34

Intrum Justitia and Lindorff to Combine November 14, 2016 Creating the industry leading provider of credit management services

Intrum Justitia and Lindorff to Combine

November 14, 2016

Creating the industry leading provider of credit management services

Disclaimer

IMPORTANT INFORMATION

This presentation is not and does not form a part of any offer for sale of securities. Copies of this presentation are not being made and may not be

distributed or sent into the United States, Australia, Canada, Japan or any other jurisdiction in which such distribution would be unlawful or would require

registration or other measures. Nor may the information in this presentation be forwarded, reproduced or disclosed in such a manner that contravenes such

restrictions or would require such additional prospectuses, other offer documentation, registrations or other actions.

This is not a prospectus for the purposes of Directive 2003/71/EC (together with any applicable implementing measures in any Member State, the

“Prospectus Directive”) but a presentation of a proposed combination between Intrum Justitia and Lindorff.

The securities referred to in this presentation have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the “Securities

Act”), and accordingly may not be offered or sold in the United States absent registration or an exemption from the registration requirements of the

Securities Act and in accordance with applicable U.S. state securities laws.

Matters discussed in this presentation may constitute forward-looking statements. Forward-looking statements are statements that are not historical facts

and may be identified by words such as “believe,” “expect,” “anticipate,” “intend,” “estimate,” “will,” “may,” “continue,” “should” and similar expressions. The

forward-looking statements in this presentation are based upon various assumptions, many of which are based, in turn, upon further assumptions. Although

Intrum Justitia believes that these assumptions were reasonable when made, these assumptions are inherently subject to significant known and unknown

risks, uncertainties, contingencies and other important factors which are difficult or impossible to predict and are beyond its control. Such risks, uncertainties,

contingencies and other important factors could cause actual events to differ materially from the expectations expressed or implied in this presentation by

such forward-looking statements. The information, opinions and forward-looking statements contained in this presentation speak only as at its date, and are

subject to change without notice.

The combined financial information set out in this presentation is only an aggregation of financial information taken from each company's financial reporting

in order to provide an indication of the new group's sales, earnings, etc. under the assumption that the activities had been included in the same group from

the beginning of each period. The aggregation is based on a hypothetical situation and should not be viewed as pro forma since adjustments for the effects

of future acquisitions analyses, various accounting standards and transaction costs have not yet been possible to make. Future synergies have not been

taken into account. The financial information has not been audited or otherwise reviewed by the companies’ auditors.

Today’s presenters

1

Lars Lundquist

Chairman of Intrum Justitia

Kristoffer Melinder

Managing Partner at

NC Advisory AB, advisor to

the Nordic Capital Funds

Today’s presenters (cont’d)

2

Mikael Ericson

President and CEO

Intrum Justitia

Klaus-Anders Nysteen

President and CEO

Lindorff

Table of contents

Transaction Highlights

Overview of Intrum Justitia and Lindorff

Strategic Rationale

Synergies and Financial Impact

Timetable

Appendix

Conclusion

Intrum Justitia and Lindorff - a highly compelling combination…

Industry leader with unparalleled scale and diversification

Excellent strategic fit with a well-balanced business mix and

integrated service offering

Complementary geographical footprint, sector expertise and

debt purchasing platforms

Strong cultural fit based on Nordic heritage and longstanding

commitment to fair collection

Ideally positioned for growth through investments in new asset

classes, segments and geographies

Significant shareholder value creation from cost and revenue

synergies

3

Considerable

synergies

Significant financial

benefits

Capital structure

optimization

● Estimated SEK 0.8bn of cost

synergies per annum to be

fully phased in 3-4 years from

closing of the transaction

● Cost synergies arising mainly

from consolidation of

operations in overlapping

countries and IT

● Revenue synergies from

combination of databases,

cross-selling and improved

cross-border offering

● Transaction accretive to

Intrum Justitia’s EPS from first

year (excluding non-recurring

items1)

● Intrum Justitia’s EPS

estimated to grow in excess of

75% on a cumulative basis in

3-4 years as synergies are

fully realised

● Combined entity to benefit

from greater scale,

diversification and cash flow

visibility

● Transaction allows both

parties to achieve a more

optimal capital structure

● Pro-forma net debt/cash

EBITDA as of 30 September

2016 is 3.6x and is expected

to reach around 3.0x over the

medium term

…creating significant value for shareholders

Note: (1) Mainly transaction costs and synergy implementation costs.

4

Snapshot of the combined entity

Source: Company information.

Note: The combined financial information on this slide is not financial pro forma information, and has not been audited or otherwise reviewed by the companies’ auditors.

(1) LTM Q3’16 figures. Lindorff‘s net revenue and EBITDA converted using EURSEK average FX rate of 9.357 for the LTM Q3’16 period. Lindorff’s portfolio carrying value converted using EURSEK FX rate of 9.626 for the LTM Q3’16 period end;

(2) Based on Lindorff’s LTM Q3’16 net revenue and EBITDA excluding non-recurring items and pro forma for acquisitions; (3) Based on YTD Q3’16 net revenues. Geographical breakdown for illustrative purposes only and not consistent with the

companies’ existing reporting. Northern Europe includes Denmark, Estonia, Finland, Latvia, Lithuania, Netherlands, Norway, Poland and Russia. Central and Eastern Europe includes Austria, Czech Republic, Germany, Hungary, Switzerland and

Slovakia. Western Europe includes Belgium, England, France, Ireland and Scotland. Southern Europe includes Italy, Portugal and Spain; (4) Based on LTM Q3’16 net revenues. Aktua consolidated since 1 June 2016.

Key financial

metrics1

Geographical

mix3

● Net Revenue: SEK 5.8bn

● EBITDA: SEK 2.0bn

● Portfolio Carrying Value: SEK 8.1bn

● Net Revenue: SEK 6.4bn2

● EBITDA: SEK 2.9bn2

● Portfolio Carrying Value: SEK 10.4bn

Northern Europe Central and Eastern Europe Western Europe Southern Europe

Purchased Debt Debt Collection Other

47%

30%

16%

7%

62% 11%

27%

5

Business

mix4

44%

54%

2%

49%

47%

4%

● Net Revenue: SEK 12.2bn

● EBITDA: SEK 4.9bn

● Portfolio Carrying Value: SEK 18.5bn

54%

20%

8%

18%

46%

51%

3%

|

Transaction summary

Note: (1) Lindorff’s implied EV of EUR 4.1bn based on Lindorff’s EUR 2,291m net debt as of 30 September 2016, Intrum Justitia's closing share price of SEK 278.30 on 11 November 2016 at Nasdaq Stockholm and ECB EURSEK FX rate of 9.861 as

of 11 November 2016. Lindorff’s EUR 310m LTM Q3’16 EBITDA excluding non recurring items and pro forma for acquisitions.

6

Consideration

Ownership

● Intrum Justitia and Lindorff shareholders to own approximately 53% and 47%, respectively

● Nordic Capital Fund VIII to become the largest indirect shareholder in the combined entity and to remain a supportive

shareholder post-transaction

● All stock transaction – Lindorff shareholders to receive 64.2m newly issued shares in Intrum Justitia

● Transaction implies an enterprise value of Lindorff of SEK 40.5bn, representing an EV/EBITDA multiple of 13.2x1

Governance

● Combined entity to be listed on Nasdaq Stockholm with legal headquarters in Stockholm and centres of excellence in

both Oslo and Stockholm

● Combined entity to have eight board members of which entities controlled by Nordic Capital Fund VIII expects to

nominate three

● CEO of the combined entity to be appointed at the latest upon closing

Timetable ● Intrum Justitia EGM to be held on December 14th to approve the transaction

● Closing expected in Q2 2017 subject to competition and regulatory authority approvals

Benefits for all stakeholders

7

Shareholders ● Expected significant value creation from cost and revenue synergies

● Ability to drive long-term shareholder value through a unique position in an attractive market

Debt investors ● Attractive risk profile with unparalleled scale and diversification

● High earnings visibility and stable cash flows

Clients ● Strengthened collection performance

● Significant investments in IT, product development and compliance infrastructure

Customers ● Commitment to highest ethical standards and fair collection practices

● Investments in digitalization and simplified customer service

Employees ● Enhanced career opportunities through better positioned pan-European platform and multiple growth initiatives

Regulators ● Best-in-class compliance framework and collection practices

Table of contents

Transaction Highlights

Overview of Intrum Justitia and Lindorff

Strategic Rationale

Synergies and Financial Impact

Timetable

Appendix

Conclusion

8

Snapshot of Intrum Justitia

Intrum Justitia highlights

● Founded in Sweden in 1923 and listed on Nasdaq Stockholm since

2002

● A European leader offering a complete range of credit management

services

● Operating across 20 European countries with approximately 4,000

employees and 75,000 clients

Purchased Debt portfolio carrying value mix1

EBITDA evolution (SEKm)

Note: (1) As of 31 December 2015.

Key financials

SEKm LTM Q3’16

Net revenues 5,765

Cash EBITDA 3,554

EBITDA 1,967

EBIT 1,804

Portfolio carrying value (PD) 8,059

678 759 880 833 902 1,041 1,066 1,364

1,601 1,787 1,967

'06A '07A '08A '09A '10A '11A '12A '13A '14A '15A LTMQ3'16

59% 18%

11%

12%

Financial Institutions Telecom Retail Other

Snapshot of Lindorff

9

SEKm LTM Q3’16

LTM Q3’16

Pro forma3

Net revenues 5,708 6,416

Cash EBITDA 3,902 4,370

EBITDA 2,442 2,904

EBIT 1,488 2,365

Portfolio carrying value (PD)5 10,425 N/A

Key financials2

Purchased Debt portfolio carrying value mix1 Lindorff highlights

● Founded in Oslo in 1898 with over 100 years of growth and

value creation

● A leading integrated credit management partner for financial

institutions in Europe

● Operating across 13 European countries with over 4,400 employees

and 20,000 clients

Note: (1) As of 31 December 2015; (2) Converted using EURSEK average FX rate of 9.357 for the LTM Q3’16 period; (3) Converted using the exchange rate for the period and excluding non recurring items and pro forma for acquisitions. Other period

figures converted at constant exchange rate; (4) LTM Q3’16 EBITDA and EBIT excluding non recurring items and pro forma for acquisitions of EUR 310m and EUR 253m, respectively; (5) Converted using EURSEK FX rate of 9.626 as of 30 September

2016; (6) CAGR calculated for comparable IFRS basis financials since 2011. Prior period accounted under local GAAP.

Cash EBITDA evolution (SEKm)

'06A '07A '08A '09A '10A '11A '12A '13A '14A '15A LTMQ3'16

4,3702,3

88%

5%

Financial Institutions Telecom Retail Other

2% 5%

4

4

Lindorff – a journey of growth and value creation

Note: (1) Entered into long term strategic partnership with large portfolio acquisition and subsequent forward flow; (2) Full time equivalents on-boarded in last 5 years through carve-outs.

Founded by

Eynar

Lindorff

Co-investments

2015–2016

Secured servicing

2015–2016

Nordic

expansion European expansion European leadership

2007–2013 2013–2016

Growth drivers

Organic

M&A

New market

entries

Carve-outs

2003–2007

2012 2014 2015 2016 1898 2001 2013 2005 2003 2010 2011 2007 2009

1

x3 x3

Unique track

record

● 10 large transactions in last 5 years

● 1,350 FTEs2 on-boarded

Strong client

relationships

● Trusted and preferred relationship

● IT integration and operation

● SLA execution

● Integrated operations with clients

● KPI reporting

Strong

pipeline

Existing markets New markets

10

16% 15% 15% 17%

2013 2014 2015 LTM Q3'16

Return on Purchased Debt (per Lindorff's definition)

Lindorff – proven financial performance

11

Strong performance from Purchased Debt portfolios…

…driving steady growth in Debt Collection revenues2 (SEKm)

Note: (1) Based on top 10 clients in every market; (2) Financials, as reported, converted using the average EURSEK FX rate for the respective periods.

Long standing client relationships…

…with attractive returns

3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Average Actual Collection as % of Forecast

105%

1,972 2,165

2,320 2,695

2013 2014 2015 LTM Q3'16

~ 9 years

Avg. Debt Collection client relationship age1

~ 7 years

Avg. carve-out remaining contract life

Table of contents

Transaction Highlights

Overview of Intrum Justitia and Lindorff

Strategic Rationale

Synergies and Financial Impact

Timetable

Appendix

Conclusion

Combined group uniquely positioned to capture market opportunity Strong NPL sale growth primarily driven by banks’ continued deleveraging

12

145–150 150–160 155–170

48

95

191

11

36 46

84 91

122 140

195

250

353

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Source: Consulting company report; Company information.

Note: (1) Asset Quality Review; (2) Effective for annual periods beginning on or after Jan 1, 2018 (if not voluntarily applied earlier).

European NPL sale scenarios (EURbn)

Base case Deleveraging scenario

Acceleration of Banks’ NPL sales drivers

● AQR1 driven increase in

bank provisioning

• Ability to recognise

potential gain on sale

• Higher stock of NPLs

from reclassification

● Higher capital requirements

against NPLs

● IFRS 92 – Expected loss

accounting driving banks to

dispose of NPLs earlier in

credit cycle

● Reduction in earnings

volatility from provisioning

and losses

Accounting Regulatory

Combined group uniquely positioned to capture market opportunity (cont’d) Set to capture a market >5x larger than historical core target market

Source: Company information.

13

Significant potential from large untapped market segments

126

284

324

324

323

734

B2Cunsecured

B2Csecured

B2BSME & corporate

TotalEurope

European stock of NPLs (EURbn) as of 2015

647 1,058

Expanded capabilities in the NPL market

B2C

B2B

Further

expansion

(Aktua core)

Opportunistic

Intrum Justitia /

Lindorff historical

core

Potential

extension

Unsecured Secured

B2C & SME Corporate

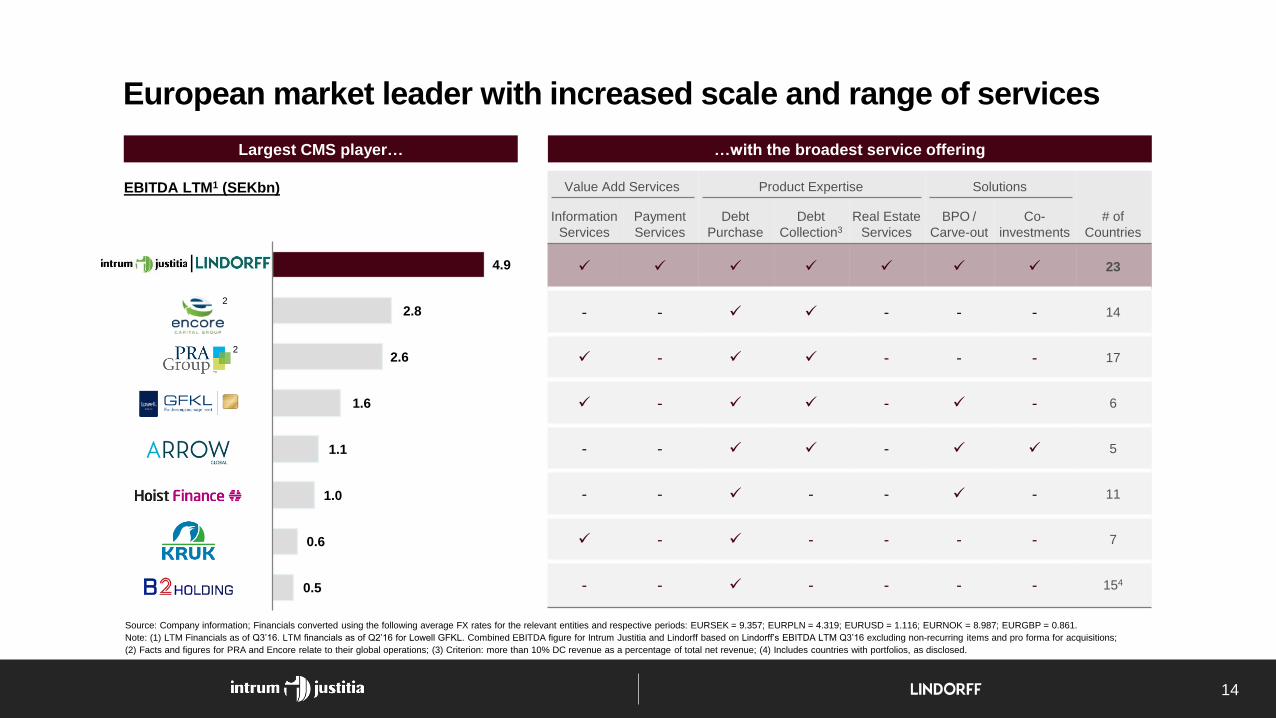

European market leader with increased scale and range of services

14

Source: Company information; Financials converted using the following average FX rates for the relevant entities and respective periods: EURSEK = 9.357; EURPLN = 4.319; EURUSD = 1.116; EURNOK = 8.987; EURGBP = 0.861.

Note: (1) LTM Financials as of Q3’16. LTM financials as of Q2’16 for Lowell GFKL. Combined EBITDA figure for Intrum Justitia and Lindorff based on Lindorff’s EBITDA LTM Q3’16 excluding non-recurring items and pro forma for acquisitions;

(2) Facts and figures for PRA and Encore relate to their global operations; (3) Criterion: more than 10% DC revenue as a percentage of total net revenue; (4) Includes countries with portfolios, as disclosed.

Largest CMS player… …with the broadest service offering

4.9

2.8

2.6

1.6

1.1

1.0

0.6

0.5

EBITDA LTM1 (SEKbn) Value Add Services Product Expertise Solutions

# of

Countries

Information

Services

Payment

Services

Debt

Purchase

Debt

Collection3

Real Estate

Services

BPO /

Carve-out Co-

investments

23

- - - - - 14

- - - - 17

- - - 6

- - - 5

- - - - - 11

- - - - - 7

- - - - - - 154

|

2

2

54%

20%

8%

18%

A truly pan-European credit management services platform

Revenue split by region1 (%) Complementary pan-European presence

Note: (1) Based on YTD Q3’16 net revenues. Geographical breakdown for illustrative purposes only and not consistent with the companies’ existing reporting. Northern Europe includes Denmark, Estonia, Finland, Latvia, Lithuania, Netherlands, Norway,

Poland and Russia. Central and Eastern Europe includes Austria, Czech Republic, Germany, Hungary, Switzerland and Slovakia. Western Europe includes Belgium, England, France, Ireland and Scotland. Southern Europe includes Italy, Portugal and Spain.

47%

30%

16%

7%

62% 11%

27%

Intrum Justitia and Lindorff

Intrum Justitia only

Lindorff only

15

|

Northern Europe Central and Eastern Europe

Western Europe Southern Europe

Strong strategic fit maintaining a balanced business model…

Business mix by revenue1 (%)

46%

51%

3%

44%

54%

2%

49% 47%

4%

Net Revenue:

SEK 5.8bn

Net Revenue:

SEK 12.2bn

Net Revenue2:

SEK 6.4bn

Purchased Debt Debt Collection Other

Note: (1) Based on LTM Q3’16 net revenues. Aktua consolidated since 1 June 2016 for revenue split calculations; (2) Lindorff’s LTM Q3’16 net revenue pro forma for acquisitions converted using an EURSEK average FX rate of 9.357 for the LTM

Q3’16 period.

16

|

…and enhancing synergies between Purchased Debt and Debt Collection

17

High complementarity between PD and DC… …resulting in tangible benefits

Flexibility

Origination

strength

● Full service offering to meet clients’ evolving needs

● Large portion of portfolio purchases originated

from existing Debt Collection clients

Operational

efficiencies

● Combined scale with more than SEK 5bn of

monthly collections

Data analytics ● More than SEK 680bn of debt under management

Financial benefits ● Capital light earnings from Debt Collection create

capacity for portfolio purchases

Origination

Operational scalability

Database and analytics

Collection strategies

Standardised processes

76%

10%

6%

8%

Highly complementary Purchased Debt portfolios and capabilities

Purchased Debt by vendor1 (%)

59%

18%

11%2

12%

88%

5%

2% 5%

Average Ticket Size:

c. SEK 9.3k

Average Ticket Size:

c. SEK 15.4k

Average Ticket Size:

c. SEK 28.9k

Financial Institutions Telecom Retail Other

PD Carrying Value:

SEK 7.0bn

PD Carrying Value:

SEK 16.8bn

PD Carrying Value:

SEK 9.8bn

Note: (1) Purchased Debt carrying value as of 31 December 2015. Lindorff’s financials converted using EURSEK FX rate of 9.198. Breakdown according to companies’ respective internal classifications.

18

|

Combined group uniquely positioned to drive profitable growth

Payment

solutions

● Leverage competences at ByJuno, Avarda and Lindorff Payment to benefit from fast growing online payments

● Partnership with Bambora in the Nordic region to benefit from combined capabilities

Secured market ● Deploy secured market and valuation expertise (incl. from Aktua) across combined geographic footprint

● Large untapped market – well suited for co-investments

Real estate

services (RES) ● Leverage unique competence (incl. from Aktua) in markets with a need for RES (eg. Italy, Netherlands and France)

SME ● Ongoing momentum at both companies to develop largely untapped profitable segment

● Capitalise on Intrum Justitia’s recent acquisitions

New geographies ● Assess new markets with attractive return potential

● Follow existing clients across expanded footprint and to new countries

Accretive

bolt-on M&A

● Continue strategy of selectively consolidating highly fragmented European market

● Focus on small, accretive bolt-on acquisitions

19

Co-investments ● Accelerated growth in Debt Collection revenues driven by full servicing of large assets acquired together with co-investors

● Ability to address the entire breadth of the NPL market and to execute on larger transactions providing data benefits

Table of contents

Transaction Highlights

Overview of Intrum Justitia and Lindorff

Strategic Rationale

Synergies and Financial Impact

Timetable

Appendix

Conclusion

Significant cost and revenue synergies to accelerate earnings growth

Note: Actual synergies and other cost savings, including the costs required to achieve these synergies and savings, may differ materially from the current expectations, and neither Intrum Justitia nor Lindorff can assure investors that they will achieve

the full amount of these estimated synergies on schedule or at all.

Cost synergies Revenue synergies

● Combination of datasets and business

intelligence driving improved collection

performance

● Improved cross-border offering

● Cross-selling of complementary offerings to

existing customers

● Strengthened Purchased Debt capabilities

20

● Estimated SEK 0.8bn of cost synergies per annum, fully

phased in 3-4 years following closing of the transaction

• Consolidation of administrative and support functions

• Optimisation of operations center network

• Harmonization of IT systems and IT infrastructure as

well as application development/maintenance

• Increased scale in procurement volumes

● Estimated implementation costs of SEK 1.0bn incurred

over the first two years following closing of the

transaction

Significant financial benefits

EPS

growth

● Transaction is accretive to Intrum Justitia’s EPS from the first year after closing, excluding synergy implementation and

transaction costs1

● Intrum Justitia’s EPS is estimated to grow in excess of 75% on a cumulative basis in three to four years as the

synergies are fully realized

Dividend

● Intrum Justitia’s board intends to propose an ordinary dividend for 2016 to the current shareholders of Intrum Justitia,

in line with the current dividend policy

• New shares issued to Lindorff shareholders are not entitled to the dividend for 2016

● Existing Intrum Justitia dividend policy to be maintained post-closing

Optimised

capital

structure2

Note: (1) Transaction costs including financing, legal, advisory and other fees (excluding take out costs for existing financing structures) amount to approximately 1.5% of the combined entities’ enterprise value implied by Intrum Justitia’s share price

as of November 11, 2016 ; (2) Net debt/cash EBITDA based on LTM Q3’16 financials, Lindorff cash EBITDA excluding non-recurring items and pro forma for acquisitions.

2.0x

4.9x

~3.6x

~3.0x

Medium term

21

|

Fully underwritten financing providing certainty and financial flexibility

● All share transaction

● New financing structure will be put in place to partially refinance existing debt structures1

● EUR 3.4bn bridge facility and EUR 850m super senior revolving credit facility (RCF)2 fully

underwritten by Goldman Sachs, J.P. Morgan and Morgan Stanley

• Bridge facility has a tenor of 5 years, providing certainty of long-term financing – however expected

to be taken out by issuance of new unsecured bonds

• RCF to support combined entity's liquidity requirements and to facilitate pursuing future investment

opportunities

● Combined entity’s financing costs expected to be substantially lower post-refinancing compared to

the pro-forma financing cost based on current capital structures3

22

Note: (1) Including substantially all of Lindorff’s financial indebtedness including its senior secured and senior notes and RCF; (2) RCF tenor of 4.5 years; (3) The refinancing of Lindorff's existing bonds will result in certain redemption costs, the size of

which depends on timing of the refinancing. The redemption costs are expected to be more than offset by the value of lower interest expenses on the new bonds relative to Lindorff's existing outstanding bonds.

Table of contents

Transaction Highlights

Overview of Intrum Justitia and Lindorff

Strategic Rationale

Synergies and Financial Impact

Timetable

Appendix

Conclusion

Indicative timetable

14-Nov

Announcement

15-25 Nov

Investor

Roadshow

14-Dec

Intrum Justitia

EGM

Q2 2017

Closing

Note: The anticipated completion of the transaction is dependent on the timing of decisions from the relevant competition and regulatory authorities and is therefore subject to change.

Nov-2016 Dec-2016 Jan-2017 Jun-2017

23

Table of contents

Transaction Highlights

Overview of Intrum Justitia and Lindorff

Strategic Rationale

Synergies and Financial Impact

Timetable

Appendix

Conclusion

Intrum Justitia and Lindorff - a highly compelling combination

Industry leader with unparalleled scale and diversification

Excellent strategic fit with a well-balanced business mix and

integrated service offering

Complementary geographical footprint, sector expertise and

debt purchasing platforms

Strong cultural fit based on Nordic heritage and longstanding

commitment to fair collection

Ideally positioned for growth through investments in new asset

classes, segments and geographies

Significant shareholder value creation from cost and revenue

synergies

24

Table of contents

Transaction Highlights

Overview of Intrum Justitia and Lindorff

Strategic Rationale

Synergies and Financial Impact

Timetable

Appendix

Conclusion

● A leader in Northern European private equity, established in 1989

● Lead investor in 90 acquisitions with a consistent track record of successful investments

• Over EUR 10bn invested in 90 portfolio companies and 150+ material add-on acquisitions

● Currently investing Nordic Capital Fund VIII of EUR 3.5bn

• Current portfolio comprises 31 companies with more than EUR 12bn of aggregated revenues

● Nordic Capital is committed to responsible ownership which is critical to creating long-term business success

• Established model for working with governance and ownership in portfolio companies, including a separate

model for publicly listed entities

● Nordic Capital has consistently supported value creation in its portfolio companies

● Creation of new and industrially sound combinations is a recurring investment theme

● Nordic Capital has been one of the most active financial sponsors when it comes to IPOs and has to date listed

sixteen companies on Nordic and international stock exchanges with solid aftermarket performance

• Since 2014, seven companies have been listed with Nordic Capital retaining a significant shareholding in each

listed entity

● Significant experience of investments in Financial Services

• Current portfolio companies in Financial Services include Lindorff, Resurs Holding, Itiviti and Bambora

Overview of Nordic Capital

Note: Nordic Capital refers to Nordic Capital Fund VIII and/or all, or some, of its predecessor funds.

25