25

Investor Presentation Dec 2019

Investor Presentation Dec 2019

o Bank Muscat Introduction

o Operating Environment

o Bank Muscat Business – Overview

o Financial Performance

o Annexure

23‐Feb‐20 2

Contents

Note: The financial information is updated as of 31st Dec 2019, unless stated otherwise.

23‐Feb‐20 3

Bank Muscat Introduction

23‐Feb‐20 4

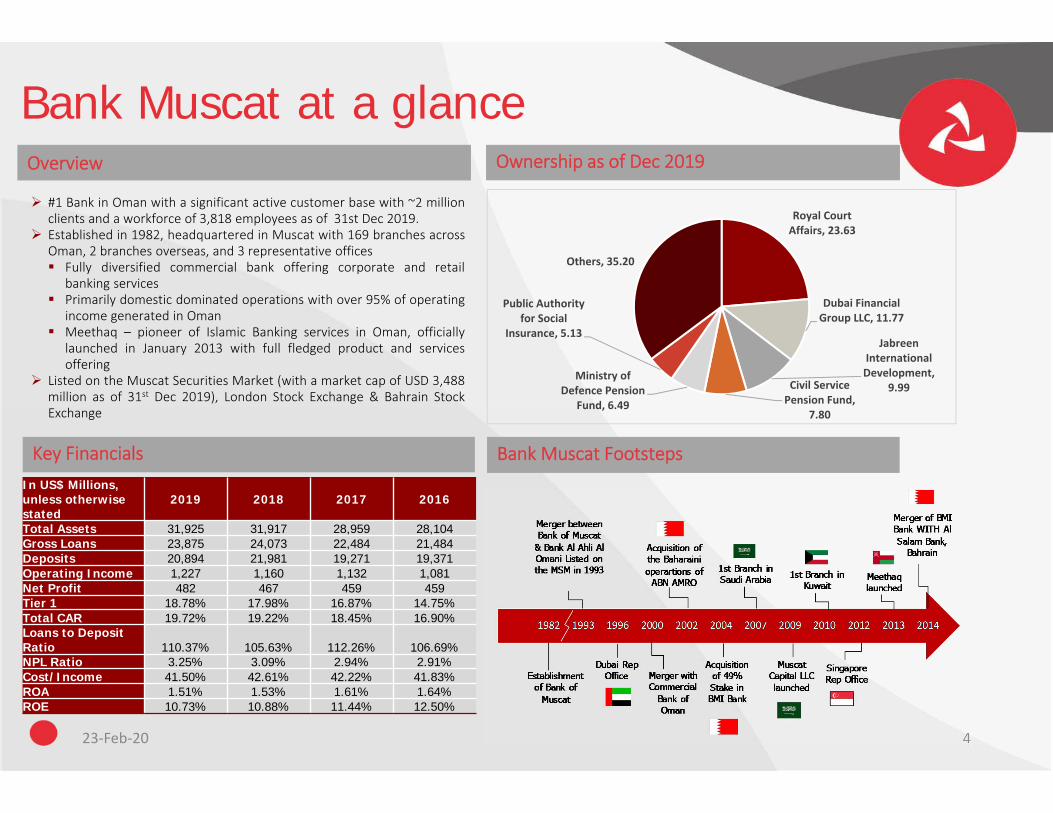

Bank Muscat at a glanceOverview

#1 Bank in Oman with a significant active customer base with ~2 millionclients and a workforce of 3,818 employees as of 31st Dec 2019.

Established in 1982, headquartered in Muscat with 169 branches acrossOman, 2 branches overseas, and 3 representative offices Fully diversified commercial bank offering corporate and retail

banking services Primarily domestic dominated operations with over 95% of operating

income generated in Oman Meethaq – pioneer of Islamic Banking services in Oman, officially

launched in January 2013 with full fledged product and servicesoffering

Listed on the Muscat Securities Market (with a market cap of USD 3,488million as of 31st Dec 2019), London Stock Exchange & Bahrain StockExchange

Ownership as of Dec 2019

Key Financials Bank Muscat Footsteps

Royal Court Affairs, 23.63

Dubai Financial Group LLC, 11.77

Jabreen International Development,

9.99Civil Service Pension Fund,

7.80

Ministry of Defence Pension

Fund, 6.49

Public Authority for Social

Insurance, 5.13

Others, 35.20

In US$ Millions, unless otherwise stated

2019 2018 2017 2016

Total Assets 31,925 31,917 28,959 28,104Gross Loans 23,875 24,073 22,484 21,484Deposits 20,894 21,981 19,271 19,371Operating Income 1,227 1,160 1,132 1,081Net Profit 482 467 459 459Tier 1 18.78% 17.98% 16.87% 14.75%Total CAR 19.72% 19.22% 18.45% 16.90%Loans to Deposit Ratio 110.37% 105.63% 112.26% 106.69%NPL Ratio 3.25% 3.09% 2.94% 2.91%Cost/Income 41.50% 42.61% 42.22% 41.83%ROA 1.51% 1.53% 1.61% 1.64%ROE 10.73% 10.88% 11.44% 12.50%

23‐Feb‐20 5

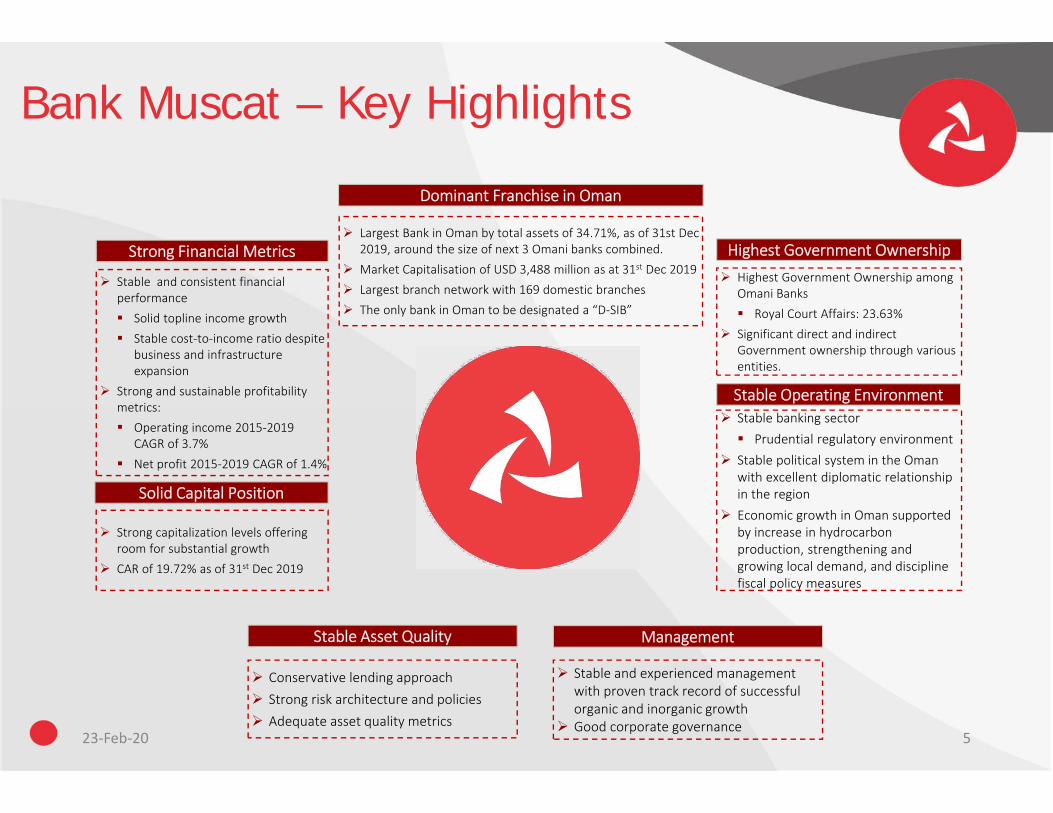

Bank Muscat – Key Highlights

Management

Largest Bank in Oman by total assets of 34.71%, as of 31st Dec 2019, around the size of next 3 Omani banks combined.

Market Capitalisation of USD 3,488 million as at 31st Dec 2019 Largest branch network with 169 domestic branches The only bank in Oman to be designated a “D‐SIB”

Strong Financial Metrics

Stable Operating Environment

Highest Government Ownership

Dominant Franchise in Oman

Highest Government Ownership among Omani Banks Royal Court Affairs: 23.63%

Significant direct and indirect Government ownership through various entities.

Stable and consistent financial performance Solid topline income growth Stable cost‐to‐income ratio despite

business and infrastructure expansion

Strong and sustainable profitability metrics: Operating income 2015‐2019

CAGR of 3.7% Net profit 2015‐2019 CAGR of 1.4%

Stable banking sector Prudential regulatory environment

Stable political system in the Oman with excellent diplomatic relationship in the region

Economic growth in Oman supported by increase in hydrocarbon production, strengthening and growing local demand, and discipline fiscal policy measures

Stable and experienced management with proven track record of successful organic and inorganic growth

Good corporate governance

Solid Capital Position

Strong capitalization levels offering room for substantial growth

CAR of 19.72% as of 31st Dec 2019

Stable Asset Quality

Conservative lending approach Strong risk architecture and policies Adequate asset quality metrics

23‐Feb‐20 6

Operating Environment

23‐Feb‐20 7

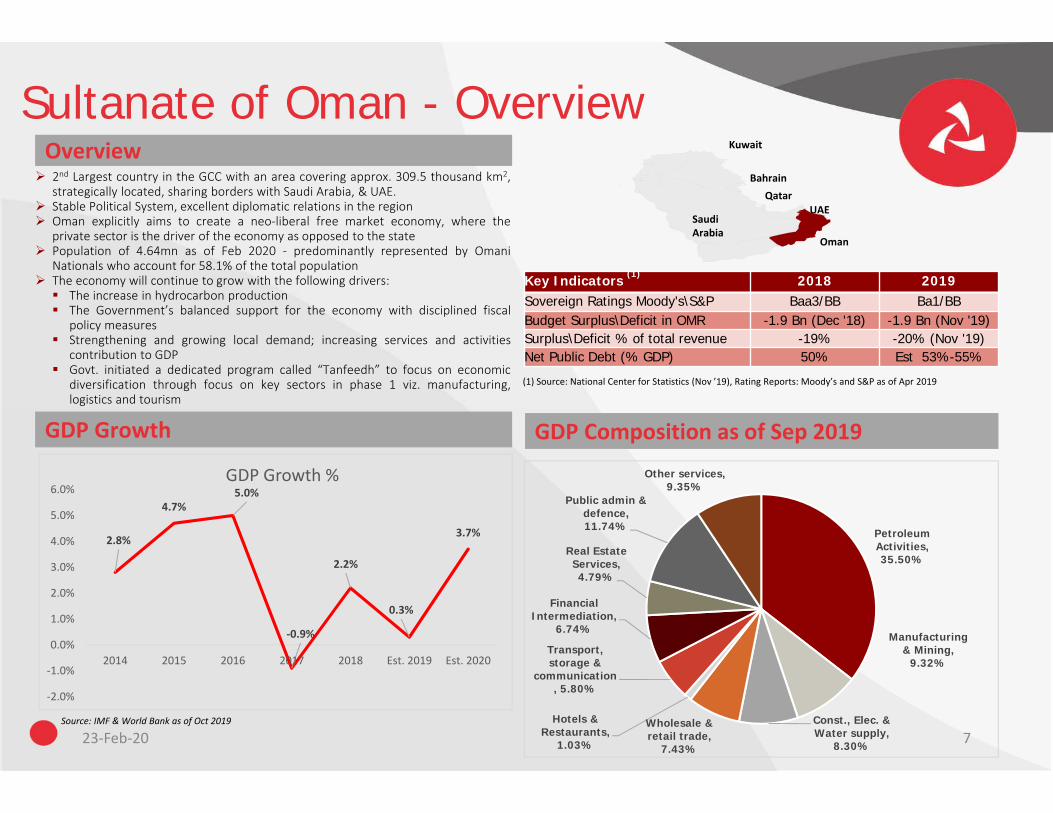

Sultanate of Oman - OverviewOverview

GDP Growth GDP Composition as of Sep 2019

(1) Source: National Center for Statistics (Nov ’19), Rating Reports: Moody’s and S&P as of Apr 2019

Oman

SaudiArabia

UAEQatar

Bahrain

Kuwait

Source: IMF & World Bank as of Oct 2019

2nd Largest country in the GCC with an area covering approx. 309.5 thousand km2,strategically located, sharing borders with Saudi Arabia, & UAE.

Stable Political System, excellent diplomatic relations in the region Oman explicitly aims to create a neo‐liberal free market economy, where the

private sector is the driver of the economy as opposed to the state Population of 4.64mn as of Feb 2020 ‐ predominantly represented by Omani

Nationals who account for 58.1% of the total population The economy will continue to grow with the following drivers: The increase in hydrocarbon production The Government’s balanced support for the economy with disciplined fiscal

policy measures Strengthening and growing local demand; increasing services and activities

contribution to GDP Govt. initiated a dedicated program called “Tanfeedh” to focus on economic

diversification through focus on key sectors in phase 1 viz. manufacturing,logistics and tourism

Key Indicators (1) 2018 2019Sovereign Ratings Moody's\S&P Baa3/BB Ba1/BBBudget Surplus\Deficit in OMR -1.9 Bn (Dec '18) -1.9 Bn (Nov '19)Surplus\Deficit % of total revenue -19% -20% (Nov '19)Net Public Debt (% GDP) 50% Est 53%-55%

Petroleum Activities, 35.50%

Manufacturing & Mining,

9.32%

Const., Elec. & Water supply,

8.30%

Wholesale & retail trade,

7.43%

Hotels & Restaurants,

1.03%

Transport, storage &

communication, 5.80%

Financial Intermediation,

6.74%

Real Estate Services, 4.79%

Public admin & defence, 11.74%

Other services, 9.35%

2.8%

4.7%5.0%

‐0.9%

2.2%

0.3%

3.7%

‐2.0%

‐1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2014 2015 2016 2017 2018 Est. 2019 Est. 2020

GDP Growth %

23‐Feb‐20 8

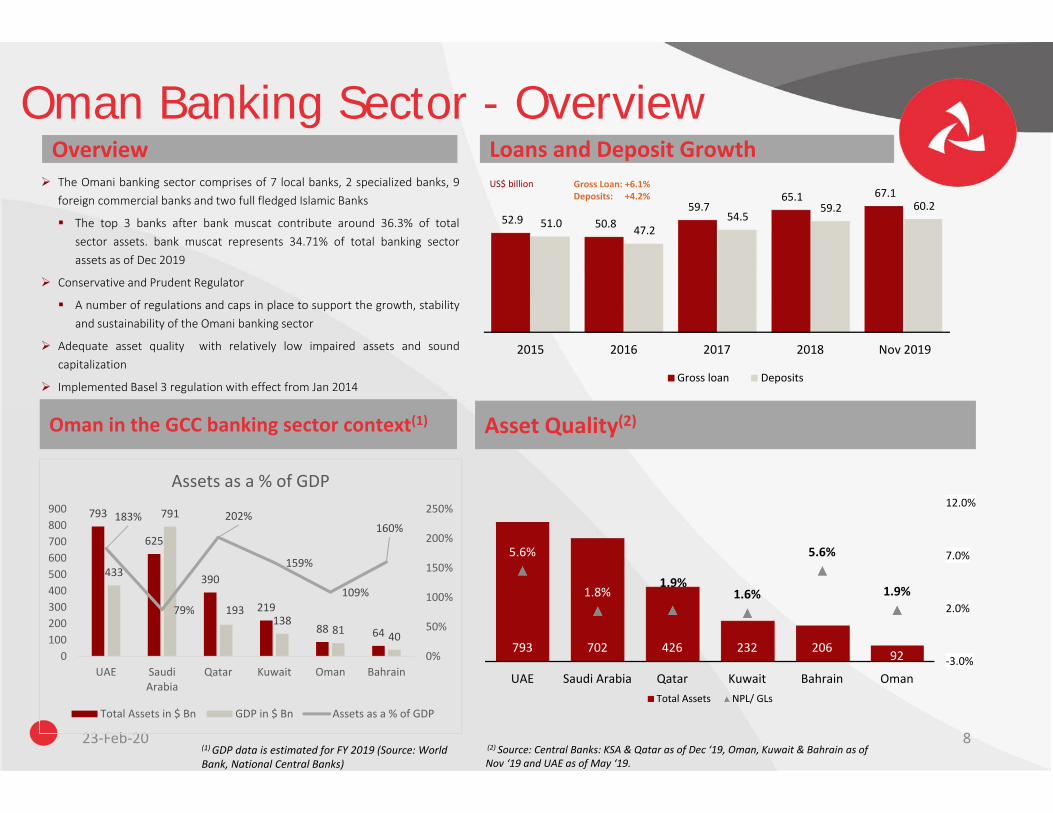

Oman Banking Sector - OverviewOverview The Omani banking sector comprises of 7 local banks, 2 specialized banks, 9

foreign commercial banks and two full fledged Islamic Banks

The top 3 banks after bank muscat contribute around 36.3% of totalsector assets. bank muscat represents 34.71% of total banking sectorassets as of Dec 2019

Conservative and Prudent Regulator

A number of regulations and caps in place to support the growth, stabilityand sustainability of the Omani banking sector

Adequate asset quality with relatively low impaired assets and soundcapitalization

Implemented Basel 3 regulation with effect from Jan 2014

Loans and Deposit Growth Gross Loan: +6.1%Deposits: +4.2%

US$ billion

Oman in the GCC banking sector context(1) Asset Quality(2)

793

625

390

219

88 64

433

791

193138

81 40

183%

79%

202%

159%

109%

160%

0%

50%

100%

150%

200%

250%

0100200300400500600700800900

UAE SaudiArabia

Qatar Kuwait Oman Bahrain

Assets as a % of GDP

Total Assets in $ Bn GDP in $ Bn Assets as a % of GDP

(2) Source: Central Banks: KSA & Qatar as of Dec ‘19, Oman, Kuwait & Bahrain as of Nov ‘19 and UAE as of May ‘19.

(1) GDP data is estimated for FY 2019 (Source: World Bank, National Central Banks)

793 702 426 232 206 92

5.6%

1.8%1.9%

1.6%

5.6%

1.9%

‐3.0%

2.0%

7.0%

12.0%

UAE Saudi Arabia Qatar Kuwait Bahrain OmanTotal Assets NPL/ GLs

52.9 50.8 59.7

65.1 67.1

51.0 47.2 54.5

59.2 60.2

2015 2016 2017 2018 Nov 2019

Gross loan Deposits

23‐Feb‐20 9

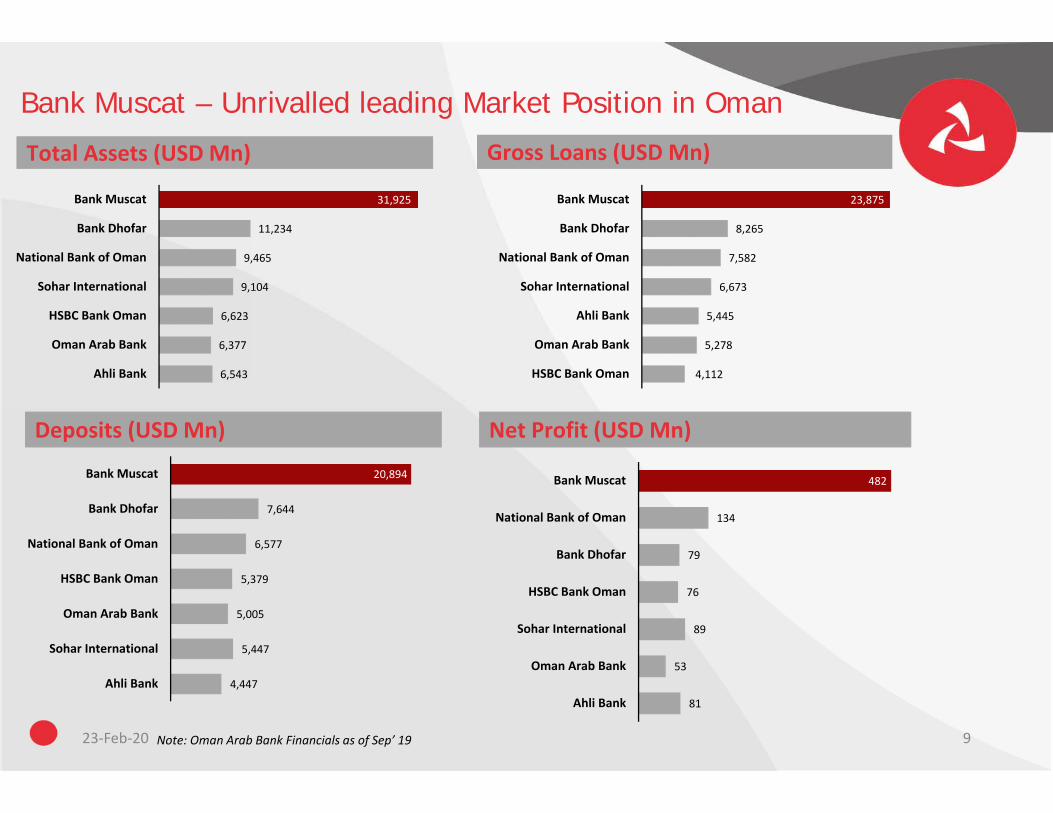

Bank Muscat – Unrivalled leading Market Position in Oman

Total Assets (USD Mn) Gross Loans (USD Mn)

Deposits (USD Mn) Net Profit (USD Mn)

Note: Oman Arab Bank Financials as of Sep’ 19

6,543

6,377

6,623

9,104

9,465

11,234

31,925

Ahli Bank

Oman Arab Bank

HSBC Bank Oman

Sohar International

National Bank of Oman

Bank Dhofar

Bank Muscat

4,112

5,278

5,445

6,673

7,582

8,265

23,875

HSBC Bank Oman

Oman Arab Bank

Ahli Bank

Sohar International

National Bank of Oman

Bank Dhofar

Bank Muscat

81

53

89

76

79

134

482

Ahli Bank

Oman Arab Bank

Sohar International

HSBC Bank Oman

Bank Dhofar

National Bank of Oman

Bank Muscat

4,447

5,447

5,005

5,379

6,577

7,644

20,894

Ahli Bank

Sohar International

Oman Arab Bank

HSBC Bank Oman

National Bank of Oman

Bank Dhofar

Bank Muscat

23‐Feb‐20 10

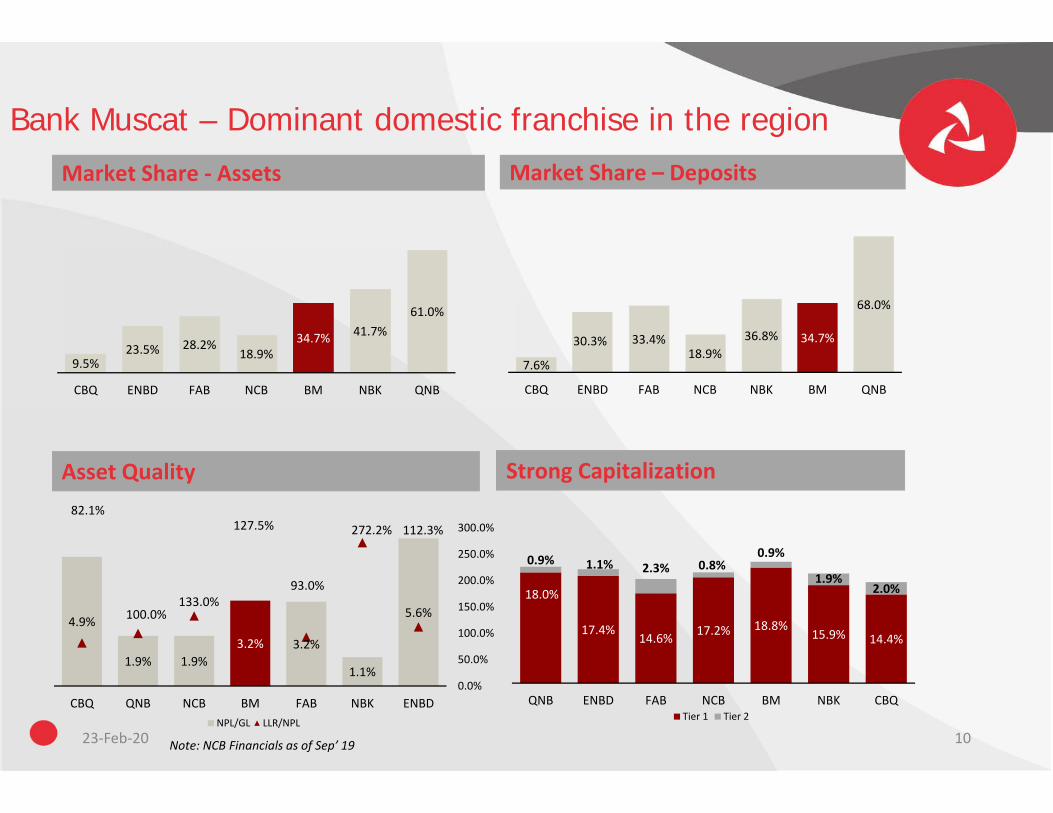

Bank Muscat – Dominant domestic franchise in the region

Market Share ‐ Assets Market Share – Deposits

Asset Quality Strong Capitalization

7.6%

30.3% 33.4%18.9%

36.8% 34.7%

68.0%

CBQ ENBD FAB NCB NBK BM QNB

4.9%

1.9% 1.9%3.2% 3.2%

1.1%

5.6%

82.1%

100.0%133.0%

127.5%

93.0%

272.2% 112.3%

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

CBQ QNB NCB BM FAB NBK ENBDNPL/GL LLR/NPL

Note: NCB Financials as of Sep’ 19

18.0%

17.4%14.6% 17.2% 18.8%

15.9% 14.4%

0.9% 1.1% 2.3% 0.8%0.9%

1.9%2.0%

QNB ENBD FAB NCB BM NBK CBQTier 1 Tier 2

9.5%23.5% 28.2%

18.9%34.7% 41.7%

61.0%

CBQ ENBD FAB NCB BM NBK QNB

23‐Feb‐20 11

Bank Muscat Business Overview

23‐Feb‐20 12

Bank Muscat Strategy – Key Pillars

Consolidate Leading Position in Oman

Capitalize on growth opportunities in Oman Infrastructure development projects and Government focus on economic diversification and developing

tourism Omanis entering the workforce; over 45% of the population is less than 19 years old

Leverage large network of branches and other delivery channels Platform to focus on the growth potential Cross sell opportunities among business lines and customer segments Continue to focus on customer acquisitions and retention

Focus on fee based income Scale up fee driven businesses both in the wholesale banking (transaction banking, investment banking,

treasury) and personal banking (credit card, bancassurance, private banking)

Leverage on technology and infrastructure investments

Pioneering investments in technology supporting growth plans Multiple digital banking channels for sales and services Technology driven banking to enhance customer experience and improve internal efficiency

Customer Convenience and Service Quality Innovative products and services offering Customer centric approach through “To Serve you better, everyday” philosophy

Regional Expansion Strengthen regional presence through focused and controlled expansion in GCC Leverage existing regional presence to scale up business growth Focus on opportunities for controlled expansion in GCC and the region

Focus on Islamic Banking Developments in Oman

Meethaq – Islamic banking platform Be the market leader in Islamic Banking Business Endeavor to offer full fledged products and services Expansion of branch and channel network

Financial strength Further enhance financial strength Strong capitalization and stable returns Further enhance the diversified funding mix and large CASA deposit base. Efficient management of operating costs

23‐Feb‐20 13

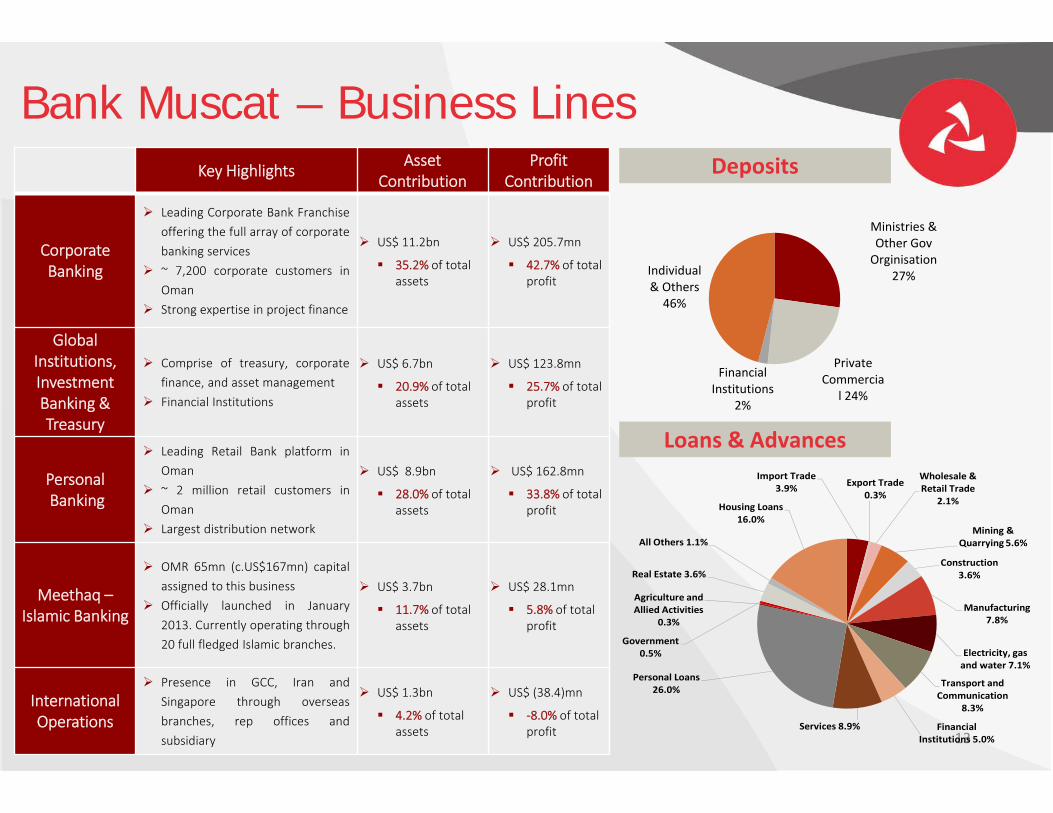

Bank Muscat – Business LinesKey Highlights Asset

ContributionProfit

Contribution

Corporate Banking

Leading Corporate Bank Franchiseoffering the full array of corporatebanking services

~ 7,200 corporate customers inOman

Strong expertise in project finance

US$ 11.2bn

35.2% of total assets

US$ 205.7mn

42.7% of total profit

GlobalInstitutions,InvestmentBanking & Treasury

Comprise of treasury, corporatefinance, and asset management

Financial Institutions

US$ 6.7bn

20.9% of total assets

US$ 123.8mn

25.7% of total profit

PersonalBanking

Leading Retail Bank platform inOman

~ 2 million retail customers inOman

Largest distribution network

US$ 8.9bn

28.0% of total assets

US$ 162.8mn

33.8% of total profit

Meethaq –Islamic Banking

OMR 65mn (c.US$167mn) capitalassigned to this business

Officially launched in January2013. Currently operating through20 full fledged Islamic branches.

US$ 3.7bn

11.7% of total assets

US$ 28.1mn

5.8% of total profit

International Operations

Presence in GCC, Iran andSingapore through overseasbranches, rep offices andsubsidiary

US$ 1.3bn

4.2% of total assets

US$ (38.4)mn

‐8.0% of total profit

Deposits

Loans & Advances

Ministries & Other Gov Orginisation

27%

Private Commercia

l 24%

Financial Institutions

2%

Individual & Others46%

Import Trade3.9% Export Trade

0.3%

Wholesale & Retail Trade

2.1%

Mining & Quarrying 5.6%

Construction3.6%

Manufacturing7.8%

Electricity, gas and water 7.1%

Transport and Communication

8.3%

Financial Institutions 5.0%

Services 8.9%

Personal Loans26.0%

Agriculture and Allied Activities

0.3%

Government0.5%

Real Estate 3.6%

All Others 1.1%

Housing Loans16.0%

23‐Feb‐20 14

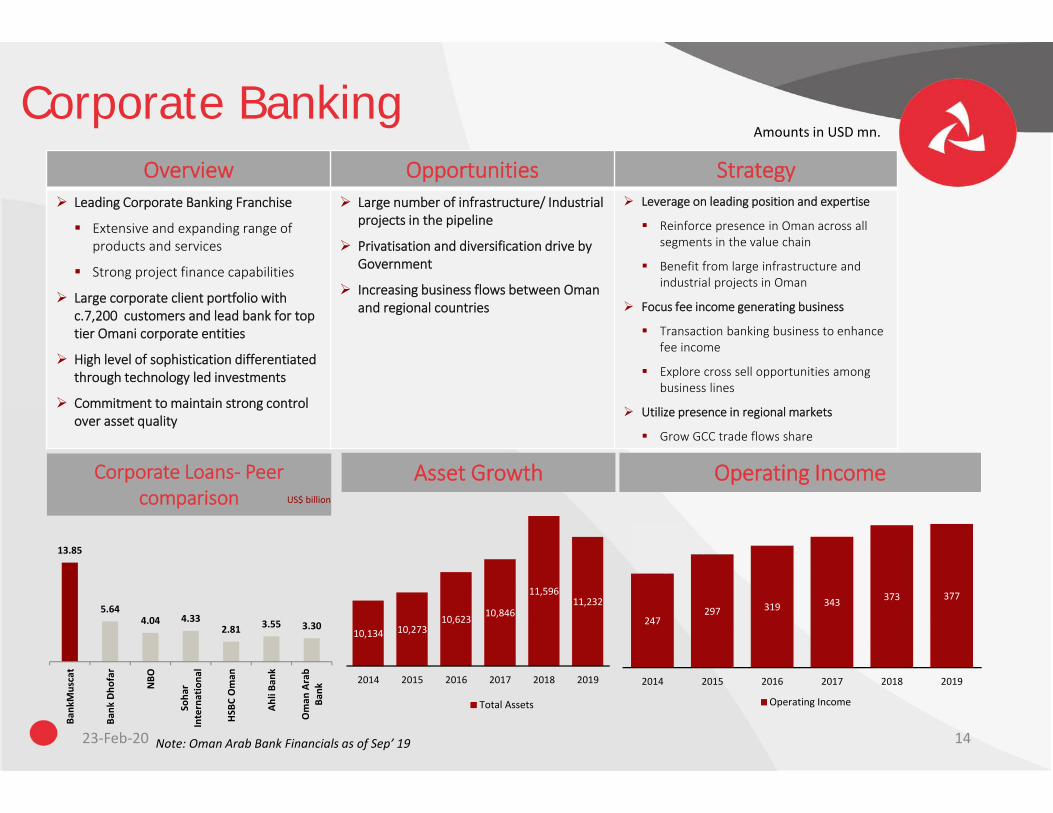

Corporate BankingAmounts in USD mn.

Overview Opportunities Strategy Leading Corporate Banking Franchise

Extensive and expanding range of products and services

Strong project finance capabilities

Large corporate client portfolio with c.7,200 customers and lead bank for top tier Omani corporate entities

High level of sophistication differentiated through technology led investments

Commitment to maintain strong control over asset quality

Large number of infrastructure/ Industrial projects in the pipeline

Privatisation and diversification drive by Government

Increasing business flows between Oman and regional countries

Leverage on leading position and expertise

Reinforce presence in Oman across all segments in the value chain

Benefit from large infrastructure and industrial projects in Oman

Focus fee income generating business

Transaction banking business to enhance fee income

Explore cross sell opportunities among business lines

Utilize presence in regional markets

Grow GCC trade flows share

Corporate Loans‐ Peer comparison

Asset Growth Operating IncomeUS$ billion

Note: Oman Arab Bank Financials as of Sep’ 19

13.85

5.644.04 4.33

2.81 3.55 3.30

Bank

Muscat

Bank

Dho

far

NBO

Soha

rInternationa

l

HSB

C Oman

Ahli Ba

nk

Oman

Arab

Bank

10,134 10,27310,623 10,846

11,59611,232

2014 2015 2016 2017 2018 2019

Total Assets

247297 319 343 373 377

2014 2015 2016 2017 2018 2019

Operating Income

23‐Feb‐20 15

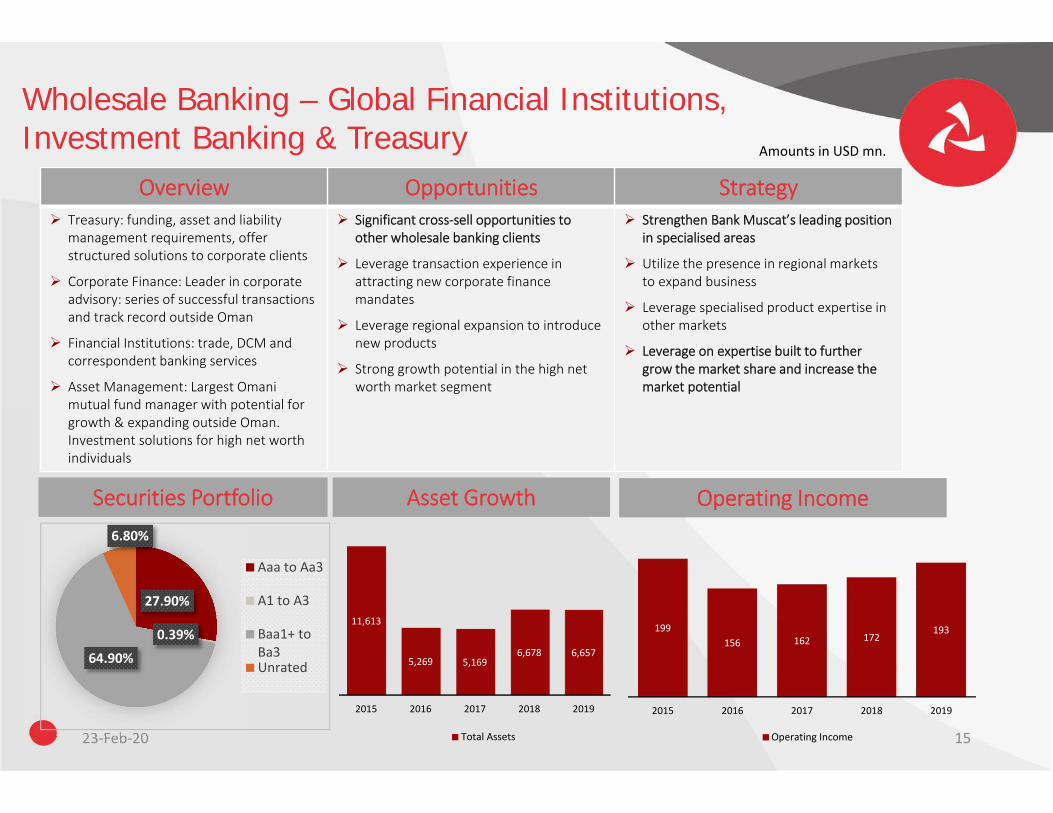

Wholesale Banking – Global Financial Institutions, Investment Banking & Treasury Amounts in USD mn.

Overview Opportunities Strategy Treasury: funding, asset and liability

management requirements, offer structured solutions to corporate clients

Corporate Finance: Leader in corporate advisory: series of successful transactions and track record outside Oman

Financial Institutions: trade, DCM and correspondent banking services

Asset Management: Largest Omani mutual fund manager with potential for growth & expanding outside Oman. Investment solutions for high net worth individuals

Significant cross‐sell opportunities to other wholesale banking clients

Leverage transaction experience in attracting new corporate finance mandates

Leverage regional expansion to introduce new products

Strong growth potential in the high net worth market segment

Strengthen Bank Muscat’s leading position in specialised areas

Utilize the presence in regional markets to expand business

Leverage specialised product expertise in other markets

Leverage on expertise built to further grow the market share and increase the market potential

Securities Portfolio Asset Growth Operating Income

27.90%

0.39%

64.90%

6.80%

Aaa to Aa3

A1 to A3

Baa1+ toBa3Unrated

11,613

5,269 5,1696,678 6,657

2015 2016 2017 2018 2019

Total Assets

199156 162 172

193

2015 2016 2017 2018 2019

Operating Income

23‐Feb‐20 16

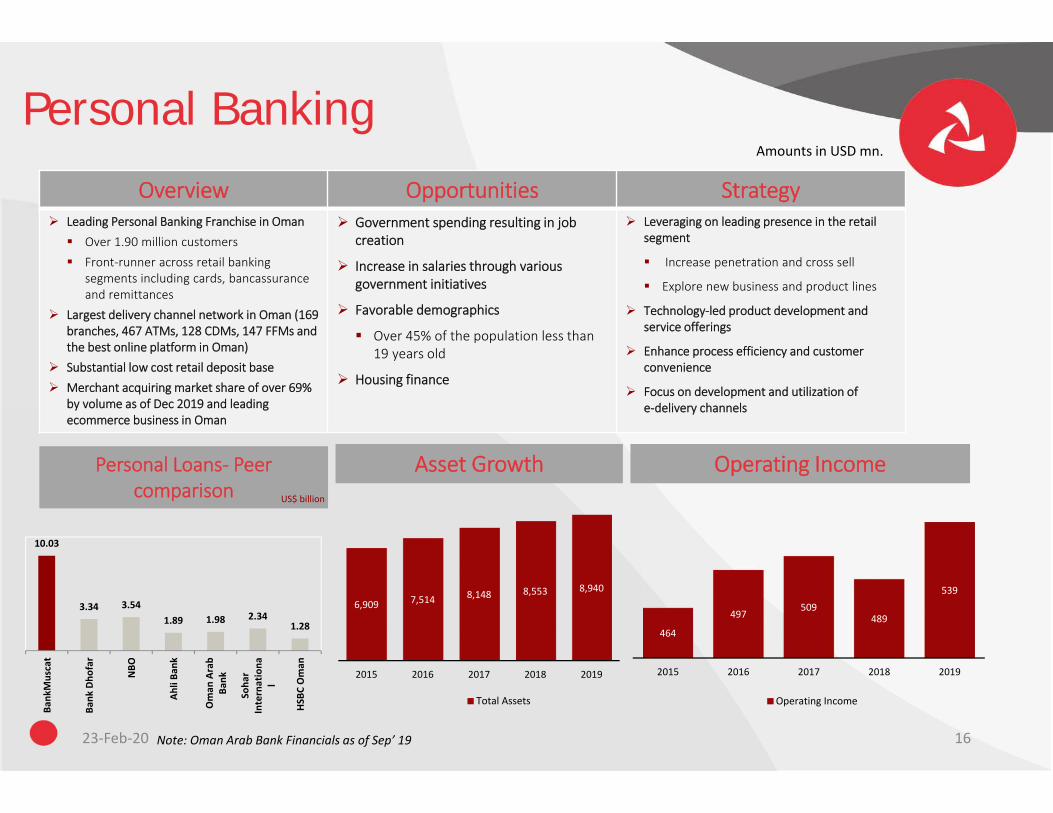

Personal BankingAmounts in USD mn.

Overview Opportunities Strategy Leading Personal Banking Franchise in Oman Over 1.90 million customers Front‐runner across retail banking

segments including cards, bancassuranceand remittances

Largest delivery channel network in Oman (169 branches, 467 ATMs, 128 CDMs, 147 FFMs and the best online platform in Oman)

Substantial low cost retail deposit base Merchant acquiring market share of over 69%

by volume as of Dec 2019 and leading ecommerce business in Oman

Government spending resulting in job creation

Increase in salaries through various government initiatives

Favorable demographics

Over 45% of the population less than 19 years old

Housing finance

Leveraging on leading presence in the retail segment

Increase penetration and cross sell

Explore new business and product lines

Technology‐led product development and service offerings

Enhance process efficiency and customer convenience

Focus on development and utilization of e‐delivery channels

Personal Loans‐ Peer comparison

Asset Growth Operating Income

Note: Oman Arab Bank Financials as of Sep’ 19

US$ billion

10.03

3.34 3.541.89 1.98 2.34

1.28

Bank

Muscat

Bank

Dho

far

NBO

Ahli Ba

nk

Oman

Arab

Bank

Soha

rInternationa

l

HSB

C Oman

6,909 7,514 8,148 8,553 8,940

2015 2016 2017 2018 2019

Total Assets

464

497509

489

539

2015 2016 2017 2018 2019

Operating Income

23‐Feb‐20 17

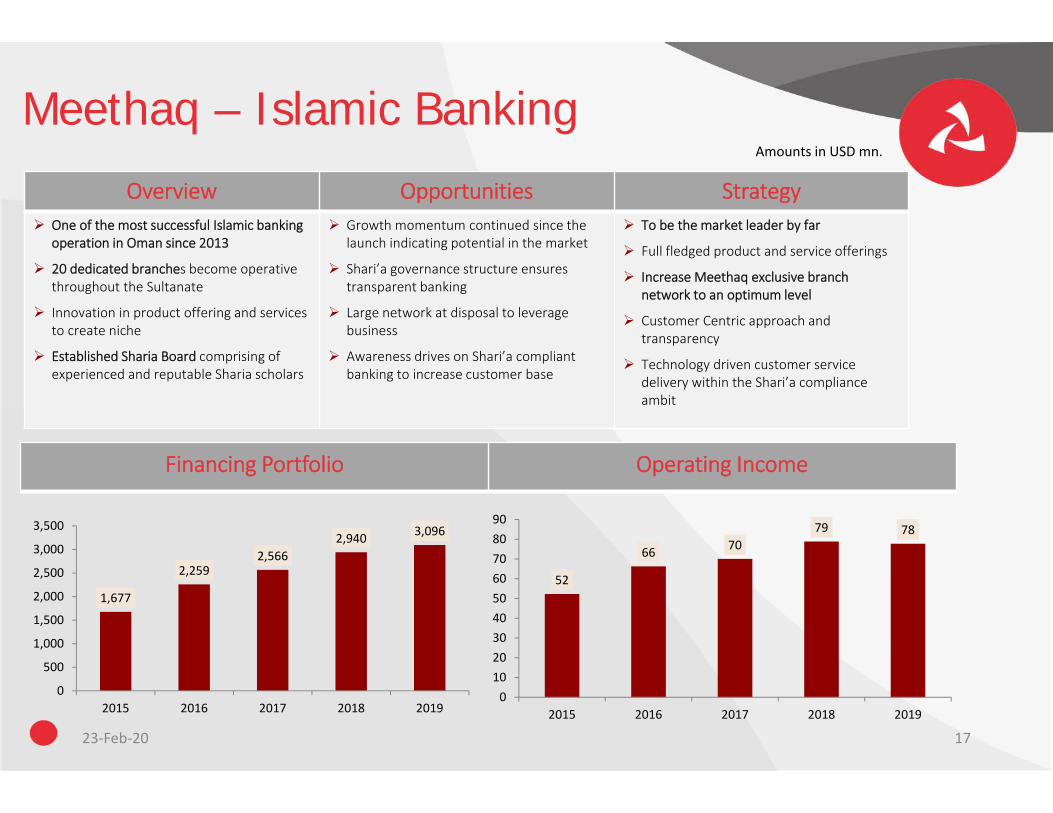

Meethaq – Islamic BankingAmounts in USD mn.

Overview Opportunities Strategy One of the most successful Islamic banking

operation in Oman since 2013

20 dedicated branches become operative throughout the Sultanate

Innovation in product offering and services to create niche

Established Sharia Board comprising of experienced and reputable Sharia scholars

Growth momentum continued since thelaunch indicating potential in the market

Shari’a governance structure ensures transparent banking

Large network at disposal to leverage business

Awareness drives on Shari’a compliant banking to increase customer base

To be the market leader by far

Full fledged product and service offerings

Increase Meethaq exclusive branch network to an optimum level

Customer Centric approach and transparency

Technology driven customer service delivery within the Shari’a compliance ambit

Financing Portfolio Operating Income

52

66 7079 78

0102030405060708090

2015 2016 2017 2018 2019

1,677

2,2592,566

2,940 3,096

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2015 2016 2017 2018 2019

23‐Feb‐20 18

Financial Performance

23‐Feb‐20 19

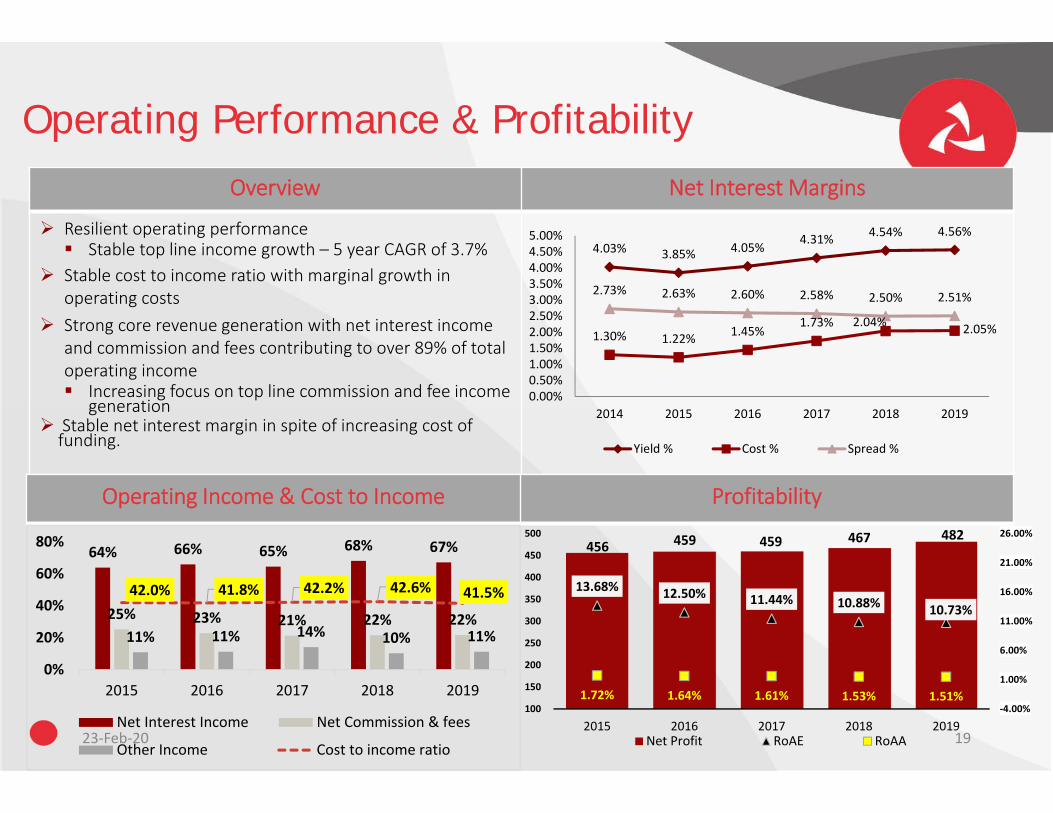

Operating Performance & ProfitabilityOverview Net Interest Margins

Resilient operating performance Stable top line income growth – 5 year CAGR of 3.7%

Stable cost to income ratio with marginal growth in operating costs

Strong core revenue generation with net interest income and commission and fees contributing to over 89% of total operating income Increasing focus on top line commission and fee income

generation Stable net interest margin in spite of increasing cost of funding.

Operating Income & Cost to Income Profitability

4.03% 3.85% 4.05% 4.31% 4.54% 4.56%

1.30% 1.22% 1.45%1.73% 2.04% 2.05%

2.73% 2.63% 2.60% 2.58% 2.50% 2.51%

0.00%0.50%1.00%1.50%2.00%2.50%3.00%3.50%4.00%4.50%5.00%

2014 2015 2016 2017 2018 2019

Yield % Cost % Spread %

456 459 459 467 482

13.68% 12.50% 11.44% 10.88% 10.73%

1.72% 1.64% 1.61% 1.53% 1.51%‐4.00%

1.00%

6.00%

11.00%

16.00%

21.00%

26.00%

100

150

200

250

300

350

400

450

500

2015 2016 2017 2018 2019Net Profit RoAE RoAA

64% 66% 65% 68% 67%

25% 23% 21% 22% 22%11% 11% 14% 10% 11%

42.0% 41.8% 42.2% 42.6% 41.5%

0%

20%

40%

60%

80%

2015 2016 2017 2018 2019

Net Interest Income Net Commission & fees

Other Income Cost to income ratio

23‐Feb‐20 20

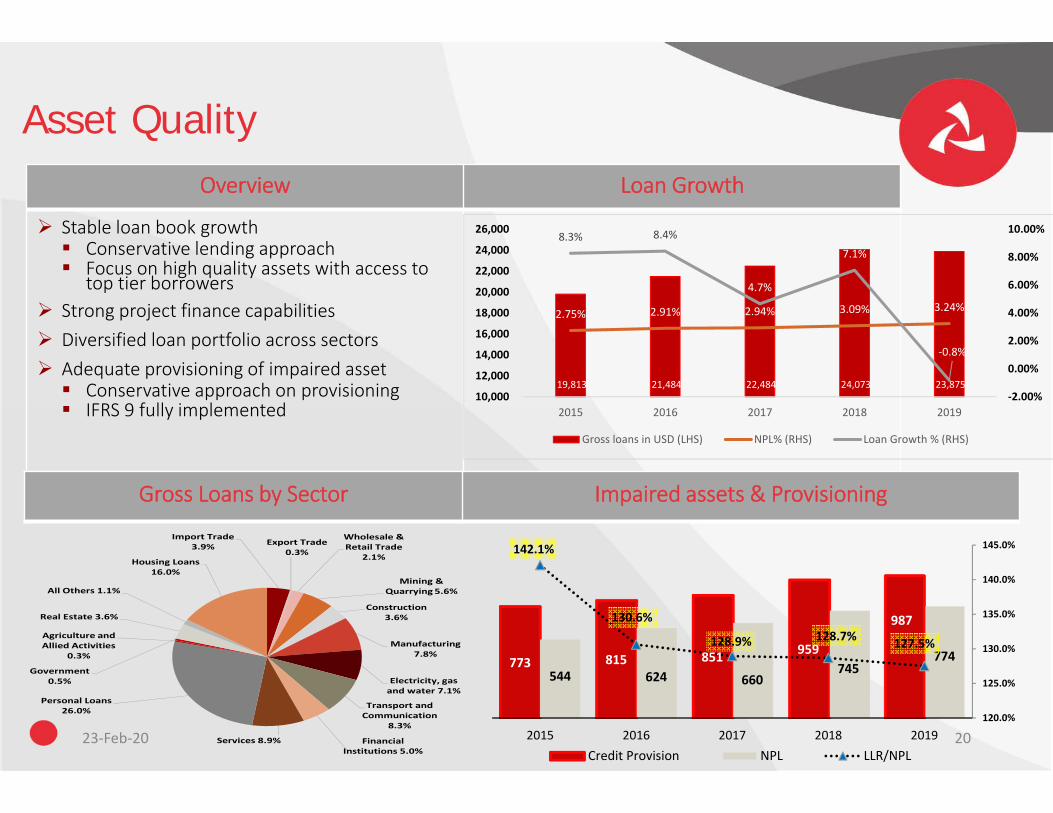

Asset QualityOverview Loan Growth

Stable loan book growth Conservative lending approach Focus on high quality assets with access to

top tier borrowers Strong project finance capabilities Diversified loan portfolio across sectors Adequate provisioning of impaired asset Conservative approach on provisioning IFRS 9 fully implemented

Gross Loans by Sector Impaired assets & Provisioning

773 815 851 959

987

544 624 660745

774

142.1%

130.6%

128.9% 128.7% 127.5%

120.0%

125.0%

130.0%

135.0%

140.0%

145.0%

2015 2016 2017 2018 2019Credit Provision NPL LLR/NPL

19,813 21,484 22,484 24,073 23,875

2.75% 2.91% 2.94% 3.09% 3.24%

8.3% 8.4%

4.7%

7.1%

‐0.8%

‐2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

2015 2016 2017 2018 2019

Gross loans in USD (LHS) NPL% (RHS) Loan Growth % (RHS)

Import Trade3.9% Export Trade

0.3%

Wholesale & Retail Trade

2.1%

Mining & Quarrying5.6%

Construction3.6%

Manufacturing7.8%

Electricity, gas and water 7.1%

Transport and Communication

8.3%

Financial Institutions 5.0%

Services 8.9%

Personal Loans26.0%

Agriculture and Allied Activities

0.3%

Government0.5%

Real Estate 3.6%

All Others 1.1%

Housing Loans16.0%

23‐Feb‐20 21

Funding & Liquidity

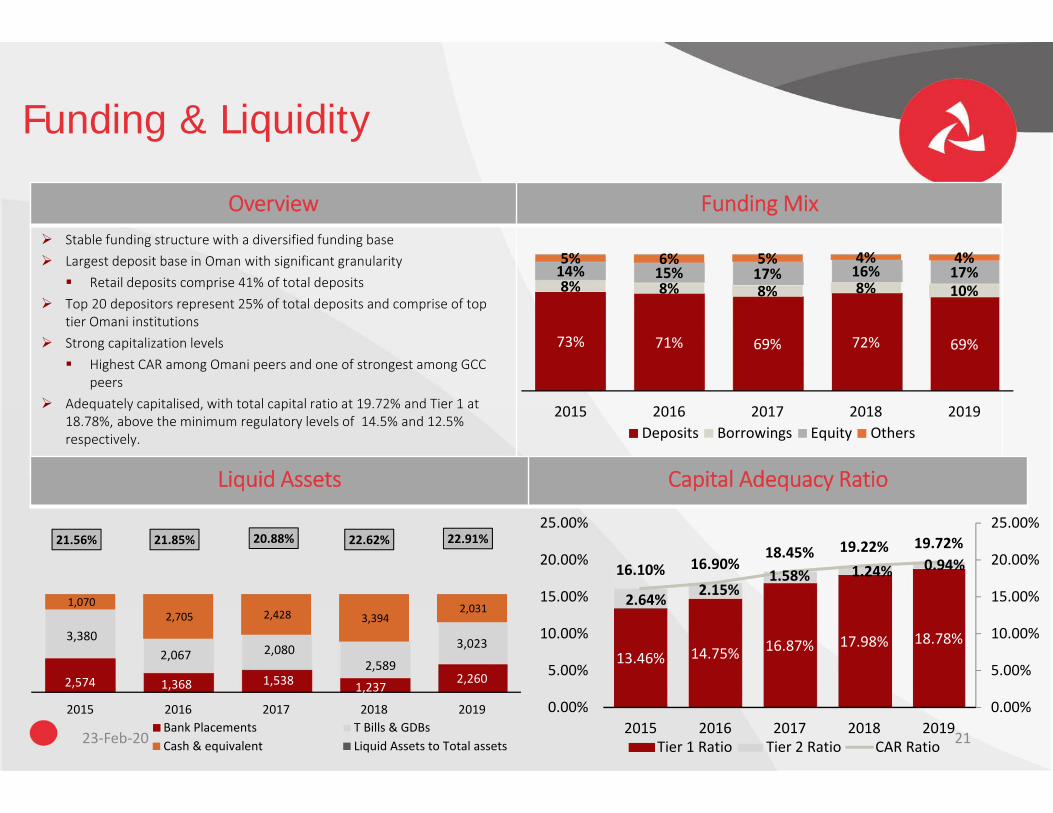

Overview Funding Mix Stable funding structure with a diversified funding base Largest deposit base in Oman with significant granularity Retail deposits comprise 41% of total deposits

Top 20 depositors represent 25% of total deposits and comprise of top tier Omani institutions

Strong capitalization levels Highest CAR among Omani peers and one of strongest among GCC

peers Adequately capitalised, with total capital ratio at 19.72% and Tier 1 at

18.78%, above the minimum regulatory levels of 14.5% and 12.5% respectively.

Liquid Assets Capital Adequacy Ratio

73% 71% 69% 72% 69%

8% 8% 8% 8% 10%14% 15% 17% 16% 17%5% 6% 5% 4% 4%

2015 2016 2017 2018 2019Deposits Borrowings Equity Others

2,574 1,368 1,538 1,2372,260

3,3802,067 2,080

2,589

3,023

1,070 2,705 2,428 3,394

2,031

21.56% 21.85% 20.88% 22.62% 22.91%

2015 2016 2017 2018 2019Bank Placements T Bills & GDBsCash & equivalent Liquid Assets to Total assets

13.46% 14.75% 16.87% 17.98% 18.78%

2.64% 2.15%1.58% 1.24% 0.94%16.10% 16.90%18.45% 19.22% 19.72%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2015 2016 2017 2018 2019Tier 1 Ratio Tier 2 Ratio CAR Ratio

23‐Feb‐20 22

Annexures

23‐Feb‐20 23

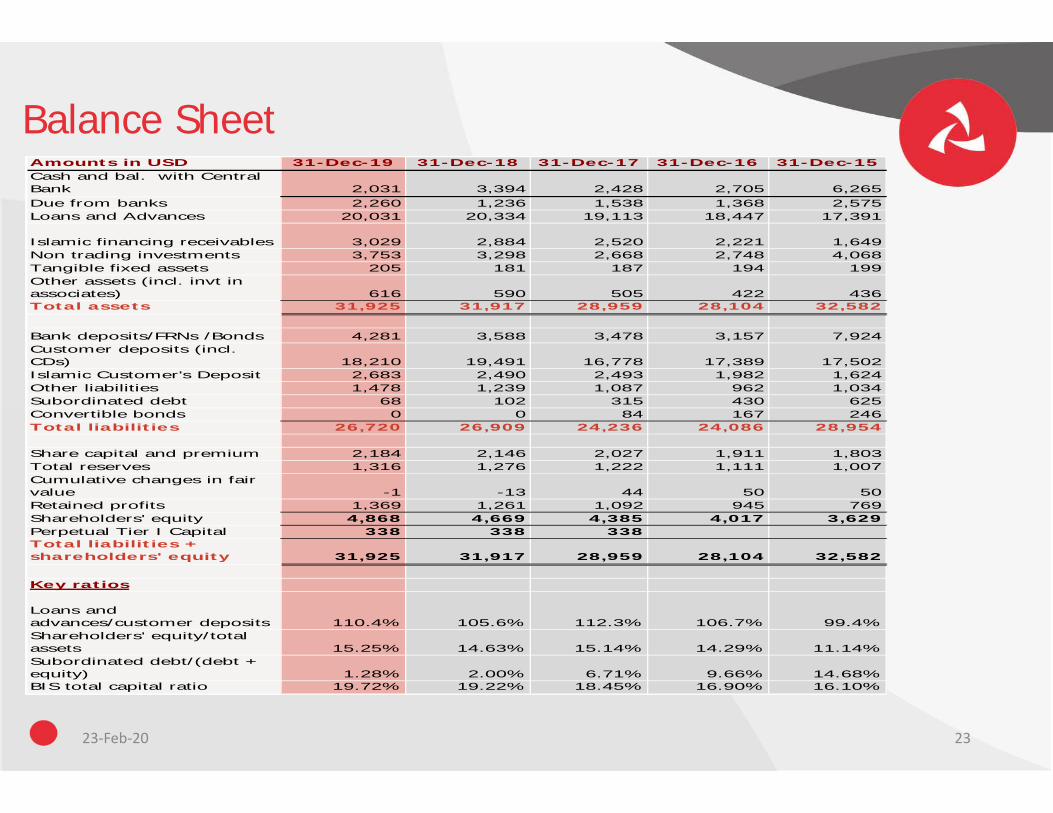

Balance SheetAmounts in USD 31-Dec-19 31-Dec-18 31-Dec-17 31-Dec-16 31-Dec-15Cash and bal. with Central Bank 2,031 3,394 2,428 2,705 6,265Due from banks 2,260 1,236 1,538 1,368 2,575Loans and Advances 20,031 20,334 19,113 18,447 17,391

Islamic financing receivables 3,029 2,884 2,520 2,221 1,649Non trading investments 3,753 3,298 2,668 2,748 4,068Tangible fixed assets 205 181 187 194 199Other assets (incl. invt in associates) 616 590 505 422 436Total assets 31,925 31,917 28,959 28,104 32,582

Bank deposits/FRNs /Bonds 4,281 3,588 3,478 3,157 7,924Customer deposits (incl. CDs) 18,210 19,491 16,778 17,389 17,502Islamic Customer's Deposit 2,683 2,490 2,493 1,982 1,624Other liabilities 1,478 1,239 1,087 962 1,034Subordinated debt 68 102 315 430 625Convertible bonds 0 0 84 167 246Total liabilities 26,720 26,909 24,236 24,086 28,954

Share capital and premium 2,184 2,146 2,027 1,911 1,803Total reserves 1,316 1,276 1,222 1,111 1,007Cumulative changes in fair value -1 -13 44 50 50Retained profits 1,369 1,261 1,092 945 769Shareholders' equity 4,868 4,669 4,385 4,017 3,629Perpetual Tier I Capital 338 338 338Total liabilities + shareholders' equity 31,925 31,917 28,959 28,104 32,582

Key ratios

Loans and advances/customer deposits 110.4% 105.6% 112.3% 106.7% 99.4%Shareholders' equity/total assets 15.25% 14.63% 15.14% 14.29% 11.14%Subordinated debt/(debt + equity) 1.28% 2.00% 6.71% 9.66% 14.68%BIS total capital ratio 19.72% 19.22% 18.45% 16.90% 16.10%

23‐Feb‐20 24

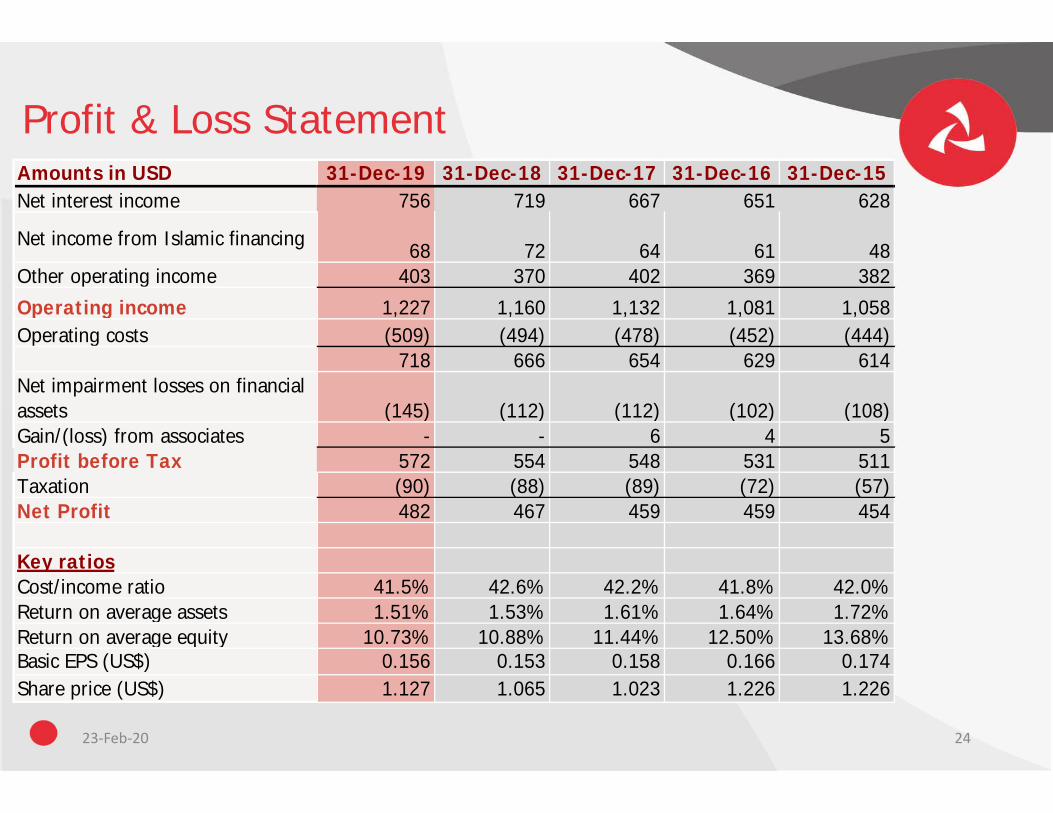

Profit & Loss StatementAmounts in USD 31-Dec-19 31-Dec-18 31-Dec-17 31-Dec-16 31-Dec-15Net interest income 756 719 667 651 628

Net income from Islamic financing 68 72 64 61 48

Other operating income 403 370 402 369 382 Operating income 1,227 1,160 1,132 1,081 1,058 Operating costs (509) (494) (478) (452) (444)

718 666 654 629 614 Net impairment losses on financial assets (145) (112) (112) (102) (108)Gain/(loss) from associates - - 6 4 5 Profit before Tax 572 554 548 531 511 Taxation (90) (88) (89) (72) (57)Net Profit 482 467 459 459 454

Key ratiosCost/income ratio 41.5% 42.6% 42.2% 41.8% 42.0%Return on average assets 1.51% 1.53% 1.61% 1.64% 1.72%Return on average equity 10.73% 10.88% 11.44% 12.50% 13.68%Basic EPS (US$) 0.156 0.153 0.158 0.166 0.174Share price (US$) 1.127 1.065 1.023 1.226 1.226