79

Introduction to Fund Management and REITs (2015 Core CPD module – C2L2SP104 ) By: Lester leow 1

| Date post: | 19-Aug-2015 |

| Category: |

Real Estate |

| Upload: | kok-wee-leow |

| View: | 9 times |

| Download: | 2 times |

Introduction to Fund Management and

REITs (2015 Core CPD module – C2L2SP104 )

By: Lester leow

1

House Rules

RCN

Speaker Background

• More than 18 years in the real estate industry;

.

Corporate Visions Pte Ltd Director - Investment Sales & Agency

B.Sc. (Estate Management) (Hons)

Work Experience : -

AIMS AMP Fund manager (formerly known as “MaCartherCook REIT”)

Ascendas : Real Estate Fund Business

Cambridge Industrial Trust : Investment

Capitaland/PREMAS : Head of Agency

Wing Tai Asia : Maketing

RCN Trainer/Module developer since 2010

Adjunct NanYang Polytechnic lecturer

Handle more than $300mn investment sales

Speciliases in Corporate real estate lease transactions, Sales & leaseback

and investment sales

Email : [email protected]

3

Agenda – Part 1

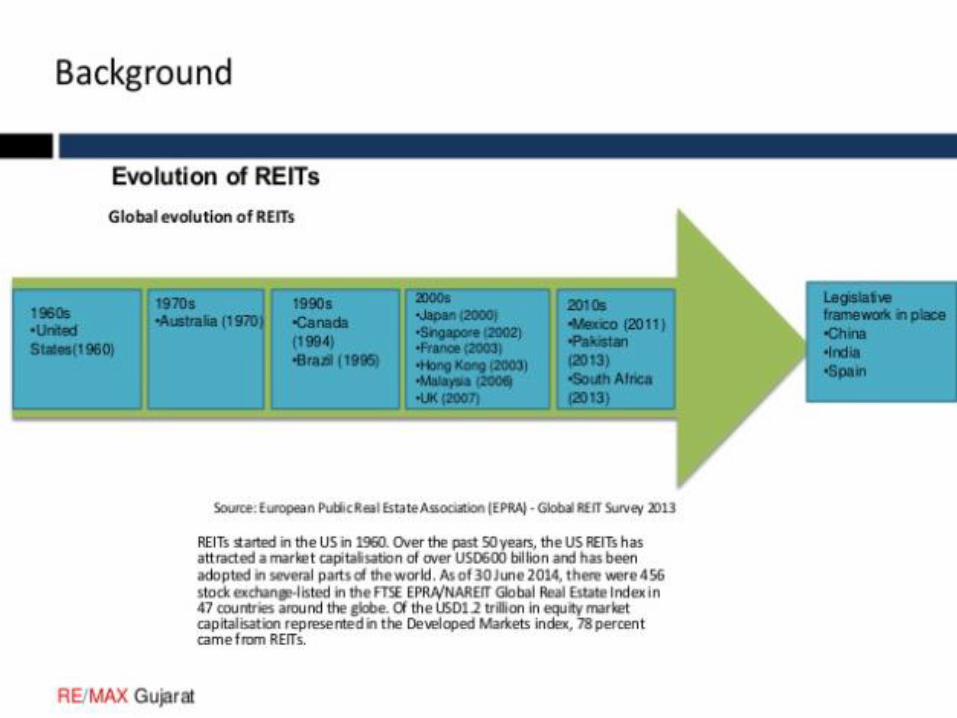

A brief history of REIT

Why Singapore REITs do well ?

Singapore Real Estate landscape

Type of real estate Funds

Source of Funds

1

2

3

4

5

Source : Ascendas and past IPO and work experience

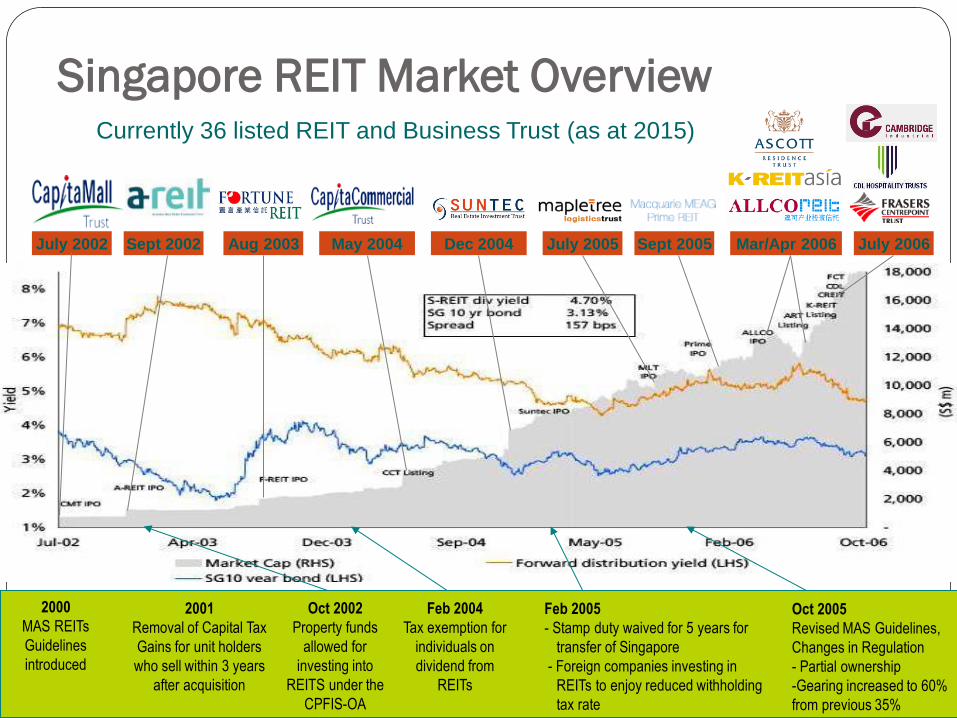

Singapore REIT Market Overview

July 2002 Sept 2002 Aug 2003 May 2004 Dec 2004 July 2005 Sept 2005 Mar/Apr 2006 July 2006

2000

MAS REITs

Guidelines

introduced

Feb 2004

Tax exemption for

individuals on

dividend from

REITs

Feb 2005

- Stamp duty waived for 5 years for

transfer of Singapore

- Foreign companies investing in

REITs to enjoy reduced withholding

tax rate

Oct 2005

Revised MAS Guidelines,

Changes in Regulation

- Partial ownership

-Gearing increased to 60%

from previous 35%

Oct 2002

Property funds

allowed for

investing into

REITS under the

CPFIS-OA

2001

Removal of Capital Tax

Gains for unit holders

who sell within 3 years

after acquisition

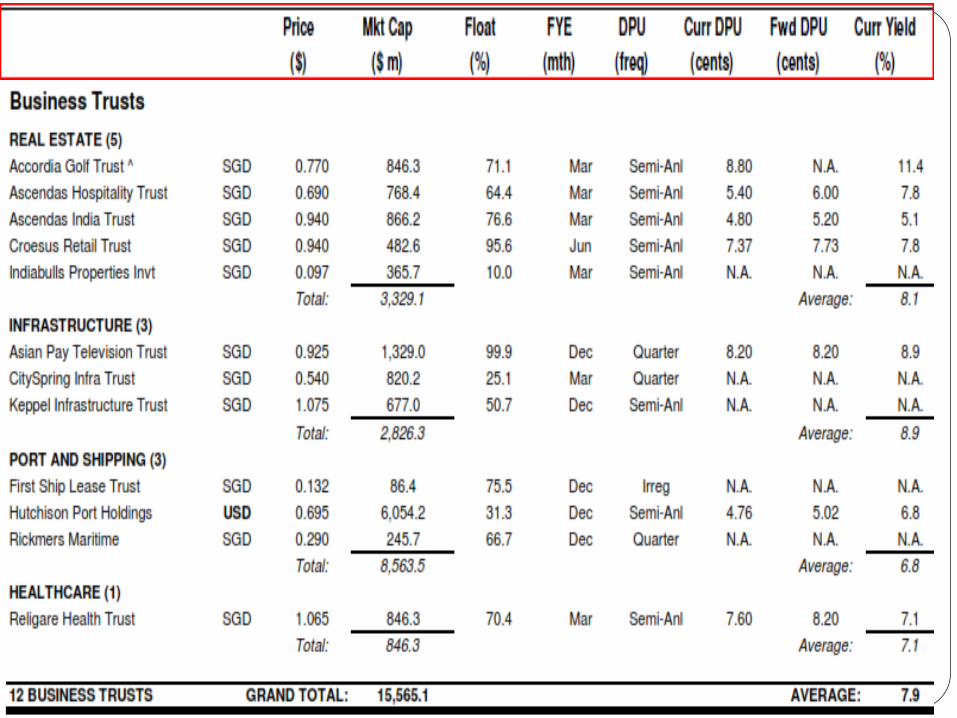

Currently 36 listed REIT and Business Trust (as at 2015)

Real estate fund management

Trend of “Financialisation” Of Real Estate Market

Going forward Previously

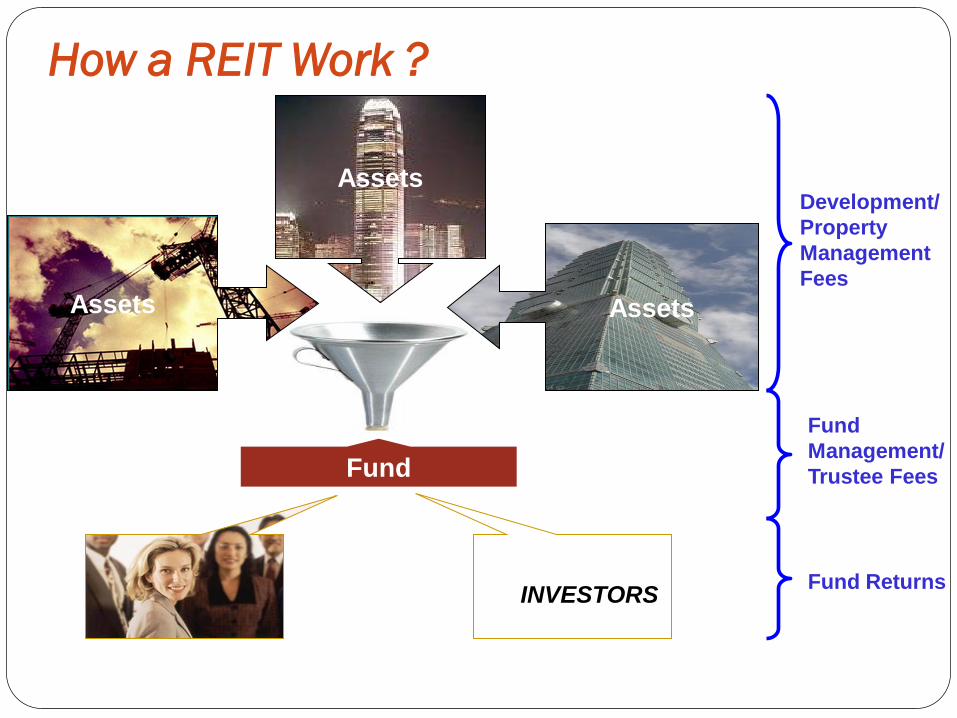

How a REIT Work ?

Assets Assets

Assets

Fund

Development/

Property

Management

Fees

Fund

Management/

Trustee Fees

Fund Returns INVESTORS

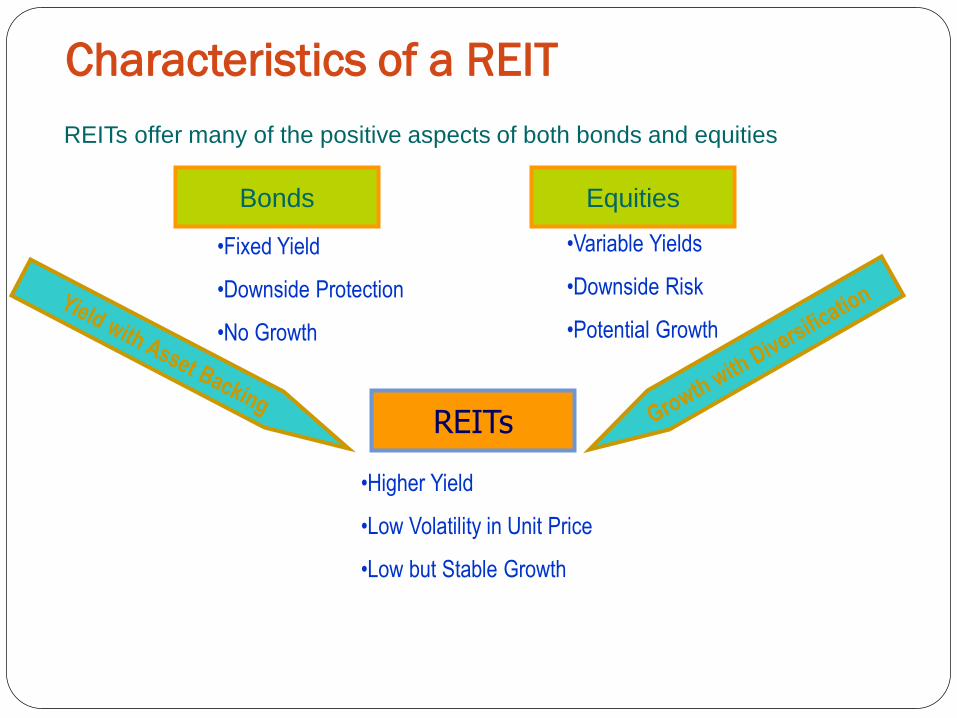

Characteristics of a REIT

Bonds Equities

REITs

•Fixed Yield

•Downside Protection

•No Growth

•Variable Yields

•Downside Risk

•Potential Growth

•Higher Yield

•Low Volatility in Unit Price

•Low but Stable Growth

REITs offer many of the positive aspects of both bonds and equities

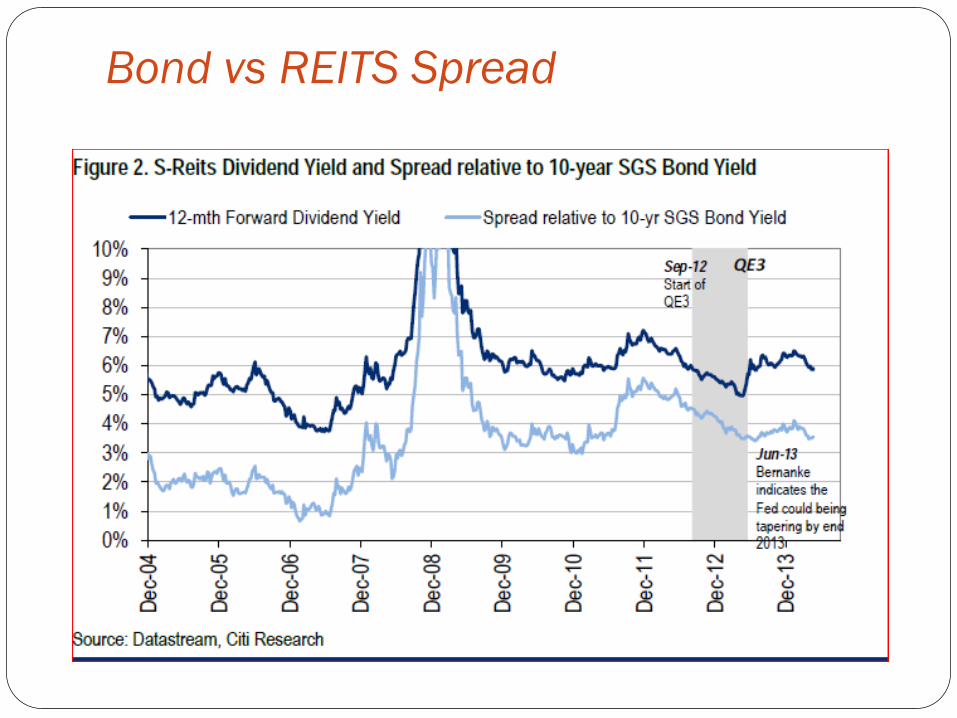

Bond vs REITS Spread

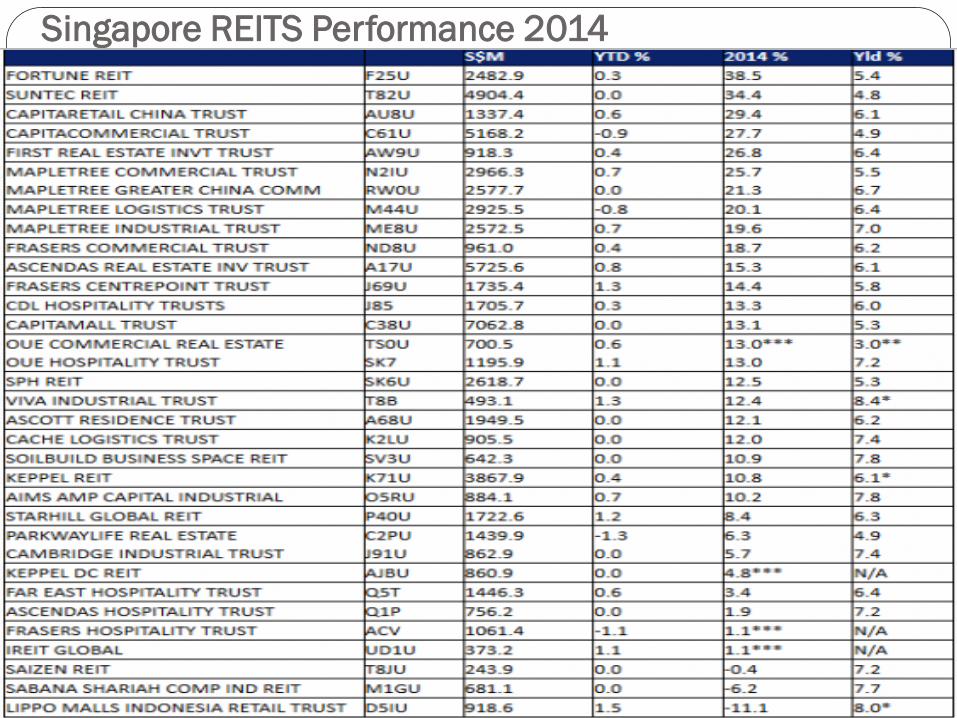

Singapore REITS Performance 2014

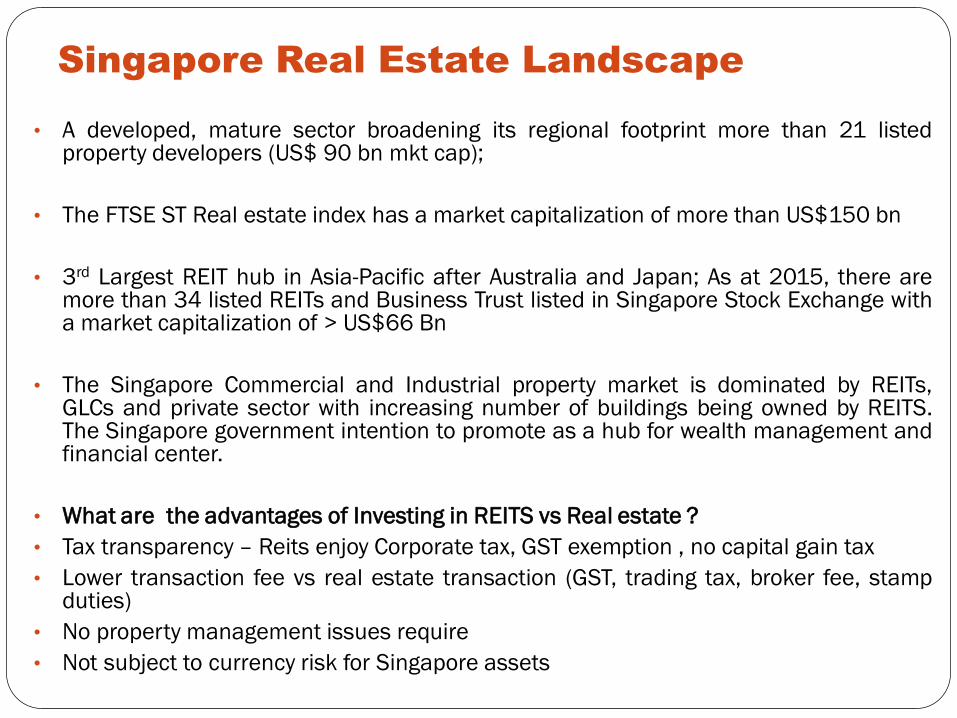

Singapore Real Estate Landscape

• A developed, mature sector broadening its regional footprint more than 21 listed property developers (US$ 90 bn mkt cap);

• The FTSE ST Real estate index has a market capitalization of more than US$150 bn

• 3rd Largest REIT hub in Asia-Pacific after Australia and Japan; As at 2015, there are more than 34 listed REITs and Business Trust listed in Singapore Stock Exchange with a market capitalization of > US$66 Bn

• The Singapore Commercial and Industrial property market is dominated by REITs, GLCs and private sector with increasing number of buildings being owned by REITS. The Singapore government intention to promote as a hub for wealth management and financial center.

• What are the advantages of Investing in REITS vs Real estate ?

• Tax transparency – Reits enjoy Corporate tax, GST exemption , no capital gain tax

• Lower transaction fee vs real estate transaction (GST, trading tax, broker fee, stamp duties)

• No property management issues require

• Not subject to currency risk for Singapore assets

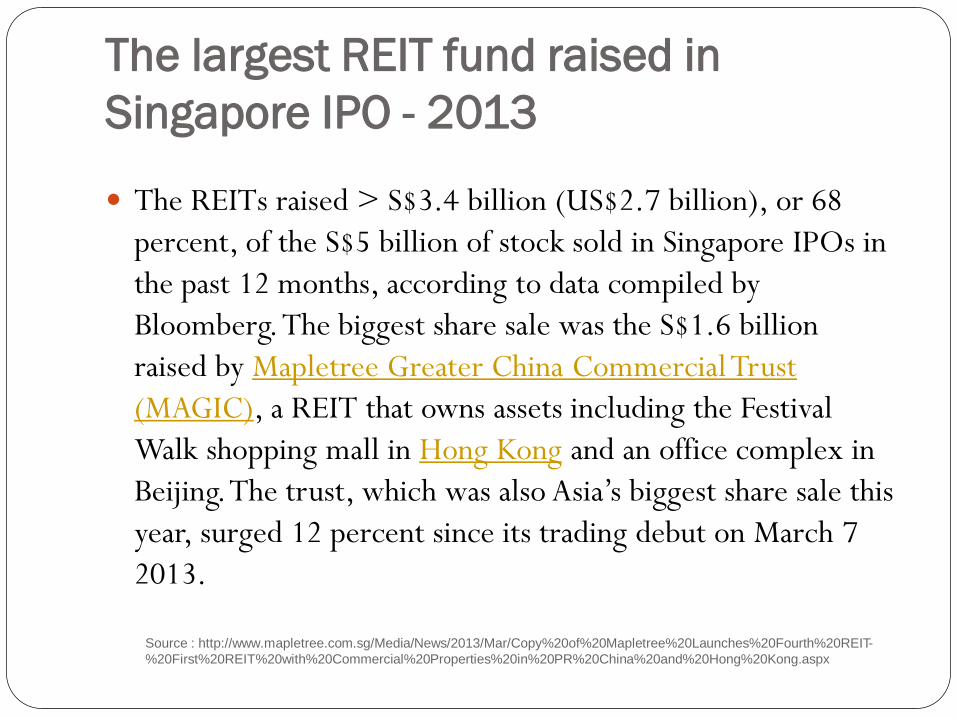

The largest REIT fund raised in

Singapore IPO - 2013

The REITs raised > S$3.4 billion (US$2.7 billion), or 68

percent, of the S$5 billion of stock sold in Singapore IPOs in

the past 12 months, according to data compiled by

Bloomberg. The biggest share sale was the S$1.6 billion

raised by Mapletree Greater China Commercial Trust

(MAGIC), a REIT that owns assets including the Festival

Walk shopping mall in Hong Kong and an office complex in

Beijing. The trust, which was also Asia’s biggest share sale this

year, surged 12 percent since its trading debut on March 7

2013.

Source : http://www.mapletree.com.sg/Media/News/2013/Mar/Copy%20of%20Mapletree%20Launches%20Fourth%20REIT-

%20First%20REIT%20with%20Commercial%20Properties%20in%20PR%20China%20and%20Hong%20Kong.aspx

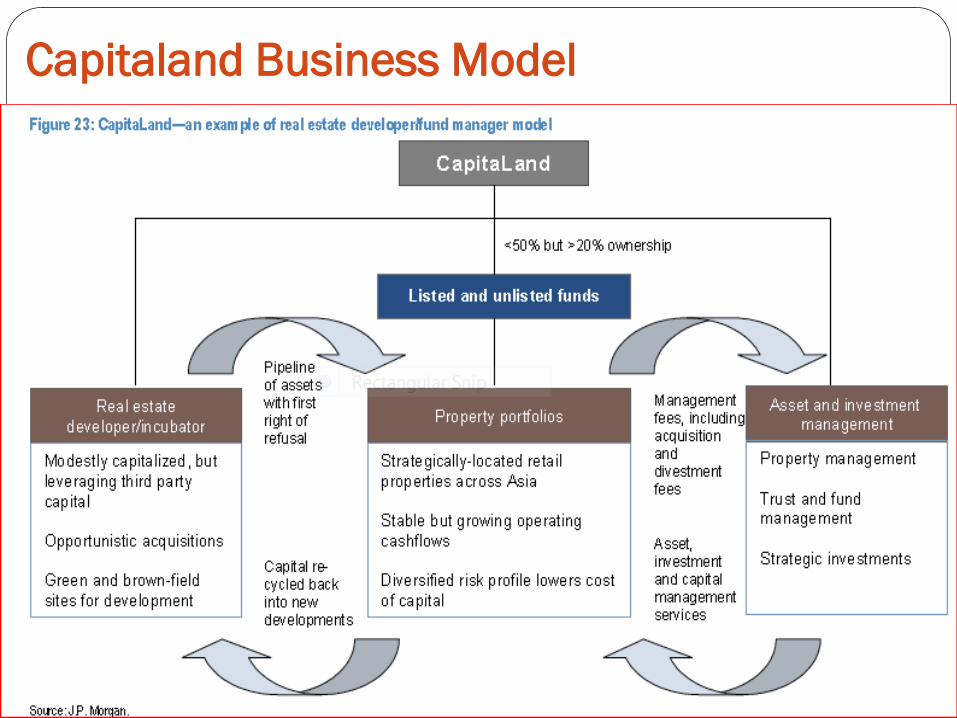

Capitaland Business Model

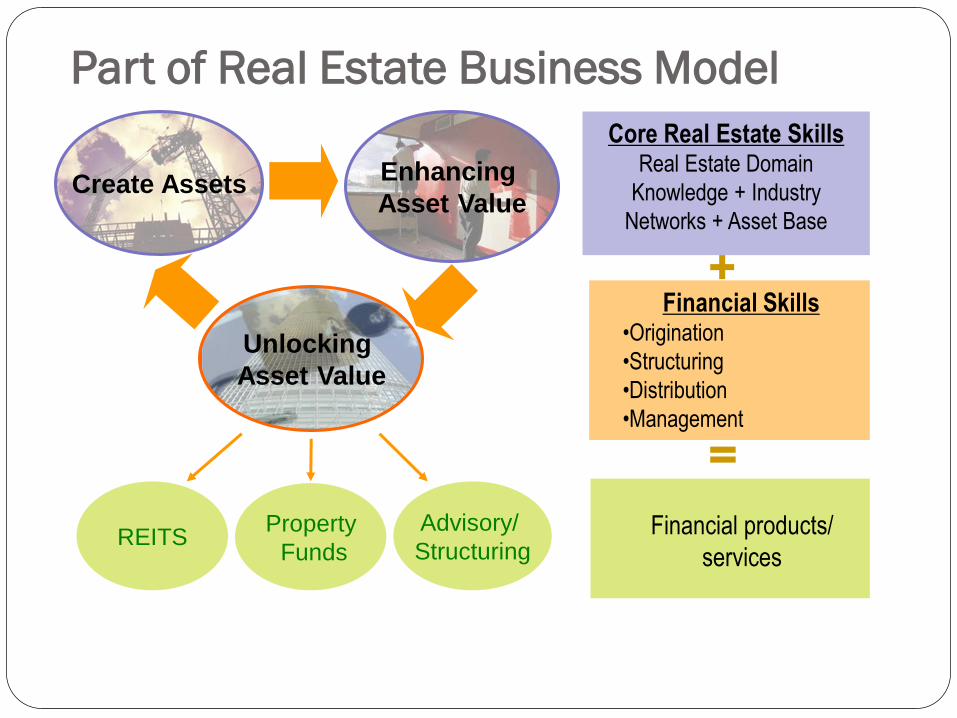

Part of Real Estate Business Model

Core Real Estate Skills Real Estate Domain

Knowledge + Industry

Networks + Asset Base

Financial Skills •Origination

•Structuring

•Distribution

•Management

Create Assets Enhancing

Asset Value

Unlocking

Asset Value

REITS Property

Funds

Advisory/

Structuring

Financial products/

services

Singapore Fund Structure Private Equity Funds

Private equity real estate is an investment opportunity in which multiple investors pool funds and invest in ownership of various real estate properties. This type of investment is achieved when individuals make a significant initial commitment of capital to a managed fund that scouts out the potential real estate investments. Strategies used by these funds vary in terms of risk involved and the types of property considered viable for investment. One main drawback to private equity real estate for investors is that their funds are generally frozen in the investments for multiple years, providing little flexibility.

Mandate of fund is set out in the placement memorandum with objectives, seed assets (if applicable), policies, investment criteria, distribution policy, borrowing, reporting, investment committee, risks factors, tax issues, redemption process and etc

Listed Funds – REIT / Business Trusts

Corporate governance is setout in the Trust deed; Trustee is approved and regulated by MAS

Two common form in Singapore :REIT & Business Trusts

What is a Real Estate Investment Trusts (REITs)?

REITs are collective investment schemes that invest in a portfolio of income generating real estate assets such as shopping malls, offices, hotels or serviced apartments, usually established with a view to generating income for unit holders.

Assets of REITs are professionally managed and net rental income generated from assets, also known as “DPU” – Distribution Per Unit are normally distributed at regular interval to you, as a unit holder.

Individuals through the purchase of a publicly-traded investment product, similar to shares of a common stock, provide dividend income - usually from rental income and capital gains from the profitable sale of real estate assets. It is important to know that REITs, like other investment products, are not completely free from risk.

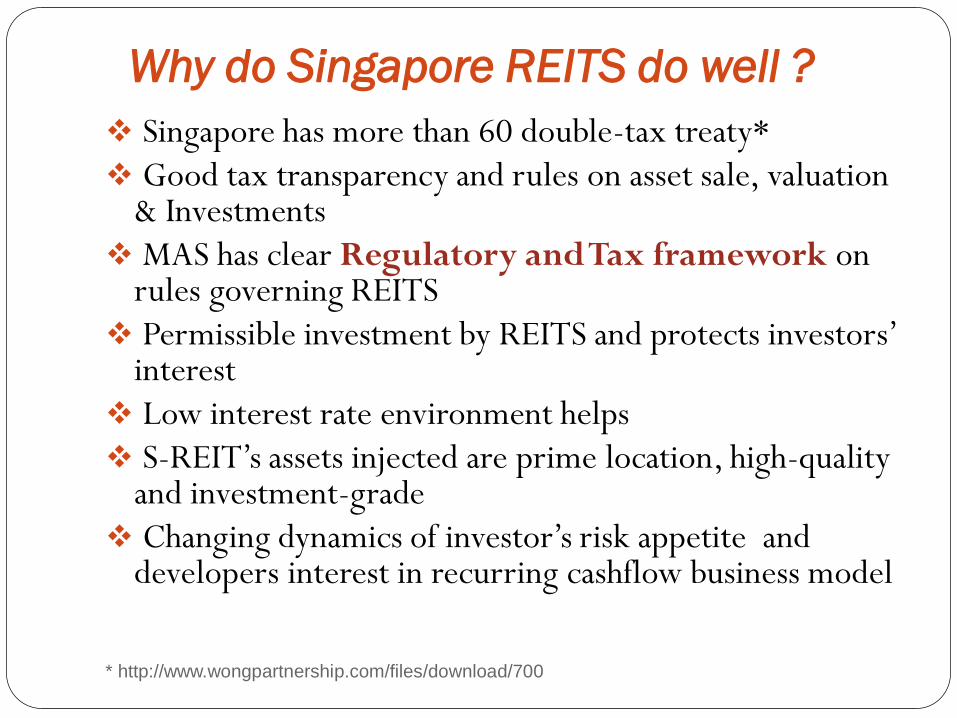

Why do Singapore REITS do well ?

* http://www.wongpartnership.com/files/download/700

Singapore has more than 60 double-tax treaty*

Good tax transparency and rules on asset sale, valuation & Investments

MAS has clear Regulatory and Tax framework on rules governing REITS

Permissible investment by REITS and protects investors’ interest

Low interest rate environment helps

S-REIT’s assets injected are prime location, high-quality and investment-grade

Changing dynamics of investor’s risk appetite and developers interest in recurring cashflow business model

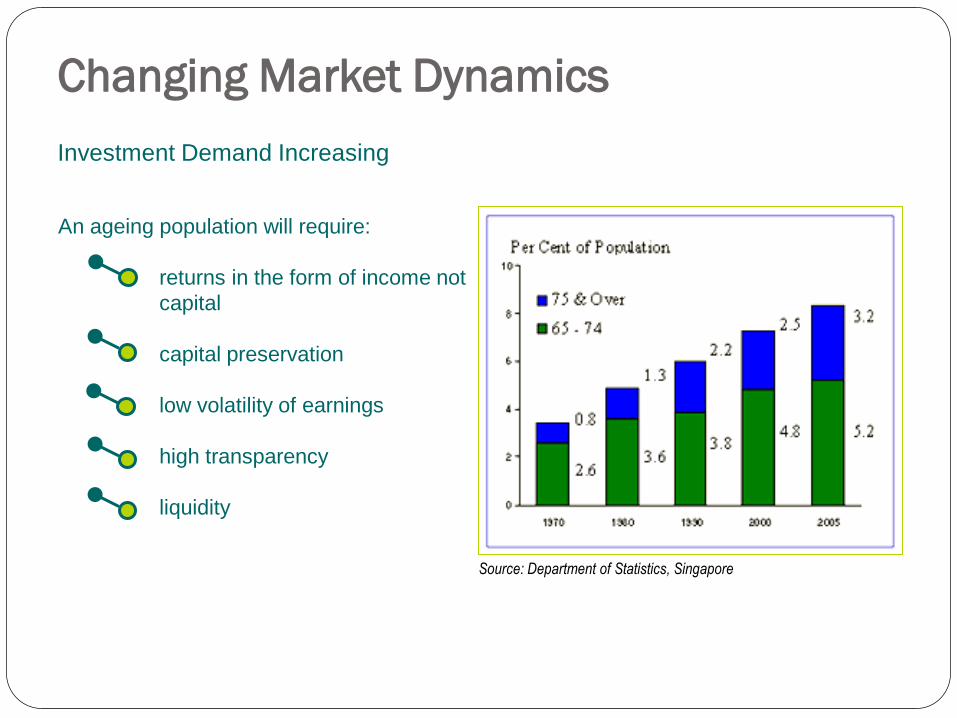

Changing Market Dynamics

Investment Demand Increasing

An ageing population will require:

returns in the form of income not

capital

capital preservation

low volatility of earnings

high transparency

liquidity

Source: Department of Statistics, Singapore

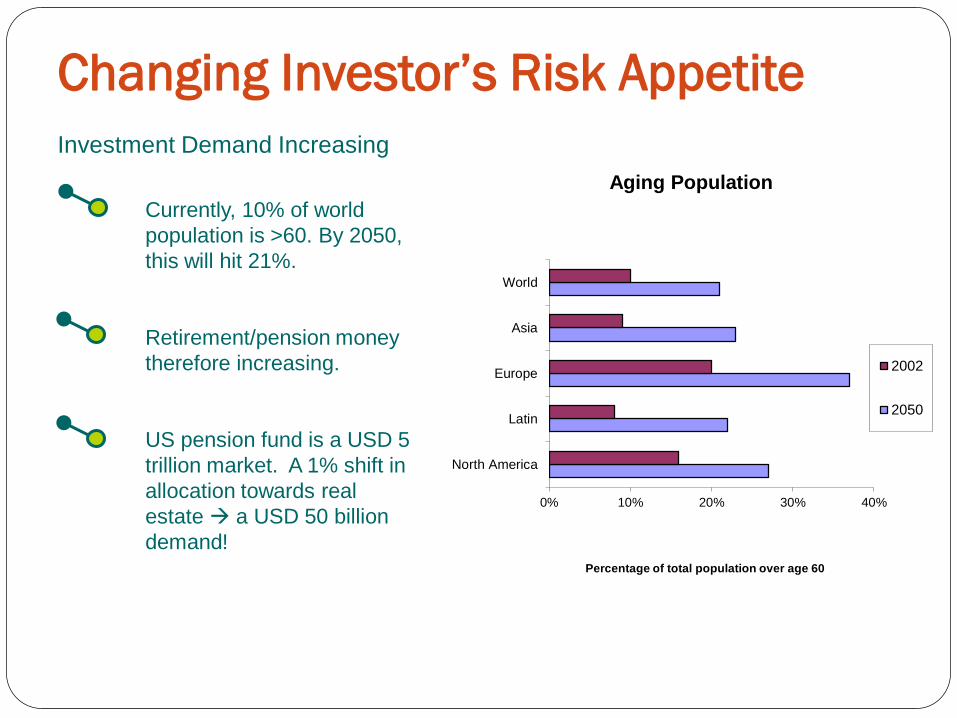

Changing Investor’s Risk Appetite

0% 10% 20% 30% 40%

North America

Latin

Europe

Asia

World

Percentage of total population over age 60

Aging Population

2002

2050

Investment Demand Increasing

Currently, 10% of world

population is >60. By 2050,

this will hit 21%.

Retirement/pension money

therefore increasing.

US pension fund is a USD 5

trillion market. A 1% shift in

allocation towards real

estate a USD 50 billion

demand!

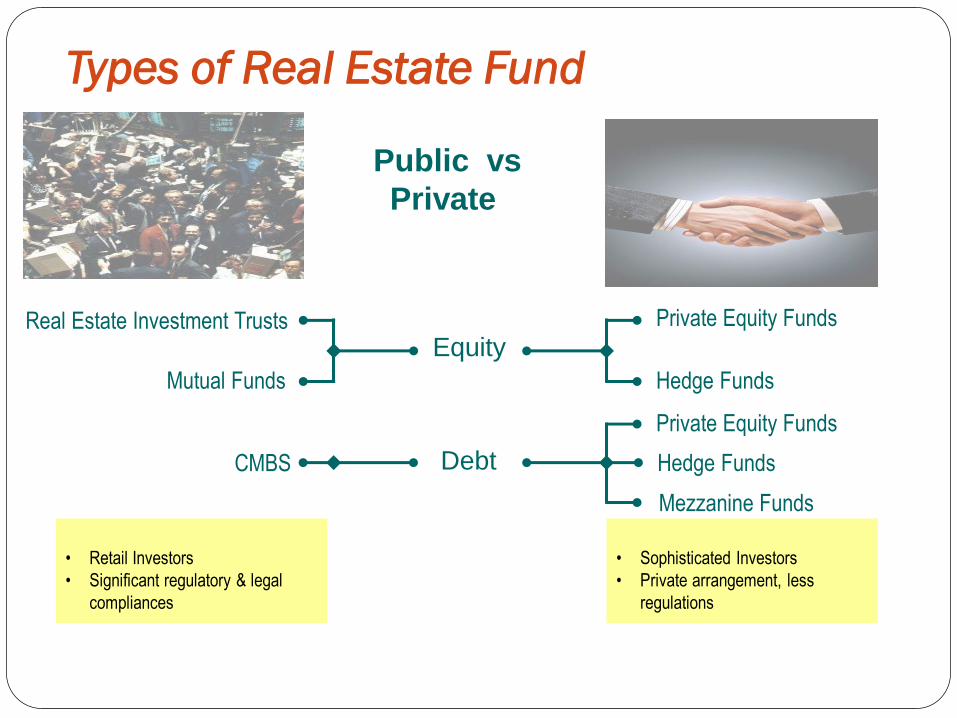

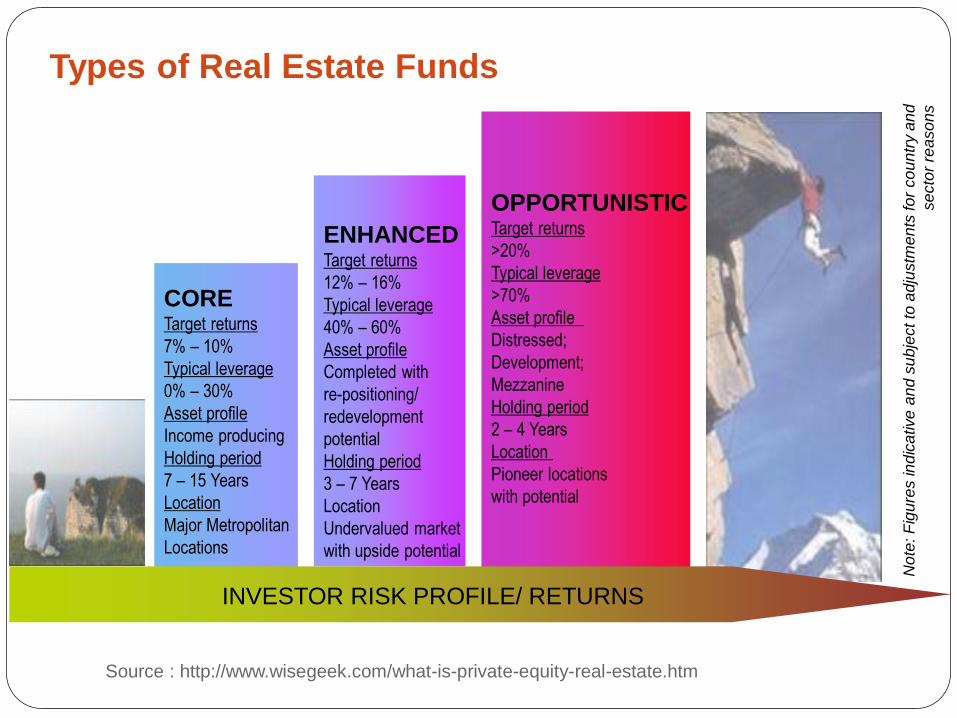

Types of Real Estate Fund

Equity Private Equity Funds

Hedge Funds

Real Estate Investment Trusts

Mutual Funds

Debt

Private Equity Funds

Hedge Funds

Mezzanine Funds

CMBS

• Sophisticated Investors

• Private arrangement, less

regulations

• Retail Investors

• Significant regulatory & legal

compliances

Public vs

Private

Types of Real Estate Funds

CORE Target returns

7% – 10%

Typical leverage

0% – 30%

Asset profile

Income producing

Holding period

7 – 15 Years

Location

Major Metropolitan

Locations

ENHANCED Target returns

12% – 16%

Typical leverage

40% – 60%

Asset profile

Completed with

re-positioning/

redevelopment

potential

Holding period

3 – 7 Years

Location

Undervalued market

with upside potential

OPPORTUNISTIC Target returns

>20%

Typical leverage

>70%

Asset profile

Distressed;

Development;

Mezzanine

Holding period

2 – 4 Years

Location

Pioneer locations

with potential

No

te: F

igu

res in

dic

ative

an

d s

ub

ject to

ad

justm

en

ts fo

r co

un

try a

nd

se

cto

r re

aso

ns

INVESTOR RISK PROFILE/ RETURNS

Source : http://www.wisegeek.com/what-is-private-equity-real-estate.htm

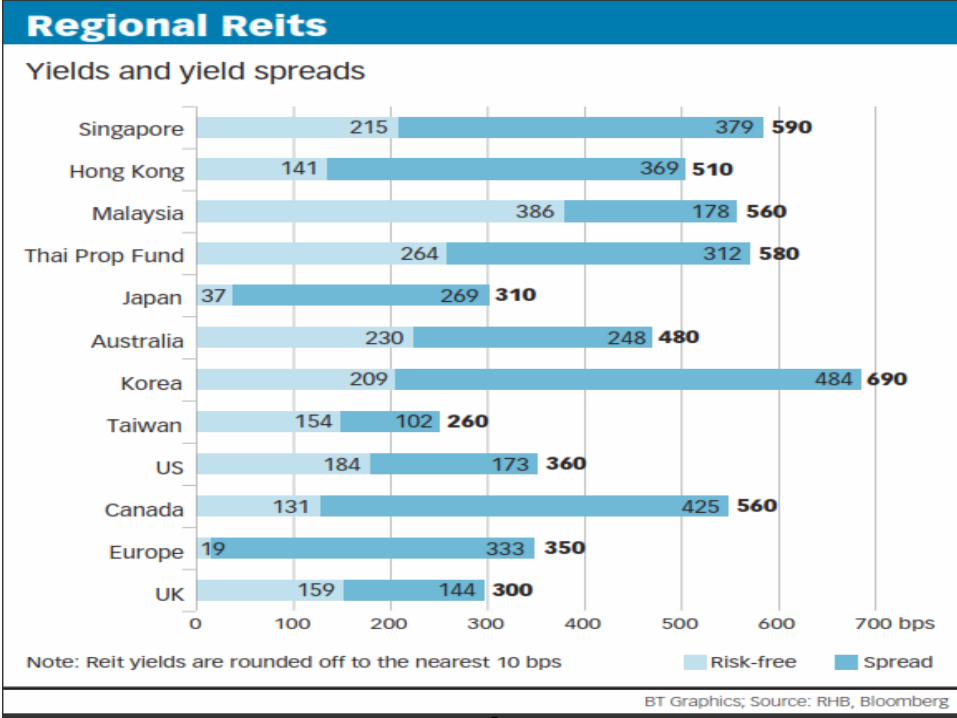

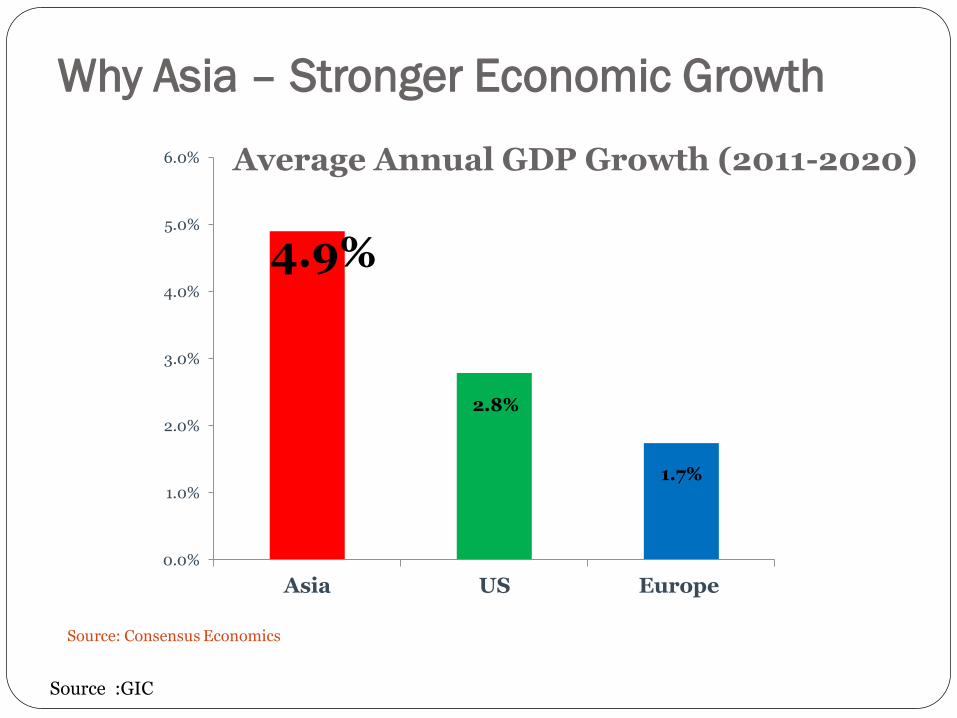

Why Asia – Stronger Economic Growth

Source :GIC

Source: Consensus Economics

4.9%

2.8%

1.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Asia US Europe

Average Annual GDP Growth (2011-2020)

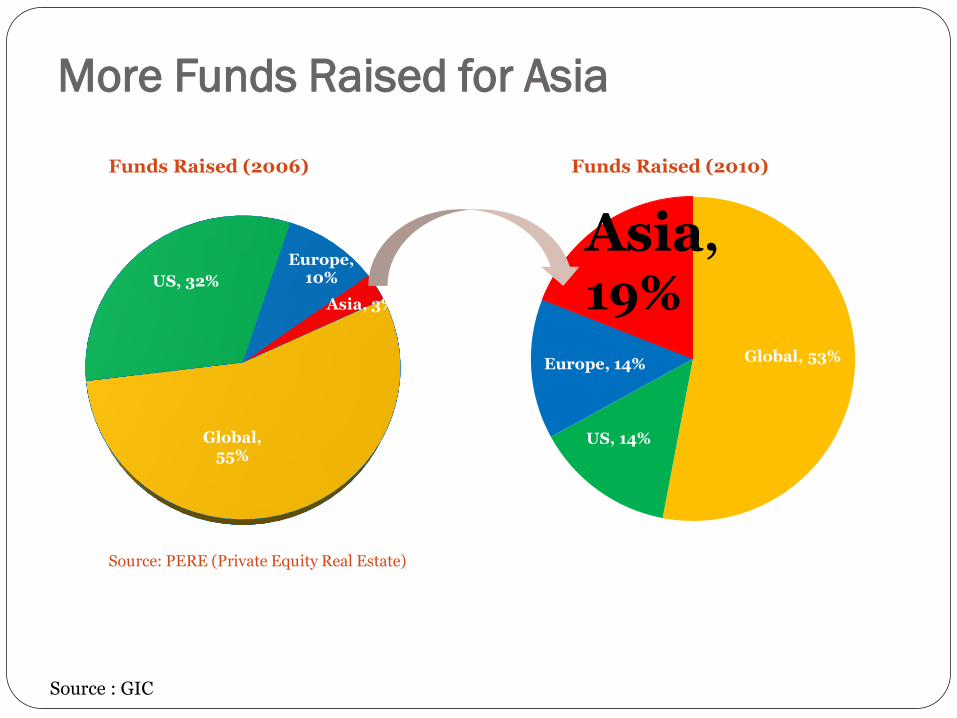

More Funds Raised for Asia

Source : GIC

Global, 55%

US, 32%

Europe, 10%

Asia, 3%

Global, 53%

US, 14%

Europe, 14%

Asia, 19%

Asia,

19%

Source: PERE (Private Equity Real Estate)

Funds Raised (2006) Funds Raised (2010)

20%

25%

30%

35%

40%

45%

Asia Europe US

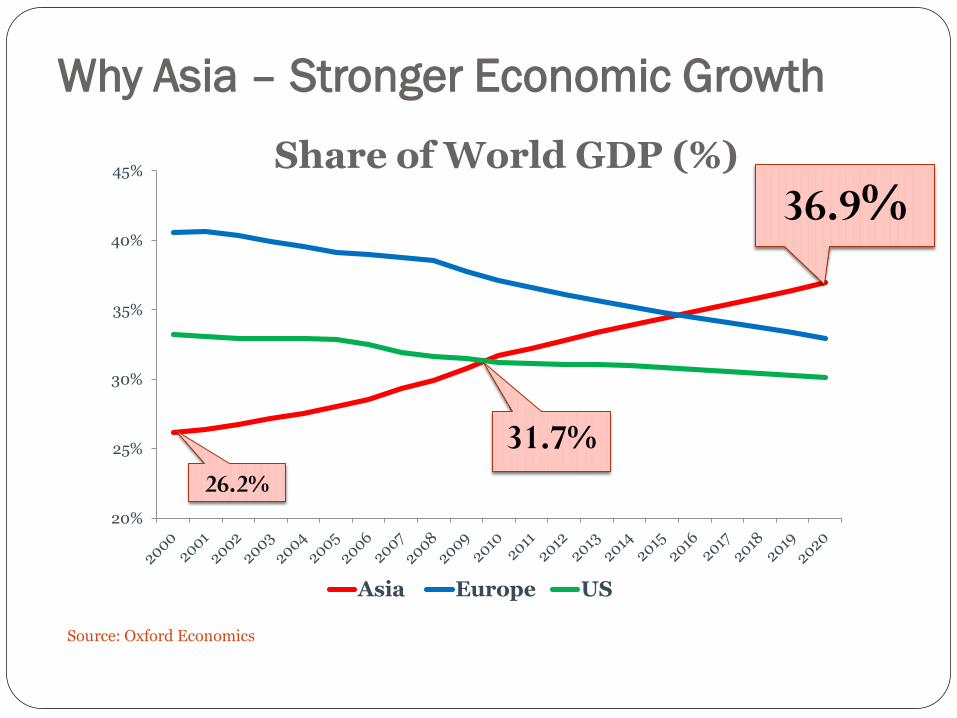

Why Asia – Stronger Economic Growth

Source: Oxford Economics

36.9%

26.2%

Share of World GDP (%)

31.7%

10%

20%

30%

40%

50%

60%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Asia Europe Americas

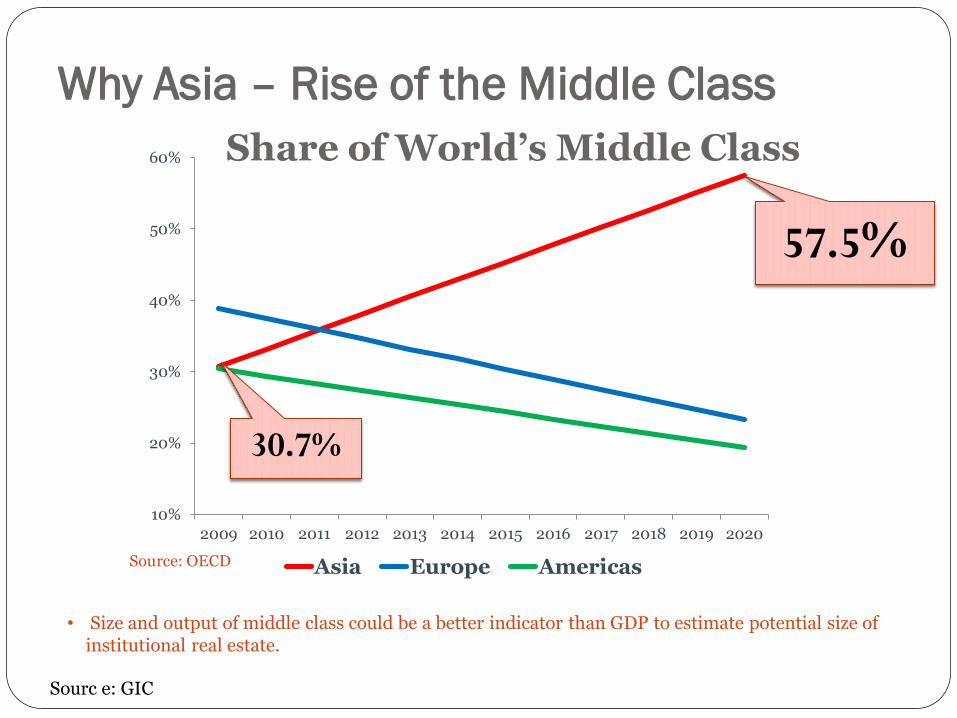

Why Asia – Rise of the Middle Class

Sourc e: GIC

Source: OECD

• Size and output of middle class could be a better indicator than GDP to estimate potential size of institutional real estate.

Share of World’s Middle Class

57.5%

30.7%

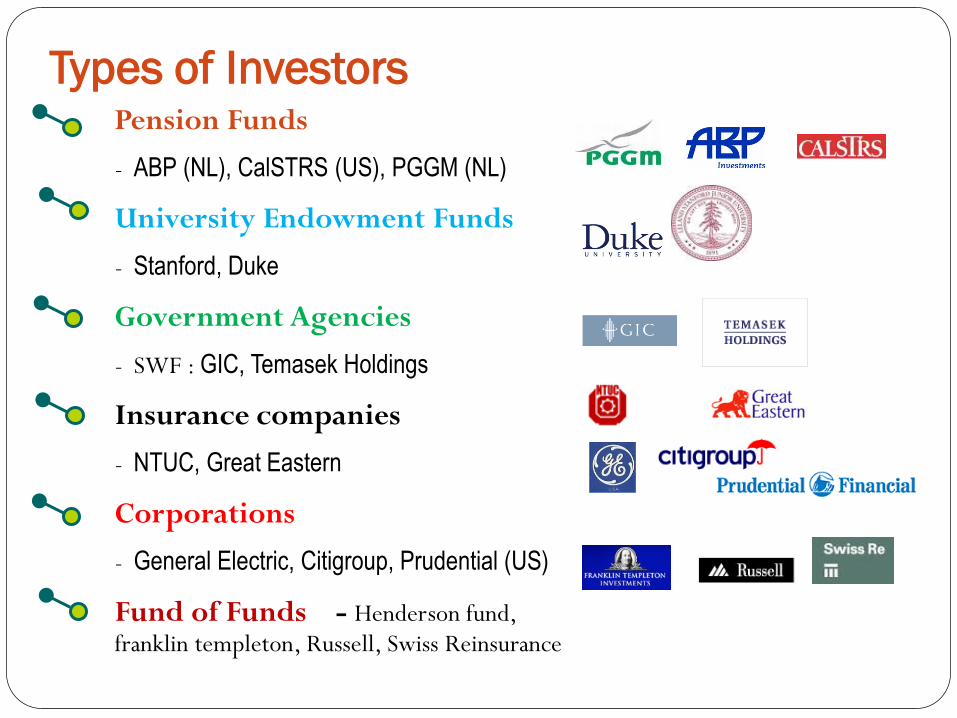

Types of Investors Pension Funds

- ABP (NL), CalSTRS (US), PGGM (NL)

University Endowment Funds

- Stanford, Duke

Government Agencies

- SWF : GIC, Temasek Holdings

Insurance companies

- NTUC, Great Eastern

Corporations

- General Electric, Citigroup, Prudential (US)

Fund of Funds - Henderson fund, franklin templeton, Russell, Swiss Reinsurance

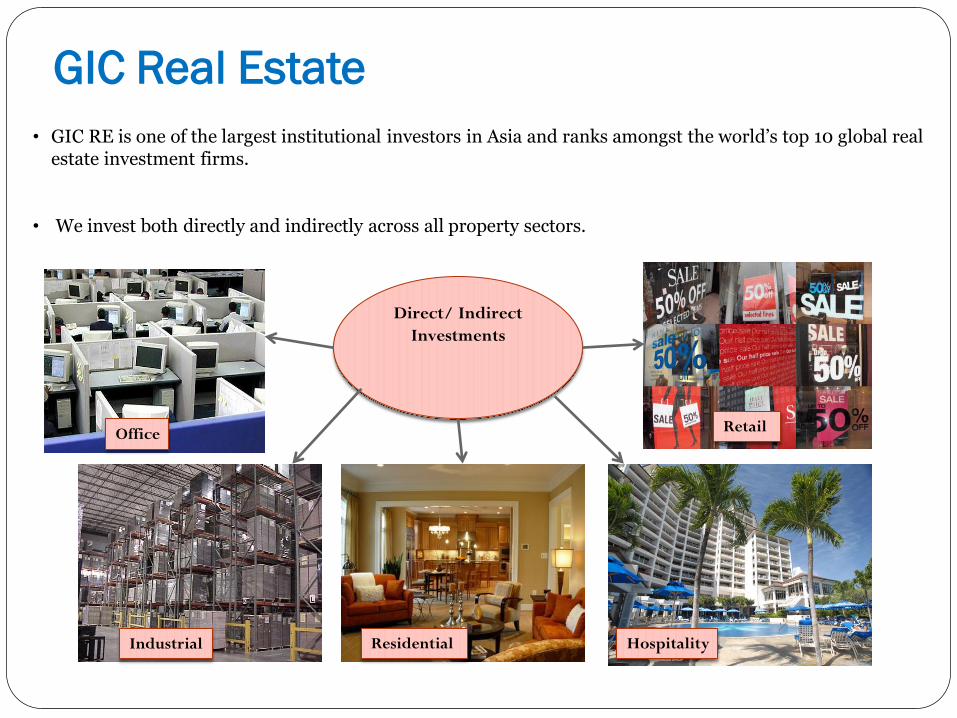

GIC Real Estate

• GIC RE is one of the largest institutional investors in Asia and ranks amongst the world’s top 10 global real estate investment firms.

• We invest both directly and indirectly across all property sectors.

Direct/ Indirect

Investments

Office

Industrial Residential Hospitality

Retail

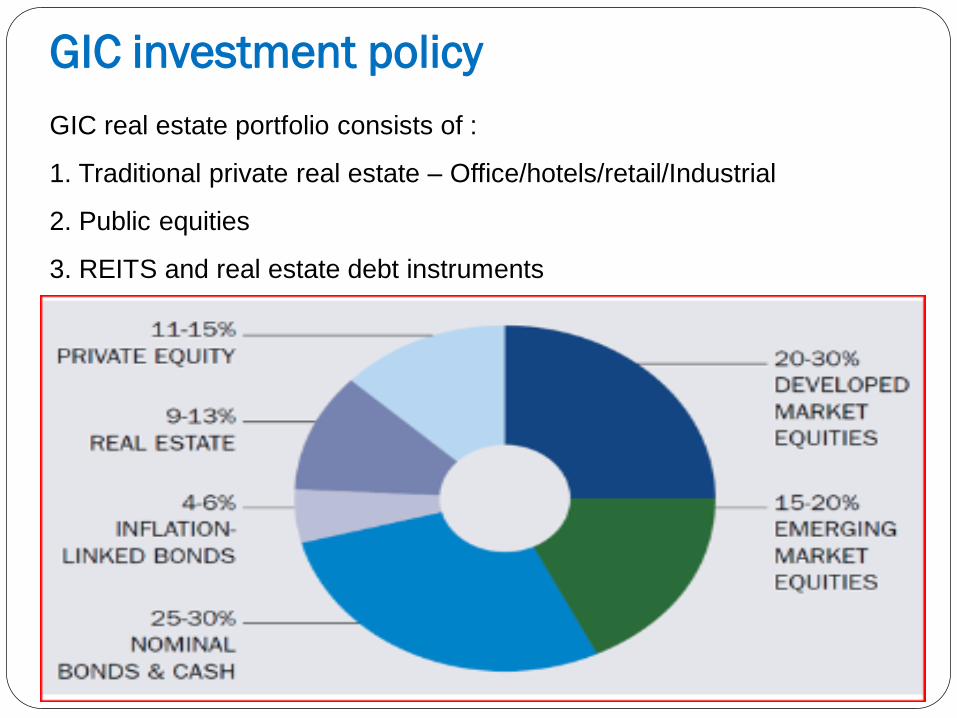

GIC investment Policy

GIC Asset under management : in excess of US$300 bn

Annualised 20 year return is 4% pa as at 31 Mar 2013

Source: www.gic.com

GIC investment policy

GIC real estate portfolio consists of :

1. Traditional private real estate – Office/hotels/retail/Industrial

2. Public equities

3. REITS and real estate debt instruments

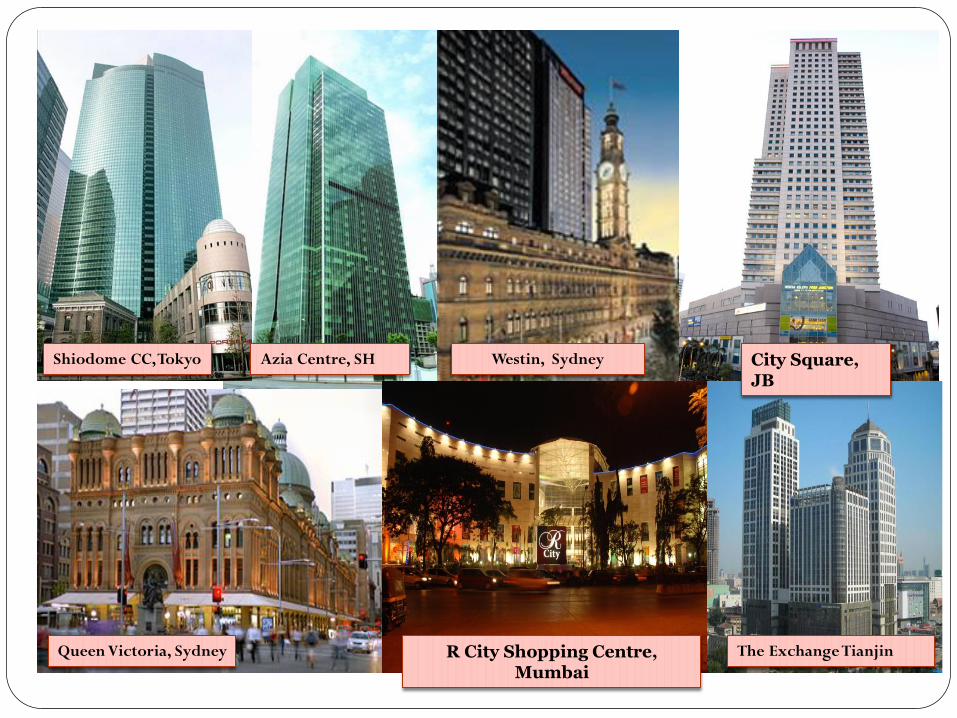

Shiodome CC, Tokyo

Queen Victoria, Sydney The Exchange Tianjin

Westin, Sydney City Square, JB

R City Shopping Centre, Mumbai

Azia Centre, SH

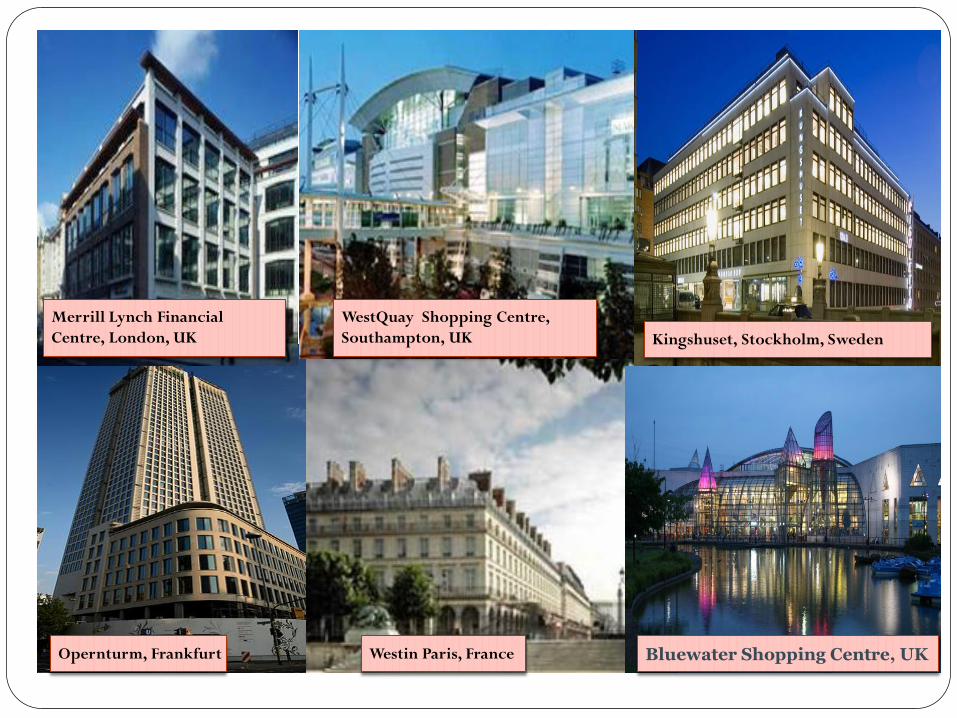

WestQuay Shopping Centre,

Southampton, UK

Westin Paris, France Opernturm, Frankfurt

Kingshuset, Stockholm, Sweden

Merrill Lynch Financial

Centre, London, UK

Bluewater Shopping Centre, UK

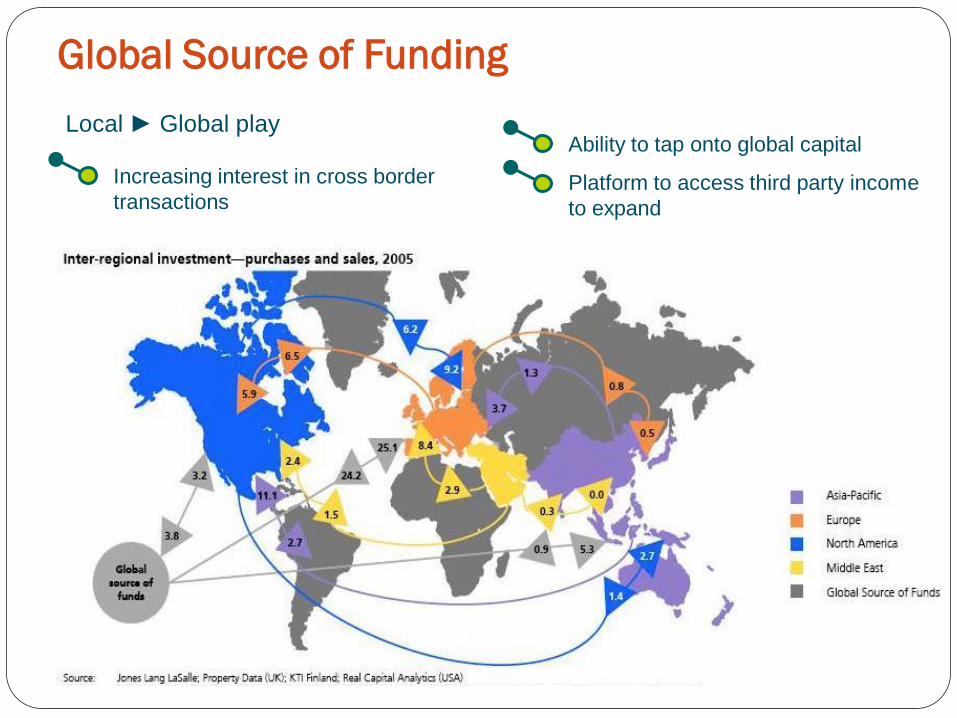

Global Source of Funding

Local ► Global play

Increasing interest in cross border

transactions

Ability to tap onto global capital

Platform to access third party income

to expand

KOPI BREAK TIME

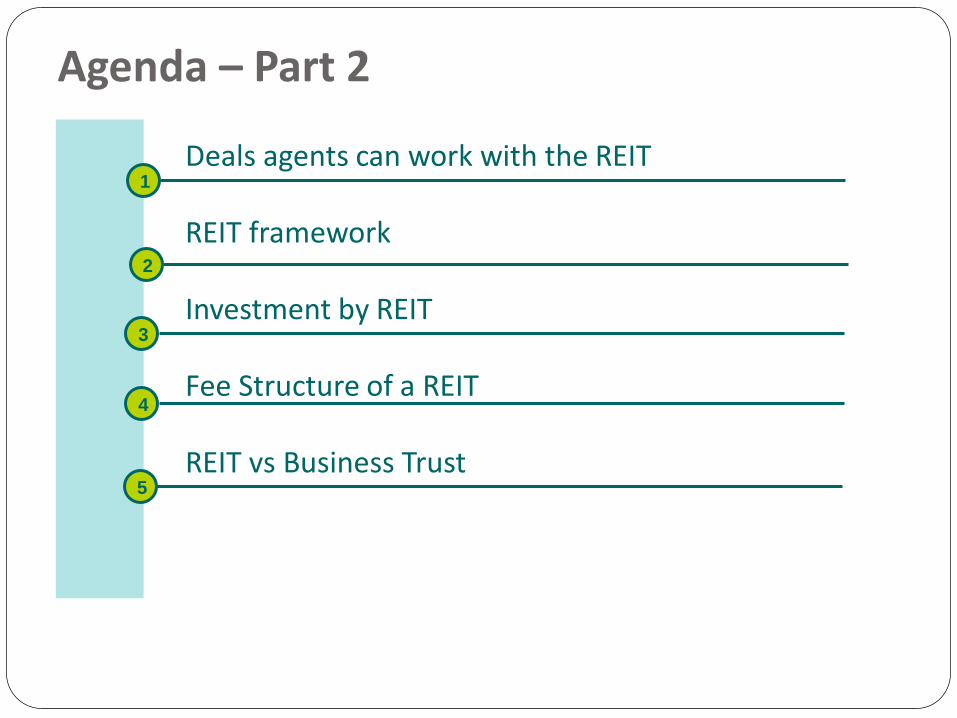

Agenda – Part 2

Deals agents can work with the REIT REIT framework Investment by REIT Fee Structure of a REIT REIT vs Business Trust

1

2

3

4

5

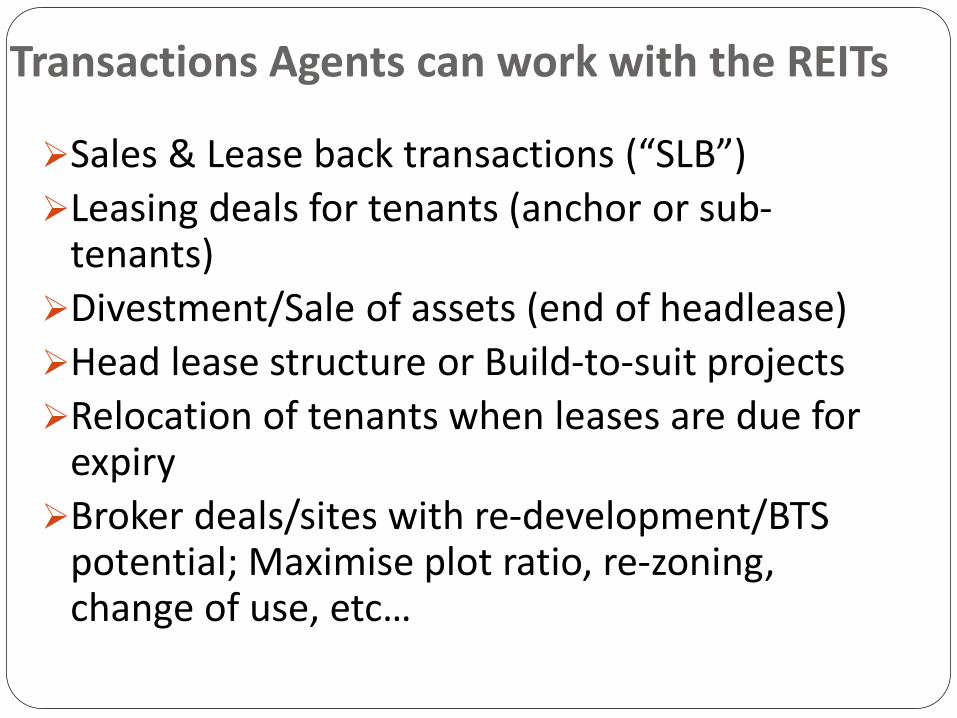

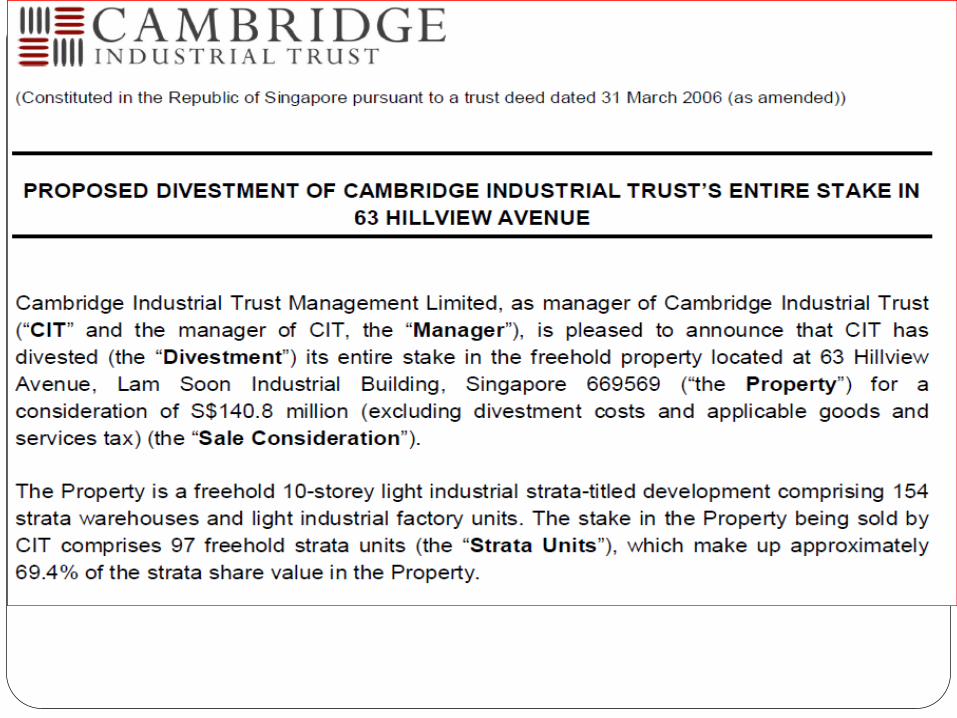

Transactions Agents can work with the REITs

Sales & Lease back transactions (“SLB”)

Leasing deals for tenants (anchor or sub-tenants)

Divestment/Sale of assets (end of headlease)

Head lease structure or Build-to-suit projects

Relocation of tenants when leases are due for expiry

Broker deals/sites with re-development/BTS potential; Maximise plot ratio, re-zoning, change of use, etc…

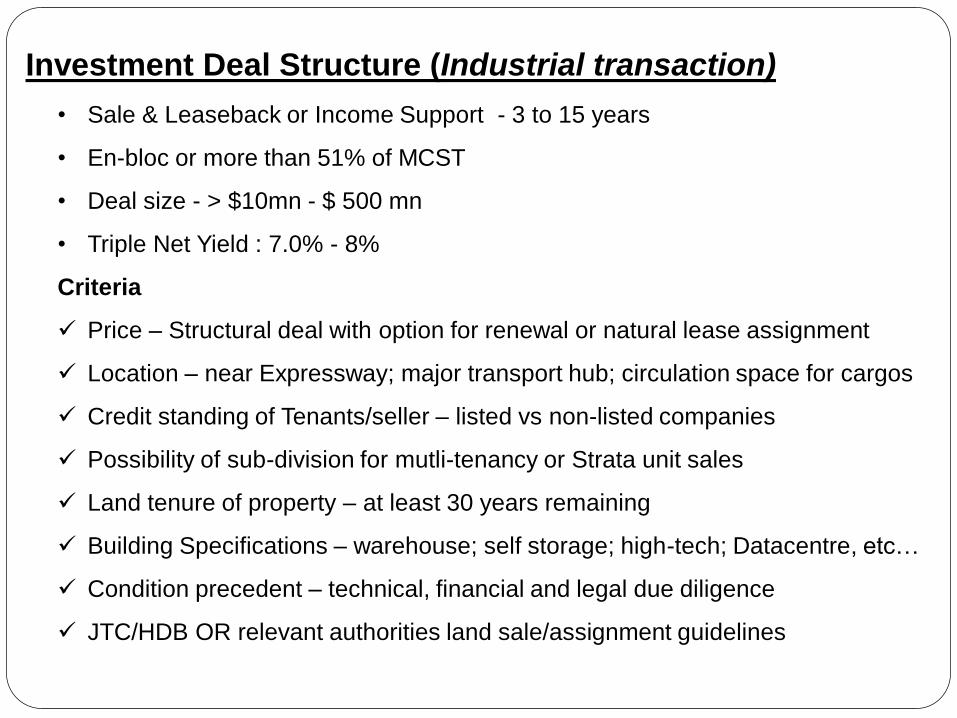

Investment Deal Structure (Industrial transaction)

• Sale & Leaseback or Income Support - 3 to 15 years

• En-bloc or more than 51% of MCST

• Deal size - > $10mn - $ 500 mn

• Triple Net Yield : 7.0% - 8%

Criteria

Price – Structural deal with option for renewal or natural lease assignment

Location – near Expressway; major transport hub; circulation space for cargos

Credit standing of Tenants/seller – listed vs non-listed companies

Possibility of sub-division for mutli-tenancy or Strata unit sales

Land tenure of property – at least 30 years remaining

Building Specifications – warehouse; self storage; high-tech; Datacentre, etc…

Condition precedent – technical, financial and legal due diligence

JTC/HDB OR relevant authorities land sale/assignment guidelines

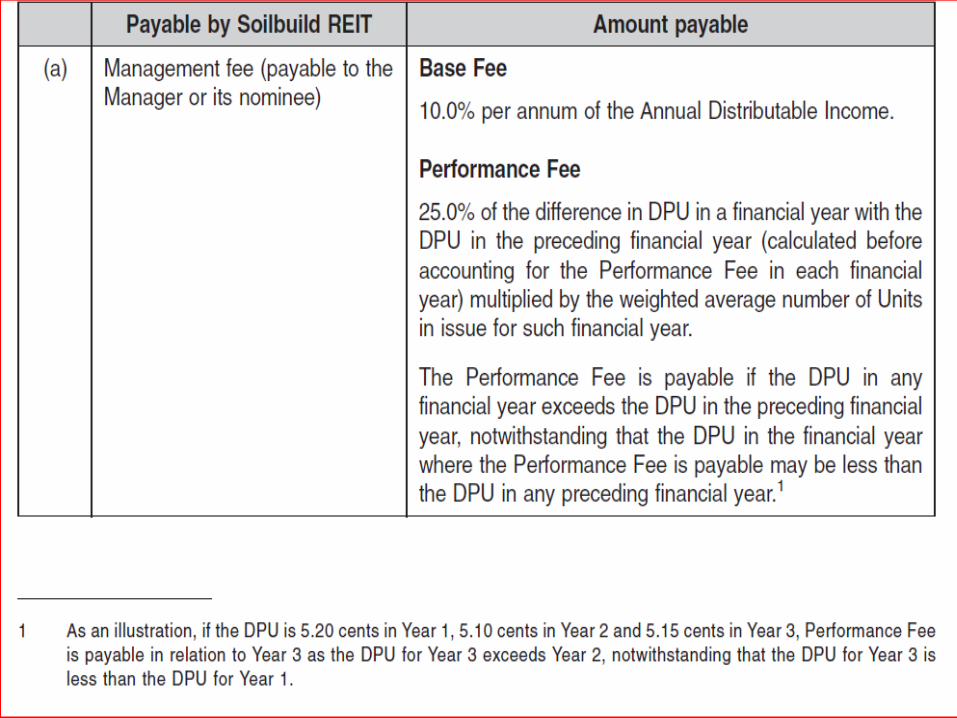

Source : http://www.soilbuildreit.com/investor-relations/announcements/

Source : http://www.soilbuildreit.com/investor-relations/announcements/

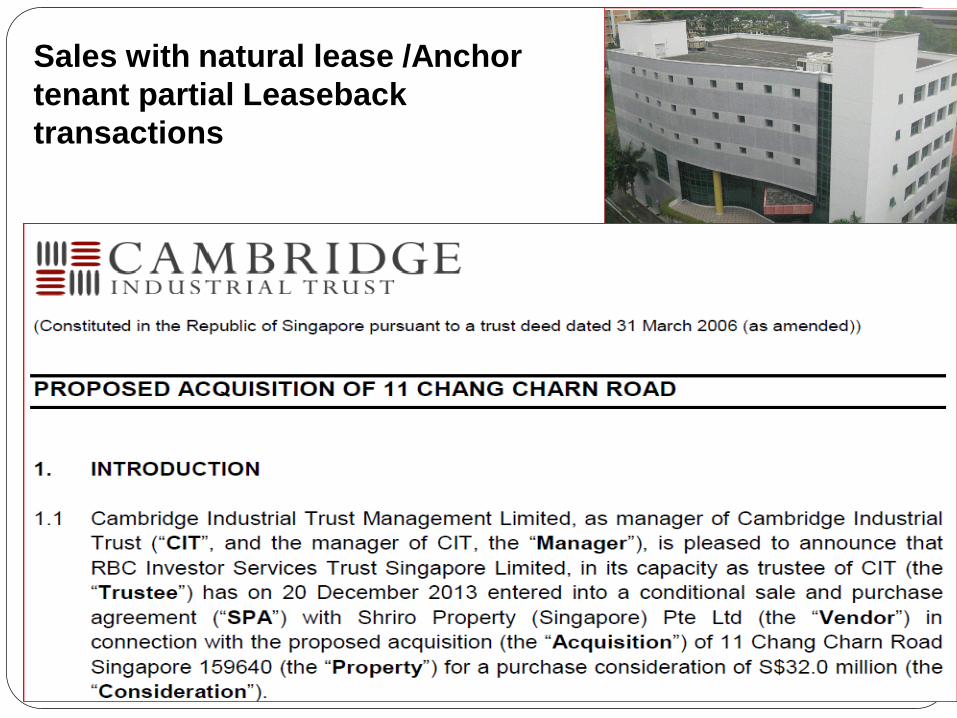

Sales with natural lease /Anchor

tenant partial Leaseback

transactions

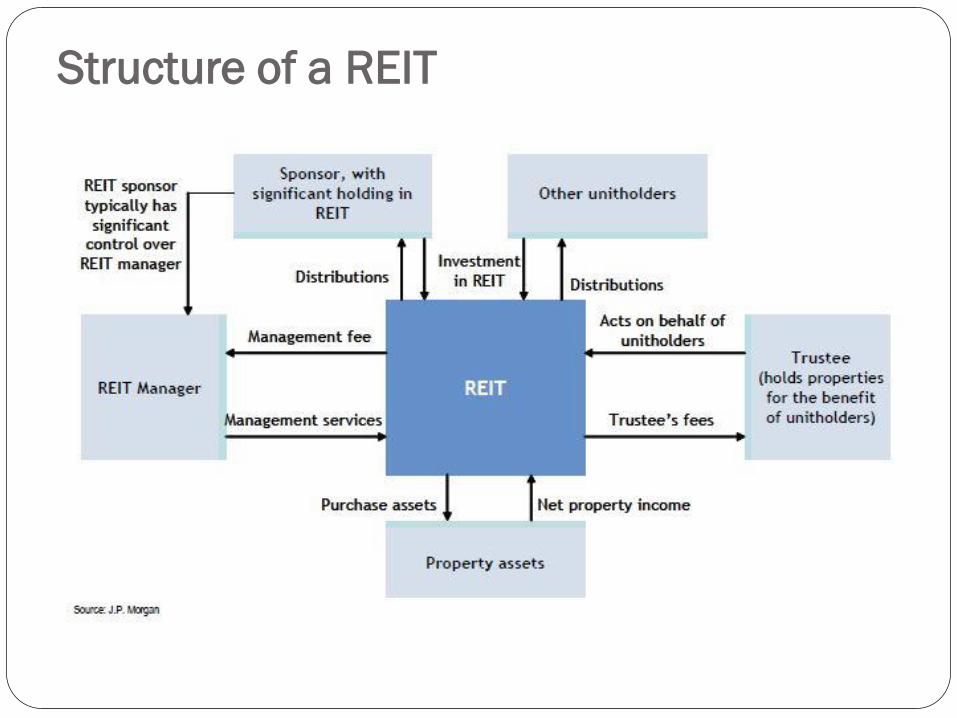

Structure of a REIT

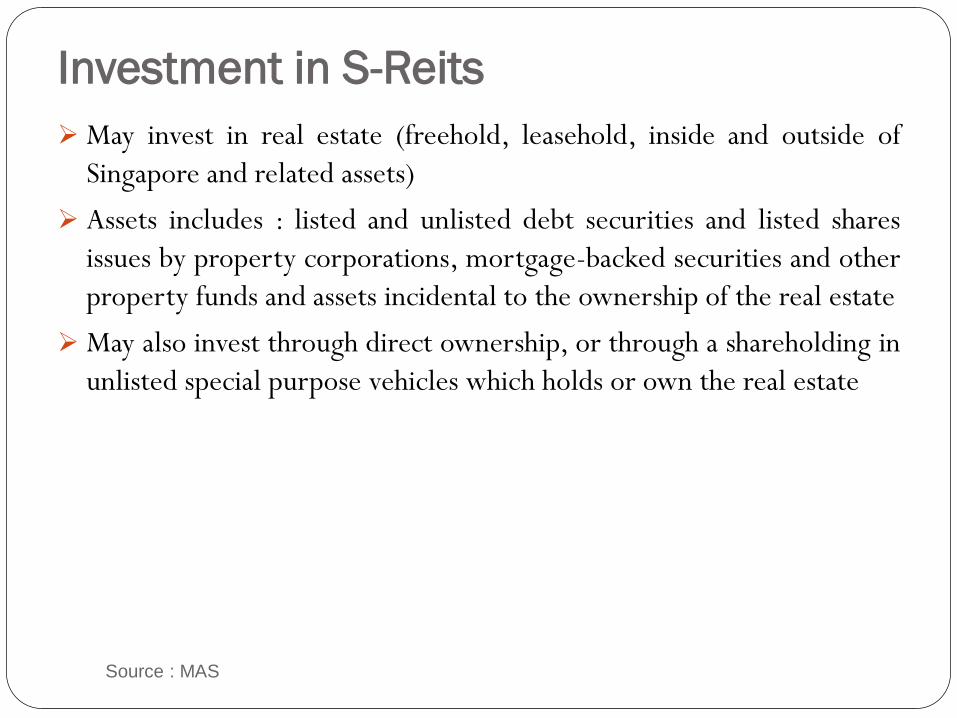

Investment in S-Reits

May invest in real estate (freehold, leasehold, inside and outside of

Singapore and related assets)

Assets includes : listed and unlisted debt securities and listed shares

issues by property corporations, mortgage-backed securities and other

property funds and assets incidental to the ownership of the real estate

May also invest through direct ownership, or through a shareholding in

unlisted special purpose vehicles which holds or own the real estate

Source : MAS

Typical fees to a REIT manager Acquisition fee: 1% of property value

Divestment fee : 0.5% of property value

Development fee : 3% of project value

New leases : 1 month for every 3 year lease; 2 month for 5 year

lease

Renewal fee : 1 month for every 5 year lease

Property management fee : 2% of gross revenue

Reimbursement of property manager costs, advertising fee,

project management fee and related staff training fee.

Source : MAS OPERA http://masnet.mas.gov.sg/opera/sdrprosp.nsf

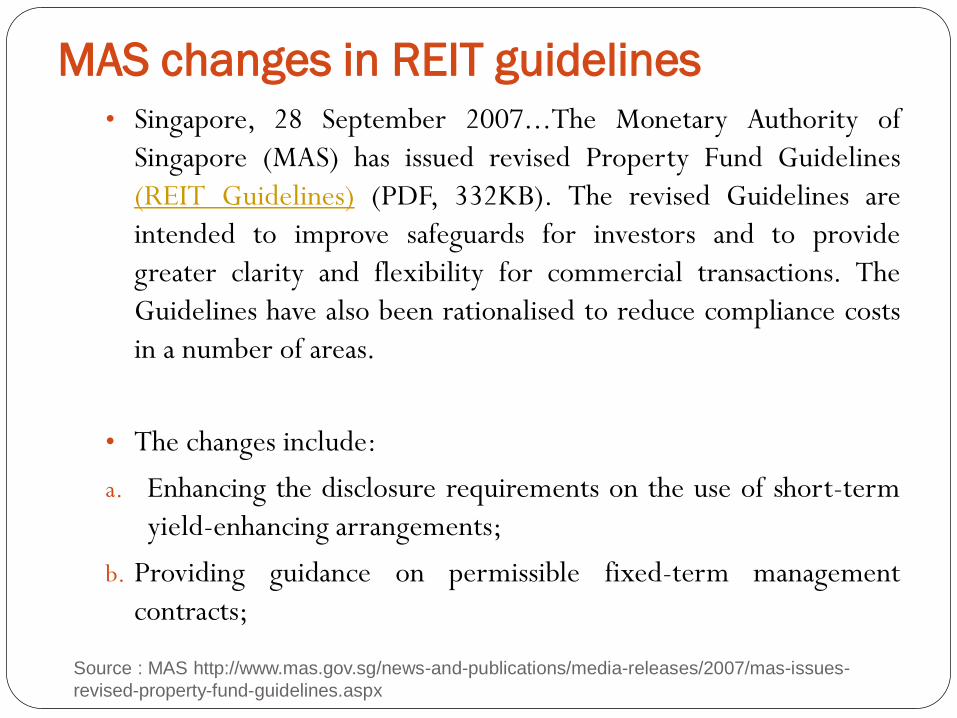

MAS changes in REIT guidelines • Singapore, 28 September 2007...The Monetary Authority of

Singapore (MAS) has issued revised Property Fund Guidelines

(REIT Guidelines) (PDF, 332KB). The revised Guidelines are

intended to improve safeguards for investors and to provide

greater clarity and flexibility for commercial transactions. The

Guidelines have also been rationalised to reduce compliance costs

in a number of areas.

• The changes include:

a. Enhancing the disclosure requirements on the use of short-term

yield-enhancing arrangements;

b. Providing guidance on permissible fixed-term management

contracts;

Source : MAS http://www.mas.gov.sg/news-and-publications/media-releases/2007/mas-issues-

revised-property-fund-guidelines.aspx

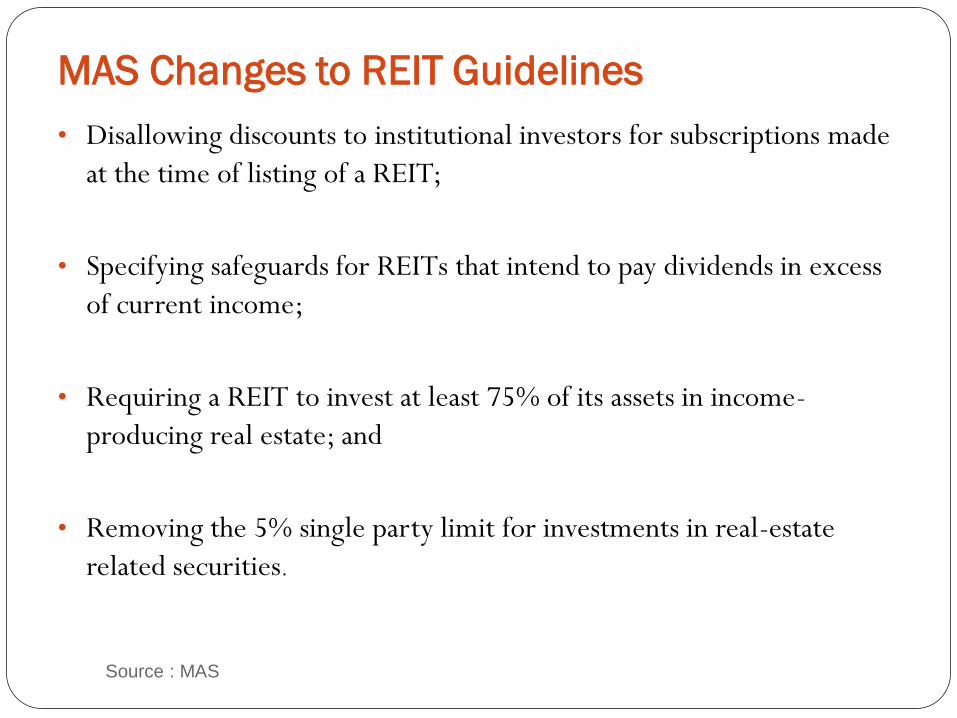

MAS Changes to REIT Guidelines

• Disallowing discounts to institutional investors for subscriptions made

at the time of listing of a REIT;

• Specifying safeguards for REITs that intend to pay dividends in excess

of current income;

• Requiring a REIT to invest at least 75% of its assets in income-

producing real estate; and

• Removing the 5% single party limit for investments in real-estate

related securities.

Source : MAS

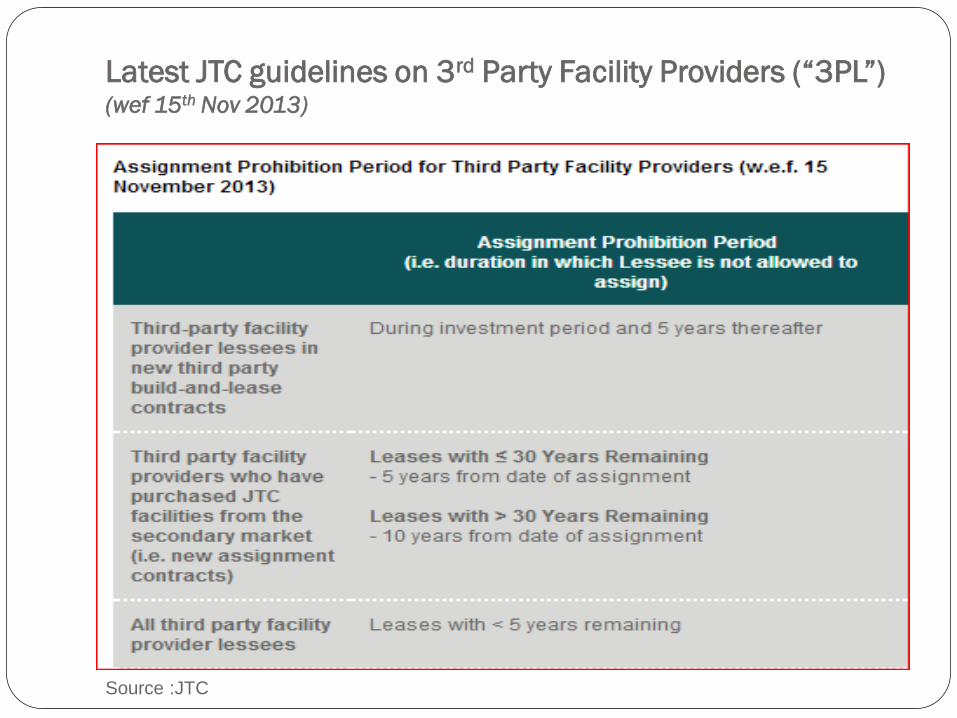

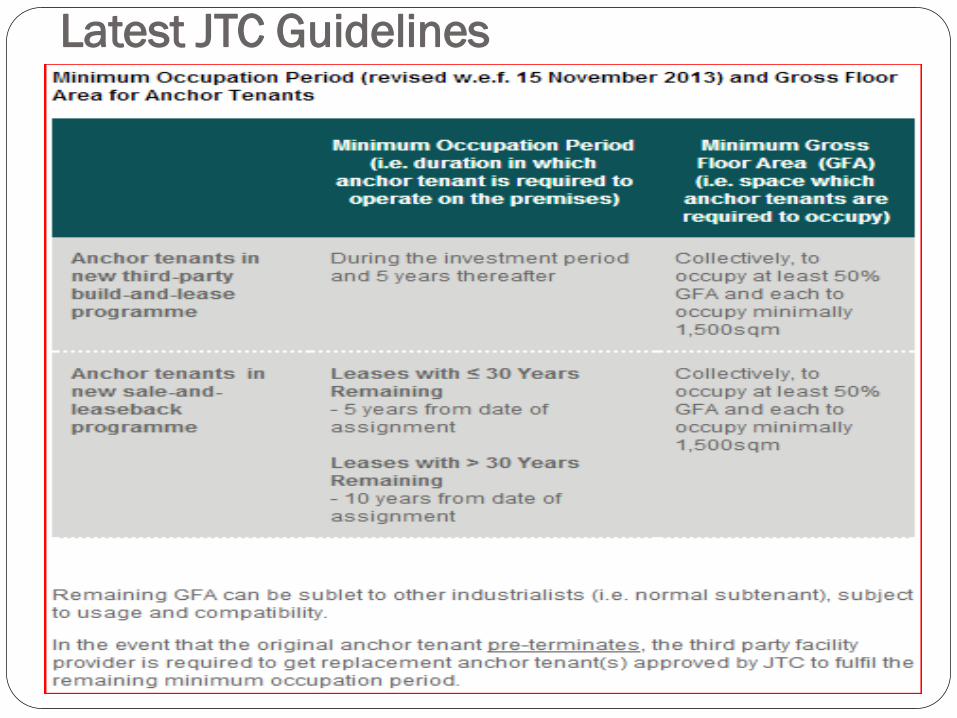

Latest JTC guidelines on 3rd Party Facility Providers (“3PL”) (wef 15th Nov 2013)

Source :JTC

Latest JTC Guidelines

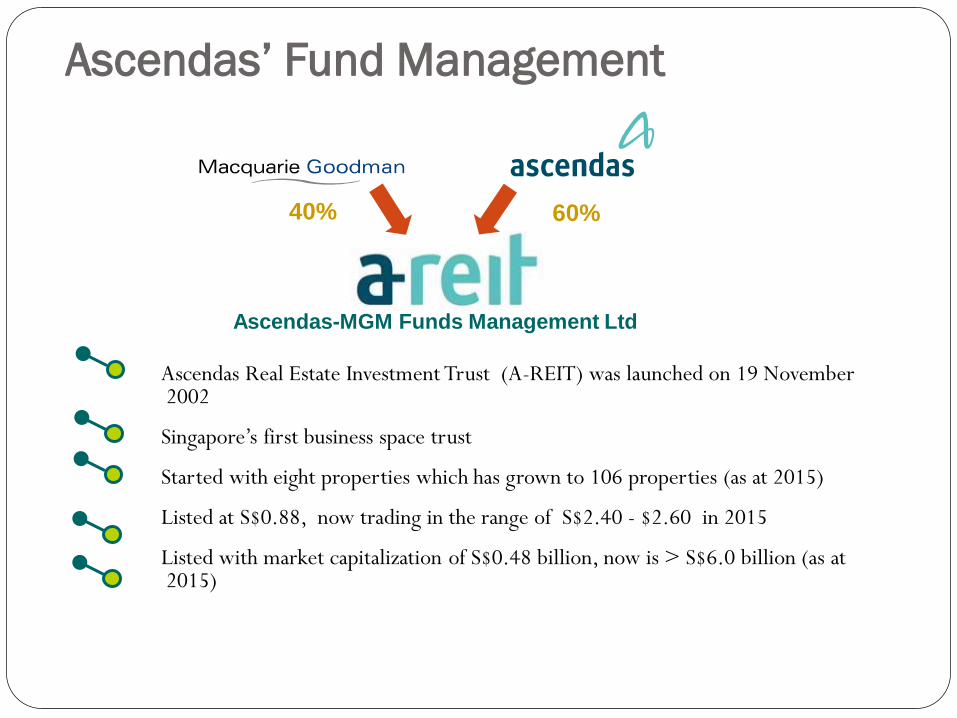

Ascendas’ Fund Management

Ascendas Real Estate Investment Trust (A-REIT) was launched on 19 November 2002

Singapore’s first business space trust

Started with eight properties which has grown to 106 properties (as at 2015)

Listed at S$0.88, now trading in the range of S$2.40 - $2.60 in 2015

Listed with market capitalization of S$0.48 billion, now is > S$6.0 billion (as at 2015)

Ascendas-MGM Funds Management Ltd

60% 40%

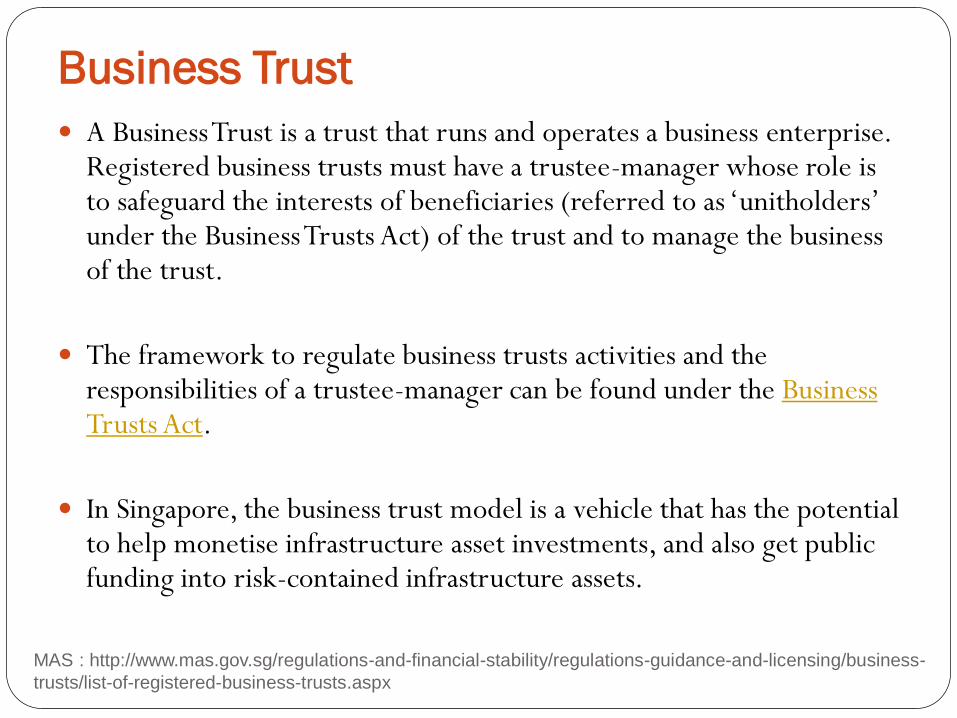

Business Trust

A Business Trust is a trust that runs and operates a business enterprise. Registered business trusts must have a trustee-manager whose role is to safeguard the interests of beneficiaries (referred to as ‘unitholders’ under the Business Trusts Act) of the trust and to manage the business of the trust.

The framework to regulate business trusts activities and the responsibilities of a trustee-manager can be found under the Business Trusts Act.

In Singapore, the business trust model is a vehicle that has the potential to help monetise infrastructure asset investments, and also get public funding into risk-contained infrastructure assets.

MAS : http://www.mas.gov.sg/regulations-and-financial-stability/regulations-guidance-and-licensing/business-

trusts/list-of-registered-business-trusts.aspx

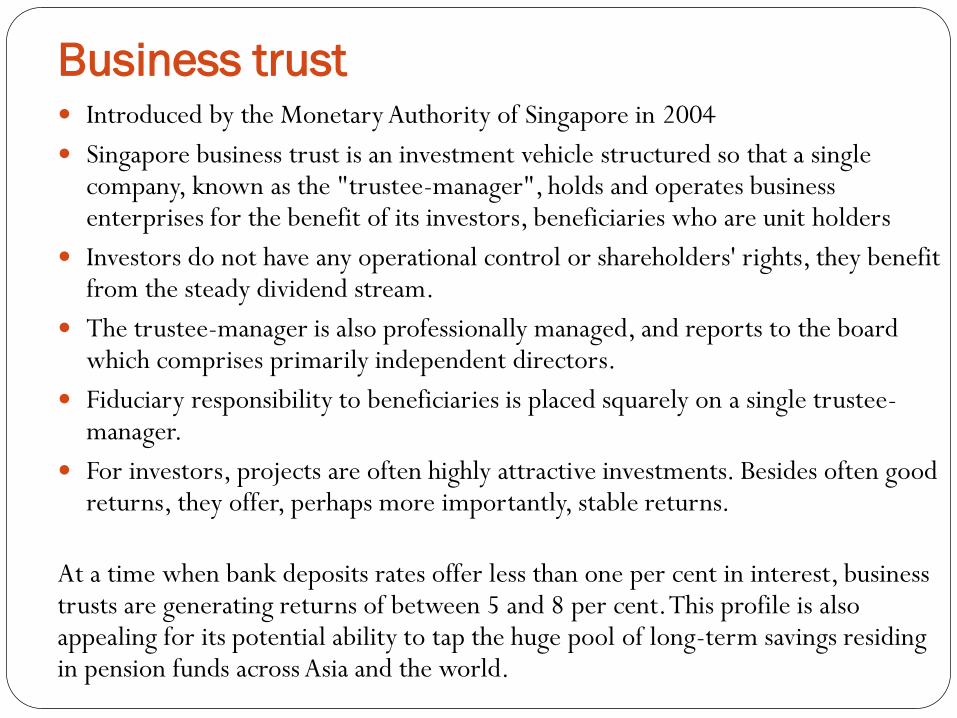

Business trust Introduced by the Monetary Authority of Singapore in 2004

Singapore business trust is an investment vehicle structured so that a single company, known as the "trustee-manager", holds and operates business enterprises for the benefit of its investors, beneficiaries who are unit holders

Investors do not have any operational control or shareholders' rights, they benefit from the steady dividend stream.

The trustee-manager is also professionally managed, and reports to the board which comprises primarily independent directors.

Fiduciary responsibility to beneficiaries is placed squarely on a single trustee-manager.

For investors, projects are often highly attractive investments. Besides often good returns, they offer, perhaps more importantly, stable returns.

At a time when bank deposits rates offer less than one per cent in interest, business trusts are generating returns of between 5 and 8 per cent. This profile is also appealing for its potential ability to tap the huge pool of long-term savings residing in pension funds across Asia and the world.

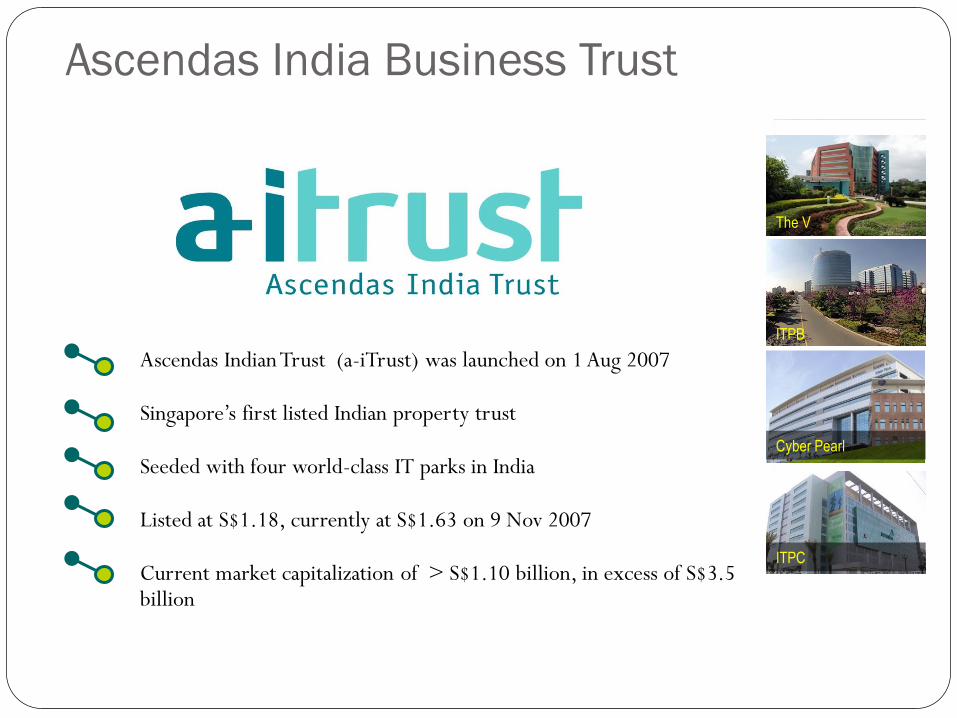

Ascendas India Business Trust

Ascendas Indian Trust (a-iTrust) was launched on 1 Aug 2007

Singapore’s first listed Indian property trust

Seeded with four world-class IT parks in India

Listed at S$1.18, currently at S$1.63 on 9 Nov 2007

Current market capitalization of > S$1.10 billion, in excess of S$3.5 billion

The V

ITPB

Cyber Pearl

ITPC

Source : Bloomberg

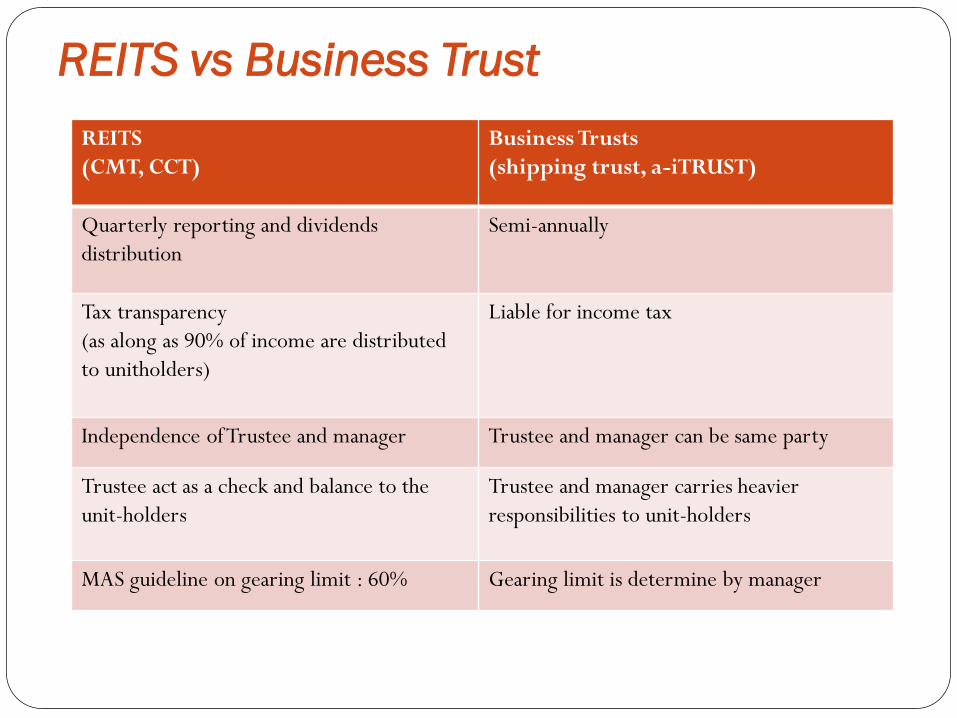

REITS vs Business Trust

REITS

(CMT, CCT)

Business Trusts

(shipping trust, a-iTRUST)

Quarterly reporting and dividends

distribution

Semi-annually

Tax transparency

(as along as 90% of income are distributed

to unitholders)

Liable for income tax

Independence of Trustee and manager Trustee and manager can be same party

Trustee act as a check and balance to the

unit-holders

Trustee and manager carries heavier

responsibilities to unit-holders

MAS guideline on gearing limit : 60% Gearing limit is determine by manager

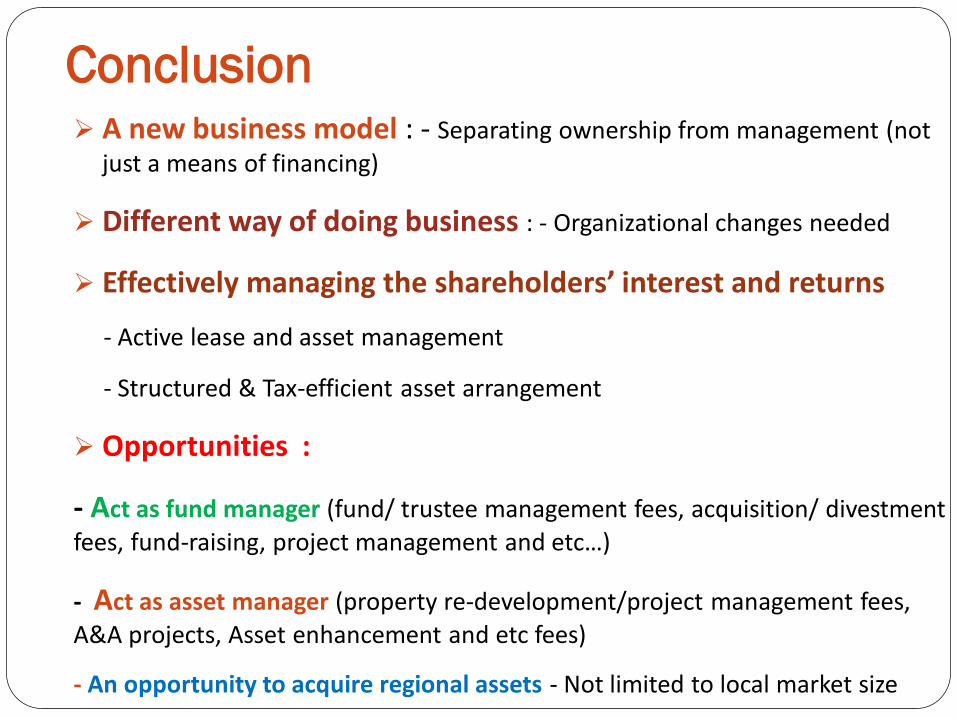

Conclusion A new business model : - Separating ownership from management (not

just a means of financing)

Different way of doing business : - Organizational changes needed

Effectively managing the shareholders’ interest and returns

- Active lease and asset management

- Structured & Tax-efficient asset arrangement

Opportunities :

- Act as fund manager (fund/ trustee management fees, acquisition/ divestment

fees, fund-raising, project management and etc…)

- Act as asset manager (property re-development/project management fees,

A&A projects, Asset enhancement and etc fees)

- An opportunity to acquire regional assets - Not limited to local market size

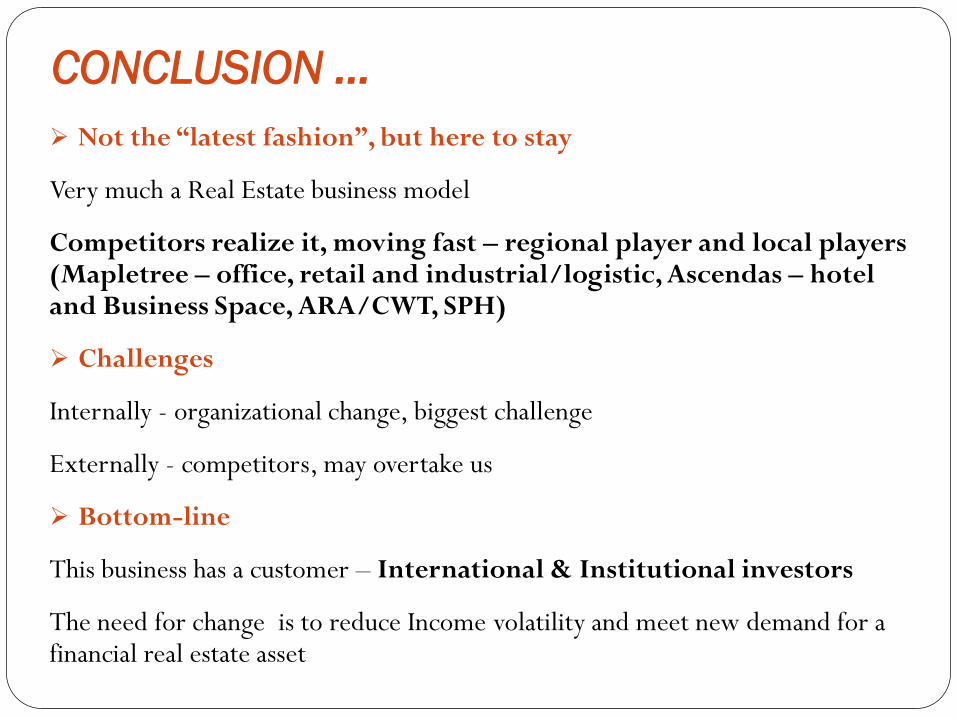

CONCLUSION …

Not the “latest fashion”, but here to stay

Very much a Real Estate business model

Competitors realize it, moving fast – regional player and local players (Mapletree – office, retail and industrial/logistic, Ascendas – hotel and Business Space, ARA/CWT, SPH)

Challenges

Internally - organizational change, biggest challenge

Externally - competitors, may overtake us

Bottom-line

This business has a customer – International & Institutional investors

The need for change is to reduce Income volatility and meet new demand for a financial real estate asset

Q & A Session &

Please assist to fill up and handover the evaluation form and

collect your certificate of attendance

C

A

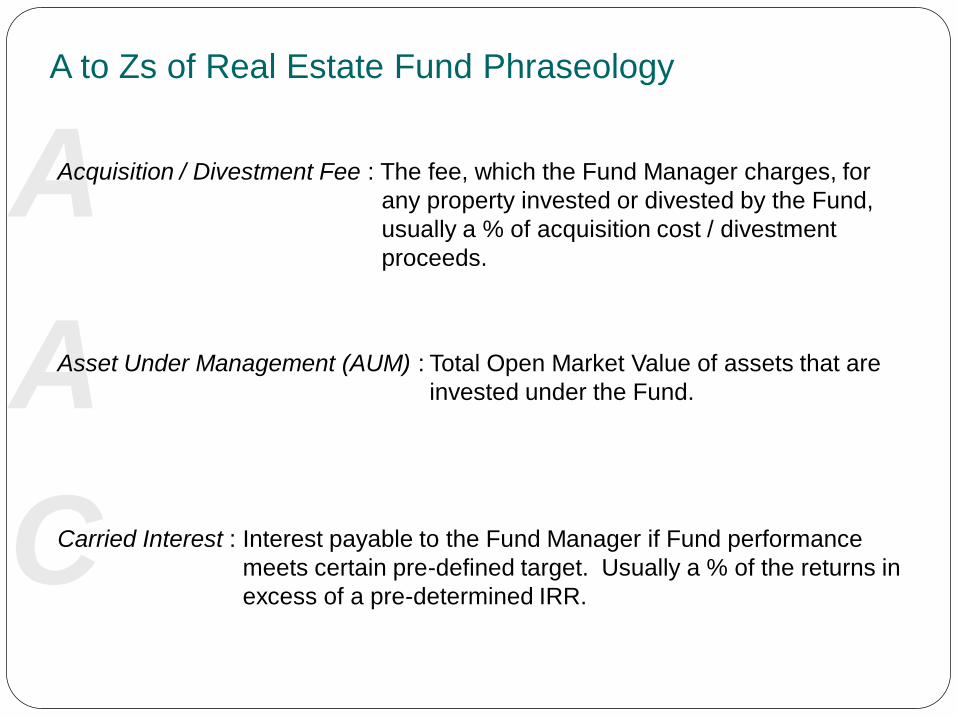

A A to Zs of Real Estate Fund Phraseology

Asset Under Management (AUM) : Total Open Market Value of assets that are

invested under the Fund.

Acquisition / Divestment Fee : The fee, which the Fund Manager charges, for

any property invested or divested by the Fund,

usually a % of acquisition cost / divestment

proceeds.

Carried Interest : Interest payable to the Fund Manager if Fund performance

meets certain pre-defined target. Usually a % of the returns in

excess of a pre-determined IRR.

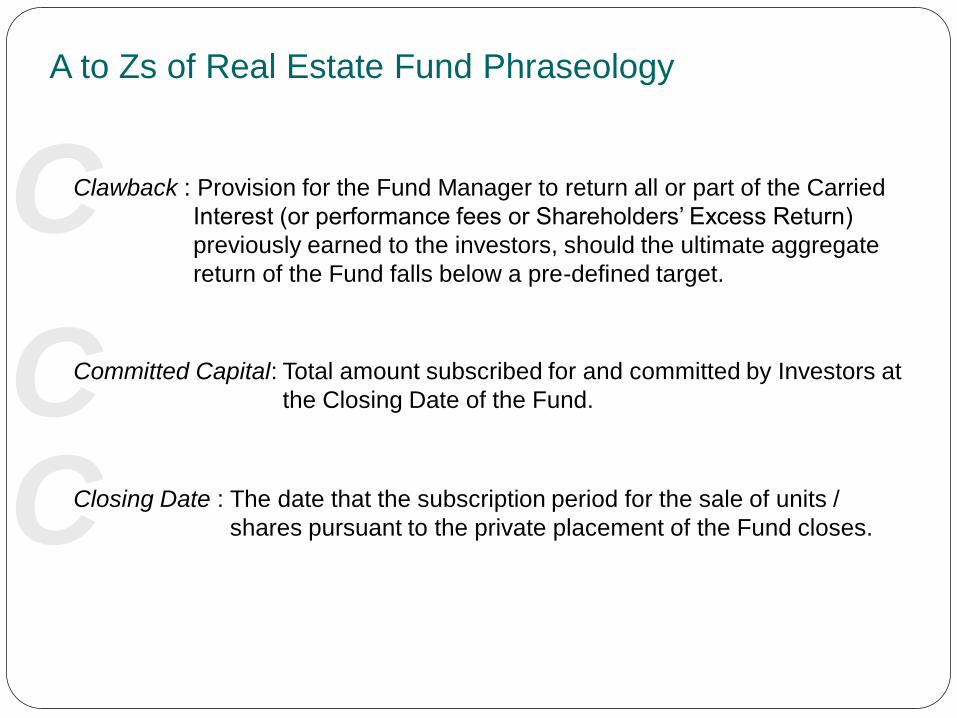

A to Zs of Real Estate Fund Phraseology

Clawback : Provision for the Fund Manager to return all or part of the Carried

Interest (or performance fees or Shareholders’ Excess Return)

previously earned to the investors, should the ultimate aggregate

return of the Fund falls below a pre-defined target.

Committed Capital: Total amount subscribed for and committed by Investors at

the Closing Date of the Fund.

Closing Date : The date that the subscription period for the sale of units /

shares pursuant to the private placement of the Fund closes. C C

C

I I

F

A to Zs of Real Estate Fund Phraseology

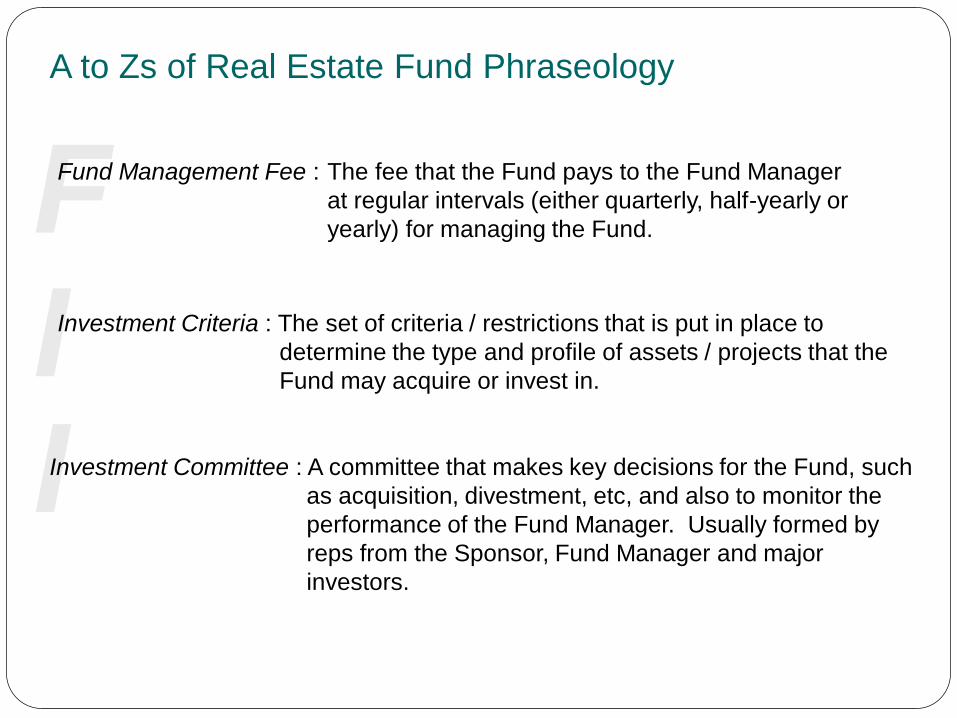

Investment Committee : A committee that makes key decisions for the Fund, such

as acquisition, divestment, etc, and also to monitor the

performance of the Fund Manager. Usually formed by

reps from the Sponsor, Fund Manager and major

investors.

Investment Criteria : The set of criteria / restrictions that is put in place to

determine the type and profile of assets / projects that the

Fund may acquire or invest in.

Fund Management Fee : The fee that the Fund pays to the Fund Manager

at regular intervals (either quarterly, half-yearly or

yearly) for managing the Fund.

I L

M

A to Zs of Real Estate Fund Phraseology

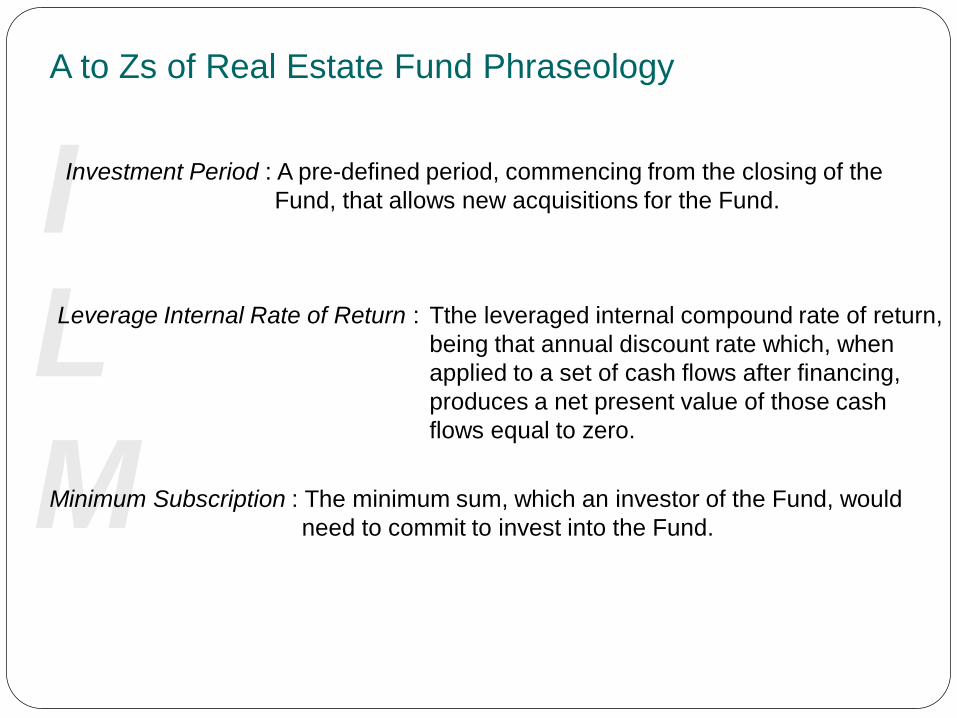

Minimum Subscription : The minimum sum, which an investor of the Fund, would

need to commit to invest into the Fund.

Leverage Internal Rate of Return : Tthe leveraged internal compound rate of return,

being that annual discount rate which, when

applied to a set of cash flows after financing,

produces a net present value of those cash

flows equal to zero.

Investment Period : A pre-defined period, commencing from the closing of the

Fund, that allows new acquisitions for the Fund.

S P P

A to Zs of Real Estate Fund Phraseology

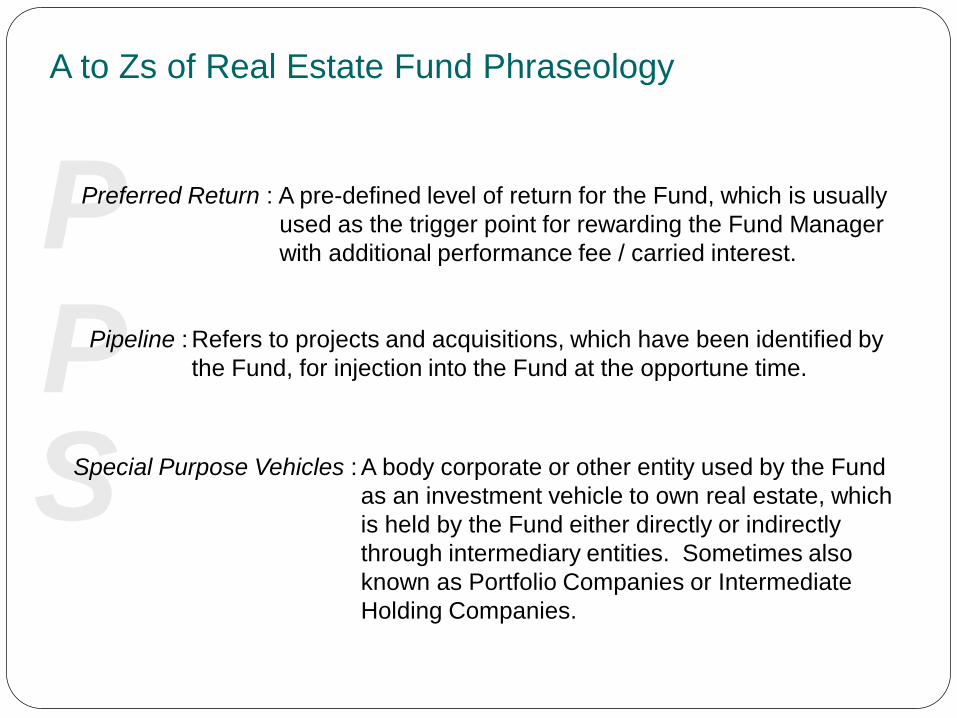

Special Purpose Vehicles : A body corporate or other entity used by the Fund

as an investment vehicle to own real estate, which

is held by the Fund either directly or indirectly

through intermediary entities. Sometimes also

known as Portfolio Companies or Intermediate

Holding Companies.

Preferred Return : A pre-defined level of return for the Fund, which is usually

used as the trigger point for rewarding the Fund Manager

with additional performance fee / carried interest.

Pipeline : Refers to projects and acquisitions, which have been identified by

the Fund, for injection into the Fund at the opportune time.

S S

S A to Zs of Real Estate Fund Phraseology

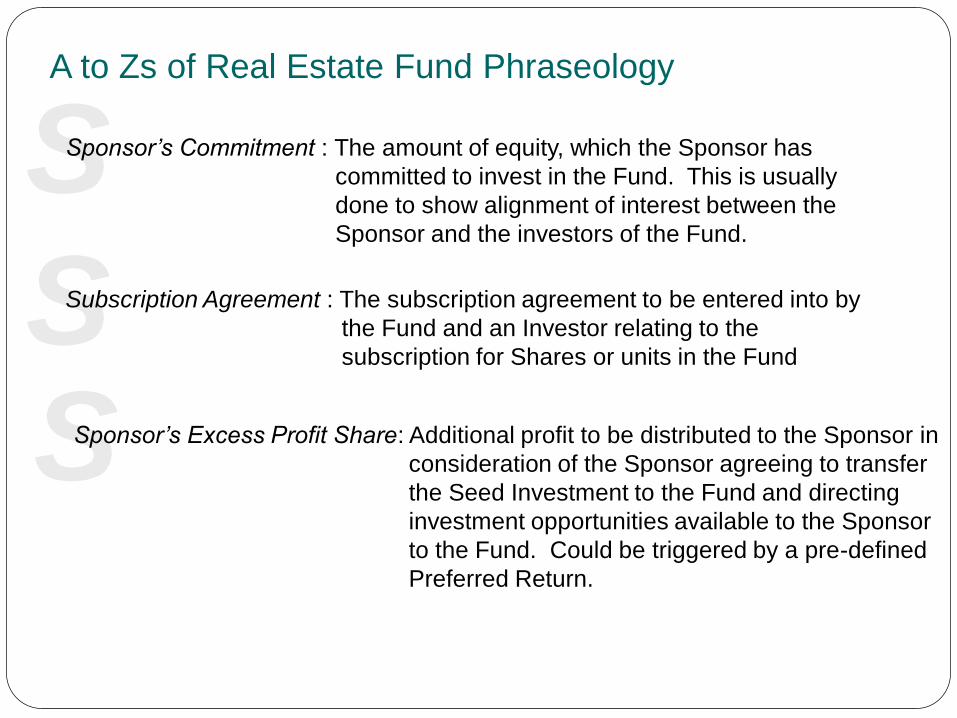

Subscription Agreement : The subscription agreement to be entered into by

the Fund and an Investor relating to the

subscription for Shares or units in the Fund

Sponsor’s Commitment : The amount of equity, which the Sponsor has

committed to invest in the Fund. This is usually

done to show alignment of interest between the

Sponsor and the investors of the Fund.

Sponsor’s Excess Profit Share: Additional profit to be distributed to the Sponsor in

consideration of the Sponsor agreeing to transfer

the Seed Investment to the Fund and directing

investment opportunities available to the Sponsor

to the Fund. Could be triggered by a pre-defined

Preferred Return.

S

T T

A to Zs of Real Estate Fund Phraseology

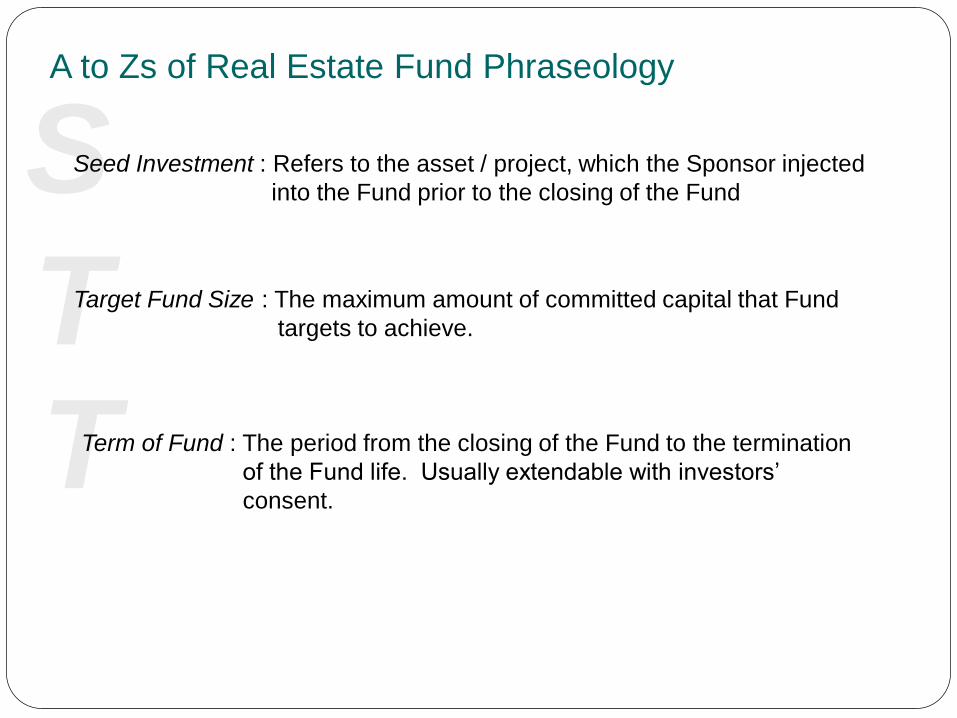

Target Fund Size : The maximum amount of committed capital that Fund

targets to achieve.

Term of Fund : The period from the closing of the Fund to the termination

of the Fund life. Usually extendable with investors’

consent.

Seed Investment : Refers to the asset / project, which the Sponsor injected

into the Fund prior to the closing of the Fund

![[Najib Razali] Islamic REITS - prres.net REITs.pdfDo Islamic REITs Behave Differently from Conventional REITs? – Empirical Evidence from Malaysian REITs Sing Tien Foo National University](https://static.documents.pub/doc/80x56/5abe8db57f8b9a7e418d14eb/najib-razali-islamic-reits-prres-reitspdfdo-islamic-reits-behave-differently.jpg)