Page 1

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

1

Introducing the Corporate Performance Index An Essential Fix for TSR

A white paper By Bennett Stewart, CEO, EVA Dimensions LLC

Page 2

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

2

Table of Contents TSR Can Mislead……………………………………………………………………………………………………………………………….3

CPI Catches TSR’s Errors……………………………………………………………………………………………………………………4

How CPI Works…………………………………………………………………………………………………………………………………5

Case Study #1: Monster Beverage…………………………………………………………………………………………………….6

Case Study #2: Dean Foods……………………………………………………………………………………………………………..11

CPI Explains TSR….………………………………………………………………………………………………………………………….12

Case Study #3: Hershey vs. Tyson.……………………………………………………………………………………………..…..14

An Exception: Coca-Cola Consolidated.………………………………………………………………………….…………..…..17

Summing Up the CPI Score.…………………………………………………………………………………………………….………17

Page 3

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

3

TSR Can Mislead

Total shareholder return is the reigning champ in the corporate governance arena. Use of TSR

has exploded since governance consultants ISS and Glass Lewis began applying it as a key variable in

developing “say on pay” proxy recommendations and in decisions to support or reject an activist’s

agenda. Today half the companies in the S&P 500 use TSR to determine incentive pay, up from fewer

than one in five a decade ago. Yet many firms and boards are dissatisfied with it, and are looking for an

alternative.

TSR almost always is more reliable than other popular performance metrics such as growth in

earnings or EPS. But even TSR can mislead, and it should not be the final word in any assessment of

corporate performance. TSR systematically overstates the performance of companies that simply have

recovered from temporary setbacks, and it unfairly and misleadingly penalizes stellar performers that

have slipped only slightly or have failed to live up to inflated expectations of investors.

Differences in leverage ratios also complicate matters. Companies with greater leverage tend to

show up at the top or bottom of the TSR league tables simply because changes in their underlying

business values are spread over a slimmer equity base, and not because they are performing

fundamentally better or worse than other, less-leveraged firms. TSR simply cannot be fairly compared

across industry peers that operate with different levels of debt, yet that comparison is invoked all the

time.

What’s more, research by Cornell University’s Institute for Compensation Studies and the Pearl

Meyer compensation consulting firm finds there is no correlation between the use of TSR in

compensation plans and subsequent company performance. That isn’t surprising, since TSR itself

provides no guidance at all as to how executives can improve it.

Page 4

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

4

CPI Catches TSR’s Errors

A new measure called the Corporate Performance Index, or CPI, provides a needed complement

to TSR that greatly improves its reliability and also provides executives with a roadmap to improve

performance and shareholder returns. CPI, developed by EVA Dimensions, ranks companies in terms of

their growth trend in generating economic profits, the profitability and market value of their business

franchises, and how well positioned investors believe they are for future profit growth. It sums up each

company’s financial health as a percentile score compared to its industry group or a broad market index.

CPI rankings generally are aligned fairly closely with TSR readings, with about a 60%

correlation. In most cases, CPI helpfully adds to the credibility of the TSR verdict and the confidence

that boards and others can have in it. It also helps to demystify TSR by providing a window into the

underlying financial factors that determine it.

But CPI and TSR give materially different ratings for about 40% of the companies on the market,

and distant outliers exist in every industry. On one side, CPI highlights those that actually are

underperforming their peers despite seemingly impressive TSRs. Equally important, it sorts out false

negatives, showing that some firms with relatively low TSRs should be given the benefit of the doubt in

light of their long-term track records and high standing among peers.

Why do TSR and CPI sometimes deviate? The main reason is that the change-in-share-price

component of TSR (which swamps the contribution of dividends) is based entirely on changes in investor

forecasts of value from the beginning to the end of a period, rather than on whether the company

actually added or subtracted value by its operating performance during the period. Shareholder returns

cannot be ignored, of course. But it is dangerous, given all that rides on it, to base decisions about

performance on a single measure, even one as good as TSR. And it always is unwise to ignore the

underlying business performance that ultimately drives stock prices.

Another, subtler reason why shareholder returns are not the full story is that returns should be

weighted by the amount of shareholder value at risk, but in practice aren’t. If a company’s stock price

falls from $10 to $5, for example, then goes back to $10, the returns read -50%, then +100%. Even

though the value change is identical – its $5 down and $5 up – the returns are materially different in

magnitude. They differ because more or less value is going along for the ride, depending on the initial

valuation base. Creating value is what matters, and that is what managers should be paid to do. But as

far as telling that story is concerned, rates of return are inherently biased upwards for weak firms that

start off with depressed valuations, and it becomes systematically harder and harder for elite firm (like

Apple) to keep generating outstanding percentage returns on top of an ever larger valuation base.

Enter CPI, which reflects the value being created as it is being created, as the profits that

underpin the value are being produced. CPI also weighs underlying business performance without the

distortion of leverage. It also takes into account a company’s accumulated track record of performance

and its general standing in its peer group, not just whether it happened to rise or slip in recent periods.

Page 5

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

5

How CPI Works

CPI uses a set of four measures to develop a comprehensive score of financial health from a

shareholder point of view. The measures are:

1. Wealth Creation and Franchise Value: the firm’s total market value premium or discount to

its book capital, stated per unit of sales (we call the valuation premium “MVA,” for market

value added)

2. Profitability: the firm’s true economic profit, expressed as a profit margin ratio of sales (the

term we use for economic profit is “EVA,” standing for economic value added; it is profit net

of a full cost-of-capital interest charge on the firm’s debt and equity capital)

3. Profitable Growth: the trend growth rate in the firm’s EVA profit over the most recent three

years

4. Strategic Position: the long-run growth in EVA profit that investors have factored into the

firm’s share price

The first two metrics are

snapshot statistics, reflecting the

firm’s profitability and market

valuation, while the latter two are

moving pictures, gauging actual

and expected profit trends. Two

are market-based, incorporating

investor perceptions and

expectations, and two reflect

actual performance in terms of

earning and increasing economic

profits. All the measures,

moreover, are in relation to the

firm’s total capital, its debt plus

equity. Because of that, they

capture the performance of the

business and aren’t affected by

financing ratios.

As you will see, EVA and MVA, measuring economic profit and owner wealth, are the two most

essential measures of corporate performance and value creation. All four of the ratio statistics in CPI

are variations on those two measures.

To reach CPI’s upper ranks, a firm has to score well on all four measures. It must first of all

preside over a valuable and profitable business franchise, one capable of generating high-quality profits,

and its stock must trade for a lofty premium to invested capital. The firm has to have generated an

exceptional growth trend in profits over the past three years and, to top it off, it must be so strategically

well positioned that investors believe its future profits will grow faster than those of its peers.

Page 6

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

6

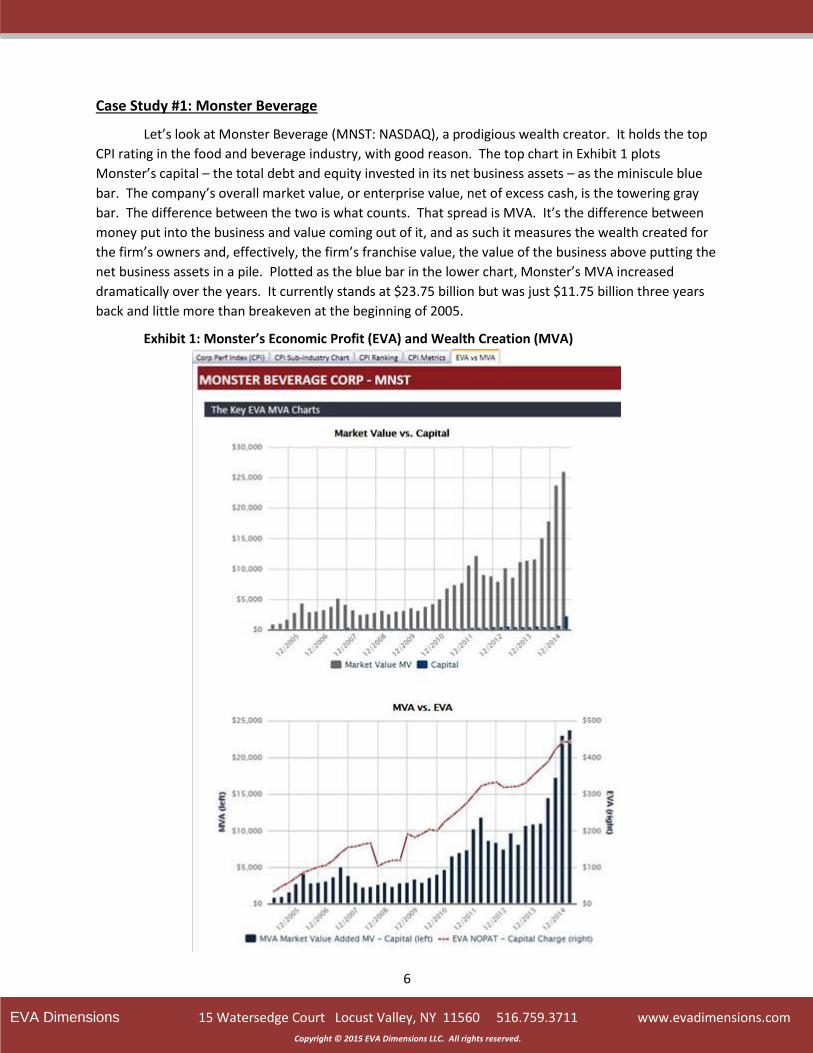

Case Study #1: Monster Beverage

Let’s look at Monster Beverage (MNST: NASDAQ), a prodigious wealth creator. It holds the top

CPI rating in the food and beverage industry, with good reason. The top chart in Exhibit 1 plots

Monster’s capital – the total debt and equity invested in its net business assets – as the miniscule blue

bar. The company’s overall market value, or enterprise value, net of excess cash, is the towering gray

bar. The difference between the two is what counts. That spread is MVA. It’s the difference between

money put into the business and value coming out of it, and as such it measures the wealth created for

the firm’s owners and, effectively, the firm’s franchise value, the value of the business above putting the

net business assets in a pile. Plotted as the blue bar in the lower chart, Monster’s MVA increased

dramatically over the years. It currently stands at $23.75 billion but was just $11.75 billion three years

back and little more than breakeven at the beginning of 2005.

Exhibit 1: Monster’s Economic Profit (EVA) and Wealth Creation (MVA)

Page 7

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

7

Monster has created such enormous owner wealth and franchise value because it has been

phenomenally successful at generating and growing economic profits. The red line on the lower chart

traces Monster’s EVA profit – the profit above and beyond its full cost of capital. The most recent

reading through mid-2015 shows EVA at a four-quarter run rate of $443 million, compared to $322

million three years before. Like MVA, EVA has been positive and it has been growing at a robust rate.

The close correspondence between Monster’s MVA wealth premium and its EVA profit is no

accident. To see why, though, we need to take a slight detour to discuss the cost of capital that is

deducted from EVA. It is not a cash cost, like interest expense. Rather, it is an opportunity cost. It is the

rate of return that the company’s investors could otherwise expect to earn by purchasing a stock and

bond portfolio that matches the company’s risk profile. That return requirement starts with the interest

rate available on long-term government bonds, which is a couple of percent these days, plus a two-to-

ten percent premium to compensate for the cycles and risks in the firm’s business, less a discount for

using debt to finance the business because the interest expense is tax deductible. Stirred together,

most companies today have an overall weighted-average cost of capital of between 4 and 10 percent. It

is lower for regulated utilities and stable food companies, and higher for home builders and brokerage

firms and tech companies – as you would expect. The key point is that EVA is measured after deducting

that full cost of capital from the firm’s after-tax operating profits. EVA only starts to count profits after

all investors, including shareholders, have received a minimum acceptable return to compensate for risk

and as set by the market.

Even though the cost of capital is never fully deducted from accounting profits, it has real

consequences. If a firm is just covering it, and is just breaking even in an economic sense, then the firm

will tend to trade just for book value, or close to it. Why would investors ever pay a market premium

over book capital if the firm is unable to give them a premium return on their capital? Put simply, if EVA

is zero, then MVA should be zero, too.

The opposite is true as well. Investors will pay market-to-book premiums for companies that

can generate premium economic profits. They will bid up the share price to the point where they

expect to earn the cost of capital as a return on the elevated value that they are paying. And the more

EVA profits a firm is earning, and the more rapidly they are expected to increase, the more owner

wealth and MVA is created.

A specific corporate finance formula encapsulates this: a firm’s MVA wealth premium at any

point in time equals the present value of the EVA profits the market projects it will earn. And as a result,

changes in MVA tend to reflect the changes in the EVA profit that a firm produces over time.

The link is quite clear for Monster. Its MVA closely mirrored the movements in its EVA profit,

just as corporate finance theory predicts it should. Monster is no aberration. Research by EVA

Dimensions confirms that changes in MVA (i.e. the changes in owner wealth and in franchise value) are

more highly correlated with the changes in EVA, in economic profits, than with any of the conventional

financial statistics.

Now let’s look at how Monster does on the four CPI ratios, which, as we have said, are all

variations on EVA and MVA, for reasons that should now be more apparent. Start in Exhibit 2 with the

status quo measures. Monster’s EVA and MVA ratios are plotted as the blue lines in the two left-side

charts. The green and red lines trace the 90th and 50th percentile values among food and beverage

Page 8

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

8

firms. Monster currently is producing almost $10 in owner wealth per $1 of sales (its MVA/Sales ratio is

near 1000%), while even the 90th percentile firm is far behind, with less than $3 of MVA per $1 of sales.

Exhibit 2: EVA and MVA, as a percent of sales

The EVA-to-sales ratio in the lower left chart gauges business model productivity. It brings

together pricing power, operating efficiency, and asset turns into a net profit margin score that is

inherently more comparable than others. Chip-maker Intel, for example, has a massive operating

margin, but because it ties up tons of risky capital in fabrication plants, its net EVA-to-sales profit margin

is much lower and a much fairer indication of the value of its business model. Its EVA Margin can also be

fairly compared with other companies, even unrelated ones like Wal-Mart Stores. The retailer operates

with a meager operating margin but compensates with hyper-rapid asset turns and much leaner capital

requirements, leaving EVA Margin as the common denominator between the two firms. It makes close

cousins of even distant relatives.

EVA Margin is especially useful for making comparisons within an industry group. Say one

competitor makes its products and another one farms out manufacturing. Operating margin

comparisons would be quite meaningless, but the firm’s EVA Margins would reveal which one netted

the most added value. On this score Monster is a winner. Its EVA Margin is an eye-popping 17.6% as

compared to just 8.6% for the 90th percentile firm in its industry (for reference, among S&P500

companies the median EVA Margin is 2.5%, the 75th percentile is 6%, and 90th percentile, 12%).

Page 9

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

9

The blue bars in the charts on the right side of Exhibit 2 are the percentile scores for Monster

versus the food and beverage peer set. It has consistently scored in the upper decile, and more often

than not has been the top-rated firm on these two metrics.

The two other CPI components are plotted for Monster in Exhibit 3. The top graph is an EVA

growth statistic called EVA Momentum. In simplest form that is the change in EVA divided by sales in

the prior period. EVA Momentum is the only performance ratio where a bigger ratio value is always

better, because it gets bigger when EVA grows faster, and EVA is the real key to creating wealth and

driving TSR. As such, EVA Momentum receives the greatest weighting, at 40%, in the CPI score.

For CPI we use a special version called three-year trend Momentum. It’s computed by running a

regression line through the firm’s EVA profits over the trailing four years, and then dividing the slope of

the line by the average of sales in the first three periods. Since all four EVA points have a magnetic pull

on the line slope, the regression provides a more accurate reading on profit growth than a point-to-

point statistic. The median EVA Momentum among S&P500 companies runs at only 0.4% per annum the

75th percentile at 1.5%. Monster’s latest trend Momentum reading is 1.9%, which is especially

impressive since EVA profit growth is hard to come by among mature food and beverage companies.

Exhibit 3: EVA Momentum and Market-Implied Momentum

The last metric in the quartet is the forward-looking EVA growth rate that investors have baked

into the firm’s stock price, shown in the bottom chart in Exhibit 3. Recall that a firm’s market-to-book

premium, its MVA, equals the present value sum of its expected EVA profits. Since we can measure a

Page 10

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

10

company’s current MVA and its current EVA profits, it is possible with a little math to derive the forecast

EVA trajectory required to justify the current share price. We call this statistic Market Implied

Momentum, or MIM. The higher it is, the more confidence investors are expressing that the company is

positioned for profitable growth over a strategic time frame.

The inclusion of the market’s forecast for EVA growth in CPI means that a company cannot score

well by puffing up short-term EVA to the detriment of long-run value. The CPI score, and this metric in

particular, rewards firms that invest in their futures and nurture new products, capabilities, brands and

business models, and that are aware of and deftly deflect risks that frighten investors and that might

snare less nimble firms.

Interestingly, and as plotted in the lower left chart of Exhibit 3, while Monster’s actual EVA

growth trend cooled in recent years, investors grew more confident about its future potential. One

reason is that Monster recently joined forces with Coca-Cola and became its global purveyor of power

drinks in a deal announced in August 2014 and closed in June 2015. Whereas investors were projecting

an EVA growth pace of just under 2% pre-announcement – essentially in line with the firm’s actual trend

Momentum – they are now projecting a phenomenal 4.5% a year growth rate for at least a decade, at

the 98th percentile in its industry.

Exhibit 4: Monster’s CPI Score Summary

The right-hand table in Exhibit 4 provides an at-a-glance status report. It displays Monster’s

sales and sales growth rates for the most recent year and over the past three years, along with its

current EVA and MVA values. More to the point, the table recapitulates the four key ratio metrics that

enter into the company’s current CPI score – its EVA and MVA Margins, and the actual three-year trend

for EVA Momentum and the market’s forecast for future Momentum. Put four home runs together and,

no surprise here, Monster is the top-rated CPI scorer in its industry. And, as is plotted in the left-hand

chart in Exhibit 4, Monster led the league with a perfect 100 score, or close to it, for most of the past

decade.

Monster’s TSR also has been very near the best in its industry. Its most recent three-year TSR,

for example, clocked in at the 86th percentile among its food and beverage brethren. The right-side grid

of Exhibit 5 plots the company’s current CPI score on the vertical axis against the three-year TSR

percentile rank versus peers on the horizontal axis (we focus on the three-year TSR because that period

Page 11

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

11

is used to measure trend EVA Momentum in CPI, and because three years are long enough to be

strategic but short enough that the most recent returns are important). If the CPI score and TSR

percentile are close, the intersection on the grid will plot on or near the diagonal series of dots in Exhibit

5, which is the line along which the CPI score aligns with and confirms the TSR percentile. That’s where

Monster plots, at the upper right corner of the chart.

Exhibit 5: Monster’s TSR Percentile Rank versus CPI score

Page 12

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

12

Case Study #2: Dean Foods

Dean Foods stands in stark contrast to Monster. It resides at the other end of the performance

spectrum. Its current CPI score is just 4, and its three-year TSR percentile rank is 8 (one-year TSR is

much higher, but that is incorporated in the three-year return). Once again, the intersecting dot plots

near the diagonal, but this time near the lower left corner. The CPI score is right in line with the firm’s

poor TSR showing, and for good and understandable reasons.

Exhibit 6: Dean Foods’ TSR Rank versus CPI Score

The summary statistics appearing in the right-side table of Exhibit 7 explain it: Dean Foods is

currently unprofitable compared to its cost of capital (EVA is negative), its EVA profits have been

trending down over the past three years, the stock trades at a discount to its economic book value (MVA

is negative), and investors are skeptical about the company achieving anything better than a modest

improvement in EVA going forward (the market’s Momentum forecast, or MIM, is just 0.11% per

annum). Dean plainly is a troubled company, but in ways that TSR never reveals.

Exhibit 7: Dean Foods’ CPI Score Summary

Page 13

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

13

CPI Explains TSR

Monster and Dean Foods illustrate an important rule: Shareholder returns generally correlate

with CPI scores. The alignment for the Russell 3000 and S&P500 universe of companies is plotted in

Exhibit 8. To produce the charts, we divided all the companies in each index into ten equal-sized groups

according to their CPI scores, and then we identified the median TSR percentile score within each of

those decile groups. The plots of the ten connecting points show a high degree of correspondence, and

the slope, as expected, is positive. Simply put, the higher a company’s current CPI score, the higher it

will tend to rank in TSR versus its competitors over the prior one, three, and five years.

Exhibit 8: TSR Percentile versus CPI Score

Page 14

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

14

The relationship is smoother and stronger across the entire Russell 3000 stock universe than for

the more narrowly defined set of S&P500 stocks. With a greater number of observations in the sample,

coincidental aberrations wash out and the underlying connection more clearly emerges.

In both charts, the dots don’t reach as high or low as they should at the tail ends. The 90th-100th

decile CPI scores, for example, correspond to only the 70th-80th decile TSR rank. That is also to be

expected. As was suggested at the outset, the very highest and lowest TSRs will tend to come from

firms that are more leveraged, or that start off with depressed market valuations, more than from firms

that have fundamentally performed very well or very poorly. The distortion in TSR weakens the

connection to CPI at the extremes.

In general, though, CPI confirms TSR, and effectively explains it. CPI suggests that to rise in TSR

rank, and answer governance critics, a company must sustain a track record of growing profits above the

cost of the capital resources used to produce the growth (which in turn is the key to producing and

increasing owner wealth). This is not just an assertion or an empirical observation. In a companion

article entitled, What Determines Total Shareholder Return, also by Bennett Stewart, a mathematical

derivation proves that TSR is determined by a firm’s EVA performance. Cash flow and capital gains are

shown to be merely the messengers that transmit the returns that actually come from earning and

increasing economic profits over time.

An implication is that boards would be wise to tie incentive pay to the growth in EVA profits, i.e.,

to EVA Momentum. With that in place, managers will naturally pursue obvious things that increase

profits, like exacting premium prices for products and services and intelligently cutting wasteful

costs. With EVA, though, they’ll look beyond the income statement and will consider the balance

sheet. They will seek ways to reduce the capital charge, such as by speeding asset turns and running

leaner, or outsourcing operations to better- equipped third parties. They’ll also want to protect EVA by

ensuring capital is allocated with discipline, with the conviction it will cover the full charge EVA imposes

– all of which help to increase the firm’s EVA profit margin. But besides constraining and managing

capital, they’ll look for ways to invest it, too. They will want to pour resources into all endeavors that

they believe will produce returns over the cost of capital. Unlike return on capital, or profit margin for

that matter, EVA is most decidedly a pro-profitable growth metric, with Monster a good example.

Besides taking actions that fall into these neat categories, EVA will guide managers though tricky

choices. Is it best to restrain price markups and emphasize lean operations in order to increase market

share and growth, or is it more valuable to invest and innovate, and drive higher margins, but at the cost

of tying up more capital and appealing to a smaller share of the market? Questions like those involve

complex tradeoffs that trip up most metrics. But the correct answer is always to choose the strategy

that produces the biggest stream of EVA over time, because that produces the most shareholder value.

Once managers establish a successful track record of growing EVA profits, they ring another bell.

They give investors the evidence they need to extrapolate even more growth in EVA, which tends to

raise the MIM statistic. In sum, when managers are paid to improve EVA Momentum, simple as that

seems, they are motivated to turn all of the gears that lead to an increase in a firm’s CPI score, in its

MVA, and ultimately, if not immediately, in its total shareholder return.

Page 15

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

15

Case Study #3: Hershey vs. Tyson

CPI is valuable not only when it lines up with TSR. It’s also interesting when the verdicts

diverge, which is fairly common. Our study shows that CPI and TSR differ by more than 20 percentile

points for about 40% of all stocks, about equally divided on both sides. The outliers jump out when

companies are plotted on the CPI/TSR grid, as we have done with the food and beverage industry in

Exhibit 9. The upper left area that is bordered in blue contains companies that score materially higher

on CPI, meaning that TSR likely understates their performance, while the lower right red zone contains

companies with TSR ranks that likely overstate performance because they are significantly higher than

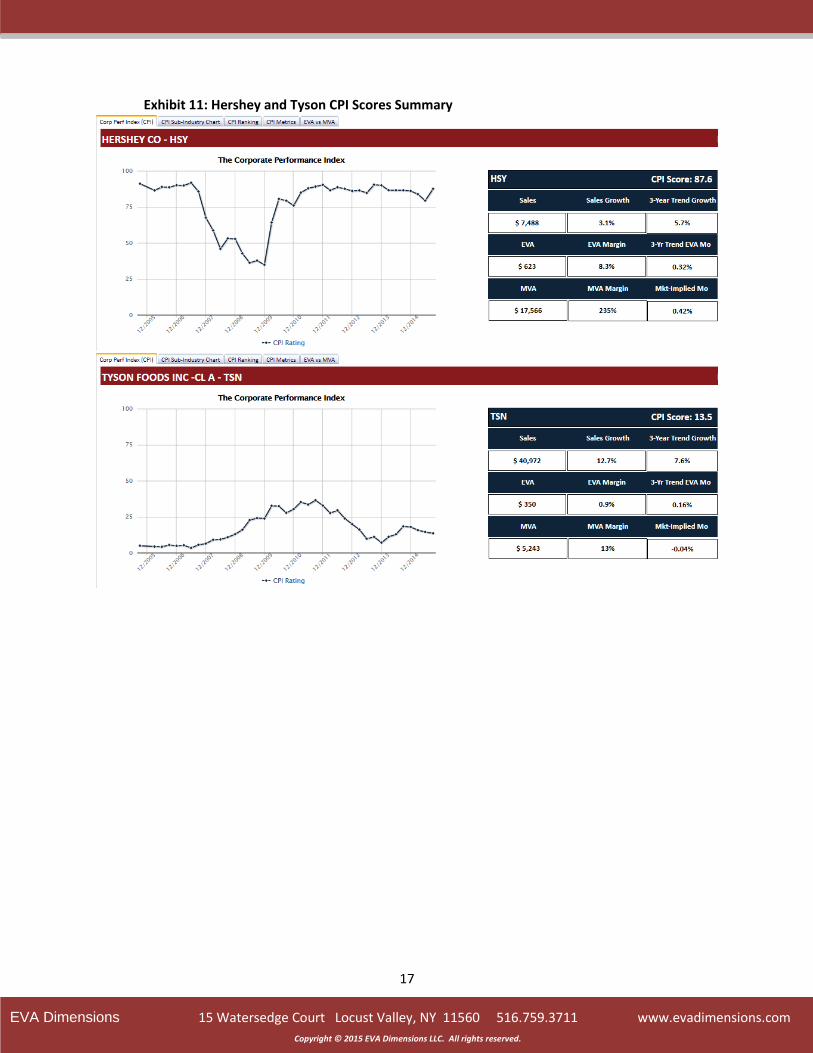

CPI. Let’s look at Hershey (HSY) in the blue zone and Tyson Foods (TSN) in the red zone as examples.

Exhibit 9: CPI Rating versus TSR Rank in the Food and Beverage Industry

Hershey’s three-year TSR was 10.9%, which put it at just 12th percentile in its industry. But the

return is low chiefly because Hershey’s MVA was at a very high level three years back. It’s not that

Hershey performed poorly since then; rather, it just didn’t do as well as investors initially expected.

More important, and what CPI recognizes (as documented in Exhibit 10), Hershey still is a

handsomely profitable and highly valuable franchise. Its current EVA Margin is 8.3%, and its MVA

wealth premium stands at 235% of sales. Hershey also generated a perfectly respectable EVA growth

trend over the past three years despite a recent lull (Momentum averaged +0.32% a year); moreover, as

far as investors can tell, the company is positioned for material growth in EVA profits over the next

decade. Its forward-looking MIM rate is +0.42%, or slightly above its recent growth trend. Putting all

Page 16

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

16

four measures together, Hershey’s CPI score is 88. Its 6th best out of 64 industry peers. Despite its weak

TSR showing, Hershey is in fact performing well and standing tall.

Exhibit 10: Hershey and Tyson Economic Profit (EVA) and Wealth Creation (MVA)

Tyson is just the opposite case. Its three-year TSR appears to be quite impressive at an average

of 28.1% a year, or 88th percentile among peers. Yet, as is evident from Exhibit 10, the return was an

aberration, so large only because Tyson’s value increased off a severely depressed MVA base. Tyson

outperformed expectations, but the expectations three years back were so low that the stock was

bound to produce an explosive return with even a relatively modest performance improvement.

The more penetrating insight, reported in the lower panel of Exhibit 11, is that Tyson’s vital

statistics are all still quite low: its EVA is barely positive, just 0.9% of sales (vs. 8.8% for Hershey); MVA,

too, is barely positive at 13% of sales; three-year trend EVA growth was 0.16%, or exactly half the pace

Hershey delivered; and most telling, the EVA growth implied by its stock price is -0.04% -- meaning that

investors don’t believe the current EVA is sustainable and think it is likely to dissipate with time. All told,

Tyson’s CPI score is just 14, or in the 47th rank out of the 64 food and beverage companies. CPI helpfully

shows that Tyson’s TSR is built on a shaky foundation, is unlikely to continue at anywhere near its

historic level, and that the company should by no means be given a pass by governance watchdogs and

activist investors.

Page 17

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

17

Exhibit 11: Hershey and Tyson CPI Scores Summary

Page 18

EVA Dimensions 15 Watersedge Court Locust Valley, NY 11560 516.759.3711 www.evadimensions.com

Copyright © 2015 EVA Dimensions LLC. All rights reserved.

18

An Exception: Coca-Cola Consolidated

Does CPI always trump TSR? No, there are instances where TSR is the more valid measure and

where CPI is a lagging indicator. That tends to happen most often when EVA is temporarily depressed

by a major capital investment or acquisition program that has not fully ripened, or when a company’s

stock price has run far ahead of recent results in anticipation of greater profit growth ahead.

The one and only example in the food and beverage business is Coke Consolidated

(NASDAQ:COKE), the nation’s largest independent Coca-Cola bottler. Its three-year TSR averaged 43% a

year, or 93rd percentile, almost all of which was due to a phenomenal 160% return in the most recent

year alone. Yet Coke Consolidated’s CPI score is only 24. The company’s EVA Margin is an uninspiring

0.2%, and its EVA has recently trended down. There’s an explanation. Acquisitions that added about

15% to the capital base over the past two years have not been fully digested. The company also

announced a deal with The Coca-Cola Company that will expand its franchise territory significantly. The

company’s stock performance is not attributable to already achieved profits, but to the creation of new

EVA growth opportunities that should increase the CPI score down the road.

Summing Up the CPI Score

Even in the case of the rare exceptions like Coke Consolidated, an analysis that combines TSR

and CPI produces a more complete and reliable understanding of corporate performance than one can

get from either measure alone. Boards will want to consult CPI to uncover the financial factors that are

shaping TSR or that will shape it. There are times, too, when a board will want to use a strong CPI score

as a counterpoint to a weak TSR, to defend its pay practices or fend off unwarranted overtures from an

activist.

Governance watchdogs, too, are apt to find value in it. They will want to consult CPI to be sure

they are not hounding the wrong companies, and to spotlight others that need attention despite a

seemingly favorable TSR record. They will also want to cite the EVA statistics when confronting an

underperforming company. They’re far less subject to the vagaries of the market and much more

reflective of management’s ability to allocate, manage and redeploy capital resources effectively, which

after all, is the real aim of the corporate governance game.

CPI reports for individual companies and for more than 75 U.S. and global business sectors are

available in an easy to use on-line tool called CPI Express, which is updated daily for more than 20,000

global tickers. Contact EVA Dimensions for a demonstration or more information.

Post Script

A companion article, Why Is EVA and Not EPS Used in the CPI Score?, examines shortcomings in conventional metrics, and highlights with two cases, Amazon and Volkswagen, the significant advantages of using economic metrics over the accounting-based ones in rating corporate performance. Available upon request from EVA Dimensions.