36

1 Investing in the UK’s heat infrastructure: Heat Networks Investing in the UK’s heat infrastructure: Heat Networks

1 InvestingintheUK’sheatinfrastructure:HeatNetworks

Investing in the UK’s heat infrastructure:

Heat Networks

2 InvestingintheUK’sheatinfrastructure:HeatNetworks

Contents

Heat networks in the UK 3

The opportunity 6

Identifying opportunities – Heat Infrastructure Investment Pipeline 6

Scale of the opportunity 7

Investment timeframes 12

Heat infrastructure investment opportunities 14

Heat infrastructure supply chain opportunities 16

Heat network components 16

Investing in the UK 21

Key features of the UK 21

Common heat network commercial structures and funding sources 23

Characteristics of commercially viable heat networks 25

Improving the climate for investment 28

Impacts of increased heat infrastructure deployment 30

Support for investors and supply chain 32

Further information 33

Frontcoverimagecredit:GatesheadEnergyCentreWSPParsonsBrinckerhoff

Forfurtherinformationpleasecontact:[email protected]

3 InvestingintheUK’sheatinfrastructure:HeatNetworks

Heat networks in the UK

BunhillHeatandPower,courtesyofIslingtonCouncil

Infrastructure is a vital part of many investment portfolios with business seeking new opportunities that deliver the stable, long-term returns characteristic of infrastructure projects. UK heat infrastructure is a significant and growing investment opportunity. Delivering the current pipeline of heat infrastructure projects will require up to £2 billion of capital investment over the next 10 years. This portfolio of heat networks will require investment from a range of funding sources not least heat network operators and third party financers, taking the form of equity, corporate loans or project finance. For the supply chain this pipeline also represents £3.2 to 6.4 billion of operations and maintenance contracts across the 40 year lifetime of these low-carbon energy infrastructure assets.

ThisguideseekstoraiseawarenessofthescaleofheatinfrastructuredevelopmentthatisunderwayintheUKcurrentlyandwillcometomarketinthenext10years.Throughthisdocument,Governmenthopestostartaconversationbetweenkeystakeholders(investors,supplychainandprojectsponsors)abouthowthemarketmightevolvetodeliverthestepchangeindeploymentlevelssuggestedbythepipelineofheatnetworkprojectsacrossEngland,ScotlandandWales.

Thiscombinedpipelineof280projectswillhaveacapitalrequirementof£2billionandwillbecommencingprocurementbetweennowand2025.Thisisonlythestartofthepipeline,however,withadditionalopportunitiesidentifiedbylocalauthorities(municipalities)atenergymasterplanningstage,thatmayproceedasthemarketevolves,andanumberofprojectsbeingdevelopedbywiderpublicsectorbodiesandcommunitygroupsaswellastheprivatesector.

GrantfundingandguidancefromcentralGovernmentanddevolvedadministrationsandsupportfromlocalgovernment,asprojectsponsorsbringingtogetherkeypartnerstoexploretheseopportunities,hasdevelopedasignificantpipelineofhighqualityinvestmentopportunitieswhosetrajectoryislikelytocontinueapace.SupportfromtheDepartmentofEnergy&ClimateChange(DECC)haslaidthegroundworkforinvestmentandsoughttoensurethatasuitablywiderangeofheatsources,commercialstructuresandfundingsourcesareexploredthroughdevelopment,tobringforwardasmanytechnicallyfeasibleandeconomicallyviableprojectsaspossible.Theseprojectsareoptimisedfortheirlocality,exploitingarangeofheatsourcesincludinglocalrecoveredorrenewableheatwheresuitable.Whentheseprojectscometomarketitislikelythattheywillmeetthetechnicalstandardsandcustomerprotectionsrecentlydevelopedbyindustry,furtherimprovingtheirattractivenessasaninvestmentopportunity.

4 InvestingintheUK’sheatinfrastructure:HeatNetworks

ThisguideintroducestheHeatInfrastructureInvestmentPipeline1developedforinvestorsandsupplychaincompanieswithapotentialinterestinthesignificantopportunitiespresentedbythefastdevelopingUKheatnetworkmarket.Keyprojectmetrics,suchascapexandpre-financinginternalratesofreturn(IRR),willberegularlypublishedforprojectopportunitiesinEnglandandWalesalongsidedetailsoftenderwebsites.ThiscomplementstheScottishheatnetworkprojectdirectory2.Thesetoolswillprovideanoverviewofthevolumeandtimingofprojectscomingtomarketandalsoprovideanoutlineofthenatureoftheseprojects,toaidinvestorandsupplychainbusinessdecisions.

AsthisHeatInfrastructureInvestmentPipelinegrowsandheatnetworkdeploymentratesincrease,thereisanopportunityforcurrentmarketparticipantstoexpandoperations,andfornewmarketplayerstoentertheUKheatnetworkmarket;includingthroughpartnershipsorjointventures.ThisgrowthmaybringaboutanevolutionoftheUK’sheatnetworkmarketoverthenext10years:–witheconomiesofscalerealised,cost-reducinginnovationdeployedandnewcommercialstructures,possiblycentredaroundaggregationorunbundlingofgenerationanddistribution,emerging.

This investment guide seeks to stimulate a conversation about how to create the heat networks market of the future.

1HeatInfrastructureInvestmentPipelinehttps://www.gov.uk/government/publications/energy-networks-in-the-uk-investment-opportunities

2Scottishheatnetworkopportunitieshttp://www.districtheatingscotland.com/hnp-projects-mapandhttp://www.districtheatingscotland.com/content/investment-heat-networks-scotland

5 InvestingintheUK’sheatinfrastructure:HeatNetworks

Customer supplyHeat Sources/Energy Centre Distribution

HeatStore

TOWN HALL

HeatStore

Energyfrom Waste

Water source

DataCentre

DeepGeothermal

Industry

Energy Centre

CHP Boiler

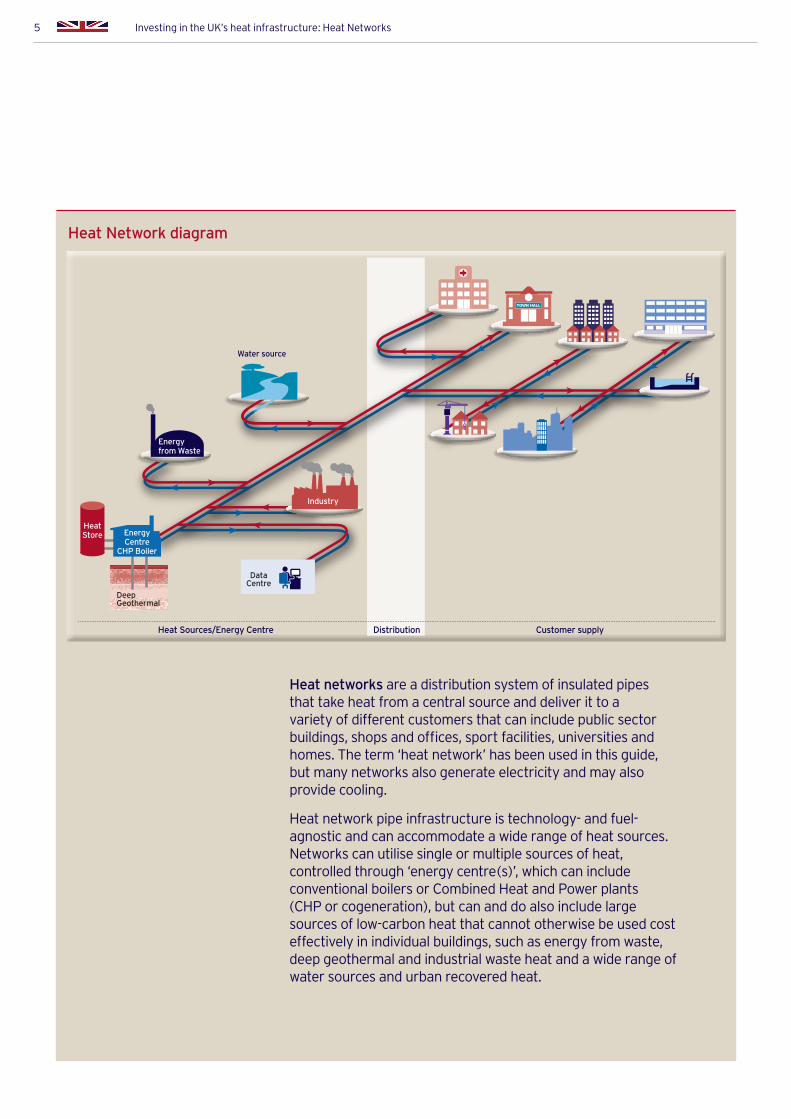

Heat Network diagram

Heat networksareadistributionsystemofinsulatedpipesthattakeheatfromacentralsourceanddeliverittoavarietyofdifferentcustomersthatcanincludepublicsectorbuildings,shopsandoffices,sportfacilities,universitiesandhomes.Theterm‘heatnetwork’hasbeenusedinthisguide,butmanynetworksalsogenerateelectricityandmayalsoprovidecooling.

Heatnetworkpipeinfrastructureistechnology-andfuel-agnosticandcanaccommodateawiderangeofheatsources.Networkscanutilisesingleormultiplesourcesofheat,controlledthrough‘energycentre(s)’,whichcanincludeconventionalboilersorCombinedHeatandPowerplants(CHPorcogeneration),butcananddoalsoincludelargesourcesoflow-carbonheatthatcannototherwisebeusedcosteffectivelyinindividualbuildings,suchasenergyfromwaste,deepgeothermalandindustrialwasteheatandawiderangeofwatersourcesandurbanrecoveredheat.

6 InvestingintheUK’sheatinfrastructure:HeatNetworks

The Opportunity

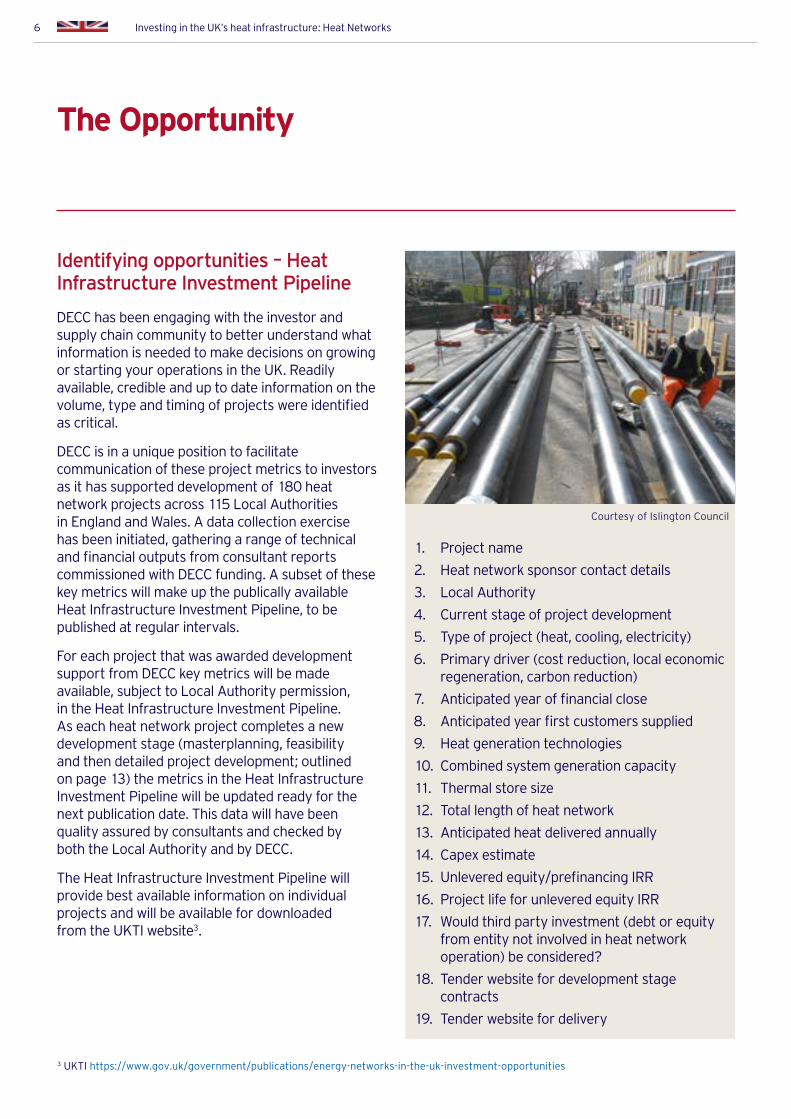

Identifying opportunities – Heat Infrastructure Investment Pipeline

DECChasbeenengagingwiththeinvestorandsupplychaincommunitytobetterunderstandwhatinformationisneededtomakedecisionsongrowingorstartingyouroperationsintheUK.Readilyavailable,credibleanduptodateinformationonthevolume,typeandtimingofprojectswereidentifiedascritical.

DECCisinauniquepositiontofacilitatecommunicationoftheseprojectmetricstoinvestorsasithassupporteddevelopmentof180heatnetworkprojectsacross115LocalAuthoritiesinEnglandandWales.Adatacollectionexercisehasbeeninitiated,gatheringarangeoftechnicalandfinancialoutputsfromconsultantreportscommissionedwithDECCfunding.AsubsetofthesekeymetricswillmakeupthepublicallyavailableHeatInfrastructureInvestmentPipeline,tobepublishedatregularintervals.

ForeachprojectthatwasawardeddevelopmentsupportfromDECCkeymetricswillbemadeavailable,subjecttoLocalAuthoritypermission,intheHeatInfrastructureInvestmentPipeline.Aseachheatnetworkprojectcompletesanewdevelopmentstage(masterplanning,feasibilityandthendetailedprojectdevelopment;outlinedonpage13)themetricsintheHeatInfrastructureInvestmentPipelinewillbeupdatedreadyforthenextpublicationdate.ThisdatawillhavebeenqualityassuredbyconsultantsandcheckedbyboththeLocalAuthorityandbyDECC.

TheHeatInfrastructureInvestmentPipelinewillprovidebestavailableinformationonindividualprojectsandwillbeavailablefordownloadedfromtheUKTIwebsite3.

3UKTIhttps://www.gov.uk/government/publications/energy-networks-in-the-uk-investment-opportunities

1. Projectname

2. Heatnetworksponsorcontactdetails

3. LocalAuthority

4. Currentstageofprojectdevelopment

5. Typeofproject(heat,cooling,electricity)

6. Primarydriver(costreduction,localeconomicregeneration,carbonreduction)

7. Anticipatedyearoffinancialclose

8. Anticipatedyearfirstcustomerssupplied

9. Heatgenerationtechnologies

10. Combinedsystemgenerationcapacity

11. Thermalstoresize

12. Totallengthofheatnetwork

13. Anticipatedheatdeliveredannually

14. Capexestimate

15. Unleveredequity/prefinancingIRR

16. ProjectlifeforunleveredequityIRR

17. Wouldthirdpartyinvestment(debtorequityfromentitynotinvolvedinheatnetworkoperation)beconsidered?

18. Tenderwebsitefordevelopmentstagecontracts

19. Tenderwebsitefordelivery

CourtesyofIslingtonCouncil

7 InvestingintheUK’sheatinfrastructure:HeatNetworks

Scale of the opportunity

With over 280 heat network projects at varying stages of development across the UK, there are significant investment and supply chain opportunities anticipated over the next 10 years; up to £2 billion of capital investment and lifetime operation and maintenance contracts of £3.2 to 6.4 billion.

ThepotentialcapitalinvestmentfiguressetoutbelowaremodelledonearlystagedescriptionsofheatnetworkambitionsprovidedbyLocalAuthoritieswhenapplyingforsupportfromDECC’sHeatNetworksDeliveryUnit.GenericassumptionsonnetworksizeandheatsourcewereusedwhereinformationwasnotyetavailableandinvestmentfiguresestimatedusingcostdatapublishedbyDECC4.ThemethodologyusedtomodeltheScottishheatnetworkopportunityissetoutinthe‘InvestmentinHeatNetworksinScotland’report5.

Whilstisitunlikelythattheexactsetofprojectscurrentlylistedinthecombinedpipelinewillachievetechnicallyfeasibleandeconomicallyviablesolutions

andnotstallduetoexternalobstacles,thereareotherprojectsthatcouldtaketheirplaceorexpandthepipeline.Masterplanningstudiescommonlyidentifyaminimumofthreepossibleheatnetworks,butsometimesthiscanbeasmanyasten.Inaddition,thereareotherpublicsectorbodiessuchashospitalsanduniversitiesdevelopingheatnetworksandnewbuildprojectsbeingdevelopedintheprivatesector.

Annualoperationandmaintenancecosts(opex)varyasapercentageofinitialcapitalinvestment(capex)dependingontheheatsourceandheatnetworksize.The‘AssessmentoftheCosts,Performance,andCharacteristicsofUKHeatNetworks’6whichgathereddatafromsevenexistingheatnetworksindicatedthatannualopex(excludingfuel)was8-10%ofcapex.AnecdotaltestingofthisproportionbyDECCsuggeststhat4-8%capexmaybeamoreaccuraterepresentationofawidervarietyofheatnetworks.Basedon£2billioncapexinvestment,thisrangecouldrepresent£80-160millionofoperationandmaintenancecontractsannually.Acrossa40-yearheatnetworklifetime,thissupplychainopportunitycouldbevaluedat£3.2to6.4billion.

Count of projects in

development

Potential capital investment

25% deployment rate

50% deployment rate

100% deployment rate

England and Wales projects supported by Heat Networks Delivery Unit1 180 £400 million £800 million £1.6 billion

Projects supported by Heat Network Partnership for Scotland2 103 £50 to £120 million £100 to £240 million £200 to £440 million

Total 283 £0.5 billion £2 billion

1Source:CalculationsunderpinningtheDeliveringUKEnergyInvestment:Networks2014report2Source:InvestmentinHeatNetworksinScotland

4Assessmentofthecosts,performanceandcharacteristicsofUKheatnetworkshttps://www.gov.uk/government/publications/assessment-of-the-costs-performance-and-characteristics-of-uk-heat-networks

5InvestmentinheatnetworksinScotlandhttp://www.districtheatingscotland.com/content/investment-heat-networks-scotland6Assessmentofthecosts,performanceandcharacteristicsofUKheatnetworkshttps://www.gov.uk/government/publications/assessment-

of-the-costs-performance-and-characteristics-of-uk-heat-networks

8 InvestingintheUK’sheatinfrastructure:HeatNetworks

EnglandandWales

TheworkofDECCoverthelasttwoyearshasestablishedbeyonddoubtthemassiveappetiteforLocalAuthorityinvolvementinheatnetworkprojects;£14.5millionoffundingintotheconsultancymarketforprojectdevelopment,115LocalAuthoritystakeholders(outofatotalof381authoritiesinEnglandandWales)supportingapipelineofnationallysignificantinfrastructure,and180projectsreceivingsupporttomakesuretheyaretechnicallyandeconomicallyoptimisedinadvanceofaninvestmentdecision.DECChasworkedwitheightofthenineCoreCities7,severalLocalEnterprisePartnerships8,dozensofthelargetownsandcitiesaswellassmallerruralandcommunity-sizedprojectsacrossEnglandandWales.

ThesuccessofDECCsofarhasbeentounlockthelatentambitionsofLocalAuthoritiesacrossEnglandandWales.LocalAuthoritiesarekeentobetterunderstandandquantifytheroleofheatnetworks,inthelocalareaandmanyoftheseLocalAuthoritieshaveambitionstotakearoleinthedeliveryofthesenetworksinordertorealisethefullrangeofbenefitstheycandeliver.

Thisportfoliohasadiverserangeofpotentialschemesrangingfrom£3to£4millionuptoprojectsinexcessof£40million.TheIRRfortheseprojectsvarybetween0and15%,butwiththemajoritysittingbetween5and9%.

Theseprojectsareworkingtosecureinitialphaseone‘anchor-load’customers(i.e.large,longterm,securecustomers,oftenpublicsector)attheearliestopportunity.Insomeprojects,theLocalAuthoritybringsheatdemandfromoffices,leisurecentres,schoolsorsocialhousing,butinotherprojectskey

heatnetworkcustomers,suchasotherpublicsectorbodies,areengagedinearlystagestofacilitateagreementofheadsoftermsforinvestmentcertainty.Whilstmanyoftheseschemesmaybebasedonpublicsectorclustersinitially,manyplantotakeadvantageofanypotentialprivatesectordemandopportunities,asthenetworkmatures.

Thetechnologyandfuelagnosticnatureofheatnetworkpipeinfrastructurehasresultedinanumber

LocalAuthoritiesawardedDECCdevelopmentsupportinHeatNetworksDeliveryUnitfundingrounds1-4.9

7TheCoreCitiesare:Birmingham,Bristol,Cardiff,Glasgow,Leeds,Liverpool,Manchester,Newcastle,Nottingham,Sheffield.Theiraimistopromotetheroleofthesecitiesindrivingeconomicgrowthandthecaseforcitydevolution.http://corecities.com/

8The39LocalEnterprisePartnershipsinEnglandbringtheprivateandpublicsectorstogethertodrivelocaleconomicgrowth.http://www.lepnetwork.net/

9DECCHeatNetworksDeliveryUnitfundingawardshttps://www.gov.uk/government/publications/heat-networks-funding-stream-application-and-guidance-pack

9 InvestingintheUK’sheatinfrastructure:HeatNetworks

ofinterestingheatsourcesbeingexploredacrosstheDECCportfolio;fromgas-CombinedHeatandPower(cogeneration),biomassincludingenergy-from-wasteandheatpumpsutilisingdeepgeothermal,minewater,industrialwasteheatandurbansourcesofrecoveredheat.Anticipatedgenerationcapacityvariesbetweenprojectswithmostsupplysolutionsrangingbetween1-5MWth(excludingenergy-from-waste~10MWth)withmanyprojectslookingatoptionsformultiplesupplysources.

Aswellasexploringasmanypotentialheatsourcesaspossibleandengaginganchorcustomersearly,LocalAuthoritiesarealsoexploringavarietyofcommercialstructuresandfundingsources.CentraltoLocalAuthoritydecisionsaroundthebalanceofpublicandprivatesectorinvolvementaretheLocalAuthoritystrategicaimsforthescheme,itsriskappetite,desiredlevelofcontroloverthescheme,theavailabilityofinternalfinanceandattractivenessofexternalfinance.

Infrastructure is a vital part of many investment portfolios.

CourtesyofVeolia

10 InvestingintheUK’sheatinfrastructure:HeatNetworks

Case study: Gateshead Town Centre District Energy Scheme

GatesheadTownCentreDistrictEnergySchemeisthefirstofitskindandscaleintheNorthEast.Havingbrokengroundinsummer2015,thenewDistrictEnergyCentreintheBalticBusinessQuarterwillhousetwo2MWgascombinedheatandpowerenginesandwillbeoperationalbyApril2016,withpublicandprivatesectorcustomersbeingfullyconnectedbyJune2016through3kmofheatandprivatewirenetwork.

The£18.5millionschemehasbeendesignedtoserve17buildings,includingGatesheadCivicCentre,severalpublicsectorpartnersandanumberoflargecommercialbuildings,hotelsandoffices.Theschemeisexpectedtohelpattractnewbusinessestothearea,thankstolowerenergypricesanditsgreencredentials.Localhomes,businessesandpublicorganisationswillalsobenefitfromlowerenergybillsandemissions.

TheprojecthasbeenfullyfinancedbyGatesheadCouncilwiththedesign,build,operationandmaintenancecontractsawardedtotheprivatesector.Theprojectwilldeliveran8%pre-financingIRRovera40-yearterm(thelifetimeofthepipeinfrastructure)withapositivecashflowfromyearone.Theschemeincomeisderivedfrombothpublicandprivatecontracts,with70%oftherevenuescomingfrompublicsectorconnections.Incomefromelectricitysaleshasalsobeenmaximisedandwillprovide75%oftheschemerevenue.

TheCouncilhasaspirationstoseemanyotherareasoftheboroughconnectedtosimilarschemesinthefuture.TheDistrictEnergyCentreandnetworkwillbeabletosupplytheenergyneedsofallthefuturedevelopmentplannedforthetowncentreandfeasibilityforfutureexpansionisunderway.

11 InvestingintheUK’sheatinfrastructure:HeatNetworks

Scotland

TheHeatNetworkPartnershipforScotland’sreportonheatnetworkinvestment10identifies103heatnetworkprojectscurrentlyindevelopment.Thisportfolioincludesarangeofprojectsincludinglarge-scaleintegratedheatnetworksinurbanareas,retrofittingsocialhousingdevelopments,particularlymulti-storeybuildings,publicbuildings,businessandindustry.Anumberofheatnetworkshavebeenbuiltorexpandedinrecentyears,forexampleinAberdeenandWick,withnewprojectsbasedaroundmajorurbanregeneration,oneofthelargestbeingtheCommonwealthGamesAthletes’VillageinGlasgow,whichbuiltincapacitytoallowittoexpandtonearbyhousingandcommercialdevelopments.Since2011theScottishDistrictHeatingLoanFund11hasprovidedover£8millionincapitaltoarangeofprojects,thelargestloantodatebeing£1milliontoAberdeenHeat&Power.TheFund’sportfolioincludesalargenumberofsmallscalerenewableheatnetworks,withloanstotalling£5millionacrossover30projects,demonstratingapotentiallysignificantinvestmentopportunityforawidelyreplicableheatnetworkmodel.

HeatNetworkPartnershipforScotlandProjectsmap.12

Masterplanning studies commonly identify a minimum of three possible heat networks, but sometimes this can be as many as ten.

10InvestmentinheatnetworksinScotlandhttp://www.districtheatingscotland.com/content/investment-heat-networks-scotland11ScottishGovernment’sdistrictheatingloanfundhttp://www.energysavingtrust.org.uk/district-heating-loan12HeatNetworkPartnershipforScotlandProjectsmaphttp://www.districtheatingscotland.com/hnp-projects-map

12 InvestingintheUK’sheatinfrastructure:HeatNetworks

BunhillHeatandPower,courtesyofIslingtonCouncil

Investment timeframes

Anassessmentofthedevelopmentstageaheatnetworkhasreachedanditslikelycomplexitycanbeusedtoprovideanestimateofwhentheprojectwillreachcommercialisationandwillthereforebeseekingfinanceandprocuringdelivery.

Whereastrategicarea-wideapproachistaken,thefirsttwodevelopmentstagesareundertakenbytheLocalAuthorityheatnetworksponsor.Heat mappingandenergy masterplanninglookarea-wideatcurrentandfutureheatdemandandheatsources,identifyarangeofheatnetworkopportunitiesandprioritisethesethroughatechno-economicanalysisthatcapturestheLocalAuthority’skeydrivers(predominantlyenergybillreductionand/orlocaleconomicregeneration).

Thenexttwostagesarefeasibilityanddetailed project development.Thesestagestakethemostpromisingsingleheatnetworkopportunityand,throughaseriesofiterations,examinethetechnical,financialandcontractualissuesinincreasinggranularity;asthesethreeaspectsareinter-dependant.

Shouldthelocalauthoritywishtobethemajorityshareholderintheheatnetworkabusinesscasewillbesubmittedforinternalapprovalrecommendingthecommercialstructure,fundingsourcesandprocurementstrategy.Shouldthelocalauthoritydecidethattheoptimalwaytodelivertheheatnetworkisthroughprivatesectorownershipandfunding,developmentstagesmaystopatfeasibilityandaCabinetorCommitteepaperorbusinesscasewillseekapprovalforthisrouteandtheinternalresourcesrequiredtoensuredelivery.

13 InvestingintheUK’sheatinfrastructure:HeatNetworks

Thecommercialisationphaseofprojectswillinvolvesecuringfinance,procuringdeliveryandnegotiatingfinalcontractswithanchor-loadcustomersandsuppliers.

Basedonthetimingsabove,itisexpectedthatasignificantnumberofthe280projectsinthecombinedpipelinewillreachcommercialisationinthenext10years.Aftertheinitialprospectidentifiedinmasterplanninghasbeenpursued,otheropportunitiescanoftenbedeveloped.Thishastwoimplicationsforinvestment.Inreality,thepipelineislargerthan280projectsandopportunitiescontainedwithinitmaybecomingtomarketoverthenext10yearsandbeyond.

ThefollowingdatawhichwillbeprovidedintheHeatInfrastructureInvestmentPipelinecanbeutilisedbyinvestorsandsupplychainwhenconsideringthetimingsofthepipelineofheatnetworkprojects:Currentstageofprojectdevelopment,(Anticipated)Yearoffinancialcloseand(Anticipated)Yearfirstcustomerssupplied.

Commercialisation Delivery

Single projectMultiple options

Heat Networks Delivery Unit support

Development

Detailed Project Development

Finance ProcureNegotiate contracts

Build, operate, maintain

Bus

ines

s ca

se

Fina

ncia

l clo

se

Dec

isio

n to

pro

ceed

Bre

ak g

roun

d

Sup

ply

firs

t cu

stom

er

“hea

t o

n”

2 months 2 months 6 months 6 months

1 m

onth

gap

Desig

n6

mon

ths

Build

14 m

onth

s

Com

mis

sion

3 m

onth

s

Exa

mpl

e

12 months

MasterplanningMapping Feasibility

Possible refinancing, acquisitions aggregation, unbundling

Exp

ansi

on, i

nter

conn

ecti

ng

seco

ndar

y m

arke

t

Operation+ 40 years

Heat Networks: Development to Delivery

14 InvestingintheUK’sheatinfrastructure:HeatNetworks

Heat infrastructure investment opportunities

Should an equivalent of the complete heat network project pipeline reach commercialisation, up to £2 billion of capital investment will be required. This presents opportunities for heat network operators, third party providers of corporate debt, project finance or equity, as illustrated below.

LocalAuthoritysponsoredheatnetworksfinancedontheLocalAuthority’sbalancesheetmayuseexistingbudgetcapacity,acorporateloanmaybetakenfromthePublicWorksLoanBoardorfromaprivatesectorinvestororaparticularcharacteristicoftheprojectmaybeeligibleforagrant,suchasfromtheEuropeanUnion.WhilstsomeLocalAuthoritiesdohaveavailablefinance,thereis,

however,increasingcompetitionforconstrainedpublicsectorbudgetswithotherspendingprioritiestakingprecedentoverheatnetworks.ForthoseLocalAuthoritiesthatdohaveanappetitetoinvestbutlacksufficientfunds,thereisanopportunityfortheprivatethirdpartyinvestorstoofferloanfundingagainstthecredentialsoftheLocalAuthority.

ForLocalAuthoritieswithnoappetitetoinvest,thereareopportunitiesfortheprivatesectorheatnetworkoperators.Inthesecircumstancestheheatnetworkmustalignwiththeprivatesector’sinvestmentstrategy,mustrepresentabetteropportunitythanotherpotentialinvestmentsandmeettheinvestmenthurdleratesandriskstrategyoftheheatnetworkoperator.Aswellasutilisingexistingbalancesheet,privatesectorheatnetworkoperatorsmayseekcorporateloanstofinancenetworkinvestment.

Investment opportunities

Finance sources

Local Authority (LA) existing budgetGrantsPrudential borrowing:- Public sector loan (PWLB)- Private loan

Corporate budgetCorporate loan

Third party investment options:Equity stakeProject finance (loan debt)

Own

LA LAOn balance sheet

Design / build /operate contract

LA & private

Heat network operator or third partyJoint venture

Special Purpose vehicle

privateOn balance sheet

of property developer or heat network

operator

Operate

LA

(Unusual)

private private private

(Often new build)

15 InvestingintheUK’sheatinfrastructure:HeatNetworks

Todate,thereislittleevidencethatprojectfinance,securingdebtbasedontheassetsandprojectedcashflowsoftheheatnetwork,hasbeenutilisedintheUK.Shouldappropriatelypricedoffersbecomeavailable,projectfinancemayinfuturebeutilisedbyheatnetworks.

Currently,equityinvestmentsaremadebytheheatnetworkowneroperator(i.e.theLocalAuthorityorprivatesectorheatnetworkoperator).Infuture,thirdpartyorganisationsnotinvolvedintheoperationoftheheatnetworkmaybeinterestedintakinganequitystake.

Oncetheheatnetworkhasbeenconstructedandhasoperatedforaninitialperiodoftime,theriskprofilewillreduceandcheaperfinancemaybeaccessedthroughrefinancing,orheatnetworksmaybeacquiredbyanotheroperatororinvestor.Asmallnumberofacquisitionshaveoccurredinrecentyears,butthissecondarymarketmaybecomemoreestablished.Considerationmaybegiventoheatnetworkaggregationortheunbundlingofheatsources(generation)anddistributionacknowledgingtheirdifferinglifetimesandrisk/returnprofiles.

Criticaltoanyinvestmentoffersforheatnetworksisrecognitionoftherevenueprofile.Heatnetworkscantakeuptofiveyearstobuild,dependingonlocation,scaleandcomplexity,andmayhavefurtherphasedbuildoutbeforefullcapacity,andthereforefull/incomepotential,isreached.Financethatalignsrepaymentswithprojectedincomeintheinitialyearscouldmakeasignificantdifferencetothesector.

ThefollowingdatathatwillbesetoutintheHeatInfrastructureInvestmentPipelinewillprovideinvestorswithanideaofthevolumeandtypesofprojectcomingforwards:Capexestimate,Unleveredequity/pre-financingIRR,ProjectlifeforunleveredequityIRRand‘Wouldthirdpartyinvestment(debtorequityfromentitynotinvolvedinheatnetworkoperation)beconsidered?’.

Delivering pipeline of 280 heat infrastructure projects currently in development will require £2 billion capital investment over next 10 yrs.

CourtesyofIslingtonCouncil

CourtesyofVeolia

16 InvestingintheUK’sheatinfrastructure:HeatNetworks

Heat infrastructure supply chain opportunities

The projects in development in England, Wales and Scotland have a combined capex of £2 billion which will be let as build contracts to the private sector supply chain alongside lifetime operation and maintenance contracts of £3.2 to 6.4 billion. This covers a wide variety of products and services.

Heat network components

Likeallenergysystems,heatnetworksarecomprisedofgeneration,distributionandcustomersupply.Thegenerationassetitselfmaybeunderthesameownershipasthedistributioninfrastructureandcustomerconnectionsormaybeownedbyathirdpartywithacontracttosupplyheat,suchasanenergy-from-wasteplant.

Heatsourcescanbesingleormultiple,withthesystemtakingamodularapproachutilisingpeakingplantfortimesofhighdemandandbackupplantformaintenance.Mostheatsourcelifetimesaresignificantlyshorterthanthepipeinfrastructure,allowingtheheatnetworktofurtherdecarboniseovertimethroughtheplannedassetreplacementprogram.

Buildings-sideheatingandhotwatersystemscanbepartoftheheatnetworkassets,ormayfallunderdifferentownershipandmanagement,butinmostcasesheatnetworkshaveheatinterfaceunitsatthebuildingconnectionand/orcustomerconnections.InlinewithEuropeanlegislation,allnewheatnetworksmustinstallheatmetersfornewbuildpropertiesandforexistingpropertiesundergoingmajorrenovations,butsubjecttoacostbenefitanalysisforexistingpropertiesnotundergoingamajorrenovation,sothatcustomerscanbechargedforconsumption(asopposedtoflatrateallocations)13.

Heatnetworksvaryincommercialcomplexitywiththesimplestschemes‘campusnetworks’withasingleentityascustomer,supplierandlandowner,thesenetworksaretypifiedbyhospitalsanduniversityheatnetworks.Morecomplexnetworks,typifiedby‘city-wideschemes’,mayincludeheatsourcesownedbyathirdparty,‘prosumers’(customersthatalsosupplyheattothenetwork)andavarietyofpublicandprivatesectorcustomers.Districtenergyschemesmaysupplyheatonlyormayalsoprovidecoolingand/orelectricity.

13Heatnetworkslegislationformeteringandbilling:complianceandguidancehttps://www.gov.uk/guidance/heat-networks

Current £3-6 billion heat network supply chain opportunities – operations and maintenance contracts over next 40 years.

17 InvestingintheUK’sheatinfrastructure:HeatNetworks

Engineering design consultants

Engineeringdesignconsultantsundertakeheatmapping,networkdesignandaresometimesretainedtosupervisetheinstallation,commissioningandoperationofheatnetworks.DECCandtheHeatNetworkPartnershipforScotlanddevelopmentfundinghasputasignificantamountofmoneyintothismarket.Asaresult,thesupplierbasehasexpandedandanumberofnewmarketentrantshavewoncontracts;eitherUKcompanieswithrelatedengineeringexperienceorheatnetworkspecialistsfromabroad.Inrecognitionofthegrowthinthismarketandthespecialistskillsrequiredtooptimisethewiderangeofheatnetworks,CIBSEandADEhaveestablishedaCodeofPractice14totrytobringaboutaconsistentqualityinthedesign,build,commissioningandoperationofheatnetworks.Thesestandardsarebeingreferencedintenderspecificationsandadoptedbyengineers.

Legal and financial consultants

ThereareanumberoflegalandfinancialconsultantswithexpertiseinheatnetworksintheUK.Thispoolofconsultantsisgrowing,withsomecompaniesoperatingnationallyandsomefocussingonspecificregionsoftheUK.ThispoolofconsultantsisamixofUKandinternationalorganisations.Itislikelythatthismarketwillmatureandsomestandardisationoccurwherecurrently,largelyduetothebespokenatureofheatnetworksandthelowdeploymentrates,learningsarenotbeingreadilytransferredacrossprojects.Strategicapproachestoheatnetworksacrossspecificgeographicareas,suchasinGreaterManchesterandGlasgow,shouldbringsynergiesacrossanumberofprojects,therebyreducingconsultantfees.

Heat network developers and operators

AsmallbutgrowingnumberofheatnetworkdevelopersandoperatorsareactiveintheUK.Thesecompaniesincludelargeutilitiesandsmallerheatnetworkspecialists.Thesecompaniesprovidearangeofdifferentrolesaloneandinpartnershipwitheachotherdependingonthecontractsoffered.Contractscanincludeanycombinationoffinance,design,build,operation,maintenance,metering,billingandcustomerservice.Theleadheatnetworkdeveloperoroperatorislikelytotakeonacoordinationroleandwillsubcontractcertainaspectstosomeofthespecialistorganisationsmentionedabove.

Energy centre building construction and pipework civil engineering

Heatnetworksconstructionandinstallationworksneedtobedeliveredbyspecialistcompanies.Amajorpartoftheinstallationofpipesistheexcavationoftrenches,backfillingandsurfacerestitution.Thisisastandardcivilengineeringactivityandthereisawell-establishedUKsupplier-base.Thecurrenttypicalapproachesare:constructionanddeliverybyaspecialistturnkeyorganisationorthroughaconstructioncompanymanagingandsubcontractingspecialistactivitiesoutsideofthestandardbuildingconstruction.LocalAuthoritiestypicallyusedesignandbuildcontractsandareusingincreasinglydetailedspecificationsandretainingclientengineersthroughoutthedesignandbuildprocess.Thereisincreasedinterestinmoretraditionalformsofprocurementwheredesignandbuildelementsareprocuredseparately.

14CharteredInstitutionofBuildingServicesEngineers(CIBSE)andAssociationforDecentralisedEnergy(ADE)HeatNetworks:CodeofPracticefortheUKhttp://www.cibse.org/knowledge/cibse-other-publications/cp1-heat-networks-code-of-practice-for-the-uk-new

18 InvestingintheUK’sheatinfrastructure:HeatNetworks

Distribution infrastructure – pipe manufacturing and installation

Networkedheatisdistributedprimarilyviahotwater,orsteam,throughpre-insulatedpolymerorsteelpipes.AlimitednumberofbrandssupplytheUKcurrently.

Steelpipes,whichhavealongerlifetimethanpolymer,commonlyhaveintegratedleakdetectionsystems.SteelpipesarenotyetmanufacturedintheUK,andtransportationfromabroadincreasesthepriceandleadtimes.Criticaltotheintegrityofsteelpipeinstallationisjointing.Thisisahighlyskilledactivitywhichisunder-developedintheUKandismuchindemand.Steelpipesarecommonlyusedfor

district-levelheatnetworkandpipeworkrunsinroadsandhighways.Plasticpolymerpipescanbeusedforshorterdistancesandcanoperateatavarietyoftemperaturesandpressures.Thesearelowercost,areflexibleandaresuppliedinlargerollsandinstallationissimplerthanforsteelpipes.

ThePotential&CostsofDistrictHeatingNetworks15reportidentifiedthatthecapitalcostsofheatnetworksintheUKare20%higherthaninmainlandEurope,asignificantproportionofwhichisthedistributioninfrastructure.Asdeploymentratesincrease,theUKshouldbenefitfromtheeconomiesofscalethathaveseenpricesfalloncontinentalEurope.

15ThepotentialandcostsofdistrictheatingnetworksPoyry/FaberMaunsellreport(2009)http://www.poyry.co.uk/news/potential-and-costs-district-heating-networks-report-decc-poyry-energy-consulting-and-faber-maunsell-aecom

QueenElizabethOlympicPark,courtesyofCofelyGDFSUEZ

19 InvestingintheUK’sheatinfrastructure:HeatNetworks

Generation (heating, cooling and electricity) plant

Heatgenerationplantandancillaryequipment,suchasboilersandCHP,arealsousedinbuildinglevelapplicationsaswellasheatnetworks,and,asaconsequence,isarelativelymaturemarket.However,newsourcesofheatarebecomingmoreprevalentandthemainstreamingofkittorecoverandupgradesourcesofindustrialandurbanheatcosteffectivelywillberequired.Thisbroadeningofheatsourceswillsupportthegrowingpipelineofheatnetworkprojectsandanincreaseinthenumberofmanufacturersandsuppliersofsuchhardwarewillexertadownwardpressureoncoststhroughacompetitivemarket.

Control systems

ControlsystemsforheatnetworksrangefrombuildingmanagementsystemstomorecomplexSCADAsystems,dependingonthescaleandthecomplexityofthesystem.Thereisscopetodevelopsmartersystemcontrolsandmetering,enhancingtheinterfacewiththecustomerandtheheatnetwork,andmaximisingopportunitiesforsmartsystemoptimisation.Theuseofsmartmeters,systemmonitoringandcontrolscouldalsobedevelopedtoimprovetheperformanceofnetworksthroughenablinglocaldiagnostics,andmaximisingthebenefitofheatnetworksthroughcontrolledandmanagedinterfaceofthegenerationequipment,thermalstorageanddemandswithotherenergynetworks,suchasthenationalgridandlocalelectricaldistributionnetworks.

Thermal storage

Efficientheat(andcooling)networkswillincorporateathermalstoretoflattentheheatdemandprofileandincreasegenerationutilisationrates.Thermalstoragecanalsofacilitatecontrolledoperationofheatgenerationassetstoreflectelectricitymarketpricesandcouldplayaroleinelectricitysystembalancing.Storagehashistoricallyutilisedhotwater,butinnovationexploringphasechangematerials,forexample,mayincreasetheimpactofthermalstorageinfuture.

Retail or customer interface

Theinterfacewiththecustomercommonlytakesplacethroughtheheatorhydraulicinterfaceunit(HIU).WhilstsomeHIU’saremanufacturedintheUK,mostareimportedandthereisanopportunityformoreUKmarketparticipants.

Variouscontrolssuchastimers,thermostatsandthermostaticradiatorvalves(TRV’s)arethesameasforstandardcentralheatingsystemsandthereisawell-developedsupplychain.

HeatmeteringandbillingregulationshavebeenintroducedtoimplementtherequirementsoftheEuropeanEnergyEfficiencyDirectiveintheUK.Allnewheatnetworksarerequiredtoinstallmetersandcontrolssothatcustomerscanmanagetheirheating.Therearealsorequirementstoprovidecustomerswithtransparentbillinginformation.Existingnetworkswithoutmetersmustundertakeacost-benefitanalysistodeterminewhetherheatmetersshouldbeinstalled.Insomeinstances,heatnetworkswithoutheatmetersmayuseheatcostallocatorsoraformulautilisingametric,suchasfloorspace,asawaytoassignvariableheatcharges.Heatmetersarespecifictoheatnetworksandthereareavarietyoftypesincludingprepayment,remoteandsmartheatmeters,butmostareimportedfromEurope.StandardsformeteringaccuracyaresetthroughtheMeasuringInstrumentsDirective.SomemetersareofferedaspartofaservicepackageofmeteringandrevenuecollectionbyUKoperators.

AsmallnumberofcompaniesintheUKareprovidingspecialistheatcustomerservice.Thiscanincludecontractmanagement,customerservices,meteringandbilling.

20 InvestingintheUK’sheatinfrastructure:HeatNetworks

HeatStore

TOWN HALL

HeatStore

Energyfrom Waste

Water source

DataCentre

DeepGeothermal

Industry

Energy Centre

CHP Boiler

Aswellasthemetricsthatindicateprojecttimings,thefollowingHeatInfrastructureInvestmentPipelinemetricswillbepublishedtoprovideahighlevelindicationoftheupcomingsupplychainopportunities:Heatgenerationtechnologies,Combinedsystemgenerationcapacity,Thermalstoresize,TotallengthofheatnetworkandAnticipatedheatdeliveredannually.

Investment opportunity

Capital investment

Heat Sources/Energy Centre

£1 billion

Distribution

£1 billion

Customer supply

£3.2 to 6.4 billion of operations and maintenance contracts across the 40 year lifetime of these low-carbon energy infrastructure assets

21 InvestingintheUK’sheatinfrastructure:HeatNetworks

Investing in the UK

Key features of the UK

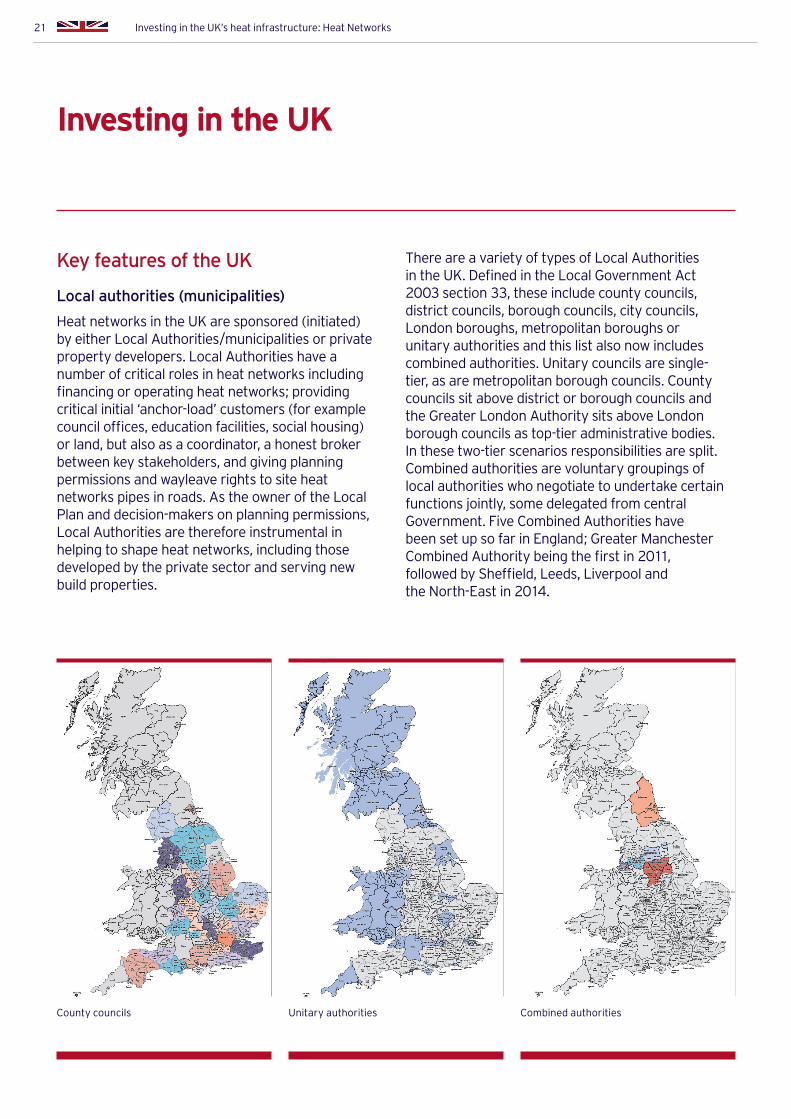

Local authorities (municipalities)

HeatnetworksintheUKaresponsored(initiated)byeitherLocalAuthorities/municipalitiesorprivatepropertydevelopers.LocalAuthoritieshaveanumberofcriticalrolesinheatnetworksincludingfinancingoroperatingheatnetworks;providingcriticalinitial‘anchor-load’customers(forexamplecounciloffices,educationfacilities,socialhousing)orland,butalsoasacoordinator,ahonestbrokerbetweenkeystakeholders,andgivingplanningpermissionsandwayleaverightstositeheatnetworkspipesinroads.AstheowneroftheLocalPlananddecision-makersonplanningpermissions,LocalAuthoritiesarethereforeinstrumentalinhelpingtoshapeheatnetworks,includingthosedevelopedbytheprivatesectorandservingnewbuildproperties.

ThereareavarietyoftypesofLocalAuthoritiesintheUK.DefinedintheLocalGovernmentAct2003section33,theseincludecountycouncils,districtcouncils,boroughcouncils,citycouncils,Londonboroughs,metropolitanboroughsorunitaryauthoritiesandthislistalsonowincludescombinedauthorities.Unitarycouncilsaresingle-tier,asaremetropolitanboroughcouncils.CountycouncilssitabovedistrictorboroughcouncilsandtheGreaterLondonAuthoritysitsaboveLondonboroughcouncilsastop-tieradministrativebodies.Inthesetwo-tierscenariosresponsibilitiesaresplit.Combinedauthoritiesarevoluntarygroupingsoflocalauthoritieswhonegotiatetoundertakecertainfunctionsjointly,somedelegatedfromcentralGovernment.FiveCombinedAuthoritieshavebeensetupsofarinEngland;GreaterManchesterCombinedAuthoritybeingthefirstin2011,followedbySheffield,Leeds,LiverpoolandtheNorth-Eastin2014.

Countycouncils Unitaryauthorities Combinedauthorities

22 InvestingintheUK’sheatinfrastructure:HeatNetworks

Wheredistrictandboroughcouncilsbringdetailedknowledgeoftheirgeographicarea,relationshipswithkeystakeholdersandstrategicvision;unitarycouncils,top-tierandcombinedauthoritiesarenaturalaggregatorsworkingacrossalargerareaandcouldcoordinateprojectsacrosscouncilboundaries.LocalAuthoritiesandCombinedAuthoritieshaveincreasinglybeendevelopingtheirroleinlocaldeliveryofenergy,settingupenergycompaniesandseekingmorelocaldecisionmaking.

LocalAuthoritiesworkcloselywithconsultantsthroughthedevelopmentstagesofheatnetworksandrequiretheinputoftheirtechnical,financialandcontractualexpertise.Theylooktoconsultantstoworkwiththemtoassessthedifferentcommercialstructuresthroughwhichtheprojectcouldbedeliveredandhaveopenconversations(throughbestpracticeleanprocurement‘pre-marketengagementdays’)withtheinvestorandsupplychainmarkettoidentifywhichcommercialstructurescouldbestsupportthedesiredbenefitrealisation.Oncethishasbeencarriedout,theLocalAuthoritywillbeinagoodpositiontounderstandtheroleofprivatefinanceandappropriateprocurementroutes.WheretheLocalAuthorityintendstoowntheheatnetwork,duringcommercialisationtheLocalAuthoritywillrunacompetitivetenderingexerciseandsotheinteractionwithinvestorsandsupplychainislikelytobethroughaformalbiddingprocess.

Public procurement

PublicprocurementopportunitieswillbeadvertisedbyLocalAuthoritiesintheOfficialJournaloftheEuropeanUnion(OJEU)16andmustbeStateAidcompliant.Guidanceonpublicprocurementis

availableontheGovernmentwebsite17andspecificinformationregardingprocuringheatnetworksinScotlandisavailablefromtheHeatNetworkPartnershipforScotlandwebsite18.HMTreasuryguidanceforpublicsectorbodiesonhowtoappraiseproposalsbeforecommittingfundstoapolicy,programmeorprojectissetoutinthe‘GreenBook’19.FromApril2016,dependingoneligibility,heatnetworkscouldbeprocuredunderPublicContractsRegulations201520,UtilitiesContractsRegulations201621orConcessionContractsRegulations201622.

Other characteristics of the UK market

Aswellasanationalelectricitynetwork,theUKalsohasanationalgasnetwork.Thecounterfactualagainstwhichtheviabilityofaheatnetworkisassessedispredominantlyindividualgasboilersorelectricheating.Thisprovidesanumberofopportunitiesforheatnetworks:

• Usegasresourcesasefficientlyaspossiblethroughaheatnetwork

• Useheatsourcesthatwouldotherwisebewastedasunsuitableforbuildingscale

• Improveenergysecuritythroughdiversificationofsources

• Delayoravoidgasorelectricitygridreinforcement

• Approximately18%ofhomesarenotconnectedtothenationalgasgrid.Forthese4millionpropertiesheatingcanbeexpensiveasfuelhastobedeliveredbyroadornewconnectiontothegasgridiscostly.

16OfficialJournaloftheEuropeanUnion(OJEU)http://www.ojeu.eu/17Tenderingforpublicsectorcontractshttps://www.gov.uk/tendering-for-public-sector-contracts/overview18HeatNetworkPartnershipforScotlandprocurementguidancehttp://www.districtheatingscotland.com/content/procurement19HMTreasuryGreenBookhttps://www.gov.uk/government/publications/the-green-book-appraisal-and-evaluation-in-central-governentand

https://www.gov.uk/government/collections/the-green-book-supplementary-guidance20PublicContractsRegulations2015http://www.legislation.gov.uk/uksi/2015/102/pdfs/uksi_20150102_en.pdf21UtilitiesContractsRegulations2016https://www.gov.uk/government/consultations/transposing-the-eu-procurement-directives-utilities-

contracts-regulations22ConcessionContractsRegulations2016https://www.gov.uk/government/consultations/transposing-the-eu-procurement-directives-

concessions-contracts-regulations

23 InvestingintheUK’sheatinfrastructure:HeatNetworks

• TheUKhasahighproportionofoldhousingstockover50yearsoldwhichisnotbuilttomoderninsulationstandards.Someoftheseperiodpropertiesarehardtoinsulateduetopracticalities,costorconservationorders.Heatnetworksmaybethemosteffectivewayofdecarbonisingandreducingbillsfortheseproperties.

• Mostexistingpropertieshaveawetradiatorheatingsystemwhichcouldberetrofitforsupplybyaheatnetwork.Over1.6millionindividualboilersarereplacedintheUKeveryyearandthiscouldbeanappropriatetriggertojoinaheatnetwork.

• TheUKismoredenselypopulatedthanmanyEuropeancountries,withmanyurbanareasabletosupporteconomicallyviableheatnetworks.Urbanisationispredictedtocontinueandthisdensificationwillbringforwardadditionalheatnetworkopportunities.

Common heat network commercial structures and funding sources

Todate,heatnetworksintheUKhavecommonlyutilisedoneofthefollowingownershipmodels:

1. Local Authority ownership–theLocalAuthorityfinancesandownstheheatnetwork.Thenetworkcouldbeundertakenin-housebytheLocalAuthorityorthroughapublicsectorwhollyownedcompanyestablishedtomanagethenetwork(e.g.Arms-LengthManagementOrganisation,SpecialPurposeVehicle,LimitedLiabilityPartnership).AnumberoflocalAuthoritiesarecurrentlyexploringdevelopmentofmunicipalenergycompaniestodeliverarangeoflocalservicesincludingheatnetworks.TheLocalAuthoritymayutilisegrantfundingorraisemoneythroughprudentialborrowing;frompublicsourcessuchasthePublicWorksLoanBoardorcorporateloansfromprivatesources.Aheatnetworkoperatorwouldtypicallybeprocuredtooperatethenetworkundercontract.

Heatnetworkscanalsobedevelopedbyotherpartsofthepublicsector,suchashospitalsanduniversities.

2. Private ownership–mayarisefromaheatnetworkoriginatedbyaLocalAuthorityorbyaprivatepropertydeveloper.

a. Whereapropertydeveloperseekstomeetcarbonreductionplanningrequirements(whichcouldbeinformedbyLocalAuthoritymappingandmasterplanningwork)innewbuildpropertiesthroughaheatnetwork.Thepropertydevelopermayowntheheatnetworkbutlease,possiblythroughaconcession,thenetworklongtermtoaspecialistheatnetworkoperator,orawardvariousspecialistsubcontractsfordesign,build,operationandmaintenanceoftheheatnetwork.A‘developercontribution’maybemade,thisisapaymentfromtheheatnetworkdevelopertothepropertydeveloper.

b. ALocalAuthoritymayidentifyatechnicallyfeasibleandeconomicallyviableheatnetworkopportunity,butmaynothavetheavailablefinanceortheriskappetitetodeveloptheheatnetworkthemselves,inthesecircumstancestheheatnetworkopportunitycouldbedevelopedbyaprivatesectorheatnetworkoperator.

Thecapitalforprivatelyownedheatnetworksmayderivefromvariousprivatesectorsourcesincludingthedeveloper’sowncorporatebudgetthroughtomoneyraisedthroughcorporateloansorthebondmarket.

3. Public/Private–

a. Apublic(LocalAuthority)andprivatesectorjointventurewherebothpartiesholdanequitystake.Thiswouldrequiretheestablishmentofa‘SpecialPurposeVehicle’(SPV).Thefundingsourceslistedabovecouldbeutilisedtosecureeachparty’sequitystake,buttheLocalAuthoritycouldsecure

24 InvestingintheUK’sheatinfrastructure:HeatNetworks

anequitystakeonanon‑cashbasisthroughcontributionoflandfortheplantroom,guaranteedanchor‑loadcustomer,valueofconcessionagreementsorwayleaves.

b. Aprofit‑shareagreementthatrecognisesthenon‑cashcontributiontheLocalAuthorityhasmadetotheproject.

Thegraphbelowmapsthedifferinglevelsofcontrolandriskbalancedbetweenthepublicandprivatesectorforavarietyofheatnetworkcommercialstructures.

DetaileddescriptionsoftherangeofcommercialstructuresrepresentedinthediagrambelowaresetoutintheScottishFuturesTrust’sdocument,‘GuidanceonDeliveryStructuresforHeatNetworks’23.

Thereareawiderangeofcontractualarrangementsthatarisefromthecommonfunding/ownershipmodelscombiningelementsoffinance,design,build,operationandmaintenance,customerserviceandbilling.

23Scottish FuturesTrust:GuidanceonDeliveryStructuresforHeatNetworkshttp://www.districtheatingscotland.com/content/procurement

Public sectorcarries risk

Private sectorcarries risk

Private sector ownership with public sector facilitation

Public funding to incentivise private sector ownership

Public private joint venture with differing levels of ownership

Private sector invests in some elements of the network

Public sector led, use of private sector contractors

Entirely public sector funded, operated and owned

Private sector ownership with public sector customer

Who bears the risk

Who

has

Con

trol

Privatesectorcontrol

Publicsectorcontrol

Commercial structure options for heat networks

25 InvestingintheUK’sheatinfrastructure:HeatNetworks

Characteristics of commercially viable heat networks

Incommonwithmostinfrastructureinvestmentopportunities,heatnetworksdemonstratethefollowingcharacteristics:

• Stable and predictable cash flows: Duetoinelasticsteadydemandfortheproduct,infrastructuredeliversstableandpredictablecashflowstreams.

• Long-term predictable income streams:Longassetlifeof40+yearsandanaturalmonopolyleadtolong-termpredictableincomestreams.Operatingcostsarelowcomparedtotheinitialcapitalinvestment.

Heatnetworksalsohave:

• Expansion potential:Potentialforvalueenhancementthroughactivemanagementoftheassets.

Economicallyviableandcommerciallyinvestableheatnetworkswillexhibitsomeofthefollowingcharacteristics:

Characteristics Key factors/consideration for supply chain and investors

Size and returns • T ypicalheatnetworkcapex ranges between £4 and £40 millionintheUK,butinitialphasesarefrequentlyatthelowerendofthisrangeaskeyanchor-loadcustomersmustbesecuredforinitialbuild-out.

• Astrategicapproachtoheatnetworksiscommonwithphased build outplannedoveranumberofyearsasadditionalcustomersarecontracted.

• Long-term stable returnsareachievedwithanchor-loadcontracts(whichminimisedemandrisk).

Heat demand • Heatnetworkscanaccommodateavarietyofcustomers;however,individualdomesticconnectionsarelesscommon.Alarger, diverse, customer basewillprovideamorestableandrobustincomebase.

• Demand is usually aggregatedvia,forexample,largerheatuserssuchaslocalauthorities,sociallandlordsandhospitalsorprivatepropertymanagersofmulti-tenantedbuildings.

• ‘Anchor-loads’,theinitialaggregatedcustomerscontractedtodeliversufficientrevenueforphaseonebuildout,arecommonlysecuredfromthepublicsectororthroughcarbonreductionrequirementsofplanningpermissions.

• Integrated into long-term Local Authority infrastructure planning, demand is expected to grow over time,enablingthesystemtoexpandtotakeonadditionalheatloadsandothercost-effectivesourcesofheatovertime,includingintheprivatesector.Potentialforupsidebyactivebusinessdevelopmentandexpansion.

26 InvestingintheUK’sheatinfrastructure:HeatNetworks

Income and contracts

• L ong-term contractsareestablishedwithanchor-loadcustomers,commonlyover20yearsinduration,alignedwiththelonglifetimesoftheinfrastructure.

• Customerheattariffsarecommonlycomprisedofafixed‘standingcharge’andavariablecharge.Thestanding charge will be structured to cover the capex of the heat networkandvariablechargeswillcovertheopexandprofit.

• Customerheattariffsarecommonlyindex linkedtoprotectoperatingmargins.

• Contractualstructuresvaryandheatnetworkoperatorsmaybillendusersdirectlyormaysellbulkheattoanintermediary,suchasaLocalAuthority,propertymanagerorsupplycompany,whotakescredit riskandon-billsendusersstandingbehindthisrevenuesteamwiththeircredit.

• E lectricity salesarealsoacommonfeatureofheatnetworks,employingcombinedheatandpower.ElectricitycouldbeusedbyaLocalAuthorityheatnetworkoperatortoreducebills,couldbesoldbytheheatnetworkoperatortolocalcustomers(privatewire)orexportedtotheelectricitygrid.Additionalelectricitysystembalancingincome,suchastheShortTermOperatingReserve(STOR),mayalsobeaccessible.

• TheHeat Trust24hasbeenestablishedbyindustrytoprovideacommonstandardinthequalityandlevelofprotectionfordomesticendusercustomersonheatnetworks.

Technology • Heatnetworksareproven energy infrastructure systemswithover2,000networksoperatingintheUKandmanymoreacrossEurope.

• Likethenationalgasandelectricitygrid,theheatnetworkpipe infrastructure is technology-agnosticandcanaccommodatemultipleheatsources.Thisallowstheheatnetworktotakeheatfromthemostsuitable/cost-effectivelocalsources.

• F lexibility to change heat sources,whichshouldfurtherdecarbonisetheheatnetworksovertime,isimportantgiventhatthepipeinfrastructurehasalifetimeofover40years,longerthanmostheatsources,whicharetypically15to30years.Overthepipeinfrastructure’slonglifetime,arangeofheatsourcetechnologiesarelikelytomatureandbecomecosteffective.Infuture,anincreasingamountofwater-sourceandrecovered-heatsourcescouldbecommonplaceonheatnetworks.WhilstthesearenotyetwidelyexploitedintheUK,thereissignificantavailabilityofcanals,rivers,lakes,minewater,sewagesystems,datacentres,chillers,andindustrythatcanbeutilisedwithorwithoutaheatpump.

• T echnology innovationscanalsoprovidesignificantopportunityforcostreductionsinnetworks,suchaslowtemperaturenetworkswhichhavetheadvantageoflowermaintenancecostsandtheabilitytoincorporatelowertemperaturesourcesofrecoveredheat.

• Boilers,CombinedHeatandPower(CHP)andheatpumpsallhaveaproventrackrecordintheUK,withappropriatemanufacturers’performancewarrantees.

24HeatTrusthttp://www.heattrust.org/index.php

27 InvestingintheUK’sheatinfrastructure:HeatNetworks

Design, construction and operating contracts

• Incommonwithallinfrastructureprojects,maintainingdesign integrityagainstconstructioncostsanddeadlinescanbeaddressedthroughcarefulselectionandmanagementofprimarycontractorandsubcontracts.

• A ppropriate operations and maintenance regimescanreduceriskprofilesandmaintainreturns.Operationalcostsshouldbeminimisedwithappropriateplannedmaintenance,monitoring,leakdetectionandcontrolsystems.

• C ontract terms,takingelementsfromJCT(building)andNEC(civils)contractsareutilisedfordesign,buildandoperationofheatnetworks,providingeffectiveriskmanagement.

• TheCIBSEADECodeofPractice25setsoutminimum technical standardsrequiredthroughdesign,construction,commissioningandoperationtodeliveranefficientheatnetwork.

• Twokeyprinciplescombinetodeliveroptimum return on investment:avariedcustomerbase,forexampleresidentialandnon-residential,thatspreadheatdemandthroughthedayandthroughtheyearcombinedwithamodularapproachtoheatsourcesonthenetworki.e.baseloadrunningallyear+shoulderfromautumntospring+peakloadduringwinter,willallowmaximiseutilisationrates.

Procurement • MostprojectswherethereisasignificantLocalAuthorityrolewillbepublically procured.Thescopeofanypublicorprivateprocurementwillvary,dependingonthefunding/ownershipmodelselected.

• P ublic procurementopportunitieswillbeadvertisedintheOfficialJournaloftheEuropeanUnion(OJEU),althoughaprocurementframeworkisindevelopment(DEPA)toencouragestandardisationofapproachestothemarket.

• TheHeat Infrastructure Investment Pipelinedatabaseofopportunitieswillprovideclearsignpostingforinvestorsandsupplychain,butthestandardsetofmetricsanddefinitionswillenhancethequalityofdevelopmentstagestudies.

25CharteredInstitutionofBuildingServicesEngineers(CIBSE)andAssociationforDecentralisedEnergy(ADE)HeatNetworks:CodeofPracticefortheUKhttp://www.cibse.org/knowledge/cibse-other-publications/cp1-heat-networks-code-of-practice-for-the-uk-new

28 InvestingintheUK’sheatinfrastructure:HeatNetworks

Improving the climate for investment

Drivers

Heat networks are recognised nationally and internationally as a cost effective way of decarbonising heat in denser urban areas.

Atglobal level,UnitedNationsEnvironmentProgramme(UNEP)researchhasconcludedthatdistrictenergysystemshaveemergedasabestpracticeapproachforprovidingalocal,affordableandlow-carbonenergysupply,representingasignificantopportunityforcitiestomovetowardsclimate-resilient,resource-efficientandlow-carbonpathways26.

ThepotentialforheatnetworksisrecognisedinanumberofimportantEuropean Directivesthatflowintonationallegislationandpolicymaking.Forexample,the2012EnergyEfficiencyDirective27directsMemberStatestodeveloppoliciesupto2030todeliverthesociallycosteffectivepotentialforDistrictHeatingandCooling.Intheshorterterm,heatnetworksprovideacosteffectivemeanstomeetingtheminimumenergyperformancestandardssetoutinnationalBuildingRegulations,onapathtowardstheEUNearZeroEnergyBuildings(nZEB)requirementfrom202128.

IntheUK,thestatutorycarbontargetssetoutunderthe2008ClimateChangeActeffectivelyrequiressome21%to45%ofheatsupplytobuildingsneedstobelow-carbonby2030,withheatsupplyalmost

totallydecarbonisedby205029.Arangeofeconomicmodelshaveconcludedthatthereiscosteffectivepotentialforheatnetworkstosupplybetween14%and43%oftotalUKbuildingsheatby2050,particularlyindenserurbanareas30.Heatnetworkscurrentlysupply2%ofbuildingheatdemand(some9TWhperyear)31soacompoundgrowthrateofaround8%perannumwouldbeneededtoachieveeventhelowestendofthecosteffectivecarbonreductionpathways.ThiswouldhelpprovidetheeconomiesofscalethathavebenefittedthesectorincontinentalEurope,wherethecapitalcostofheatnetworkequipmentissome20%lowerthanintheUK32.

Atalocal level,thedriverstobuildlocalheatinfrastructureareasvariedastheheatnetworksthemselves,butcanbroadlybecategorisedas:energybillreduction,localeconomicregenerationorameanstomeetcarbonreductionrequirementsinnewbuilddevelopments.ThesedriversarelikelytocontinuetobecriticalasLocalAuthorities(municipalities)seektousetheirresourcesaseffectivelyaspossibleinordertobeabletodeliverabroadrangeoffrontlineservicestotheirresidents.

Asaresult,anumberofindustry-ledinitiativessupportedbyGovernmentareinplacetoreducecostsofdeployment,increaseefficiencyofsystemsandtoimproveconsumerprotectionsandthereforeattractivenessofthesectortonewcustomers.

26DistrictEnergyinCities:UnlockingthePotentialofEnergyEfficiencyandRenewableEnergy(2015)http://www.unep.org/energy/districtenergyincities

27NationalComprehensiveAssessment:Article14ofthe2012EnergyEfficiencyDirectiveobligatesmemberstatestoundertakeacostbenefitanalysistoidentifythesociallycosteffectivepotentialforCHPandDistrictHeating&Coolingandtodeveloppoliciesupto2030todeliverthispotential,includingbyencouragingtheuseofrecoveredwasteheatorrenewableheatandconnectionofheatsourcesandheatdemandstoDistrictHeatnetworkshttp://ec.europa.eu/energy/en/topics/energy-efficiency/energy-efficiency-directive

282010EUEnergyPerformanceofBuildingsDirectiverequiresallnewbuildingstobeNearZeroEnergyBuildings(nZEB)from2021andallexistingbuildingsundergoingmajorrenovationaretomeetminimum‘costoptimal’energyperformancerequirements,wherefeasible.http://www.epbd-ca.eu/themes/nearly-zero-energy

292011UKCarbonPlanhttps://www.gov.uk/government/publications/the-carbon-plan-reducing-greenhouse-gas-emissions--230March2013HeatStrategyTheFutureofHeating:MeetingtheChallengehttps://www.gov.uk/government/publications/the-future-of-

heating-meeting-the-challenge31March2013HeatStrategyTheFutureofHeating:MeetingtheChallengehttps://www.gov.uk/government/publications/the-future-of-

heating-meeting-the-challenge32ThepotentialandcostsofdistrictheatingnetworksPoyry/FaberMaunsellreport(2009)identifiedthatthecapitalcostofheatnetworksin

theUKare20%higherthaninmainlandEuropehttp://www.poyry.co.uk/news/potential-and-costs-district-heating-networks-report-decc-poyry-energy-consulting-and-faber-maunsell-aecom

29 InvestingintheUK’sheatinfrastructure:HeatNetworks

Promotinghightechnicalstandards

TheHeatNetworkCode of Practice33isanindustry-ledinitiativethatcomprisesasetoftechnicalstandardsdevelopedforusebyprojectsponsors,specifiersandengineersthroughheatnetworkdesign,construction,commissioningandoperation.TheCodeofPracticeaimstoensurehighqualityheatnetworksinstallationsthat:

• Deliverenergyefficiencyandenvironmentalbenefits;

• Provideagoodlevelofcustomerservice;and

• Promotelong-lastingheatnetworksinwhichcustomersandinvestorscanhaveconfidence.

TheCodewaslaunchedinJuly2015andissupportedbyatrainingandregistrationprogrammeforthosedeliveringprojectsundertheCode.

Improvingconsumerprotections

Heat Trust34isavoluntaryschemethatisbeingsetuptoestablishacommonstandardinthequalityandlevelofprotectionforcustomersonheatnetworks.Itsetsout,amongstotherthings,heatsupplierobligationsandperformancestandards,supportforvulnerablecustomersandintroducesanindependentdisputeresolutionservice.HeatTrusthasbeendevelopedwithindustry,consumergroups,nationalanddevolvedadministrations.Theschemewilllaunchinlate2015.

DistrictEnergyProcurementAgency

AmembershipbasedprocurementframeworkforLocalAuthoritiesiscurrentlyindevelopment.TheDistrictEnergyProcurementAgency(DEPA)willbenefitsuppliersandmanufacturersofdistrictenergygoodsandservicesbyactingasacompetentnegotiatingpartner,standardisingproceduresandthusreducingtheirtransactioncosts.ForcompanieswishingtojointheUKmarket,itwillprovideasinglepointofentry.

Promotinginnovationtolowerdeploymentcosts

Small Business Research Initiative (SBRI) Heat Networks Demonstrator:A£7millionheatnetworkinnovationanddemonstrationprogrammeisbeingmanagedbyDECCtostimulateinnovationthatwillbringdownheatnetworkscostsandimproveperformance35.

Thereisabroadrangeofinnovativeprojectsbeingsupported.Somearefocussedonimprovingnetworkefficiencybydevelopingsmartheatingcontrolstomanagedomesticdemandontheheatnetwork,toreducepeakloadordiagnosenetworkperformanceissues.Smarttechnologyisalsobeingusedtodevelopaheatnetworkmonitoringandbillingapplicationtomakethefullextentofmeteringdataopenlyavailabletooperators.

33CharteredInstitutionofBuildingServicesEngineers(CIBSE)andAssociationforDecentralisedEnergy(ADE)HeatNetworks:CodeofPracticefortheUKhttp://www.cibse.org/knowledge/cibse-other-publications/cp1-heat-networks-code-of-practice-for-the-uk-new

34HeatTrusthttp://www.heattrust.org/index.php35Costreducinginnovation-SBRIHeatNetworksDemonstratorhttps://sbri.innovateuk.org/competition-display-page/-/asset_publisher/

E809e7RZ5ZTz/content/heat-networks-demonstrator/1524978andhttps://www.gov.uk/guidance/innovation-funding-for-low-carbon-technologies-opportunities-for-bidders

30 InvestingintheUK’sheatinfrastructure:HeatNetworks

Attheotherendofthescale,anotherprojectaimstodeliverdeepgeothermalheatprojectsinunder12months.ThedemonstrationprojectwillbethefirstconnecteddeepgeothermalsinglewellsystemintheUKandthefirstdeepgeothermalheatprojectfor25years.Similarly,oneprojectwillseethefirstlarge-scalesolarthermalheatpumpbeingdeployedonaheatnetworkintheUK.

Smart Systems & Heat Programme (SS&H):ThisjointGovernmentandindustry-fundedprogramme,runbytheEnergyTechnologyInstitute(ETI),isdevelopingthemodelsandplansrequiredforasignificantsystem-leveldemonstrationtodecarboniseheatinginthreeLocalAuthorityareas,comprisingsome3,000to10,000properties36.

Impacts of increased heat infrastructure deployment

AsthisHeatInfrastructureInvestmentPipelinegrowsandheatnetworkdeploymentratesincrease,thereisanopportunityforcurrentmarketparticipantstoexpandoperations,butalsofornewmarketplayerstoentertheUKheatnetworkmarket;includingthroughpartnershipsorjointventures.ThisgrowthmaybringaboutanevolutionoftheUK’sheatnetworkmarketoverthenext10years:–witheconomiesofscalerealised,costreducinginnovationdeployedandnewcommercialstructures,possiblycentredaroundaggregationorunbundlingofgenerationanddistribution,emerging.

Feedback loop

Innovation

Deploying cost reducing

innovation

Reduced risk perception

Increased availability of appropriate

finance

Improved IRR =more networks

viable

Increased deployment

rates

36EnergyTechnologiesInstituteSmartSystems&Heat:Creatingfuture-proofandeconomiclocalheatingsolutionsfortheUKhttp://www.eti.co.uk/programme/smart-systems/

31 InvestingintheUK’sheatinfrastructure:HeatNetworks

How would you likethe conversationto continue… ?

32 InvestingintheUK’sheatinfrastructure:HeatNetworks

Support for investors and supply chain

UKTrade&Investment(UKTI)

UKTIisthespecialistGovernmentdepartmentthatsupportsforeigncompaniesseekingtosetuporexpandintheUK.UKTIprovidesafullyintegratedadvisoryservice,deliveringthelatestbusinessintelligencethroughaglobalnetworkofcommercialteamsworldwide.UKTIworksinclosepartnershipwithinvestmentandeconomicdevelopmentagenciesinEngland,Scotland,WalesandNorthernIrelandtohelpoverseascompaniestomaximisetheirbusinessobjectivesintheUK.

EnquiriesforoverseascompanieslookingtosetupintheUK:

Email:[email protected]

Telephone:+44(0)2073335442

AssociationforDecentralisedEnergy(ADE)

TheAssociationforDecentralisedEnergy(ADE)istheleadingadvocateofanintegratedapproachtodeliveringenergyservicesfromdecentralisedenergysourcessuchascombinedheatandpoweranddistrictheatingandcooling.

AssociationforDecentralisedEnergy,6thFloor,10DeanFarrarStreet,London,SW1H0DX

Email:[email protected]

Telephone:+44(0)2030318740

www.theade.co.uk

TheHeatNetworkPartnershipforScotland

TheHeatNetworkPartnershipisacollaborationofagenciesinScotlandfocusedonthepromotionandsupportofDistrictHeatingschemesinScotland.Thiswebsiteoffersexperience,informationandkeycontactsthatwillhelpboostthegrowthofdistrictheating.

TheScottishprojectpipelineandinvestmentreportareavailableat:http://www.districtheatingscotland.com/content/investment-heat-networks-scotland

Procurementguidance:http://www.districtheatingscotland.com/content/procurement

Forfurtherinformation,visit:http://www.districtheatingscotland.com/form/contact-us-0

CreatingvaluefromstartupstocorporatesUKTIdevelopsbespokeprogrammesinsupportofeachsegmentoftheinwardinvestorvaluechain.

High Growth Potential

UKTI Services

Sirius Programme

Global Entrepreneurs Programme

Access to networks and the entrepreneur ecosystem

International trade (export) advice

UK Product offer

Seed Enterprise Investment Scheme

Enterprise Investment Scheme

R&D Tax Credit/Corporate Tax Relief

Catapult Centres

Medium and Large

UKTI Services

Relationship management

International trade (export) advice

Sector Trade & Investment Organisations

Access to industry networks and sector ecosystems

UK Product offer

Enterprise Investment Scheme

R&D Tax Credit/Corporate Tax Relief

Enterprise Zones

Catapult Centres

Innovation Gateway

Institutional Investors

UKTI Services

Relationship management

Regeneration Investment Organisation/online platform

Infrastructure and regeneration pitch books

Infrastructure and regeneration pipelines

UK Product offer

Regeneration Investment Plan

UK Infrastructure Guarantee

Enterprise Zones

National Infrastructure Plan

Innovation Gateway

33 InvestingintheUK’sheatinfrastructure:HeatNetworks

UKGreenInvestmentBank(GIB)

TheUKGreenInvestmentBankinvestsinspecificareasofthelowcarboneconomywithaspecificmandatetosupportthecreationofmarketsandtocrowdinotherformsofcapital.Thisspecificallyincludesheatnetworks.GIB’scapitalishighlyflexible,beingabletobedeployedasdebt,equityormezzanineintoprojectswithchallengingstructuringissues.Projectscanbefinancedovera30yeartermandrepaymentssculptedtofitrevenueprojections.FinancingavailablefromGIBrangesfrom£1millionto£100million.TheGIBteamincludes,equity,debt,projectfinanceandprojectdevelopment/technicalspecialistsabletoaddressanyissuewithrespecttothecommercialandfinancialstructuringofaheatnetworkproject.

Enquiriesshouldbeaddressedto:

IainWatson,Director–EnergyEfficiencyEmail:[email protected]:+44(0)3301232136,+44(0)7802447082

AlinaGheorghiu-CurrieEmail:[email protected]:+44(0)3301233042,+44(0)7557089756

Further information

Planning

England

• NationalPlanningPolicyFrameworkforEnglandhttps://www.gov.uk/government/publications/national-planning-policy-framework--2

• PlanningPracticeGuidanceforEnglandhttp://planningguidance.planningportal.gov.uk

Scotland

• NationalPlanningFrameworkforScotlandhttp://www.gov.scot/Topics/Built-Environment/planning/National-Planning-Framework

• ScottishPlanningPolicyhttp://www.gov.scot/Topics/Built-Environment/planning/Policy

• Planningandheatonlineguidancehttp://www.gov.scot/Topics/Built-Environment/planning/Policy/Subject-Policies/low-carbon-place/Heat-Electricity

34 InvestingintheUK’sheatinfrastructure:HeatNetworks

Wales

• PlanningWaleshttp://gov.wales/topics/planning/?lang=en

Combined heat and power Quality Assurance (CHPQA)• CombinedHeat&PowerQualityAssuranceProgramme

https://www.gov.uk/guidance/combined-heat-power-quality-assurance-programme

Renewable Heat Incentive• Non-domesticRenewableHeatIncentive(RHI)DECC

https://www.gov.uk/non-domestic-renewable-heat-incentive

• Non-DomesticRenewableHeatIncentive(RHI)Ofgemhttps://www.ofgem.gov.uk/environmental-programmes/non-domestic-renewable-heat-incentive-rhi

EU ETS – Large heat networks• EuropeanUnionEmissionsTradingSystem(EUETS)Union

Registryhttps://www.gov.uk/guidance/eu-ets-carbon-markets

• ParticipatingintheEUETShttps://www.gov.uk/guidance/participating-in-the-eu-ets

Energy Company Obligation (ECO)• EnergyCompanyObligation(ECO)https://www.ofgem.gov.uk/

environmental-programmes/energy-company-obligation-eco

• EnergyCompanyObligation(ECO2):MeasuresTablehttps://www.ofgem.gov.uk/publications-and-updates/energy-company-obligation-eco2-measures-table

District Heating Connections Lifetime in years

Biomass boiler (Upgrade) 30

Gas/oil boiler (Upgrade) 25

CHP (Upgrade) 25

Energy from Waste (Upgrade) 25

Ground Source Heat Pump (Upgrade) 20

Air Source Heat Pump (Upgrade) 15

Heat network pipe infrastructure (New Connection All generator types)

40

35 InvestingintheUK’sheatinfrastructure:HeatNetworks

Heat Network (Metering and Billing) Regulations 2014: guidance to compliance and enforcement of the legislation• https://www.gov.uk/guidance/heat-networks

BSRIA UK District Energy 2013 market intelligence report• https://www.bsria.co.uk/market-intelligence/market-

reports/publication/uk-district-energy-2013/

Assessment of the costs, performance and characteristics of UK heat networks• https://www.gov.uk/government/publications/assessment-

of-the-costs-performance-and-characteristics-of-uk-heat-networks

CIBSE/ADE Heat Networks: Code of Practice for the UK• http://www.cibse.org/Knowledge/CIBSE-other-publications/

CP1-Heat-Networks-Code-of-Practice-for-the-UK

Heat Trust: independent heat customer protection scheme• http://www.heattrust.org/index.php

Delivering UK Energy Investment: Networks 2014• https://www.gov.uk/government/publications/delivering-

uk-energy-investment-networks-2014

Heat maps• Englandhttp://tools.decc.gov.uk/nationalheatmap/

• WatersourceheatmapforEnglandhttps://www.gov.uk/government/publications/water-source-heat-map

• Scotlandwww.gov.scot/heatmap

For more information, please contact the DECC Email:[email protected]@decc.gsi.gov.uk

36 InvestingintheUK’sheatinfrastructure:HeatNetworks

gov.uk/decc

DECCTheDepartmentofEnergy&ClimateChange(DECC)workstomakesuretheUKhassecure,clean,affordableenergysuppliesandpromoteinternationalactiontomitigateclimatechange.

DisclaimerWhereaseveryefforthasbeenmadetoensurethattheinformationinthisdocumentisaccurateDepartmentofEnergy&ClimateChangeacceptliabilityforanyerrors,omissionsormisleadingstatements,andnowarrantyisgivenorresponsibilityacceptedastothestandingofanyindividual,firm,companyorotherorganisationmentioned.

©Crowncopyright2015

Youmayre-usethisinformationfreeofchargeinanyformatormedium,strictlyinaccordancewiththetermsoftheOpenGovernmentLicence.Toviewthislicence,visit:

www.nationalarchives.gov.uk/doc/open-government-licenceore-mail:[email protected].

Wherewehaveidentifiedanythirdpartycopyrightinformationinthematerialthatyouwishtouse,youwillneedtoobtainpermissionfromthecopyrightholder(s)concerned.

Anyenquiriesregardingthismaterialshouldbesenttousatcorrespondence@decc.gsi.gov.ukortelephone+44(0)3000604000Thisdocumentisalsoavailableatwww.gov.uk/ukti

Published November 2015 by DECC URN: 15D/453