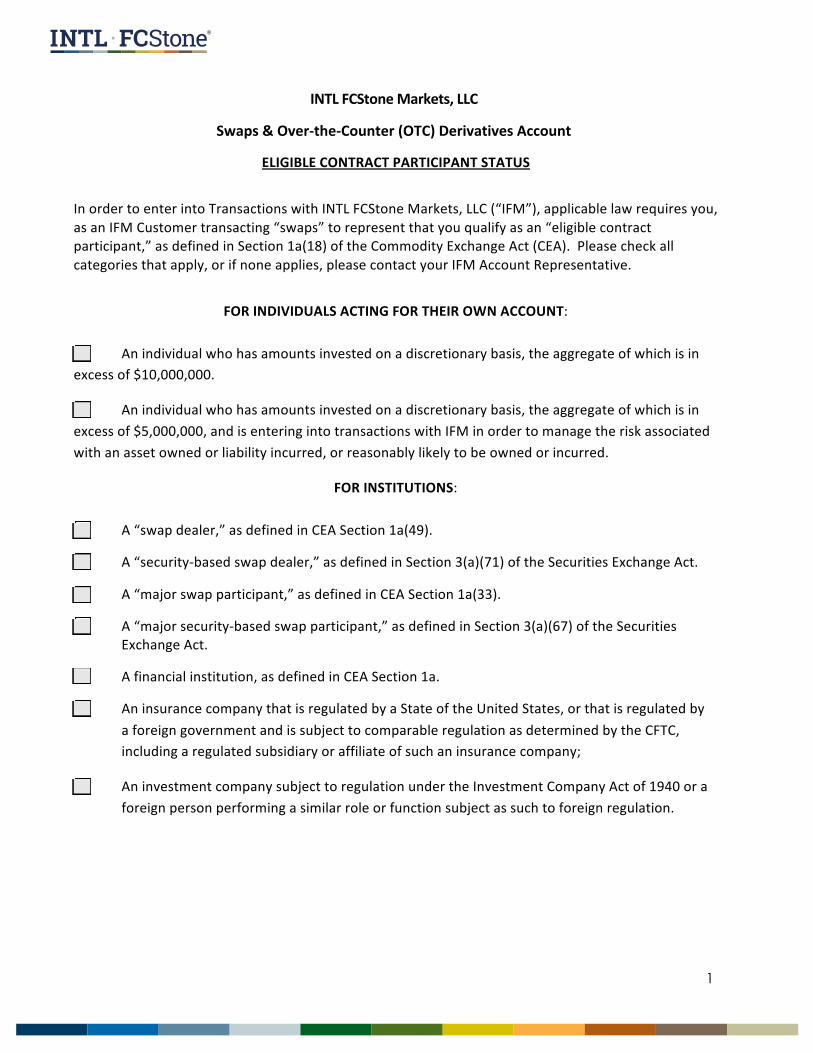

In order to enter into Transactions with INTL FCStone Markets, LLC (“IFM”), applicable law requires you,

as an IFM Customer transacting “swaps” to represent that you qualify as an “eligible contract

participant,” as defined in Section 1a(18) of the Commodity Exchange Act (CEA). Please check all

categories that apply, or if none applies, please contact your IFM Account Representative.

FOR INDIVIDUALS ACTING FOR THEIR OWN ACCOUNT:

An individual who has amounts invested on a discretionary basis, the aggregate of which is in

excess of $10,000,000.

An individual who has amounts invested on a discretionary basis, the aggregate of which is in

excess of $5,000,000, and is entering into transactions with IFM in order to manage the risk associated

with an asset owned or liability incurred, or reasonably likely to be owned or incurred.

FOR INSTITUTIONS:

A “swap dealer,” as defined in CEA Section 1a(49).

A “security‐based swap dealer,” as defined in Section 3(a)(71) of the Securities Exchange Act.

A “major swap participant,” as defined in CEA Section 1a(33).

A “major security‐based swap participant,” as defined in Section 3(a)(67) of the Securities

Exchange Act.

A financial institution, as defined in CEA Section 1a.

An insurance company that is regulated by a State of the United States, or that is regulated by

a foreign government and is subject to comparable regulation as determined by the CFTC,

including a regulated subsidiary or affiliate of such an insurance company;

An investment company subject to regulation under the Investment Company Act of 1940 or a

foreign person performing a similar role or function subject as such to foreign regulation.

2

A commodity pool that—

(i) has total assets exceeding $5,000,000; and

(ii) is formed and operated by a person subject to regulation under the CEA or a foreign person

performing a similar role or function subject as such to foreign regulation.

If you are a commodity pool or similar foreign person that will be entering into

transactions in foreign exchange (including foreign exchange derivative transactions), check

this box to confirm that each investor in the commodity pool or the foreign person is itself an

eligible contract participant as defined in CEA Section 1a.

A corporation, partnership, proprietorship, organization, trust, or other entity that has total

assets exceeding $10,000,000.

A corporation, partnership, proprietorship, organization, trust or other entity whose

obligations under transactions with IFM are guaranteed or otherwise supported by a letter of credit or

keepwell, support, or other agreement by an entity that meets the qualifications described in CEA

Section 1a(18)(a)(v) (please provide a copy of such letter of credit or other support document).

A corporation, partnership, proprietorship, organization, trust, or other entity that has a net

worth exceeding $1,000,000 and is entering into transactions with IFM in connection with the conduct

of its business or to manage the risk associated with an asset or liability owned or incurred or

reasonably likely to be owned or incurred in the conduct of your business.

An employee benefit plan subject to the Employee Retirement Income Security Act of 1974, a

governmental employee benefit plan, or a foreign person performing a similar role or function subject

as such to foreign regulation, and either:

has total assets exceeding $5,000,000; or

the investment decisions of which are made by‐

an investment adviser or commodity trading advisor subject to regulation

under the Investment Advisers Act of 1940 or the CEA;

a foreign person performing a similar role or function subject as such to foreign

regulation;

a financial institution as defined in CEA Section 1a; or

an insurance company described in CEA Section 18(A)(ii) or a regulated

subsidiary or affiliate of such an insurance company.

3

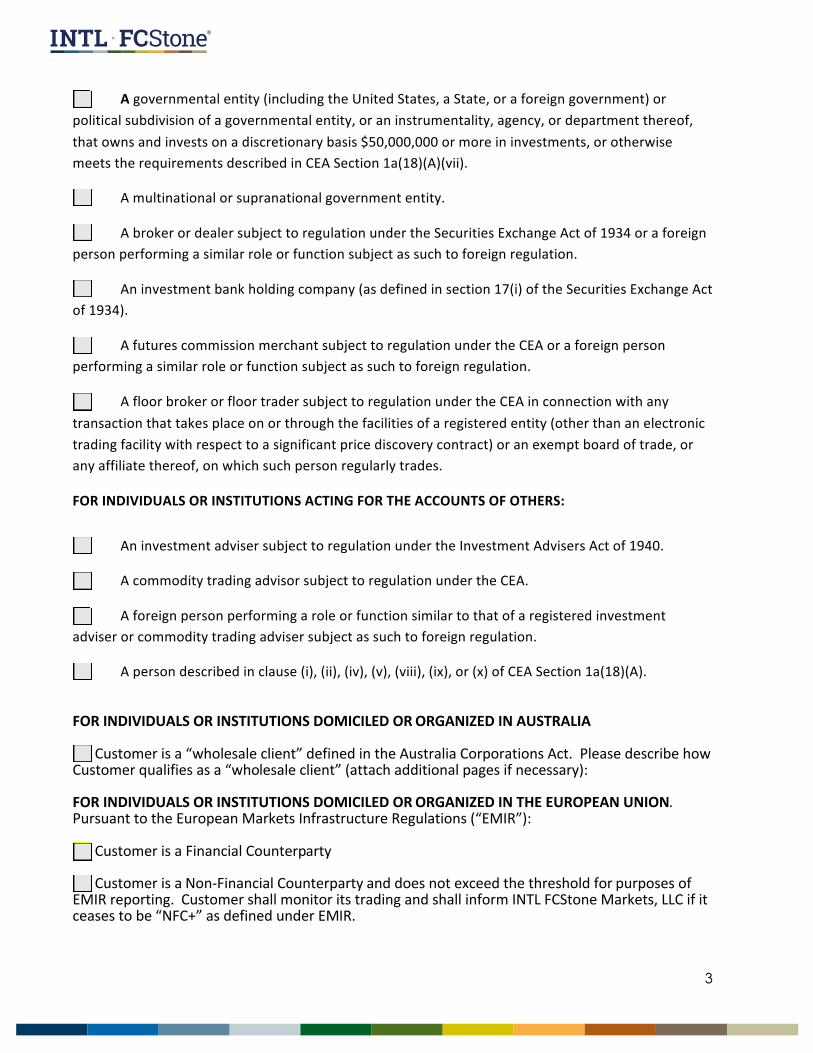

A governmental entity (including the United States, a State, or a foreign government) or

political subdivision of a governmental entity, or an instrumentality, agency, or department thereof,

that owns and invests on a discretionary basis $50,000,000 or more in investments, or otherwise

meets the requirements described in CEA Section 1a(18)(A)(vii).

A multinational or supranational government entity.

A broker or dealer subject to regulation under the Securities Exchange Act of 1934 or a foreign

person performing a similar role or function subject as such to foreign regulation.

An investment bank holding company (as defined in section 17(i) of the Securities Exchange Act

of 1934).

A futures commission merchant subject to regulation under the CEA or a foreign person

performing a similar role or function subject as such to foreign regulation.

A floor broker or floor trader subject to regulation under the CEA in connection with any

transaction that takes place on or through the facilities of a registered entity (other than an electronic

trading facility with respect to a significant price discovery contract) or an exempt board of trade, or

any affiliate thereof, on which such person regularly trades.

FOR INDIVIDUALS OR INSTITUTIONS ACTING FOR THE ACCOUNTS OF OTHERS:

An investment adviser subject to regulation under the Investment Advisers Act of 1940.

A commodity trading advisor subject to regulation under the CEA.

A foreign person performing a role or function similar to that of a registered investment

adviser or commodity trading adviser subject as such to foreign regulation.

A person described in clause (i), (ii), (iv), (v), (viii), (ix), or (x) of CEA Section 1a(18)(A).

FOR INDIVIDUALS OR INSTITUTIONS DOMICILED OR ORGANIZED IN AUSTRALIA

Customer is a “wholesale client” defined in the Australia Corporations Act. Please describe how Customer qualifies as a “wholesale client” (attach additional pages if necessary): FOR INDIVIDUALS OR INSTITUTIONS DOMICILED OR ORGANIZED IN THE EUROPEAN UNION. Pursuant to the European Markets Infrastructure Regulations (“EMIR”):

Customer is a Financial Counterparty

Customer is a Non‐Financial Counterparty and does not exceed the threshold for purposes of EMIR reporting. Customer shall monitor its trading and shall inform INTL FCStone Markets, LLC if it ceases to be “NFC+” as defined under EMIR.

4

Customer is a Non‐Financial Counterparty and does exceed the threshold for purposes of EMIR reporting, has informed the relevant competent authority of such status, shall monitor its trading and shall inform INTL FCStone Markets, LLC if it ceases to be “NFC+” as defined under EMIR. Signature: ________________________________ Name (Print):______________________________ Signatory Title (if an entity) or Agent Name (if documents are being executed by an Agent on Applicant’s behalf): ________________________________________

Date: _____________________________ month day year

5

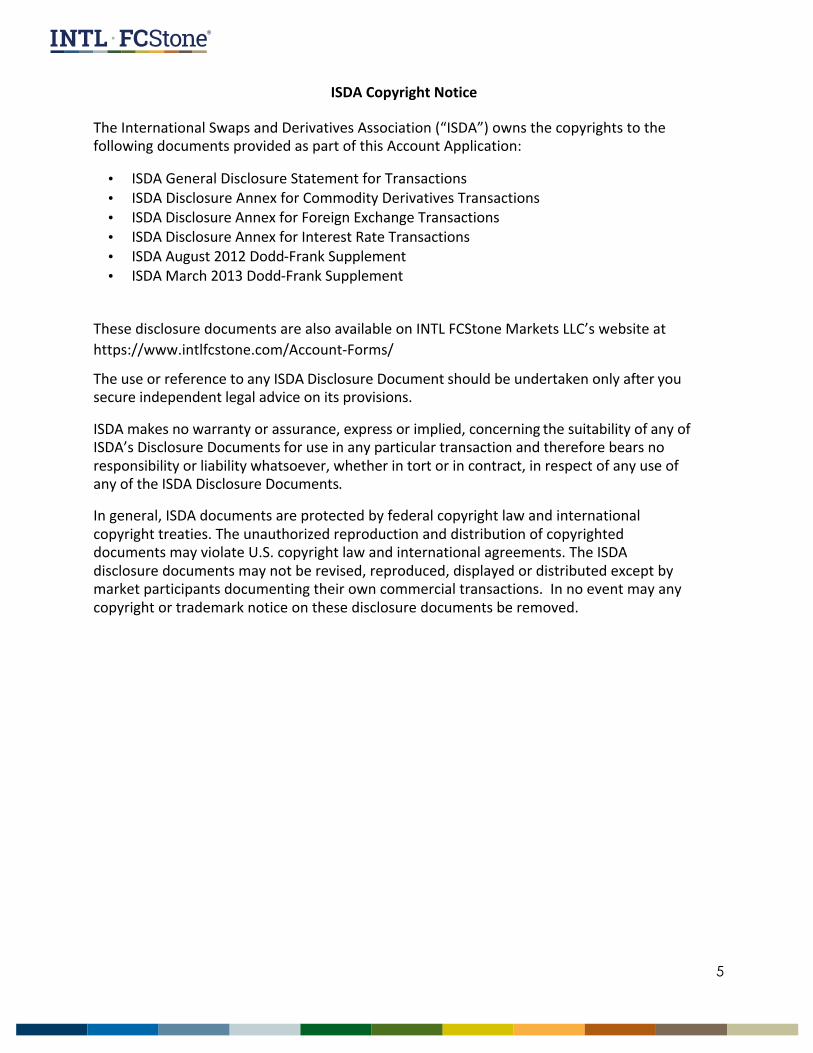

ISDA Copyright Notice

The International Swaps and Derivatives Association (“ISDA”) owns the copyrights to the following documents provided as part of this Account Application:

• ISDA General Disclosure Statement for Transactions

• ISDA Disclosure Annex for Commodity Derivatives Transactions

• ISDA Disclosure Annex for Foreign Exchange Transactions

• ISDA Disclosure Annex for Interest Rate Transactions

• ISDA August 2012 Dodd‐Frank Supplement

• ISDA March 2013 Dodd‐Frank Supplement

These disclosure documents are also available on INTL FCStone Markets LLC’s website at

https://www.intlfcstone.com/Account‐Forms/

The use or reference to any ISDA Disclosure Document should be undertaken only after you secure independent legal advice on its provisions.

ISDA makes no warranty or assurance, express or implied, concerning the suitability of any of ISDA’s Disclosure Documents for use in any particular transaction and therefore bears no responsibility or liability whatsoever, whether in tort or in contract, in respect of any use of any of the ISDA Disclosure Documents.

In general, ISDA documents are protected by federal copyright law and international copyright treaties. The unauthorized reproduction and distribution of copyrighted documents may violate U.S. copyright law and international agreements. The ISDA disclosure documents may not be revised, reproduced, displayed or distributed except by market participants documenting their own commercial transactions. In no event may any copyright or trademark notice on these disclosure documents be removed.

International Swaps and Derivatives Association, Inc.

GENERAL DISCLOSURE STATEMENT FOR TRANSACTIONS

All Applicants: Please click on the following link on INTL FCStone Markets, LLC website to access the complete ISDA General Disclosure Statement for Transactions (“General Disclosure

[__] Please check here to acknowledge that you have read and understand the General Disclosure Statement.

The General Disclosure Statement describes (1) the material characteristics of a wide variety of Transactions; (2) the material risks of such Transactions, including risks related to liquidity and counterparty credit risk; and (3) typical material incentives and conflicts of interest that we may have with respect to such Transactions.

The General Disclosure Statement also provides information regarding certain rights you may have, as follows:

• Scenario Analysis: Prior to entering into a Transaction in any swap that is not available fortrading on a designated contract market or swap execution facility, you may request, andconsult on the design of, a scenario analysis to allow you to assess your potential exposurein connection with such swap. The General Disclosure Statement provides moreinformation on the procedures for preparation of a scenario analysis. Such a scenarioanalysis is not a prediction of actual Transaction results, and there can be no assurancethat the range of assumptions employed will encompass all possible market conditions.

• Select DCO or Clearing Agency: With respect to any swap subject to the mandatoryclearing requirements under Section 2(h) of the Commodity Exchange Act, subject to theterms of any agreement between us and to applicable laws, you have the sole right toselect the derivatives clearing organization (DCO) or clearing agency at which the swapwill be cleared. With respect to any swap that is not subject to these mandatory clearingrequirements but is eligible for clearing, subject to the terms of any agreement betweenus and to applicable laws, you may in your sole discretion elect to clear such swap, and, ifyou so elect, select the DCO or clearing agency at which the swap will be cleared.

• Daily Mark: For uncleared swaps and uncleared security‐based swaps, we will provide youwith a “daily mark” as of the close of business or at such other time that we agree with youin writing. The General Disclosure Statement provides a description of these daily marks.Note that a daily mark does not reflect the actual market price at which an offer would bemade to purchase, sell, enter into, exercise, novate, unwind, terminate or settle aTransaction. Rather, it will represent a mathematical approximation of market values as ofa given date derived from proprietary models and methodologies based on certainassumptions regarding past, present and future market conditions or other factors, orfrom other sources of pricing information (e.g., third party quotes, prices on tradingvenues, or clearinghouse marks for comparable or interpolated Transactions).

• Option to Segregate Margin: For uncleared Transactions, subject to the terms of anyagreement between us and to applicable laws, you have the right to require segregationof the funds or other property that you provide to us to margin, guarantee, or secure yourobligations, other than with respect to variation margin and provided that the property isof a type that may be held by a third party custodian. Segregated funds will bemaintained in an account with an independent third‐party custodian. You will be requiredto reimburse us for the costs of such custodial arrangements.

• ERISA and Non‐ERISA Special Entity Status: If you are an employee benefit plan defined inSection 3 of the Employee Retirement Income Security Act of 1974 (29 U.S.C. 1002)(“ERISA”) that is not subject to Title I of ERISA or otherwise defined as a “Special Entity”pursuant to CFTC Rule 23.401(c)(1), (2), (4) or (5), you may elect to be treated as a SpecialEntity pursuant to CFTC Rule 23.401(c)(6).

Please note that Transactions may give rise to significant risks and are intended primarily for

knowledgeable and sophisticated parties that are willing to accept such risks and able to absorb the losses that may arise. Therefore, it is important that you as the Customer or the

person exercising discretion on the Customer’s behalf understand these risks before entering

into any Transactions, regardless of the Customer’s level of prior experience in financial transactions or instruments.

There can be no assurance that a Transaction will provide a Customer with the desired return or achieve the desired hedging objectives.

In addition to the General Disclosure Statement, please check one or more of the following specific product disclosures that apply to you.

8

International Swaps and Derivatives Association, Inc.

DISCLOSURE ANNEX FOR COMMODITY DERIVATIVE TRANSACTIONS

Please click on the following link on our website to access the complete ISDA Disclosure Annex for Commodity Derivative Transactions (“Commodity Derivative Disclosure Annex”):

https://www.intlfcstone.com/Account‐Forms/

[__] Please check here to acknowledge that you have read and understand the Commodity

Derivative Disclosure Annex.

The Commodity Derivative Disclosure Annex supplements and should be read in conjunction with the General Disclosure Statement. Nothing in the Commodity Derivative Disclosure Annex amends or supersedes the express terms of any transaction between you and us or any related governing documentation. Accordingly, descriptions in the Commodity Derivative Disclosure Annex of the operation of Commodity Transactions and the consequences of various events are in all cases subject to the actual terms of a Commodity Transaction executed between you and us and its governing documentation (whether or not such qualification is expressly stated).

The Commodity Derivative Disclosure Annex provides further description of Transactions in which the underliers are physical commodities, contracts for the future delivery of physical commodities, physical events (such as weather, transportation or emissions), rights or indexes relating to physical commodities, contracts for the future delivery of physical commodities or physical events, indices of commodities, or indices of commodity indexes (“Commodity Transactions”).

The Commodity Derivative Disclosure Annex also describes the material risks of such Transactions, including risks related to physical markets, price sources and valuation, and physical settlement, as well as special risks related to specific types of Commodity Transactions.

The terms of a Commodity Transaction may incorporate standard definitions, annexes thereto and other market standard terms, including terms, customs and usages from the physical markets for underliers. Such terms may in turn be amended or customized pursuant to the terms of the Commodity Transaction and its governing documentation. Before entering into a Commodity Transaction, you should obtain and review carefully any such materials incorporated by reference as their content could materially affect your rights and obligations under the Commodity Transaction, its value and its appropriateness for your particular objectives.

International Swaps and Derivatives Association, Inc.

DISCLOSURE ANNEX FOR FOREIGN EXCHANGE TRANSACTIONS

Please click on the following link on our website to access the complete ISDA Disclosure Annex for Foreign Exchange Transactions (“FX Derivative Disclosures Annex”):

https://www.intlfcstone.com/Account‐Forms/

[__] Please check here to acknowledge that you have read and understand the FX Derivative

Disclosure Annex.

The FX Derivative Disclosure Annex supplements and should be read in conjunction with the General Disclosure Statement. Nothing in the FX Derivative Disclosure Annex amends or supersedes the express terms of any transaction between you and us or any related governing documentation. Accordingly, descriptions in the FX Derivative Disclosure Annex of the operation of Foreign Exchange Transactions and the consequences of various events are in all cases subject to the actual terms of a Foreign Exchange Transaction executed between you and us and its governing documentation (whether or not such qualification is expressly stated).

The FX Derivative Disclosure Annex provides further description of Transactions in which the

underliers are foreign currencies. The FX Derivative Disclosure Annex also describes the material

risks of such Transactions, including settlement risks and risks related to market disruptions, as

well as special risks related to specific types of FX Transactions.

International Swaps and Derivatives Association, Inc.

DISCLOSURE ANNEX FOR INTEREST RATE TRANSACTIONS

Please click on the following link on our website to access the complete ISDA Disclosure Annex

for Interest Rate Transactions (“Interest Rate Transactions Disclosures Annex”):

https://www.intlfcstone.com/Account‐Forms/

[__] Please check here to acknowledge that you have read and understand the Interest Rate

Transactions Disclosure Annex.

The Interest Rate Transactions Disclosure Annex supplements and should be read in conjunction with the General Disclosure Statement. Nothing in the Interest Rate Transactions Disclosure Annex amends or supersedes the express terms of any transaction between you and us or any related governing documentation. Accordingly, descriptions in the Interest Rate Transactions Disclosure Annex of the operation of Rates Transactions and the consequences of various events are in all cases subject to the actual terms of a Rates Transaction executed between you and us and its governing documentation (whether or not such qualification is expressly stated).

manager, investment adviser, commodity trading advisor, municipal advisor, market maker,

trader, prime broker or clearing broker. In those and other capacities, IFM, its directors, officers,

employees and affiliates may take or hold positions in, or advise other customers and

counterparties concerning, or publish research or express a view with respect to, Transactions or

related financial instruments that may be the subject of advice from us to you. Any such positions

and other advice may not be consistent with, or may be contrary to, your interests or to positions

which are the subject of advice previously provided by IFM or its affiliate to you, and unless

otherwise disclosed in writing or required pursuant to regulation, we are not necessarily acting in

your best interest and are not assessing the suitability for you of any Transactions or related

financial instruments. Acting in one or more of the capacities noted above may give IFM or its

affiliate access to information relating to markets, investments and products. As a result, IFM or its

affiliate may be in possession of information which, if known to you, might cause you to seek to

dispose of, retain or increase your position in one or more Transactions or other financial

instruments. IFM and its affiliate will be under no duty to make any such information available to

you, except to the extent we have agreed in writing or as may be required under applicable law.

NOTICE OF CERTAIN RIGHTS WITH RESPECT TO CLEARING SWAPS

With respect to any swap that is subject to the mandatory clearing requirements under Section 2(h) of the Commodity Exchange Act, subject to the terms of any agreement between us and to applicable laws, you have the sole right to select the derivatives clearing organization or clearing agency at which the swap will be cleared. With respect to any swap that is not subject to these mandatory clearing requirements but is eligible for clearing, subject to the terms of any agreement between us and to applicable laws, you may in your sole discretion elect to clear such swap, and, if you so elect, select the derivatives clearing organization or clearing agency at which the swap will be cleared. IFM’s conflict of interest rules prohibit sales personnel from negotiating or agreeing to prices for the provision of clearing services.

12

NOTICE OF MARK‐UP AND COMMISSION STRUCTURE

IFM will provide you with a “daily mark” for uncleared swaps each day as of the close of business or at

such other time as we agree in writing. Daily marks will not reflect the actual market price at which an

offer would be made to enter into a Transaction with you, or to novate, unwind, terminate or settle a

Transaction. In addition, our margin calls may be based on factors other than the daily mark or the

valuation of the swap on our books. IFM uses a third party vendor to prepare its daily marks, based on

valuation techniques used by our third‐party vendor described below and reserve the right to replace our

third‐party vendor at any time. We also reserve the right to alter, replace or vary valuation techniques,

methodologies and assumptions from time to time, and if materials, we will disclose such changes. IFM

relies on its third‐party vendor to supply both valuation models and the vast majority of market data used

as pricing inputs. In rare cases, pricing data is sourced from a broker or other vendor more closely

associated with trading a specialty product, and manually entered into the firm’s third party vendor

system. The pricing algorithms used by our vendor are based upon industry‐standard models to price

derivatives, such as:

• European options: Black‐Scholes

• American options: Modified Black‐Scholes (similar to Whaley)

• Asian options: Moment‐matching method (similar to Turnbull & Wakeman)

• FX options: Vanna‐Volga model with an adjustment for foreign‐domestic interest rates

• Barrier options: Leverages Heynan & Kat (1994), with proprietary extensions for differing

window permutations; automatically falls back to Black‐Scholes if option is knocked‐in

• Digital options: Modified Black‐Scholes, similar to Reiner‐Rubinstein (1991)

As the volatility of an asset is a required input to option models and is not directly observable, certain

estimates must be made regarding the volatility parameter, based on observable prices, historical volatility,

and others factors. The vendor’s volatility grid is produced using the following methodology:

• Option settlement prices are collected from various exchanges and vendors

• Using standard Black‐Scholes (for European options) or Whaley (for American options), implied

volatility and deltas are backed out from out‐of‐the‐money call and put prices

• The deltas and volatilities of the traded options are used to interpolate/extrapolate a standardized

delta‐based volatility grid

If the option is a term option (i.e., expires on the standard exchange expiry day), then the volatility grid is

used without modifications. If the option is an over‐the‐counter (OTC) option that expires early, then the

vendor’s Early Expiry Vol (EEV) model will be used to determine the volatility. The EEV model is a 2‐factor

model based on Gabillon (1992). The two factors are the short vol, (volatility of the nearby, or spot,

contract) and long vol (extrapolated from the volatility of the most far‐dated contract), as well as the

correlation between the long and short vols. Using those parameters, one can calculate an early expiry

volatility. The daily marks provided will not include the compensation we receive in connection with your

transactions, and thus will vary from the actual price you receive and the value at which we carry the

transaction on our books. The daily mark is intended to be the theoretical fair value of the transaction, not

the price we have offered to deal (which includes our compensation). The prices at which we offer to deal

are our own prices, and may be more or less than what you would receive from another dealer. In this

regard, we do not purport to offer best execution on your behalf. The amount of commission to be charged

in connection with a given trade will be agreed to in writing in advance.

13

NOTICE OF PROCEDURE FOR CLIENT COMPLAINTS

In the event that you wish to bring a complaint to our attention that you were unable to resolve directly with your Account Representative, you may direct your complaint to the INTL FCStone Markets, LLC (“IFM”) Compliance Department at the following address: INTL FCStone Markets, LLC c/o Chief Compliance Officer, 230 S LaSalle St, Chicago, IL 60604. Alternatively, complaints may be emailed to: [email protected] or may be made by telephone at (312) 789‐2517 or (312) 780‐6700. Please note that if you decide to register your complaint viatelephone, you must follow up with IFM via email or in writing within 10 business days. Anycomplaint must include your name, address and IFM account number. In addition, the complaintmust contain the name of the IFM employee(s) that the complaint relates to and a detaileddescription of the nature of the complaint.

ELECTION TO RECEIVE PRE‐TRADE INFORMATION IN WRITING

Pursuant to CFTC regulations, prior to entering into any swap, foreign exchange forward or foreign

exchange swap with you, IFM is required to provide you with a pre‐trade “mid‐market mark” (a

theoretical fair value of the transaction, which may or may not be the same as the price we have

offered to you and which will not include our commission), and a description of the material

economic terms of the transaction. If you agree, IFM may provide these disclosures orally to you.

Otherwise, IFM will provide these disclosures in writing (including via email). You can change your

election at any time by contacting your account representative.

Please indicate below whether you choose to receive pre‐trade mid‐market marks and transaction

descriptions orally or in writing, and sign below to confirm this election:

[__] Customer elects to receive pre‐trade mid‐market marks and descriptions of the

material economic terms of transactions orally.

OR

[__] Customer elects to receive pre‐trade mid‐market marks and descriptions of the

material economic terms of transactions in writing.

Customer Name (Print):______________________________ Date: ______________

Signatory Title (if Customer is an entity) or Agent Name (if documents are being executed by an Agent on

behalf of Customer): ________________________________________

month day year

15

ACKNOWLEDGEMENT OF SWAPS DISCLOSURES

Please sign below to acknowledge that you have received, read and understand the following

disclosure documents:

• ISDA Copyright Notice

• ISDA General Disclosure Statement for Transactions

• ISDA August 2012 Dodd‐Frank Supplement

• ISDA March 2013 Dodd‐Frank Supplement

• INTL FCStone Markets, LLC Disclosure of Material Conflicts of Interest

• INTL FCStone Markets, LLC Notice of Certain Rights with Respect to Clearing of Swaps

• INTL FCStone Markets, LLC Notice of Mark‐Up and Commission Structure

• INTL FCStone Markets, LLC Notice of Procedures for Reporting Client Complaints

• INTL FCStone Markets, LLC Notice of Right to Segregate Initial Margin

Please check the box to indicate which swaps you elect to transact and acknowledge that you have

received, read and understand the following disclosure document(s):

• ISDA Disclosure Annex for Commodity Derivative Transactions [___]

• ISDA Disclosure Annex for Foreign Exchange Transactions [___]

• ISDA Disclosure Annex for Interest Rate Transactions [___]

Customer Signature: ________________________________ Customer Name (Print):______________________________ Signatory Title (if Customer is an entity) or Agent Name (if documents are being executed by an Agent on behalf of Customer): ________________________________________ Date: _____________________________

month day year

16

INTL FCSTONE MARKETS, LLC

TERMS OF BUSINESS

This Terms of Business agreement for swaps and

over‐the‐counter (OTC) derivatives (the

“Agreement”) is dated ______between INTL

FCStone Markets, LLC, an Iowa limited liability

company (“IFM”) and

___________________________ an eligible contract

participant (“ECP”) within the meaning of Section

1a(18) of the Commodity Exchange Act, as amended

organized under the laws of

_________________________________

(“Counterparty”), each referred to individually as a

“Party” or collectively as the “Parties” and

supersedes all prior agreements between the Parties

with respect to its subject matter and constitutes,

along with the documents referred to in this

Agreement and the Account Application, a complete

and exclusive statement of the terms of the

Agreement between the Parties with respect to its

subject matter.

ARTICLE 1 Scope of Agreement, Definitions

and Contracting Procedure

1.1 Scope. This Agreement governs

each transaction defined by the CEA as a “swap,”

including any “foreign exchange swap” and “foreign

exchange forward” as defined in the CEA (each a

“Transaction”) that the Parties may enter into from

time to time after the date of this Agreement.

1.2 Definitions. Capitalized terms used

in this Agreement are defined in Exhibit A hereto, or,

if not defined in Exhibit A hereto, have the meanings

given in the 2006 ISDA Definitions published by ISDA

and, as applicable, the 2005 ISDA Commodity

Definitions published by ISDA, the 1998 FX and

Currency Option Definitions published by ISDA, the

Emerging Markets Traders Association and The

Foreign Exchange Committee, and any other

definitions specified in the relevant Confirmation for

such Transaction, as published by or in conjunction

with ISDA (collectively, the “Definitions”), except

that any references to “Swap Transactions” in the

Definitions will be deemed to be references to

“Transactions.” The Definitions are incorporated by

reference in, and made part of, this Agreement and

each relevant Confirmation as if set forth in full in

this Agreement and such Confirmation.

1.3 Single Agreement. The Parties may

agree from time to time to enter into one or more

Transactions, each of which shall be governed by this

Agreement and the Confirmation with respect to

such Transaction. In the event of any inconsistency

between the terms of a specific Transaction (as set

forth in the Confirmation for such Transaction) and

any provision of this Agreement, the terms of such

Confirmation shall control. This Agreement

(including all exhibits and annexes hereto), all

Confirmations, the Account Application, and all

documents incorporated by reference therein form a

single agreement between the Parties. Counterparty

acknowledges and agrees that it is bound by the

elections made by Counterparty in the Account

Application.

1.4 Limited Undertaking. Neither

Party commits, by entering into this Agreement, to

enter into any individual Transaction with the other

Party.

1.5 Confirmations. The Parties intend

that they are legally bound by the terms of each

Transaction from the moment they agree to those

terms (whether orally or otherwise). On or promptly

following the date on which the Parties reach

agreement on the terms of a Transaction, IFM will

send a Confirmation to Counterparty via email

outlining the commercial terms of such Transaction.

Counterparty will immediately review the terms of

each Transaction Confirmation to determine if it

accurately reflects Counterparty’s understanding of

the terms of the Transaction, and if Counterparty

believes the terms reflected in the Confirmation

accurately reflect the Transaction, Counterparty

shall confirm the same to IFM via email. If

Counterparty believes there is any discrepancy

between its understanding of the Transaction and

the terms reflected in the Confirmation,

Counterparty shall contact IFM via email (as set forth

below) within two Business Days of receiving the

Confirmation. If Counterparty has not accepted or

disputed a Confirmation in the manner set forth

above within two Business Days of receipt thereof,

Counterparty will be deemed to have accepted all

terms of such Confirmation absent manifest error.

17

ARTICLE 2 Payments, Margin and Netting.

2.1 Payments. Each Party will make

each payment or delivery specified in each

Confirmation to be made by it, subject to the other

provisions of this Agreement. Payments shall be

made on the due date, in the currency and to the

account, each as specified in the Account Application

or if not set forth in the Account Application, the

relevant Confirmation. Where settlement is by

delivery rather than by payment, delivery will be

made for receipt on the due date in the manner

customary for the relevant obligation unless

otherwise specified in the relevant Confirmation.

2.2 Early Termination. The Parties

may liquidate or terminate a Transaction prior to

maturity by written consent of both Parties, subject

to a payment based upon revised Transaction terms

adjusted to reflect prevailing rates over the

remaining term of the Transaction. Any such

payment shall be calculated by IFM.

2.3 Initial Margin. As security to

maintain the Counterparty’s position for each

Transaction, IFM may request Counterparty to pay

IFM an amount of cash calculated by IFM in its sole

discretion as “Initial Margin.” Payment of Initial

Margin for a Transaction shall be made on the day

such Transaction is initiated, as specified in the

relevant Confirmation. IFM may reject or delay any

Transaction prior to the payment of Initial Margin.

2.4 Variation Margin. As further

security to maintain the Counterparty’s position for

each Transaction, Counterparty shall pay to IFM daily

variation margin in the amount calculated by IFM in

its sole discretion (“Variation Margin”). If IFM

provides notice by 11:00 am New York time on any

Business Day to Counterparty that a payment of

Variation Margin is required, Counterparty shall pay

such Variation Margin by 5:00 pm New York time on

the same Business Day. If IFM provides any such

notice after 11:00 am New York time on a Business

Day, Counterparty shall pay the Variation Margin

specified in such notice by 12:00 pm New York Time

on the next Business Day. Upon Counterparty’s

request, IFM may return excess amounts of Variation

Margin (as determined by IFM in its sole discretion),

provided, that in no event shall the total amount of

Initial Margin and Variation Margin deposited by

Counterparty with respect to any Transaction be less

than the Initial Margin with respect to such

Transaction.

2.5 Use of Margin. Counterparty

hereby pledges to IFM, as security for its obligations

hereunder and under all Transactions, and grants to

IFM a first priority continuing security interest in,

lien on and right of set‐off against all Margin

transferred to or received by IFM hereunder. Upon

the transfer by IFM to Counterparty of any Margin,

the security interest and lien granted hereunder on

that Margin will be released immediately, without

any further action by either party. IFM shall be

entitled to hold Variation Margin and, subject to any

elections made by Counterparty in the Account

Application, Initial Margin, itself or to appoint an

agent (a “Custodian”) to hold Margin on its behalf.

Upon Counterparty’s election or notice by IFM to

Counterparty of the appointment of a Custodian, or

Counterparty’s election to appoint a Custodian,

Counterparty’s obligations to make any transfer of

Margin will be discharged by making the transfer to

that Custodian. The holding of Margin by a

Custodian will be deemed to be the holding of that

Margin by IFM. Subject to any elections made by

Counterparty in the Account Application with

respect to Initial Margin, IFM shall be entitled to

pledge, rehypothecate, invest, use, and commingle

Margin deposited by Counterparty, free from any

claim or right of any nature whatsoever. Upon the

occurrence of an Event of Default with respect to

Counterparty, IFM may exercise all rights as a

secured party under Law or in contract, including the

right to immediately apply Margin deposited by

Counterparty against any amounts owed to IFM by

Counterparty hereunder or under any other

agreement. Following the termination of a

Transaction, IFM shall return to Counterparty any

Margin deposited by Counterparty with respect to

such Transaction, net of any amounts owed by

Counterparty with respect to such Transaction.

Counterparty shall not be entitled to interest on any

Margin deposited with IFM.

2.6 Next Business Day. If a payment is

due under this Agreement on a day that is not a

Business Day, then such payment shall be made on

the next Business Day following the due date.

2.7 Netting of Payment Obligations. If

payments are due from both Parties on the same

day in the same currency, the Parties shall net the

amounts due to one Party against the amounts due

18

to the other Party, with the Party owing the greater

aggregate amount paying to the other Party the

difference between the amounts owed.

2.8 Default Interest. If a Party fails to

remit any amount payable by it when due, interest

on such unpaid portion shall accrue at the Default

Interest Rate from (and including) the due date to

(but excluding) the actual date of payment.

2.9 Condition Precedent for Payment.

Each obligation of each Party to pay any amount due

under this Agreement (other than an amount that is

due under Articles 5 or 6) is subject to the condition

precedent that no Event of Default (or event, act or

omission which, with the passing of time and/or the

giving of notice, will give rise to an Event of Default)

has occurred and is continuing with respect to the

other Party, provided, that any deferred payment

obligation shall be accounted for and settled on a

net basis on the later of (a) the date the relevant

Event of Default or potential Event of Default is

cured or waived, and (b) the scheduled termination

date of the Transaction with the latest scheduled

termination date in existence on the date the

deferral commences.

2.10 Tax Forms, Documents or

Certificates. Each Party agrees to promptly provide

to the other Party (or to such government or taxing

authority as the other Party reasonably directs), any

form, certificate or document required or reasonably

requested by the other Party in order to allow such

other Party to make a payment under the

Agreement without any deduction or withholding for

or on account of any tax, or with such deduction or

withholding at a reduced rate.

2.11 Disputed Statements. If

Counterparty, in good faith, disputes the amount (in

whole or in part) of any invoice, statement or other

payment demand, Counterparty shall pay to IFM the

undisputed portion thereof, and the Parties shall

work in good faith to resolve the dispute. If it is

ultimately determined that Counterparty owes all or

a portion of the disputed amount, Counterparty shall

immediately pay to IFM that amount upon such

determination with interest at the Default Interest

Rate from and including the original due date to but

excluding the date payment is actually made.

2.12 Verification of Information. In the

event of a good faith dispute regarding payments to

be made pursuant to any Transaction, each Party

shall have the right to verify the accuracy of any

invoice, payment demand, charge, payment or

computation made under this Agreement by

requesting copies of relevant portions of the books

and records of the other Party, which records the

other Party shall provide within a reasonable time.

Any request for verification must be made within

one (1) year after the date of the invoice or other

item with respect to which the request is made.

ARTICLE 3 Representations and Warranties

3.1 Mutual Representations and

Warranties. Each Party represents and warrants to

the other Party, as of the date of this Agreement

(which representations will be deemed to be

repeated by each Party on each date on which a

Transaction is entered into):

(a) It is either an individual, or an

entity duly organized and validly existing under the

laws of the jurisdiction of its organization or

incorporation and, if relevant under such laws, in

good standing, as described in the Account

Application;

(b) It is either an individual or a

corporation, limited liability company or partnership

or other entity described in the Account Application,

and as applicable, created or organized under the

laws of the jurisdiction identified on the first page of

this Agreement, and it is a taxpayer of the

jurisdiction identified in Section 7.1(a) below;

(c) It has the power to execute this

Agreement and all other documents relating hereto

to which it is a party (including the Account

Application), to deliver this Agreement and each

other document relating hereto that it is required

hereby to deliver (including the Account

Application), to perform its obligations under this

Agreement and any obligations it has under any

document relating hereto to which it is a party

(including the Account Application), and has taken all

necessary action to authorize such execution,

delivery and performance;

(d) Such execution, delivery and

performance do not violate or conflict with any Law

applicable to it, any provision of its constitutional

documents, any order or judgment of any court or

other agency of government applicable to it or any

19

of its assets or any contractual restriction binding on

or affecting it or any of its assets;

(e) All governmental and other

authorizations, approvals, consents, notices and

filings that are required to have been obtained or

submitted by it with respect to this Agreement or

any document relating hereto to which it is a party

have been obtained or submitted and are in full

force and effect and all conditions of any such

authorizations, approvals, consents, notices and

filings have been complied with;

(f) Its obligations under this

Agreement and any other document relating hereto

to which it is a party constitute its legal, valid and

binding obligations, enforceable in accordance with

The International Swaps and Derivatives Association (“ISDA”) has developed materials referred

to as the “ISDA August 2012 DF Protocol,” intended to facilitate industry compliance with

certain CFTC rulemakings under the Dodd‐Frank Act. The ISDA August 2012 DF Protocol adds

notices, representations and covenants responsive to Dodd‐Frank requirements that must be

satisfied at or prior to the time that transactions are executed. Information regarding the ISDA

August 2012 DF Protocol is available at: http://www2.isda.org/functional-areas/protocol-managment/protocol/12

IFM is a provisionally registered swap dealer. As a condition to contracting with IFM, IFM requires that Customers agree to certain provisions set out in the Schedules to the ISDA 2012

DF Protocol (the “ISDA 2012 DF Schedules”). These important contractual provisions are

summarized below, however, you should review the full text and by signing this Agreement,

you acknowledge that you have read and understand the full text of the ISDA 2012 DF

Schedules that apply to you and that you are able to make the representations, warranties and

agreements therein. The ISDA 2012 DF Schedules are available at: http://www2.isda.org/functional-areas/protocol-managment/protocol/12

Schedule 1 of the ISDA 2012 DF Schedules contains definitions for terms that are used in the

remainder of the ISDA 2012 DF Schedules.

[___] Please check here to confirm that Customer has reviewed and agrees to the

provisions of Schedule 1 of the ISDA 2012 DF Schedules, and that the terms of Schedule 1 will

apply to all transactions between Customer and IFM.

Schedule 2 of the ISDA 2012 DF Schedules covers matters including (but not limited to) the

following:

• Representations and warranties regarding information IFM and Customer have provided

to each other, as well as requirements to update that information.

• Agreements regarding reporting of transactions and notifications regarding transactions.

• Agreements and disclosures regarding clearing of Transactions and the provision of daily

marks and scenario analyses.

[___] Please check here to confirm that Customer has reviewed and agrees to theprovisions of Schedule 2 of the ISDA 2012 DF Schedules, and that the terms of Schedule 2 will

apply to all transactions between Customer and IFM.

The International Swaps and Derivatives Association (“ISDA”) has developed materials referred

to as the “ISDA March 2013 DF Protocol,” which are intended to facilitate industry compliance

with certain CFTC rulemakings under the Dodd‐Frank Act. The ISDA March 2013 DF Protocol

adds notices, representations and covenants responsive to Dodd‐Frank requirements that must

be satisfied at or prior to the time that transactions are executed. Information regarding the

ISDA March 2013 DF Protocol is available at: http://www2.isda.org/functional-areas/protocol-managment/protocol/13

IFM is not an “insured depository institution” but may be considered a “financial company” for purposes of CFTC 23.504(b)(5). As a condition to transacting with IFM, IFM requires that its

customers agree to certain provisions set out in the Schedules to the ISDA 2013 DF Protocol (the

“ISDA 2013 DF Schedules”). These important contractual provisions are summarized below,

however, you should review the full text of the ISDA 2013 DF Schedules that apply to you and by

signing this Agreement, you acknowledge that you have read and understand the full text that

apply to you, and that you are able to make the representations, warranties and agreements

therein. The ISDA 2013 DF Schedules are available at: http://www2.isda.org/functional-areas/protocol-managment/protocol/13

Schedule 1 of the ISDA 2013 DF Schedules contains definitions for terms that are used in the

remainder of the ISDA 2013 DF Schedules.

[___] Please check here if Customer is “an insured depository institution” as defined in 12 U.S.C. 1813 or check here [___] if Customer is a “financial company” as defined in 12 U.S.C. 5381(a)(11) for purposes of CFTC 23.504(b)(5).

[___] Please check here to confirm that Customer has reviewed and agrees to the

provisions of Schedule 1 of the ISDA 2013 DF Schedules, and that the terms of Schedule 1 will

apply to all transactions between Customer and IFM.

Schedule 2 of the ISDA 2013 DF Schedules covers matters including (but not limited to) the

following:

• Representations and warranties regarding information IFM and Customer have provided

to each other, as well as requirements to update that information.

• Agreements regarding how confirmations are finalized.

• Agreements and disclosures regarding clearing of transactions.

• End‐user exemption to the clearing requirement for Transactions.

• Orderly liquidation for certain financial institutions.

[___] Please check here to confirm that Customer has reviewed and agrees to the

provisions of Schedule 2 of the ISDA 2013 DF Schedules, and that the terms of Schedule 2 will

apply to all transactions between Customer and IFM.

Schedule 3 of the ISDA 2013 DF Schedules includes procedures for valuation of swaps and for

resolution of disputes regarding those valuations. If Customer is a “swap dealer,” as defined in

Section 1a(49) of the Commodity Exchange Act, a “security‐based swap dealer,” as defined in

Section 3(a)(71) of the Securities Exchange Act, a “major swap participant,” as defined in

Section 1a(33) of the Commodity Exchange Act, a “major security‐based swap participant,” as

defined in Section 3(a)(67) of the Securities Exchange Act, or a “financial entity,” as defined in

Section 2(h)(7)(C)(i) of the Commodity Exchange Act, IFM requires that Customer agree to the

terms of Schedule 3 of the ISDA 2013 DF Schedules.

[___] If Customer is a “swap dealer,” as defined in Section 1a(49) of the Commodity

Exchange Act, a “security‐based swap dealer,” as defined in Section 3(a)(71) of the Securities

Exchange Act, a “major swap participant,” as defined in Section 1a(33) of the Commodity

Exchange Act, a “major security‐based swap participant,” as defined in Section 3(a)(67) of the

Securities Exchange Act, or a “financial entity,” as defined in Section 2(h)(7)(C)(i) of the

Commodity Exchange Act, please check here to confirm that Customer has reviewed and

agrees to the provisions of Schedule 3 of the ISDA 2013 DF Schedules, and that the terms of

Schedule 3 will apply to all transactions between Customer and IFM.

If Customer is not a “swap dealer,” as defined in Section 1a(49) of the Commodity Exchange

Act, a “security‐based swap dealer,” as defined in Section 3(a)(71) of the Securities Exchange

Act, a “major swap participant,” as defined in Section 1a(33) of the Commodity Exchange Act, a

“major security‐based swap participant,” as defined in Section 3(a)(67) of the Securities

Exchange Act, or a “financial entity,” as defined in Section 2(h)(7)(C)(i) of the Commodity

Exchange Act, Customer may elect to utilize the valuation methodologies and valuation dispute

resolution procedures contained in Schedule 3 of the ISDA 2013 DF Schedules.

[___] If Customer is not a “swap dealer,” as defined in Section 1a(49) of the

Commodity Exchange Act, a “security‐based swap dealer,” as defined in Section 3(a)(71) of

the Securities Exchange Act, a “major swap participant,” as defined in Section 1a(33) of the

Commodity Exchange Act, a “major security‐based swap participant,” as defined in Section

3(a)(67) of the Securities Exchange Act, or a “financial entity,” as defined in Section

2(h)(7)(C)(i) of the Commodity Exchange Act, please check here if Schedule 3 of the ISDA 2013

Dodd‐Frank Schedules will apply to transactions between Customer and IFM. Checking this

box constitutes confirmation that Customer has reviewed and agrees to the provisions of

Schedule 3 of the ISDA 2013 DF Schedules, and that the terms of Schedule 3 will apply to all

transactions between Customer and IFM.

Schedule 4 of the ISDA 2013 DF Schedules includes procedures for reconciliation of portfolios

among swap counterparties. If Customer is a “swap dealer,” as defined in Section 1a(49) of the

Commodity Exchange Act, a “security‐based swap dealer,” as defined in Section 3(a)(71) of the

Securities Exchange Act, a “major swap participant,” as defined in Section 1a(33) of the

Commodity Exchange Act, or a “major security‐based swap participant,” as defined in Section

38

3(a)(67) of the Securities Exchange Act, IFM requires that Customer agree to the terms of

Schedule 3 of the ISDA 2013 DF Schedules.

[___] If Customer is a “swap dealer,” as defined in Section 1a(49) of the Commodity

Exchange Act, a “security‐based swap dealer,” as defined in Section 3(a)(71) of the Securities

Exchange Act, a “major swap participant,” as defined in Section 1a(33) of the Commodity

Exchange Act, or a “major security‐based swap participant,” as defined in Section 3(a)(67) of

the Securities Exchange Act, please check here to confirm that Customer has reviewed and

agrees to the provisions of Schedule 4 of the ISDA 2013 DF Schedules, and that the terms of

Schedule 4 will apply to all transactions between Customer and IFM.

If Customer is not a “swap dealer,” as defined in Section 1a(49) of the Commodity Exchange

Act, a “security‐based swap dealer,” as defined in Section 3(a)(71) of the Securities Exchange

Act, a “major swap participant,” as defined in Section 1a(33) of the Commodity Exchange Act,

or a “major security‐based swap participant,” as defined in Section 3(a)(67) of the Securities

Exchange Act, Customer may elect to utilize the portfolio reconciliation procedures contained in

Schedule 4 of the ISDA 2013 DF Schedules.

[___] If Customer is not a “swap dealer,” as defined in Section 1a(49) of the

Commodity Exchange Act, a “security‐based swap dealer,” as defined in Section 3(a)(71) of

the Securities Exchange Act, a “major swap participant,” as defined in Section 1a(33) of the

Commodity Exchange Act, or a “major security‐based swap participant,” as defined in Section

3(a)(67) of the Securities Exchange Act, please check here if Schedule 4 of the ISDA 2013

Dodd‐Frank Schedules will apply to transactions between Customer and IFM. Checking this

box constitutes confirmation that Customer has reviewed and agrees to the provisions of

Schedule 4 of the ISDA 2013 DF Schedules, and that the terms of Schedule 4 will apply to all

transactions between Customer and IFM.

If Customer has elected to have Schedule 4 of the ISDA 2013 DF Schedules apply to transactions

with IFM, and is not a “swap dealer,” as defined in Section 1a(49) of the Commodity Exchange

Act, a “security‐based swap dealer,” as defined in Section 3(a)(71) of the Securities Exchange

Act, a “major swap participant,” as defined in Section 1a(33) of the Commodity Exchange Act,

or a “major security‐based swap participant,” as defined in Section 3(a)(67) of the Securities

Exchange Act, Customer may elect to only review portfolio data from IFM, or may elect to

exchange portfolio data with IFM.

[___] Please check here if (i) Customer has elected to have Schedule 4 of the ISDA

2013 DF Schedules apply to transactions between Customer and IFM, (ii) Customer elects to

only review portfolio data provided by IFM, and (iii) Customer is not a “swap dealer,” as

defined in Section 1a(49) of the Commodity Exchange Act, a “security‐based swap dealer,” as

39

defined in Section 3(a)(71) of the Securities Exchange Act, a “major swap participant,” as

defined in Section 1a(33) of the Commodity Exchange Act, or a “major security‐based swap

participant,” as defined in Section 3(a)(67) of the Securities Exchange Act.

[___] Please check here if (i) Customer has elected to have Schedule 4 of the ISDA

2013 DF Schedules apply to transactions between you and IFM, (ii) Customer elects to

exchange portfolio data with IFM, and (iii) Customer is not a “swap dealer,” as defined in

Section 1a(49) of the Commodity Exchange Act, a “security‐based swap dealer,” as defined in

Section 3(a)(71) of the Securities Exchange Act, a “major swap participant,” as defined in

Section 1a(33) of the Commodity Exchange Act, or a “major security‐based swap participant,”

as defined in Section 3(a)(67) of the Securities Exchange Act.

Customers whose transactions are subject to Schedule 4 of the ISDA 2013 DF Schedules may

elect to reconcile portfolio data with data provided to a swap data repository, rather than

exchanging data directly with IFM.

[___] Please check here if (i) Customer is required to be subject to Schedule 4 of the

ISDA 2013 DF Schedules, or has elected to be subject to Schedule 4 of the ISDA 2013 DF

Schedules, and (ii) Customer elects to reconcile portfolio data with data provided to a swap

data repository. By checking this box, Customer agrees that Part VI of Schedule 4 of the ISDA

2013 DF Schedules will apply to transactions between Customer and IFM.

Please sign below to confirm the information provided and elections made with respect to the ISDA 2013 Dodd‐Frank Supplement: Customer Signature: ________________________________ Customer Name (Print):______________________________ Signatory Title (if Customer is an entity) or Agent Name (if documents are being executed by an Agent on behalf of Customer): ________________________________________ Date: _____________________________ month day year

40

END USER EXCEPTION TO THE CLEARING REQUIREMENT

With respect to any swap that is subject to the mandatory clearing requirements under Section

2(h) of the Commodity Exchange Act, there is an exemption available from this requirement for

persons that are considered “end users.” This exemption is described in CFTC Regulation

The questions in this section are designed to enable us to determine whether you are eligible

for this exemption from the clearing requirement, and to enable you to elect to take advantage

of this exemption, if you desire to do so. Please check the boxes below as appropriate:

[___] Customer is NOT any of the following: (i) a “swap dealer,” as defined in Section

1a(49) of the Commodity Exchange Act, (ii) a “security‐based swap dealer,” as defined in

Section 3(a)(71) of the Securities Exchange Act, (iii) a “major swap participant,” as defined in

Section 1a(33) of the Commodity Exchange Act, (iv) a “major security‐based swap participant,”

as defined in Section 3(a)(67) of the Securities Exchange Act, or (v) a “financial entity,” as

defined in Section 2(h)(7)(C)(i) of the Commodity Exchange Act

[___] Customer is a “financial entity,” and is eligible for an exemption from the clearing

requirement because it meets the qualifications under Section 2(h)(7)(C)(iii) of the Commodity

Exchange Act (the “finance affiliate exemption”)

[___] Customer is a “financial entity,” and is eligible for an exemption from the clearing

requirement because it meets the qualifications under Section 2(h)(7)(D) of the Commodity

Exchange Act (the “hedging affiliate exemption”)

[___] Customer is a “financial entity,” and is eligible for an exemption from the clearing

requirement because it meets the qualifications under Section 2(h)(7)(C)(ii) of the Commodity

Exchange Act (the “small bank exemption”)

End User Exception Election:

[___] Please check here if any of the four Boxes above are checked, Customer is

entering into swap transactions with IFM solely for purposes of hedging or mitigating

commercial risks as described in CFTC Regulation 50.50(c), and Customer elects to NOT clear

swap transactions that would otherwise be subject to the CFTC’s mandatory clearing

requirement.

The answer to this question can be changed at any time, or with respect to any particular

swap transaction. If you have elected to use the End User Exception, you are required to

provide certain information to a registered Swap Data Repository (or to the CFTC if no Swap

Data Repository is available to receive such information). This filing can be made on an annual

1 The CFTC re-codified the end-user exception from swap clearing from Part 39 to Part 50 of the regulations, to consolidate the CFTC clearing rules in the Code of Federal Regulations.

basis, or on a trade‐by‐trade basis. If Customer has made the annual filing, please provide the

date on which this filing was made, and the identity of the Swap Data Repository to which it was

made:

Date: __________________

Swap Data Repository: ____________________________________________

If Customer has not made an annual filing, you are required to provide us with the

information we need to make this filing (which is set out in CFTC Regulation 50.50), at the time

of each swap transaction entered into with IFM.

Customer Signature: _______________________ Customer Name (Print):______________________________ Signatory Title (if Customer is an entity) or Agent Name (if documents are being executed by an Agent on behalf of Customer): ________________________________________ Date: _____________________________