Working Capital Management. 1 INTRODUCTION : One of the most important functions in day to day management of the firm is the management of working capital. Working capital is defined as the capital required for the day to day working of the firm. It is also referred to short term assets used in daily operations. These consist primarily of cash marketable securities, account receivable and inventories. Effective management of working capital requires effective planning and control. Working capital management is one of the functional areas of finance that covers financing the required volume from various sources of a reasonable cost of capital. It involves in maintaining adequacy of current assets as well as reducing the level of risk posed by current Liabilities. Once the level of working capital is fixed, a firm has to find out the sources of finance. In this project, attempt have been made to highlight the concept of working capital, the volume of working capital; various constituent of current assets to gross working capital i.e. total current assets and financing of gross working capital. There may be difference in approach in arrangement of chapterisation. However the scheme of study is planned as follows: –Working Capital –Conceptual Aspect. –Financing Working Capital. –Profile of the company (Reliance Industries Ltd.). –Methodology. –Case Study. –Conclusion. Bibliography. Acknowledgement

One of the most important functions in day to day management of the firm is the

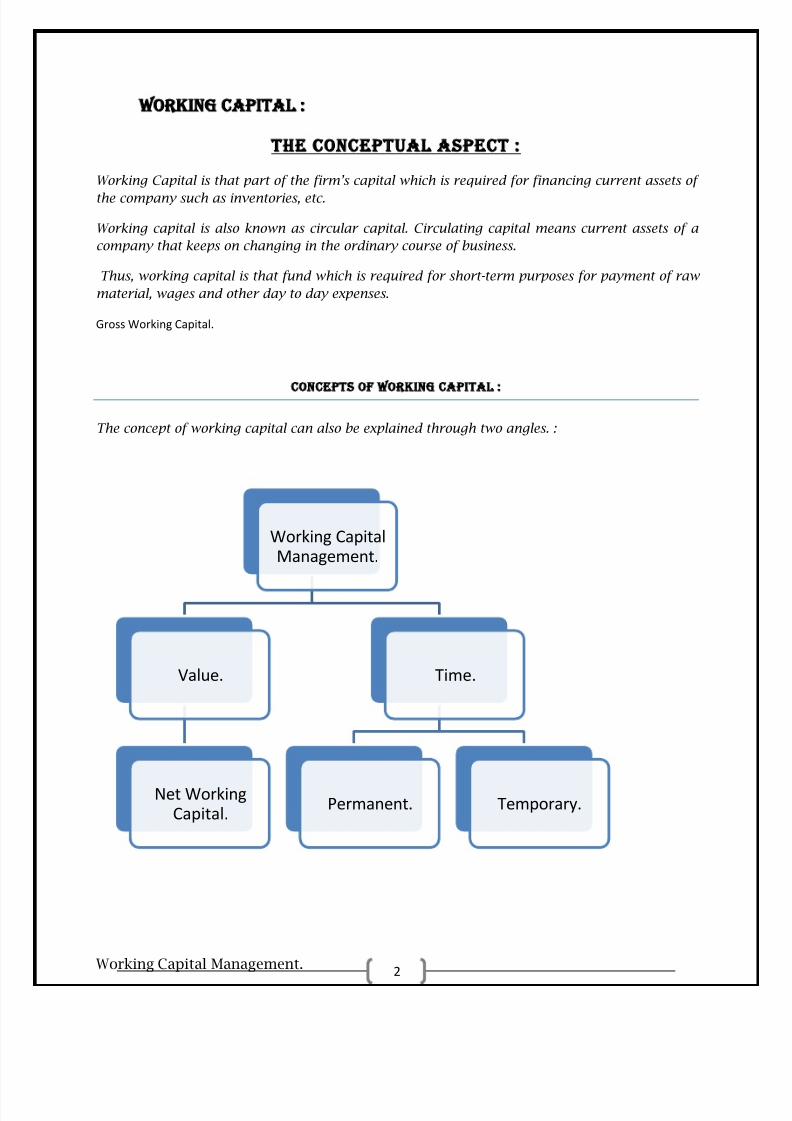

management of working capital. Working capital is defined as the capital

required for the day to day working of the firm. It is also referred to short term

assets used in daily operations. These consist primarily of cash marketable

securities, account receivable and inventories. Effective management of working

capital requires effective planning and control.

Working capital management is one of the functional areas of finance that

covers financing the required volume from various sources of a reasonable cost

of capital. It involves in maintaining adequacy of current assets as well as

reducing the level of risk posed by current Liabilities. Once the level of working

capital is fixed, a firm has to find out the sources of finance.

In this project, attempt have been made to highlight the concept of workingcapital, the volume of working capital; various constituent of current assets to

gross working capital i.e. total current assets and financing of gross working

capital.

There may be difference in approach in arrangement of chapterisation. However

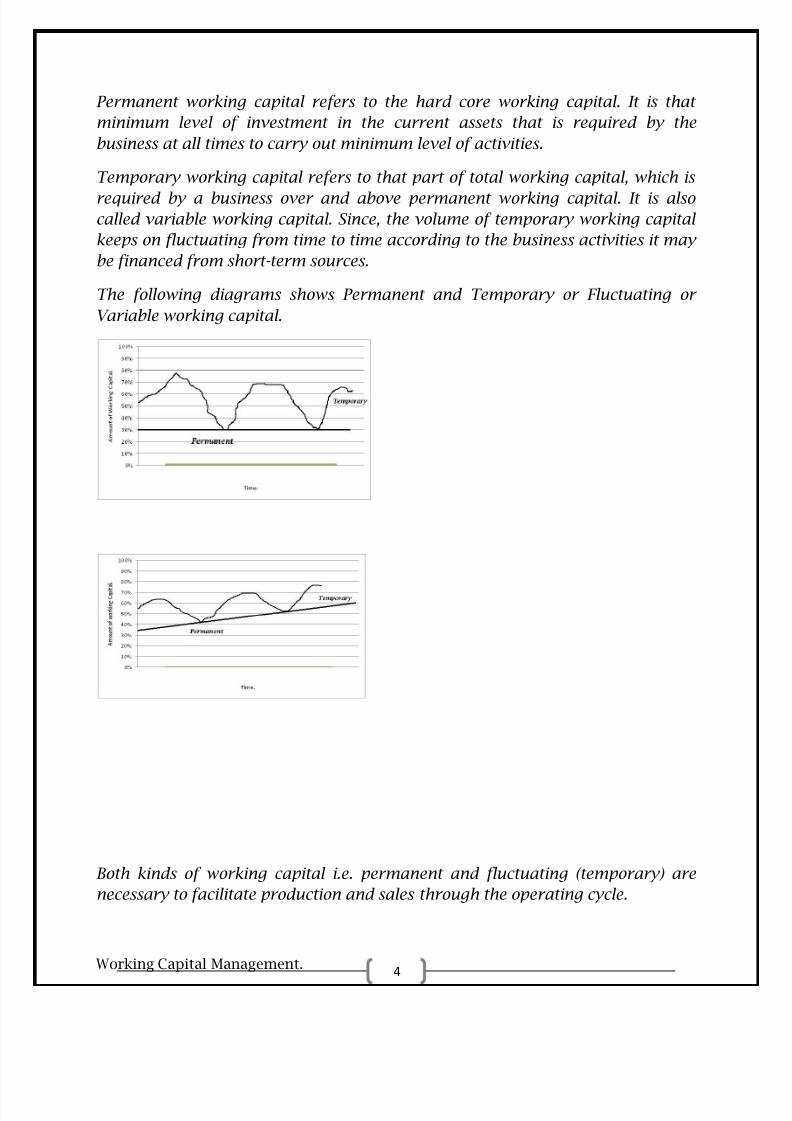

Permanent working capital refers to the hard core working capital. It is that

minimum level of investment in the current assets that is required by the

business at all times to carry out minimum level of activities.

Temporary working capital refers to that part of total working capital, which is

required by a business over and above permanent working capital. It is alsocalled variable working capital. Since, the volume of temporary working capital

keeps on fluctuating from time to time according to the business activities it may

be financed from short-term sources.

The following diagrams shows Permanent and Temporary or Fluctuating or

Variable working capital.

Both kinds of working capital i.e. permanent and fluctuating (temporary) are

necessary to facilitate production and sales through the operating cycle.

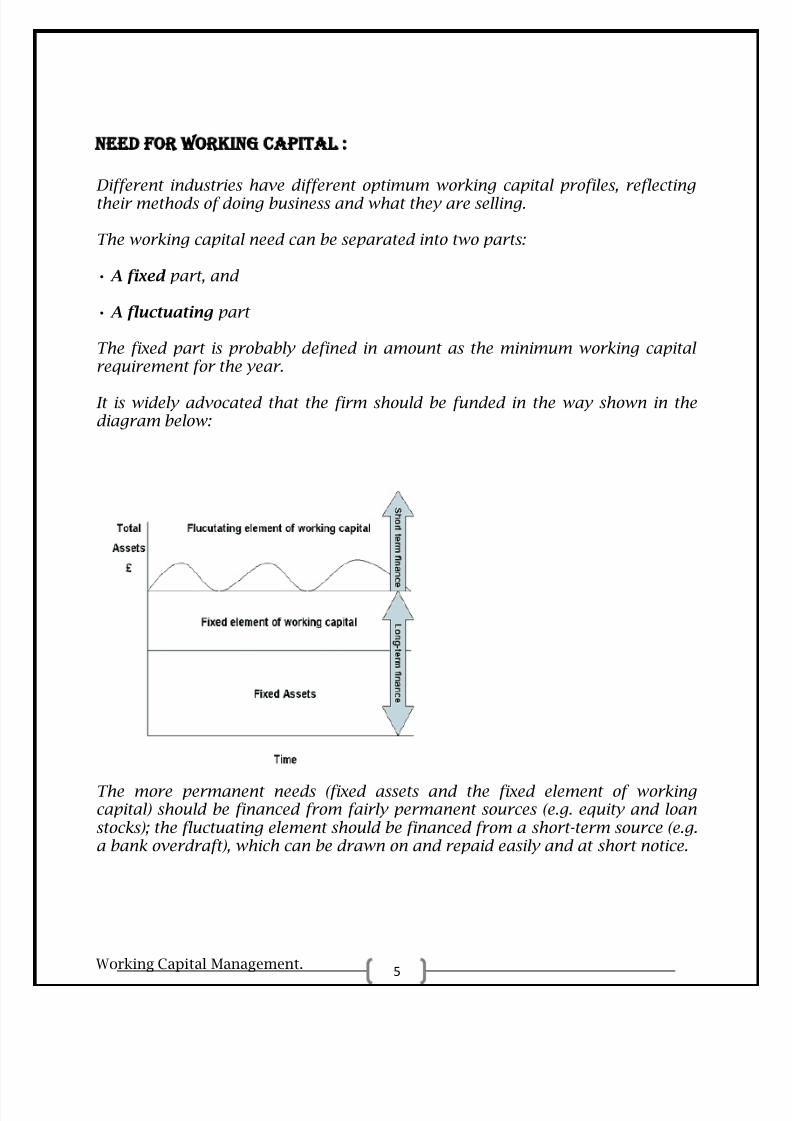

Different industries have different optimum working capital profiles, reflectingtheir methods of doing business and what they are selling.

The working capital need can be separated into two parts:

• A fixed part, and

• A fluctuating part

The fixed part is probably defined in amount as the minimum working capitalrequirement for the year.

It is widely advocated that the firm should be funded in the way shown in thediagram below:

The more permanent needs (fixed assets and the fixed element of workingcapital) should be financed from fairly permanent sources (e.g. equity and loanstocks); the fluctuating element should be financed from a short-term source (e.g.a bank overdraft), which can be drawn on and repaid easily and at short notice.

B ill discounting is recognized as an important short term financial instrument and it is widely

used method of short term financing. In a process of bill discounting, the supplier of goods draws

a bill of exchange with direction to the buyer to pay a certain amount of money after a certain

period, and gets its acceptance from the buyer or drawee of the bill.

6. Bill Rediscounting Scheme :

T he bill rediscounting scheme was introduced by Reserve Bank of India with effect from 1 st

November, 1970 in order to extend the use of the bill of exchange as an instrument for providing

credit. Under this scheme, all licensed scheduled banks are eligible to offer bills of exchange to

the Reserve Bank for rediscount.

7. Factoring :

F actoring is a method of financing whereby a firm sells its trade debts at a discount to a financial

institution. Thus, factoring is a continuous arrangement between a financial institution, (namely

the factor) and a firm (namely the client) which sells goods and services to trade customers on

credit. As per this arrangement, the factor purchases the client‟s trade debts including accounts

receivables either with or without recourse to the client, and thus, exercises control over the credit

extended to the customers and administers the sales ledger of his client.

8. Finance from Banks :

B anks today constitute the major suppliers of working capital credit to any business activity.

Reserve Bank of India has withdrawn the prescription, in regard to assessment of working

capital needs, based on the concept of Maximum Permissible Bank Finance, in April 1997. Banks

are now free to evolve, with the approval of their boards, methods for assessing the working

capital requirements of borrowers, within the prudential guidelines and exposure norms.

Profile of Reliance Industries Limited :

History:

The Reliance Group, founded by Dhirubhai H. Ambani (1932-2002) on 11th February 1966, isIndia's largest private sector enterprise, with businesses in the energy and materials value chain.Group's annual revenues are in excess of US$ 66 billion. The flagship company, RelianceIndustries Limited, is a Fortune Global 500 company and is the largest private sector company inIndia. Reliance Industries Limited (RIL) is a conglomerate with business in the energy andmaterials value chain.The Company operates in three segments: petrochemicals, refining and oil & gas.

The petrochemicals segment includes production and marketing operations of petrochemical

products. The refining segment includes production and marketing operations of the petroleum

products. The oil and gas segment includes exploration, development and production of crude oil

and natural gas. It‟s others segment includes textile, retail business, special economic zone (SEZ)

development and telecom/broadband business.

Reliance Industries Limited is one of the largest publicly traded company in India by market

capitalization and is the second largest company in India by revenue after Indian Oil

Corporation. It is also India's largest private sector company by revenue and profit.

The company is ranked 99th on Fortune Global 500 list of the world's biggest corporations for

the year 2012. Backward vertical integration has been the cornerstone of the evolution and

growth of Reliance.

Starting with textiles in the late seventies, Reliance pursued a strategy of backward vertical

integration in polyester, fiber intermediates, plastics, petrochemicals, petroleum refining and oil

and gas exploration and production - to be fully integrated along the materials and energy value

chain.

Reliance enjoys global leadership in its businesses, being the largest polyester yarn and fiberproducer in the world and among the top five to ten producers in the world in majorpetrochemical products.

Major Group Companies are Reliance Industries Limited , including its subsidiaries and RelianceIndustrial Infrastructure Limited.

Businesses divisions:

Major subsidiaries and associates

Reliance Life Sciences centers its profit-making ventures around medical, plant and

industrial biotechnology opportunities. Specifically, this company specializes inmanufacturing, branding, and marketing Reliance Industries' products inbiopharmaceuticals, pharmaceuticals, clinical research services, regenerative medicine,molecular medicine, novel therapeutics, biofuels, plant biotechnology, and industrialbiotechnology sectors of the medical business industry.

Reliance Institute of Life Sciences (RILS), established by Dhirubhai AmbaniFoundation, is an institution offering higher education in various fields of life sciences andrelated technologies.

Reliance Logistics (P) Limited is a single-window company selling transportation,distribution, warehousing, logistics, and supply chain-related products, supported by in- house state of the art telemetric and telemetry solutions.

Reliance Clinical Research Services (RCRS), a contract research organization (CRO)and wholly owned subsidiary of Reliance Life Sciences, specializes in the clinical research

services industry. Its clients are primarily pharmaceutical, biotechnology, and medicaldevice companies.

Reliance Solar, the solar energy subsidiary of Reliance, aims to produce and retail solarenergy systems primarily to remote and rural areas and to bring about a 'transformationin the quality of life'.

Relicord is a stem-cell banking service owned by Reliance Industries.

Infotel Broadband is a broadband service provider which gained 4G licenses for

operating across India, now it is wholly owned by RIL for 48 billion ( US 873.6 million).

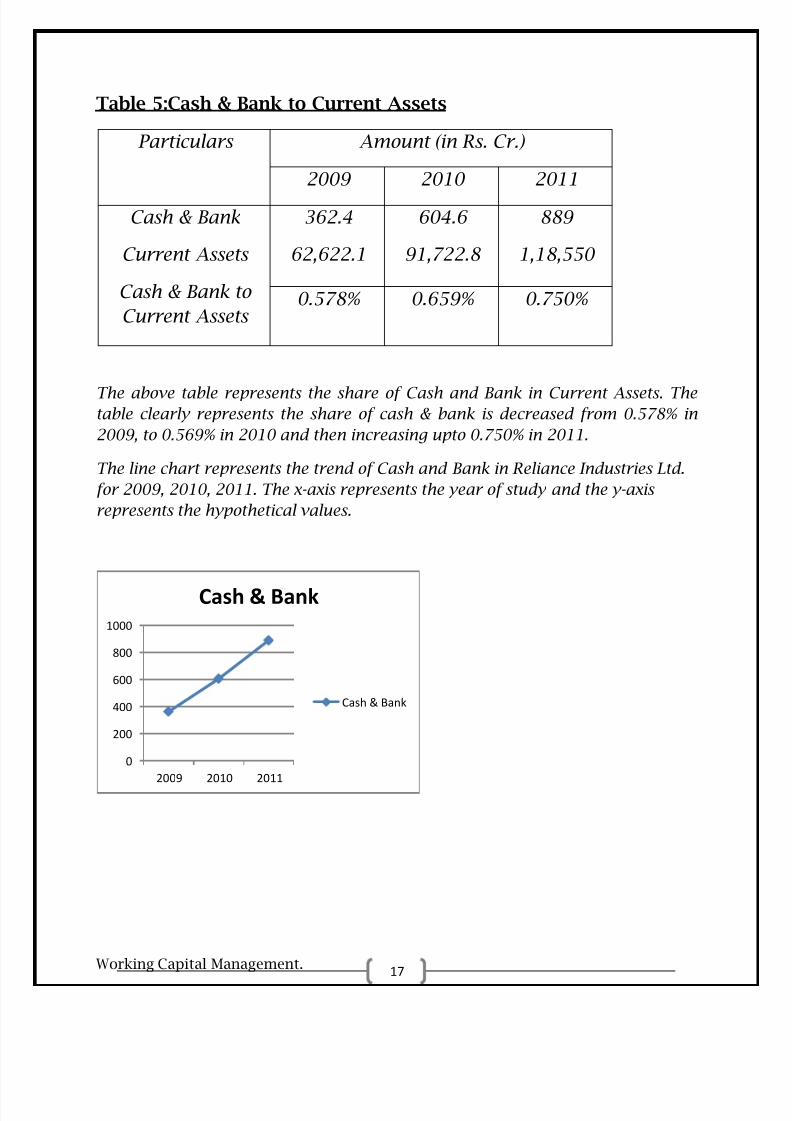

The above table represents the share of Cash and Bank in Current Assets. Thetable clearly represents the share of cash & bank is decreased from 0.578% in

2009, to 0.569% in 2010 and then increasing upto 0.750% in 2011.

The line chart represents the trend of Cash and Bank in Reliance Industries Ltd.

for 2009, 2010, 2011. The x-axis represents the year of study and the y-axis

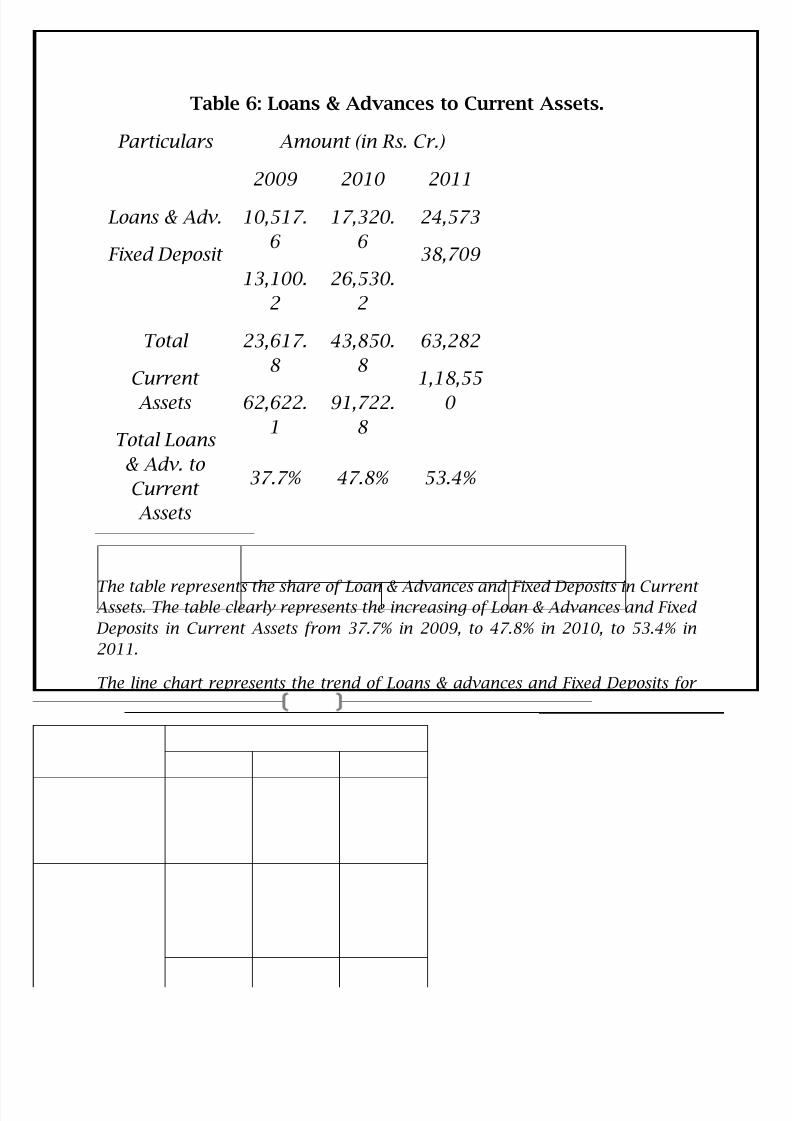

The table represents the share of Loan & Advances and Fixed Deposits in CurrentAssets. The table clearly represents the increasing of Loan & Advances and Fixed

Deposits in Current Assets from 37.7% in 2009, to 47.8% in 2010, to 53.4% in

2011.

The line chart represents the trend of Loans & advances and Fixed Deposits for

the year 2009, 2010, 2011 of Reliance Industries Ltd. The x-axis represents the

years of study and y-axis represents hypothetical valueTable7:Statement of

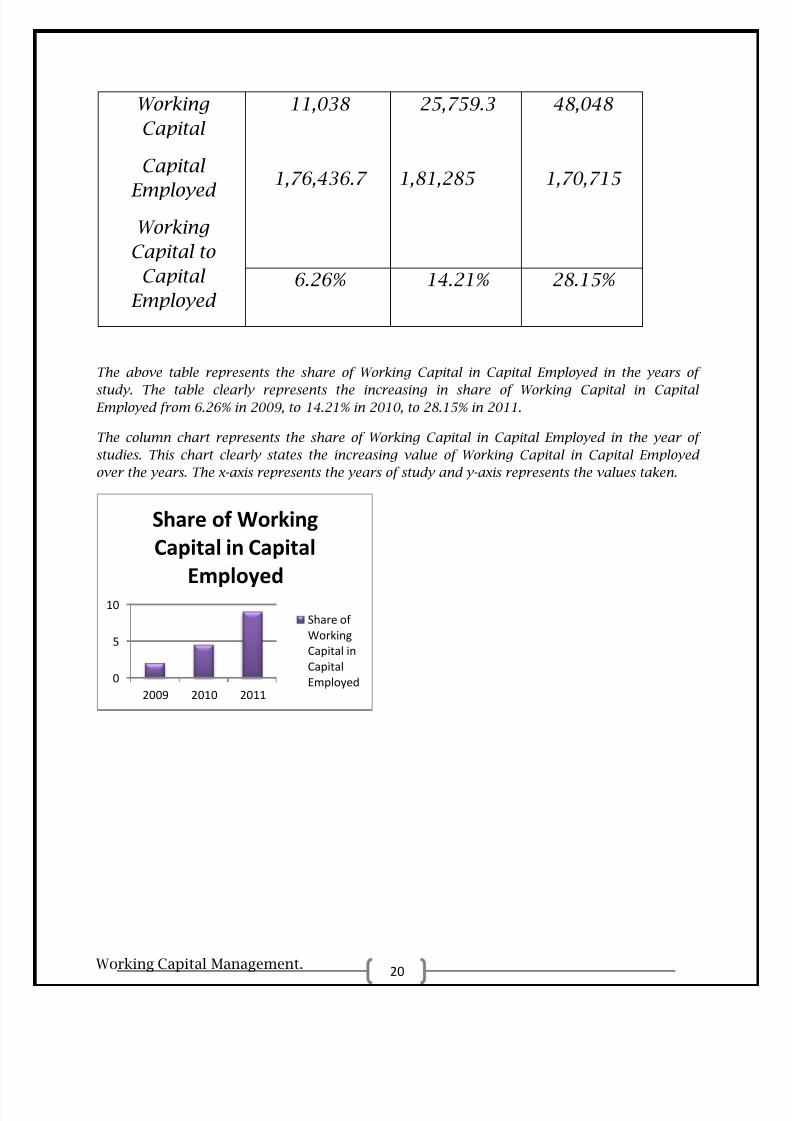

The above table represents the share of Working Capital in Capital Employed in the years of

study. The table clearly represents the increasing in share of Working Capital in CapitalEmployed from 6.26% in 2009, to 14.21% in 2010, to 28.15% in 2011.

The column chart represents the share of Working Capital in Capital Employed in the year of

studies. This chart clearly states the increasing value of Working Capital in Capital Employed

over the years. The x-axis represents the years of study and y-axis represents the values taken.

The above table represents the share of total debt i.e. Secured Loan and Unsecured Loan to

Current Assets of Reliance Industries Ltd. for the years of study. The table clearly represents thatTotal Debt to Current Assets is decreasing from 99.8% in 2009, to 73.55 in 2010, to 49.5% in

2012. This is a good scenario for the company as total debt of the company comprises of less

amount of its Current Assets.

The line chart is a graphical representation of the table. The x-axis represents the years of study

and the y-axis represents the values of study. The blue line represents secured debt of the

company, the red line represents the unsecured debt, and the green line represents the total debt

of the company. The chart also represents the trend followed through the years.