22

May 19, 2015 Investor and Analyst Day Eli Amon, SVP Marketing, Sales and Logistics

May 19, 2015

Investor and Analyst Day Eli Amon, SVP Marketing, Sales and Logistics

Safe Harbor

All statements in this communication, other than those relating to historical facts, are “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended These forward-looking statements and projections are not guarantees of future performance and are subject to a number of assumptions, risks, projections and uncertainties, many of which are beyond our control, which could cause actual results to differ materially from such statements or projections. Important factors that could cause actual results to differ materially from our expectations include, among others: loss or impairment of business licenses or mining permits or concessions; natural disasters; failure to raise the water level in evaporation Pond 5 in the Dead Sea; accidents or disruptions at our seaport shipping facilities or regulatory restrictions affecting our ability to export our products overseas; labor disputes, slowdowns and strikes involving our employees; currency rate fluctuations; rising interest rates; general market, political or economic conditions in the countries in which we operate; pension and health insurance liabilities; price increases or shortages with respect to our principal raw materials; volatility of supply and demand and the impact of competition; changes to laws or regulations (including environmental protection and safety and tax laws or regulations), or the application or interpretation of such laws or regulations; government examinations or investigations; the difference between actual reserves and our reserve estimates; failure to integrate or realize expected benefits from acquisitions and joint ventures; volatility or crises in the financial markets; cyclicality of our businesses; changes in demand for our fertilizer products due to a decline in agricultural product prices, lack of available credit, weather conditions, government policies or other factors beyond our control; decreases in demand for bromine-based products and other industrial products; litigation, arbitration and regulatory proceedings; and war or acts of terror. More detailed information about factors that may affect our performance may be found in “Risk Factors” in our Annual Report Form 20-F filed with the U.S. Securities and Exchange Commission on March 20, 2015. Forward-looking statements and projections represent our views and are given only as of the date of this communication and we disclaim any obligation to update or revise them, whether as a result of new information, future events or otherwise, except as required by law.

All information included in this document speaks only as of the date on which they are made, and we do not undertake any obligation to update such information afterwards. Some of the market and industry information is based on independent industry publications or other publicly available information, while other information is based on internal studies. Although we believe that these independent sources and our internal data are reliable as of their respective dates, the information contained in them has not been independently verified and we can not assure you as to the accuracy or completeness of this information.

2

Strategic Goals for the Next Decade

Expanding our potash production capability in order to grow with our main markets:

Distinctive advantages in the faster growing markets support ICL’s higher market share

Farmer education initiatives

Expand our phosphate fertilizers sales and diversify our product portfolio

Expand polysulphate sales through farmer education

ICL’s potash production capacity growth targets

Million Tonnes ICL Growth 2015-2025

1.3 ICL Iberia: Phoenix I-IV

0.1- 0.5 ICL Dead Sea

0- (0.8) ICL UK

1.0 ICL Africa

2.8-1.6 Total

4

Diminishing Arable Land Will Require More Intensive Agriculture

5

Fertilizers Demand Correlates with Improved Dietary Consumption

Meat Consumption

Population

Fertilizer consumption

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

1962 1964 1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Ind

ex, r

ela

tive

to

19

62

Population, Meat and Fertilizers [Base 1962]

Source: IFA, USDA, USA Census

6

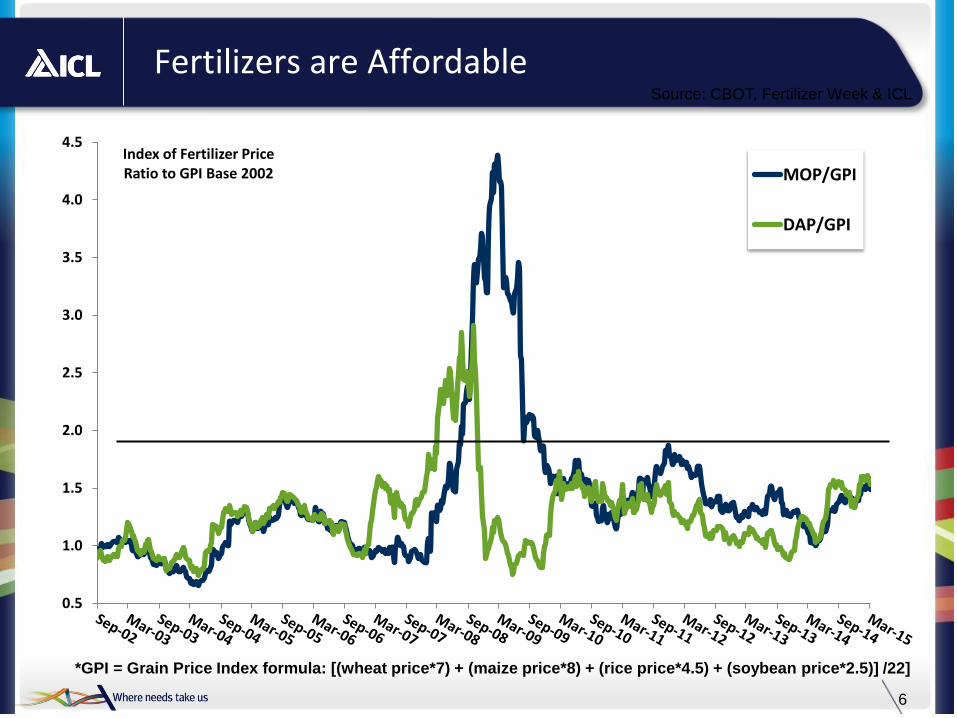

Fertilizers are Affordable Source: CBOT, Fertilizer Week & ICL

*GPI = Grain Price Index formula: [(wheat price*7) + (maize price*8) + (rice price*4.5) + (soybean price*2.5)] /22]

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5Index of Fertilizer Price Ratio to GPI Base 2002 MOP/GPI

DAP/GPI

7

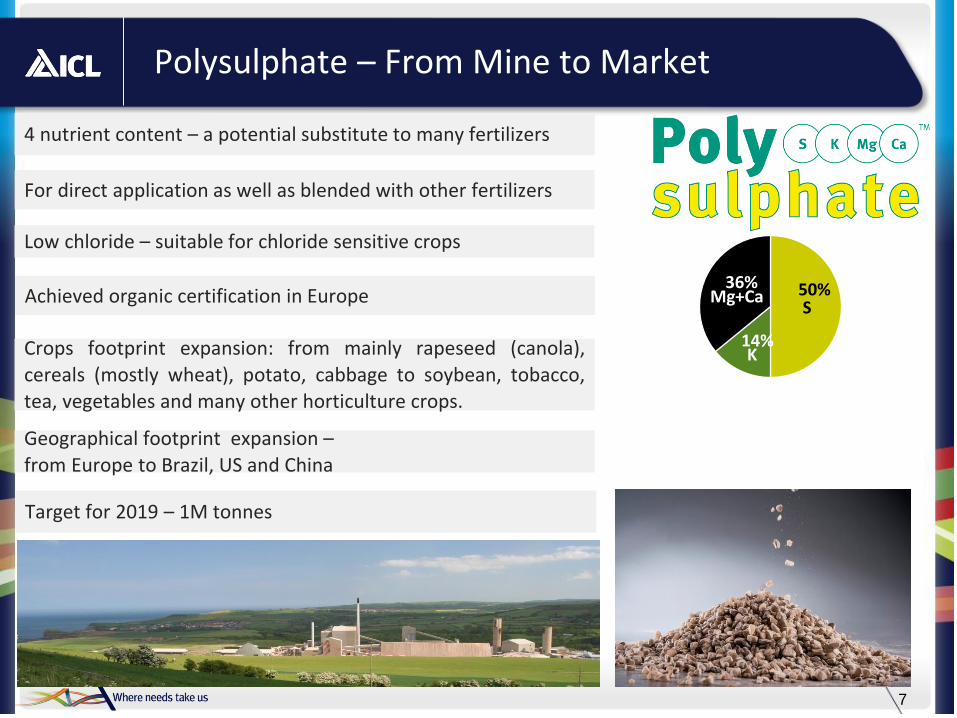

Polysulphate – From Mine to Market

Crops footprint expansion: from mainly rapeseed (canola),

cereals (mostly wheat), potato, cabbage to soybean, tobacco, tea, vegetables and many other horticulture crops.

Target for 2019 – 1M tonnes

Low chloride – suitable for chloride sensitive crops

Geographical footprint expansion –

from Europe to Brazil, US and China

Achieved organic certification in Europe

4 nutrient content – a potential substitute to many fertilizers

For direct application as well as blended with other fertilizers

50%

14% K

S

36% Mg+Ca

8

China China China

China China India

India India

India India

Brazil

Brazil Brazil

Brazil

Brazil

USA

USA

USA

USA

USA

SE Asia

SE Asia

SE Asia

SE Asia

SE Asia

RoW

RoW

RoW

RoW

RoW China India

Brazil RoW

1999 2006 2013 2014 China India Brazil RoW 2020 2025

80*

72*

53

62

Potash Demand Growth Estimates Source: CRU

Region 1999-2014

CAGR

2014-2020

Growth (tonnes)

2014-2020

CAGR

China 7% 1.3 1.5%

India 3% 2.2 7%

Brazil 6% 2.7 4%

USA 1% (0.4) 1%-

SE Asia 6% 2.1 4.4%

RoW 0% 2 2%

Total 3% 10 2.5%

After 2020 annual growth rate returns declines to 2%, and reaches 18M tonnes growth from 2014 to 2025

*FertEcon estimations for 2020 & 2025: 75M tonnes & 81.5M tonnes, respectively

Million tonnes KCl

Source: CRU, ICL estimates

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Source: Industry publications, ICL estimates

Potash Market is Expected to Remain Balanced Source: CRU, DSW

68

79

88

Million tonnes 2014 2020 2025

Demand 62 72 80

Operating Capacity 68 79 88

Gap 6 7 8

Utilization rate 91% 91% 91%

* Greenfields capacity is multiplied by realization factor that takes into account the probability of realization, based on its category – Firm (80%), Probable (60%), Speculative (30%), ICL (100%). Not including BHP

Probable Brownfields

Firm Greenfields

Probable Greenfields

Speculative Greenfields

ICL growth

Firm Brownfields

Supply (Million tonnes KCl)

ICL’s growth: 2.8 million tonnes

10

The Phosphate Market and ICL’s Position

43.0

46.4

- 0.2 0.2 0.4

1.7

1.2

2014consumption

USA China Brazil India RoW 2019consumption

Million tonnes P2O5

Source: CRU

We are active in the Triple Super Phosphates, Single Super Phosphates and Phosphoric Acid

• TSP marketing focuses on Brazil, USA and Europe

SSP marketing focuses mainly on Brazil

• We are the largest supplier of PK compound fertilizers in Europe

• We plan to become a supplier of DAP in future

CAGR 2014-2019: 1.5%

11

BPC 17.1%

ICL 15.0%

APC 12.5%

K & S 2.1%

Uralkali 31.2%

BPC 26.1%

Uralkali 19.2%

K+S 12.4%

ICL 9.1%

SQM 5.7%

Uralkali 32.5%

BPC 22.5%

ICL 16.3%

APC 7.1%

K+S 2.6%

SQM 1.4%

Other 1.3%

ICL’s Market Share in Potash in the Faster Growing Markets (2014)

Sources: BOABC, SIACESP, Company estimates

India Brazil China

Total import: 4.3 Mt Total import: 9.1 Mt Total import: 8.0 Mt

Canpotex 22.5%

Canpotex 27.5%

Canpotex 27.5%

Demand CAGR 2014-2020: 7% Demand CAGR 2014-2020: 1.5% Demand CAGR 2014-2020: 4%

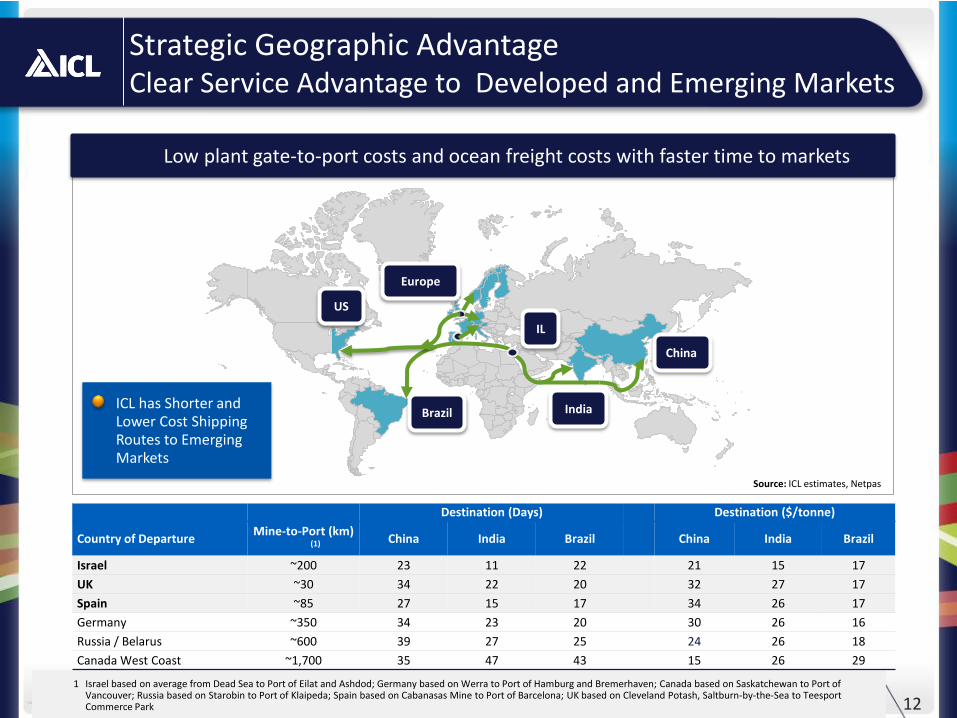

Strategic Geographic Advantage Clear Service Advantage to Developed and Emerging Markets

Destination (Days) Destination ($/tonne)

Country of Departure Mine-to-Port (km)

(1) China India Brazil China India Brazil

Israel ~200 23 11 22 21 15 17

UK ~30 34 22 20 32 27 17

Spain ~85 27 15 17 34 26 17

Germany ~350 34 23 20 30 26 16

Russia / Belarus ~600 39 27 25 24 26 18

Canada West Coast ~1,700 35 47 43 15 26 29

Source: ICL estimates, Netpas

China

India

IL

Europe

Brazil

US

Low plant gate-to-port costs and ocean freight costs with faster time to markets

• ICL has Shorter and Lower Cost Shipping Routes to Emerging Markets

12 1 Israel based on average from Dead Sea to Port of Eilat and Ashdod; Germany based on Werra to Port of Hamburg and Bremerhaven; Canada based on Saskatchewan to Port of

Vancouver; Russia based on Starobin to Port of Klaipeda; Spain based on Cabanasas Mine to Port of Barcelona; UK based on Cleveland Potash, Saltburn-by-the-Sea to Teesport Commerce Park

13

China Domestic Potash Production still Lags Behind Demand

Million tonnes 2015E 2020E 2025E

Production 6.8 7.5 7.5

Imports 6.5 7.4 9.1

Total deliveries 13.3 14.9 16.6

-

2

4

6

8

10

12

14

16

18

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Million Tonnes Product

Total Deliveries Production Imports

14

China - Market Share Increase due to Sales Strategy Change

Until 2009, we had long term agreements with Sinofert

• In 2010, sales contracts were signed one level down the value chain with distributors and NPK producers

0%

5%

10%

15%

20%

25%

-

1

2

3

4

5

6

7

8

9

10

2006 2007 2008 2009 2010 2011 2012 2013 2014

ICL Share Million Tonnes Product China Potash Imports and ICL Share

Total ICL ICL %

First year of new sales

strategy

Source: FertEcon Potash Outlook (Feb. 2015)

2015 contracts: 1.1M tonnes with an option for additional 0.1M tonnes. Delayed quantities as a result of the strike, will be delivered during H2 2015

15

Strategic Alliance with Yunnan Yuntianhua– an Important Addition to Our Product Slate

Kunming

We plan to export phosphates from China to Brazil, USA and India

This will expand our product portfolio in those

markets to further strengthen our foot print and customer relations

Sales in China: expand from MOP to other additional phosphate based fertilizers

Export phosphates to African markets

16

India’s Nutrient Ratio Challenge

India needs to feed a growing population

N:K Ratio was moving in the right direction, until the Nutrient Based Subsidy (NBS) was introduced

Fertilizers subsidies favor urea (N) over P and K, causing distorted NPK ratio. N:K ratio increased to more than 8:1

India has potential to improve crop yields

8.62

6.72

5.79

3.64

United States China Vietnam India

Rice yield comparison (tonne/Ha) India potash imports

-

2

4

6

8

10

12

2005 2010 2015 2020 2025

Million tonnes

Source: FertEcon Potash Outlook (Feb. 2015) Source: USDA

Introduction of NBS

17

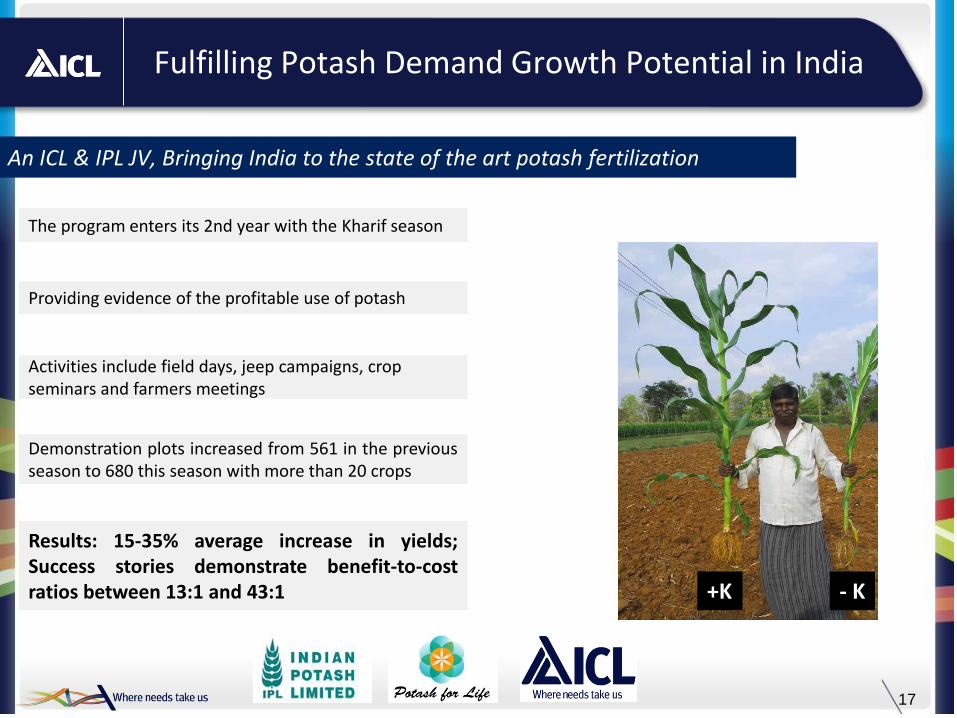

Fulfilling Potash Demand Growth Potential in India

The program enters its 2nd year with the Kharif season

Providing evidence of the profitable use of potash

Activities include field days, jeep campaigns, crop seminars and farmers meetings

Demonstration plots increased from 561 in the previous season to 680 this season with more than 20 crops

Results: 15-35% average increase in yields; Success stories demonstrate benefit-to-cost ratios between 13:1 and 43:1

An ICL & IPL JV, Bringing India to the state of the art potash fertilization

- K +K

18

ICL in Brazil – Solid Position in a Growing Market

The world’s largest reserves of arable land (exc. rain forest)

The world’s largest volumes of fresh water

Agriculture strong development rates expected to continue

Agriculture expansion into the “Cerrado”, soils containing low levels of nutrients, will require intensive fertilization

Brazil

USA

Other

-

20

40

60

80

100

120

140

160

2012/13 2014/15 2016/17 2018/19 2020/21 2022/23

Global soybean export - Million tonnes

Logistical advantage through combined cargo of MOP & Phosphates from Israel (Supermarket vessel)

Advantage supports solid customer relations

ICL has a well established sales office in Brazil

Brazil Fertilizer demand fundamentals

ICL’s position

Source: OECD

19

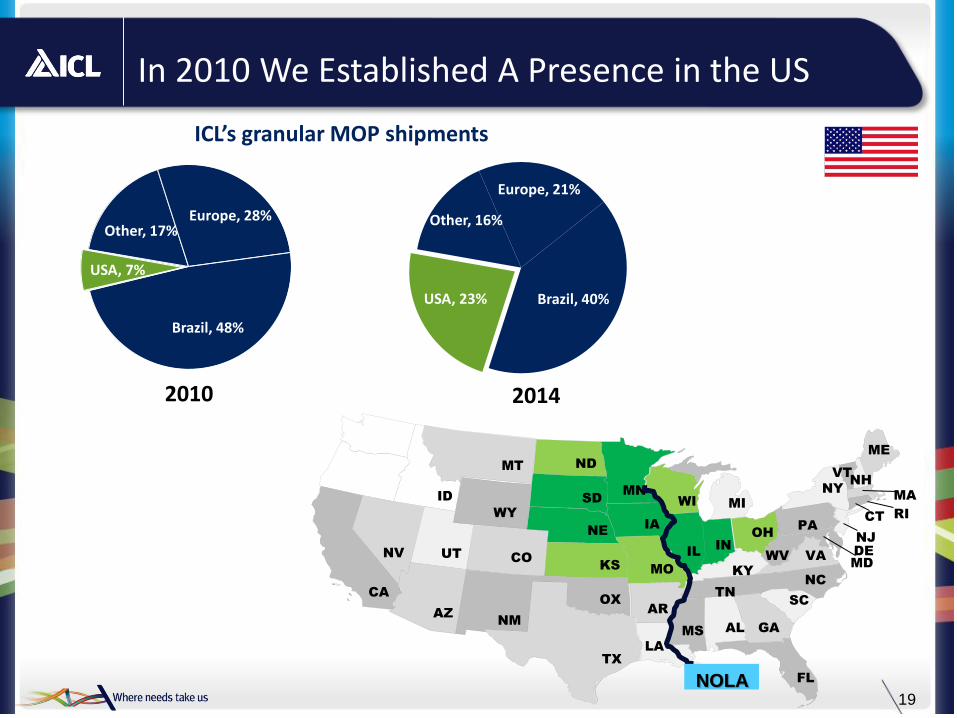

In 2010 We Established A Presence in the US

CA

ID

MT

WY

NV UT CO

ND

SD

NE

KS

MN

IA

MO

WI

IN

KY

OH

WV IL

MI

AZ NM

TX

OX

AR

LA

MS AL

TN

GA

SC

NC

FL

ME

VT NH

NY

PA

VA

MA

RI CT

NJ

DE

MD

NOLA

Other, 16%

Europe, 21%

Brazil, 40% USA, 23%

Other, 17% Europe, 28%

Brazil, 48%

USA, 7%

ICL’s granular MOP shipments

2010 2014

20

Africa - Evolution of Fertilizer Demand

Source: IFA - Fertilizer Demand in Sub-Saharan Africa, Enlarged Council Meeting – Marrakech, Morocco – November 2014

+43% for Africa (CAGR ~5%)

+70% for sub-Saharan Africa without South Africa (CAGR ~8%)

Regional demand seen reaching 6 Mt by 2015

Strong demand growth since 2008, driven by Sub-Saharan Africa

Million tonnes

21

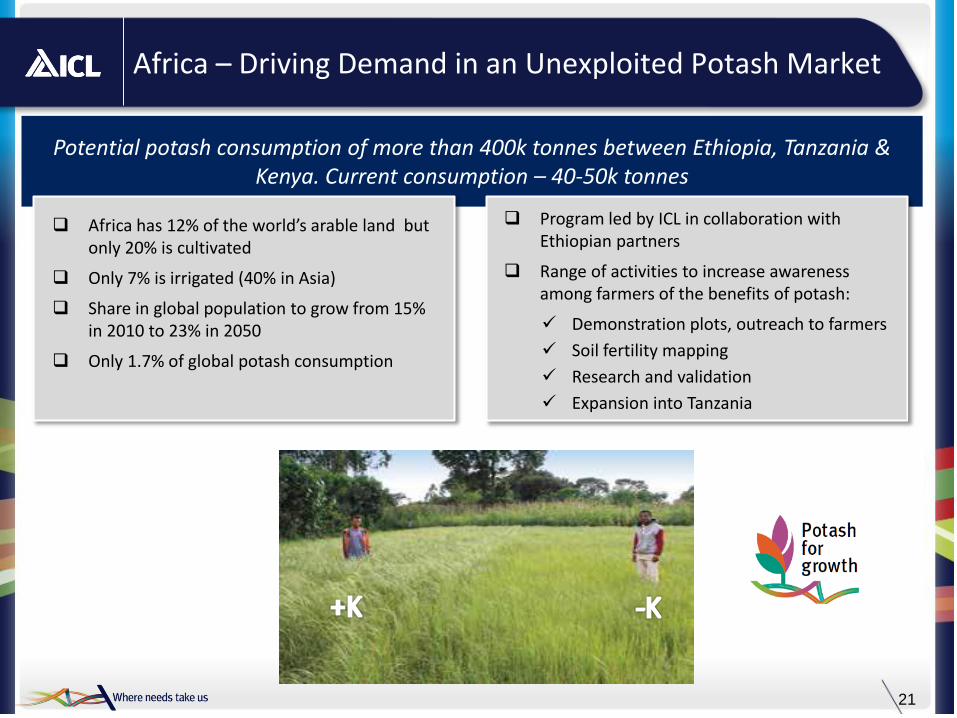

Africa – Driving Demand in an Unexploited Potash Market

Potential potash consumption of more than 400k tonnes between Ethiopia, Tanzania & Kenya. Current consumption – 40-50k tonnes

Africa has 12% of the world’s arable land but only 20% is cultivated

Only 7% is irrigated (40% in Asia)

Share in global population to grow from 15% in 2010 to 23% in 2050

Only 1.7% of global potash consumption

Program led by ICL in collaboration with

Ethiopian partners

Range of activities to increase awareness among farmers of the benefits of potash:

Demonstration plots, outreach to farmers

Soil fertility mapping

Research and validation

Expansion into Tanzania

Thank You

![Investor Presentation - Analyst / Institutional Investor Meeting [Company Update]](https://static.documents.pub/doc/80x56/577c98301a28ab163a8b4855/investor-presentation-analyst-institutional-investor-meeting-company-update.jpg)