29

Investor Update 13 November 2002 www.banpu.co.th Rawi Corsiri Rawi Corsiri COO COO Somruedee Somphong Somruedee Somphong CFO CFO

Investor Update13 November 2002

www.banpu.co.th

Rawi CorsiriRawi Corsiri COOCOO

Somruedee Somphong Somruedee Somphong CFOCFO

2www.banpu.co.th

Agenda

Quarterly overviewQuarterly overviewResults highlightResults highlight

Coal industry snapshotCoal industry snapshot

Business scenarioBusiness scenario

3www.banpu.co.th

Quarterly overview

� Coal Business- Spot coal prices bottomed-out in 3Q and started to show a strong

recovery in 4Q- Cost reduction programs have been done in mining process at

Indominco & Kitadin- Successful implementation of Centralization and Marketing Logistics- Achieved shipments to European market

� Power Business- TECO achieved 100% AP during Aug-Oct after the inspectation in 2Q- On-course project financing process of BLCP

� Finance- Completion in securing long-term bank loan for ECD and bonds

refinancing- 2002 interim dividend of Bt1.50/share

4www.banpu.co.th

Coal tonnage sales

Source: Banpu (Indocoal consolidation started in Mar02)

� A significant increase in volume sales in 3Q mainly from Thai market and International sales from Jorong

� Tonnage sales from Indocoal posted a slight decline due mainly from pending delivery in 4Q

� Anticipation of higher sales from Indocoalexport in 4Q

986 981 1,038 1,0251,356

431 554 458 441

513590

1,870

1,815

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Jul-Sep, 01 Oct-Dec, 01 Jan-Mar, 02 Apr-Jun, 02 Jul-Sep, 02

Unit

in '0

00 to

nnes

International sales - IndocoalInternational sales - JorongThai market sales

10%

5www.banpu.co.th

Sales revenue

Source: Banpu (Indocoal consolidation started in Mar02)

796 739 729 7461,015

321 356 310 313

320634

1,8841,643

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Jul-Sep, 01 Oct-Dec,01 Jan-Mar,02 Apr-Jun,02 Jul-Sep,02

Unit

in '0

00 B

aht

International sales - IndocoalInternational sales - JorongThai market sales

1%� Steady sales revenue

despite a sharp decline in coal prices

� Significant increase on Thai market sales due to temporarily domestic supply shortage

� Indocoal sales revenue anticipated to increase with more shipment in 4Q

6www.banpu.co.th

Market share - Thailand

Source: Banpu

Note: Total domestic coal consumptions in Thailand estimated at 10 MT

3Q02 9-month 2002

G Prem Jee9% Lanna

11%

Siam Cement7%

Others21%

Banpu52%

Siam Cement

6%

G Prem Jee9%

SBC6%

Marubeni3%

Others20%

Banpu44%

Lanna12%

� Banpu’s sales in Thailand achieved 52% market share

� YTD, Banpu shared 44% of the homeland market

7www.banpu.co.th

Agenda

Quarterly overviewQuarterly overview

Results highlightResults highlightCoal industry snapshotCoal industry snapshot

Business scenarioBusiness scenario

8www.banpu.co.th

Quarterly results

� Despite a strong growth in tonnage sales, 3Q revenues were steady due to the sharp decline in coal price

� Coal price also impacts gross profit and EBIT margins

� Strong core earnings (before FX) mainly from lower interest expense, and improved equity income

� However, the bottom-line dragged by TECO’s FX

Year-end Dec (Btm) 3Q02 2Q02Revenues 3,048 3,078 Gross profit 791 847 SG&A (373) (333) Royalty (249) (251) Other income 28 14 EBIT 196 277 Interest expense (168) (218) Equity income (bef. FX) 115 (13) Dividend income - 234 Income tax 19 (91) Minorities 11 (43) Net profit before extra items 173 146 Non-recurring items 69 172 ECD redemption premiums (19) (231) Mine property expenses (47) 57 Net profit before FX 177 143 Net profit 114 612

9www.banpu.co.th

9-month results

� Indocoal consolidation enhanced Banpu’srevenues by 71% y-y

� Gross profit margin significantly improved post-termination of EGAT’soverburden work

� Core-operation profits (before FX) solidly improved thanks to strong associate contributions

Year-end Dec (Btm) 9-mo02 9-mo01Revenues 7,742 4,136 Gross profit 2,169 852 SG&A (988) (894) Royalty (612) (79) Other income 165 162 EBIT 734 40 Interest expense (528) (359) Equity income (bef. FX) 222 157 Dividend income 267 9 Income tax (79) (65) Minorities (55) (23) Net profit before extra items 561 (242) Non-recurring items 384 1,099 ECD redemption premiums (337) (169) Mine property expense (25) - Net profit before FX 583 689 Net profit 1,271 659

10www.banpu.co.th

Operational breakdown

YTD 3Q02 2Q02 1Q02Tonnage sales ('000 tonnes)

Thai market 3,420 1,356 1,025 1,038 - Domestic 2,297 849 690 757 - Import 1,123 508 335 281 Jorong 1,411 513 441 458 Indocoal 4,275 1,815 1,870 590

Sales revenue (Btm)Thai market 2,490 1,015 746 729 - Domestic 1,090 410 342 338 - Import 1,399 605 404 390 Jorong 943 320 313 310 Indocoal 4,000 1,643 1,723 634

GPMThai market 23% 25% 21% 23% - Domestic 38% 33% 38% 42% - Import 12% 20% 11% 6%Jorong 49% 44% 54% 48%Indocoal 24% 22% 25% 27%

11www.banpu.co.th

Balance sheet

1.11.01.2

1.00.8

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Jul-Sep, 01 Oct-Dec, 01 Jan-Mar, 02 Apr-Jun, 02 Jul-Sep, 02

Historical net D/E

(Btm) Jul-Sep, 01 Oct-Dec, 01 Jan-Mar, 02 Apr-Jun, 02 Jul-Sep, 02

Total assets 16,397 15,799 23,291 23,310 23,584

Total liabilities 8,980 8,988 15,246 14,399 9,962

Net debts 5,932 6,454 9,238 9,193 9,460

Equity 7,417 6,811 8,045 8,911 8,449

12www.banpu.co.th

Agenda

Quarterly overviewQuarterly overview

Results highlightResults highlight

Coal industry snapshotCoal industry snapshotBusiness scenarioBusiness scenario

13www.banpu.co.th

Banpu’s position in Indonesia

Source: Indonesia Coal Mining Association, Banpu

Note: Banpu’s productions include Indominco, Kitadin, and Jorong

� Amongst key players in Indonesia, Banpu ranked 4th after Adaro, KPC, and Kideco

� Banpu’s productions of 11.2mtpa in 2002 to be increase in 2004 with new production of Trubaindo

� Indonesia target to export just above 70% in 2002 –the rest for domestic consumptions

Top-ten producers (mtpa) 2002E Sharing

Adaro Indonesia 20.5 19%

Kaltim Prima Coal 17.0 16%

Kideco Jaya Agung 11.5 11%

Banpu 11.2 11%Bukit Asam 10.5 10%

BHP Aruthmin 10.2 10%

Berau Coal 7.0 7%

Ganung Bayan Pratama 2.5 2%

Bukit Daiduri Enterprise 2.3 2%

Others 13.1 12%

Total 105.8 100%

14www.banpu.co.th

Thermal coal spot price

Source: International Coal Report (28 Oct 2002)

Kcal/kg Current 3Q 2Q 1Q

Australia

Gladstone 6500 24.50-25.50 23.69-25.34 26.62-28.15 28.51-29.41

Newcastle 6300 24.00-25.00 22.17-23.63 25.70-26.99 26.78-28.68

China - Qinghuadao 6200 25.50-26.80 23.47-24.47 26.74-27.78 28.77-29.77

Indonesia

Kalimantan 6300 23.50-24.50 21.89-23.32 24.44-25.37 26.81-27.68

Russia Pacific 6300 25.00-25.50 23.06-24.44 25.77-27.96 27.35-28.85

15www.banpu.co.th

Demand outlook – Asia (Pacific Rim)

� Demand of thermal coal is expected to increase at a steady pace driven by Pacific Rim countries of 4% pa in next 10-yr*

� Assumptions used are conservative given:

� Average GDP growth of 1.0-2.0%� Energy reform in Hong Kong� Kyoto protocol� Proposed coal tax of Japan� Korean’s utilities restructuring� Nuclear capacity addition in

Taiwan*Source: Hill & Associates (2002)

0

50

100

150

200

250

300

2001 2006 2011

Unit

in m

illio

n to

nnes

4.4% CAGR

Taiwan

S Korea

HK

Japan

16www.banpu.co.th

Demand outlook – Other Asia

� China: A record imported of 5.6mt in 1H02 compared with 0.8mt during the same period last year

� Malaysia: A rapid demand driven by increased coal-fired power plants from 700MW in 2001 to 7,300MW in 2006

� India: High demand frustrated by three obstacles: import levies, high rail rates, and limited port capacity

� Philippines: Despite a huge electricity consumption, coal-fired generation highly depends on the two government initiatives

� Thailand: Strong environmental opposition to some coal-fired power plants project

Source: Hill & Associates (2002)

17www.banpu.co.th

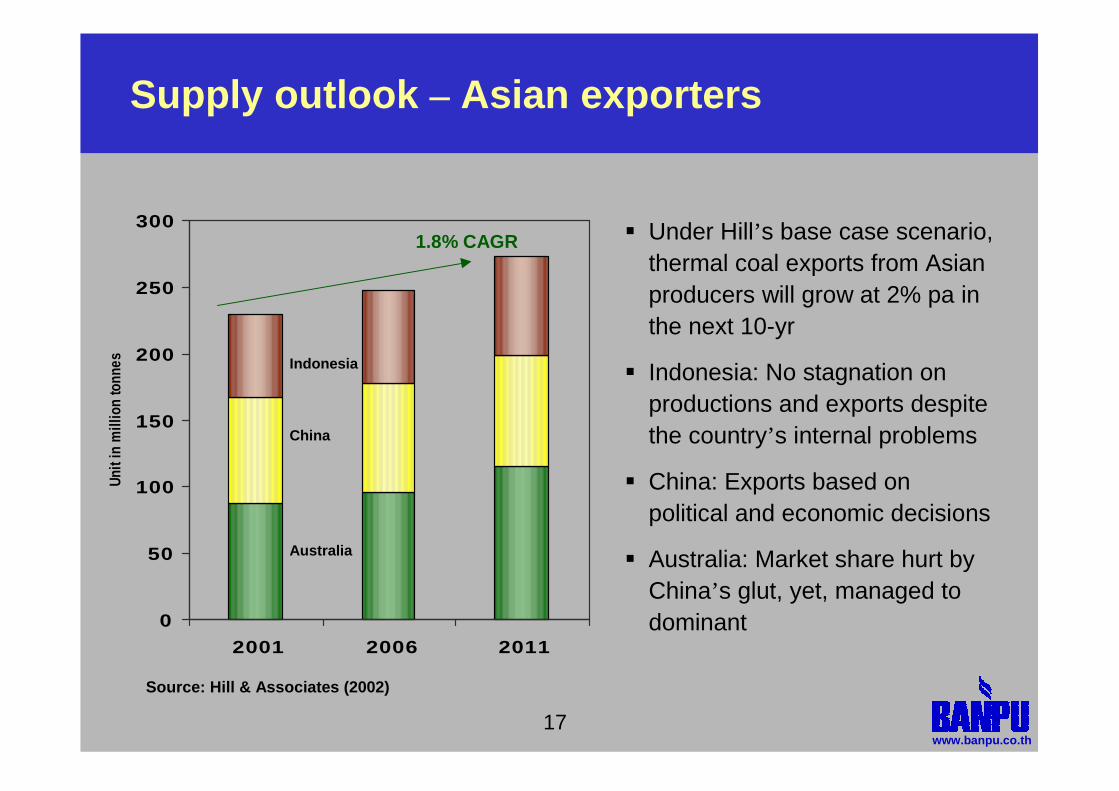

Supply outlook – Asian exporters

� Under Hill’s base case scenario, thermal coal exports from Asian producers will grow at 2% pa in the next 10-yr

� Indonesia: No stagnation on productions and exports despite the country’s internal problems

� China: Exports based on political and economic decisions

� Australia: Market share hurt by China’s glut, yet, managed to dominant

Source: Hill & Associates (2002)

0

50

100

150

200

250

300

2001 2006 2011

Unit

in m

illio

n to

nnes Indonesia

China

Australia

1.8% CAGR

18www.banpu.co.th

Agenda

Quarterly overviewQuarterly overview

Results highlightResults highlight

Coal industry snapshotCoal industry snapshot

Business scenarioBusiness scenario

19www.banpu.co.th

Ramp-up capacity production of Indocoal

0

1

2

3

4

5

6

7

1999 2000 2001 2002 2003 2004 2005 20060%

5%

10%

15%

20%

25%

30%

Indominco Kitadin Trubaindo Overall GPM

Post acquisition(MT)

20www.banpu.co.th

Implementation of cost reduction program

Crusher System

TWIN BOOMSTACKER

Coal Transport to Port34 Km

MINE STOCKYARD

PORT STOCKYARD

PIT

SHIP LOADER

Conve

yor 6

.5 Km

Truck Dump

C24-1C24-2

C24-3

C24-4

C25-1 C25-2C25-3

C25-4

Result QualityCV : 6000 - 6700kcalAsh: 5.0%Ts : 0.8%

Cross Belt Sample

Cross Belt SampleINDOMINCO

1

3

2

21www.banpu.co.th

Other issues

� Imposition of Japan coal tax

� The Bali Blast

� News on possible delay of BLCP

22www.banpu.co.th

Upcoming events

� Independent review of Banpu’s reserves figures by international technical consulting firm

� Secure additional investment insurance policy of Indonesian assets worth US$55m

Question & Answer

24www.banpu.co.th

Appendices

� Planned CAPEX 2002-06

� Debt portfolio

� Summary of Indocoal financials

� Summary of TECO’s financials

� BLCP development

25www.banpu.co.th

Planned Capex (Maintained)

(US$m) 2002 2003E 2004E 2005E 2006E

Coal Thailand __ 1 2 1 __

Jorong 12 3 6 1 2

Indocoal 11 11 10 11 9

Power 11 22 __ 21 49

Total 34 37 18 34 60

26www.banpu.co.th

Debt portfolio: as at September 2002

Debentures BANPUECD #2

BANPU #3

BANPU #4

BANPU #5

BANPU #6

IndocoalCD

O/S amount US$3.1m Bt937.5m Bt750m Bt2,500m Bt500m US$30m

Maturity date Apr-03 Nov-02 Nov-04 Apr-06 Apr-08 2004

Interest rate 2.75% 8.125% MLR-0.25% 5.80% MLR-0.375% 2.75%

Rating - - - "A-" (TRIS) "A-" (TRIS)

Bank Loans BANPU Indocoal

Long-term Bt2,280m US$61.1m

Short-term Bt1,200m Rp5,936m

27www.banpu.co.th

Indocoal’s financials

Y/E Dec (Btm) 3Q02 2Q02Revenues 1,932 1,911Cost of sales (1,439) (1,420)SG&A (277) (120)Royalty (183) (193)Interest expenses (68) (84)Net operating profit (35) 94FX translation (149) 572Mining property (47) 57Minority interest 0 0Income tax 38 (88)Reported net profit (193) 635

28www.banpu.co.th

TECO’s financials

Y/E Dec (Btm) 3Q02 2Q02

Revenues 2,376 1,767

Cost of sales (1,723) (1,423)

SG&A (33) (34)

Swap cost (123) (112)

Interest expenses (113) (118)

Net operating profit 384 78

FX translation (438) 481

Reported net profit (54) 559

29www.banpu.co.th

BLCP development

�1,434MW coal-fired power plant (50% held by Banpu and CLP Powergen Southeast Asia, 47 km transmission line)

�25-year PPA with EGAT, the national utility

�Environmental approvals in place for the industrial location

�25-year Coal Supply agreement with coal source portfolio

�Financial close expected by July 2003