22

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 2

Invest Mantra September 2017

TABLE OF CONTENTS

Market Strategy – Equity Market Outlook

Theme 1 : Beaten Down Large Cap Stocks

Gail India Ltd

ITC Ltd

Mahindra & Mahindra

Tata Motors

Theme 2 : Old Private Sector Banks

Karnataka Bank

South Indian Bank

Theme 3 : PSU Strategic Stake Sale

Balmer Lawrie & Company

Shipping Corporation of India Ltd

Theme 4 : Deep Value Stock

Bombay Burmah Trading Corporation

1M Portfolio : September 2017

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 3

Invest Mantra September 2017

EQUITY MARKET OUTLOOK

Long-term Optimism remains intact, but invest cautiously in the Short-term

Long-term outlook of the Indian equity markets remain robust

India has got solid political stability after two-and-half decades. We have already seen bold

economic reforms / initiatives like GST, demonetization, FDI in insurance, shutting down of loss-making government-owned companies, etc. Such measures provide us the optimism that many

more economic initiatives could be in the offing. Normal monsoon is expected for the second year

in a row – the same is likely to provide a fillip to aggregate demand from the rural economy. Total food grains production for 2017 is projected to hit a record level of 276 million tonnes.

In the current year, the government has given major boost to Public Expenditure -during the period

April-July 2017, the total government expenditure has increased by a robust 28.3% yoy to Rs.8.1 trillion, with revenue expenditure rising by 21.8% yoy and capital expenditure by 33.4% yoy. On

monetary front, the benchmark interest rates had been slashed cumulatively by 200 bps in the last

3 years.

On external economic front also, a comfortable situation is emerging – the country's foreign

exchange reserves touched a new life-time high of over $393 billion. Foreign Direct Investment

inflows remain robust – it increased by 23% year-on-year (yoy) during April-May 2017. External debt management and Current Account Deficit of the Balance of Payments are also well under

control. Global oil price is expected to remain subdued around $50 a barrel at least for another 2

years. Over 90% jump in the deployment of oil rigs by the US drillers, forecast of reduced oil demand from the OPEC by the emerging economies and failure of OPEC and Non-OPEC members

to fully adhere to the compliance on oil output cut (actual cut is in the range of 67% o 75%) are

likely to enable India to enjoy cheap oil for two more years at least.

Global economic conditions turn favourable

Global deflationary trends have moderated substantially as compared to early 2016. Prices of oil,

metals, resources and agri crops have gone up substantially over the year. Global growth is improving.

The US economic expansion is expected to last at least another two years, according to a poll of

economists which suggests 2.1% to 2.5% growth each quarter to the end of next year. The US economy continues to remain near-full employment. Euro zone’s annual GDP upgraded to 2.2%

growth in the second quarter of 2017.Although China’s debt levels remain at alarming level, its

economy is unlikely to see hard landing in the near future. The IMF has raised its forecast for China's average annual growth to 6.4% from 6.0% for the period 2018-2020.

Both the US FED and the European Central Bank are talking about the reversal of monetary stimulus

- consequence of such withdrawal is an outcome of growth recovery in these economies. Hence, it is actually not a major concern for the emerging markets in the long-term.

However, there are some concerns on the Indian equities in the short-term

As economic Survey has also pointed out, a number of indicators like GDP, IIP, credit offtake, investment, capacity utilization, etc., point to a deceleration in real activity since first quarter of

FY2017. Farm loan waivers expected to cut economic demand up to 0.7% of GDP.

Industrial economy is yet to pick up – the Gross Value Added (GVA) growth in manufacturing came in at mere 1.2% in Q1FY2018 as compared to 10.7% in Q1FY2017. Chief Statistician has

reported in the media that 74% of manufacturing GVA was accounted for by the corporate

sector, which has posted very poor performance in Q1FY2018;

Though yoy growth has picked up to 9%, monthly export bill still remains almost stagnant at

around $23 billion – even much before oil price spike in 2014, India’s monthly export bill stood

at around $25 billion a month;

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 4

Invest Mantra September 2017

Banking industry credit growth hovers around 6%, at decades low level and, bad assets remain

at record levels (9.6% for the banking system) and they are expected to taper off by March 2018;

A sample of over 1,000 companies’ results (excluding banks & finance companies) indicate 9.7%

yoy growth in net sales, but 1.7% yoy decline in net profits in Q1FY2018. Only hopes on forward corporate earning remain alive: Since 2013 the Sensex earnings moved up mere 3%

cumulatively (from Rs.1,322 in 2013 to Rs.1,360 now);

Apart from fundamental aspect, tactically also there is some short-term risk to the markets – the foreign investors have been largely investing in the debt instruments rather than in the equities. FIIs

prefer debt than equities at this juncture – year to date in CY2017, FIIs have invested Rs.1.2 trillion

in the debt instruments as against Rs.496 billion in Indian equities. They may tilt towards domestic equities only in the event of some further correction in the equity prices or after seeing some visibility

in actual improvements of corporate earnings.

Tactically, the domestic equity market faces short-term risk also from the growing gap between the value of overall equity markets and available investible surplus at this juncture. The market cap of

entire BSE-listed stocks stands at around Rs.132 trillion. Small & mid cap stocks (less than $2 billion

market cap) rallied and total valuation stand at over Rs.25 trillion now– a historical peak. Due to global or domestic macro factors, any selling lead to the extent of even just 1% of entire market

cap that would mean a supply pressure of around $20 billion. However, despite robust inflows into

the mutual funds’ equity assets, the existing appetite is very low for any such possible shocks. Household financial savings flowing into equities is less than Rs.2 trillion per annum – most of them

already invested (a natural phenomenon in a bull market).

Moreover, a large number of IPOs have been lined up, apart from QIPs from the listed companies. Twelve government banks have also lined up for tapping the markets for re-building their capital

base. Further the government has lined up listing of several wholly-owned companies, further

divestments and also stake sale in already listed companies – more than Rs.500 billion worth of government’s equities are targeted to be supplied in the markets in the next 7 months itself. The

overall new issuance of equities (including IPOs, QIPs, banks' proposals and PSUs divestments &

stake sales) is estimated to be around Rs.2.5 trillion in the new future - such huge figure can make a dent on either primary or secondary markets or on both in scaling down the valuations.

Apart from the macroeconomic and liquidity issues, the international political issues are also not

conducive at this juncture. Although holding of nuclear weapons by all countries involved in the current disputes act as a war deterrent, any further war of words or intensified troubles on the

border could lead to some corrections in the markets in the short term.

Strategy Way Forward for Indian equities?

Although short-term fear exists, the medium to long-term outlook (beyond March 2018) remains

optimistic. In this background, it would be wise to play on large cap stocks to the extent of at least

50% of equity portfolios and also on select fundamentally sound equity themes, which offer a lot of comfort on valuation front.

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 5

Invest Mantra September 2017

THEME 1 - BEATEN DOWN LARGE CAP STOCKS

In the past, we had seen Maruti falling as low as Rs.1500 in early 2014 and then the stock multiplying; in August 2015, the share price of Hindustan Zinc fell as low as Rs.117, the same stock

in the next 18 months (February 2017) rose nearly three times to Rs.333. Large cap stocks go

through stress sometimes, but they rarely fail permanently, provided the quality of the management, balance sheet and the business model are unquestionable.

Of course, no longer large cap stocks assure protection of capital – even large cap stocks from the

so-called “defensive sectors” have destroyed wealth. For instance, Lupin and Sun Pharmaceutical Industries have eroded their market caps by 54% and 61% respectively since March / April 2015.

During the same period, the Sensex has moved up by about 8%. Even large IT stocks could fall as

high as 14% in a single day. However, unique advantage of banking on large cap segment is that they provide easy opportunity to exit which is not the case with the most small and mid cap stocks.

We believe that in the current political, economic and market conditions, it would be an apt

approach for the conservative investors to invest around 50% of the equity portfolio in the large cap stocks. To mitigate further possible risks even in the large cap segment, we have picked up

some of the stocks which were already beaten down in the markets. These are GAIL India, ITC,

Mahindra & Mahindra and Tata Motors.

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 6

Invest Mantra September 2017

Current Market Price (Rs) 52 Week H/L (Rs) Mkt Cap (Rs mn)

384 434 / 268 649545

Source: Bloomberg

Source: KIE

Financials (Rs mn) FY17 FY18E FY19E

Sales 481,489 562,169 642,050

Growth (%) 16.8% 14.2%

EBITDA 65,584 72,573 78,623

EBITDA margin (%) 13.6 12.9 12.2

PBT 56,886 65,134 72,519

Net profit 37,806 43,729 48,556

EPS (Rs) 22.4 25.9 28.7

Growth (%) NA 15.6% 10.8%

Dividend Yield (%) 2.4% 2.4% 2.6%

Dividend per share (Rs) 9.1 9.1 9.9

ROE (%) 9.0 10.1 10.2

ROCE (%) 9.0 9.4 9.8 Source: KIE

Net cash (debt) (37,481) (25,585) (25,013)

Valuation Parameters FY17 FY18E FY19E

P/E (x) 17.1 14.8 13.4

EV/Sales (x) 1.4 1.2 1.1

EV/EBITDA (x) 10.5 9.3 8.6

Price Performance (%) 1M 3M 6M

2.7 (6.4) 1.1

Source: Bloomberg, Company, Kotak Securities - Private Client Research Source: KIE

LPG sales volumes ('000 tons)

Potential Upside (%)

14.6%

1 Year Performance

Gas transmission volumes (mcm/d)

Petrochemical sales volumes ('000 tons)

Last report at Rs.424 on 23 February 2017

GAIL India Analyst: [email protected]

Target Price (Rs)

440

FY15 FY16 FY17 FY18E FY19E

0.0

30.0

60.0

90.0

120.0

0

100

200

300

400

500

600

700

800

900

FY15 FY16 FY17 FY18E FY19E

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

FY15 FY16 FY17 FY18E FY19E

60

90

120

150

180 GAIL India Ltd Nifty

Investment Argument

GAIL management indicated that the economics of petchem expansion has improved with ramp-up in utilization to ~70% currently, led by (1) rising efficiency in conversion of gas to C2- C3 and subsequently to ethylene and (2) a reduction in operating costs and unit overheads.

The company has also initiated exports to a few countries preparing itself for the imminent increase in domestic supplies from other new plants (BCPL, OPAL and RIL’s ROGC).GST implementation will result in increased vehicle sales and freight movement, we opine, resulting in higher sales.

The company was optimistic on gas transmission segment, indicating (1) pickup in gas volumes to 106-108 mcm/d during March and (2) possibility of overhaul in tariff mechanism for pipelines. The government is considering implementation of postal tariffs, which will result in uniform tariff for all consumers in each integrated pipeline network (instead of current zonal tariffs), subject to regulatory cap of 12% on project IRR. The new mechanism will be adopted for the Urja Ganga pipeline project (East India gas grid) and may get implemented for existing pipelines as well, which may result in better realizations for some networks such as HVJ. GAIL also provided an update on East India gas grid, detailed later in the note.

We remain constructive on the stock, given (1) our expectations of robust volume-led earnings growth in the medium term driven by dominant presence across the gas value chain and (2) inexpensive valuation core gas business profitability, which gets overlooked due to significant value locked in investments.

Risks & Concerns

Lower industrial activity can impact volume growth

Company Background

GAIL (India) Ltd is India’s largest gas transmission and marketing company

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 7

Invest Mantra September 2017

Current Market Price (Rs) 52 Week H/L (Rs) Mkt Cap (Rs mn)

284 368 / 222 3291745

Source: Bloomberg

Source: Capitaline

Financials (Rs mn) FY17 FY18E FY19E

Sales 554,485 586,315 641,457

Growth (%) 7.5 5.7 9.4

EBITDA 145,780 161,193 179,123

EBITDA margin (%) 26.3 27.5 27.9

PBT 155,030 173,602 196,605

Net profit 102,009 113,709 128,776

EPS (Rs) 8.4 9.4 10.6

Growth (%) 10.3 11.5 13.3

CEPS (Rs) 9.3 10.3 11.5

Book value (Rs/share) 26.2 30.5 35.8

Dividend per share (Rs) 4.8 4.8 5.0 Source: Kotak Securities - Private Client Research

ROE (%) 31.5 33.0 36.2

ROCE (%) 25.7 28.0 28.6

Net cash (debt) 95,158 134,808 186,318

Net Working Capital (Days) 193 204 210

Valuation Parameters FY17 FY18E FY19E

P/E (x) 33.8 30.3 26.8

P/BV (x) 10.8 9.3 7.9

EV/Sales (x) 5.8 5.4 4.8

EV/EBITDA (x) 21.9 19.6 17.3

Price Performance (%) 1M 3M 6M

(1.5) (9.7) 5.6

Source: Bloomberg, Company, Kotak Securities - Private Client Research Source: Company

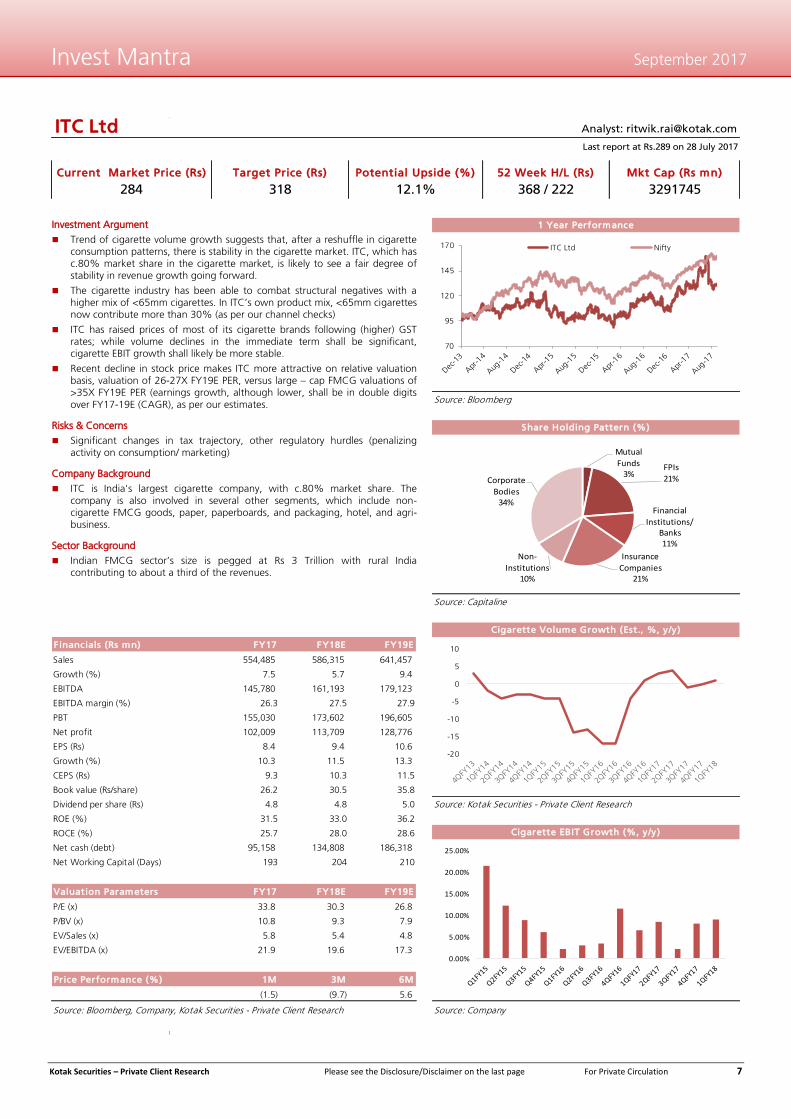

Cigarette EBIT Growth (%, y/y)

Potential Upside (%)

12.1%

1 Year Performance

Share Holding Pattern (%)

Cigarette Volume Growth (Est., %, y/y)

Last report at Rs.289 on 28 July 2017

ITC Ltd Analyst: [email protected]

Target Price (Rs)

318

70

95

120

145

170 ITC Ltd Nifty

Investment Argument

Trend of cigarette volume growth suggests that, after a reshuffle in cigarette consumption patterns, there is stability in the cigarette market. ITC, which has c.80% market share in the cigarette market, is likely to see a fair degree of stability in revenue growth going forward.

The cigarette industry has been able to combat structural negatives with a higher mix of <65mm cigarettes. In ITC’s own product mix, <65mm cigarettes now contribute more than 30% (as per our channel checks)

ITC has raised prices of most of its cigarette brands following (higher) GST rates; while volume declines in the immediate term shall be significant, cigarette EBIT growth shall likely be more stable.

Recent decline in stock price makes ITC more attractive on relative valuation basis, valuation of 26-27X FY19E PER, versus large – cap FMCG valuations of >35X FY19E PER (earnings growth, although lower, shall be in double digits over FY17-19E (CAGR), as per our estimates.

Risks & Concerns

Significant changes in tax trajectory, other regulatory hurdles (penalizing activity on consumption/ marketing)

Company Background

ITC is India's largest cigarette company, with c.80% market share. The company is also involved in several other segments, which include non-cigarette FMCG goods, paper, paperboards, and packaging, hotel, and agri-business.

Sector Background

Indian FMCG sector’s size is pegged at Rs 3 Trillion with rural India contributing to about a third of the revenues.

-20

-15

-10

-5

0

5

10

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Mutual

Funds3%

FPIs

21%

Financial

Institutions/ Banks11%

Insurance

Companies21%

Non-

Institutions10%

Corporate

Bodies34%

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 8

Invest Mantra September 2017

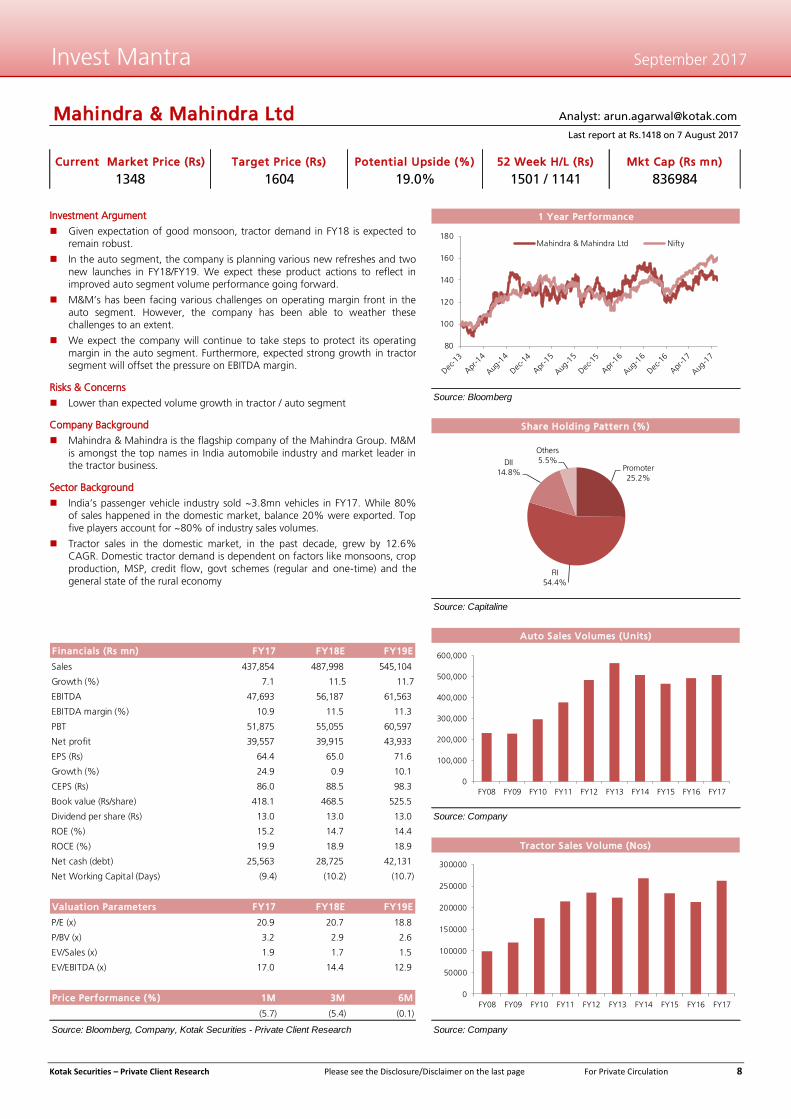

Mahindra & Mahindra Ltd

Current Market Price (Rs) 52 Week H/L (Rs) Mkt Cap (Rs mn)

1348 1501 / 1141 836984

Source: Bloomberg

Source: Capitaline

Financials (Rs mn) FY17 FY18E FY19E

Sales 437,854 487,998 545,104

Growth (%) 7.1 11.5 11.7

EBITDA 47,693 56,187 61,563

EBITDA margin (%) 10.9 11.5 11.3

PBT 51,875 55,055 60,597

Net profit 39,557 39,915 43,933

EPS (Rs) 64.4 65.0 71.6

Growth (%) 24.9 0.9 10.1

CEPS (Rs) 86.0 88.5 98.3

Book value (Rs/share) 418.1 468.5 525.5

Dividend per share (Rs) 13.0 13.0 13.0 Source: Company

ROE (%) 15.2 14.7 14.4

ROCE (%) 19.9 18.9 18.9

Net cash (debt) 25,563 28,725 42,131

Net Working Capital (Days) (9.4) (10.2) (10.7)

Valuation Parameters FY17 FY18E FY19E

P/E (x) 20.9 20.7 18.8

P/BV (x) 3.2 2.9 2.6

EV/Sales (x) 1.9 1.7 1.5

EV/EBITDA (x) 17.0 14.4 12.9

Price Performance (%) 1M 3M 6M

(5.7) (5.4) (0.1)

Source: Bloomberg, Company, Kotak Securities - Private Client Research Source: Company

Last report at Rs.1418 on 7 August 2017

Analyst: [email protected]

Target Price (Rs)

1604

Tractor Sales Volume (Nos)

Potential Upside (%)

19.0%

1 Year Performance

Share Holding Pattern (%)

Auto Sales Volumes (Units)

Promoter

25.2%

FII

54.4%

DII

14.8%

Others

5.5%

0

100,000

200,000

300,000

400,000

500,000

600,000

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

0

50000

100000

150000

200000

250000

300000

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

80

100

120

140

160

180Mahindra & Mahindra Ltd Nifty

Investment Argument

Given expectation of good monsoon, tractor demand in FY18 is expected to remain robust.

In the auto segment, the company is planning various new refreshes and two

new launches in FY18/FY19. We expect these product actions to reflect in improved auto segment volume performance going forward.

M&M’s has been facing various challenges on operating margin front in the

auto segment. However, the company has been able to weather these challenges to an extent.

We expect the company will continue to take steps to protect its operating

margin in the auto segment. Furthermore, expected strong growth in tractor segment will offset the pressure on EBITDA margin.

Risks & Concerns

Lower than expected volume growth in tractor / auto segment

Company Background

Mahindra & Mahindra is the flagship company of the Mahindra Group. M&M

is amongst the top names in India automobile industry and market leader in the tractor business.

Sector Background

India’s passenger vehicle industry sold ~3.8mn vehicles in FY17. While 80% of sales happened in the domestic market, balance 20% were exported. Top

five players account for ~80% of industry sales volumes.

Tractor sales in the domestic market, in the past decade, grew by 12.6% CAGR. Domestic tractor demand is dependent on factors like monsoons, crop

production, MSP, credit flow, govt schemes (regular and one-time) and the

general state of the rural economy

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 9

Invest Mantra September 2017

Current Market Price (Rs) 52 Week H/L (Rs) Mkt Cap (Rs mn)

391 599 / 358 1240558

Source: Bloomberg

Source: Capitaline

Financials (Rs mn) FY17 FY18E FY19E

Sales 2,696,925 2,991,612 3,459,935

Growth (%) (2.1) 10.9 15.7

EBITDA 334,988 329,895 465,501

EBITDA margin (%) 12.4 11.0 13.5

PBT 93,148 145,527 206,501

Net profit 74,544 127,723 172,414

EPS (Rs) 22.0 37.6 50.8

Growth (%) (32.4) 71.3 35.0

CEPS (Rs) 74.7 93.1 116.0

BV (Rs/share) 171.0 208.6 259.4

DPS(Rs) - - - Source: Company

ROE (%) 10.7 19.8 21.7

ROCE (%) 11.4 18.2 21.2

Net cash (debt) (233,701) (256,768) (240,736)

NWC (Days) (26.1) (29.4) (30.2)

Valuation Parameters FY17 FY18E FY19E

P/E (x) 17.8 10.4 7.7

P/BV (x) 2.3 1.9 1.5

EV/Sales (x) 0.5 0.5 0.4

EV/EBITDA (x) 4.4 4.5 3.2

Price Performance (%) 1M 3M 6M

(12.5) (18.0) (13.0)

Source: Bloomberg, Company, Kotak Securities - Private Client Research Source: Company

JLR Sales Volumes (Units)

Potential Upside (%)

31.5%

1 Year Performance

Share Holding Pattern (%)

Domestic sales Volumes (Units)

Last report at Rs.416 on 10 August 2017

Tata Motors Ltd Analyst: [email protected]

Target Price (Rs)

514

Promoter

34.7%

FII

23.5%

DII

16.1%

Others

25.7%

0

200,000

400,000

600,000

800,000

1,000,000

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

0

100000

200000

300000

400000

500000

600000

700000

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

60

85

110

135

160

185 Tata Motors Ltd Nifty

Investment Argument

Over the next two years, we expect continued healthy volume traction in the passenger car business - driven by new products. In the commercial vehicle

segment, we expect demand in MHCV segment to remain subdued in

1HFY18. Over the medium to long term, we anticipate gradual improvement in demand.

JLR's volume growth outlook remains positive. In FY18, JLR will be ramping-

up the Discovery and Rover Velar and will launch XF Sportbrake. I-Pace and another new product is expected to be launched in CY18/FY19.

Forex loss on hedges is expected to remain at elevated levels over the next

two quarters. GBP depreciation is positive for JLR over long term. JLR's EBITDA margin in FY19 will receive support from positive operating leverage,

improvement in product mix and British Pound depreciation.

Risks & Concerns

Lower than expected volume growth at JLR

Unfavorable currency movement

Company Background

Tata Motors Limited (TAMO), part of Tata Group, is India's largest automobile

company. Established in 1945, TAMO has presence in the commercial vehicle

and passenger vehicle segments. In the domestic market, the company is the market leader in both the LCV and M&HCV segment.

Sector Background

Commercial vehicle industry fortunes depend on the overall economic development in the economy. In the passenger car segment, the growth

opportunities are high, given lower car penetration levels in India.

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 10

Invest Mantra September 2017

THEME 2 – OLD PRIVATE SECTOR BANKS

There are around 7 listed Old Private Sector Banks (OPSBs) in the country. This OPSB space has seen

a significant momentum of M&A activities since mid 1990s starting with the acquisition of Bank of

Madura by ICICI Bank. Other OPSBs, which were acquired by large New Private Sector Banks (NPSBs)

over the last ten years were: Lord Krishna Bank, Bank of Rajasthan and Vysya Bank. Two more mid-

sized new private banks viz., Centurion Bank and Bank of Punjab were also acquired by the NPSBs

in this period.

Now we believe that the time could be possibly once again ripe for further consolidation in the

OPSB segment considering the structural changes happening in the banking industry and, nature

and valuation of Old Private Sector Banks.

Structural changes in the Banking Industry

Most of the NPSBs have grown their advances substantially higher than the average industry

credit growth by huge margins over the last 2 decades. However, the industry credit growth itself has crashed to near two-decade low of around 6%. Going forward, this crash in credit

growth might make it quite difficult for some of the NPSBs to maintain the kind of credit growth

they maintained in the past in the absolute terms;

Both the lending and saving rates in the system have also fallen significantly after the 200 bps

cut in the benchmark interest rates over the last three years. As the base of lending rate itself

has fallen substantially in recent times, in our view, it is going to be a tough task for some of the NPSBs in the future to maintain very high interest margins, which they enjoy now;

Despite these structural changes in the industry, some of the large private banks enjoy record

high level of valuation over 4 times Price to Adjusted Book Values on the secondary markets. To continue to enjoy such huge valuation premium on the markets despite adverse structural

changes, a few of NPSBs may possibly consider inorganic route to grow.

Nature and Valuation of OPSBs

Most of the OPSBs, which used to have a business size of less than Rs.500 billion about 5 years

ago have grown their business to a meaningful size of over or near Rs.1 trillion now. In our view,

this becomes an attractive proposition for the NPSBs as combining such business size makes significant positive dent on the overall business;

Most of these OPSBs have survived 8 to 10 decades in the business quite successfully – this gives

some confidence on the stability of future business of these OPSBs;

Some of these OPSBs do not have identifiable promoters – promoters’ stake is zero in some of

these banks. Nor these banks have reputed institutions as the majority stake holders. Therefore,

in our view, the regulator may be comfortable in allowing consolidation of these banks;

Valuation – in terms of price to adjusted book value, these stocks remain quite cheap. They

command price to adjusted book values in the range of 1.2 to 2.5 times as compared to around

4 or higher multiples for NPSBs. Consolidation of such banks would be valuation accretive for large NPSBs;

While the levels of bad assets (Net NPAs) are at slightly elevated levels as compared to large

NPSBs, they are far superior as compared to the government-owned banks. In fact, some of these OPSB’s Net NPAs are comparable to a couple of large private banks;

Considering these facts, the consolidation of Old Private Sector Banks could emerge as theme in

the stock markets. Hence, it could be a worth option for the retail investors to evaluate Old Private

Sector Banks (OPSBs) as a thematic investment. In this theme, we have identified Karnataka Bank

and South Indian Bank as good candidates.

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 11

Invest Mantra September 2017

Current Market Price (Rs) 52 Week H/L (Rs) Mkt Cap (Rs mn)

153 181 / 100 43281

Source: Bloomberg

Source: Bloomberg

FINANCIALS (RS MN) FY17 FY18E FY19E

Interest income 51,854 57,376 65,498

Interest expense 36,948 39,936 45,238

Net interest income 14,906 17,440 20,260

Growth (%) 14.4% 17.0% 16.2%

Other income 8,093 7,015 7,764

Net profit 4,523 5,000 5,800

Growth (%) 8.9% 10.5% 16.0%

Gross NPA (%) 4.2 4.0 3.7

Net NPA (%) 2.6 2.4 2.0

Net interest margin (%) 2.6 2.7 2.8

CAR (%) 13.3 12.8 12.3

RoE (%) 10.2 10.6 10.8 Source: Company, Equinomics Research & Advisory Private Ltd

RoAA (%) 1.2 1.3 1.4

Dividend per share (Rs) 4.0 4.0 4.0

EPS (Rs) 16.0 17.7 20.5

Adjusted BVPS (Rs) 147.5 158.9 177.1

VALUATION PARAMETERS FY17 FY18E FY19E

P/E (x) 9.6 8.7 7.5

P/BV (x) 1.0 1.0 0.9

PRICE PERFORMANCE (%) 1M 3M 6M

0.2 (14.4) 11.3

Source: Bloomberg, Company, Equinomics Research & Advisory Private Ltd Source: Company

Last report at Rs.166 on 17 July 2017

Analyst: [email protected]

Target Price (Rs)

220

Karnataka Bank Ltd

Trend in Asset Quality

Potential Upside (%)

43.7%

1 Year Performance

Share Holding Pattern (%)

Trend in earnings (Rs bn)

FII

21.9%

DII

10.0%

Others

68.1%

50

100

150

200

250 Karnataka Bank Ltd Nifty

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18

NII PAT

2.0

2.5

3.0

3.5

4.0

4.5

5.0

10

12

14

16

18

Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18

Gross NPA (Rs bn - LHS)

Gross NPA (% - RHS)

Investment Argument

Karnataka Bank Ltd (KBL)is the cheapest Old Private Sector Bank (OPSB), trading at 1.2x trailing Adjusted Book Value;

KBL maintains the highest low-cost (CASA) deposits at around 29%

within the OPSB segment;

While the banking industry is growing credit at poor rate of around 6%,

KBL is one of few mid-sized private banks to grow its advances in double-

digit (10.2%) on year-on-year basis in the last two quarters;

KBL has built a business size of close to Rs.1 trillion, making it an

attractive play for any possible consolidation;

Promoter’s equity stake in the bank continues to remain “ZERO”, which could encourage any possible consolidation, in our view;

Risks & Concerns

Any possible deepening of deflationary pressures in the industrial economy could impact the banking sector including Karnataka Bank quite

adversely.

Company Background

Karnataka Bank survived successfully for 9 decades, built a network of

769 branches spread across India and has the strong presence in southern

India;

Sector Background

The average industry credit growth has crashed to near 2-decade low,

base lending rate has fallen substantially and bad assets remain at record high levels;

In the future, it is going to be a tough task for some of the large new

private banks (NPSBs) to continue to maintain margins and credit growth at very high levels. Hence, these NPSBs may be possibly opt for inorganic

route to grow.

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 12

Invest Mantra September 2017

South Indian Bank Ltd

Current Market Price (Rs) 52 Week H/L (Rs) Mkt Cap (Rs mn)

29 32 / 17 52618

Source: Bloomberg

Source: Bloomberg

Financia ls (Rs mn) FY17 FY18E FY19E

Interest income 58,471 68,058 79,478

Interest expense 41,716 48,351 56,243

Net interest income 16,755 19,707 23,235

Growth (%) 11.0% 17.6% 17.9%

Other income 7,156 6,440 7,084

Gross profit 12,146 13,185 16,029

Net profit 3,925.0 4,500.0 5,500.0

Growth (%) 17.7% 14.6% 22.2%

Gross NPA (%) 2.1 2.4 2.2

Net NPA (%) 1.9 1.6 1.1

Net interest margin (%) 2.4 2.5 2.5

CAR (%) 12.4 11.2 10.2 Source: Company, Equinomics

RoE (%) 9.0 10.5 13.3

RoAA (%) 0.6 0.6 0.7

Dividend per share (Rs) 0.4 0.5 0.5

EPS (Rs) 2.5 2.5 3.1

Adjusted BVPS (Rs) 22.2 24.4 25.5

Valuat ion parameters FY17 FY18E FY19E

P/E (x) 11.7 11.7 9.4

P/BV (x) 1.3 1.2 1.1

Price Performance (%) 1M 3M 6M

(2.3) 2.6 40.0

Source: Bloomberg, Company, Equinomics Research & Advisory Private Ltd Source: Company

Last report at Rs.30 on 2 August 2017

Analyst: [email protected]

Target Price (Rs)

36

Trend in Asset Quality

Potential Upside (%)

23.3%

1 Year Performance

Share Holding Pattern (%)

Trend in earnings (Rs bn)

FII

38.0%

DII

13.1%

Others

48.9%

70

90

110

130

150

170

190South Indian Bank Ltd Nifty

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18

NII PAT

2.0

2.5

3.0

3.5

4.0

4.5

5.0

10

12

14

16

18

20

Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18

Gross NPA (Rs bn - LHS) Gross NPA (% - RHS)

Investment Argument

South Indian Bank (SIB) is the second cheapest bank in the Old Private Sector Bank (OPSB) segment in terms of price to adjusted book value. However, in terms of market cap to business (at 4%), SIB is the cheapest along with Karnataka Bank. For other

banks in OPSB, this ratio is as high as 13%;

SIB highly attractive as compared to much smaller banks in the OPSB segment – it is 40% cheaper than Dhanlaxmi Bank and Lakshmi Vilas Bank in terms of price to Adjusted Book Value;

SIB has successfully maintained its double digit credit growth in June 2017 Quarter also as compared to the industry growth rate of ~6%;

In June 2017 Quarter, SIB recognized entire corporate watch list of Rs.6 billion as NPA (Non-performing Assets). This signals the completion of the clean-up exercise to a large extent;

Business size exceeds Rs.1 trillion and the Promoter’s stake continues to remain “ZERO”;

Risks & Concerns

Any possible deepening of slowdown in the Industrial economy and any massive fall in oil price could impact this bank. SIB draws a significant portion of business from the NRIs working in the oil regions;

Company Background

South Indian Bank (SIB), incorporated in 1928 at Thrissur in Kerala, survived successfully over 8 decades. The bank has a strong presence in south India (80%+ branches).

Sector Background

The average industry credit growth has crashed to near 2-decade low, base lending rate has fallen substantially and bad assets remain at record high levels;

In the future, it is going to be a tough task for some of the large new private banks

(NPSBs) to continue to maintain margins and credit growth at very high levels. Hence, these NPSBs may be possibly opt for inorganic route to grow.

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 13

Invest Mantra September 2017

THEME 3 - PSU STRATEGIC STAKE SALE

The government has kept the fiscal deficit target at 3.2% for FY2018. Already both Fiscal and Revenue Deficits have shot up. Spectrum revenues (part of non-tax revenues) from the telecom

industry are also under severe pressures. Poor industrial growth and gradual fall in the capital

formation (the gross fixed capital formation has consistently come down from 32.3% of GDP on FY2013 to 29.5% in FY2017) require continued boost to the expenditures. These economic

conditions could warrant aggressive approach to stake sale (with change of management into the

hands of private sector). Already, the government has proposed to go for strategic sale of stakes in several mid-sized PSUs like BEML, Dredging Corporation and Shipping Corporation of India;

In the listed space, such stake sale was proved to be highly successful in creating wealth for the

shareholders. Ever since the government sold its majority stake and changed the management control to the private sector, the market cap of Hindustan Zinc multiplied to over Rs.1.2 trillion from

a couple of billion rupees at the time of its stake sale. Other reasons to bank on these themes are:

Cash-rich PSUs may once again announce high dividend payouts due to soaring deficits and the government’s commitment to stick to the fiscal target;

Media sources had reported that the government may adopt auction route to divest the stake

in PSUs bringing out the true potential in the value of PSUs by promoting healthy competition among the private entrepreneurs;

Some of the PSUs have strong balance sheet, solid cash and also rich assets. Hence, stake sale in

such PSUs could help in finding true market value of these companies. We believe that their operating performance could also substantially improve over the years once they come under the

management of private entrepreneurs. In this investment theme, we have identified Balmer Lawrie

& Co and Shipping Corporation of India as potential candidates.

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 14

Invest Mantra September 2017

Current Market Price (Rs) 52 Week H/L (Rs) Mkt Cap (Rs mn)

246 287 / 163 28033

Source: Bloomberg

Source: Bloomberg

Financia ls (Rs mn) FY17 FY18E FY19E

Sales 17,790 19,000 21,500

Growth (%) 7.4 6.8 13.2

EBIT 2,580 2,950 3,330

EBIT margin (%) 14.5% 15.5% 15.5%

PBT 2,540 2,900 3,270

Net profit 1,700 1,940 2,170

EPS (Rs) 14.9 17.0 19.0

Growth (%) 3.6 14.0 11.8

CEPS 17.6 19.8 21.9

Book Value (Rs / Share) 119.0 124.0 129.0

Dividend per Share (Rs) 7.0 7.0 7.0

ROE (%) 12.5 14.3 15.9 Source: Company

ROCE (%) 17.8 19.3 21.2

Net cash (debt) 5,298 5,248 5,198

Net working capital (Days) 133.6 130.5 128.5

Valuat ion Parameters FY17 FY18E FY19E

P/E (x) 16.5 14.5 12.9

P/BV (x) 2.1 2.0 1.9

EV/Sales (x) 1.3 1.2 1.1

EV/EBITDA (x) 8.8 7.7 6.9

Price Performance (%) 1M 3M 6M

(1.4) 5.3 16.2

Source: Bloomberg, Company, Equinomics Research & Advisory Private Ltd

Potential Upside (%)

17.5%

1 Year Performance

Share Holding Pattern (%)

Segment revenu breakup (%)

Last report at Rs.243 on 10 August 2017

Analyst: [email protected]

Target Price (Rs)

289

Balmer Lawrie Company Ltd

FII

3.3% DII

8.5%

Others

88.2%

80

140

200

260

320

380

440 Balmer Lawrie Co Ltd Nifty

0%

7%

14%

21%

28%

35%

42%

FY13 FY14 FY15 FY16 FY17

Travel and tours Industrial Packaging

Logistics & Infrastructure. Greases and Lubricants

Others

Investment Argument

Balmer Lawrie Company (BLC) is known for consistent growth in revenues and

profits in a span of over 18 years (except for a couple of years in recent times) and has an impressive dividend track record. It holds free cash of around Rs.5 billion;

Over a period of 21 years, BLC has increased its Gross Block by more than 7 fold to about Rs.6.5 billion (by 2017 year-end) from Rs.0.87 billion in FY1995;

Strong balance sheet – net cash is over Rs.5 billion which is 1/5th of its market cap

– augurs well for possible special dividends and aggressive capex plans;

Looking at the government’s move to divest stake in BEML, a company with such strategic importance, the government may eventually divest its indirect stake

(36.88%) in BLC as it is focused mainly on commercial ventures;

BLC’s holding company, Balmer Lawrie Investments (BLIL, a government-owned company) still maintains (on its web site, www.blinv.com) its proposal to divest the

stake (61.8%) in BLC. BLC’s logistic segment holds rich real estate assets and hence, it could attract acquisition by the private sector at significant premium, if the

government decides to divest the stake held in BLC by BLIL;

Risks & Concerns

Profits are majorly derived from logistic infra and travel business. Hence, any

possible severe slowdown in the industrial and service economies could impact the performance adversely;

Company Background

BLC, over 150-year old company, has rich real estate assets spread over 30 facilities, mostly in cities. While 50% of total profits accrue from the logistic business, the

balance is contributed by industrial packaging, travel and grease & lubricants;

Sector Background

The growth of Logistic, industrial packaging and Greases & Lubricants segments

depends on the prospects of industrial economy, which is expected to improve going forward as the government has been pushing public expenditures;

Its travel segment, which has improved profitability substantially in the recent period due to major restructuring, depends on the growth of Indian service economy, which is still growing over 8%;

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 15

Invest Mantra September 2017

Shipping Corporation of India Ltd

Current Market Price (Rs) 52 Week H/L (Rs) Mkt Cap (Rs mn)

97 103 / 56 45229

Source: Bloomberg

Source: Capitaline

FINANCIALS (RS MN) FY17 FY18E FY19E

Sales 34,618 36,673 39,110

Growth (%) (16.0) 5.9 6.6

EBITDA 7,570 8,138 9,198

EBITDA margin (%) 21.9 22.2 23.5

PBT 1,776 2,643 3,729

Net profit 1,598 2,379 3,356

EPS (Rs) 3.4 5.1 7.2

Growth (%) (68.5) 48.8 41.1

CEPS (Rs) 15.6 17.0 18.9

Book value (Rs/share) 151.8 156.9 164.1

Dividend per share (Rs) - - 1.0 Source: Company, Kotak Securities - Private Client Research

ROE (%) 2.3 3.3 4.4

ROCE (%) 3.1 3.6 4.5

Net cash (debt) (26,762) (24,585) (22,498)

Net Working Capital (Days) 99.0 98.0 99.0

VALUATION PARAMETERS FY17 FY18E FY19E

P/E (x) 28.3 19.0 13.5

P/BV (x) 0.6 0.6 0.6

EV/Sales (x) 2.1 1.9 1.7

EV/EBITDA (x) 9.5 8.6 7.4

PRICE PERFORMANCE (%) 1M 3M 6M

18 25 54

Source: Bloomberg, Company, Kotak Securities - Private Client Research Source: Company

Last report at Rs.93 on 24 August 2017

Analyst: [email protected]

Target Price (Rs)

125

Book Value for SCI (Rs/Share)

Potential Upside (%)

28.7%

1 Year Performance

Share Holding Pattern (%)

Gross debt of the company (Rs mn)

Promoter

63.7%FII

3.6%

DII

18.8%

Others

13.8%

50

110

170

230

290

350 Shipping Corporation of India Ltd Nifty

Investment Argument

Shipping markets have become stable and is expected to improve going

forward

We also expect operating cost to remain low with lower bunker cost that should translate into improvement in EBIDTA and return ratios of the

company.

Company is well diversified into every segment of shipping

The balance sheet health of the company has improved over the last two

years with debt prepayment and is expected to improve further going forward

Strategic sale by government is expected to remove government bound constraints and improve management of SCI which should add value to the

company

Risks & Concerns

Healthy new ship build orders to keep shipping rates subdued

Weak trade can negatively impact freight rates.

Company Background

SCI is a PSU with GOI holding around 64% in the company

SCI primarily operate in the tanker segments.

Sector Background

There are three main segments of shipping including tankers, dry bulk, and

liners.

Shipping companies usually operate through three types of contracts including spot, contract and contract of Affreightment

0

20,000

40,000

60,000

80,000

FY14 FY15 FY16 FY17 FY18E FY19E

0

30

60

90

120

150

180

FY14 FY15 FY16 FY17 FY18 FY19

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 16

Invest Mantra September 2017

THEME 4 - DEEP VALUE STOCKS

Deep value stocks are the ones which have rich assets or huge free cash or substantial growth potential but the market hasn’t fully discounted such valuations. Such stocks normally show resilient

when the equity markets go through huge volatility with downward bias. Even if such deep value

stocks give in to the market pressures, the investors could confidently make use of such opportunities to continuously accumulate the stock. (However, from the perspective of risk-

management, the investors shouldn’t exceed 5% to 10% allocation per stock depending upon their

risk profile). In this investment theme, we have identified Bombay Burmah Trading Corporation as a potential candidate.

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 17

Invest Mantra September 2017

Bombay Burmah Trading Corporation

Current Market Price (Rs) 52 Week H/L (Rs) Mkt Cap (Rs mn)

1021 1085 / 441 71230

Source: Bloomberg

Source: Bloomberg

Financia ls (Rs mn) FY17 FY18E FY19E

Sales 96,093 105,700 118,390

Growth (%) 7.7 10.0 12.0

EBIT 14,529 15,525 16,859

EBIT margin (%) 15.1% 14.7% 14.2%

PBT 12,786 13,735 14,909

Net profit 8,582 9,434 10,109

EPS (Rs) 123.0 135.3 144.5

Growth (%) 7.6 9.9 7.2

CEPS 141.8 154.6 165.7

Book Value (Rs / Share) 346.7 368.2 396.8

Dividend per Share (Rs) 1.0 1.0 1.0

ROE (%) 39.6 37.7 37.8 Source: Company

ROCE (%) 44.6 47.7 51.8

Net cash (debt) (7,536) 1,464 15,216

Net working capital (Days) 10.8 10.8 10.8

Valuat ion Parameters FY17 FY18E FY19E

P/E (x) 8.3 7.5 7.1

P/BV (x) 2.9 2.8 2.6

EV/Sales (x) 0.7 0.6 0.6

EV/EBITDA (x) 4.5 4.3 3.9

Price Performance (%) 1M 3M 6M

16.1 14.0 47.9

Source: Bloomberg, Company, Equinomics Research & Advisory Private Ltd

Last report at Rs.878 on 10 August 2017

Analyst: [email protected]

Target Price (Rs)

1130

Potential Upside (%)

10.7%

1 Year Performance

Share Holding Pattern (%)

BBTC EVs % Discount to its Investmets (Trend)

Promoter

60.1%

FII

11.0%

DII

4.4%

Others

24.5%

80

280

480

680

880

Bombay Burmah Trading Corporation Ltd Nifty

Investment Argument

Bombay Burmah Trading Corporation (BBTC) holds 50.75% stake in in Britannia Industries (a step-down subsidiary). While the Enterprise Value (EV) of BBTC stands

at Rs.72,688 million, the market value of its investments in Britannia alone is worth

4-times at Rs.2,58,870 million, which is at 72% discount to value of total investments. However, the average of holding companies (HCs) discount stands at

around 55% only;

BBTC deserves much lower discount:

95% of BBTC’s total investment value comes from Britannia. For most HCs, they come from several companies – theoretically speaking, unlocking possibility

from a single investment is relatively higher;

Most HCs hold shares of firms engaged in diversified and cyclical businesses. However, Britannia is engaged in consistently growing FMCG business, which

enjoys much higher premium in markets;

While many HCs do not have any assets on their own, BBTC has rich assets like huge plantations, and also reportedly significant land parcels;

Risks & Concerns

Only possible risk to our view is any possible governance issue in terms of divestment of holdings in Britannia in favour of any promoters. However,

considering India’s regulatory set up, we believe that such risk is too low.

Company Background

BBTC, part of the Wadia Group, is engaged majorly in tea & coffee plantations,

and auto electric component manufacturing;

Sector Background

Plantations, auto-electric components and Investment are key segments for BBTC. Plantation business remains highly cyclical and expected to remain so;

Auto-electric business is quite stable one in terms of revenues and profits streams.

This segment is expected to remain stable going forward as well;

Investment incomes are mainly from Britannia, which is expected to continue to

maintain consistent growth in both profits and dividend payments over the years;

60%

65%

70%

75%

80%

85%

-

50

100

150

200

250

300

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Current

Enterprise Value (EV ) (Rs.bn - LHS)

Value of Investment in Britannia (Rs.bn - LHS)

% Discount (RHS)

SEPTEMBER 1, 2017

PRIVATE CLIENT RESEARCH 1-MONTH PORTFOLIO

STRICTLY FOR INTERNAL CIRCULATION ONLY

NIFTY: 9918 Stock Weight M Cap Current

(%) (Rs mn) Price PE (x) Comment (Rs) FY18 FY19E

ITC 10 3,390,486 282 30.0 26.6 Reassuring signals from the government, as excise duty hikewell below past five years' average

Discount to average FMCG multiples provides protectionfrom downsides

Genus Power 9 12,760 50 16.6 13.8 Demand for meters is gaining traction

Smart meters offers a good long term opportunity

Shipping Corp of India 9 46,580 100 19.6 13.9 Shipping markets have become stable which is positive forthe stock

Strategic sale by government is expected to improvemanagement of SCI

Stock is trading at attractive valuations

M&M 9 825,830 1,345 20.7 18.8 Good monsoons is likely to keep tractor demand robustin FY18

Increased share of tractor revenues will be positive foroverall EBITDA margins

UPL 9 422,231 831 18.5 14.7 UPL is coming into the Nifty in end of Sep’17. This shouldlead to re-rating of the stock

In the Agrochemical space the company is way ahead of itspeers in terms of size. It has best in class RoE of 25% onsuch a high base and earnings CAGR forecast of 22%(for FY17-19E).

Engineers India 9 105,124 156 25.6 17.3 EIL expected to benefit from recovery in spending by major

hydrocarbon players like HPCL, BPCL and IOC. Company

likely to expand margins in FY17/FY18.

Kansai Nerolac 9 274,890 510 48.6 44.0 Strong automotive demand is a big positive for the companywhich is the market leader in automotive paints

Company is also aggressively expanding the decorativesegment

Raw material situation to remain benign

Guj. Alkalies & Chem 9 32239 439 6.8 6.7 Caustic soda prices have risen to US$470/tonne in the lastsix months. We expect the prices to remain firm for the next one or two years, which would drive the earnings for GACLin FY18E & FY19E

Asian Granito 9 13,846 461 25.9 17.6 With its continuous innovations for introducing value addedproducts, access to low cost gas, shift towards increasingB2C sales, we expect company’s revenues and PAT to growat a CAGR of 17%/42% between FY17-19. Stock is tradingat attractive valuations

TV18 Broadcast 9 65,056 38 28.8 17.5 See pick-up in near-term ratings of Hindi GEC channels,valuations reasonable at 18.5x PER FY19E

Finolex Industries 9 75,576.9 609 20.5 17.1 GST led disruption is over and demand has recovered fromend of July. Good monsoon poositive for rural economy and agri pipes demand.

Targets for double digit volume growth in pipes and fittingbusiness in FY18

Source : Kotak Securities - Private Client research

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 18

Invest Mantra September 2017

RATING SCALE Definitions of ratings BUY – We expect the stock to deliver more than 12% returns over the next 9 months

ACCUMULATE – We expect the stock to deliver 5% - 12% returns over the next 9 months

REDUCE – We expect the stock to deliver 0% - 5% returns over the next 9 months

SELL – We expect the stock to deliver negative returns over the next 9 months

NR – Not Rated. Kotak Securities is not assigning any rating or price target to the stock. The report has been prepared for

information purposes only.

RS – Rating Suspended. Kotak Securities has suspended the investment rating and price target for this stock, either because there

is not a Sufficient fundamental basis for determining, or there are legal, regulatory or policy constraints around publishing,

an investment rating or target. The previous investment rating and price target, if any, are no longer in effect for this stock

and should not be relied upon.

NA – Not Available or Not Applicable. The information is not available for display or is not applicable

NM – Not Meaningful. The information is not meaningful and is therefore excluded.

NOTE – Our target prices are with a 9-month perspective. Returns stated in the rating scale are our internal benchmark.

FUNDAMENTAL RESEARCH TEAM

Sanjeev Zarbade Ruchir Khare Amit Agarwal Nipun Gupta Capital Goods, Engineering Capital Goods, Engineering Logistics, Paints, Transportation Information Technology

[email protected] [email protected] [email protected] [email protected]

+91 22 6218 6424 +91 22 6218 6431 +91 22 6218 6439 +91 22 6218 6433

Teena Virmani Ritwik Rai Jatin Damania Ashini Shah Construction, Cement FMCG, Media Metals & Mining Midcap

[email protected] [email protected] [email protected] [email protected]

+91 22 6218 6432 +91 22 6218 6426 +91 22 6218 6440 +91 22 6218 5438

Arun Agarwal Sumit Pokharna Pankaj Kumar K. Kathirvelu Auto & Auto Ancillary Oil and Gas Midcap Production

[email protected] [email protected] [email protected] [email protected]

+91 22 6218 6443 +91 22 6218 6438 +91 22 6218 6434 +91 22 6218 6427

TECHNICAL RESEARCH TEAM

Shrikant Chouhan Amol Athawale

[email protected] [email protected]

91 22 6218 5408 +91 20 6620 3350

DERIVATIVES RESEARCH TEAM

Sahaj Agrawal Malay Gandhi Prashanth Lalu Prasenjit Biswas

[email protected] [email protected] [email protected] [email protected]

+91 79 6607 2231 +91 22 6218 6420 +91 22 6218 5497 +91 33 6625 9810

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 19

Invest Mantra September 2017

Disclosure/Disclaimer – The disclaimer/disclosure for Balmer Lawrie, BBTC, Karnataka Bank, South Indian Bank is as follows.

The information contained herein is being circulated by KSL based on the Research Report obtained from Equinomics Research & Advisory Private Ltd (Equinomics), a SEBI Registered Investment Advisor (Registration No. INA000001712). As declared by Equinomics, the said investment advisory firm, its Research Analyst and its Managing Director

Mr. I. G. Chokkalingam and his relatives have no material conflict of interest in providing the said details to us except the below.

Disclosure/Disclaimer of Equinomics Research & Advisory Private Ltd as declared by it:

Whether Research Analyst's or relatives/ Equinomics/ Associate Company have any financial interest in the Subject Company and nature of such financial interest – South Indian

Bank - Yes

Whether Research Analyst or relatives/ Equinomics/ Associate Company have actual/beneficial ownership of 1% or more in the securities of Subject Company at the end of the

month immediately preceding the date of publication of the document- No

Whether the Research Analyst/ Equinomics/ Associate Company has received any compensation or any other benefits from the Subject Company or third party in connection

with the research report or any other activity. Whether Managing Director of Equinomics / Research Analyst has served as an officer, director or employee of the subject company. Whether the Research Analyst/ Equinomics/ Associate Company has been engaged in market making activity of the subject company. Whether the Research Analyst/

Equinomics/ Associates or Relatives, have any other material conflict of interest at the time of publication of the research report or at the time of public appearance. Whether

Equinomics or its associate company have managed or co-managed public offering of securities for the subject company in the past twelve months. Whether Equinomics or its

associate company have received any compensation for investment banking or merchant banking or brokerage services from the subject company. Whether Equinomics or its associate company have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject

company - No

Whether Research Analyst / Equinomics has recommended the scrip to its clients in the past and the recommendation is active as on the date of this report- Yes

Equinomics' Ratings and Other Definitions

BUY- We expect this stock to deliver more than 15% returns over the next 12 months.

ACCUMULATE- We expect this stock to deliver 5-10% returns over the next 12 months.

HOLD- We expect this stock to deliver 5% returns over the next 12 months.

SELL- Above Target Price. *Wait for stock update when target price reached.

Equinomics Research & Advisory Private Ltd, Chokkalingam - Founder & Managing Director, Address: J-1, J-2, New Gitanjali Society, Gate No: 3, Raheja Township, (Opp. To Malad Panchvati Co Op Housing Society), Malad East, Mumbai - 400 097. Ph: +91 22 28769268 | Email: [email protected] | Website: www.equinomics.in.

CIN:U67190MH2014PTC252252. For general disclosures of Equinomics Research & Advisory Private Ltd, pls refer the link http:// equinomics.in/wp-

content/uploads/2017/05/Equinomics-Morning-Insight-Disclaimer.pdf

Disclosure/Disclaimer of KSL

Kotak Securities Limited established in 1994, is a subsidiary of Kotak Mahindra Bank Limited. Kotak Securities is one of India's largest brokerage and distribution house. Kotak

Securities Limited is a corporate trading and clearing member of Bombay Stock Exchange Limited (BSE), National Stock Exchange of India Limited (NSE), Metropolitan Stock

Exchange of India Limited (MSE). Our businesses include stock broking, services rendered in connection with distribution of primary market issues and financial products like

mutual funds and fixed deposits, depository services and Portfolio Management. Kotak Securities Limited is also a depository participant with National Securities Depository Limited (NSDL) and Central Depository Services (India) Limited (CDSL). Kotak Securities Limited is also registered with Insurance Regulatory and Development Authority as

Corporate Agent for Kotak Mahindra Old Mutual Life Insurance Limited and is also a Mutual Fund Advisor registered with Association of Mutual Funds in India (AMFI). We are

registered as a Research Analyst under SEBI (Research Analyst) Regulations, 2014.

We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in last five years. However SEBI, Exchanges and Depositories have conducted the routine inspection and based on their observations have issued advise/warning/ deficiency letters/ or levied minor penalty

on KSL for certain operational deviations. We have not been debarred from doing business by any Stock Exchange/ SEBI or any other authorities; nor has our certificate of

registration been cancelled by SEBI at any point of time. We offer our research services to clients as well as our prospects.

This document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any other person. Persons

into whose possession this document may come are required to observe these restrictions. This material is for the personal information of the authorized recipient, and we are not soliciting any action based upon it. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an

offer or solicitation would be illegal. It is for the general information of clients of Kotak Securities Ltd. It does not constitute a personal recommendation or take into account

the particular investment objectives, financial situations, or needs of individual clients. Neither Kotak Securities Limited, nor any person connected with it, accepts any liability

arising from the use of this document. The recipients of this material should rely on their own investigations and take their own professional advice. Price and value of the investments referred to in this material may go up or down. Past performance is not a guide for future performance. Certain transactions -including those involving futures,

options and other derivatives as well as non-investment grade securities - involve substantial risk and are not suitable for all investors. Reports based on technical analysis centers

on studying charts of a stock's price movement and trading volume, as opposed to focusing on a company's fundamentals and as such, may not match with a report on a

company's fundamentals.

Opinions expressed are the current opinions as of the date appearing on this material only. While we endeavor to update on a reasonable basis the information discussed in

this material, there may be regulatory, compliance or other reasons that prevent us from doing so. Prospective investors and others are cautioned that any forward-looking

statements are not predictions and may be subject to change without notice. Our proprietary trading and investment businesses may make investment decisions that are

inconsistent with the recommendations expressed herein. Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group.

The views and opinions expressed in this document may or may not match or may be contrary with the views, estimates, rating, and target price of the Institutional Equities Research Group of Kotak Securities Limited.

We and our affiliates/associates, officers, directors, and employees, Research Analyst(including relatives) worldwide may: (a) from time to time, have long or short positions in,

and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other

compensation or act as a market maker in the financial instruments of the subject company/company (ies) discussed herein or act as advisor or lender / borrower to such company (ies) or have other potential/material conflict of interest with respect to any recommendation and related information and opinions at the time of publication of

Research Report or at the time of public appearance.

Kotak Securities Limited (KSL) may have proprietary long/short position in the above mentioned scrip(s) and therefore may be considered as interested. The views provided

herein are general in nature and does not consider risk appetite or investment objective of particular investor; readers are requested to take independent professional advice before investing. This should not be construed as invitation or solicitation to do business with KSL. Kotak Securities Limited is also a Portfolio Manager. Portfolio Management

Team (PMS) takes its investment decisions independent of the PCG/Institutional Equities research and accordingly PMS may have positions contrary to the PCG/Institutional

Equities research recommendation. Kotak Securities Limited does not provide any promise or assurance of favorable view for a particular industry or sector or business group

in any manner. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to risk return profile and take professional

advice before investing.

No part of this material may be duplicated in any form and/or redistributed without Kotak Securities' prior written consent. Details of Associates are available on our website ie

www.kotak.com

We or our associates may have received compensation from the subject company(ies) in the past 12 months.

We or our associates have managed or co-managed public offering of securities for the subject company(ies) in the past 12 months: No

We or our associates may have received compensation for investment banking or merchant banking or brokerage services from the subject company(ies) in the past 12

months. We or our associates may have received any compensation for products or services other than investment banking or merchant banking or brokerage services from

the subject company(ies) in the past 12 months. We or our associates may have received compensation or other benefits from the subject company(ies) or third party in

connection with the research report. Our associates may have financial interest in the subject company(ies).

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 20

Invest Mantra September 2017

Research Analyst or his/her relative's financial interest in the subject company(ies): No

Kotak Securities Limited has financial interest in the subject company(ies) at the end of the month immediately preceding the date of publication of Research Report: Balmer

Lawrie & Co - Yes

Our associates may have actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately preceding the date of

publication of Research Report.

Kotak Securities Limited has actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately preceding the date of

publication of Research Report: No

Subject company(ies) may have been client during twelve months preceding the date of distribution of the research report.

"A graph of daily closing prices of securities is available at www.nseindia.com and http://economictimes.indiatimes.com/markets/stocks/stock-quotes. (Choose a company from

the list on the browser and select the "three years" icon in the price chart)."

Kotak Securities Limited. Registered Office: 27 BKC, C 27, G Block, Bandra Kurla Complex, Bandra (E), Mumbai 400051. CIN: U99999MH1994PLC134051, Telephone No.: +22 43360000, Fax No.: +22 67132430. Website: www.kotak.com/www.kotaksecurities.com. Correspondence Address: Infinity IT Park, Bldg. No 21, Opp. Film City Road, A K

Vaidya Marg, Malad (East), Mumbai 400097. Telephone No: 42856825. SEBI Registration No: NSE INB/INF/INE 230808130, BSE INB 010808153/INF 011133230, MSE INE

260808130/INB 260808135/INF 260808135, AMFI ARN 0164, PMS INP000000258 and Research Analyst INH000000586. NSDL/CDSL: IN-DP-NSDL-23-97.

Our research should not be considered as an advertisement or advice, professional or otherwise. The investor is requested to take into consideration all the risk factors including

their financial condition, suitability to risk return profile and the like and take professional advice before investing. Investments in securities market are subject to market risks, read all the related documents carefully before investing. Derivatives are a sophisticated investment device. The investor is requested to take into consideration all the risk factors

before actually trading in derivative contracts. Compliance Officer Details: Mr. Manoj Agarwal. Call: 022 - 4285 8484, or Email: [email protected].

In case you require any clarification or have any concern, kindly write to us at below email ids:

Level 1: For Trading related queries, contact our customer service at '[email protected]' and for demat account related queries contact us at [email protected] or call us on: Online Customers - 30305757 (by using your city STD code as a prefix) or Toll free numbers 18002099191 / 1800222299, Offline Customers - 18002099292

Level 2: If you do not receive a satisfactory response at Level 1 within 3 working days, you may write to us at [email protected] or call us on 022- 42858445 and if

you feel you are still unheard, write to our customer service HOD at [email protected] or call us on 022-42858208.

Level 3: If you still have not received a satisfactory response at Level 2 within 3 working days, you may contact our Compliance Officer (Mr. Manoj Agarwal) at [email protected] or call on 91- (022) 4285 8484.

Level 4: If you have not received a satisfactory response at Level 3 within 7 working days, you may also approach CEO (Mr. Kamlesh Rao) at [email protected] or call on

91- (022) 4285 8301.

Kotak Securities – Private Client Research Please see the Disclosure/Disclaimer on the last page For Private Circulation 21

Invest Mantra September 2017

Disclosure/Disclaimer Kotak Securities Limited established in 1994, is a subsidiary of Kotak Mahindra Bank Limited. Kotak Securities is one of India's largest brokerage and distribution house.

Kotak Securities Limited is a corporate trading and clearing member of Bombay Stock Exchange Limited (BSE), National Stock Exchange of India Limited (NSE), Metropolitan Stock

Exchange of India Limited (MSE). Our businesses include stock broking, services rendered in connection with distribution of primary market issues and financial products like mutual funds and fixed deposits, depository services and Portfolio Management.

Kotak Securities Limited is also a depository participant with National Securities Depository Limited (NSDL) and Central Depository Services (India) Limited (CDSL). Kotak Securities

Limited is also registered with Insurance Regulatory and Development Authority as Corporate Agent for Kotak Mahindra Old Mutual Life Insurance Limited and is also a Mutual Fund Advisor registered with Association of Mutual Funds in India (AMFI). We are registered as a Research Analyst under SEBI (Research Analyst) Regulations, 2014.

We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in last five years. However

SEBI, Exchanges and Depositories have conducted the routine inspection and based on their observations have issued advise/warning/deficiency letters/ or levied minor penalty on KSL for certain operational deviations. We have not been debarred from doing business by any Stock Exchange / SEBI or any other authorities; nor has our certificate of registration

been cancelled by SEBI at any point of time.

We offer our research services to clients as well as our prospects.

This document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any other person. Persons

into whose possession this document may come are required to observe these restrictions.

This material is for the personal information of the authorized recipient, and we are not soliciting any action based upon it. This report is not to be construed as an offer to sell or

the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It is for the general information of clients of Kotak Securities

Ltd. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients.

We have reviewed the report, and in so far as it includes current or historical information, it is believed to be reliable though its accuracy or completeness cannot be guaranteed.

Neither Kotak Securities Limited, nor any person connected with it, accepts any liability arising from the use of this document. The recipients of this material should rely on their

own investigations and take their own professional advice. Price and value of the investments referred to in this material may go up or down. Past performance is not a guide for future performance. Certain transactions -including those involving futures, options and other derivatives as well as non-investment grade securities - involve substantial risk and

are not suitable for all investors. Reports based on technical analysis centers on studying charts of a stock's price movement and trading volume, as opposed to focusing on a

company's fundamentals and as such, may not match with a report on a company's fundamentals.

Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavor to update on a reasonable basis the information discussed in this

material, there may be regulatory, compliance or other reasons that prevent us from doing so. Prospective investors and others are cautioned that any forward-looking statements

are not predictions and may be subject to change without notice. Our proprietary trading and investment businesses may make investment decisions that are inconsistent with

the recommendations expressed herein.

Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report has been prepared by the Private Client Group.

The views and opinions expressed in this document may or may not match or may be contrary with the views, estimates, rating, target price of the Institutional Equities Research

Group of Kotak Securities Limited.

We and our affiliates/associates, officers, directors, and employees, Research Analyst(including relatives) worldwide may: (a) from time to time, have long or short positions in,

and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other

compensation or act as a market maker in the financial instruments of the subject company/company (ies) discussed herein or act as advisor or lender / borrower to such company (ies) or have other potential/material conflict of interest with respect to any recommendation and related information and opinions at the time of publication of Research Report

or at the time of public appearance. Kotak Securities Limited (KSL) may have proprietary long/short position in the above mentioned scrip(s) and therefore may be considered as

interested. The views provided herein are general in nature and does not consider risk appetite or investment objective of particular investor; readers are requested to take

independent professional advice before investing. This should not be construed as invitation or solicitation to do business with KSL. Kotak Securities Limited is also a Portfolio Manager. Portfolio Management Team (PMS) takes its investment decisions independent of the PCG research and accordingly PMS may have positions contrary to the PCG

research recommendation. Kotak Securities Limited does not provide any promise or assurance of favourable view for a particular industry or sector or business group in any

manner. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to risk return profile and take professional advice

before investing.

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or

their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

No part of this material may be duplicated in any form and/or redistributed without Kotak Securities' prior written consent.

Details of Associates are available on our website ie www.kotak.com

Research Analyst has served as an officer, director or employee of subject company(ies): No

We or our associates may have received compensation from the subject company(ies) in the past 12 months.

We or our associates have managed or co-managed public offering of securities for the subject company(ies) in the past 12 months: No

We or our associates may have received compensation for investment banking or merchant banking or brokerage services from the subject company(ies) in the past 12 months. We or our associates may have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject

company(ies) in the past 12 months. We or our associates may have received compensation or other benefits from the subject company(ies) or third party in connection with the

research report. Our associates may have financial interest in the subject company(ies).

Research Analyst or his/her relative's financial interest in the subject company(ies): No

Kotak Securities Limited has financial interest in the subject company(ies) at the end of the month immediately preceding the date of publication of Research Report: Gail India,

ITC, Tata Motors- Yes

Our associates may have actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately preceding the date of publication

of Research Report.

Research Analyst or his/her relatives has actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately preceding the date

of publication of Research Report: No.