29

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | marjorie-watkins |

| View: | 221 times |

| Download: | 2 times |

Investment holdings > 50% = Large holdings The holding company > The subsidiary

To give shareholders

An overview of their investments

An overall financial position and performance of the group

To prepare a group financial statement

As a Single Economic Entity

Transactions between the group companies do not reflect transactions between the external partiesand therefore should be eliminated

Inter company indebtedness e.g. inter company loan debentures proposed dividends

Long term investment of H

Share capital + reserves of S

1. Unrealized Profits from intra-group transactions- on unsold inventories- on fixed assets

Pre-acquisition Reserves- Cost of control- Minority interests

Pre-acquisition Reserves

- Share Premium

- General Reserve

- Revaluation Reserve of subsidiary

Minority interests - Profit and loss account - Balance sheet

Proposed dividend

pay out from Pre-acquisition Profit

- should not be treated as investment income

- It is a reduction in the cost of investment

Proposed dividendPay out from Post-acquisition Profit - investment income

% of holdings: 4000/5000 = 80%

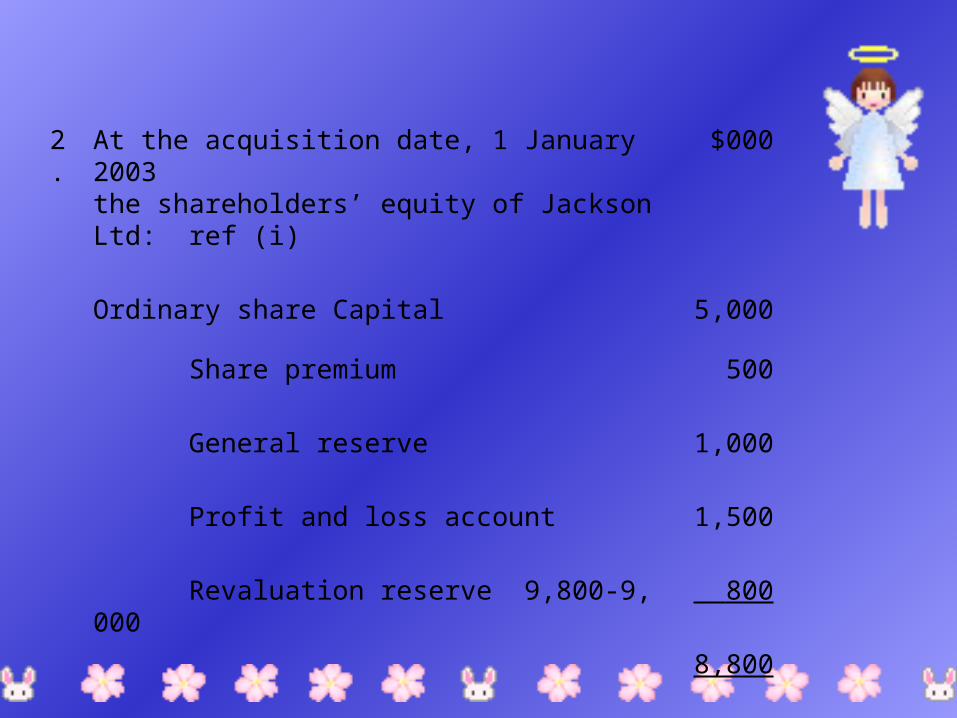

2. At the acquisition date, 1 January 2003the shareholders’ equity of Jackson Ltd: ref (i)

$000

Ordinary share Capital 5,000

Share premium 500

General reserve 1,000

Profit and loss account 1,500

Revaluation reserve 9,800-9,000 800

8,800

3.

Calculation of Goodwill Answer (a)

$000 $000

Investment in Jackson Ltd 7,500

Ordinary share Capital 5,000 x 80% 4,000

Share premium 500 x 80% 400

General reserve 1,000 x 80% 800

Profit and loss account 1,500 x 80% 1,200

Revaluation reserve 800 x 80% 640 7,040

460

4. Goodwill amortization

460 / 5 = 92 ------- Consolidated profit and loss account

460 – 92 = 368 ----- Consolidated Balance Sheet

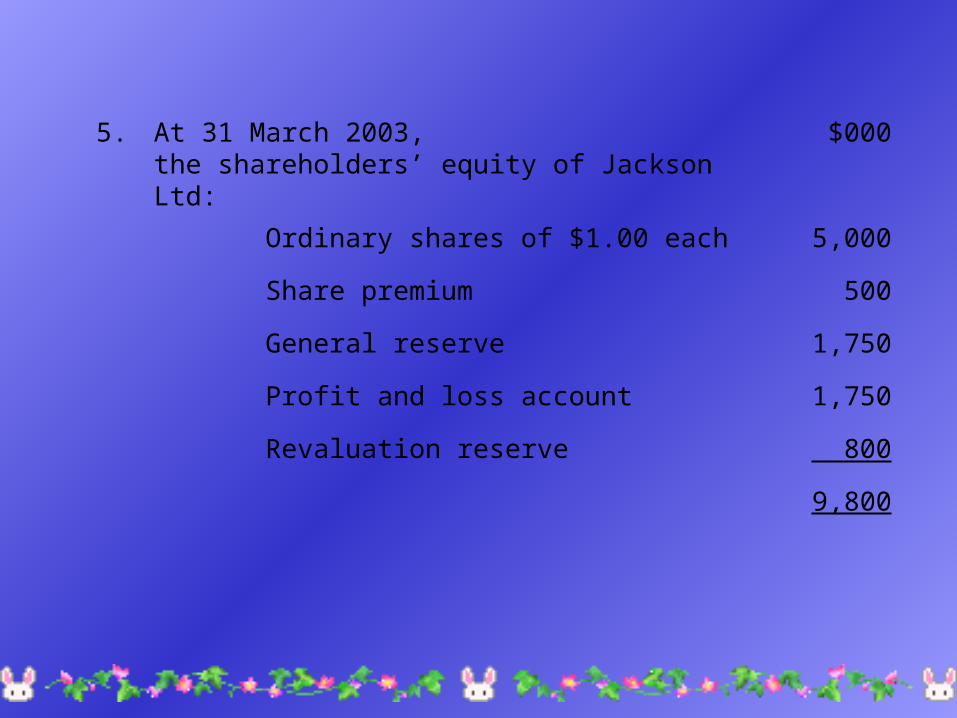

5. At 31 March 2003, the shareholders’ equity of Jackson Ltd:

$000

Ordinary shares of $1.00 each 5,000

Share premium 500

General reserve 1,750

Profit and loss account 1,750

Revaluation reserve 800

9,800

6. Minority interests

Ref: (ii) (3) Depreciation adjustment

(iv) Unrealized profit on inventories

$000 $000

Ordinary shares of $1.00 each 5,000 x 20% 1,000

Share premium 500 x 20% 100

General reserve 1,750 x 20% 350

Profit and loss account 1,750 x 20% 350

Revaluation reserve 800 x 20% 160 1,960

To share unrealized profit on inventories 160

Transfer to consolidated balance sheet 1,800

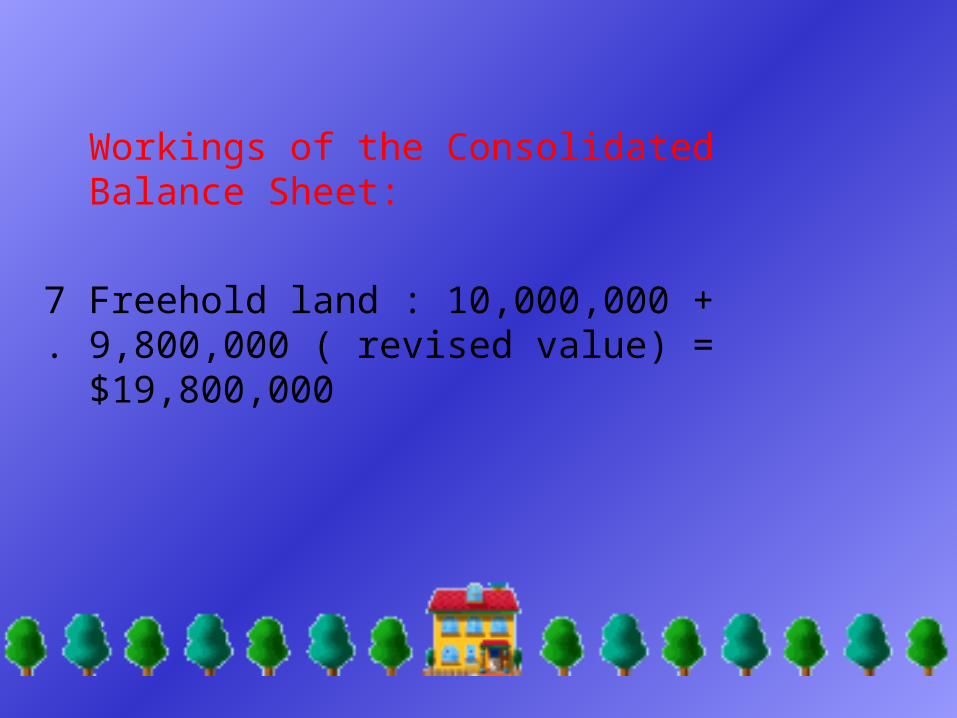

Workings of the Consolidated Balance Sheet:

7.

Freehold land : 10,000,000 + 9,800,000 ( revised value) = $19,800,000

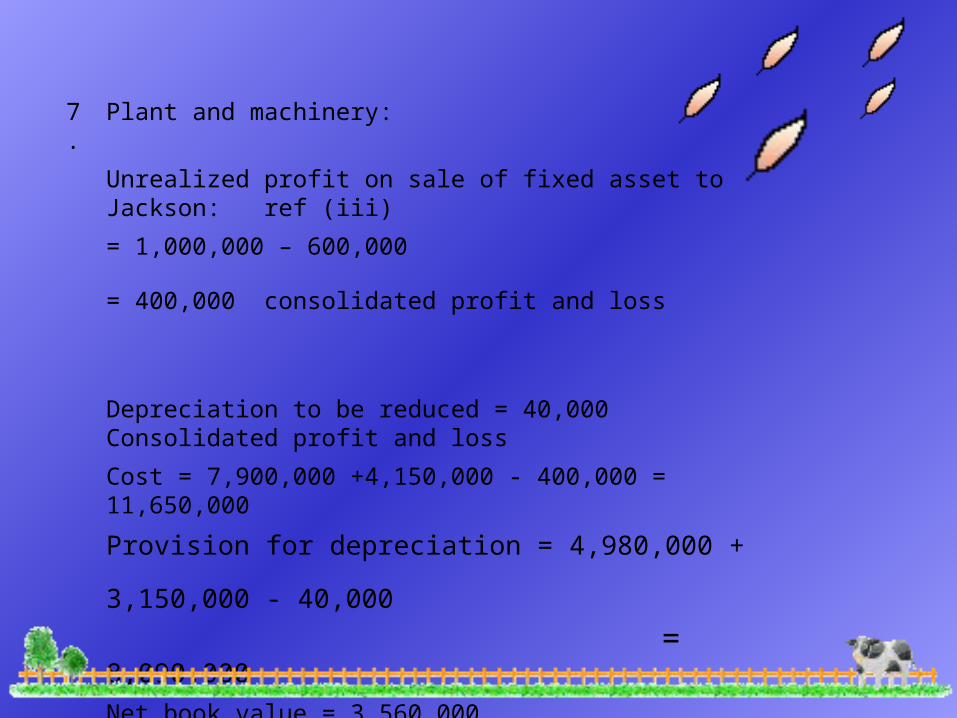

7. Plant and machinery:

Unrealized profit on sale of fixed asset to Jackson: ref (iii)

= 1,000,000 – 600,000

= 400,000 consolidated profit and loss

Depreciation to be reduced = 40,000 Consolidated profit and loss

Cost = 7,900,000 +4,150,000 - 400,000 = 11,650,000

Provision for depreciation = 4,980,000 + 3,150,000 - 40,000 = 8,090,000

Net book value = 3,560,000

8. Shareholders’ Fund: $000

Ordinary shares of $1.00 each 15,000

Share premium 3,000

General reserve 1,400 + (1750-1000) x 80% 2,000

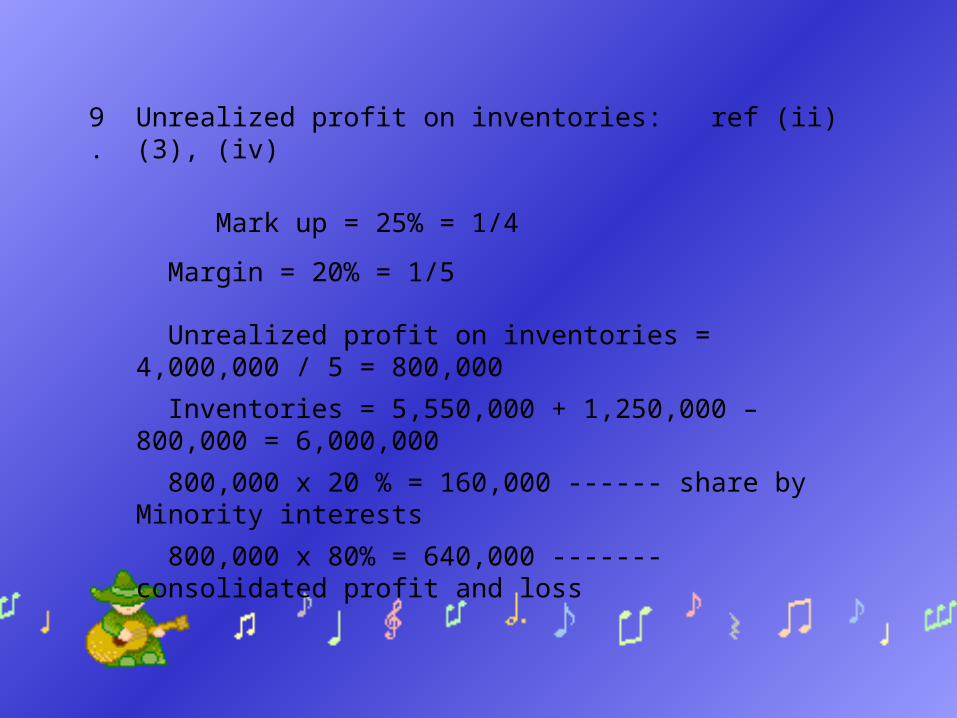

9. Unrealized profit on inventories: ref (ii)(3), (iv)

Mark up = 25% = 1/4

Margin = 20% = 1/5

Unrealized profit on inventories = 4,000,000 / 5 = 800,000

Inventories = 5,550,000 + 1,250,000 – 800,000 = 6,000,000

800,000 x 20 % = 160,000 ------ share by Minority interests

800,000 x 80% = 640,000 ------- consolidated profit and loss

10.

Intra-group indebtedness: ref: (v), (ii) (4),

Accounts receivable: 1,500,000 +750,000 -500,000 = 1,750,000

Accounts payable: 3,050 – 500 + 1,600 = 4,150

Dividend payable: 750

Dividend payable to Minority interests = 500 x 20% = 100,000

11.

Bank: 1,450,000 + 100,000 = 1,550,000

Tax payable: 1,200,000 + 1,000,000 = 2,200,000

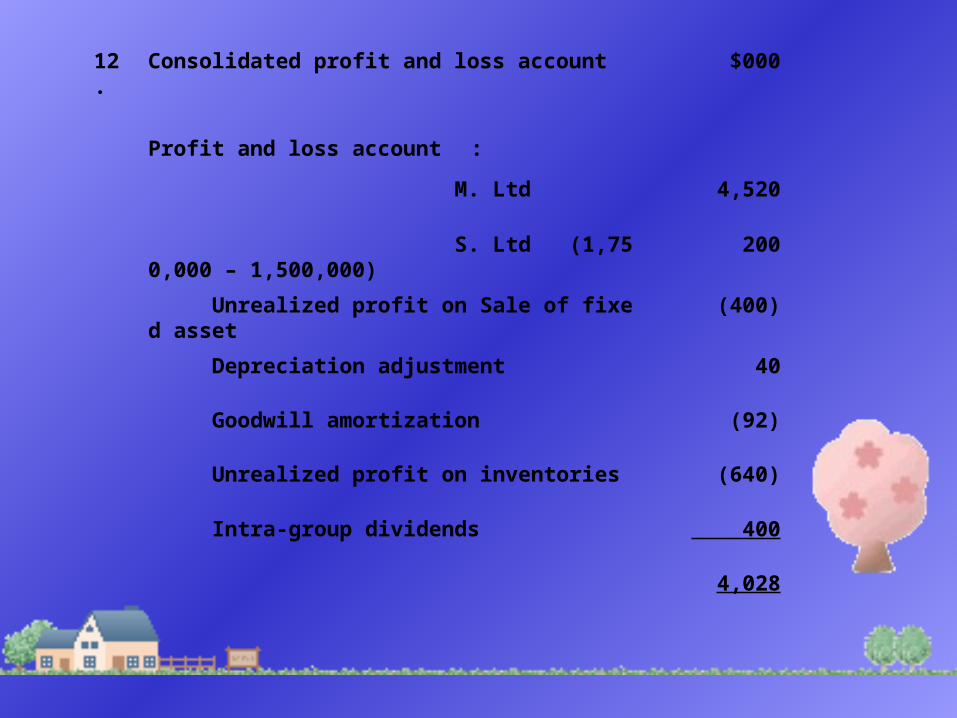

12. Consolidated profit and loss account $000

Profit and loss account :

M. Ltd 4,520

S. Ltd (1,750,000 – 1,500,000) 200

Unrealized profit on Sale of fixed asset (400)

Depreciation adjustment 40

Goodwill amortization (92)

Unrealized profit on inventories (640)

Intra-group dividends 400

4,028

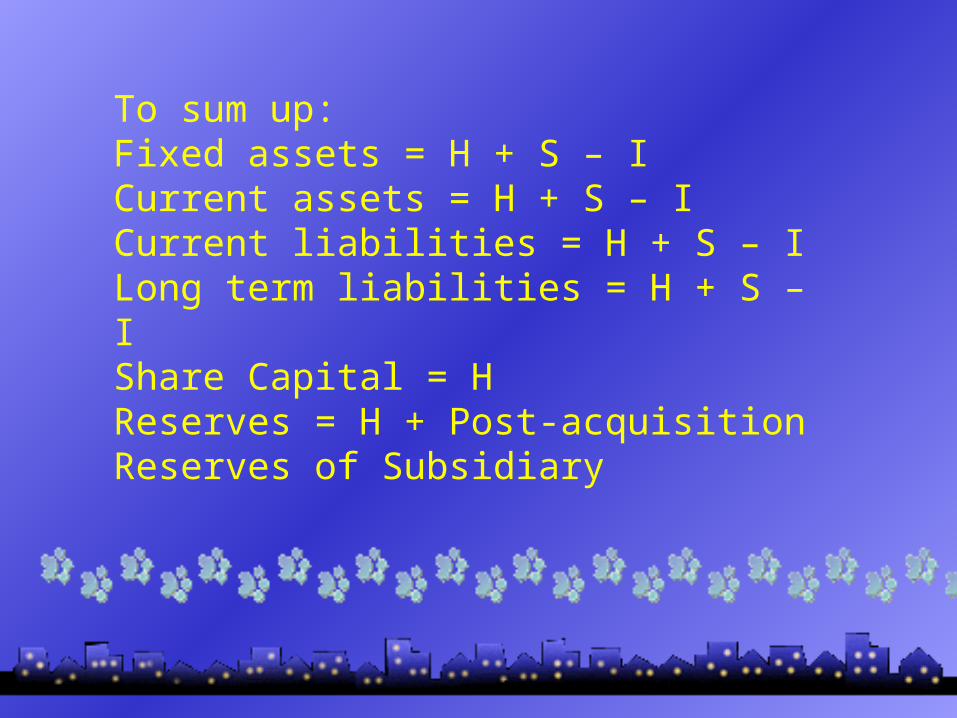

To sum up:Fixed assets = H + S – ICurrent assets = H + S – ICurrent liabilities = H + S – ILong term liabilities = H + S – IShare Capital = HReserves = H + Post-acquisition Reserves of Subsidiary