56

Olefins Refinery Aromatics Polymers HVS High Volume Specialties EO Based Performance Green Chemicals Services and Others Investors Presentation NDR in Malaysia with CIMB January 20, 2014

Olefins Refinery

Aromatics Polymers

HVS High

Volume Specialties

EO Based Performance

Green Chemicals

Services and Others

Investors Presentation

NDR in Malaysia with CIMB January 20, 2014

Disclaimer

This presentation includes forward-looking statements that are subject to risks and uncertainties, including

those pertaining to the anticipated benefits to be realized from the proposals described herein. This

presentation contains a number of forward-looking statements including, in particular, statements about future

events, future financial performance, plans, strategies, expectations, prospects, competitive environment,

regulation and supply and demand.

PTTGC has based these forward-looking statements on its views with respect to future events and financial

performance. Actual financial performance of the entities described herein could differ materially from that

projected in the forward-looking statements due to the inherent uncertainty of estimates, forecasts and

projections, and financial performance may be better or worse than anticipated. Given these uncertainties,

readers should not put undue reliance on any forward-looking statements.

Forward-looking statements represent estimates and assumptions only as of the date that they were made.

The information contained in this presentation is subject to change without notice and PTTGC does not

undertake any duty to update the forward-looking statements, and the estimates and assumptions associated

with them, except to the extent required by applicable laws and regulations.

2

Agenda

PTTGC Business Overview

Strategy and Execution

Recent Happenings

9M/13 Operating Results

Market Outlook

3

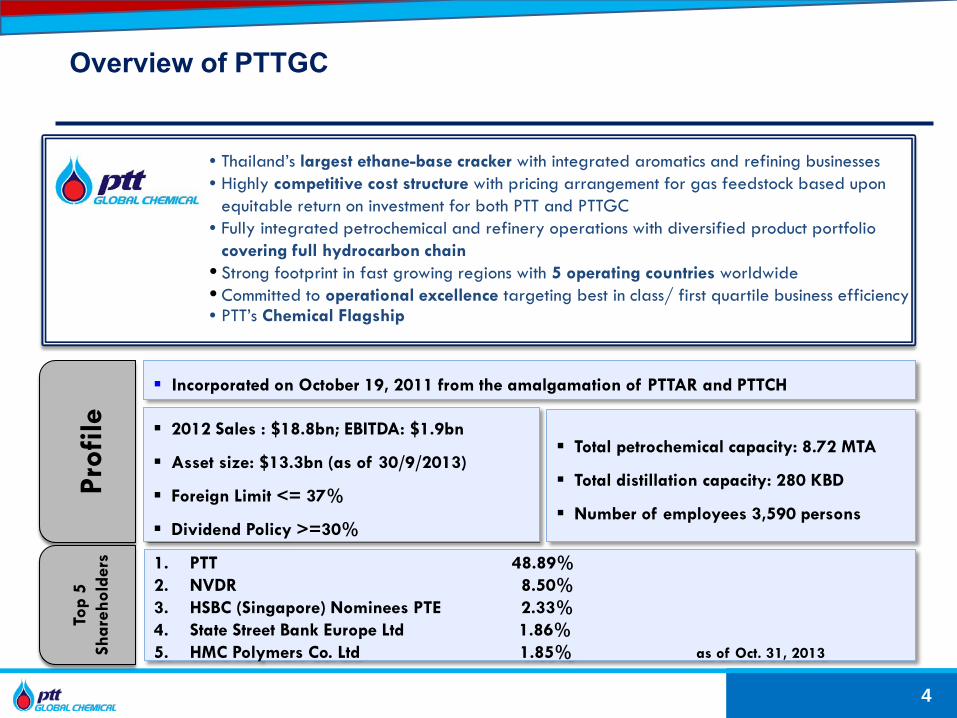

• Thailand’s largest ethane-base cracker with integrated aromatics and refining businesses • Highly competitive cost structure with pricing arrangement for gas feedstock based upon

equitable return on investment for both PTT and PTTGC • Fully integrated petrochemical and refinery operations with diversified product portfolio

covering full hydrocarbon chain • Strong footprint in fast growing regions with 5 operating countries worldwide • Committed to operational excellence targeting best in class/ first quartile business efficiency • PTT’s Chemical Flagship

Prof

ile Incorporated on October 19, 2011 from the amalgamation of PTTAR and PTTCH

Total petrochemical capacity: 8.72 MTA

Total distillation capacity: 280 KBD

Number of employees 3,590 persons

2012 Sales : $18.8bn; EBITDA: $1.9bn

Asset size: $13.3bn (as of 30/9/2013)

Foreign Limit <= 37%

Dividend Policy >=30%

Top

5 Sh

areh

olde

rs

1. PTT 48.89% 2. NVDR 8.50% 3. HSBC (Singapore) Nominees PTE 2.33% 4. State Street Bank Europe Ltd 1.86% 5. HMC Polymers Co. Ltd 1.85% as of Oct. 31, 2013

Overview of PTTGC

4

Flexible Feedstock and Highly Competitive Cost Structure

5

Flexible Feedstock and By-Product Enhancement

PTTGC's refinery (145 KBD) is one of the most complex refineries in Thailand, with Nelson Index of 10.17 and refining capacity accounting for 13% of country’s total capacity

Value enhancement from by-product exchange among Olefins, Aromatics and Refinery units highlights operational integration and efficiency:

- CR from Aromatics units sent to Refinery to produce middle distillate

- Pygas from Olefins unit sent to Aromatics for BTX - Offgas from Refinery sent to Cracker for olefins

products

Feedstock Supply Product Marketing

Refinery

Aromatics

Olefins / Polymers

Others

Condensate

Crude Oil

Others

Ethane, Propane, LPG

C5-C9

C10-C25

C2-C4

Olefins

100% Polymers (1)

46% (2)

54% (2)

Feedstock Supply Commercial Agreements Product Marketing Commercial Agreements

Customers

Others

70% (2)

30% (2)

103

318

799 824 830 883

951 967 1,006

-

200

400

600

800

1,000

1,200

MDEEthane

NAMEthane

NEA LPG NAMNaphtha

MDE LPG MDENaphtha

NEANaphtha

SEANaphtha

WEPNaphtha

Global Ethylene Cash Cost by Region

USD/Ton

2012E (3)

1. PTT owns 50%, PTTGC and IRPC each owns 25% in PTTPM. 2. FY12

(5)

Source: IHS (formerly CMAI) as of July 2012. Note: MDE = Middle East, NAM = North America, NEA = Northeast Asia, SEA = Southeast Asia, WEP = Western Europe.

3. PTTGC ethylene cash cost is based on Company estimate and ethane cracker only. 2012 PTTGC cash cost takes into account the effect of the renewal of gas price agreement. 4. MDE cash costs are average values of Iran and Saudi Arabia.

(5) (4)

Natural Gas

Crude Palm Oil

Crude

Condensate

Cracker

Aromatics Plants

Refinery

Ethylene

HDPE

LLDPE

LDPE

MEG

Propylene

Oleochemicals

Paraxylene

Benzene

PTAPET Fiber/Resin

EO

Ethanolamine

Ethoxylate

Cyclohexane

CumenePhenol

Acetone

EB/SM

PS

BPA

Methyl Ester(B-100)

PC

Caprolactam Nylon 6

Fatty Alcohol

MMA PMMA

Epoxy Resins

ABS

SBR

PP

PTT Phenol

Petroleum Products- LPG- Reformate- Light Naptha- Jet Fuel- Diesel- Fuel Oil

Reformate, Heavy

Naphtha

Pygas

Condensate Residue,

Hydrogen

Light Naphtha

C3,C4

OffGas Mixed C4 Butadiene

PO

PUTDI/HDI

Toluene

Polyols

Orthoxylene

Cracker Bottom,

Hydrogen

PA Plasticizer

1. PTTGC does not currently produce these products.

REFINERY & SHARED FACILITIES AROMATICS OLEFINS POLYMERS EO-BASED

PERFORMANCE GREEN CHEMICALS HIGH VOLUME SPECIALTIES

Feedstock Upstream Intermediates Downstream Proximity to Suppliers and Customers

Exchange Stream Products By-Products

Potential Product Opportunities (1)

Petroleum Products - LPG - Reformate - Light Naphtha - Jet Fuel - Diesel - Fuel Oil

Fully Integrated Petrochemical and Refinery Operations with Diversified Product Portfolio

6

Agenda

PTTGC Business Overview

Strategy and Execution

Recent Happenings

9M/13 Operating Results

Market Outlook

7

PTTGC’s Strategies Overview

8

Increasing distance from core

Business As Usual

• Operational

Excellence

• Marketing

Excellence

• Synergy Project

Excellence

• Debottlenecking /

Expansion

New Geography

New Products

• PU Chain

• PC Chain

• BV Derivatives

• Nylon 6,6

• PMMA

• Bio-Plastic

• VAO

Growth initiatives

Core uplift initiatives

REF ARO OLE

POL EOB GRN XVS

26 Plants Globally

ROIC 12% ROIC Uplift 2% 14% ROIC >14%

One Step Adjacency Green Business

“To be a Leading Chemical Company for Better Living”

9

Continues to Strive for Strong Profitable Growth

~800-900

~620-650

Green

563

Actual2012

Target2017

Target2022

Expected EBITDA BenefitUplift 15-30%

Phase 1 : Foundation for Growth Phase 2: The Growth Mode

Green

HVS

New Global Hub

Debottleneck

Synergy Project Excellence

Operational Excellence Marketing Excellence Capital Expenditure Excellence

We aim to grow ~5 percent p.a. in the next ten years

Sales in THB Bn Based on constant Dubai crude year 2012 at USD 109 per bbl

Execution Led by a Well Defined Strategy

10

Operational Excellence

Marketing Excellence

Synergy Project Excellence

Debottleneck CAPEX

Excellence

Reliability improvement

Energy efficiency improvement

Cost reduction

Product development

Customer/Portfolio mgmt

Strategic pricing

Product upgrade

Cost saving from share tank and facility

Steam Cost reduction

BV Project

Quench Tower

PX expansion

PTTPE Cracker and Polymer Plants Debottleneck

Capital Project Management

Engineering

Procurement

Construction

Project Mgmt.

1 2 3 4 5

EBITDA Uplift (USD mn)

Target EBITDA Uplift of Excellence Programs and Synergy Projects 2013-2017

28 83 87 91 91 113

79 81 83 85 36 83

149 149 149 43

75 108 108

177

289

392 431 433

2013 2014 2015 2016 2017

Operational Excellence Marketing Excellence Synergy Debottleneck (exclude PE expansion)

* Debottleneck EBITDA Uplift includes 1Q/14 BV project starts up 3Q/15 TOCGC Plant Improvement Project 4Q/15 PX expansion starts up

*

Excellence Programs 1H/13 9M/13 Target FY13

1. Operational excellence 1.1 7.9 28

- Reliability improvement - Energy efficiency improvement - Cost reduction

2. Marketing excellence 84.6 111.3 113

- HVP Sales Performance exceeded target - 7 New HVP Grades and 3 New Commodities Grades - Exported Mixed C4 - Export PE to alternative markets ie. South Africa3. Synergy projects 10.0 17.1 36

- EBITDA uplift in 3Q/13 was mainly contributed from C3/C4 Stream and 3 Streams (Heavy Gasoline, LCB, and CB) - Heavy gas (Offgas) - Construction Progress at 27.5% (End Sep) - Pure H2 via New PSA - Construction Progress at 83.2% (End Sep)4. Opportunity Synergy Benefits 0.0 13.1 0

- Biodiesel Export to China (B-100 from TOL blend with Diesel from Refinery) - Due to I-4/1 TA, transfer excess offspec Raw Pygas (normally flare) to upgrade at ARO2 - Due to I-4/1 TA, transfer excess offspec C3C4 from PTTPE Cracker to Refinery C3C4 pool for blending Total 95.7 149.4 177.0

Update Excellence Programs

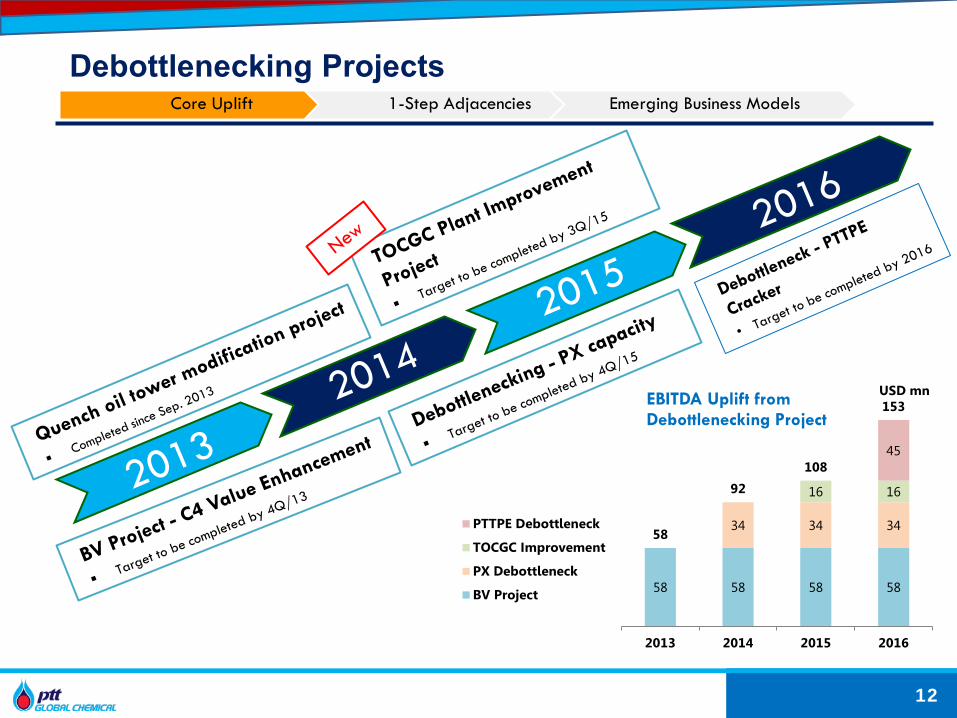

11

Core Uplift 1-Step Adjacencies Emerging Business Models

58 58 58 58

34 34 34

16 16

45

153

108

92

58

2016 2015 2014 2013

USD mn

PTTPE Debottleneck

TOCGC Improvement

PX Debottleneck

BV Project

Debottlenecking Projects

12

Core Uplift 1-Step Adjacencies Emerging Business Models

EBITDA Uplift from Debottlenecking Project

Quench oil tower modification project

13

Quench Oil Tower Modification project at I4-1 olefins plant

• To reduce naphtha to gas portion in I4-1 mixed feed cracker

Naphtha : Gas

From 0.95 : 1.0

To 0.60 : 1.0

• Project completed during I4-1 plant turnaround in Aug-Sept 2013

• Passed Operational Test

Core Uplift 1-Step Adjacencies Emerging Business Models

Status Completed

CAPEX 3 MUSD

Vapor Flute

C4 Value Enhancement (BV Project) BV Project

14

BV Project will enhance PTTGC’s C4 value chain by upgrading to Butadiene and Butene-1, which will pave a way towards Butadiene derivatives

Construction completed, now in test run period

C4 From

PTTGC’s Cracker

Butadiene Plant Synthetic Rubber

Customer 90% Domestic: 10% Export

Nameplate Capacity 75 KTA of Butadiene 25 KTA of Butene-1

Technology License ABB LUMMUS

Project Management Consulting PTTME

EPC Contractor Chiyoda (Thailand)

CAPEX 262 MUSD

EBITDA Uplift 58 MUSD/Year

Target Completed 4Q/13

Direction forward • Expand into Synthetic rubber business by using

butadiene from PTTGC and from JV Investment Plant

PTTGC LLDPE Plant

Butene -1

Butadiene

Core Uplift 1-Step Adjacencies Emerging Business Models

TOCGC Plant Improvement Project

15

Core Uplift 1-Step Adjacencies Emerging Business Models

EOE Capacity 336 KTA + Additional Capacity

90 KTA

Plant improvement to expand EOE capacity

• Improve catalyst usage to enhance production yield and also reduce CO2 emission.

• Increases EOE capacity by 90 KTA from 336 KTA to 426 KTA

• Additional EOE capacity will improve capacity of EO/EG depending on production mode.

• Progress: Construction

Purified EO

Ethylene Glycol (EG)

Additional Capacity 90 KTA of EOE

EPC Contractor Samsung Engineering

CAPEX 94.2 MUSD

EBITDA Uplift 16 MUSD/Year

Target Completion 3Q/15

PX Expansion Project

16

Core Uplift 1-Step Adjacencies Emerging Business Models

Increase PX and BZ capacity at ARO#2

• Board approved and EPC Awarded • Progress : construction

PAREX

Additional Capacity 115 KTA of PX 35 KTA of BZ

EPC Contractor PTTME and SK Engineering

CAPEX 128.8 MUSD

EBITDA Uplift 34 MUSD/year

Target Completion 4Q/15 during ARO2 TA period

Aromatics (KTA) Existing Debot. 2015 Total after Debot.

Paraxylene 655 +115 770

Benzene 355 +35 390

Orthoxylene 0 +20 20

PTTPE Cracker Debottlenecking

17

Core Uplift 1-Step Adjacencies Emerging Business Models

PTTPE debottlenecking with additional capacity of 12%

Downstream debottleneck expansion to capture fully-integrated margin by converting additional ethylene into downstream products

Adding 1 furnace to PTTPE cracker The additional volume of gas feedstock from

PTT will be ethane : LPG or 60 : 40 Progress: basic engineering package

Additional Capacity of PTTPE Cracker

12% Increase

CAPEX 285 MUSD

Expected IRR 17%

Target Completion 2016

Additional Olefins

Capacity

Possible value added downstream • m-LLDPE • LLDPE Expansion

Phenol 2 Project “Road to PC/Nylon”

18

Phenol 2 Project will capture longer value chain of benzene and propylene. Pave a way towards downstream phenol derivatives. Financing: Project Financing Scheme, D/E 2:1 Progress: Construction

Nameplate Capacity 250 KTA of Phenol 155 KTA of Acetone

Technology License UOP

Project Management Consulting

Bechtel

EPC Contractor POSCO CAPEX 348 MUSD Expected IRR 17%

Target Completed 3Q/15

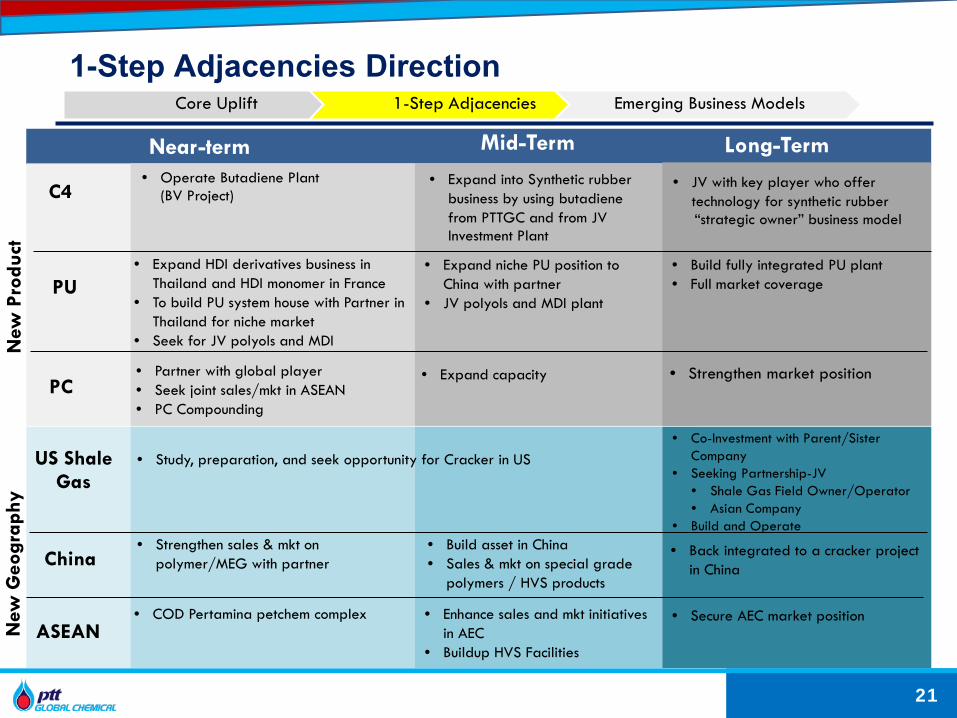

Our 1-Step Adjacencies Direction • Partner with global player • Seek joint sales/mkt in ASEAN • PC Compounding

Phenol Chain

Core Uplift 1-Step Adjacencies Emerging Business Models

JV with PERTAMINA

19

Competitive advantage over size and vicinity

World-scale integrated petrochemical complex covering upstream to downstream Pave a way towards HVS product offering Estimated investment of USD 4-5 bn Expected COD 2018

Updated Progress • On December 10, 2013 PTTGC and Pertamina:

• Signed Manufacturing Joint Venture – HOA which includes a world scale cracker and downstream products complex, with no investment in the refinery complex.

• Entered into a marketing and trading JV to initially conduct polymer products marketing and distribution throughout Indonesia.

Core Uplift 1-Step Adjacencies Emerging Business Models

Pieces of Jigsaw to our downstream aspiration

20

Vencorex to HDI to system house Expand HDI derivatives business in Thailand and HDI monomer in

France Restructure Business in France to enhance its competitiveness. Build PU system house with Partner in Thailand for niche market Seek for JV polyols and MDI

Sinochem to secure access to China downstream market Signed MoU to jointly explore potential collaboration e.g., PU and

PC chains and Bio-based chemicals Strengthen sales & market in China

Petronas to expand into PC and PO chain Expand downstream product portfolio (PC and PO chain) and

support HVS strategic initiative Signed HoA with Petronas and Itochu, target completion by 2017 for

feasibility study Estimated Investment of USD 2 bn, PTTGC expects to contribute

25% of the equity component

Core Uplift 1-Step Adjacencies Emerging Business Models

New

Pro

duct

N

ew G

eogr

aphy

C4

PU

PC

• Expand into Synthetic rubber business by using butadiene from PTTGC and from JV Investment Plant

Near-term

• JV with key player who offer technology for synthetic rubber

“strategic owner” business model

Mid-Term Long-Term

• Expand HDI derivatives business in Thailand and HDI monomer in France

• To build PU system house with Partner in Thailand for niche market

• Seek for JV polyols and MDI

• Expand niche PU position to China with partner

• JV polyols and MDI plant

• Build fully integrated PU plant • Full market coverage

• Partner with global player • Seek joint sales/mkt in ASEAN • PC Compounding

• Expand capacity • Strengthen market position

ASEAN

China

US Shale Gas

• Study, preparation, and seek opportunity for Cracker in US • Co-Investment with Parent/Sister

Company • Seeking Partnership-JV

• Shale Gas Field Owner/Operator • Asian Company

• Build and Operate

• COD Pertamina petchem complex • Enhance sales and mkt initiatives in AEC

• Buildup HVS Facilities

• Secure AEC market position

• Strengthen sales & mkt on polymer/MEG with partner

• Build asset in China • Sales & mkt on special grade

polymers / HVS products

• Back integrated to a cracker project in China

1-Step Adjacencies Direction

21

Core Uplift 1-Step Adjacencies Emerging Business Models

• Operate Butadiene Plant (BV Project)

Biochemical to Support Future Growth

22

Core Uplift 1-Step Adjacencies Emerging Business Models

Applications PTTGC holds 50% in NatureWorks. A manufacture of polylactic acid (PLA) and lactides, plant-based biopolymers used to manufacture plastics and fibers with world scale PLA capacity of 150,000 ton/year. Planned to build second plant

potentially in Asia Studied the possibilities to use

alternative feedstock

PTTGC holds 84.77% in Myriant Corporation. An R&D based company with proven technology platform. In April 2013, Myriant Corporation had completed the

construction of a 14,000 ton/year Succinic Acid Plant in Louisiana State and is currently commissioning.

USD 4.5 Bn

USD 2 Bn from Debt Financing

USD 2.5 Bn from Cash Flows from Operation

CAPEX to Support Growth Approved and Uncommitted CAPEX Plan for year 2013 - 2017

23

31%

64%*

5% Core Uplift

1 Step Adjacencies

Green

USD 4.5 Bn Uncommitted CAPEX

USD 1 Bn secured from USD Bond Issued in Sep. 2012

Agenda

PTTGC Business Overview

Strategy and Execution

Recent Happenings

3Q/13 Operating Results

Market Outlook

24

Award and Recognition

25

Mission to be Continued

Bowon Vongsinudom

President and CEO

26

PTTGC’s Top Management Team’s Commitment

New Organization Structure to Support Growth

27

PTTGC Board of Directors

VP – Internal Audit

EVP – Polymers Business

Unit

SVP - High

Volume Specialties Business

Unit

EVP – EO Based

Performance

Business Unit

EVP – Green

Chemicals Business

Unit

EVP – Marketing, Commercial and Supply

EVP – Finance and

Accounting

EVP – Corporate Strategy

EVP – Strategic

Execution and Excellence

EVP – Corporate

Affairs

EVP – Organizational Effectiveness

EVP – Project Executive Director

Head – Science and Innovation

EVP – GPC Olefins

EVP – GPC

Refinery and

Shared Facilities

EVP – GPC

Aromatics

EVP – Engineering

and Maintenance

SVP – Quality, Safety,

Occupational Health and

Environment

Audit Committee CG Committee Risk Management Committee

Nomination and Remuneration Committee

President and CEO

COD – Down Stream Petrochemical Business COU – Up Stream Petrochemical Business

Agenda

PTTGC Business Overview

Strategy and Execution

Recent Happenings

9M/13 Operating Results

Market Outlook

28

What happens in 2013?

29

US slowly recover

Unplanned S/D LDPE -

PTTGC’s Operating Performance

Petchem market stronger

Lower F/S supply (GSP 5) -

China econ slowdown

-

Oil price Fluctuation + Fluctuation THB -

Euro crisis -

+ +

Oil spill & rehabilitation -

Key Financial Highlights

30

45,

642

41,

106

44,

273

54,

423

57,

168

39,

886

40,

609

42,

569

47,

645

56,

993

11% 10%

11% 10%

10%

0%

2%

4%

6%

8%

10%

12%

-

20,000

40,000

60,000

80,000

100,000

120,000

9M/11 9M/12 9M/13 FY 11* FY 12

THB mn

EBITDAAdjusted EBITDAAdjusted EBITDA Margin (RHS)

25,981 24,239 25,856 30,033 34,001

5.77 5.38 5.73 6.66

7.50

-

2.00

4.00

6.00

8.00

-

10,000

20,000

30,000

40,000

9M/11 9M/12 9M/13 FY 11* FY 12

THB mn Net Profit EPS (Baht/Share) (RHS)

374,188 418,216 394,590

500,305 562,811

-

100,000

200,000

300,000

400,000

500,000

600,000

9M/11 9M/12 9M/13 FY 11* FY 12

THB mn Sales Revenue

Dividend - Solid Payout Ratio FY11 FY 12 6M/13

EPS (THB/Share) 6.66 7.50 3.60

Dividend (THB/Share) 2.98 3.4 1.62

Payout Ratio (%) 45% 45% 45%

* Proforma Statements

Dividend Policy: As least 30% of Net Profit

Refinery 8%

Aromatics 24%

Olefins and

Derivative 61%

Green 3% HVS

1% Others 2.96%

Refinery 43%

Aromatics 22%

Olefins and Derivative

23%

Green 5%

HVS 7%

Others 0.05%

31

Adjusted EBITDA Margin % by Core BU

Segmental Results Olefins and Olefins Derivatives Business contributed greatly to EBITDA

9M/13 Revenue Breakdown (%)*

9M/13 Adjusted EBITDA Breakdown (%)*

THB 42.4 Bn

THB 395 Bn

Refinery 16%

Aromatics 16%

Olefins and

Derivative

56%

Green 3%

HVS 3% Others

4.94%

Refinery 48%

Aromatics

20%

Olefins and

Derivative

21%

Green 5%

HVS 5%

Others 0.98%

FY12 Revenue Breakdown (%)

FY12 Adjusted EBITDA Breakdown (%)

THB 57 Bn

THB 563 Bn

*Refinery T/A in 1Q/13

Unit:% FY 12 9M/13Refinery 3 2Aromatics 8 11Olefins & Derivatives

27 28

Green 5 7HVS 7 2PTTGC 10 11

5.2

16.4

8.4 9.6 14.8 14.3

7.7 11.6

0.5

31.4

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

PTTGC PPCL Others

35 39

240 226

101 98

60 50

238 237

137 121

61 55

Strong Financial Position

32

Key Financial Ratios

As of Dec 31, 2012 As of Sep. 30, 2013

THB 413 Bn THB 436 Bn

Cash + ST Investment

CA

PPE

Non CA

Share holders’ Equity

IBD

Liab.

Statements of Financial Position Interest Rate Currencies

68 % Fixed 56 % THB

32 % Float 44 % USD & Others

Loan Type

• Cost of long term debts ~ 5.0%

(Include W/H Tax)

• Average loan life after refinancing -

5.0 Years

Treasury policy Net IBD to Equity ratio of ≤ 0.7x Net IBD to EBITDA ratio of ≤ 2.4x

Maturity of Financial Debt* as at 30 Sep., 2013

THB 121 Bn

THB Bn

ST Loan 3%

LT Loan 35% Deben

ture 62%

* After Refinance

1.34 1.06 0.98

1.18

0.32 0.25 0.26 0.30

0.0x0.2x0.4x0.6x0.8x1.0x1.2x1.4x1.6x

31 Dec.12

31 Mar.13

30 Jun.13

30 Sep.13

Net IBD / EBITDANet IBD/Equity

16.15% 16.39% 17.09% 16.11%

10.43% 11.13% 11.83% 10.50%

5%

10%

15%

20%

31 Dec. 1231 Mar. 1330 Jun. 13 30 Sep. 13

ROE ROA

Agenda

PTTGC Business Overview

Strategy and Execution

Recent Happenings

3Q/13 Operating Results

Market Outlook

33

Key Market Trends in 2014

34

Dubai Crude oil prices is expected to average 102 USD/BBL in 2014, softening from average 105 USD/BBL in 2013 due to addition Non-OPEC supply.

World Oil Demand should grow around 1.1 MMBD in 2014, while net additional of 2.25 MMBD refinery capacities will be added.

GRM should be pressure from these addition capacities.

Source: JBC, Nov. 2013

IEA Demand(mbd)

Growth (mbd)

2012 89.98 +1.02

2013 91.17 +1.19

2014 92.37 +1.20

EIADemand(mbd)

Growth (mbd)

2012 89.17 +0.87

2013 90.38 +1.21

2014 91.59 +1.21

Source: EIA, STEO Jan. 14

Source: IEA, OMR Dec. 13

OPECDemand(mbd)

Growth (mbd)

2012 88.90 +0.80

2013 89.80 +0.90

2014 90.80 +1.00

Source: OPEC, OMR Dec. 13

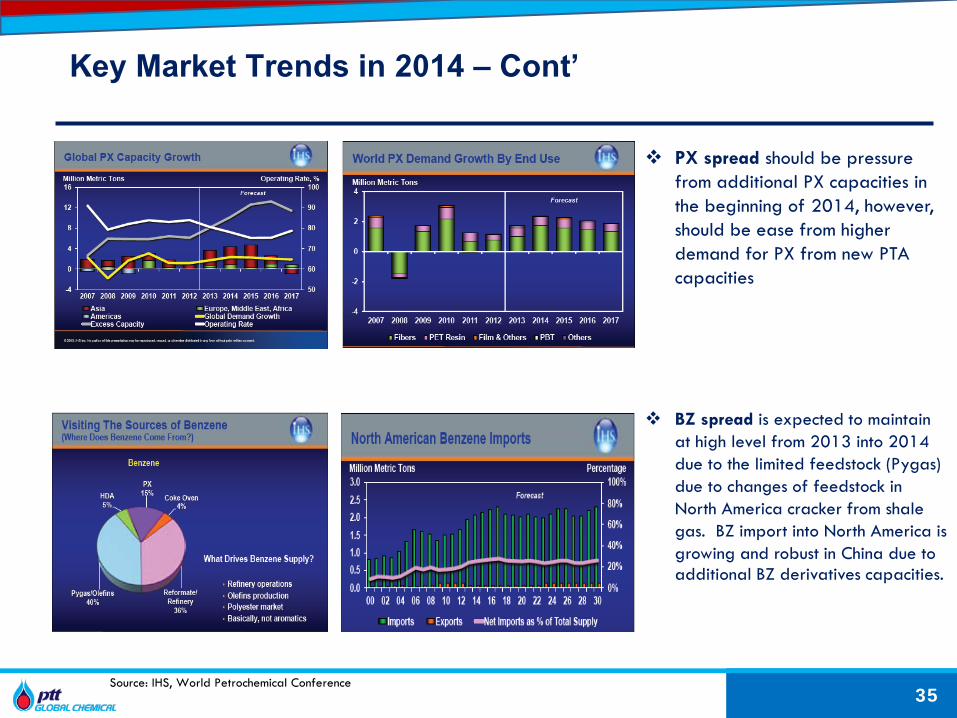

Key Market Trends in 2014 – Cont’

35

PX spread should be pressure from additional PX capacities in the beginning of 2014, however, should be ease from higher demand for PX from new PTA capacities

BZ spread is expected to maintain at high level from 2013 into 2014 due to the limited feedstock (Pygas) due to changes of feedstock in North America cracker from shale gas. BZ import into North America is growing and robust in China due to additional BZ derivatives capacities.

Source: IHS, World Petrochemical Conference

Key Market Trends in 2014 – Cont’

36

Global Ethylene supply & demand is expected to be tight in 2014 even though new capacities are being add into the market where global operating rate to be flat YoY at 87%

Global PE demand is still growing at 4.6% per year

HDPE price is expected to remain at high level from improving economic and less supply coming in 2014

Source: IHS, World Petrochemical Conference

37

For further information & enquiries, please contact our Investor Relations Team at [email protected]

Thank You

1 Thitipong Jurapornsiridee VP - Corporate Finance & IR [email protected] +662-265-85742 Puvadol Vasudhara IR Manager [email protected] +662-140-87123 Panugorn Puengpradit IR Analyst [email protected] +662-140-87144 Prang Chudasring IR Analyst [email protected] +662-265-83275 Chutima Jarikasem IR Coordinator [email protected] +662-140-8713

Agenda

Appendix

3Q/13 Detail Performance

Product Demand/Supply

The 3 Incidents in 2013

38

70

80

90

100

110

120

130

Jan-

12Fe

b-12

Mar

-12

Apr-

12M

ay-1

2Ju

n-12

Jul-1

2Au

g-12

Sep-

12O

ct-1

2N

ov-1

2D

ec-1

2Ja

n-13

Feb-

13M

ar-1

3Ap

r-13

May

-13

Jun-

13Ju

l-13

Aug-

13Se

p-13

Oct

-13

Dubai

3Q/13 Business Environment and Operations Recap

39

THB/USD

USD/BBL

116.1 106.4 106.3 107.4 108.2 100.7 106.3 1Q/12 2Q/12 3Q/12 4Q/12 1Q/13 2Q/13 3Q/13

27.00

28.00

29.00

30.00

31.00

32.00

33.00

Jan-

12Fe

b-12

Mar

-12

Apr-

12M

ay-1

2Ju

n-12

Jul-1

2Au

g-12

Sep-

12O

ct-1

2N

ov-1

2De

c-12

Jan-

13Fe

b-13

Mar

-13

Apr-

13M

ay-1

3Ju

n-13

Jul-1

3Au

g-13

Sep-

13O

ct-1

3N

ov-1

3

31.0 31.3 31.3 30.7 29.8 29.9 31.51Q/12 2Q/12 3Q/12 4Q/12 1Q/13 2Q/13 3Q/13

Unrests in several oil producing countries supported Dubai crude price to average at 106 USD/BBL in 3Q/13, increased 6% from 101 USD/BBL in 2Q/13.

Rising oil price contributed to a stock gain&NRV of Baht 3,768 mn

Baht depreciated from US FED’s signal on QE tapering from avg. 29.9 Baht/USD in 2Q/13 to 31.5 Baht/USD in 3Q/13

Higher crude price pushes products prices up while mix margin among products

Most Products Price/spreads increased

Diesel-Dubai 17.32 USD/BBL +3% QoQ -18% YoY

PX-Cond 511 USD/Ton -5% QoQ +20% YoY

HDPE 1,489 USD/Ton +3% QoQ +11% YoY

MEG 1,143 USD/Ton -3% QoQ +7% YoY

Overall utilization rate of major businesses

3Q/12 2Q/13 3Q/13Refinery 101% 63% 98%Aromatics 90% 84% 91%Olefins 91% 93% 75%Polymers 102% 90% 88%MEG 93% 100% 92%Green - FA 116% 112% 139%Green - ME 84% 106% 129%Phenol 128% 127% 124%

3Q/13 Key Financial Highlights

40

(Unit: Million Baht) 3Q/2013 3Q/2012

(Restate) 2Q/2013

YoY

% + /(-)

QoQ

% + /(-)

9 Month

Ending

June 30, 2013

9 Month

Ending

June 30, 2012

YoY

% + /(-)

Sale Revenue 141,394 145,309 111,887 -3% 26% 394,590 418,216 -6%

EBITDA 16,388 18,581 11,466 -12% 43% 44,273 41,106 8%

EBITDA Margin (%) 12% 13% 10% -1% 1% 11% 10% 14%

Net Profit 9,610 12,879 4,172 -25% 130% 25,857 24,239 7%

Earnings Per Share 2.13 2.86 0.93 -26% 129% 5.73 5.38 7%

Adjusted EBITDA 12,619 15,306 12,888 -18% -2% 42,569 40,609 5%

Adjusted EBITDA Margin (%) 9% 11% 12% -2% -3% 11% 10% 1%

9M/13 Sales Split Domestic : Export Volume

11% 74%

85% 38%

91% 64%

76%

89% 26%

15% 62%

9% 36%

24%

0% 20% 40% 60% 80% 100%

Phenol & BPAGreen

EO-basedPolymers

OlefinsAromatics

Refinery

Domestic Export

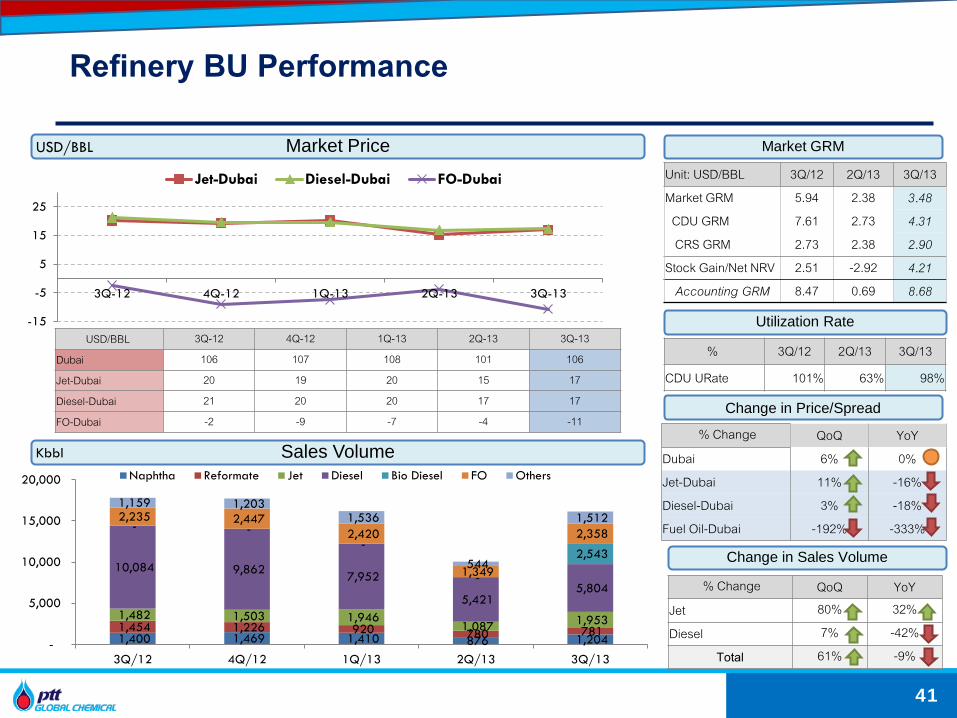

Refinery BU Performance

41

Market Price

-15

-5

5

15

25

3Q-12 4Q-12 1Q-13 2Q-13 3Q-13

Jet-Dubai Diesel-Dubai FO-Dubai

Sales Volume

USD/BBL 3Q-12 4Q-12 1Q-13 2Q-13 3Q-13

Dubai 106 107 108 101 106

Jet-Dubai 20 19 20 15 17

Diesel-Dubai 21 20 20 17 17

FO-Dubai -2 -9 -7 -4 -11

1,400 1,469 1,410 876 1,204 1,454 1,226 920 780 781 1,482 1,503 1,946

1,087 1,953

10,084 9,862 7,952

5,421 5,804

- - -

-

2,543

2,235 2,447 2,420

1,349

2,358

1,159 1,203 1,536

544

1,512

-

5,000

10,000

15,000

20,000

3Q/12 4Q/12 1Q/13 2Q/13 3Q/13

Naphtha Reformate Jet Diesel Bio Diesel FO Others

Market GRM

Change in Price/Spread

Change in Sales Volume

Utilization Rate

% 3Q/12 2Q/13 3Q/13

CDU URate 101% 63% 98%

% Change QoQ YoY

Dubai 6% 0%

Jet-Dubai 11% -16%

Diesel-Dubai 3% -18%

Fuel Oil-Dubai -192% -333%

% Change QoQ YoY

Jet 80% 32%

Diesel 7% -42%

Total 61% -9%

USD/BBL

Kbbl

Unit: USD/BBL 3Q/12 2Q/13 3Q/13

Market GRM 5.94 2.38 3.48

CDU GRM 7.61 2.73 4.31

CRS GRM 2.73 2.38 2.90

Stock Gain/Net NRV 2.51 -2.92 4.21

Accounting GRM 8.47 0.69 8.68

Aromatics BU Performance

42

Market Price

800

1,000

1,200

1,400

1,600

1,800

3Q-12 4Q-12 1Q-13 2Q-13 3Q-13

Naphtha Condensate PX BZ

Sales Volume

P2F

Change in Price/Spread

Change in Sales Volume

Utilization Rate

% Change QoQ YoY

Condensate 7% 1%

PX-Cond -5% 20%

BZ-Cond -21% 27%

% Change QoQ YoY

BTX 2% -5%

% 3Q/12 2Q/13 3Q/13

BTX U-Rate 90% 84% 91%

USD/Ton 3Q/12 2Q/13 3Q/13

Market P2F 243 325 260

Stock Gain 41 -46 84

210 193 181 213 189

330 324 318 291 325

208 248 216 189 270

102 118 109 96

93

-

200

400

600

800

1,000

3Q/12 4Q/12 1Q/13 2Q/13 3Q/13

Benzene Paraxylene Ref+LN Other By-Products

USD/Ton

USD/Ton 3Q-12 4Q-12 1Q-13 2Q-13 3Q-13

PX- Cond 426 605 669 539 511

BZ-Cond 259 431 430 415 329

KTon

*Benzene = BZ+Cyclohexane Paraxylene = PX + Other BTX

Olefins and Olefins Derivatives BU Performance

43

800

1,000

1,200

1,400

1,600

3Q-12 4Q-12 1Q-13 2Q-13 3Q-13

Naphtha HDPE LLDPE LDPE MEG

Market Price

Sales Volume

188 169 200 218 129 198 203 216 193 208

111 117 102 70 119 96 63 75

71 25

91 101 83 104 95

404 383 393 334 352

0100200300400500

3Q-12

4Q-12

1Q-13

2Q-13

3Q-13

Olefins HDPE LLDPE LDPE MEG Total PE

QoQ YoYEthylene 5% 10%HDPE 3% 11%LLDPE 4% 11%LDPE 9% 18%MEG -3% 7%

QoQ YoYOlefins 41% -32%HDPE 8% 5%LLDPE 70% 7%LDPE -66% -74%MEG -8% 5%

Change in Price

Utilization

Change in Sales Volume

USD/Ton

USD/Ton 3Q-12 4Q-12 1Q-13 2Q-13 3Q-13

Naphtha 915 944 961 858 920

HDPE 1,343 1,393 1,482 1,443 1,489

LLDPE 1,341 1,399 1,477 1,433 1,490

LDPE 1,327 1,369 1,459 1,444 1,569

MEG 1,065 1,247 1,282 1,173 1,143

KTon

3Q/12 2Q/13 3Q/13

Olefins 91% 93% 75%

HDPE 100% 96% 106%

LLDPE 113% 72% 113%

LDPE 113% 99% 5%

MEG 93% 100% 92%

Phenol Performance

44

Market Price

Sales Volume

Change in Spread

Utilization

Change in Sales Volume

100

150

200

250

300

3Q-12 4Q-12 1Q-13 2Q-13 3Q-13

Phenol-BZ BPA-Phenol

USD/Ton 3Q-12 4Q-12 1Q-13 2Q-13 3Q-13

Phenol-BZ 264 165 233 245 244

BPA-Phenol 212 189 268 188 128

34,407 40,988 37,842 34,436 24,099

32,880 34,827

25,128 41,751 44,946

-

20,000

40,000

60,000

80,000

3Q-12 4Q-12 1Q-13 2Q-13 3Q-13

Phenol BPA

3Q/12 2Q/13 3Q/13

Phenol 128% 127% 124%

BPA 36% 116% 116%

QoQ YoY

Phenol-BZ 0% -8%

BPA-Phenol -32% -39%

QoQ YoY

Phenol -30% -30%

BPA 8% 37%

USD/Ton

Ton

3Q/13 Profit and Loss Statement

45

3Q/2012(Restate) 2Q/2013

THB Mn % THB Mn % THB Mn % THB Mn % THB Mn %1 Sales Revenue 145,309 100 111,887 100 141,394 100 (3,915) (3) 29,507 26 2 Feedstock Cost (119,602) (82) (87,594) (78) (116,522) (82) 3,080 3 (28,928) (33)3 Product to Feed Margin 25,707 18 24,293 22 24,872 18 (835) (3) 579 2 4 Variable Cost (5,136) (4) (6,204) (6) (6,211) (4) (1,075) (21) (7) (0)5 Fixed Cost (3,940) (3) (4,163) (4) (4,028) (3) (88) (2) 135 3 6 Stock Gain/(Loss) & NRV 3,275 2 (1,422) (1) 3,768 3 493 15 5,190 365 7 Gain/(Loss) Hedging Commodity (30) (0) 419 0 560 0 590 141 34 8 Other Income 1,311 1 1,362 1 1,235 1 (76) (6) (127) (9)9 SG&A (2,606) (2) (2,819) (3) (3,808) (3) (1,202) (46) (989) (35)

10 EBITDA 18,581 13 11,466 10 16,388 12 (2,193) (12) 4,922 43 11 Depreciation & Amortization (4,328) (3) (4,187) (4) (4,149) (3) 179 4 38 1 12 EBIT 14,253 10 7,279 7 12,239 9 (2,014) (14) 4,960 68 13 Financing Expenses (Net Interest Earned) (1,438) (1) (1,120) (1) (1,144) (1) 294 20 (24) (2)14 FX Gain/(Loss) 746 1 (2,726) (2) (738) (1) (1,484) (199) 1,988 73 15 Shares of gain/(loss)from investments 25 0 (22) (0) (54) (0) (79) (316) (32) (145)16 Corporate Income Tax (562) (0) 509 0 (708) (1) (146) (26) (1,217) (239)17 Net Profit After Income Tax 13,024 9 3,920 4 9,595 7 (3,429) (26) 5,675 145

Portion of Net Profit: 18 Shareholders 12,879 9 4,172 4 9,610 7 (3,269) (25) 5,438 130 19 Minorities 145 0 (252) (0) (15) (0) (160) (110) 237 94

20 Adjusted EBITDA 15,306 11 12,888 12 12,619 9 (2,687) (18) (269) (2)

3Q/2013 YoY QoQ

Note: Adjusted EBITDA = EBITDA – Stock Gain/(Loss) &NRV

9M/13 Profit and Loss Statement

46

THB Mn % THB Mn % THB Mn %1 Sales Revenue 418,216 100 394,590 100 (23,626) (6)2 Feedstock Cost (351,638) (84) (316,235) (80) 35,403 10 3 Product to Feed Margin 66,578 16 78,355 20 11,777 18 4 Variable Cost (12,271) (3) (19,318) (5) (7,047) (57)5 Fixed Cost (10,588) (3) (12,319) (3) (1,731) (16)6 Stock Gain/(Loss) & NRV 498 0 1,703 0 1,205 242 7 Gain/(Loss) Hedging Commodity 367 0 1,127 0 760 207 8 Other Income 4,128 1 3,921 1 (207) (5)9 SG&A (7,605) (2) (9,196) (2) (1,591) (21)

10 EBITDA 41,106 10 44,273 11 3,167 8 11 Depreciation & Amortization (12,290) (3) (12,288) (3) 2 0 12 EBIT 28,816 7 31,985 8 3,169 11 13 Financing Expenses (Net Interest Earned) (4,136) (1) (3,379) (1) 757 18 14 FX Gain/(Loss) 502 0 (1,478) (0) (1,980) (395)15 Shares of gain/(loss)from investments 84 0 (94) (0) (178) (212)16 Corporate Income Tax (618) (0) (1,419) (0) (801) (130)17 Net Profit After Income Tax 24,648 6 25,615 6 967 4

Portion of Net Profit: 18 Shareholders 24,239 6 25,857 7 1,618 7 19 Minorities 409 0 (242) (0) (651) (159)

20 Adjusted EBITDA 40,609 10 42,570 11 1,961 5

YoY9M/12 9M/13

Note: Adjusted EBITDA = EBITDA – Stock Gain/(Loss) &NRV

Agenda

Appendix

3Q/13 Detail Performance

Product Demand/Supply

The 3 Incidents in 2013

47

434 407 402 480 531

467 456 463 345

439 415 420 460 477 486 486

961 858

920 946 928 896 878 872

1,395

1,265 1,322

1,427 1,459

1,363 1,333 1,335 1,306

1,297 1,336

1,367 1,388

1,373 1,363 1,358

0

200

400

600

800

1,000

1,200

1,400

1,600

1Q/13 2Q/13 3Q/13 4Q/13 1Q/14F 2Q/14F 3Q/14F 4Q/14F

Olefins Improved derivatives demand will support to Olefins market

USD/Ton Short-term Price Forecast Short-Term • Olefins prices remain high in 2H-13 due to

improve demand in derivatives markets in line with new PE plants in Asia will come on-stream

• However , For year 2014 the market will be pressured from

1) Additional new supply in Asia (mainly from China)

2) Turnaround and shutdown for maintenance of Asia cracker

3) Global economic outlook show the sign of

recovery Long-term Supply/Demand

Additional (2013-2018) (Unit : MMT)

Supply Demand 40.70 36.04

America24%

Middle East19%

Europe5%

China35%

Other Asia17%

Source: CMAI January 2014

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2013 2014 2015 2016 2017 2018

America Europe Middle East China Other Asia Additional demand

Unit : KMT

Reliance India 1,350 KMT Q1-16 to Q3-16

SINOPEC Wuhan CH 800 KMT Q1-11 to Q3-13

ExxonMobil SG 1,000 KMT Q3-11 to Q2-13

Sichuan PC China 800 KMT Q3-11 to Q4-13

Ilam Iran 458 KMT Q1-15 to Q1-16 OPAL India

1,100 KMT Q1-14 to Q3-14

CNOOC & Shell China 1,000 KMT Q1-16 to Q1-17

Sinopec Zhijin China 300 KMT Q4-14 to Q2-13

48

522 585 568 590

621 595 577 596 516

449 569 599 627 592 560 583

498 586

649 718 758

672 604 626

961 858 920 946 928 896 878 872

1,483 1,443 1,489 1,536 1,550 1,492 1,455 1,468 1,477

1,433 1,489 1,545 1,555 1,488 1,438 1,455 1,459

1,444

1,569 1,664 1,687 1,569 1,482 1,499

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1Q/13 2Q/13 3Q/13 4Q/13 1Q/14F 2Q/14F 3Q/14F 4Q/14F

Short-term Price Forecast USD/Ton Short-Term • PE prices should still be supported from

growing demand in 2014 while new supplies are limited when compared to 2013 which should continue to support HDPE price to remain at high level

Polyethylene The market will be pressured from new supply in the short term

HDPE Long-term Supply/Demand

Additional (2013-2018) (Unit : MMT)

Supply Demand 12.92 11.54

America22%

Middle East24%

Europe8%

China39%

Other Asia7%

-5000

5001,0001,5002,0002,5003,000

2013 2014 2015 2016 2017 2018

America Europe Middle East China Other Asia Additional demand

Unit : KMT

Ilam Iran 300 KMT Q1-14 to Q1-15 SINOPEC Wuhan CH

300 KMT Q1-11 to Q3-13

Saudi Polymers Saudi 550 KMT Q3-11 to Q1-13

BPCL India 110 KMT Q3-13 to Q4-14

OPAL India 350 KMT Q1-13 to Q3-14

Sichuan PC China 300 KMT Q1-12 to Q4-13

Shanxi Coking Corp China 150 KMT Q2-15 to Q2-16

Source: CMAI January 2014 49

LLDPE & LDPE New Capacities and Closures

50 Source: CMAI January 2014

LDPE Long-term Supply/Demand

LLDPE Long-term Supply/Demand

Additional (2013-2018) (Unit : MMT)

Supply Demand 12.05 9.13

Additional (2013-2018) (Unit : MMT)

Supply Demand 5.96 3.80

America20%

Middle East15%

Europe2%

China38%

Other Asia25%

America22%

Middle East30%

Europe18%

China24%

Other Asia8%

-5000

5001,0001,5002,0002,5003,0003,500

2013 2014 2015 2016 2017 2018 America Europe Middle East China Other Asia Additional demand

Unit : KMT

SINOPEC Wuhan China 300 KMT Q1-11 to Q3-13

Sichuan PC China 300 KMT Q3-12 to Q4-13

OPAL India 350 KMT Q1-13 to Q3-14

Yulin Energy China 300 KMT Q2-13 to Q2-14

CNOOC & Shell China 300 KMT Q1-16 to Q1-17

Reliance India 550 KMT Q1-16 to Q4-16

-500

0

500

1,000

1,500

2,000

2013 2014 2015 2016 2017 2018

America Europe Middle East China Other Asia Additional demand

Unit : KMT Borouge UAE. 350 KTA Q1-14 to Q3-14

Reliance India 400 KTA Q1-15 to Q4-16

50

Short-term Price Forecast USD/Ton Short-Term • MEG market will be driven up from stronger

demand in the downstream textiles and fabrics sectors in China due to high seasonal demand in 2H-2013

• For year 2014, the market remain robust continuously from previous year due to strong derivative demand from new Polyester plants in China will start up

375 351 284 281 256

421 503 552

961 858 920 946 928 896 878 872

1,395 1,265 1,322

1,427 1,459 1,363

1,333 1,335 1,282

1,173 1,143 1,208 1,204 1,307

1,370 1,420

0

200

400

600

800

1,000

1,200

1,400

1,600

1Q/13 2Q/13 3Q/13 4Q/13 1Q/14F 2Q/14F 3Q/14F 4Q/14F

MEG the market remain robust due to seasonal and strong derivative demand

MEG Long-term Supply/Demand

Additional (2013-2018) (Unit : MMT)

Supply Demand 14.98 8.89

America14%

Europe5%

Middle East13%India

5%

China60%

Other Asia3%

51 Source: PCI November 2013

01,0002,0003,0004,0005,0006,0007,000

2013 2014 2015 2016 2017 2018

America Europe India Middle East

China Other Asia Additional demand

Ningbo Heyuan China 500 KTA Q4-12 to Q1-13

Unit : KMT PetroChina Sichuan China 380 KTA Q3-13 to Q1-14

Dahua Chemical China 500 KTA Q2-15 to Q1-16

Sinopec Wuhan China 295 KTA Q1-13 to Q3-13

51

Short-term Price Forecast Short-Term • Additional new supply in Asia and squeezed

PTA margins and high inventory levels among downstream Polyester market will affect the PX market in 2H-2013

• For year 2014, PX market still be pressured on more new supplies in Asia mainly from China

USD/Ton

673 551 528 496 477 500 474 458

961 858 920 946 928 896 878 872

1,634

1,409 1,449 1,442 1,405 1,397 1,352 1,330

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1Q/13 2Q/13 3Q/13 4Q/13 1Q/14F 2Q/14F 3Q/14F 4Q/14F

Paraxylene Additional new supplies will pressure on PX market

PX Long-term Supply/Demand

52

Additional (2013-2018) (Unit : MMT)

Supply Demand 24.42 14.93

Source: PCI November 2013

America2%

Europe3%

Middle East24%

India15%

China24%

Other Asia32%

01,0002,0003,0004,0005,0006,0007,0008,000

2013 2014 2015 2016 2017 2018

America Europe India Middle East China Other Asia Additional demand

Unit : KMT PetroRabigh Saudi. 1,400 KTA Q3-15 to Q3-16

SK Energy S. Korea 800 KTA Q3-12 to Q1-14

Tenglong Aromatics1 China 800 KTA Q2-12 to Q3-13

52

Short-term Price Forecast USD/Ton Short-Term • Benzene supply in 2H-2013 will depend

on the shutdown for maintenance of Aromatics plants and higher operating rate of Cracker in Asia due to high margin

• For year 2014, Benzene market will be depend on volatile crude and feedstock prices and improve derivatives demand from SM and Phenol market

428 429 336 337 387 335 325 347

961 858 920 946 928 896 878 872

1,389 1,287 1,256 1,283 1,315

1,231 1,203 1,219

0

200

400

600

800

1,000

1,200

1,400

1,600

1Q/13 2Q/13 3Q/13 4Q/13 1Q/14F 2Q/14F 3Q/14F 4Q/14F

Benzene the market will still be driven by the main products

Additional (2013-2018) (Unit : MMT)

Supply Demand 8.76 8.01

BZ Long-term Supply/Demand

America2%

Middle East25%

Europe3%China

24%

Other Asia59%

53 Source: CMAI January 2014

-500

0

500

1,000

1,500

2,000

2,500

2013 2014 2015 2016 2017 2018

America Europe Middle East China Other Asia Additional demand

Anqing PC China 54 KTA Q3-12 to Q1-13

Samsung Total PC S. Korea 422 KTA Q4-14 to Q3-14

Nghi Son Vietnam 246 KTA Q1-15 to Q3-17

ExxonMobil Sing. 340 KTA Q1-13 to Q2-13

Unit : KMT

Reliance India 260 KTA Q1-16 to Q-15

53

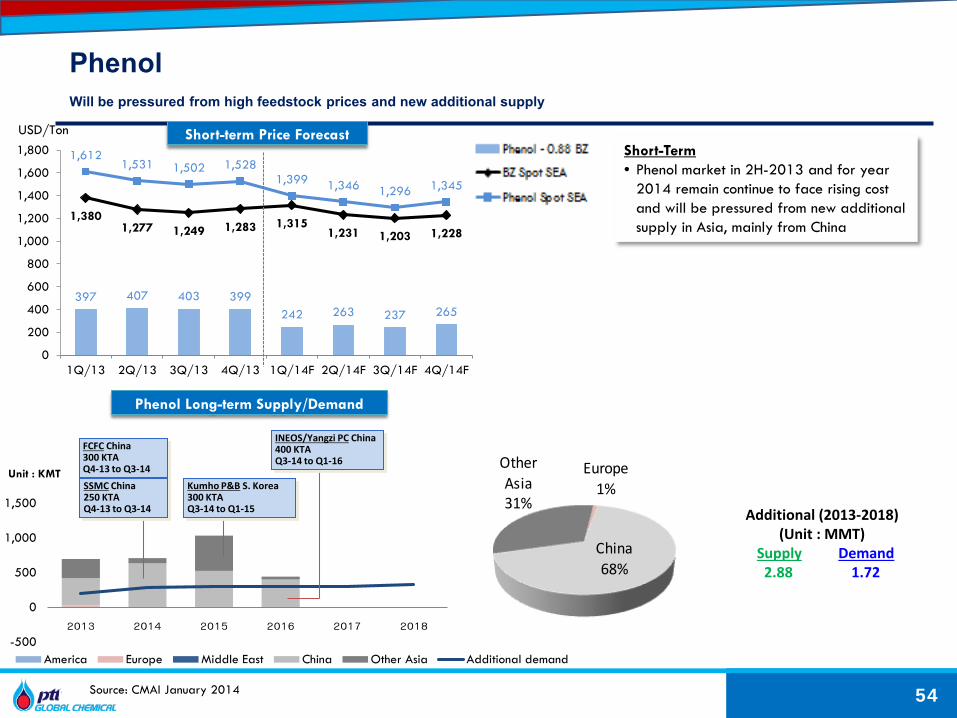

Short-term Price Forecast USD/Ton

Short-Term • Phenol market in 2H-2013 and for year

2014 remain continue to face rising cost and will be pressured from new additional supply in Asia, mainly from China

397 407 403 399 242 263 237 265

1,380 1,277 1,249 1,283 1,315

1,231 1,203 1,228

1,612 1,531 1,502 1,528

1,399 1,346 1,296 1,345

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1Q/13 2Q/13 3Q/13 4Q/13 1Q/14F 2Q/14F 3Q/14F 4Q/14F

Phenol Will be pressured from high feedstock prices and new additional supply

Additional (2013-2018) (Unit : MMT)

Supply Demand 2.88 1.72

Phenol Long-term Supply/Demand

Europe1%

China68%

Other Asia31%

54 Source: CMAI January 2014

-500

0

500

1,000

1,500

2013 2014 2015 2016 2017 2018

America Europe Middle East China Other Asia Additional demand

Unit : KMT

INEOS/Yangzi PC China 400 KTA Q3-14 to Q1-16

FCFC China 300 KTA Q4-13 to Q3-14

SSMC China 250 KTA Q4-13 to Q3-14

Kumho P&B S. Korea 300 KTA Q3-14 to Q1-15

54

Agenda

Appendix

3Q/13 Detail Performance

Product Demand/Supply

The 3 Incidents in 2013

55

The 3 Incidents in 2013

56

Oil Spill What happened? On July 27, 2013 leakage in the flexible hose was found at the SPM while discharging crude oil. The leakage resulted in oil spill of 54,341 liters. On and off shore cleanup operation was done quickly and effectively. What’s the update? The oil spill incident expenses, including provision, for 3Q/13 was Baht1,059 mn. - Recovery expenses Baht 192 mn - Restoration expenses Baht 791 mn - Other expenses Baht 76 mn PTTGC and the insurance company are in the process of negotiation of the reimbursement claim covered by the insurance company.

GSP#5 Shutdown What happened? On August 14, 2013, thunder storm and lightning strike on the Waste Heat Recovery Unit or WHRU of PTT’s GSP#5 which is the gas supplier of I4-2 plant (capacity 450 KTA) PTT anticipated that the repairs will take approximately 3-5 months. What’s the update? -PTT’s GSP#5 is back to run at 50% and expects to run at 100% in early 2Q/14 and 100% back to normal operation by Aug. 2014. -PTTGC’s overall olefin utilization rate to be around 90% in 4Q/13.

LDPE Shutdown What happened? LDPE (capacity 300KTA) shutdown since July 10, 2013 to repair the cylinder of the Booster/Primary Compressor. PTTGC expected to take approximately 3.5 months to repair the LDPE plant. Impact estimated 2% of NI. What’s the update? -Start up on Sep. 26, 2013, which was earlier than plan. -Resume with utilization rate of 77% in Oct. with target of over 100% for the remaining of the year. -In the process of doing Root- Cause Analysis