55

INVESTOR & ANALYST UPDATE 24 th February 2012 2011 results and comments 1

INVESTOR & ANALYST UPDATE

24th February 2012

2011 results and comments

1

Disclaimer

The views expressed here contain information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. Any forward looking information in this presentation has been prepared on the basis of a number of assumptions which may prove to belooking information in this presentation has been prepared on the basis of a number of assumptions which may prove to be incorrect. This presentation should not be relied upon as a recommendation or forecast by Banpu pcl. Nothing in this release should be construed as either an offer to sell or a solicitation of an offer to buy or sell shares in any jurisdiction.

2

1. Focus: reserves update

2. Coal operations

3. Coal marketing

4. Power business

5. Financial summary

Appendices

3

1. Focus: reserves update

4

Changes in Banpu coal reserves 2011 (equity basis)Unit: Mt

CHINA146

-50

96

-1

95-51Daning

divestment

INDONESIA

218 218

-16 +68

270+52

-15 +4 +32

AUSTRALIA +21308 308 329

BASIS END 2010 DIVESTMENT POST-TRANSACTION

BASIS

SALES DEPLETION

END 2011REVISED MINE PLAN

EXTENDED MINE PLAN

5

S S

Growth in Banpu’s coal reserves (equity basis) since 2006

Organic increase in reserves*

Study and LT price1, Geotech impact :

Exploration, study and LT price2:

Exploration, study and LT price2:

Study2: Exploration, study and LT price2:

Exploration, new technology (IPCC):

Indominco (+24) Indominco (+14)

Kitadin (+7)

Bharinto (+13)

Indominco (+49)

Trubaindo (+20)

Trubaindo (+3)

Daning (+17)

Indominco (+30)

Trubaindo (+26)

Termination UG project:

Indominco UG (-9)

Indonesia coal (+68)

Australia coal (+36)

+11Mt

+34Mt +69 Mt +20

Mt+47Mt

+104Mt

2006 2007 2008 2009 2010 2011

-61 Mt** +97 Mt +308 Mt -30 Mt -50 Mt

ITM IPODaning (+29)Gaohe (+68) Centennial

ITM 9%Sell down

DaningDivestment

Acquisition increase (and divestment decrease) in reserves

6

q ( )

* Not including the effect of sales depletion**Excludes divestment of Barasentosa

Note1: ITM 100% Note 2: ITM 74%

Focus on reserves growth 2011: Indonesia coal (equity basis)JORONG INDOMINCO KITADIN EMB & TM TRUBAINDO BHARINTO

Unit: Mt

SALES

-1097+25 112

25

RESERVES GROWTH SALES

-470 66

29

+43 72

YE 2010 YE 2011SALES

-15 4

YE 2010 YE 2011 YE 2010 YE 2011

SALES

-116 15

YE 2010 YE 2011 YE 2010 YE 2011

RESERVES GROWTH

• In-Pit Crushing Conveying (‘IPCC’) system means it will be economic to go deeper (and mine more resources)

RESERVES GROWTH: INDOMINCO

• Engineering studies (including IPCC) and further exploration drilling have boosted reserves estimates

RESERVES GROWTH: BHARINTO

economic to go deeper (and mine more resources)

• IPCC facilitates cheaper and quicker OB removal costs from deeper pits (enabling overall OB costs per bcm to remain competitive).

E l ti k h l b t d t E Bl k i

exploration drilling have boosted reserves estimates

• Further reserves upgrades are planned at Bharinto based on additional exploration and mining studies

• Exploration work has also boosted reserves at E Block in 2011

• Further reserves upgrades are planned at E Block based on additional exploration and mining studies

7

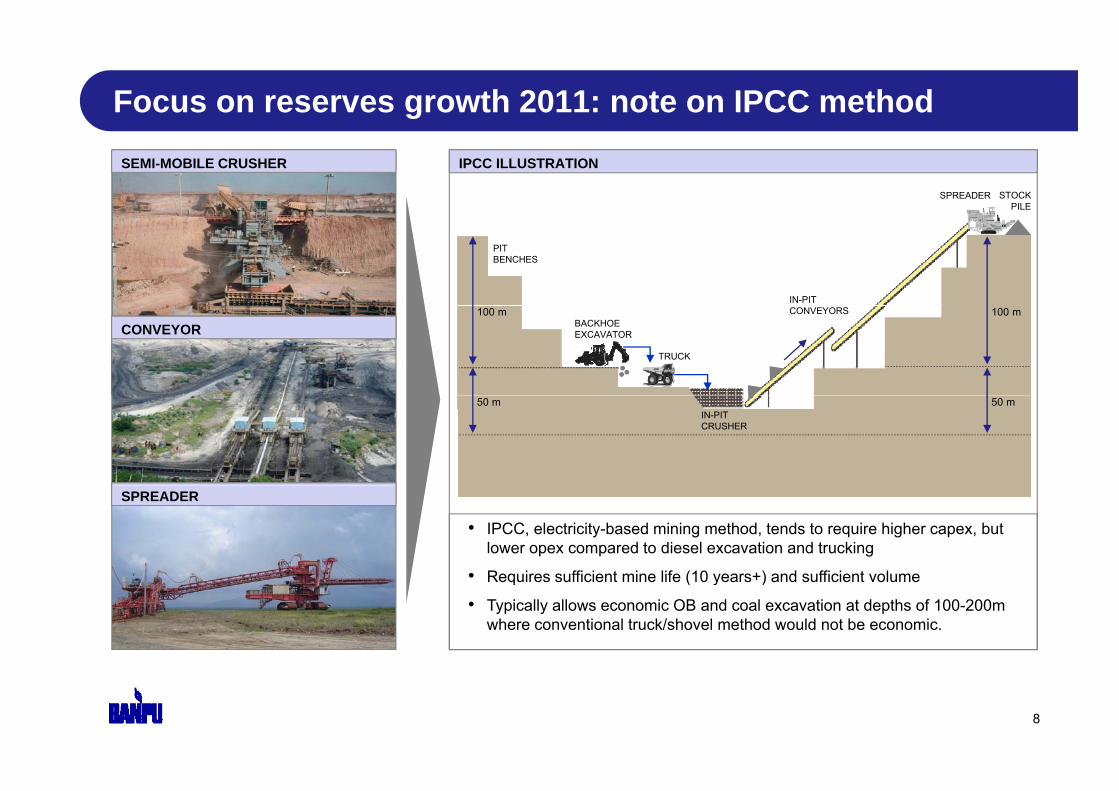

Focus on reserves growth 2011: note on IPCC method

SPREADER STOCKPILE

IPCC ILLUSTRATIONSEMI-MOBILE CRUSHER

PIT BENCHES

IN-PIT100 m

BACKHOEEXCAVATOR

TRUCK

CONVEYORS 100 m

CONVEYOR

50 mIN-PITCRUSHER

50 m

• IPCC, electricity-based mining method, tends to require higher capex, but lower opex compared to diesel excavation and trucking

• Requires sufficient mine life (10 years+) and sufficient volume

SPREADER

• Requires sufficient mine life (10 years+) and sufficient volume

• Typically allows economic OB and coal excavation at depths of 100-200m where conventional truck/shovel method would not be economic.

8

Focus on reserves growth 2011: Australia coal (equity basis)MANDALONG NEWSTAN (EXTENSION) ANGUS PLACE SPRINGVALE OTHERS

Unit: Mt

88 5 MINE PLAN 118 +10-6 122

MINE PLAN REVISED

SALES

8883

-5

57 57

252

+32

13

43DEVELOPED

SALES

MINE PLAN REVISED

32 -6-125

SALES

118 6

YE 2010 YE 2011 YE 2010 YE 2011 YE 2010 YE 2011

SALES

-213

YE 2010 YE 2011 YE 2010 YE 2011

• ANGUS PLACE (+32 Mt)Completion of a pre feasibility and accompanying exploration drilling programme has resulted in a 64 Mt (100% basis)

RESERVES GROWTH: WESTERN OPERATIONS

Completion of a pre-feasibility and accompanying exploration drilling programme has resulted in a 64 Mt (100% basis) increase in reserves.

• CLARENCE (+9 Mt) A review of the mine plan has resulted in 11 Mt (100% basis) increase in reserves.

• SPRINGVALE (-6 Mt) Change to the mine plan to reduce surface land subsidence to comply with State and Federal approval processes.

9

Banpu’s reserves and resources at YE 2011 (equity basis)

MONGOLIAUnit: Year*

IMPLIED MINE LIFE RESERVES AND RESOURCES AT YE 2011

CHINA 95

695**

26

28

AACI ACQUISITION

ORGANIC RESERVES GROWTH

CEY ACQUISITION

ITM SELL DOWNDANING DIVESTMENT

ORGANIC RESERVES 95

190

22

2423 yrs @ 16Mtpa

20 yrs @ 19Mtpa

22 yrs @

RESERVES GROWTH

Banpu

INDONESIA270

60318

20

15 yrs @

22 yrs @ 31Mtpa

22 yrs @ 32Mtpa

18 yrs @ 13Mtpa

ITM

AUSTRALIA330Total resources: 3 457 Mt12

14

16 15Mtpa

13 yrs @ 14 yrs @ 16Mtpa

15 yrs @ 14Mtpa

17 yrs @ at 16Mtpa

Resources (equity basis)

Reserves (equity basis)

1,696

330Total resources: 3,457 Mt

Total reserves: 695 Mt10

12

2007 2008 2009 2010 2011

y @13Mtpa

p

Note: Banpu’s reported resources are measured and i di t d l ( i f d )

10

Reserves (equity basis)

* Year end reserves divided by saleable output (equity basis).** Hunnu’s reserves and resources are currently under review post-acquisition.

indicated only (no inferred resources).

2. Coal divisions2. Coal operations

(a) Indonesia coal

(b) Australia coal

(c) China coal

(d) Mongolia coal

11

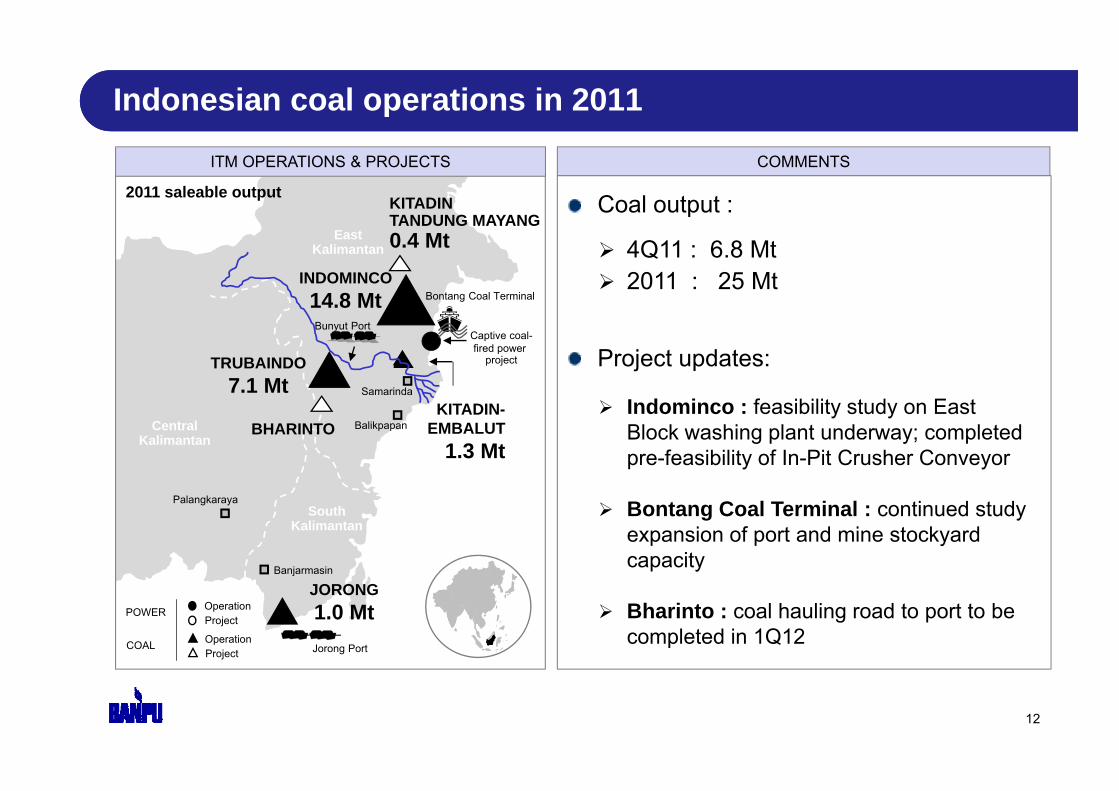

Indonesian coal operations in 2011

Coal output :2011 saleable output KITADINTANDUNG MAYANG

ITM OPERATIONS & PROJECTS COMMENTS

p

4Q11 : 6.8 Mt 2011 : 25 Mt

East Kalimantan

INDOMINCO 14.8 Mt Bontang Coal Terminal

TANDUNG MAYANG0.4 Mt

Project updates:Bunyut Port

14.8 Mt

TRUBAINDO 7.1 Mt Samarinda

Captive coal-fired power

project

Indominco : feasibility study on East Block washing plant underway; completed pre-feasibility of In-Pit Crusher Conveyor

BalikpapanCentral Kalimantan

KITADIN-EMBALUT

1.3 MtBHARINTO

Bontang Coal Terminal : continued study expansion of port and mine stockyard capacity

Palangkaraya

Banjarmasin

South Kalimantan

Bharinto : coal hauling road to port to be completed in 1Q12

j

JORONG 1.0 MtJorong Port

OperationProject

OperationProject

POWER

COAL

12

Indonesian quarterly output and SR analysis INDOMINCO - BONTANG TRUBAINDO - BHARINTO OTHER OPERATIONS

COAL OUTPUT (Mt)*

CV: 6050 - 6500 kcal/kg**

COAL OUTPUT (Mt)*

CV: 6250 - 7200 kcal/kg**

COAL OUTPUT (Mt)*

CV: 5750 kcal/kg**

2 1 2 0

0.4

0.5

CV: 6050 6500 kcal/kg CV: 6250 7200 kcal/kg CV: 5750 kcal/kg

3.6Mt3.1Mt

4.4Mt

3.4Mt

4.5Mt

TDM

YC

K

NTO

0.3Mt 0.3Mt0.3Mt

1Q11 2Q11 3Q11 4Q11 1Q12e

0.5Mt0.4MtKIT

AD

IN

1 7 1 8 2.11 8 1 7 2.1 2.1

1.3 1.7

2.1 2.0

1.5CV: 5300 kcal/kg**

BLO

CK

WB

LO

1.5Mt1.8Mt1.7Mt

BA

IND

OB

HA

RIN

1.6Mt2.1Mt

1Q11 2Q11 3Q11 4Q11 1Q12e

RO

NG

1.5 1.7 1.8 2.11.61.8 1.7 2.1 2.1

1.6

1Q11 2Q11 3Q11 4Q11 1Q12e

E B

TRU

B1Q11 2Q11 3Q11 4Q11 1Q12e

0.3Mt 0.4Mt0.4Mt

1Q11 2Q11 3Q11 4Q11 1Q12e

0.2Mt0.3MtJOR

STRIP RATIOS (b /t) STRIP RATIOS (b /t) STRIP RATIOS (b /t)STRIP RATIOS (bcm/t) STRIP RATIOS (bcm/t) STRIP RATIOS (bcm/t)

13.1 13.315.8

12.5

WB

LOC

K

11.58.9 8.7

11.2

KIT

AD

IN

10.9 10.910.1 10.9

E B

LOC

K

14.1 12.410.0

11.9

TRU

BA

IND

O

8.68.6 8.6 8.6JOR

ON

G

1Q11 2Q11 3Q11 4Q11 1Q11 2Q11 3Q11 4Q11 1Q11 2Q11 3Q11 4Q11

13

Note: *Output figures are saleable coal

**CV figures are air-dried basis

Banpu average selling prices in 3Q10Banpu’s Indonesian coal average selling prices in 4Q11

BJI vs. BANPU’S INDONESIAN ASP COMMENTS

USD/tonne

Comparative ASP trend shows traditional lag, due to mix of pricing and contract length vs.160

180

200

Monthly BJI

Quarterly BJI

Quarterly ASPpricing and contract length vs. spot indices

ASP captured earlier premium so80

100

120

140

160

ASP captured earlier premium so that the impact of more lower quality tonnes was limited (or albeit at higher margin)0

20

40

60

7 7 7 7 8 8 8 8 9 9 9 9 0 0 0 0 1 1 1 1ASP 4Q11 $102.84 (+4% QoQ)

ASP 2011 $ 97 06 (+30% YoY)

g g )

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

ASP 2011 $ 97.06 (+30% YoY)

BJI* February 23, 2012 $116.30

* Barlow Jonker Index: benchmark NSW FOB thermal coal index

1414

Indicative 2012 coal sales

COAL SALES CONTRACT AND PRICING STATUS COMMENTS

Contract Status Price Status

Contracted Fixed

87% 51%

Marginally higher priced commitment than usual for risk management

13%31%

13%

Can still capture upside in Unpriced and in the decreasingly elastic prices

6% of indices IndexedUncontracted

Unpriced

Unsold

As at 9 Feb 2012

TARGET SALES 2012: C. 27 Mt

15

Coal sales by geographic destination (ITM and Thai) Indonesian coal sales by destination 2011 (24.7 Mt)

JAPAN

0 9Mt1.3Mt

HONG KONG S.KOREA1.2 Mt

2012 20122012ITALY

1 8Mt

2012 CHINA 2012

4.5Mt4 2Mt

5.8Mt1 8Mt

5.1Mt

2009 2010 2011

0.9Mt

1.3Mt

0.6Mt

1.8Mt1.4 Mt1.8Mt

2.6Mt

4.0Mt4.2Mt1.8Mt

2009 2010 2011

2009 2010 2011

2009 2010 2011

INDIA2.2Mt 2.3Mt

2012

2009 2010 2011

2009 2010 2011

0.9MtTAIWAN

2.1Mt2.6Mt 2.5Mt

2012

INDONESIA PHILIPPINESTHAILAND

OTHERS*

0 9Mt 1.1Mt 1.3Mt 2012 2012 2012

2009 2010 2011

2009 2010 2011

Mid-to-High CV (≥ 6200 kcal/kg adb)

Low-to-Mid CV (< 6200 Kcal/kg adb)

2.1Mt

1.3Mt1.8Mt1.8 Mt

1.1Mt1.6Mt

1.3Mt

2.1Mt

0.7Mt*Includes small non-

0.9Mt

162009 2010 20112009 2010 20112009 2010 2011

2012 Banpu sales trend

Includes small, nonregular purchasers

16

2. Coal divisions2. Coal operations

(a) Indonesia coal

(b) Australia coal

(c) China coal

(d) Mongolia coal

17

Australian coal operations in 2011

WESTERNNORTHERN

OPERATIONSROM output (equity basis) :

CENTENNIAL’S OPERATIONS & PROJECTS COMMENTS

Charbon Newstan Lochiel(development project) Newcastle

(NCIG)

Newcastle

Inglenook

WESTERN OPERATIONS

OPERATIONS

4Q11 : 3.7 Mt 2011 : 15.4 Mt

Key operation and project updates:

Ivanhoe

Airly

Neubecks Angus Place Mandalong

Mannering

Myuna

Awaba (NCIG)Port Waratah (PWCS)

Key operation and project updates: Mandalong: ROM 1.19 Mt down 32%

due to LW changeover as plannedIvanhoe

North

Clarence

Springvale Angus Place: ROM 1.06 Mt up 156%

QoQ, smooth ramp-up following LW changeover in September

Sydney

Open-cut mineUnderground mine

Springvale: ROM down 49% QoQ due to reduction in panel length and LW changeover

Wollongong

Port Kembla (PKCT)

Project

Port

Power station

RoadRail

Note: Centennial equity ownership 100% unless shown

Newstan : Continued roadway development

Note: Centennial equity ownership 100% unless shown in brackets

18Note: LW = Longwall

Australian coal in 4Q11 (equity basis)

W

CENTENNIAL ROM OUTPUT (Mt) SALES (Mt) SALES: EXPORT/DOMESTIC (Mt)

1 4

Western OperationsAirly (100%)

3.73.71.6 1.71.5 1.4

1.6 1.7 1.7 1.7 1.6

4.1

3.4

1.61.4

1.4

1.3

Angus Place (50%)

Charbon (95%)

Clarence (85%)

Springvale (50%) Exp

ort

1Q11 2Q11 3Q11 4Q111Q11 2Q11 3Q11 4Q11 1Q12p g ( )

Northern Operations es

tic

1Q11 2Q11 3Q11 4Q11

2.6

1Q11 2Q11 3Q11 4Q11 1Q12e

2 0

2.7

2 02.3

2.12.3

2.7

2.1

OperationsAwaba (100%)

Newstan (100%)

Mandalong (100%)

Dom

e

2.1 2.0 2.01.9 2.0 2.0

g ( )

Mannering (100%)

Myuna (100%)1Q11 2Q11 3Q11 4Q111Q11 2Q11 3Q11 4Q11 1Q12e 1Q11 2Q11 3Q11 4Q11

19Note: 14.9 Mt sales (export/domestic) includes 400,000 tonnes third-party output coal sales.

Australian coal sales and revenue structure (equity basis)

2010 2011

ExportExport

SALES TONNESDomestic 61%

Export 39%

Domestic 66%

Export 34%

SALES REVENUEDomestic 40%

Export 60%

Domestic 50%

Export 50% 50%50%

20

Australian indicative export sales 2012

COAL EXPORT SALES CONTRACT AND PRICING STATUS SALES BY DESTINATION 2011

Contract Status Price Status Total 5.8 Mt

36%

Contracted Fixed 3%12%

Others / Traded coal

China

72%

28%16%

28%

20% Indexed29%

33%

22%Korea Taiwan

Uncontracted

33%

JapanUnpricedUnsold

As at 20 February 2012

TARGET EXPORT SALES 2012: c. 6.3 Mt (equity basis)

21

Quarterly equity ROM output

4.55.0

Total equity ROM (Mt)

3 7

4.43.9 3.9

4.8

4.0

ACTUAL PLANNED (INDICATIVE ONLY)

1.9 2.02.7

2.0 2.31.8

2.5

2.1

2 02.53.03.54.0 3.6 3.7 3.7

NO

RTH

ER

N

1.6 1.7 1.7 1.7 1.62.1 2.3 1.9

0.00.51.01.52.0

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

WE

STE

RN

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12West North

2011 2012

LW move Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mandalong(100%)

Angus Place

3wks

3wks

3wks

7 wks(50%)

Springvale(50%)

6 wks 12 wks

22

Normal production Bolt-up/commissioning LW relocationNote: Bar width is indicative of the equity production contributions to Centennial

Indicative operating costs and ASP

A$/t50 Mining costs in 2011: A$48/t$48

INDICATIVE AVERAGE MINING COSTS COMMENTS

40

45

50

$43 $42

Open cut contractor cost

Mining costs in 2011: A$48/t (2010: A$47/t)

Selling, distribution and royalties in 2011: A$13/t

$48$47

Depreciation

30

35

General expenses

Coal handling & preparationCash overhead

Open-cut contractor cost royalties in 2011: A$13/t (2010: A$11/t)

As exports grow the average operating costs per tonne will

20

25 Repairs & maintenance

Stores & supplies

operating costs per tonne will increase - but ASP will also increase

2011 ASP was A$72.5/t with

5

10

15

Labor

0 S as $ 5/continued improvement expected in 2012 as exports increase

0

5

FY09 FY10 2010 2011

Export plan 2012 (Mt): c. 40% (2011: 39%)

2011Years ending June

23

Centennial gearing

0 49 C t i l’ t i t t b i d bt

NET DEBT TO EQUITY RATIO CENTENNIAL’S DEBT

0.24

0.35

0.490.36

Centennial’s net interest-bearing debt at end Dec 2011 was A$ 323 million

Balance sheet shareholder’s equity at $

2008 2009 2010 2011

end Dec 2011: A$ 901 million

Centennial has a mix of AUD fixed rate, AUD floating rate and USD fixed rate debt

USD 225 million debt private placement completed in October with

FX STRUCTURE OF DEBT (END December 2011)

Fixed 11% USD Fixed48%

AUD Fixed37%

p prange of 10 to 15 year maturities at weighted average coupon of 4.55%

Placement took advantage of lowerAUD Float15%

Placement took advantage of lower cost USD debt and is hedge vs USD export revenues

2424

Australian coal: key takeaways

Sales revenue A$1,093.8m ▲ 25% YoY

EBITDA A$328.3m ▲ 78%

FINANCIALS Strong output performanceRecord performances from Mandalong, Clarence andEBITDA A$328.3m ▲ 78%

NPAT A$122.4m ▲ 217%

Cash flow From operations A$314 1m ▲150%

Mandalong, Clarence and Myuna with strong performances from Angus Place and Awaba also Increasing export focus

- From operations- CAPEX

A$314.1mA$243.0m

▲150%▼1%

Gearing – Net debt / EV 26.4% ▼ 6.5%

Improved sales mix, with exports representing 39% of sales (2010: 34%)

DEVELOPMENTS ORGANIC GROWTH LOGISTICS PORT ALLOCATION

Significant increase in reserves at Angus Place.

Banpu Board Approval for development of NewstanE t i bt i d

3 of 7 locomotives delivered, and a fleet of wagons already in service -enabling greater control of export logistics.

Additional 4.6 million tonne preliminary allocation at Newcastle recently obtained, with an EOI process underway at PKCT.

2525

Extension obtained p g p y

2. Coal divisions2. Coal operations

(a) Indonesia coal

(b) Australia coal

(c) China coal

(d) Mongolia coal

26

China coal operations

PRICE vs. COST (RMB/t)PRICE vs. COST (RMB/t)

AVERAGE793

771

BANPU’S CHINA 2011 COAL PRODUCTION TARGETS*

AVERAGE

PRODUCTION COST

AVERAGE COAL PRICE

627

742

480

512

764

480

629

638

PRODUCTION COST

AVERAGE COAL PRICE

BEIJING

Gaohe (45%),Shanxi

6 Mt

COAL OUTPUT (Mt ROM)

COST

4Q10 3Q11 4Q11

407

COAL OUTPUT (Mt ROM)

4Q10 3Q11 4Q11

435

COST

0.49Mt

COAL OUTPUT (Mt ROM)COAL OUTPUT (Mt ROM)

0.35Mt 0.31Mt0.49Mt0.57Mt

0.30Mt 0.30Mt0.80Mt

Hebi (40%),Henan1.5 Mt Gaohe

CV: 6500-8000 Kcal/kg**

4Q10 3Q11 4Q11 1Q12eHebi Zhong Tai MiningCV: 5300-6800 Kcal/kg**

4Q10 3Q11 4Q11 1Q12e

OperationProject

OperationProject

POWER

COAL

Banpu 45% Banpu 40%

Hebi obtained approval from the Henan Energy Bureau in early July for expansion of its coal output to 1 5 Mtpa

Pre-production stage.

27

coal output to 1.5 Mtpa

Note: *ROM production

**Air-dried basis

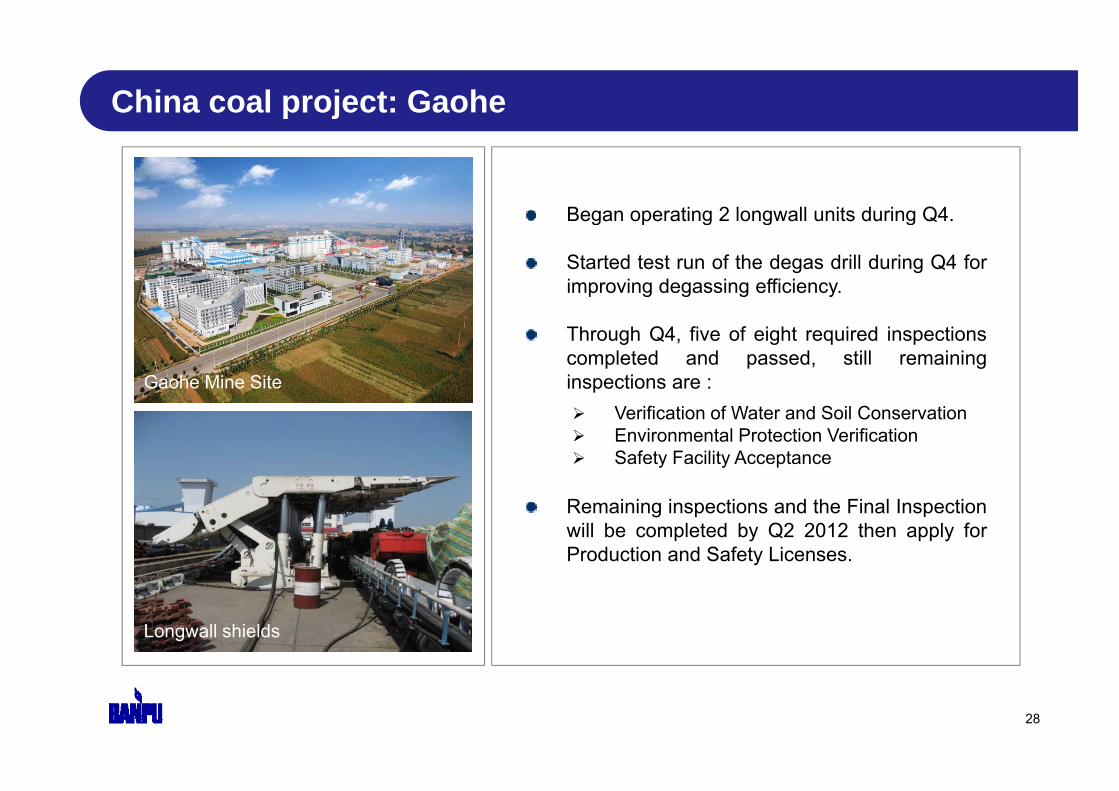

China coal project: Gaohe

Began operating 2 longwall units during Q4Began operating 2 longwall units during Q4.

Started test run of the degas drill during Q4 forimproving degassing efficiency.

Through Q4, five of eight required inspectionscompleted and passed, still remaininginspections are :Gaohe Mine Site Verification of Water and Soil Conservation Environmental Protection Verification Safety Facility Acceptance

Remaining inspections and the Final Inspectionwill be completed by Q2 2012 then apply forProduction and Safety Licenses.

Longwall shields

28

2. Coal divisions2. Coal operations

(a) Indonesia coal

(b) Australia coal

(c) China coal

(d) Mongolia coal

29

Hunnu projects (under review)HUNNU PROJECTS MAP

N ii

Unst KhudagAltai NuursAr Zuun Gol/Zuun Gol

Buyan Bulag

Tsagaan

Delgerekh

Khavtsal

Nariin Munh Haan

Tenuun-2Khuree-2

BuyanBuyan Bulag

Tsant Uul

Tsokhio

Projects

Project Location Interest (%)Altai Nuurs Gobi Altai 70%Unst Khudag Middle Gobi 80%Tsant Uul South Gobi 80-90%Buyan South Gobi 60%Tenuun-2 South Gobi 60%Tsokhio South Gobi 60%Khuree-2 South Gobi 60%Tsagaan Delger Middle Gobi 85%Delgereh Middle Gobi 85%Ar Zuun Gol/ Zuun Gol Gobi Altai 70%Sukhbaatar* Other 60%

3030*Includes Munh Haan, Nariin and Khavtsal

3. Coal marketing

31

Main 2012 coal market drivers

WEATHER CHINESE DEMAND OTHER DRIVERS

• Gas/oil (and nuclear) favour coal.

• Developing scarcity of benchmark

• Indonesia wet season seems normal (↓ 20% rain) but some operations more affected than others Can 2H be as

• Currently demand weak, stocks high, but not versus consumption level. p g y

quality coal

• Growing supply (and demand) for off-spec coal.

• Europe a supply issue not demand i

affected than others. Can 2H be as good as 2H 2011?

• Chinese winter is normal. Will wet season boost hydro?

• Production varies by region, transport and lower quality still a constraint.

issue

• Can U.S.A. continue to sell below cost?

• How much LRC can be shipped in 2012?

season boost hydro?

• Australian weather damage yet to appear.

• 2011 weak 1Q, improving 2Q and exceptionally strong 3 and 4Q.

• 2012 similar? But higher starting 2012?

• How long can Indian politics cap tariffs/ slow growth/ and cap currency

• World growth forecast 2.0% Asian growth forecast 6.0%

base?

Sources: Country Forecast February 2012 from The Economist Intelligence Unit Limited 2012 32

Banpu average selling prices in 3Q10Seaborne thermal coal benchmark prices

Indonesian indices followFOB Richards Bay 6000 kcal/kg NAR

COAL PRICE BENCHMARKS COMMENTS

Indonesian indices follow seasonal impact more than other indices

S th Af i i d i ff t d b150

FOB Richards Bay 6000 kcal/kg, NARFOB Newcastle 6300 kcal/kg, GARFOB Kalimantan 5900 kcal/kg, GARFOB Kalimantan 5000 kcal/kg, GAR

South African index is affected by higher railing, coinciding with greater competition from Indonesia and lately Australia and120

130

140

Indonesia and lately Australia and Colombia for off-spec coal

100

110

120

US$

/ to

nne

70

80

90

60Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12

3333

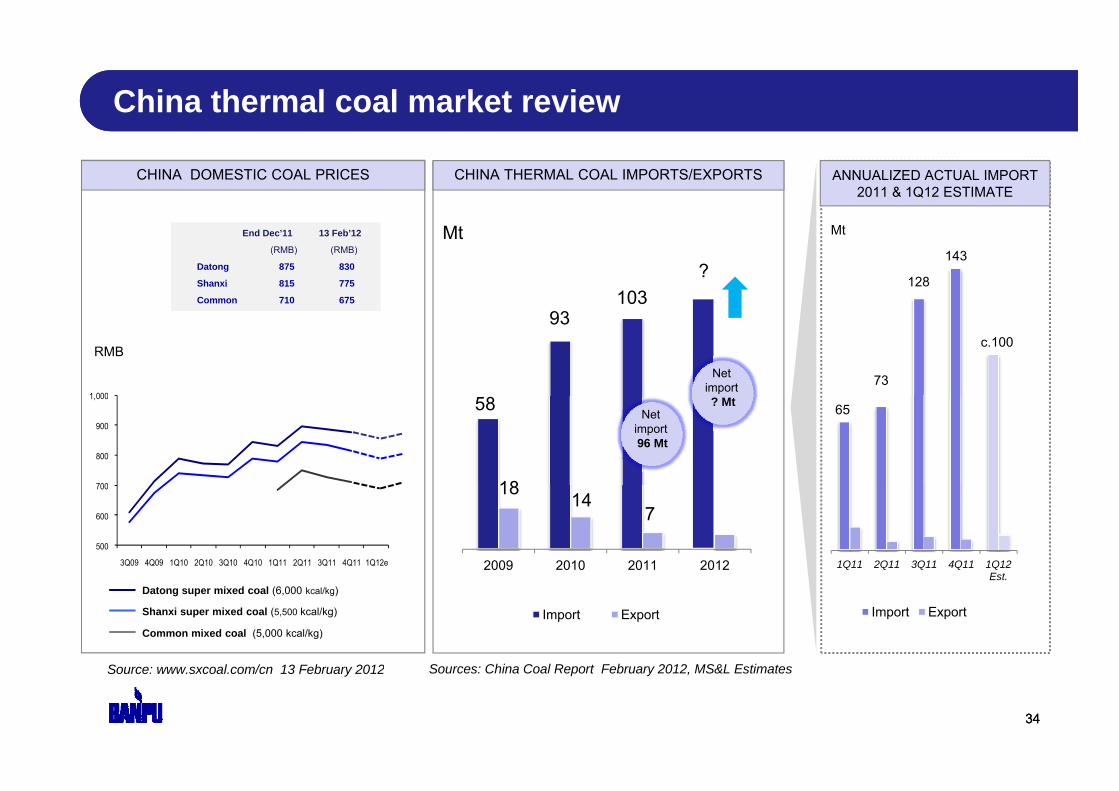

China thermal coal market reviewChina thermal coal market review

CHINA DOMESTIC COAL PRICES CHINA THERMAL COAL IMPORTS/EXPORTS ANNUALIZED ACTUAL IMPORT 2011 & 1Q12 ESTIMATE

128

143

103

End Dec’11 13 Feb’12

(RMB) (RMB)

Datong 875 830

Shanxi 815 775

Common 710 675

MtMt

?

73

c.100

93

1 000

RMBNet

import

6558

18700

800

900

1,000

Net import96 Mt

? Mt

1Q11 2Q11 3Q11 4Q11 1Q12 Est

18 147

2009 2010 2011 2012500

600

700

3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12eEst.

Import ExportImport Export

S l / 13 F b 2012

Datong super mixed coal (6,000 kcal/kg)

Shanxi super mixed coal (5,500 kcal/kg)

Common mixed coal (5,000 kcal/kg)

S Chi C l R t F b 2012 MS&L E ti t

34

Source: www.sxcoal.com/cn 13 February 2012 Sources: China Coal Report February 2012, MS&L Estimates

34

4. Power business

35

Thailand power : BLCP in 4Q11 (100% basis)Bt. million

Q-Q: -57%

Y-Y: 320%

Q-Q: -31%Y-Y: 9%

Q-Q: -17%Y-Y: 36%

Y-Y: 320%

1,3052,066

1,4202,843

4,6873,868

Q-Q: -5%Y-Y: 72%

Q-Q: -36%Y-Y: 186%

4Q10 3Q11 4Q11 4Q10 3Q11 4Q11Total revenueAvailability Payment (AP)

564

FX gain

Y Y: 72% Y Y: 186%

1,281

2,329 2,206

344

1,527983

241607

Q-Q: -29%Y Y 74%

99%

4Q10 3Q11 4Q11Energy Payment (EP)

4Q10 3Q11 4Q11

EBIT57 308

607

41Y-Y: 74%

87%90%

4Q10 3Q11 4Q11843

2,0621,463

16

-43 FX loss-67

* Based on Banpu’s 50% interest

Equity income*4Q10 3Q11 4Q11

Dispatch (%)4Q10 3Q11 4Q11

EBITDA 36

Thailand power: Hongsa project in Laos

1,800 MW mine-mouth lignite-fired power plant project

COD targeted in 2015

Partnership between Banpu (40%), Ratch (40%) and Lao Government (20%)

Power Plant cornerstone laying ceremony on November 18, 2011

Power Plant completed site leveling and ongoing for foundation work

A d t it i d f

Event: Cornerstone Laying Ceremony on November 18, 2011President of the ceremony: HE Mr Azang Laoly Deputy Prime Minister of Lao PDR Access road to site is ready for

construction materials transportation.HE. Mr. Azang Laoly, Deputy Prime Minister of Lao PDRHosted by:• Minister of Energy and Mines, Mr. Soulivong Daravong; • Chairman of Hongsa Power, Mr. Noppon Milintanggoon.

37

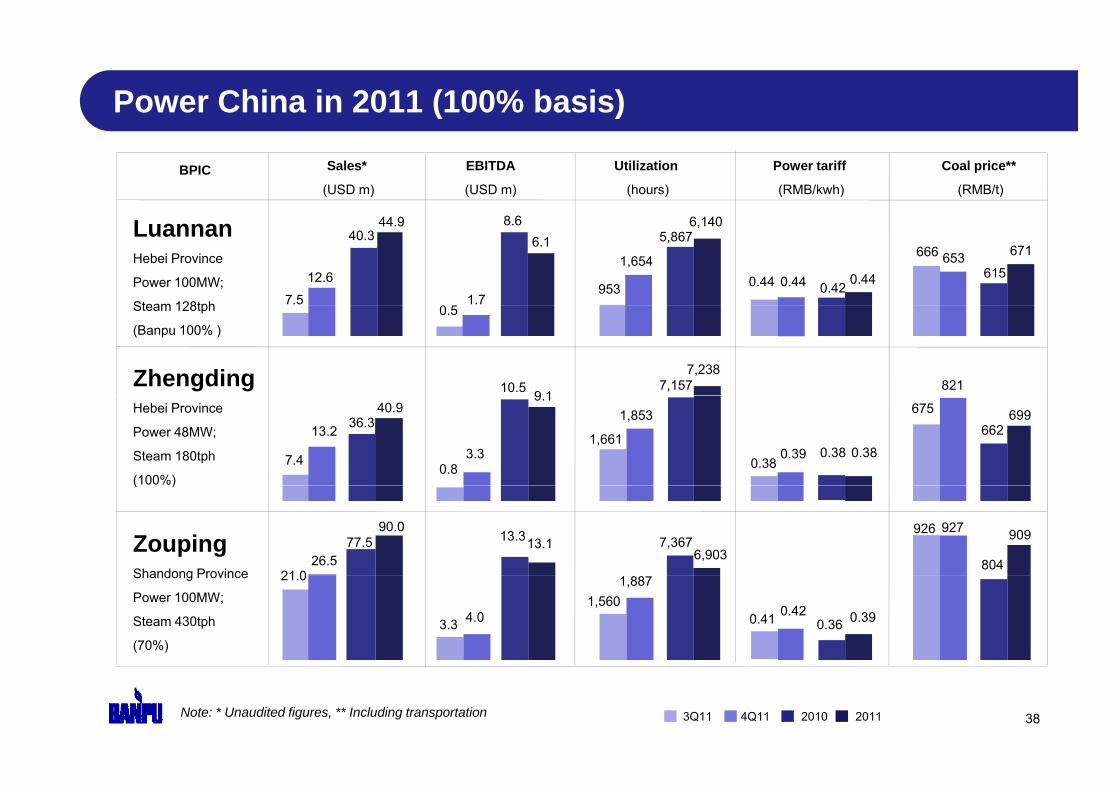

Power China in 2011 (100% basis)

Sales*

(USD m)

EBITDA

(USD m)

Utilization

(hours)

Power tariff

(RMB/kwh)

Coal price**

(RMB/t)BPIC

8 6LuannanHebei Province

Power 100MW;

Steam 128tph

0.44 0.44

666 653

953

1,654

7.5

12.6

0 51.7

40.38.6

6.1 5,8676,140

0.42 0.44 615

671

44.9

Steam 128tph

(Banpu 100% )

Zhengding 821

0.5

10.5 9 17,157

7,238

Hebei Province

Power 48MW;

Steam 180tph

(100%)

1,661

1,853

0.380.397.4

13.2

0.83.3

67540.99.1

0.38 0.38

66269936.3

( )

ZoupingShandong Province 21 0

26.5

926 92790.013.313.1 7,367

6,903804

90977.5

Shandong Province

Power 100MW;

Steam 430tph

(70%)

21.0

3.3 4.01,560

1,887

0.41 0.420.36 0.39

Note: * Unaudited figures, ** Including transportation 3Q11 4Q11 2010 2011 38

5. Financial summary

39

Key external and corporate events N

TS Pheu ThaiUS raising debt

ceiling World growth Th i fl d Italy debt crisis? S&P Glencore

ERN

AL

EVEN

Pheu Thai Party wins general elections

g

S&P downgrades US AAA, markets

growth forecast

downgraded to 4%

Thai flood crisis

Greece

Italy debt crisis?

M h k

downgrades 9 euro zone

nations

Ban BoT cuts

interest rate

Xstrata annouces$90bn merger

EXTE

3Q11 4Q11 Jan 12 Feb 12

Australia carbon tax

US AAA, markets tumble, gold prices soar

Greece referendum Mahakam

Bridge collapse

Iranian oil?interest rate

to 3% Greece passes austerity plan amid protests

VEN

TS

Q Q

10 NovBanpu 3Q11

27 OctUS$225M

RPO

RA

TE

EV

31 AugAnnouncement of

1H11 Bt 9 dividend to be paid on 13 Sep

2011

resultsUS$225M private

placement

7 Nov Closed Offer

of HunnuCompletion of

HAnnouncement

28 Dec 18 Jan

• Banpu 2011 results• 2H11 Bt 9 dividend

to be paid on 30 Apr• R&R upgrades

22 Feb

CO

R 2011 of Hunnu

8 Nov Australia’s carbon tax

(Clean Energy Act) passed

Hunnuacquisition

12 SepAnnouncement

takeover offer

of special Bt 3 dividend to be paid on 10 Feb

40

passed100% of Hunnu

Banpu in 20114Q11 FY 2011

COAL SALES COAL SALES

Bt. million Bt. million

1,489 5,23632,653 112,404

COAL SALES

Down 0.4 Mt-3% Q-Q

COAL SALES

Up 13.7 Mt14% Y-YCEY

ITM

CEY

10.6 Mt 39.6 Mt

3.4

14.9

24.7

Power

31 164

ITM

ITM

7.2

31,164

6 649

68

107,168

1,4991 063

6,718

3,52825,732

20,060*

Coal

P6,649 3,571-43 24,233 18,997

1,063

Revenue EBIT Net Revenue EBIT Net

Coal

Power

Revenue EBIT Net income

Revenue EBIT Net income

Y-Y 52%

Q-Q 6%

Y-Y 117%

Q-Q -21%

Y-Y -28%

Q-Q -16% Y-Y 72% Y-Y 39% Y-Y -19%

Coal Power 41Note: Revenue from others is included in coal

• Includes gains from divestment in Daning

Banpu consolidated sales revenues

Bt. million USD 1,019 m

USD 1,046 m

1,082 1,489

+6% Q – Q +52% Y –Y

Power38% Q – Q+7% Y - Y

Bt 30,685 M Bt 32,653 M

1,019 m

USD 717 m

8,8307,858

1 391

Bt 21,507 M Coal Australia-11% Q- Q+21% Y - Y

*Australian GAAP (AUD Million)

287 260

11* Gain

f10

6,498

1,391

C l I d i

11 from forward

10

276261

13,618

20,77423,306

Coal Indonesia

+12% Q – Q+71% Y - YPower

Coal Australia

3Q11 4Q11

4Q10 3Q11 4Q11

Coal Indonesia

42

4Q10 3Q11 4Q11

Note: USD exchange rate is the average exchange rate of the corresponding period, Revenue from other is included in Coal.* Under Thai GAAP, this is not included in the revenue.

Banpu consolidated coal gross margin 4Q11 : 48%

12,893

Coal sales12,726 Indonesia gross margin: 52%

AUD millionBt. million

Australia gross margin: 40%287

Australian GAAP

8,254

6 688

230

40%

260

40%

52% 3,948

6,688

49%

6,427

4Q10

36%

3Q11 4Q11

%

49%52%

33%

1 130

49%

53%

6 498

Gross Margin

(%)8,830

7,858

Bt million

Australia gross margin: 38%Thai GAAP

1,604

49%

654624

855

38%

690

1,130

56%47%

6,498

32%

893

53%38% 38%

74%

4Q10 3Q11 4Q11

Indominco

4Q10 3Q11 4Q11

Trubaindo

4Q10 3Q11 4Q11

Jorong

28% 38%

Kitadin

47% 21%

Centennial

4Q104Q10 3Q11 4Q11 3Q11 4Q11

TandungMayang

4Q11

43

Mayang

Banpu consolidated EBITDA and NPAT

Bt. millionBt. million

EBITDA NET PROFIT AFTER TAX

4,923513

183

9,924 8,439 Power

-64% Q-Q615% Y Y

-15% Q – Q+72% Y –Y

-16%

Q on Q

924 1,050

279

4,2083,528

Power

Coal - Australia

308

2,3402,231

183

4 912

+615% Y-Y

Coal - Australia -5% Q-Q+41% Y-Y

-28%

Y on Y

Q on Q

3073,818

Coal - Indonesia

Coal - Australia +14% Q-Q+166% Y-Y

6,764 6,489547

1,577

26

4,912

Coal - Indonesia

*

163

2,697 2,985

547

395

Coal Indonesia +11% Q-Q+1,731% Y-Y

2,764

6,489547 Coal Indonesia -4% Q-Q+135% Y-Y

Coal - China 251% Q Q

Coal - China 251% Q Q163

-464-43

4Q10 3Q11 4Q11

(464)

4Q10 3Q11 4Q11

-251% Q-Q-185% Y-Y

-251% Q-Q-185% Y-YPower

44

Power Coal - Australia Coal - China Coal - Indonesia * Including RATCH divestment gain

Banpu consolidated balance sheetGEARING DEBT STRUCTURE

Net D/E (X)

Net gearing (%)

1.06

0 7451% USD Float

THB Fixed18%

Fixed 11% 0.66

0.36

0.74

40%

51% 50%

AUD Fi d

THB Float10%42%

0.14 0.16

2006 2007 2008 2009 2010 2011

12%

26%14% USD Fixed

15%AUD Float

2%

Fixed5%

As at end of December 2011* Net gearing = ND / (ND+E)

2006 2007 2008 2009 2010 2011

Note: the consolidated net debt for Banpu (as of the end of Dec 2011) stood at Bt 65.3bn

4545

Appendices

46

Banpu’s resources & reserves statement (100% basis)

Mine operation and project

InterestEnd December 2011 2011 End December 2010

Measured Resources

Indicated Resources

Total Resources

Proved Reserves

Probable Reserves

Total Reserves Coal Sales Total

ResourcesTotal

Reserves

Jorong 65% 131 4 12 4 143 8 5 7 - 5 7 1 4 145 4 7 2

IND

ON

ESIA

Jorong 65% 131.4 12.4 143.8 5.7 5.7 1.4 145.4 7.2

Indominco 65% 590.6 104.7 695.2 129.8 44.0 173.8 14.8 697.2 149.6

Kitadin 65% 111.3 51.5 162.8 5.8 17.5 23.3 1.7 164.6 24.9

Trubaindo 65% 185.8 141.1 326.9 60.4 41.4 101.7 6.8 334.7 108.5

Bharinto 64% 183 5 114 5 298 0 41 3 71 1 112 4 - 298 0 45 4Bharinto 64% 183.5 114.5 298.0 41.3 71.1 112.4 298.0 45.4

Airly 100% - 96.0 96.0 - 33.7 33.7 0.4 97.7 34.2

Angus Place 50% 73.4 176.9 250.3 18.0 67.3 85.3 1.7 254.5 25.2

Awaba 100% 2.0 - 2.0 - - - 0.8 3.6 1.0

Charbon 95% 7 9 7 2 15 1 2 9 1 3 4 2 0 7 17 1 7 0

AUST

RA

LIA

Charbon 95% 7.9 7.2 15.1 2.9 1.3 4.2 0.7 17.1 7.0

Clarence 85% 34.7 189.0 223.7 7.1 48.3 55.5 1.5 227.1 46.7

Ivanhoe 100% 2.5 4.2 6.7 1.3 0.2 1.5 0.2 7.0 1.7

Mandalong 100% 83.0 185.2 268.2 25.9 56.5 82.4 5.5 275.1 88.0

Mannering 100% 19.4 189.2 208.6 - 11.8 11.8 0.6 300.5 9.1A Mannering 100% 19.4 189.2 208.6 11.8 11.8 0.6 300.5 9.1

Myuna 100% 2.7 335.5 338.2 - 15.6 15.6 1.6 343.5 17.2

Springvale 50% 101.9 60.5 162.4 26.9 24.0 50.9 1.3 166.2 62.9

Inglenook 95% - 54.4 54.4 - - - - 54.4 -

Neubecks 50% 31.0 1.9 32.9 16.4 1.7 18.1 - 32.9 18.1Neubecks 50% 31.0 1.9 32.9 16.4 1.7 18.1 32.9 18.1

Newstan Lochiel* 100% 86.0 211.4 297.4 2.3 54.6 56.9 0.04 297.6 57.0

CH

INA Hebi Zhongtai 40% 58.2 - 58.2 25.7 - 25.7 1.7 60.1 27.4

Gaohe 45% 252.7 116.9 369.6 68.9 119.1 188.0 1.8 371.7 189.8

TOTAL 1,957.7 2,052.5 4,010.3 438.4 608.0 1,046.7 42.5 4,339.1 1,010.2

47

TOTAL 1,957.7 2,052.5 4,010.3 438.4 608.0 1,046.7 42.5 4,339.1 1,010.2

Note: Newstan Lochiel is Newstan’s expansion project

Operating profit

2011 Y Y %2010Units: Bt. million 2011 YoY %

112,404 72%

Sales revenues Coal

Total sales revenues*

106 874 78%

2010

65,28559 901

Sales revenues – Power (BIC) 5,236Cost of sales (62,960)

Sales revenues – Coal 106,874 78%8%4,865

(38,640)

59,901

Gross profit* 49,444 86%Gross profit - Coal 48,899 90%Gross profit – Power (BIC) 527 -34%

26,64525,788

796

GPM 44%

GPM Power (BIC) 10%GPM - Coal 46%

41%

16%43%

GPM – Power (BIC) 10% 16%

Note: * Including other business48

Operating profit

Units: Bt million 2011 YoY %2010Units: Bt. million

Gross profit 49,444 86%GPM 44%

2011 YoY %

26,64541%

2010

SG&A (13,687)Royalty (11,370)Income from associates 1,939

(7,447)(6,925)6,117

Dividend income – Coal & Power -Other income 1,105

EBITOther expenses - Operations (1,698)

4891,017

(1,327)EBIT 25,731 39%EBIT - Coal 24,232 61%EBIT - Power 1,499 -58%

18,56915,0083,561

EBITDA 31,768 45%EBITDA - Coal 29,846 66%EBITDA - Power 1,922 -51%

21,95917,9983,961

49

Operating profit

Units: Bt million YoY %2011 2010Units: Bt. million

EBITInterest expenses (3,051)

YoY %2011

25,736 33%(1,682)

2010

18,575

Financial expenses (349)Income tax (core business) (6,565)Minorities (5,338)

(299)(3,301)(1,987)

Net profit before extra items 10,433Non-recurring items* 8,058

-14%11,30613,235

Income tax for non-core (1,941)Net profit before FX 16,550 -35%FX translations 3,510Net profit 20,060 -21%

24,541187

24,728EPS (Bt/share) 73.82

Note: * Income from non-core assets and other non-operating expenses 91.00

50

Banpu consolidated : Operating profit

Units: Bt. million 4Q11 QoQ% YoY%

32,653 6% 52%Total sales revenues*

4Q10

21,507

3Q11

30,685

Sales revenues – Power (BIC) 1,489Cost of sales (17,580)

Sales revenues – Coal 31,034 5% 55%38% 7%1,391

(14,277)

20,0261,082

(16,576)

29,538

Gross profit* 15,073 7% 108%Gross profit - Coal 14,998 40% 134%Gross profit – Power (BIC) 91 10% -55%

7,2307,066

203

14,10914,026

83

GPM 46%Gross profit Power (BIC) 9

GPM P (BIC) 6%GPM - Coal 48%

10% 55%34%

03

1 %35%

46%83

%47%

GPM – Power (BIC) 6% 15%8%

Note: * Including other business 51

Banpu consolidated : Operating profit

Units: Bt. million

Gross profit 15,073 7% 108%GPM 46%

4Q11 QoQ% YoY%

7,23034%

4Q10

14,10946%

3Q11

GPM 46%SG&A (4,550)Royalty (3,438)Income from associates (207)

34%(2,771)(2,066)

522

46%(3,007)(3,199)

843Other income 394

EBIT 6,717 -21% 117%

(207)

Other expenses - Operations (554)374

3,099

522

(190)272

8,549

843

(469)6,717 21% 117%

EBITDA 8,439 -15% 72%

EBIT - Coal 6,649 -18% 108%EBIT - Power 68 -83% -172%

3,099

4,914

3,194(93)

8,549

9,924

8,145404

EBITDA 8,439 15% 72%EBITDA - Coal 8,256 -12% 69%EBITDA - Power 183 -64% -615%

4,9144,886

26

9,9249,412

513

52

Banpu consolidated : Net profit

Units: Bt. million

EBITInterest expenses (818)

YoY%4Q11 QoQ%

6,718 -21% 117%(719)

4Q10

3,101(763)

3Q11

8,549Interest expenses (818)Financial expenses (117)Income tax (core business) (1,897)Minorities (1 691)

(719)(126)(754)(467)

(763)(79)

(2,205)(1 656)Minorities (1,691)

Net profit before extra items 2,194

Non-recurring items* 347

112%-43%(467)1,034

3,586

(1,656)3,847

(236)

Net profit before FX 2,540 -45%FX translations 988Net profit 3 528 28%

-30%

16%

4,620303

4 923

3,610597

4 208Net profit 3,528 -28%EPS (Bt/share) 12.98

Note: * Income from non-core assets and other non-operating expenses

-16%4,92318.12

4,20815.48

53

Centennial : Income Statement

Units: Bt million (THAI GAAP) 4Q11 QoQ%4Q103Q11 YoY%

Cost of sales (4,869) (4,394)

3,395 -17%Sales revenue

Sales volume (k tonnes)

7,858 -11%3,5726,498

(5,446)

4,1048,830

-5%21%

Gross profit 2,989 -12%2,104GPM 38% 32%SG&A (1,376) 5%(982)

3,38338%

(1,316)

42%

40%Royalty (550)SG&A (1,376) 5%

-15% (447)(982)

1 140 -24%EBIT 771Other income 77 -7% 97

(646)(1,316)

1 50483

40%23%

48%-21%

1,140 24%EBIT 771Interest expenses (211)Financial expenses (72)Gain (loss) on exchange rate 83

(193)(65)(37)

1,504(175)(33)(61)

48%

Gain (loss) on exchange rate 83

Corporate income tax 138N t fit

(37)

-Gain (loss) on derivative 348 315

(61)

(302)344

54

Net profit 1,426 12%7911,277 80%

Thermal coal market analysis – 4Q 2010 updateThermal coal market analysis – 1Q 2012 update

RUSSIARising production and CHINA

D d l / t k hi hEAST ASIA

Japan coming to maximum coal burn.

Korea and Taiwan

rail availability supportslimited export increase,

including to Europe.

Demand lower / stocks higher than plan. Wait and see

attitude. ATLANTIC

Demand holds. Supply in excess at present.

USAThermal export up 15 Mt in 2011. Now price below cost for many

consistent.

REST OF ASIAbelow cost for many.

COLOMBIAWeather constraints but

excess Atlantic supply prompts

REST OF ASIAContinued growth

INDONESIA

INDIASOUTH AFRICA

Rail performing well, mines havingAUSTRALIA

Port and rail mismatch.

excess Atlantic supply prompts Pacific sales. 1Q wet season (↓20%)

normal

Gradual stock reduction. Political drag continues.

Rail performing well, mines having trouble adjusting.

Port and rail mismatch. Limited weather impacts so far. Clear shortage of

better coals. = Demand/Supply

= Demand

= Supply

5555