28

daa Defined Contribution Retirement Savings Scheme May 2016 Investment Guide

| Date post: | 29-Jul-2016 |

| Category: |

Documents |

| Upload: | daa-dc-scheme |

| View: | 226 times |

| Download: | 0 times |

daa Defined Contribution Retirement Savings Scheme

May 2016

Investment Guide

32

daa Defined Contribution Retirement Savings Scheme

1

Investment Guide

Contents

Introduction 2

Considerations when making investment choices 3Who will make my investment decisions? ....................................................3How do my needs change as I approach retirement? .................................3Other considerations ...................................................................................4

Back to basics: investment fund options 5

What risks do my investments face? 7Inflation risk .................................................................................................7Market risk ..................................................................................................7Manager risk ...............................................................................................8Annuity risk .................................................................................................8

How do I decide how much risk to take? 9Time horizon ...............................................................................................9Attitude to risk .............................................................................................9Other assets .............................................................................................. 10

What are my investment options? 10If you want someone else to manage your savings .................................... 10If you want to manage your savings yourself ............................................. 10

Investment fund options 11daa Equity Fund ........................................................................................ 11 daa Growth Fund ...................................................................................... 12daa Cautious Growth Fund ....................................................................... 14daa Annuity Fund ...................................................................................... 16daa Cash Fund .......................................................................................... 17Lifestyle Strategies .................................................................................... 18

Making your decision 22How to select your investment options ......................................................22How can I make changes to my choices? .................................................22

Glossary 23

Further information 24

Who’s who 24

2

daa Defined Contribution Retirement Savings Scheme

Introduction

With a Defined Contribution Retirement Savings Scheme, you’re in control of how your Retirement Savings Account is managed. You decide how much you want to contribute, and how you want the money in your account to be invested.

Two of the key factors in the amount of savings you will have for your retirement are (i) the amount that is contributed into your Retirement Savings Account during your working life and (ii) how early those contributions are made. But another key factor is the investment decisions that are made in relation to those savings, which can make a real difference when you retire.

The purpose of this Investment Guide is to provide you with information about investing your retirement savings in the daa Defined Contribution Retirement Savings Scheme (the DC Scheme). The guide covers:

What to consider when choosing investments

Investment options and explanations

How investment needs change with age

Your decisions

This guide will help you understand the investment options available and what they mean to you. It contains a lot of information, so for clarity we have included a glossary at the back of the guide to explain pension terminology.

There is also a separate Member Guide (ex-IASS or non-IASS), which provides a summary of the principal features of the DC Scheme. The Investment Guide should be read in conjunction with the Member Guide.

Other more formal documents, such as the Trust Deed and Rules, give legal backing to the DC Scheme and these can be viewed by requesting copies from the DC Scheme Administrator, Invesco Limited, 2 Sandyford Business Centre, Burtonhall Road, Sandyford, Dublin 18 (telephone 01 2947600) or by visiting www.invescoonline.ie. If there is a difference between this guide and the provisions of the Trust Deed and Rules, then the provisions of the Trust Deed and Rules will apply.

Investment Guide

Considerations when making investment choices

The DC Scheme offers members a range of investment options to meet different needs. How you invest your retirement savings is very important. The better your investments perform, the faster your Retirement Savings Account will grow and the better your benefits in retirement will be. There are a number of factors to consider:

3

Who will make my investment decisions?The key choice when making your investment decision is:

A. Do you want your investments managed for you? B. Do you wish to select your own investment funds?

If you want someone else to make your decisions for you, your contributions will be invested at the direction of the Trustee in the daa Growth Fund. This fund is specifically tailored to members of the DC Scheme and is managed by an investment manager with oversight from the Trustee. It aims to provide stable growth in excess of inflation over time and it prepares for retirement by gradually and automatically moving to less risky assets as you approach retirement (pre-retirement phase).

If you have some investment knowledge and want to manage your own investments, there is a range of funds to choose from. You can choose one of the funds or a combination of two or more funds. These are detailed later in this guide. Note that if you choose to select your own investment fund(s), your savings will not be automatically moved into less risky assets as you approach retirement.

How do my needs change as I approach retirement?As a member approaches retirement, the mix of assets that will provide the best outcome generally changes. Most members’ retirement savings goals change from creating long-term growth towards the preservation of retirement savings. If you select to have your investments managed for you or you do not make any selection at all, a Lifestyle Strategy will automatically change the investment profile of your Retirement Savings Account. As you approach retirement, the amount invested in the daa Growth Fund will be reduced in favour of lower risk funds in order to provide more protection for your savings.

4

daa Defined Contribution Retirement Savings Scheme

If you decide to select your own mix of funds your retirement savings will not be automatically moved to lower risk assets. You will need to make your own choices reflecting your personal approach to risk and your own retirement goals.

Note

�This�guide�is�only�intended�for�use�by�members�of�the�daa�Defined�Contribution�Retirement Savings Scheme

The information in this guide is based on the understanding of legislation and Revenue requirements at the time of writing

The Trustee may amend, remove and add investment options at any time

Some�funds�may�be�affected�by�changes�in�currency�exchange�rates

Past performance is not a reliable guide to future performance

Investments may fall as well as rise in value

Other considerationsThere are a number of other things to consider when thinking about your investment options:

How much time do you have to save until your retirement?

What level of income would you like to have at retirement?

What level of investment risk are you comfortable with?

What combination of benefits might you want to take at retirement (annuity, lump sum, income for dependants, Approved Retirement Fund (ARF), etc.)?

What are your contribution levels?

5

Investment Guide

Back to basics: investment fund options

Before reading about your fund options, here is a brief overview of the main types of investments that the funds can hold:

EquitiesEquity funds are made up of shares in companies traded on stock markets. As an incentive for people to buy shares, some companies offer shareholders a share of their profits, paid out as an annual dividend. Dividends can vary and are never guaranteed.

Equity funds are affected by rises and falls in the stock markets. Their value can go up and down significantly and suddenly, and are considered a volatile investment.

Historically, equities have outperformed every other asset class over the long-term.Equity funds would usually be considered suitable if you have more than ten years to retirement as they are very volatile investments but offer the potential for long-term growth.

BondsBonds are traded on investment markets. Their prices are linked to interest rates. While historically bond prices have typically been less volatile than equity prices they can fall sharply, particularly in low interest rate environments. Bonds do not typically experience the strong long-term growth that shares can potentially enjoy.

Bond funds may be suitable in the period leading up to your planned retirement date if you intend to purchase an annuity (pension for life) with your Retirement Savings Account as the capital value of these funds tends to move in line with the cost of purchasing a pension.

CashCash funds are made up of cash deposits (similar to a bank account) and cash-like investments issued by financial institutions. Cash funds are generally considered a low-risk, low-return investment option. Cash funds generally offer lower returns over the long-term than all other asset classes and may not keep pace with inflation. In times of low interest rates, returns on cash can be negative.

Cash funds may be suitable if you are within a few years of your planned retirement date and wish to preserve the value of your Retirement Savings Account.

6

daa Defined Contribution Retirement Savings Scheme

Multi-Asset Growth FundsThe daa Growth Fund and the daa Cautious Growth Fund are examples of multi-asset growth funds.

These are funds that invest in a wide variety of asset types and typically include equities, bonds and cash, as well as more specialist investments such as property, commodities, infrastructure and currencies.

Multi-asset growth funds are managed to deliver long-term growth above inflation but with fewer ups and downs than equity investments. They are designed to protect against significant falls in markets and may use derivative instruments to achieve their objectives. However, capital is not guaranteed and there can be falls in the value of assets. Multi-asset funds are typically actively managed and the Annual Management Charge (AMC) is normally higher than other funds.

Multi-asset growth funds are suitable at most stages of your retirement savings as they offer long-term growth potential with lower volatility. They may also be suitable if you are planning to fund your retirement income by investing in an Approved Retirement Fund (ARF), as they should help you to continue to grow the value of your investment into your retirement.

If you do not make a decision about where your contributions should be invested, they will be automatically invested in the daa Growth Fund until seven years before your Normal Retirement Date. In the seven years before your retirement, your assets will be gradually switched into lower risk assets. The type of�lower�risk�assets�you�are�moved�into�will�depend�on�the�mix�of�assets�you�will�most likely need in your portfolio at retirement. For more information please refer to the Lifestyle Strategies on page 18.

7

Investment Guide

What risks do my investments face?

The four main types of risk that you should be aware of when considering your investment options are as follows:

Inflation risk Market risk Manager risk Annuity risk

Inflation riskOver the long-term, inflation erodes the real value of your Retirement Savings Account and increases the cost of purchasing your retirement benefits.

In order to maximise your income in retirement, you should aim to achieve an investment return that keeps up with, and ideally exceeds, long-term inflation. Keeping up with inflation preserves the purchasing power of your savings.

Equity and multi-asset funds are most likely to produce returns in excess of inflation. Cash funds may produce returns less than inflation, which would cause the real value of your retirement savings to fall over time.

Market riskIt is important to remember that the value of investments can fall as well as rise. Market risk is the risk that your investments may fall (and rise) in line with market movements (volatility).

Different types of investments have different levels of volatility. Historically, market risk (volatility) and return have been linked; the more volatile the investment, the higher the average returns over time, although this is not guaranteed. Equities tend to have higher and more volatile returns than cash or bonds.

When building up your retirement savings, you can generally afford to take more risk the longer you have to retirement as you will have the time to recoup any losses that occur and ride out the ups and downs of volatile markets.

8

daa Defined Contribution Retirement Savings Scheme

Manager riskThis is the risk that a particular investment manager underperforms the benchmark index. This can occur in actively managed funds where the manager takes different positions to the benchmark in an attempt to achieve higher returns than the index and/or competitors.

Using passive funds virtually eliminates manager risk; these are funds where the manager follows the market index with the aim of matching index returns rather than beating them. Fees for active management are higher than for passive management.

Annuity riskThis is the risk that the cost of purchasing annuities (pensions) becomes more expensive as you approach retirement. If you are expected to purchase an annuity with your Retirement Savings Account and are invested in the daa Growth Fund, you will automatically be invested in an annuity fund as you approach retirement in order to minimise annuity risk. Annuity funds move broadly in line with the cost of purchasing annuities.

9

Investment Guide

How do I decide how much risk to take?

Your personal circumstances play a huge part in deciding what investment risk to take. The key factors are:

Time horizon Attitude to risk Other assets

Time horizonTime horizon is the key determinant in some of the risks we have outlined.

A 25-year-old may be more concerned about missed opportunity and inflation risk rather than market or annuity risk. Members with a long time to go until retirement might focus on maximising long-term returns with less concern about the possibility of day-to-day or even year-on-year drops in the value of their portfolio. This is because they have plenty of time to recoup losses incurred.

A 64-year-old planning on taking a cash lump sum and buying an annuity (pension) at retirement is likely to be more focused on capital preservation (market risk) and annuity/pension conversion risk and will wish to protect their investments against these.

Attitude to riskEveryone has a different appetite for, and attitude towards, risk and it is important to know where your own tolerance for risk lies. There are those who focus purely on maximising long-term investment return, unfazed by the fact that this can often involve a rollercoaster ride of peaks and troughs in value. Others prefer a smoother ride and are willing to sacrifice growth potential for a less stressful investment journey.

Market timing risk needs to be particularly guarded against for those invested in assets more exposed to market risk (such as equities and property). The temptation is to buy an asset after it has risen in value - when prices are high - and sell when it has done badly - when prices are low. This is of course the opposite of what long-term investors try to achieve.

This Investment Guide is intended to help you make important decisions which�will�affect�your�income�when�you�retire.�If�you�do�not�feel�comfortable�making these decisions yourself, you always have the option to seek independent�financial�advice�about�your�investment�options.�Alternatively,�you�can choose to have your investments managed for you by the Trustee.

10

daa Defined Contribution Retirement Savings Scheme

Other assetsIn general, those with other sources of wealth can afford to take greater investment risk than those who will rely heavily on one particular pension. In this context, it is important that former members of the IASS take into account their likely pension from that scheme.

What are my investment options?If you want someone else to manage your savings:

If you want your investments managed for you, they will be invested in the daa Growth Fund in the period up to seven years before your Normal Retirement Date. This is a multi-asset fund managed specifically for DC Scheme members. It invests in a mix of assets (including equities, property, alternative assets and bonds) and is designed to provide real long-term growth. As you approach retirement, the amount invested in the daa Growth Fund will be reduced in order to provide more protection for your savings. There are more details on these funds in the following pages.

If you want to manage your savings yourself:

If you are familiar with investments and wish to select your own funds, then you can choose to invest in one or a combination of the funds outlined below and detailed on the following pages. It is important to note that for self-selectors, there is no automatic move into less risky assets on approaching retirement.

daa Equity Fund daa Growth Fund daa Cautious Growth Fund daa Annuity Fund daa Cash Fund

For the options mentioned above, there is an underlying investment manager appointed by the Trustee who manages the funds on behalf of members. These managers are closely monitored and may be changed in the future, but the name of the fund will remain the same regardless of who the underlying manager is. The investment managers are currently Legal and General Investment Management and Principal Global Investors. These managers, in turn, have the capability to allocate to a broad range of other managers within the growth funds.

11

Investment Guide

daa Equity Fund

Investment Goal To target the long-term returns that global equity markets provide in the most cost-effective way possible.

How are assets invested?

The fund invests to produce returns in line with the FTSE World Index. It tracks the market return by investing in a basket of securities in the same proportion as they are represented in the FTSE World Index.

50% of exposure to currencies other than Euro is hedged. This fund is passively managed.

This fund might be suitable for you if:

You are more than seven years from retirement. You are prepared to accept the volatility of returns and asset values associated with investments in equity markets in exchange for potentially higher associated long-term returns.

You are willing to take the risks associated with investment in equities.

You want the growth of your account to match or outpace inflation over time.

Risk Characteristics Equities are high-volatility investments. Values can go up as well as down by significant amounts in the short-term.

Current Fees 0.10% Total Expense Ratio.

Are there any investment charges?The investment managers charge a fee for managing the funds, which is deducted from your Retirement Savings Account automatically. The Trustee has negotiated with the investment managers to ensure a competitive fee for members. Your annual benefit statement will show the respective funds’ unit prices after these fees have been deducted and this will be reflected in your Retirement Savings Account value. Details of these charges are contained below and in the glossary of terms at the end of this guide.

daa pays the day-to-day costs associated with administering the DC Scheme.

Investment fund options

12

daa Defined Contribution Retirement Savings Scheme

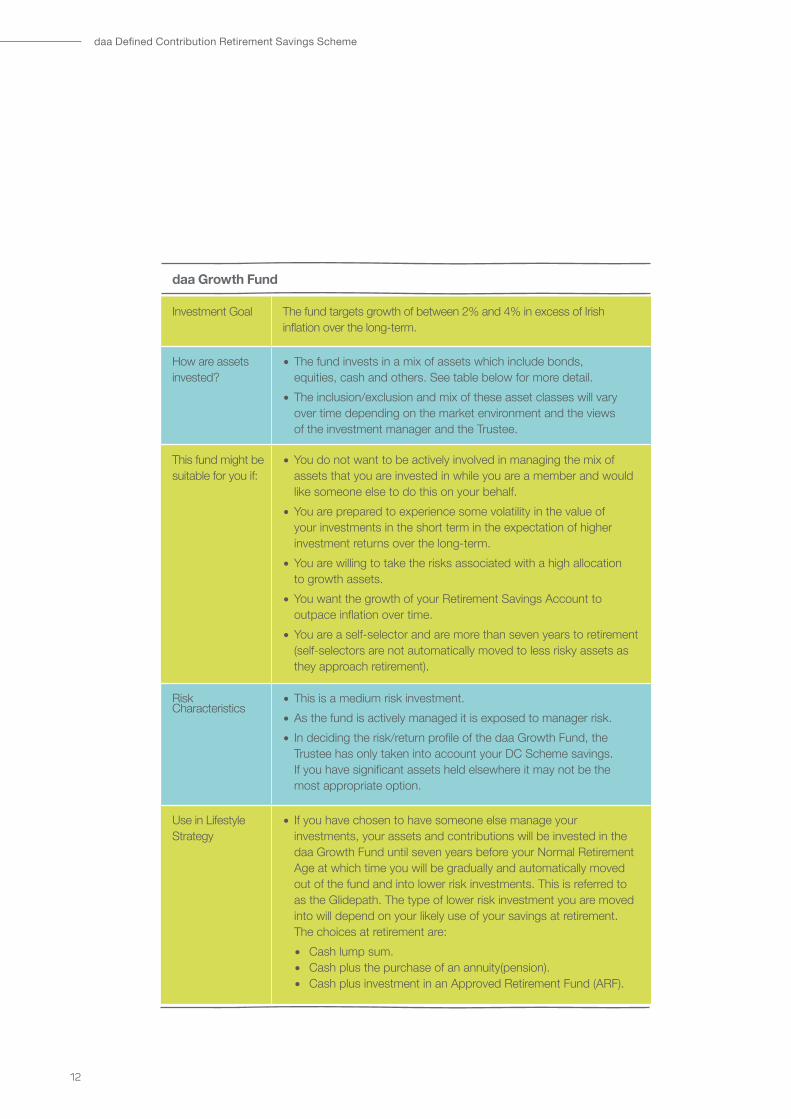

daa Growth Fund

Investment Goal The fund targets growth of between 2% and 4% in excess of Irish inflation over the long-term.

How are assets invested?

The fund invests in a mix of assets which include bonds, equities, cash and others. See table below for more detail.

The inclusion/exclusion and mix of these asset classes will vary over time depending on the market environment and the views of the investment manager and the Trustee.

This fund might be suitable for you if:

You do not want to be actively involved in managing the mix of assets that you are invested in while you are a member and would like someone else to do this on your behalf.

You are prepared to experience some volatility in the value of your investments in the short term in the expectation of higher investment returns over the long-term.

You are willing to take the risks associated with a high allocation to growth assets.

You want the growth of your Retirement Savings Account to outpace inflation over time.

You are a self-selector and are more than seven years to retirement (self-selectors are not automatically moved to less risky assets as they approach retirement).

Risk Characteristics

This is a medium risk investment. As the fund is actively managed it is exposed to manager risk. In deciding the risk/return profile of the daa Growth Fund, the Trustee has only taken into account your DC Scheme savings. If you have significant assets held elsewhere it may not be the most appropriate option.

Use in Lifestyle Strategy

If you have chosen to have someone else manage your investments, your assets and contributions will be invested in the daa Growth Fund until seven years before your Normal Retirement Age at which time you will be gradually and automatically moved out of the fund and into lower risk investments. This is referred to as the Glidepath. The type of lower risk investment you are moved into will depend on your likely use of your savings at retirement. The choices at retirement are:

Cash lump sum. Cash plus the purchase of an annuity(pension). Cash plus investment in an Approved Retirement Fund (ARF).

13

Investment Guide

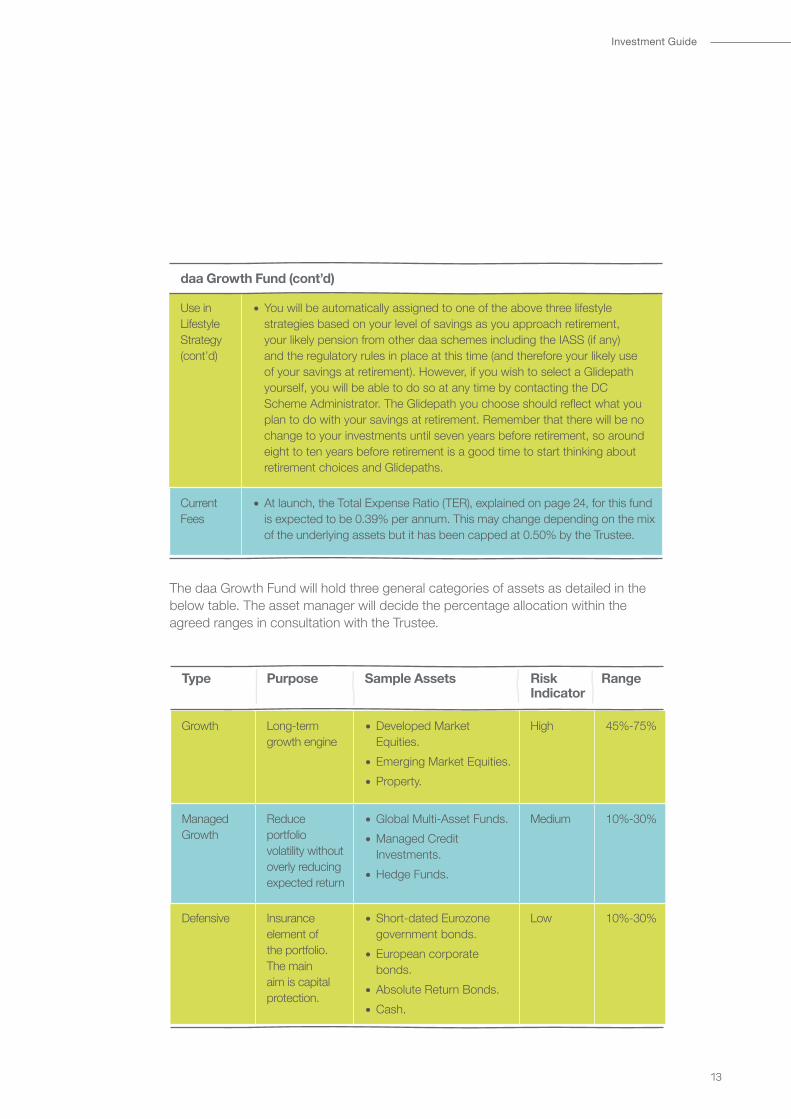

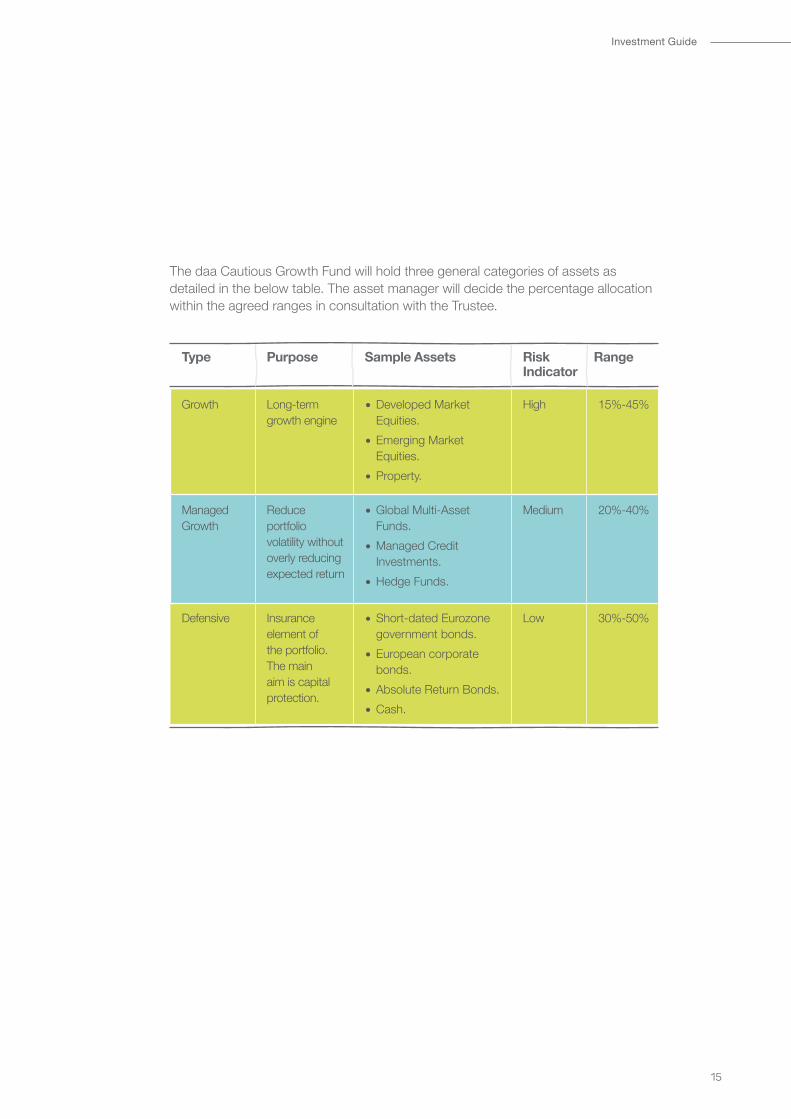

The daa Growth Fund will hold three general categories of assets as detailed in the below table. The asset manager will decide the percentage allocation within the agreed ranges in consultation with the Trustee.

daa Growth Fund (cont’d)

Use in Lifestyle Strategy (cont’d)

You will be automatically assigned to one of the above three lifestyle strategies based on your level of savings as you approach retirement, your likely pension from other daa schemes including the IASS (if any) and the regulatory rules in place at this time (and therefore your likely use of your savings at retirement). However, if you wish to select a Glidepath yourself, you will be able to do so at any time by contacting the DC Scheme Administrator. The Glidepath you choose should reflect what you plan to do with your savings at retirement. Remember that there will be no change to your investments until seven years before retirement, so around eight to ten years before retirement is a good time to start thinking about retirement choices and Glidepaths.

Current Fees

At launch, the Total Expense Ratio (TER), explained on page 24, for this fund is expected to be 0.39% per annum. This may change depending on the mix of the underlying assets but it has been capped at 0.50% by the Trustee.

Type Purpose Sample Assets Risk Indicator

Range

Growth Long-term growth engine

Developed Market Equities.

Emerging Market Equities. Property.

High 45%-75%

Managed Growth

Reduce portfolio volatility without overly reducing expected return

Global Multi-Asset Funds. Managed Credit Investments.

Hedge Funds.

Medium 10%-30%

Defensive Insurance element of the portfolio. The main aim is capital protection.

Short-dated Eurozone government bonds.

European corporate bonds.

Absolute Return Bonds. Cash.

Low 10%-30%

14

daa Defined Contribution Retirement Savings Scheme

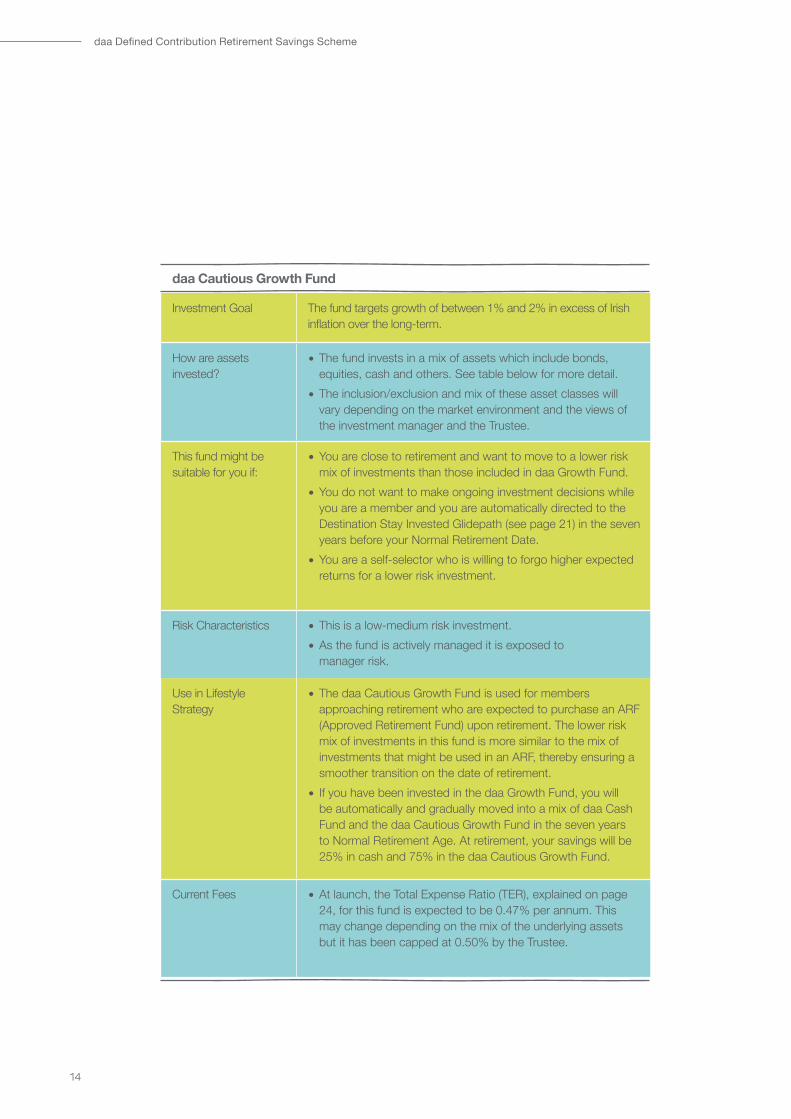

daa Cautious Growth Fund

Investment Goal The fund targets growth of between 1% and 2% in excess of Irish inflation over the long-term.

How are assets invested?

The fund invests in a mix of assets which include bonds, equities, cash and others. See table below for more detail.

The inclusion/exclusion and mix of these asset classes will vary depending on the market environment and the views of the investment manager and the Trustee.

This fund might be suitable for you if:

You are close to retirement and want to move to a lower risk mix of investments than those included in daa Growth Fund.

You do not want to make ongoing investment decisions while you are a member and you are automatically directed to the Destination Stay Invested Glidepath (see page 21) in the seven years before your Normal Retirement Date.

You are a self-selector who is willing to forgo higher expected returns for a lower risk investment.

Risk Characteristics This is a low-medium risk investment. As the fund is actively managed it is exposed to manager risk.

Use in Lifestyle Strategy

The daa Cautious Growth Fund is used for members approaching retirement who are expected to purchase an ARF (Approved Retirement Fund) upon retirement. The lower risk mix of investments in this fund is more similar to the mix of investments that might be used in an ARF, thereby ensuring a smoother transition on the date of retirement.

If you have been invested in the daa Growth Fund, you will be automatically and gradually moved into a mix of daa Cash Fund and the daa Cautious Growth Fund in the seven years to Normal Retirement Age. At retirement, your savings will be 25% in cash and 75% in the daa Cautious Growth Fund.

Current Fees At launch, the Total Expense Ratio (TER), explained on page 24, for this fund is expected to be 0.47% per annum. This may change depending on the mix of the underlying assets but it has been capped at 0.50% by the Trustee.

15

Investment Guide

The daa Cautious Growth Fund will hold three general categories of assets as detailed in the below table. The asset manager will decide the percentage allocation within the agreed ranges in consultation with the Trustee.

Type Purpose Sample Assets Risk Indicator

Range

Growth Long-term growth engine

Developed Market Equities.

Emerging Market Equities.

Property.

High 15%-45%

Managed Growth

Reduce portfolio volatility without overly reducing expected return

Global Multi-Asset Funds.

Managed Credit Investments.

Hedge Funds.

Medium 20%-40%

Defensive Insurance element of the portfolio. The main aim is capital protection.

Short-dated Eurozone government bonds.

European corporate bonds.

Absolute Return Bonds. Cash.

Low 30%-50%

16

daa Defined Contribution Retirement Savings Scheme

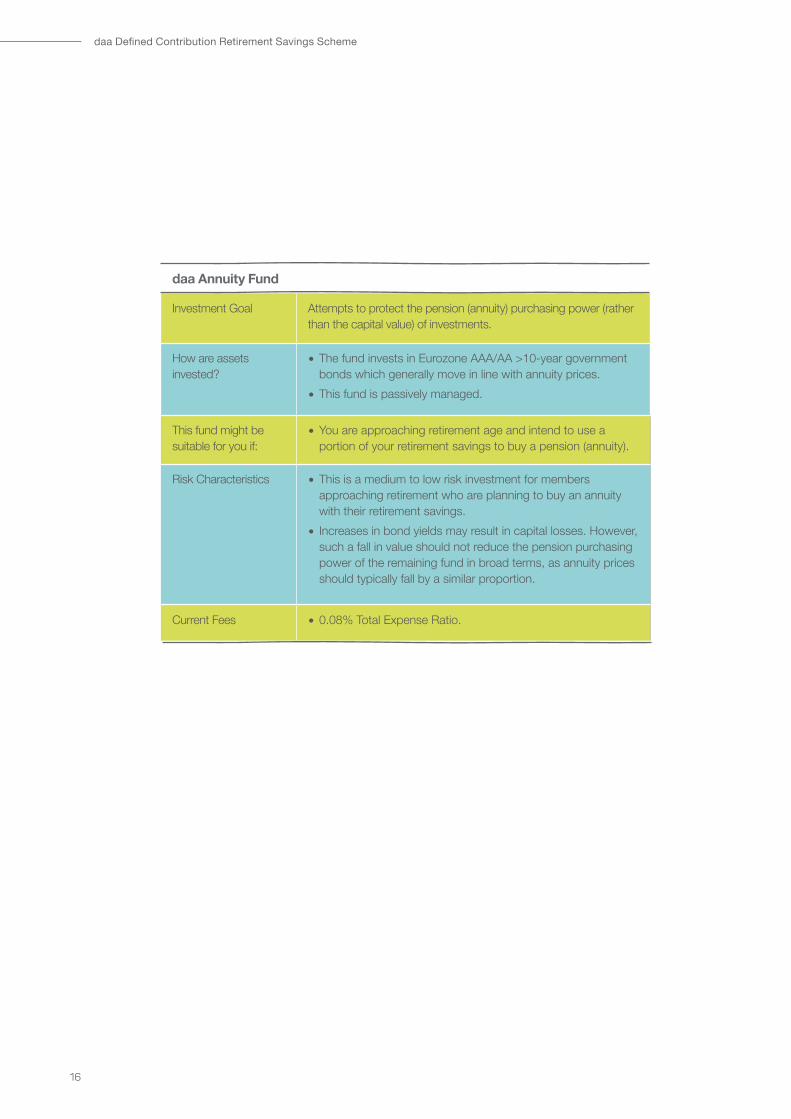

daa Annuity Fund

Investment Goal Attempts to protect the pension (annuity) purchasing power (rather than the capital value) of investments.

How are assets invested?

The fund invests in Eurozone AAA/AA >10-year government bonds which generally move in line with annuity prices.

This fund is passively managed.

This fund might be suitable for you if:

You are approaching retirement age and intend to use a portion of your retirement savings to buy a pension (annuity).

Risk Characteristics This is a medium to low risk investment for members approaching retirement who are planning to buy an annuity with their retirement savings.

Increases in bond yields may result in capital losses. However, such a fall in value should not reduce the pension purchasing power of the remaining fund in broad terms, as annuity prices should typically fall by a similar proportion.

Current Fees 0.08% Total Expense Ratio.

17

Investment Guide

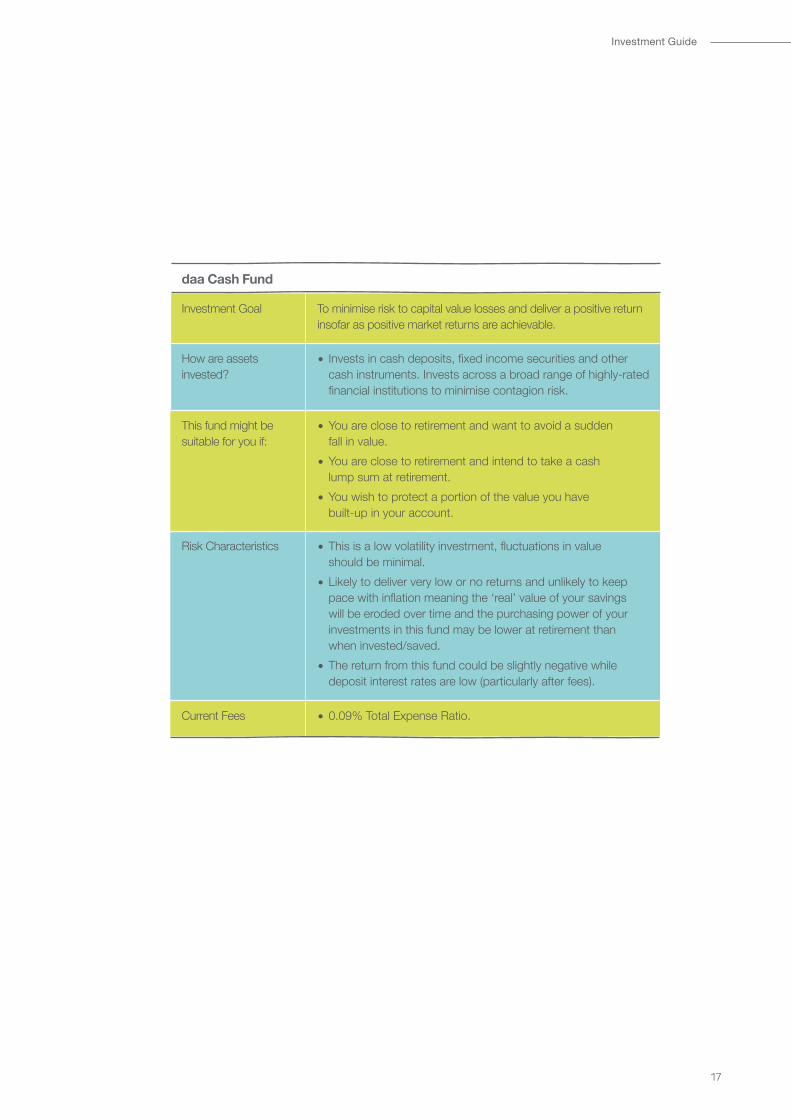

daa Cash Fund

Investment Goal To minimise risk to capital value losses and deliver a positive return insofar as positive market returns are achievable.

How are assets invested?

Invests in cash deposits, fixed income securities and other cash instruments. Invests across a broad range of highly-rated financial institutions to minimise contagion risk.

This fund might be suitable for you if:

You are close to retirement and want to avoid a sudden fall in value.

You are close to retirement and intend to take a cash lump sum at retirement.

You wish to protect a portion of the value you have built-up in your account.

Risk Characteristics This is a low volatility investment, fluctuations in value should be minimal.

Likely to deliver very low or no returns and unlikely to keep pace with inflation meaning the ‘real’ value of your savings will be eroded over time and the purchasing power of your investments in this fund may be lower at retirement than when invested/saved.

The return from this fund could be slightly negative while deposit interest rates are low (particularly after fees).

Current Fees 0.09% Total Expense Ratio.

18

daa Defined Contribution Retirement Savings Scheme

The Lifestyle Strategies are designed to reduce the level of investment risk within your Retirement Savings Account as you approach retirement.

If you choose to have your investments managed for you, at the direction of the Trustee, or do not make any choice as to how your savings are to be invested, your savings will be invested in daa Growth Fund until you are within seven years of retirement, at which stage they will automatically and gradually be moved into lower risk investments in the lead up to retirement. This process of moving to less risky investments over time is called lifestyling and the mix of assets you will have during this period is determined by the “Glidepath” that is selected for you.

The Glidepath you will be directed towards depends on your personal circumstances and your likely use of savings at retirement according to current Revenue rules, based on the information available to the Trustee in relation to your daa retirement savings, e.g. taking a tax-free lump sum, buying an annuity (or pension) or staying invested. In selecting a Glidepath for you, the Trustee will assume that you will choose to maximise your tax-free lump sum at retirement. Under current Revenue rules, the maximum tax-free lump sum that you can take at retirement is the higher of:

25% of the value of your Retirement Savings Account at retirement, with the balance available to purchase an income for life (annuity) or for continued investment i.e. an Approved Retirement Fund (ARF)

Subject to completion of a minimum of 20 years’ service, 150% of your final earnings but the balance must be used to purchase an income for life (annuity).

The current overall maximum retirement lump sum you can receive tax-free from all your retirement savings plans is €200,000.

There will be no change to your investments until seven years before retirement so beginning to think about your retirement choices and the corresponding Glidepaths around eight to ten years before retirement is sufficient.

If at that time, or any time before retirement, you consider that the Glidepath selected for you is not appropriate, you can change to a different Glidepath by contacting the DC Scheme Administrator. This may be particularly relevant if you have other retirement benefits built up from other employment outside of daa. The Glidepath is designed to position your investments for your likely use of them at retirement, but how you actually use them is finally determined only at the point of retirement and can differ from the Glidepath if necessary.

Lifestyle strategies

19

Investment Guide

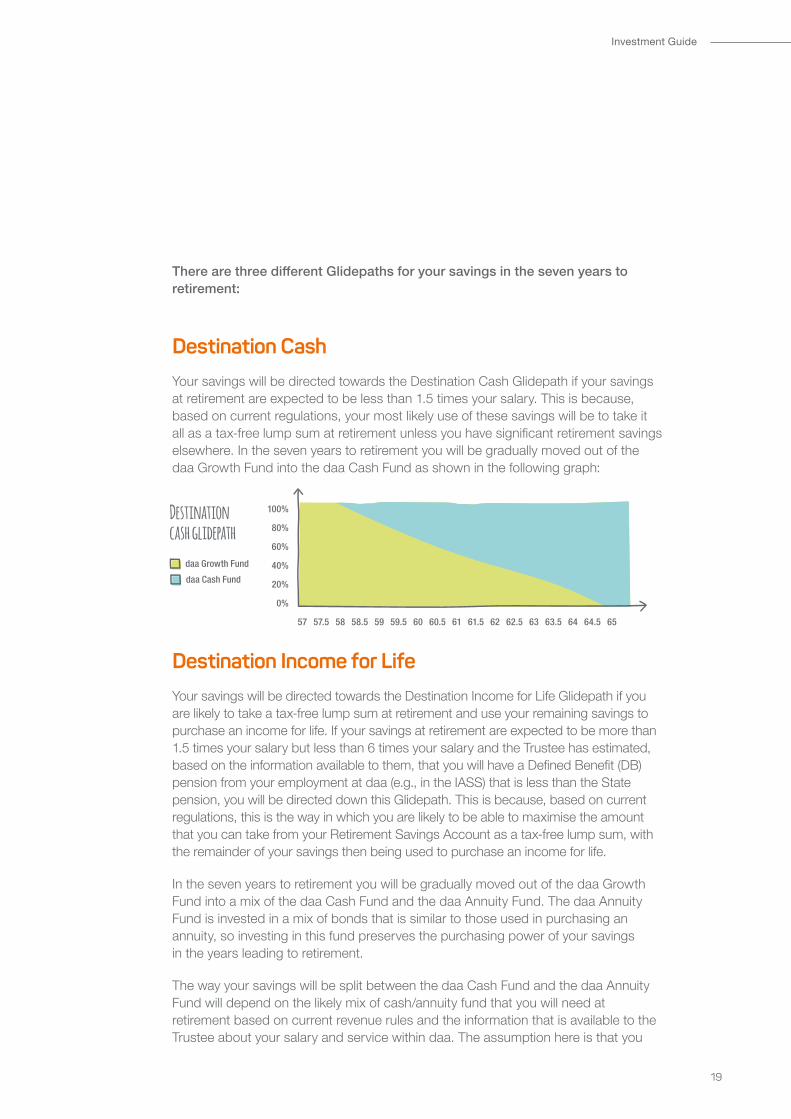

There are three different Glidepaths for your savings in the seven years to retirement:

Destination CashYour savings will be directed towards the Destination Cash Glidepath if your savings at retirement are expected to be less than 1.5 times your salary. This is because, based on current regulations, your most likely use of these savings will be to take it all as a tax-free lump sum at retirement unless you have significant retirement savings elsewhere. In the seven years to retirement you will be gradually moved out of the daa Growth Fund into the daa Cash Fund as shown in the following graph:

Destination cash glidepath

57 57.5 58 58.5 59 59.5 60 60.5 61 61.5 62 62.5 63 63.5 64 64.5 65

daa Growth Fund

daa Cash Fund

100%

80%

60%

40%

20%

0%

Destination Income for LifeYour savings will be directed towards the Destination Income for Life Glidepath if you are likely to take a tax-free lump sum at retirement and use your remaining savings to purchase an income for life. If your savings at retirement are expected to be more than 1.5 times your salary but less than 6 times your salary and the Trustee has estimated, based on the information available to them, that you will have a Defined Benefit (DB) pension from your employment at daa (e.g., in the IASS) that is less than the State pension, you will be directed down this Glidepath. This is because, based on current regulations, this is the way in which you are likely to be able to maximise the amount that you can take from your Retirement Savings Account as a tax-free lump sum, with the remainder of your savings then being used to purchase an income for life.

In the seven years to retirement you will be gradually moved out of the daa Growth Fund into a mix of the daa Cash Fund and the daa Annuity Fund. The daa Annuity Fund is invested in a mix of bonds that is similar to those used in purchasing an annuity, so investing in this fund preserves the purchasing power of your savings in the years leading to retirement.

The way your savings will be split between the daa Cash Fund and the daa Annuity Fund will depend on the likely mix of cash/annuity fund that you will need at retirement based on current revenue rules and the information that is available to the Trustee about your salary and service within daa. The assumption here is that you

20

daa Defined Contribution Retirement Savings Scheme

Destination income for life glidepath (b)

57 57.5 58 58.5 59 59.5 60 60.5 61 61.5 62 62.5 63 63.5 64 64.5 65

daa Growth Fund

daa Cash Funddaa Annuity Fund

100%

80%

60%

40%

20%

0%

Destination income for life glidepath (c)

57 57.5 58 58.5 59 59.5 60 60.5 61 61.5 62 62.5 63 63.5 64 64.5 65

daa Growth Fund

daa Cash Fund

daa Annuity Fund

100%

80%

60%

40%

20%

0%

daa Growth Fund

100%

80%

60%

40%

20%

0%

daa Cash Fund

daa Annuity Fund

57 57.5 58 58.5 59 59.5 60 60.5 61 61.5 62 62.5 63 63.5 64 64.5 65

will aim to maximise your tax-free lump sum, and so this Glidepath aims to ensure you have an adequate amount of your savings in the daa Cash Fund to fund your tax-free lump sum payment.

Within the Destination Income for Life Glidepath there are three ways your savings may be invested at retirement in the Destination Income for Life Glidepath, and the one that is chosen for you will depend on the likely mix of cash and annuity that you are expected to take at retirement:

25% daa Cash Fund and 75% daa Annuity Fund

50% daa Cash Fund and 50% daa Annuity Fund

75% daa Cash Fund and 25% daa Annuity Fund

The following graphs illustrate the three versions of the Destination Income for Life Glidepath:

Destination income for life (a)

21

Investment Guide

Destination Stay InvestedYour savings will be directed down the Destination Stay Invested Glidepath if your expected savings at retirement are greater than 6 times your salary at retirement. You will also be directed down this Glidepath if your expected savings at retirement are greater than 1.5 times your expected salary but less than 6 times your expected salary and your estimated DB pension entitlement relating to your employment at daa is greater than the state pension. This is because, based on current regulations you can take 25% of your savings as a tax-free lump sum, and if your savings are more than 6 times your salary, 25% of your savings will be higher than 1.5 times your salary, which is the alternative way of calculating your maximum tax-free lump sum. In addition, taking 25% of your savings as a lump sum and investing the remainder in an Approved Retirement Fund (ARF) is the manner that gives members the highest degree of flexibility over the use of their savings in retirement. When interest rates are low this is an option that is increasingly favoured by people reaching retirement, especially those with other sources of income in retirement, e.g. a DB pension entitlement.

Approved Retirement Funds (ARFs) are used by those who wish to remain invested post retirement (instead of buying a pension), recognising that there is no guaranteed income for life with this option. In the seven years to retirement, if you are on the Destination Stay Invested Glidepath, you will remain invested in growth funds up to retirement, but the risk profile of the growth fund will be reduced. This is achieved by moving your savings from the daa Growth Fund into a mixture of the daa Cash Fund (for a tax-free lump sum at retirement) and the daa Cautious Growth Fund (which is a lower risk version of the daa Growth Fund, and is therefore similar to the underlying investments in an ARF). At retirement your savings will be invested 25% in the daa Cash Fund and 75% in the daa Cautious Growth Fund as shown in the below graph:

Destination stay investment

57 57.5 58 58.5 59 59.5 60 60.5 61 61.5 62 62.5 63 63.5 64 64.5 65

daa Growth Fund daa Cash Fund daa Cautious Growth Fund

100%

80%

60%

40%

20%

0%

22

daa Defined Contribution Retirement Savings Scheme

Having read through this guide, we hope you are now in a better position to make investment decisions and understand the importance of investing your retirement savings appropriately.

How to select your investment optionsIf you would like to make your own investment choices, you must log in to your online account at www.invescoonline.ie and make your investment selections.

If you would like your investments managed for you, you can select this option by logging in to your online account at www.invescoonline.ie. If you make no selection, your savings will also be automatically managed for you.

Alternatively, you can also complete a paper form, which is available on iConnect, and return this to Invesco, the DC Scheme Administrator.

If you have forgotten how to log in to your online account or need any assistance, please contact Invesco, the DC Scheme Administrator, for whom contact details are provided on page 24.

How can I make changes to my choices?You can make changes to your investment choices any time by logging in to your online account at www.invescoonline.ie.

Making your decision

23

Investment Guide

Glossary

AllocationThis is the way in which investments are split between a number of investment asset classes or investment strategies.

Annual Management Charge

Investment managers charge a fee for their services, often in the form of a percentage of the value of the fund. This is different to the Total Expense Ratio (TER), which is defined below.

AnnuityAn annuity is a life assurance product which, beginning at your retirement, pays you a guaranteed income for the rest of your life.

Approved Retirement Fund (ARF)

A type of investment fund, operated by certain authorised investment institutions, which allows members to retain an element of control over both their investment strategy and ownership of their retirement savings account post-retirement, within certain guidelines and restrictions dictated by the Revenue Commissioners.

Asset ClassType of investment with similar characteristics. Common asset classes include bonds, equities, property, cash etc.

BondA security issued by a government or company that provides regular interest payments and promises the return of the initial capital on a fixed date or dates.

Capital GrowthThis is an increase in the market price of an asset.

DiversificationThe spreading of your retirement savings account across different asset classes.

EquitiesEquities are shares in the value of a company.

GlidepathThe process of gradually moving into lower risk assets in the approach to retirement. Different glidepaths are defined by the desired mix of assets at retirement.

InflationInflation is the rise in the general level of prices of goods and services in an economy over a period of time.

Investment StrategyThis is an approach to investment with its own aims and objectives. Each strategy will invest in a suitable mix of underlying funds to achieve its objective. Particular underlying funds and managers may be changed from time to time by the Trustee.

Lifestyle StrategyThis is an investment strategy that automatically changes the asset classes it invests in, depending on how close the member is to normal retirement age.

Normal Retirement Date

The first anniversary of when you joined the DC Scheme following your 65th birthday.

Retirement Savings Account

The accumulated value of your retirement savings which means the accumulated value, taking into account investment returns/losses and any deductions in respect of investment management charges or levies that the Member is liable for, of:

• the contributions paid by the Employer towards your retirement savings; and

• the contributions you pay including additional voluntary contributions, and

• any amounts transferred to the DC Scheme from a previous pension plan of which you were a member.

Your retirement benefits will depend on the value of your Retirement Savings Account at the time the account is applied to purchase the benefits.

ReturnsThe investment return is the change in the value of the investment over a given time period. Positive returns increase the amount in your retirement savings account. Negative returns will reduce it.

RiskRefers to the potential fall in value of different types of investment.

Total Expense Ratio (TER)

The total costs associated with managing and operating an investment fund. These costs consist primarily of management fees and additional expenses such as trading fees and other operating expenses. These additional expenses can vary over time and are an indication only.

VolatilityHow easily and quickly investments can rise and fall in value. For example, equities can be very volatile because their values can change rapidly and by large amounts.

24

daa Defined Contribution Retirement Savings Scheme

For help logging on, navigating the DC Scheme website or submitting your investment choices, please contact:

Invesco Limited 2 Sandyford Business Centre, Burtonhall Road, Sandyford, Dublin 18 T +353 1 294 7600 | E [email protected] | W www.invescoonline.ie

Who’s who

Further information

Trustee daa Pension Corporate Trustee Limited

Trustee Investment Advisor Acuvest Limited

DC Scheme Administrator Invesco Limited

![DAA MID2 [UandiStar.org]](https://static.documents.pub/doc/80x56/545a7372af7959755d8b5b4b/daa-mid2-uandistarorg.jpg)