argo AI subsidiary recently acquired (lidar sensor maker) Princeton Lightwave. If we we want access to that technology or have preferential treatment, it’s helpful to have an equity stake.

Batteries will also be key as the industry moves to elec-tric propulsion. Do you expect Ford to get into battery cells too?Battery cell production is very asset-intensive. Look at Tes-la’s Gigafactory, which will cost billions of dollars. It also requires quite a bit of scale to justify such an investment. At the moment, the Ford product portfolio doesn’t have enough volume to justify that level of investment. That’s why it would be better to buy battery cells from the supply base, which can leverage demand across various automakers and even across industries. For us, that’s a much more efficient and better use of capital. We’re also not sure whether battery chemistry will change. So today we cannot justify the investment. That may change over time.

How – and how fast – are electric vehicles changing the industry?Electric motors simplify things with much fewer moving parts than a combustion engine. Electric vehicles have really re-duced or even eliminated barriers to entry into the automotive space. The internal combustion engine has served as a barri-er to entry for 100 years, but now we don’t just find compa-nies such as Tesla, Apple and Google coming in, but also the likes of Dyson, which makes vacuum cleaners and hair dryers, and several Chinese start-ups. All can become automakers. But even if there will be a tipping point for electric vehicles around 2025, a big chunk of new products will be hybrids. The transition period will be a couple of decades, which means we will still have to master both electric-motor and combus-tion-engine technologies. But electric mobility will have a lot of repercussions all the way through the value chain. Fewer moving parts means less service revenue. It will affect the af-

termarket and dealerships, where a big part of the profits come from service. There will be no more oil changes and a lot of the traditional maintenance will go away.

Ford has embarked on a course to become a mobility and software company. How are things going with this massive culture change?We’re a public company but the family’s name is on the build-ing and Bill Ford is executive chairman. The perspective of the Ford family is very much long term. We realize the shift in the value chain is happening right before our eyes. Once the car becomes part of the internet of things, you’re no longer just selling a physical product. You have data and services you can provide and that’s where you’ll be able to capture value. Micro-soft CEO Satya Nadella told us that Google makes more money per PC than Microsoft does. Microsoft was slow to reocgnize the shift in value creation and that’s a lesson for Ford. We're going to make sure we still deliver great products, but we real-ize that the value creation will move beyond the physical hard-ware. That’s the future we’re trying to prepare for.

As of June 1 you head both purchasing and product development. Is that a good combination?I spent 25 years in product development before moving to pur-chasing these past four years. The biggest thing I learned in the past four years was that, if we want to deliver innovative solutions and bring new technology to market, we have to start collaborating with our suppliers much earlier. The tradi-tional product-development model, where you engineer a part and let purchasing request quotes, does work, but there’s a lot more that can be done to make designs more efficient. If the supply chain comes up with a great idea, it's typically too late to incorporate it. The shift we’re making is to let suppliers bet-ter use the parts and investments they’ve already made. That approach creates greater value and improves quality. There’s a huge opportunity for us to work together more efficiently with product development, purchasing and the supply base.

Like many executives in the auto industry, you have a mechanical engineering degree. Does that mean you’ve had to learn a whole lot of new skills as the automotive focus is moving more toward digital technologies?Evolving and learning is a lifelong process that doesn’t end when you get out of school. Having a good grounding in me-chanical engineering is a good solid technology foundation to build on.

And how do you divide your time between product devel-opment and purchasing?I spend most of my time managing the progression of the 60 or so product programs that are somewhere between engineer-ing, launch and mass production. That includes making sure we have the right supplier partners, are sourcing business to the right people and are delivering best value. I probably spend about 65 percent of my time on product-related measures and about 35 percent on the procurement side of the business.

Interview: Arjen Bongard

Winter 2017-20188

CAR IT

Pressure to innovateRankings show growing role for China

The auto industry is navigating choppy seas these days. Volkswagen Group’s diesel scandal, antitrust investigations at German car companies, the high cost of digitization, the electrification of the car, autonomous driving, new business models, etc. These are just a few of the challenges faced by global automakers today. Especially in Germany, VW’s admission of cheating on diesel emission tests has led to an erosion of trust in the auto industry as a whole. And it couldn’t have come at a worse time. After all, carmak-ers are engaged in a veritable paradigm shift from sheet metal to mobility. And, as they make the transition, they are encountering increased competition from non-automo-tive players.

Against this backdrop, it is good news for the industry that in-novation, as measured by the Connected Car Innovation Index (CCI), is alive and well. The index, calculated this year for the third time by Germany’s Center of Automotive Management (CAM) in cooperation with automotiveIT, compares the per-formance and innovative capacity of 19 automotive manufac-turers and the most important automotive nations based on a wide variety of core indicators. One trend already became clear last year: the number of connected-car innovations is steadily growing with the advance of the digital transforma-tion. While the share of such innovations was still at 33 per-cent in 2006, one out of every two are now networking solu-tions. This year the total even climbed to a new record: 621

VW's I.D. Crozz is a fully connected show car that feeds the

driver with all the information he needs while on the road.

Innovationindex

Illus

trat

ion:

VW

Winter 2017-2018 9

CAR IT

connected car innovations could be identified from the fields of telematics, safety systems and controls and display concepts within the 2016 survey timeframe.

The Audi factor

In 2016, both the overall number of innovations and the new connected-car products and services – adjusted for slight changes in methods – were higher than the totals for the pre-vious year. “An end to the enormous innovation dynamic in the connected-car area is not in sight,” the study’s manager, Stefan Bratzel of CAM, said. “Networking and digitalization remain central paradigms in manufacturers’ research and de-velopment.” Once again, the undisputed number one for inno-vations in vehicle technology is the Volkswagen Group. But as in previous years, its success depended heavily on its Audi pre-mium-car subsidiary, which scored 85 out of the VW Group’s 134 index points by itself. If the VW brand had competed in the ranking on its own, it would only have landed in midfield with 30 points. There are questions over whether Audi can continue its innovation course. “The VW Group has been badly battered lately, and now Audi has to meet ambitious cost-cutting goals in coming years,” Bratzel said. “It will be interesting to see whether the group will maintain its position.”

Mercedes-Benz scored the highest in the individual-brand ranking, giving Daimler a leap forward as well. It pulled past electric car pioneer Tesla to the second spot. Daimler owes its improvement over the previous year to the new innova-tion-packed E-Class. Tesla, the big surprise in 2016, was able to maintain its position ahead of BMW thanks to new tech-nology features in autonomous driving, parking and other areas. In general, the electric-car specialist seems to have es-tablished itself as one of the industry’s top innovators. Tesla exhibited the greatest innovation intensity of all 19 automak-ers for the third year in a row. The established players would be wise to take this as more than a hint. That would seem to apply to BMW. It slipped from the top three this year. The Mu-nich-based automaker was revealed to be a bit weak in “world-firsts.” Among other things, the market introduction of the new 5 Series might be to blame. It came along at the start of 2017 and thus was too late to be considered in the ranking. But the automaker should not be written off in the competition for the top spot: “BMW is a pioneer of connected-car technologies, which they have strongly advanced over the past 20 years,” said CCI juror and automotive analyst Hans-Georg Frischkorn. “Perhaps we are seeing a strategic shift in emphasis at BMW, perhaps towards mobility services. It is doubtful whether the same thing applies to other mid-range and low performers in the field.” The trend at the two giants General Motors and Toy-ota is especially dramatic. Between 2005 and 2009, they could still compete on a par with Germany’s manufacturers. In 2016, however, GM only managed a 5th place – up one spot from last year, while Toyota was 14th on the list, down from 10. And the number and quality of innovations at both companies was sharply below those of the two leaders, VW Group and Daim-ler, according to the CCI jury.

Vehicle-technology innovations

Innovation strength (Number and quallity of innovations)

0 20 40 60 80 100 120 140

Aut

om

aker

gro

ups

VW

Honda

Tesla

Toyota

BMW

Renault

Daimler

Mazda

Tata*

Nissan

PSA

Subaru

GM

Geely

Mitsubishi

Hyundai

Fiat Chrysler

Ford

Suzuki

No. of innovations (index points)

■ 2016 ■ 2015

BMW, No. 4 in the innovation rankings, aims to seamlessly

integrate the car into customers’ digital world. (Photo: BMW)

The Sedric. CEO Matthias Mueller shows what a fully autono-

mous Volkswagen vehicle could look lilke. (Photo: VW)

Winter 2017-201810

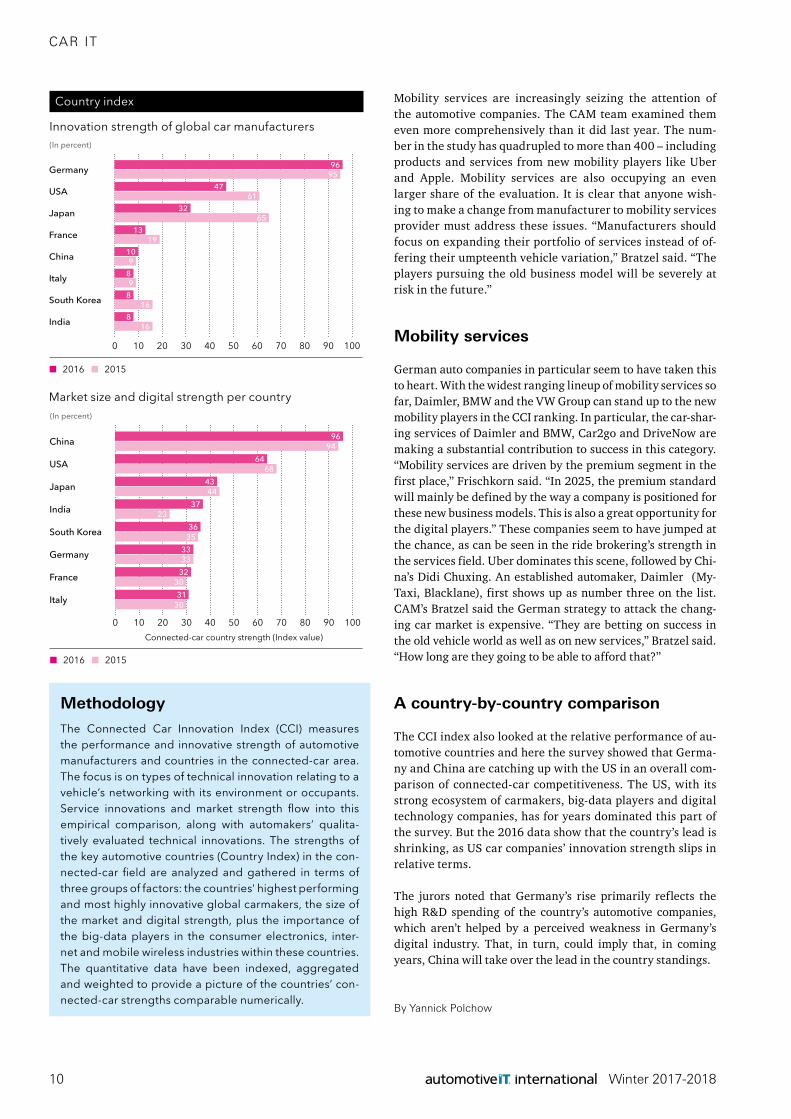

Mobility services are increasingly seizing the attention of the automotive companies. The CAM team examined them even more comprehensively than it did last year. The num-ber in the study has quadrupled to more than 400 – including products and services from new mobility players like Uber and Apple. Mobility services are also occupying an even larger share of the evaluation. It is clear that anyone wish-ing to make a change from manufacturer to mobility services provider must address these issues. “Manufacturers should focus on expanding their portfolio of services instead of of-fering their umpteenth vehicle variation,” Bratzel said. “The players pursuing the old business model will be severely at risk in the future.”

Mobility services

German auto companies in particular seem to have taken this to heart. With the widest ranging lineup of mobility services so far, Daimler, BMW and the VW Group can stand up to the new mobility players in the CCI ranking. In particular, the car-shar-ing services of Daimler and BMW, Car2go and DriveNow are making a substantial contribution to success in this category. “Mobility services are driven by the premium segment in the first place,” Frischkorn said. “In 2025, the premium standard will mainly be defined by the way a company is positioned for these new business models. This is also a great opportunity for the digital players.” These companies seem to have jumped at the chance, as can be seen in the ride brokering’s strength in the services field. Uber dominates this scene, followed by Chi-na’s Didi Chuxing. An established automaker, Daimler (My-Taxi, Blacklane), first shows up as number three on the list. CAM’s Bratzel said the German strategy to attack the chang-ing car market is expensive. “They are betting on success in the old vehicle world as well as on new services,” Bratzel said. “How long are they going to be able to afford that?”

A country-by-country comparison

The CCI index also looked at the relative performance of au-tomotive countries and here the survey showed that Germa-ny and China are catching up with the US in an overall com-parison of connected-car competitiveness. The US, with its strong ecosystem of carmakers, big-data players and digital technology companies, has for years dominated this part of the survey. But the 2016 data show that the country’s lead is shrinking, as US car companies’ innovation strength slips in relative terms.

The jurors noted that Germany’s rise primarily reflects the high R&D spending of the country’s automotive companies, which aren’t helped by a perceived weakness in Germany’s digital industry. That, in turn, could imply that, in coming years, China will take over the lead in the country standings.

By Yannick Polchow

0 10 20 30 40 50 60 70 80 90 100

Country index

Innovation strength of global car manufacturers

Germany 9695

4761

3265

1319

109

89

816

Japan

USA

France

India

South Korea

Italy

China

816

(In percent)

■ 2016 ■ 2015

0 10 20 30 40 50 60 70 80 90 100

Connected-car country strength (Index value)

China 9694

USA 6468

Japan 4344

South Korea

3723

Germany

3682

Italy

3333

France 3230

30

India

31

35

Market size and digital strength per country (In percent)

■ 2016 ■ 2015

Methodology

The Connected Car Innovation Index (CCI) measures the performance and innovative strength of automotive manufacturers and countries in the connected-car area. The focus is on types of technical innovation relating to a vehicle’s networking with its environment or occupants. Service innovations and market strength flow into this empirical comparison, along with automakers’ qualita-tively evaluated technical innovations. The strengths of the key automotive countries (Country Index) in the con-nected-car field are analyzed and gathered in terms of three groups of factors: the countries' highest performing and most highly innovative global carmakers, the size of the market and digital strength, plus the importance of the big-data players in the consumer electronics, inter-net and mobile wireless industries within these countries. The quantitative data have been indexed, aggregated and weighted to provide a picture of the countries’ con-nected-car strengths comparable numerically.

CAR IT

Winter 2017-2018 11

In-Car Security. We create more security for connected vehicles and the entire Connected Ecosystem – mainly through enabling encryption for data-in-motion and data-at-rest through a certi� cate based-authentication infra-structure inside the car.

5G. We are involved in the development of the mobile radio standard of the future - the basis for automated driving. We enable the exchange of the required data volumes in the Connected Car Ecosystem, for example for monitoring and controlling the advanced driver assistance system and high quality VR overlay.

CloudWAN. With CloudWAN we support the development of the Connected Car Ecosystem. The technology enables, among other things, rapid deployment of updates in the conncted vehicle, data protection with managed security services and seamless networking between cars, enterprise locations and cloud services.

Urban Mobility Marketplace (UMM). The NTT Group has been working for many years on the development of intermodal forms of mobility. With the intermodal and urban mobility concept UMM, mobility providers can implement their services in order to bene� t from networking among themselves and the large number of customers. As a global company, we offer the opportunity to roll out mobility services and platforms in a highly ef� cient and reliable manner via our global network.

Big Data. everisMoriarty is an analytical model developed by us with reasoning engine, machine learning, deep learning and pattern recognition. It enables the evaluation of digital media, semantic search, adaptive recommendations and advanced customer pro� ling.

Driver assistance. With COREVO we increase driving safety through the use of arti� cial intelligence. The t-shirt HITOE, developed by us and equipped with sensors, can measure the driver’s vitality (ECG) with sensors, makes stress-free driving possible and gets help if needed.

When the car takes control …Electric car, autonomous driving, car sharing –We develop safe and connected mobility concepts of the future.

Being successful means meeting customer expectations. So far, this meant building the best cars in the world. If you want to continue being successful tomorrow, you have to think about it today. Focus on new driving modes and technologies. Breathe connectivity. Develop new business models. Being successful tomorrow means growing into a mobility service provider.

Examples of our high automotive and IT competenceWith our sister companies Dimension Data, NTT Communications, NTT Security, NTT Docomo and everis we support the automotive and supplier industry in the design and development of innovative integrated solutions for tomorrow’s mobility.

NTT DATA

NTT DATA is one of the world’s leading business and IT consulting company, with business operations in more than 50 countries. As a global innovation partner for our customers, we combine global reach with local proximity that is closely interconnected with our innovation centers.

We accompany our customers on their journey to becoming a digital company. Our portfolio includes business and IT consulting, system integration and application management services. Our technological leadership is paired with a deep understanding of our target markets: automotive, manufacturing, banking, insurance and telecommunication.

ADVERTISEMENT

Winter 2017-201812

Pho

to: A

udi,

Big

chai

nDB

Ill

ustr

atio

n: S

abin

a V

ogel

With the versatility of a Swiss Army knife, blockchain is rapidly attracting interest across the automotive indus-try. The technology may not be ready for a major role in business processes just yet, but its time is coming rapidly.

Bruce Pon, the CEO of BigchainDB, is optimistic. “The internet has reduced the costs of transferring information by a factor of 1,000, blockchain will cut transaction costs by a factor of 1,000,” predicts the CEO of the Berlin-based operator of a scal-able database that can provide an easy entry into the block-

BlockchainDigital ledger technology set to grow in auto industry

Security & efficiency

ENTERPRISE SYSTEMS & SOFTWARE

Winter 2017-2018 13

chain world. Blockchain, which was originally developed as an accounting system for the online currency bitcoin, is a technol-ogy that could become an extremely powerful force in stream-lining data and business processes. It employs a decentralized ledger that allows digital information to be distributed across a multitude of computers. It lets users of digital currency keep track of their transactions without central accounting. And be-cause data is distributed widely across many computers, it is held more safely and is less subject to fraud.

New initiatives

The auto industry has recognized the potential, but, when it comes to implementation, it’s early days. Still, several auto-makers and suppliers are beginning to use blockchain:

· Daimler has started to deploy blockchain in some finan-cial transactions. Together with Germany’s Landesbank Baden-Wuerttemberg (LBBW) the premium car group used blockchain to arrange a 100m euro loan. Blockchain digi-tally took care of origination, distribution, allocation and execution of the loan agreement as well as the confirmation of repayment and of interest payments. Daimler’s finance chief, Bodo Uebber, said the project was the “first step in testing the wide variety of possibilities for using blockchain technology and assessing this technology’s potential for fu-ture transactions and financial processes.” Kurt Schaefer, vice-president at Daimler’s treasury, said he saw wider po-tential as well. “Other possible applications of blockchain technology in the financial sector include payment trans-actions, the securities trade, and the cross-border shipment of goods,” he said.

· In July, Renault announced a prototype for a digital car maintenance book it developed together with Microsoft and digital service company Viseo. The project used block-chain technology to make sure that data in the document are transparent and stored securely. “This digital car main-tenance book will enable us to provide our customers with new services in an ecosystem alongside insurers and deal-ers,” said Elie Elbaz, Renault’s digital & connected vehicles director. “Blockchain technology is able to create a reliable trust protocol.”

· Toyota said in May it was working with partners exploring how blockchain and distributed ledger technology could help accelerate development of autonomous driving tech-nology. The Japanese carmaker said its advanced research arm, the Toyota Research Institute (TRI), believed block-chain may bolster trust among its users by creating greater transparency. TRI also said blockchain could reduce fraud risk and reduce or eliminate transaction costs.

· Together with partners, supplier ZF Friedrichshafen has developed a so-called Car eWallet, which uses block-chain technology provided by IBM. The digital assistant allows secure payments, even while a car is in motion. It

also can perform other tasks in the vehicle, such as opening the trunk or doors. Blockchain makes it possible to secure-ly synchronize the information of each participant in the network and ZF believes the open automotive transaction platform could radically change e-commerce between au-tomakers, suppliers, service providers and customers.

· Automotive supplier Robert Bosch has expressed strong support for the technology and is looking into at least one application that could be ready for the market in a few years. “For us, blockchain and its related technologies are strategically very important,” Bosch CEO Volkmar Denner said in September.

· And Audi indicated recently that it is testing whether block-chain could be used across its operations. One possible ap-plication would be its use in documenting international logistics processes. In this case, shipping documents would be replaced by blockchain entries that represent individual deliveries or components with the help of so-called digital twins. Adoption of blockchain would enhance transparency.

More efficient

Auto industry insiders said they are keen to adopt the new technology, in particular because of the added data security it provides. But that sentiment contrasts with a poll published in September during the Frankfurt Auto Show by Germany’s high-tech association Bitkom. The survey showed that a mere one-third of automakers and suppliers had heard of block-

Source: Bosch

Bosch CEO Volkmar Denner says blockchain is "strategically

very important" for the supplier group. (Photo: Bosch)

ENTERPRISE SYSTEMS & SOFTWARE

Winter 2017-201814

chain as a technology to be used in company processes. Bitkom asked 177 management board member of companies with at least 20 employees. But BigchainDB chief Pon sees big oppor-tunities for automotive companies. “The current IT landscape in the auto industry doesn’t work 100 percent at the moment,” he said. Particular areas for improvement are ERP and MES systems that produce car data and control manufacturing processes. That’s because these systems have to communicate with numerous other systems that all rely on data. “This com-plexity makes business processes less agile and leads to a par-tial loss of information or to contradictory information, when data come from different sources,” Pon said. His vision: Block-chain provides a reliable source of data that can, ideally, make parts of companies’ middleware superflous. That, in turn, can help simply the IT landscape.

Autonomous vehicle testing

Blockchain may also help solve one of the major R&D challeng-es the auto industry faces when it wants to test autonomous vehicles. Today, it is virtually impossible to devise a cost-ef-fective way to absolve the tests necessary to get regulatory ap-proval for a driverless car or the assistance systems for such vehicles. The reason: Because highway accidents statistically only occur every 5 million kilometers driven, an autonomous vehicle would have to be tested over 50 million kilometers to get a reliable test result. That would cost about 50 million eu-ros. Moreover, every time a carmaker modifies a car, new tests would be necessary. The Toyota Research Institute earlier this year addressed this problem, together with the MIT Media Lab. One of the ideas that came out of this cooperation was to have companies and individuals share driving information securely with the help of blockchain. A market for this data would be created where the information would be available to interested parties. All this information could be used for the testing of autonomous cars and a range of other applications. “Hundreds of billions of miles of human driving data may be needed to develop safe and reliable autonomous vehicles,” TRI’s director of mobility services, Chris Ballinger, said in a statement. “Blockchains and distributed ledgers may enable

pooling data from vehicle owners, fleet managers, and man-ufacturers to shorten the time for reaching this goal, thereby bringing forward the safety, efficiency and convenience bene-fits of autonomous driving technology.”

Odometer fraud

Yet another use case for blockchain could be the reliable doc-umentation of a car’s history. The technology would allow, for example, the verification of car components without the need for a central authority or a critical mass of participants. Two partners would be sufficient to start the system. BigchainDB, Volkswagen Financial Services and German energy company Innogy worked on such a project in a hackathon earlier this year. “The idea is a digital vehicle file that can be used in an interoperable way,” said Carsten Stoecker, senior manager at Innogy Innovation Hub. One concrete implementation the three companies are researching is how to combat odometer fraud, which helps make a car look younger than it is by wind-ing back the gauge that records kilometers driven. Bosch, to-gether with testing company TUEV Rheinland, is engaged in similar research. Using blockchain, a car would get a digital certificate that verifies the data is authentic. And because data is distributed across a multitude of computers, it is safer and cannot be manipulated easily. A Bosch spokesman said a prod-uct to fight odometer fraud using blockchain could be ready for market introduction “in 2020 at the latest.”

A digital certificate would also be an asset in manufactur-ing and supply chain logistics. Cryptographic signatures can be used to confirm the identity of parts across the transport and after-sales process. Bosch said such a system could im-prove quality and efficiency and lower costs. Innogy’s Stoeck-er agreed that there are many use cases for blockchain. Said Stoecker: “There are umpteen kinds of data that would be in-teresting for other conceivable applications.”

By Michael Vogel

and Arjen Bongard

ZF's Car eWallet uses blockchain technology developed by

IBM. (Photo: ZF)

Renault has produced a digital car maintenance book with

the help of blockchain technology. (Photo: Renault)

ENTERPRISE SYSTEMS & SOFTWARE

Winter 2017-2018 15

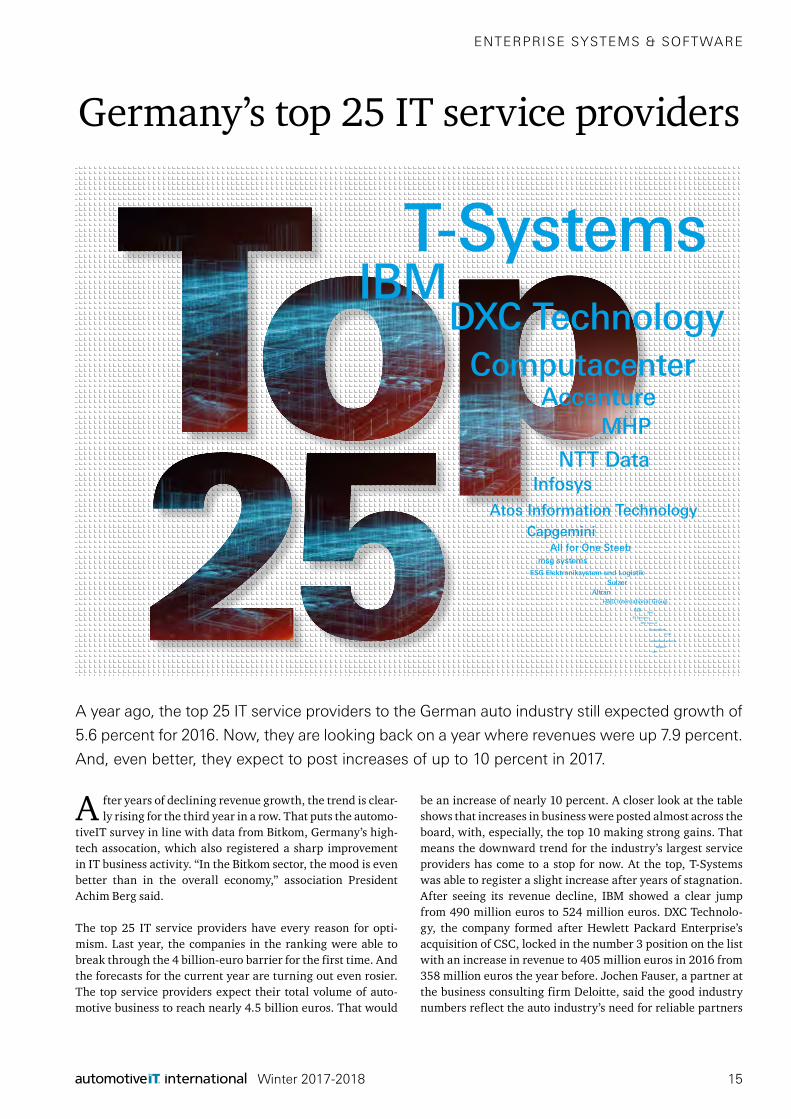

A fter years of declining revenue growth, the trend is clear-ly rising for the third year in a row. That puts the automo-

tiveIT survey in line with data from Bitkom, Germany’s high-tech assocation, which also registered a sharp improvement in IT business activity. “In the Bitkom sector, the mood is even better than in the overall economy,” association President Achim Berg said.

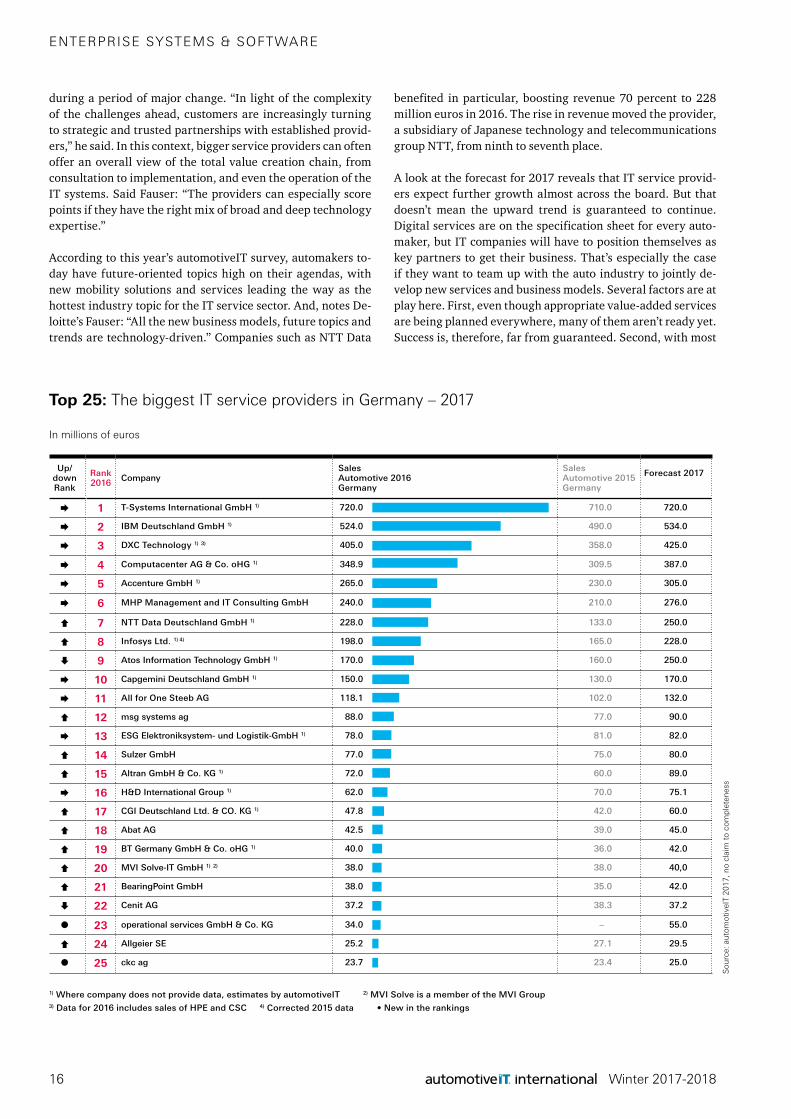

The top 25 IT service providers have every reason for opti-mism. Last year, the companies in the ranking were able to break through the 4 billion-euro barrier for the first time. And the forecasts for the current year are turning out even rosier. The top service providers expect their total volume of auto-motive business to reach nearly 4.5 billion euros. That would

be an increase of nearly 10 percent. A closer look at the table shows that increases in business were posted almost across the board, with, especially, the top 10 making strong gains. That means the downward trend for the industry’s largest service providers has come to a stop for now. At the top, T-Systems was able to register a slight increase after years of stagnation. After seeing its revenue decline, IBM showed a clear jump from 490 million euros to 524 million euros. DXC Technolo-gy, the company formed after Hewlett Packard Enterprise’s acquisition of CSC, locked in the number 3 position on the list with an increase in revenue to 405 million euros in 2016 from 358 million euros the year before. Jochen Fauser, a partner at the business consulting firm Deloitte, said the good industry numbers reflect the auto industry’s need for reliable partners

ENTERPRISE SYSTEMS & SOFTWARE

24 Management · Top 25 der IT-Dienstleister

automotiveIT 08/09 · 2017

_Unter Vorbehalt. Die 25 größten IT-Dienstleister in der Autoindustrie überraschen mit guten Zahlen und noch besseren Prognosen. Doch die Zukunft der Branche ist ungewiss und die Stimmung könnte jederzeit umschlagen.

T-Systems

18

IBM

13

DXC Technology

10

Computacenter

9

Accenture

6

Sonstige

44

In Prozent

Marktanteile der Top Five: Die fünf größten Anbieter können Boden gutmachen.

Qu

elle

: au

tom

oti

veIT

In Prozent

Umfrage: Welches Thema sollte bei den OEMs in den kommenden Jahren ganz oben auf der Agenda stehen?

Künstliche Intelligenz und Big Data

17

Vernetzte Mobilität und neue Services

63

Vernetzung von Produktion und Logistik

12

IT-Security

8

T-SystemsIBM

DXC TechnologyComputacenter

AccentureMHP

NTT DataInfosys

Atos Information TechnologyCapgemini

All for One Steeb

ESG Elektroniksystem und LogistikSulzer

AltranH&D International Group

CGIAbat

BT Germany

MVI Solve-IT

BearingPoint

Cenit

operational services

Allgeier

ckc

msg systems

Germany’s top 25 IT service providers

A year ago, the top 25 IT service providers to the German auto industry still expected growth of

5.6 percent for 2016. Now, they are looking back on a year where revenues were up 7.9 percent.

And, even better, they expect to post increases of up to 10 percent in 2017.

Winter 2017-201816

during a period of major change. “In light of the complexity of the challenges ahead, customers are increasingly turning to strategic and trusted partnerships with established provid-ers,” he said. In this context, bigger service providers can often offer an overall view of the total value creation chain, from consultation to implementation, and even the operation of the IT systems. Said Fauser: “The providers can especially score points if they have the right mix of broad and deep technology expertise.”

According to this year’s automotiveIT survey, automakers to-day have future-oriented topics high on their agendas, with new mobility solutions and services leading the way as the hottest industry topic for the IT service sector. And, notes De-loitte’s Fauser: “All the new business models, future topics and trends are technology-driven.” Companies such as NTT Data

benefited in particular, boosting revenue 70 percent to 228 million euros in 2016. The rise in revenue moved the provider, a subsidiary of Japanese technology and telecommunications group NTT, from ninth to seventh place.

A look at the forecast for 2017 reveals that IT service provid-ers expect further growth almost across the board. But that doesn’t mean the upward trend is guaranteed to continue. Digital services are on the specification sheet for every auto-maker, but IT companies will have to position themselves as key partners to get their business. That’s especially the case if they want to team up with the auto industry to jointly de-velop new services and business models. Several factors are at play here. First, even though appropriate value-added services are being planned everywhere, many of them aren’t ready yet. Success is, therefore, far from guaranteed. Second, with most

Top 25: The biggest IT service providers in Germany – 2017

Sou

rce:

aut

omot

iveI

T 20

17, n

o cl

aim

to

com

plet

enes

s

In millions of euros

Up/down Rank

Rank2016 Company

SalesAutomotive 2016 Germany

Sales Automotive 2015 Germany

Forecast 2017

1 T-Systems International GmbH 1) 720.0 710.0 720.0

2 IBM Deutschland GmbH 1) 524.0 490.0 534.0

3 DXC Technology 1) 3) 405.0 358.0 425.0

4 Computacenter AG & Co. oHG 1) 348.9 309.5 387.0

5 Accenture GmbH 1) 265.0 230.0 305.0

6 MHP Management and IT Consulting GmbH 240.0 210.0 276.0

7 NTT Data Deutschland GmbH 1) 228.0 133.0 250.0

8 Infosys Ltd. 1) 4) 198.0 165.0 228.0

9 Atos Information Technology GmbH 1) 170.0 160.0 250.0

10 Capgemini Deutschland GmbH 1) 150.0 130.0 170.0

11 All for One Steeb AG 118.1 102.0 132.0

12 msg systems ag 88.0 77.0 90.0

13 ESG Elektroniksystem- und Logistik-GmbH 1) 78.0 81.0 82.0

14 Sulzer GmbH 77.0 75.0 80.0

15 Altran GmbH & Co. KG 1) 72.0 60.0 89.0

16 H&D International Group 1) 62.0 70.0 75.1

17 CGI Deutschland Ltd. & CO. KG 1) 47.8 42.0 60.0

18 Abat AG 42.5 39.0 45.0

19 BT Germany GmbH & Co. oHG 1) 40.0 36.0 42.0

20 MVI Solve-IT GmbH 1) 2) 38.0 38.0 40,0

21 BearingPoint GmbH 38.0 35.0 42.0

22 Cenit AG 37.2 38.3 37.2

23 operational services GmbH & Co. KG 34.0 – 55.0

24 Allgeier SE 25.2 27.1 29.5

25 ckc ag 23.7 23.4 25.0

1) Where company does not provide data, estimates by automotiveIT 2) MVI Solve is a member of the MVI Group3) Data for 2016 includes sales of HPE and CSC 4) Corrected 2015 data • New in the rankings

ENTERPRISE SYSTEMS & SOFTWARE

Winter 2017-2018 17

ENTERPRISE SYSTEMS & SOFTWARE

24 Management · Top 25 der IT-Dienstleister

automotiveIT 08/09 · 2017

_Unter Vorbehalt. Die 25 größten IT-Dienstleister in der Autoindustrie überraschen mit guten Zahlen und noch besseren Prognosen. Doch die Zukunft der Branche ist ungewiss und die Stimmung könnte jederzeit umschlagen.

T-Systems

18

IBM

13

DXC Technology

10

Computacenter

9

Accenture

6

Other providers

44

In percent

Marktanteile der Top Five: Die fünf größten Anbieter können Boden gutmachen.

Qu

elle

: au

tom

oti

veIT

In percent

Umfrage: Welches Thema sollte bei den OEMs in den kommenden Jahren ganz oben auf der Agenda stehen?

Atos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgemini

All for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One Steeb

ESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikSulzerSulzerSulzerSulzerSulzerSulzer

AltranAltranAltranAltranAltranH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International Group

Poll: Which issue should be top of the agenda for automakers in coming years?

On the record:

“Carmakers that don’t want to miss out on a big trend today don’t get around artificial intelligence and big data. Especially with the complexity of autonomous driving, traditional algorithms are no longer sufficient as a solution.”Henrik Ljungstroem, executive vice president & head of automotive, Capgemini Deutschland

“While artificial intelligence will make autonomous driving possible in five or 10 years, the question that’s decisive for customers today is who offers the best connected mobility services”Ansgar Gruendler, sales director automotive, BT Germany

“Analysis of car data with the help of big data and AI platforms opens the door to data, the new gold of the 21st century.”Ruchir Budhwar, regional head manufacturing Europe, Infosys

“Especially the fusion of on-board and off-board technologies represents a central and differentiating work area for engineering service providers.”Berthold Puchta, executive vice president automotvie division, ESG

“Autonomous driving turns the auto industry’s traditional business model on its head. In the battle with new tech players, key is who will dominate tomorrow’s mobility ecosystem.”Axel Schmidt, managing director, automotive, Accenture

“The horizontal and vertical networking of people, machines and goods, even across different plants, makes it possible to make today’s heavily sequential production process more flexible. That will massively increase efficiency and flexibility.”Thomas Garn, sector director, Computacenter

“Increasing hacker attacks show that protection against cyber attacks while driving in a connected car has become one of the most important challenges for the automotive industry.”Dominik Neumann, vice president, CGI Germany.

Market shares of the top 5: The five largest suppliers make up ground.

companies now employing chief digital officers (CDOs), they are more likely to develop programs on their own in-house. A third problem is the public’s loss of confidence in the auto industry, following revelations of cheating on emissions tests, allegations of collusion between German carmakers and other news that has raised questions about the integrity of the indus-try. Insiders say such an environment is not conducive to the

introduction of services based on customer and vehicle data. Finally, industry sources say, the hard-fought “war for talent” is proving to be a real obstacle to the development of new con-cepts.

By Pascal Nagel

24 Management · Top 25 der IT-Dienstleister

automotiveIT 08/09 · 2017

_Unter Vorbehalt. Die 25 größten IT-Dienstleister in der Autoindustrie überraschen mit guten Zahlen und noch besseren Prognosen. Doch die Zukunft der Branche ist ungewiss und die Stimmung könnte jederzeit umschlagen.

T-Systems

18

IBM

13

DXC Technology

10

Computacenter

9

Accenture

6

Other providers

44

In percent

Marktanteile der Top Five: Die fünf größten Anbieter können Boden gutmachen.

Qu

elle

: au

tom

oti

veIT

In percent

Umfrage: Welches Thema sollte bei den OEMs in den kommenden Jahren ganz oben auf der Agenda stehen?

Atos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyAtos Information TechnologyCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgeminiCapgemini

All for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One SteebAll for One Steeb

ESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikESG Elektroniksystem und LogistikSulzerSulzerSulzerSulzerSulzerSulzer

AltranAltranAltranAltranAltranH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International GroupH&D International Group

Connected cars are beginning to pave the way for new mobili-ty ventures and automotive use cases are on the rise. Already, shared mobility or mobility on demand is gaining ground in markets traditionally dominated by classic automotive retail, private car ownership and the corporate leasing of vehicles. The auto industry is facing a paradigm shift, which is especial-ly clear in the views expressed by younger consumers. Accord-ing to a Ford Motor study, four out of 10 so-called millennials are, in principle, willing to share cars. And, if traffic congestion in ever-expanding urban centers is to be addressed effectively, new mobility concepts have to be developed. Carmakers and other transportation stakeholders are hard at work to develop car-sharing, ride-hailing and other new forms of mobility. And traditional dealerships will have to evolve from providers of sales and maintenance to moblity service providers.

In Europe, a recent example provided evidence that the retail sector is, indeed, on the move. In July, AMAG, a large Switzer-land-based dealer group, said it had acquired a majority stake in car sharing company Sharoo, in a transaction specifically designed to meet customers’ changing mobility needs. “Mobil-ity requirements are changing constantly and we want to meet these requirements in the future as well,” AMAG CEO Morten Hannesbo said in a statement. “ For AMAG, it means that, next to sales, financing, repairs and spare parts, car sharing will be-come another source of revenue. Said Hannesbo: “The prom-ising start-up expands our service portfolio perfectly.” AMAG already owns part of Catch a Car, a provider of free floating car services in Basel and Geneva.

Volvo Cars also is working with its dealers to offer new ser-vices. In 2015, the Swedish car brand offered dealers the op-tion to offer short- and long-term rentals. “The goal was to ex-pand Volvo’s often very rigid leasing offerings,” said Thomas

Bauch, managing director of Volvo Cars Germany. He said the program in particular offers as much flexibility as possible on the term of a lease. The program also offers dealers the option of starting a car-sharing scheme, which would be another step in the transformation to mobility service provider.

Opportunities

In many cities, established car-sharing companies such as BMW’s DriveNow and Daimler’s car2go dominate the mar-ket, but the situation is different outside major urban centers. “In rural areas, there are opportunities for car dealerships to become active on their own with new forms of mobility,” said Stefan Bratzel, who heads Germany’s Center of Automo-tive Management (CAM). A study by the Carl von Ossietzky University in Oldenburg in northern Germany confirmed that dealerships are well positioned for new mobility offerings out-side big cities. Car dealers already have rental and test vehi-cles available and they have knowledgeable staff and an infra-structure in place, the study said. Those factors provide a good starting point for the development of a car-sharing product. The university researchers warned, however, that regional car dealerships will have to be ready to move quickly, once they see demand for shared mobility grow in their area. If they don’t, bigger and already established providers could move in and they would lose a possible first-mover advantage.

By Werner Beutnagel

What about the dealer?Automakers are developing new forms of personal mobility that move away from traditional car

sales. If the trend picks up speed, car retailers will have to adapt their business models.

Source: Car Sharing Association, Statista

Nu

mb

er o

f u

sers

Car sharing becomes more popular: Number of registered users in Germany

2,000,000

1,500,000

1,000,000

500,000

02013

453,000

2014

757,000

2015

1,040,000

2016

1,260,000

2017

1,715,000

Shared mobility

DIGITAL RETAIL & SERVICE

19

D A I M L E R S P E C I A L

Winter 2017-2018

Daimler's R&D operations are changing, much like the premium car group itself. And

new business processes are in line with the transformation of the auto industry as a

whole. The company now has development centers all over the world and is imple-

menting new technologies across its process chain. automotiveIT discussed Daimler's

R&D strategy and the group's digitalization with R&D chief Ola Kaellenius and explored

some of the issues he confronts as the car group readies itself for a new era. More

stories on Daimler's engineering operations can be found at: www.automotiveIT.com.

Daimler’s globalization

Idea generatorWorldwide R&D and engineering centers make localization easier and provide new ideas.

Shifting boundariesDaimler IT is supporting the digital transformation of the company's global R&D operations.

Ola KaelleniusR&D boss says future cars will see systematic decoupling of software and hardware.

20

D A I M L E R S P E C I A L

Winter 2017-2018

Research and development begins and shapes the automotive process chain. Daimler AG has

strategically distributed its R&D facilities around the world – and benefits from an expanding trove

of experience.

Idea generator and trailblazer

T he figures speak for themselves: Daimler is now provid-ing more than 7.5 billion euros for research and develop-

ment, the largest sum in the company’s history. In late 2016, it had 24,200 people working in R&D. Engineers in Group Research & Mercedes-Benz Cars Development continue to constitute the largest share: More than 17,000 employees at 24 locations in 12 countries form the nucleus of a global R&D network. “The know-how, the creativity and the motivation of these employees are key factors in the success of our vehi-cles in the market,” said board member Ola Kaellenius. In an exclusive interview with automotiveIT, the head of Group Re-search and Mercedes-Benz Cars Development, said: “Over the

years, we have built up an international network and defined various competency themes. The locations were chosen very deliberately.” For example, Sunnyvale in the heart of Silicon Valley is one of the leading centers in North America, along with Long Beach (California), Portland (Oregon) and Redford (Michigan). In Asia, the key hotspots are Bangalore (India), the global hybrid center in Kawasaki (Japan), and the research and development center in Beijing.

The strategy makes sense: It puts the complany as close as pos-sible to the customer, even with research and development. Daimler needs international facilities so it can understand

Germany

Powertrain and testing, R&D department, design, future-oriented products, testing and technical center, mobility services

USA

Design and telematics, powertrain development, E-drive components,testing and emissions, autonomous driving, advanced vehicle design

China

Telematics and infotainment, powertrain and testing, design, localization, safety, comfort, authorizations and patents, trends and innovation

India

Design and telematics, IT, CAD simulation, E/E development

Daimler also has R&D centers in Canada, the UK, Italy, Sweden, Israel, South Korea and Japan.

A global R&D network

21

D A I M L E R S P E C I A L

Winter 2017-2018

what is happening in the world. For instance, if you are trav-eling on Indian roads, you don’t see what you see in Sindelfin-gen. It is not a matter of putting more development hubs on the map. In car manufacturing, the trick is building up a globally integrated network and managing it efficiently without losing the company’s identity. “We have replaced ‘Made in Germa-ny’ with ‘Made by Mercedes.’ It no longer makes a difference where our engineers work worldwide,” Kaellenius said. And the already respectable network is growing: In late 2016, a new technology center in Tel Aviv went into operation – the research projects in Israel especially revolve around digita-lization. Sajjad Khan, Daimler AG’s connectivity chief, went into the details: “Aside from developing and testing pilot proj-ects for new operating concepts, we are building a network of local partners, universities and high-tech companies.” Then, in Lisbon, the opening of the first-ever Mercedes-Benz Digital Delivery Hub followed in early May 2017. The goal of the agile unit in the Portuguese capital: Along with the inventive spirit of young talent, the brand’s strengths and experience are sup-posed to lead to new digital products and business models. So it can expand the Digital Delivery Hub, Mercedes Benz is look-ing for talent with backgrounds in software development, app programming, big data, cloud computing, Java, JavaScript, and Adobe Experience Manager.

Design drawings on your phone

„Digitalization is Daimler’s greatest asset since the invention of the automobile,” said CEO Dieter Zetsche. More and more, the digital transformation is changing the entire auto indus-try, he added. To shape the mobility of tomorrow and to link trends, future technologies and individual customer needs, the company must systematically digitize the value creation chain – starting with the engineering methods and IT tools that are used in the development area. In the core Smaragd system, for example, Mercedes engineers do not just manage the CAD design data for all the mechanical parts. They are in-creasingly storing data from electric and electronic systems, even information from functional and requirements specifi-cations. Employees along the entire automotive value chain, including those in manufacturing and after-sales, can access these central data hubs.

Changes in developers’ workplaces have gone hand-in-hand with the extra functions that state-of-the-art applications of-fer. “We work in a composite world: There are many full-time designers that use high-performance workstations with two screens. And we have occasional users, mobile workers who travel for test drives and work while they are on the road. They prefer to use lean end devices such as tablet computers,” said Siegmar Haasis, who is in charge of IT equipment in the Mer-cedes-Benz Cars R&D area. Today, design drawings can even be called up on smartphones, which may make sense when fast visualization is needed. In any case, the number of mobile users is growing significantly because the mechanical share of development work is on the decline, and the proportion of

electric/electronic systems and software is growing. The re-sult: The once purely CAD-dominated design chain is looking more and more like a software-based design chain. Daimler IT serves it with a multitude of partners that are highly net-worked with the automaker. The job at hand is no longer sim-ply the programming of control devices but rather a universal responsibility, reaching all the way to software deployment with updates over the air.

IT tools for the user

The operating departments and IT share the job of building up the enthusiasm of R&D employees for new digital tools, pro-gramming interfaces, and workplaces. It takes the best possi-ble user experience for the R&D engineers to work effectively. One of the new insights is that the enthusiasm for IT tools is not a question of age. It always comes down to the technical requirements that are embedded in the user role. Employees in charge of components, for example, don’t just work with-in a CAD program. They work in a multitude of core systems every day. It would be a great start if IT could offer them a smart interface cockpit for this, and it effectively bundled all the applications and clearly aggregated the data that they constantly need. Jan Brecht, Daimler’s CIO, is frank about IT’s prior focus. “In IT, we have been looking at the back side of the screen for too long and have been optimizing the functional-ity in individual systems. The time has come to take the user’s perspective.” Here information technology closes the circle between research, design, development, production and sales. In coming years, Daimler wants to play a role in shaping mo-bility with pioneering innovations and to advance digitaliza-tion across the company. Especially in future strategic fields, including networking (Connected), autonomous driving (Au-tonomous), flexible use and services (Shared & Services) and electric powertrains (Electric), it is imperative to know the needs of the customer as precisely as possible throughout the world and respond to them flexibly.

By Ralf Bretting

Photos: Daimler

Heavy R&D focus on cars

Research and development expenditures for Daimler business areas in 2016 (in billions of euros)

Daimler Group 7.57

Mercedes-Benz Cars 5.67

Daimler Trucks 1.26

Mercedes-Benz Vans 0.44

Daimler Buses 0.20

22

D A I M L E R S P E C I A L

Winter 2017-2018

Shifting boundaries

International locations, short development cycles, greater virtualization – Daimler IT is supporting the

digital transformation of R&D with process know-how and technical expertise.

T he times are long past when Daimler vehicles were exclusively designed in the Mercedes-Benz Technology

Center in Sindelfingen, Germany, and the powertrains were produced in the Neckar Valley. Today more than 17,000 engineers work in a global development network, at locations spread throughout the world. This is made possible by standardized processes, sophisticated methods and above all state-of-the-art IT tools. They connect developers in California, India and China with Germany like a nervous system. “More than 50 centrally operated core systems such as Smaragd and Dialog provide a uniform database at any time. It doesn’t matter where a Mercedes designer works in the world – he benefits from direct remote access to individual

applications, nearly without the loss of performance,” said Siegmar Haasis, CIO, Research & Development Mercedes-Benz Cars. The menus in the programs are multilingual, and the concept for authorizations and roles is clearly defined across all disciplines. “That last part is especially important because we cooperate with third-party companies in joint ventures and want to integrate our development partners closely into the processes,” Haasis said. “Each user only gets to see the data that are relevant for his activity and form of cooperation.”

New technologies such as virtual and augmented reality are explicitly included. When engineers in the United States, Germany and China collectively ponder a component, vivid

23

D A I M L E R S P E C I A L

Winter 2017-2018

visualization makes it easier to understand the specific tasks and coordinate the local work packages with one another. Since CAD applications always also store the internationally standardized graphic format JT, all the engineering data can flow back and forth without difficulty. Meanwhile, even VR/AR representations can be generated with JT. The information reaches the displays of mixed reality glasses directly, via inte-grated converters. A tedious translation process is eliminated. This helps to speed up development cycles and systematically bypass hardware in the product development process. The dig-ital boundary keeps moving toward the launch of series pro-duction. The most important transformation project currently in R&D is PDM 2020. It revolves around the so-called “digital

twin.” The goal is to produce a digital picture of all vehicles over their entire lifecycle. Core systems are not being repro-grammed from the ground up for this; they are being strength-ened with micro services. “With the digital twin approach, we will address the backend system on a targeted basis and feed mobile apps with data relevant to development and produc-tion, using a multiway connector with defined interfaces,” Haasis said. In the future, thanks to in-depth integration with-in a three-layer-model framework, process control data will be available in role-based cockpits, whatever upstream system they are coming from. Engineering IT is working on the digital twin at full speed. It wants to deliver up to 15 usable building blocks each year between now and 2020 that can collectively form the complete solution in specific products.

CIO: AI is next springboard