48

Investment Products & Investment Products & Client File Review Client File Review 2010 NASAA Investment Adviser Training Dallas, TX ____________________ Presented by: Darren D. Kearns CFP®

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | marilyn-fitzgerald |

| View: | 217 times |

| Download: | 0 times |

Investment Products & Investment Products & Client File ReviewClient File Review

2010 NASAA Investment Adviser TrainingDallas, TX

____________________

Presented by:

Darren D. Kearns CFP®

Introduction / Topics to be Covered

Investments as they relate to the examination process (interview & exam modules)

Investment types, vehicles, and details Investment strategies, analysis & suitability Investment terminology Areas of abuse NASAA Modules Red flags

Types of Investments Debt - Represents money borrowed that

must be repaid, generally having a fixed amount, a specific maturity, and usually a specific rate of interest or an original purchase discount

Equities - Represents ownership shares of an asset

Alternative - All others (Options, Futures, Real Estate, Limited Partnerships, Direct Participation Programs)

Types of Debt

CD’s - Redeemable debt obligation issued by a bank or other depository institutions

Commercial Paper - Usually low-risk debt issued by large corporations usually with strong credit. Issued in large amounts with short maturities

Types of Debt (cont’d)

Bonds– Corporate

– Municipal

– Federal

– Government Agencies (government sponsored)

Equity Securities

Represents ownership shares of an asset (such as a corporation)– Individual Stocks

» Common Stock

» Preferred Stock

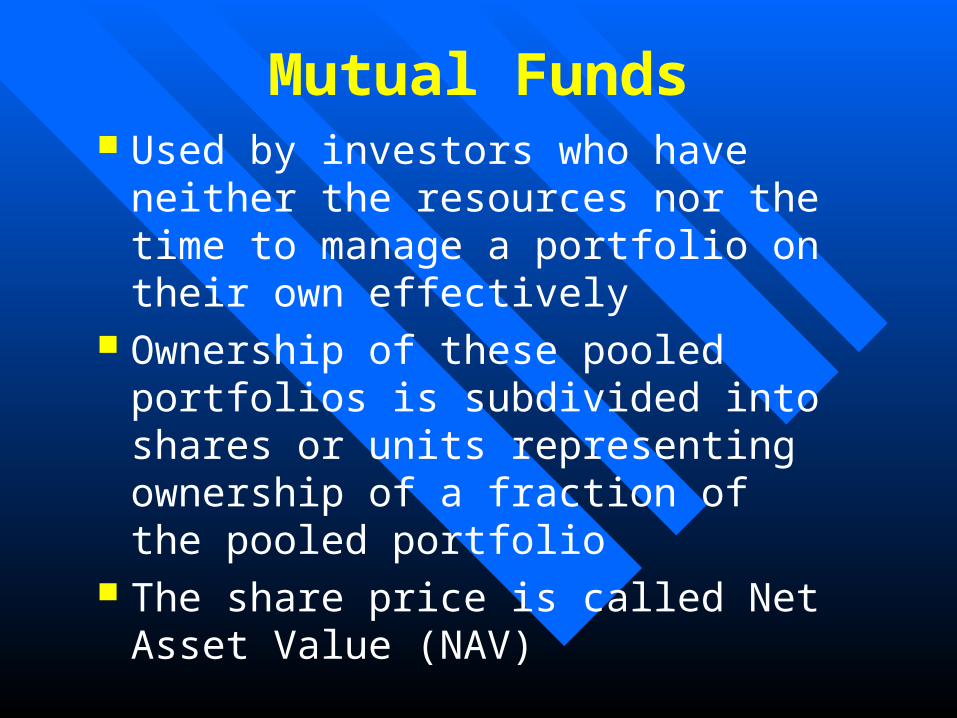

Mutual Funds Used by investors who have neither the

resources nor the time to manage a portfolio on their own effectively

Ownership of these pooled portfolios is subdivided into shares or units representing ownership of a fraction of the pooled portfolio

The share price is called Net Asset Value (NAV)

Mutual Funds Marketed two ways

– No-load funds - Sold directly to fund’s investors» Example: Fidelity, Vanguard, Schwab

– Load funds - Sold through an agent (registered representative). Primarily sold as A, B & C shares

» Example: Van Kampen, American Funds, AIM

What are 12b-1 fees? - Named after an SEC rule, these fees are not directly paid but taken out of funds assets annually to cover costs of marketing and distributing the fund. These fees are paid to the salesperson

Types of Load Funds A Shares - Front end load (5.75%)

– Client purchases $10,000 of American Funds Growth Fund of America Class A» $9,425 goes to purchase shares in mutual fund» Agent receives commission of 5% ($500)» 12b-1 fee is lower – .25% annually» Annual operating expenses is .65%

Offers breakpoints on commission when large amounts are purchased

Front end load can also be reduced by signing a letter of intent or with rights of accumulation

Types of Load Funds B Shares - Contingent deferred sales charge

(CDSC) if sold during the first five years– Client purchases $10,000 of American Funds

Growth Fund of America Class B» $10,000 goes to purchase shares in mutual fund» If client sells in first 5 years a CDSC is charged

CDSC declines for each of first 5 years from 5% to 1.5%

» One-time commission of 5% ($500) » Annual operating expense is 1.36% annually» 12b-1 fee is higher - 1% annually

B shares convert to A shares after 8 years

Types of Load Funds C Shares - Contingent deferred sales

charge (CDSC) if sold during 1st year– Client purchases $10,000 of American Funds

Growth Fund of America Class C

» $10,000 goes to purchase shares in mutual fund (sold in 1st year client is charged a 1% fee)

» One-time commission of 1% ($100) and on-going annual fee of 1%

» 12b-1 fee is 1% annually

»Annual operating expenses is 1.41% annually

Cost of Ownership for $50,000 in theAmerican Funds - Growth Fund of America

A SharesA Shares B SharesB Shares C SharesC Shares

1-year1-year $52,090$52,090 $51,658$51,658 $53,631$53,631

3-years3-years $61,989$61,989 $61.542$61.542 $63,447$63,447

5-years5-years $73,769$73,769 $73,551$73,551 $74,365$74,365

10-years10-years $113,965$113,965 $112,746$112,746 $110,602$110,602

*Based on $50,000 investment and 9.80% annual growth *Class B share automatically converts to A share after 8 years*Class C share automatically converts to A share after 10 years

FINRA Mutual Fund Expense Analyzer Website:

http://apps.finra.org/fundanalyzer/1/fa.aspx

Cost of Ownership for $100,00 Investment in American Funds – Growth Fund of America

A Shares B Shares C Shares

1-year $105,271 $103,317 $107,263

3-years $125,276 $123,084 $126,893

5-years $149,082 $147,102 $148,730

10-years $230,316 $225,493 $221,205

*Based on $100,000 investment and 9.80% annual growth*Class B share automatically converts to A share after 8 years*Class C share automatically converts to A share after 10 years

FINRA Mutual Fund Expense Analyzer Website:

http://apps.finra.org/fundanalyzer/1/fa.aspx

Mutual Fund Abuses Mutual fund switching

– Selling out of one company’s fund and purchasing into a different company’s fund to generate a commission

Mutual fund breakpoint – Selling B or C Shares when A shares

would have earned the client a reduced sales charge

– Buying in multiple lots at a price under the breakpoint

Exchange Traded Fund (ETF) An ETF is an investment vehicle traded on a

stock exchange An ETF holds assets such as stocks and trades

at the same price as the NAV of its underlying assets

Most ETF’s track an index like the S&P 500 (SPDR)

ETF’s traditionally have been index funds, but in 2008 the SEC began to authorize the creation of actively-managed ETF’s

Annuities

Types of Annuities– Fixed - An insurance contract in which the

insurance company makes fixed dollar payments to the annuitant for the term of the contract, usually until the annuitant dies

– Variable - An insurance contract in which the insurance company makes variable dollar payments to the annuitant which varies based on the performance of underlying equity investments

Variable Annuities Typically purchased for benefit of tax

deferral or death benefit Offers a range of investment options in

sub-accounts Investment options are typically mutual

funds that invest in stocks and bonds Value of variable annuity will vary based

on performance of investments chosen

Benefits of Variable Annuities Tax-deferred

– No taxes on income earned and gains realized until you withdraw your money

» No benefit to having a variable annuity purchased in a tax-advantaged retirement plan, such as 401(k)

Death benefit– If owner dies before receiving payments then

beneficiary is guaranteed to received specified amount

Variable Annuity Disclosures Surrender charges

– 7-10 year surrender period High cost of ownership

– Annual administrative fees» Record keeping costs

– Mortality and expense risk fee» The cost of insurance

– Management fees» Indirectly paid to mutual fund for managing assets

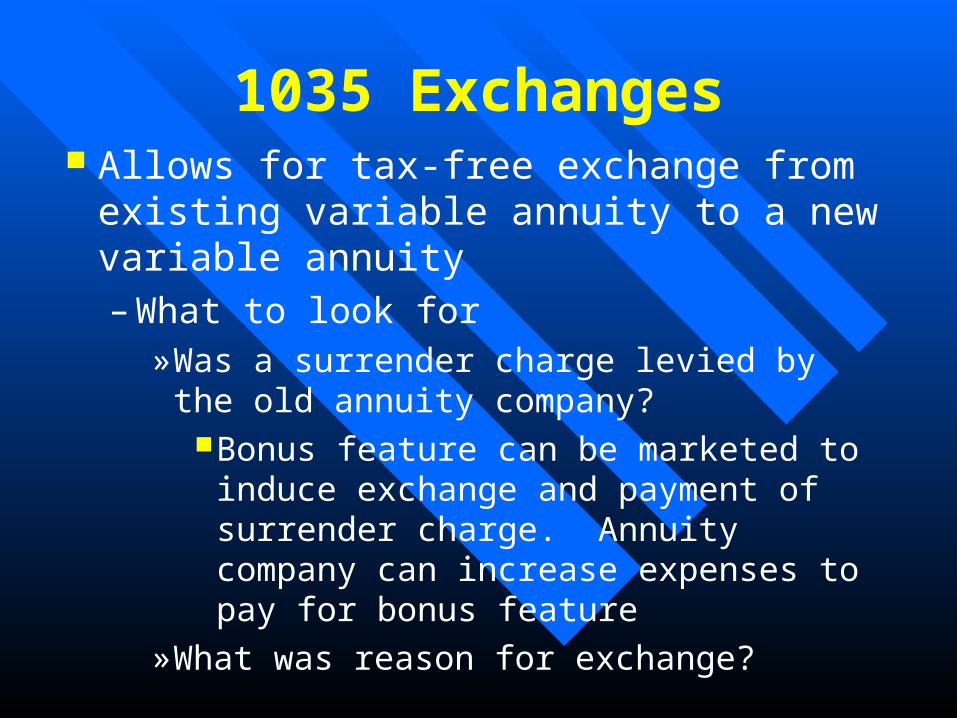

1035 Exchanges Allows for tax-free exchange from existing

variable annuity to a new variable annuity– What to look for

» Was a surrender charge levied by the old annuity company?

Bonus feature can be marketed to induce exchange and payment of surrender charge. Annuity company can increase expenses to pay for bonus feature

» What was reason for exchange?

Alternative Investments

Options Hedge Funds Futures Real Estate Direct Participation Programs

Options

A put, call, warrant, right or other security giving the holder the right but not the obligation to purchase or sell a security at a set price for a specified period

Highly speculative – Magnifies gains and losses

BP Option

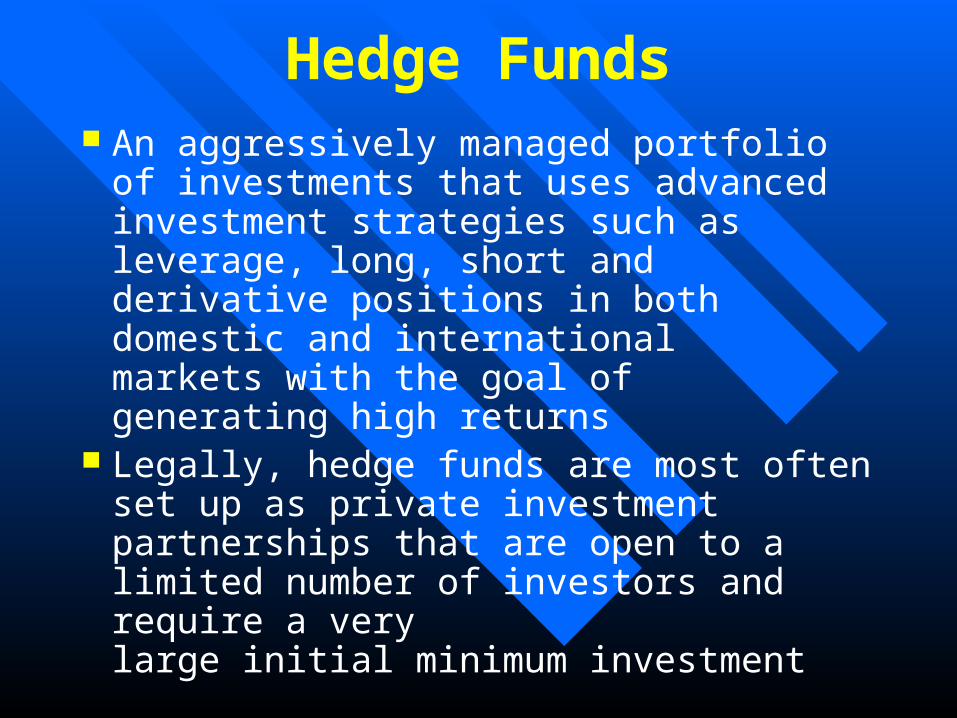

Hedge Funds An aggressively managed portfolio of

investments that uses advanced investment strategies such as leverage, long, short and derivative positions in both domestic and international markets with the goal of generating high returns

Legally, hedge funds are most often set up as private investment partnerships that are open to a limited number of investors and require a very large initial minimum investment

Futures A financial contract obligating the buyer

to purchase an asset (or the seller to sell an asset), such as a physical commodity or a financial instrument, at a predetermined future date and price. The futures markets are characterized by the ability to use very high leverage relative to stock markets

Futures can be used either to hedge or to speculate on the price movement of the underlying asset

Real Estate

Real Estate Investment Trust (REITs) - A security that sells like a stock on the major exchanges and invests in real estate directly, either through properties or mortgages

REITs receive special tax considerations and typically offer investors high yields, as well as a highly liquid method of investing in real estate

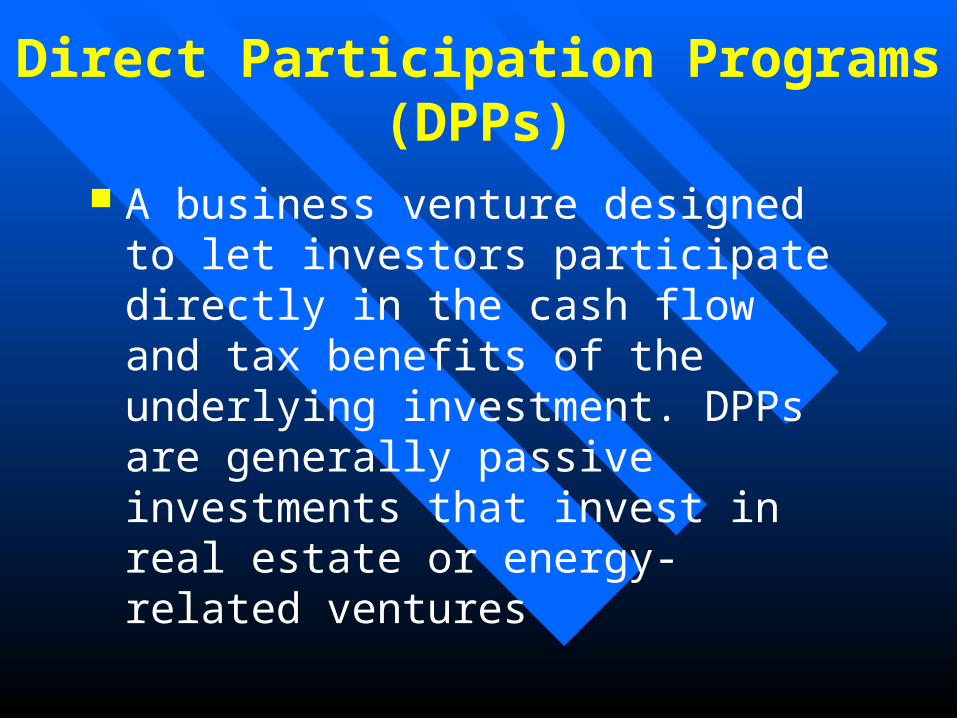

Direct Participation Programs (DPPs)

A business venture designed to let investors participate directly in the cash flow and tax benefits of the underlying investment. DPPs are generally passive investments that invest in real estate or energy-related ventures

Investment Strategies Long-term - Buy & hold Short-term – Daytrade Margin - Borrow money to purchase

investments (leverage investments) Option Writing - Generates Income Shorting - Sell a security you do not own in

hopes price declines and you make a profit• Naked short selling is illegal practice of shorting

stocks and failing to deliver the shares shorted

Type of Analysis - Fundamental

– Macroeconomic analysis – Business Cycle– Industry analysis – Sector rotation– Company analysis – Financial position

(balance sheet, income statement), earnings per share, book value

– Mutual fund analysis – Review of mutual fund performance based on statistical data

Type of Analysis - Technical

Seeks to time trades by assessing psychological state of the market– Types of charts – Bar, line, candle charts &

point-and-figure charts

Bar Chart

Point and Figure Chart

Dartboard Theory of Investing

Sources of Investment Information

News Papers & Periodicals– Wall Street Journal, Business Week, Money

Mutual Fund Research– Morning Star – Principia – Lipper

The Web– www.stockcharts.com,

www.finance.yahoo.com, www.thestreet.com Company Analysis

– Standard & Poors, Moody’s, Value Line

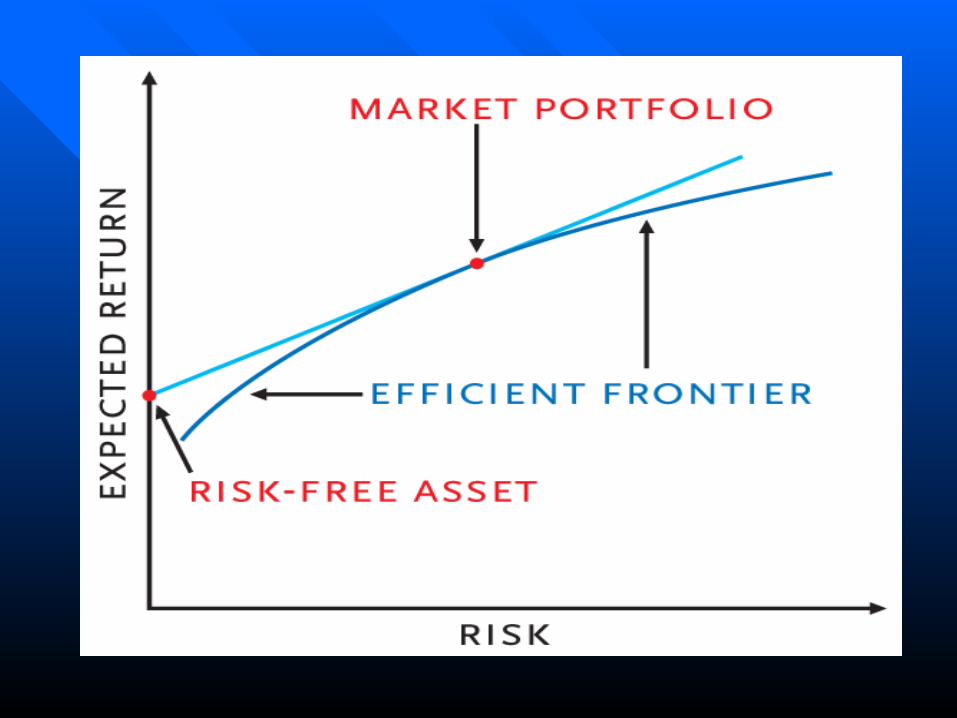

Suitability Has the Investment Adviser determined the

client’s suitability?– Has the client completed a risk tolerance &

objective questionnaire?– Has a client profile been completed?– Have they been periodically updated?– Is the Investment Adviser doing due diligence in

ascertaining client’s wants and needs? – Proper asset allocation requires a determination of

the client’s risk tolerance Efficient Frontier

Suitability (cont’d)

Aggressive Asset Allocation

Equity 80%

Cash5%Debt

15%

Sample Asset Allocation

Suitability (cont’d)Moderate Asset Allocation

Equity 40%

Cash25%

Debt35%

Sample Asset Allocation

Suitability (cont’d)

Conservative Asset Allocation

Equity 20%

Debt50%

Cash30%

Sample Asset Allocation

Equity AllocationEquity Allocation

Small Cap Value10%

International20%

Small Cap Growth

10% Mid Cap Value10%

Mid Cap Growth

10%

Large Cap Value20%

Large Cap Growth

20%

Suitability (cont’d) Do the investments in client account match the

client’s suitability (risk tolerance & time horizon)? Ask Adviser “Why did you recommend this

investment?” Check client files for profile of the client as well

as basis for what is recommended and determine whether profiles are regularly updated?

Annuities – Is an annuity suitable? Are investments in sub-accounts suitable? Are riders suitable?

Mutual Fund – Is the class of fund sold suitable and appropriate for client’s needs and objectives?

Investment Adviser Interview Module Questionnaire

– Products Section: What types of products does the firm recommend?

» Equity Securities BP PLC - BP Cree Research – CREE General Electric - GE

» Corporate Debt Securities Credit Suisse High Yield Bond Fund General Electric Corporate Bond 30 yr 6%

» Federal, state, or municipal securities Wake County Revenue Bond 6 ½% New Jersey Municpal Bond Fund

» Mutual Funds Van Kampen Equity Growth A - VEGAX Fidelity Select Technology - FSPTX

Investment Adviser Interview Module Questionnaire (cont’d)

– Variable Products (Annuities or Variable Life)» Fidelity Personal Retirement annuity

– Wrap Programs» Raymond James Freedom Account

– 3rd Party Money Managers» Brinker Capital

– Insurance (Life, Health, Long Term Care, Property/Casualty)

– Options

– Futures

Investment Adviser InterviewModule Questionnaire (cont’d)

– Pooled Investment vehicles (Hedge Fund)Pooled Investment vehicles (Hedge Fund)» Highbridge Capital Management, LLC – $21 billion in managementHighbridge Capital Management, LLC – $21 billion in management» Bridgewater Associates, Inc. - $43.6 billion in managementBridgewater Associates, Inc. - $43.6 billion in management

– Limited PartnershipsLimited Partnerships» Armadillo Oil Wells, LPArmadillo Oil Wells, LP

– Promissory NotesPromissory Notes» 10% promissory note10% promissory note

– Viaticals, Life SettlementsViaticals, Life Settlements» Viatical settlement providerViatical settlement provider

– Proprietary ProductsProprietary Products» OfferingsOfferings» LLC’sLLC’s

– Other Other » Exchange Traded FundExchange Traded Fund

Investment Adviser Interview Investment Adviser Interview Module Questionnaire (cont’d)Module Questionnaire (cont’d)

Product Comments: Product Comments: – Make notes about a unique product and note which account it is inMake notes about a unique product and note which account it is in

Does the firm provide advice not involving securities? If yes, describe. Does the firm provide advice not involving securities? If yes, describe. – ““We offer estate planning advice”We offer estate planning advice”– ““We provide insurance advice”We provide insurance advice”– ““We provide real estate advice” We provide real estate advice”

What are the firm’s investment strategy, analysis, and research methods? What are the firm’s investment strategy, analysis, and research methods?

– Investment strategy should be based on client’s needs and objectives Investment strategy should be based on client’s needs and objectives – Analysis – Fundamental and/or technicalAnalysis – Fundamental and/or technical– Research methods – Proprietary research, Morningstar, third-party (Standard and Poors, Research methods – Proprietary research, Morningstar, third-party (Standard and Poors,

Moody’s, etc)Moody’s, etc)

Investment Adviser Exam Module– Investment Activities Section (page 4 of module)– Does it appear that the adviser’s actual research and analysis

methods, investment policies, and securities selection are determined and carried out in accordance with the client agreement and/or the advisers disclosure brochure?

» Review Investment policy statement if used» Review client contract» Review client file (notes, risk tolerance questionnaire)» Review client statements» Review Form ADV and advertising» Ask questions

Thank You

Questions?