36

August 2010 Investor Presentation

1

August 2010

Investor Presentation

2

Contents

Company Snapshot1.

Business Analysis

Financial Performance

Industry Opportunity

Growth Plans & Strategy

Annexure

2.

3.

4.

5.

6.

3

Company Snapshot

4

Net Sales Break Up

Q1 FY‟11 – `2,335.5mn

One of the largest vertically integrated textile player in South India with presence

across the entire value chain - from “fibre to fashion”

Marquee relationships of over 15 years with about 1,000 regular domestic clients

for yarn and fabric and around 40 international apparel retailers

First spinning mill in India to obtain all three international certifications including

ISO 9001:2000, ISO 14001:2004 and SA 8000:2001

Investment of `1.05bn from consortium of private equity investors including Ares

Investments, Brandot Investments and Argonaut (for 11% combined stake)

Currently employs 9,802 full time employees

6 state-of-the-art production facilities

located in Tamilnadu

Total capacity of 212,064 spindles; 201

circular knitting machines and 1,750 sewing

machines

Manufacturing capacity of 54,000MT of yarn;

21,000MT of fabric and 63mn pieces of

readymade knitted apparel per annum

Processing facility for 23MT of fabric per day

Unique raw material procurement policy

Distinctive workforce model to lower attrition

and personnel costs

Strategic investment in windmill farms to

become self-sufficient with reduced dependence

on the State for energy needs (40 wind mills

installed with a total power capacity of 40MW)

Presence across the Textile Value Chain

Complete Textile Solutions Provider

Knitted Garments,

27.2%

Fabric, 13.3%

Yarn, 55.9%

Others, 3.6%

State-of-the-Art Manufacturing Facilities Cost-effective Operating Model

5

4,3914,974

6,064

7,477

8,340

0

1,800

3,600

5,400

7,200

9,000

FY'06 FY'07 FY'08 FY'09 FY'10

Total Operating Revenue EBITDA

Net Worth

Note: EBITDA declined during FY’09 due to significant increase in raw material prices and other direct expenses

With consistent track record of growth`M

n

`Mn

6

Yarn Sales (`mn)

2,0672,450

3,3353,654

4,088

0

900

1,800

2,700

3,600

4,500

FY'06 FY'07 FY'08 FY'09 FY'10

736810 776

902

1,139

0

240

480

720

960

1200

FY'06 FY'07 FY'08 FY'09 FY'10

Led by increasing sales across key segments

Yarn Sales (MT)

20,27422,473

32,793 32,440 32,882

0

7,000

14,000

21,000

28,000

35,000

FY'06 FY'07 FY'08 FY'09 FY'10

Yarn sales grew at a 4-year CAGR of 18.6% to reach `4,088mn in FY‟10 driven by 1.6x growth in volumes

Fabric Sales (`mn) Fabric Sales (MT)

6,1395,608

7,325

9029

10,690

0

2,000

4,000

6,000

8,000

10,000

12,000

FY'06 FY'07 FY'08 FY'09 FY'10

Fabric sales grew at a 4-year CAGR of 11.5% to reach `1,139mn in FY‟10 driven by 1.7x growth in volumes

7

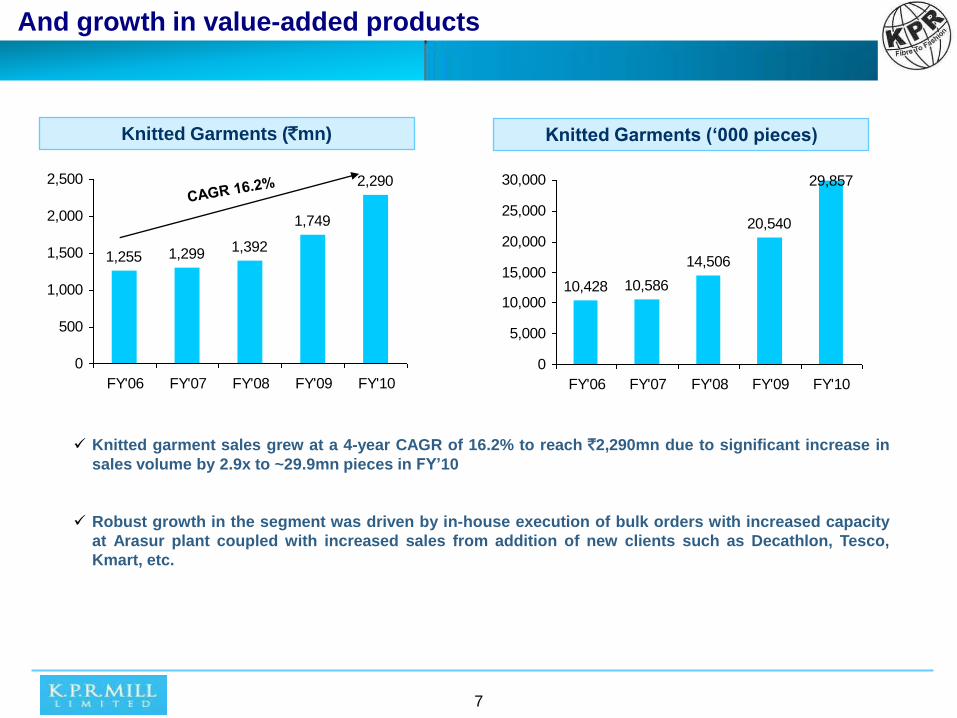

Knitted Garments (`mn)

1,255 1,299 1,392

1,749

2,290

0

500

1,000

1,500

2,000

2,500

FY'06 FY'07 FY'08 FY'09 FY'10

Knitted garment sales grew at a 4-year CAGR of 16.2% to reach `2,290mn due to significant increase in

sales volume by 2.9x to ~29.9mn pieces in FY‟10

Robust growth in the segment was driven by in-house execution of bulk orders with increased capacity

at Arasur plant coupled with increased sales from addition of new clients such as Decathlon, Tesco,

Kmart, etc.

And growth in value-added products

Knitted Garments („000 pieces)

10,428 10,586

14,506

20,540

29,857

0

5,000

10,000

15,000

20,000

25,000

30,000

FY'06 FY'07 FY'08 FY'09 FY'10

8

Backed by an experienced management team

Name Brief Profile

Mr. K. P. Ramasamy

Chairman•Over 38 years of experience in the apparel business, particularly in the production and marketing of woven

fabric, knitted apparel, cotton yarn and hosiery fabric as well as in dyeing of yarn and fabric

•Spearheads the strategic expansion plan initiatives of the company and supervises manufacturing and

human resource related functions

Mr. K.P.D Sigamani

Managing Director•Holds a Master of Science degree in Mathematics

•Over 25 years of experience in the apparel industry, with specialized experience in the production and

marketing of Knitted apparel

•Heads the apparel division and also supervises company’s export business

Mr. P. Nataraj

Managing Director•Chartered Accountant and holds a Bachelor of Science degree

•Over 2 decades of experience in the apparel industry and is also experienced in internal controls, project

implementation and tax planning

•Special invitee at the South India Mills Association and also the President of the Coimbatore chapter of the

Indian Institution of Industrial Engineering 2003 -2004

•Manages the finance function and also oversees cotton procurement and yarn marketing activities of the

spinning division

Mr. Shujaat Khan

Non-Executive Director•MBA from Harvard University

•Nominee of ‘Ares Investments' on the Board and is associated with the company since November 2006 as

non-independent director

•Over 16 years of experience in investment banking and private equity activities

•Was the Managing Director of ChrysCapital for 4 years from 2000 and worked with Merrill Lynch

International in Asia for 4 years from 1997 and with the Travelers Group in New York for 5 years from 1991

•Managing Director of Blue River Capital Advisors (India) Private Limited since 2005

9

And a strong board of directors

Name Brief Profile

Mr. K.N.V. Ramani

Non-Executive Director•Corporate lawyer and independent director of the company. Has been practicing for over 47 years in legislations like the

Companies Act, Taxation and Labour Laws

•Presently the senior partner of the law firm M/s. Ramani & Shankar, Advocates, Coimbatore

•Holds directorships in Bannari Amman Spinning Mills Ltd., Sri Kannapiran Mills Ltd., Sri. Chamundeswari Sugars Ltd., K.G.

Denim Ltd and L.G.B. Forge Ltd

Mr. M.J. Vijyaraaghavan •An independent director and is associated with the company since October 2006

Non-Executive Director •Chartered Accountant by profession and has over 4 decades of experience

•Senior partner of M.S. Jagannathan & Visvanathan, the statutory auditors of leading companies located in Coimbatore,

Bangalore and Kerala

Dr. K. Sabapathy •An independent director and the Chairman of the Investors Grievance Committee

Non-Executive Director •Holds degree of Master of Science, Master of Philosophy and Ph.D. in Physics

•A member of the Coimbatore Stock Exchange for 16 years since 1992 and was its Vice President during 2003 and 2005 and

also held the position of Director in Inter Connected Stock Exchange of India Ltd at Mumbai during 2002 -2005

Mr. A. Sekar •Joined in Sree Ramakrishna Textiles as an employee and is a non-independent director

Whole-time Director •Over 21 years experience in the apparel industry

•Has been assisting the management in setting up of various units and implementation of several projects including expansion

programme, right from the inception of the company

Mr. A.M. Palanisamy

Non-Executive Director•Chartered Accountant for 16 years with specialization of production planning, financials management and taxation

•Holds a bachelors degree in Commerce and is an F.C.A.

•Presently the Chairman of Aerospace Materials Private Limited, Pollachi, Coimbatore

•Holds Directorship in Kovai Medicals Center and Hospital Ltd, Coimbatore and Tanmic India Pvt Ltd

•Management Trustee in Vivek Vidyalaya Matric Higher Secondary School, Kinathukadavu, Orison School Coimbatore, Dharma

Chakkara Trust

•Member of Systems Society of India and Indian Carbon Society, New Delhi

Mr. G.P. Muniappan

Non-Executive Director•An independent director of the company and specialized in the areas of Forex management, banking operations, banking

regulations and supervision

•University rank holder in M.A. Economics

•Elevated to prestigious position of ‘Deputy Governor of R.B.I.' in 2001 and held positions such as Chairman of Bank of Madura,

R.B.I.'s Nominee on SEBI Board, Indian Overseas Bank, Indian Bank and a Trustee of U.T.I.

10

Business Analysis

11

49% 51%58%

51% 51% 56%

17% 17%14%

13% 14%13%

30% 27% 24%24%

29%27%

4% 5% 4% 12% 6%4%

0%

20%

40%

60%

80%

100%

FY06 FY 07 FY 08 FY 09 FY'10 Q1 FY'11

Yarns Fabrics Knitted Garments Export Others

Product Mix

Well-defined vertically integrated operations

Largest revenue contributing

segment with over 50% share of

the revenues. Both carded and

combed yarn are produced

In-house consumption: 25%-

30% of total production.

Remaining is sold in domestic

markets

Contributed 13% of the revenues

during Q1 FY‟11.

In-house consumption: 25%-30%

of total production. Remaining is

sold in domestic markets

Contributed 27% of the revenues

during Q1 FY‟11

100% production exported to the

US and European countries.

Outsources small orders to local

manufacturers and executes bulk

orders in-house to achieve

efficiency

Yarn Fabric Knitted Garments

12

With strong & diversified client base

Over 15 years of relationship with a diversified customer base of over 1,000 regular

domestic clients

Strong relationships with over 40 international apparel retailers

Some Key International Customers

Ernsting‟s

Family

13

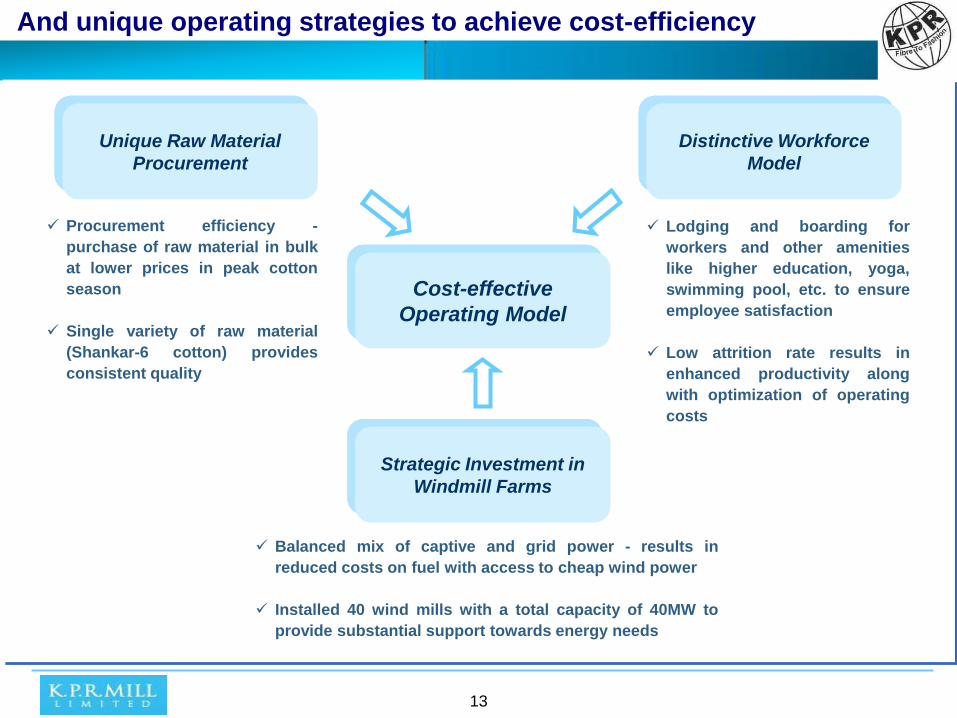

And unique operating strategies to achieve cost-efficiency

Cost-effective

operating model

Procurement efficiency -

purchase of raw material in bulk

at lower prices in peak cotton

season

Single variety of raw material

(Shankar-6 cotton) provides

consistent quality

Lodging and boarding for

workers and other amenities

like higher education, yoga,

swimming pool, etc. to ensure

employee satisfaction

Low attrition rate results in

enhanced productivity along

with optimization of operating

costs

Balanced mix of captive and grid power - results in

reduced costs on fuel with access to cheap wind power

Installed 40 wind mills with a total capacity of 40MW to

provide substantial support towards energy needs

Unique Raw Material

Procurement

Distinctive Workforce

Model

Strategic Investment in

Windmill Farms

Cost-effective

Operating Model

14

Strategically located manufacturing facilities

Location of Facilities Nature of Work Capacity

Sathyamangalam Spinning 30,240 spindles

Karumathampatti Spinning 30,240 spindles

Neelambur Spinning & Knitting 50,784 spindles

Arasur Spinning, Knitting &

Garmenting

1,00,800 spindles

Garmenting :85,000 pieces per day

(single shift)

Storage : 450 tons

Tirupur Garmenting 12mn pieces capacity outsource

SIPCOT, Perundurai Fabric Processing 23 tons/day

Tirunelveli, Tenkasi & Coimbatore Wind Mills (40 nos.) 40MW

Facilities located within a 50km radius from Tirupur, regarded as one of the Asia’s largest apparel

manufacturing clusters

Proximity to buyers helps to reduce the material handling costs and facilitates immediate feedback

regarding the quality of the product

Utilize the key technical personnel across all plant sites and allows taking advantage of Coimbatore

climate, conducive for spinning operations

15

Enforcing stringent quality control measures

Accreditations:

ISO 9001: 2000 – certification for quality management system

ISO 14001: 2004 – certification for environmental management systems

SA 8000: 2001 – certification for social accountability management system

Certified by International Association for Research and Testing in the field of Textile Ecology with respect to

apparel manufacturing operations

Certified as a Trading House by the Indian Ministry of Commerce and Trade

Global Organic Textile Standard (GOTS) - for organic cotton products

OEKO-TEX for responsible and ethical endeavors

Ethical Trade Initiative (ETI) for sound working condition of workers

WRAP – Worldwide Responsible Apparel Production

TUV- SIMA- A Five Star category indicating ‘Excellence in Code of Discipline’ for providing women employment

Installation of high-tech quality control equipment such as Uster Tester-4, Uster HVI Spectrum, Uster AFIS Pro,

Zweigle Hariness Tester-G566 and Uster Classimat Quantum

Latest technology equipment Jossi Vision Shield for contamination free yarn

Installed Schlafhorst Autoconer that ensures sophistication and homogenous quality in yarn and better productivity

Mandatory usage of hand gloves, hair net, mask, aprons, etc. for the twin benefits of safety and quality

Inspection at every stage to ensure stringent quality conformance

Quality Control Initiatives:

16

Financial Performance

17

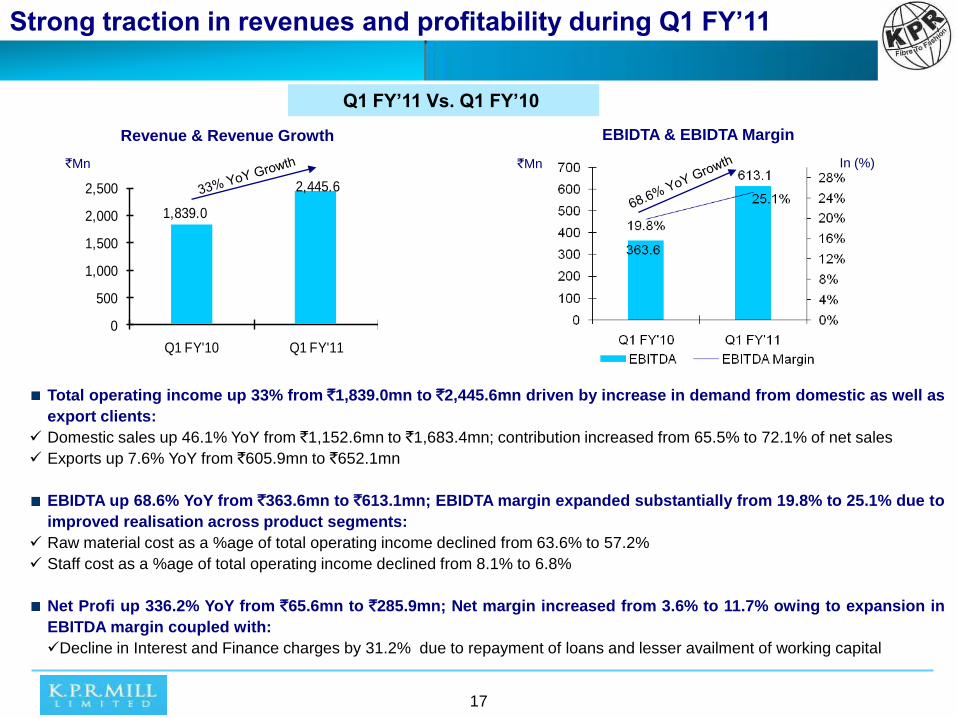

Q1 FY‟11 Vs. Q1 FY‟10

Total operating income up 33% from `1,839.0mn to `2,445.6mn driven by increase in demand from domestic as well as

export clients:

Domestic sales up 46.1% YoY from `1,152.6mn to `1,683.4mn; contribution increased from 65.5% to 72.1% of net sales

Exports up 7.6% YoY from `605.9mn to `652.1mn

EBIDTA up 68.6% YoY from `363.6mn to `613.1mn; EBIDTA margin expanded substantially from 19.8% to 25.1% due to

improved realisation across product segments:

Raw material cost as a %age of total operating income declined from 63.6% to 57.2%

Staff cost as a %age of total operating income declined from 8.1% to 6.8%

Net Profi up 336.2% YoY from `65.6mn to `285.9mn; Net margin increased from 3.6% to 11.7% owing to expansion in

EBITDA margin coupled with:

Decline in Interest and Finance charges by 31.2% due to repayment of loans and lesser availment of working capital

`Mn

1,839.0

2,445.6

0

500

1,000

1,500

2,000

2,500

Q1 FY'10 Q1 FY'11

Strong traction in revenues and profitability during Q1 FY‟11

Revenue & Revenue Growth EBIDTA & EBIDTA Margin

`Mn In (%)

18

With robust growth witnessed across all key segments

Knitted Garment Exports

Net Sales from Knitted Garment exports up 5.4% from

`603.5mn to `635.9mn: Sales volume increased by 16.3%

from 8,131(‘000 pieces) to 9,457(‘000 pieces)

Fabric

230.7

310.8

Q1 FY'10 Q1 FY'11

Net Sales from Fabrics up 34.7% from `230.7mn to

`310.8mn: Sales volume decreased by 7.2% from

2,520MT to 2,339MT

Yarn

805.6

1,304.3

Q1 FY'10 Q1 FY'11

Net Sales from Yarn up 61.9% YoY from `805.6mn to

`1,304.3mn: Sales volume increased by 25.3% from

6,890MT to 8,630MT

Others

118.6

84.4

Q1 FY'10 Q1 FY'11

Contribution from others (including dyed fabrics, waste and

others) down by 28.8% from `118.6mn to `84.4mn

603.5

635.9

Q1 FY'10 Q1 FY'11

19

Industry Opportunity

20

Huge growth potential in the industry

67

115

0

30

60

90

120

150

2009 2012E

Source: Technopak, Ministry of Textiles estimates

Size of Indian Textile Industry ($ bn)

Indian textiles industry is currently pegged at $67bn in size and is likely to grow by 1.7x to reach $115bn

by 2012

Growth to be largely driven by export contribution expected to constitute 44% of the total market size in

2012E from current ~33%; exports to grow at a 3 year CAGR of ~31% to reach $50bn in size by 2012

Domestic consumption also likely to remain robust, witnessing 3-year CAGR of 13% to reach $65bn in

size by 2012

Contribution of the export market to the total industry size is estimated to increase from 33% at present

to 44% by 2012

67%56%

33%44%

0%

20%

40%

60%

80%

100%

2009 2012E

Domestic Export

Exports Vs Domestic

21

Backed by key growth drivers

Abundant

Raw Material

Availability

Growing Domestic

Demand

Low Cost Skilled

Labour

2nd largest producer

of cotton in the world

Accounts for 12% of

the world's production

of textile fibre and yarn

Domestic textile

market is growing at

a very good pace

driven by favorable

demographics

Abundant availability

of manpower with skill

sets across the value

chain

Cost advantage over

comparative countries

with low labour cost

Backed by Government Initiatives

22

And strong support extended by the Government

Technology Upgradation Fund Scheme (TUFS): Allocation of `31.4bn for the current fiscal for TUFS scheme. Though,

TUFS has been temporarily withdrawn – it would provide KPR with competitive edge as it has already received loan

under TUFS for its ongoing expansion whereas other players might have to put their capex plans on hold

Government intervention has persuaded the spinners to reduce yarn prices by `6 - `9 per kg which would benefit

weavers and apparel producers

Exemption of readymade garments from 4% Special Additional Duty (SAD)

Continued interest subvention of 2% for one more year for exports covering textiles

One-time grant of `2bn to Tamil Nadu towards the cost of installation of a zero liquid discharge system at Tirupur

Current limit of `1,00, 000 per annum for duty free import of samples has been enhanced to `3,00,000 per annum

SMEs in textile sector have been given full CENVAT credit on capital goods in one installment in the year of receipt of

such goods and the facility of payment of excise duty in quarterly basis

Government policies have been largely supportive of growth of the textile industry, given its

potential for export and employment generation:

23

With increasing global competitiveness

Indian Textile Industry will have a competitive advantage vis-à-vis China in global market due to:

Increasing labor costs in China on account of Minimum Wages Act

Appreciation of Chinese currency

Higher power cost

24

Growth Plans & Strategy

25

Increased focus on high margin garment export segment

Current Revenue Mix (Q1 FY‟11)

Export contribution expected to increase to 40% of the revenues by FY‟12 from 29% at

present (Q1 FY‟11)

Plans to double contribution from US and other markets to 20% in next 4-5 years from

~10% in Q1 FY‟11

Projected Revenue Mix (FY‟12)

26

Along with expansion in 100% compact spinning capacity

Planned expenditure of `4.38bn for capacity expansion in 100% compact spinning facility

100% Compact Spinning Facility:

Incremental capacity addition: 1,03,680 spindles

Capital Expenditure: `3.1bn Expansion to be partly financed through balance IPO proceeds and partly through debt

for which financial closure has been achieved

Expansion is expected to be completed by end of April 2011 in phased manner and plant to be fully operational from

May 2011

Capacity addition to take place adjacent to the existing plant of Karumathampatti in order to achieve cost and

location benefits

27

And modernization of existing facility for productivity enhancement

Modernization of Sathyamangalam spinning unit to increase productivity and enhance quality of output :

Modernize the existing 30,240 spindleage at the spinning unit at Sathyamangalam by replacing the existing ring

frames by new ring frames

Expand existing spindleage capacity by adding 17,952 spindles of recently launched LR9/AX 1,632 spindles with

cutting edge technologies. This would result in considerable reduction in per spindle cost

Total Project Outlay: `300mn. Financial closure has been achieved

28

Attaining self-sufficiency for power requirement

60%

75%

90% 90% 90%

0%

20%

40%

60%

80%

100%

Q1 FY'10 Q2 FY'10 Q3 FY'10 Q4 FY'10 Q1 FY'11

Quarterly Capacity Utilization

One of the largest in-house power generation capacity (installed 40MW windmills), sufficient to meet about

75% of the power requirement through captive consumption

Further plans to add wind power generation plant to support expansion in 100% compact spinning:

Incremental capacity addition: 24MW windmills

Capital Expenditure: `1.28bn

Turnkey project expected to be completed by end of November 2010 in a phased manner

40

64

0

15

30

45

60

75

FY'10 FY'11

Expansion in Capacity

29

Thank You Annexure

30

Shareholding pattern as of 30th June 2010

No. of shares outstanding: 37.68mn

Promoters,

74.48%

Body Corporate, 4.69%

FIIs, 0.35%

Foreign Venture Capital

Investors, 9.29%

Others, 9.70%

MFs/Banks, 1.49%

31

Income Statement & Key Ratios - Quarterly

Particulars (`mn) Q1 FY'11 Q1 FY'10 % Chg YoY Q4 FY'10 % Chg QoQ

Net sales 2,335.5 1,758.5 32.8% 2,439.5 -4.3%

Other Operating Income 110.1 80.6 36.7% 235.4 -53.2%

Total Operating Income 2,445.6 1,839.0 33.0% 2,674.9 -8.6%

Total Expenditure 1,832.4 1,475.5 24.2% 2,186.6 -16.2%

(Increase) / Decrease In Stock In Trade & WIP (67.1) (65.5) NA (17.4) NA

Consumption of Raw Materials 1,466.2 1,234.7 18.7% 1,584.3 -7.5%

Employees Cost 165.4 149.4 10.7% 154.9 6.7%

Other Expenditure 268.0 156.8 70.9% 464.8 -42.3%

EBIDTA 613.1 363.6 68.6% 488.3 25.6%

Depreciation 177.4 174.4 1.7% 175.1 1.3%

EBIT 435.8 189.2 130.4% 313.2 39.1%

Interest & Finance charges 58.6 85.3 -31.2% 54.4 7.9%

Other Income 4.3 4.4 -0.6% 5.4 -20.3%

PBT 381.5 108.2 252.4% 264.3 44.4%

Tax Expense 95.6 42.7 124.0% 102.2 -6.4%

PAT 285.9 65.6 336.0% 162.1 76.3%

Basic & Diluted EPS (Rs.) 7.6 1.7 336.2% 4.3 76.5%

Key Ratios Q1 FY'11 Q1 FY'10 Q4 FY'10

EBIDTA Margin 25.1% 19.8% 18.3%

Net Margin 11.7% 3.6% 6.1%

Total Expenditure/ Total Operating Income 74.9% 80.2% 81.7%

Raw Material Cost/ Total Operating Income 57.2% 63.6% 58.6%

Staff Cost/ Total Operating Income 6.8% 8.1% 5.8%

Other Expenditure/ Total Operating Income 11.0% 8.5% 17.4%

32

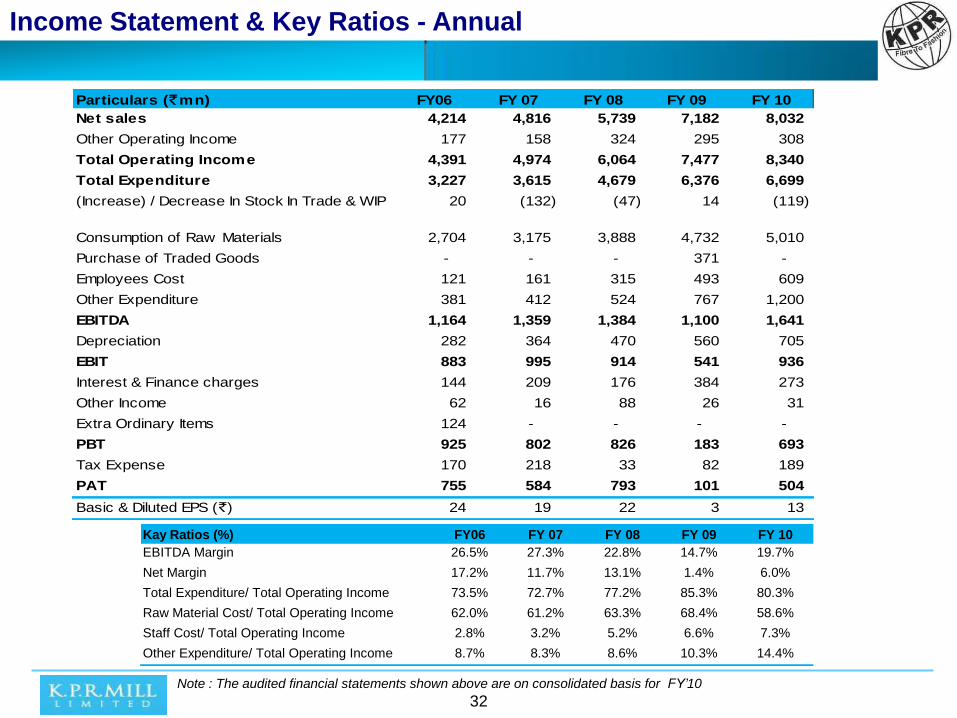

Income Statement & Key Ratios - Annual

Kay Ratios (%) FY06 FY 07 FY 08 FY 09 FY 10

EBITDA Margin 26.5% 27.3% 22.8% 14.7% 19.7%

Net Margin 17.2% 11.7% 13.1% 1.4% 6.0%

Total Expenditure/ Total Operating Income 73.5% 72.7% 77.2% 85.3% 80.3%

Raw Material Cost/ Total Operating Income 62.0% 61.2% 63.3% 68.4% 58.6%

Staff Cost/ Total Operating Income 2.8% 3.2% 5.2% 6.6% 7.3%

Other Expenditure/ Total Operating Income 8.7% 8.3% 8.6% 10.3% 14.4%

Note : The audited financial statements shown above are on consolidated basis for FY’10

Particulars (`mn) FY06 FY 07 FY 08 FY 09 FY 10

Net sales 4,214 4,816 5,739 7,182 8,032

Other Operating Income 177 158 324 295 308

Total Operating Income 4,391 4,974 6,064 7,477 8,340

Total Expenditure 3,227 3,615 4,679 6,376 6,699

(Increase) / Decrease In Stock In Trade & WIP 20 (132) (47) 14 (119)

Consumption of Raw Materials 2,704 3,175 3,888 4,732 5,010

Purchase of Traded Goods - - - 371 -

Employees Cost 121 161 315 493 609

Other Expenditure 381 412 524 767 1,200

EBITDA 1,164 1,359 1,384 1,100 1,641

Depreciation 282 364 470 560 705

EBIT 883 995 914 541 936

Interest & Finance charges 144 209 176 384 273

Other Income 62 16 88 26 31

Extra Ordinary Items 124 - - - -

PBT 925 802 826 183 693

Tax Expense 170 218 33 82 189

PAT 755 584 793 101 504

Basic & Diluted EPS (`) 24 19 22 3 13

33

Balance Sheet

Particulars ( `mn) FY06 FY 07 FY 08 FY 09 FY 10

Sources of Funds:

Shareholders' Funds

Share Capital 150.1 317.7 376.8 376.8 376.8

Reserves and Surplus 2,095.7 3,009.0 4,710.6 4,722.4 4,985.0

2,245.8 3,326.7 5,087.4 5,099.2 5,361.8

Loan Funds

Secures Loans 2,895.2 3,938.1 6,032.3 5,098.9 4,392.0

Unsecured Loans 216.5 225.4 212.1 190.0 158.2

3,111.7 4,163.5 6,244.4 5,288.9 4,550.2

Deferred Tax Liablity 190.2 316.8 336.9 395.7 534.0

Total 5,547.7 7,807.0 11,668.7 10,783.8 10,446.0

Application of Funds :

Fixed Assets 5,065.4 6,683.4 8,468.8 8,208.8 7,945.0

Investments 2.5 2.5 50.0 - -Current Assets, Loans & Advances

Inventories 832.9 1,219.1 1,679.4 2,070.4 1,360.5

Sundry Debtors 414.5 598.6 941.8 1,164.5 1,160.7

Cash and Bank Balances 152.2 272.5 594.1 462.3 522.0

Other Current Assets 96.2 133.4 181.8 229.4 149.2

Loan and Advances 248.0 383.5 562.0 530.7 667.7

1,743.8 2,607.0 3,959.1 4,457.3 3,860.1

Less: Current Liabilities & Provision

Current Liablities 1,179.5 1,365.0 581.0 1,791.5 1,117.4

Provision 84.8 120.9 228.2 90.8 241.7

1,264.3 1,485.9 809.2 1,882.3 1,359.1

Net Current Assets 479.4 1,121.1 3,149.9 2,574.9 2,501.0

Miscellaneous Expenditure 0.4 - - - -

Total 5,547.7 7,807.0 11,668.7 10,783.8 10,446.0

34

K.P.R. Mill Limited

KPR Mill Limited is a vertically integrated apparel company with major interest in manufacturing and marketing readymade knitted apparel, knitted fabric

and cotton yarn; with production facilities located at Coimbatore, Sathyamangalam, Perundurai and Tirupur in Tamilnadu, in India. The Company has a

total capacity of 212,064 spindles; 201 circular knitting machines; garmenting facility to produce 63.0 Million pieces per annum of readymade knitted

apparel; 54,000 MT of yarn making ability and production of 21,000 MT of fabrics per annum; processing facility to handle 23MT of fabric per day; 40

windmills with total power generation capacity of 40MW. With international accreditations for quality control, environmental standards and social

accountability, the Company has a diversified customer base of international apparel retailers including Tesco, Decathlon, Marks & Spencer, Coles, Wal

Mart, Primark, Ernstings’ Family, GAP, H & M, C & A and Carrefour. For further information please visit www.kprmilllimited.com

Four-S Services Pvt. Ltd.

Four-S Services provides customized business and financial research to organizations across the globe. The company also provides Investor Relations

consulting to corporates based on in-depth sectoral and company research. The company has an impressive client profile and a team of experienced

analysts covering the key sectors including Finance & Banking, IT & Telecom, Retail, Media & Entertainment, Pharmaceuticals, Infrastructure and

Manufacturing amongst others. For further information on the company please visit www.four-s.com

Forward Looking Statements

Certain statements in this document with words or phrases such as “will”, “should”, etc., and similar expressions or variation of these expressions or those

concerning our future prospects are forward looking statements. Actual results may differ materially from those suggested by the forward looking

statements due to a number of risks or uncertainties associated with the expectations. These risks and uncertainties include, but are not limited to, our

ability to successfully implement our strategy and changes in government policies. The company may, from time to time, make additional written and oral

forward looking statements, including statements contained in the company’s filings with the stock exchanges and our reports to shareholders. The

company does not undertake to update any forward-looking statements that may be made from time to time by or on behalf of the company.

About Us

35

Contacts

For any Investor Relations queries please contact:

J.S.Kumar

Vice President (Finance)

K.P.R.Mill Limited

Email: [email protected]

Tel. No. +91-421-2487051

Seema Shukla

Four-S Services Pvt. Ltd.

Email: [email protected]

Tel. No. +91-124-4251443

Four-S Services Locations

Gurgaon: 214, Udyog Vihar Phase I, Gurgaon – 122016. Tel: +91-124-4251443

Mumbai: 503, Twin Complex Phase 1, Opp. Marol Fire Station, Marol Naka, Andheri East, Mumbai 400 059, Tel: 022 - 42153659

36

Concept, Research and Design by

www.four-s.com

Thank You

Four-S Services Locations

Gurgaon: 214, Udyog Vihar Phase I, Gurgaon – 122016. Tel: +91-124-4251443

Mumbai: 503, Twin Complex Phase 1, Opp. Marol Fire Station, Marol Naka, Andheri East, Mumbai 400 059, Tel: 022 - 42153659