28

setting up an investment fund in luxembourg investment management

setting up an investment fund in luxembourg

investment management

3

table of contents

Definitions 5

I. Legal framework for setting up an investment fund in Luxembourg 6

II. Investment funds subject to the 2002 Law 7

III. Specialised investment funds (“SIFs”) 12

IV. Available structures 14 1. FCP - SICAV - SICAF 14 2. Umbrella funds/share classes 15 3. Main features of the different company forms 16

V Main players 18 1. The management company 18 2. The custodian bank 19 3. The central administration agent 20 4. The auditor 20

VI. Regulatory supervision 21

VII. Taxation 22

VIII. Once-off and ongoing costs at a glance 24

3

definitions

1993 Law Law of 5 April 1993 on the financial sector, as amended

2002 Law Law of 20 December 2002 on undertakings for collective investment, as amended

2007 Law Law of 13 February 2007 on specialised investment funds, as amended

UCITS Directive Council directive 85/611/EEC of 20 December 1985 on the coordination of laws, regulations and administrative

provisions relating to undertakings for collective investment in transferable securities (UCITS), as amended

EU Savings Directive Council directive 2003/48/EC on taxation of savings in the form of interest payments

MiFID Directive Directive 2004/39/EC of the European Parliament and of the Council of 21 April 2004 on markets in financial

instruments

Grand Ducal Regulation on eligible assets

Grand Ducal Regulation of 8 February 2008 relating to certain definitions of the law of 20 December 2002,

as amended, concerning undertakings for collective investment and implementing directive 2007/16/EC of

the European Commission implementing Council directive 85/611/EEC on the coordination of laws,

regulations and administrative provisions relating to undertakings for collective investment in transferable

securities (UCITS) as regards the clarification of certain definitions

Circular 91/75 CSSF circular 91/75 of 21 January 1991 on the revision and remodelling of the rules to which Luxembourg

undertakings governed by the law of 30 March 1988 on undertakings for collective investment (“UCIs”) are subject1

Circular 02/80 CSSF circular 02/80 of 5 December 2002 concerning the specific rules applicable to Luxembourg

undertakings for collective investment (UCIs) pursuing alternative investment strategies

Circular 02/81 CSSF circular 02/81 of 6 December 2002 concerning the task of auditors of undertakings for collective investment

Circular 03/88 CSSF circular 03/88 of 22 January 2003 concerning the classification of undertakings for collective investment

subject to the provisions of the law of 20 December 2002 relating to undertakings for collective investment

Circular 05/186 CSSF circular 05/186 of 25 May 2005 concerning Luxembourg management companies subject to the

provisions of chapter 13 of the law of 20 December 2002 relating to undertakings for collective investment,

as well as self-managed investment companies subject to the provisions of article 27 or article 40 of the law

of 20 December 2002 relating to undertakings for collective investment

1 The title of this circular has not been amended in order to take into account the fact that the law of 30 March 1988 has been replaced by the 2002 Law.

5

Circular 07/308 CSSF circular 07/308 of 2 August 2007 concerning the rules of conduct to be adopted by undertakings for

collective investment in transferable securities with respect to the use of a method for the management of

financial risks, as well as the use of financial derivative instruments

Circular 07/309 CSSF circular 07/309 of 3 August 2007 concerning risk diversification in relation to specialised investment funds

Circular 08/356 CSSF circular 08/356 of 4 June 2008 concerning the rules applicable to undertakings for collective investment when

they employ certain techniques and instruments relating to transferable securities and money market instruments

CSSF Commission de Surveillance du Secteur Financier (the Luxembourg supervisory authority of the financial sector)

EEA European Economic Area

EU European Union

FCP Fonds Commun de Placement (common fund)

OECD Organisation for Economic Cooperation and Development

Mémorial The official gazette of Luxembourg, Mémorial C, Journal Officiel du Grand-Duché de Luxembourg, Recueil des

Sociétés et Associations

SICAV Société d’investissement à capital variable (investment company with variable capital)

SICAF Société d’investissement à capital fixe (investment company with fixed capital)

SIF Specialised investment fund, subject to the 2007 Law

TA Transfer agent

UCI Undertaking for collective investment, subject to Part II of the 2002 Law

UCITS Undertaking for collective investment in transferable securities, subject to Part I of the 2002 Law

I. legal framework for setting up an investment fund in luxembourg

6

2002 LAW PART I (UCITS) or PART II (UCIs)

2007 LAW (SIFs)

Criteria to be

cumulatively met

in order to be subject

to the 2002 Law

or the 2007 Law

The savings must be invested on a

collective basis;

The savings used for collective

investment must have been

collected from the public;

The investment which forms the

object of the collective investment

must be made in accordance with

the principle of risk spreading.

The assets must be invested on a

collective basis in order to spread

the investment risks and to ensure

that the investors receive the benefit

of the results of the management of

the assets;

The securities of the SIF must be

reserved to one or more

well-informed investors;

The constitutional documents or

offering documents must provide

that the SIF is subject to the 2007 Law.

II. investment funds subject to the 2002 law

7

Key features2

Eligible assets and general investment restrictions

Part I (UCITS) Part II (UCIs)

Part I funds invest in transferable securities and

other liquid financial assets authorised by the

UCITS Directive. They qualify as UCITS and, as

such, benefit from the European passport.

In order to qualify as a UCITS, the following criteria

need to be met:

The sole object must be the collective investment in

transferable securities and/or in other liquid

financial assets authorised by the UCITS Directive;

The UCITS must be open to the public of the EEA;

The UCITS must redeem the units at the request

of the investors;

The UCITS must not be excluded from the UCITS

status by reason of its investment or borrowing

policy.

Part II funds may invest in securities other than

those authorised by the UCITS Directive, but they

do not benefit from the European passport, since

they are outside the scope of the UCITS Directive.

Part II of the 2002 Law applies to:

All funds, the principal object of which is the

investment in securities other than transferable

securities and other liquid financial assets;

All UCITS excluded from Part I of the 2002 Law, i.e.:

UCITS of the closed-ended type;

UCITS which raise capital without promoting

the sale of their units or shares to the public

within the EU or any part of it;

UCITS, the units or shares of which may, under

their constitutional documents, only be sold to

the public in countries which are not members

of the EEA;

Specific categories of UCIs which, in light of

their investment and borrowing policies, must

be subject to Part II of the 2002 Law.

Part I (UCITS) Part II (UCIs)

Article 41 of the 2002 Law sets out the list of

eligible assets;

The Grand Ducal Regulation on eligible assets

clarifies a certain number of definitions

contained in the 2002 Law;

Article 41 (1) of the 2002 Law:

1. Transferable securities and money market

instruments admitted to or dealt in on a

regulated market;

2. Transferable securities and money market

instruments dealt in on another market in a

Member State of the EU which is regulated,

operates regularly and is recognised and open

to the public;

Part II of the 2002 Law does not contain a defined

list of eligible assets and there are no restrictions

with respect to investment strategies that may be

used by UCIs;

Thus, there is a larger flexibility regarding the

investments which may be undertaken by UCIs;

Circular 91/75 sets out general rules applicable to

all UCIs and specific investment rules applicable

to UCIs investing in options and futures, venture

capital UCIs and real estate UCIs;

2 Circular 03/88 highlights the classification of investment funds subject to either Part I or Part II of the 2002 Law.

8

Part I (UCITS) Part II (UCIs)

3. Transferable securities and money market instru-

ments admitted to official listing on a stock exchange

in a non-member state of the EU or dealt in on another

market in a non-member state of the EU which is

regulated, operates regularly and is recognised

and open to the public, provided that the choice of

the stock exchange or market has been provided

for in the constitutional documents of the UCITS;

4. Recently issued transferable securities and

money market instruments, provided that:

The terms of issue include an undertaking that

application will be made for admission to official

listing on a stock exchange or on another regulated

market as described under (1)-(3) above;

Such admission is secured within one year of issue.

5. Units of UCITS and/or other UCIs within the

meaning of the first and second indents of article 1(2)

of the UCITS Directive, whether situated in an EU

member state or in another state, provided that:

Such other UCIs are authorised under laws which

provide that they are subject to supervision

considered by the CSSF to be equivalent to that

laid down in Community law, and that ooperation

between authorities is sufficiently ensured;

The level of protection for unitholders in such

other UCIs is equivalent to that provided for

unitholders in a UCITS, and in particular that the

rules on assets segregation, borrowing, lending,

and uncovered sales of transferable securities

and money market instruments are equivalent to

the requirements of the UCITS Directive;

The business of the other UCIs is reported in

half-yearly and annual reports to enable an

assessment of the assets and liabilities, income

and operations over the reporting period;

No more than 10% of the assets of the UCITS

or of the other UCIs, the acquisition of which

is contemplated, can, according to their

constitutional documents, in the aggregate be

invested in units of other UCITS or other UCIs.

Investment limits applicable to UCIs investing in

transferable securities which do not represent

investments in real estate or venture capital are

the following:

No more than 10% of the net assets may be

invested in securities not listed on a stock

exchange or dealt in on another regulated

market which operates regularly and is

recognised and open to the public;

No more than 10% of the securities of the same

kind issued by the same issuing body may be

acquired; and

No more than 10% of the net assets may be

invested in securities issued by the same

issuing body.

These restrictions are not applicable to securities

issued or guaranteed by a member state of the OECD

or their local authorities or a public international body

with an EU, regional or worldwide scope.

Units/shares of closed-ended investment funds

are treated in the same way as other transferable

securities and are therefore subject to the general

rules applicable to transferable securities.

UCIs may borrow up to 25% of their net assets

(except leveraged UCIs where the investment policy

provides for a permanent borrowing for investment

purposes of at least 25% of their net assets);

Derogations to Circular 91/75 may be granted

on a case-by-case basis;

6. Deposits with credit institutions which are repayable

on demand or have the right to be withdrawn, and

which mature in no more than 12 months, provided

that the credit institution has its registered office in a

member state of the EU or, if the registered office of

the credit institution is situated in a non-member

state, provided that it is subject to prudential rules

considered by the CSSF to be equivalent to those

laid down in Community law;

9

Part I (UCITS) Part II (UCIs)

7. Financial derivative instruments, including

equivalent cash-settled instruments, dealt in on a

regulated market referred to in (1), (2) and (3) above,

and / or financial derivative instruments dealt in over

the counter (“OTC derivatives”), provided that:

The underlying consists of instruments covered

by article 41 (1) of the 2002 Law, financial

indices, interest rates, foreign exchange rates

or currencies, in which the UCITS may invest

according to its investment objectives;

The counterparties to OTC derivative

transactions are institutions subject to

prudential supervision, and belonging to the

categories approved by the CSSF; and

The OTC derivatives are subject to reliable and

verifiable valuation on a daily basis and can be

sold, liquidated or closed by an offsetting

transaction at any time at their fair value at the

UCITS’ initiative.

8. Money market instruments other than those dealt in

on a regulated market, to the extent that the issue or

the issuer of such instruments is itself regulated for

the purpose of protecting investors and savings, and

provided that such instruments are:

Issued or guaranteed by a central, regional or

local authority or by a central bank of an EU

member state, the European Central Bank, the EU

or the European Investment Bank, a non-member

state of the EU or, in case of a federal state, by one

of the members making up the federation, or by a

public international body to which one or more EU

member states belong, or

Issued by an undertaking any securities of

which are dealt in on regulated markets

referred to in (1), (2) or (3) above, or

Issued or guaranteed by an establishment

subject to prudential supervision, in

accordance with criteria defined by Community

law, or by an establishment which is subject to

and complies with prudential rules considered

by the CSSF to be at least as stringent as those

laid down by Community law; or

Specific rules regarding UCIs pursuing

alternative investment strategies (hedge funds

and funds of hedge funds) are set out in Circular

02/80 and consist, in particular, of:

Risk-diversification rules regarding short sales;

Restrictions applicable to target UCIs;

Restrictions relating to financial derivative

instruments;

Provisions applicable to securities lending

transactions; and

Provisions applicable to sale with right of

repurchase transactions and repurchase

transactions.

Issued by other bodies belonging to the

categories approved by the CSSF provided that

investments in such instruments are subject to

investor protection equivalent to that laid down in

the first, second or third indent and provided that

the issuer is a company whose capital and

reserves amount to at least EUR 10 million and

10

Part I (UCITS) Part II (UCIs)

which presents and publishes its annual accounts in

accordance with directive 78/660/EEC, is an entity

which, within a group of companies which includes

one or several listed companies, is dedicated to the

financing of the group or is an entity which is

dedicated to the financing of securitisation vehicles

which benefit from a banking liquidity line.

Article 41 (2) of the 2002 Law:

Transferable securities and money market

instruments not fulfilling the requirements of (1)–(8)

above also constitute eligible assets, provided that

they do not in the aggregate exceed 10% of the

assets of the UCITS.

Article 41 (3) of the 2002 Law:

A UCITS may hold ancillary liquid assets.

Circular 08/356 clarifies the rules applicable to

UCIs when they employ certain techniques and

instruments relating to transferable securities

and money market instruments:

Securities lending transactions

- UCITS may lend directly to a borrower or

through a standardised lending system

(organised by a recognised clearing institution

or organised by a financial institution subject

to equivalent prudential supervision rules);

- The counterparty must be subject to

equivalent prudential supervision;

- The UCITS must receive a guarantee the value

of which is at least equivalent to 90% of the

global valuation of the securities lent;

- The volume of securities lending transactions

must be kept at an appropriate level;

- Disclosure of the global valuation of the securities

lent must be made in the financial reports;

Circular 08/356 clarifies the rules applicable to

UCIs when they employ certain techniques and

instruments relating to transferable securities

and money market instruments:

Securities lending transactions;

- UCIs may lend directly to a borrower or

through a standardised lending system

(organised by a recognised clearing institution

or organised by a financial institution subject

to equivalent prudential supervision rules);

- The counterparty must be subject to

equivalent prudential supervision;

- The UCIs must receive a guarantee the value

of which is at least equivalent to 90% of the

global valuation of the securities lent;

- The volume of securities lending transactions

must be kept at an appropriate level;

- Disclosure of the global valuation of the securities

lent must be made in the financial reports;

Sale with right of repurchase transactions

The purchase or sale of securities with a

repurchase option is allowed (i) if the

counterparties are subject to equivalent prudential

supervision, (ii) if disclosure of the total amount

of the open transactions is made in the financial

reports and (iii) subject to the limits set out in

Circular 08/356.

Sale with right of repurchase transactions.

The purchase or sale of securities with a

repurchase option is allowed (i) if the

counterparties are subject to equivalent prudential

supervision, (ii) if disclosure of the total amount

of the open transactions is made in the financial

reports and (iii) subject to the limits set out in

Circular 08/356.

11

Part I (UCITS) Part II (UCIs)

- Reverse repurchase and repurchase agreement

transactions

Reverse repurchase agreement transactions or

repurchase agreement transactions are allowed

(i) if the counterparties are subject to equivalent

prudential supervision, (ii) if disclosure of the

total amount of the open transactions is made in

the financial reports and (iii) subject to the limits

set out in Circular 08/356.

- Limitation of the counterparty risk

The risk exposure to a single counterparty

arising from one or more securities lending

transactions, sale with right of repurchase

transactions and/or reverse repurchase/

repurchase transactions may not exceed 10% of

its assets when the counterparty is a credit

institution referred to in article 41, paragraph (1)

(f) of the 2002 law or 5% of its assets in other

cases. The conditions and form of the guarantee

and the possibilities to reduce the counterparty

risk are detailed in Circular 08/356.

- The cash provided as a guarantee may be

reinvested, under the conditions set out in

Circular 08/356.

- Reverse repurchase and repurchase agreement

transactions

Reverse repurchase agreement transactions or

repurchase agreement transactions are allowed

(i) if the counterparties are subject to equivalent

prudential supervision, (ii) if disclosure of the

total amount of the open transactions is made in

the financial reports and (iii) subject to the limits

set out in Circular 08/356.

- Limitation of the counterparty risk

The risk exposure to a single counterparty arising

from one or more securities lending transactions,

sale with right of repurchase transactions and / or

reverse repurchase / repurchase transactions

may not exceed 10% of its assets when the

counterparty is a credit institution referred to in

article 41, paragraph (1) (f) of the 2002 law or 5%

of its assets in other cases. The conditions and

form of the guarantee and the possibilities to

reduce the counterparty risk are detailed in

Circular 08/356.

- The cash provided as a guarantee may be

reinvested, under the conditions set out in

Circular 08/356.

12

Key features of the 2007 Law

Large eligibleinvestor base

No promoter5

requirement

No limitation regardingeligible assets andlow risk diversification

The regime implemented by the 2007 Law is a “stand-alone” regime providing an appropriate statutory regime for “sophisticated” investors, who do not need the same level of protection as retail investors.

The 2007 Law is largely based on the 2002 Law, but provides (i) a more flexible framework to accommodate various types of funds, in particular hedge funds, real estate funds and private equity funds, and (ii) a lighterprudential regime than that applicable to funds dedicated to retail investors.

III. specialised investment funds (“SIFs”)

3 There does not exist any legal definition of the term “institutional investor”. According to CSSF interpretation and parliamentary documents relating to laws using this concept, the main characteristic any institutional investor must exhibit is to have a business purpose that requires the management of substantial assets. Insurance companies, social security institutions, credit institutions, UCIs, local authorities, unregulated investment companies (such as, for example, holding companies) under certain conditions, commercial companies with substantial assets under management, pension funds or other professionals of the financial sector are considered to be institutional investors. Credit institutions and other professionals of the financial sector investing in institutional funds in their own name but on behalf of another party on the basis of a discretionary management relationship are also considered as institutional investors, even if the third party on behalf of which the investment is undertaken is not itself an institutional investor.

4 According to Annex II of MiFID, a professional client is a client who possesses the experience, knowledge and expertise to make its own investment decisions and properly assess the risks that it incurs.

5 The term “promoter” does not appear in Luxembourg law, but is used by the CSSF as an administrative practice. As a general rule, any UCI (except SIFs) must be promoted by a well known institution which commits its name and reputation to the proper functioning of the UCI. The promoter designates the entity under the initiative of which a UCI is created. The promoter’s responsibility is i.a. to make good all damage caused by managerial and administrative faults, negligence, irregularities or shortcomings in the management and administration of the UCI.

SIFs are reserved to well-informed investors.

A well-informed investor is an institutional investor3, professional investor4

or any other investor who meets the following conditions:

- He has confirmed in writing that he adheres to the status of

well-informed investor; and

- (i) He invests a minimum of EUR 125,000.- in the SIF; or

- (ii) He has been the subject of an assessment made by a credit

institution within the meaning of directive 2006/48/EC, by an

investment firm within the meaning of directive 2004/39/EC or by a

management company within the meaning of directive 2001/107/EC

certifying his expertise, his experience and his knowledge in

adequately appraising an investment in the SIF.

In practice, this means that sophisticated retail or private investors may

invest in a SIF.

The 2007 Law does not contain any provisions regarding eligible assets;

thus, a SIF may invest in a very broad range of eligible assets. Although

risk spreading must be ensured, the 2007 Law does not foresee any risk

diversification rules. As a general principle, lower risk diversification is

possible, since SIFs are reserved to sophisticated investors.

Circular 07/309 provides that as a general rule, a SIF may not invest

more than 30% of its assets or commitments in securities of the same

type, issued by the same issuer. However, derogations may be granted

in this respect.

There is no requirement with respect to the necessity to have an institutional

promoter with significant financial resources approved by the CSSF.

13

Key features of the 2007 Law

Investment manager The CSSF does not scrutinise the experience and reputation of the

investment manager.

Regulatory approval The SIF may start its activities before having received regulatory

approval. The application for approval must be filed with the CSSF within

the month following the creation of the SIF.

Capital requirement The minimum capitalisation amounts to EUR 1,250,000 and must be

achieved only within a 12-month period after approval of the SIF.

Issue of units/shares There is the possibility to issue partly paid units or shares both in an FCP

and a SICAV or SICAF. The issue and redemption prices of units or

shares do not have to be based on the net asset value.

Light reporting requirements

Only an annual report must be produced. There is no requirement to

publish neither a semi-annual report nor a long form report.

Issuing document There is no requirement regarding the minimum content of the issuing

document or other offering documents. The issuing document must

include the information necessary for investors to be able to make an

informed judgment of the investment proposed to them and in particular

of the risks attached thereto.

No consolidation requirements

When investments are made through a subsidiary, there are no

consolidation requirements with respect to the accounts.

14

1. FCP - SICAV - SICAF

IV. available structures

Both the 2002 Law and the 2007 Law permit the creation of funds as stand-alone funds or as umbrella funds with different sub-funds (see section “Umbrella Funds” hereafter).

The 2002 Law and the 2007 Law permit the creation of FCPs and investment companies. The latter may be established either as SICAVs or as SICAFs.

FCP SICAV SICAF

Legal form of vehicle

Contractual vehicle. Corporate vehicle. Corporate vehicle.

Key features - Undivided co-ownership of

assets;

- Has no legal personality;

- Very flexible vehicle,

because it is not subject to

any specific corporate law

requirements.

- Variable share capital

equal to the net assets;

- Has a legal personality;

- No need to formally

increase or reduce the

share capital.

- Fixed share capital;

- Has a legal personality;

- Formal decision to increase

or reduce the share capital is

necessary; such decision is

subject to specific corporate

law requirements.

Management Managed by a management

company either subject to

Chapter 13 or Chapter 14 of

the 2002 Law.

Depending on legal form,

managed by a board of

directors, manager(s),

general partner(s) or a

board of managers.

Depending on legal form,

managed by a board of

directors, manager(s),

general partner(s) or a

board of managers.

Shareholders/ - One or several unitholders;

- Liability of unitholders

limited to the amount

committed to the FCP;

- Possibility to be protected

from hostile takeovers,

since investors usually do

not have voting rights;

- Voting rights may however

be granted in respect of

certain matters or a

committee of investors can

be established.

- One or several shareholders;

- Liability of shareholders in

principle limited to the

amount committed to the

SICAV;

- Shares entitle shareholders

to voting rights.

- One or several shareholders;

- Liability of shareholders in

principle limited to the

amount committed to the

SICAV;

- Shares entitle shareholders

to voting rights.

Paid-in capital

Partly paid units may be

issued.

2002 Law:

Shares must be fully paid.

2007 Law:

Partly paid shares may be

issued.

2002 Law

and 2007 Law:

Partly paid shares may be

issued.

Unitholders

15

2. Umbrella funds / share classes

where each sub-fund corresponds to a distinct portfolio of assets and liabilities of the fund.

The 2002 Law and the 2007 Law permit the creation of funds as stand-alone funds or as umbrella funds with different sub-funds,

FCP SICAV SICAF

Preferredcompany forms

N/A 2002 Law (Part I and Part II):

- Public limited company

(Société anonyme, S.A.).

2002 Law (Part I):

- Public limited company

(Société anonyme, S.A.);

- Corporate partnership limited

by shares (Société en

commandite par actions, S.C.A.).

2007 Law:

- Public limited company

(Société anonyme, S.A.);

- Private limited company (Société à

responsabilité limitée, S.à r.l.);

- Corporate partnership limited by

shares (Société en commandite

par actions, S.C.A.).

2002 Law (Part I and Part II):

- Public limited company

(Société anonyme, S.A.);

- Corporate partnership limited by

shares (Société en commandite

par actions, S.C.A.);

- Private limited company (Société

à responsabilité limitée, S.à r.l.);

- Limited partnership (Société en

commandite simple, S.C.S.).

Applicable provisions

- Permitted under Article 133 of the 2002 Law (constitutional documents must provide for

the possibility);

- Permitted under Article 71 of the 2007 Law (constitutional documents must provide for the

possibility).

For funds subject to the 2002 Law, Chapter J of Circular 91/75 sets out the conditions

applicable to FCPs and investment companies in the form of umbrella funds. For SIFs,

article 71 of the 2007 Law sets out the conditions applicable to umbrella funds.

Objectives May accommodate various needs, such as for example:

- Different investment policies; - Different reference currencies;

- Different categories of investors; - Different distribution channels.

One single entity

A UCITS may not comprise simultaneously sub-funds governed by Part I and Part II of the

2002 Law (in such case, the entire umbrella fund is subject to Part II).

Ring fencing Each sub-fund is only responsible for its own debts, commitments and other obligations,

unless the constitutional documents of the fund provide otherwise.

Conversion In principle, possibility to convert shares/units from one sub-fund to another.

Cross- investment

At present, no cross-investments between sub-funds of the same fund are allowed.

16

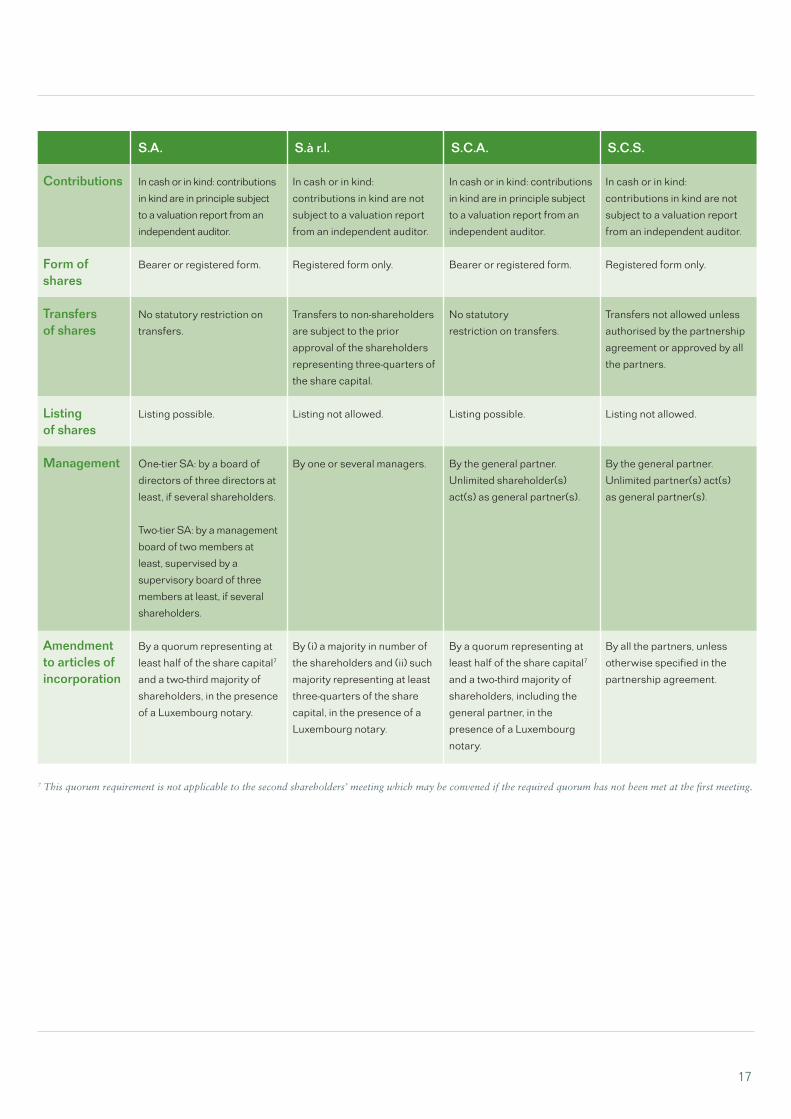

3. Main features of the different company forms

Investors targeted (either retail, professional or institutional investors, investors of a different nationality, etc).

Structure of fees (different fee structures may be accommodated, such as e.g. in relation to the subscription fee, redemption fee, conver-sion fee, deferred sales charge, distribution fee, management fee, etc).

Currency hedging (hedged classes or not). Minimum subscription and holding requirements.

One or more classes of shares or units that match various characteristics may be created in a stand-alone fund or in each sub-fund of an umbrella fund. The classes of shares or units may for example have the following distin-guishing features: Distribution policy (distribution or capitali-zation shares / units).

Currency (different currencies for the shares/units may be accommodated, e.g. USD, EUR, JPY, etc).

The table below details the most common corporate forms used for setting up an investment fund subject to the 2002 Law or the 2007 Law.

S.A. S.à r.l. S.C.A. S.C.S.

Key features Most commonly used

corporate form.

Originally created for share-

holders with a significant

personal relationship with one

another (intuitu personae), as

evidenced by specific rules still

in place (see “Transfers of

shares”, “Listing of shares”,

“Amendment to articles of

incorporation” below) although

practice shows that this form

is now used despite a lack of

any sort of link among the

shareholders.

Particularly convenient for

fund initiators who want to

retain total control of the

management.

Particularly convenient for

fund vehicles where (i) tax

transparency is required at

the level of the company itself

and (ii) fund initiators want to

retain total control of the

management.

Partnership formed by written

agreement of its partners.

No need for a notarial deed.

Share-holders /Partners

One or more limited

shareholders

(no upper limit).

One or more limited

shareholders

(no more than 40).

One or more unlimited

shareholders and several

limited shareholders

(no upper limit).

One or more unlimited

partners and one or more

limited partners

(no upper limit).

Liability Shareholders are only liable

up to the amount committed.

Shareholders are only liable

up to the amount committed.

Unlimited

shareholders are indefinitely,

jointly and severally liable

(but may be incorporated as

limited liability companies or

partnerships).

Limited

shareholders are only liable

up to the amount committed.

Unlimited

partners are indefinitely, jointly

and severally liable (but may

be incorporated as limited

liability companies or

partnerships).

Limited

partners are only liable up to

the amount committed.

17

S.A. S.à r.l. S.C.A. S.C.S.

Contributions In cash or in kind: contributions

in kind are in principle subject

to a valuation report from an

independent auditor.

In cash or in kind:

contributions in kind are not

subject to a valuation report

from an independent auditor.

In cash or in kind: contributions

in kind are in principle subject

to a valuation report from an

independent auditor.

In cash or in kind:

contributions in kind are not

subject to a valuation report

from an independent auditor.

Form of shares

Bearer or registered form. Registered form only. Bearer or registered form. Registered form only.

Transfers of shares

No statutory restriction on

transfers.

Transfers to non-shareholders

are subject to the prior

approval of the shareholders

representing three-quarters of

the share capital.

No statutory

restriction on transfers.

Transfers not allowed unless

authorised by the partnership

agreement or approved by all

the partners.

Listing of shares

Listing possible. Listing not allowed. Listing possible. Listing not allowed.

Management One-tier SA: by a board of

directors of three directors at

least, if several shareholders.

Two-tier SA: by a management

board of two members at

least, supervised by a

supervisory board of three

members at least, if several

shareholders.

By one or several managers. By the general partner.

Unlimited shareholder(s)

act(s) as general partner(s).

By the general partner.

Unlimited partner(s) act(s)

as general partner(s).

Amendment to articles of incorporation

By a quorum representing at

least half of the share capital7

and a two-third majority of

shareholders, in the presence

of a Luxembourg notary.

By (i) a majority in number of

the shareholders and (ii) such

majority representing at least

three-quarters of the share

capital, in the presence of a

Luxembourg notary.

By a quorum representing at

least half of the share capital7

and a two-third majority of

shareholders, including the

general partner, in the

presence of a Luxembourg

notary.

By all the partners, unless

otherwise specified in the

partnership agreement.

7 This quorum requirement is not applicable to the second shareholders’ meeting which may be convened if the required quorum has not been met at the first meeting.

18

V. main players

Part I of the 2002 Law. Management compa-nies may either be subject to the provisions of Chapter 13 or Chapter 14 of the 2002 Law, depending on the status of the investment fund they manage.

FCPs subject to the 2002 Law and the 2007 Law are necessarily managed by a manage-ment company. SICAVs may also appoint a management company, in particular in order to comply with the substance requirements of

Chapter 13 of the 2002 Law Chapter 14 of the 2002 Law

Scope of application - Applies to management companies managing at

least one UCITS;

- Benefits from the European passport.

- Applies to management companies managing at

least one UCI;

- Does not benefit from the European passport.

Available company forms - Public limited company (S.A.);

- Private limited company (S.à r.l.);

- Cooperative company;

- Cooperative company set up as a public limited

company;

- Corporate partnership limited by shares (S.C.A).

- Public limited company (S.A.);

- Private limited company (S.à r.l.);

- Cooperative company;

- Cooperative company set up as a public limited

company;

- Corporate partnership limited by shares (S.C.A).

Permitted activities - Core services: provision of collective portfolio mana-

gement services to UCITS, UCIs and SIFs (including

asset management, administration and marketing);

- Additional services:

Management of individual portfolios on

a discretionary and individual basis;

Investment advice;

Safekeeping and administration of shares/units

of UCITS, UCIs and SIFs.

- Possibility to delegate activities to third parties.

- Activity limited to the management of UCIs and SIFs,

the management of own assets being only an

ancillary activity;

- Possibility to delegate activities to third parties.

Requirements to be fulfilled - Minimum capital requirements: initial capital of

at least EUR 125,000; if the value of the portfolios

managed by a management company exceeds

EUR 250 million, the capital must be increased

by an amount equal to 0.02% of the amount by which

the value of the managed portfolios exceeds EUR 250

million, provided that a management company is not

required to have a capital of more than EUR 10 million;

- Directors and persons who conduct the business

must be of good repute and have the necessary

professional experience. Identity of directors and

of persons succeeding them in office must be

communicated to the CSSF.

- Identity of shareholders or members having a

qualified holding must be communicated to the

CSSF. Any change in the persons having a qualified

holding must be notified to the CSSF.

- The organisational structure of the management

company must be described to the CSSF;

- Must have sufficient financial resources (minimum

paid-up capital of EUR 125,000).

- Directors and persons who conduct the business

must be of good repute and have the necessary

professional experience. Identity of directors and of

persons succeeding them in office must be

communicated to the CSSF.

- Identity of shareholders or members must be

communicated to the CSSF. Any change in the

shareholders or members should be notified to the

CSSF.

- The organisational structure of the management

company must be described to the CSSF;

1. The management company

19

Chapter 13 of the 2002 Law Chapter 14 of the 2002 Law

Requirements to be fulfilled - Technical and human means necessary for the good

performance of its duties:

Head office in Luxembourg;

Permanent staff, which is suitable for the

contemplated activities;

Senior management carried out by at least two

persons (who may not be employees of the

custodian bank) of good repute and having the

necessary professional experience, one of which

must in principle be on site in Luxembourg;

Adequate technical infrastructure.

2. The custodian bank

Common conditions applicable to UCITS, UCIs and SIFs

- UCITS, UCIs and SIFs must appoint a custodian bank;

- The choice of the custodian bank must be approved by the CSSF;

- The custodian bank must be a credit institution within the meaning of the 1993 Law.

Specific conditions applicable to UCITS and SIFs

The custodian bank must have its registered office in Luxembourg or be established in Luxembourg, if its

registered office is in another member state of the EU.

Specific conditions applicable to UCIs

The custodian bank must have its registered office in Luxembourg or be established in Luxembourg, if its

registered office is in another member state of the EU or in a state which is a non-member state.

Duties of the custodian bank under Part I and Part II of the 2002 Law

SICAV/SICAF - Safekeeping of assets;

- Ensure that the issues and redemptions of shares are made in accordance with applicable

law and the articles of incorporation;

- Ensure that settlements are executed in a timely manner;

- Ensure that income is applied in accordance with the articles of incorporation.

FCP - Safekeeping of assets;

- Day-to-day administration of the fund;

- Ensure that the issues and redemptions of units are made in accordance with applicable

law and the management regulations;

- Ensure that settlements are executed in a timely manner;

- Ensure that income is applied in accordance with the management regulations;

- Ensure that the net asset value is calculated in accordance with the law and the

management regulations (not applicable to Part II FCPs);

- Compliance monitoring of instructions from the management company.

Duties of the custodian bank under the 2007 Law

SICAV/SICAF - Safekeeping of assets.

FCP - Safekeeping of assets;

- Day-to-day administration of the fund.

20

3. The central administration agent

4. The auditor

Processing of issue and redemption of units/shares.

Keeping the register of units or shares. Establishing the prospectus and financial reports.

Dispatching notices and reports from Luxembourg.

Under the 2002 Law and the 2007 Law, a number of administrative duties (duties of the “central administration”) must be carried out in Luxembourg. These duties are: Calculation of the net asset value. Keeping of the accounts and making them available.

Status - Independent auditor, designated by the fund with CSSF approval;

- Remunerated out of the assets of the fund.

Duties - Reporting on the annual accounts;

- Reporting on the activities of the investment fund (financial and organizational aspects);

so-called long form report (not applicable to SIFs);

- Reporting to the CSSF.

21

VI. regulatory supervision

2002 Law 2007 Law

Entity in charge of the supervision

CSSF (its main function is the supervision of the Luxembourg financial sector, in particular of the investment

fund sector).

Approval procedure - A fund may only be launched upon CSSF approval.

A written application for fund approval must be filed

with the CSSF (if applicable, a specific application for

approval of the management company must also be

filed). The CSSF approval also encompasses the

approval of the fund’s promoter;

- The documents requested for fund approval may be

filed in French, English or German;

- Approval of the following fund documents:

Constitutional documents (i.e. management

regulations of an FCP and articles of incorporation

of an investment company);

Full prospectus (which must contain at least the

information provided for in Schedule A of Annex I of

the 2002 Law, in so far as such information does not

already appear in the constitutional documents);

Simplified prospectus (required only for UCITS,

and which must contain at least the information

provided for in Schedule C of Annex I of the 2002

Law);

For UCITS and some UCIs (e.g. hedge funds), the

description of the risk management process;

Agreements to be entered into between the fund

and its service providers (e.g. agreement between

fund and management company, if applicable, and

agreements with custodian, central administration

agent, investment manager, investment adviser,

paying agent, distributor, etc).

- Approval process generally takes 2-3 months,

depending on the complexity of the project;

- Approval of the fund is announced by inscription on the

official list of Luxembourg UCITS/UCIs (published in

the Mémorial).

- SIFs may be launched without prior approval, but the

application for approval must be filed within one

month of the SIFs’ creation. The CSSF does not need

to approve the promoter;

- The documents requested for fund approval may be

filed in French, English or German;

- Approval of the following fund documents:

Constitutional documents (i.e. management

regulations of an FCP and articles of incorporation

of an investment company);

Prospectus: the content of the issuing document

is not legally defined, but must include at least

the information that enables investors to make

an informed judgment on the investment proposed

to them;

Agreements to be entered into between the fund

and its service providers (e.g. agreements with

custodian, central administration agent,

investment manager, investment adviser, paying

agent, distributor, etc).

- Approval of SIF is announced by inscription on the

official list of Luxembourg SIFs (published in the

Mémorial).

22

VII. taxation

2002 Law 2007 Law

Subscription tax(levied on a quarterlybasis on the net assets)

- Generally 0.05% per annum calculated on the net

asset value (valued on the last day of each quarter);

- Exemptions:

Portion of assets represented by holdings in units

of other funds already subject to subscription tax;

Institutional cash/money market funds or

sub-funds, where the portfolio has a residual

maturity of less than 90 days and where the assets

have the highest possible rating;

Pension pooling vehicles.

- Reduced rate of 0.01% per annum:

Money market and cash funds or sub-funds;

Individual sub-funds or classes of shares designed

for institutional investors.

- Generally 0.01% per annum calculated on the net

asset value (valued on the last day of each quarter);

- Exemptions:

Portion of assets represented by holdings in units

of other funds already subject to subscription tax;

Institutional cash/money market funds or

sub-funds, where the portfolio has a residual

maturity of less than 90 days and where the assets

have the highest possible rating;

Pension pooling vehicles.

Corporate income taxand municipalbusiness tax

No. No.

Registration tax Contributions to a corporate investment fund structure (SICAV/SICAF) or to a management company of an FCP

are subject to a fixed registration duty of EUR 75. This amount is also due in case of any amendment to the articles

of incorporation.

Double tax treaty benefits - FCP: the FCP is transparent for taxation purposes and is thus not entitled to double tax treaty benefits;

- SICAV or SICAF: yes, unless excluded under a double tax treaty (the following double tax treaties are generally

applicable to SICAVs or SICAFs, i.e. those concluded with the following countries: Austria, China, Denmark,

Finland, Germany, Indonesia, Ireland, Israel, South Korea, Malaysia, Malta, Mongolia, Morocco, Poland, Portugal,

Romania, San Marino, Singapore, Slovakia, Slovenia, Spain, Thailand, Trinidad and Tobago, Tunisia, Turkey,

Uzbekistan and Vietnam).

Taxation of investors - Investors are not subject to capital gains or income tax in Luxembourg, except for:

(a) Those residing or having a permanent establishment /permanent representative in Luxembourg, or

(b) Non-residents of Luxembourg who hold more than 10% of the shares of a fund of the corporate type, who

dispose of all or part of their holdings within six months from the date of acquisition (subject to the provisions

of an applicable double tax treaty), or

(c) In some limited cases, some former residents of Luxembourg who hold more than 10% of the shares of such a

corporate type of fund (subject to the provisions of an applicable double tax treaty).

23

2002 Law 2007 Law

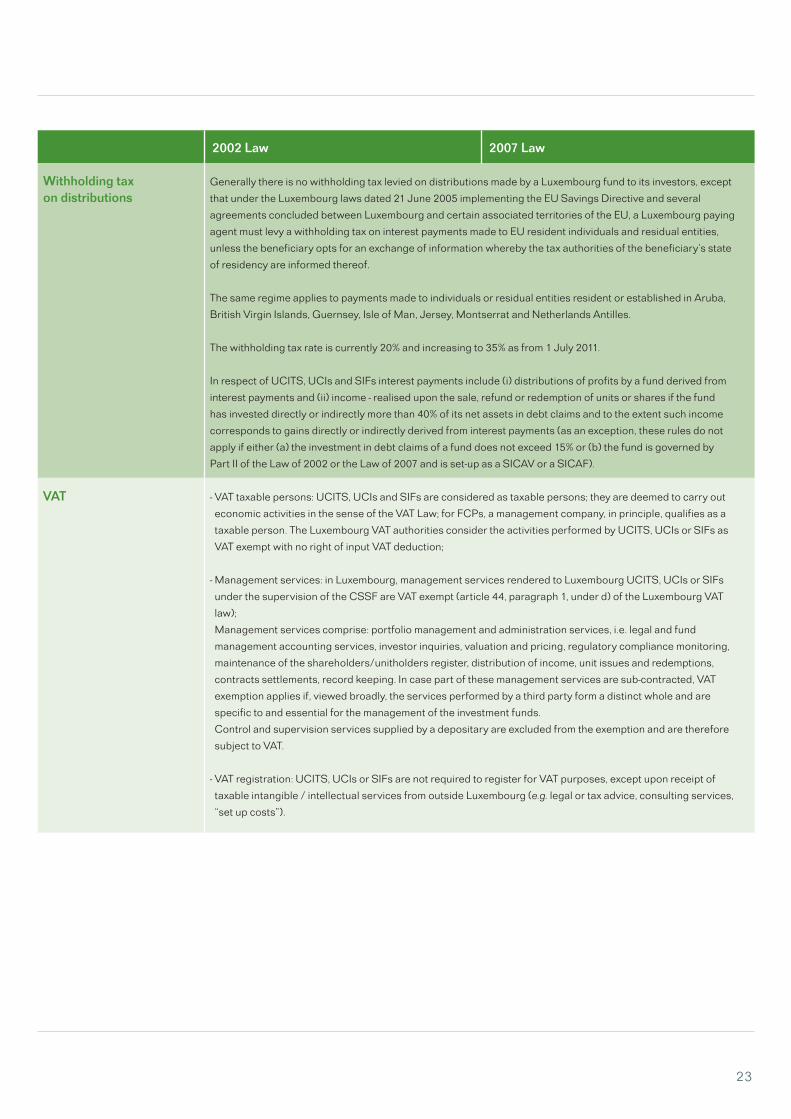

Withholding tax on distributions

Generally there is no withholding tax levied on distributions made by a Luxembourg fund to its investors, except

that under the Luxembourg laws dated 21 June 2005 implementing the EU Savings Directive and several

agreements concluded between Luxembourg and certain associated territories of the EU, a Luxembourg paying

agent must levy a withholding tax on interest payments made to EU resident individuals and residual entities,

unless the beneficiary opts for an exchange of information whereby the tax authorities of the beneficiary’s state

of residency are informed thereof.

The same regime applies to payments made to individuals or residual entities resident or established in Aruba,

British Virgin Islands, Guernsey, Isle of Man, Jersey, Montserrat and Netherlands Antilles.

The withholding tax rate is currently 20% and increasing to 35% as from 1 July 2011.

In respect of UCITS, UCIs and SIFs interest payments include (i) distributions of profits by a fund derived from

interest payments and (ii) income - realised upon the sale, refund or redemption of units or shares if the fund

has invested directly or indirectly more than 40% of its net assets in debt claims and to the extent such income

corresponds to gains directly or indirectly derived from interest payments (as an exception, these rules do not

apply if either (a) the investment in debt claims of a fund does not exceed 15% or (b) the fund is governed by

Part II of the Law of 2002 or the Law of 2007 and is set-up as a SICAV or a SICAF).

VAT - VAT taxable persons: UCITS, UCIs and SIFs are considered as taxable persons; they are deemed to carry out

economic activities in the sense of the VAT Law; for FCPs, a management company, in principle, qualifies as a

taxable person. The Luxembourg VAT authorities consider the activities performed by UCITS, UCIs or SIFs as

VAT exempt with no right of input VAT deduction;

- Management services: in Luxembourg, management services rendered to Luxembourg UCITS, UCIs or SIFs

under the supervision of the CSSF are VAT exempt (article 44, paragraph 1, under d) of the Luxembourg VAT

law);

Management services comprise: portfolio management and administration services, i.e. legal and fund

management accounting services, investor inquiries, valuation and pricing, regulatory compliance monitoring,

maintenance of the shareholders/unitholders register, distribution of income, unit issues and redemptions,

contracts settlements, record keeping. In case part of these management services are sub-contracted, VAT

exemption applies if, viewed broadly, the services performed by a third party form a distinct whole and are

specific to and essential for the management of the investment funds.

Control and supervision services supplied by a depositary are excluded from the exemption and are therefore

subject to VAT.

- VAT registration: UCITS, UCIs or SIFs are not required to register for VAT purposes, except upon receipt of

taxable intangible / intellectual services from outside Luxembourg (e.g. legal or tax advice, consulting services,

“set up costs”).

24

VIII. once-off and ongoing costs at a glance

Registration duty (only for UCITS, UCIs or SIFs in corporate form)

EUR 75.

Notary fees for incorporation of UCITS, UCIs or SIFs in corporate form and management companies

Approximately between EUR 2,000 and EUR 5,000.

Publication fees in the Mémorial of articles of incorporation of UCITS, UCIs or SIFs in corporate form and management companies

Approximately EUR 1,200, varying in particular if the articles are drawn up in one language

or are followed by a translation (French or German translation required if articles are drawn up

in English).

Registration costs in the Companies’ Registrar of UCITS, UCIs or SIFs in corporate form and management companies

Approximately EUR 150.

Registration costs with the CSSF for a UCITS/UCI/SIF

2002 Law - Single UCITS/UCI other than self-managed:

EUR 2,650 (upon filing and on an annual basis);

- Part I self-managed SICAV/SICAF: EUR 5,000 (on an annual basis);

- Umbrella fund: EUR 5,000.

2007 Law - Single SIF: EUR 1,500 (upon filing and on an annual basis);

- Umbrella SIF: EUR 2,650 (upon filing and on an annual basis).

Registration costs with the CSSF for a Chapter 13 management company

2002 Law - Activity limited to collective portfolio management services:

EUR 5,000 (on an annual basis);

- Activity encompassing discretionary portfolio management services:

EUR 12,000 (on an annual basis);

- For each branch established abroad by a management company:

EUR 2,000 (on an annual basis).

© Arendt & Medernach, 2009

25

26

The Association of the Luxembourg Fund Industry (ALFI), the representative body for the Luxembourg investment fund community, was founded in 1988. Today it represents over a thousand Luxembourg-domiciled investment funds, asset management companies and a wide variety of service providers including depositary banks, fund administrators, transfer agents, distributors, law firms, consultants, tax advisers, auditors and accountants, specialist IT providers and communications agencies.

Luxembourg is the largest fund domicile in Europe and its investment fund industry is a worldwide leader in cross-border fund distribution. Luxembourg-domiciled investment structures are distributed in more than 50 countries around the globe, with a particular focus on Europe, Asia, Latin America and the Middle East.

ALFI defines its mission as to “Lead industry efforts to make Luxembourg the mostattractive international centre”. Its main objectives are to:

Help members capitalise on industry trends ALFI’s many technical committees and working groups constantly review and analyse developments worldwide, as well as legal and regulatory changes in Luxembourg, the EU and beyond, to identify threats and opportunities for the Luxembourg fund industry.

Shape regulation An up-to-date, innovative legal and fiscal environment is critical to defend and improve Luxembourg’s competitive position as a centre for the domiciliation, administration and distribution of investment funds. Strong relationships with regulatory authorities, the government and the legislative body enable ALFI to make an effective contribution to decision-making through relevant input for changes to the regulatory framework, implementation of European directives and regulation of new products or services.

Foster dedication to professional standards, integrity and quality Investor trust is essential for success in collective investment services and ALFI thus does all it can to promote high professional standards, quality products and services, and integrity. Action in this area includes organising training at all levels, defining codes of conduct, transparency and good corporate governance, and supporting initiatives to combat money laundering.

Promote the Luxembourg investment fund industry ALFI actively promotes the Luxembourg investment fund industry, its products and its services. It represents the sector in financial and in economic missions organised by the Luxembourg government around the world and takes an active part in meetings of the global fund industry.

For more information, visit our website at www.alfi.lu

alfiassociation of the luxembourg fund industry

October 2010 ALFI thanks Arendt & Medernach, which produced the content of this brochure, for its authorization to reprint. Arendt & Medernach is a member of ALFI.

alfi | association of the luxembourg fund industry

B.P. 206L - 2012 Luxembourg

Tel: +352 22 30 26 - 1Fax: +352 22 30 93