23

Investment Options for Crude & Condensate Stabilization and Splitting Ryan M. Couture Senior Consultant 2015 AFPM Annual Meeting March 23, 2015 San Antonio, TX AM-15-13

Investment Options for Crude & Condensate

Stabilization and Splitting

Ryan M. Couture Senior Consultant

2015 AFPM Annual Meeting March 23, 2015 San Antonio, TX

AM-15-13

Presentation Outline

• U.S. Production and the Condensate Challenge

• Regulatory Environment

• Crude/Condensate Processing Options

• Factors Affecting Investment Decisions

AM-15-13 Slide 2

U.S. Production Growth

• Since 2008, U.S. crude production has grown by over 4 MMBPD – Vast majority of this production growth has been

from light tight oil development

• Natural gas production has also grown rapidly • This has resulted in

increasing amounts of condensate and NGL production

3

4

5

6

7

8

9

2007 2008 2009 2010 2011 2012 2013 2014

Prod

uctio

n (M

MB

PD)

PermianNiobraraEagle FordBakkenAll Other

AM-15-13 Slide 3

Source: EIA

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

29

29.5

30

30.5

31

31.5

32

32.5

33

1985 1990 1995 2000 2005 2010 2015

Sulfu

r (w

t %)

API G

ravi

ty

API Gravity Sulfur (wt%)

Crude Quality Mismatch

AM-15-13 Slide 4

Source: EIA

U.S. refining system “heavied-up” crude slate,

Importing price-advantaged heavy crude

Domestic production

has reversed this trend

Presentation Outline

• U.S. Production and the Condensate Challenge

• Regulatory Environment

• Crude/Condensate Processing Options

• Factors Affecting Investment Decisions

AM-15-13 Slide 5

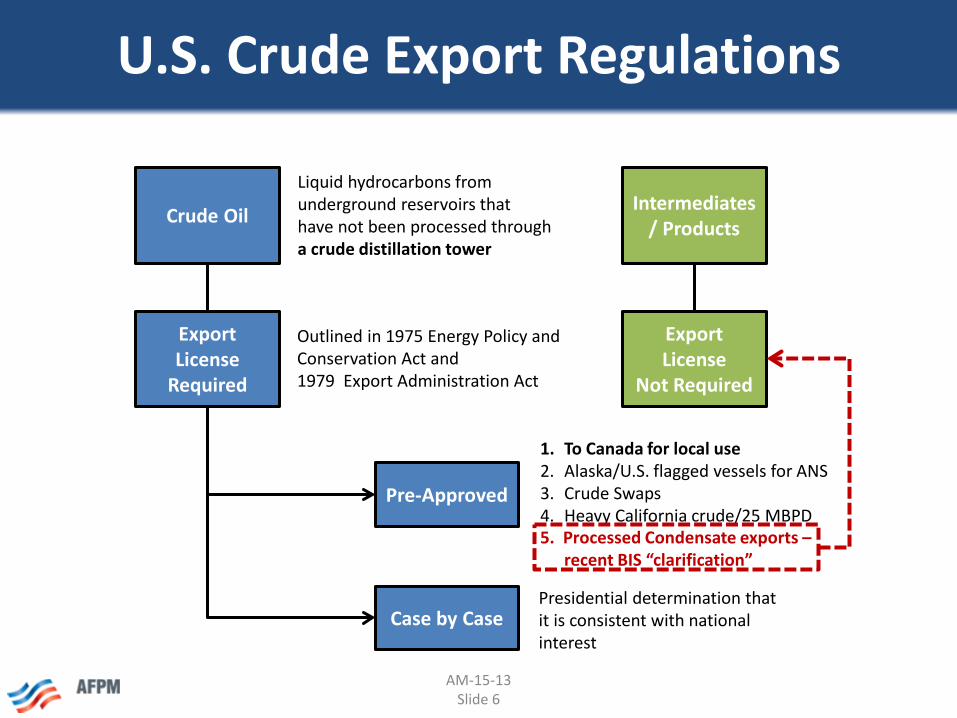

U.S. Crude Export Regulations

Liquid hydrocarbons from underground reservoirs that have not been processed through a crude distillation tower

1. To Canada for local use 2. Alaska/U.S. flagged vessels for ANS 3. Crude Swaps 4. Heavy California crude/25 MBPD

Presidential determination that it is consistent with national interest

Outlined in 1975 Energy Policy and Conservation Act and 1979 Export Administration Act

Crude Oil

Export License

Required

Pre-Approved

Case by Case

Intermediates / Products

Export License

Not Required

5. Processed Condensate exports – recent BIS “clarification”

AM-15-13 Slide 6

Condensate Classification

Wellhead

Natural Gas Processing

Plant

Liquids

Raw Natural Gas

Plant Condensates

(NGL/Y Grade)

Condensate

Lease/Field Condensate

“Condensate” Grade Crude Oil

(API 45°+) (TM&C: 50°+)

Crude Oil

Natural Gas

Not Exportable

Exportable Product

AM-15-13 Slide 7

Condensed Liquids

“Crude Distillation Tower” • Law states crude must be processed through a “crude distillation

tower” before it can be exported

• In June 2014, news came out that two companies were issued private BIS rulings, allowing for export of “stabilized condensate”

• BIS released FAQs in December 2014, laid out factors evaluated when determining minimum processing requirement: – Material transformation using evaporation/condensation – Change in API gravity – Change in % hydrocarbon in product streams – Whether product streams have alternate uses besides export

(blendstock, petrochemical feedstock, etc.) – Distillation process uses temperature gradients, significant internal

structures (trays/packing) and has differentiated output streams – Process goes beyond equipment required to separate vapors and

liquids for transportation needs

AM-15-13 Slide 8

Presentation Outline

• U.S. Production and the Condensate Challenge

• Regulatory Environment

• Crude/Condensate Processing Options

• Factors Affecting Investment Decisions

AM-15-13 Slide 9

Overview of Options

• Several levels of processing – Field level stabilizers – Centralized stabilizers – Crude/condensate fractionators (splitters)

• Refinery processing of LTOs – Primary outlet for domestic production thus far – Will shift some if exports increase or as projects

come on-line

AM-15-13 Slide 10

Field Stabilizer

• Processing at or near wellhead • Intended to strip light ends

from “wild” crude/condensate for transport/storage

• Produces two streams, overhead mixed LPGs and stabilized bottoms stream

• Low complexity, skid mounted and package designed

Field Stabilizer

AM-15-13 Slide 11

Centralized Stabilizer

• Located at/near transportation hubs (pipeline, rail, port)

• Larger than field stabilizers • Towers are more complex,

with packing or trays (simple crude distillation tower)

• May have one or more product side draws (naphtha, etc.) in addition to overhead LPGs and stabilized bottoms stream

Centralized Stabilizer

AM-15-13 Slide 12

Crude/Condensate Fractionator

• Located at/near ports • Intent to export some/all

products • Similar to conventional refinery

crude distillation tower, requires substantial infrastructure

• Often run by midstream operators on take-or-pay agreements

• Produce LPGs, naphthas, distillate and VGO

Crude/Condensate Fractionator (Splitter)

AM-15-13 Slide 13

Refinery Processing

• While dedicated condensate processing is growing, to date refiners have absorbed nearly all production growth

• The shift in crude qualities, including condensates, has prompted refiners to invest to maximize throughput – Variety of upgrades to maintain/increase capacity – Colleague Jim Jones presenting on Delek Refining

expansion tomorrow morning (9:00 AM)

AM-15-13 Slide 14

Modifications For LTO Processing

•Required modifications are very refinery specific

Pre-flash Tower

Distillation Tower Capacity Increase

Overhead Cooling and Light Ends Processing

Upgrades

Naphtha/ Distillate Treating Capacity Increases

AM-15-13 Slide 15

Presentation Outline

• U.S. Production and the Condensate Challenge

• Regulatory Environment

• Crude/Condensate Processing Options

• Factors Affecting Investment Decisions

AM-15-13 Slide 16

Supply & Demand Balance

• Global condensate production has doubled since 2007 – Led by Middle East and U.S. growth

• Condensate demand growth greatest in Asia

– Korea, China and Singapore biggest consumers – Majority of condensate imported from Middle East

• Over 1 MMBPD of condensate processing

capacity built globally since 2006 – Additional 400 MBPD anticipated through 2018 – Middle East projects will reduce condensate exports

AM-15-13 Slide 17

2014 Global Condensate Trade Flows

The Drivers For Domestic Processing

• U.S. supply/demand mismatch – U.S. refining – significant conversion capacity – Gasoline surplus – lessens naphtha demand or

the incentive to produce more gasoline – Petrochemical – U.S. demand primarily C1-C3, limited

naphtha/condensate consumption vs. Europe/Asia

• U.S. crude export restriction – Limited market for unprocessed condensate

• Refinery feedstock or for export to Canada as diluent

– Limited potential for crude swaps

AM-15-13 Slide 19

Economic Considerations

• Location – Proximity to crude production, product markets and export facilities – U.S. Gulf Coast has ideal infrastructure/market – Also allows for easy segregation of processed

condensates for export (for stabilizers)

• Feedstock quality – Drives product yields

• Relative crude price • Product demand

8%

29% 34% 27%

32% 35% 36%

20% 19% 23%

15% 9% 6% 4% 3%

0%

20%

40%

60%

80%

100%

Eagle FordCondensate

Eagle FordCrude

WTI Crude

LPG

LSR

Naphtha

Distillate

Gasoil*

*Gasoil cut quality varies, affects product value and market. AM-15-13

Slide 20

Economic Considerations (cont’d)

• Historical look at fractionation profitability – Looked at light sweet crude and condensate on USGC – Fractionation was profitable on average over past

several years – Cracking refinery remained more profitable through

same period

• Backcast is hypothetical – Skewed, does not account for price relationships

• Both crude/condensate and product market impacts

– Assumptions on transportation and operating costs

AM-15-13

Slide 21

Conclusions

• U.S. production growth has prompted industry investment – Refinery upgrades/expansions – Dedicated stabilizer/fractionator projects – Processing economics dependent on export policy

• Several key factors remain: – Impact of low crude prices on global product demand – Demand growth, primarily in Asia and Latin America – Level of crude/condensate production – Level of processing required for export – Market impacts on stabilizer vs. fractionator economics – Middle East export competition – Domestic vs. international and crude vs. condensate

discounts

AM-15-13 Slide 22

Presenter

Ryan M. Couture Senior Consultant

2100 Ross Ave, Suite 2920 Dallas, TX 75201

214.754.0898

turnermason.com

AM-15-13 Slide 23