Page 1

1

CHAPTER I

INTRODUCTION

The economic development of a country depends upon the efficiency and

effectiveness of the resources mobilised by its financial system. Without an efficient

financial system the lending process will become difficult and risky. The financial

system is the key instrument for the achievement of socio-economic objectives. The

financial system comprises of various markets and institutions. According to Levine

(1997), financial services affect economic growth through five main channels viz.,

saving mobilisation, resource allocation, risk management, management monitoring

and trade facilitation. Each of the five main channels contributes to both capital

accumulation and the process of technological innovation (Desai, 2011: p. 9). From

years, the Indian financial system was caught in the restricted regulatory framework

and due to the non-existence of a strong financial institution mechanism, the position

of Indian financial system was not considered good.

The Indian financial system primarily comprises the financial institutions and

the financial markets. Both of these consist of organised and unorganised sector. The

unorganised sector includes lenders, indigenous bankers, pawnbrokers, traders etc.

while the organised sector comprises of various financial institutions which include

the regulatory and promotional institutions, banking institutions, investment

institutions and specialised institutions (Gupta and Chopra, 2008: pp. 3 and 4). The

banking institutions are major segment of the Indian financial system and have basic

three categories. These are commercial banks, cooperative banks and the development

banks. The development banks form an important segment of the financial system in

India (Figure 1.1).

Page 2

2

Figure 1.1

Financial System in India

Unorganised

Financial System

Financial Institutions Financial Market

Organised Organised Unorganised

Regular and

Promotional

Institutions

Banking

Institutions

NBFCs Specialized

Institutions

Investment

Institutions

Commercial

Banks

Cooperative

Banks

Development

Banks

Page 3

3

CONCEPT AND SIGNIFICANCE OF DEVELOPMENT BANKING

The origin of the concept of development banking was first experienced in the

Western countries with the establishment of „Societe General Pour Favoriser

Pindustrie Nationale‟ in Belgium in 1822. During 1852, another important institution

„Credit Mobiliser‟ was established in France for financing railways, insurance and

banking companies. After the World War II, due to heavy destruction the necessity of

restructuring of industries arises at different parts of the country. This led to the

establishment of new institutions to cater to the financial needs of post-war areas. As

a result, the Industrial Bank of Japan was incorporated in 1902, the Industrial

Development Bank of Canada in 1944 and the Industrial and Commercial Finance

Corporation Ltd. (ICFC) of England in 1945 were established as modern development

banks to provide term loans to industry (Mathur et al. 2005: p. 79). In 1949, the

Industry Credit Bank was established in Germany to cater to the financial needs of

German industries. The International Bank for Reconstruction and Development

(IBRD) also known as the World Bank and the International Monetary Fund (IMF)

also contributes for meeting the long term capital requirements of various industrial

units. These institutions proved that their formation results in stimulating the

economic growth especially by restructuring the war affected industries of different

countries of the world (Pathak, 2009: p. 406).

In India, the concept of development banking was the post-independence

phenomena. The large capital requirements for growth, expansion and diversification

of existing units was an issue of concern on one hand but the huge investment

requirement in new industrial projects by upcoming new industries was an another

notable issue. Although the country had a strong network of financial institutions but

these institutions were unable to meet the long-term financial requirements of the

industries. Thus, the need for establishment of new financial institutions was felt in

order to meet the total financial requirements of existing as well as new industrial

projects (Desai, 2011: p. 542).

In the present context, Development Banking has many variants in its form

and structure. It is a multi-sector institution that covers public sector, private sector,

joint sector as well as commercial banks. These are regarded as multi-purpose

Page 4

4

specialised financial agencies that provide medium as well as long-term financial

assistance to other financial institutions that aid in fostering the industrial growth and

development of an economy. Its vision is to bring innovative change in the

institutions. The importance of the role of development financial institutions was

strongly reiterated by S.S. Jagannathan, once governor of the Reserve Bank of India

(RBI) as, “In a country which has adopted planning as a technique of development,

deployment of resources according to the needs of the plan is an important as a

realisation of resources; hence, measures have been taken to ensure such conformity

to plan priorities” (Rohtagi, 2007: p. 200). Dr. Desai defines Development Bank as, “a

financial institution concerned with providing all types of financial assistance to

enterprises in the form of loans, underwriting, investment, guarantee operations and

promotional activities to accelerate the process of sustainable socio-economic

development and fosters growth and co-operation” (Desai, 2011: p. 542). According

to Encyclopedia Britannica 2001, “Development Banks are national or regional

financial institution designed to provide medium and long term capital for productive

investment, often accompanied by technical assistance, in less-developed

areas”(Rohtagi, 2007: p. 212). Thus, development banks are in true sense

development oriented.

Development bank is a distinguished institution having major impetus on

promoting economic development by encouraging new and small entrepreneurs for

making real investments in long-term projects. Managerial development is another

unique characteristic of the development banks. Due to industrialisation, the

technology also underwent rapid changes and becomes more and more complex.

Thus, these institutions enhance managerial skills among entrepreneurs by providing

training to them. These institutions are also regarded as purveyors of economic

planning. The decisions related to the credit allocation, resource mobilisation etc. for

creating productive capacities is facilitated by the development banks. These

institutions are induced by social profits rather than commercial profits. Their main

interest is to work for the general benefit of the public rather than seeking monetary

gain. Further, these banks are regarded as an engine of economic growth and

development of an economy. By providing profitable opportunities for investment,

Page 5

5

conducting feasibility analysis and through updated market information, these

institutions encourage entrepreneurs in utilising their entrepreneurial capacity. These

institutions also eliminate the problem of regional economic inequalities. Thus,

adequate attention should be given in the backward areas through diversification of

funds in those areas so as to promote balanced regional development.

Another major role played by development banks is of a „Gap Filler.‟ As

commercial banks are induced by profit motive and they fulfill the short-term

requirements of the industries, while development banks own their origin for meeting

the peculiar needs of not only private sector but public sector undertakings also. These

banks fill up the deficiencies of the existing financial institutions. These institutions

also help in strengthening the capital market of our economy. Through timely and

adequate availability of short-term, medium-term and long-term funds for projects it

leads to improve the existing position of the capital market. Apart from this,

development banks conduct market surveys, investment research and economic

studies to widen their experiences for the development of industries. These

experiences help the institutions in dealing with the problems arises in the future.

These institutions also act as an educator, guide, counsellor by providing guidance

related to the project formulation, implementation etc. to their entrepreneurs. Thus,

they not only provides finance but also encourages their entrepreneurs in bringing and

developing new ideas, techniques etc. related to the project. In addition, these

development financial institutions borrow from the World Bank and IDA and utilise

this foreign exchange in meeting the requirements of needy and productive

enterprises. This borrowed foreign exchange help in maintaining sound financial

status of the country. These banks also coordinates with the government, RBI and

other financial institutions engaged in the similar activities in order to avoid the

complexities arising in the growth of development finance. Thus, development banks

should adopt and apply new methods of financing along with traditional modes for

meeting the developmental as well as financial requirements of the country (Mathur et

al. 2005: pp. 80-81).

Page 6

6

DEVELOPMENT FINANCIAL INSTITUTIONS IN INDIA

The growing importance of the financial intermediaries has led the

government to realise the necessity of slowly transferring the ownership of some of

the important financial institutions from private ownership to state control (Clifford

Gomez, 2010: p.11). Accordingly, the Government took initiative for setting up of

new financial institutions and to nationalise some existing private financial

institutions. As a result, in 1948 the Reserve Bank of India was the first institution

that was nationalised by the government. Further, Industrial Finance Corporation of

India (IFCI) was the first development financial institution established in the year

1948. This institution was set up by an Act of the Parliament with an objective of

providing medium and long-term credit to the industrial concerns in India. It was

originally incorporated as statutory corporation but with a view to impart greater

operational flexibility as also to enhance its ability to respond to the need of changing

financial system, it was incorporated as a company in May 1993 (Mathur et al. 2005:

p. 93). Later on, it has been realised that, it was not possible for a single institution to

meet the diverse credit needs of small and medium enterprises dispersed in other parts

of the country. Consequently, some institutions were established at the state level also

for the promotion and development of medium and small-scale industries in the

particular states. Hence, State Financial Corporation Act was passed in 1951 for

setting up of State Financial Corporations in various territories. As a result, in 1953,

the first State Finance Corporation was established in Punjab. Further, 12 SFCs were

set up by 1955-56 and in all 18 SFCs came into existence by 1967-68. SFCs function

at the state level and extend financial assistance to small enterprises located in

backward areas at concessional rates (Pathak, 2009: p. 407). These SFCs act as an

agent of the Central as well as State government for bridging the gap of loan

requirements to small and medium scale industries. On the other hand, IFCI provides

assistance to large enterprises in the developed regions of the country at high interest

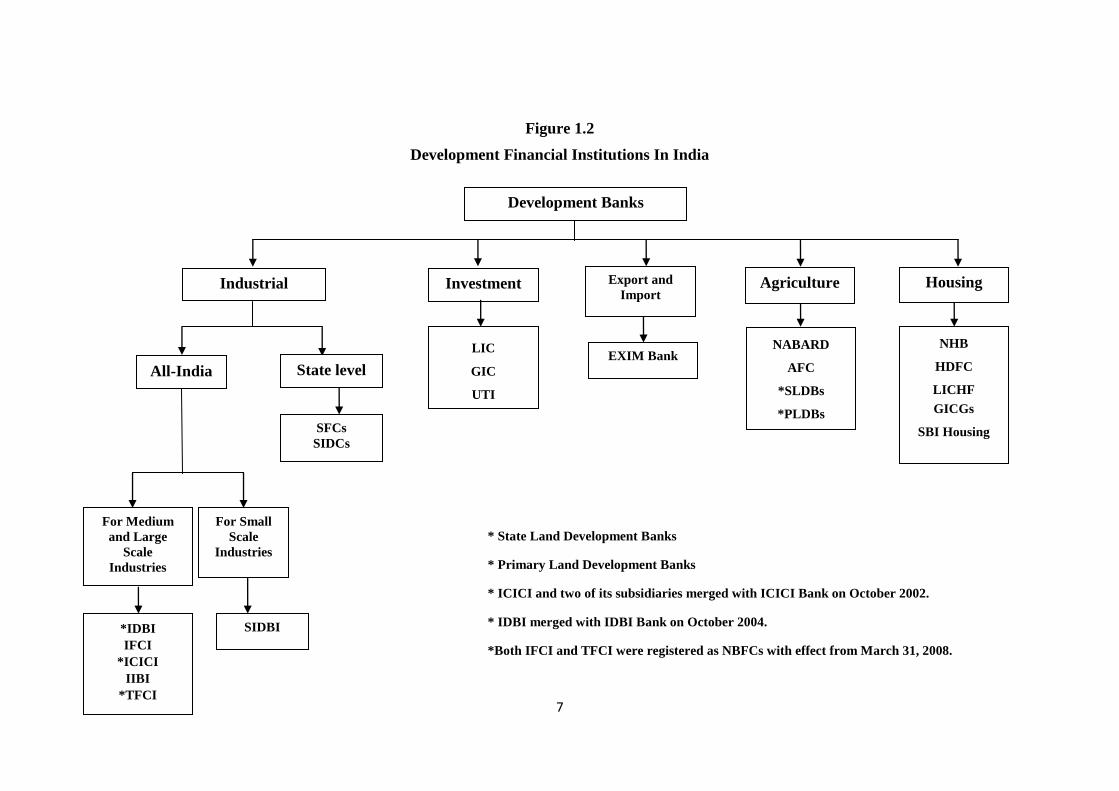

rates. Figure 1.2 shows the development financial institutions in India.

Page 7

7

Figure 1.2

Development Financial Institutions In India

* State Land Development Banks

* Primary Land Development Banks

* ICICI and two of its subsidiaries merged with ICICI Bank on October 2002.

* IDBI merged with IDBI Bank on October 2004.

*Both IFCI and TFCI were registered as NBFCs with effect from March 31, 2008.

Development Banks

Industrial Investment

All-India State level

SFCs

SIDCs

LIC

GIC

UTI

Export and

Import

EXIM Bank

Agriculture

NABARD

AFC

*SLDBs

*PLDBs

Housing

NHB

HDFC

LICHF

GICGs

SBI Housing

For Medium

and Large

Scale

Industries

For Small

Scale

Industries

SIDBI

*IDBI

IFCI

*ICICI

IIBI

*TFCI

Page 8

8

Besides this, further to widen the scope of small industries, a new corporation

was established at the all-India level known as the National Small Industries

Corporation (NSIC) in 1955. The NSIC is not a financing institution rather it helps in

making arrangements related to supply of machinery, training of workers, marketing

of products etc. of small-scale industries. The NSIC operates as a fully government-

owned corporation. On January 5, 1955, a new institution called Industrial Credit and

Investment Corporation of India (ICICI) was set up as a wholly owned private

institution to provide assistance to industrial concerns in the private sector. The bank

provides medium and long-term loans and issue guarantees on loans. It underwrites

new issue of shares and securities of industrial units. The bank also provides merchant

banking services (Mathur et al. 2005: p. 94). Apart from this, the government merged

245 life insurance companies in 1956 and established the Life Insurance Corporation

(LIC) of India during the same year to augment the total resources of the industrial

finance (Gomez, 2010: p. 11). In addition, during June 1958, the Refinance

Corporation of India Limited (RCI) was set up to stimulate commercial banks to

provide term finance facilities. Afterwards, another institution namely, the State

Industrial Development Corporation (SIDC) was set up during 1960s to act as a

catalytic agent for the promotion and development of medium and large scale

industries in the respective states. The SIDCs were the wholly-owned State

Government Corporations established to undertake various promotional activities

through conducting industrial surveys, entrepreneurship development programmes,

preparing feasibility reports etc. In July 1964, Industrial Development Bank of India

(IDBI) was set up as a wholly-owned subsidiary of the RBI to act as a coordinating

agency for industrial finance. As a result, the Refinance Corporation of India Limited

was merged with the IDBI during the same year. IDBI act as an apex institution and

performs promotional activities, co-ordinates the activities of other term-lending

institutions, works for the rehabilitation of sick units to strengthen the Indian financial

system.

Further, it was realised that besides providing financial assistance there must

be an institution at all-India level to mobilise the savings of the public. Accordingly,

the Unit Trust of India (UTI) was established in 1964 to pool the savings of the

public. The UTI achieves its objectives through purchase and sale of industrial and

corporate securities in the secondary market and underwriting of new capital issues.

Page 9

9

UTI has also established various companies in the areas of banking, investment

advice, securities trading, investors servicing etc. in order to fulfil the different needs

of the investors. With a view to act as an independent financial intermediary between

all-India and State level institutions and public sector commercial banks, the IDBI

was restructured and separated from the control of RBI on February 16, 1976. The

bank is now emerged as an autonomous corporation, taken over by the Government of

India (Srivastava and Nigam, 2008: p. 479). Another milestone in the field of

industrialisation was the establishment of Industrial Reconstruction Corporation of

India (IRCI) in 1971 mainly to concentrate on the problems of sick industrial units.

As the IRCI faced the risk of closure, so the Government of India converted IRCI into

Industrial Reconstruction Bank of India (IRBI) in March 1985. Now, this bank acts as

the principle reconstruction agency at all-India level and performs the similar

functions assigned to the IRCI. But the role of IRBI as a reconstruction agency comes

to an end when the Government convert the IRBI into a development finance

institution. This change took place when the Board for Industrial and Financial

Reconstruction (BIFR) was set up by the Government of India. The General Insurance

Companies in the country were also merged in 1973 to form the General Insurance

Corporation (GIC) of India. In December 1986, SCICI Limited was promoted by

ICICI together with other all-India financial institutions as a specialised financial

institution for encouraging and assisting development and investing in shipping,

fishing and related industries (Srivastava, and Nigam, 2008: p. 480). But, on April 1,

1996 SCICI Ltd. was merged with ICICI to achieve operational efficiency in

changing economy. In addition, three more financial institutions were set up to serve

in the agriculture, export-import and the housing sector. Accordingly, in July 1982

National Bank for Agriculture and Rural Development (NABARD) was established as

an apex refinancing institution. The bank aimed at promotion and development of

agriculture, small, cottage and village industries in the rural areas. NABARD also co-

ordinates with the institutions engaged in providing investment and financing credit in

rural areas. The bank acts as a refinancing agency between the State Government,

RBI and other national level institutions and helps in monitoring and evaluation of

projects (Pathak, 2009: p. 409). During the same year i.e. on January 1, 1982 the

Export-Import Bank of India (EXIM Bank) was established by an Act of Parliament,

commenced its operations from March 1, 1982. The bank acts as a principal financial

institution by providing direct financial assistance to exporters and importers for

Page 10

10

promoting international trade. The bank rediscounted the export bills discounted by

commercial banks for a period not exceeding 90 days. EXIM Bank also provides

assistance to foreign importers in the form of overseas Buyers Credit, technology and

other related services. With a view to expand housing finance to various income

groups in our country, another institution namely National Housing Bank (NHB) was

established in July 1988. The bank was set up under the National Housing Bank Act

1987 as a wholly owned subsidiary of the RBI to function as the principal agency for

promoting housing finance. Thus, NHB as the chief refinancing institution

channelized funds for housing finance through different housing linked saving

schemes while functioning within the network of housing policy regulations.

Another specialised financial institution at all-India level i.e. Tourism Finance

Corporation of India (TFCI) Ltd. was established on February 1, 1989 to cater

exclusively to the needs of tourism industry. However, the two financial institutions

i.e. ICICI and IDBI have decided to merge due to severe problem of bad debts faced

by them. This led to the beginning of a new era for the financial sector with the

emergence of new concept of Universal banking. As a result, both banks restructured

themselves to meet the global competitive challenges and repositioned themselves to

become a largest universal bank. A universal bank refers to a bank providing all types

of services like investment banking, commercial banking, merchant banking, project

advisory services etc. under one roof. Finally, on October 2002, ICICI Ltd. was

merged with ICICI Bank Ltd. and emerged as a largest private sector bank. Similarly,

on October 2004, IDBI merged with its IDBI Bank (Srivastava and Nigam, 2008: p.

481). Another move was made in regard to IFCI Ltd. and TFCI Ltd. as both the

financial institutions were registered as non-banking financial corporation‟s (NBFCs)

with effect from March 31, 2008. Among others, Industrial Investment Bank of India

(IIBI) was under the process of voluntary winding up due to its poor financial position

as on March 31, 2007 till date. As on March 31, 2013, there were four financial

institutions operating at all-India level i.e. Export-Import Bank of India (EXIM Bank),

National Bank for Agriculture and Rural Development (NABARD), National Housing

Bank (NHB) and Small Industries Development Bank of India (SIDBI) under the

regulation of Reserve Bank of India (RBI, Report on Trend and Progress of Banking,

2012-13: p. 118). The ownership pattern of development banks in India has been

shown in Table 1.1.

Page 11

11

Table 1.1

Ownership Pattern of Development Banks in India

(As at end-March 2013)

Institution Ownership Per cent

1 2 3

EXIM Bank Government of India 100

NABARD Government of India 99.3

Reserve Bank of India 0.7

NHB Reserve Bank of India 100

SIDBI*

Public Sector Banks 62.5

Insurance Companies 21.9

Financial Institutions 5.3

Others 10.3

* Three major shareholders of SIDBI are-IDBI Bank Ltd. (19.2%), State Bank of

India (15.5%) and Life Insurance Corporation of India (14.4%).

Source: RBI, Report on Trend and Progress of Banking, 2012-13, p. 118.

These financial institutions provide term finance, promote entrepreneurship,

enhance organisational effectiveness, undertake feasibility studies, developing

managerial skills and upgrade technical know-how. Thus, the basic motive of all these

development financial institutions at all-India and State level is to fill up the

deficiencies of the existing financial facilities and to serve and work to accelerate the

pace of industrialisation.

SMALL INDUSTRIES DEVELOPMENT BANK OF INDIA (SIDBI)

With a view to encourage small-scale sector in Indian economy, the need for

setting up of a separate institution to cater exclusively to the needs of small business

enterprises all over the country was strongly felt. Accordingly, the Government of

India established Small Industries Development Bank of India (SIDBI) under Section

3(1) of Small Industries Development Bank of India Act, 1989 as a wholly-owned

subsidiary of Industrial Development Bank of India (IDBI). The bank started its

operations from April 2, 1990. In the year 2000, the SIDBI was delinked from IDBI

as subsidiary. In pursuance of the amendments approved by the Parliament, 51 per

Page 12

12

cent shares of the SIDBI held by IDBI have been transferred to public sector banks,

LIC, GIC and other institutions owned and controlled by the central government. The

shares of SIDBI are held by thirty-three institutions comprising Insurance companies

owned or controlled by Central Government, various PSBs, with Industrial

Development Bank of India Ltd., State Bank of India and Life Insurance Corporation

of India being its three largest shareholders (SIDBI Annual Report 2012-13, p. 23).

The bank is an apex financial institution for the promotion, financing and

development of Micro, Small and Medium Enterprises (MSMEs) in the country

(Pathak, 2009: p. 425). The objective of SIDBI is to emerge as an only financial

institution to strengthen the Micro, Small and Medium Enterprises (MSMEs) sector

by providing promotional and developmental credit in order to contribute in the

process of economic growth and development. Thus, to increase the shareholder‟s

wealth and to make the MSME sector as strong, vibrant and globally competitive has

been the approach of SIDBI. As the basic idea underlying the formation of the SIDBI

was to foster the growth of MSME sector which occupies a vital position in Indian

economy (SIDBI Annual Report, 2011: p. vi). The main functions of SIDBI are:

To render direct assistance and refinance of loans and advances to micro, small

and medium industries, to subscribe stocks, shares, bonds or debentures of SFCs

and SIDCs, to initiate steps for technological upgradation and modernisation of

MSMEs. Thus, the bank has been assigned the role of principal financial

institution for promotion, financing and development of industry in small, tiny and

cottage sectors and to co-ordinate the functioning of institutions engaged in

similar activities.

It has to pay concentrated attention to the multi-dimensional growth and

development of Industries in the small-scale sector with special emphasis on the

micro, small and medium enterprises. Initially, SIDBI's business comprised of

refinancing to term loans granted by SFCs, SIDCs, banks and other eligible

financial institutions, direct discounting and rediscounting of bills arising out of

sale of machinery or any capital equipment by manufacturer in the MSME sector

and re-discounting of short-term trade bills arising out of sale of products in the

micro, small and medium enterprise sector (Srivastava and Nigam, 2008: p. 485-

486).

Page 13

13

For promotion, development and growth of micro, small and medium sector, the

bank extends technical and related support services. The bank provides

promotional and developmental support to the MSME sector to make it strong

and competitive in the international markets. The promotional and developmental

activities organised through the bank are categorized into Micro Enterprises

Promotion Programme (MEPPs), Entrepreneurship Development Programme

(EDPs), Skill-cum-Technology Upgradation Programmes (STUPs) and Small

Industries Management Programmes (SIMAP). These activities aim at generating

employment in rural areas.

After identifying the gaps in existing credit delivery system, the bank designed

schemes for direct lending to micro, small and medium enterprises so as to

provide assistance to Primary Lending Institutions which include State Financial

Corporation‟s (SFCs) and State Industrial Development Corporations (SIDCs).

Under indirect assistance, the bank provides assistance to MSMEs through the

Primary Lending Institutions by way of refinance, bills rediscounting and resource

support to institutions. Over the period, the bank has introduced new products and

modified the existing products to meet the financial and non-financial credit

requirements of micro, small and medium enterprise sector. It includes term loan

assistance, working capital assistance and non-fund based facility.

Apart from retail credit, the bank has been providing assistance through

infrastructure financing, venture capital, securitization to help to increase the flow

of credit to micro, small and medium enterprises (MSMEs).

Small and medium enterprises play a catalytic role in the growth and

development of global output. Over the years, this sector has been considered as an

important pillar of Indian economy. In order to increase the flow of credit to small and

medium enterprises, the Government of India has created Small and Medium

Enterprises (SME) Fund in April 2004. Since then, SIDBI has been structuring the

fund and providing financial assistance to Small and Medium Enterprises (SMEs) at

an interest rate of two per cent below the bank prime lending rate (PLR) (SIDBI

Page 14

14

Annual Report, 2005: p. 4). In addition, the Micro, Small and Medium Enterprises

Development Act, 2006 (MSMED Act, 2006), has been established by the

Government of India (GOI) for the promotion and development of MSMEs in the

country. The Act came into force with effect from October 2, 2006. The major

objective of the government behind enactment of this act is to fulfil the requirements

of the Micro, Small and Medium Enterprises (MSMEs) and to enhance the

competitiveness of these sectors. This Act provides the first-ever legal framework

recognising the concept of enterprise (comprising both manufacturing and service

entities), defining medium enterprises and integrating the three tiers of these

enterprises, namely micro, small and medium (Chatterjee and Jetli, 2009: p. 79). The

manufacturing and service enterprises are classified as micro, small and medium

according to the Micro, Small and Medium Enterprises Development Act, 2006.

Table 1.2 depicts the classification of MSMEs under the MSMED Act, 2006.

Table 1.2

Classification of MSMEs

Enterprises Manufacturing Enterprises

(Investment limit in plant and

machinery)

Service Enterprises

(Investment limit in

equipment)

Micro Upto Rs 25 lac Upto Rs 10 lac

Small Rs 25 lac-Rs 5 crore Rs 10 lac-Rs 2 crore

Medium Rs 5 crore-Rs 10 crore Rs 2 crore-Rs 5 crore

Source: Industry and Infrastructure Development in India since 1947, Chatterjee and

Jetli, p. 80).

The objective behind such classification aims at boosting the growth of

MSMEs within the social and economic policy framework of the country. It also

encourages new entrepreneurs in setting up of new units with advance technology that

helps in improving product quality. The growth and contribution of MSME sector in

terms of MSME units, employment, investment and gross output has been shown in

the Table 1.3.

Page 15

15

Table 1.3

Growth of MSMEs in India

SL.

No.

Year Total Working

MSMEs (In

Lac)

Employment

(In Lac)

Market Value of

Fixed Assets (In

Crore)

Gross Output

(In Crore)

1 1992-93 73.51(4.07) 174.84(5.33) 109623(9.24) 84413(4.71)

2 1993-94 76.49(4.07) 182.64(4.46) 115795(5.63) 98796(17.04)

3 1994-95 79.60(4.07) 191.40(4.79) 123790(6.9) 122154(23.64)

4 1995-96 82.84(4.07) 197.93(3.42) 125750(1.58) 147712(20.92)

5 1996-97 86.21(4.07) 205.86(4.00) 130560(3.82) 167805(13.60)

6 1997-98 89.71(4.07) 213.16(3.55) 133242(2.05) 187217(11.57)

7 1998-99 93.36(4.07) 220.55(3.46) 135482(1.68) 210454(12.41)

8 1999-00 97.15(4.07) 229.10(3.88) 139982(3.32) 233760(11.07)

9 2000-01 101.1(4.07) 238.73(4.21) 146845(4.90) 261297(11.78)

10 2001-02 105.21(4.07) 249.33(4.44) 154349(5.11) 282270(8.03)

11 2002-03 109.49(4.07) 260.21(4.36) 162317(5.16) 314850(11.54)

12 2003-04 113.95(4.07) 271.42(4.31) 170219(4.87) 364547(15.78)

13 2004-05 118.59(4.07) 282.57(4.11) 178699(4.98) 429796(17.90)

14 2005-06 123.42(4.07) 294.91(4.37) 188113(5.27) 497842(15.83)

15 2006-07 261.01(111.48) 594.61(101.62) 500758(166.20) 709398(42.49)

16 2007-08# 377.37 842.23 917437.46 1435179.26

17 2008-09# 393.70 881.14 971407.49 1524234.83

18 2009-10# 410.82 922.19 1029331.46 1619355.53

19 2010-11# 428.77 965.69 1094893.42 1721553.42

20 2011-12# 447.73 1012.59 1176939.36 1834332.05

Source: MSME (Micro, Small and Medium Enterprises) Annual Reports from 2010-

11 to 2012-13.

Note: The figures in brackets show the percentage growth over the previous year. The

data for the period up to 2005-06 is only for small-scale industries (SSI). Subsequent

to 2005-06, data with reference to micro, small and medium enterprises (MEMEs) are

being compiled.

# Projected

Page 16

16

The significant contribution of MSME sector has been reflected in the

establishment of about 447 lac total working enterprises, providing employment to

about 1012 lac persons and gross output of Rs 1834332.05 crore respectively over the

period.

Thus, it reflects that Micro, Small and Medium Enterprises (MSME) sector

plays a crucial role in employment generation and industrialisation of rural and

backward areas. This sector not only serves the basic needs of the MSMEs but also

helps in promoting socio-economic growth and development of the country. The

motto as envisioned by the 12th

Five Year Plan is to achieve, “Faster, Sustainable and

more Inclusive Growth,” of the Indian economy (SIDBI Annual Report 2011-12, p.

vi).

In addition, the bank has also taken some important initiatives since inception,

for the growth and development of MSMEs. These are:

In January 1995, the bank has established the Technology Bureau for Small

Enterprises (TBSE) as a joint venture of SIDBI. It helps in providing information

related to innovative technologies available, export promotion, financial

requirements and other support services for micro, small and medium enterprises

to meet the challenges of international competitiveness. TBSE is regarded as a

Technology Bank for the MSME sector.

On July, 1999, „SIDBI Venture Capital Limited‟ (SVCL), was established to

manage the venture capital fund and to act as the Asset Management Company of

National Venture Fund for Software and Information Technology Industry

(NFSIT).

During the year 2004-05, the GoI announced the setting up of a SME Growth

Fund (SGF) in SIDBI. It is an 8-year close ended Venture Capital Fund. The

major objective of this fund is to meet the risk capital requirements of SMEs

engaged in retailing, food processing, information technology, light engineering,

auto components, textiles, etc.

A new close ended venture fund named, “India Opportunities Fund” (IOF) has

been introduced by SVCL for a period of 10 years in 2010. The IOF has received

a corpus of Rs 671 crore upto April 2012. The Fund has been launched to meet the

needs of unlisted MSMEs in the areas of infrastructure, IT, clean technologies,

agro based industries, educational services, etc.

Page 17

17

On August 30, 2000 the GoI introduced Credit Guarantee Scheme (CGS) to assist

new and existing industrial units in the Micro and Small Enterprises (MSEs). For

this purpose, “Credit Guarantee Fund Trust for Micro and Small Enterprises

(CGTMSE) has been created. This scheme helps MSEs by providing both term

and working capital loan without collateral security and third party guarantees.

Under CGS, credit upto Rs 100 lac have been extended by Member Lending

Institutions (MLIs) like Scheduled Commercial Banks, selected Regional Rural

Banks and those institutions considered as eligible institutions by the Government.

In pursuance of SIDBI (Amendment) Act, 2000, the provisions of SIDBI Act,

1989 has been amended relating to the appointment of Chairman, Managing

Director and Board of Directors of SIDBI. The bank provides special focus to

attain Corporate Governance of International Standards by restructuring its

ownership structure.

In order to enhance the flow of credit from the banks to MSMEs at reasonable

terms, Small Industries Development Bank of India has set up SME Rating

Agency of India Ltd. (SMERA) on August 26, 2005. It started its operations from

September 05, 2005. SMERA is the country‟s first and only exclusive rating

agency for providing credit to MSMEs at concessional rates. SIDBI also offers

credit at 1 per cent less rate of interest to MSME clusters on the basis of SMERA

ratings (SIDBI Annual Reports 2005-2013).

The bank during the year 2007-08 has implemented the Right to Information

(RTI) Act, 2005.

With an objective to restructure the non-performing assets (NPAs) of MSME

sector, an Asset Reconstruction Company (Ltd.) was incorporated in April 2008

by SIDBI and its shareholders comprising 10 Public Sector Banks, 3 State Level

Institutions and Life Insurance Corporation.

Thus, over the years, SIDBI performed multifarious functions to develop the

MSME sector. The bank through its innovative products and services has been

meeting diverse credit and non-credit needs of the micro, small and medium

enterprises. Being a principal financial institution, the bank has taken number of

initiatives for strengthening the MSME sector. SIDBI puts special impetus towards

human resource development, quality promotion, corporate governance etc. Besides

Page 18

18

this, the bank also played its apex role more effectively through development of

infrastructure in the areas of Industrial, marketing, tourism etc. Thus, bank has been

consistently performing its responsibility by assisting the whole spectrum of the

micro, small and medium enterprises in our country.

NEED OF THE STUDY

SIDBI was established as an apex financing institution for growth, financing

and development of micro, small and medium enterprises (MSMEs) in April 2, 1990.

The primary objective of the bank is to strengthen the MSME sector though

employment generation, economic growth, balanced regional development, export

promotion etc. In the development of Indian economy, MSMEs plays a vital role

through its significant contribution in terms of Gross Domestic Product (GDP). Thus,

MSME sector undoubtedly has been considered as the most vital sector of our

economy. Since inception, the bank has introduced new products and modified the

existing products to meet the credit requirements of the small and medium enterprise

sector. The bank has been instrumental in providing assistance to all manufacturing

and service sectors for setting up for of new units, modernisation, expansion and

diversification of business for micro, small and medium enterprises. Although,

various studies have been conducted from time to time regarding different

development banks. But, it has been observed that over the period, there has been

progressive growth and change in the policies of the bank. So, it becomes important to

intensively examine the working and performance of SIDBI. It is with this

consideration, that the present study has been undertaken to assess the performance of

this institution from different perspectives.

OBJECTIVES OF THE STUDY

The main objectives of the study are:

1. To study the growth of SIDBI.

2. To study various schemes of SIDBI regarding financing of entrepreneurs.

3. To examine the promotional and developmental activities of SIDBI.

4. To evaluate financial performance of SIDBI.

5. To assess the opinion of entrepreneurs regarding functioning of SIDBI.

6. To make suggestions on the basis of findings of the study.

Page 19

19

CHAPTER SCHEME

The present study has been organised into eight chapters:

The first chapter is introduction. It describes the historical background of

development banking in western countries and in India. It also discusses in detail the

profile of SIDBI through its management, corporate governance, subsidiaries and

associate organisations. Further, it also highlights the contribution of the bank in the

growth and development of MSME sector.

Chapter two presents the review of related studies on development financial

institutions, entrepreneurship and micro, small and medium enterprises (MSMEs).

Chapter three presents the research methodology applied in the study. It

outlines the need, scope, objectives, selection of sample, data collection methods,

tools of analysis and limitations of the study.

Chapter four studied the growth of the bank in terms of branch expansion,

manpower, net worth, deposits, borrowings, investments, loans and advances and total

assets.

Chapter five outlines the various direct and indirect credit schemes of SIDBI

for financing of entrepreneurs. This chapter also examined the various promotional

and developmental activities of SIDBI namely MEPPs, EDPs, SIMAPs and STUPs.

Chapter six analyses the financial performance of the bank on the basis of

accounting ratios and productivity ratios.

Chapter seven includes a comprehensive study of perception of entrepreneurs

regarding functioning of SIDBI on the basis of questionnaire.

Chapter eight presents the summary and conclusions based on the previous

chapters and made suggestions for improving the services and performance of the

bank.

Page 20

20

REFERENCES

Akhtar, S.M. Jawed; and Alam, Md. Shabbir (2011), “Banking System in India-

Reforms and Performance Evaluation”, New Century Publications, New

Delhi.

Annual Reports of Small Industries Development Bank of India, 1990-91 to 2012-13.

Chatterjee, Anup; and Jetli, K. Narinder (2009), “Industry and Infrastructure

Development in India since 1947”, New Century Publications, New Delhi,

pp. 79 & 80.

Choudhary, A.K. (1998), “Bank Management”, Rajat Publications, Delhi.

Debasish, Sathya Swaroop; and Mishra Bishnupriya (2005), “Indian Banking System

Development Performance and Services”, Mahamaya Publishing House, New

Delhi.

Desai, Vasant (2011), “The Indian Financial System and Development,” Himalaya

Publishing House, Mumbai, pp. 9 & 542.

Gomez, Clifford (2010), “Financial Markets, Institutions and Financial Services,”

PHI Learning Private Limited, New Delhi, p.11.

Gupta, N.K.; and Chopra, Monika (2008), “Financial Markets, Institutions and

Services”, Ane Books India, New Delhi, pp. 3-6.

Kohn, Meir (2003), “Financial Institutions and Markets”, Tata McGraw Hill

Publishing Company Limited, New Delhi.

Mathur, B.L; Yadav, J.P.; Mathur, Sunita; Vyas, Bhunesh; and Mishra, A.K. (2005),

“Banking and Finance,” RBSA Publishers, Jaipur, pp.79 & 93.

MSME (Micro, Small & Medium Enterprises) Annual Report 2010-11, 2011-12,

2012-13.

Pathak, Bharti V. (2009), “The Indian Financial System-Markets, Institutions and

Services,” Dorling Kindersley (India) Pvt. Ltd., Delhi, p. 425.

Page 21

21

Reserve Bank of India, “Report on Trend and Progress of Banking in India 2012-13”,

p. 118.

Rohtagi, Anshu. (2007), “Banking Development and Financial Management”, Cyber

Tech Publications, New Delhi, pp. 200 & 212.

SIDBI Annual Report 2011-12, p. vi.

SIDBI Annual Report 2012-13, pp. 23, 38 and 40.

Sharma, K.C. (2007), “Modern Banking in India”, Deep and Deep Publications Pvt.

Ltd., New Delhi.

Srivastava, R.M.; and Nigam, Divya (2008), “Management of Indian Financial

Institutions”, Himalaya Publishing House, Mumbai, p. 480.

Uppal, R.K.; and Kaur, Rimpy (2007), “Banking in the New Millennium-Issues,

Challenges and Strategies”, Mahamaya Publishing House, New Delhi.