26

Investing in minerals and metals production Olle Östenson, Caromb Consulting

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | roy-whitehead |

| View: | 224 times |

| Download: | 2 times |

Investing in minerals and metals production

Olle Östenson, Caromb Consulting

Outline of the presentation• Providing a perspective – basic characteristics of mining• Mining taxation

– Mining law or agreements?– Profit tax or royalties?– Taxation and ownership– Stability and security– Smoothing out variations– Windfall profits– Recent policy changes and

tax reforms• Some non-tax issues

– Security of title– Foreign exchange regulations– Environment– Support to national economic development and diversification– Local development issues– Transparency– Human rights

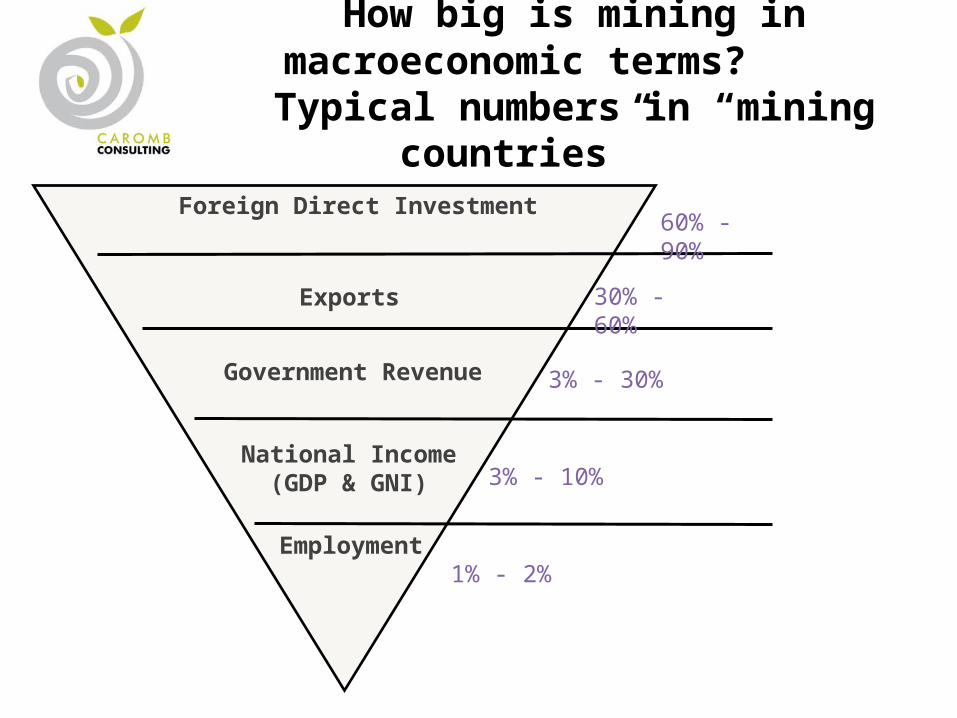

How big is mining in macroeconomic terms? Typical numbers in “mining countries”

www.icmm.com

Foreign Direct Investment

Exports

Government Revenue

National Income (GDP & GNI)

Employment

60% - 90%

30% - 60%

3% - 30%

3% - 10%

1% - 2%

www.icmm.com

A few words on the particularities of mining

• Foreign investment: few countries have the necessary capital• Large economic importance

– Major economic changes and dislocations– Important distribution issues– Scope for diversion of revenue

• Long time scale: decades, even centuries– Need for adaptability and for review mechanisms– Danger of myopia, exaggerating the relevance of the present

• Fixed location: you can´t move a mine– The investor is captive– Irreversability, get it right the first time

• High risks– Geological risks– Market risks (price and volume fluctuations)

Mining also shares some characteristics with other natural resource

based industries• Highly capital intensive, generates very few jobs

directly• Export oriented, part of transparent and open world

market• Operates under conditions of strong competition• Uses labour with specialized skills• Produces standardized, homogeneous products• Depends on imports of specialized equipment

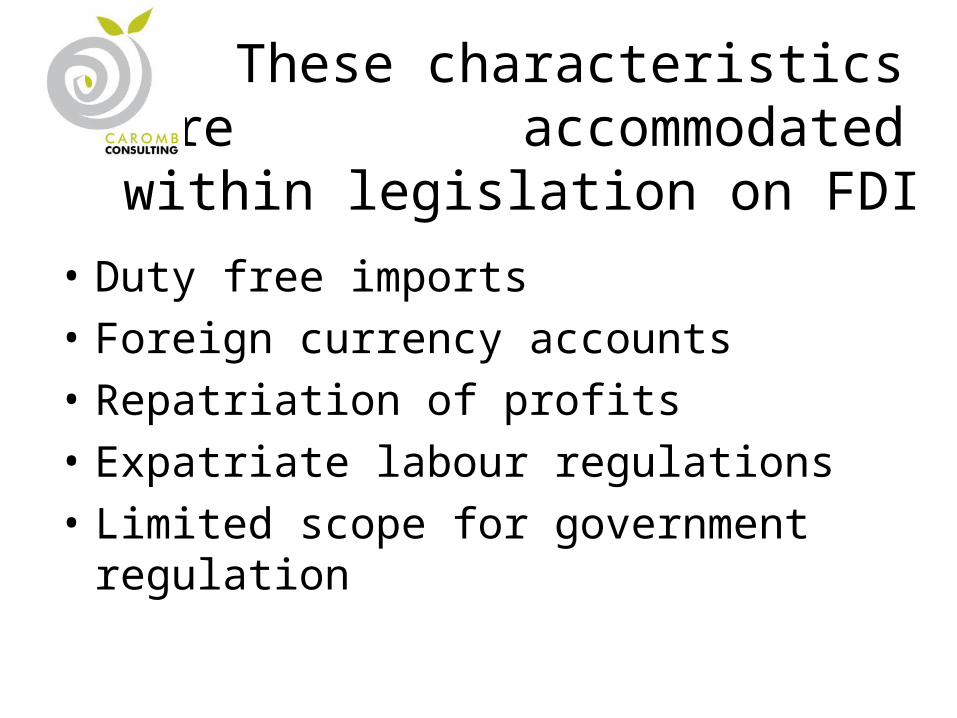

These characteristics are accommodated within legislation

on FDI• Duty free imports• Foreign currency accounts• Repatriation of profits• Expatriate labour regulations• Limited scope for government regulation

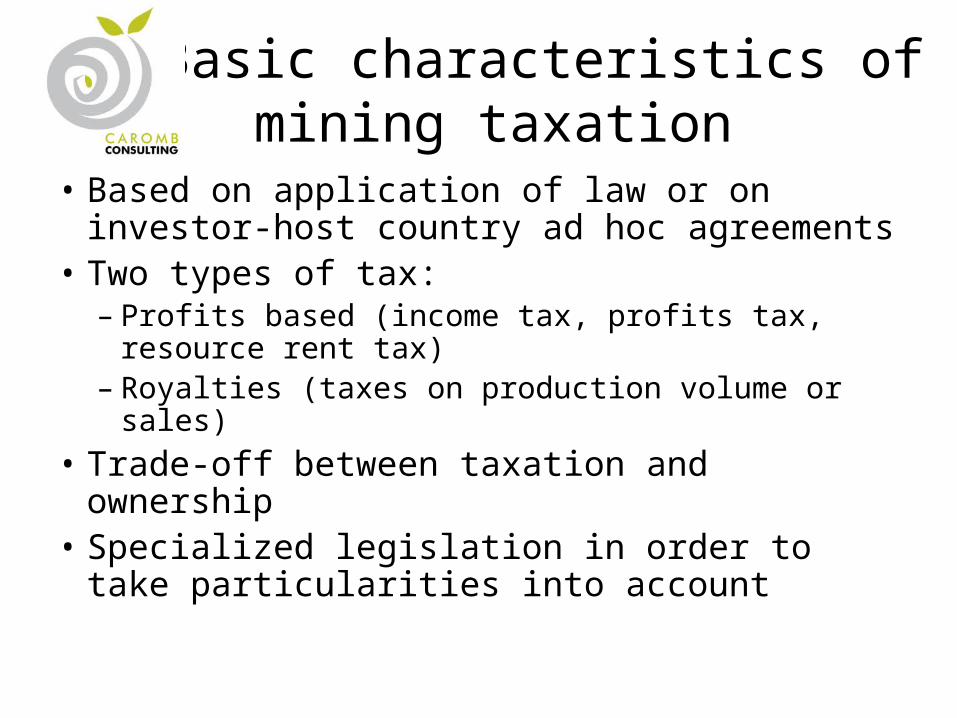

Basic characteristics of mining taxation

• Based on application of law or on investor-host country ad hoc agreements

• Two types of tax:– Profits based (income tax, profits tax, resource

rent tax)– Royalties (taxes on production volume or sales)

• Trade-off between taxation and ownership• Specialized legislation in order to take

particularities into account

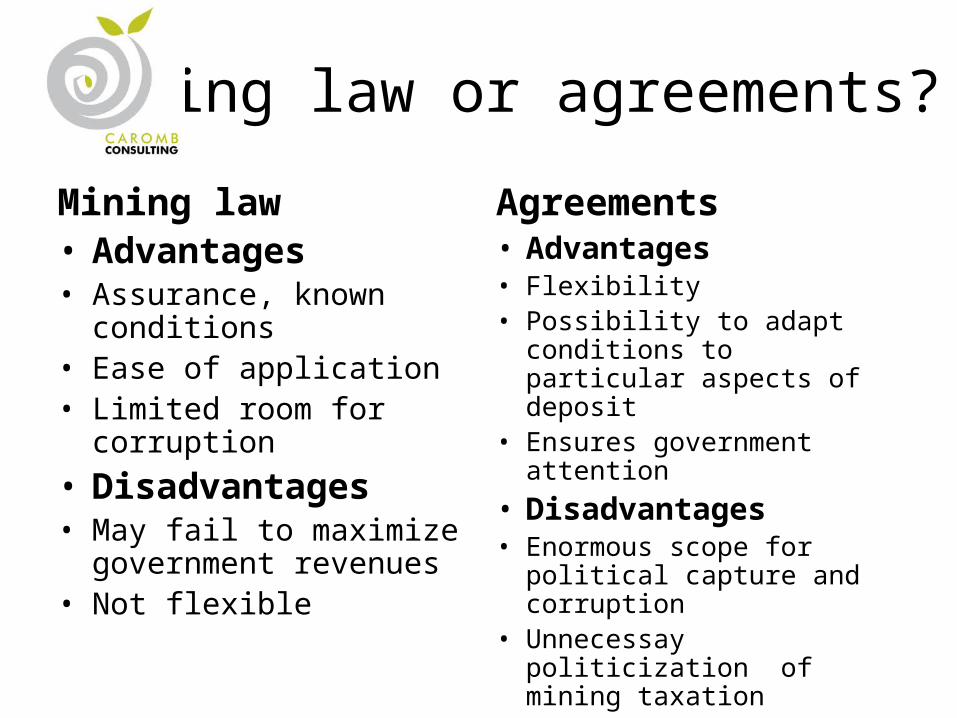

Mining law or agreements?

Mining law• Advantages• Assurance, known

conditions• Ease of application• Limited room for corruption• Disadvantages• May fail to maximize

government revenues• Not flexible

Agreements• Advantages• Flexibility• Possibility to adapt

conditions to particular aspects of deposit

• Ensures government attention

• Disadvantages• Enormous scope for political

capture and corruption• Unnecessay politicization of

mining taxation

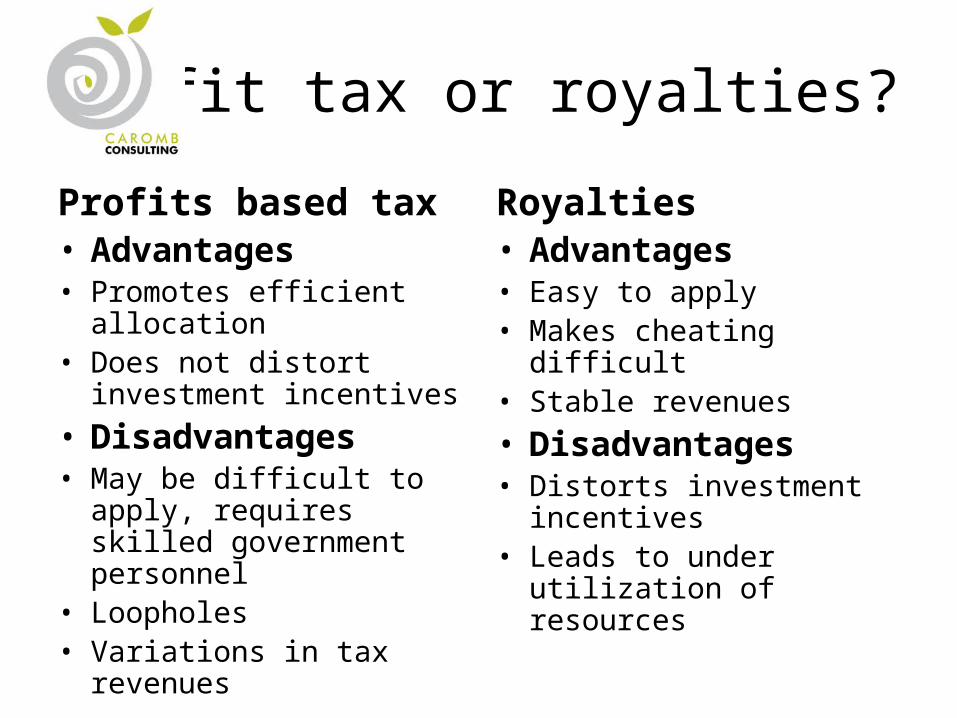

Profit tax or royalties?

Profits based tax• Advantages• Promotes efficient

allocation• Does not distort investment

incentives• Disadvantages• May be difficult to apply,

requires skilled government personnel

• Loopholes• Variations in tax revenues

Royalties• Advantages• Easy to apply• Makes cheating difficult• Stable revenues • Disadvantages• Distorts investment

incentives• Leads to under utilization of

resources

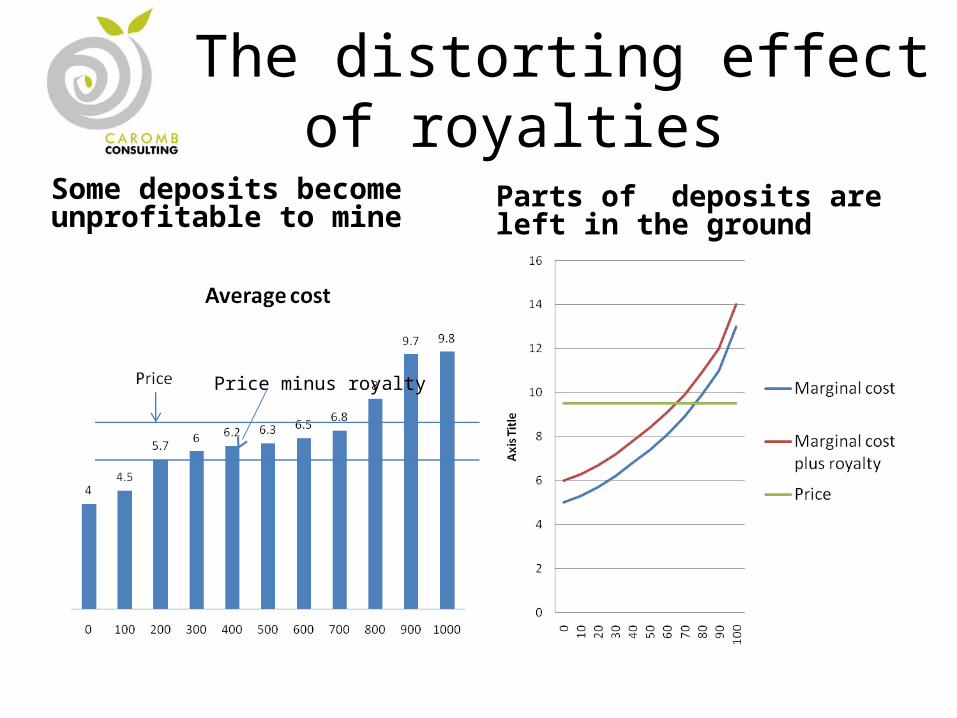

The distorting effect of royaltiesSome deposits become unprofitable to mine

Parts of deposits are left in the ground

Price minus royalty

Taxation and ownership• Ownership… • …gives the government a share of the profits even if the company evades taxes• …provides some control over operating decisions• …may be a good investment• …can be paid out of future dividends• But ownership…• …implies a commitment to provide risk capital if needed• …gives little control if you are not a majority owner• …may not be as good an investment of scarce funds as education, for instance• ……provides uncertain income and comes with a risk• …means the government has dual roles, as a regulator and an operator• And, anything that a government requires in terms of ownership has to be paid for

with lower taxes

Mining particularities: Particular measures

• Measures to ensure the stability and security desired by investors

• Smoothing out variations – of interest both to investor and host country

• Capture windfall profits

Stability and security

• Guarantee of tenure• Stability clauses: taxation regime frozen for

20-30 years• Accelerated depreciation• Capitalization of exploration expenditure• Arbitration clauses• For government: environmental guarantees,

performance bonds

Smoothing out variations

• For company– Loss carry forward provisions– Provisions for hedging in tax code

• For government– Royalties

Windfall profits• Profits resulting from very high prices or exceptional high

quality deposits form part of the resource rent• A tax on rents does not, in principle, distort investment

incentives• A resource rent tax is imposed on the rent that is left after all

production factors have been compensated• Very few countries (Mongolia, Papua New Guinea and, soon,

Australia) use resource rent tax• Reasons

– Resistance from mining companies– Difficult to calculate– Only comes into play after several years, discounted value is low

Recent policy changes and tax reforms

• After more than two decades of emphasizing investment attraction, the pendulum has swung back to tax revenue maximization

• Reasons:– Previous legislation was not sufficiently balanced– Mineral demand and prices increased– Increased accountability of governments

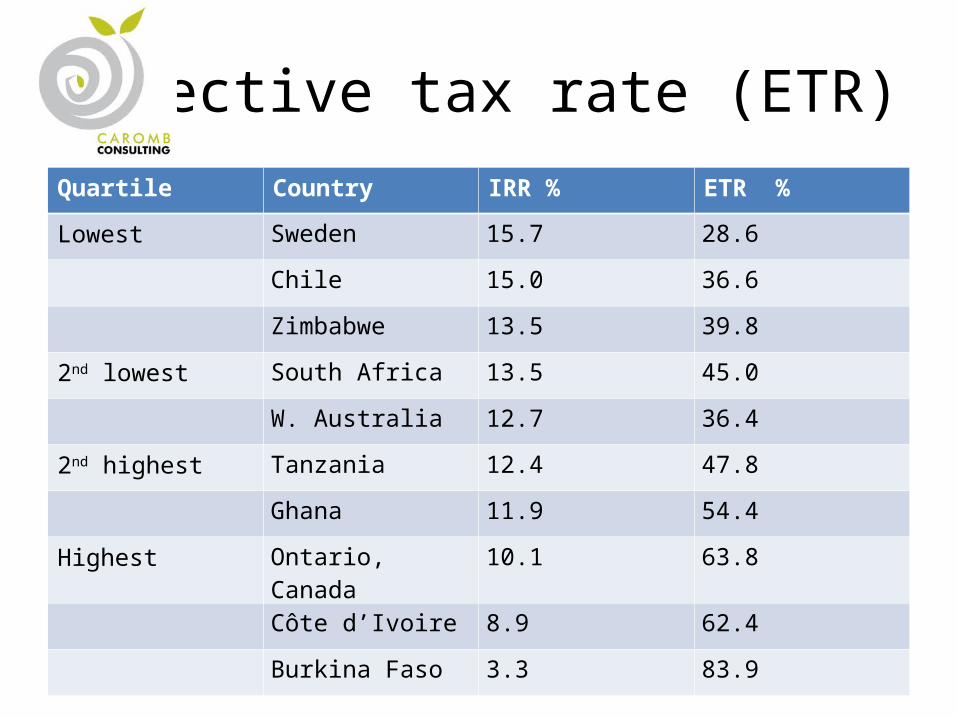

Effective tax rate (ETR)Quartile Country IRR % ETR %

Lowest Sweden 15.7 28.6

Chile 15.0 36.6

Zimbabwe 13.5 39.8

2nd lowest South Africa 13.5 45.0

W. Australia 12.7 36.4

2nd highest Tanzania 12.4 47.8

Ghana 11.9 54.4

Highest Ontario, Canada 10.1 63.8

Côte d’Ivoire 8.9 62.4

Burkina Faso 3.3 83.9

Previous mining tax legislation in many countries built on a

misconception • It was assumed by donors and advisors that governments

had a lower discount rate than investors – maybe zero• Therefore, returns to investors were front loaded through

incentives, the supposed trade-off being progressive taxation

• The changing nature of the social contract was poorly understood – the acquiescence of the population was taken for granted

• The difficulties of explaining how the system was intended to work were underestimated

• The lag in imposition of taxes created an impression of governments being cheated – the pattern of revenues over the life cycle of the mine was not understood

• Tax systems were not progressive

Governments are now reforming mining taxes

• Booming mineral demand has changed the relative bargaining positions

• Populations are demanding accountability from governments and mining companies do not vote

• The failure to integrate mining operations into local/regional economies has undermined the credibility of both government and mining companies

• Local populations have seen little development and blame investors• Because governments’ freedom of action is often constrained by

stability clauses, the solutions tried are often less than ideal– Increased royalties and other regressive taxes that create allocation

inefficiencies – Review of agreements on a shaky legal basis– Political arm twisting of investors– Disturbing the balance between the centre and regions

Security of title

• The one thing investors value above all is security of title; therefore it is a strong point for attracting exploration and investment funds

• Hence, the absence of government discretion is important to investors

• Host governments want to see deposits developed by encouraging competition between investors

• The potential or actual contradiction underlies many disputes• Many governments opt for some form of “use it or lose it”

– Fee structure– Performance obligations– Time limits on permits– Successive relinquishment of exploration areas– Reporting obligations

Foreign exchange regulations• Provide an additional means of control• Floating exchange rates have in principle made regulation less

necessary, but small economies are vulnerable to fluctuations• Most African countries guarantee transferability of foreign

exchange for purchase of inputs, debt service and dividends repatriation

• Regulatory practices for retaining export revenues vary, from obligatory surrender of receipts (Central African Republic) to allowing unlimited offshore accounts (Côte d’Ivoire), most African countries require some receipts to be converted to domestic currency

Environment• Steadily growing importance• At the root of many disputes• Large divide between legislative texts and actual

practices• Capacity for EIAs lacking in many cases• In the context of FDI: provisions for reclamation– Contributions to general government reclamation funds

(Nigeria, Zambia)– Annual provisions for site reclamation (Algeria)– Environmental performance bonds (Uganda)– Bank or other guarantee (Eritrea)

Support to national economic development and diversification

• Detailed regulations by and large abandoned• Experiments with local content legislation

generally disappointing, often results in rent seeking

• The “fiscal link”, from tax revenue to general development programmes is often considered to work better

Local development issues• Difficult to produce detailed regulations• Partnerships hold potential, but sometimes suffer

from a lack of clarity about roles• A middle of the road solution in Peru: Programa

Minero de Solidaridad con el Pueblo (PMSP)– Voluntary support by mining companies to local

development, facilitated by a framework drawn up at the national level

– Most mining companies in Peru, and all foreign investors, have PMSP programmes, which often include capacity building elements

– Lack of clarity about the role of government and investors

Transparency• Extractive Industries Transparency Initiative (EITI)

– UK Government initiative – Imposes obligations on both host country governments and investors

– but relates to countries rather than investors• Publish What you Pay

– NGO initiative– Imposes obligations on investors, aims to make compliance a

condition for stock market listing• Global Reporting Initiative• Disclosure requirements for listing on Toronto exchanges (TSX

and TSX-V)

Human rights• Is mining worse than other industries? 28 per cent of

cases under review by the Human Rights Council• Increasing support for actions by home states,

although legal situation is ambiguous• “Soft law” and voluntary initiatives important– Kimberley Process– IFC Performance Standards– Equator Principles– ICMM Sustainable Development Framework– Initiatives focused on Export Credit Agencies