80

INVESTOR RELATIONS FACTBOOK February 2017 © 2017 Software AG. All rights reserved.

INVESTOR RELATIONS FACTBOOK

February 2017

© 2017 Software AG. All rights reserved.

2 |

This presentation includes forward-looking statements based on the beliefs of Software AG management.

Such statements reflect current views of Software AG with respect to future events

and results and are subject to risks and uncertainties. Actual results may vary materially from those

projected here, due to factors including changes in general economic and business conditions, changes in

currency exchange, the introduction of competing products, lack of market acceptance

of new products, services or technologies and changes in business strategy. Software AG does not intend

or assume any obligation to update these forward-looking statements.

This presentation constitutes neither an offer nor recommendation to subscribe or buy in any other way

securities of Software AG or any of the companies that are members of the Group at present or in the

future, nor does it form part of such an offer and it should not be understood as such. This presentation

does not constitute an offer of sale of securities in the United States of America. Securities may not be

offered or sold in the United States of America without registration or exemption from registration in

accordance with the U.S. Securities‘ Act of 1933 in its currently valid form.

The Gartner Report(s) described herein, (the "Gartner Report(s)") represent(s) research opinion or viewpoints published, as part of a syndicated

subscription service, by Gartner, Inc. ("Gartner"), and are not representations of fact. Each Gartner Report speaks as of its original publication date

(and not as of the date of this Prospectus) and the opinions expressed in the Gartner Report(s) are subject to change without notice.

© 2017 Software AG. All rights reserved.

SAFE-HARBOR-STATEMENT

3 |

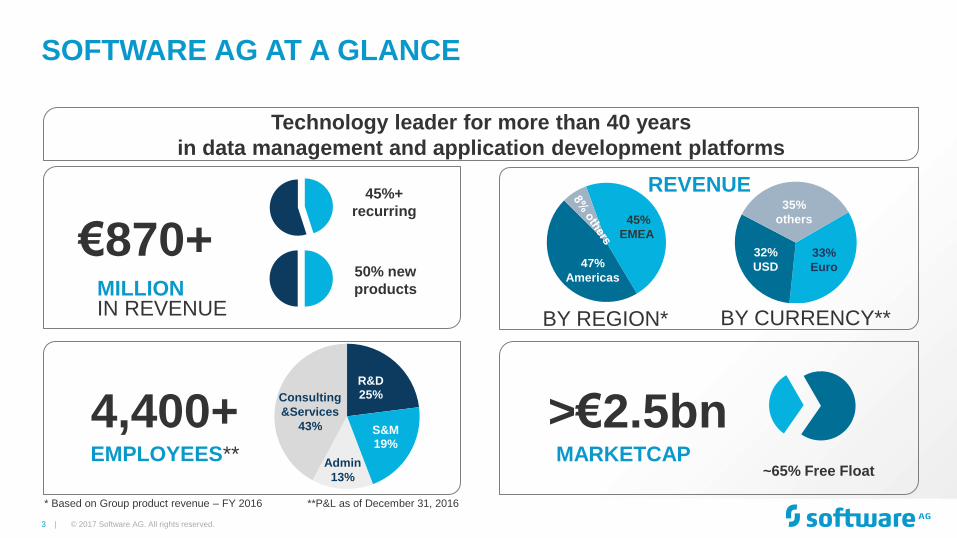

SOFTWARE AG AT A GLANCE

Technology leader for more than 40 years

in data management and application development platforms

>€2.5bn MARKETCAP

~65% Free Float

€870+ MILLION IN REVENUE

45%+

recurring

50% new

products

4,400+ EMPLOYEES**

R&D 25%

S&M 19%

Consulting

&Services

43%

Admin

13%

© 2017 Software AG. All rights reserved.

47%

Americas

45%

EMEA

REVENUE

33%

Euro

32%

USD

35%

others

BY REGION* BY CURRENCY**

* Based on Group product revenue – FY 2016 **P&L as of December 31, 2016

4 | © 2017 Software AG. All rights reserved.

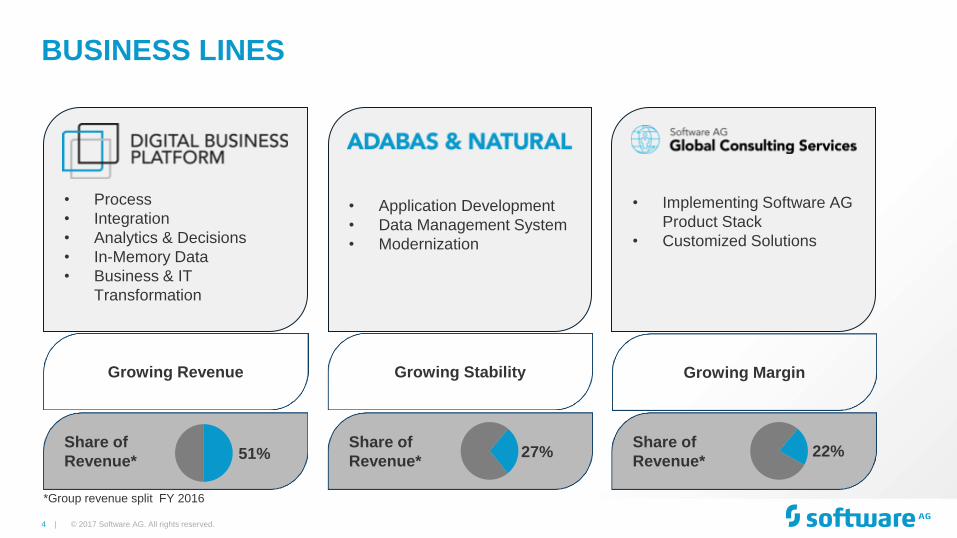

BUSINESS LINES

• Implementing Software AG

Product Stack

• Customized Solutions

• Application Development

• Data Management System

• Modernization

• Process

• Integration

• Analytics & Decisions

• In-Memory Data

• Business & IT

Transformation

Share of

Revenue*

Share of

Revenue*

Share of

Revenue* 51% 27% 22%

*Group revenue split FY 2016

Growing Stability Growing Revenue Growing Margin

5 |

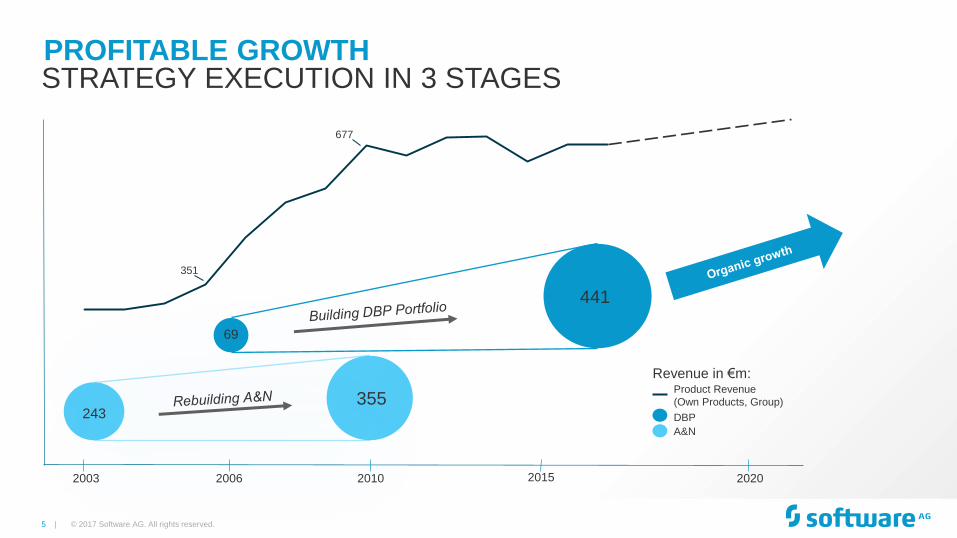

PROFITABLE GROWTH

© 2017 Software AG. All rights reserved.

STRATEGY EXECUTION IN 3 STAGES

243 355

441

2003 2010 2006 2015 2020

Revenue in €m: Product Revenue

(Own Products, Group)

DBP

A&N

69

677

351

6 |

INDEX

© 2017 Software AG. All rights reserved.

Key Investment Indicators 1. 7

Business Model, Characteristics & GTM 2. 21

Markets, Positioning & Competition 3. 28

Digital Business Platform - Core Capabilities 4. 37

Customers References & Use Cases 5. 44

Financials 6. 57

Shares & Ownership 7. 73

7 |

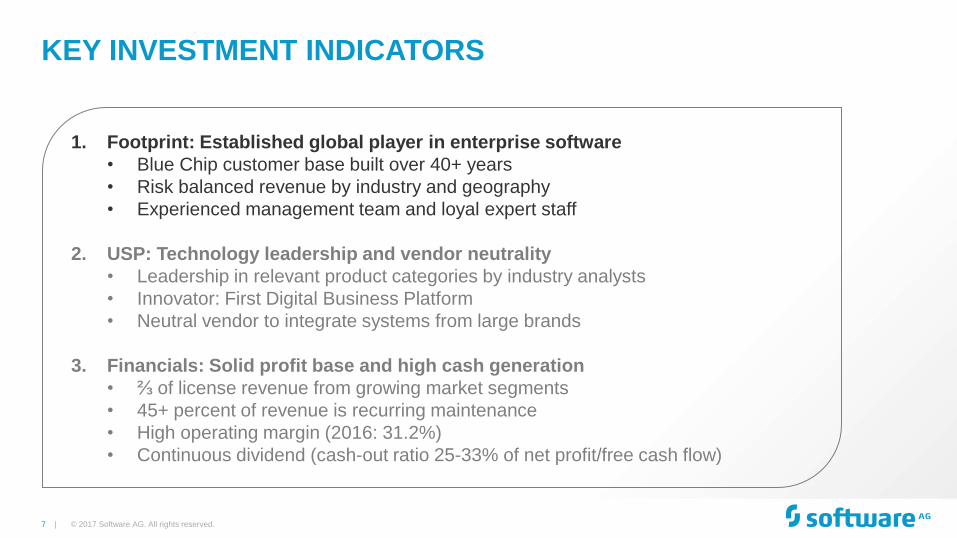

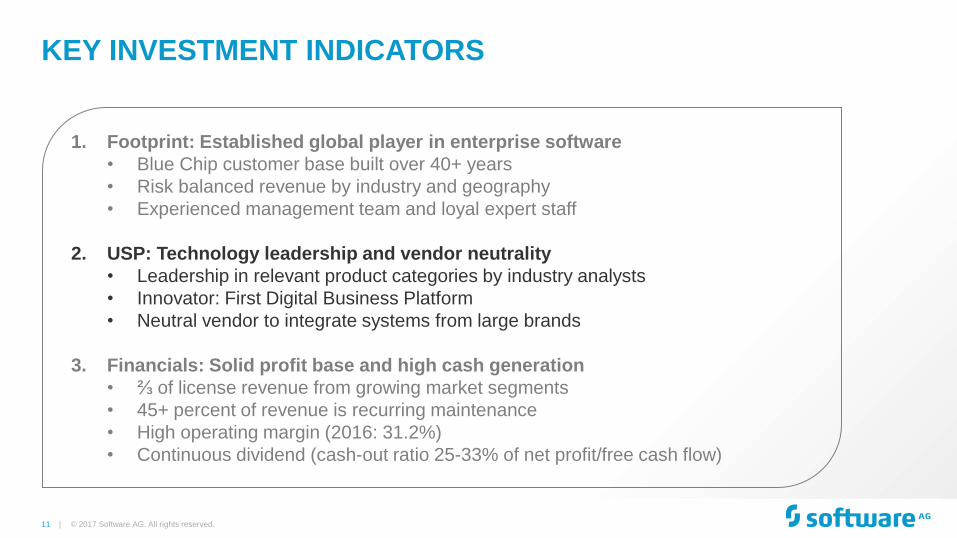

KEY INVESTMENT INDICATORS

© 2017 Software AG. All rights reserved.

1. Footprint: Established global player in enterprise software

• Blue Chip customer base built over 40+ years

• Risk balanced revenue by industry and geography

• Experienced management team and loyal expert staff

2. USP: Technology leadership and vendor neutrality

• Leadership in relevant product categories by industry analysts

• Innovator: First Digital Business Platform

• Neutral vendor to integrate systems from large brands

3. Financials: Solid profit base and high cash generation

• ⅔ of license revenue from growing market segments

• 45+ percent of revenue is recurring maintenance

• High operating margin (2016: 31.2%)

• Continuous dividend (cash-out ratio 25-33% of net profit/free cash flow)

8 |

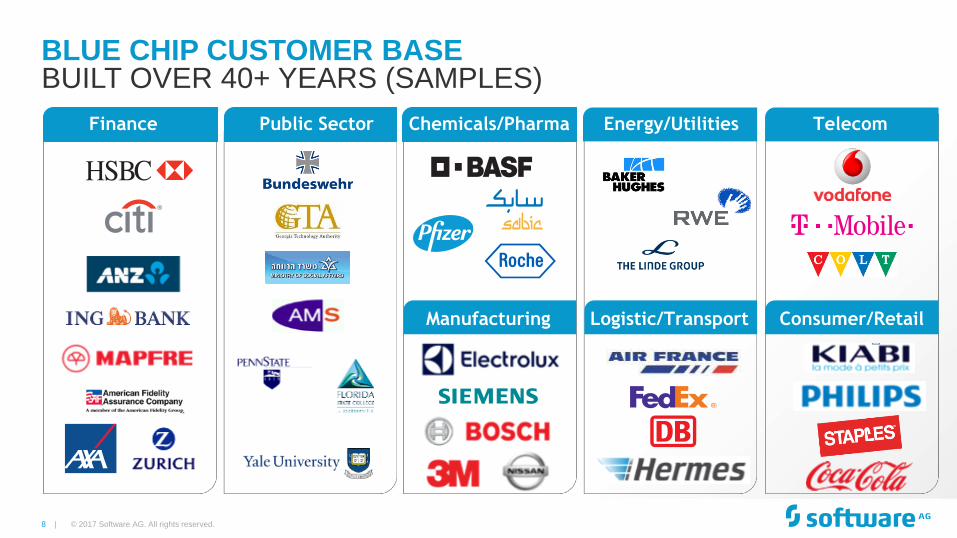

Public Sector Telecom Chemicals/Pharma Energy/Utilities

Manufacturing Logistic/Transport Consumer/Retail

Finance

BLUE CHIP CUSTOMER BASE BUILT OVER 40+ YEARS (SAMPLES)

© 2017 Software AG. All rights reserved.

9 |

20%

19%

18%

12%

10%

Government Financial Services

IT Services Manufacturing

Services Telco & Media

Transport & Logistics Other

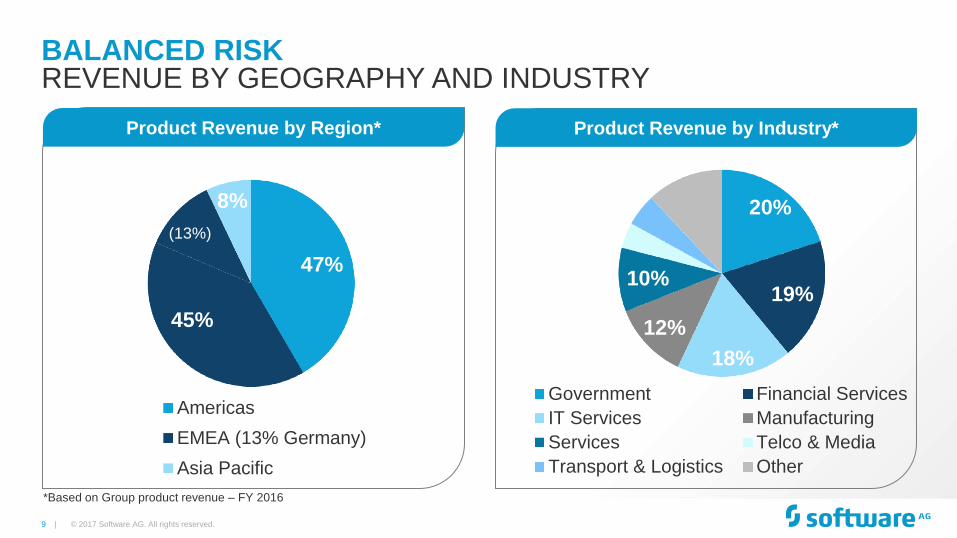

BALANCED RISK

© 2017 Software AG. All rights reserved.

REVENUE BY GEOGRAPHY AND INDUSTRY

Product Revenue by Region* Product Revenue by Industry*

47%

45%

(13%)

8%

Americas

EMEA (13% Germany)

Asia Pacific

*Based on Group product revenue – FY 2016

10 |

EXPERIENCED MANAGEMENT TEAM AND LOYAL EXPERT STAFF

Karl-Heinz Streibich Eric Duffaut Dr. Wolfram Jost Arnd Zinnhardt Chief Executive Officer

- since 2003 -

Chief Customer Officer

- since 2014 -

Chief Technology Officer

- since 2010 -

Chief Financial Officer

- since 2002 -

Human Resources, Legal,

Information Services (IT),

Corporate Communications,

Processes, Audits & Quality,

Corporate Office

Sales, Marketing, Partner

Ecosystem, Global

Consulting Services &

Support

Research & Development,

Product Management,

Product Marketing, Industry

Analyst Relations

Finance, Controlling,

Taxes, Treasury,

Business Operations,

Mergers & Acquisitions,

Investor Relations,

Global Purchasing

© 2017 Software AG. All rights reserved.

11 |

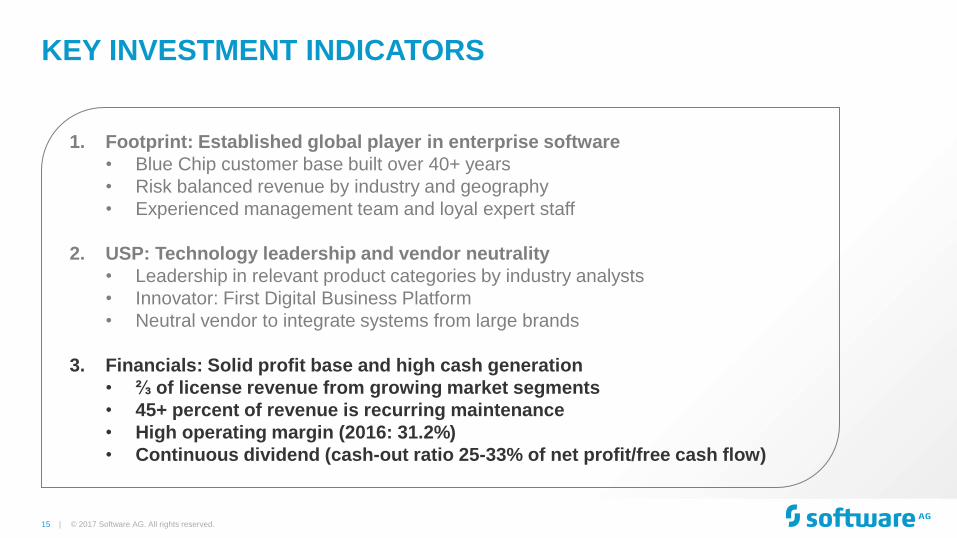

KEY INVESTMENT INDICATORS

1. Footprint: Established global player in enterprise software

• Blue Chip customer base built over 40+ years

• Risk balanced revenue by industry and geography

• Experienced management team and loyal expert staff

2. USP: Technology leadership and vendor neutrality

• Leadership in relevant product categories by industry analysts

• Innovator: First Digital Business Platform

• Neutral vendor to integrate systems from large brands

3. Financials: Solid profit base and high cash generation

• ⅔ of license revenue from growing market segments

• 45+ percent of revenue is recurring maintenance

• High operating margin (2016: 31.2%)

• Continuous dividend (cash-out ratio 25-33% of net profit/free cash flow)

© 2017 Software AG. All rights reserved.

12 |

TECHNOLOGY LEADERSHIP

© 2017 Software AG. All rights reserved.

SOFTWARE AG SUITE IS A LEADER IN 6 MARKETS

The Gartner Report(s) described herein, (the "Gartner Report(s)") represent(s) research opinion or viewpoints published, as

part of a syndicated subscription service, by Gartner, Inc. ("Gartner"), and are not representations of fact. Each Gartner Report

speaks as of its original publication date (and not as of the date of this Prospectus) and the opinions expressed in the

Gartner Report(s) are subject to change without notice.

To access the Analyst research reports, please follow the hyperlink.

The Forrester Wave™: In-Memory Data Grids,

Q3 2015

The Forrester Wave™: Hybrid Integration For

Enterprises, Q4 2016

The Forrester Wave™: Enterprise

Architecture Management Suites, Q3 2015

The Forrester Wave™: Big Data Streaming

Analytics, Q1 2016 Enterprise Architecture Tools

Integrated IT Portfolio Analysis Application

13 |

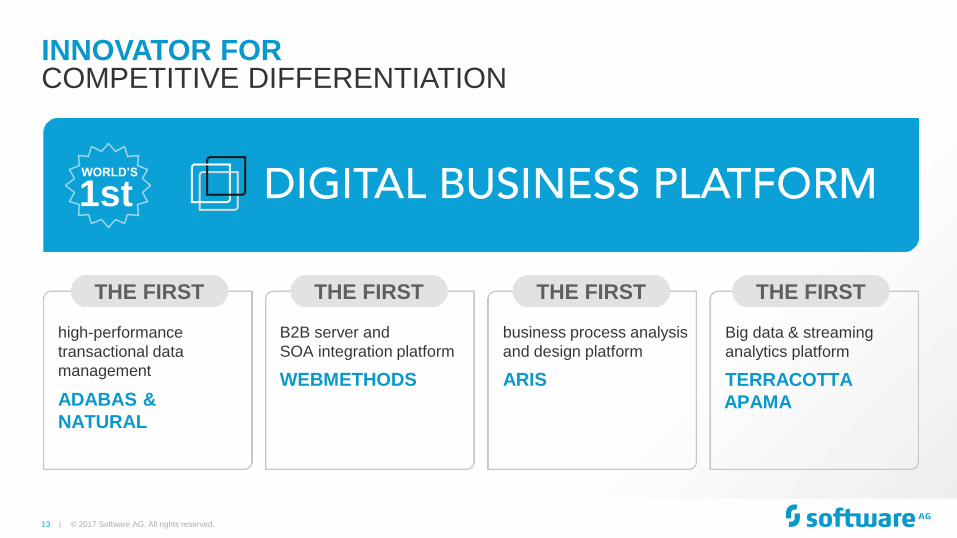

INNOVATOR FOR

© 2017 Software AG. All rights reserved.

COMPETITIVE DIFFERENTIATION

WORLD’S

1st

high-performance

transactional data

management

ADABAS &

NATURAL

B2B server and

SOA integration platform

WEBMETHODS

business process analysis

and design platform

ARIS

Big data & streaming

analytics platform

TERRACOTTA

APAMA

THE FIRST THE FIRST THE FIRST THE FIRST

14 | © 2017 Software AG. All rights reserved.

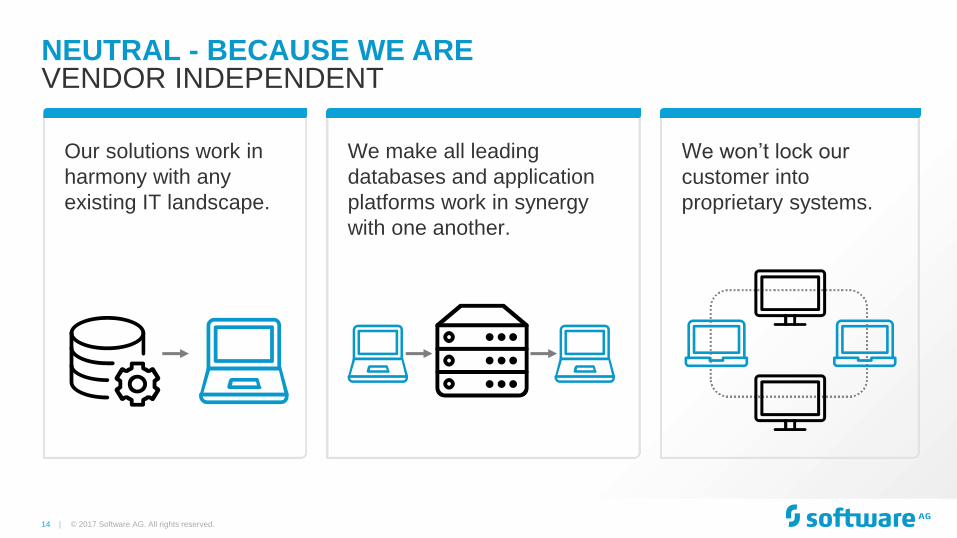

Our solutions work in

harmony with any

existing IT landscape.

We make all leading

databases and application

platforms work in synergy

with one another.

We won’t lock our

customer into

proprietary systems.

NEUTRAL - BECAUSE WE ARE VENDOR INDEPENDENT

15 |

KEY INVESTMENT INDICATORS

© 2017 Software AG. All rights reserved.

1. Footprint: Established global player in enterprise software

• Blue Chip customer base built over 40+ years

• Risk balanced revenue by industry and geography

• Experienced management team and loyal expert staff

2. USP: Technology leadership and vendor neutrality

• Leadership in relevant product categories by industry analysts

• Innovator: First Digital Business Platform

• Neutral vendor to integrate systems from large brands

3. Financials: Solid profit base and high cash generation

• ⅔ of license revenue from growing market segments

• 45+ percent of revenue is recurring maintenance

• High operating margin (2016: 31.2%)

• Continuous dividend (cash-out ratio 25-33% of net profit/free cash flow)

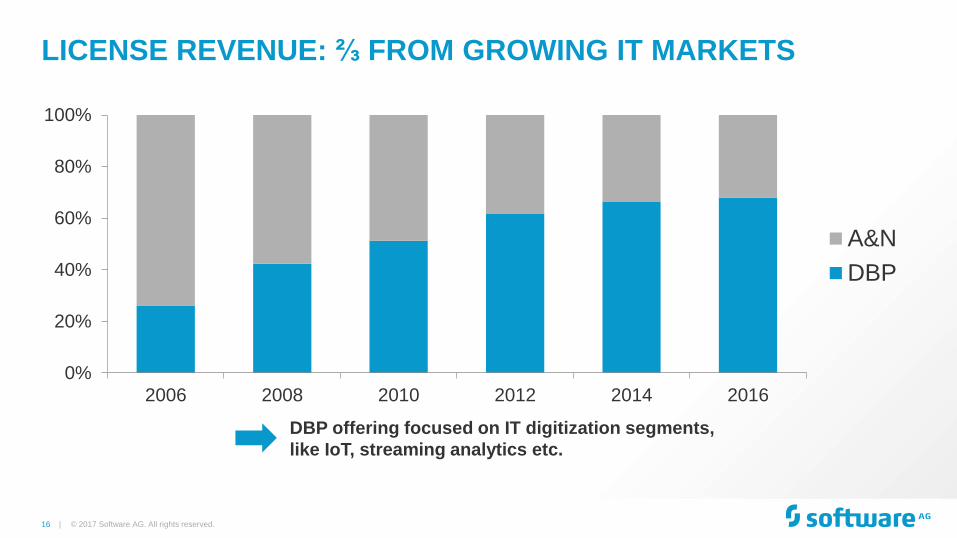

16 |

LICENSE REVENUE: ⅔ FROM GROWING IT MARKETS

© 2017 Software AG. All rights reserved.

0%

20%

40%

60%

80%

100%

2006 2008 2010 2012 2014 2016

A&N

DBP

DBP offering focused on IT digitization segments,

like IoT, streaming analytics etc.

17 |

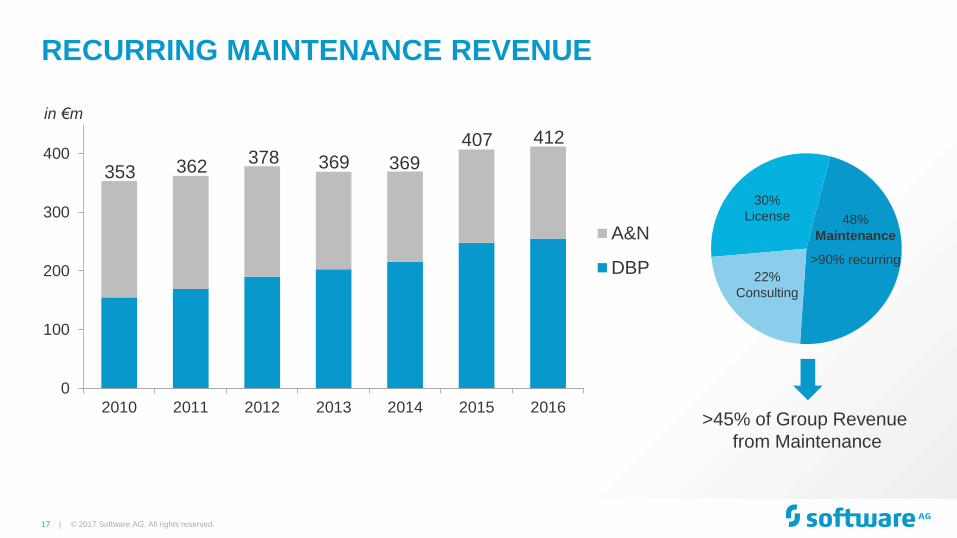

RECURRING MAINTENANCE REVENUE

© 2017 Software AG. All rights reserved.

0

100

200

300

400

2010 2011 2012 2013 2014 2015 2016

A&N

DBP

353 362 378 369 369

407

>45% of Group Revenue

from Maintenance

in €m

48%

Maintenance

>90% recurring

30%

License

22%

Consulting

412

18 |

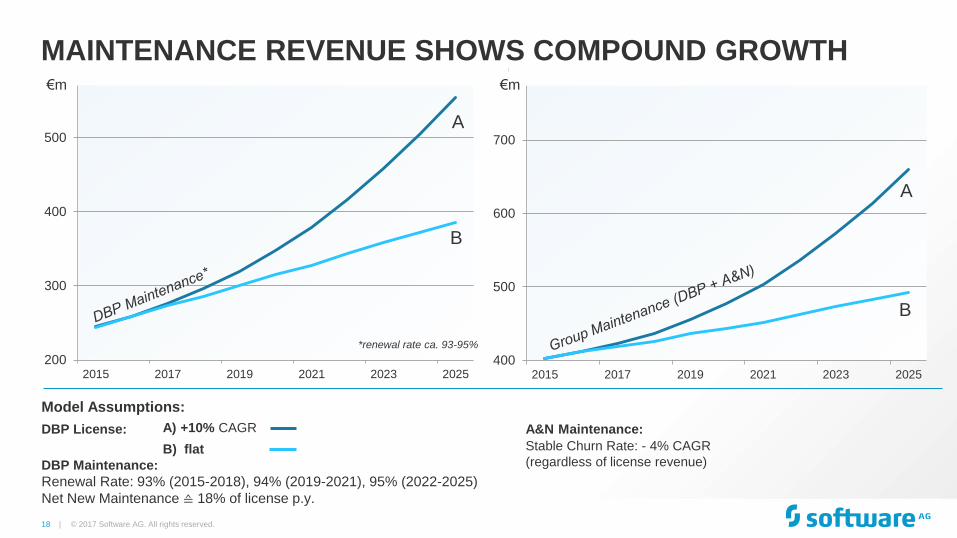

200

300

400

500

600

2015 2017 2019 2021 2023 2025

*renewal rate ca. 93-95%

400

500

600

700

800

2015 2017 2019 2021 2023 2025

© 2017 Software AG. All rights reserved.

A) +10% CAGR

B) flat

€m

€m

€m

MAINTENANCE REVENUE SHOWS COMPOUND GROWTH

DBP Maintenance:

Renewal Rate: 93% (2015-2018), 94% (2019-2021), 95% (2022-2025)

Net New Maintenance ≙ 18% of license p.y.

Stable Churn Rate: - 4% CAGR

(regardless of license revenue)

DBP License:

A

A

B

B

Model Assumptions:

A&N Maintenance:

19 |

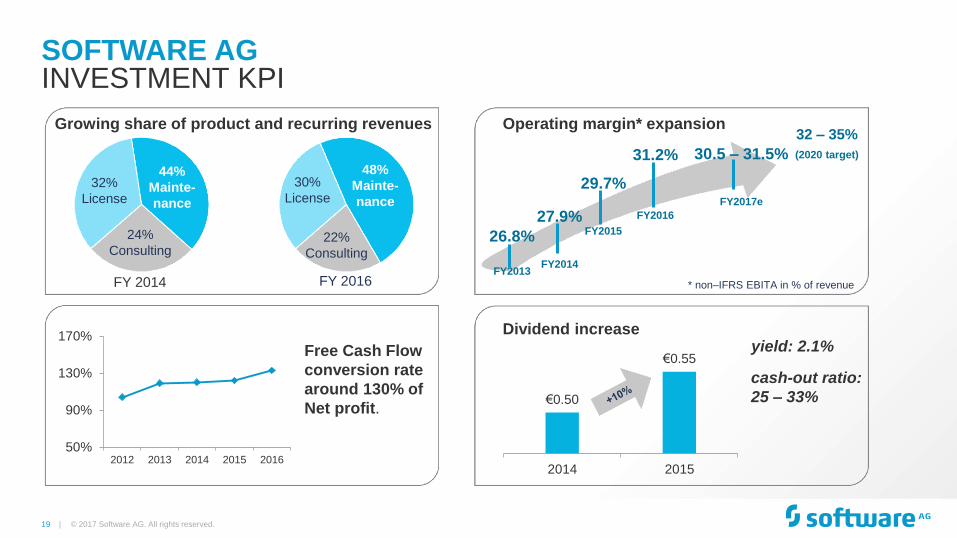

31.2%

FY2016

29.7%

FY2015 26.8%

FY2013

27.9%

FY2014

SOFTWARE AG INVESTMENT KPI

44%

Mainte-

nance

32%

License

24%

Consulting

Growing share of product and recurring revenues

€0.50

€0.55

2014 2015

Dividend increase

Free Cash Flow

conversion rate

around 130% of

Net profit.

50%

90%

130%

170%

2012 2013 2014 2015 2016

yield: 2.1%

Operating margin* expansion

FY 2014 * non–IFRS EBITA in % of revenue FY 2016

48%

Mainte-

nance

30%

License

22%

Consulting

© 2017 Software AG. All rights reserved.

32 – 35%

(2020 target)

cash-out ratio:

25 – 33%

30.5 – 31.5%

FY2017e

20 |

INDEX

© 2017 Software AG. All rights reserved.

Key Value Investment Indicators 1. 7

Business Model, Characteristics & GTM 2. 21

Markets, Positioning & Competition 3. 28

Digital Business Platform - Core Capabilities 4. 37

Customers References & Use Cases 5. 44

Financials 6. 57

Shares & Ownership 7. 73

21 |

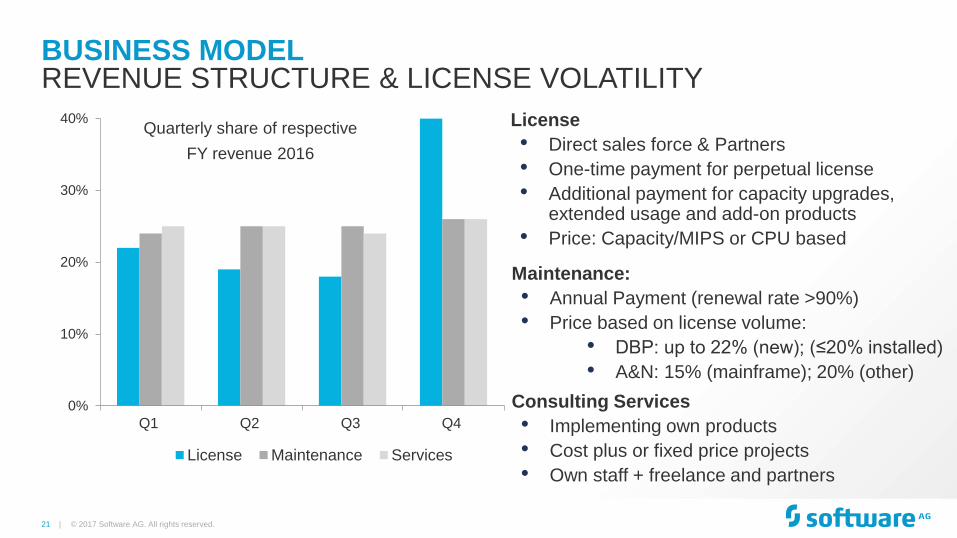

BUSINESS MODEL

© 2017 Software AG. All rights reserved.

REVENUE STRUCTURE & LICENSE VOLATILITY

License

• Direct sales force & Partners

• One-time payment for perpetual license

• Additional payment for capacity upgrades, extended usage and add-on products

• Price: Capacity/MIPS or CPU based

Maintenance:

• Annual Payment (renewal rate >90%)

• Price based on license volume:

• DBP: up to 22% (new); (≤20% installed)

• A&N: 15% (mainframe); 20% (other)

Consulting Services

• Implementing own products

• Cost plus or fixed price projects

• Own staff + freelance and partners

0%

10%

20%

30%

40%

Q1 Q2 Q3 Q4

License Maintenance Services

Quarterly share of respective

FY revenue 2016

22 |

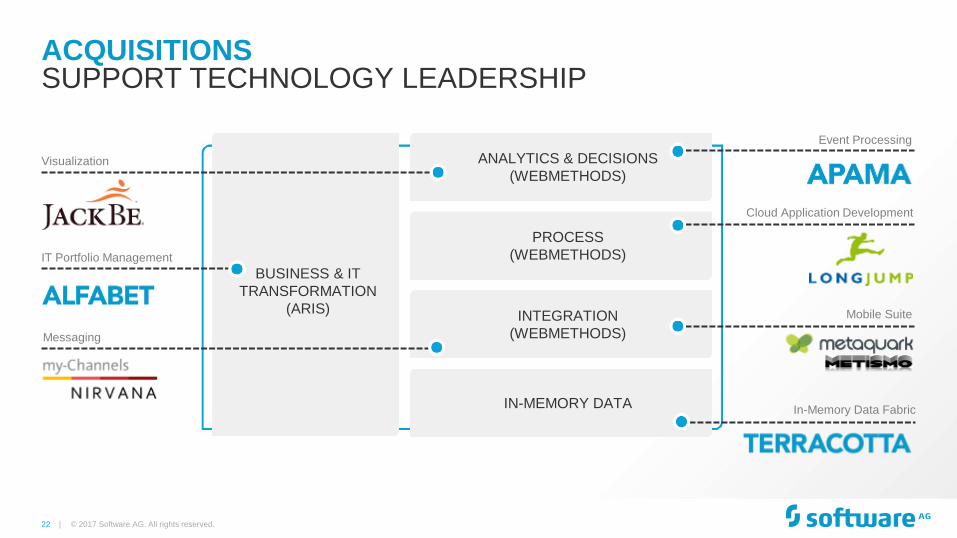

ACQUISITIONS

© 2017 Software AG. All rights reserved.

SUPPORT TECHNOLOGY LEADERSHIP

BUSINESS & IT

TRANSFORMATION

(ARIS)

ANALYTICS & DECISIONS

(WEBMETHODS)

PROCESS

(WEBMETHODS)

INTEGRATION

(WEBMETHODS)

IN-MEMORY DATA

Event Processing

IT Portfolio Management

Visualization

Cloud Application Development

Messaging

Mobile Suite

In-Memory Data Fabric

23 |

PARTNER SOLUTIONS DIGITAL MARKETPLACE - A CREDIBLE INDUSTRY ECOSYSTEM

MEDIA BACKBONE

CONDUCTOR

SCHEER BPAAS

ARIS MOBILE SERVICES

INTRADAY LIQUIDITY

MONITORING

CONNECTED SERVICE

EXPERIENCE

ACCORD ALFABET

ACCELERATOR

CONTINUOUS

ASSURANCE

WIPRO LOOKING

GLASS

GLOBAL OPERATIONS

SOLUTIONS

SMART WORK BENCH

AUTOMATED TEST

ENGINE

PREDICTIVE

MAINTENANCE

SERVICE

INTEGRATION SUITE

© 2017 Software AG. All rights reserved.

24 |

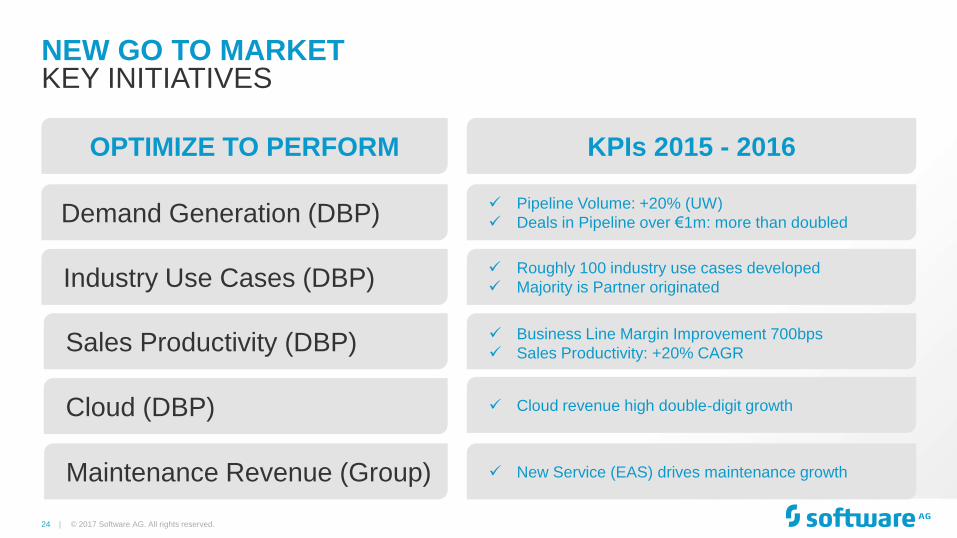

NEW GO TO MARKET KEY INITIATIVES

Pipeline Volume: +20% (UW)

Deals in Pipeline over €1m: more than doubled

New Service (EAS) drives maintenance growth

KPIs 2015 - 2016

Demand Generation (DBP)

Industry Use Cases (DBP)

Maintenance Revenue (Group)

Sales Productivity (DBP)

OPTIMIZE TO PERFORM

© 2017 Software AG. All rights reserved.

Cloud (DBP)

Business Line Margin Improvement 700bps

Sales Productivity: +20% CAGR

Cloud revenue high double-digit growth

Roughly 100 industry use cases developed

Majority is Partner originated

25 |

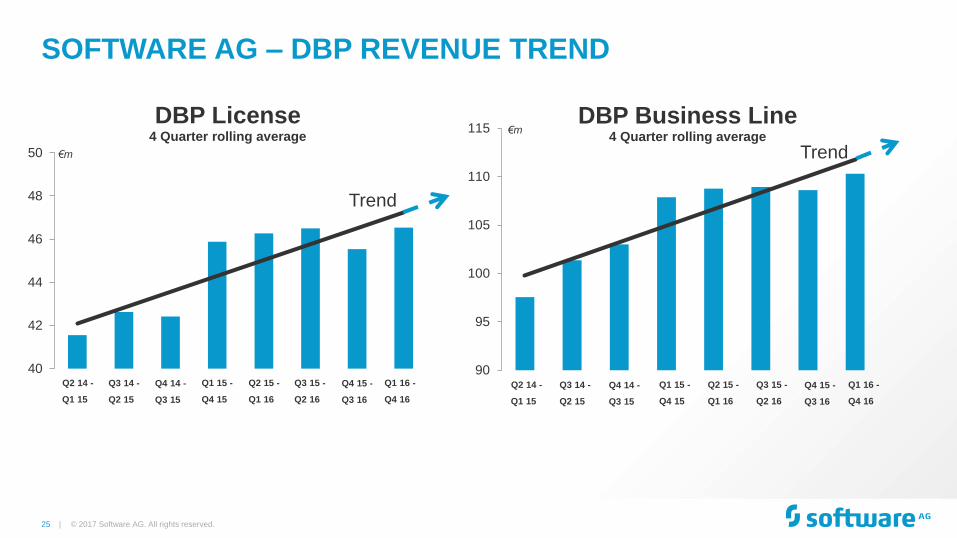

90

95

100

105

110

115DBP Business Line

4 Quarter rolling average

SOFTWARE AG – DBP REVENUE TREND

© 2017 Software AG. All rights reserved.

€m

40

42

44

46

48

50

DBP License 4 Quarter rolling average

Trend

€m

Q2 14 -

Q1 15

Q3 14 -

Q2 15

Q4 14 -

Q3 15

Q1 15 -

Q4 15

Q2 15 -

Q1 16

Q3 15 -

Q2 16

Q4 15 -

Q3 16

Q1 16 -

Q4 16

Trend

Q2 14 -

Q1 15

Q3 14 -

Q2 15

Q4 14 -

Q3 15

Q1 15 -

Q4 15

Q2 15 -

Q1 16

Q3 15 -

Q2 16

Q4 15 -

Q3 16

Q1 16 -

Q4 16

26 |

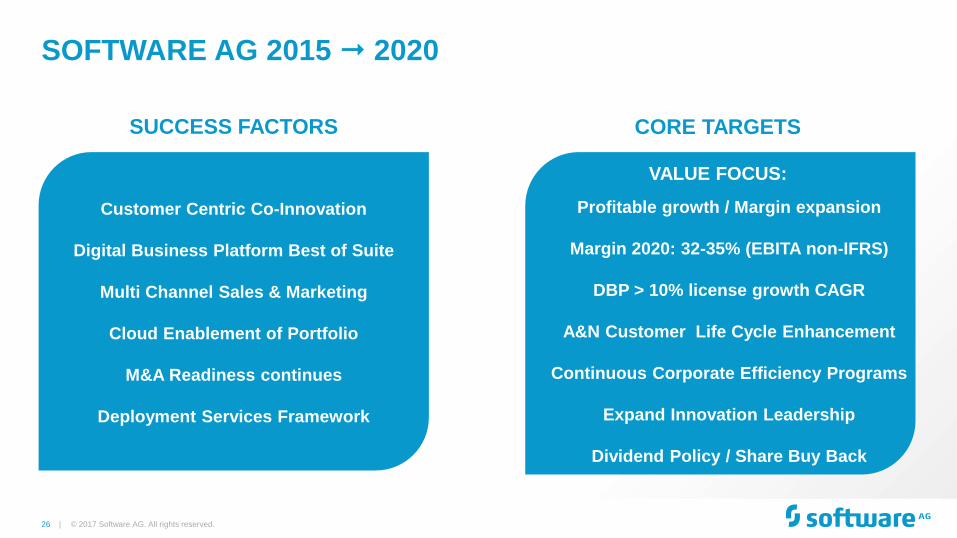

SOFTWARE AG 2015 2020

© 2017 Software AG. All rights reserved.

SUCCESS FACTORS

Customer Centric Co-Innovation

Digital Business Platform Best of Suite

Multi Channel Sales & Marketing

Cloud Enablement of Portfolio

M&A Readiness continues

Deployment Services Framework

CORE TARGETS

Profitable growth / Margin expansion

Margin 2020: 32-35% (EBITA non-IFRS)

DBP > 10% license growth CAGR

A&N Customer Life Cycle Enhancement

Continuous Corporate Efficiency Programs

Expand Innovation Leadership

Dividend Policy / Share Buy Back

VALUE FOCUS:

27 |

INDEX

© 2017 Software AG. All rights reserved.

Key Value Investment Indicators 1. 7

Business Model, Characteristics & GTM 2. 21

Markets, Positioning & Competition 3. 28

Digital Business Platform - Core Capabilities 4. 37

Customers References & Use Cases 5. 44

Financials 6. 57

Shares & Ownership 7. 73

28 |

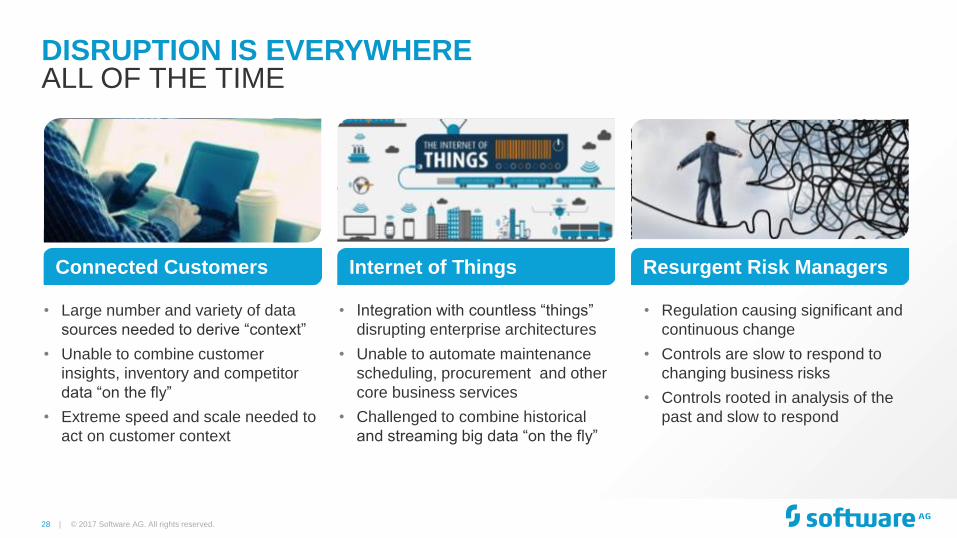

DISRUPTION IS EVERYWHERE ALL OF THE TIME

Resurgent Risk Managers Connected Customers Internet of Things

• Regulation causing significant and

continuous change

• Controls are slow to respond to

changing business risks

• Controls rooted in analysis of the

past and slow to respond

• Large number and variety of data

sources needed to derive “context”

• Unable to combine customer

insights, inventory and competitor

data “on the fly”

• Extreme speed and scale needed to

act on customer context

• Integration with countless “things”

disrupting enterprise architectures

• Unable to automate maintenance

scheduling, procurement and other

core business services

• Challenged to combine historical

and streaming big data “on the fly”

© 2017 Software AG. All rights reserved.

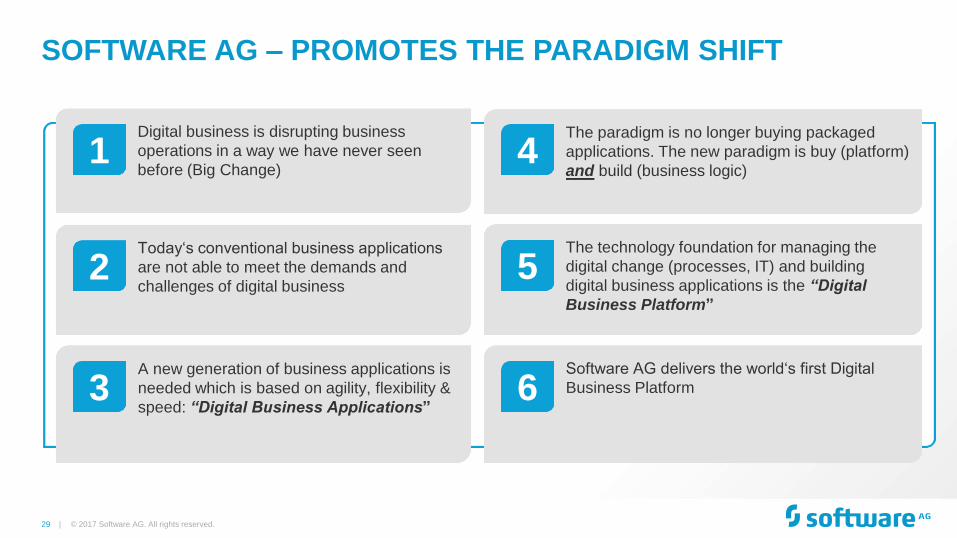

29 | © 2017 Software AG. All rights reserved.

Digital business is disrupting business

operations in a way we have never seen

before (Big Change)

1

Today‘s conventional business applications

are not able to meet the demands and

challenges of digital business 2

A new generation of business applications is

needed which is based on agility, flexibility &

speed: “Digital Business Applications”

3

The technology foundation for managing the

digital change (processes, IT) and building

digital business applications is the “Digital

Business Platform”

5

The paradigm is no longer buying packaged

applications. The new paradigm is buy (platform)

and build (business logic) 4

Software AG delivers the world‘s first Digital

Business Platform 6

SOFTWARE AG – PROMOTES THE PARADIGM SHIFT

30 |

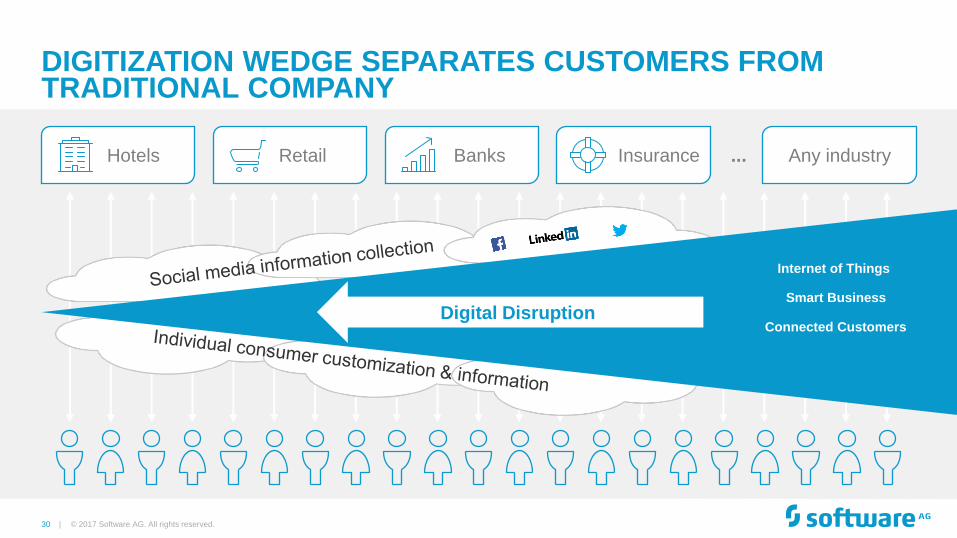

DIGITIZATION WEDGE SEPARATES CUSTOMERS FROM TRADITIONAL COMPANY

DIGITAL DISRUPTION

Any industry ... Retail Hotels Banks Insurance

© 2017 Software AG. All rights reserved.

Digital Disruption

Internet of Things

Smart Business

Connected Customers

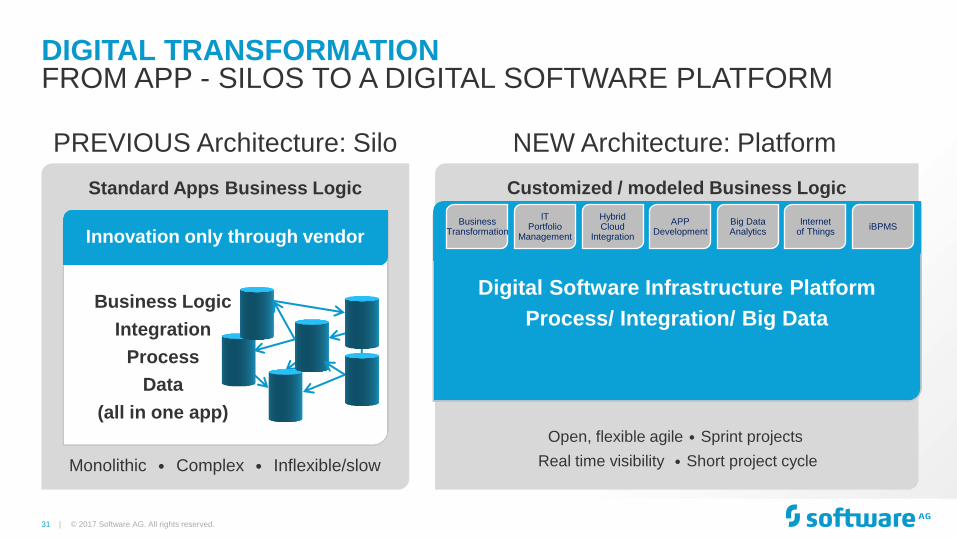

31 |

Customized / modeled Business Logic Standard Apps Business Logic

DIGITAL TRANSFORMATION

Innovation only through vendor

Open, flexible agile • Sprint projects

Real time visibility • Short project cycle

PREVIOUS Architecture: Silo NEW Architecture: Platform

Monolithic • Complex • Inflexible/slow

Business Logic

Integration

Process

Data

(all in one app)

FROM APP - SILOS TO A DIGITAL SOFTWARE PLATFORM

Business Transformation

IT Portfolio

Management

Hybrid Cloud

Integration

APP Development

Big Data Analytics

Internet of Things

iBPMS

Digital Software Infrastructure Platform

Process/ Integration/ Big Data

© 2017 Software AG. All rights reserved.

32 |

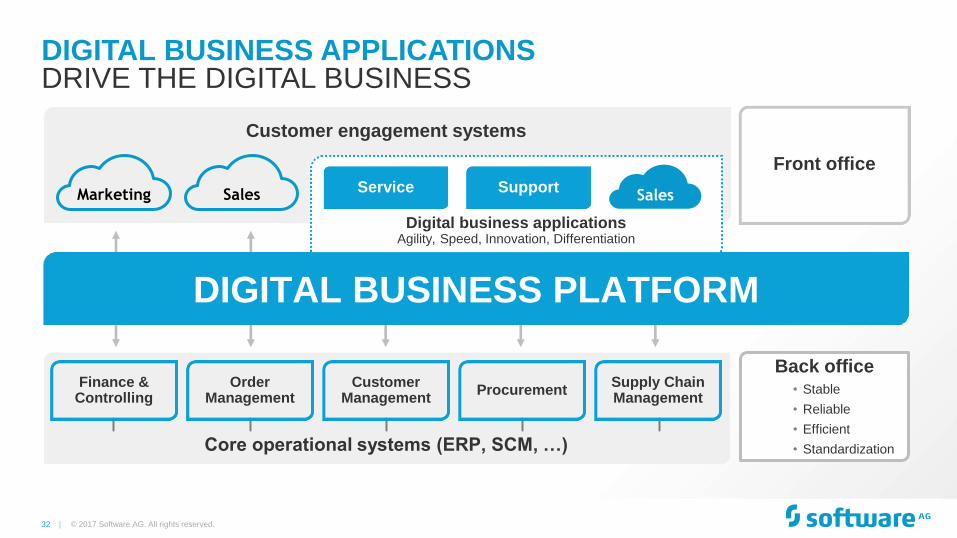

Front office

Customer engagement systems

DIGITAL BUSINESS PLATFORM

Core operational systems (ERP, SCM, …)

Finance & Controlling

Order Management

Customer Management

Procurement Supply Chain Management

Digital business applications Agility, Speed, Innovation, Differentiation

Sales Service Support

DIGITAL BUSINESS PLATFORM

Marketing

Sales

Back office • Stable

• Reliable

• Efficient

• Standardization

DIGITAL BUSINESS APPLICATIONS

© 2017 Software AG. All rights reserved.

DRIVE THE DIGITAL BUSINESS

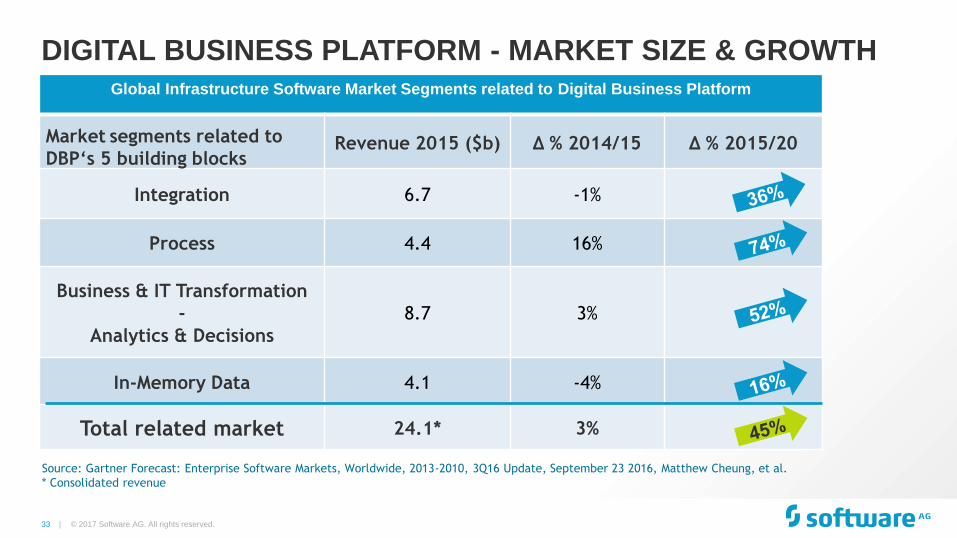

33 | © 2017 Software AG. All rights reserved.

Global Infrastructure Software Market Segments related to Digital Business Platform

Market segments related to

DBP‘s 5 building blocks Revenue 2015 ($b) Δ % 2014/15 Δ % 2015/20

Integration 6.7 -1%

Process 4.4 16%

Business & IT Transformation

-

Analytics & Decisions

8.7 3%

In-Memory Data 4.1 -4%

Total related market 24.1* 3%

Source: Gartner Forecast: Enterprise Software Markets, Worldwide, 2013-2010, 3Q16 Update, September 23 2016, Matthew Cheung, et al.

* Consolidated revenue

DIGITAL BUSINESS PLATFORM - MARKET SIZE & GROWTH

34 |

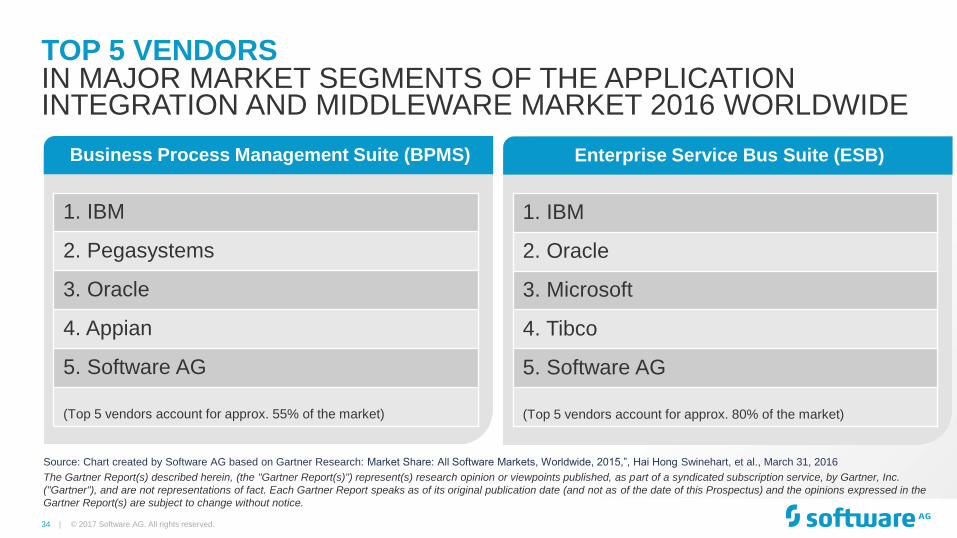

TOP 5 VENDORS

© 2017 Software AG. All rights reserved.

IN MAJOR MARKET SEGMENTS OF THE APPLICATION INTEGRATION AND MIDDLEWARE MARKET 2016 WORLDWIDE

Business Process Management Suite (BPMS)

1. IBM

2. Pegasystems

3. Oracle

4. Appian

5. Software AG

(Top 5 vendors account for approx. 55% of the market)

Enterprise Service Bus Suite (ESB)

1. IBM

2. Oracle

3. Microsoft

4. Tibco

5. Software AG

(Top 5 vendors account for approx. 80% of the market)

Source: Chart created by Software AG based on Gartner Research: Market Share: All Software Markets, Worldwide, 2015,”, Hai Hong Swinehart, et al., March 31, 2016

The Gartner Report(s) described herein, (the "Gartner Report(s)") represent(s) research opinion or viewpoints published, as part of a syndicated subscription service, by Gartner, Inc.

("Gartner"), and are not representations of fact. Each Gartner Report speaks as of its original publication date (and not as of the date of this Prospectus) and the opinions expressed in the

Gartner Report(s) are subject to change without notice.

35 |

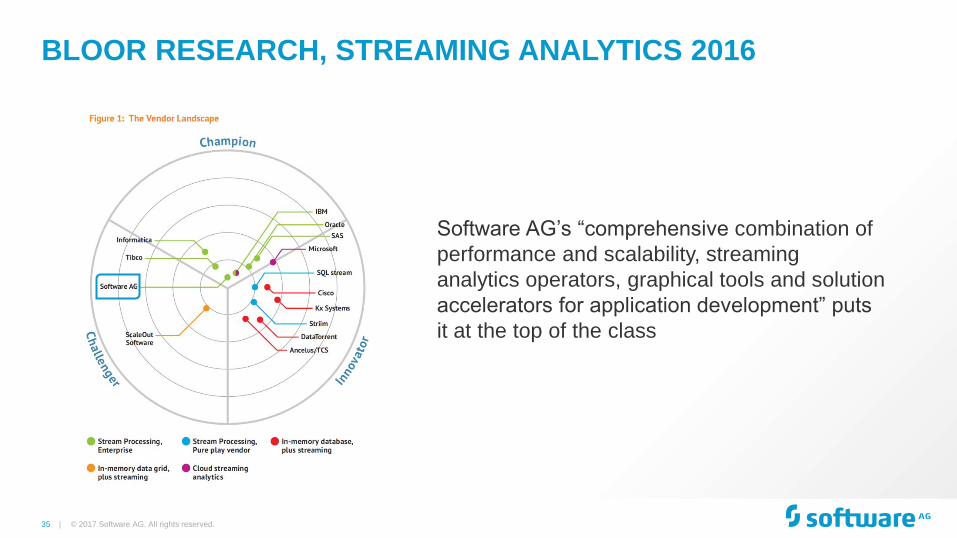

BLOOR RESEARCH, STREAMING ANALYTICS 2016

© 2017 Software AG. All rights reserved.

Software AG’s “comprehensive combination of

performance and scalability, streaming

analytics operators, graphical tools and solution

accelerators for application development” puts

it at the top of the class

36 |

INDEX

© 2017 Software AG. All rights reserved.

Key Value Investment Indicators 1. 7

Business Model, Characteristics & GTM 2. 21

Markets, Positioning & Competition 3. 28

Digital Business Platform - Core Capabilities 4. 37

Customers References & Use Cases 5. 44

Financials 6. 57

Shares & Ownership 7. 73

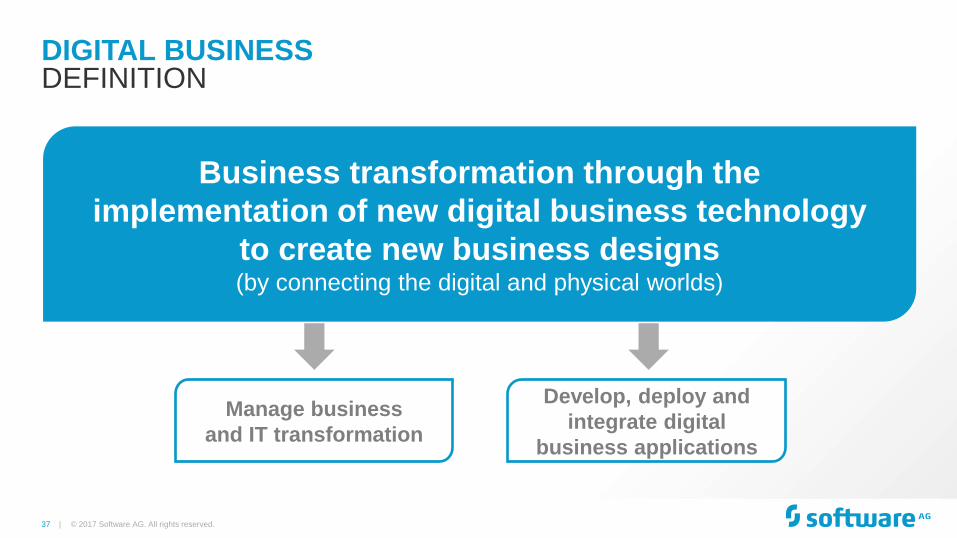

37 |

© 2017 Software AG. All rights reserved.

DIGITAL BUSINESS DEFINITION

Business transformation through the

implementation of new digital business technology

to create new business designs (by connecting the digital and physical worlds)

Manage business

and IT transformation

Develop, deploy and

integrate digital

business applications

38 |

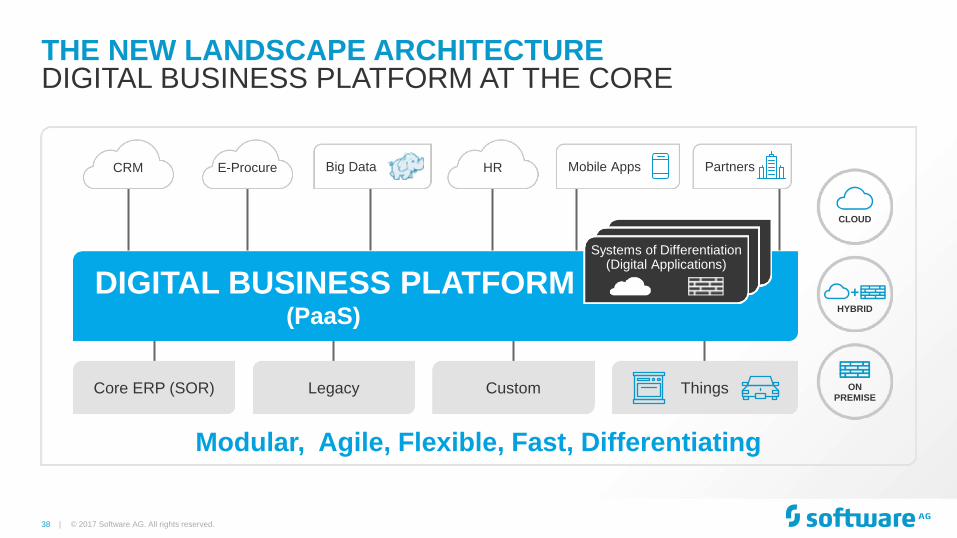

© 2017 Software AG. All rights reserved.

Core ERP (SOR) Legacy Custom Things

E-Procure CRM HR

THE NEW LANDSCAPE ARCHITECTURE DIGITAL BUSINESS PLATFORM AT THE CORE

DIGITAL BUSINESS PLATFORM (PaaS)

+ HYBRID

CLOUD

ON PREMISE

Systems of Differentiation (Digital Applications)

Big Data Mobile Apps Partners

Modular, Agile, Flexible, Fast, Differentiating

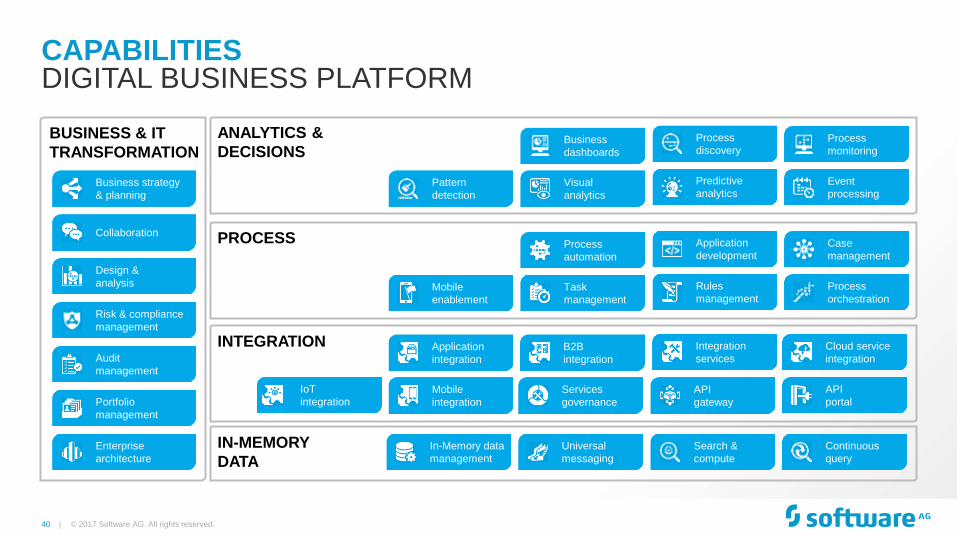

39 |

DIGITAL BUSINESS PLATFORM 5 BUILDING BLOCKS

ANALYTICS & DECISIONS

Enabling faster and better decisions

PROCESS

Combining people, business and things

INTEGRATION

Connecting multiple endpoints

IN-MEMORY DATA

Providing performance and scale

BUSINESS & IT

TRANSFORMATION

Manage and govern

the change

+ HYBRID

CLOUD

ON PREMISE

© 2017 Software AG. All rights reserved.

40 |

© 2017 Software AG. All rights reserved.

DIGITAL BUSINESS PLATFORM CAPABILITIES

Business strategy

& planning

Collaboration

Design &

analysis

Risk & compliance

management

Audit

management

Portfolio

management

Enterprise

architecture

BUSINESS & IT

TRANSFORMATION

PROCESS

IoT

integration

INTEGRATION

Pattern

detection

Mobile

enablement

Application

integration

Mobile

integration

In-Memory data

management

Visual

analytics

Business

dashboards

Process

automation

Task

management

B2B

integration

Services

governance

Universal

messaging

Predictive

analytics

Process

discovery

Application

development

Rules

management

API

gateway

Integration

services

Search &

compute

Event

processing

Process

monitoring

Case

management

Process

orchestration

API

portal

Cloud service

integration

Continuous

query

IN-MEMORY

DATA

ANALYTICS &

DECISIONS

41 |

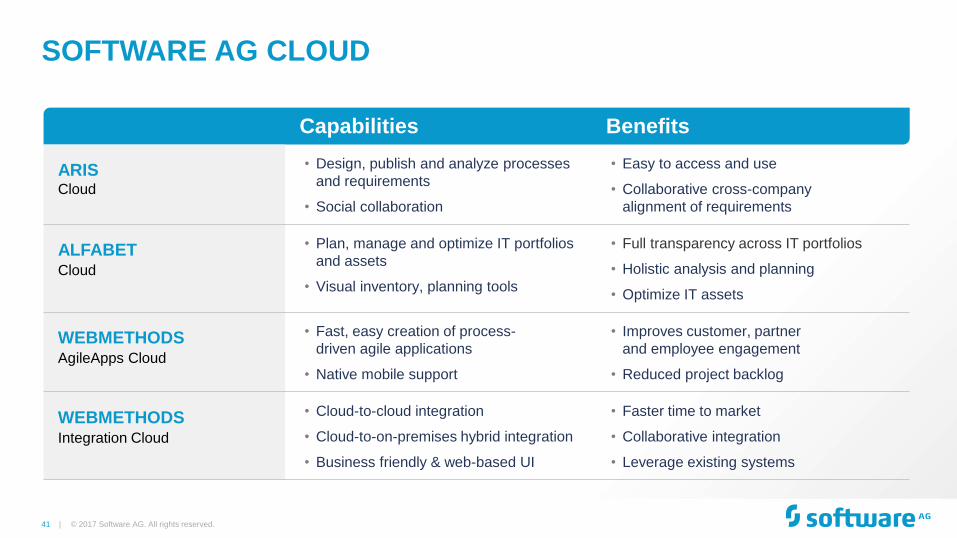

SOFTWARE AG CLOUD

Capabilities Benefits

ARIS Cloud

• Design, publish and analyze processes

and requirements

• Social collaboration

• Easy to access and use

• Collaborative cross-company

alignment of requirements

ALFABET Cloud

• Plan, manage and optimize IT portfolios

and assets

• Visual inventory, planning tools

• Full transparency across IT portfolios

• Holistic analysis and planning

• Optimize IT assets

WEBMETHODS AgileApps Cloud

• Fast, easy creation of process-

driven agile applications

• Native mobile support

• Improves customer, partner

and employee engagement

• Reduced project backlog

WEBMETHODS Integration Cloud

• Cloud-to-cloud integration

• Cloud-to-on-premises hybrid integration

• Business friendly & web-based UI

• Faster time to market

• Collaborative integration

• Leverage existing systems

© 2017 Software AG. All rights reserved.

42 |

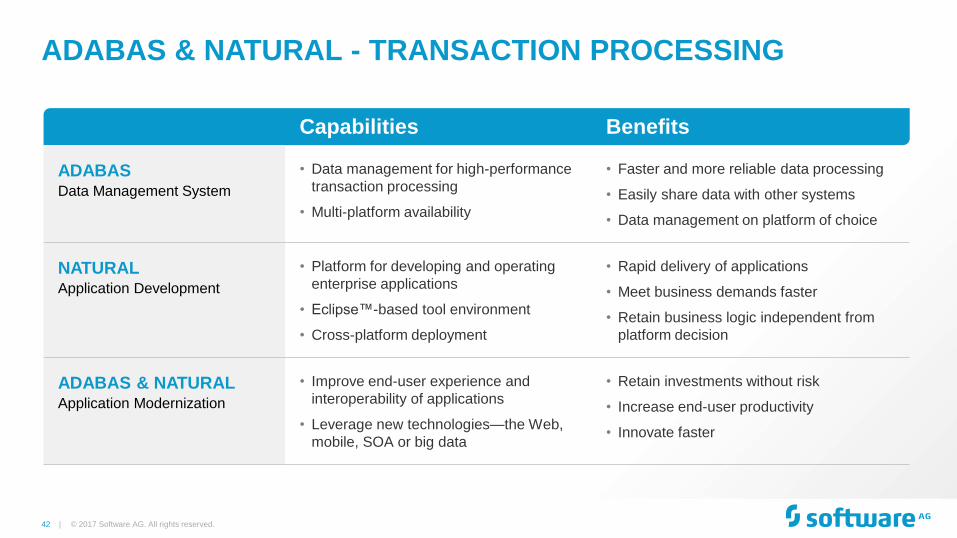

Capabilities Benefits

ADABAS Data Management System

• Data management for high-performance

transaction processing

• Multi-platform availability

• Faster and more reliable data processing

• Easily share data with other systems

• Data management on platform of choice

NATURAL Application Development

• Platform for developing and operating

enterprise applications

• Eclipse™-based tool environment

• Cross-platform deployment

• Rapid delivery of applications

• Meet business demands faster

• Retain business logic independent from

platform decision

ADABAS & NATURAL Application Modernization

• Improve end-user experience and

interoperability of applications

• Leverage new technologies—the Web,

mobile, SOA or big data

• Retain investments without risk

• Increase end-user productivity

• Innovate faster

ADABAS & NATURAL - TRANSACTION PROCESSING

© 2017 Software AG. All rights reserved.

43 |

INDEX

© 2017 Software AG. All rights reserved.

Key Value Investment Indicators 1. 7

Business Model, Characteristics & GTM 2. 21

Markets, Positioning & Competition 3. 28

Digital Business Platform - Core Capabilities 4. 37

Customers References & Use Cases 5. 44

Financials 6. 57

Shares & Ownership 7. 73

44 |

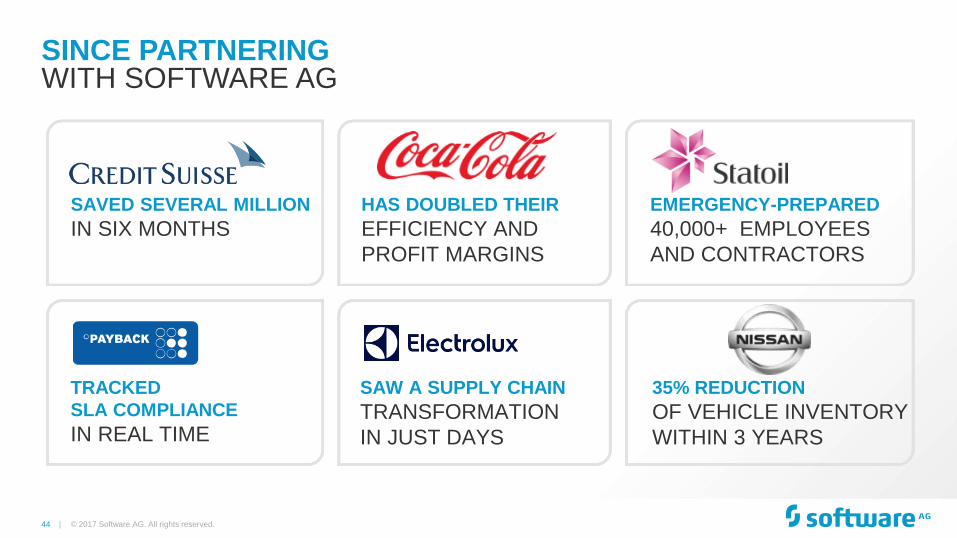

SINCE PARTNERING WITH SOFTWARE AG

SAVED SEVERAL MILLION

IN SIX MONTHS

HAS DOUBLED THEIR

EFFICIENCY AND

PROFIT MARGINS

EMERGENCY-PREPARED

40,000+ EMPLOYEES

AND CONTRACTORS

TRACKED

SLA COMPLIANCE

IN REAL TIME

SAW A SUPPLY CHAIN

TRANSFORMATION

IN JUST DAYS

35% REDUCTION

OF VEHICLE INVENTORY

WITHIN 3 YEARS

© 2017 Software AG. All rights reserved.

45 |

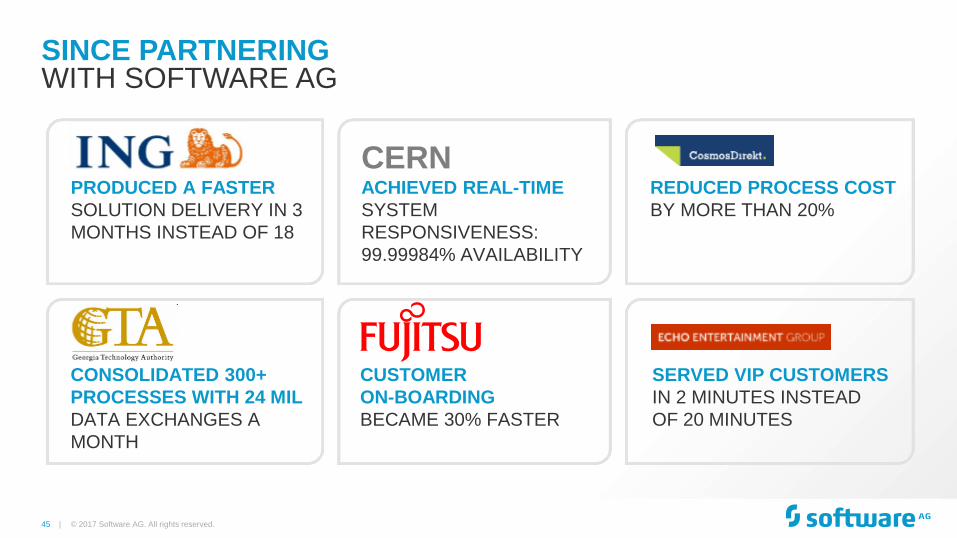

SINCE PARTNERING WITH SOFTWARE AG

PRODUCED A FASTER

SOLUTION DELIVERY IN 3

MONTHS INSTEAD OF 18

ACHIEVED REAL-TIME

SYSTEM

RESPONSIVENESS:

99.99984% AVAILABILITY

CERN REDUCED PROCESS COST

BY MORE THAN 20%

CONSOLIDATED 300+

PROCESSES WITH 24 MIL

DATA EXCHANGES A

MONTH

CUSTOMER

ON-BOARDING

BECAME 30% FASTER

SERVED VIP CUSTOMERS

IN 2 MINUTES INSTEAD

OF 20 MINUTES

© 2017 Software AG. All rights reserved.

46 |

CO-INNOVATION CUSTOMERS 2016

© 2017 Software AG. All rights reserved.

47 |

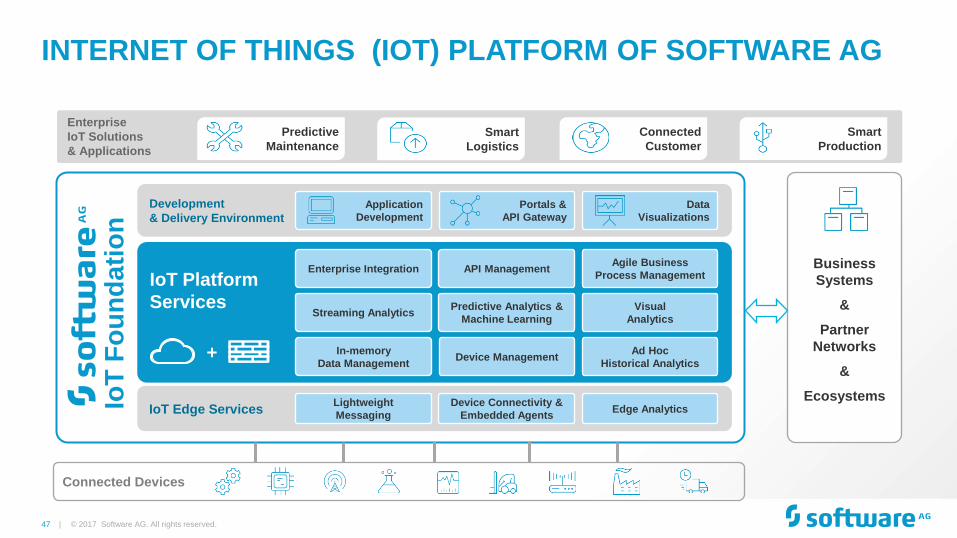

INTERNET OF THINGS (IOT) PLATFORM OF SOFTWARE AG

Connected Devices

Enterprise

IoT Solutions

& Applications

Predictive

Maintenance

Smart

Production

Connected

Customer

Smart

Logistics

Development

& Delivery Environment

Application

Development

Portals &

API Gateway

Data

Visualizations

IoT Edge Services Lightweight

Messaging Edge Analytics

Device Connectivity &

Embedded Agents

© 2017 Software AG. All rights reserved.

Business

Systems

&

Partner

Networks

&

Ecosystems

IoT Platform

Services

Agile Business

Process Management

Predictive Analytics &

Machine Learning Streaming Analytics

In-memory

Data Management

Enterprise Integration

Visual

Analytics

Device Management Ad Hoc

Historical Analytics

API Management

+

IoT

Fo

un

dati

on

48 |

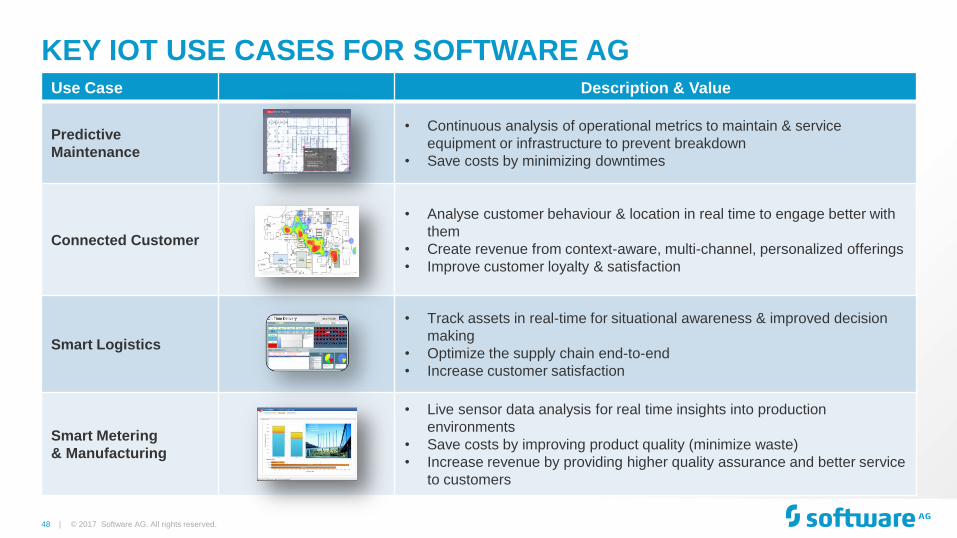

KEY IOT USE CASES FOR SOFTWARE AG Use Case Description & Value

Predictive

Maintenance

• Continuous analysis of operational metrics to maintain & service

equipment or infrastructure to prevent breakdown

• Save costs by minimizing downtimes

Connected Customer

• Analyse customer behaviour & location in real time to engage better with

them

• Create revenue from context-aware, multi-channel, personalized offerings

• Improve customer loyalty & satisfaction

Smart Logistics

• Track assets in real-time for situational awareness & improved decision

making

• Optimize the supply chain end-to-end

• Increase customer satisfaction

Smart Metering

& Manufacturing

• Live sensor data analysis for real time insights into production

environments

• Save costs by improving product quality (minimize waste)

• Increase revenue by providing higher quality assurance and better service

to customers

© 2017 Software AG. All rights reserved.

49 |

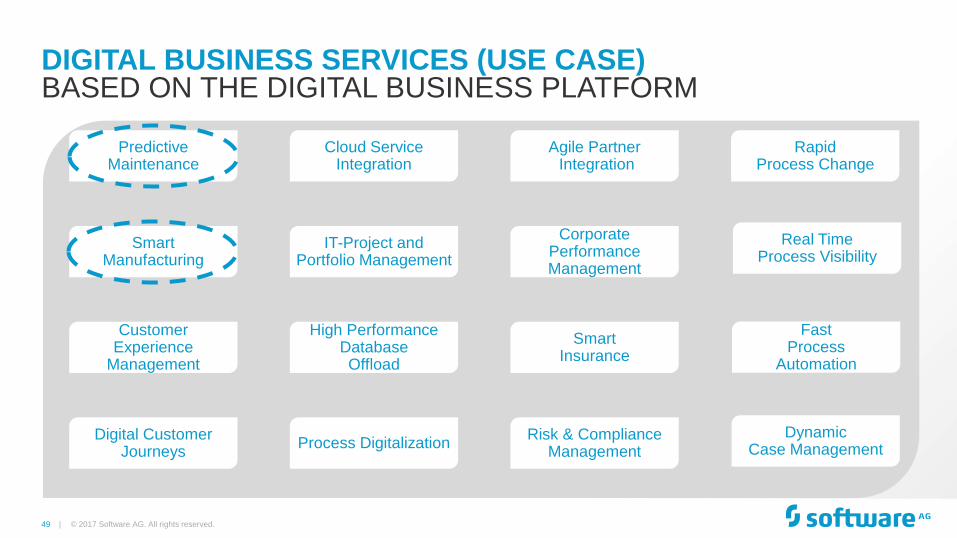

Predictive Maintenance

Cloud Service Integration

Agile Partner Integration

Rapid Process Change

Smart Manufacturing

IT-Project and Portfolio Management

Corporate Performance Management

Customer Experience

Management

High Performance Database Offload

Smart Insurance

Digital Customer Journeys

Process Digitalization Risk & Compliance

Management

Real Time Process Visibility

Fast Process

Automation

Dynamic Case Management

© 2017 Software AG. All rights reserved.

DIGITAL BUSINESS SERVICES (USE CASE) BASED ON THE DIGITAL BUSINESS PLATFORM

50 |

INTERNET OF THINGS

© 2017 Software AG. All rights reserved. For internal use only

PREDICTIVE MAINTENANCE Monitor equipment condition and predict failures using sensor data

Combine historical maintenance trends and real-time sensor data

Predict when plant or field assets require maintenance

Obtain real-time visibility of technician tasks and performance

Improved operating margins on technician and maintenance costs

Improved remedial planning and insights into preventative measures

More stringent SLAs resulting in higher revenue

51 |

OMNI-CHANNEL

© 2017 Software AG. All rights reserved.

ORCHESTRATION

Centralized orchestration of the customer’s shopping experience

Seamless order fulfillment across multiple channels and systems

Streamlined systems interaction and omni-channel business processes

Satisfy customer desire to buy and acquire from any channel they desire

Optimize inventory sourcing for every order

Bring together multi-line orders at the customer’s chosen location

Helps retailers keep their brand promise by meeting

customer expectations

52 |

CUSTOMER JOURNEY MAPPING

© 2017 Software AG. All rights reserved

An approach to digital transformation that starts with mapping customer journeys

Create detailed maps describing the nature of existing customer journeys

Design and manage customer journeys for a seamless omni-channel experience

Understand how your existing processes and channels support those journeys

Identify opportunities for process improvement

Maps a comprehensive path for digital transformation

Describes how effectively omni-channel journeys are supported today

Improves the customer’s experience across all channels and touchpoints

53 |

LOCATION-BASED MARKETING

© 2017 Software AG. All rights reserved.

Right-time, personalized, location-based targeting

Analyze customer location in real time

Segment customers based on historical & real-time context & profiles

Deliver offers, promotions, product & service updates to a segment-of-one

Improved response rates through real-time location analytics

Boost your customer interaction & brand loyalty

Increase promotion conversion rates by up to factor 10

54 |

COMPLIANCE MANAGEMENT

© 2017 Software AG. All rights reserved.

Process-driven approach to risk and compliance management

Design, implement and document controls, tests and risk assessment

Analyze and evaluate compliance and operational risks

Update management via an up-to-the minute graphical dashboard

Automatically escalate issues for resolution

Improve transparency and decision-making

Reduce ongoing compliance and audit costs

Adapt to new regulation faster

55 |

INTEGRATED IT PORTFOLIO MANAGEMENT

© 2017 Software AG. All rights reserved.

Optimize the portfolios in terms of KPIs, such as risk, cost agility and suitability

for future use

Create portfolio improvement scenarios and develop road maps

Synchronize road maps across the different IT portfolios

Align road maps with business stakeholders

Impose governance workflows on portfolio decision-making

Aligning business and IT

Optimizing IT costs

Making the right investments

56 |

INDEX

© 2017 Software AG. All rights reserved.

Key Value Investment Indicators 1. 7

Business Model, Characteristics & GTM 2. 21

Markets, Positioning & Competition 3. 28

Digital Business Platform - Core Capabilities 4. 37

Customers References & Use Cases 5. 44

Financials 6. 57

Shares & Ownership 7. 73

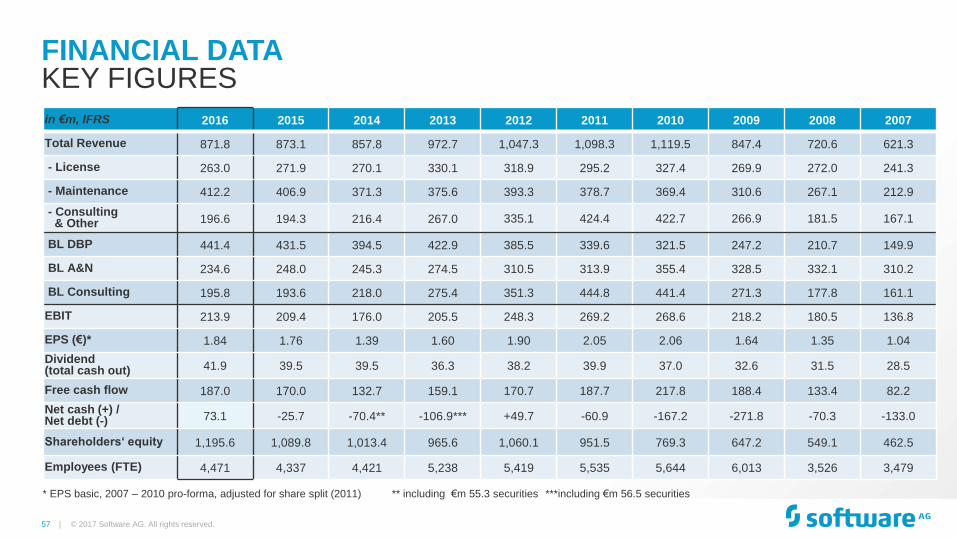

57 |

* EPS basic, 2007 – 2010 pro-forma, adjusted for share split (2011) ** including €m 55.3 securities ***including €m 56.5 securities

in €m, IFRS 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007

Total Revenue 871.8 873.1 857.8 972.7 1,047.3 1,098.3 1,119.5 847.4 720.6 621.3

- License 263.0 271.9 270.1 330.1 318.9 295.2 327.4 269.9 272.0 241.3

- Maintenance 412.2 406.9 371.3 375.6 393.3 378.7 369.4 310.6 267.1 212.9

- Consulting & Other 196.6 194.3 216.4 267.0 335.1 424.4 422.7 266.9 181.5 167.1

BL DBP 441.4 431.5 394.5 422.9 385.5 339.6 321.5 247.2 210.7 149.9

BL A&N 234.6 248.0 245.3 274.5 310.5 313.9 355.4 328.5 332.1 310.2

BL Consulting 195.8 193.6 218.0 275.4 351.3 444.8 441.4 271.3 177.8 161.1

EBIT 213.9 209.4 176.0 205.5 248.3 269.2 268.6 218.2 180.5 136.8

EPS (€)* 1.84 1.76 1.39 1.60 1.90 2.05 2.06 1.64 1.35 1.04

Dividend (total cash out) 41.9 39.5 39.5 36.3 38.2 39.9 37.0 32.6 31.5 28.5

Free cash flow 187.0 170.0 132.7 159.1 170.7 187.7 217.8 188.4 133.4 82.2

Net cash (+) / Net debt (-) 73.1 -25.7 -70.4** -106.9*** +49.7 -60.9 -167.2 -271.8 -70.3 -133.0

Shareholders‘ equity 1,195.6 1,089.8 1,013.4 965.6 1,060.1 951.5 769.3 647.2 549.1 462.5

Employees (FTE) 4,471 4,337 4,421 5,238 5,419 5,535 5,644 6,013 3,526 3,479

FINANCIAL DATA

© 2017 Software AG. All rights reserved.

KEY FIGURES

58 |

1. Return on equity: Operating EBIT / Equity

2. Return on cap. employed: Operating EBIT / (Fixed assets + Working capital)

3. Current assets ./. Cash and Cash Equivalents ./. Current liabilities

4. Current assets ./. Current liabilities / Total revenue

5. (Operating Cash flow ./. Capex) / Revenue.

IFRS unless stated different

FY 2016 FY 2015 FY 2014 FY 2013 FY 2012 FY 2011 FY 2010 FY 2009 FY 2008 FY 2007

Operating margin (EBITA, non-IFRS)

31.2% 29.7% 27.9% 26.8% 28.5% n.a. n.a. n.a. n.a. n.a.

EBITDA margin 29.1% 29.7% 26.4% 26.6% 28.6% 28.7% 28.1% 30.3% 28.6% 25.7%

EBIT margin 24.5% 24.0% 20.5% 21.1% 23.7% 24.5% 24.0% 25.8% 25.1% 23.3%

ROE1 17.9% 19.2% 17.4% 21.3% 23.4% 28.3% 34.9% 33.7% 32.9% 31.8%

ROCE2 15.2% 16.1% 12.6% 14.6% 18.2% 20.5% 27.4% 20.9% 26.2% 22.5%

Net Working Capital (€m)3 -€200.2 -€155.9 -€98.1 -€213.5 -€41.6 -€23.8 -€194.4 -€211.3 -€74.1 -€55.0

Working Capital ratio4 20.0% 16.6% 25.7% 24.3% 26.2% 17.5% -8.2% 0.8% 3.2% 4.2%

Free Cash Flow margin5 21.4% 19.5% 15.5% 16.4% 16.3% 17.1% 19.5% 22.2% 18.5% 13.2%

Corporate tax rate 33.0% 32.4% 33.7% 32.0% 31.2% 31.7% 31.0% 32.7% 34.0% 35.4%

WACC6 4.05% 4.13% 4.35% 5.12% 5.1% 5.7% 6.8% 5.5% 6.8% 8.4%

Equity ratio 61.2% 60.1% 54.8% 48.4% 59.8% 56.6% 48.1% 39.1% 51.8% 47.2%

DSO (Days Sales Outstanding) 113 111 115 107 105 93 100 109 120 119

Capex (€m) 16.7 €15.5 €10.5 €12.7 €13.3 €10.9 €9.7 €12.1 €6.6 €11.8

Capital Employed7 (€m) 1,381.9 €1,282.8 €1,326.0 €1,346.3 €1,313.0 €1,262.0 €929.6 €1,002.2 €669.9 €655.2

KEY FINANCIAL RATIOS IN % OF REVENUE

6. Pro forma, not applied for corporate management

7. Fixed assets + Working capital

© 2017 Software AG. All rights reserved.

59 |

Product Revenue

Digital Business Platform

Product Revenue

Adabas & Natural

Operating Margin

(EBITA non-IFRS)2)

OUTLOOK – CONFIRMED

© 2017 Software AG. All rights reserved.

FULL YEAR 2017

1) At constant currency rates

2) Adjusted for non-operating items (see non-IFRS earnings results)

30.5% to 31.5%

-2% to -6%1)

+5% to +10%1)

Outlook FY 2017 FY 2016 (in €m)

233.9

441.4

31.2%

60 |

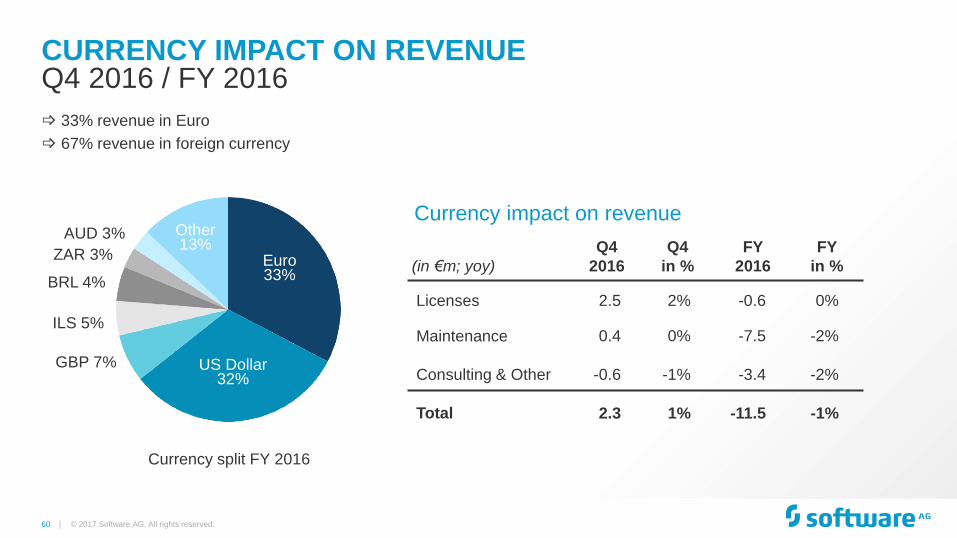

CURRENCY IMPACT ON REVENUE

© 2017 Software AG. All rights reserved.

Q4 2016 / FY 2016

Euro 33%

US Dollar 32%

Other 13%

(in €m; yoy)

Q4

2016

Q4

in %

FY

2016

FY

in %

Licenses 2.5 2% -0.6 0%

Maintenance 0.4 0% -7.5 -2%

Consulting & Other -0.6 -1% -3.4 -2%

Total 2.3 1% -11.5 -1%

Currency impact on revenue

33% revenue in Euro

67% revenue in foreign currency

Currency split FY 2016

Euro 33%

US Dollar 32%

Other 13%

BRL 4%

ZAR 3%

AUD 3%

GBP 7%

ILS 5%

61 |

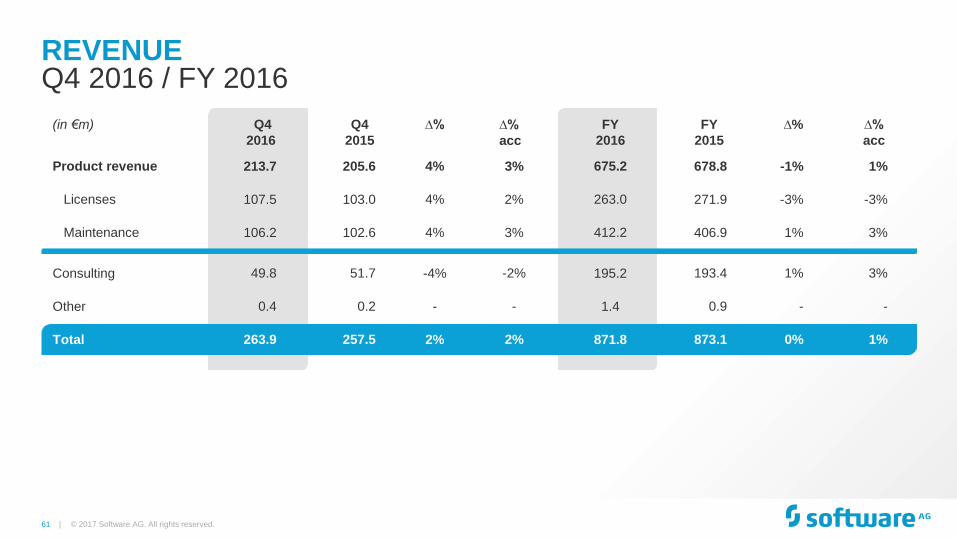

(in €m) Q4

2016

Q4

2015

∆% ∆%

acc

FY

2016

FY

2015

∆% ∆%

acc

Product revenue 213.7 205.6 4% 3% 675.2 678.8 -1% 1%

Licenses 107.5 103.0 4% 2% 263.0 271.9 -3% -3%

Maintenance 106.2 102.6 4% 3% 412.2 406.9 1% 3%

Consulting 49.8 51.7 -4% -2% 195.2 193.4 1% 3%

Other 0.4 0.2 - - 1.4 0.9 - -

Total 263.9 257.5 2% 2% 871.8 873.1 0% 1%

REVENUE

© 2017 Software AG. All rights reserved.

Q4 2016 / FY 2016

62 |

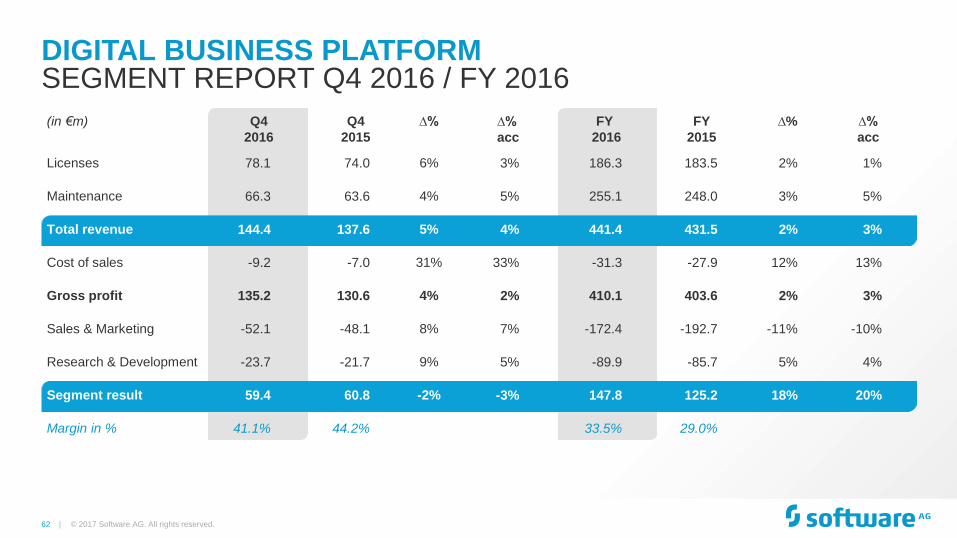

DIGITAL BUSINESS PLATFORM SEGMENT REPORT Q4 2016 / FY 2016

(in €m) Q4

2016

Q4

2015

∆% ∆%

acc

FY

2016

FY

2015

∆% ∆%

acc

Licenses 78.1 74.0 6% 3% 186.3 183.5 2% 1%

Maintenance 66.3 63.6 4% 5% 255.1 248.0 3% 5%

Total revenue 144.4 137.6 5% 4% 441.4 431.5 2% 3%

Cost of sales -9.2 -7.0 31% 33% -31.3 -27.9 12% 13%

Gross profit 135.2 130.6 4% 2% 410.1 403.6 2% 3%

Sales & Marketing -52.1 -48.1 8% 7% -172.4 -192.7 -11% -10%

Research & Development -23.7 -21.7 9% 5% -89.9 -85.7 5% 4%

Segment result 59.4 60.8 -2% -3% 147.8 125.2 18% 20%

Margin in % 41.1% 44.2% 33.5% 29.0%

© 2017 Software AG. All rights reserved.

63 |

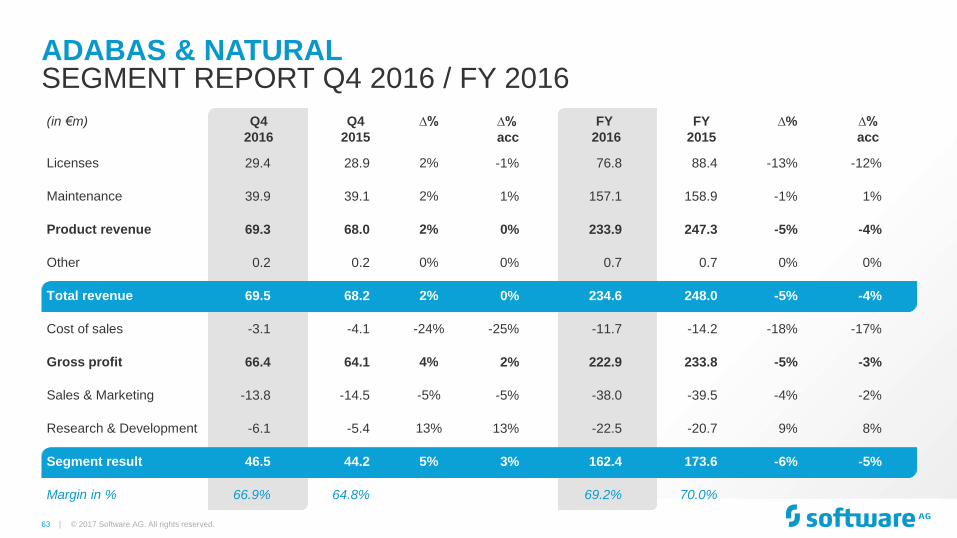

ADABAS & NATURAL SEGMENT REPORT Q4 2016 / FY 2016

© 2017 Software AG. All rights reserved.

(in €m) Q4

2016

Q4

2015

∆% ∆%

acc

FY

2016

FY

2015

∆% ∆%

acc

Licenses 29.4 28.9 2% -1% 76.8 88.4 -13% -12%

Maintenance 39.9 39.1 2% 1% 157.1 158.9 -1% 1%

Product revenue 69.3 68.0 2% 0% 233.9 247.3 -5% -4%

Other 0.2 0.2 0% 0% 0.7 0.7 0% 0%

Total revenue 69.5 68.2 2% 0% 234.6 248.0 -5% -4%

Cost of sales -3.1 -4.1 -24% -25% -11.7 -14.2 -18% -17%

Gross profit 66.4 64.1 4% 2% 222.9 233.8 -5% -3%

Sales & Marketing -13.8 -14.5 -5% -5% -38.0 -39.5 -4% -2%

Research & Development -6.1 -5.4 13% 13% -22.5 -20.7 9% 8%

Segment result 46.5 44.2 5% 3% 162.4 173.6 -6% -5%

Margin in % 66.9% 64.8% 69.2% 70.0%

64 |

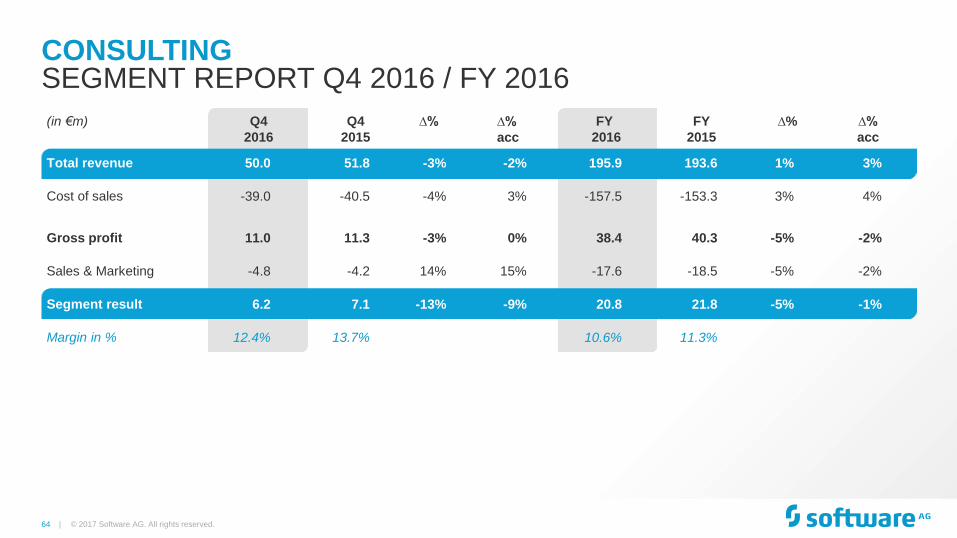

CONSULTING SEGMENT REPORT Q4 2016 / FY 2016

© 2017 Software AG. All rights reserved.

(in €m) Q4

2016

Q4

2015

∆% ∆%

acc

FY

2016

FY

2015

∆% ∆%

acc

Total revenue 50.0 51.8 -3% -2% 195.9 193.6 1% 3%

Cost of sales -39.0 -40.5 -4% 3% -157.5

-153.3 3% 4%

Gross profit 11.0 11.3 -3% 0% 38.4 40.3 -5% -2%

Sales & Marketing -4.8 -4.2 14% 15% -17.6 -18.5 -5% -2%

Segment result 6.2 7.1 -13% -9% 20.8 21.8 -5% -1%

Margin in % 12.4% 13.7% 10.6% 11.3%

65 |

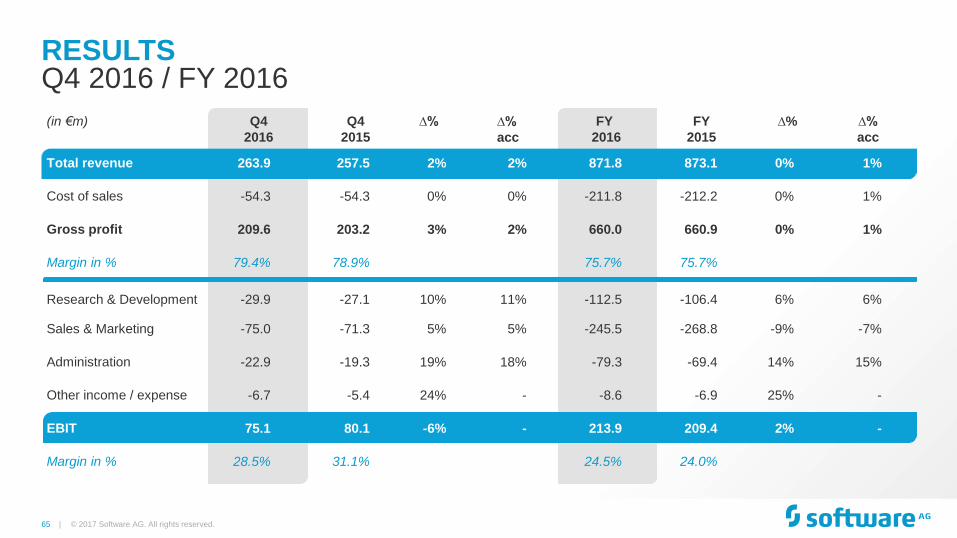

RESULTS Q4 2016 / FY 2016

© 2017 Software AG. All rights reserved.

(in €m) Q4

2016

Q4

2015

∆% ∆%

acc

FY

2016

FY

2015

∆% ∆%

acc

Total revenue 263.9 257.5 2% 2% 871.8 873.1 0% 1%

Cost of sales -54.3 -54.3 0% 0% -211.8 -212.2 0% 1%

Gross profit 209.6 203.2 3% 2% 660.0 660.9 0% 1%

Margin in % 79.4% 78.9% 75.7% 75.7%

Research & Development -29.9 -27.1 10% 11% -112.5 -106.4 6% 6%

Sales & Marketing -75.0 -71.3 5% 5% -245.5 -268.8 -9% -7%

Administration -22.9 -19.3 19% 18% -79.3 -69.4 14% 15%

Other income / expense -6.7 -5.4 24% - -8.6 -6.9 25% -

EBIT 75.1 80.1 -6% - 213.9 209.4 2% -

Margin in % 28.5% 31.1% 24.5% 24.0%

66 |

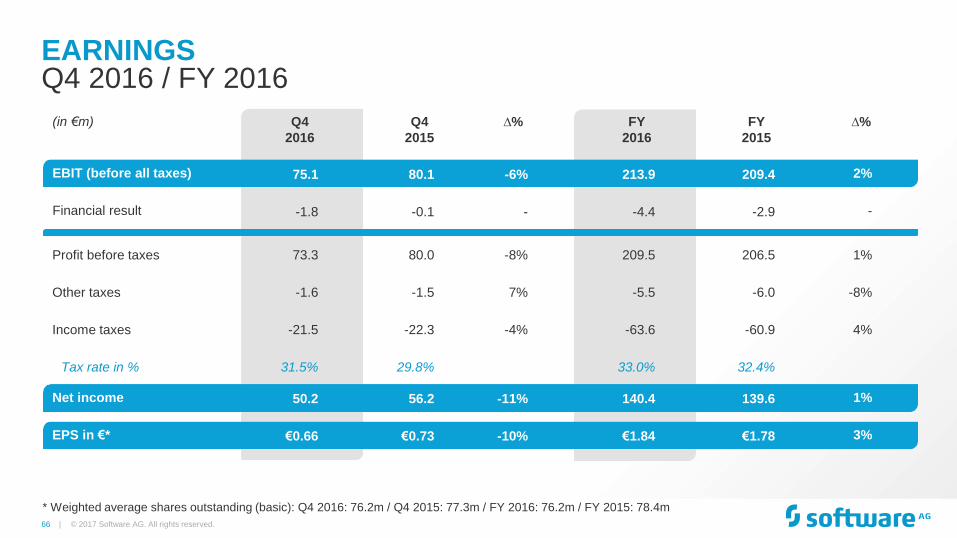

EARNINGS

© 2017 Software AG. All rights reserved.

Q4 2016 / FY 2016

* Weighted average shares outstanding (basic): Q4 2016: 76.2m / Q4 2015: 77.3m / FY 2016: 76.2m / FY 2015: 78.4m

(in €m) Q4

2016

Q4

2015

∆% FY

2016

FY

2015

∆%

EBIT (before all taxes) 75.1 80.1 -6% 213.9 209.4 2%

Financial result -1.8 -0.1 - -4.4 -2.9 -

Profit before taxes 73.3 80.0 -8% 209.5 206.5 1%

Other taxes -1.6 -1.5 7% -5.5 -6.0 -8%

Income taxes -21.5 -22.3 -4% -63.6 -60.9 4%

Tax rate in % 31.5% 29.8% 33.0% 32.4%

Net income 50.2 56.2 -11% 140.4 139.6 1%

EPS in €* €0.66 €0.73 -10% €1.84 €1.78 3%

67 |

NON-IFRS EARNINGS

© 2017 Software AG. All rights reserved.

Q4 2016 / FY 2016

* Weighted average shares outstanding (basic) Q4 2016: 76.2m / Q4 2015: 77.3m / FY 2016: 76.2m / FY 2015: 78.4m

(in €m) Q4

2016

Q4

2015

FY

2016

FY

2015

EBIT (before all taxes) 75.1 80.1 213.9 209.4

Amortization on acquisition related intangible assets 7.3 7.4 29.1 35.0

Share based payments 3.2 2.8 14.2 -3.1

Restructuring / severances / legal case 2.9 1.9 11.8 15.3

Other impacts / impacts from M&A activities 1.7 0.0 3.0 2.5

EBITA (non-IFRS) 90.2 92.2 272.0 259.1

in % of revenue (Non-IFRS) 34.2% 35.8% 31.2% 29.7%

Net income (non-IFRS) 61.1 64.8 180.4 173.9

EPS (non-IFRS)* €0.80 €0.84 €2.37 €2.22

68 |

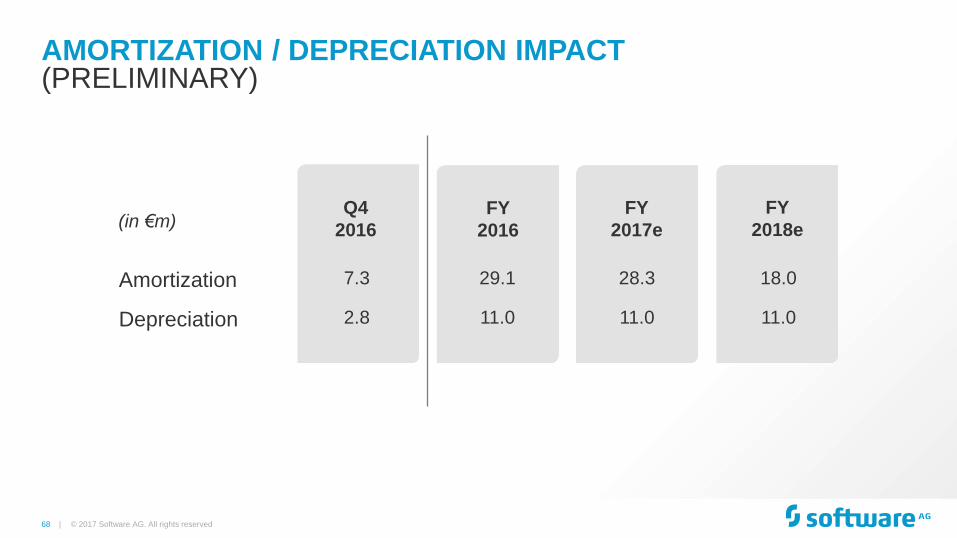

Q4

2016

FY

2016

FY

2017e

Amortization

(in €m)

Depreciation

FY

2018e

AMORTIZATION / DEPRECIATION IMPACT

© 2017 Software AG. All rights reserved

(PRELIMINARY)

29.1

11.0

28.3

11.0

7.3

2.8

18.0

11.0

69 |

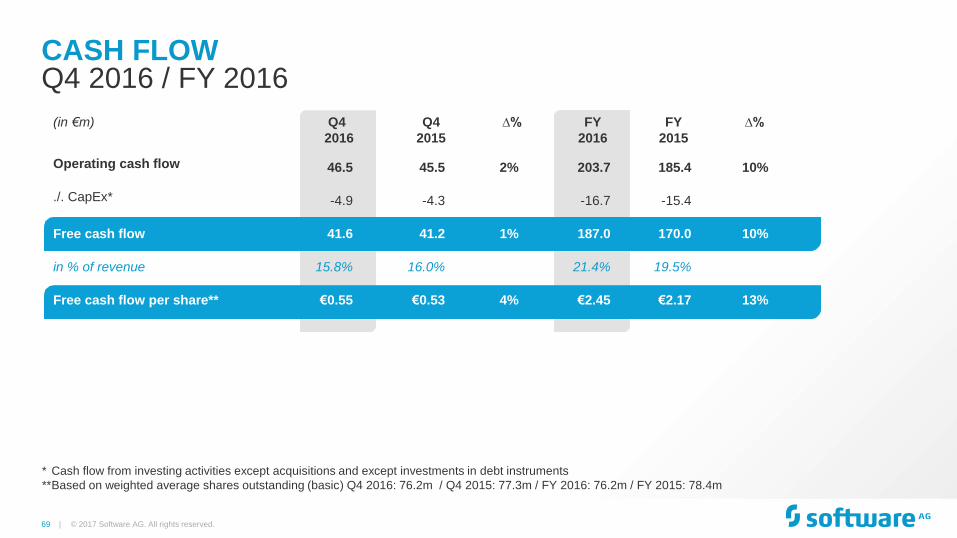

CASH FLOW

© 2017 Software AG. All rights reserved.

Q4 2016 / FY 2016

* Cash flow from investing activities except acquisitions and except investments in debt instruments

** Based on weighted average shares outstanding (basic) Q4 2016: 76.2m / Q4 2015: 77.3m / FY 2016: 76.2m / FY 2015: 78.4m

(in €m) Q4

2016

Q4

2015

∆% FY

2016

FY

2015

∆%

Operating cash flow 46.5 45.5 2% 203.7 185.4 10%

./. CapEx* -4.9 -4.3 -16.7 -15.4

Free cash flow 41.6 41.2 1% 187.0 170.0 10%

in % of revenue 15.8% 16.0% 21.4% 19.5%

Free cash flow per share** €0.55 €0.53 4% €2.45 €2.17 13%

70 |

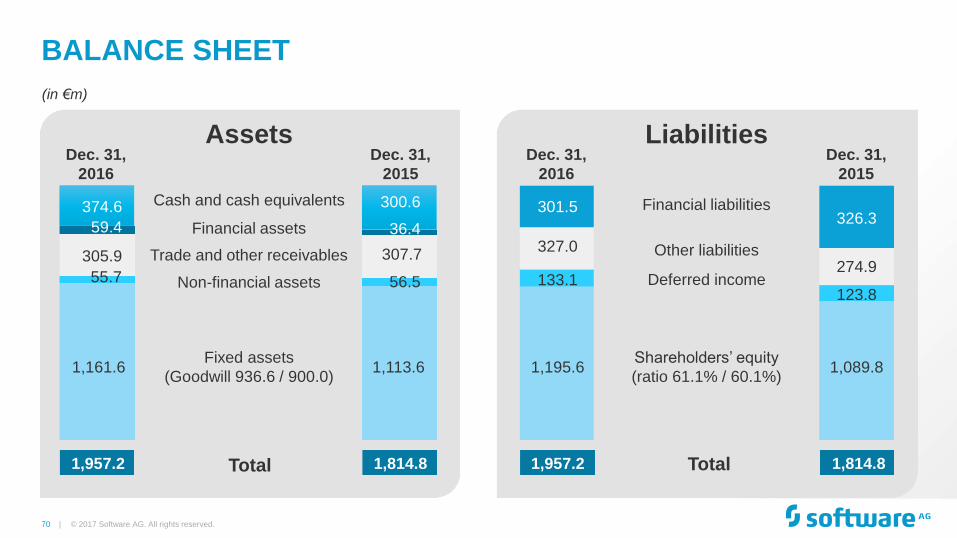

Dec. 31,

2016

Dec. 31,

2016

Assets Liabilities

BALANCE SHEET

© 2017 Software AG. All rights reserved.

(in €m)

Dec. 31,

2015

Dec. 31,

2015

Cash and cash equivalents

Financial assets

Trade and other receivables

Fixed assets

(Goodwill 936.6 / 900.0)

Total

Non-financial assets

Financial liabilities

Other liabilities

Deferred income

Shareholders’ equity

(ratio 61.1% / 60.1%)

Total

300.6

307.7

56.5

1,113.6

1,814.8

36.4 326.3

274.9

123.8

1,089.8

1,814.8

374.6

305.9

55.7

1,161.6

1,957.2

59.4

1,957.2

301.5

327.0

133.1

1,195.6

71 |

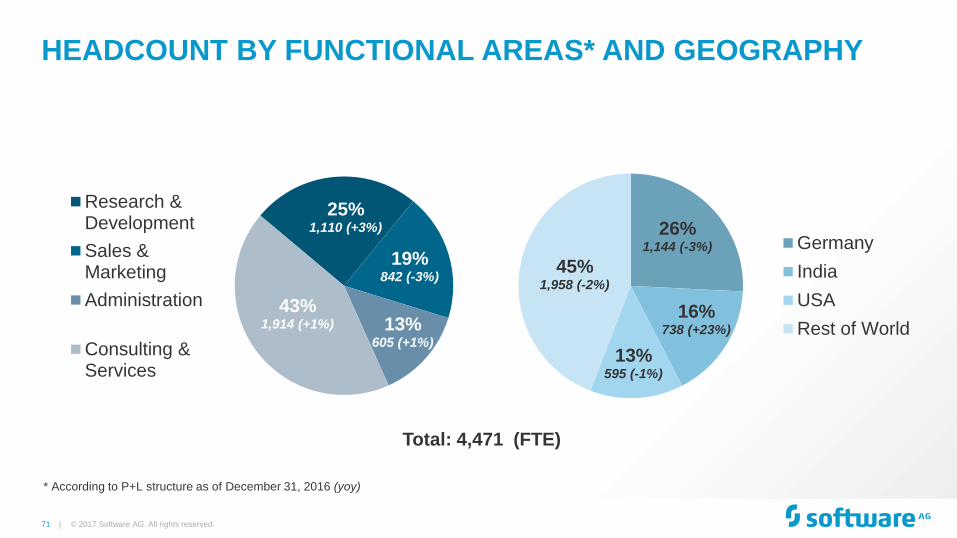

HEADCOUNT BY FUNCTIONAL AREAS* AND GEOGRAPHY

© 2017 Software AG. All rights reserved.

25% 1,110 (+3%)

19% 842 (-3%)

13% 605 (+1%)

43% 1,914 (+1%)

Research &Development

Sales &Marketing

Administration

Consulting &Services

26% 1,144 (-3%)

16% 738 (+23%)

13% 595 (-1%)

45% 1,958 (-2%)

Germany

India

USA

Rest of World

* According to P+L structure as of December 31, 2016 (yoy)

Total: 4,471 (FTE)

72 |

INDEX

© 2017 Software AG. All rights reserved.

Key Value Investment Indicators 1. 7

Business Model, Characteristics & GTM 2. 21

Markets, Positioning & Competition 3. 28

Digital Business Platform - Core Capabilities 4. 37

Customers References & Use Cases 5. 44

Financials 6. 57

Shares & Ownership 7. 73

73 |

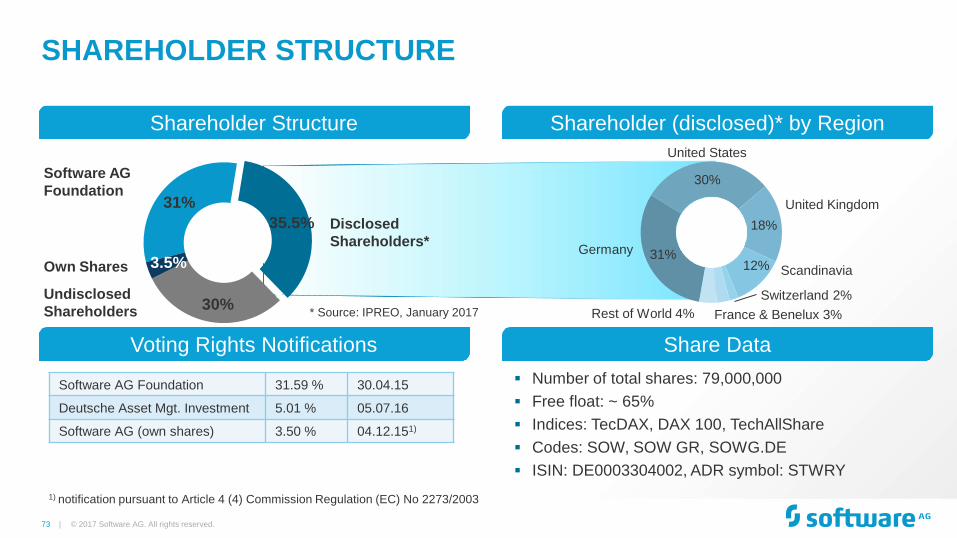

31%

35.5%

30%

3.5%

SHAREHOLDER STRUCTURE

© 2017 Software AG. All rights reserved.

31%

30%

18%

12%

Number of total shares: 79,000,000

Free float: ~ 65%

Indices: TecDAX, DAX 100, TechAllShare

Codes: SOW, SOW GR, SOWG.DE

ISIN: DE0003304002, ADR symbol: STWRY

Germany

United States

France & Benelux 3%

Scandinavia

United Kingdom

Rest of World 4%

Shareholder Structure

Share Data

Shareholder (disclosed)* by Region

Software AG Foundation 31.59 % 30.04.15

Deutsche Asset Mgt. Investment 5.01 % 05.07.16

Software AG (own shares) 3.50 % 04.12.151)

Voting Rights Notifications

Switzerland 2%

1) notification pursuant to Article 4 (4) Commission Regulation (EC) No 2273/2003

* Source: IPREO, January 2017

Software AG

Foundation

Disclosed

Shareholders*

Undisclosed

Shareholders

Own Shares

74 |

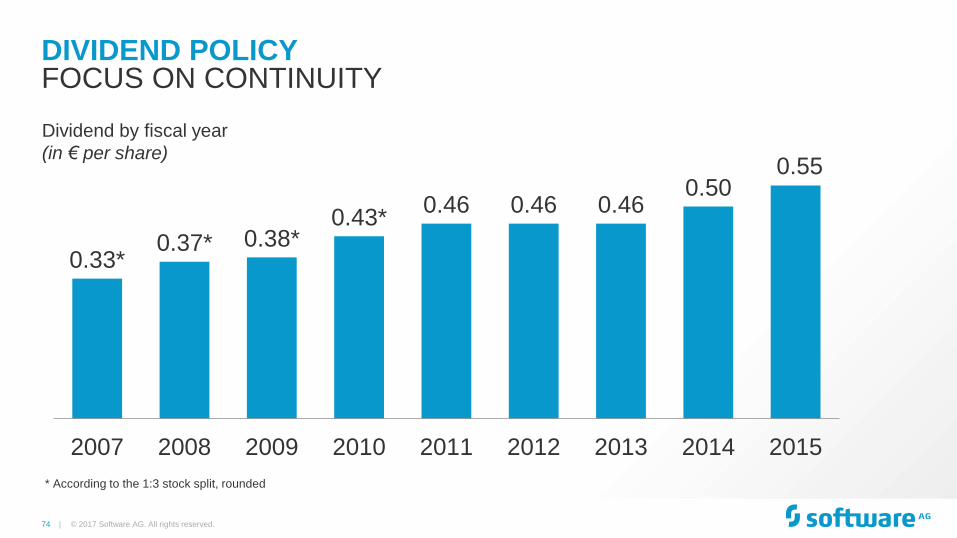

0.33* 0.37* 0.38*

0.43* 0.46 0.46 0.46

0.50 0.55

2007 2008 2009 2010 2011 2012 2013 2014 2015

DIVIDEND POLICY

© 2017 Software AG. All rights reserved.

FOCUS ON CONTINUITY

Dividend by fiscal year

(in € per share)

* According to the 1:3 stock split, rounded

75 |

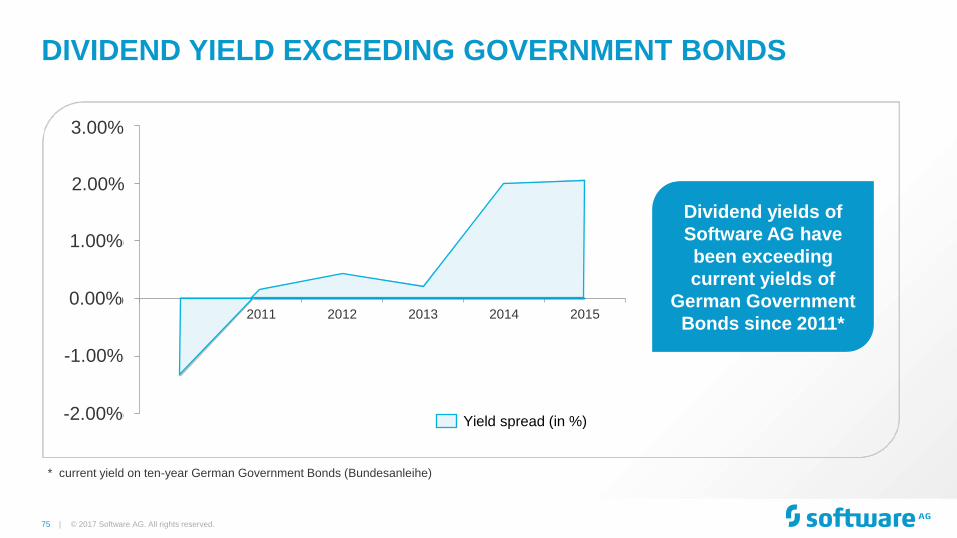

DIVIDEND YIELD EXCEEDING GOVERNMENT BONDS

© 2017 Software AG. All rights reserved.

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

2010 2011 2012 2013 2014 2015

Yield spread (in %)

* current yield on ten-year German Government Bonds (Bundesanleihe)

Dividend yields of

Software AG have

been exceeding

current yields of

German Government

Bonds since 2011*

3.00%

2.00%

1.00%

0.00%

-1.00%

-2.00%

76 |

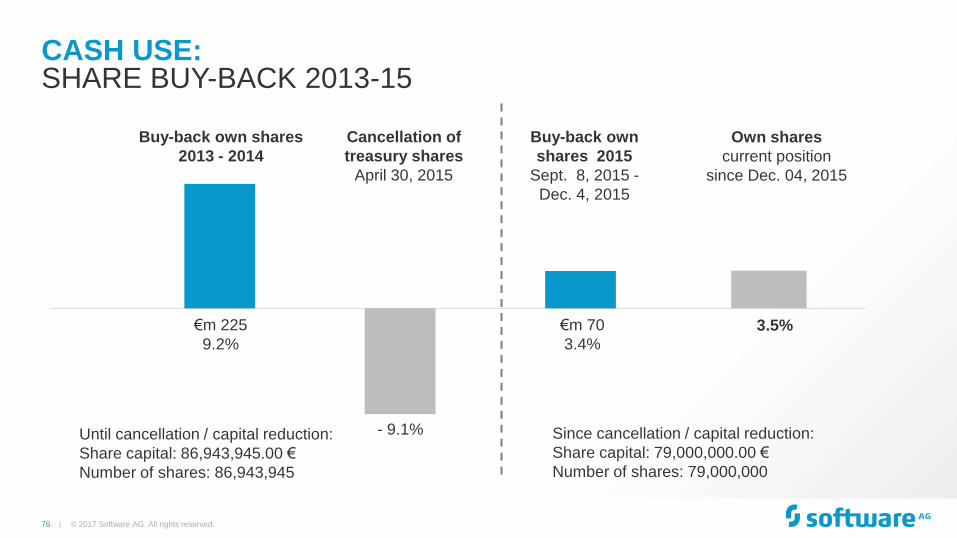

CASH USE:

© 2017 Software AG. All rights reserved.

SHARE BUY-BACK 2013-15

Buy-back own shares

2013 - 2014

Cancellation of

treasury shares

April 30, 2015

Buy-back own

shares 2015

Sept. 8, 2015 -

Dec. 4, 2015

Until cancellation / capital reduction:

Share capital: 86,943,945.00 €

Number of shares: 86,943,945

€m 225

9.2%

€m 70

3.4%

- 9.1%

Own shares

current position

since Dec. 04, 2015

3.5%

Since cancellation / capital reduction:

Share capital: 79,000,000.00 €

Number of shares: 79,000,000

77 |

SOFTWARE AG FOUNDATION

© 2017 Software AG. All rights reserved.

ANCHOR SHAREHOLDER

The Software AG Foundation is one of Germany’s ten largest foundations

(capital stock € 1bn+, Software AG shares and other assets)

Founded by Dr. hc. Peter M. Schnell in 1992

Disburses financial support amounting to approx. € 30 million annually

Principle of a “self-help grant” (supports nonprofit organizations)

The Foundation focuses on many different projects in areas including:

• science and research, environment

• support for the elderly and disabled, support for children and young people

• education and training

78 |

ANALYST COVERAGE

© 2017 Software AG. All rights reserved.

Baader Helvea E.R.

Barclays Capital

Bryan, Garnier & Co

Commerzbank

Crédit Suisse

Deutsche Bank

DZ Bank

Equinet

Goldman Sachs

Hauck & Aufhäuser

HSBC

Independent Research

J.P. Morgan Cazenove

Kepler Cheuvreux

LBBW

MainFirst Bank AG

Metzler

Morgan Stanley

Oddo Seydler

Société Générale

UBS I.R.

Warburg Research

For latest consensus of analysts‘ financial estimates visit our

IR website on: www.softwareag.com

Banks / Broker who cover Software AG on a regular base

79 | © 2017 Software AG. All rights reserved.

Investor Relations

Uhlandstrasse 12

64297 Darmstadt

Germany

phone: +49 (0) 6151 / 92 1900

fax: +49 (0) 6151 / 9234 1900

softwareag.com

e-mail: [email protected]