38

15-1 INVENTORIES CHAPTER 15

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | baker-harmon |

| View: | 37 times |

| Download: | 4 times |

15-1

INVENTORIES

CHAPTER 15CHAPTER 15

15-2

Merchandise inventory Merchandise inventory

Merchandise inventory consists of all goods that are owned and held for sale in the regular course of business, including goods in transit.

All the items for sale

The goods in stock for sale

SupermarketMerchandising company

15-3

Merchandise inventoryMerchandise inventory

The Title of the merchandise passed to the company

Purchased merchandise in transit should be included in the inventory count.

15-4

Merchandise inventoryMerchandise inventory

Outgoing goods Incoming goods

FOB Destination FOB Shipping Point

Merchandise inventory

15-5

Merchandise inventoryMerchandise inventory

Company AConsigned

Company BMerchandise

Title belongs to Company A

Merchandise inventory

??

15-6

Beginning inventory and ending Beginning inventory and ending inventoryinventory

At the beginning of the accounting period

Merchandise inventory

At the end of accounting period

The beginning inventory The ending inventory

The beginning inventory for the next accounting period

15-7

The cost of goods sold The cost of goods sold

Formula

Goods Available for Sale = Beginning Inventory +

Net Purchases

Purchases – Purchase Returns and Allowances – Purchase Discount + Freight In

Cost of Goods Sold = Goods Available for Sale – Ending Inventory

Gross Margin from Sales =Revenues from Sales –Cost of Goods Sold

15-8

The cost of goods soldThe cost of goods sold

The higher the cost of ending inventory, the lower the cost of goods sold will be and the higher the gross margin.

Vice versa, the lower the ending inventory, the higherThe cost of goods sold will be and the lower the gross margin.

15-9

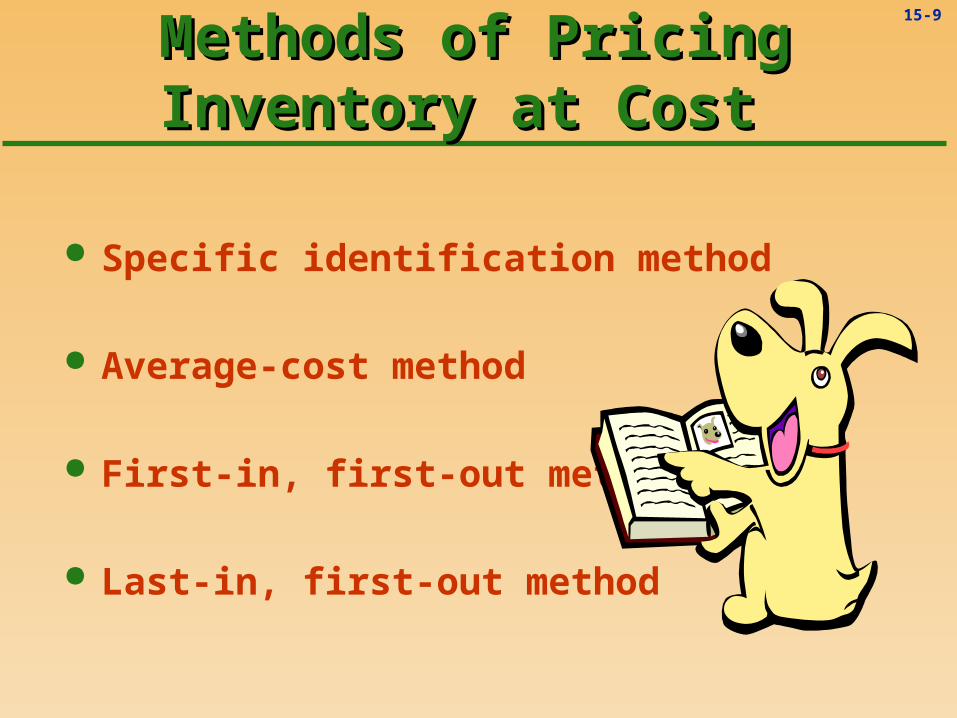

Methods of Pricing Inventory at Methods of Pricing Inventory at Cost Cost

Specific identification method

Average-cost method

First-in, first-out method

Last-in, first-out method

15-10

Methods of Pricing Inventory at Methods of Pricing Inventory at CostCost

Suppose that the following transactions happened in August , 2006.

Date Item Quantity

(Units)

Unit price ($)

Total

($)

August 1 Beginning inventory 50 $2.00 100.00

6 Purchase 60 $2.20 132.00

17 Purchase 80 $2.40 192.00

20 Purchase 100 $2.50 250.00

27 Purchase 150 $2.60 390.00

Goods Available for Sale 440 $1,064

Sale 200

Ending Inventory August 31 240

15-11

Specific Identification MethodSpecific Identification Method

1

Specific Identification Method

Method

15-12

Specific Identification MethodSpecific Identification Method

A method of tracking inventory when each item can be identified. This method used in the purchase and sale of high-priced articles such as automobile, heavy equipment, jewels and dear fashions.

15-13

Specific Identification MethodSpecific Identification Method

First, let’s Look at an example …

15-14

Specific Identification MethodSpecific Identification Method

Suppose that the sale consists of 50 units from beginning inventory, 60 units of August 6, 80 units of August 17 and 10 units of August 20.

Value of the ending inventory

90 × $2.50 + 150 × $2.60 = $615

$1064 - $615 = $449

Ending Inventory =

Cost of Goods Sold =

15-15

Specific Identification MethodSpecific Identification Method

Disadvantages

First, it is difficult and impractical in most cases to keep track of the purchase and sale of individual items.

Second, the company could raise or reduce income by choosing whether to sell either the high-cost or the low-cost items.

15-16

Weighted-Average-Cost MethodWeighted-Average-Cost Method

Weighted-Average-Cost Method

Method

2

15-17

Weighted-Average-Cost Method Weighted-Average-Cost Method

Under this method, it is assumed that the cost of inventory is the average cost of goods on hand at the beginning of the period plus all goods purchased during the accounting period.

The weighted-average unit cost =Total cost of goods available for sale

Total units available for sale

15-18

Weighted-Average-Cost MethodWeighted-Average-Cost Method

Average Unit Cost =Total cost of goods available for sale

Total units available for sale

Cost of Beginning Inventory + ∑(unit price per purchase × quantity per purchase)

Formula

Quantity of beginning inventory+∑quantity of each purchase

15-19

Weighted-Average-Cost MethodWeighted-Average-Cost Method

Let’s go back to the previous example …

15-20

Weighted-Average-Cost MethodWeighted-Average-Cost Method

Average Unit Cost =(100 + 132 + 192 + 250 + 390)

440

=$2.42

Cost of Goods Sold Quantity of sale = × Average unit cost

= 200×$2.42 = $484

Ending Inventory = $1,064 - $484 = $580

15-21

Weighted-Average-Cost MethodWeighted-Average-Cost Method

Advantages

Disadvantages

The value of ending inventory is influenced by all the prices of beginning inventory and purchases for the period, so it overlooks the effects of the prices increases and decreases.

The method doesn't't make the recent costs gain more Attention and doesn't't reflect the relevance between the recent prices with the income measurement and decision-making.

15-22

First-In, First-Out MethodFirst-In, First-Out Method

Method

3

First-In, First-Out Method

15-23

First-In, First-Out MethodFirst-In, First-Out Method

Under this method, it is assumed that the first lots of Merchandise purchased are sold firstly.

During periods of consistently rising prices

When the prices are decreasing

Net Income

Net Income DECREASE

INCREASE

15-24

First-In, First-Out MethodFirst-In, First-Out Method

Let’s go back to the previous example again …

15-25

First-In, First-Out MethodFirst-In, First-Out Method

Cost of Goods Sold = 50×$2.00 + 60 × $2.20 +80 × $2.40 + 10 × 2.50

=

$(100 + 132.00 + 192.00 + 25)

= $449

Ending Inventory = $(1064 – 449) = $615

Net Income = Revenues from Sales – Cost of Goods Sold

– Operating Expenses

15-26

First-In, First-Out MethodFirst-In, First-Out Method

Suppose the business encounters a price-decreasing period, the result will be opposite to that of the price-increasing period.

Date Item Quantity

(Units)

Unit price ($)

Total

($)

August 1 Beginning inventory 50 $2.60 130.00

6 Purchase 60 $2.50 150.00

17 Purchase 80 $2.40 192.00

20 Purchase 100 $2.20 220.00

27 Purchase 150 $2.00 300.00

Goods Available for Sale 440 $992

Sale 200

Ending Inventory August 31 240

15-27

First-In, First-Out MethodFirst-In, First-Out Method

Cost of Goods Sold 50 ×$2.60 + 60 × $2.50 + 80 × $2.40 + 10 × $2.20=

= $494

$494 > $449 During the period of price-decreasing, the cost of goods sold will be higher.

The gross marginLOWER

The net income

15-28

Last-In, First-Out MethodLast-In, First-Out Method

Method

4

Last-In, First-Out Method

15-29

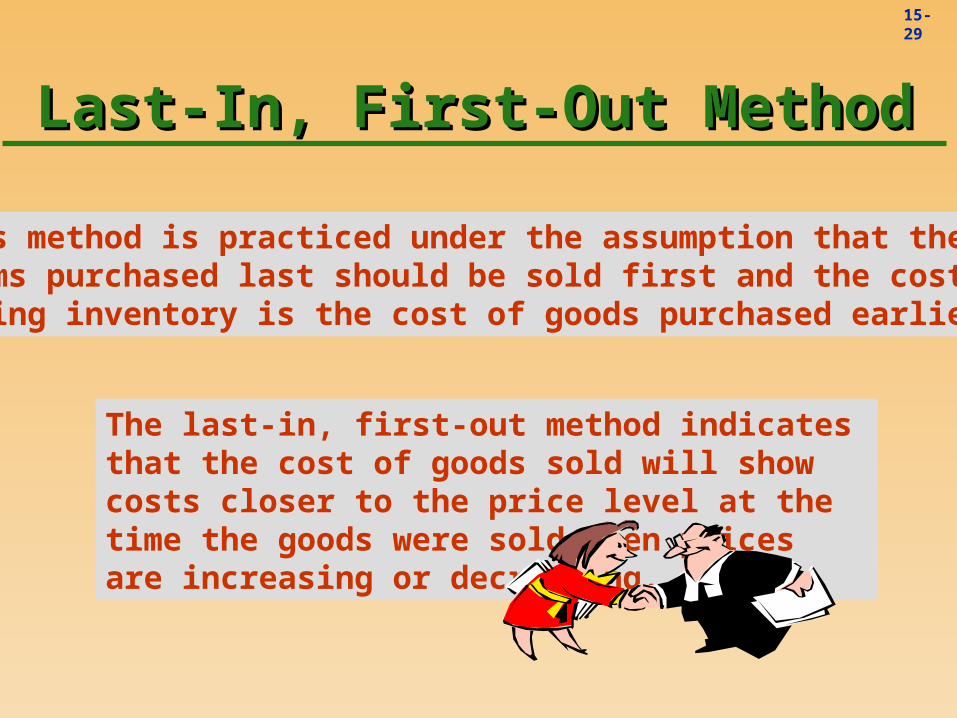

Last-In, First-Out MethodLast-In, First-Out Method

This method is practiced under the assumption that theitems purchased last should be sold first and the cost of ending inventory is the cost of goods purchased earliest.

The last-in, first-out method indicates that the cost of goods sold will show costs closer to the price level at the time the goods were sold when prices are increasing or decreasing.

15-30

Last-In, First-Out MethodLast-In, First-Out Method

Let’s still look at the previous example …

15-31

Last-In, First-Out MethodLast-In, First-Out Method

Cost of Goods Sold = 150×$2.60 + 50×$2.50

= $515

Ending Inventory = $1064 - $515

= $549

15-32

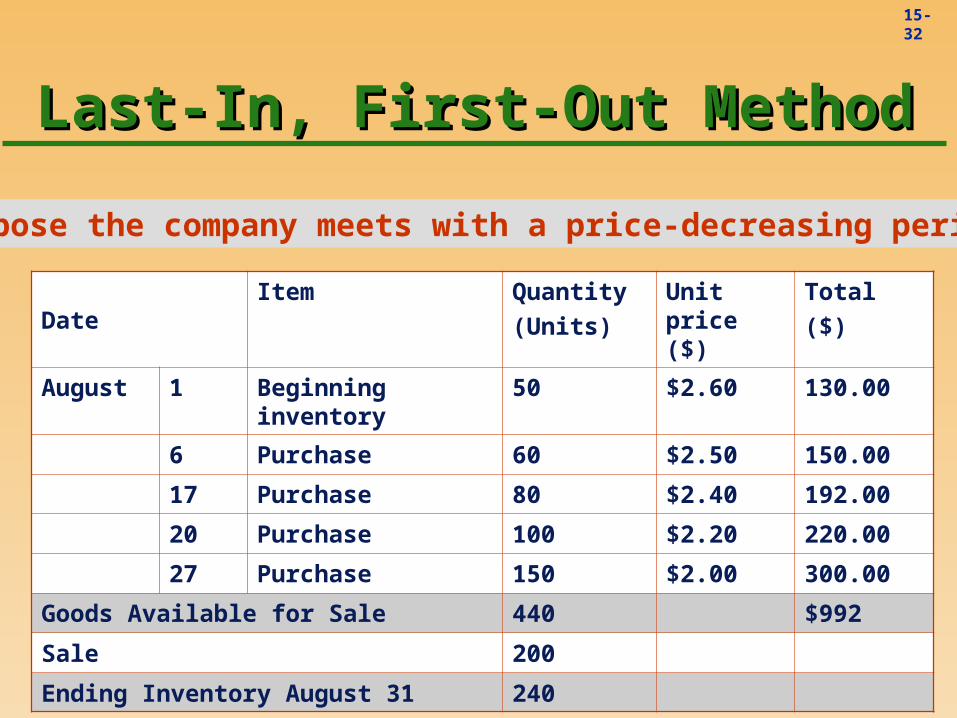

Last-In, First-Out MethodLast-In, First-Out Method

Date Item Quantity

(Units)

Unit price ($)

Total

($)

August 1 Beginning inventory 50 $2.60 130.00

6 Purchase 60 $2.50 150.00

17 Purchase 80 $2.40 192.00

20 Purchase 100 $2.20 220.00

27 Purchase 150 $2.00 300.00

Goods Available for Sale 440 $992

Sale 200

Ending Inventory August 31 240

Suppose the company meets with a price-decreasing period

15-33

Last-In, First-Out MethodLast-In, First-Out Method

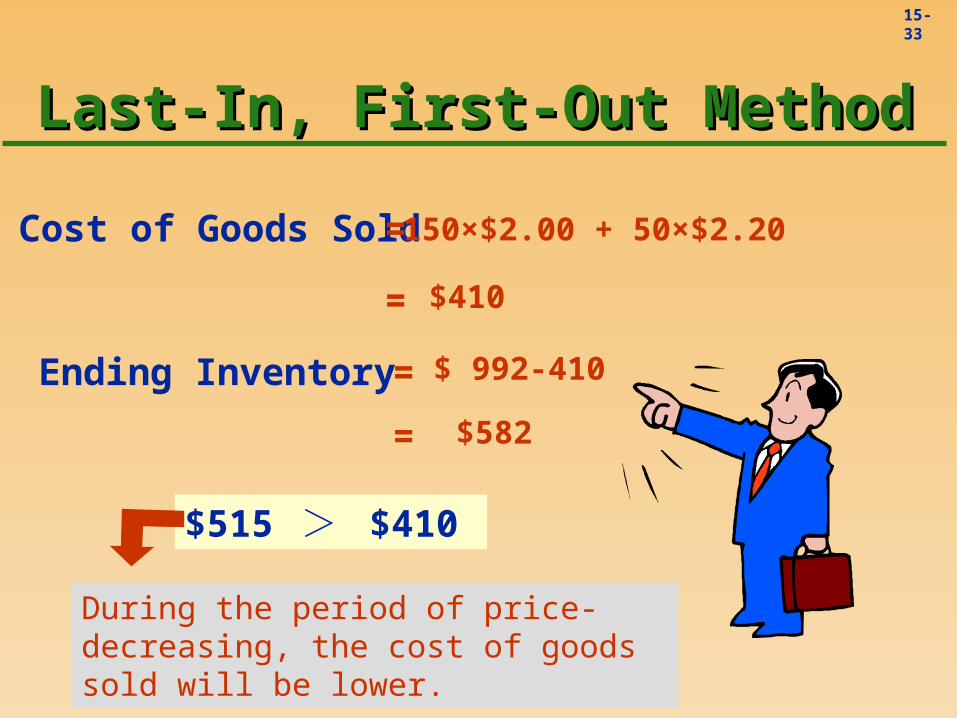

Cost of Goods Sold = 150×$2.00 + 50×$2.20

= $410

Ending Inventory = $ 992-410

= $582

$515 > $410

During the period of price-decreasing, the cost of goods sold will be lower.

15-34

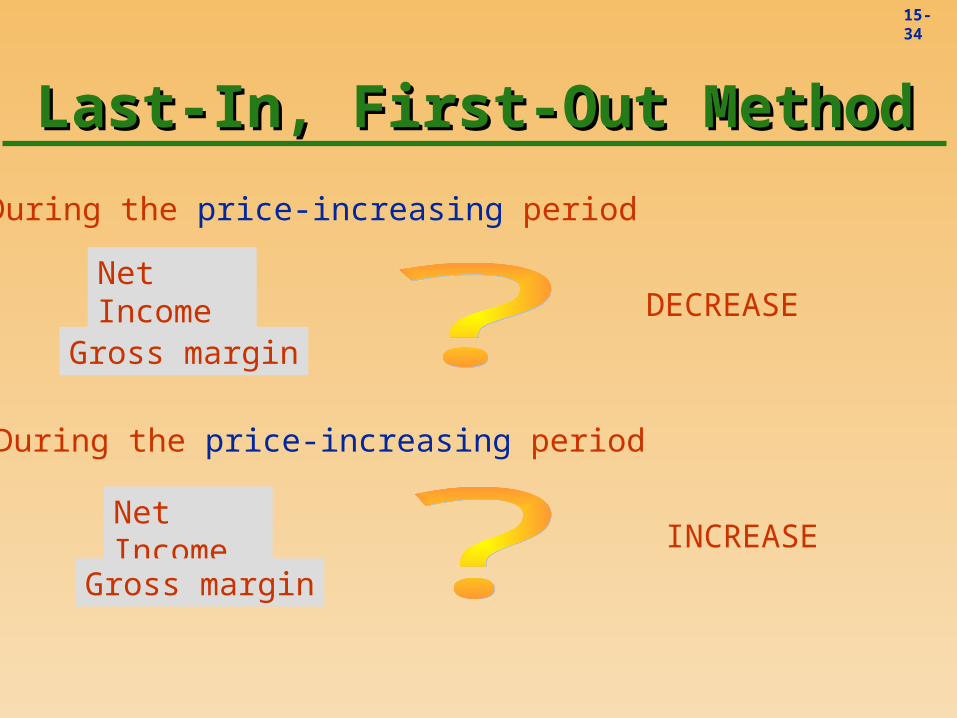

Last-In, First-Out MethodLast-In, First-Out Method

During the price-increasing period

Net Income

Gross margin

DECREASE

During the price-increasing period

Net Income

Gross margin

INCREASE

15-35

Comparison of the four methodsComparison of the four methods

Suppose the revenue from sales is the same data, $1,000.

Methods of inventory pricing Cost of goods sold gross margin

The specific identification method $449 $551

The weighted-average-cost method $484 $516

The first-in, first-out method $449 $551

The last-in, first-out method $515 $485

15-36

Comparison of the four methodsComparison of the four methods

The accrual costSpecific identification method

Average-cost method

First-in, first-out method

Last-in, first-out method

The assumption that cost is flowing, not the physical

movement of goods

Based

on

Based

on

15-37

Comparison of the four methodsComparison of the four methods

First-in, first-out method

Beneficial to yielding higher gross margin and net income.

Last-in, first-out method

Incur higher gross margin and net income than other methods.

During the period of price decreasing,

During the period of price increasing,

15-38

WE ARE SAILING RIGHT ALONG!!