75

INTRODUCTION TO UPSTREAM OIL CONTRACTS AND TAXATION Organización Latinoamericana de Energía October 2010

INTRODUCTION TO UPSTREAM OIL CONTRACTS AND TAXATION

Organización Latinoamericana de Energía

October 2010

Agenda

Day 1 : Oil and Gas Supply, Demand and Pricing

Day 2 : Petroleum Law, Mineral Rights andRegulations

Day 3 : Concessions and Production SharingContracts

Day 4: Petroleum Taxation

Day 5: Case Study

Day 6 : Review and Discussion of Main Themesand Concepts

Day 1

Oil and Gas Supply, Demand and

Pricing

World Crude Oil Production80 million bopd

Crude Oil

Production

fell by 2.5

million bopd

in 2009

Saudi Arabia

reduced by

1.1 million

bopd

Bp Statistical Review 2009

Crude Oil Reserves to Production Ratio by Regions

Bp Statistical Review 2009

Oil Product Consumption

Bp Statistical Review 2009

Major Oil Trade Flows 2009

Bp Statistical Review 2009

Historical Oil Prices 1978 to 2010

Crude Oil Prices 2009 to 2010

Crude Oil ProductionLatin American Countries

2009 2008

Argentina 473 -5.7% 0.6%

Brazil 2405 -0.2% 2.7%

Chile 333 -7.5% 0.4%

Colombia 194 -2.7% 0.2%

Ecuador 216 5.2% 0.3%

Peru 188 8.8% 0.2%

Venezuela 609 0.9% 0.7%

Other S. & Cent. America 1235 -0.8% 1.5%

Total S. & Cent. America 5653 -0.01 0.07

Percentage of

World Production

Percentage

Change from

Natural Gas Production by Regions

Natural Gas Reserves and R/P Ratios by Regions

Natural Gas Consumption by Regions

World Natural Gas Trade Flows

Natural Gas Prices Historical and 2009 - 2010

Crude Oil Pricing

• Prices based on supply and demand. Equilibrium occurs where the supply and demand curves intersect. The short-term equilibrium price is the market price.

• Term Contracts – 1 year period based on a hubprice

• Futures Contracts – Tradeable contracts

Crude Oil Pricing

• Transport Differentials are based on the distance of the crude oil from the eventual market e.g. tanker shipping costs called freight, insurance, duties etc

• Quality Differential based on the API, metal content, acidity

• Sulphur Discount – reduced price based on the % of sulphur in the crude oil

Transportation is

the biggest user

Industry is the

second major

user

Main Conclusions

• Fossil fuels, oil and gas will continue to be the main energy source for the next 50 years

• The majority of oil and gas reserves belong to the National Oil Companies

• Crude oil price is excellent when compared to natural gas prices on an energy equivalent basis

• Costs and expenses in upstream operations have tripled over the last 5 years

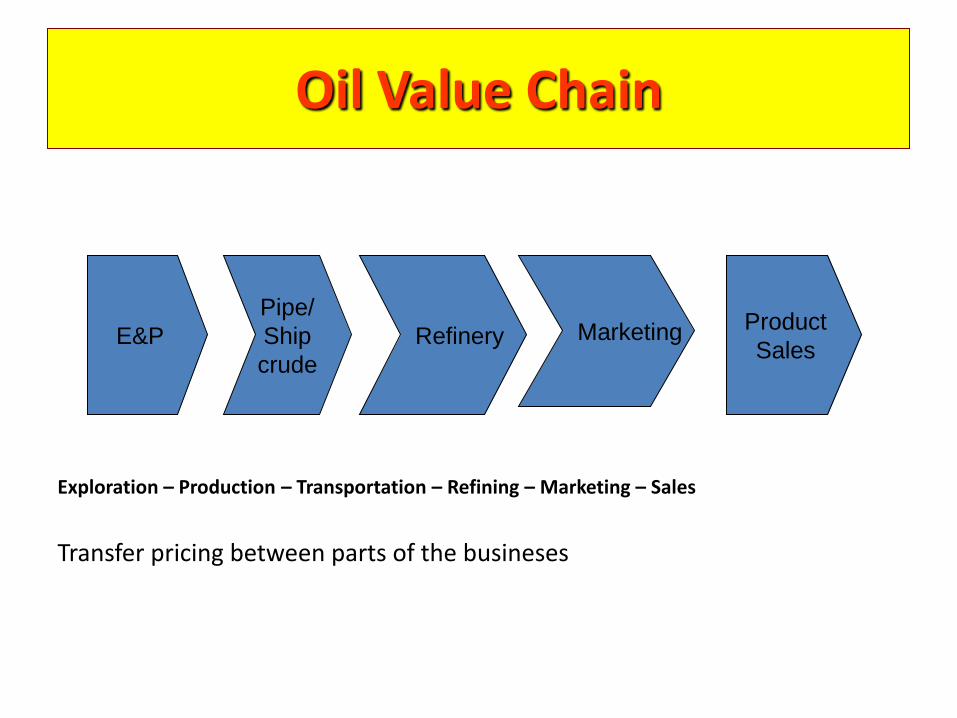

Crude Oil Value Chain

• Integrated oil and Gas Companies

• Horizontally Integrated companies –Independents

Oil Value Chain

Exploration – Production – Transportation – Refining – Marketing – Sales

Transfer pricing between parts of the busineses

E&P

Pipe/

Ship

crude

RefineryProduct

SalesMarketing

Oil versus a Gas regime (Equivalence Factor 6:1 )

Difference : Method of Extraction Method of Storage

Method of Transportation ( LNG Tankers, CNG Tankers)

Value Chain Oil or Gas Regime

Life History of Oil and Gas Fields

Marketing the

Prospects

Taxes

Understanding the Business Environment, theCapital market and the environment

Oil Price US$70/BBl ( Not US$147/BBl but good)Strong Gas PriceStrong Increase in DemandConflicts Globally reducing Access

( Iran, Iraq, Nigeria, Russia pipeline)Emerging Markets competing with United States and Developed Euro States

for scarce hydrocarbon resourcesBRIC – Large Economies ( China, India, Japan)

- Smaller Economies ( indonesia, Phillipine,, etc.)

Global WarmingA consequence

Renewable Energy – A Desire, but;the US produces most wind turbine power ( still small)

US failed to renew US$1. /gal Tax Credit on BiofuelsIndia imports 90% of oil @US$90 b annually

The Status Quo- A Financial Reality due to:Constraints - Technology to make substitute cheaper

Gov’t Policy backed by LegislationIndividual AttitudesA new invention to replace the internal combustion Engine

Exxon Mobil predicts demand in 2030 to be 35% higher than 2005 levels

In Considering Taxation, Regulations and Legislations, both the host country and the investor must ensuring

A Competitive Advantage( on both sides)

Some of these are:Addressing Sustainability Issues - ( air, water , soil)

standards of environmental stewardship and social responsible performanceComplying with regulatory and reporting requirements

variety of reporting landscapes, each gov’t – individual policies, oil and gas regimeaccounting proceedures, revenue recognition, intangibles

Improving Performance and Operational efficiencyFinancial, Governance, Risk, Compliance

Industry Transactions and ConsolidationTax strategy and Structured Services

Managing Financial Risk(Evaluating the market, Risk identification)

Managing Geopolitical Risk( to enhance cross border expansion)

Recruiting and Retaining Skilled WorkforceSaving the Supply

( harder to exploit deeper waters, pipeline security, the environment)

A Commercial Perspective

Question: What do you replace this type of capital market with ?

837 Energy related deals announced in 2009 of which 72% were upstream ,down by 24% from previous year. But the value was US$198 Billion up 10%

of the previous year value

In terms of Mergers and Acquisitions. America most active - 65% Private :

Exxon Mobil acquire XTO - US$41BSuncor acquire PetroCanada US$21B

Public:Asian National Oil Companies – supporting domestic growth

Sinopec US$9B - Swiss Oil Co. AddaxKNOC US$9 B - Harvest Energy TrustPetro China US$1.7B - Canada Oil Sands

Answer : Nothing

Readings for Next Day Presentation

Pedro Van Muers Powerpoint

Sample PSC and E& P Licence

Trinidad Legislations

Questions

Which Olade Member Country , having discovered hydrocarbon reserves

in large Commercial quantities can stand alone to develop these

And why ?

End of Day 1

Send question on today’s lectures for clarification via email prior to

next session

Day 2

Objective :

Defining the types of Legislation and Regulations

that are required to administrate a win-win arrangement

for both parties, the foreign investor using the host

country natural

resources.

Day 2Mineral Rights, Petroleum Law

and Regulations

Constitution

Country Laws

Petroleum Laws and Regulations

State Oil Companies

Petroleum

Contracts

The Legal Process

Mineral Rights and Royalty

Mineral Rights

• Individual persons as well as the State own mineral rights in T&T

• Private Oil Mining Rights

• State Oil Mining Rights

• Alienated Lands occur when the sub-surface is in-accessible due to surface occupation

• Freehold Lands are lands owned by the company including the oil rights

Mineral Rights

• An oil-mining lease or a licence is both a conveyance and a contract

– It conveys the mineral rights to the leasee for the consideration of a royalty, and

– It contains such terms and conditions for the operations

SOML – “petroleum in strata” belongs to the State

Concepts of “won and saved” and “quietly hold and enjoy”

Law of Capture

• Ownership is derived from the act of winning the mineral, even though it may come from another lease

• Oil and Gas are fluids and can cross a boundary line

• Concept of pooling and unitisation

Petroleum Laws

• Usually, the constitution of a country states that minerals found in that country belongs to the State

• Oil and gas law is usually separated from other laws in a country because of its importance

• The Petroleum Law will state which member of government usually the minister of energy or petroleum will be responsible for all mattersrelating to petroleum

• There will also be some alignment to competitive bidding for the mineral rights of blocks in respect of petroleum

Petroleum Laws

• Types of licences to be granted by the State

• Exploration rights and production term

• Defaults and Disputes

• Confidentiality

• Financial obligations of Licensee– Payment of royalties, surface rentals, impost,

import duties

– Payment of income tax, corporation tax, excise duties, charges and fees etc

Petroleum Regulations

• Defines types of licences to be granted by the State e.g. exploration, exploration & production, refining, liquefaction of natural gas, pipeline and transportation, marketing, petrochemical or compressed natural gas licence

• Operator’s rights

• Fiscalisation procedures

• Oil tanks regulations

Petroleum Contractual Systems

PETROLEUM CONTRACTUAL

SYSTEMS

Concessionary Contractual

E&P

Licence

PSC ServiceConcession

Concessions

• Large areas, even entire countries e.g. Iran and Iraq

• Minimal Royalty

• Strong dependence on the international oil companies

• Used in the early 1900s as an early form of contract

E&P Licences

• Competitive Bidding

• Exploration Term of 6 years divided into two 3-year phases

• Production Term of 25 years upon successful completion of the Minimum Work Programme

• Payment of Royalty to the Mineral Rights Owner

• Payment of Taxes, Levies, Subsidies and abide by all the country’s laws

Production Sharing Contracts

• Two types of PSCs– Contains a Cost recovery feature (Indonesian Model)

– Does not contain a Cost recovery feature (Peruvian Model)

• Based on a sharing of production basis where the multi-national oil company works as a contractor for the State

• The Contractor does not own any oil or gas up to the Sales Point; in this way, governments exert direct control over its resources

Service Contracts

• The Multi-national Company works as a service contractor in the aspects of exploration, development and production of oil and gas

• Contractor receives a fee per barrel for the performance of his work

Typical features of Licences and PSCs

• Bonuses

– Signature Bonus payable via bidding;

– Production Bonus payable upon reaching a set production target, bopd

• Work Obligations

– Seismic acquisition

– Drill exploration and appraisal wells to target depths

• Surrender Obligations

– Relinquish rights over 50% to 25% of initial area

– Remain with only producing field areas

• Financial Commitments and Guarantees

• Ownership and title of produced oil and gas

• Control of Operations

E&P Licences

Royalty

• Royalty is a share of the production paid to the owner of the mineral rights for the conveyancing.

• The royalty owner can be a person or the State

• Values can vary between 5% to 15% of the gross production. The usual value is 10% oil royalty.

• Can be “taken in kind” i.e. taken in the actual liquid form for refining and distribution or in “equivalent cash” based upon agreed pricing parameters

• The Royalty transfer point is usually at the fiscalisationpoint where the crude oil or natural gas is measured.

Royalty

• Sliding Scale Rates are used whenever there is a change in profitability due to lower production rates. For example– 50 bopd 3% oil royalty

– 100 bopd 5% oil royalty

– 200 bopd 75 oil royalty

• Fiscalisation Point is where the mineral owner accepts his share of the crude oil or natural gas

• Natural Gas royalty rates have been very low in old E&P Licences, TT1.5 cents/mcf

E&P Licences

• Surrender Obligation – 50% of the original area by year 3 and 25% of the original area by year 5. Licensee to keep only the discovered and producing fields including a 0.5 kilometre halo around same

• Commerciality and Development Plan

• Signature Bonus, Production Bonus, administrative Fees

Production Sharing Contract

• PSC may contain Royalty or not

• Cost Recovery runs from 40 to 80% of the costs and expenses incurred in the exploration, development and production of petroleum

• Cost Recovery is very important since it determines how fast the contractor can recover the investments

• The remaining oil volume is known as Profit Oil and is shared between the State and the contractor on a production rate basis

• .

Work Commitments

• Acquire 2000 sq km of 3D seismic data

• Drill 2 exploration wells before the end of Year 3

• Drill 1 exploration well by year 4

Readings for Next Day Presentation

World Bank Working Papers 123 & 179

International Petroleum Taxation paper

Questions

Are more internal factors or external factors influencing legislations and

Regulations. Are the investors a significant determinant. Why ?

End of Day 2

Information for Clarification

Day 3

Day 3Objective: Analysing the elements of Production Sharing Contracts ( PSC),

Exploration and Production Licence and their ancillary sub-contracts

Case Study : ( Aim) The evolution of a small developing country administrating its

upstream hydrocarbon interest, ensuring these interest are protected and

That the concept of “rent” due to ownership and “ Title” to the natural

resource is not eroded.

54

Main Concerns with 2003 PSC

• Arrangement for payment of taxes• Gross-up provision

• Coverage of taxes by Minister’s share

• Perceived freezing of taxation system• Government control over future changes

• Project risk to company

• Collection of Government take• Board of Inland Revenue

• Ministry of Energy and Energy Industries

Contracts Case Study : Trinidad and Tobago

55

Ownership & Control of Resources

• PSC

– State retains majority ownership

• Up to 80%

– Government approval required to export gas

• E&P Licence

– Title transferred to licensee

• State entitlement based only on royalty ‘in kind’ – 0 to 15%

– Operator has right to export

Contracts

56

Protection of Government Revenues

• PSC

– Ring Fencing

• No consolidation of profit and loss across contract areas

• Exploration risk solely with contractor

• Equitable basis for evaluation

• E&P– No Ring Fencing

• Consolidation of profit and loss

• Government assumes at least 55% of exploration risks

• Funded by taxable profits of existing operations in T&T

Contracts

57

Flexibility of Agreement

• PSC

– Flexible

• May reflect prevailing circumstances

• Fiscal – Varies with hydrocarbon

potential

• Relinquishment– Phased

– Early

– Variable percentage

• E&P

– Rigid

• Legally unyielding requiring Legal Order or legislative changes

• Fiscal– Standard tax regime

• Relinquishment provision fixed

– Fifty percent (50%) by 6th year

Contracts

58

Cost control

• PSC– Government

approval• Budgets

• Cost verification

• Expenditure

– Quarterly reporting • Statement of

expenditure

• Recoverable cost

• Revenue

– Quarterly audits

• E&P

– No Government approval required

– Ad Hoc cost reporting

• Not specified in licence

– Time-lag in cost verification for Tax Audit reconciliation

• up to 6 yrs after spend

Contracts

59

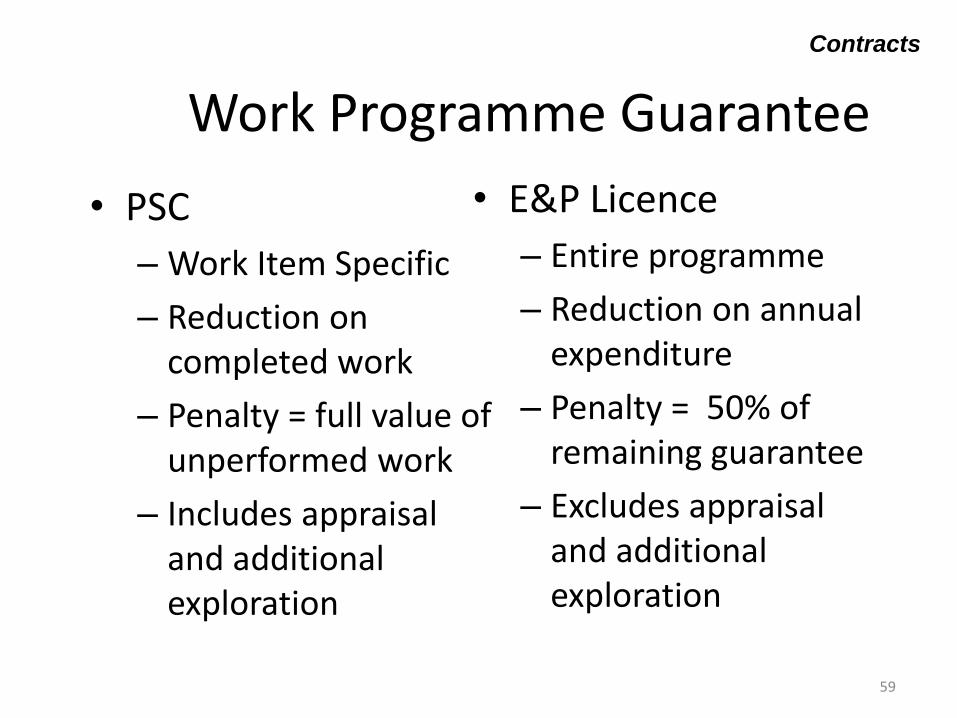

Work Programme Guarantee

• PSC

– Work Item Specific

– Reduction on completed work

– Penalty = full value of unperformed work

– Includes appraisal and additional exploration

• E&P Licence

– Entire programme

– Reduction on annual expenditure

– Penalty = 50% of remaining guarantee

– Excludes appraisal and additional exploration

Contracts

60

Key Advantages of PSC vs. E&P Licence

• Ownership & Control of Resources

• Protection of Government Revenues

• Flexibility of Agreement

• Cost Control

• Efficacy of guarantees

Contracts Case Study : Trinidad and Tobago

61

Production Sharing Contract

( Advantages to Gov’t)

Title to Resources

Protection of revenue flow (Ringfencing)

Flexibility of agreement

Cost Control

Efficacy of Guarantees

Contracts

Readings for Next Day Presentation

World Bank Working Papers 123 & 179

International Petroleum Taxation paper

Project – Excel Spreadsheet

Using fictitious numbers, provide a spreadsheet, showing by months, your

monthly salary, an extra income from from an additional job, show your

expenses under five different categories , one of those categories being you

are now building a house or just paid for a new car. Pay the gov‟t all their taxes.

Research the words cahflow, timeline, Net Present Value, Rate of Return

End of Day 3

Information for Clarification

Day 4

Day 4

Objective: Defining the elements of Petroleum Taxation

The Focus

To understand the design and strategies used by the host country

to maximize its extractive potential and remain competitive as it

collects taxes and fees from the investor based on oil/gas price and

The production levels the operator is able to obtain.

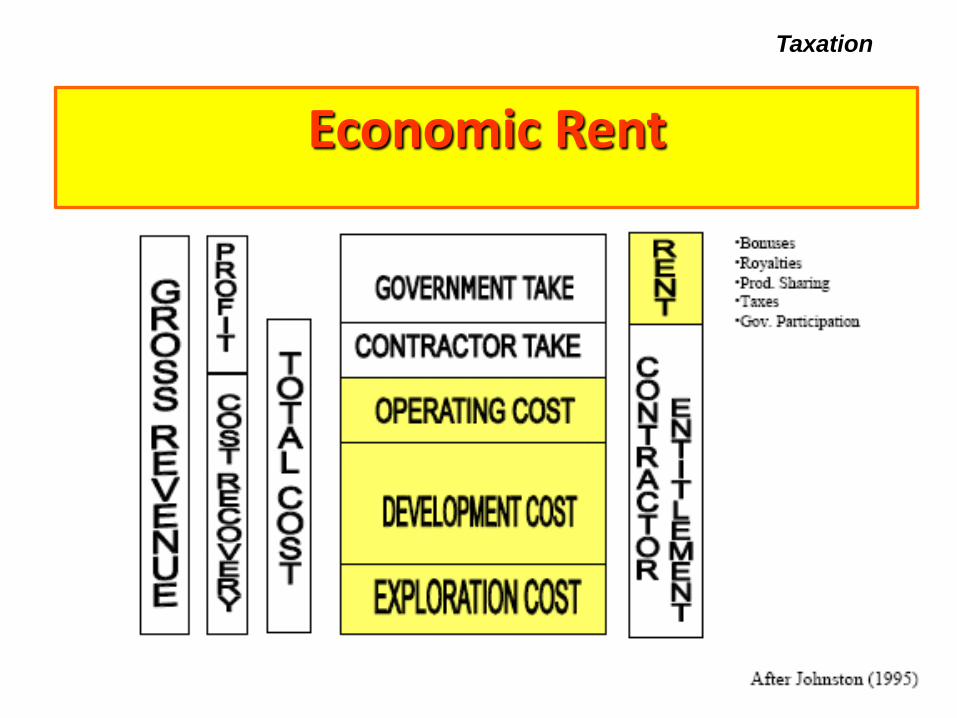

Economic Rent

Taxation

Petroleum Fiscal Systems

Taxation

Petroleum Fiscal Systems

Taxation

Taxation

Signature Bonus Award of PSC

Production Bonus 1st Oil or Gas Prod‟n

Main taxes

Income Taxes Paid

Petroleum Profit Tax (PPT) 50% Qtr in Arrears

Unemployment Levy Qtr in Arrears

Dividend April subsequent year

Production Taxes

Supplemental Petroleum Tax Qtr in Arrears

Royalty Qtr in Arrears

Petroleum Impost Annually

Petroleum Levy Monthly

Other taxes

Minimum Payment Qtr in Arrears

Land and Building Annually

Environmental Levy ( 0.1% of Gross) Qtr in Arrears

Value Added Tax Bi-monthly

Taxation

Case Study : Trinidad and Tobago

Legislation

Petroleum Act 1969 – Principal Statue regulating licenses to explore

Petroleum Regulation 1970 – Section 29 of the Petroleum Act

introduced Exploration License

Exploration and Production License ( Private Rights)

Exploration and Production License ( Public Rights )

Petroleum Taxes Act (1974) -

introduced Product Sharing Contracts

Petroleum Profit Tax

Supplemental Petroleum Tax

Petroleum Production Levy and Subsidy Act 1974

Petroleum Production Levy and Subsidy Act 1992

Petroleum Finance Act 2005

These are all influenced by Global Price of Oil and Gov’t intent on

maximizing “ Economic Rent:”

Legislation

Note the introduction of new

Legislations or Contracts

The structure and intent of the

new fiscal terms:

Supplemental Petroleum

Unemployment Levy

Subsidy

Taxable PSC

Trinidad and Tobago Milestones

>>„ 69 , „70 „‟74 , „92 , „05

Presentation for Discussion : Pedro Van Meurs: Trends in Gov’t Take and

the future of Trinidad and Tobago - 2007

Allowances for Taxation

1st Year Subsequent Years

Exploration

Exploration well 100%

Geological & Geophysical 100%

Development Phase

Development Well

Intangible 20% 20%

Tangible

Sidetrack Well

Depreciation

Profit Re-invested

Geological & Geophysical 50%

Development Dry Hole 100%

Taxation

Readings for Next Day Presentation

Research Paper on small independent or Junior Oil Co.

Concepts used in mature oil fields, Overriding Royalties

Sub License, Third Party Operators

Project – Excel Spreadsheet

Replace the spreadsheet with an Oilfiled Spreadsheet. You now own a

Small mature oilfiled, Show your income, your expenses and pay the

Gov‟t taxes

End of Day 4

Information for Clarification at next session

Day 5 – Interactive Workshop

Objective: An in-depth understanding of the numerical implications

of hydrocarbon legislations, regulations, Productions Sharing and

Exploration & Production Contracts

Methodology: Examine the “hydrocarbon” spreadsheets prepared by

the participants, relate to the prior theory sessions to ensure the spreadsheets

Include all the elements of contracts, taxation and allowances

Provide a standard but complex spreadsheet used by Operating Upstream

investors and analyse various investment options

For example, drilling a new well, exploration versus the development phase

Mature field and the introduction of an exclusive third party operator with a

Sub- licence

Recap\Session

Ten Question will be provided to be submitted with brief and short

answers one (1) hour before the final session.

Like questions and answers will be grouped for discussion by

the panel of participants .

The lecturer will attempt to direct the questions and answers to

The lecture notes

The structure of this session will not expose the source of the answers

Only the individual participant will know his or her answer

End of Day 5

Day 6

Interactive Discussion Workshop

Recap

Questions and Answers