50

Introduction to Financial Services Vinil Gupta

| Date post: | 17-Jan-2017 |

| Category: |

Documents |

| Upload: | vinil-gupta |

| View: | 198 times |

| Download: | 0 times |

Introduction to Financial Services

Vinil Gupta

Debt ‘Merry-go-Round’

Players for Financial Industry

Lender Intermediaries Market Borrower

Individuals Banks Interbank Individuals

Companies Insurance Companies Stock Exchange Companies

Pension Funds Money Market Central Government

Mutual Funds Bond Market Municipalities

Public Corporations

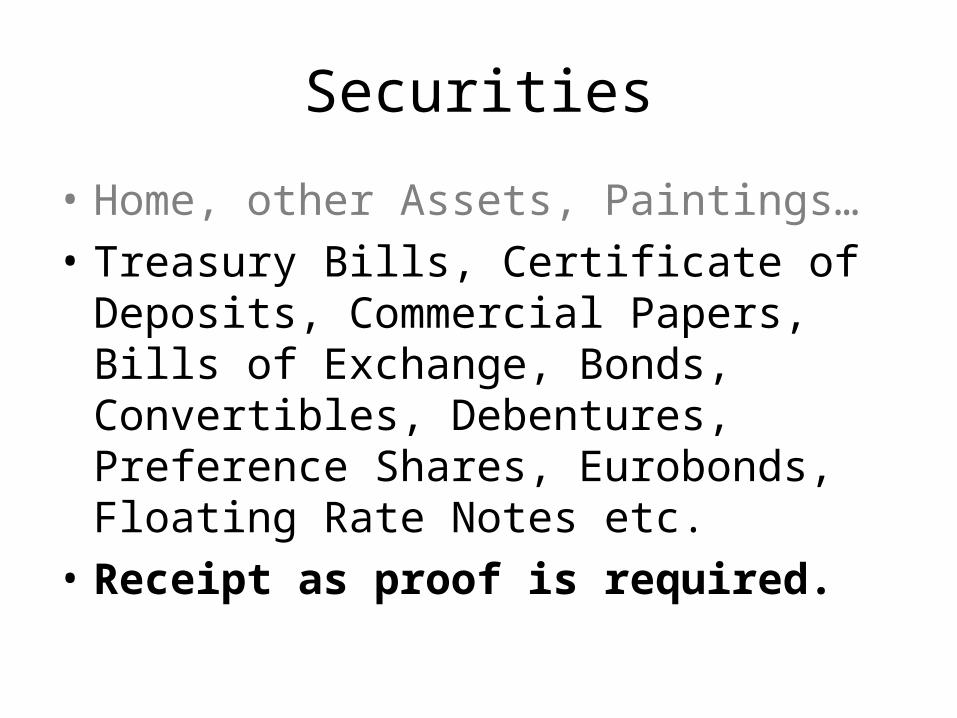

Securities

• Home, other Assets, Paintings…• Treasury Bills, Certificate of Deposits,

Commercial Papers, Bills of Exchange, Bonds, Convertibles, Debentures, Preference Shares, Eurobonds, Floating Rate Notes etc.

• Receipt as proof is required.

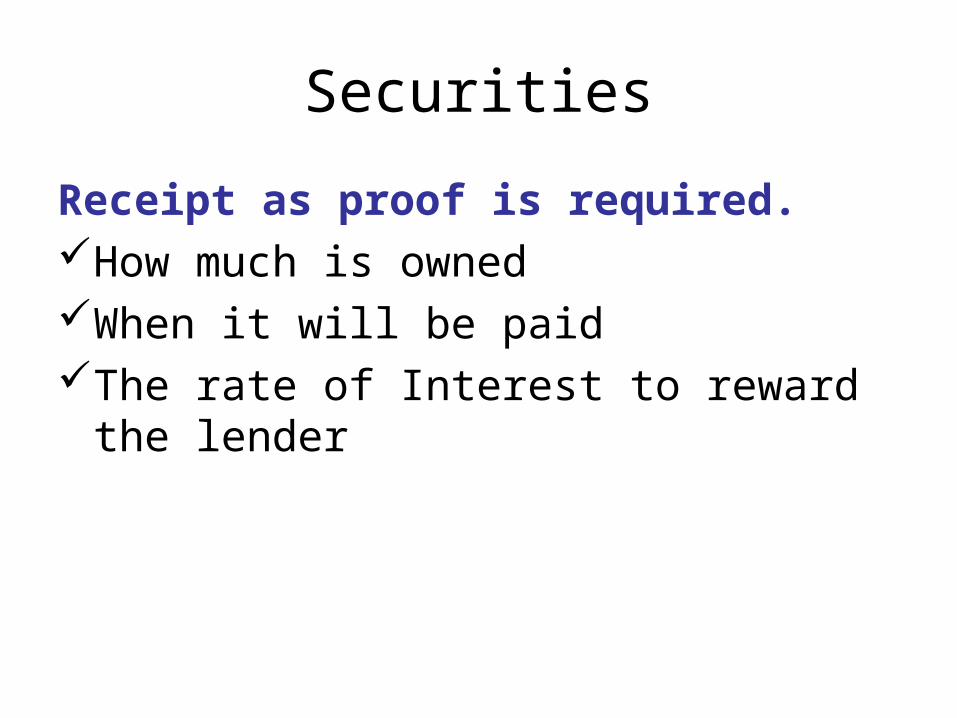

Securities

Receipt as proof is required. How much is ownedWhen it will be paidThe rate of Interest to reward the lender

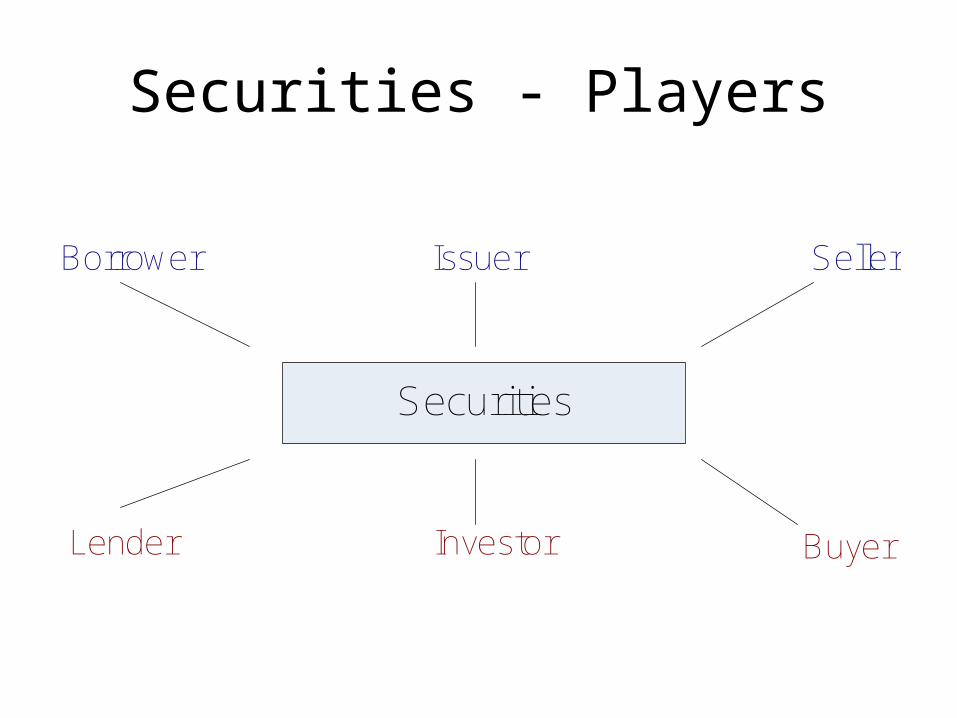

Securities - Players

Securities

Borrower Issuer Seller

Lender Investor Buyer

Very Large Orders

SyndicatesBanks create a syndicate for large loansInsurance companies create syndicate for

large insurance i.e. say GBP(£) 1Billion insurance cover.

1. Interest Rates

Fixed Rate Floating Rate

Let’s say 8% per annum

Let’s say LIBOR + 1.5 % per annum

Shares (Equity) ShareholderShare - Piece of the pie.

Bank Loans

• Bank needs to insure Loan + Interest will be repaid timely.

• Does Borrower own Assets?• Assess: How risky is the loan?• More Risk More Interest required.

Company Needs MoneyCapital Need of Company

Equity Bonds Bank Loan

Reward: Dividends Fixed Interest Variable Interest

• Part owner, hence no end date loan• Risk: Value can go up or down

• Money to be paid back with interest – Set dates• Strict rules for obligations

• Money to be paid back with interest – Set dates

Note: Equity is exception in the merry-go-round, it is not debt

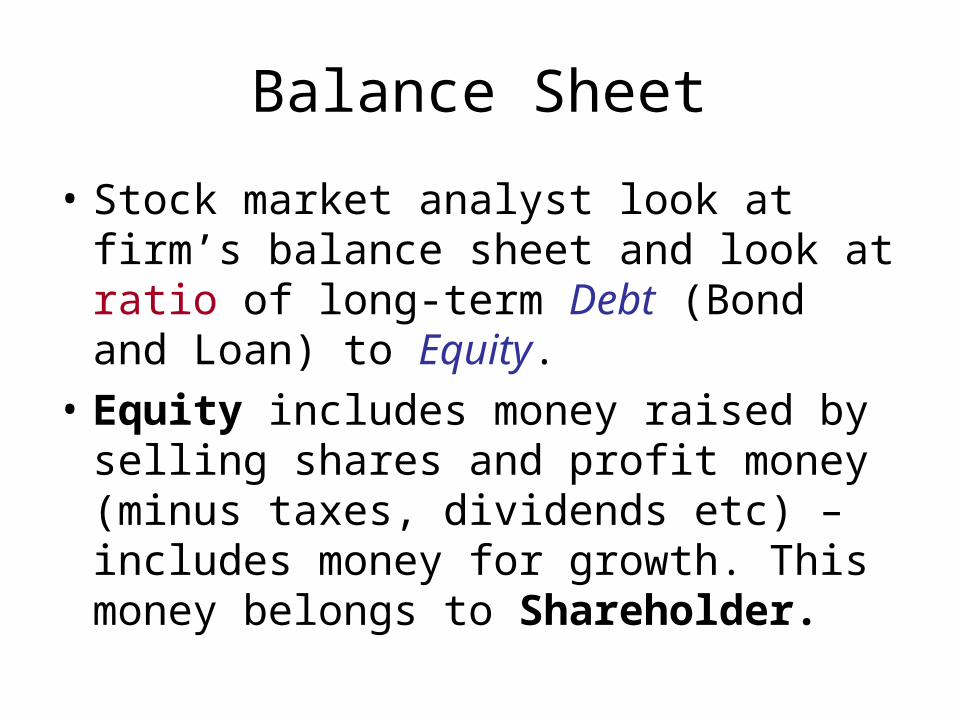

Balance Sheet

• Stock market analyst look at firm’s balance sheet and look at ratio of long-term Debt (Bond and Loan) to Equity.

• Equity includes money raised by selling shares and profit money (minus taxes, dividends etc) – includes money for growth. This money belongs to Shareholder.

Shareholder’s fund

Money belonging to shareholder

Shareholder’s fund = Rights Issues + Retained Profits + Original

Equity

Banking Supervision

Who is in charge of the bank? Answer: ‘The Central Bank’ of respective

countries or some separate authority and decides on rules.Condition of entryCapital RatioLiquidity RulesForeign Exchange controlRights of Inspection

Type of Banks

• Central Banks• Commercial Banks (Retail and Wholesale Banks)

• Investment (or Merchant) Banks• Savings Banks• Cooperative Banks• Mortgage Banks• Giro Banks and National Savings Banks

Central Banks

• An economy will have a central bank.• Reserve Bank of India (RBI)

Commercial Banks

• Retail Bank (incl. Private Banking) – High street branches, dealing with general public, small businesses. Cheque clearing, high volume, low value.

• Wholesale Bank – Low volume, high value. Dealing with other banks, central bank, corporate, pension funds, and other investment institutions. – electronic settlement – CHIPS, CHAPS, BACS, SEPA etc.

Private Banking

• High net worth individuals• Deposits, loans, fund management,

investment advice etc.• Switzerland specialisation originally

Investment (Merchant USA) Banks

• Commercial banking is about Lending money.

• Merchant banking is ‘helping people to find the money’

• Raising Capital - bank loans, bond issue or equity.

Savings Banks

• In modern world they are looking more and more like ordinary commercial banks, due to mergers, deregulation.

Co-operative Banks

• These are owned by the members and with maximum profit not necessarily the main objective – they may aim to give low cost loans to members.

Mortgage Banks

• Building Societies

Giro Banks (1 of 2)

• Giro – Greek ‘Guros’, meaning a wheel or circle. The circle in finance is the passing round of payment between counterparties.

• Debt circle A owes B owes C owes D owes A owes.

• The bankers setup a clearing system – the giro of ledger entries.

Giro Banks (2 of 2)

Modern days uses: (i) Individual sends a giro slip to their bank

instructing them to pay a sum of money to electricity or water supply.

(ii) Giro Bank and use of Post Office for those who do not have bank accounts pay their bills to GB/PO and GB/PO forward payment to the utility firms.

Other Banking Terminologies

• Clearing Banks – Clearing cheques – large volumes.

• Cheques drawn in favour of other banks are sent to a central clearing system where they can be gathered together and sent to each bank for posting to individual accounts.

• State or public banks – • International banking -

Bank’s Balance Sheet

First a few terms that will be discussed later:√ Creation of Credit√ Liquidity√ Capital Ratio

Other terms: Asset Liability

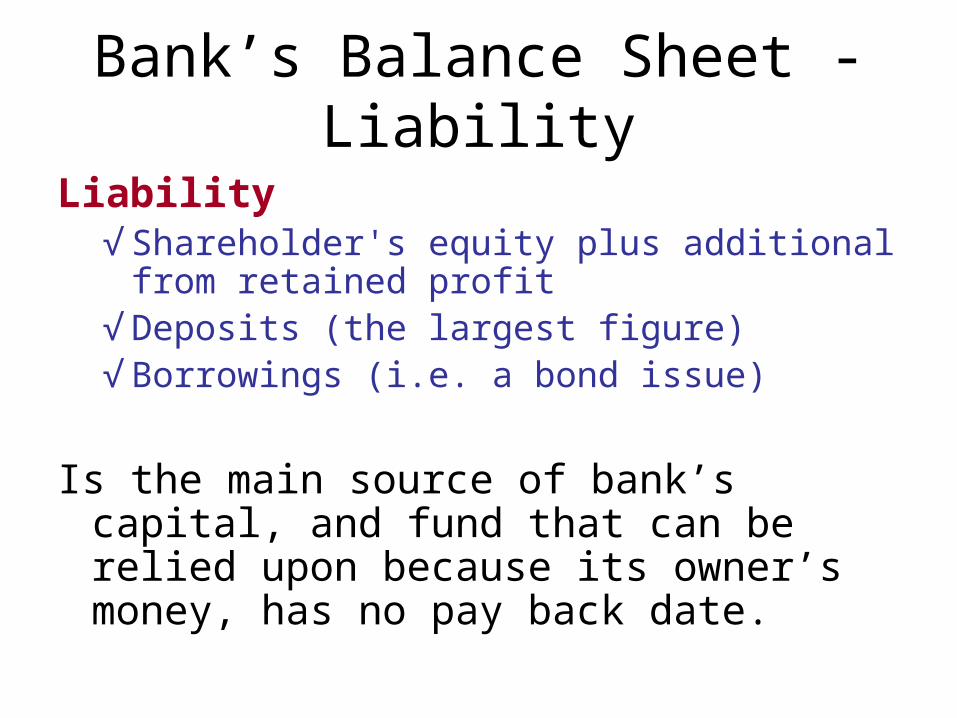

Bank’s Balance Sheet - Liability

Liability • Liability in accounting does not mean

‘disadvantage’. It is money for which the entity concerned is liable. If money is borrowed, the borrower is liable to repay it, hence liability.

• Liabilities are claims against the bank

Bank’s Balance Sheet - Liability

Liability √ Shareholder's equity plus additional from

retained profit√ Deposits (the largest figure)√ Borrowings (i.e. a bond issue)

Is the main source of bank’s capital, and fund that can be relied upon because its owner’s money, has no pay back date.

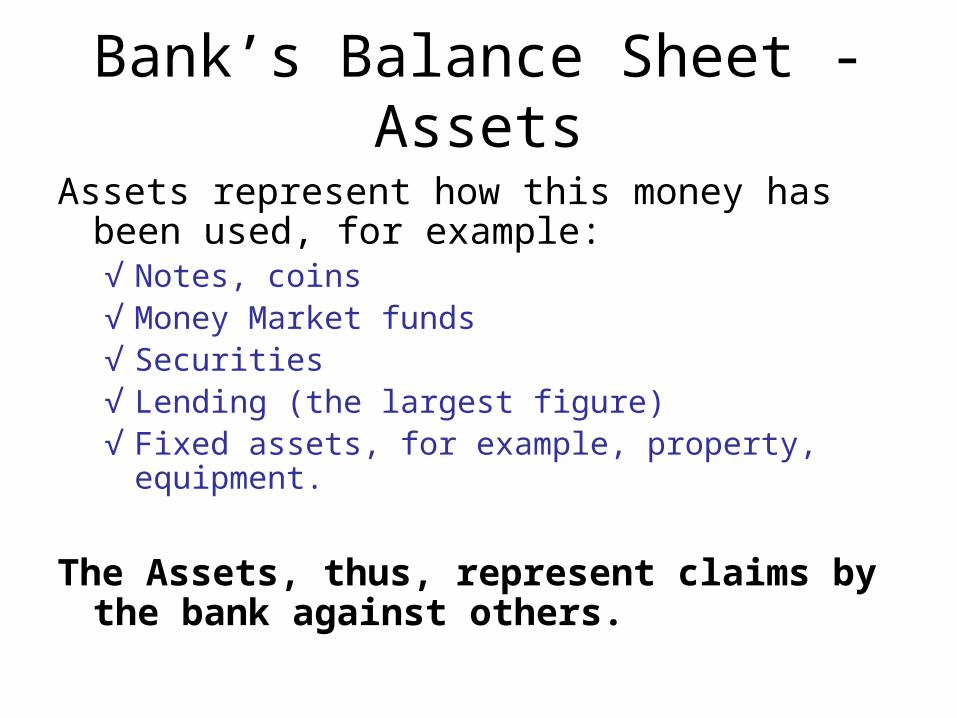

Bank’s Balance Sheet - AssetsAssets represent how this money has been used,

for example: √ Notes, coins√ Money Market funds√ Securities√ Lending (the largest figure)√ Fixed assets, for example, property, equipment.

The Assets, thus, represent claims by the bank against others.

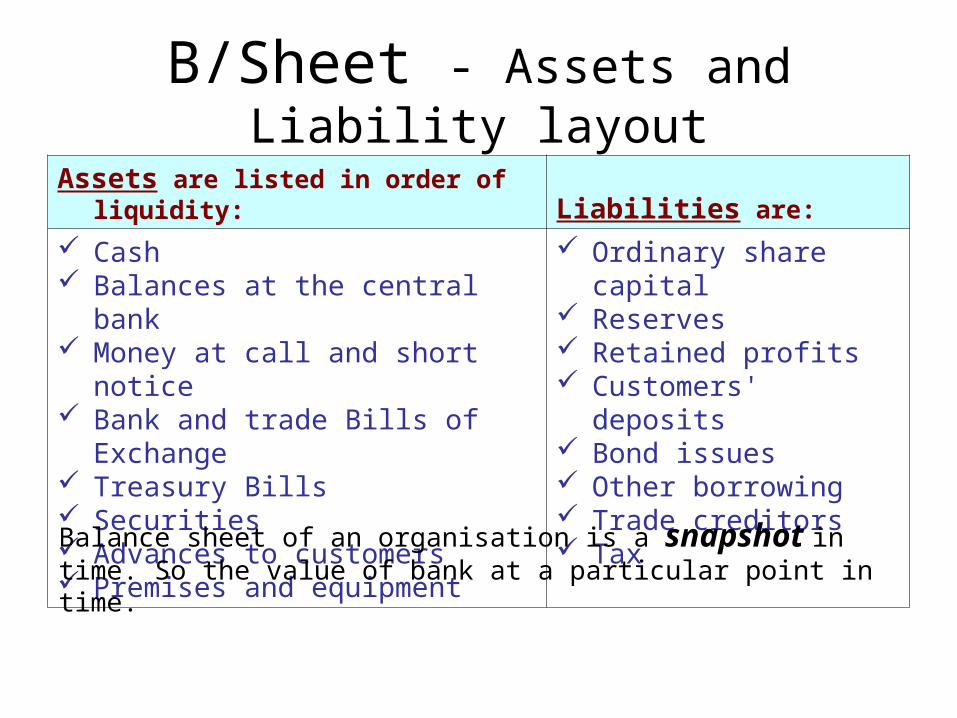

B/Sheet - Assets and Liability layoutAssets are listed in order of liquidity: Liabilities are: Cash Balances at the central bank Money at call and short notice Bank and trade Bills of Exchange Treasury Bills Securities Advances to customers Premises and equipment

Ordinary share capital Reserves Retained profits Customers' deposits Bond issues Other borrowing Trade creditors Tax

Balance sheet of an organisation is a snapshot in time. So the value of bank at a particular point in time.

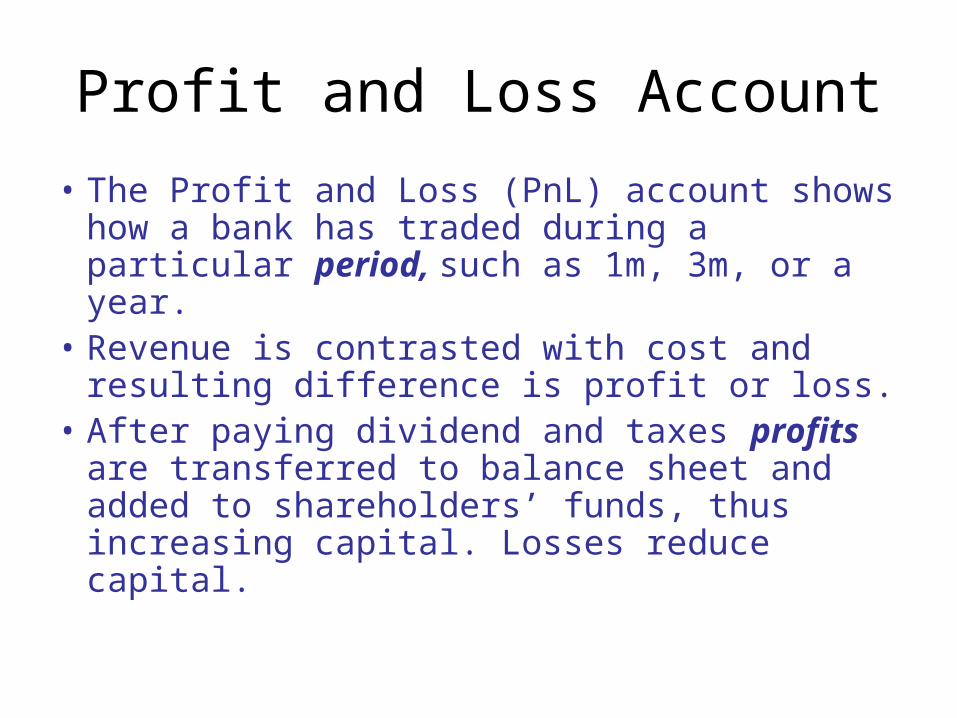

Profit and Loss Account

• The Profit and Loss (PnL) account shows how a bank has traded during a particular period, such as 1m, 3m, or a year.

• Revenue is contrasted with cost and resulting difference is profit or loss.

• After paying dividend and taxes profits are transferred to balance sheet and added to shareholders’ funds, thus increasing capital. Losses reduce capital.

Creation of Credit

• Banks have surplus credit cash from deposits and therefore facility to create credit.

• For example, bank gives you overdraft facility of say £2K and you purchase goods with it. Banks has created £2K expenditure that did not exist.

• Supplier of £2K goods now has £2K disposable money.

Creation of Credit

• Where did £2K come from?• Not from you because you did not have it. • It came from bank that allowed you the

overdraft of £2K – bank has created money.

• Bank lending = spending and excessive spending may mean unacceptable inflation and imports the nation can’t afford.

Creation of Credit

• Remember banking depends on confidence• Govt. and central bank will want to control it in

view of implication for inflation and imports.• Banks will need internal controls called

‘Liquidity Ratio’• An external control enforced by bank supervisor

called ‘Capital Ratio’ is required.

Banking Depends on Confidence

• Govt and central bank will want to control credit and measure ‘Money Supply’. This figure is a measure of bank deposits as being best guide to bank lending.

Central Bank - Controls

Central bank has number of weapons.• Raising mandatory reserves – to CB• Raising Interest Rates• General ‘Open market operations’ i.e.

selling more government papers than it needs to in order to drain credit and keep monitory conditions tight. Not lending money to banks quickly.

Liquidity Ratios

• Liquidity Ratio is controlled internally by banks and regulators.

• What percentage of Cash, short notice, short-term securities (T-bills, Bills of Exchange) and so on.

Capital Ratio

• Capital Ration is the external control imposed by bank supervisors in the interest of prudence.

• Banks take money from depositors and lend money, some borrowers default.

• The buffer, the money the bank can rely on is its capital. Thus there should be prudent relationship between capital and lending – this is Capital Ratio.

Capital Ratio - RWA

• Not all assets are same, so assets are given weighting.

Central Bank Activities• Supervision of the banking system• Advise the government on monetary policy• Issue bank notes• Acting as banker to the other banks• Acting as banker to the government• Raising money for the government• Controlling the nation’s currency reserves• Acting as ‘lender of last resort’ • Liaison with international bodies

Bank Lending

• Overdraft – Bank’s base rate + margin, arrangements may be renewable.

• Line of Credit – borrow up to a given amount.

• Bankers acceptance – Accept ‘bills of exchange’. The best bill are bank or eligible bills. Recognised top quality by central bank.

Bank Lending

• Eligible bills are eligible for sale to the central bank list.

• Ineligible bills – bills signed by traders and therefore called Trade-Bills. Sometimes traders are more creditworthy than some Banks, nevertheless Central Bank will not rediscount them.

Committed Facilities

Loan facilities are typically for one or more years. There are three main types, plus a special case – Project Finance.

• Term Loans – typically 5y to 7y. Loan is amortised (borrower pays back in stages), sometimes in ‘bullet’ payment. Floating IR.

• Standby Credit – Loan can be drawn down in stages. Repaid money can not be re-borrowed.

Committed Facilities

• Revolving Credit – loans can be drawn in tranches, repaid fund can be reused. Generally unsecured loans.

• Project Finance – is special case of Term Loan – projects are typically for longer durations –require complex time consuming loan agreements

Investment Banking

• Accepting• Corporate Finance• Securities Trading• Investment Management• Loan Arrangement• Foreign Exchnage

Investment Bank - Accepting

02 November 2011

You own me £100,000 for goods received. Please pay on 2 February 2012

Signed: A.N. Exporter

Yes, I agree.Signed: A.N. Importer

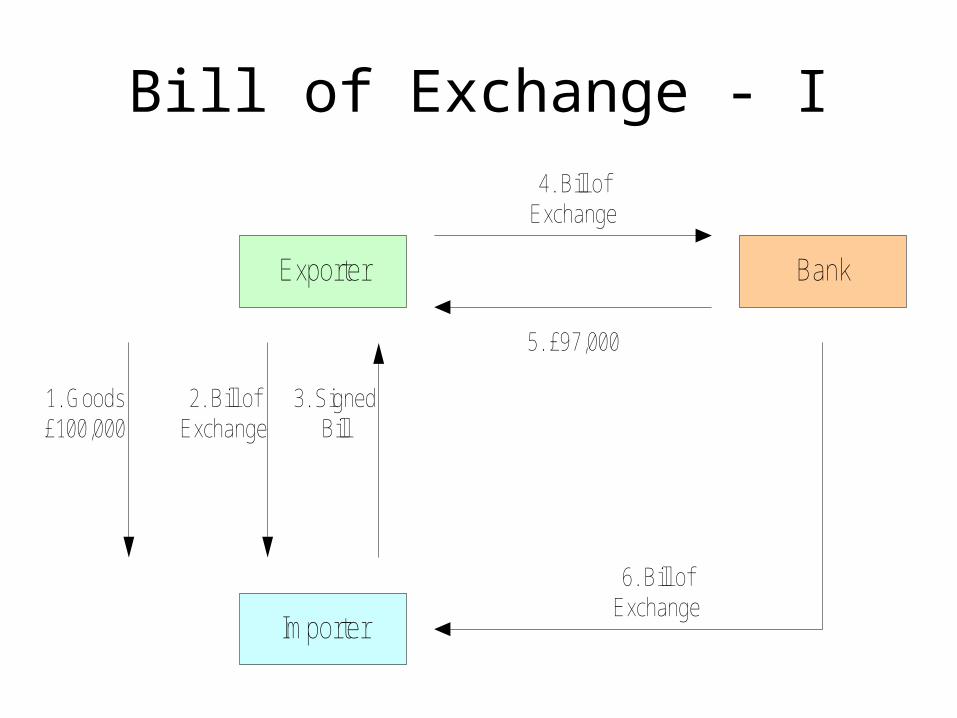

Bill of Exchange - I

Exporter Bank

Importer

1. Goods£100,000

2. Bill ofExchange

3. SignedBill

4. Bill of Exchange

5. £97,000

6. Bill of Exchange

Bill of Exchange – I Notes

1. Exporter ships goods worth £100,000 to importer2. Exporter asks importer to sign the Bill of Exchange

(BoE), undertaking to pay £100,000 in, say three months.

3. Importer signs the bill and returns it.4. Exporter presents the bill to a bank and asks them to

‘discount’ it.5. The bank discounts the bill for say, £97,000.6. Three months later, the bank presents the bill to the

importer for payment.Problem: How credit worthy is Importer?

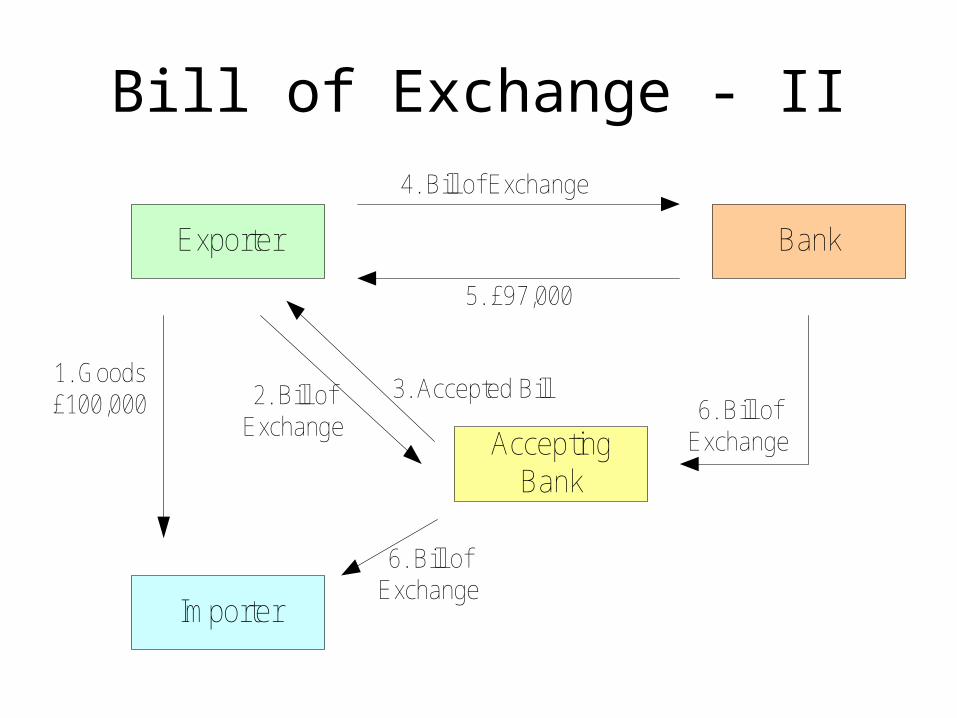

Bill of Exchange - II

Exporter Bank

Importer

1. Goods£100,000 2. Bill of

Exchange3. Accepted Bill

4. Bill of Exchange

5. £97,000

6. Bill of ExchangeAccepting

Bank

6. Bill of Exchange

Bill of Exchange – II Notes

1. Exporter ships goods worth £100,000 to importer2. Exporter asks a bank to ‘accept’ the bill, undertaking to pay

£100,000 in three months.3. The bank accepts the bill and returns it. 4. Exporter presents the bill to a bank and asks them to ‘discount’ it.5. The bank discounts the bill for say, £97,000.6. Three months later, the bank presents the bill to the accepting bank

for payment of £100,000. The latter will recoup this from the importer, or the importer’s bank.

N.B. √ A bill signed by a trader is a Trader Bill.√ A bill accepted by a bank recognised for this purpose by Central

Bank is a Bank Bill or Eligible Bill.√ The Central Bank will itself discount the bill as part of its ‘lender of

last resort’ role.