49

Investor Presentation August 2017

Investor

Presentation

August 2017

This presentation, including the accompanying oral presentation (collectively, this “presentation”), does not constitute an offer to sell or the solicitation of an offer to buy any

securities. This presentation is provided by On Deck Capital, Inc. (“OnDeck”) for informational purposes only. No representations express or implied are being made by OnDeck or

any other person as to the accuracy or completeness of the information contained herein.

This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and other legal authority. Forward-looking

statements include statements about scalability, growing distribution channels, credit predictability and information concerning our future financial performance, business plans and

objectives, potential growth opportunities, financing plans, competitive position, industry environment and potential market opportunities. Forward-looking statements can also be

identified by words such as "will," "enables," "expects”, “may,” "allows," "continues," "believes,” “intends,” "anticipates," "estimates" or similar expressions. Forward-looking

statements are neither historical facts nor assurances of future performance. They are based only on our current beliefs, expectations and assumptions regarding the future of our

business, anticipated events and trends, the economy and other future conditions. Moreover, we do not assume responsibility for the accuracy and completeness of forward-looking

statements. As such, they are subject to inherent uncertainties, changes in circumstances, known and unknown risks and other factors that are difficult to predict and in many cases

outside our control.

As a result, you should not rely on any forward-looking statements. Our expected results may not be achieved, and actual results may differ materially from our expectations.

Important factors that could cause actual results to differ from our forward-looking statements are the risks that we may not be able to manage our anticipated or actual growth

effectively, that our credit models do not adequately identify potential risks, the timing and amount of expected savings from cost rationalization programs and other risks, including

those under the heading “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2016 and in other documents that we file with the Securities and

Exchange Commission, or SEC, from time to time which are available on the SEC website at www.sec.gov. We undertake no obligation to publicly update any forward-looking

statements for any reason after the date of this presentation to conform these statements to actual results or to changes in our expectations, except as required by law.

In addition to U.S. GAAP financial information, this presentation includes certain non-GAAP financial measures. We believe that non-GAAP measures can provide useful

supplemental information for period-to-period comparisons of our core business and are useful to investors and others in understanding and evaluating our operating results. These

non-GAAP measures have not been calculated in accordance with U.S. GAAP. You should not consider them in isolation or as a substitute for an analysis of our results under U.S.

GAAP. There are a number of limitations related to the use of these non-GAAP measures compared to their nearest U.S. GAAP equivalents. In addition, other companies may

calculate non-GAAP financial measures differently or may use other measures to evaluate their performance, all of which could reduce the usefulness of our non-GAAP financial

measures as tools for comparison. The non-GAAP measures contained in this presentation include Adjusted EBITDA, Adjusted Net Income (Loss), Adjusted Expense Ratio,

Adjusted Operating Yield and certain operating expense categories, all of which exclude stock-based compensation, as well as Net Interest Margin After Credit Losses. Please refer

to pages 35 through 49 in the Appendix of this presentation for a description of these non-GAAP measures, their respective limitations and reconciliations to U.S. GAAP.

Forward-Looking Statements

2

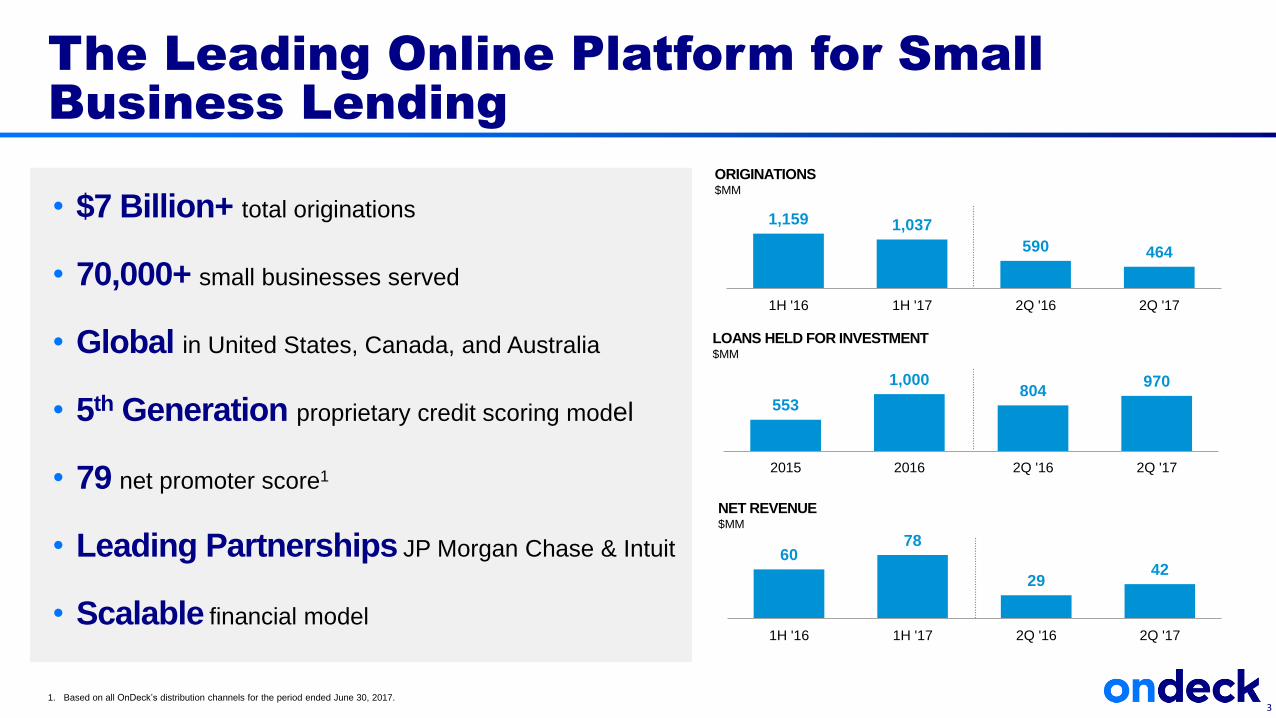

1,159 1,037

590 464

1H '16 1H '17 2Q '16 2Q '17

ORIGINATIONS$MM

• $7 Billion+ total originations

• 70,000+ small businesses served

• Global in United States, Canada, and Australia

• 5th Generation proprietary credit scoring model

• 79 net promoter score1

• Leading Partnerships JP Morgan Chase & Intuit

• Scalable financial model

The Leading Online Platform for Small

Business Lending

1. Based on all OnDeck’s distribution channels for the period ended June 30, 2017.3

6078

2942

1H '16 1H '17 2Q '16 2Q '17

NET REVENUE$MM

LOANS HELD FOR INVESTMENT$MM

553

1,000804

970

2015 2016 2Q '16 2Q '17

4

Investment Highlights

• Massive and underserved market

• Diversified acquisition channels

• Small business tailored product set

• Proprietary analytics and scoring models

• Improving operating leverage

• Strengthening credit

• Execution on strategic priorities

• Driving toward near term profitability goals

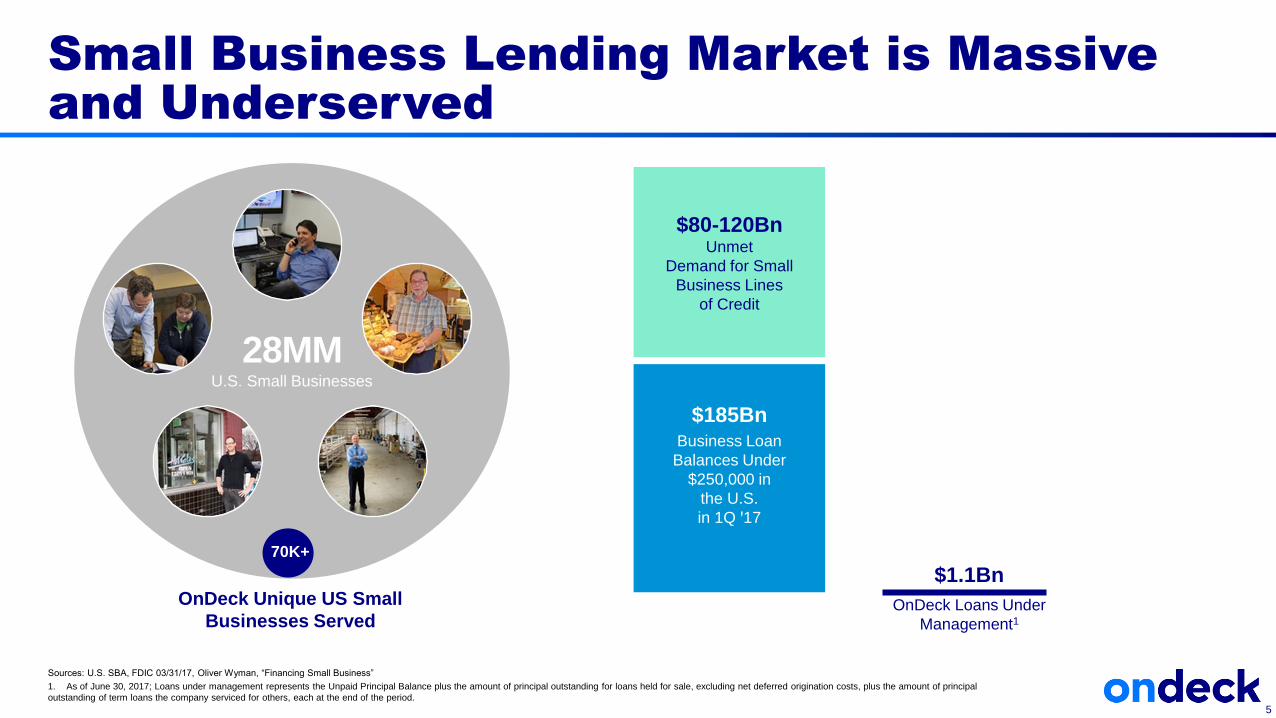

Small Business Lending Market is Massive

and Underserved

Sources: U.S. SBA, FDIC 03/31/17, Oliver Wyman, “Financing Small Business”

1. As of June 30, 2017; Loans under management represents the Unpaid Principal Balance plus the amount of principal outstanding for loans held for sale, excluding net deferred origination costs, plus the amount of principal

outstanding of term loans the company serviced for others, each at the end of the period.

5

28MMU.S. Small Businesses

OnDeck Unique US Small

Businesses Served

70K+

$80-120BnUnmet

Demand for Small

Business Lines

of Credit

$185BnBusiness Loan

Balances Under

$250,000 in

the U.S.

in 1Q ꞌ17

$1.1Bn

OnDeck Loans Under

Management1

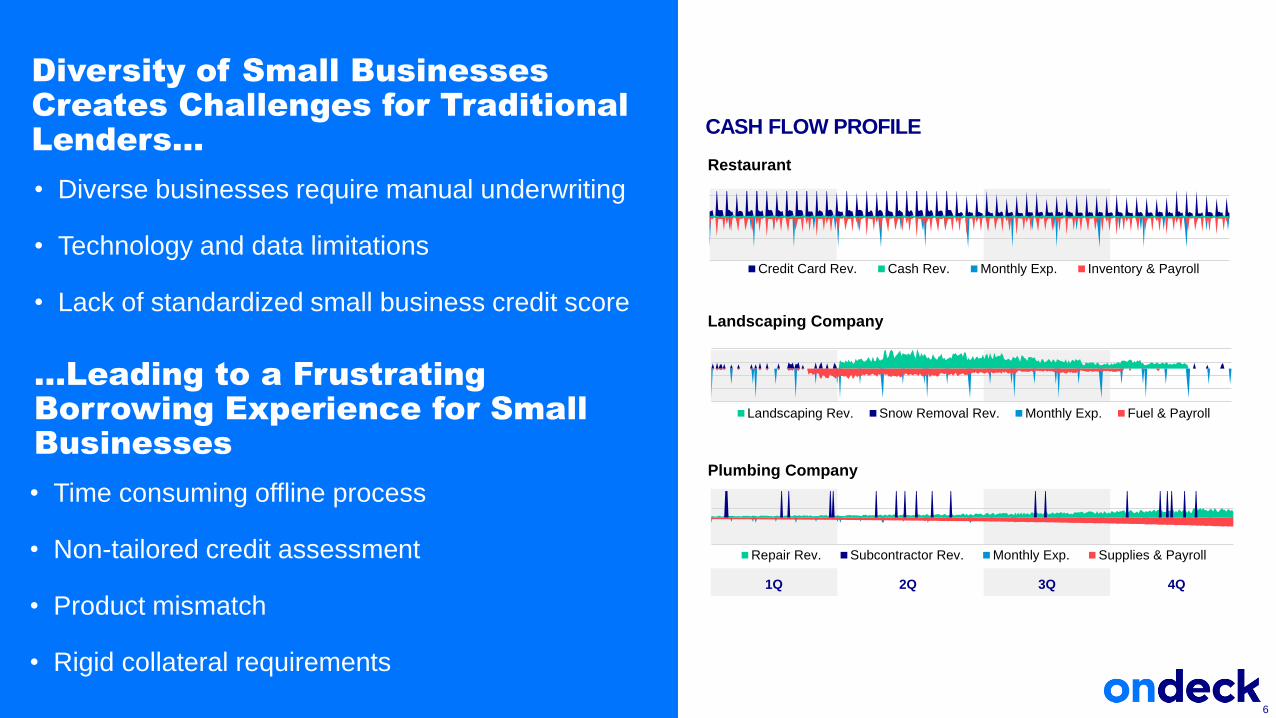

Diversity of Small Businesses

Creates Challenges for Traditional

Lenders…

• Diverse businesses require manual underwriting

• Technology and data limitations

• Lack of standardized small business credit score

6

Credit Card Rev. Cash Rev. Monthly Exp. Inventory & Payroll

Landscaping Rev. Snow Removal Rev. Monthly Exp. Fuel & Payroll

Repair Rev. Subcontractor Rev. Monthly Exp. Supplies & Payroll

CASH FLOW PROFILE

Restaurant

Landscaping Company

Plumbing Company

1Q 2Q 3Q 4Q

…Leading to a Frustrating

Borrowing Experience for Small

Businesses

• Time consuming offline process

• Non-tailored credit assessment

• Product mismatch

• Rigid collateral requirements

Manual ReviewWeeks or Months

Offline33 Hours2

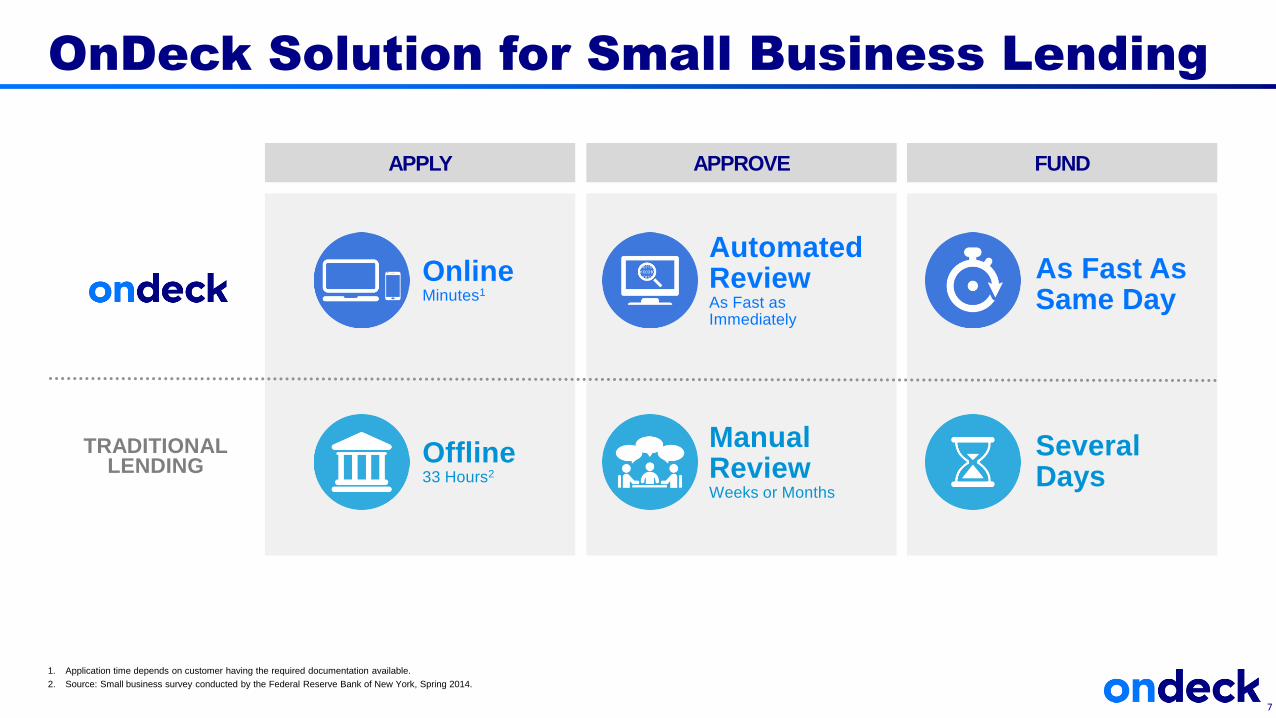

OnDeck Solution for Small Business Lending

1. Application time depends on customer having the required documentation available.

2. Source: Small business survey conducted by the Federal Reserve Bank of New York, Spring 2014.

7

APPLY

TRADITIONAL LENDING

Several Days

OnlineMinutes1

Automated ReviewAs Fast as Immediately

As Fast As Same Day

APPROVE FUND

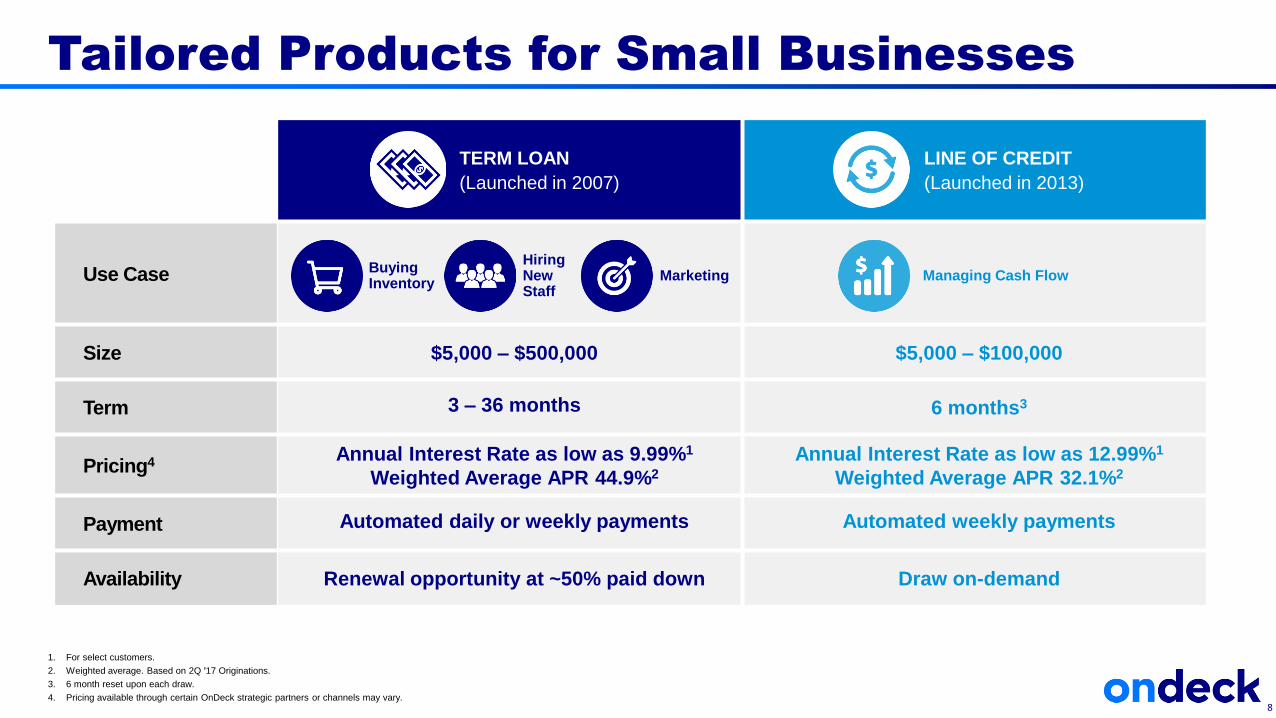

TERM LOAN

(Launched in 2007)

LINE OF CREDIT

(Launched in 2013)

Use Case

Size $5,000 – $500,000 $5,000 – $100,000

Term 3 – 36 months 6 months3

Pricing4 Annual Interest Rate as low as 9.99%1

Weighted Average APR 44.9%2

Annual Interest Rate as low as 12.99%1

Weighted Average APR 32.1%2

Payment Automated daily or weekly payments Automated weekly payments

Availability Renewal opportunity at ~50% paid down Draw on-demand

Tailored Products for Small Businesses

1. For select customers.

2. Weighted average. Based on 2Q ꞌ17 Originations.

3. 6 month reset upon each draw.

4. Pricing available through certain OnDeck strategic partners or channels may vary.

HiringNewStaff

Buying Inventory

Marketing Managing Cash Flow

8

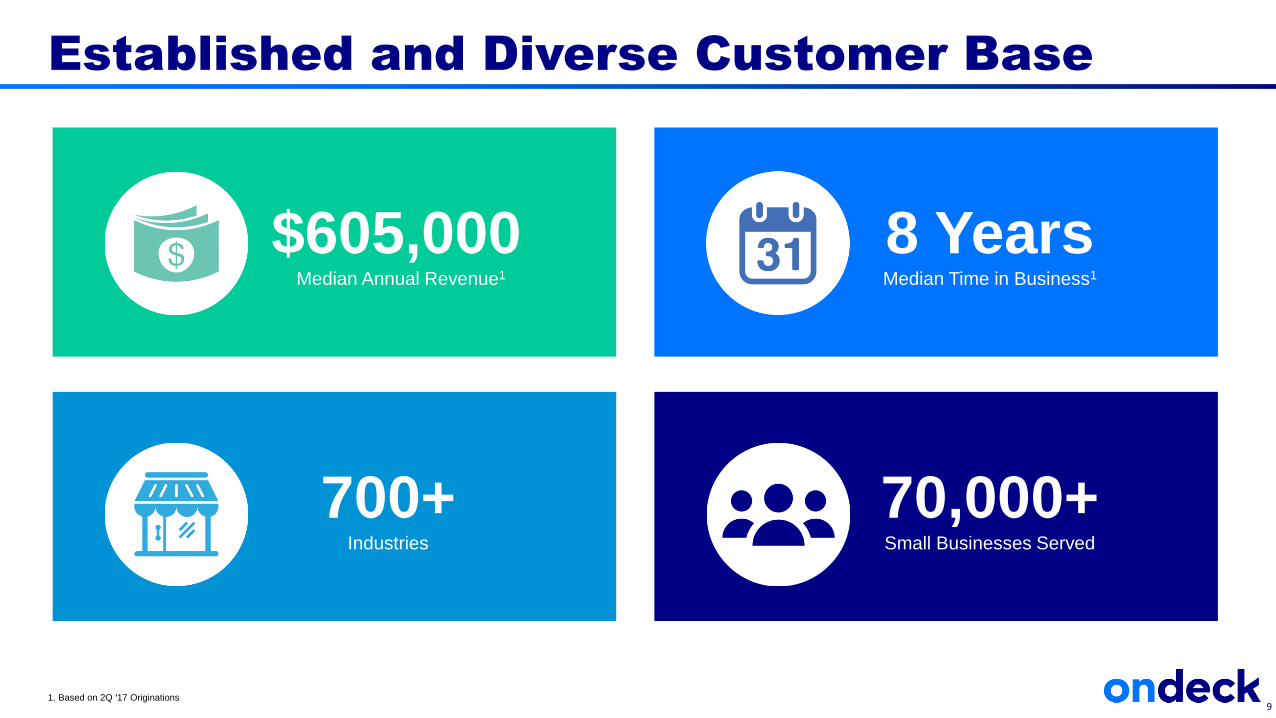

70,000+Small Businesses Served

8 YearsMedian Time in Business1

Established and Diverse Customer Base

1. Based on 2Q ꞌ17 Originations

$605,000Median Annual Revenue1

700+Industries

9

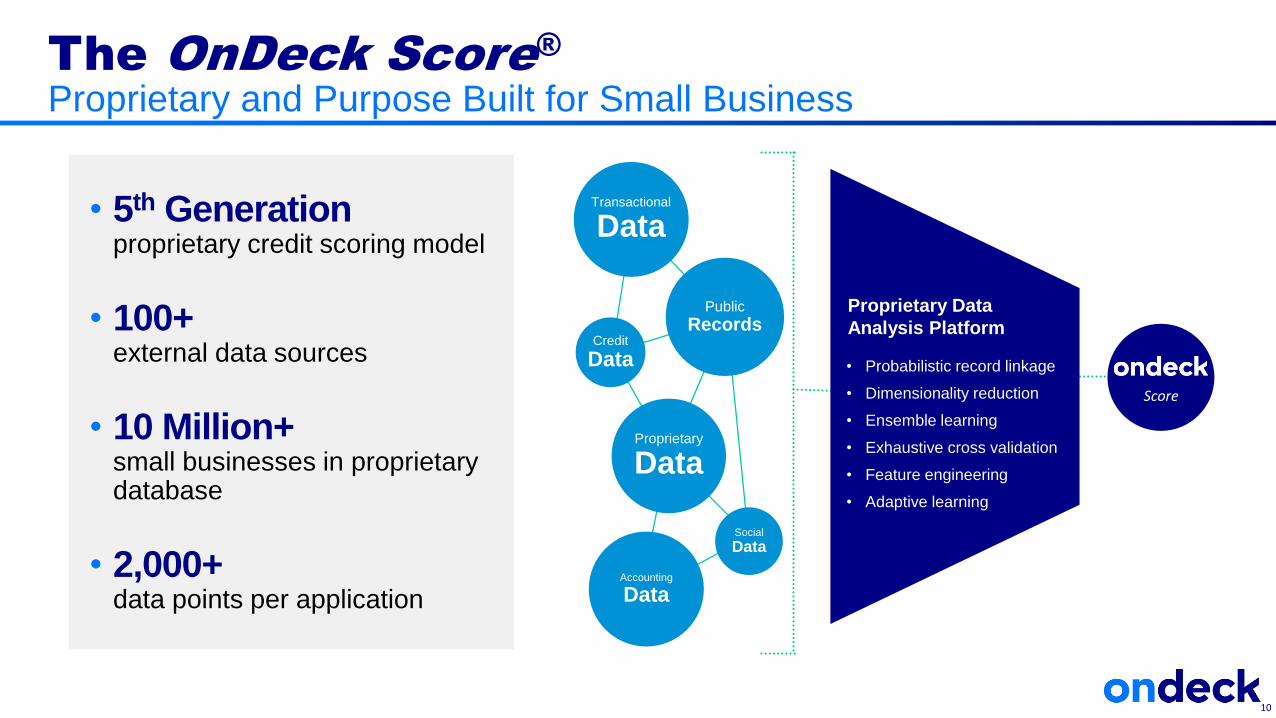

• 5th Generationproprietary credit scoring model

• 100+ external data sources

• 10 Million+ small businesses in proprietary database

• 2,000+ data points per application

The OnDeck Score®

Proprietary and Purpose Built for Small Business

10

Score

• Probabilistic record linkage

• Dimensionality reduction

• Ensemble learning

• Exhaustive cross validation

• Feature engineering

• Adaptive learning

Proprietary Data

Analysis Platform

Public

RecordsCredit

Data

Social

Data

Proprietary

Data

Transactional

Data

Accounting

Data

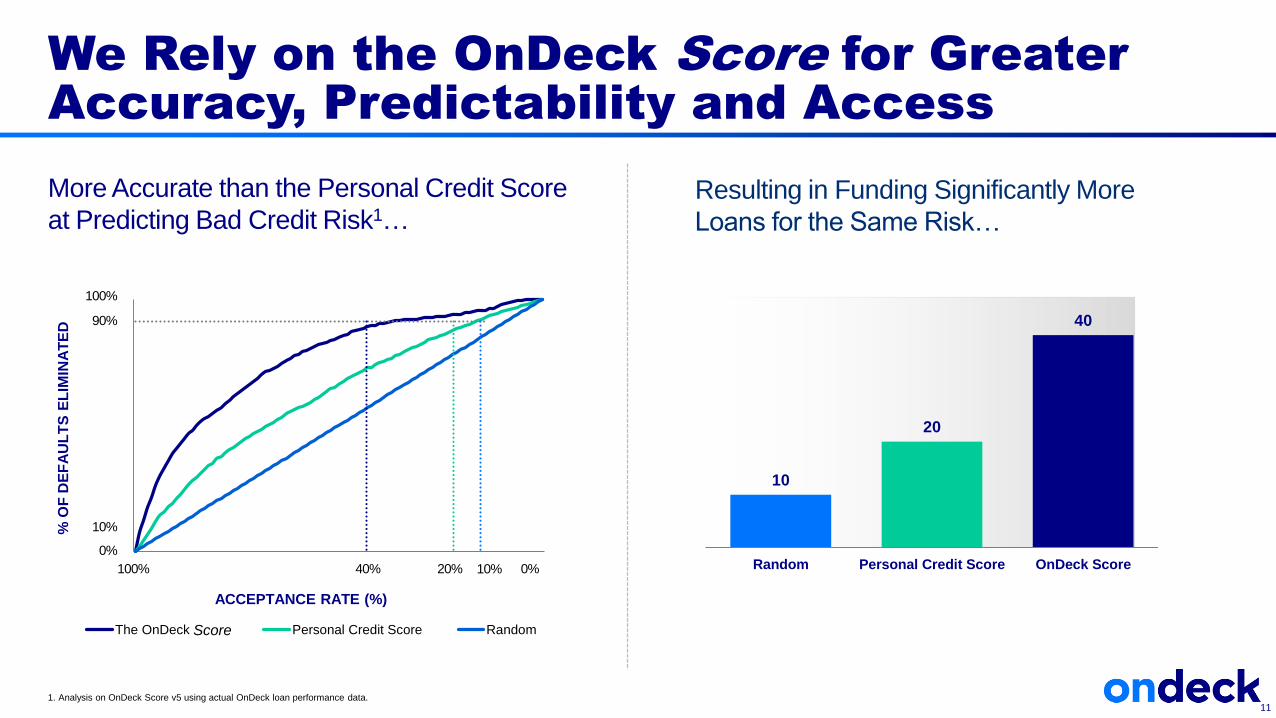

We Rely on the OnDeck Score for Greater

Accuracy, Predictability and Access

1. Analysis on OnDeck Score v5 using actual OnDeck loan performance data.11

10

20

40

Random Personal Credit Score OnDeck Score

More Accurate than the Personal Credit Score

at Predicting Bad Credit Risk1…Resulting in Funding Significantly More

Loans for the Same Risk…

ACCEPTANCE RATE (%)

The OnDeck Score Personal Credit Score Random

90%

100%

0%

100% 40% 20% 10% 0%

% O

F D

EF

AU

LT

S E

LIM

INA

TE

D

10%

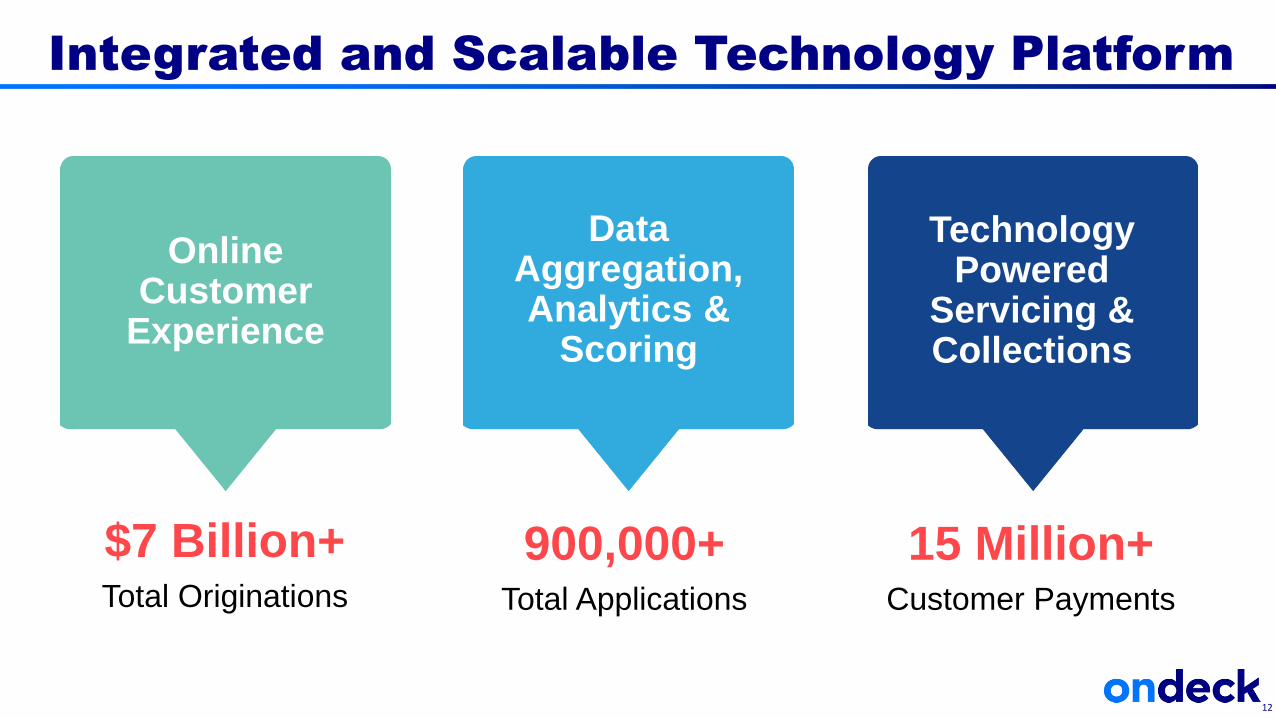

Score

Online Customer

Experience

Integrated and Scalable Technology Platform

900,000+Total Applications

Data Aggregation, Analytics &

Scoring

15 Million+Customer Payments

Technology Powered

Servicing & Collections

12

$7 Billion+Total Originations

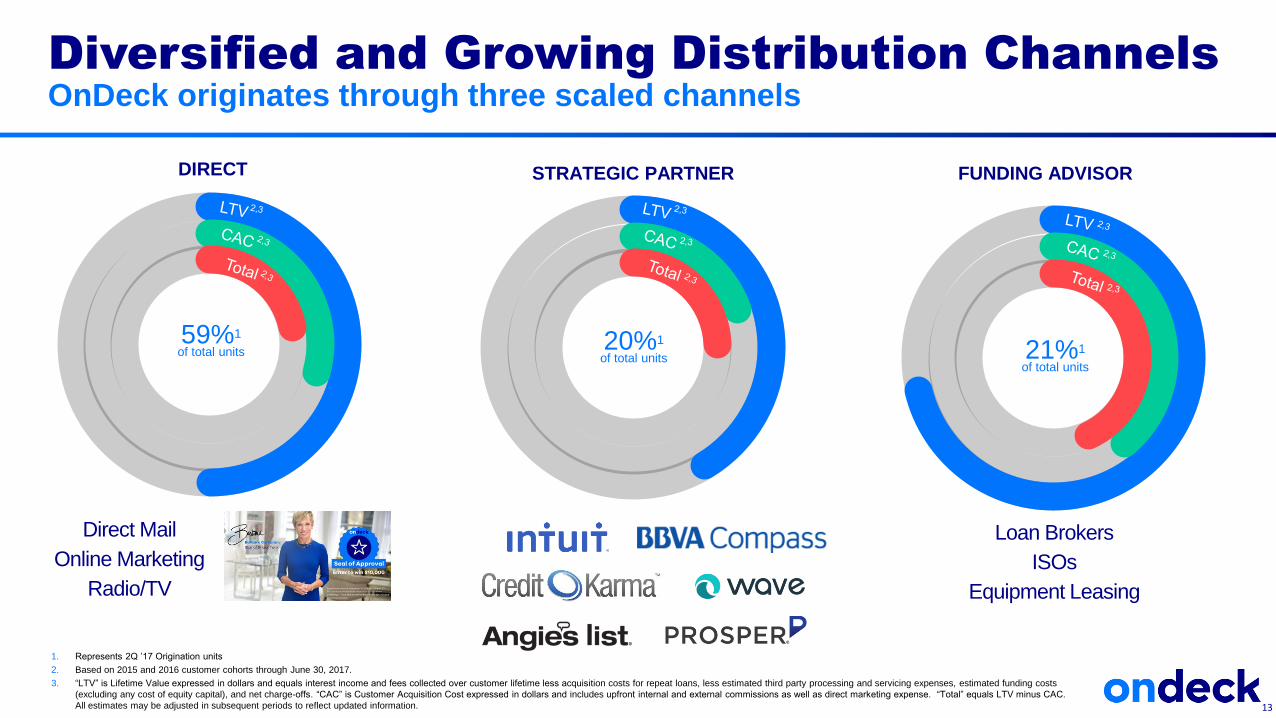

Diversified and Growing Distribution Channels

OnDeck originates through three scaled channels

1. Represents 2Q ’17 Origination units

2. Based on 2015 and 2016 customer cohorts through June 30, 2017.

3. “LTV” is Lifetime Value expressed in dollars and equals interest income and fees collected over customer lifetime less acquisition costs for repeat loans, less estimated third party processing and servicing expenses, estimated funding costs

(excluding any cost of equity capital), and net charge-offs. “CAC” is Customer Acquisition Cost expressed in dollars and includes upfront internal and external commissions as well as direct marketing expense. “Total” equals LTV minus CAC.

All estimates may be adjusted in subsequent periods to reflect updated information.

Direct Mail

Online Marketing

Radio/TV

Loan Brokers

ISOs

Equipment Leasing

DIRECT STRATEGIC PARTNER FUNDING ADVISOR

59%1

of total units20%1

of total units 21%1

of total units

13

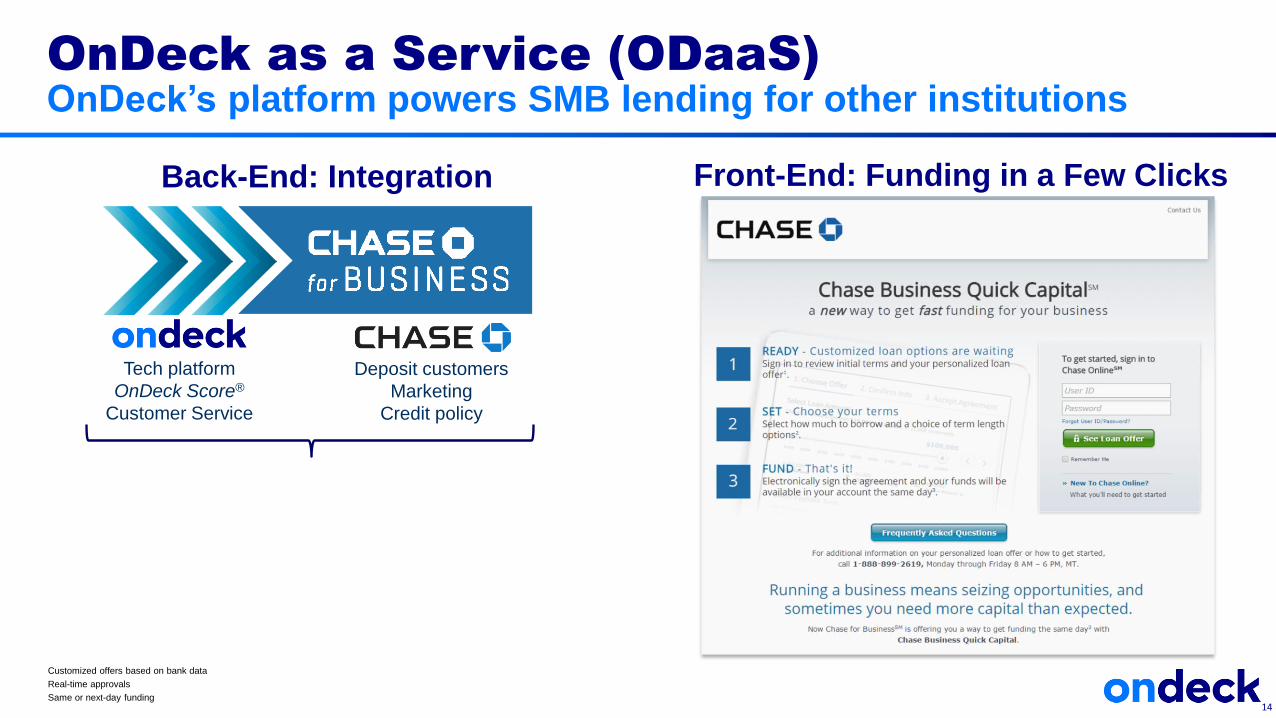

OnDeck as a Service (ODaaS)

OnDeck’s platform powers SMB lending for other institutions

Customized offers based on bank data

Real-time approvals

Same or next-day funding14

Deposit customers

Marketing

Credit policy

Tech platform

OnDeck Score®

Customer Service

Back-End: Integration Front-End: Funding in a Few Clicks

15

Strategic Priorities

Achieve profitability by YE 2017 and profitable growth in 2018 by:

• Growing responsibly

• Strengthening credit

• Improving operating leverage

• Diversifying funding

• Broadening product reach

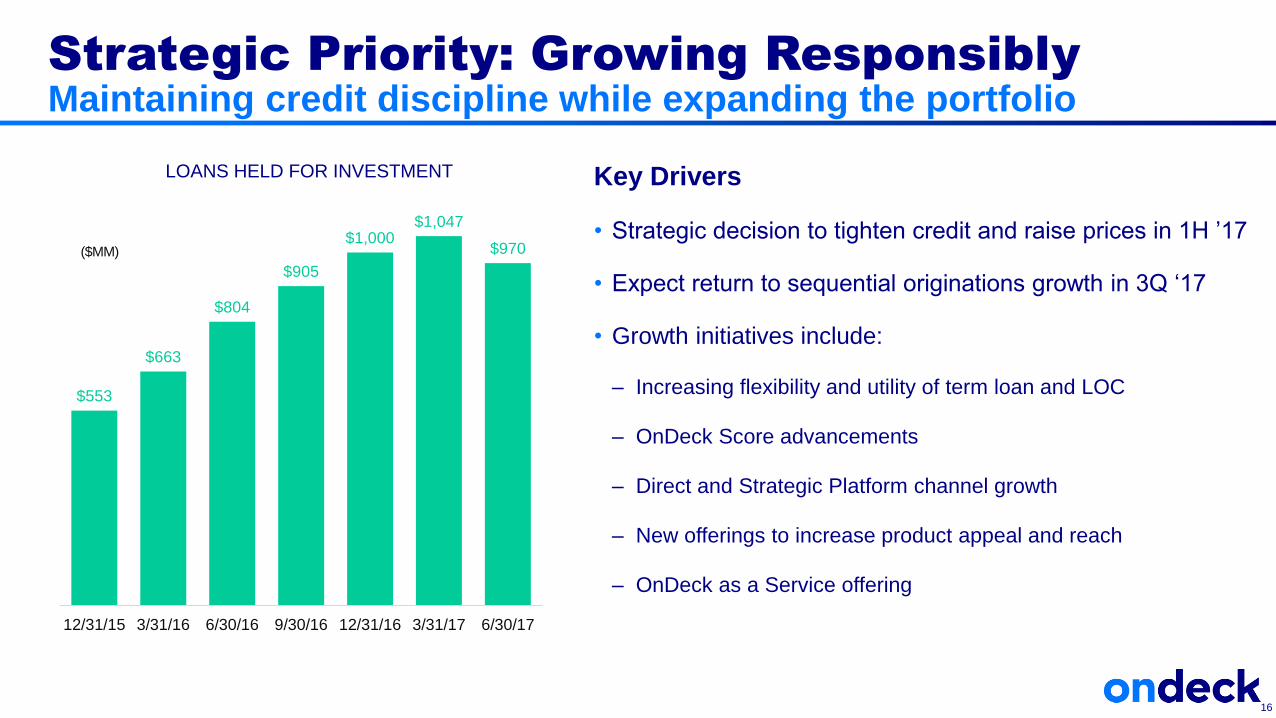

$553

$663

$804

$905

$1,000$1,047

$970

0

200

400

600

800

1000

1200

12/31/15 3/31/16 6/30/16 9/30/16 12/31/16 3/31/17 6/30/17

Strategic Priority: Growing Responsibly

Maintaining credit discipline while expanding the portfolio

16

LOANS HELD FOR INVESTMENT

($MM)

Key Drivers

• Strategic decision to tighten credit and raise prices in 1H ’17

• Expect return to sequential originations growth in 3Q ‘17

• Growth initiatives include:

– Increasing flexibility and utility of term loan and LOC

– OnDeck Score advancements

– Direct and Strategic Platform channel growth

– New offerings to increase product appeal and reach

– OnDeck as a Service offering

17

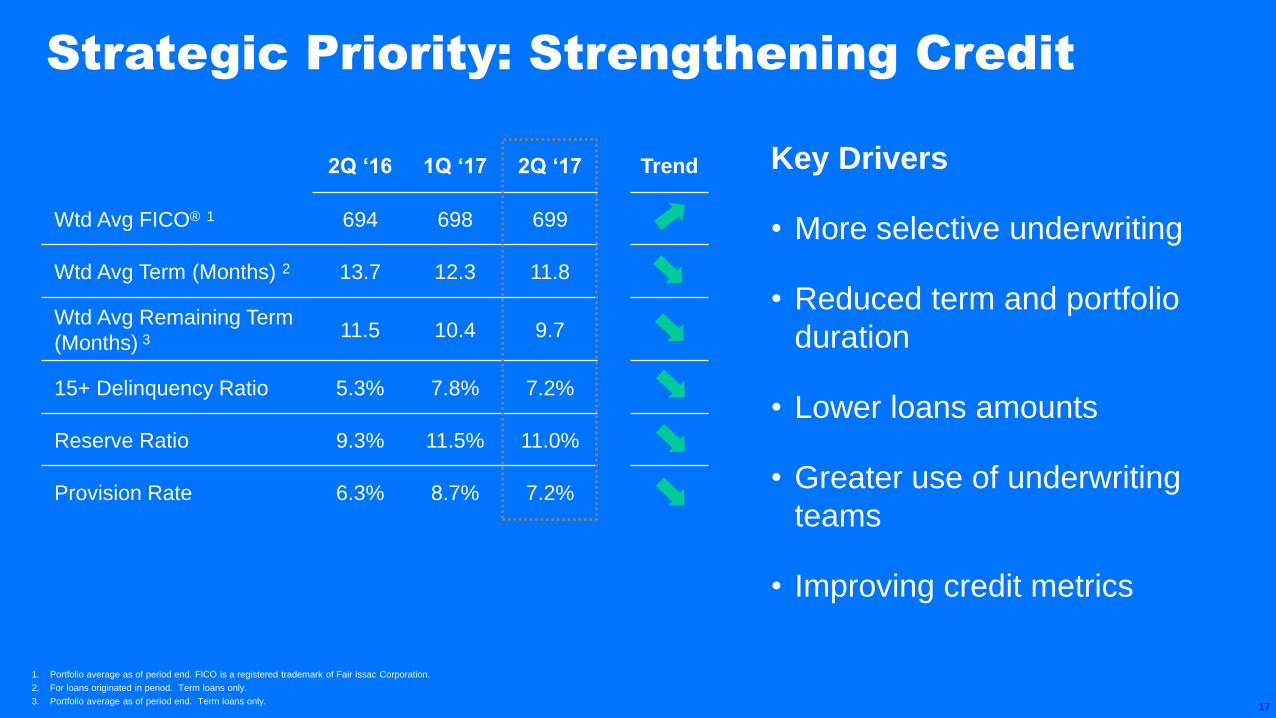

Key Drivers

• More selective underwriting

• Reduced term and portfolio

duration

• Lower loans amounts

• Greater use of underwriting

teams

• Improving credit metrics

2Q ‘16 1Q ‘17 2Q ‘17 Trend

Wtd Avg FICO® 1 694 698 699

Wtd Avg Term (Months) 2 13.7 12.3 11.8

Wtd Avg Remaining Term

(Months) 311.5 10.4 9.7

15+ Delinquency Ratio 5.3% 7.8% 7.2%

Reserve Ratio 9.3% 11.5% 11.0%

Provision Rate 6.3% 8.7% 7.2%

1. Portfolio average as of period end. FICO is a registered trademark of Fair Issac Corporation.

2. For loans originated in period. Term loans only.

3. Portfolio average as of period end. Term loans only.

Strategic Priority: Strengthening Credit

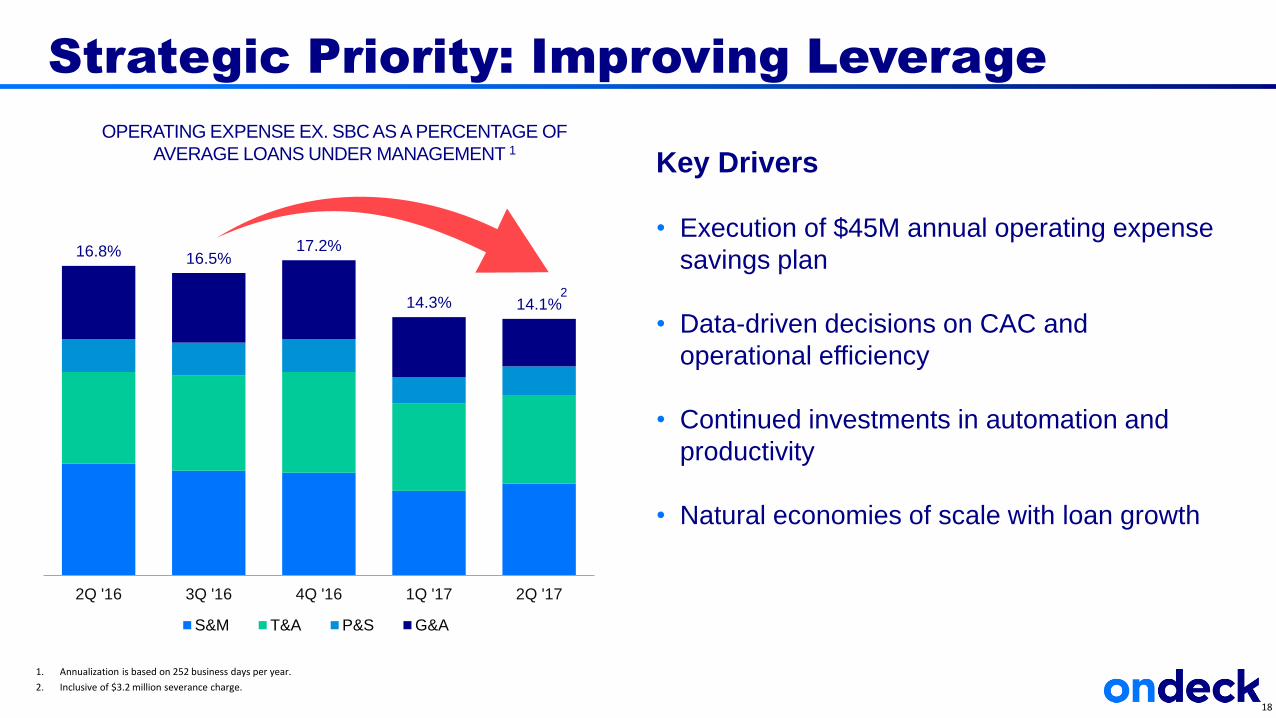

16.8% 16.5%17.2%

14.3% 14.1%

2Q '16 3Q '16 4Q '16 1Q '17 2Q '17

S&M T&A P&S G&A

Key Drivers

• Execution of $45M annual operating expense

savings plan

• Data-driven decisions on CAC and

operational efficiency

• Continued investments in automation and

productivity

• Natural economies of scale with loan growth

Strategic Priority: Improving Leverage

18

OPERATING EXPENSE EX. SBC AS A PERCENTAGE OF

AVERAGE LOANS UNDER MANAGEMENT 1

1. Annualization is based on 252 business days per year.

2. Inclusive of $3.2 million severance charge.

2

12/31/14 12/31/15 12/31/16 6/30/17

Warehouse Securitization 100% Equity Funded Off-Balance Sheet

$388 $380

$733 $726

$100

$265

$186$256

12/31/14 12/31/15 12/31/16 6/30/17

Funding Debt Excess Capacity

Serviced for

Third Parties1

Balance

Sheet Model

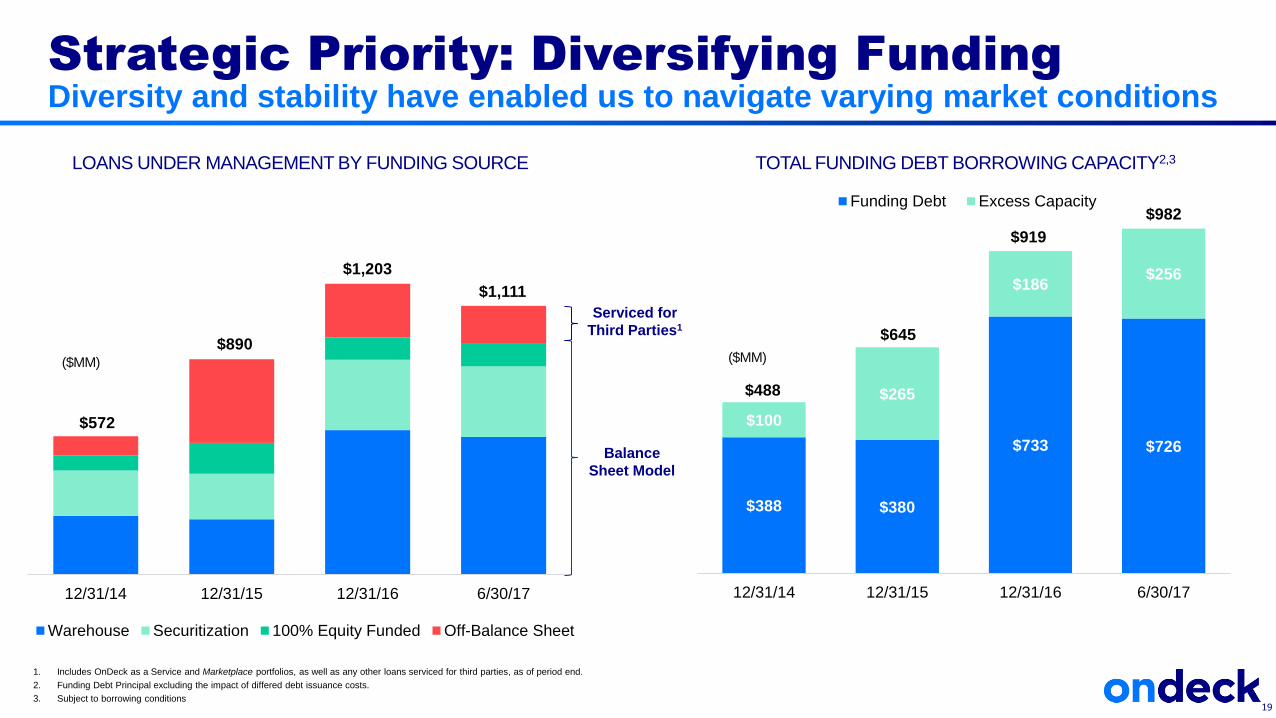

Strategic Priority: Diversifying Funding

Diversity and stability have enabled us to navigate varying market conditions

19

LOANS UNDER MANAGEMENT BY FUNDING SOURCE TOTAL FUNDING DEBT BORROWING CAPACITY2,3

$572

$890

$1,203

$1,111

1. Includes OnDeck as a Service and Marketplace portfolios, as well as any other loans serviced for third parties, as of period end.

2. Funding Debt Principal excluding the impact of differed debt issuance costs.

3. Subject to borrowing conditions

$488

$645

$919

$982

($MM) ($MM)

Enhanced Flexibility & Utility

Strategic partnerships

Data and analytics

New Products

Loyalty Benefits

International expansion

20

Strategic Priority: Broadening Product Reach

• Improving bottom line performance

• Attractive loan portfolio characteristics

• Compelling customer lifetime value

• Substantial lending spreads

• Inherent operating leverage

• GAAP profitable by end of year 2017

21

Financial Highlights

22

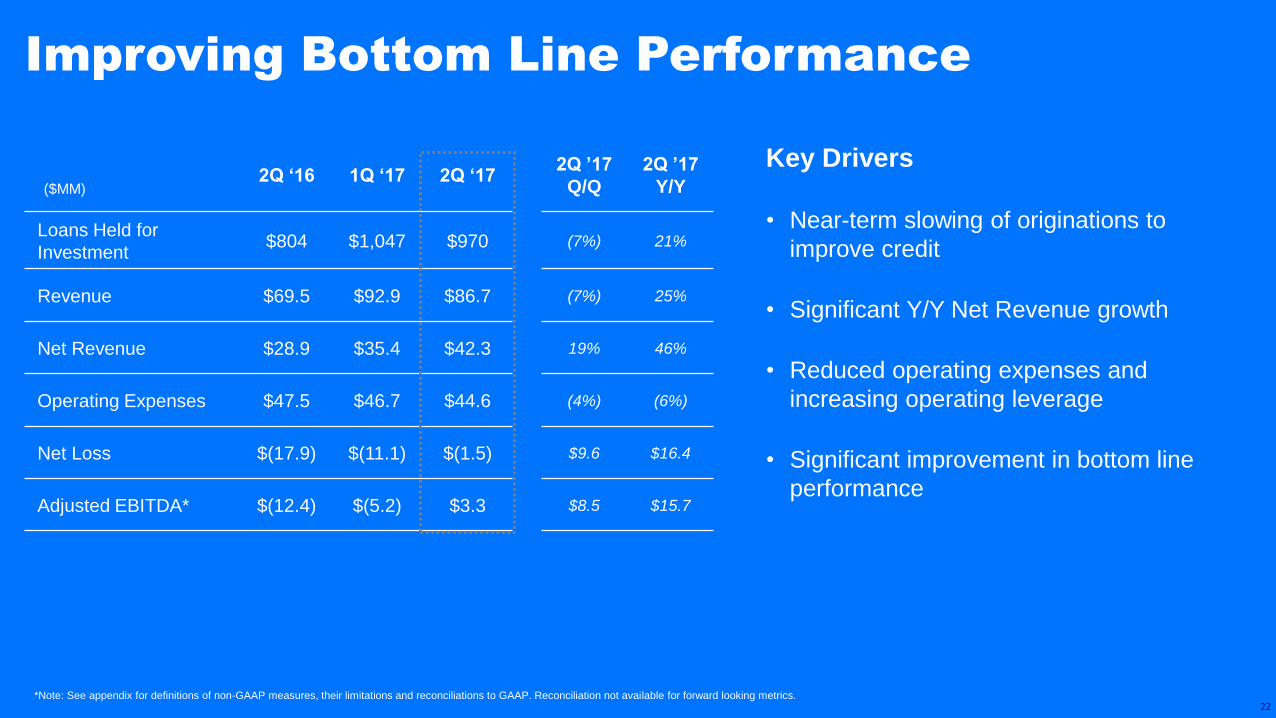

Improving Bottom Line Performance

Key Drivers

• Near-term slowing of originations to

improve credit

• Significant Y/Y Net Revenue growth

• Reduced operating expenses and

increasing operating leverage

• Significant improvement in bottom line

performance

($MM)2Q ‘16 1Q ‘17 2Q ‘17

2Q ’17

Q/Q

2Q ’17

Y/Y

Loans Held for

Investment$804 $1,047 $970 (7%) 21%

Revenue $69.5 $92.9 $86.7 (7%) 25%

Net Revenue $28.9 $35.4 $42.3 19% 46%

Operating Expenses $47.5 $46.7 $44.6 (4%) (6%)

Net Loss $(17.9) $(11.1) $(1.5) $9.6 $16.4

Adjusted EBITDA* $(12.4) $(5.2) $3.3 $8.5 $15.7

*Note: See appendix for definitions of non-GAAP measures, their limitations and reconciliations to GAAP. Reconciliation not available for forward looking metrics.

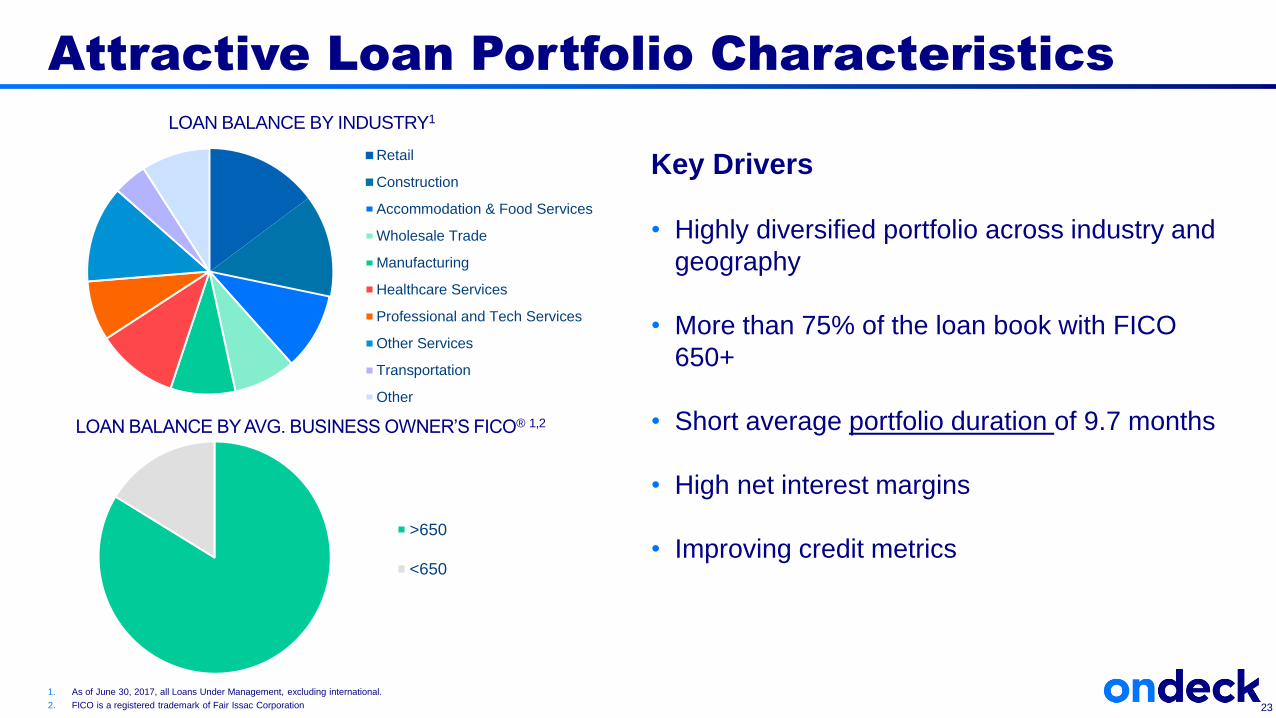

Attractive Loan Portfolio Characteristics

LOAN BALANCE BY INDUSTRY1

LOAN BALANCE BY AVG. BUSINESS OWNER’S FICO® 1,2

Key Drivers

• Highly diversified portfolio across industry and

geography

• More than 75% of the loan book with FICO

650+

• Short average portfolio duration of 9.7 months

• High net interest margins

• Improving credit metrics>650

<650

Retail

Construction

Accommodation & Food Services

Wholesale Trade

Manufacturing

Healthcare Services

Professional and Tech Services

Other Services

Transportation

Other

1. As of June 30, 2017, all Loans Under Management, excluding international.

2. FICO is a registered trademark of Fair Issac Corporation. 23

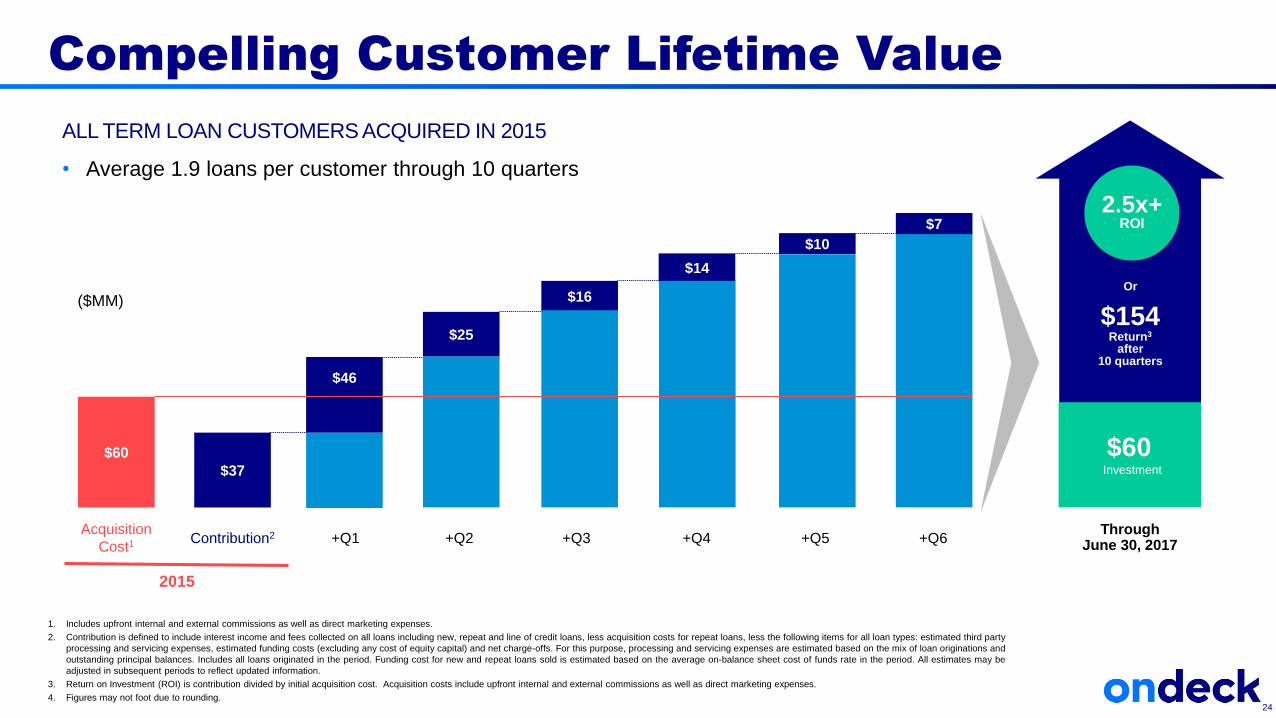

Compelling Customer Lifetime Value

1. Includes upfront internal and external commissions as well as direct marketing expenses.

2. Contribution is defined to include interest income and fees collected on all loans including new, repeat and line of credit loans, less acquisition costs for repeat loans, less the following items for all loan types: estimated third party

processing and servicing expenses, estimated funding costs (excluding any cost of equity capital) and net charge-offs. For this purpose, processing and servicing expenses are estimated based on the mix of loan originations and

outstanding principal balances. Includes all loans originated in the period. Funding cost for new and repeat loans sold is estimated based on the average on-balance sheet cost of funds rate in the period. All estimates may be

adjusted in subsequent periods to reflect updated information.

3. Return on Investment (ROI) is contribution divided by initial acquisition cost. Acquisition costs include upfront internal and external commissions as well as direct marketing expenses.

4. Figures may not foot due to rounding.24

ALL TERM LOAN CUSTOMERS ACQUIRED IN 2015

• Average 1.9 loans per customer through 10 quarters

Or

$154Return3

after 10 quarters

$60Investment

2.5x+ROI

($MM)

2015

$60

$37

$25

Acquisition

Cost1Contribution2 +Q1 +Q2

$46

Through June 30, 2017

$16

+Q3

$14

+Q4

$10

+Q5

$7

+Q6

25

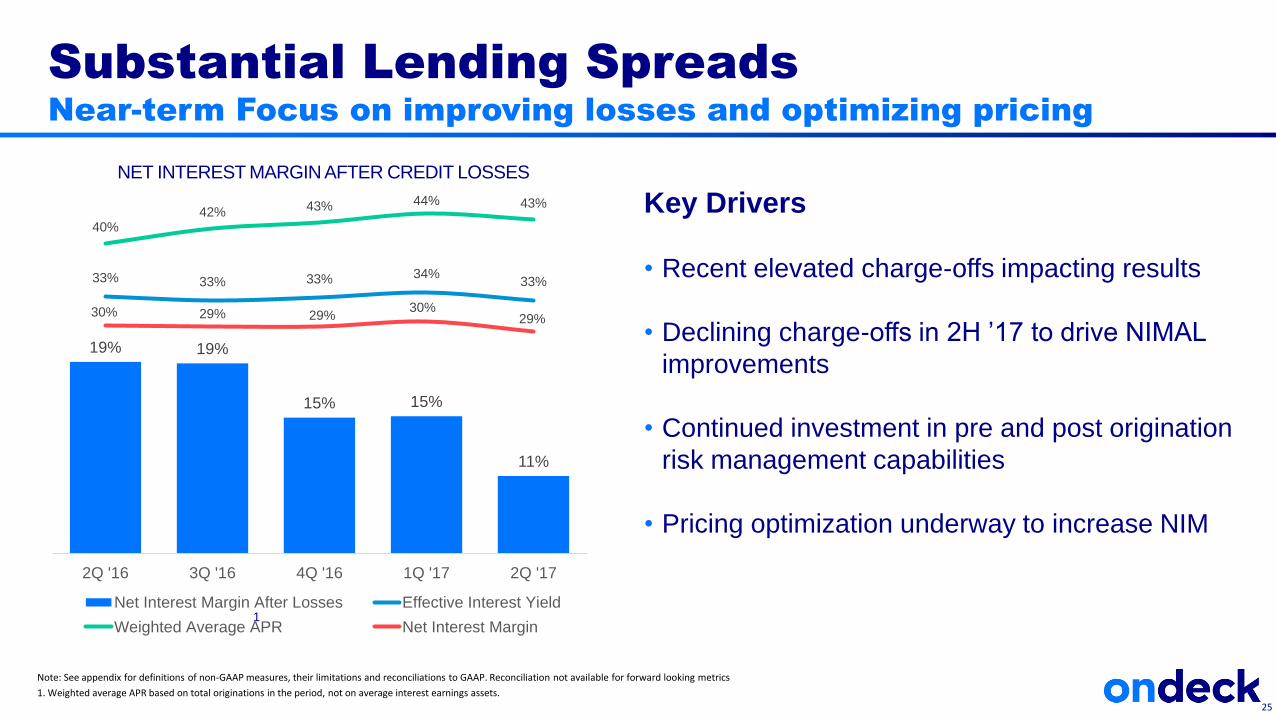

19% 19%

15% 15%

11%

33% 33% 33% 34%33%

40%42% 43% 44% 43%

30% 29% 29%30%

29%

--

0.1%

0.1%

0.2%

0.2%

0.3%

0.3%

0.4%

0.4%

0.5%

0.05

0.1

0.15

0.2

0.25

0.3

2Q '16 3Q '16 4Q '16 1Q '17 2Q '17

Net Interest Margin After Losses Effective Interest Yield

Weighted Average APR Net Interest Margin

Substantial Lending Spreads

Near-term Focus on improving losses and optimizing pricing

Key Drivers

• Recent elevated charge-offs impacting results

• Declining charge-offs in 2H ’17 to drive NIMAL

improvements

• Continued investment in pre and post origination

risk management capabilities

• Pricing optimization underway to increase NIM

NET INTEREST MARGIN AFTER CREDIT LOSSES

Note: See appendix for definitions of non-GAAP measures, their limitations and reconciliations to GAAP. Reconciliation not available for forward looking metrics

1. Weighted average APR based on total originations in the period, not on average interest earnings assets.

1

18.3%17.9%

18.8%

15.4%15.1%

ANNUALIZED GAAP OPERATING EXPENSE / AVERAGE LUM1 Key Drivers

• Execution of $45M annual operating expense

savings plan nearly complete as of 2Q ‘17

• Targeted cost reductions while maintaining focus

on long-term growth

• Data-driven decisions on CAC and operational

efficiency

• Operating Expense Target of approximately

$40M in each 3Q ’17 and 4Q ’17

• Natural economies of scale with Loan growth

1. Annualization is based on 252 business days per year, which is typical weekdays per year less U.S. Federal Reserve Bank holidays.

2. Includes $3.2 million severance charge.

$47.5 $49.4$52.5

$46.7$44.6

2Q '16 3Q '16 4Q '16 1Q '17 2Q '17

GAAP OPERATING EXPENSE

S&M T&A P&S G&A

Inherent Operating Leverage

Executing Against Cost Reduction Plans

($MM)

2

2

26

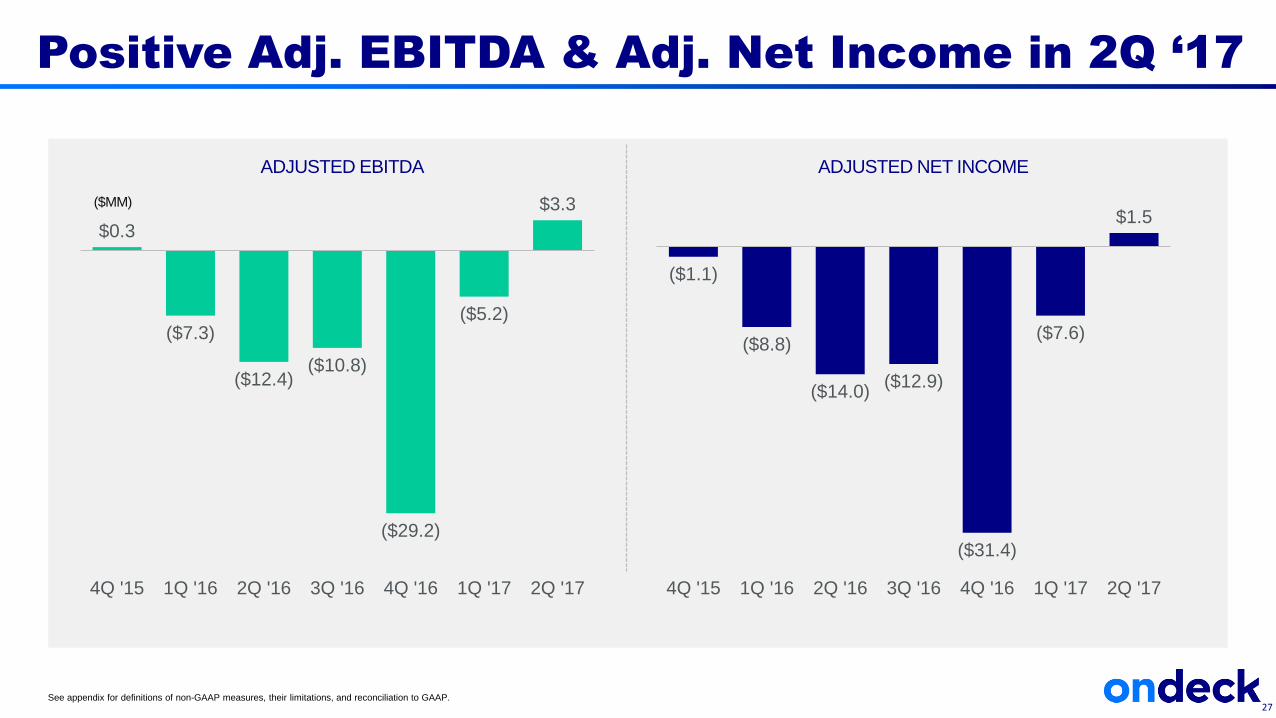

Positive Adj. EBITDA & Adj. Net Income in 2Q ‘17

See appendix for definitions of non-GAAP measures, their limitations, and reconciliation to GAAP.

$0.3

($7.3)

($12.4)($10.8)

($29.2)

($5.2)

$3.3

4Q '15 1Q '16 2Q '16 3Q '16 4Q '16 1Q '17 2Q '17

($MM)

($1.1)

($8.8)

($14.0)($12.9)

($31.4)

($7.6)

$1.5

4Q '15 1Q '16 2Q '16 3Q '16 4Q '16 1Q '17 2Q '17

ADJUSTED EBITDA ADJUSTED NET INCOME

27

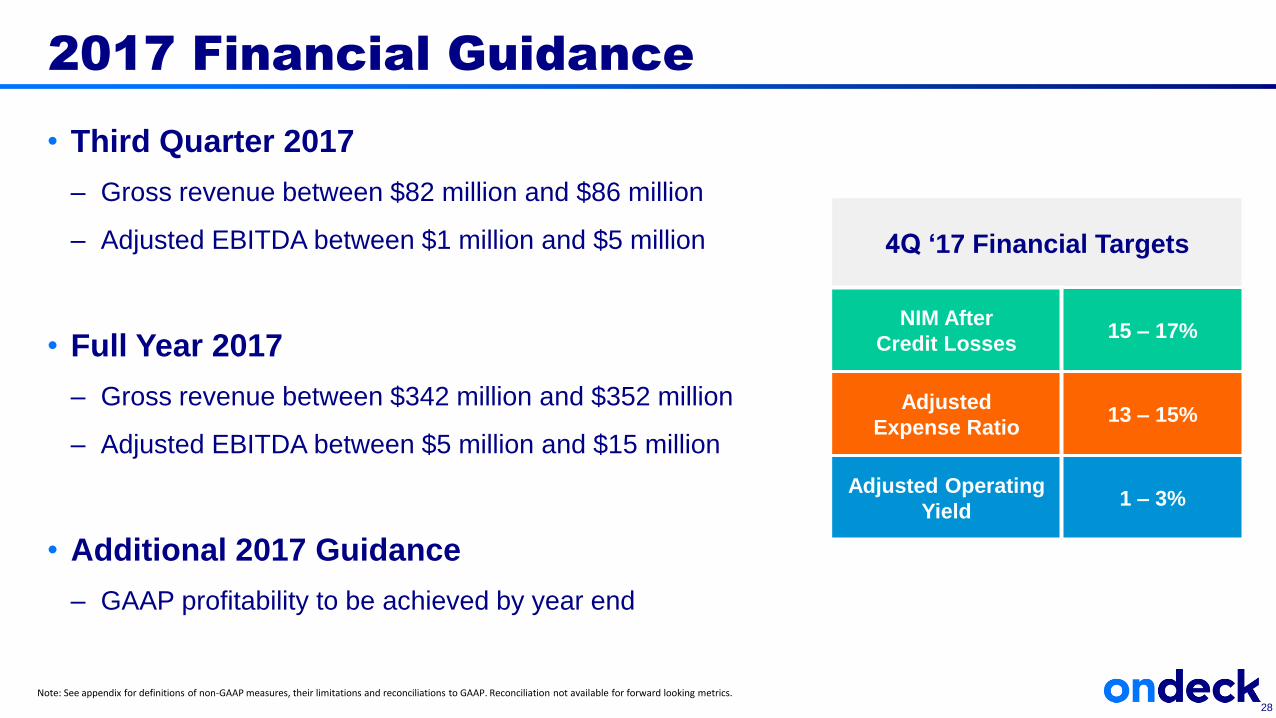

2017 Financial Guidance

• Third Quarter 2017

– Gross revenue between $82 million and $86 million

– Adjusted EBITDA between $1 million and $5 million

• Full Year 2017

– Gross revenue between $342 million and $352 million

– Adjusted EBITDA between $5 million and $15 million

• Additional 2017 Guidance

– GAAP profitability to be achieved by year end

4Q ‘17 Financial Targets

NIM After

Credit Losses15 – 17%

Adjusted

Expense Ratio13 – 15%

Adjusted Operating

Yield1 – 3%

Note: See appendix for definitions of non-GAAP measures, their limitations and reconciliations to GAAP. Reconciliation not available for forward looking metrics.

28

Appendix

29

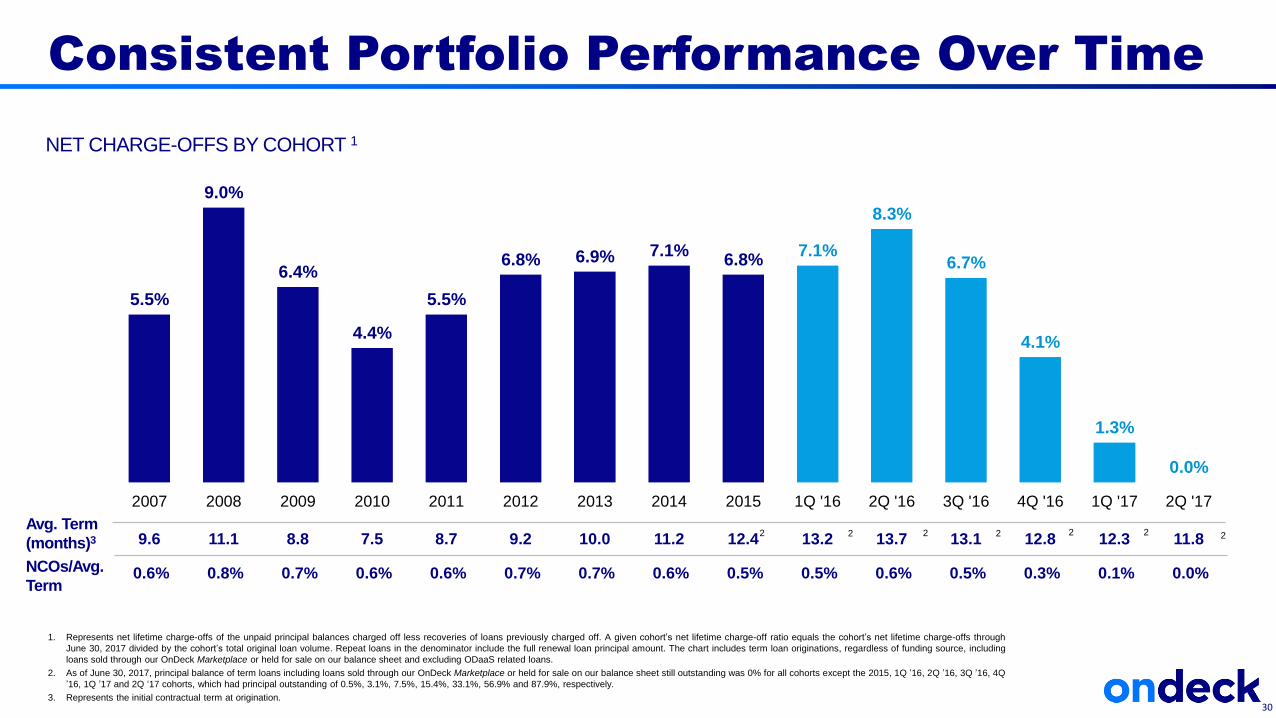

5.5%

9.0%

6.4%

4.4%

5.5%

6.8% 6.9% 7.1%6.8%

7.1%

8.3%

6.7%

4.1%

1.3%

0.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 1Q '16 2Q '16 3Q '16 4Q '16 1Q '17 2Q '17

2 2 2 2 2

Consistent Portfolio Performance Over Time

1. Represents net lifetime charge-offs of the unpaid principal balances charged off less recoveries of loans previously charged off. A given cohort’s net lifetime charge-off ratio equals the cohort’s net lifetime charge-offs through

June 30, 2017 divided by the cohort’s total original loan volume. Repeat loans in the denominator include the full renewal loan principal amount. The chart includes term loan originations, regardless of funding source, including

loans sold through our OnDeck Marketplace or held for sale on our balance sheet and excluding ODaaS related loans.

2. As of June 30, 2017, principal balance of term loans including loans sold through our OnDeck Marketplace or held for sale on our balance sheet still outstanding was 0% for all cohorts except the 2015, 1Q ’16, 2Q ’16, 3Q ’16, 4Q

’16, 1Q ’17 and 2Q ‘17 cohorts, which had principal outstanding of 0.5%, 3.1%, 7.5%, 15.4%, 33.1%, 56.9% and 87.9%, respectively.

3. Represents the initial contractual term at origination.

NET CHARGE-OFFS BY COHORT 1

9.6 11.1 8.8 7.5 8.7 9.2 10.0 11.2 12.4 13.2 13.7 13.1 12.8 12.3 11.8Avg. Term

(months)32 2

0.6% 0.8% 0.7% 0.6% 0.6% 0.7% 0.7% 0.6% 0.5% 0.5% 0.6% 0.5% 0.3% 0.1% 0.0%NCOs/Avg.

Term

30

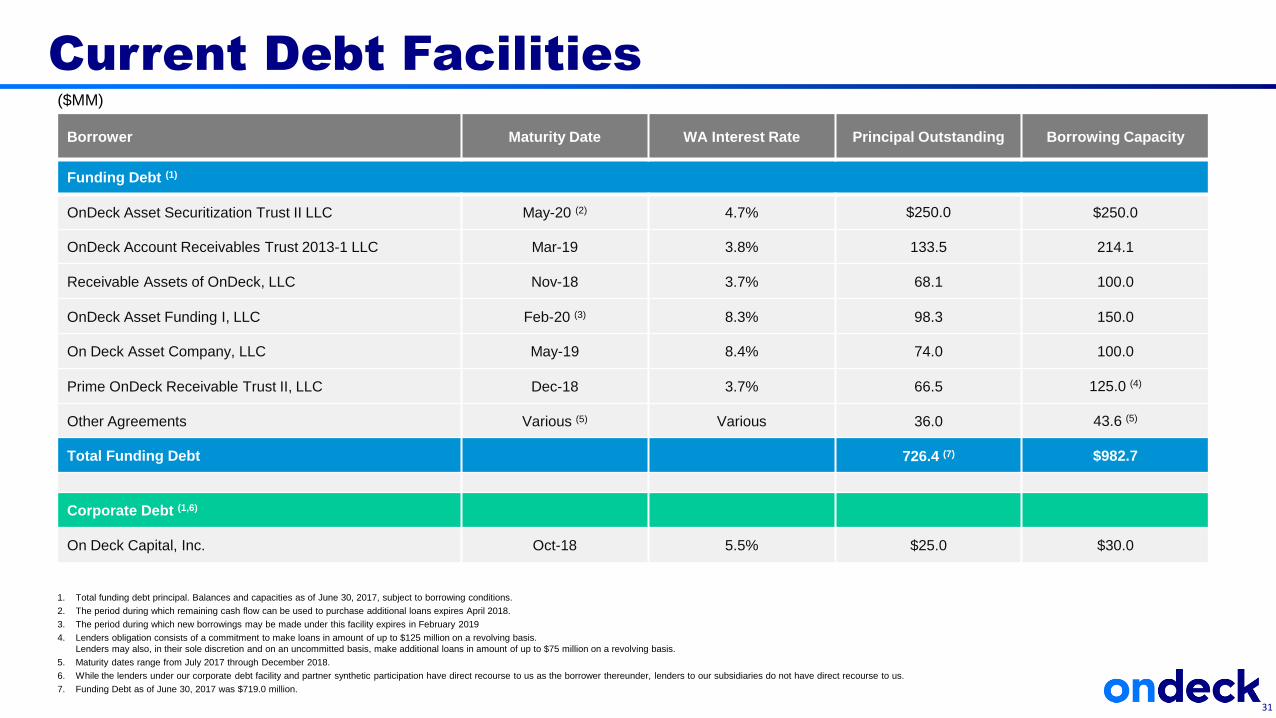

Current Debt Facilities

1. Total funding debt principal. Balances and capacities as of June 30, 2017, subject to borrowing conditions.

2. The period during which remaining cash flow can be used to purchase additional loans expires April 2018.

3. The period during which new borrowings may be made under this facility expires in February 2019

4. Lenders obligation consists of a commitment to make loans in amount of up to $125 million on a revolving basis.

Lenders may also, in their sole discretion and on an uncommitted basis, make additional loans in amount of up to $75 million on a revolving basis.

5. Maturity dates range from July 2017 through December 2018.

6. While the lenders under our corporate debt facility and partner synthetic participation have direct recourse to us as the borrower thereunder, lenders to our subsidiaries do not have direct recourse to us.

7. Funding Debt as of June 30, 2017 was $719.0 million.

Borrower Maturity Date WA Interest Rate Principal Outstanding Borrowing Capacity

Funding Debt (1)

OnDeck Asset Securitization Trust II LLC May-20 (2) 4.7% $250.0 $250.0

OnDeck Account Receivables Trust 2013-1 LLC Mar-19 3.8% 133.5 214.1

Receivable Assets of OnDeck, LLC Nov-18 3.7% 68.1 100.0

OnDeck Asset Funding I, LLC Feb-20 (3) 8.3% 98.3 150.0

On Deck Asset Company, LLC May-19 8.4% 74.0 100.0

Prime OnDeck Receivable Trust II, LLC Dec-18 3.7% 66.5 125.0 (4)

Other Agreements Various (5) Various 36.0 43.6 (5)

Total Funding Debt 726.4 (7) $982.7

Corporate Debt (1,6)

On Deck Capital, Inc. Oct-18 5.5% $25.0 $30.0

31

($MM)

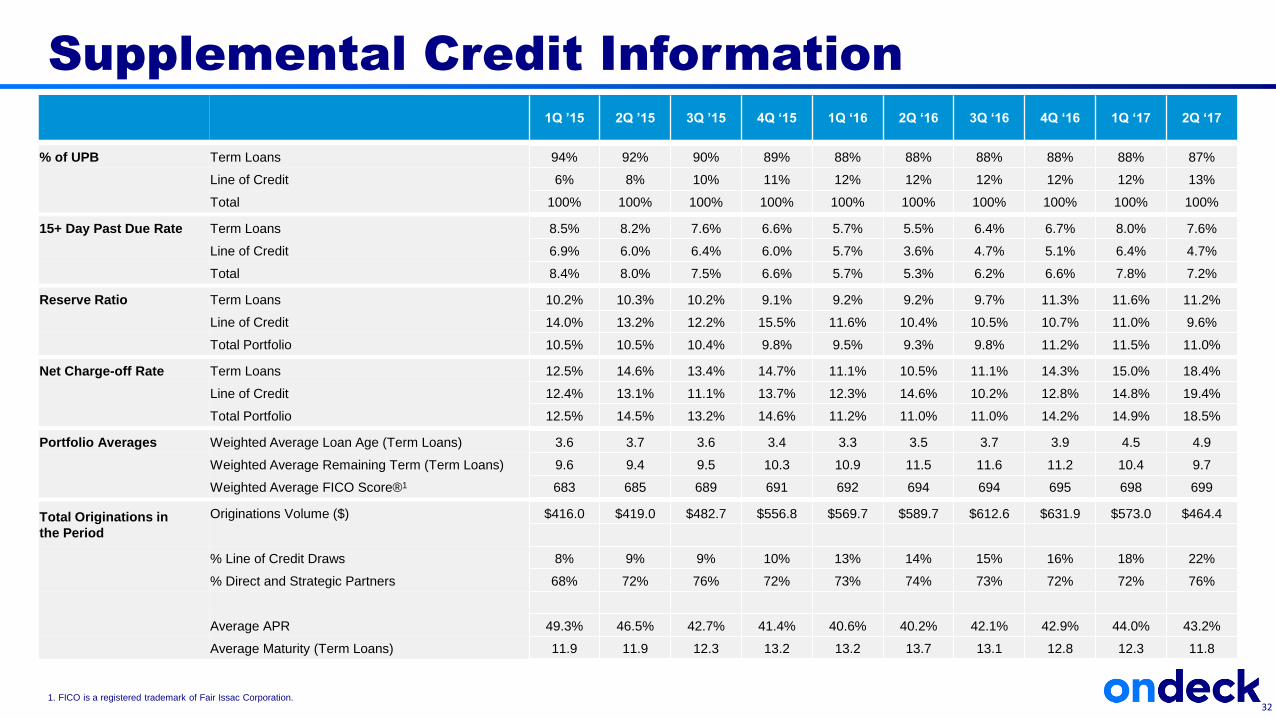

Supplemental Credit Information

1. FICO is a registered trademark of Fair Issac Corporation.32

1Q ’15 2Q ’15 3Q ’15 4Q ‘15 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

% of UPB Term Loans 94% 92% 90% 89% 88% 88% 88% 88% 88% 87%

Line of Credit 6% 8% 10% 11% 12% 12% 12% 12% 12% 13%

Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

15+ Day Past Due Rate Term Loans 8.5% 8.2% 7.6% 6.6% 5.7% 5.5% 6.4% 6.7% 8.0% 7.6%

Line of Credit 6.9% 6.0% 6.4% 6.0% 5.7% 3.6% 4.7% 5.1% 6.4% 4.7%

Total 8.4% 8.0% 7.5% 6.6% 5.7% 5.3% 6.2% 6.6% 7.8% 7.2%

Reserve Ratio Term Loans 10.2% 10.3% 10.2% 9.1% 9.2% 9.2% 9.7% 11.3% 11.6% 11.2%

Line of Credit 14.0% 13.2% 12.2% 15.5% 11.6% 10.4% 10.5% 10.7% 11.0% 9.6%

Total Portfolio 10.5% 10.5% 10.4% 9.8% 9.5% 9.3% 9.8% 11.2% 11.5% 11.0%

Net Charge-off Rate Term Loans 12.5% 14.6% 13.4% 14.7% 11.1% 10.5% 11.1% 14.3% 15.0% 18.4%

Line of Credit 12.4% 13.1% 11.1% 13.7% 12.3% 14.6% 10.2% 12.8% 14.8% 19.4%

Total Portfolio 12.5% 14.5% 13.2% 14.6% 11.2% 11.0% 11.0% 14.2% 14.9% 18.5%

Portfolio Averages Weighted Average Loan Age (Term Loans) 3.6 3.7 3.6 3.4 3.3 3.5 3.7 3.9 4.5 4.9

Weighted Average Remaining Term (Term Loans) 9.6 9.4 9.5 10.3 10.9 11.5 11.6 11.2 10.4 9.7

Weighted Average FICO Score®1 683 685 689 691 692 694 694 695 698 699

Total Originations in

the Period

Originations Volume ($) $416.0 $419.0 $482.7 $556.8 $569.7 $589.7 $612.6 $631.9 $573.0 $464.4

% Line of Credit Draws 8% 9% 9% 10% 13% 14% 15% 16% 18% 22%

% Direct and Strategic Partners 68% 72% 76% 72% 73% 74% 73% 72% 72% 76%

Average APR 49.3% 46.5% 42.7% 41.4% 40.6% 40.2% 42.1% 42.9% 44.0% 43.2%

Average Maturity (Term Loans) 11.9 11.9 12.3 13.2 13.2 13.7 13.1 12.8 12.3 11.8

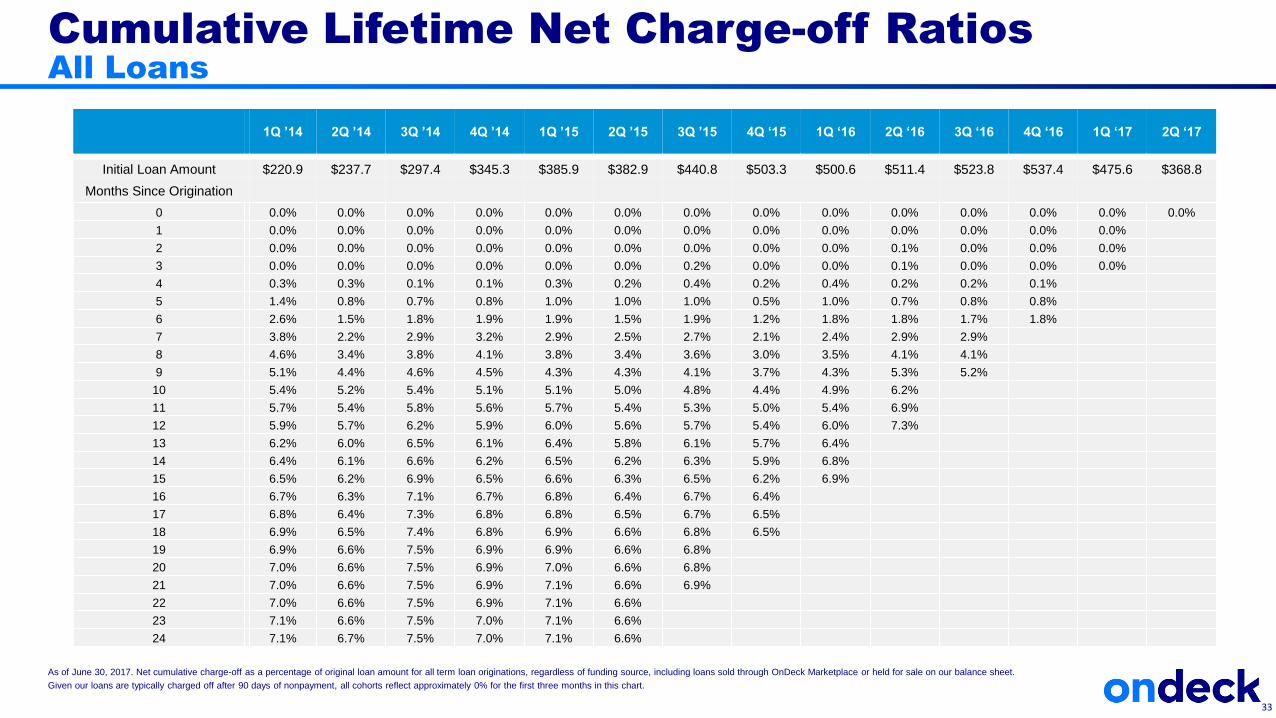

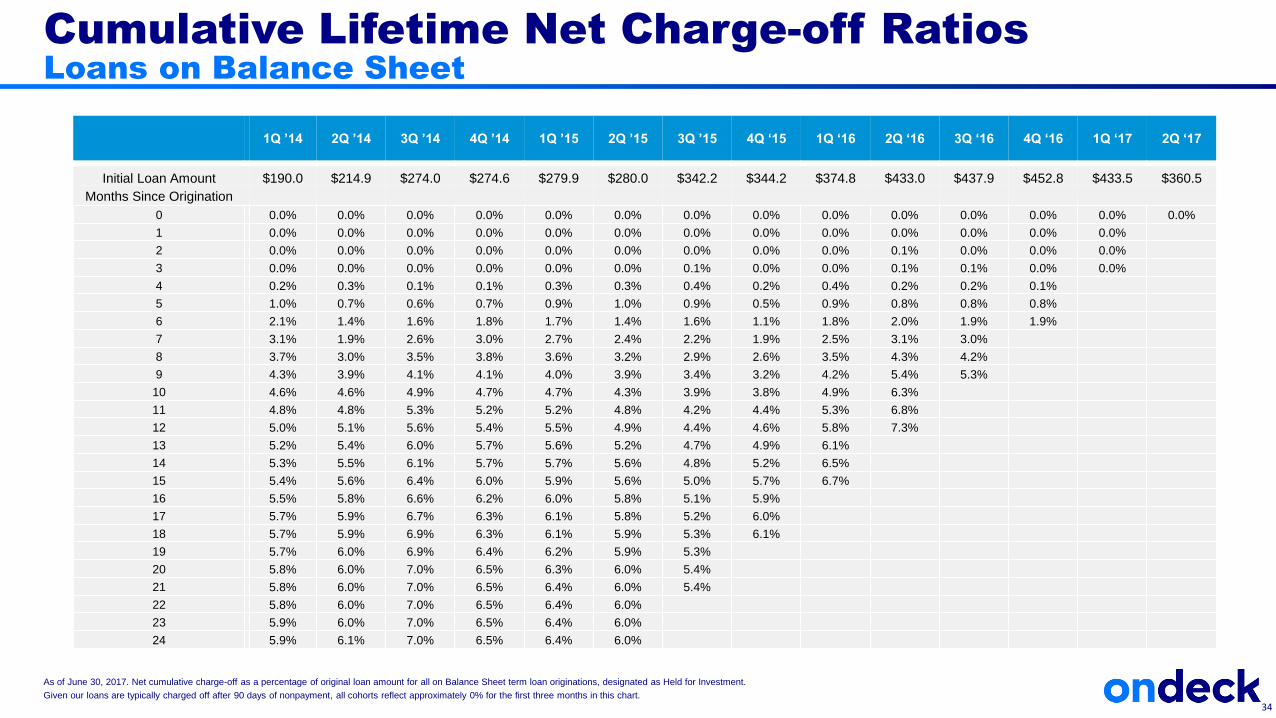

Cumulative Lifetime Net Charge-off Ratios

All Loans

As of June 30, 2017. Net cumulative charge-off as a percentage of original loan amount for all term loan originations, regardless of funding source, including loans sold through OnDeck Marketplace or held for sale on our balance sheet.

Given our loans are typically charged off after 90 days of nonpayment, all cohorts reflect approximately 0% for the first three months in this chart.

33

1Q ’14 2Q ’14 3Q ’14 4Q ’14 1Q ’15 2Q ’15 3Q ’15 4Q ‘15 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

Initial Loan Amount $220.9 $237.7 $297.4 $345.3 $385.9 $382.9 $440.8 $503.3 $500.6 $511.4 $523.8 $537.4 $475.6 $368.8

Months Since Origination

0 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

1 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

2 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% 0.0% 0.0% 0.0%

3 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.2% 0.0% 0.0% 0.1% 0.0% 0.0% 0.0%

4 0.3% 0.3% 0.1% 0.1% 0.3% 0.2% 0.4% 0.2% 0.4% 0.2% 0.2% 0.1%

5 1.4% 0.8% 0.7% 0.8% 1.0% 1.0% 1.0% 0.5% 1.0% 0.7% 0.8% 0.8%

6 2.6% 1.5% 1.8% 1.9% 1.9% 1.5% 1.9% 1.2% 1.8% 1.8% 1.7% 1.8%

7 3.8% 2.2% 2.9% 3.2% 2.9% 2.5% 2.7% 2.1% 2.4% 2.9% 2.9%

8 4.6% 3.4% 3.8% 4.1% 3.8% 3.4% 3.6% 3.0% 3.5% 4.1% 4.1%

9 5.1% 4.4% 4.6% 4.5% 4.3% 4.3% 4.1% 3.7% 4.3% 5.3% 5.2%

10 5.4% 5.2% 5.4% 5.1% 5.1% 5.0% 4.8% 4.4% 4.9% 6.2%

11 5.7% 5.4% 5.8% 5.6% 5.7% 5.4% 5.3% 5.0% 5.4% 6.9%

12 5.9% 5.7% 6.2% 5.9% 6.0% 5.6% 5.7% 5.4% 6.0% 7.3%

13 6.2% 6.0% 6.5% 6.1% 6.4% 5.8% 6.1% 5.7% 6.4%

14 6.4% 6.1% 6.6% 6.2% 6.5% 6.2% 6.3% 5.9% 6.8%

15 6.5% 6.2% 6.9% 6.5% 6.6% 6.3% 6.5% 6.2% 6.9%

16 6.7% 6.3% 7.1% 6.7% 6.8% 6.4% 6.7% 6.4%

17 6.8% 6.4% 7.3% 6.8% 6.8% 6.5% 6.7% 6.5%

18 6.9% 6.5% 7.4% 6.8% 6.9% 6.6% 6.8% 6.5%

19 6.9% 6.6% 7.5% 6.9% 6.9% 6.6% 6.8%

20 7.0% 6.6% 7.5% 6.9% 7.0% 6.6% 6.8%

21 7.0% 6.6% 7.5% 6.9% 7.1% 6.6% 6.9%

22 7.0% 6.6% 7.5% 6.9% 7.1% 6.6%

23 7.1% 6.6% 7.5% 7.0% 7.1% 6.6%

24 7.1% 6.7% 7.5% 7.0% 7.1% 6.6%

Cumulative Lifetime Net Charge-off Ratios

Loans on Balance Sheet

34

1Q ’14 2Q ’14 3Q ’14 4Q ’14 1Q ’15 2Q ’15 3Q ’15 4Q ‘15 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

Initial Loan Amount $190.0 $214.9 $274.0 $274.6 $279.9 $280.0 $342.2 $344.2 $374.8 $433.0 $437.9 $452.8 $433.5 $360.5

Months Since Origination

0 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

1 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

2 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% 0.0% 0.0% 0.0%

3 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% 0.0% 0.0% 0.1% 0.1% 0.0% 0.0%

4 0.2% 0.3% 0.1% 0.1% 0.3% 0.3% 0.4% 0.2% 0.4% 0.2% 0.2% 0.1%

5 1.0% 0.7% 0.6% 0.7% 0.9% 1.0% 0.9% 0.5% 0.9% 0.8% 0.8% 0.8%

6 2.1% 1.4% 1.6% 1.8% 1.7% 1.4% 1.6% 1.1% 1.8% 2.0% 1.9% 1.9%

7 3.1% 1.9% 2.6% 3.0% 2.7% 2.4% 2.2% 1.9% 2.5% 3.1% 3.0%

8 3.7% 3.0% 3.5% 3.8% 3.6% 3.2% 2.9% 2.6% 3.5% 4.3% 4.2%

9 4.3% 3.9% 4.1% 4.1% 4.0% 3.9% 3.4% 3.2% 4.2% 5.4% 5.3%

10 4.6% 4.6% 4.9% 4.7% 4.7% 4.3% 3.9% 3.8% 4.9% 6.3%

11 4.8% 4.8% 5.3% 5.2% 5.2% 4.8% 4.2% 4.4% 5.3% 6.8%

12 5.0% 5.1% 5.6% 5.4% 5.5% 4.9% 4.4% 4.6% 5.8% 7.3%

13 5.2% 5.4% 6.0% 5.7% 5.6% 5.2% 4.7% 4.9% 6.1%

14 5.3% 5.5% 6.1% 5.7% 5.7% 5.6% 4.8% 5.2% 6.5%

15 5.4% 5.6% 6.4% 6.0% 5.9% 5.6% 5.0% 5.7% 6.7%

16 5.5% 5.8% 6.6% 6.2% 6.0% 5.8% 5.1% 5.9%

17 5.7% 5.9% 6.7% 6.3% 6.1% 5.8% 5.2% 6.0%

18 5.7% 5.9% 6.9% 6.3% 6.1% 5.9% 5.3% 6.1%

19 5.7% 6.0% 6.9% 6.4% 6.2% 5.9% 5.3%

20 5.8% 6.0% 7.0% 6.5% 6.3% 6.0% 5.4%

21 5.8% 6.0% 7.0% 6.5% 6.4% 6.0% 5.4%

22 5.8% 6.0% 7.0% 6.5% 6.4% 6.0%

23 5.9% 6.0% 7.0% 6.5% 6.4% 6.0%

24 5.9% 6.1% 7.0% 6.5% 6.4% 6.0%

As of June 30, 2017. Net cumulative charge-off as a percentage of original loan amount for all on Balance Sheet term loan originations, designated as Held for Investment.

Given our loans are typically charged off after 90 days of nonpayment, all cohorts reflect approximately 0% for the first three months in this chart.

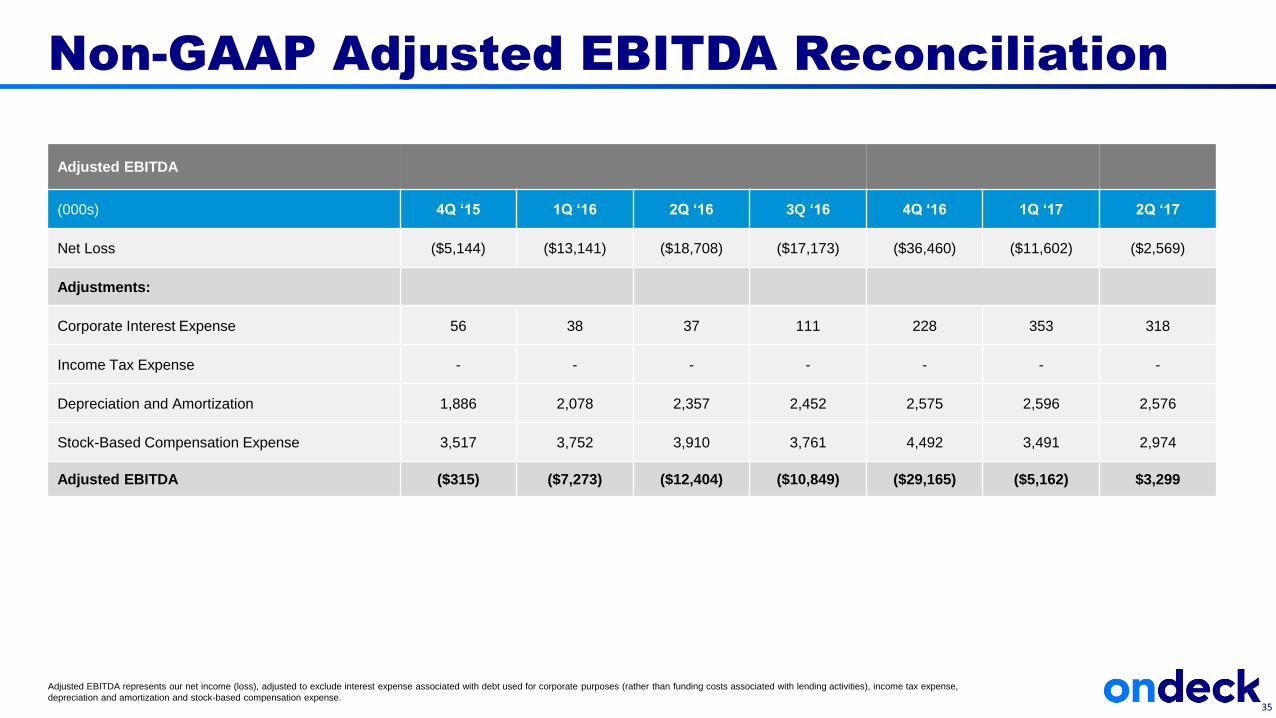

Adjusted EBITDA

(000s) 4Q ‘15 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

Net Loss ($5,144) ($13,141) ($18,708) ($17,173) ($36,460) ($11,602) ($2,569)

Adjustments:

Corporate Interest Expense 56 38 37 111 228 353 318

Income Tax Expense - - - - - - -

Depreciation and Amortization 1,886 2,078 2,357 2,452 2,575 2,596 2,576

Stock-Based Compensation Expense 3,517 3,752 3,910 3,761 4,492 3,491 2,974

Adjusted EBITDA ($315) ($7,273) ($12,404) ($10,849) ($29,165) ($5,162) $3,299

Non-GAAP Adjusted EBITDA Reconciliation

Adjusted EBITDA represents our net income (loss), adjusted to exclude interest expense associated with debt used for corporate purposes (rather than funding costs associated with lending activities), income tax expense,

depreciation and amortization and stock-based compensation expense. 35

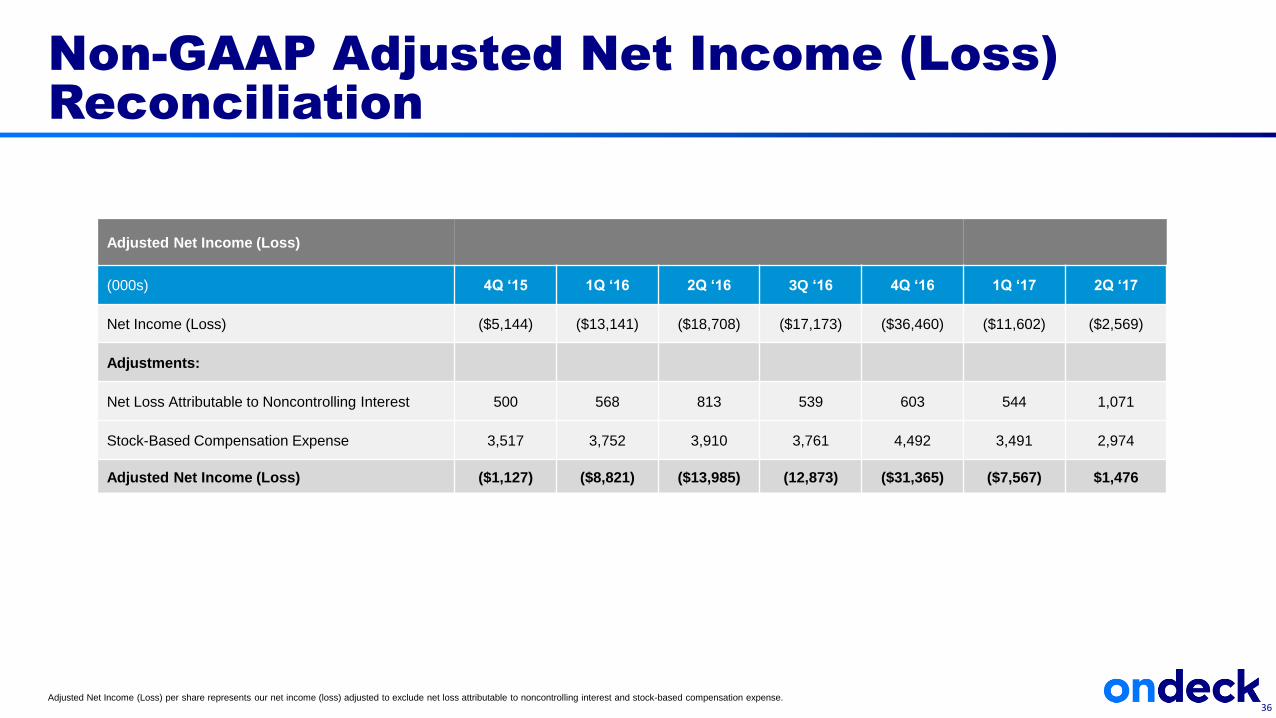

Adjusted Net Income (Loss)

(000s) 4Q ‘15 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

Net Income (Loss) ($5,144) ($13,141) ($18,708) ($17,173) ($36,460) ($11,602) ($2,569)

Adjustments:

Net Loss Attributable to Noncontrolling Interest 500 568 813 539 603 544 1,071

Stock-Based Compensation Expense 3,517 3,752 3,910 3,761 4,492 3,491 2,974

Adjusted Net Income (Loss) ($1,127) ($8,821) ($13,985) (12,873) ($31,365) ($7,567) $1,476

Non-GAAP Adjusted Net Income (Loss)

Reconciliation

Adjusted Net Income (Loss) per share represents our net income (loss) adjusted to exclude net loss attributable to noncontrolling interest and stock-based compensation expense.36

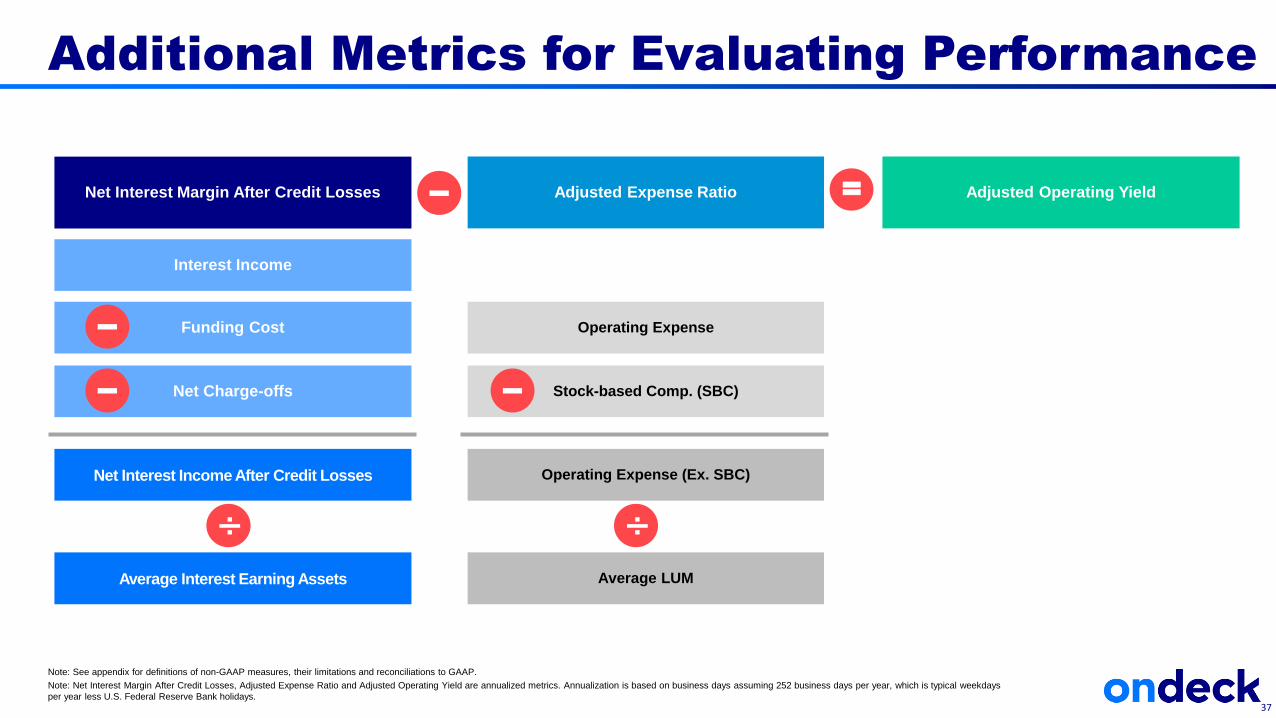

Additional Metrics for Evaluating Performance

37

Note: See appendix for definitions of non-GAAP measures, their limitations and reconciliations to GAAP.

Note: Net Interest Margin After Credit Losses, Adjusted Expense Ratio and Adjusted Operating Yield are annualized metrics. Annualization is based on business days assuming 252 business days per year, which is typical weekdays

per year less U.S. Federal Reserve Bank holidays.

Funding Cost

Interest Income

Net Charge-offs

Net Interest Income After Credit Losses

Average Interest Earning Assets

Stock-based Comp. (SBC)

Operating Expense

Operating Expense (Ex. SBC)

Average LUM

÷

Net Interest Margin After Credit Losses Adjusted Expense Ratio Adjusted Operating Yield=

÷

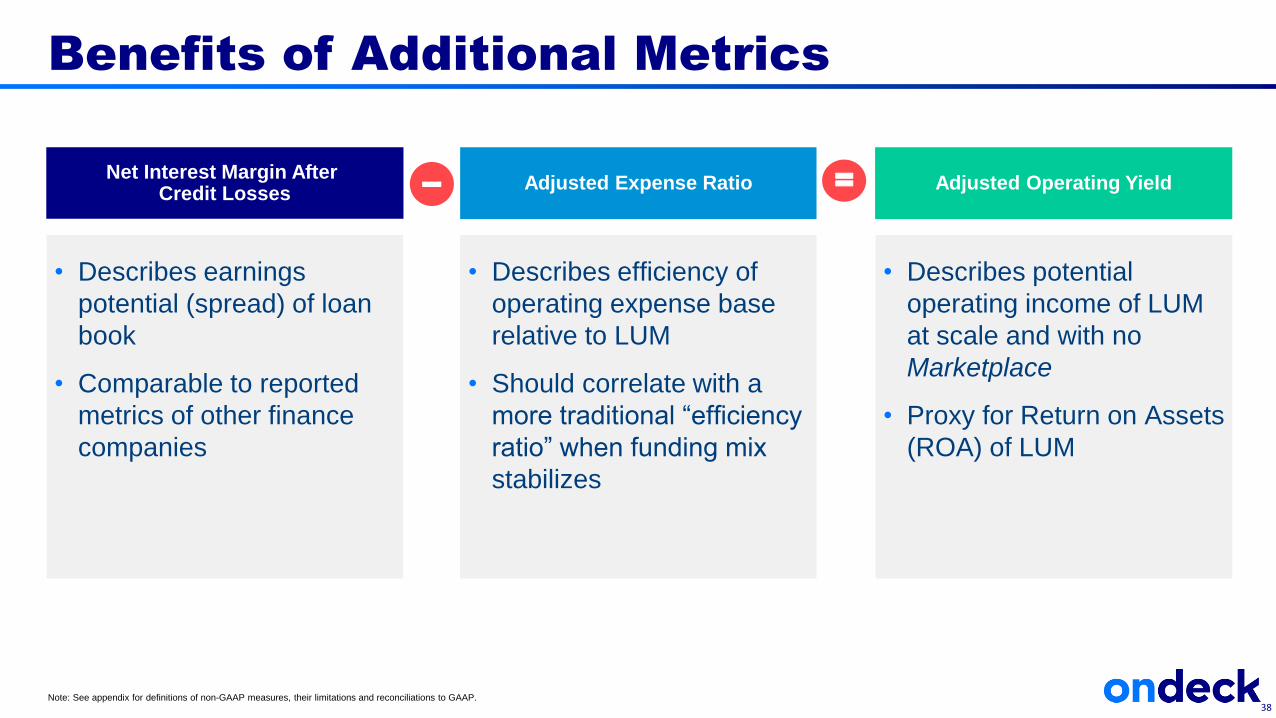

• Describes earnings

potential (spread) of loan

book

• Comparable to reported

metrics of other finance

companies

Benefits of Additional Metrics

Note: See appendix for definitions of non-GAAP measures, their limitations and reconciliations to GAAP.

Net Interest Margin After Credit Losses

Adjusted Expense Ratio Adjusted Operating Yield=

• Describes efficiency of

operating expense base

relative to LUM

• Should correlate with a

more traditional “efficiency

ratio” when funding mix

stabilizes

• Describes potential

operating income of LUM

at scale and with no

Marketplace

• Proxy for Return on Assets

(ROA) of LUM

38

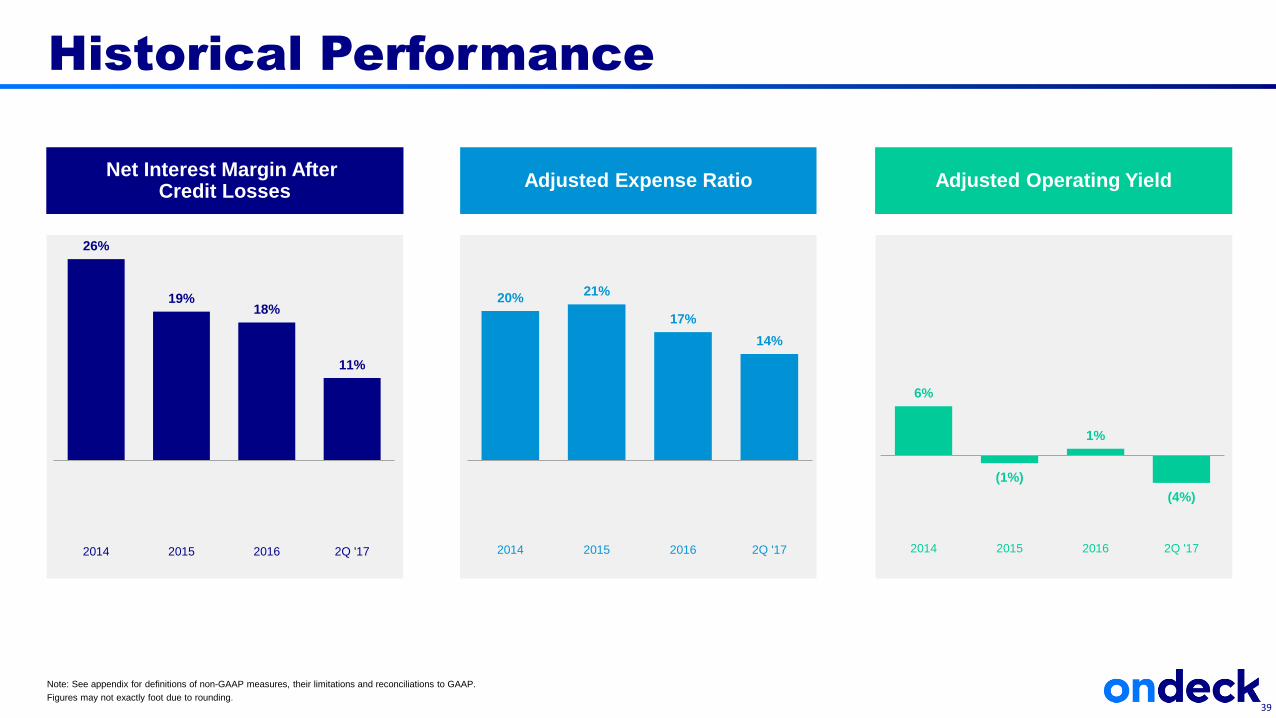

Historical Performance

Note: See appendix for definitions of non-GAAP measures, their limitations and reconciliations to GAAP.

Figures may not exactly foot due to rounding.

Net Interest Margin After Credit Losses

26%

19%18%

11%

2014 2015 2016 2Q '17

Adjusted Expense Ratio

20%21%

17%

14%

2014 2015 2016 2Q '17

Adjusted Operating Yield

6%

(1%)

1%

(4%)

2014 2015 2016 2Q '17

39

Non-GAAP Net Interest Margin After Credit

Losses Calculation and Reconciliation

Note: See following slide for further definition, uses and limitations of this non-GAAP metric.

1. Annualization is based on business days assuming 252 business days per year, which is typical weekdays per year less U.S. Federal Reserve Bank holidays.40

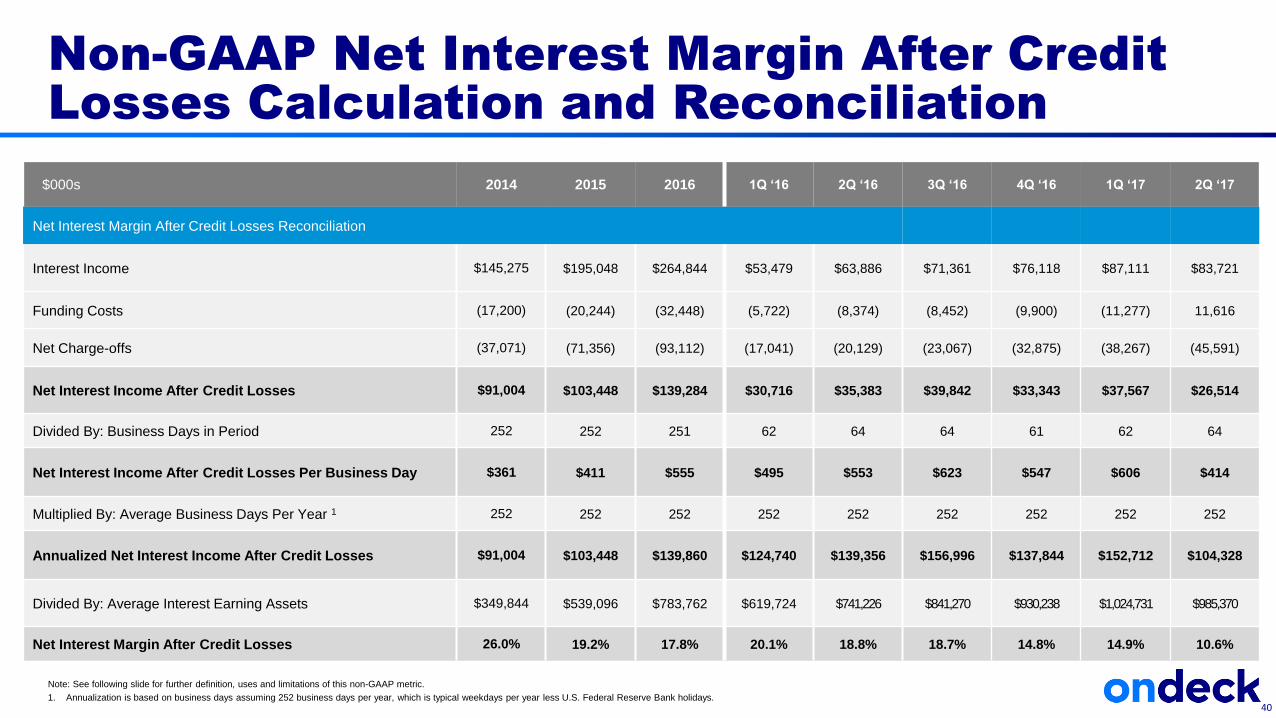

$000s 2014 2015 2016 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

Net Interest Margin After Credit Losses Reconciliation

Interest Income $145,275 $195,048 $264,844 $53,479 $63,886 $71,361 $76,118 $87,111 $83,721

Funding Costs (17,200) (20,244) (32,448) (5,722) (8,374) (8,452) (9,900) (11,277) 11,616

Net Charge-offs (37,071) (71,356) (93,112) (17,041) (20,129) (23,067) (32,875) (38,267) (45,591)

Net Interest Income After Credit Losses $91,004 $103,448 $139,284 $30,716 $35,383 $39,842 $33,343 $37,567 $26,514

Divided By: Business Days in Period 252 252 251 62 64 64 61 62 64

Net Interest Income After Credit Losses Per Business Day $361 $411 $555 $495 $553 $623 $547 $606 $414

Multiplied By: Average Business Days Per Year 1 252 252 252 252 252 252 252 252 252

Annualized Net Interest Income After Credit Losses $91,004 $103,448 $139,860 $124,740 $139,356 $156,996 $137,844 $152,712 $104,328

Divided By: Average Interest Earning Assets $349,844 $539,096 $783,762 $619,724 $741,226 $841,270 $930,238 $1,024,731 $985,370

Net Interest Margin After Credit Losses 26.0% 19.2% 17.8% 20.1% 18.8% 18.7% 14.8% 14.9% 10.6%

Net Interest Margin After Credit Losses, or NIM After Credit Losses, is calculated as our business day adjusted annualized Net Interest Income After Credit Losses divided by Average Interest Earning Assets.

Net Interest Income After Credit Losses represents interest income less funding cost and net charge-offs. Interest income is net of deferred costs and fees on loans held for investment and held for sale. Net deferred origination costs in loans held for investment and loans held for sale consist of deferred origination costs as offset by corresponding deferred origination fees. Deferred origination fees include fees paid up front to us by customers when loans are funded. Deferred origination costs are limited to costs directly attributable to originating loans such as commissions, vendor costs and personnel costs directly related to the time spent by the personnel performing activities related to loan origination. Funding cost is the interest expense, fees, and amortization of deferred debt issuance costs we incur in connection with our lending activities across all of our debt facilities. Net charge-offs are charged-off loans in the period, net of recoveries. Annualization is based on business days assuming 252 business days per year, which is typical weekdays per year less U.S. Federal Reserve Bank holidays.

Management believes that using Net Interest Margin After Credit Losses is useful to analyze the lending operating performance of the business unaffected by the provision for loan losses impact of the growth in originations. In accordance with GAAP, we recognize revenue on loans over their term, but provide for probable credit losses on the loans at the time they are originated. With respect to the forward-looking guidance of this metric, OnDeck is not able to provide a reconciliation of this non-GAAP measure to GAAP. Certain items that impact these measures have not yet occurred, are out of OnDeck’s control and/or cannot be reasonably predicted, and as a result, reconciliation of the forward-looking non-GAAP guidance measures to GAAP is not available without unreasonable effort.

Our use of Net Interest Margin After Credit Losses has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are:

• Net Interest Margin After Credit Losses is the rate of net return we achieve on our Average Interest Earning Assets outstanding during a period. It does not reflect the return from loans sold through OnDeck Marketplace, specifically our gain on sale revenue. Similarly, Average Interest Earning Assets does not include the unpaid principal balance of loans sold through Marketplace. Further, Net Interest Margin After Credit Losses does not include servicing revenue related to loans previously sold, fair value adjustments to servicing rights, monthly fees charged to customers for our line of credit, and marketing fees earned from our issuing bank partners, which are recognized as the related services are provided.

• Net Interest Margin After Credit Losses reflects net charge-offs in the period rather than provision for loan losses. To the extent that originations continue to grow significantly, our charge-offs will likely be lower than the probable credit losses inherent in the portfolio upon origination. Furthermore, provision for loan losses consists of amounts charged to income during the period to maintain an allowance for loan losses, or ALLL. In addition to net charge-offs, our ALLL represents our estimate of the expected credit losses inherent in our portfolio of term loans and lines of credit and is based on a variety of factors, including the composition and quality of the portfolio, loan specific information gathered through our collection efforts, delinquency levels, our historical loss experience and general economic conditions.

• Funding cost does not reflect interest associated with debt used for corporate purposes.

Net Interest Margin After Credit Losses

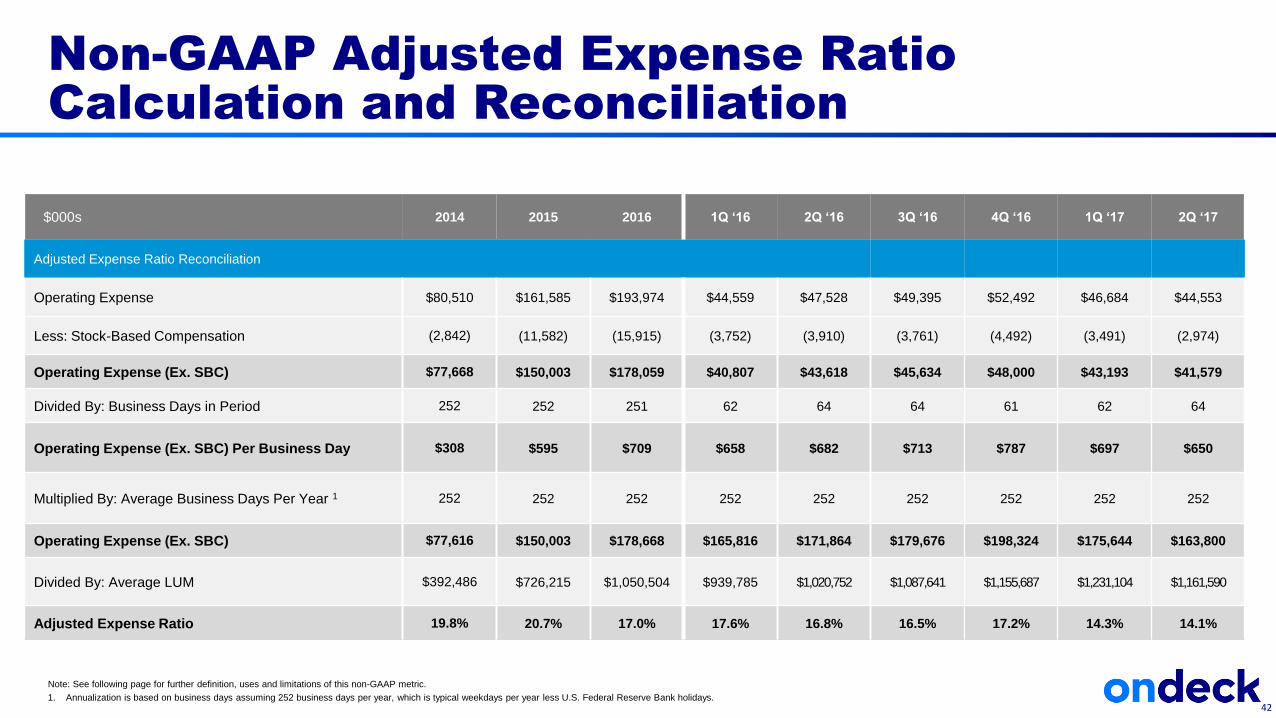

41

$000s 2014 2015 2016 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

Adjusted Expense Ratio Reconciliation

Operating Expense $80,510 $161,585 $193,974 $44,559 $47,528 $49,395 $52,492 $46,684 $44,553

Less: Stock-Based Compensation (2,842) (11,582) (15,915) (3,752) (3,910) (3,761) (4,492) (3,491) (2,974)

Operating Expense (Ex. SBC) $77,668 $150,003 $178,059 $40,807 $43,618 $45,634 $48,000 $43,193 $41,579

Divided By: Business Days in Period 252 252 251 62 64 64 61 62 64

Operating Expense (Ex. SBC) Per Business Day $308 $595 $709 $658 $682 $713 $787 $697 $650

Multiplied By: Average Business Days Per Year 1 252 252 252 252 252 252 252 252 252

Operating Expense (Ex. SBC) $77,616 $150,003 $178,668 $165,816 $171,864 $179,676 $198,324 $175,644 $163,800

Divided By: Average LUM $392,486 $726,215 $1,050,504 $939,785 $1,020,752 $1,087,641 $1,155,687 $1,231,104 $1,161,590

Adjusted Expense Ratio 19.8% 20.7% 17.0% 17.6% 16.8% 16.5% 17.2% 14.3% 14.1%

Non-GAAP Adjusted Expense Ratio

Calculation and Reconciliation

Note: See following page for further definition, uses and limitations of this non-GAAP metric.

1. Annualization is based on business days assuming 252 business days per year, which is typical weekdays per year less U.S. Federal Reserve Bank holidays.42

Adjusted Expense Ratio represents our annualized operating expense, adjusted to exclude the impact of stock-based compensation, divided

by Average Loans Under Management, or Average LUM. Loans Under Management represents the Unpaid Principal Balance plus the amount

of principal outstanding of loans held for sale, excluding net deferred origination costs, plus the amount of principal outstanding of term loans

we serviced for others at the end of the period. Average LUM is calculated as the average of Loans Under Management at the beginning of

the period and the end of each month in the period. Annualization is based on business days assuming 252 business days per year, which is

typical weekdays per year less U.S. Federal Reserve Bank holidays.

Management believes that using the Adjusted Expense Ratio is a useful to analyze the level of operating expenses incurred by the business

compared to the level outstanding principal of loans, regardless of the funding source deployed to fund the loan. With respect to the forward-

looking guidance of this metric, OnDeck is not able to provide a reconciliation of this non-GAAP measure to GAAP. Certain items that impact

these measures have not yet occurred, are out of OnDeck’s control and/or cannot be reasonably predicted, and as a result, reconciliation of

the forward-looking non-GAAP guidance measures to GAAP is not available without unreasonable effort.

Our use of Adjusted Expense Ratio has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for

analysis of our results as reported under GAAP. Some of these limitations are:

• Adjusted Expense Ratio does not reflect the potentially dilutive impact of equity-based compensation.

• Adjusted Expense Ratio is based on the unpaid principal balance of loans outstanding, regardless of funding source, and does not take into

account the revenue earned in the period and may not correspond with the timing of the expenses incurred to originate new loans.

Adjusted Expense Ratio

43

$000s 2015 2016 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

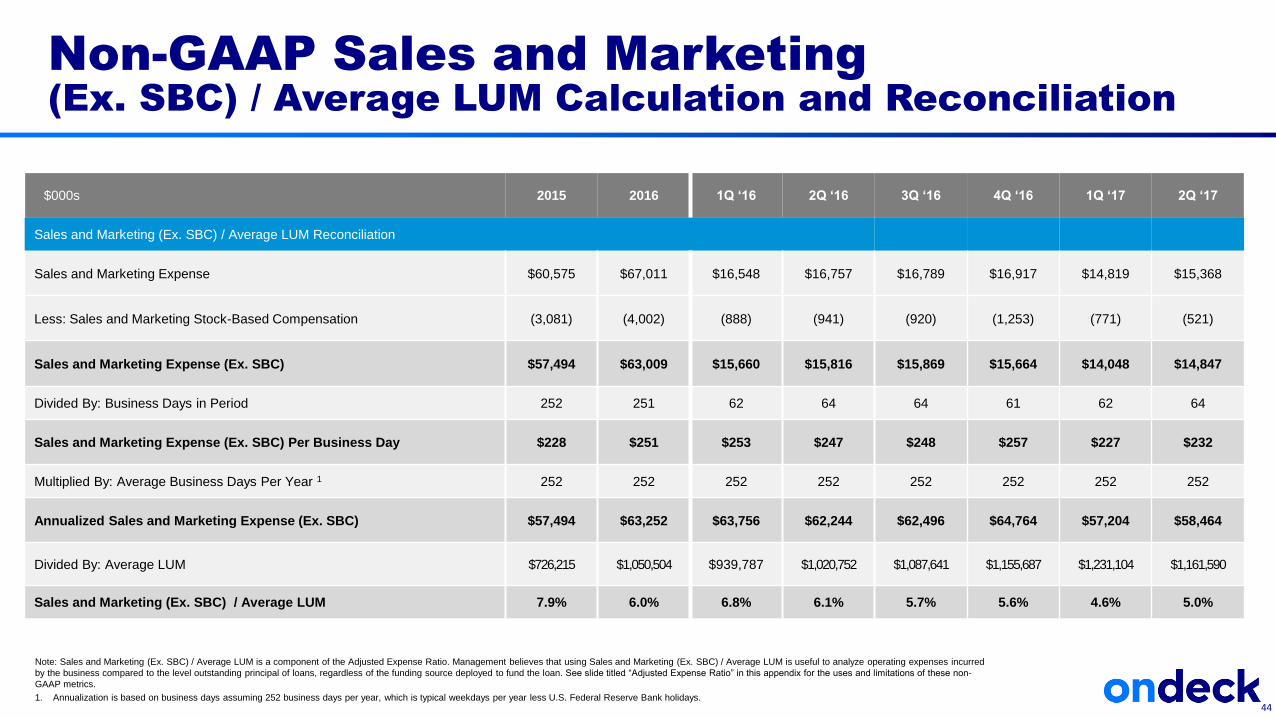

Sales and Marketing (Ex. SBC) / Average LUM Reconciliation

Sales and Marketing Expense $60,575 $67,011 $16,548 $16,757 $16,789 $16,917 $14,819 $15,368

Less: Sales and Marketing Stock-Based Compensation (3,081) (4,002) (888) (941) (920) (1,253) (771) (521)

Sales and Marketing Expense (Ex. SBC) $57,494 $63,009 $15,660 $15,816 $15,869 $15,664 $14,048 $14,847

Divided By: Business Days in Period 252 251 62 64 64 61 62 64

Sales and Marketing Expense (Ex. SBC) Per Business Day $228 $251 $253 $247 $248 $257 $227 $232

Multiplied By: Average Business Days Per Year 1 252 252 252 252 252 252 252 252

Annualized Sales and Marketing Expense (Ex. SBC) $57,494 $63,252 $63,756 $62,244 $62,496 $64,764 $57,204 $58,464

Divided By: Average LUM $726,215 $1,050,504 $939,787 $1,020,752 $1,087,641 $1,155,687 $1,231,104 $1,161,590

Sales and Marketing (Ex. SBC) / Average LUM 7.9% 6.0% 6.8% 6.1% 5.7% 5.6% 4.6% 5.0%

Non-GAAP Sales and Marketing

(Ex. SBC) / Average LUM Calculation and Reconciliation

Note: Sales and Marketing (Ex. SBC) / Average LUM is a component of the Adjusted Expense Ratio. Management believes that using Sales and Marketing (Ex. SBC) / Average LUM is useful to analyze operating expenses incurred

by the business compared to the level outstanding principal of loans, regardless of the funding source deployed to fund the loan. See slide titled “Adjusted Expense Ratio” in this appendix for the uses and limitations of these non-

GAAP metrics.

1. Annualization is based on business days assuming 252 business days per year, which is typical weekdays per year less U.S. Federal Reserve Bank holidays.44

$000s 2015 2016 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

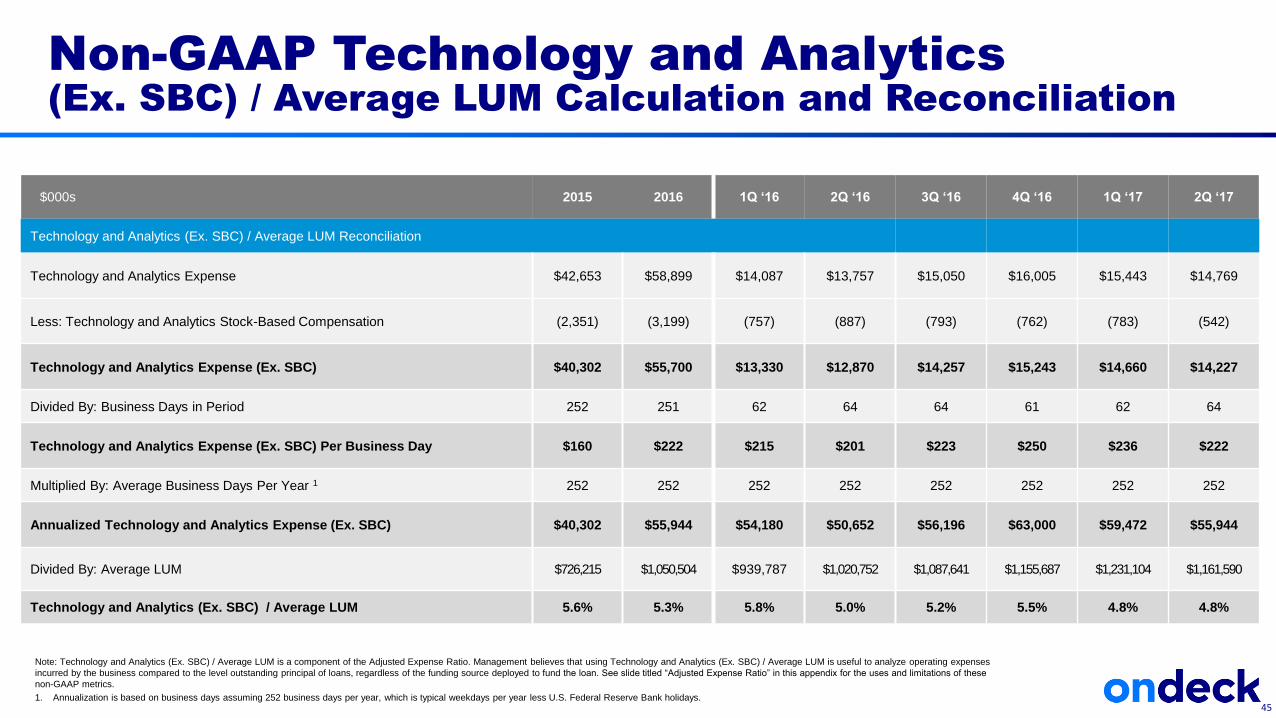

Technology and Analytics (Ex. SBC) / Average LUM Reconciliation

Technology and Analytics Expense $42,653 $58,899 $14,087 $13,757 $15,050 $16,005 $15,443 $14,769

Less: Technology and Analytics Stock-Based Compensation (2,351) (3,199) (757) (887) (793) (762) (783) (542)

Technology and Analytics Expense (Ex. SBC) $40,302 $55,700 $13,330 $12,870 $14,257 $15,243 $14,660 $14,227

Divided By: Business Days in Period 252 251 62 64 64 61 62 64

Technology and Analytics Expense (Ex. SBC) Per Business Day $160 $222 $215 $201 $223 $250 $236 $222

Multiplied By: Average Business Days Per Year 1 252 252 252 252 252 252 252 252

Annualized Technology and Analytics Expense (Ex. SBC) $40,302 $55,944 $54,180 $50,652 $56,196 $63,000 $59,472 $55,944

Divided By: Average LUM $726,215 $1,050,504 $939,787 $1,020,752 $1,087,641 $1,155,687 $1,231,104 $1,161,590

Technology and Analytics (Ex. SBC) / Average LUM 5.6% 5.3% 5.8% 5.0% 5.2% 5.5% 4.8% 4.8%

Non-GAAP Technology and Analytics

(Ex. SBC) / Average LUM Calculation and Reconciliation

Note: Technology and Analytics (Ex. SBC) / Average LUM is a component of the Adjusted Expense Ratio. Management believes that using Technology and Analytics (Ex. SBC) / Average LUM is useful to analyze operating expenses

incurred by the business compared to the level outstanding principal of loans, regardless of the funding source deployed to fund the loan. See slide titled “Adjusted Expense Ratio” in this appendix for the uses and limitations of these

non-GAAP metrics.

1. Annualization is based on business days assuming 252 business days per year, which is typical weekdays per year less U.S. Federal Reserve Bank holidays.45

$000s 2015 2016 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

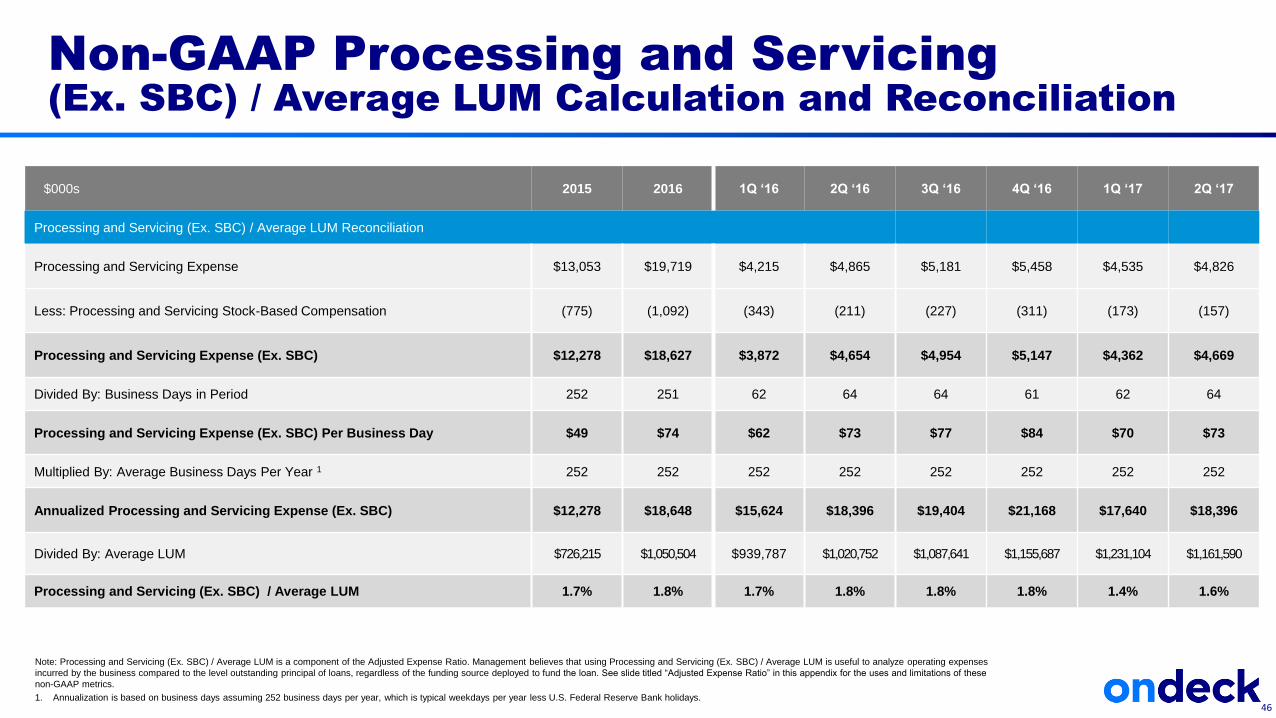

Processing and Servicing (Ex. SBC) / Average LUM Reconciliation

Processing and Servicing Expense $13,053 $19,719 $4,215 $4,865 $5,181 $5,458 $4,535 $4,826

Less: Processing and Servicing Stock-Based Compensation (775) (1,092) (343) (211) (227) (311) (173) (157)

Processing and Servicing Expense (Ex. SBC) $12,278 $18,627 $3,872 $4,654 $4,954 $5,147 $4,362 $4,669

Divided By: Business Days in Period 252 251 62 64 64 61 62 64

Processing and Servicing Expense (Ex. SBC) Per Business Day $49 $74 $62 $73 $77 $84 $70 $73

Multiplied By: Average Business Days Per Year 1 252 252 252 252 252 252 252 252

Annualized Processing and Servicing Expense (Ex. SBC) $12,278 $18,648 $15,624 $18,396 $19,404 $21,168 $17,640 $18,396

Divided By: Average LUM $726,215 $1,050,504 $939,787 $1,020,752 $1,087,641 $1,155,687 $1,231,104 $1,161,590

Processing and Servicing (Ex. SBC) / Average LUM 1.7% 1.8% 1.7% 1.8% 1.8% 1.8% 1.4% 1.6%

Non-GAAP Processing and Servicing

(Ex. SBC) / Average LUM Calculation and Reconciliation

Note: Processing and Servicing (Ex. SBC) / Average LUM is a component of the Adjusted Expense Ratio. Management believes that using Processing and Servicing (Ex. SBC) / Average LUM is useful to analyze operating expenses

incurred by the business compared to the level outstanding principal of loans, regardless of the funding source deployed to fund the loan. See slide titled “Adjusted Expense Ratio” in this appendix for the uses and limitations of these

non-GAAP metrics.

1. Annualization is based on business days assuming 252 business days per year, which is typical weekdays per year less U.S. Federal Reserve Bank holidays.46

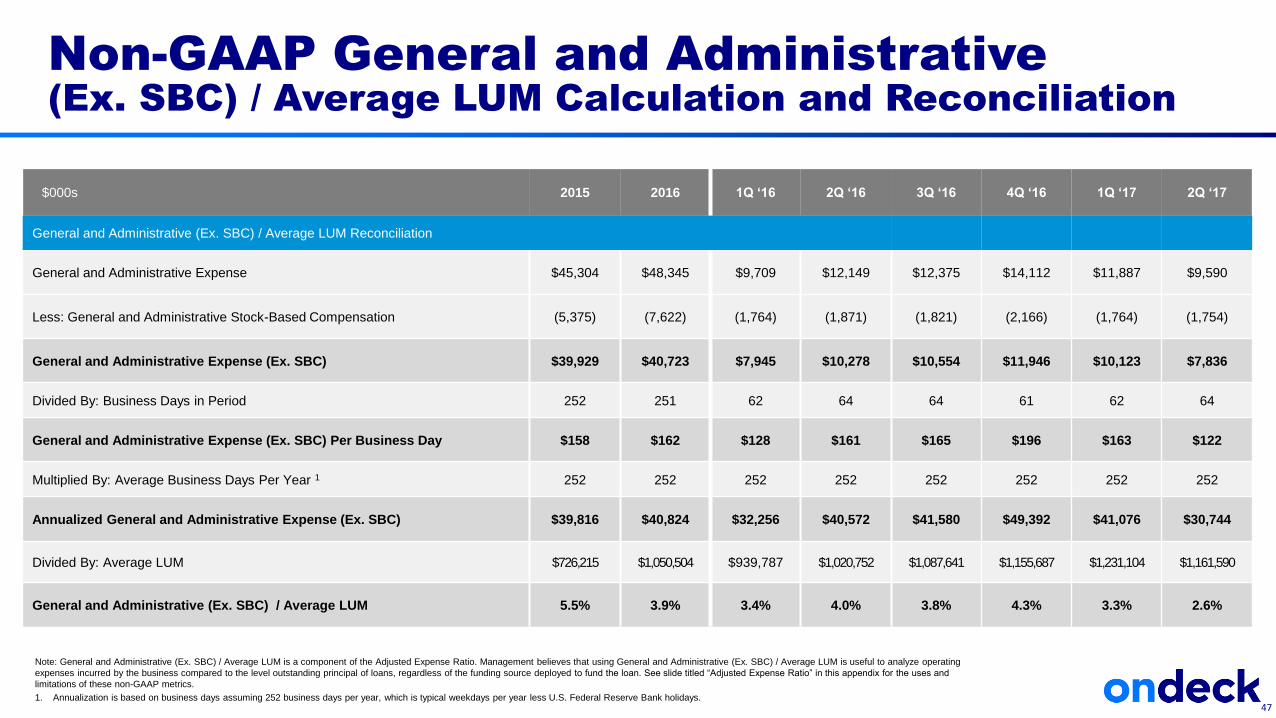

$000s 2015 2016 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

General and Administrative (Ex. SBC) / Average LUM Reconciliation

General and Administrative Expense $45,304 $48,345 $9,709 $12,149 $12,375 $14,112 $11,887 $9,590

Less: General and Administrative Stock-Based Compensation (5,375) (7,622) (1,764) (1,871) (1,821) (2,166) (1,764) (1,754)

General and Administrative Expense (Ex. SBC) $39,929 $40,723 $7,945 $10,278 $10,554 $11,946 $10,123 $7,836

Divided By: Business Days in Period 252 251 62 64 64 61 62 64

General and Administrative Expense (Ex. SBC) Per Business Day $158 $162 $128 $161 $165 $196 $163 $122

Multiplied By: Average Business Days Per Year 1 252 252 252 252 252 252 252 252

Annualized General and Administrative Expense (Ex. SBC) $39,816 $40,824 $32,256 $40,572 $41,580 $49,392 $41,076 $30,744

Divided By: Average LUM $726,215 $1,050,504 $939,787 $1,020,752 $1,087,641 $1,155,687 $1,231,104 $1,161,590

General and Administrative (Ex. SBC) / Average LUM 5.5% 3.9% 3.4% 4.0% 3.8% 4.3% 3.3% 2.6%

Non-GAAP General and Administrative

(Ex. SBC) / Average LUM Calculation and Reconciliation

Note: General and Administrative (Ex. SBC) / Average LUM is a component of the Adjusted Expense Ratio. Management believes that using General and Administrative (Ex. SBC) / Average LUM is useful to analyze operating

expenses incurred by the business compared to the level outstanding principal of loans, regardless of the funding source deployed to fund the loan. See slide titled “Adjusted Expense Ratio” in this appendix for the uses and

limitations of these non-GAAP metrics.

1. Annualization is based on business days assuming 252 business days per year, which is typical weekdays per year less U.S. Federal Reserve Bank holidays.47

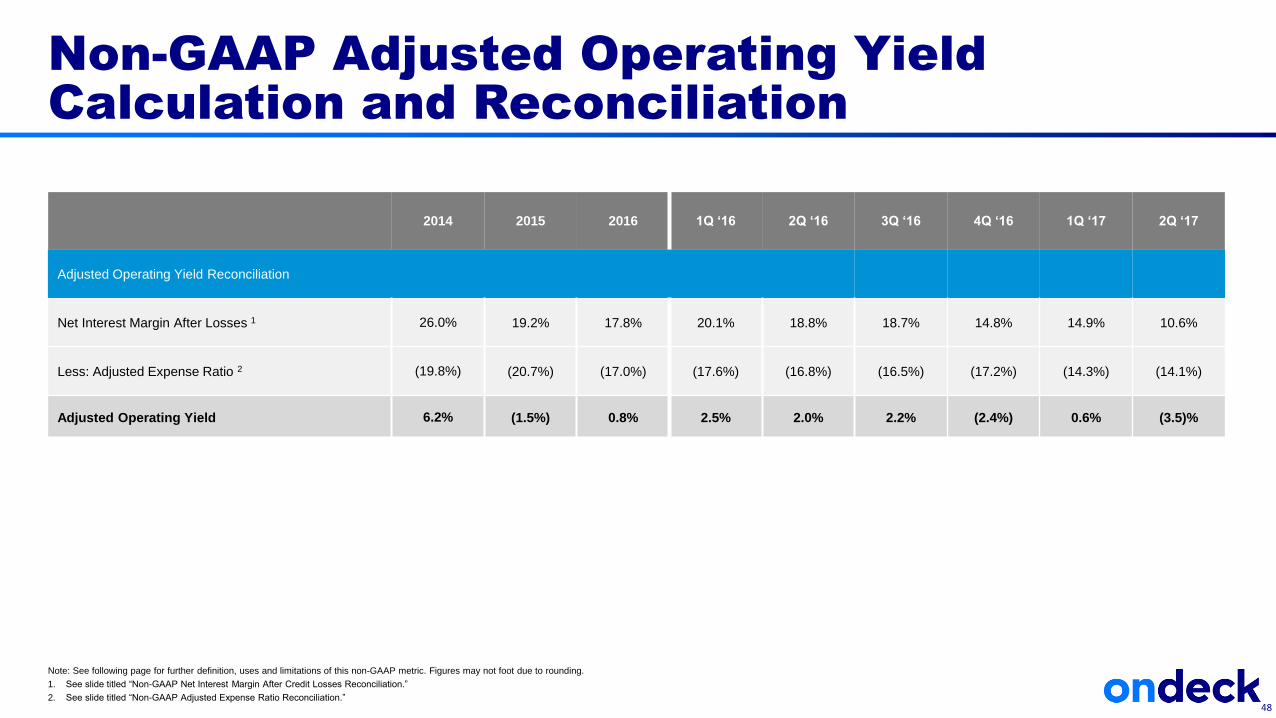

2014 2015 2016 1Q ‘16 2Q ‘16 3Q ‘16 4Q ‘16 1Q ‘17 2Q ‘17

Adjusted Operating Yield Reconciliation

Net Interest Margin After Losses 1 26.0% 19.2% 17.8% 20.1% 18.8% 18.7% 14.8% 14.9% 10.6%

Less: Adjusted Expense Ratio 2 (19.8%) (20.7%) (17.0%) (17.6%) (16.8%) (16.5%) (17.2%) (14.3%) (14.1%)

Adjusted Operating Yield 6.2% (1.5%) 0.8% 2.5% 2.0% 2.2% (2.4%) 0.6% (3.5)%

Non-GAAP Adjusted Operating Yield

Calculation and Reconciliation

Note: See following page for further definition, uses and limitations of this non-GAAP metric. Figures may not foot due to rounding.

1. See slide titled “Non-GAAP Net Interest Margin After Credit Losses Reconciliation.”

2. See slide titled “Non-GAAP Adjusted Expense Ratio Reconciliation.”48

Adjusted Operating Yield represents our Net Interest Margin After Credit Losses less the Adjusted Expense Ratio.

Management believes that using Adjusted Operating Yield is a useful tool to evaluate the operating performance of the business unaffected by

the growth in originations and regardless of funding strategy. With respect to the forward-looking guidance of this metric, OnDeck is not able to

provide a reconciliation of this non-GAAP measure to GAAP. Certain items that impact these measures have not yet occurred, are out of

OnDeck’s control and/or cannot be reasonably predicted, and as a result, reconciliation of the forward-looking non-GAAP guidance measures

to GAAP is not available without unreasonable effort.

Our use of Adjusted Operating Yield has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for

analysis of our results as reported under GAAP. Some of these limitations are:

• Net Interest Margin After Credit Losses uses Average Interest Earning Assets in the denominator of the calculation whereas Adjusted

Expense Ratio uses Average Loans Under Management in the denominator. Subtracting one metric from the other is purely illustrative and

does not reflect the operating performance of the business.

• Using Adjusted Operating Yield as a measure to compare Net Interest Margin After Credit Losses to Adjusted Expense Ratio assumes that

loans sold through the OnDeck Marketplace are of similar origination, performance characteristics and return as loans held for investment

and held for sale, which are funded on-balance sheet through our asset-backed revolving facilities, asset-backed securitization facilities,

and internal equity.

• Using Net Interest Margin After Credit Losses as a measure to compare against Adjusted Expense Ratio assumes that the rate of return of

loans funded through the OnDeck Marketplace is similar to that of our loans held for investment or held for sale. Should our Marketplace

Gain on Sale Rates materially differ, both positively or negatively, this may limit the utility of comparing Net Interest Margin After Credit

Losses to Adjusted Expense Ratio as a means of measuring the operations of the business.

Adjusted Operating Yield

49

![Investor Presentations2.q4cdn.com/.../[FINAL]-September-Investor-Presentation.pdf2 These materials and the accompanying oral presentation contain “forward-looking statements”within](https://static.documents.pub/doc/80x56/5ffa2febc342c265233a1664/investor-presentations2q4cdncomfinal-september-investor-2-these-materials.jpg)